survey and analysis of capital budgeting methods

TRANSCRIPT

COURSE TITLE: SEMINOR IN FINANCE COURSE CODE: MPH 622

Presentation on

Survey and Analysis of Capital Budgeting Methods

Written by: Lawarance. D. Schall, Gary L. Sundem and William R. Geijsbeek, Jr.

University of Washington and Finance Manager, The Boeing Company

Published in: Journal of Finance, Vol. XXXIII, No. 1, March 1978

10th April, 2011

Article Outline

I. Background

II. Survey sample and findings

A. Sample

B. Results

III. Analysis of results

IV. Conclusions

Presentation Outline

Background & Objectives

Motivation of the study

Research Methodology

Major Findings

Conclusions

Comments

Background

Istvan (1961), Klammer (1972) and Fremgren (1973)

and Lawarance, et.al (1977) are the only previous

works concentrated towards the gradual sophistication

of capital budgeting techniques in the area of finance.

The insight of the study emerges from the mutual needs

of such kind of works from both the academicians’ and

practitioners’ area of interest.

The study thus try to entitle the needful blend.

Back…..

Objectives

i) To find the most popular CBTs employed in

practices.

ii) To explore the computation of discount rates and

cash flows, and

iii) To identify the method of estimation and

adjustment of project risk.

Research Gap:

The need of further assessment of CBTs, as

suggested by the trend of limited previous works.

The growing concern over the use of CBTs in

practices.

Implications of the results.

Motivation

Population: large US firms which are included on the COMPUSTAT tape.

Selection of sample (424 firms) constitute 3 condition; i) net plant assets exceeding $200 million,

ii) capital expenditures exceeding $20 million, or

iii) net plant assets exceeding $150 million and capital expenditures exceeding $10 million.

Since the inability of 17 firms, only 407 firms were entertained for the survey.

Major financial officers are the respondents .

Response rate was 46.4%.

Methodology

Method… Variables:

Payback period (PBK)

Accounting rate of return (ARR)

Internal rate of return (IRR)

Net present value (NPV)

Cost of debt

Cost of equity

Weighted average cost of capital (WACC)

Growth and dividend payout ratio, and

Risk-free rate

Tools : The study uses the naïve methods for

analysis which includes frequency distribution,

range and percentile.

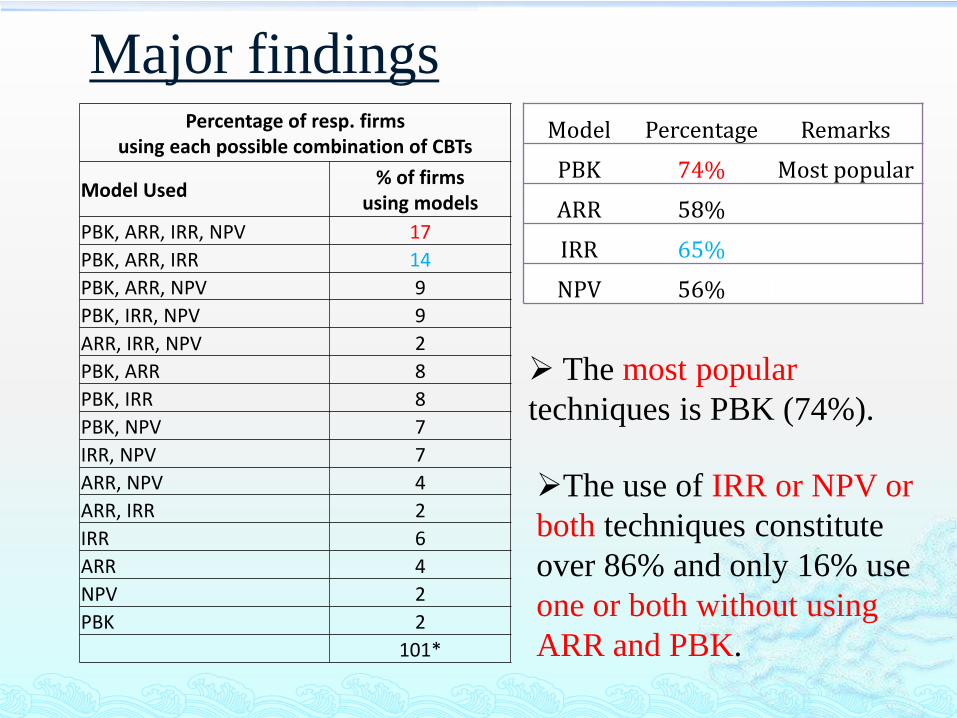

Major findingsModel Percentage Remarks

PBK 74% Most popular

ARR 58%

IRR 65%

NPV 56%

The most popular

techniques is PBK (74%).

Percentage of resp. firms using each possible combination of CBTs

Model Used% of firms

using models

PBK, ARR, IRR, NPV 17

PBK, ARR, IRR 14

PBK, ARR, NPV 9

PBK, IRR, NPV 9

ARR, IRR, NPV 2

PBK, ARR 8

PBK, IRR 8

PBK, NPV 7

IRR, NPV 7

ARR, NPV 4

ARR, IRR 2

IRR 6

ARR 4

NPV 2

PBK 2

101*

The use of IRR or NPV or

both techniques constitute

over 86% and only 16% use

one or both without using

ARR and PBK.

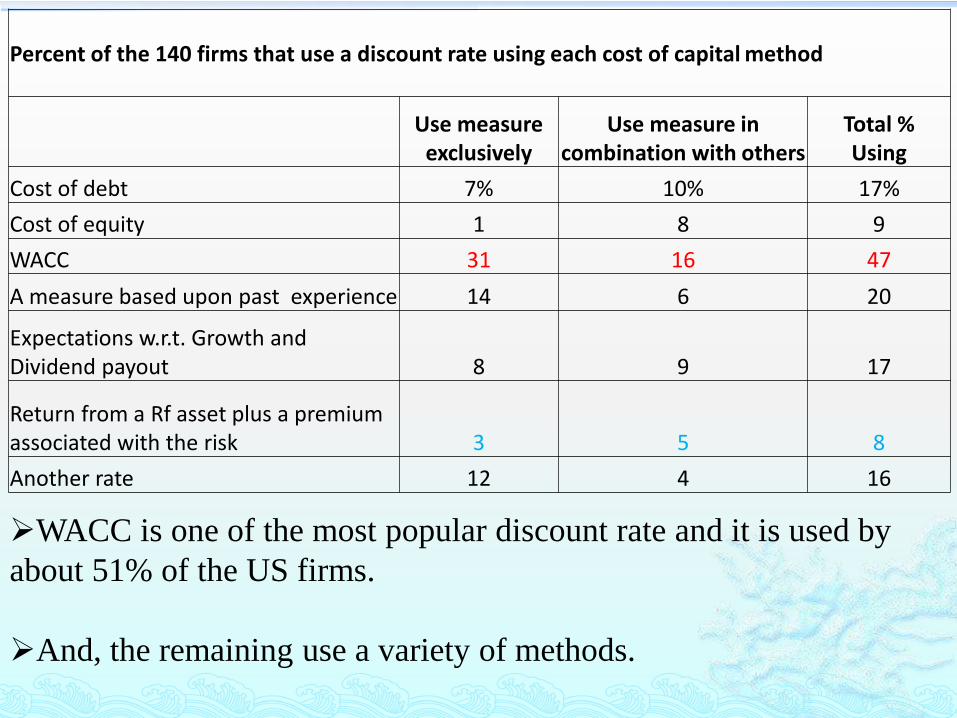

Percent of the 140 firms that use a discount rate using each cost of capital method

Use measure exclusively

Use measure in combination with others

Total % Using

Cost of debt 7% 10% 17%

Cost of equity 1 8 9

WACC 31 16 47

A measure based upon past experience 14 6 20

Expectations w.r.t. Growth and Dividend payout 8 9 17

Return from a Rf asset plus a premium associated with the risk 3 5 8

Another rate 12 4 16

WACC is one of the most popular discount rate and it is used by

about 51% of the US firms.

And, the remaining use a variety of methods.

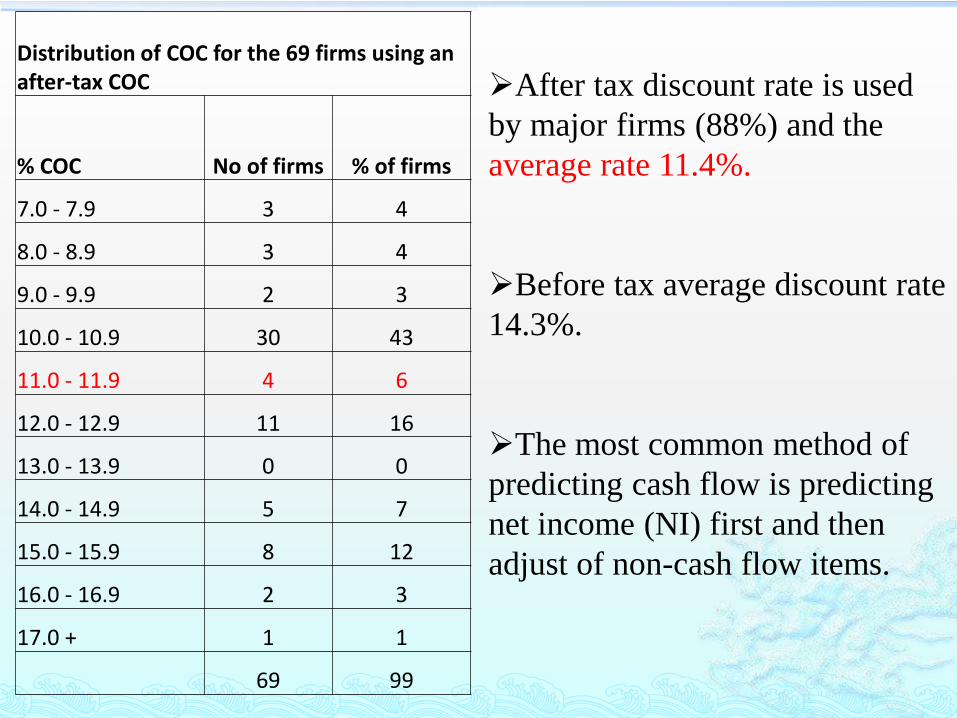

Distribution of COC for the 69 firms using an after-tax COC

% COC No of firms % of firms

7.0 - 7.9 3 4

8.0 - 8.9 3 4

9.0 - 9.9 2 3

10.0 - 10.9 30 43

11.0 - 11.9 4 6

12.0 - 12.9 11 16

13.0 - 13.9 0 0

14.0 - 14.9 5 7

15.0 - 15.9 8 12

16.0 - 16.9 2 3

17.0 + 1 1

69 99

After tax discount rate is used

by major firms (88%) and the

average rate 11.4%.

Before tax average discount rate

14.3%.

The most common method of

predicting cash flow is predicting

net income (NI) first and then

adjust of non-cash flow items.

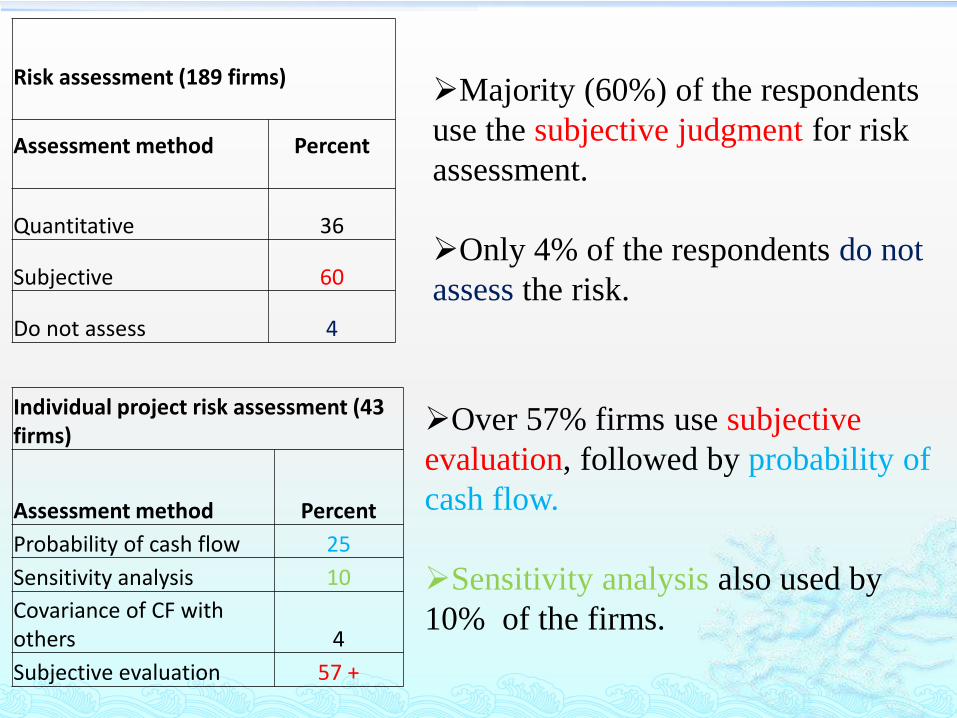

Risk assessment (189 firms)

Assessment method Percent

Quantitative 36

Subjective 60

Do not assess 4

Majority (60%) of the respondents

use the subjective judgment for risk

assessment.

Only 4% of the respondents do not

assess the risk.

Individual project risk assessment (43 firms)

Assessment method Percent

Probability of cash flow 25

Sensitivity analysis 10

Covariance of CF with others 4

Subjective evaluation 57 +

Over 57% firms use subjective

evaluation, followed by probability of

cash flow.

Sensitivity analysis also used by

10% of the firms.

Klammer (1972) and Fremgren (1973) on study of CBTs shows the increasing trend of its use for the investment decision making. Former showed 39% and later 67% of the decision based use CBTs. Lawarance, et.al (1977) found 78%as the increasing parameter of popularity. On top of the previous works, the study suggest that 86% of the firms use more than one CBTs.

After-tax WACC is the most common method of determining a required rate of return.

Project risk is usually assessed subjectively, and

The level of sophistication in CBTs is positively related to the size of the firm’s capital budget and negatively related to risk.

Conclusions

The study use the simpler methods of analysis so that readers can easily understand the theme.

The findings could impart the understanding about the importance of CBTs and its pervasive use from the very beginning.

The results of the study are very much useful to the learners and beginners (practitioners), and

The study was conducted by the authors from the academic and practitioner field of finance, thus it is an interesting blend of two opponents.

Comments

Thank you.