study: brazil and germany: a 21st-century relationship

TRANSCRIPT

Brazil and Germany:

A 21st-Century RelationshipOpportunities in Trade, Investment and Finance

Brazil and Germany:

A 21st-Century RelationshipOpportunities in Trade, Investment and Finance

Viviane Maria Bastos, Andreas Esche, Renato Flores, Samuel George, Antonio Carlos Porto Gonçalves, Thieß Petersen and Thomas Rausch

5

Table of Contents

Table of Contents

Introduction 7

ChapterI: Trade 11

1. AComplimentaryRelationshipwithRoomForGrowth 12

2. TheDriversofTrade 12

3. GermanandBrazilianTradePolicy 16

4. OverviewofBrazilian-GermanBilateralTrade 18

5. ComplicationsinBrazilian-German-Trade 20

6. TowardsaMercosul–EUFTA? 21

7. 21stCenturyOpportunitiesfora21stCenturyRelationship 24

ChapterII:CapitalFlows&Investment 26

1. TheMicroeconomicsofInternationalFinancialFlows 27

2. DirectInvestmentandPortfolioInvestmentfromAbroad,

inBrazilandinGermany 30

3. TheMacroeconomicsofInternationalFinancialFlows 36

ChapterIII:Recommendations 43

1. AFocusonBilateralDirectInvestment 44

2. HarmonizingMonetaryPolicy 45

3. TowardsanAgreementonMigration 47

4. Findingthecommongroundontradepolicy 48

5. Brazil&GermanyasLeadersinEU-MercosulFreeTradeRelations 49

MovingForward:FindingtheCommonGround 51

WorksCited 52

GlobalEconomicDynamics(GED) 56

6

Brazilian-German Trade and Finance: Complements and Caveats

Brazilian-German Trade and Finance: Complements and Caveats

ComplementsEndowment: Natural resources

Brazil is abundantly endowed in natural resources and land, whereas Germany is poor in the first and relatively poor in the second. Therefore, Brazilian exports of natural resources are welcome in Germany, which depends on importing raw materials from abroad.

Endowment: Labor Germany is relatively abundant in skilled labor and less so in unskilled labor. Hence, Germany holds a comparative advantage in producing goods and services that require advanced labor. Meanwhile, populous Brazil is working to improve its education system. Thus Brazil and Ger-many are not competitors with respect to products that either require significant skilled labor or rely upon unskilled labor.

Endowment: Capital and current account balances

In order to enlarge the Brazilian capital stock, large investments are necessary. Brazil’s savings are not large enough to finance domestic investment. Germany has a high income level, high saving rate and current account surplus. Germany’s savings (and current account surplus) are therefore available to finance Brazil’s investment (and current account deficit).

CaveatsContext of trade policy Brazilian and German trade policies are firmly rooted in differences between the countries’

long-standing institutional structures and mind-sets. Brazil’s trade policy places a high pre-mium on developing national industries and promoting the interests of developing countries. Germany’s economic policy is traditionally export-oriented and strongly intertwined with its European neighbors, to the degree that there is no independent German trade policy, only German interests that contribute to the formulation of the EU’s trade policy. These separate approaches can lead to differing trade strategies.

Agricultural products Brazil holds a comparative advantage in many agricultural products, which implies a disadvantage for German producers. German farmers, in turn, are being protected through restrictions and subsidies of the EU’s common agricultural policy. These measures are an object of consistent dispute.

Export-oriented job creation

Both countries have a strong interest in obtaining and maintaining high levels of employment. Increasing exports are a key instrument to satisfy this goal, especially for Germany. As a result, both countries pursue high exports and, consequently, current account surpluses. As all coun-tries cannot simultaneously have current account surpluses, Germany’s surplus might sooner or later become an object of dispute.

Desired outcomes Although Brazil and Germany share the common aim to increase employment by foreign trade activities, they differ with respect to deeper desired outcomes of trade. In Brazil, fighting poverty, increasing the material prosperity of the population and importing technological knowledge are of greater importance than in Germany. In Germany, economic growth and full employment are the primary goals of trade.

Terms of trade and wealth

If the terms of trade of one country rise, that country receives a larger quantity of imported goods for a given bundle of exported goods. Therefore, an increase in the terms of trade of an economy has a positive impact on the wealth of the country. However, given the contrasting export portfolios, an improvement in Brazilian terms of trade would imply a reduction to German terms of trade (and vice versa). This represents an irresolvable trade-off.

Exchange rate policy The real depreciation of the domestic currency has a positive impact on the volume of a country’s exports. If, for example, Brazil tries to increase its exports by devaluing its currency, the result is a relative appreciation of Germany’s currency, which has a negative impact on German exports. As a result, there is another irresolvable trade-off if both countries try to incre-ase exports by devaluing their currencies. However, as a member of the eurozone, Germany has limited influence on the exchange rate.

7

Introduction

Introduction

Onthesurface, itwouldseemthatBrazilandGermanypresentmanyopportunitiesforfruitful

bilateral trade and investment. In terms of comparative advantages, the Brazilian export

portfolio tacksheavilytowardspreciselytherawmaterialsGermanmanufacturersrequire—and

lack domestically. Conversely, German producers specializing in high-end technological and

knowledge-basedgoodscouldfindanexpandingconsumerbasebothintheburgeoningBrazilian

middleclassandinbusiness-to-businesstradewithBrazilianpartners.Intermsof investment,

BrazilwouldappeartobeaprimedestinationforsurplusGermansavings.Forexample,Brazil

facesaninfrastructuredeficitwhileGermanfirmshaveachievedparticularsophisticationinthis

field.ForGermanfirms,investmentinthissectorinBrazilcanofferreturnscurrentlyunavailable

incontinentalEurope.

To an extent, the statistics reflect the growing opportunities between the two. As this study

demonstrates,bothbilateraltradeandinvestmenthaveincreasedinrecentyears.Nevertheless,

the relationship has yet to reach its full potential. Politics and policies have curtailed trade

expansion.Brazil’smembership in theMercosul tradeblocandGermany’smembership in the

EuropeanUnionhavehamperedthepair’sabilitytoforwardabilateraltradeagreement,aseach

blocmaintainscertaindefensivepositions that limit theother fromexercising its comparative

advantages. Capital flows between the two countries—especially long-term foreign direct

investments—remainunderwhelming.

Thispaper,jointlyauthoredbyeconomistsandpoliticalscientistsfromtheBertelsmannStiftung

ofGermanyandtheFundaçãoGetúlioVargasofBrazil,reviewseconomicrelationsbetweenthe

two countries with a particular focus on highlighting the opportunities while addressing the

bottlenecksthatslowbilateraltradeandinvestment.Thetextisorganizedasfollows:

• ChapterI,authoredprimarilybyspecialistsfromtheBertelsmannStiftung,reviewsthestate

ofBrazilian-Germantrade.Thechapterreviewseachcountry’sdriversoftradeaswellaseach

country’stradepolicies.Itcontinuestoanalyzethenatureofthebilateraltradeitself,aswellas

policyissuesthatpreventfurthertrade.ThechapterthenreviewsprogressonaMercosul-EU

freetradeagreement,andconcludesbyconsidering21stcenturytradeopportunities.

• ChapterII,authoredprimarilybyspecialistsfromtheGetúlioVargasFoundation,considers

investment, comparing German and Brazilian capital flows against what traditional theory

predicts.Thechapterdistinguishesbetweenmoretransientportfolioinvestmentandlonger-

termforeigndirectinvestment.Italsoreviewshowalackofharmonizationinmacroeconomic

policycanleadtodistortionsinfinancialflows.

8

Introduction

• ChapterIIIattemptstodrawtangibleandactionablerecommendationsbasedonthefirsttwo

chapters.This chapter accepts thatGermanyandBrazilmaypursuedifferingpolicies, and

areconstrainedbytheirrespectiveregionalblocs,butitarguesthatcommongroundexists.

Forthcomingpolicycanbegearedtowardsthiscommonground.

Inthe21stcentury,neitheremergingmarketsnordevelopedcountriesalonecansustainglobal

growth.Rather,itwillbetheinteractionbetweentheknowledgeofadvancedeconomiesandthe

dynamismsofemergingeconomiesthatwillmostlikelymotorglobalgrowth.WebelieveBrazil

andGermanycanbeattheforefrontofthisinteraction.

This text represents the outcome of a year-long collaboration between Bertelsmann Stiftung

and the Fundação Getúlio Vargas. Moving forward, both sides are dedicated to continuing the

explorationofbilateraltiesbetweenBrazilandGermanyandtohelpingbuildatruly21stcentury

relationship.

Priortoaddressingthefutureoftherelationship,thisintroductionfirstoffersaperspectiveonthe

pastandthepresent.

Brazil and Germany: Two countries with strong historical ties

BilateralrelationsbetweenBrazilandGermanyarelong-standingandcomprehensive.Thehistory

ofGermanimmigrationtoBraziltracesbacktothe16thcentury.Thisimmigrationincreasedat

thebeginningofthe19thcentury;from1872through1939,nearly200,000Germansimmigrated

toBrazil.Thistidereachedanapexbetween1920and1929,when76,000Germanscrossedthe

Atlantic to Brazil. In the 1940s and 1950s, people of German origin accounted for roughly 20

percentofthepopulationinsomeBrazilianstates,suchasSantaCatarinaandRioGrandedoSul

(seeGregory,2013,pp.114–121).

Thesestrongtiesresultedinanintensivebilateraleconomicpartnershipstartinginthesecond

halfofthe1950s.In1954,forexample,theGermansteelcompanyMannesmannbeganoperations

inBrazil.In1955,Sofunge,whichlaterbecameapartofMercedes-Benz,didthesame.German

automakerVolkswagenopenedaplantin1959.Inthe1970s,Germancommitmentreacheditspeak

whenGermancompaniesfromheavyindustry,chemicalindustry,machinery,plantengineering

andtheautomobileindustryinvestedlargesumsofmoneyinBrazilandestablishednumerous

plants.Duringthe1980s,Germancompaniesandinvestorsreducedtheirinvolvementsbecause

oftheeconomicdownturninBrazil.Nevertheless,atpresentthereareabout1,600companiesin

BrazilwithGermancapital,andGermanchambersofcommerceinSaoPaulo,RiodeJaneiroand

PortoAlegre(seeLohbauer,2013,pp.133–135and144–145).

9

Introduction

Thereisalsoastrongtraderelationshipbetweenbothcountries.Brazilisbyfarthemostimportant

LatinAmericantradingpartnerforGermany,whileGermanyisatpresentthefifthorsixthmost

importanttradingpartnerforBrazil,behindChina,theUS,Argentina,theNetherlandsandJapan

(seeLohbauer,2013,p.144).

RelationsbetweenBrazil andGermanyarenot restricted to economic ties. Formore than140

years,thetwohavebeenlinkedbyactivebilateraldiplomaticrelations.Peopleinbothcountries

share important values, most notably for democracy and corresponding institutions. Bilateral

cooperation has occurred on issues including education, culture (there are, for example, five

Goethe-Instituts inBrazil),scienceandtechnology,climatechangeandenvironment, laborand

socialaffairs,energyandinternationalcrisismanagement.

Theseextensiveconnectionsformasoundbaseofmutualtrust,respectandsupportthatserves

asthefoundationforanexpansionofbilateraleconomicrelationstothebenefitofbothcountries.

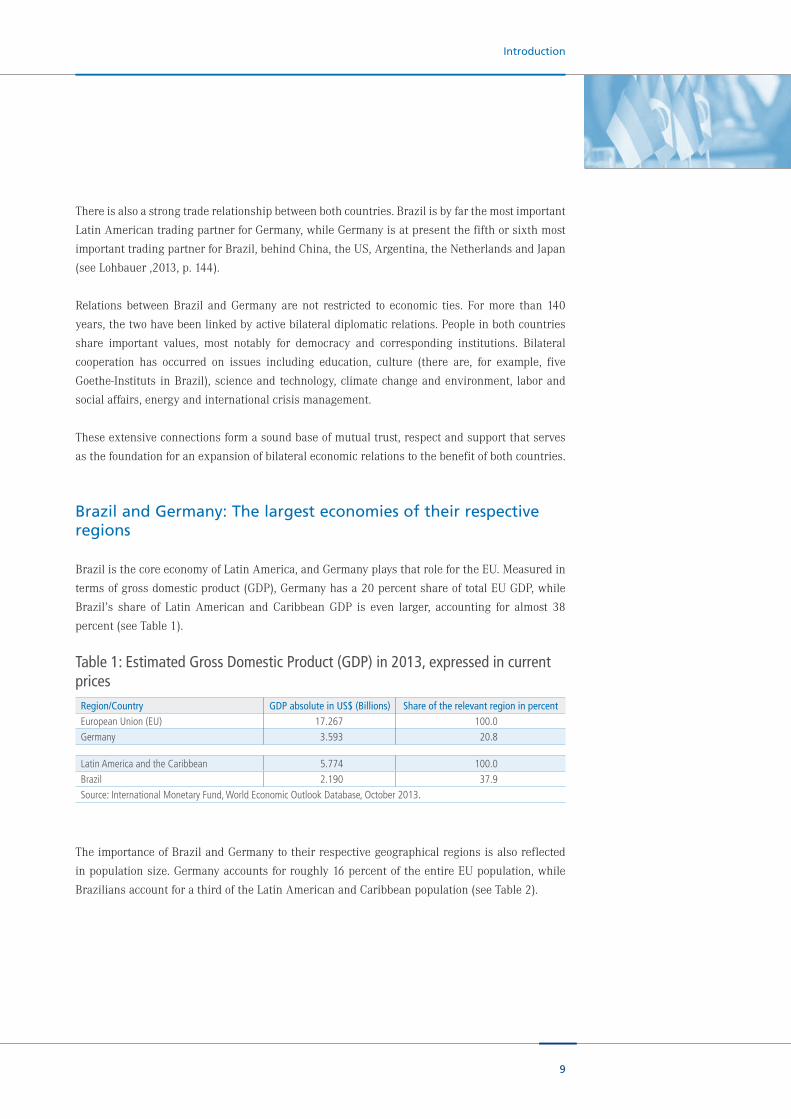

Brazil and Germany: The largest economies of their respective regions

BrazilisthecoreeconomyofLatinAmerica,andGermanyplaysthatrolefortheEU.Measuredin

termsofgrossdomesticproduct(GDP),Germanyhasa20percentshareoftotalEUGDP,while

Brazil’s share of Latin American and Caribbean GDP is even larger, accounting for almost 38

percent(seeTable1).

TheimportanceofBrazilandGermanytotheirrespectivegeographicalregionsisalsoreflected

inpopulationsize.Germanyaccountsforroughly16percentoftheentireEUpopulation,while

BraziliansaccountforathirdoftheLatinAmericanandCaribbeanpopulation(seeTable2).

Table 1: Estimated Gross Domestic Product (GDP) in 2013, expressed in current prices

Region/Country GDP absolute in US$ (Billions) Share of the relevant region in percentEuropean Union (EU) 17.267 100.0 Germany 3.593 20.8

Latin America and the Caribbean 5.774 100.0 Brazil 2.190 37.9 Source: International Monetary Fund, World Economic Outlook Database, October 2013.

10

Introduction

Henceduetotheireconomicstrength,BrazilandGermanycanbeconsideredanchoreconomies

forLatinAmericaandtheEuropeanUnion.

Table 2: Population, expressed in millionsRegion/Country Population mid-2013 Share of the relevant region in percentEuropean Union (EU) 506.0 100.0 Germany 80.6 15.9

Latin America and the Caribbean 606.0 100.0 Brazil 195.5 32.3 Source: World Population Reference Bureau: World Population Data Sheet 2013, p. 8–11.

11

Chapter I: Trade

Chapter I:

Trade

1. A Complementary Relationship with Room for Growth 2. The Drivers of Trade 3. German and Brazilian Trade Policy 4. Brazilian-German Trade 5. Complications in Brazilian-German Trade 6. Towards a Mercosul – EU Free Trade Agreement? 7. 21st-Century Opportunities for a 21st-Century Relationship

12

Chapter I: Trade

Chapter I: Trade

This chapter reviews thedrivers of trade forBrazil andGermany, aswell as theopportunities

inherentinthepair’sbilateraltraderelationship.Section 1offersabriefoverviewofBraziland

Germany’s complementary relationship with room for growth, while Section 2 considers the

driversoftradeforbothcountries.Section 3reviewsGermanandBraziliantradepolicy,which,

inturn,influencesSection 4,whichanalyzesactualGerman-Braziliantrade.Section 5considers

thecomplicationsofthattrade,whiletheSection 6reviewsprogresstowardsaMercosul-EUFree

TradeAgreement(FTA).

1. A Complementary Relationship With Room for Growth

TheBrazilian-Germantraderelationshipismutuallybeneficialandgrowing.Burgeoningcommerce

stemsfromcompatibleexportportfoliosandnationalendowments.GermandemandforBrazilian

rawmaterialsismatchedbyBraziliandemandforhigh-qualitygoodsmanufacturedinGermany.

Germany offers Brazil diversification away from predominant partners such as China and the

US,aswellasaccesstocapitalandcutting-edgetechnology.Meanwhile,BraziloffersGermanya

modicumofresourcesecurity,aswellasaccesstoamassiveandrapidlyexpandingmiddleclass

whosemembersarepotentialcustomersforGermanindustrialgoods.

Unfortunately,thetraderelationshipisnotdictatedbyeconomicsalone.Inbothcountries,trade

policyispartiallyshapedbypoliticalandinstitutionalfactorsthatmaymakethepathtoimproving

therelationshipmorecomplicatedthansimplyincreasingbilateralinvestment.

2. The Drivers of Trade

Drivers of Brazilian Foreign Trade

DeterminingBrazil’s factorendowmentsismoredifficult thaninitsregion’s lesseconomically

dynamiccountries,suchasArgentinaandChile,becauseofBrazil’s large,complexportfolioof

imports and exports (Muriel and Terra, 2009). Moreover, the country’s true abundances and

deficiencieshavemost likelybeenobscuredorat leastdistortedbyyearsofprotectionist trade

policy.

Despitethiscaveat,certainfactortrendsareclear.Inparticular,Brazilenjoysstrongendowments

inlaborandespeciallylandandnaturalresources.Withapopulationofmorethan200million

andastill-developingschoolsystem,Brazilmaintainsfactorabundanceinunskilledlabor.This

abundanceisoftenexploitedthroughagriculturallaborsuchascoffeecultivation.Brazil,which

isthefifthlargestcountryintheworldbyareabuthasarelativelylowpopulationdensity,clearly

13

Chapter I: Trade

hasanabundanceofland.Itisrichinnaturalresources,includingfertileland,minerals,waterand

forests.Braziliantradepatternsalsoindicateadegreeofcapital.MurielandTerrapositthatthis

capitalcouldreflectinteractionswithevenless-developedcountries,oraresidualdistortionfrom

theimportsubstitutionindustrialization(ISI)period.

In Brazil, the volume and structure of exports is heavily influenced by an abundance of raw

resources, high commodity prices and strong global growth levels. Brazil is rich in mineral

resources such as iron ore and agricultural products such as soybeans that are vital for large

emergingmarkets,specificallythosepursuinganurbanizationstrategysuchasChina.Emerging-

marketgrowthand,subsequently,strongcommoditypriceshavebeendriversofBrazilianexports

in the21stcentury.Beyondcertainniche industriessuchasEmbraeraircraft,Brazilianexport

expansioninrecentyearshasbeenpushedbyglobaldemandforrawmaterials.

Brazilianimportsaretypicallydrivenbytheneedtosupplydomesticmanufacturerswithparts,

aswellastheneedtosatisfyBraziliandemandformanufacturedgoodsbeyondthecapacitiesof

domesticfirms.Stronggrowthinformalemploymentandrealwages,combinedwithinitiatives

such as the conditional cash transfer program Bolsa Familia, have lifted tens of millions of

Braziliansfrompovertyandhavecreatedagrowinglower-middleandmiddleclassofconsumers

whocannowaffordimportedmanufacturedgoods.Therecenteconomicgrowthhasalsofostered

anupperclasskeenonhigh-endEuropeanimports.

Brazil’sendowmentweaknessappearstolieinitsrelativelackofskilledlabor,suchasengineers.

Hereit isimportanttodrawregionaldistinctions,asBrazil’slaborendowmentisdifferentiated

acrossthecountry.UrbancenterssuchasSãoPauloandRiodeJaneiromayhavemoreaccessto

skilledlabor.Otherareas,suchasthenorthandthenortheast,arelackinginit.Overall,Brazil

is experiencing a shortage of skilled labor in important industries such as infrastructure and

resourceextraction.

Regardingoverallcompetitiveness,Brazilhasdemonstratedtremendouspotentialbut lingering

inefficiencies.Thecountryishometoasophisticatedbusinesscommunityandhastheadvantages

of a massive internal market. But its competitiveness is hindered by, among other things,

infrastructuredeficienciesthatcostBrazilianbusinessesbillionsofdollarsannually.1

1 Accordingtoa2010MorganStanleyBluePaper,Brazilianfieldsproducegraintwiceasfastastherestoftheworld,butgettingthatgraintoportacrossunpavedroadscancostalmosthalfitsvalue.Meanwhile,vastmineraldepositsremainburieddeepwithin the earth for want of railroads to transport the goods. Statistics support these anecdotes. The paper found the thatBrazilianinfrastructureinvestmenthasbeenonaconsistentdecline,from5.4percentofGDPinthe1970sdownto2.1percentinthe2000s—onlyslightlyabovetheestimated2.0percentrequiredtosimplymaintaintheexistinginfrastructurestock(SeePaiva2010).Asa result, theWorldEconomicForum’sGlobalCompetitivenessReport2013–2014 ranksBrazil114thof148countriesinqualityofoveralltransportinfrastructure(WorldEconomicForum2013).

14

Chapter I: Trade

Drivers of German Foreign Trade

In Germany the volume and structure of exports and imports are mainly determined by an

abundance of capital, a well-trained work force, favorable unit labor costs, a high standard of

scientificandtechnicalknowledge,supply-chainintegrationwithinEuropeandthelackofnatural

resources. Hence the German economy depends on importing raw materials from abroad and

exportingmanufacturedproductsthatcontainahighdegreeofhumanandphysicalcapital.

Germanyhasahighlyskilledandspecializedlaborforce,whichcaninparticularbeattributedtothe

country’ssystemofvocationaleducation.This“dualeducationsystem”combinesapprenticeships

inacompanywithtraininginvocationalschools.Asaresult,Germanycanbedescribedasan

economythatiswellendowedinskilledlaborbutrelativelypoorlyendowedinunskilledlabor.

Thusthecountryexportsgoodsandservicesproducedwiththehelpofskilledlaborandimports

productsfromabroadthatrequireunskilledlabor.Intermsofcapital,Germanycanbeclassified

asacapital-richcountry,andthereforetheoreticallymeanttoexportcapital-intensivegoodsand

services.

Another driver of the volume and structure of German exports is the country’s high level of

technology, which allows Germany to export high-tech products, knowledge and technology-

intensivegoodsandservices.One indicatorofGermantechnologicalprowess is thenumberof

annualpatentapplications.In2009,Germanyrankedfifthinthenumberofpatentapplicationsper

onemillionemployedpersons,aheadofallotherlargeindustrialcountries(Expertenkommission

ForschungundInnovation,2012).

Despite being labor-poor in a global context, Germany benefits from favorable labor costs per

unit.Thoughit isahigh-wagecountry,growthofwagesoverthepast15yearshasbeenlower

thaninotherdevelopedeconomies.Therestraintonwagesisrootedprimarilyinaperiodofhigh

unemploymentandstructuralreformofthelabormarketinthe2000s,aswellasaweakeningof

thebargainingpowerofGermanunions.

Followingreunificationin1990,unemploymentinGermanyreacheddoubledigitsby1994and

remained elevated for more than a decade. Persistent high unemployment and the increasing

possibility of outsourcing jobs to Central and Eastern Europe exhorted significant downward

pressureonGermanrealwages.Inresponsetothecontinuingemploymentcrisis,thegovernment,

underChancellorGerhardSchröder,enactedasetof labormarketreformsaimedat increasing

participationinthelaborforcebyallowingformoreflexibleformsofemploymentandreducing

benefitstothelong-termjobless.Thesereformsalsoactedtoslowwagegrowth.Finally,andrelated

tothesestructuralchangesoftheGermaneconomy,theunionizationofthelaborforcedecreased

significantly.In1990,morethan11millionpeopleweremembersofaunion.By2011,membership

haddroppedto6.15million.

15

Chapter I: Trade

Another driver of German exports is its membership in the EU and the eurozone. Germany’s

central location in Europe and high degree of integration with neighboring countries through

thecommonEuropeanmarkethasledtostronggrowthinintra-industrytradebetweenGermany

and other European countries. German producers draw on asupply chain that includes firms

in many European countries and makes use of advantageous product specialization and cost

competitiveness(i.e.,lowerlaborcostsinCentralandEasternEurope).Themonetaryunionofthe

eurozonealsobenefitsGermancompetitivenessbypreventinganappreciationofthecurrency.

Inaseparatestudy,theBertelmannStiftungestimatesthatiftheseparateGermancurrencystill

existed,itwouldhaveappreciatedbyroughly23percent,whereasthecurrenciesoftheremaining

countries of the eurozone would have been devalued by an average of nearly seven percent

(Bertelsmann Stiftung, 2013a). Such an increase in relative prices would have had a negative

impact onGermanexports.At the same time,German importswouldhave increased.Beinga

memberof thesingleEuropeancurrency,Germanydoesnotsuffer fromanappreciationof its

currencybecausetheexportsofall17countriesusingtheeuroaremoreorlessbalancedtothe

imports–atleastuntil2011.

Evaluatingtheoverallcompetitiveness,Germanyisspecificallystronginmacroeconomicstability,

capacityforinnovation,quantityandqualityoflocalsuppliers,judicialindependence,intellectual

propertyprotectionandqualityofoverallinfrastructure.Germanymaintainsalargetradesurplus

andacurrentaccountsurplus.

Figure 1: Labor costs per unit across countries and times (index: labor costs per unit in the base year 2000 = 100)

Source: OECD, calculations of the Institute for the Study of Labor (IZA), Bonn.

UK Italy Canada

USA Germany OECD

France

60

70

80

90

100

110

120

130

140

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

2000

1999

1998

1997

1996

1995

1994

1993

1992

1991

1990

16

Chapter I: Trade

3. German and Brazilian Trade Policy

Brazilian Trade Policy

Braziliantradepolicyhashistoricallybeenprotectionist,datingbacktothe importsubstitution

industrialization (ISI) model of development employed during the middle of the 20th century.

Sincethemarket liberalizationof the1980s,Brazilhasembarkedonacourseofrelativetrade

openness, lowering tariffsunilaterally andpursuing regional trade integrationwithArgentina,

UruguayandParaguayviaMercosul.

ImplementationofBrazilian tradepolicy isoverseenby theMinistryofDevelopment, Industry

andTrade,theministerofwhichalsoservesasthechairmanoftheChamberofForeignTrade

(CAMEX).ThisbodywascreatedbythegovernmentofPresidentFernandoHenriqueCardosoin

1995toensuremulti-agencypolicycoordinationaswellastoadvisethepresident(Cantarinoda

CostaRamos,2010).AsamemberofMercosul,Brazilisrequiredtonegotiatenewtradeagreements

withtheregionalblocasawholeratherthanbilaterally.Afterbeingstalledforanumberofyears,

EU-Mercosulnegotiationsrestartedin2010.

Brazil’scurrenttradepolicystillhasattributesinheritedfromitsISIperiod,withanemphasison

protectionofimport-competingsectors,notablyautomobiles,electricalandelectronicequipment,

textiles,clothing,rubberandplastics(DaMottaVega,2009).Protectiongenerallytakestheform

not only of tariffs but also of non-tariff barriers, including complex import licensing schemes,

importfeesandanti-dumpingduties,whichincreasedfrom63measuresin2008to83measures

inmid-2012(WTO,2009;WTO,2013).2

InMay2010,asa resultofadeteriorating tradebalance inmanufacturedgoods, theBrazilian

governmentintroduceda25percentpreferencemarginingovernmentprocurementfordomestic

biddersaswellasanincreaseinimporttariffsoncarparts(Cornetetal.,2010).In2011,Brazil

implementeda30percenttaxonimportedvehicleswhileexemptingdomesticallyproducedcars

andtrucks,inameasureoriginallyintendedtolastoneyearbutextendedforfiveadditionalyears

in2012.ThesemeasureshaveresultedinaformalrequestforconsultationsattheWTOfiledby

theEuropeanUniononDecember19,2013.

Brazil’stradepolicyalsofeaturesexportpromotion.ToolsforthisincludetheExportFinancing

Program(PROEX),primarilytargetingsmallandmedium-sizedenterprisesthatotherwisestruggle

toobtaincredit,aswellastheExportGuaranteeFund(FGE).In2012,PROEXprovidedUS$4.88

billion to Brazilian exporters. Between 2009 and 2012, FGE supported 253 export operations

totalingUS$32.6billion.3Finally,theBrazilianDevelopmentBank(BNDES)hasseveralprograms

inplacetoeasetheinterestrateburdenonexporters(WTO,2013).

2 Morethanhalfoftheanti-dumpingmeasuresinplacein2011weredirectedagainstChina(Lima/Ragir2011).

3 FGEsupportedtheseexportoperationsbyguaranteeingupto100percentofthecommercial,political,andextraordinaryrisk.

17

Chapter I: Trade

German Trade Policy

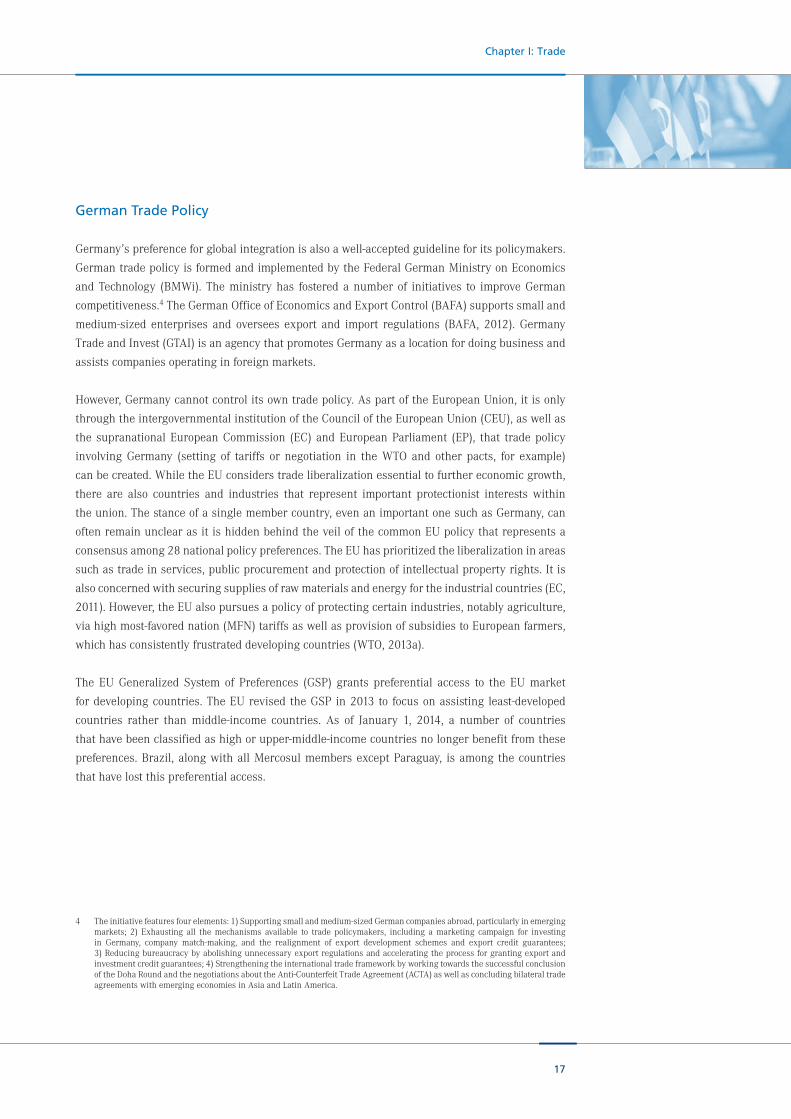

Germany’spreferenceforglobalintegrationisalsoawell-acceptedguidelineforitspolicymakers.

GermantradepolicyisformedandimplementedbytheFederalGermanMinistryonEconomics

andTechnology (BMWi).Theministryhas fosteredanumberof initiatives to improveGerman

competitiveness.4TheGermanOfficeofEconomicsandExportControl(BAFA)supportssmalland

medium-sized enterprises and oversees export and import regulations (BAFA, 2012). Germany

TradeandInvest(GTAI)isanagencythatpromotesGermanyasalocationfordoingbusinessand

assistscompaniesoperatinginforeignmarkets.

However,Germanycannotcontrolitsowntradepolicy.AspartoftheEuropeanUnion,itisonly

throughtheintergovernmentalinstitutionoftheCounciloftheEuropeanUnion(CEU),aswellas

thesupranationalEuropeanCommission (EC)andEuropeanParliament (EP), that tradepolicy

involving Germany (setting of tariffs or negotiation in the WTO and other pacts, for example)

canbecreated.WhiletheEUconsiderstradeliberalizationessentialtofurthereconomicgrowth,

there are also countries and industries that represent important protectionist interests within

theunion.Thestanceofasinglemembercountry,evenanimportantonesuchasGermany,can

oftenremainunclearasitishiddenbehindtheveilofthecommonEUpolicythatrepresentsa

consensusamong28nationalpolicypreferences.TheEUhasprioritizedtheliberalizationinareas

suchastradeinservices,publicprocurementandprotectionofintellectualpropertyrights.Itis

alsoconcernedwithsecuringsuppliesofrawmaterialsandenergyfortheindustrialcountries(EC,

2011).However,theEUalsopursuesapolicyofprotectingcertainindustries,notablyagriculture,

viahighmost-favorednation(MFN)tariffsaswellasprovisionofsubsidiestoEuropeanfarmers,

whichhasconsistentlyfrustrateddevelopingcountries(WTO,2013a).

The EU Generalized System of Preferences (GSP) grants preferential access to the EU market

fordevelopingcountries.TheEUrevisedtheGSPin2013to focusonassisting least-developed

countries rather than middle-income countries. As of January 1, 2014, a number of countries

thathavebeenclassifiedashighorupper-middle-incomecountriesnolongerbenefitfromthese

preferences.Brazil,alongwithallMercosulmembersexceptParaguay, isamongthecountries

thathavelostthispreferentialaccess.

4 Theinitiativefeaturesfourelements:1)Supportingsmallandmedium-sizedGermancompaniesabroad,particularlyinemergingmarkets; 2) Exhausting all the mechanisms available to trade policymakers, including a marketing campaign for investingin Germany, company match-making, and the realignment of export development schemes and export credit guarantees;3)Reducingbureaucracybyabolishingunnecessaryexportregulationsandacceleratingtheprocessforgrantingexportandinvestmentcreditguarantees;4)StrengtheningtheinternationaltradeframeworkbyworkingtowardsthesuccessfulconclusionoftheDohaRoundandthenegotiationsabouttheAnti-CounterfeitTradeAgreement(ACTA)aswellasconcludingbilateraltradeagreementswithemergingeconomiesinAsiaandLatinAmerica.

18

Chapter I: Trade

4. Overview of Brazilian-German Bilateral Trade

Brazilian-Germantradehasconsistently increasedoverthepastdecade, thoughgrowthslowed

following the economic crisis of 2008–2009. Of major EU member states, Germany is by far

Brazil’slargesttradingpartner,bothintermsofimportsandexports.GermanyiscurrentlyBrazil’s

fourthlargesttradingpartnerbehindChina,theUSandArgentina(GED,2013).

TheGerman-BrazilianconnectionfuelstradebetweentheEUandSouthAmerica.In2010,Germany

accountedforonethirdofallBraziliantradewiththeEU,andthisfigurelikelyunderestimatesthe

totalvalueowingtotheso-calledRotterdameffect.5

Brazil’smajorexportstoGermanyincludeironore,soyandsoyproducts,coffeeproducts,meat,

copper and crude oil (German Foreign Office, 2012). While raw materials predominate, some

machinery and aircraft parts also figure into Brazil’s German export portfolio. The majority of

BrazilianexportstotheEUoverallarelikewiseinrawcommodities.Twenty-onepercentofeurozone

oreandmineralimportsoriginateinBrazil,asdo11percentofagriculturalimports(EC,2012).

KeyGermanexportstoBrazilincludemachinery,carsandcarparts,aswellasbasicchemicals

andpharmaceuticalproducts(GermanForeignOffice,2012).IncontrastwiththeBrazilianexport

portfolio, German exports to Brazil are overwhelmingly manufactured goods, either for final

consumptionorintermediategoodsandcapitalgoodsforBrazilianbusinesses.Onceagainhere,

German-BraziliantradeisindicativeofthegreaterEU-SouthAmericanrelationship.In2011,for

example,88.5percentofMercosulimportsfromtheEUweremanufacturedgoods,withtradefor

machineryandintransportequipmentaccountingfor49.2percentofthetotal(EC2012).

Intermsofoverallvalue,Brazilian-Germantradeisrelativelybalanced.Brazilhadatradesurplus

withGermanysevenof theeightyearsbetween2003and2010,peakingatUS$2.78billion in

2007.ThissurplushasaveragedonlyUS$1.1billion.Brazil’stradesurpluswithGermanyappears

toreflectatidechangeasBraziltradedatadeficitwithGermanyfrom2000to2003.

ThetransitiondoesnotreflectadecreaseinBrazilianappetiteforGermangoods.Onthecontrary,

GermanexportstoBrazilnearlytripledbetween2000and2010,fromUS$4.43billiontoUS$11.75

billion. Increases in Brazilian exports simply outpaced increases in Brazilian imports from

Germany.

5 The Rotterdam effect refers to goods destined for a given country that enter the eurozone in third countries such as theNetherlands. Incaseswhere thesegoodsare then traded toGermany, these transactionsare recordedasDutch tradewithBrazil,andsubsequentlyaseurozonetradebetweentheNetherlandsandGermany.

19

Chapter I: Trade

Bilateraltradeflowsarecomplementaryandmutuallybeneficial.FromtheGermanperspective,

exportingtoBraziloffersdomesticmanufacturerstheopportunitytoreachthecountry’sgrowing

middle class—a massive new group of consumers. There is also a growing class of extremely

wealthyBrazilianconsumerswhorepresentaprimemarketforhigh-endGermangoods.Finally,

increasedbusinessactivityinBrazilgeneratesopportunitiesforGermanintermediategoodsand

capitalgoodssuchaschemicalsandmachinepartsandequipmentthatmakeupthebackboneof

theGermanexportingsector.

Source: Bertelsmann Stiftung, Global Economic Dynamics

Figure 2: Overview of Brazilian-German trade

Germany Brazil

426.89 bn

Import

497.44 bnExport

46.47

bn

Impo

rt

51.94

bn

Expo

rt

2001

Germany Brazil 0 500 1000 1500 2000 2500

Import Export

178,8

8 bn

Impo

rt

210,8

2 bn

Expo

rt

0 500 1000 1500 2000 2500

2011

Germany Brazil

846.21 bn

Import

957.51 bnExport

69.35

bn

Impo

rt

177.8

8 bn

Expo

rt

2006

0 500 1000 1500 2000 2500

1,091 bnImport

1,242 bnExport

20

Chapter I: Trade

FromtheBrazilianperspective,exporting toGermanyhelpsBrazildiversify its tradeportfolio.

Without trade to Europe, Brazilian commodity exporters could be particularly vulnerable to a

downturninChina.WhileBrazilexecutesagreatervolumeoftradewithbothArgentinaandthe

US,Brazilalsocompeteswiththesenationsonexportssuchassoy,beefandhydrocarbons.Not

onlycanthiscreatetradepolicyfriction,butitalsomeansBrazilmustfindadditionalconsumers

forsuchgoods.Germanyfitsthisdescriptionneatly,asitdoesnotcompetewithBrazilinmost

commoditysectors.

Germanmanufacturesrelyoncommodityimportstogeneratetheirfinishedproducts.Amassive,

politically stable commodity producer such as Brazil can offer resource security for Germany.

Meanwhile,GermandemandforBraziliancommoditiesnotonlyexpandsthequantityofannual

sales,butalsohelpsbiduptheglobalprice—bothtotheadvantageofBrazil.

5. Complications in Brazilian-German-Trade

Despite—orperhapsbecauseof—thecomplementarynatureofthetwocountries’factorendowments,

theEUandBrazilareinvolvedinaseriesoflong-standingtradedisputes.BrazilandtheEUhave

beeninvolvedin12casesbeforetheWTO;sevenofthemwerebroughtbyBrazil,whiletheEUhas

actedasacomplainantfivetimes(foranoverview,seeTable1).

WhileBraziliancomplaintshavefocusedontheEU’simportrestrictionsonagriculturalproducts

andrawmaterials,theEUhasobjectedtowhatitseesasBrazilianprotectionismonintermediate

inputs and final goods. Non-tariff and behind-the-border trade barriers feature prominently in

mostofthedisputes.WiththeEUstillstrugglingtorecoverfromthefalloutofthefinancialand

economiccrisis thatbegan in2008, theriskofprotectionismandnewtradedisputesremains

high.ExpertsfearthatastheDohaDevelopmentAgendanegotiationsremaininastalemate,the

riskof tradedisputesettlement initiationsrisesaswell.Asonediplomatput it, “The lessyou

negotiate,themoreyoulitigate”(Miles2012).

InthecurrentDoharound,BrazilandtheEUholdopposingviewsonmanycrucialissues.Most

importantly, theydisagreeon furtherconcessions foragriculturaland industrialproducts.Due

to the high competitiveness of its farmers, Brazil sees huge potential to increase the global

Figure 3: Overview of trade driversFor Germany For BrazilLarge growing market for German goods , Key trade diversification from USA & ChinaBrazilian development means increased trade opportu-nities for German firms

, German expertise key for Brazilian infrastructure development

Maintain national resource security for manufacturing sector

, German commodity demand increases quantity/prices of Brazilian exports

Global leader in green energy exports , Dedicated to green developmentSource: Bertelsmann Stiftung

21

Chapter I: Trade

marketshareofitsagriculturalproducts.Therefore,ithasbeenparticularlyconcernedwiththe

liberalizationofagriculturalmarkets.Brazilhastakenafairlyaggressivestanceonmarketaccess,

domesticsupportaswellasexportsubsidies(Nogueira,2009).Developedeconomies,inparticular

the EU and the US have offered cuts but they have been rather unrelenting about employing

thespecialsafeguardmeasures(SSM)thatallowforthetemporaryuseofimportrestrictionson

certainproducts(forexample,sugar)incaseofasuddensurgeinimports.

6. Towards a Mercosul-EU Free Trade Agreement?

Given their complementary and growing trade ties, Germany and Brazil would both stand to

benefitfromcloser,directbilateraltraderegulations.However,giventheformer’smembershipin

theEUandthelatter’sassociationwithMercosul,anFTAwouldrequirealargeraccordbetween

thetwoblocs.Asearlyas1995,theEUandMercosulsignedaframeworkagreementandinitiated

adialogueaimingtoestablishfreetradebetweenthetwoblocs.Sincethen,however,negotiations

regardingapossibleEU-MercosulFTAhaveoscillatedbetweennewpushesforanagreementand

lacklusterattemptstohammeroutthedetails.

OnMay29,1992,aJointInstitutionalCooperationAgreementwassignedbytheEUandthe(then)

fourMercosulcountries.InJuly1998,theEUdecidedtonegotiateanFTAwithMercosulandChile;

meetingsanddiscussionsstartedthatsameyear.Negotiationshavesinceoscillatedbetweennew

thruststofixtheagreementandlacklusterattemptstohammeroutthedetails(Flôres,2013a).

Duringthisperiodofmorethan15years,notmanyformalstudieshavebeenmadeonthelikely

impactoftheFTA.

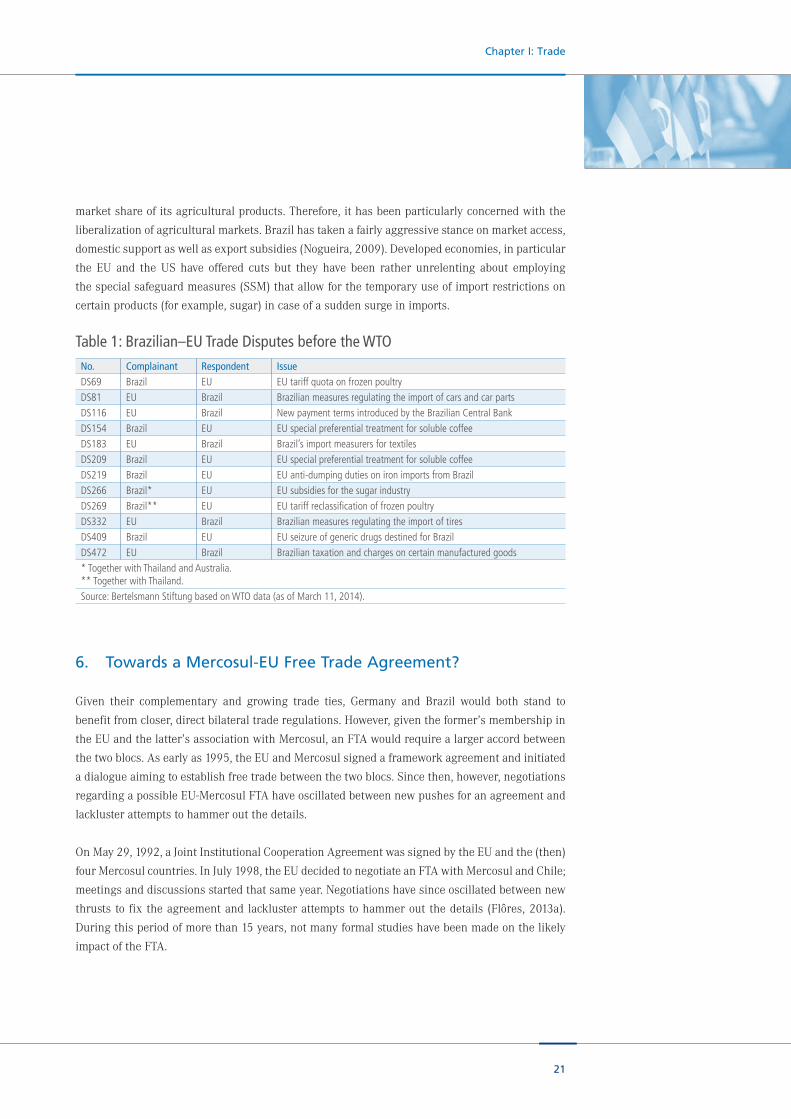

Table 1: Brazilian–EU Trade Disputes before the WTONo. Complainant Respondent IssueDS69 Brazil EU EU tariff quota on frozen poultryDS81 EU Brazil Brazilian measures regulating the import of cars and car parts DS116 EU Brazil New payment terms introduced by the Brazilian Central BankDS154 Brazil EU EU special preferential treatment for soluble coffeeDS183 EU Brazil Brazil’s import measurers for textilesDS209 Brazil EU EU special preferential treatment for soluble coffeeDS219 Brazil EU EU anti-dumping duties on iron imports from BrazilDS266 Brazil* EU EU subsidies for the sugar industryDS269 Brazil** EU EU tariff reclassification of frozen poultryDS332 EU Brazil Brazilian measures regulating the import of tiresDS409 Brazil EU EU seizure of generic drugs destined for BrazilDS472 EU Brazil Brazilian taxation and charges on certain manufactured goods* Together with Thailand and Australia.** Together with Thailand.Source: Bertelsmann Stiftung based on WTO data (as of March 11, 2014).

22

Chapter I: Trade

Inapervasivepartial-equilibriumanalysis,CalfatandFlôres(2006)showthatpotentialEUgains

from such an agreement are much more widespread, in particular for several manufactured

goods,whileMercosulwillreapadvantagesfromanumberofcommodityexports.Inspiteofthe

significanttradedeviationtoChinabymostMercosulmemberssincethetimeofthestudy,the

evaluationsarestillvaluableasupperboundsforgainsattheindividualproductlevel.

Flôres andMarconini (2003) argued thatmany synergies couldbe foundoutside the classical

realmofagriculture.Migrationofhumancapital—aticklishissuefortheEU—couldbearinteresting

andrewardingoutcomes forbothsides; telecommunicationservicesareanotherpotentialwin-

winarea.

NegotiationsofficiallyreopenedinMay2010,withBrazilemergingasakeyleaderinthedialogues.

BothBrazil andGermanycould realizesignificantgains fromanagreement:Brazilian-German

tradeflowsaccountedformorethanone-fifthofEU-Mercosultradein2010.

BrazilwouldverymuchliketocompleteanFTAwithamoredevelopedeconomy.Butdifficulties

andhesitationsstillplaguetheadvancementoftheprocess.OntheMercosulside,Argentina,and

toalesserextentVenezuela,haveposedquiteafewdemandsandobjections.FromtheEuropean

side, despite the extremely positive rhetoric, not much enthusiasm has been demonstrated in

termsofconcessions,whichactuallymimicthepatternofthoseofferedlongago.

Moreover,twonewvariablesareatstake.

ThefirstisChina,anewandmassivemarketthathasconsiderablyeasedtheanxietyofMercosul

commodityexporters—especiallymeatproducers—makingtheEUastillattractivebutlesscrucial

marketthanitwastenyearsago.OntheEUside,beyondtheseveralcrisesstilloccupyingthe

largerfractionoftheBrusselsstaff,inthetradearena,theprospectsofaTrans-AtlanticTradeand

InvestmentPartnership(TTIP)isdrawingconsiderableattention.Thisisacomplicated,ambitious

attempt, with no clear outcome but giving way to an extremely time and human resource-

consumingprocess.

A study by the Bertelsmann Stiftung and the IFO-Institute concluded that in global economic

terms,boththeUSandtheEUwouldprofitfromacomprehensiveTTIP(Felbermayr,2013),with

southernEUmemberstatesandtheUKbeingthemainbeneficiaries.CountriesoutsidetheTTIP,

especiallythosewithveryclosetraderelationswithoneofthetwoblocs,suchasMexico,would

facetradecontractionthatwouldresultindecreasestorealincomeandemployment.

ThestudyforecastsBrazilianexportstotheEUtocontractby9.4percentiftheTTIPisconcluded,

andBrazilianexportstoGermanytocontractby7.9percent.ThestudyalsofindsthatBrazilian

exportstotheUScoulddeclinebyasmuchas29.7percent.Overall,thesecontractionscouldcost

Brazilmorethantwopercentofper-capitaGDP.

23

Chapter I: Trade

The impactonBrazil issomewhatdebatableandpreliminary,ageneralevaluationwithwhich

Flôres(2013b)agrees.Thekeyissue,morethantradedeviation,istheenvisagedunifiedplatform

oftechnicalnorms,rulesandstandardsformanufactures,servicesandcommodities.Thisimplies

thatBrazil,andMercosulaswell,shouldsetataskforcetodeeplyanalyze,outofthepotentially

commonnorms thatcouldresult6, thosewithwhich italreadycomplies, those itwould like to

adopt,andthosethecountryseesnopointinfollowing.Inconductingthiseffort,Germany,withits

closetieswithBrazilianindustryanditssuperiortechnicalexpertise,couldbeafriendlypartner

toBrazil.

InFebruary2012,GermanForeignMinisterGuidoWesterwellevisitedBrazilianForeignMinister

AntonioPatriota,andthetwojointlycalledforprogressintheEU-MercosulFTAdialogues.While

theyconcededthatEurope’ssubsidiestofarmersrepresentacrucialdividingpoint,bothmade

clear that their governments supported an agreement. At a summit meeting in January 2013,

GermanChancellorAngelaMerkelwonthecommitmentofBrazilianPresidentDilmaRousseff

and Argentine President Cristina Fernández de Kirchner to exchange concrete proposals for

loweringtradebarriersbytheendof2013(Emmott,2013),somethingBrusselshasfailedtodo.

On February 24, 2014, Rousseff met with EU leaders to discuss negotiations (GMF, 2014).

Mercosulmembershadmetearlier thatmonthtodiscussa jointproposalontariff reductions.

Additionally,discussionsofthepotentialfornegotiationstomoveforwardwithoutArgentina;aso-

called“two-speed”negotiationprocesshaveemerged.Whilethisapproachwouldrequirerevising

Mercosulrules,BrazilandUruguayhavehintedatpreparationstodosoifArgentinacontinuesto

pursueamoreprotectionisttradepolicy(Mercopress,2014b).Brazil’spowerfulConfederationof

Industries(CNI)hasrecentlycomeoutinsupportofthisidea,notingthatFTAswiththeEUand

USarenecessarytomaintainBrazil’scompetitiveness(Ridout,2014).Paraguayalsoindicatedan

inclinationtofollowtheothertwomembers.

Yetobstaclesremain.Europeanfarmlobbiesplacea€25billionpricetagonapotentialEU-Mercosul

FTA, claiming thatEuropean farmerswill suffer extensive losses in the event of liberalization

of theagricultural sector (Mercopress,2011).TheEC’sownassessment found the losses tobe

considerablylower,rangingbetween€1billionand€3billion(Burrelletal.,2011).Theagricultural

lobby,however,isunlikelytobeconvincedbythecalculationsoftheEC—aknownsupporterof

freetrade.

ThesedevelopmentssuggestBrazilandGermanyshouldexploitdeeperbilateralrelations,without

violatingtherulesoftheexistingcustomsunions,andthatthiswouldcreatemoreopportunities

andtargetedbusinessventuresinatraditionalrelationshipthatisfortunatelybloomingagain.

6 Wesay“potentiallycommonnormsthatcouldresult”becauseinmanyareas,suchasGMOs,theInternetrealmandchemicalgoods,itishardtoconceiveaEU-USharmonization(seealsoFlôres,2013b).

24

Chapter I: Trade

7. 21st-Century Opportunities for a 21st-Century Relationship

ThetraderelationshipbetweenBrazilandGermanyisnotjustcharacterizedbycomplementary

endowmentsandcompetitionbetweennationalindustries.Italsofeaturessignificantopportunities

inso-called“new”or“21st-century”trade—manyofwhichremaintobeseized.

Newtradetheorywasdevelopedasearlyasthe1970s,basedontheobservationthatanincreasing

shareofinternationaltradewastakingplacewithinindustriesandcouldnotbeexplainedbythe

classicaltheoriesofcomparativeadvantageanddifferencesinfactorendowments(Krugman,1979).

Intra-industrytrade,countriestradingfinalgoodsbutalsopartsandcomponentswithinthesame

industry,isseentobedrivenbyfactorssuchasmonopolisticcompetition,consumerpreferencefor

diversity,increasingreturnstoscaleandagglomerationeffects.Intra-industrytradeaccountsfora

largepartoftheexponentialgrowthofinternationaltradeintheageofglobalization(beginningin

the1990s),asopenbordersaswellasfallingcostsoftransportationandcommunicationallowed

forsupplychainintegrationacrosscountries.

BrazilandGermanyhavetakenremarkablydifferentapproachesto thesedevelopments.While

Germanyhasembracedintegrationintoregionalglobalsupplychains,Brazilhasgenerallyfavored

verticalintegration—thelinkingofvariousstagesofproductionwithinacountry.

ForGermany,supplychainintegrationcamenaturallygiventhecountry’scentralpositioninthe

commonEuropeanmarket,scarcityofresourcesandhighdegreeofindustrialspecialization.The

openingofCentralandEasternEurope’seconomiesinthe1990sprovidedaspecialopportunity

forGermanbusinessestotapnotonlynewmarketsbutalsonewsourcesofrelativelycheaplabor.

OutsourcingorrelocatingpartsofproductiontoGermany’seasternneighborsallowedcompanies

tofocusonthestagesofproductionmostefficientlydoneathome,increasingoverallproductivity.

InBrazil,verticalintegrationislargelyarelicoftheISImodelofdevelopmentofdecadespast.

Thecountry’sprotectionofindustriesthroughtariffandnon-tariffmeasuresandpreferencefor

domesticindustryisoneimportantfactorpreventingsupplychainintegration.Anotherkeyfactor

isitsgeographicdistancefromtheworldeconomy’smostdynamicandintegratedregions(Europe,

NorthAmerica,EastAsia),combinedwithpoor logistics infrastructure.Withtheestablishment

of Mercosul in 1991, Brazil bet on its own model of regional integration. Mercosul has led to

some supply-chain integration in the region—a notable example is the automotive industry in

BrazilandArgentina—butMercosul’sclosedapproachtotheoutsideandlongstagnationinterms

ofdeepeninginternal integrationhasseverely limitedthesupplychainintegrationofBrazilian

industries.Interestingly,theonlyindustrialsegmentinBrazilwithstronginternationalintegration,

aerospace (heavilyconcentratedaroundaircraftmanufacturerEmbraer), isalsooneof the few

Brazilianmanufacturingsegmentsexperiencingstronggrowthinrecentyears.

25

Chapter I: Trade

Consideringtherangeofindustriespresentinbothcountries,increasedsupplychainintegration

betweenBrazilandGermanyshouldpresentsignificantopportunitiesforbothcountries,especially

inthemanufacturingsector.ForBrazil,transferofGermanknowledgeandtechnologycouldhelp

firmsbecomemoreefficient.ForGermany,Brazilpresentsnotjustanattractivemarketbutalsoa

potentialsourceofinputs(thoseincorporatinglaborandnaturalresources)andeventechnology

inareaswhereBrazilianfirmshavefoundniches(e.g.biofuels,aerospace).

Supplychainintegrationisalsolinkedtoanotherimportantnewthemeininternationaltrade:trade

inservices.Theproductionoffinalgoodsinamodern,globallyintegratedindustryincorporates

notjustalargenumberofcomponentsorintermediategoodsbutalsoarangeofservices,manyof

whichcanbegloballysourced.Thesetradableservicesincludediverseactivitiessuchastransport,

logistics,IT,finance,insuranceanddesign.Inadditiontosuchbusiness-orientedservices,tourism

isalsoagrowingtradableservice.

Astradeinserviceshasgrown,Brazilhasnotfullytakenadvantageoftheresultingopportunities.

This isnosurprise, asbusinessservices tend tobeclosely linked to supplychain integration.

Germanyhowever,isalsorelativelypoorlyintegratedinglobalservicestrade,asmanyimportant

sectors remain closed. Hence, services present an opportunity for both countries to deepen

integrationwitheachotheraswellaswiththerestoftheworld.Tourismalsopresentsabilateral

opportunity.Brazil,withitsplentifulsunshineandlushbeaches,shouldbeabletotapintothe

marketforsun-hungryGermans,rivalingtheCaribbeanandSoutheastAsiaasawarm-weather

touristdestination.Bythesametoken,Germanyhassofarmissedoutonthedramaticincreasein

Brazilianstravelingabroad.GiventhatmanyBraziliansareofGermandescentandthecountryhas

muchtoofferintermsofhistoryandculture,thereisagreatopportunitytoattractmoretourists.

AnotherinterestingareaofopportunityforintegrationbetweenGermanyandBrazilisinthearea

ofgreenenergyandbiofuels.Bothcountriesareleadersinsubsectorsinthisareabutcooperation

hasbeenlimited.Brazilhasbeenleading inthedevelopmentofethanolmadefromsugarcane

(a more efficient source than corn or other plants) and related technologies such as flex-fuel

engines(thatrunongasoline,ethanoloranymixtureofthetwo)andelectricityfromthebiomass

byproducts of sugarcane (rather thanbeingnet consumers of electricity,Brazilian sugarmills

actuallysupplysignificantamountstothegrid).Germany,meanwhile,hasbeenaleaderinthe

development of solar panels and wind turbines, which are clearly an attractive energy option

for Brazil. However, instead of benefiting from each other’s strengths, each country has taken

aprotectionistapproachtowardstheother’sproducts,withcostsforbotheconomiesaswellas

theenvironment.GiventhatBrazilandGermanybothaspiretobeleadersontheglobalclimate

agenda,greatercooperation in thisareashouldbeapoliticalpriority. In the20thcentury, the

twocountriescooperatedinthedevelopmentofnuclearenergy,withtheGermanfirmSiemens

supplying thereactors forBrazil’snuclearplant inAgradosReis.Whynotembarkonsimilar

cooperationonenergysourcesforthe21stcentury?

26

Chapter II: Capital Flows and Investment

Chapter II:

Capital Flows and Investment

1. Financial Flows 2. Foreign Direct Investment and Portfolio Investment 3. Macroeconomic Stability and International Financial Flows

27

Chapter II: Capital Flows and Investment

Chapter II: Capital Flows and Investment

ThischapteroutlinesthekeyissuesinfluencingfinancialflowsandinvestmentbetweenGermany

andBrazil.Section1reviewsthemainfactorsinfluencinginternationalfinancialflows,asrevealed

bytherelevantliterature,whileSection2describesandanalyzesdataondirectforeigninvestment

andinternationalportfolioinvestment,withaparticularfocusonBrazilandGermany.Section3

analyzesthelinkbetweenmacroeconomicstabilityandinternationalfinancialflows,particularly

in light of recent Brazilian exchange rate volatility, and concludes by briefly considering the

potentialbenefitsofmacroeconomicpolicyharmonization.

1. The Microeconomics of International Financial Flows

Thefinancialdecisionsofforeigninvestorsareinfluencedbyexpectedrisksandreturns,asisthe

caseofanyfinancialflow.Theeconomicroleofinternationalfinancialflowsistotransfersavings

betweencountries.AccordingtoLucas(1990),oneshouldthusexpectlargecapitalflowsfromrich

topoorcountries,giventhatthelowerratioofcapitalperworkerinpoorcountrieswouldimply

largermarginalreturnstocapital.However,asReinhartandRogoff(2004)noted,externaldebtper

capitadoesnotseemtofollowthislogic.Rather,thelargertheincomepercapitaofacountry,the

largertendstobeitsexternaldebtpercapita.GertlerandRogoff(1989,1990)showthatthereis

evidenceofexpandingcapitalflowsfrompoortorichcountries,whileAlfaroetal.(2003)present

evidenceofincreasingdirectforeigninvestmentincountrieswithhighpercapitaincome.

Finally,ReinhardandRogoff (2004) found thatagroupof20orsoemerging-marketcountries

receivethebulkoffinancialflowsfromrichercountries,withtheremainingdevelopingcountries

generallyreceivingfundsthroughaidanddirectforeigninvestment.Theseempiricaldisagreements

withLucas’sexpectationsregardingcapitalflowshavecometobeknownasthe“LucasParadox.”

Whilethiscouldbepartiallyrelatedtothephenomenonofthe“homebiaspuzzle”(reviewedin

Lewis,1999,thisreferstothepreferenceofinvestorstoinvestintheircountryoforigin),thereare

severaladditionalfactorsinvolved,someofwhicharediscussedbelow.

Scarcity of Human Capital and Natural Resources

ContrarytoLucas’spostulation,thereturnstocapitalarenotnecessarilyhigherinpoorcountries.

Onekeyreasonisthatequipmentandphysicalcapitalingeneralarecomplementaryfactorsof

productiontohumancapitalandnaturalresources.Consequently,therelativescarcityofhuman

capitalinmanypoorcountriesandofnaturalresourcesinwealthierones,decreasesthemarginal

productofphysicalcapital.

28

Chapter II: Capital Flows and Investment

ThiscontentionissupportedbyCaselliandFeyrer(2007),whodevelopedamethodologytocorrect

themarginalproductofcapital(MPC)thataccountsforitscomplementaritieswithhumancapital

andnatural resources. They find that although there are significant differentials in calculated

MPCbetweenrichandpoorcountriesaccordingto“naïve”methodologies(11.4inrichcountries

against 27.2 in poor ones), corrections for the complementarities between capital and human

capitalaswellasnaturalresourceslargelyequalizesthem(8.4forrichcountriesagainst6.9for

poorcountries),suggestinginfactthatrichcountriesmayhaveasomewhathigherMPC.

If capital, despite being the relatively mobile factor of production, must have complementary

humancapital(and/ornaturalresources),onemayaskwhethermigrationofworkerscouldnotbe

animportantforceequalizingmarginalproducts.Therecentintensificationofinternationallabor

migrationsuggeststhatitis,tosomeextent,butthattherearestillrestrictionsandconstraints.

These includeconflicts (religious, ethnic)andpecuniaryandnon-pecuniarycostsofmigration

(legal restrictions, differences of cultural values, habits, loss of relations and network, lack of

informationetc.).

Brazil has ample natural resources, but its dearth of human capital may discourage potential

investors,atleastintheshortandmediumterms.Thecountry’seducationsystemdoesnotprovide

thenecessarynumberofqualifiedworkers,norhasmigrationrecentlybeenabletofillthisgap.

Institutional Quality

Another factorbehind the relativescarcityofcapital inpoorcountries is the increasedriskof

investment. Papaionnau (2004, 2009) examined the financial flow data from banks of 140

(industrial, emerging and underdeveloped) countries. His main finding was that institutional

qualityisakeycorrelatetoforeignbanklending.Acountrywithpoorlyperforminginstitutions,

includingweakpropertyrightsandhighrisksofexpropriation, legal inefficiency,bureaucratic

corruption, etc., inhibits foreignbank lending. In effect, these factors act as (uncertain) taxes,

restrictingcapitalinflows.Ontheotherhand,politicalliberalization,privatization,anindependent

bankingsystemandsimilarstructuralcharacteristicsenableaneconomytoattractsubstantially

moreforeignbankcapital.

Papaionnau(2009)alsotestedforinformationalasymmetriesandethno-linguistictiesascontrol

variables(seealsoGlickandRose,2002),buttheinstitutionalfactorsremainedprominent.Lane

(2003)arrivedatasimilarconclusionregardingequityanddirectforeigninvestment;hisresearch

suggestedthatthepoorqualityofinstitutionsandtheprevalenceofcorruptioninhibitedforeign

investment. Somewhat to the contrary, Lucas (1990) dismisses the importance of the political

riskfactor,citingtheexampleofIndiapriorto1945.Duringthatperiod,Indiawasstillsubjectto

Britishruleand,consequently,tothesamepoliticalrisk,yetitscapitallaborratioremainedbelow

thatofBritain.

29

Chapter II: Capital Flows and Investment

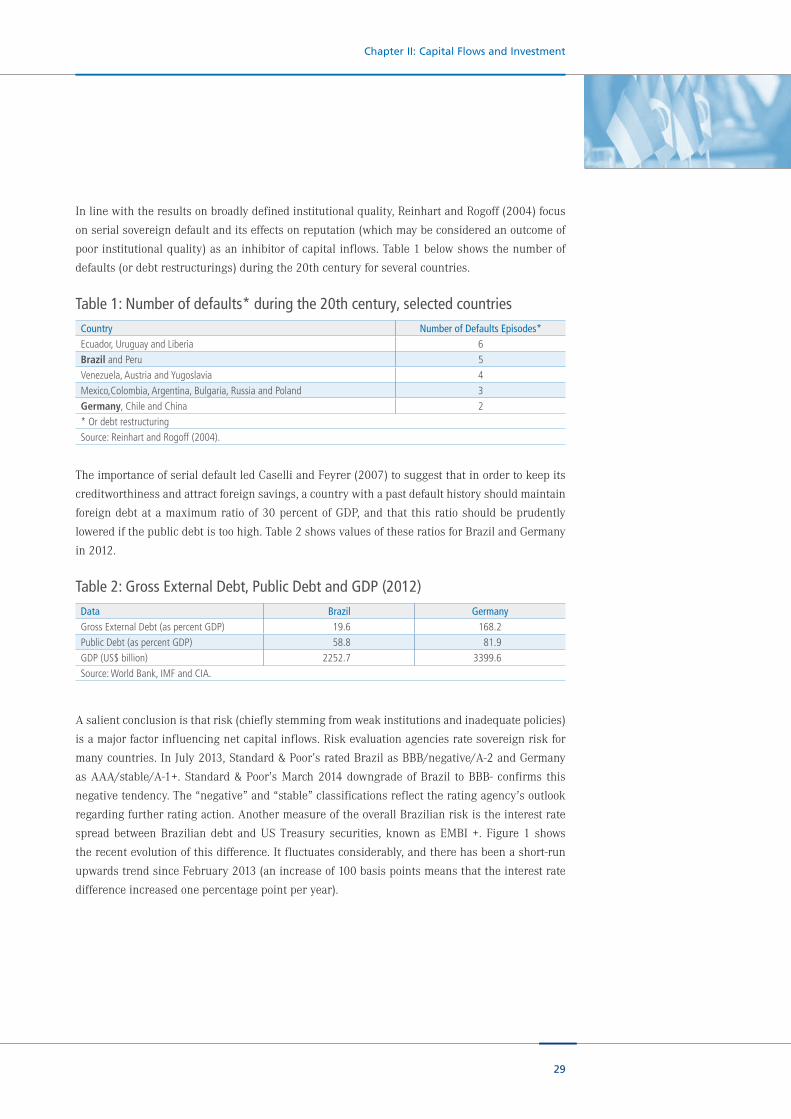

Inlinewiththeresultsonbroadlydefinedinstitutionalquality,ReinhartandRogoff(2004)focus

onserialsovereigndefaultanditseffectsonreputation(whichmaybeconsideredanoutcomeof

poorinstitutionalquality)asaninhibitorofcapitalinflows.Table1belowshowsthenumberof

defaults(ordebtrestructurings)duringthe20thcenturyforseveralcountries.

TheimportanceofserialdefaultledCaselliandFeyrer(2007)tosuggestthatinordertokeepits

creditworthinessandattractforeignsavings,acountrywithapastdefaulthistoryshouldmaintain

foreigndebtatamaximumratioof30percentofGDP,andthatthisratioshouldbeprudently

loweredifthepublicdebtistoohigh.Table2showsvaluesoftheseratiosforBrazilandGermany

in2012.

Asalientconclusionisthatrisk(chieflystemmingfromweakinstitutionsandinadequatepolicies)

isamajorfactorinfluencingnetcapitalinflows.Riskevaluationagenciesratesovereignriskfor

manycountries.InJuly2013,Standard&Poor’sratedBrazilasBBB/negative/A-2andGermany

asAAA/stable/A-1+.Standard&Poor’sMarch2014downgradeofBrazil toBBB-confirms this

negativetendency.The“negative”and“stable”classificationsreflecttheratingagency’soutlook

regardingfurtherratingaction.AnothermeasureoftheoverallBrazilianriskistheinterestrate

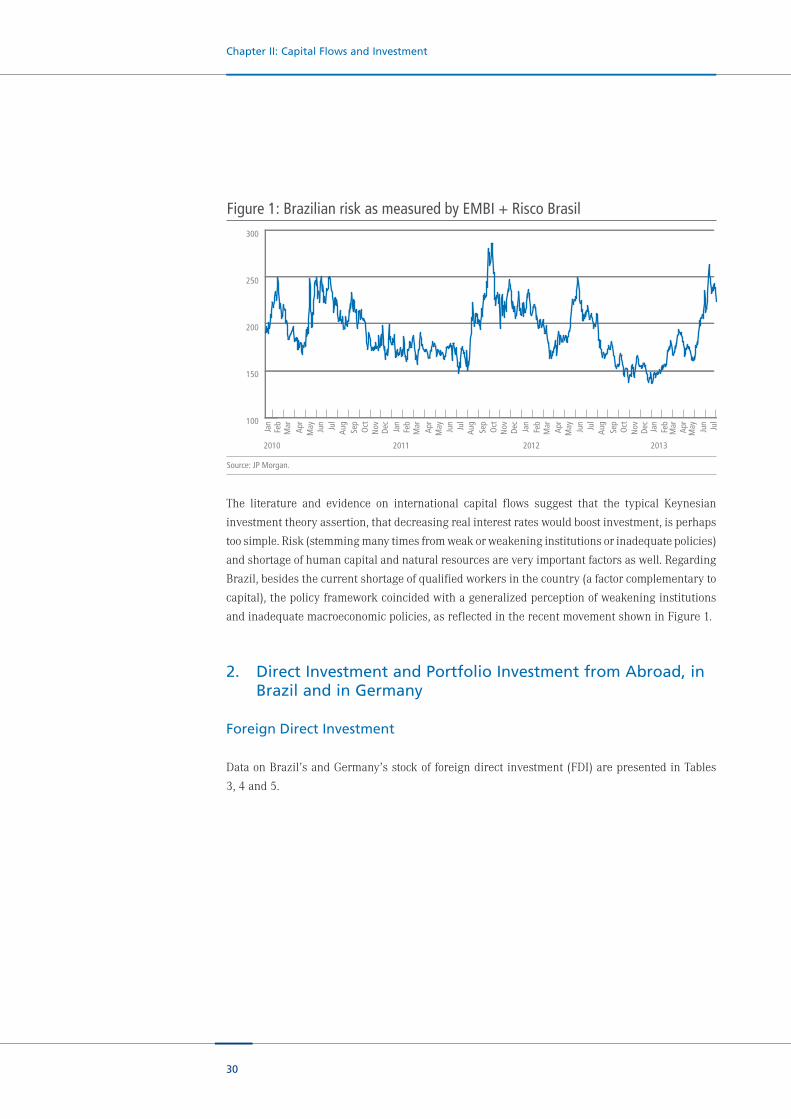

spreadbetweenBraziliandebt andUSTreasury securities,knownasEMBI+.Figure1 shows

therecentevolutionofthisdifference.Itfluctuatesconsiderably,andtherehasbeenashort-run

upwardstrendsinceFebruary2013(anincreaseof100basispointsmeansthattheinterestrate

differenceincreasedonepercentagepointperyear).

Table 1: Number of defaults* during the 20th century, selected countriesCountry Number of Defaults Episodes*Ecuador, Uruguay and Liberia 6Brazil and Peru 5Venezuela, Austria and Yugoslavia 4Mexico,Colombia, Argentina, Bulgaria, Russia and Poland 3Germany, Chile and China 2* Or debt restructuringSource: Reinhart and Rogoff (2004).

Table 2: Gross External Debt, Public Debt and GDP (2012)Data Brazil GermanyGross External Debt (as percent GDP) 19.6 168.2Public Debt (as percent GDP) 58.8 81.9GDP (US$ billion) 2252.7 3399.6Source: World Bank, IMF and CIA.

30

Source: JP Morgan.

Figure 1: Brazilian risk as measured by EMBI + Risco Brasil

100

150

200

250

300

Jul

Jun

MayAp

rM

arFeb

Jan

Dec

NovOct

Sep

AugJul

Jun

MayAp

rM

arFeb

Jan

Dec

NovOct

Sep

AugJul

Jun

MayAp

rM

arFeb

Jan

Dec

NovOct

Sep

AugJul

Jun

MayAp

rM

arFeb

Jan

100

150

200

250

300 EMBI + Risco-Brasil - - - JP Morgan - JPM366_EMBI366

2010 2011 20132012

Chapter II: Capital Flows and Investment

The literature and evidence on international capital flows suggest that the typical Keynesian

investmenttheoryassertion,thatdecreasingrealinterestrateswouldboostinvestment,isperhaps

toosimple.Risk(stemmingmanytimesfromweakorweakeninginstitutionsorinadequatepolicies)

andshortageofhumancapitalandnaturalresourcesareveryimportantfactorsaswell.Regarding

Brazil,besidesthecurrentshortageofqualifiedworkersinthecountry(afactorcomplementaryto

capital),thepolicyframeworkcoincidedwithageneralizedperceptionofweakeninginstitutions

andinadequatemacroeconomicpolicies,asreflectedintherecentmovementshowninFigure1.

2. Direct Investment and Portfolio Investment from Abroad, in Brazil and in Germany

Foreign Direct Investment

DataonBrazil’sandGermany’sstockofforeigndirectinvestment(FDI)arepresentedinTables

3,4and5.

31

Chapter II: Capital Flows and Investment

Table 3: Direct Foreign Investment Position in Brazil, by country of origin, end of 2011Rank Country US$ Billion

Total 688.61 Netherlands 171.22 United States 119.33 Spain 92.44 France 34.25 Japan 34.26 Luxembourg 32.77 United Kingdom 20.48 Mexico 17.19 Germany 16.7

10 Cayman Islands 16.5Source: Coordinated Direct Investment Survey (CDIS) – IMF.

Table 4: Direct Foreign Investment Position of Germany in other countries, end of 2011

Rank Country US$ BillionTotal 1,206.3

1 United States 221.52 United Kingdom 126.53 Netherlands 113.54 Luxembourg 101.65 Belgium 55.36 France 52.57 China, P.R.: Mainland 44.28 Austria 43.09 Italy 42.0

10 Spain 33.917 Brazil 16.3

Source: Coordinated Direct Investment Survey (CDIS) – IMF.

Table 5: Direct Foreign Investment Position in Germany, end of 2011Rank Country US$ Billion

Total 915.31 Netherlands 229.32 Luxembourg 130.93 United States 91.44 France 83.45 Switzerland 79.16 United Kingdom 75.57 Italy 46.58 Austria 30.99 Japan 20.6

10 Sweden 19.7161 Brazil 0.3

Source: Coordinated Direct Investment Survey (CDIS) – IMF.

32

Chapter II: Capital Flows and Investment

Table6showsthestockofFDIrelativetoGDPoftheworld’s20largesteconomies.Thestockof

FDIinthesecountriescorrespondsto28.3percentoftheircombinedGDP,whiletheirstockofFDI

abroadcorrespondsto32.1percent.Asawhole,thisgroupofcountriesreceivedandsentabroad

aboutthesameamountofdirectinvestment.Brazil(andotheremergingmarketssuchasMexico)

receivedFDIinlinewiththeoverallaverage,buttheysentabroadafigurequitebelowtheaverage.

Germanyreceivedslightlybelowtheaverageandsentabroadasumaboveit. Japan,Indiaand

SouthKoreamaybeconsideredrelativelyclosedeconomiesintermsofreceivingFDI.

TheexaminationofTables3,4,5and6allowsseveralconclusions:

1) ThetotalstockofFDIinBrazil,relativetoGDP,is31percent.ForGermany,thefigureis27

percent.Thefiguresareclosetoeachother,suggesting,asarguedbytheauthorsmentionedin

theprevioussection,thatemergingeconomiesarenotnecessarilypreferredrecipientsofFDI.

Rather,richcountriesreceiveasizableportionofit.

Thefigures inthefinalcolumnofTable6areameasureoftheopennessofeacheconomy

withrespecttoFDI. It isanimportantmeasure,sincethestockofFDIisaccumulatedover

Table 6: Stock of Foreign Direct Investment (FDI) as percent of GDP (for the 20 largest GDP countries)

RANK (based on GDP)

Country 1. Stock of FDI in the country as percent of GDP

2. Stock of FDI of the country abroad as percent of GDP

1 + 2

1 United States 16.2 26.5 42.72 China 23.2 0.0 23.23 Japan 3.8 16.2 19.94 Germany 26.9 35.5 62.45 France 37.2 61.1 98.46 United Kingdom 43.7 70.8 114.57 Brazil 30.6 6.8 37.48 Russian Federation 22.6 18.0 40.69 Italy 16.9 25.8 42.7

10 India 9.7 3.3 13.011 Canada 32.2 36.3 68.512 Australia 33.9 22.6 56.513 Spain 43.8 44.9 88.714 Mexico 29.8 8.4 38.215 Korea, Rep. 11.8 15.2 27.016 Indonesia 21.2 0.0 21.217 Turkey 14.4 3.3 17.718 Netherlands 443.1 550.8 993.919 Switzerland 102.0 162.9 264.920 Sweden 64.7 67.2 131.9

OVERALL 28.3 32.1 Source: Coordinated Direct Investment Survey (CDIS) – IMF.

33

Chapter II: Capital Flows and Investment

manyyears.Consequently,itreflectsinformationregardingthelong-runhistoricalbehavior

ofthecountrywithrespecttoFDI—i.e.,informationaboutitseconomicrelationshipwithother

countriesand,particularly,itsabsorptionofforeigncapitalandtechnology.

The coefficient of correlation between the measure of openness described in Table 6 (last

column)—and a more traditional measure of openness, such as (import + exports)/GDP—is

0.368.Anda“Studentt”statisticaltestshowsthatthecorrelationissignificantlydifferentfrom

zeroatthe95percentconfidencelevel.Theconclusionisthatcountriesthatareopentotrade

tendtobeopentoFDI(andviceversa).

AccordingtotheFDIopennesscriteria,asarecipientcountryBrazilranksninthamongthe20

largesteconomies.Germanyranks11th.

2) Assuminganincome/capitalratioof20percent,thetotalcapitalstockinBrazilwouldhavea

valueofUS$11.3trillion.Consequently,consideringTable3,thevalueofthestockofforeign

directinvestmentinBrazilwouldbeaboutsixpercentofthevalueofthetotalcapitalstockin

thecountry.Iftheincome/capitalratiowere25percent,thepercentageofthestockofforeign

directinvestmentinBrazilwouldbearound7.5percentofthetotalstockofcapital.

ForGermany, theratios foreachhypothesiswouldbeslightlysmaller:5.5percentand6.9

percent,respectively.Consequently,thereisnotmuchdifferencebetweenahigh-income-per-

capitacountrysuchasGermanyandamedium-income-per-capitacountrysuchasBrazil.The

overall figures (see the last lineofTable6) also suggest that,makingsimilarassumptions

abouttheincome/capitalratioforallthe20countries,thepercentageofthestockofforeign

direct investment to the total capital stock, for an average country of the group, would be

aroundsixorsevenpercent.

3) The stock of German direct investment in Brazil is 1.4 percent of the total German direct

investmentabroad.Throughtheyears,ithasbeentheUS—adevelopedcountry—thathasbeen

theprincipalrecipientofGermandirect investment(18.4percentof thetotal, representing

US$119billion);datafromthesamesourceshowthattheUSowns10percent(worthUS$91.4

billion)ofthestockofFDIinGermany.Brazil,withUS$260millionoftotaldirectinvestment

inGermany,istheglobe’s161stforeigndirectinvestorinGermany.Giventhatthetotalstock

ofBraziliandirectinvestmentabroadisworthUS$154billion,Braziliandirectinvestmentin

thecapitalstockinGermanyisquitesmall.

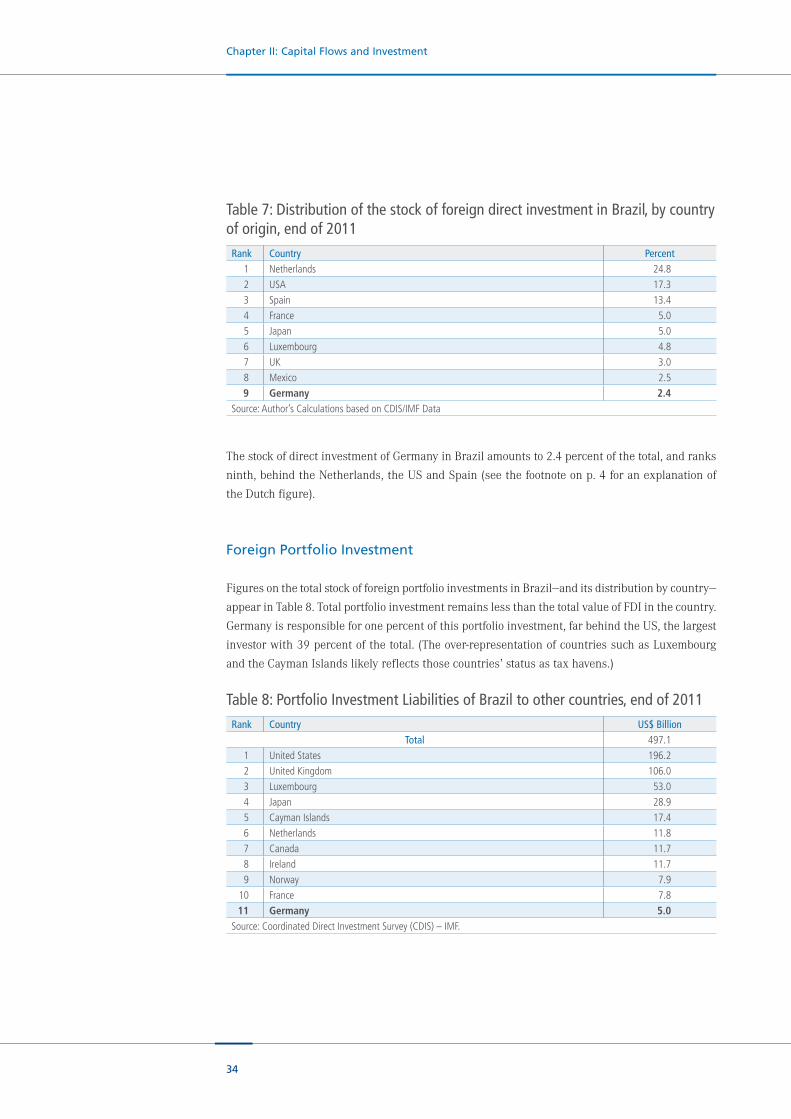

4) Table7(derivedfromtheprevioustables)showsthepercentagedistributionofFDIinBrazil,

bycountryoforigin.

34

Chapter II: Capital Flows and Investment

ThestockofdirectinvestmentofGermanyinBrazilamountsto2.4percentofthetotal,andranks

ninth,behindtheNetherlands,theUSandSpain(seethefootnoteonp.4foranexplanationof

theDutchfigure).

Foreign Portfolio Investment

FiguresonthetotalstockofforeignportfolioinvestmentsinBrazil—anditsdistributionbycountry—

appearinTable8.TotalportfolioinvestmentremainslessthanthetotalvalueofFDIinthecountry.

Germanyisresponsibleforonepercentofthisportfolioinvestment,farbehindtheUS,thelargest

investorwith39percentofthetotal.(Theover-representationofcountriessuchasLuxembourg

andtheCaymanIslandslikelyreflectsthosecountries’statusastaxhavens.)

Table 7: Distribution of the stock of foreign direct investment in Brazil, by country of origin, end of 2011

Rank Country Percent1 Netherlands 24.82 USA 17.33 Spain 13.44 France 5.05 Japan 5.06 Luxembourg 4.87 UK 3.08 Mexico 2.59 Germany 2.4

Source: Author’s Calculations based on CDIS/IMF Data

Table 8: Portfolio Investment Liabilities of Brazil to other countries, end of 2011Rank Country US$ Billion

Total 497.11 United States 196.22 United Kingdom 106.03 Luxembourg 53.04 Japan 28.95 Cayman Islands 17.46 Netherlands 11.87 Canada 11.78 Ireland 11.79 Norway 7.9

10 France 7.811 Germany 5.0

Source: Coordinated Direct Investment Survey (CDIS) – IMF.

35

Chapter II: Capital Flows and Investment

Table9showsGermanportfolioinvestmentsinothercountries(whichtotalabouttwicetheamount

ofGermandirectinvestmentsabroad).LuxembourgistheNo.1recipient,whileBrazilaccounts

foronly0.2percentofthetotal.

Table10makesacomparisonoftheBrazilianandtheGermanstockpositionsofforeigndirect

investmentsandportfolioinvestments,asrecipientandinvestorcountries.Again,Germanportfolio

investmentinLuxembourgissignificantlyoverstatedasthefundsdonotstayinLuxembourg,but

areonlyroutedthroughthecountry.

Table10showsthat,overall,Brazilreceivesfarmoreportfolioinflowthanitinvestsabroad.While

Germanydoesinvestheavilyabroad,itisstillanetrecipientofportfolioinvestment.

Table 9: Portfolio Investment Assets of Germany in other countries, end of 2011Rank Country US$ Billion

Total 2,380.41 Luxembourg 301.52 France 237.33 Netherlands 202.54 United States 202.25 United Kingdom 173.76 Italy 163.77 Spain 125.38 Ireland 92.09 Austria 53.8

28 Brazil 5.0Source: Coordinated Direct Investment Survey (CDIS) – IMF.

Table 10: Stock of Foreign Direct and Portfolio Investment; Brazil and Germany as recipient and investor countries, end of 2011

Brazil Percent of GDP Germany Percent of GDPRecipient Investor Recipient Investor

Foreign Direct Investment 30.6 6.8 26.9 35.5Portfolio Investment 22.1 1.3 82.9 70.0Source: CPIS/IMF and CDIS/IMF

36

Chapter II: Capital Flows and Investment

3. The Macroeconomics of International Financial Flows

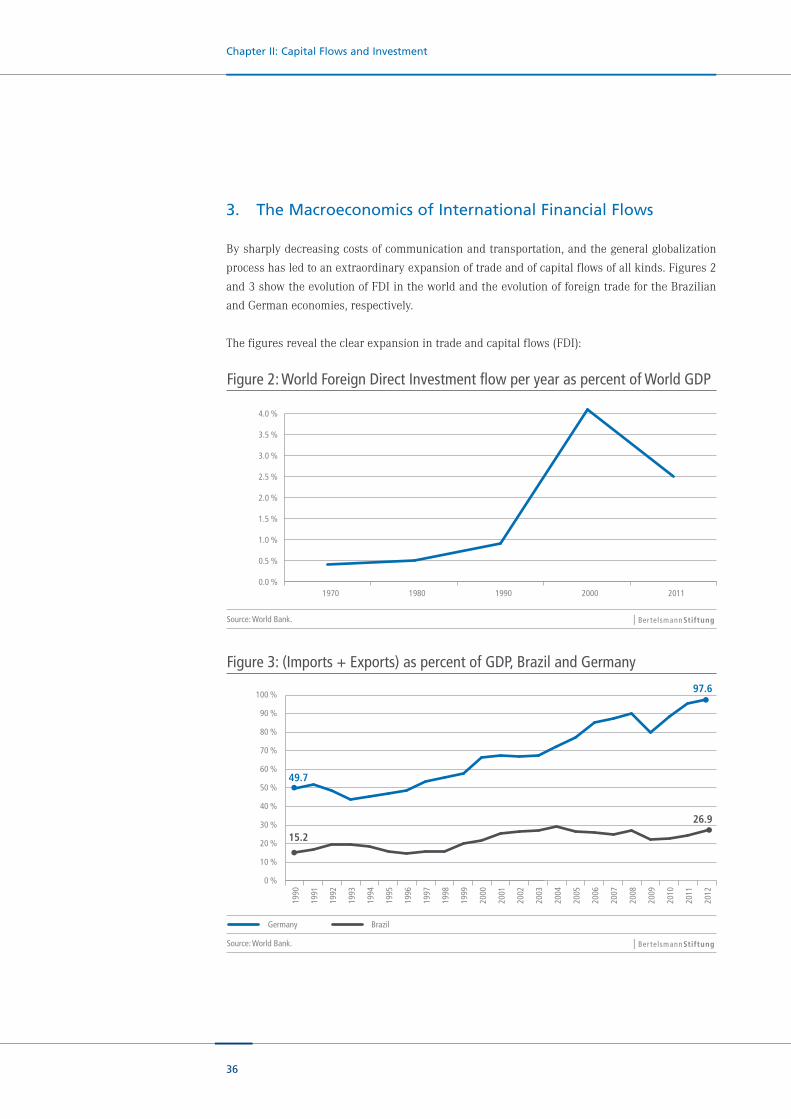

Bysharplydecreasingcostsofcommunicationandtransportation,andthegeneralglobalization

processhasledtoanextraordinaryexpansionoftradeandofcapitalflowsofallkinds.Figures2

and3showtheevolutionofFDIintheworldandtheevolutionofforeigntradefortheBrazilian

andGermaneconomies,respectively.

Thefiguresrevealtheclearexpansionintradeandcapitalflows(FDI):

Figure 3: (Imports + Exports) as percent of GDP, Brazil and Germany

0 %

10 %

20 %

30 %

40 %

50 %

60 %

70 %

80 %

90 %

100 %20

12

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

2000

1999

1998

1997

1996

1995

1994

1993

1992

1991

1990

49.7

97.6

15.2

26.9

Source: World Bank.

Germany Brazil

Source: World Bank.

Figure 2: World Foreign Direct Investment flow per year as percent of World GDP

0.0 %

0.5 %

1.0 %

1.5 %

2.0 %

2.5 %

3.0 %

3.5 %

4.0 %

20112000199019801970

37

Chapter II: Capital Flows and Investment

Net recipientsof financial flowsmay runcurrentaccountdeficits (i.e., theymay receiveanet

positiveexcessvalueofgoodsandservicesfromabroad,allowingthemtosustainahigherlevel

ofinvestmentand,consequently,obtainahigherpotentialGDPgrowthrate).Countriesthatare

suppliersofsavingsruncurrentaccountsurpluses,transferringabroadgoodsandservicesnow

andexpectingtoreceivefuturerepaymentsofgoodsandservices(seeObstfeldandRogoff,1996).

Figure4shows that,during thepast20years,Brazilhasabsorbedmore foreignsavings than

Germany:Germanyhasbeenanexporterofsavingssince2000,andparticularlyinthelastfive

years,theGermancurrentaccountwasinconsiderablesurpluswhileBrazil’swasindeficit.

Foritspart,Brazilneedsforeignsavingstoincreaseitsrelativelylowfixedinvestment/GDPratio,

whichoscillatedaround17to18percent,wellabovethelowlevelofdomesticsavings(14to15

percentofGDP).Table11,below,showsthetotalfixedinvestmentinBrazilasapercentofGDP.

Theratiohasbeensomewhatbelow20percentduring the firstdecadeof thecurrentcentury.

Bycomparison,inChinaithasbeenaround50percent.TheBrazilianinvestmenttoGDPratiois

twotofivepercentagepointslowerthanthesamerateinseveralotherLatinAmericancountries,

includingChile,Argentina,Peru,ColombiaandMexico.

Figure 4: Current Account Balance as percent of GDP; Germany and Brazil.

–5 %

–4 %

–3 %

–2 %

–1 %

0 %

1 %

2 %

3 %

4 %

5 %

6 %

7 %

8 %

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

2000

1999

1998

1997

1996

1995

1994

1993

1992

1991

1990

Source: World Bank.

Germany Brazil

38

Chapter II: Capital Flows and Investment

Internationalfinancialflowsarethecrucialtransmissionmechanismofsavingsamongcountries.

These flows finance current account deficits. Yet the recent and substantial expansion of

internationalcapitalflowsbetweencountriesandcurrencieshasraisedthequestionofwhether

theseflowsareathreattomacroeconomicstability.Thefearisthatasharp,possiblyunwarranted,

redirectionoftheseflowscouldoverstateboththeupsideanddownsideofacountry’seconomic

conditions.

Thus,thekeyquestioniswhetherthefreeflowofcapitalisonthewholemoreofabenefitforthe

countriesinvolvedthanitisadetraction.Toanswerthatquestion,weturntoProfessorJagdish

Bhagwati and his well-known article entitled “The Capital Myth” (1998). Bhagwati favors free

tradeingoodsandservices,buthearguesthattotallyliberalizedcapitalmovements—thatisto

say,capitalofanysortandofanyamount—havedisadvantagesthatarenotpresentinthecaseof

freetrade.

The problem inherent to portfolio capital flows is that they are subject to contagion and herd

behavior,whichisattimesdrivenbypanics,maniasandcrashes.Destabilizingspeculators,defined

asthosewhobetagainstagivencountry’seconomicfundamentals,mayrealizehugeprofitsasthe

speculativebehavioritselfchangesthefundamentals.Economicmodelswithspeculativebehavior

havedifferentequilibriumpositions.Consequently,thewell-knownargumentofMiltonFriedman

(1953),thatdestabilizingspeculationwouldeventuallypunishthespeculatorswithlossesonce

theunderlyingfundamentalsreassertthemselves, istheoreticallyincorrect.Speculationsimply

changesthefundamentalsinmodelswithspeculation.ResearcherssuchasTriffin(1957),Aliber

(1962),Obstfeld(1986)andothershaveshownthiswhilealsoraisingthepossibilityofmultiple

economicequilibria.Moreover,freecapitalflowsinthepresenceoftradedistortions(tariffs,quotas,

etc.)maynotbeasecond-bestsolution,accordingtoargumentsdevelopedbyCooper(1998,1999).

Notallformsofinvestmentcausethesekindsofrisks.Infact,themajorgainsfromcapitalflows

todevelopingcountries(includingtheacquisitionofskillsandtechnology)maybeobtainedby

Table 11: Fixed Investment as percent of GDP in BrazilYear Fixed Investment2000 16.82001 17.02002 16.42003 15.32004 16.12005 15.92006 16.42007 17.42008 18.72009 16.72010 18.4Source: IpeaData

39

Chapter II: Capital Flows and Investment

encouraging direct foreign investment. This would imply that a successful policy grants free

exchangeconvertibilityonly to firms’earningsandcapital.Banks, firmsandcommoncitizens

shouldnothave theability to freelywithdrawshort-termcapital fromthecountry inwhatever

magnitudetheylike.Neithershouldtheybeabletomakeshort-termloans,whichcanincrease

sharply in the presence of unsustainable asset price movements and can reinforce economic

instability.

The case of Brazil presents an illuminating example of instabilities related to capital inflows.

In particular, in Brazil we find interesting results when these flows interact with the political

system,makingforanexcellentpoliticaleconomycasestudy.Capitalflowvolatilityhasbeenan

importantfactorbehindtheincreasedvolatilityofthedomesticexchangerateforthepastdecade.

Forexample,theshockstemmingfromtheSeptember2008globalcrisis(seeninFigure5),acting

through the flight of portfolio investments to other countries, was followed by an increase of

roughly50percentinthemarketexchangerateoftheBrazilianrealtotheUSdollarinlessthan

amonth.Beyondinflationarypressure,thiscurrencymovementcausedproblemsforcompanies

andbankswithdollarliabilities,withseveralsuchfirmsendingupgoingbankrupt.Laterinthe

sameyear,whentheextentofthecrisisbecameclearer(andtherelativelysolidfinancialposition

ofBrazilbecamewell-known),theexchangerateoftherealtothedollarreturnedtoitsprevious

level.

CapitalinflowswereattractedbythehighinterestratesinBrazil(thesehighrateswereaholdover

from the1990s,whenBrazil facedextremelyhighdomestic ratesof inflation).Figure7below

showstheevolutionofthemoneymarketinterestrateinBrazil,whileFigure6showstheend-of-

the-yearexchangerates.

Figure 5: Portfolio Investment Liabilities of Brazil to other countries. Stock of Equity Securities from 2001–2011, reported by Brazil

0

50

100

150

200

250

300

350

400

20112010200920082007200620052004200320022001

Source: CPIS/IMF.

Equity Securities

US$

, mill

ions

40

Chapter II: Capital Flows and Investment

The substantial appreciation of the real in this period caused problems for the export sector.

Moreover, the averageBrazilian rate of inflation in the sameperiodwasgreater than the rate

of inflationofBrazil’smore important tradingpartners.Brazilian ratesof inflation reachedan

averageof justunder sixpercent in2003–2013, consistently reaching theceilingofmonetary

policytargetsandfarsurpassingratesintradepartnercountriessuchasGermany(1.82percent

inthatperiod)andtheUS(2.40percent).Brazilianindustrialexportstookaserioushitfromthe

combinationofnominalexchangeappreciationandhigher inflation,as it impliedasignificant

appreciationofthereal.

TheBraziliangovernmentreactedtotheappreciationoftherealbybuyingforeigncurrencyin

theexchangemarketsinordertoavoiddevaluation.Asaresulttheinternationalreservesofthe

Source: IPEAdata.

Figure 6: Exchange Rates R$/US$

0.0 %

0.5 %

1.0 %

1.5 %

2.0 %

2.5 %

3.0 %

3.5 %

20122011201020092008200720062005200420032002

2.892.65

2.342.14

1.77

2.34

1.74 1.67 1.88 1.97

0 %

5 %