study perfect your score score analyzing accounts … · analyzing accounts affected by adjusting...

TRANSCRIPT

Name Perfect YourScore Score

Analyzing Accounts Affected by Adjusting and Closing Entries 24 Pts.Examining Adjusting and Closing Entries 18 Pts.

Analyzing the Accounting Cycle for a Merchandising Business9 Pts.Organized as a Corporation

Total 51 Pts.

StudyGuide

16Part One—Analyzing Accounts Affected by Adjusting andClosing EntriesDirections: For each adjusting or closing entry described, decide which accountsare debited and credited. Print the letter identifying your choice in the properAnswers column.

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING Chapter 16 • 421

Accounts to Be

Debited Credited

T C

I K

R P

S Q

J L

E A

F B

G H

O I

I M

I N

N D

Account Title

A. AccumulatedDepreciation—OfficeEquipment

B. AccumulatedDepreciation—StoreEquipment

C. Allowance forUncollectible Accounts

D. Dividends

E. Depreciation Expense—Office Equipment

F. Depreciation Expense—Store Equipment

G. Federal Income TaxExpense

H. Federal Income TaxPayable

I. Income Summary

J. Insurance Expense

K. Merchandise Inventory

L. Prepaid Insurance

M. Purchases

N. Retained Earnings

O. Sales

P. Supplies—Office

Q. Supplies—Store

R. Supplies Expense—Office

S. Supplies Expense—Store

T. Uncollectible Accounts Expense

Transaction

1–2. Adjusting entry for allowance for uncollectibleaccounts. (p. 482)

3–4. Adjusting entry for a decrease in merchandiseinventory. (p. 482)

5–6. Adjusting entry for office supplies. (p. 483)

7–8. Adjusting entry for store supplies. (p. 483)

9–10. Adjusting entry for prepaid insurance. (p. 484)

11–12. Adjusting entry for depreciation of officeequipment. (p. 484)

13–14. Adjusting entry for depreciation of storeequipment. (p. 485)

15–16. Adjusting entry for federal income taxes. (p. 485)

17–18. Closing entry for the sales account. (p. 488)

19–20. Closing entry for the purchases account. (p. 490)

21–22. Closing entry for the income summary accountwith a net income. (p. 491)

23–24. Closing entry for dividends. (p. 491)

b-te_16-study-421-424.qxd 11/9/07 9:07 PM Page 421 SECOND REVISED

422 • Working Papers TE CENTURY 21 ACCOUNTING, 9TH EDITION

Part Two—Examining Adjusting and Closing EntriesDirections: Place a T for True or an F for False in the Answers column toshow whether each of the following statements is true or false.

Answers

1. T

2. F

3. F

4. T

5. T

6. T

7. T

8. F

9. F

10. T

11. T

12. F

13. T

14. F

15. T

16. F

17. F

18. T

1. General ledger account balances are changed only by posting journal entries. (p. 481)

2. Adjusting entries bring subsidiary ledger accounts up to date. (p. 481)

3. Hobby Shack records the adjusting entries in the general journal on the next line followingthe last daily transaction. (p. 481)

4. Indicating a source document is not necessary when journalizing adjusting entries. (p. 481)

5. Temporary accounts are closed at the end of a fiscal period to prepare the general ledgerfor the next fiscal period. (p. 487)

6. Closing the temporary accounts at the end of a fiscal period is an application of theaccounting concept Matching Expenses with Revenue. (p. 487)

7. A temporary account is closed by recording an equal amount on the side opposite thebalance. (p. 487)

8. The Trial Balance columns of a work sheet and an income statement contain theinformation needed to journalize closing entries. (p. 487)

9. Permanent accounts are sometimes referred to as nominal accounts. (p. 487)

10. The ending account balances of permanent accounts for one fiscal period are the beginningaccount balances for the next fiscal period. (p. 487)

11. Contra accounts with credit balances are closed by debiting the accounts and creditingIncome Summary. (p. 488)

12. Expense accounts are closed by debiting the expense accounts and crediting IncomeSummary. (p. 489)

13. The Income Summary account is closed into the Retained Earnings account. (p. 491)

14. Dividends increase the earnings retained by a corporation. (p. 491)

15. After the closing entry for the Dividends account is posted, the Dividends account has azero balance. (p. 491)

16. After all closing entries are posted, the income statement accounts are the only generalledger accounts that have balances. (p. 494)

17. When the general ledger is ready for the next fiscal period, this is an application of theBusiness Entity accounting concept. (p. 494)

18. The purpose of the post-closing trial balance is to prove the general ledger equality ofdebits and credits. (p. 496)

b-te_16-study-421-424.qxd 11/9/07 9:07 PM Page 422 SECOND REVISED

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING Chapter 16 • 423

Name Date Class

Part Three—Analyzing the Accounting Cycle for a MerchandisingBusiness Organized as a CorporationDirections: Write a number from 1 to 9 to the left of each step to indicate the correct sequence ofall the steps in the accounting cycle. (p. 497)

Answers

1. 3

2. 1

3. 7

4. 2

5. 4

6. 9

7. 6

8. 8

9. 5

Post journal entries to the subsidiary ledgers and the general ledger.

Check source documents for accuracy, and analyze transactions into debit and credit parts.

Journalize adjusting and closing entries from the work sheet.

Record transactions in journals, using information on source documents.

Prepare the schedules of accounts payable and accounts receivable, using information fromthe subsidiary ledgers.

Prepare a post-closing trial balance of the general ledger.

Prepare financial statements from the work sheet.

Post adjusting and closing entries to the general ledger.

Prepare a work sheet, including a trial balance, from the general ledger.

b-te_16-study-421-424.qxd 11/9/07 9:07 PM Page 423 SECOND REVISED

424 • Working Papers TE CENTURY 21 ACCOUNTING, 9TH EDITION

Making a Speech

You will often be responsible for making a speech or presentation while you are in school and after schoolas well. Many people fear speaking in front of others, but it is actually very easy if you are well prepared.

Choosing Your TopicYour topic must be of interest to your audience and one that you can cover adequately in the time available.A common error that students make is to pick a topic that is so broad that they cannot really cover the topicin a short speech. The result is that the speech may ramble and not make any real points. Another errorstudents sometimes make is that they use only one idea. In this case, they may simply make the same pointover and over.

Practicing Your TalkYou should always practice giving your speech before you actually make it before the group. Practicing willhelp you work out any rough spots, and it will make you feel much more at ease when you make the actualpresentation.

A good technique is to give the talk in front of a mirror. Watching yourself while speaking can be verydistracting, but it will give you valuable practice in keeping on the subject and avoiding distractions.

Your AppearanceOn the day you are to give your talk, be sure to be well rested, and be sure to dress appropriately. Whenyou are introduced, walk directly to the platform. Stand straight without slouching or leaning on the deskor lectern. A sloppy appearance will detract from your talk.

Giving Your SpeechIn most cases you should not read a speech. You should talk to the members of the audience, following theideas from notes that you have made.

When you begin your talk, start with a point that will gain the attention of the group. It is not necessaryto try to tell a joke. If you do not get the attention of the group at the outset, however, you may have troublemaintaining their interest.

Each point should be easy to understand, and you may illustrate it with examples that are clearly relatedand support the point. When you proceed to the next point, you should make it clear to the group that youare moving to the next item of interest.

A common error is to direct your talk to only one person in the audience, particularly someone whoagrees with your points. However, you are speaking to all members of the audience and you should lookat all of them.

After you have made your major points, you should summarize briefly. Your conclusions should bebased on the material that you have presented and should be easy to follow. Your talk should end on astrong note, and you should then stop. A common error is for a speaker to repeat the conclusion severaltimes, allowing the speech to end on a low note.

Keep on TimeKeep your speech to the allotted time. If you have 20 minutes, be sure that you do not take 25 minutes. Paceyourself so that you will finish all points on time. Do not go too slowly at first and then rush at the end.This can make your talk dull at the beginning and hard to follow at the end.

With proper planning and practice, you will soon be making excellent talks.

StudySkills

b-te_16-study-421-424.qxd 11/9/07 9:07 PM Page 424 SECOND REVISED

Name Date Class

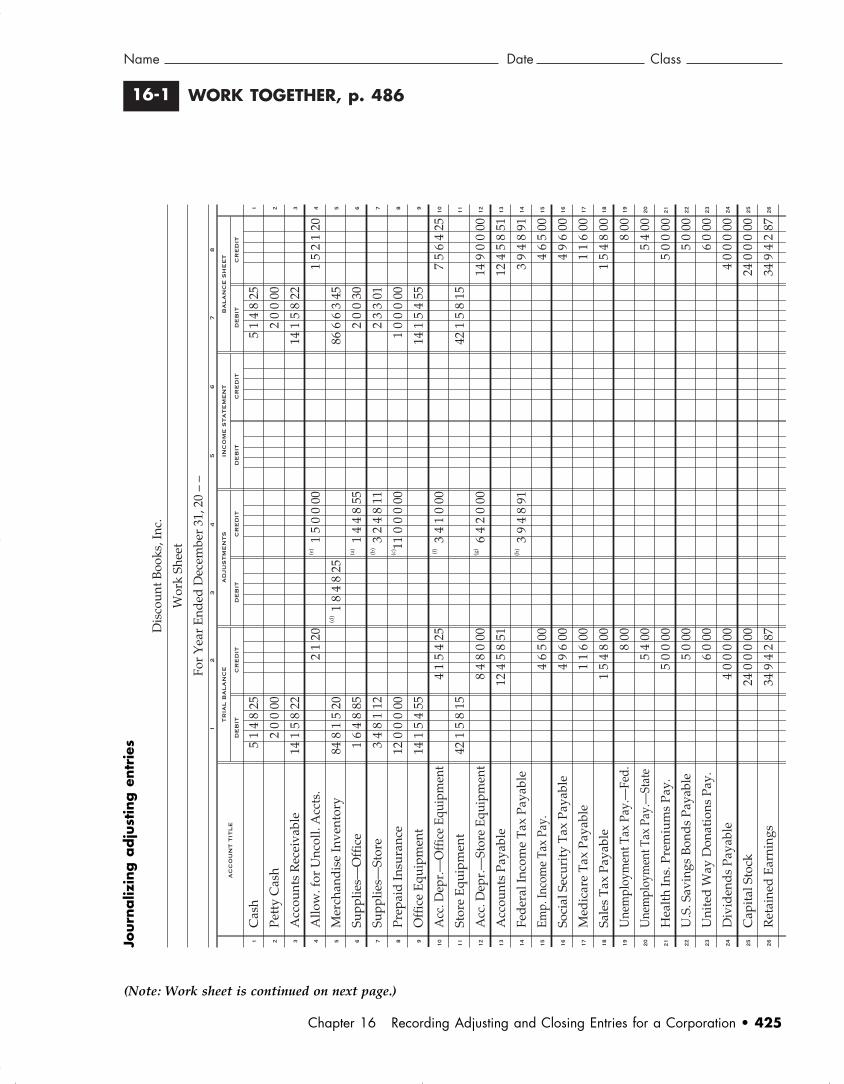

WORK TOGETHER, p. 48616-1

Journ

aliz

ing a

dju

stin

g e

ntr

ies

Chapter 16 Recording Adjusting and Closing Entries for a Corporation • 425

12

34

AC

CO

UN

T T

ITL

E

TR

IAL

BA

LA

NC

E

DE

BIT

CR

ED

IT

AD

JUS

TM

EN

TS

DE

BIT

CR

ED

IT

INC

OM

E S

TA

TE

ME

NT

DE

BIT

CR

ED

IT

BA

LA

NC

E S

HE

ET

DE

BIT

CR

ED

IT

56

78

1 2 3 4 5 6 7 8 9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26

51

48

25

20

000

141

58

22

848

15

20

16

48

85

34

81

12

120

00

00

141

54

55

421

58

15

21

20

41

54

25

84

80

00

124

58

51

46

500

49

600

11

600

15

48

00

800

54

00

50

000

50

00

60

00

40

00

00

240

00

00

349

42

87

(d)

18

48

25

(e)

15

00

00

(a)

14

48

55(b

) 3

24

811

(c) 11

00

000

(f)

34

10

00

(g)

64

20

00

(h)

39

48

91

51

48

25

20

000

141

58

22

866

63

45

20

030

23

301

10

00

00

141

54

55

421

58

15

15

21

20

75

64

25

149

00

00

124

58

51

39

48

91

46

500

49

600

11

600

15

48

00

800

54

00

50

000

50

00

60

00

40

00

00

240

00

00

349

42

87

Cas

h

Pett

y C

ash

Acc

ount

s R

ecei

vabl

e

Allo

w. f

or U

ncol

l. A

ccts

.

Mer

chan

dis

e In

vent

ory

Supp

lies—

Off

ice

Supp

lies—

Stor

e

Prep

aid

Insu

ranc

e

Off

ice

Equ

ipm

ent

Acc

. Dep

r.—

Off

ice

Equi

pmen

t

Stor

e E

quip

men

t

Acc

. Dep

r.—

Stor

e Eq

uipm

ent

Acc

ount

s Pa

yabl

e

Fed

eral

Inco

me

Tax

Pay

able

Emp.

Inco

me

Tax

Pay.

Soci

al S

ecur

ity

Tax

Pay

able

Med

icar

e T

ax P

ayab

le

Sale

s T

ax P

ayab

le

Une

mpl

oym

ent T

ax P

ay.—

Fed.

Une

mpl

oym

ent T

ax P

ay.—

Stat

e

Hea

lth

Ins.

Pre

miu

ms

Pay.

U.S

. Sav

ings

Bon

ds

Paya

ble

Uni

ted

Way

Don

atio

ns P

ay.

Div

iden

ds

Paya

ble

Cap

ital

Sto

ck

Ret

aine

d E

arni

ngs

Dis

coun

t Boo

ks, I

nc.

Wor

k Sh

eet

For

Yea

r E

nded

Dec

embe

r 31

, 20

– –

(Note: Work sheet is continued on next page.)

BTE_Ch16-425-465.qxd 11/9/07 9:05 PM Page 425 SECOND REVISED

WORK TOGETHER (continued)16-1

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING426 • Working Papers TE

12

34

AC

CO

UN

T T

ITL

E

TR

IAL

BA

LA

NC

E

DE

BIT

CR

ED

IT

AD

JUS

TM

EN

TS

DE

BIT

CR

ED

IT

INC

OM

E S

TA

TE

ME

NT

DE

BIT

CR

ED

IT

BA

LA

NC

E S

HE

ET

DE

BIT

CR

ED

IT

56

78

27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52

27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52

160

00

00

21

500

41

53

28

174

48

120

60

00

00

484

51

48

25

41

50

00

87

45

25

120

00

00

974

58

84

56

48

40

160

00

00

527

76

940

430

52

158

34

525

55

48

74

527

76

940

(f)

34

10

00(g

) 6

42

000

(c) 11

00

000

(a)

14

48

55(b

) 3

24

811

(e)

15

00

00

(h)

39

48

91

328

23

82

(d)

18

48

25

328

23

82

21

500

41

53

28

174

48

120

60

00

00

484

51

48

25

34

10

00

64

20

00

110

00

00

41

50

00

87

45

25

120

00

00

974

58

84

14

48

55

32

48

11

15

00

00

56

48

40

199

48

91

364

98

063

732

83

19

438

26

382

18

48

25

430

52

158

34

525

55

48

74

438

26

382

438

26

382

160

00

00

179

91

593

179

91

593

106

63

274

732

83

19

179

91

593

Div

iden

ds

Inco

me

Sum

mar

y

Sale

s

Sale

s D

isco

unt

Sale

s R

etur

ns a

nd A

llow

ance

s

Purc

hase

s

Purc

hase

s D

isco

unt

Purc

h. R

etur

ns a

nd A

llow

ance

s

Ad

vert

isin

g E

xpen

se

Cas

h Sh

ort a

nd O

ver

Cre

dit

Car

d F

ee E

xpen

se

Dep

r. Ex

p.—

Off

ice

Equi

pmen

t

Dep

r. E

xp.—

Stor

e Eq

uipm

ent

Insu

ranc

e E

xpen

se

Mis

cella

neou

s E

xpen

se

Payr

oll T

axes

Exp

ense

Ren

t Exp

ense

Sala

ry E

xpen

se

Supp

lies

Exp

ense

—O

ffic

e

Supp

lies

Exp

ense

—St

ore

Unc

olle

ctib

le A

ccou

nts

Exp

.

Uti

litie

s E

xpen

se

Fed

. Inc

ome

Tax

Exp

ense

Net

Inco

me

afte

r Fed

. Inc

ome

Tax

Dis

coun

t Boo

ks, I

nc.

Wor

k Sh

eet

For

Yea

r E

nded

Dec

embe

r 31

, 20

– –

BTE_Ch16-425-465.qxd 11/9/07 9:05 PM Page 426 SECOND REVISED

Name Date Class

WORK TOGETHER (concluded)16-1

1.

Chapter 16 Recording Adjusting and Closing Entries for a Corporation • 427

GENERAL JOURNAL PAGE 18

DATE ACCOUNT TITLE DEBIT CREDITDOC.NO.

POST.REF.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

Dec.20 – –

31

31

31

31

31

31

31

31

Uncollectible Accounts Expense

Allowance for Uncollectible Accounts

Merchandise Inventory

Income Summary

Supplies Expense—Office

Supplies—Office

Supplies Expense—Store

Supplies—Store

Insurance Expense

Prepaid Insurance

Depreciation Expense—Office Equipment

Accumulated Depreciation—Office Equipment

Depreciation Expense—Store Equipment

Accumulated Depreciation—Store Equipment

Federal Income Tax Expense

Federal Income Tax Payable

1 5 0 0 00

1 8 4 8 25

1 4 4 8 55

3 2 4 8 11

11 0 0 0 00

3 4 1 0 00

6 4 2 0 00

3 9 4 8 91

1 5 0 0 00

1 8 4 8 25

1 4 4 8 55

3 2 4 8 11

11 0 0 0 00

3 4 1 0 00

6 4 2 0 00

3 9 4 8 91

Adjusting Entries

BTE_Ch16-425-465.qxd 11/9/07 9:05 PM Page 427 SECOND REVISED

ON YOUR OWN, p. 48616-1

Journ

aliz

ing a

dju

stin

g e

ntr

ies

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING428 • Working Papers TE

12

34

AC

CO

UN

T T

ITL

E

TR

IAL

BA

LA

NC

E

DE

BIT

CR

ED

IT

AD

JUS

TM

EN

TS

DE

BIT

CR

ED

IT

INC

OM

E S

TA

TE

ME

NT

DE

BIT

CR

ED

IT

BA

LA

NC

E S

HE

ET

DE

BIT

CR

ED

IT

56

78

1 2 3 4 5 6 7 8 9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26

201

58

25

50

000

424

88

25

315

41

825

71

48

48

61

54

88

180

00

00

414

84

89

901

84

11

10

88

18

161

80

00

221

80

00

221

54

17

32

10

00

94

550

22

113

42

15

02

32

00

21

600

12

00

00

12

000

14

000

90

00

00

225

00

000

381

79

53

(e)

32

50

00(d

) 1

64

822

(a)

68

47

15(b

) 5

54

811

(c) 16

00

000

(f)

84

50

00

(g)

86

00

00

(h) 24

16

372

201

58

25

50

000

424

88

25

313

77

003

30

133

60

677

20

00

00

414

84

89

901

84

11

43

38

18

246

30

00

307

80

00

221

54

17

241

63

72

32

10

00

94

550

22

113

42

15

02

32

00

21

600

12

00

00

12

000

14

000

90

00

00

225

00

000

381

79

53

Cas

h

Pett

y C

ash

Acc

ount

s R

ecei

vabl

e

Allo

w. f

or U

ncol

l. A

ccts

.

Mer

chan

dis

e In

vent

ory

Supp

lies—

Off

ice

Supp

lies—

Stor

e

Prep

aid

Insu

ranc

e

Off

ice

Equ

ipm

ent

Acc

. Dep

r.—

Off

ice

Equi

pmen

t

Stor

e E

quip

men

t

Acc

. Dep

r.—

Stor

e Eq

uipm

ent

Acc

ount

s Pa

yabl

e

Fed

eral

Inco

me

Tax

Pay

able

Emp.

Inco

me

Tax

Pay.

Soci

al S

ecur

ity

Tax

Pay

able

Med

icar

e T

ax P

ayab

le

Sale

s T

ax P

ayab

le

Une

mpl

oym

ent T

ax P

ay.—

Fed.

Une

mpl

oym

ent T

ax P

ay.—

Stat

e

Hea

lth

Ins.

Pre

miu

ms

Pay.

U.S

. Sav

ings

Bon

ds

Paya

ble

Uni

ted

Way

Don

atio

ns P

ay.

Div

iden

ds

Paya

ble

Cap

ital

Sto

ck

Ret

aine

d E

arni

ngs

Stur

gis

Supp

ly, I

nc.

Wor

k Sh

eet

For

Yea

r E

nded

Dec

embe

r 31

, 20

– –

(Note: Work sheet is continued on next page.)

BTE_Ch16-425-465.qxd 11/9/07 9:05 PM Page 428 SECOND REVISED

Name Date Class

ON YOUR OWN (continued)16-1

Chapter 16 Recording Adjusting and Closing Entries for a Corporation • 429

12

34

AC

CO

UN

T T

ITL

E

TR

IAL

BA

LA

NC

E

DE

BIT

CR

ED

IT

AD

JUS

TM

EN

TS

DE

BIT

CR

ED

IT

INC

OM

E S

TA

TE

ME

NT

DE

BIT

CR

ED

IT

BA

LA

NC

E S

HE

ET

DE

BIT

CR

ED

IT

56

78

27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52

27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52

360

00

00

12

48

22

64

88

95

442

51

825

150

00

00

525

184

87

15

94

80

00

184

86

69

240

00

00

183

00

000

95

81

25

500

00

00

1,355

83

287

998

14

815

71

54

25

64

48

94

1,355

83

287

(d)

16

48

22

(f)

8

45

000

(g)

86

00

00(c

) 160

00

00

(a)

68

47

15(b

) 5

54

811

(e)

32

50

00

(h) 24

16

372

745

07

2074

50

720

16

48

22

12

48

22

64

88

95

442

51

825

150

00

00

525

184

87

15

84

50

00

86

00

00

160

00

00

94

80

00

184

86

69

240

00

00

183

00

000

68

47

15

55

48

11

32

50

00

95

81

25

741

63

72

852

80

296

158

94

838

1,011

75

134

998

14

815

71

54

25

64

48

94

1,011

75

134

1,011

75

134

360

00

00

547

49

363

547

49

363

388

54

525

158

94

838

547

49

363

Div

iden

ds

Inco

me

Sum

mar

y

Sale

s

Sale

s D

isco

unt

Sale

s R

etur

ns a

nd A

llow

ance

s

Purc

hase

s

Purc

hase

s D

isco

unt

Purc

h. R

etur

ns a

nd A

llow

ance

s

Ad

vert

isin

g E

xpen

se

Cas

h Sh

ort a

nd O

ver

Cre

dit

Car

d F

ee E

xpen

se

Dep

r. Ex

p.—

Off

ice

Equi

pmen

t

Dep

r. E

xp.—

Stor

e Eq

uipm

ent

Insu

ranc

e E

xpen

se

Mis

cella

neou

s E

xpen

se

Payr

oll T

axes

Exp

ense

Ren

t Exp

ense

Sala

ry E

xpen

se

Supp

lies

Exp

ense

—O

ffic

e

Supp

lies

Exp

ense

—St

ore

Unc

olle

ctib

le A

ccou

nts

Exp

.

Uti

litie

s E

xpen

se

Fed

. Inc

ome

Tax

Exp

ense

Net

Inco

me

afte

r Fed

. Inc

ome

Tax

Stur

gis

Supp

ly, I

nc.

Wor

k Sh

eet

For

Yea

r E

nded

Dec

embe

r 31

, 20

– –

BTE_Ch16-425-465.qxd 11/9/07 9:05 PM Page 429 SECOND REVISED

ON YOUR OWN (concluded)16-1

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING430 • Working Papers TE

GENERAL JOURNAL PAGE 24

DATE ACCOUNT TITLE DEBIT CREDITDOC.NO.

POST.REF.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

Dec.20 – –

31

31

31

31

31

31

31

31

Uncollectible Accounts Expense

Allowance for Uncollectible Accounts

Income Summary

Merchandise Inventory

Supplies Expense—Office

Supplies—Office

Supplies Expense—Store

Supplies—Store

Insurance Expense

Prepaid Insurance

Depreciation Expense—Office Equipment

Accumulated Depreciation—Office Equipment

Depreciation Expense—Store Equipment

Accumulated Depreciation—Store Equipment

Federal Income Tax Expense

Federal Income Tax Payable

3 2 5 0 00

1 6 4 8 22

6 8 4 7 15

5 5 4 8 11

16 0 0 0 00

8 4 5 0 00

8 6 0 0 00

24 1 6 3 72

3 2 5 0 00

1 6 4 8 22

6 8 4 7 15

5 5 4 8 11

16 0 0 0 00

8 4 5 0 00

8 6 0 0 00

24 1 6 3 72

Adjusting Entries

1.

BTE_Ch16-425-465.qxd 11/9/07 9:05 PM Page 430 SECOND REVISED

Name Date Class

WORK TOGETHER, p. 49316-2

Journalizing closing entries

1.

Chapter 16 Recording Adjusting and Closing Entries for a Corporation • 431

GENERAL JOURNAL PAGE 19

DATE ACCOUNT TITLE DEBIT CREDITDOC.NO.

POST.REF.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

Dec.20 – –

31

31

31

31

Closing Entries

Sales

Purchases Discount

Purchases Ret. and Allow.

Income Summary

Income Summary

Sales Discount

Sales Returns and Allow.

Purchases

Advertising Expense

Cash Short and Over

Credit Card Fee Expense

Depr. Exp.—Office Equipment

Depr. Exp.—Store Equipment

Insurance Expense

Miscellaneous Expense

Payroll Taxes Expense

Rent Expense

Salary Expense

Supplies Expense—Office

Supplies Expense—Store

Uncollectible Accounts Expense

Utilities Expense

Federal Income Tax Expense

Income Summary

Retained Earnings

Retained Earnings

Dividends

430 5 2 1 58

3 4 5 25

5 5 4 8 74

364 9 8 0 63

73 2 8 3 19

16 0 0 0 00

436 4 1 5 57

2 1 5 00

4 1 5 3 28

174 4 8 1 20

6 0 0 0 00

4 84

5 1 4 8 25

3 4 1 0 00

6 4 2 0 00

11 0 0 0 00

4 1 5 0 00

8 7 4 5 25

12 0 0 0 00

97 4 5 8 84

1 4 4 8 55

3 2 4 8 11

1 5 0 0 00

5 6 4 8 40

19 9 4 8 91

73 2 8 3 19

16 0 0 0 00

BTE_Ch16-425-465.qxd 11/9/07 9:05 PM Page 431 SECOND REVISED

ON YOUR OWN, p. 49316-2

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING432 • Working Papers TE

Journalizing closing entries

1.

GENERAL JOURNAL PAGE 25

DATE ACCOUNT TITLE DEBIT CREDITDOC.NO.

POST.REF.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

Dec.20 – –

31

31

31

31

Sales

Purchases Discount

Purchases Ret. and Allow.

Income Summary

Income Summary

Sales Discount

Sales Returns and Allow.

Purchases

Advertising Expense

Cash Short and Over

Credit Card Fee Expense

Depr. Exp.—Office Equipment

Depr. Exp.—Store Equipment

Insurance Expense

Miscellaneous Expense

Payroll Taxes Expense

Rent Expense

Salary Expense

Supplies Expense—Office

Supplies Expense—Store

Uncollectible Accounts Expense

Utilities Expense

Federal Income Tax Expense

Income Summary

Retained Earnings

Retained Earnings

Dividends

998 1 4 8 15

7 1 5 4 25

6 4 4 8 94

851 1 5 4 74

158 9 4 8 38

36 0 0 0 00

1,011 7 5 1 34

1 2 4 8 22

6 4 8 8 95

442 5 1 8 25

15 0 0 0 00

5 25

18 4 8 7 15

8 4 5 0 00

8 6 0 0 00

16 0 0 0 00

9 4 8 0 00

18 4 8 6 69

24 0 0 0 00

183 0 0 0 00

6 8 4 7 15

5 5 4 8 11

3 2 5 0 00

9 5 8 1 25

74 1 6 3 72

158 9 4 8 38

36 0 0 0 00

Closing Entries

BTE_Ch16-425-465.qxd 11/9/07 9:05 PM Page 432 SECOND REVISED

Name Date Class

WORK TOGETHER, p. 49816-3

Preparing a post-closing trial balance

1.

Chapter 16 Recording Adjusting and Closing Entries for a Corporation • 433

Cash

Petty Cash

Accounts Receivable

Merchandise Inventory

Supplies—Office

Supplies—Store

Prepaid Insurance

Accounts Payable

Sales Tax Payable

Capital Stock

Retained Earnings

Totals

Visual Art Center

Post-Closing Trial Balance

December 31, 20 – –

CREDITDEBITACCOUNT TITLE

21 8 1 0 20

3 5 0 00

8 3 9 8 80

190 9 8 0 00

1 3 1 4 00

2 2 6 8 00

1 9 8 0 00

227 1 0 1 00

11 6 7 6 50

1 5 8 4 00

100 0 0 0 00

113 8 4 0 50

227 1 0 1 00

BTE_Ch16-425-465.qxd 11/9/07 9:05 PM Page 433 SECOND REVISED

ON YOUR OWN, p. 49816-3

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING434 • Working Papers TE

Cash

Petty Cash

Accounts Receivable

Allow. for Uncoll. Accts.

Merchandise Inventory

Supplies

Prepaid Insurance

Equipment

Acc. Depr.—Equipment

Accounts Payable

Federal Income Tax Payable

Sales Tax Payable

Dividends Payable

Capital Stock

Retained Earnings

Totals

Welding Supply

Post-Closing Trial Balance

December 31, 20 – –

CREDITDEBITACCOUNT TITLE

26 4 8 5 00

5 0 0 00

15 4 8 7 00

134 1 5 2 00

7 4 1 00

1 0 0 0 00

25 4 8 7 00

203 8 5 2 00

1 4 5 7 00

12 4 5 0 00

13 1 5 4 00

2 4 8 9 00

1 5 4 8 00

5 0 0 0 00

50 0 0 0 00

117 7 5 4 00

203 8 5 2 00

Preparing a post-closing trial balance

1.

BTE_Ch16-425-465.qxd 11/9/07 9:05 PM Page 434 SECOND REVISED

Name Date Class

APPLICATION PROBLEM, p. 50016-1

Chapter 16 Recording Adjusting and Closing Entries for a Corporation • 435

12

34

AC

CO

UN

T T

ITL

E

TR

IAL

BA

LA

NC

E

DE

BIT

CR

ED

IT

AD

JUS

TM

EN

TS

DE

BIT

CR

ED

IT

INC

OM

E S

TA

TE

ME

NT

DE

BIT

CR

ED

IT

BA

LA

NC

E S

HE

ET

DE

BIT

CR

ED

IT

56

78

1 2 3 4 5 6 7 8 9 10

11

12

13

14

26

27

28

29

30

31

32

1 2 3 4 5 6 7 8 9

10

11

12

13

14

26

27

28

29

30

31

32

164

85

00

40

000

414

83

15

248

75

230

61

48

28

51

74

85

140

00

00

384

58

25

414

78

50

120

00

00

14

54

85

42

15

48

284

83

525

94

815

174

80

00

234

50

00

199

48

80

170

02

463

668

74

220

(d)

21

54

25

(e)

14

58

00(d

) 2

15

425

(a)

58

18

66(b

) 4

84

804

(c) 12

00

000

(f)

64

80

00

(g)

76

50

00

(h)

36

60

23

21

54

25

14

54

85

42

15

48

284

83

525

668

74

220

164

85

00

40

000

414

83

15

246

59

805

32

962

32

681

20

00

00

384

58

25

414

78

50

120

00

00

24

06

15

239

60

00

311

00

00

199

48

80

36

60

23

170

02

463

Cas

h

Pett

y C

ash

Acc

ount

s R

ecei

vabl

e

Allo

w. f

or U

ncol

l. A

ccts

.

Mer

chan

dis

e In

vent

ory

Supp

lies—

Off

ice

Supp

lies—

Stor

e

Prep

aid

Insu

ranc

e

Off

ice

Equ

ipm

ent

Acc

. Dep

r.—

Off

ice

Equi

pmen

t

Stor

e E

quip

men

t

Acc

. Dep

r.—

Stor

e Eq

uipm

ent

Acc

ount

s Pa

yabl

e

Fed

eral

Inco

me

Tax

Pay

able

Ret

aine

d E

arni

ngs

Div

iden

ds

Inco

me

Sum

mar

y

Sale

s

Sale

s D

isco

unt

Sale

s R

etur

ns a

nd A

llow

.

Purc

hase

s

h

Cel

lar

Boo

ks, I

nc.

Wor

k Sh

eet

For

Yea

r E

nded

Dec

embe

r 31

, 20

– –

Journ

aliz

ing a

dju

stin

g e

ntr

ies

(Note: Work sheet is continued on next page.)

BTE_Ch16-425-465.qxd 11/9/07 9:05 PM Page 435 SECOND REVISED

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING436 • Working Papers TE

APPLICATION PROBLEM (continued)16-1

12

34

AC

CO

UN

T T

ITL

E

TR

IAL

BA

LA

NC

E

DE

BIT

CR

ED

IT

AD

JUS

TM

EN

TS

DE

BIT

CR

ED

IT

INC

OM

E S

TA

TE

ME

NT

DE

BIT

CR

ED

IT

BA

LA

NC

E S

HE

ET

DE

BIT

CR

ED

IT

56

78

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

33

34

35

36

37

38

39

40 41

42

43

44

45

46

47

48

49

50 51 52

125

40

00

808

94

81

10

54

10

00

158

41

20

180

00

00

174

96

033

45

48

20

200

00

00

975

67

482

24

18

81

41

58

41

975

67

482

(f)

64

80

00(g

) 7

65

000

(c) 12

00

000

(a)

58

18

66(b

) 4

84

804

(e)

14

58

00

(h)

36

60

23

440

69

1844

06

918

125

40

00

808

94

81

10

64

80

00

76

50

00

120

00

00

54

10

00

158

41

20

180

00

00

174

96

033

58

18

66

48

48

04

14

58

00

45

48

20

236

60

23

595

36

367

799

55

75

675

31

942

24

18

81

41

58

41

675

31

942

675

31

942

399

55

938

399

55

938

319

60

363

799

55

75

399

55

938

Purc

hase

s D

isco

unt

Purc

h. R

etur

ns a

nd A

llow

.

Ad

vert

isin

g E

xpen

se

Cas

h Sh

ort a

nd O

ver

Cre

dit

Car

d F

ee E

xpen

se

Dep

r. E

xp. —

Off

ice

Equ

ip.

Dep

r. E

xp. —

Stor

e E

quip

.

Insu

ranc

e E

xpen

se

Mis

cella

neou

s E

xpen

se

Payr

oll T

axes

Exp

ense

Ren

t Exp

ense

Sala

ry E

xpen

se

Supp

lies

Exp

ense

—O

ffic

e

Supp

lies

Exp

ense

—St

ore

Unc

olle

ctib

le A

ccou

nts

Exp

.

Uti

litie

s E

xpen

se

Fed

. Inc

ome

Tax

Exp

ense

Net

Inco

me

afte

r Fed

. Inc

ome

Tax

Cel

lar

Boo

ks, I

nc.

Wor

k Sh

eet

For

Yea

r E

nded

Dec

embe

r 31

, 20

– –

BTE_Ch16-425-465.qxd 11/9/07 9:05 PM Page 436 SECOND REVISED

Name Date Class

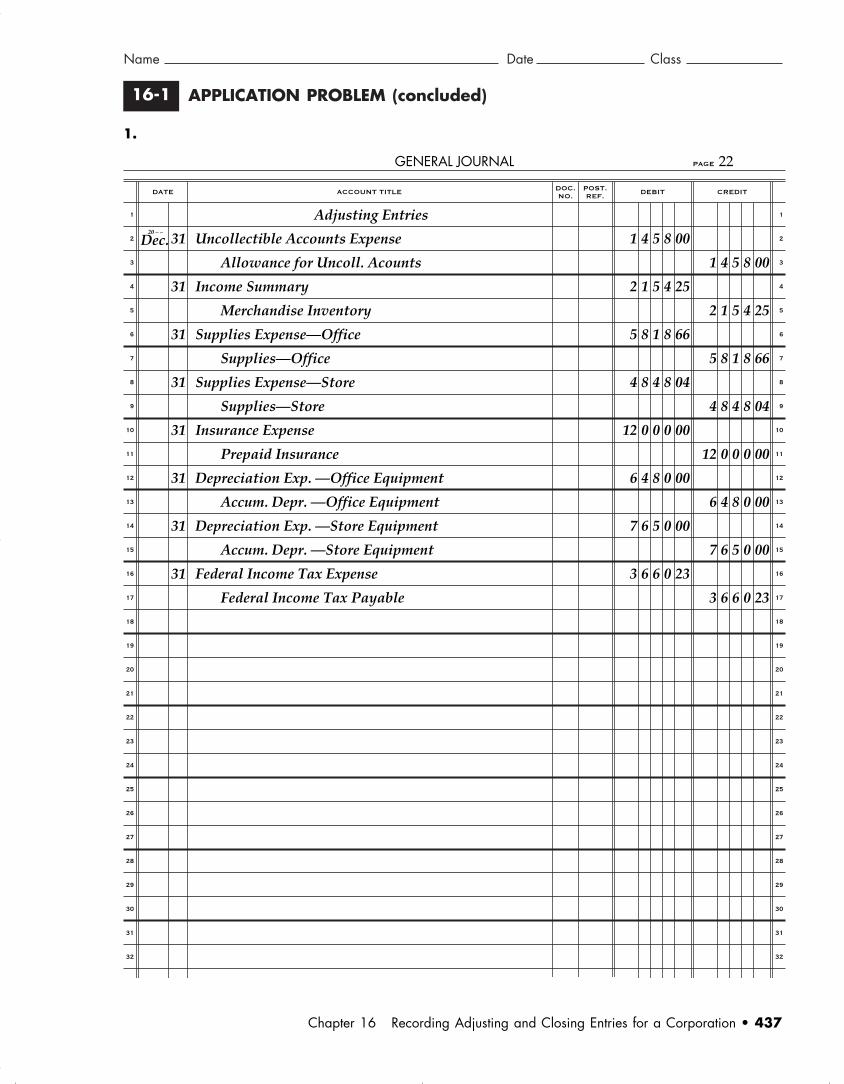

APPLICATION PROBLEM (concluded)16-1

1.

Chapter 16 Recording Adjusting and Closing Entries for a Corporation • 437

GENERAL JOURNAL PAGE 22

DATE ACCOUNT TITLE DEBIT CREDITDOC.NO.

POST.REF.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

Dec.20 – –

31

31

31

31

31

31

31

31

Uncollectible Accounts Expense

Allowance for Uncoll. Acounts

Income Summary

Merchandise Inventory

Supplies Expense—Office

Supplies—Office

Supplies Expense—Store

Supplies—Store

Insurance Expense

Prepaid Insurance

Depreciation Exp. —Office Equipment

Accum. Depr. —Office Equipment

Depreciation Exp. —Store Equipment

Accum. Depr. —Store Equipment

Federal Income Tax Expense

Federal Income Tax Payable

1 4 5 8 00

2 1 5 4 25

5 8 1 8 66

4 8 4 8 04

12 0 0 0 00

6 4 8 0 00

7 6 5 0 00

3 6 6 0 23

1 4 5 8 00

2 1 5 4 25

5 8 1 8 66

4 8 4 8 04

12 0 0 0 00

6 4 8 0 00

7 6 5 0 00

3 6 6 0 23

Adjusting Entries

BTE_Ch16-425-465.qxd 11/9/07 9:05 PM Page 437 SECOND REVISED

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING438 • Working Papers TE

APPLICATION PROBLEM, p. 50016-2

Journalizing closing entries

1., 2., 3., 4.

GENERAL JOURNAL PAGE 23

DATE ACCOUNT TITLE DEBIT CREDITDOC.NO.

POST.REF.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

Dec.20 – –

31

31

31

31

Sales

Purchases Discount

Purchases Ret. and Allow.

Income Summary

Income Summary

Sales Discount

Sales Returns and Allow.

Purchases

Advertising Expense

Cash Short and Over

Credit Card Fee Expense

Depr. Exp.—Office Equipment

Depr. Exp.—Store Equipment

Insurance Expense

Miscellaneous Expense

Payroll Taxes Expense

Rent Expense

Salary Expense

Supplies Expense—Office

Supplies Expense—Store

Uncollectible Accounts Expense

Utilities Expense

Federal Income Tax Expense

Income Summary

Retained Earnings

Retained Earnings

Dividends

668 7 4 2 20

2 4 1 8 81

4 1 5 8 41

593 2 0 9 42

79 9 5 5 75

12 0 0 0 00

675 3 1 9 42

1 4 5 4 85

4 2 1 5 48

284 8 3 5 25

12 5 4 0 00

8 08

9 4 8 1 10

6 4 8 0 00

7 6 5 0 00

12 0 0 0 00

5 4 1 0 00

15 8 4 1 20

18 0 0 0 00

174 9 6 0 33

5 8 1 8 66

4 8 4 8 04

1 4 5 8 00

4 5 4 8 20

23 6 6 0 23

79 9 5 5 75

12 0 0 0 00

Closing Entries

BTE_Ch16-425-465.qxd 11/9/07 9:05 PM Page 438 SECOND REVISED

Name Date Class

APPLICATION PROBLEM, p. 50016-3

Preparing a post-closing trial balance

1.

Chapter 16 Recording Adjusting and Closing Entries for a Corporation • 439

Cash

Petty Cash

Accounts Receivable

Allow. for Uncoll. Accts.

Merchandise Inventory

Supplies—Office

Supplies—Store

Prepaid Insurance

Office Equipment

Acc. Depr.—Office Equipment

Store Equipment

Acc. Depr.—Store Equipment

Accounts Payable

Federal Income Tax Payable

Employee Income Tax Payable

Social Security Tax Payable

Medicare Tax Payable

Sales Tax Payable

Unemployment Tax Payable—Federal

Unemployment Tax Payable—State

Health Insurance Premiums Payable

U.S. Savings Bonds Payable

United Way Donations Payable

Dividends Payable

Capital Stock

Retained Earnings

Totals

Cellar Books, Inc.

Post-Closing Trial Balance

December 31, 20 – –

CREDITDEBITACCOUNT TITLE

16 4 8 5 00

4 0 0 00

41 4 8 3 15

246 5 9 8 05

3 2 9 62

3 2 6 81

2 0 0 0 00

38 4 5 8 25

41 4 7 8 50

387 5 5 9 38

2 4 0 6 15

23 9 6 0 00

31 1 0 0 00

19 9 4 8 80

3 6 6 0 23

1 2 4 8 20

9 0 3 96

2 1 1 41

2 4 5 8 25

2 8 00

1 8 9 00

4 0 0 00

2 5 00

4 0 00

3 0 0 0 00

60 0 0 0 00

237 9 8 0 38

387 5 5 9 38

BTE_Ch16-425-465.qxd 11/9/07 9:05 PM Page 439 SECOND REVISED

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING440 • Working Papers TE

APPLICATION PROBLEM, pp. 501, 50216-4

Journalizing and posting adjusting and closing entries; preparing a post-closing trial balance

1., 2.

GENERAL JOURNAL PAGE 22

DATE ACCOUNT TITLE DEBIT CREDITDOC.NO.

POST.REF.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

Dec.20 – –

31

31

31

31

31

31

31

31

Uncollectible Accounts Expense

Allowance for Uncoll. Accounts

Merchandise Inventory

Income Summary

Supplies Expense—Office

Supplies—Office

Supplies Expense—Store

Supplies—Store

Insurance Expense

Prepaid Insurance

Depreciation Exp. —Office Equipment

Accum. Depr. —Office Equipment

Depreciation Exp. —Store Equipment

Accum. Depr. —Store Equipment

Federal Income Tax Expense

Federal Income Tax Payable

3 5 6 0 00

1 4 8 3 60

5 8 4 7 10

4 9 1 8 50

7 2 0 0 00

3 5 8 0 00

6 1 4 0 00

1 3 5 6 14

3 5 6 0 00

1 4 8 3 60

5 8 4 7 10

4 9 1 8 50

7 2 0 0 00

3 5 8 0 00

6 1 4 0 00

1 3 5 6 14

6165

1135

1140

3140

6155

1145

6160

1150

6130

1160

6120

1210

6125

1220

7105

2120

Adjusting Entries

BTE_Ch16-425-465.qxd 11/9/07 9:05 PM Page 440 SECOND REVISED

Name Date Class

APPLICATION PROBLEM (continued)16-4

3., 4.

Chapter 16 Recording Adjusting and Closing Entries for a Corporation • 441

GENERAL JOURNAL PAGE 23

DATE ACCOUNT TITLE DEBIT CREDITDOC.NO.

POST.REF.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

Dec.20 – –

31

31

31

31

Sales

Purchases Discount

Purchases Ret. and Allow.

Income Summary

Income Summary

Sales Discount

Sales Returns and Allow.

Purchases

Advertising Expense

Cash Short and Over

Credit Card Fee Expense

Depr. Exp.—Office Equipment

Depr. Exp.—Store Equipment

Insurance Expense

Miscellaneous Expense

Payroll Taxes Expense

Rent Expense

Salary Expense

Supplies Expense—Office

Supplies Expense—Store

Uncollectible Accounts Expense

Utilities Expense

Federal Income Tax Expense

Income Summary

Retained Earnings

Retained Earnings

Dividends

724 1 8 3 99

3 4 1 8 47

4 6 8 4 69

641 7 7 7 81

91 9 9 2 94

20 0 0 0 00

732 2 8 7 15

1 6 9 4 48

4 1 8 9 64

331 8 0 5 18

14 5 1 8 00

4 60

12 1 8 0 00

3 5 8 0 00

6 1 4 0 00

7 2 0 0 00

6 4 8 1 00

14 1 8 4 60

20 1 5 0 00

168 4 8 3 60

5 8 4 7 10

4 9 1 8 50

3 5 6 0 00

5 4 8 4 97

31 3 5 6 14

91 9 9 2 94

20 0 0 0 00

4110

5120

5130

3140

3140

4120

4130

5110

6105

6110

6115

6120

6125

6130

6135

6140

6145

6150

6155

6160

6165

6170

7105

3140

3120

3120

3130

Closing Entries

BTE_Ch16-425-465.qxd 11/9/07 9:05 PM Page 441 SECOND REVISED

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING442 • Working Papers TE

APPLICATION PROBLEM (continued)16-4

2., 4. GENERAL LEDGER

ACCOUNT NO. 1110

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 15 4 8 2 00

POST.REF.

✔20 – –

ACCOUNT Cash

DEBIT CREDIT

ACCOUNT NO. 1120

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 5 0 0 00

POST.REF.

✔20 – –

ACCOUNT Petty Cash

DEBIT CREDIT

ACCOUNT NO. 1130

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 42 1 5 8 80

POST.REF.

✔20 – –

ACCOUNT Accounts Receivable

DEBIT CREDIT

ACCOUNT NO. 1135

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

3 5 6 0 00

6 8 4 20

4 2 4 4 20

POST.REF.

✔

G22

20 – –

ACCOUNT Allow. for Uncoll. Accts.

DEBIT CREDIT

ACCOUNT NO. 1140

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

1 4 8 3 60

274 5 3 5 33

276 0 1 8 93

POST.REF.

✔

G22

20 – –

ACCOUNT Merchandise Inventory

DEBIT CREDIT

BTE_Ch16-425-465.qxd 11/9/07 9:05 PM Page 442 SECOND REVISED

Name Date Class

APPLICATION PROBLEM (continued)16-4

Chapter 16 Recording Adjusting and Closing Entries for a Corporation • 443

ACCOUNT NO. 1145

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

5 8 4 7 10

6 1 5 8 84

3 1 1 74

POST.REF.

✔

G22

20 – –

ACCOUNT Supplies—Office

DEBIT CREDIT

ACCOUNT NO. 1150

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

4 9 1 8 50

5 5 4 8 55

6 3 0 05

POST.REF.

✔

G22

20 – –

ACCOUNT Supplies—Store

DEBIT CREDIT

ACCOUNT NO. 1160

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

7 2 0 0 00

8 0 0 0 00

8 0 0 00

POST.REF.

✔

G22

20 – –

ACCOUNT Prepaid Insurance

DEBIT CREDIT

ACCOUNT NO. 1205

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 22 1 5 8 66

POST.REF.

✔20 – –

ACCOUNT Office Equipment

DEBIT CREDIT

ACCOUNT NO. 1210

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

3 5 8 0 00

4 8 4 8 00

8 4 2 8 00

POST.REF.

✔

G22

20 – –

ACCOUNT Acc. Depr. —Office Equipment

DEBIT CREDIT

ACCOUNT NO. 1215

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 34 1 5 8 11

POST.REF.

✔20 – –

ACCOUNT Store Equipment

DEBIT CREDIT

BTE_Ch16-425-465.qxd 11/9/07 9:05 PM Page 443 SECOND REVISED

APPLICATION PROBLEM (continued)16-4

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING444 • Working Papers TE

ACCOUNT NO. 1220

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

6 1 4 0 00

12 4 8 0 00

18 6 2 0 00

POST.REF.

✔

G22

20 – –

ACCOUNT Acc. Depr. —Store Equipment

DEBIT CREDIT

ACCOUNT NO. 2110

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 15 4 8 7 99

POST.REF.

✔20 – –

ACCOUNT Accounts Payable

DEBIT CREDIT

ACCOUNT NO. 2120

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 1 3 5 6 14 1 3 5 6 14

POST.REF.

G2220 – –

ACCOUNT Federal Income Tax Payable

DEBIT CREDIT

ACCOUNT NO. 2130

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 1 1 2 5 58

POST.REF.

✔20 – –

ACCOUNT Employee Income Tax Payable

DEBIT CREDIT

ACCOUNT NO. 2135

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 9 0 3 96

POST.REF.

✔20 – –

ACCOUNT Social Security Tax Payable

DEBIT CREDIT

ACCOUNT NO. 2140

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 2 1 1 41

POST.REF.

✔20 – –

ACCOUNT Medicare Tax Payable

DEBIT CREDIT

BTE_Ch16-425-465.qxd 11/9/07 9:05 PM Page 444 SECOND REVISED

Name Date Class

APPLICATION PROBLEM (continued)16-4

Chapter 16 Recording Adjusting and Closing Entries for a Corporation • 445

ACCOUNT NO. 2145

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 2 3 4 5 99

POST.REF.

✔20 – –

ACCOUNT Sales Tax Payable

DEBIT CREDIT

ACCOUNT NO. 2150

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 2 5 60

POST.REF.

✔20 – –

ACCOUNT Unemployment Tax Payable—Federal

DEBIT CREDIT

ACCOUNT NO. 2155

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 1 7 2 80

POST.REF.

✔20 – –

ACCOUNT Unemployment Tax Payable—State

DEBIT CREDIT

ACCOUNT NO. 2160

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 3 5 0 00

POST.REF.

✔20 – –

ACCOUNT Health Insurance Premiums Payable

DEBIT CREDIT

ACCOUNT NO. 2165

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 5 0 00

POST.REF.

✔20 – –

ACCOUNT U.S. Savings Bonds Payable

DEBIT CREDIT

ACCOUNT NO. 2170

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 6 0 00

POST.REF.

✔20 – –

ACCOUNT United Way Donations Payable

DEBIT CREDIT

BTE_Ch16-425-465.qxd 11/9/07 9:06 PM Page 445 SECOND REVISED

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING446 • Working Papers TE

APPLICATION PROBLEM (continued)16-4

ACCOUNT NO. 2180

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 5 0 0 0 00

POST.REF.

✔20 – –

ACCOUNT Dividends Payable

DEBIT CREDIT

ACCOUNT NO. 3110

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 125 0 0 0 00

POST.REF.

✔20 – –

ACCOUNT Capital Stock

DEBIT CREDIT

ACCOUNT NO. 3120

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 1

31

31

Balance

20 0 0 0 00

91 9 9 2 94

136 8 4 3 68

228 8 3 6 62

208 8 3 6 62

POST.REF.

✔

G23

G23

20 – –

ACCOUNT Retained Earnings

DEBIT CREDIT

ACCOUNT NO. 3130

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

20 0 0 0 00

20 0 0 0 00

POST.REF.

✔

G23

20 – –

ACCOUNT Dividends

DEBIT CREDIT

ACCOUNT NO. 3140

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

31

31

641 7 7 7 81

91 9 9 2 94

1 4 8 3 60

732 2 8 7 15

POST.REF.

G22

G23

G23

G23

20 – –

ACCOUNT Income Summary

DEBIT CREDIT

1 4 8 3 60

733 7 7 0 75

91 9 9 2 94

BTE_Ch16-425-465.qxd 11/9/07 9:06 PM Page 446 SECOND REVISED

Name Date Class

APPLICATION PROBLEM (continued)16-4

Chapter 16 Recording Adjusting and Closing Entries for a Corporation • 447

ACCOUNT NO. 4110

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

724 1 8 3 99

724 1 8 3 99

POST.REF.

✔

G23

20 – –

ACCOUNT Sales

DEBIT CREDIT

ACCOUNT NO. 4120

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

1 6 9 4 48

1 6 9 4 48

POST.REF.

✔

G23

20 – –

ACCOUNT Sales Discount

DEBIT CREDIT

ACCOUNT NO. 4130

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

4 1 8 9 64

4 1 8 9 64

POST.REF.

✔

G23

20 – –

ACCOUNT Sales Returns and Allowances

DEBIT CREDIT

ACCOUNT NO. 5110

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

331 8 0 5 18

331 8 0 5 18

POST.REF.

✔

G23

20 – –

ACCOUNT Purchases

DEBIT CREDIT

ACCOUNT NO. 5120

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

3 4 1 8 47

3 4 1 8 47

POST.REF.

✔

G23

20 – –

ACCOUNT Purchases Discount

DEBIT CREDIT

BTE_Ch16-425-465.qxd 11/9/07 9:06 PM Page 447 SECOND REVISED

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING448 • Working Papers TE

APPLICATION PROBLEM (continued)16-4

ACCOUNT NO. 5130

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

4 6 8 4 69

4 6 8 4 69

POST.REF.

✔

G23

20 – –

ACCOUNT Purch. Returns and Allowances

DEBIT CREDIT

ACCOUNT NO. 6105

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

14 5 1 8 00

14 5 1 8 00

POST.REF.

✔

G23

20 – –

ACCOUNT Advertising Expense

DEBIT CREDIT

ACCOUNT NO. 6110

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

4 60

4 60

POST.REF.

✔

G23

20 – –

ACCOUNT Cash Short and Over

DEBIT CREDIT

ACCOUNT NO. 6115

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

12 1 8 0 00

12 1 8 0 00

POST.REF.

✔

G23

20 – –

ACCOUNT Credit Card Fee Expense

DEBIT CREDIT

ACCOUNT NO. 6120

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

3 5 8 0 00

3 5 8 0 00

3 5 8 0 00

POST.REF.

G22

G23

20 – –

ACCOUNT Depr. Exp. —Office Equipment

DEBIT CREDIT

ACCOUNT NO. 6125

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

6 1 4 0 00

6 1 4 0 00

6 1 4 0 00

POST.REF.

G22

G23

20 – –

ACCOUNT Depr. Exp. —Store Equipment

DEBIT CREDIT

BTE_Ch16-425-465.qxd 11/9/07 9:06 PM Page 448 SECOND REVISED

Name Date Class

APPLICATION PROBLEM (continued)16-4

Chapter 16 Recording Adjusting and Closing Entries for a Corporation • 449

ACCOUNT NO. 6130

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

7 2 0 0 00

7 2 0 0 00

7 2 0 0 00

POST.REF.

G22

G23

20 – –

ACCOUNT Insurance Expense

DEBIT CREDIT

ACCOUNT NO. 6135

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

6 4 8 1 00

6 4 8 1 00

POST.REF.

✔

G23

20 – –

ACCOUNT Miscellaneous Expense

DEBIT CREDIT

ACCOUNT NO. 6140

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

14 1 8 4 60

14 1 8 4 60

POST.REF.

✔

G23

20 – –

ACCOUNT Payroll Taxes Expense

DEBIT CREDIT

ACCOUNT NO. 6145

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

20 1 5 0 00

20 1 5 0 00

POST.REF.

✔

G23

20 – –

ACCOUNT Rent Expense

DEBIT CREDIT

ACCOUNT NO. 6150

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

168 4 8 3 60

168 4 8 3 60

POST.REF.

✔

G23

20 – –

ACCOUNT Salary Expense

DEBIT CREDIT

ACCOUNT NO. 6155

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

5 8 4 7 10

5 8 4 7 10

5 8 4 7 10

POST.REF.

G22

G23

20 – –

ACCOUNT Supplies Expense—Office

DEBIT CREDIT

BTE_Ch16-425-465.qxd 11/9/07 9:06 PM Page 449 SECOND REVISED

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING450 • Working Papers TE

APPLICATION PROBLEM (continued)16-4

ACCOUNT NO. 6160

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

4 9 1 8 50

4 9 1 8 50

4 9 1 8 50

POST.REF.

G22

G23

20 – –

ACCOUNT Supplies Expense—Store

DEBIT CREDIT

ACCOUNT NO. 6165

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

3 5 6 0 00

3 5 6 0 00

3 5 6 0 00

POST.REF.

G22

G23

20 – –

ACCOUNT Uncollectible Accounts Expense

DEBIT CREDIT

ACCOUNT NO. 6170

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

5 4 8 4 97

5 4 8 4 97

POST.REF.

✔

G23

20 – –

ACCOUNT Utilities Expense

DEBIT CREDIT

ACCOUNT NO. 7105

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

31

Balance

1 3 5 6 14

31 3 5 6 14

30 0 0 0 00

31 3 5 6 14

POST.REF.

✔

G22

G23

20 – –

ACCOUNT Federal Income Tax Expense

DEBIT CREDIT

BTE_Ch16-425-465.qxd 11/9/07 9:06 PM Page 450 SECOND REVISED

Name Date Class

APPLICATION PROBLEM (concluded)16-4

5.

Chapter 16 Recording Adjusting and Closing Entries for a Corporation • 451

Cash

Petty Cash

Accounts Receivable

Allow. for Uncoll. Accts.

Merchandise Inventory

Supplies—Office

Supplies—Store

Prepaid Insurance

Office Equipment

Acc. Depr.—Office Equipment

Store Equipment

Acc. Depr.—Store Equipment

Accounts Payable

Federal Income Tax Payable

Employee Income Tax Payable

Social Security Tax Payable

Medicare Tax Payable

Sales Tax Payable

Unemployment Tax Payable—Federal

Unemployment Tax Payable—State

Health Insurance Premiums Payable

U.S. Savings Bonds Payable

United Way Donations Payable

Dividends Payable

Capital Stock

Retained Earnings

Totals

Wilson Paint, Inc.

Post-Closing Trial Balance

December 31, 20 – –

CREDITDEBITACCOUNT TITLE

15 4 8 2 00

5 0 0 00

42 1 5 8 80

276 0 1 8 93

3 1 1 74

6 3 0 05

8 0 0 00

22 1 5 8 66

34 1 5 8 11

392 2 1 8 29

4 2 4 4 20

8 4 2 8 00

18 6 2 0 00

15 4 8 7 99

1 3 5 6 14

1 1 2 5 58

9 0 3 96

2 1 1 41

2 3 4 5 99

2 5 60

1 7 2 80

3 5 0 00

5 0 00

6 0 00

5 0 0 0 00

125 0 0 0 00

208 8 3 6 62

392 2 1 8 29

BTE_Ch16-425-465.qxd 11/9/07 9:06 PM Page 451 SECOND REVISED

MASTERY PROBLEM, pp. 502, 50316-5

Journalizing and posting adjusting and closing entries; preparing a post-closing trial balance

1., 2.

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING452 • Working Papers TE

GENERAL JOURNAL PAGE 18

DATE ACCOUNT TITLE DEBIT CREDITDOC.NO.

POST.REF.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

Dec.20 – –

31

31

31

31

31

31

31

31

Uncollectible Accounts Expense

Allowance for Uncollectible Accounts

Income Summary

Merchandise Inventory

Supplies Expense—Office

Supplies—Office

Supplies Expense—Store

Supplies—Store

Insurance Expense

Prepaid Insurance

Depreciation Expense—Office Equipment

Accumulated Depreciation—Office Equipment

Depreciation Expense—Store Equipment

Accumulated Depreciation—Store Equipment

Federal Income Tax Expense

Federal Income Tax Payable

2 1 2 0 00

3 4 8 8 14

3 1 4 8 66

5 3 4 8 84

6 0 0 0 00

3 5 8 0 00

6 1 4 0 00

9 6 5 64

2 1 2 0 00

3 4 8 8 14

3 1 4 8 66

5 3 4 8 84

6 0 0 0 00

3 5 8 0 00

6 1 4 0 00

9 6 5 64

6165

1135

3140

1140

6155

1145

6160

1150

6130

1160

6120

1210

6125

1220

7105

2120

Adjusting Entries

BTE_Ch16-425-465.qxd 11/9/07 9:06 PM Page 452 SECOND REVISED

Name Date Class

MASTERY PROBLEM (continued)16-5

3., 4.

Chapter 16 Recording Adjusting and Closing Entries for a Corporation • 453

GENERAL JOURNAL PAGE 19

DATE ACCOUNT TITLE DEBIT CREDITDOC.NO.

POST.REF.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

Dec.20 – –

31

31

31

31

Sales

Purchases Discount

Purchases Ret. and Allow.

Income Summary

Income Summary

Sales Discount

Sales Returns and Allow.

Purchases

Advertising Expense

Cash Short and Over

Credit Card Fee Expense

Depr. Exp.—Office Equipment

Depr. Exp.—Store Equipment

Insurance Expense

Miscellaneous Expense

Payroll Taxes Expense

Rent Expense

Salary Expense

Supplies Expense—Office

Supplies Expense—Store

Uncollectible Accounts Expense

Utilities Expense

Federal Income Tax Expense

Income Summary

Retained Earnings

Retained Earnings

Dividends

514 8 1 5 35

2 1 5 4 65

2 8 8 9 41

488 2 3 2 65

28 1 3 8 62

16 0 0 0 00

519 8 5 9 41

2 1 5 4 94

6 1 8 4 74

301 5 4 8 60

2 4 9 1 95

5 25

8 1 5 4 62

3 5 8 0 00

6 1 4 0 00

6 0 0 0 00

4 1 0 00

14 1 8 4 60

15 4 0 0 00

102 2 4 0 30

3 1 4 8 66

5 3 4 8 84

2 1 2 0 00

4 1 5 4 51

4 9 6 5 64

28 1 3 8 62

16 0 0 0 00

4110

5120

5130

3140

3140

4120

4130

5110

6105

6110

6115

6120

6125

6130

6135

6140

6145

6150

6155

6160

6165

6170

7105

3140

3120

3120

3130

Closing Entries

BTE_Ch16-425-465.qxd 11/9/07 9:06 PM Page 453 SECOND REVISED

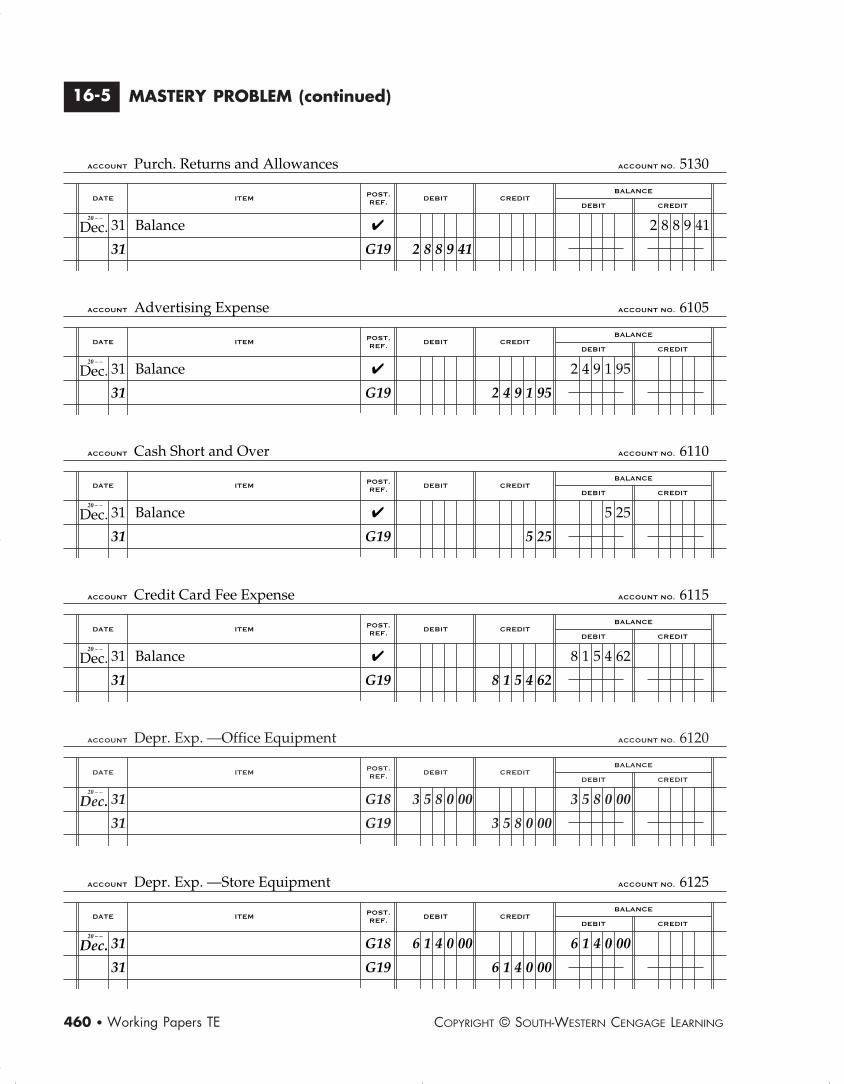

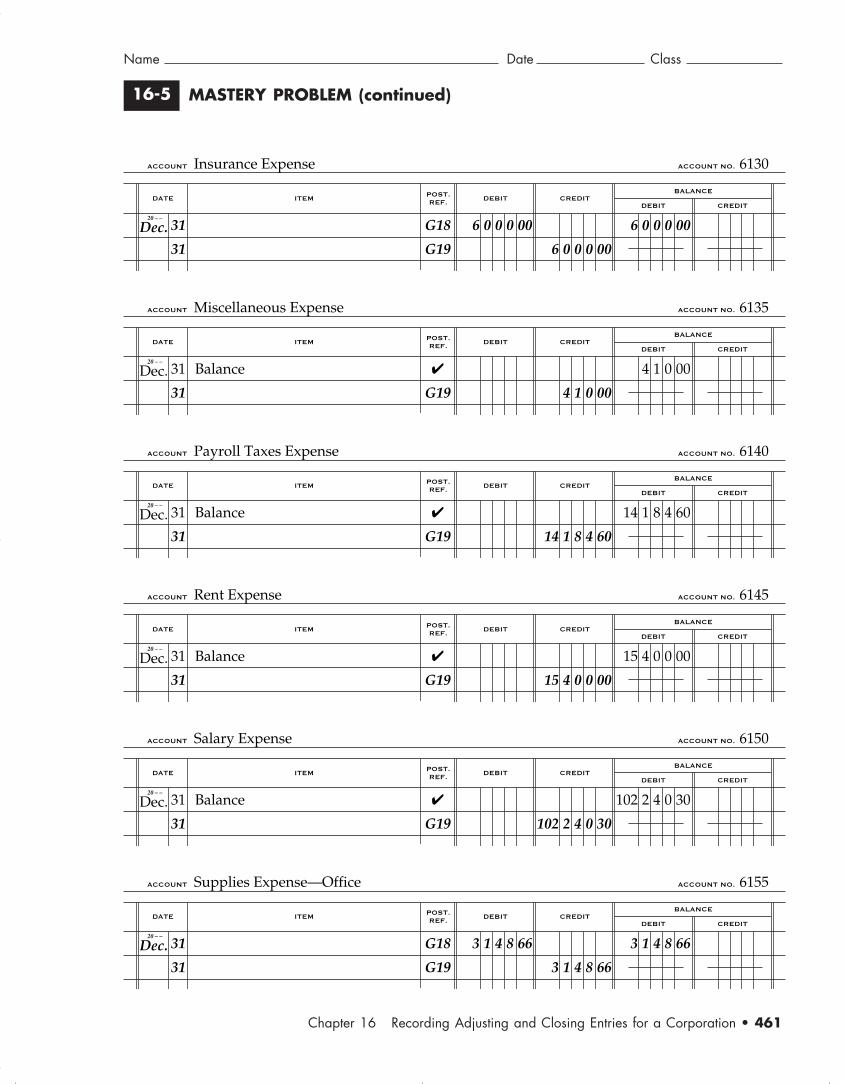

MASTERY PROBLEM (continued)16-5

2., 4. GENERAL LEDGER

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING454 • Working Papers TE

ACCOUNT NO. 1110

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 5 1 2 4 12

POST.REF.

✔20 – –

ACCOUNT Cash

DEBIT CREDIT

ACCOUNT NO. 1120

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 2 5 0 00

POST.REF.

✔20 – –

ACCOUNT Petty Cash

DEBIT CREDIT

ACCOUNT NO. 1130

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 14 8 4 3 30

POST.REF.

✔20 – –

ACCOUNT Accounts Receivable

DEBIT CREDIT

ACCOUNT NO. 1135

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

2 1 2 0 00

1 2 4 55

2 2 4 4 55

POST.REF.

✔

G18

20 – –

ACCOUNT Allow. for Uncoll. Accts.

DEBIT CREDIT

ACCOUNT NO. 1140

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

3 4 8 8 14

154 3 1 8 22

150 8 3 0 08

POST.REF.

✔

G18

20 – –

ACCOUNT Merchandise Inventory

DEBIT CREDIT

BTE_Ch16-425-465.qxd 11/9/07 9:06 PM Page 454 SECOND REVISED

Name Date Class

MASTERY PROBLEM (continued)16-5

Chapter 16 Recording Adjusting and Closing Entries for a Corporation • 455

ACCOUNT NO. 1145

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

3 1 4 8 66

3 4 1 5 58

2 6 6 92

POST.REF.

✔

G18

20 – –

ACCOUNT Supplies—Office

DEBIT CREDIT

ACCOUNT NO. 1150

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

5 3 4 8 84

6 1 8 4 56

8 3 5 72

POST.REF.

✔

G18

20 – –

ACCOUNT Supplies—Store

DEBIT CREDIT

ACCOUNT NO. 1160

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

6 0 0 0 00

7 0 0 0 00

1 0 0 0 00

POST.REF.

�

G18

20 – –

ACCOUNT Prepaid Insurance

DEBIT CREDIT

ACCOUNT NO. 1205

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 21 4 8 2 66

POST.REF.

✔20 – –

ACCOUNT Office Equipment

DEBIT CREDIT

ACCOUNT NO. 1210

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

3 5 8 0 00

6 4 8 0 00

10 0 6 0 00

POST.REF.

✔

G18

20 – –

ACCOUNT Acc. Depr. —Office Equipment

DEBIT CREDIT

ACCOUNT NO. 1215

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 40 4 8 1 66

POST.REF.

✔20 – –

ACCOUNT Store Equipment

DEBIT CREDIT

BTE_Ch16-425-465.qxd 11/9/07 9:06 PM Page 455 SECOND REVISED

COPYRIGHT © SOUTH-WESTERN CENGAGE LEARNING456 • Working Papers TE

MASTERY PROBLEM (continued)16-5

ACCOUNT NO. 1220

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31

31

Balance

6 1 4 0 00

18 4 8 0 00

24 6 2 0 00

POST.REF.

✔

G18

20 – –

ACCOUNT Acc. Depr. —Store Equipment

DEBIT CREDIT

ACCOUNT NO. 2110

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 8 4 1 8 36

POST.REF.

✔20 – –

ACCOUNT Accounts Payable

DEBIT CREDIT

ACCOUNT NO. 2120

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 9 6 5 64 9 6 5 64

POST.REF.

G1820 – –

ACCOUNT Federal Income Tax Payable

DEBIT CREDIT

ACCOUNT NO. 2130

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 4 5 8 00

POST.REF.

✔20 – –

ACCOUNT Employee Income Tax Payable

DEBIT CREDIT

ACCOUNT NO. 2135

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 5 2 8 24

POST.REF.

✔20 – –

ACCOUNT Social Security Tax Payable

DEBIT CREDIT

ACCOUNT NO. 2140

DATE ITEMBALANCE

DEBIT CREDIT

Dec. 31 Balance 1 2 3 54

POST.REF.

✔20 – –

ACCOUNT Medicare Tax Payable

DEBIT CREDIT