strategic debt with multi-task technologies

TRANSCRIPT

Strategic debt with multi-task technologies

A L B E RT O DA L M A Z Z O Universita di Siena

Abstract.In this paper it is shown that when employees have ex post bargaining power, theentrepreneur will try to avoid technologies that are based on a large number of complemen-tary tasks. We demonstrate that the entrepreneur can shelter profit from the employees’ rent-seeking behaviour by raising debt. Moreover, the strategic use of debt financing can favourthe adoption of technologies that rely on synergies. JEL Classification: G31, J30, L20

Dette strate´gique en pre´sence de technologies impliquant plusieurs taˆches.Ce memoiremontre que quand les employes ont un pouvoir de negociation ex post, l’entrepreneur vatenter d’eviter les technologies qui sont basees sur un grand nombre de taches complemen-taires. On montre que l’entrepreneur peut proteger ses profits des activites de chasse auxrentes des employes en accroissant sa dette. De plus, l’utilisation strategique du financementpar la dette peut favoriser l’adoption de technologies qui dependent de synergies.

1. Introduction

As Harris and Raviv noted in their 1991 survey, the relation between capital struc-ture on the one hand, and product and input markets on the other hand had beensomewhat underexplored. Since then, some authors have further investigated therole of leverage on oligopolistic competition, following the seminal work ofBrander and Lewis (1986) (see, e.g., Zechner 1996). Other authors, following Bald-win (1983), have focused on the role of debt in wage bargaining when long-termlabour contracts cannot be written. In this paper we explore the effect of the capitalstructure on the investment decision when employees bargain over the firm’s sur-plus ex post.

I am grateful to Agnes Allansdottir, Melvyn Coles, Alan Manning, David Ulph, and, in particular,to an anonymous referee for their comments and suggestions on previous versions of this paper.All remaining errors are mine. Financial support from MURST and CNR is gratefully acknowl-edged. E-mail: [email protected]

Canadian Journal of Economics / Revue canadienne d’Economique, Vol. 33, No. 1February / fevrier 2000. Printed in Canada / Imprime au Canada

0008-4085 / 00 / 252–70 $1.50 � Canadian Economics Association

Strategic debt 253

In our model, the entrepreneur has access to an investment project for which hecan choose the level of technological ‘sophistication,’ defined as the number oftasks that have to be performed in production. Both the returns and the investmentcosts increase as technological sophistication rises. Each task is performed by asingle employee who acquires some specific knowledge in production. The inter-dependence among the productive tasks is such that if one or more employeesdecide not to contribute to the production process, output drops to zero. Our notionof technology is compatible with other contributions. Kremer (1993) and Milgromand Roberts (1990, 1995) consider production functions with complementary tasks.Hart (1995) and Stole and Zwiebel (1996) analyse models where asset-complementarity generates ‘synergies’ among the productive activities of the firm.

When binding labour contracts cannot be written,1 the employee’s specificity inproduction is particularly important. The ex ante investment decision made by theentrepreneur is distorted, since each employee has some bargaining power over thereturns that the firm will generate. In particular, we show that the type of projectchosen in equilibrium tends to be under-sophisticated, since any additional invest-ment in technological sophistication must be financed entirely up front by the en-trepreneur, while the benefits will be shared by all the employees through thebargaining process. The central issue of the paper is how the capital structure affectsthe investment decision. We show that the entrepreneur benefits from raising debton a competitive financial market. By issuing debt, the entrepreneur gets cash todayagainst the promise to repay tomorrow. If the employees halt production and pre-vent debt repayment, bankruptcy occurs and the debtholder obtains the propertyrights over the firm’s physical assets. Bankruptcy thus makes the debtholder abargaining agent, as in Hart and Moore (1994). We show that when debt is not toohigh, the employees will prefer to agree and have debt repaid, rather than to starta bankruptcy process where creditors seize part of the surplus. Once debt has beenrepaid, however, the net size of the surplus that is bargained over is reduced. Theability of debt to reduce the workers’ bargaining power has been demonstrated byseveral authors, such as Sarig (1988), Bronars and Deere (1991), Perotti and Spier(1993), Dasgupta and Sengupta (1993), and Dalmazzo (1996). What distinguishesthis paper from other contributions on debt and wages is the finding that debt canfavour the selection of technologically sophisticated projects. This result is relevantbecause it suggests that some technologies based on interdependent activities, or‘synergies,’ can be implemented only whenefficient financial markets exist.

Our model is very stylized and it abstracts from many relevant issues (such asasymmetric information, agency problems between managers and shareholders).The special relevance to debt given by our setup, however, is empirically justified.Debt is the most relevant form of finance, especially where new corporate invest-ment is concerned (see Mayer 1988). Bolton and Scharfstein (1996) report thatfirms raise external funds mainly in the form of debt, which accounts for 85 percent of all external financing. The implication that debt issues reduce the labour

1 For a discussion of labour-contract incompleteness, see Stole and Zwiebel (1996).

254 A. Dalmazzo

share is also supported by recent empirical findings (see Hanka 1998). Moreover,our paper opens up an interesting perspective on the role of financial markets.Recently, Caballero and Hammour (1998) have shown that the ‘holdup’ problemsgenerated at the microeconomic level by specific firm-worker relationships can alsolead to heavy distortions at the macroeconomiclevel, such as involuntary unem-ployment, inefficient technology choice, and ‘sclerosis.’ Although our analysis iskept exclusively at the firm level, the idea that debt has redistributive propertiesmay constitute a building block for integrating financial markets into Caballero andHammour’s ‘macroeconomics of specificity.’

The setup and the basic results of our analysis are presented in sections 2 and3. In section 4, we analyse the effect of multiple credit relationships. Since eachdebtholder has some bargaining power in case of bankruptcy, the employees’ sharedecreases as the number of creditors rises. The firm’s debt capacity also increases,reducing the net surplus that is bargained over. Thus, multiple credit relationshipsreinforce the redistributive impact of debt and reduce the extent of inefficiency dueto ex post bargaining. In section 5, we briefly consider the employees’ firm-specificinvestment in human capital. Debt can have perverse effects on the workers’ in-centive to invest in firm-specific human capital, since the strategic use of debtreduces the employees’ share. Therefore, when the workers’ investment is essential,the entrepreneur will have an incentive to commit not to use debt strategically. Thiscan be done through several mechanisms, such as building a reputation or frag-menting the control on financial and economic decisions. We conclude in sec-tion 6.

2. The basic framework

In what follows, we give a detailed description of the model.

2.1 Technology and efficiencyThe entrepreneur (agent 1) has access to a set of N alternative investment projects.Each project is characterized by a number n of complementary tasks, with n �[1,N]. Although the functions we consider are defined only for discrete values ofn, it will be useful to treat n as a continuous variable. A project of type n costsI(n), with I�(n) � 0 and will yield a return equal to Y(n), with Y�(n) � 0, if allthe n tasks are performed. We assume that the interdependence among the produc-tive activities is such that, if one or more tasks are not performed, returns drop tozero. Our notion of technology is consistent with other approaches. In Kremer’s(1993) O-Ring production theory, the complexity of a technology is measured bythe number of indispensable tasks required to produce the output. Thus, an Amer-ican jet-fighter airplane is a more sophisticated product than a Korean automobile,because its production requires the execution of a greater number of operations,such as design, production, and assemblage of many special components. Milgromand Roberts (1990, 1995) provide a theory of ‘complementarity,’ induced by stronginterconnections among the various productive activities. They argue that the in-

Strategic debt 255

troduction of computers has progressively increased complementarity in moderntechnologies. The degree of interdependence among tasks has risen not only withinthe boundaries of the manufacturing process, but also among different sets of ac-tivities performed within the firm, such as manufacturing, marketing, and engi-neering. Hart (1995, 51) and Stole and Zwiebel (1996) analyse models in whichasset-complementarity generates ‘economies of scope,’ or synergies. The interde-pendence among productive activities may also depend on factors other than tech-nology. Organizational or strategic concerns may as well increase integration amongthe firm’s activities. As reported by The Economist(2 January 1999, 57), somelarge Italian firms prefer to rely on specific equipment produced by in-house work-shops to avoid disclosing sensitive information to competitors.

In our model, the entrepreneur retains the option of liquidating the project andobtains L(n), with L(n) � [0,I(n)], once the investment cost I(n) has been sunk.The liquidation value L(n) measures the degree of ‘reversibility’ of the investmentproject: when L(n) is low, the degree of asset-specificity is high.

An individual who opts for an autarkic project (n � 1) will obtain Y(1) �I(1) � y, which is normalized to zero. We also assume that net returns Y(n) � I(n)are positive and increasing in n (i.e., it holds that Y�(n) � I �(n) � 0). Sinceefficiency requires that Y(n) � I(n) be maximized, the social optimumwill corre-spond to n � N, the most sophisticated project.

2.2 Contracting problems and surplus distributionWe assume that binding labour contracts cannot be written. As in Grout (1984),Stole and Zwiebel (1996), and many others, the employees are unable to committo a future wage decision and can enter into wage negotiations at any momentbefore production takes place. Further, because of the specific knowledge acquiredby the workers, they are very costly to replace. Employees thus have ex postbargaining power over the surplus generated by the firm.2

For simplicity, we suppose that each task is performed by a single employee.3

A production process with n complementary activities has an important implication:when the worker assigned to a task ‘strikes,’ production will be halted. Thus, then tasks required by the chosen technology are associated with an equal number ofbargaining parties. We adopt the Nash-bargaining solution generalized to k � 2players (see Osborne and Rubinstein 1990). Agent i’s equilibrium payoff in thebargaining game over R is given by

2 We rule out the possibility that employees are able to pay an entry fee to the firm (see also Stoleand Zwiebel (1996, 196, n3)). This is a reasonable assumption when workers are subject to liquid-ity costraints. If, on the contrary, each employee could make an up front payment to the firmequal to the value of the bargaining rents that he can appropriate ex post, social optimality wouldbe attained.

3 The assumption that each task is performed by a single employee is not crucial for the results weobtain. As shown by Horn and Wolinsky (1988), when there are more workers performing thesametask, they have an incentive to constitute a coalition (a ‘union’) to avoid being ‘played oneagainst the other’ by the entrepreneur during the bargaining process.

256 A. Dalmazzo

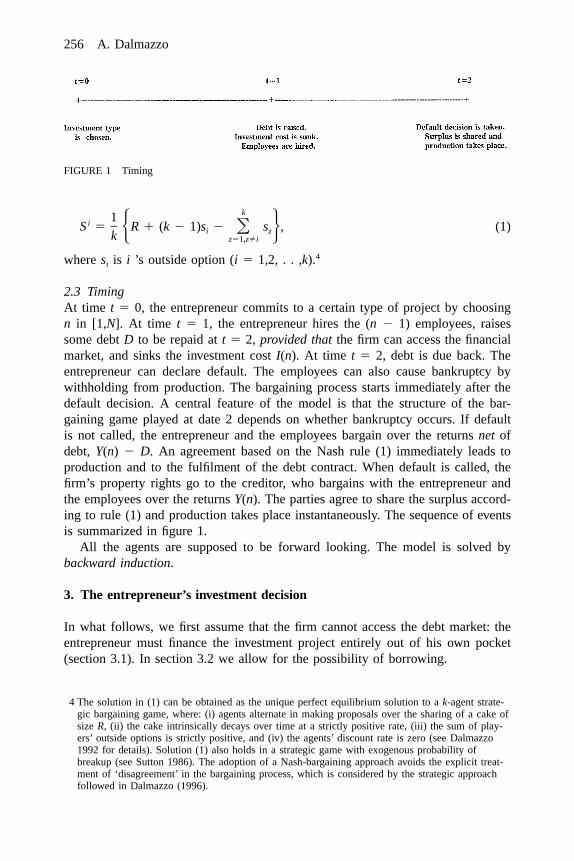

FIGURE 1 Timing

k1iS � R � (k � 1)s � s , (1)�� �i zk z�1,z�i

where si is i ’s outside option (i � 1,2, . . ,k).4

2.3 TimingAt time t � 0, the entrepreneur commits to a certain type of project by choosingn in [1,N]. At time t � 1, the entrepreneur hires the (n � 1) employees, raisessome debt D to be repaid at t � 2, provided thatthe firm can access the financialmarket, and sinks the investment cost I(n). At time t � 2, debt is due back. Theentrepreneur can declare default. The employees can also cause bankruptcy bywithholding from production. The bargaining process starts immediately after thedefault decision. A central feature of the model is that the structure of the bar-gaining game played at date 2 depends on whether bankruptcy occurs. If defaultis not called, the entrepreneur and the employees bargain over the returns net ofdebt, Y(n) � D. An agreement based on the Nash rule (1) immediately leads toproduction and to the fulfilment of the debt contract. When default is called, thefirm’s property rights go to the creditor, who bargains with the entrepreneur andthe employees over the returns Y(n). The parties agree to share the surplus accord-ing to rule (1) and production takes place instantaneously. The sequence of eventsis summarized in figure 1.

All the agents are supposed to be forward looking. The model is solved bybackward induction.

3. The entrepreneur’s investment decision

In what follows, we first assume that the firm cannot access the debt market: theentrepreneur must finance the investment project entirely out of his own pocket(section 3.1). In section 3.2 we allow for the possibility of borrowing.

4 The solution in (1) can be obtained as the unique perfect equilibrium solution to a k-agent strate-gic bargaining game, where: (i) agents alternate in making proposals over the sharing of a cake ofsize R, (ii) the cake intrinsically decays over time at a strictly positive rate, (iii) the sum of play-ers’ outside options is strictly positive, and (iv) the agents’ discount rate is zero (see Dalmazzo1992 for details). Solution (1) also holds in a strategic game with exogenous probability ofbreakup (see Sutton 1986). The adoption of a Nash-bargaining approach avoids the explicit treat-ment of ‘disagreement’ in the bargaining process, which is considered by the strategic approachfollowed in Dalmazzo (1996).

Strategic debt 257

3.1. Investment when no debt is raisedWhen the firm cannot raise any debt, the analysis of the investment decision isstraightforward. At t � 0, the entrepreneur decides the investment type by selectingthe profit-maximizing level of n. At t � 1, the investment cost I(n) is sunk, andthe (n � 1) employees are hired. At t � 2, the n-party bargaining occurs. Sincethe liquidation value of the project is positive, the entrepreneur’s outside option isL(n) � 0. The outside option available to each of the (n � 1) employees is supposedto be negligible. In order to evaluate the equilibrium payoffs at date 2, we useexpression (1) by setting R � Y(n) and k � n. The entrepreneur’s and the em-ployees’ (i � 2, . . , n;i � 1) shares are, respectively,

Y(n) � (n � 1)L(n) Y(n) � L(n)1 iS � , S � , (i � 2, . . ,n). (2)0 0n n

This setup generates two sources of inefficiency. First, the set of profitable projectsis smaller than the set of efficient projects (under-investment). Second, the type ofproject selected entails an inefficiently low number of tasks (for mere terminolog-ical convenience, we denote this kind of inefficiency with the term under-sophistication).

3.1.1 Under-investmentAs shown by Grout (1984), firms invest too little when workers cannot make cred-ible wage commitments before investment is sunk. Once the cost I(n) has beensunk at t � 1, the (n � 1) employees can appropriate part of the surplus ex post,at t � 2. Anticipating the employees’ rent-seeking behaviour, the entrepreneur willchoose to implement a n-task project at t � 0 only if the following condition holds:

Y(n) � (n � 1)L(n)M(n,0) � � I(n) � 0. (3)

n

Condition (3), which can be rewritten as Y(n) � I(n) � (n � 1)[I(n) � L(n)], ismore restrictive than the socially efficient condition Y(n) � I(n). Some sociallydesirable projects are not profitable and thus will not be implemented. The extentof the deviation from social efficiency amounts to (n � 1)[I(n) � L(n)] � 0. Thedifference (I(n) � L(n)) can be interpreted as a measure of project specificity, sincethe more the capital assets are specific to the project, the lower is their liquidationvalue.5

3.1.2 Under-sophisticationSocial efficiency requires that the project type is chosen to maximize Y(n) � I(n).Since it holds that Y�(n) � I �(n) � 0, the socially optimal investment type is N.Thus, projects aimed at producing sophisticated goods, or involving ‘synergies,’ aresupposed to generate the highest net returns. Consider the entrepreneur’s choice of

5 The outside option value in bargaining given by ‘capital reversibility’ is also discussed by Stoleand Zwiebel (1996, 218).

258 A. Dalmazzo

n when no debt can be raised (D � 0). At t � 0, the project choice solves thefollowing problem6:

Y(n) � (n � 1)L(n)max M(n,0) � max � I(n) , (4)� �n{n} {n}

where M(0,n) is assumed to be concave over [2,N].By solving (4), one obtains the following:

F.O.C. : (Y�(n) � I �(n)) � (n � 1)[I �(n) � L�(n)](D�0)

Y(n) � L(n)� � 0. (5)

n

When L�(n) is not too large,7 both the second and the third term on the l.h.s. of(5) are negative, leading to a deviation from the socially optimal rule, Y�(n) �I �(n) � 0. The private choice of n thus tends to be inefficiently low. Two distinctmechanisms cause under-sophistication. The first is due to the number of the partiesparticipating in the bargaining process.8 Selecting a higher n has benefits as wellas costs for the entrepreneur. On the one hand, a higher n raises the level of surplusto be shared, Y(n). On the other hand, a higher n reduces the entrepreneur’s shareof surplus, 1/n. A similar kind of mechanism has been pointed out by other authors.Chatterjee et al. (1993) consider a multi-party bargaining game a la Rubinstein(1982). They show that when all the coalition members have bargaining power overthe entire size of the cake, the size of the equilibrium coalition tends to be ineffi-ciently small. Similar results are obtained within bargaining frameworks that arequite different from ours, such as the ‘pairwise’ bargaining model proposed byStole and Zwiebel (1996). Since the workers manage to extract some surplus whenperforming tasks essential to the realization of economies of scope, the entrepreneurwill tend to avoid the adoption of technologies that involve synergies.

The second mechanism that drives under-sophistication is the following. SinceI(n) is increasing in n, ex post bargaining reduces the incentive to choose moresophisticated technologies. While the gains from a higher level of n, Y�(n), areappropriated by all the agents participating in production, the additional investmentcosts, I �(n), will be borne entirely by the entrepreneur. Thus, our model generatesthe incrementalversion of the classical ‘hold-up’ problem (see Williamson 1975;Grout 1984). These conclusions can be summarized as follows:

6 We suppose that condition (3) is respected at least for the value of n that maximizes (4).7 The difference I �(n) � L�(n) is surely positive when the liquidation value is decreasing in n (i.e.,

L�(n) � 0). This theoretical possibility has some plausibility, since n may measure the degree ofspecialization of the project (e.g., special components for a complex product, degree of interde-pendent activities in production, etc.). According to Williamson (1988), the more specialized aninvestment project, the lower the value of assets for alternative uses.

8 To gain a neater intuition of this mechanism, one can refer to the expressions in (2) calculated forL(n) � 0.

Strategic debt 259

RESULT 1. (Inefficiency of the private investment choice). When the employees whotake part in a project can bargain ex post over the surplus, the entrepreneur maydiscard socially efficient projects(under-investment). Further, the entrepreneurtends to select projects with an inefficiently low level of tasks(under-sophistication).

Result 1 has relevant implications for the models based on complementary tasks.Kremer (1993) assumes a competitive labour market and that workers do not ac-quire any specific knowledge in production. For this reason, the adoption of com-plex (multi-task) technologies is limited only by the availability of a high-qualityworkforce. Milgrom and Roberts (1990) assume that all the bargaining power iswith the firm. They thus avoid the problems raised by ex post wage negotiations.Our main conclusion so far is that sophisticated technologies may fail to be im-plemented even when the necessary know-how is available. We next show that thestrategic use of debt may offer a (partial) remedy to the distortions emphasized byresult 1.

3.2. Debt issuesSeveral authors have demonstrated that the strategic choice of leverage can affectthe distribution of surplus and increase the profit share. In particular, Dasgupta andSengupta (1993) and Dalmazzo (1996) have shown that debt issues can reduce theholdup problem by increasing the entrepreneur’s incentives to invest. We will showthat debt can also have relevant implications for the typeof project selected.

We exploit the ‘control rights’ approach to debt put forward by Hart and Moore(1994). Once that debt has been issued (at t � 1), the entrepreneur may decide todefault voluntarily at t � 2.9 Default may also occur when the workers refuse tobargain over the net surplus with the entrepreneur and prevent the firm from pro-ducing. Under default, the property rights on the firm’s assets pass from the entre-preneur to the lender. The lender decides whether to liquidate the firm or keep itas a going concern: in the latter case, the lender will bargain over the firm’s surplus.The peculiarity of the present approach is that default modifies the structure of thebargaining game to be played.

Suppose that at t � 1 the entrepreneur issues an amount of debt D to be repaidat t � 2 (the net interest rate is taken to be zero and the debt-market is competi-tive10). We claim the following:

LEMMA. The entrepreneur will not have an incentive to default on debt if and onlyif D � D*, where D* � [Y(n) � nL(n)] / (n � 1). Moreover, when the entrepreneurhas no incentive to default, the employees will not gain from bankruptcy.

9 In the present non-stochastic context, involuntary default never takes place.10 Debt-issues are particularly convenient when financial markets are efficient, since the entrepreneur

gets a fair price for the debt that is sold at the beginning.

260 A. Dalmazzo

In order to prove the lemma and show its implications, we distinguish betweentwo cases: (i) D � L(n), and (ii) D � L(n).

Case(i). Since D � L(n), the entrepreneur retains the possibility of liquidating theproject and repaying debt. Suppose, first, that the entrepreneur does not take actionsleading to default at t � 2. In the bargaining game over (Y(n) � D) the entrepreneurhas an outside option equal to L(n) � D, and will obtain a payoff equal to Snd �[(Y(n) � D) � (n � 1)(L(n) � D)] /n � [Y(n) � (n � 1)L(n)] /n � D. Suppose,instead, that the entrepreneur decides to default. The firm’s property rights go tothe lender, whose outside alternative is the liquidation value L(n). The entrepreneur,the lender, and the (n � 1) employees bargain over Y(n). Since the entrepreneur’sdefault payoff is equal to Sd � [Y(n) � L(n)] / (n � 1), it can be readily shownthat Snd � Sd: when the liquidation value is lower than debt repayments, the en-trepreneur will neverdefault. This has an important implication. When D � L(n),debt has no impacton the employee’s share, which is equal to [(Y(n) � D) �(L(n) � D)] /n � [Y(n) � L(n)] /n. It is also evident that employees have no in-centive to trigger bankruptcy, because each would receive only [Y(n) � L(n)] /(n � 1).

Case(ii ). When D � L(n), the entrepreneur implicitly gives up the possibility ofliquidating the project. His outside option is now equal to zero. When default doesnot occur, the entrepreneur bargains over Y(n) � D with the (n � 1) employeesand receives Snd � [Y(n) � D] /n. In case of default, the entrepreneur bargains overY(n) with the employees and the lender, obtaining Sd � [Y(n) � L(n)] / (n � 1).Hence, the entrepreneur will have no incentive to trigger bankruptcy when theinequality Snd � Sd holds. This condition corresponds to D � D* � [Y(n) �nL(n)] / (n � 1). D* is the lender’s share in case of default (the lender will neverfind it convenient to liquidate the firm, since D* � L(n)). This result leads to somerelevant consequences. First, the lender will never concede an amount larger thanD* to the entrepreneur. D* defines the firm’s debt-capacity,a function of theproject type n: D* � D* (n).11 Second, any level of D in(L(n),D*] reduces theemployee’s share in bargaining. Each employee will receive [Y(n) � D] /n. It isevident that even if debt diminishes the labour share, no employee would benefitfrom default when the condition D � D* holds!

The debt contract is a credible threat in wage negotiations only when the entre-preneur commits to surrender control to the lender in the case that workers takeactions leading to default. The enforcement of this commitment requires only thatdebt repayments exceed the firm’s liquidation value. When the level of debt is less

11 The implication that the debt-capacity D*(n) is increasing in the liquidation value L(n) is consis-tent with empirical observation: see the literature quoted by Harris and Raviv (1991). More re-cently, Rajan and Zingales (1995) have found that measures of ‘asset tangibility’ are positivelyrelated to leverage in all the G7 countries.

Strategic debt 261

than D* , the employees will prefer to agree and have debt repaid, rather thantriggering a bankruptcy process where creditors can grab part of the surplus.

In order to analyse the effects of debt on the investment choice (at t�0), profitmust first be characterized as a function of debt. Under Case (i), debt has no effecton the employees’ shares; thus the analysis coincides with the one developed inthe absence of debt(see section 3.1). Debt has a strategic role when the conditionsof Case (ii) are met. For any D � (L(n),D*], the payoff of each employee is equalto [Y(n) � D] /n, and the entrepreneur’s profit function is

Y(n) � DM(n;D) � Y(n) � (n � 1) � I(n)� �n

Y(n) n � 1� � D � I(n). (6)

n n

Since profit M(n,D) is monotonically increasing in D, at time t � 1 the entrepreneurwill borrow up to the firm’s debt-capacity, D*(n). The lender’s payoff is equal toD* , the amount lent (the competitive lender breaks even on the debt contract of-fered). When D � D* , each of the n agents taking part in bargaining at t � 2 willbe indifferent to having debt repaid, or defaulting. Since default does not bring anyadvantage, we assume that debt will be paid back. By evaluating (6) for D � D*,we obtain

2Y(n) � (n � 1)L(n)M(n,D*(n)) � � I(n), (7)

n � 1

which is greater than M(n,0) in (3) for any level of n. Thus, the entrepreneur willprefer to borrow up to D* , rather than to fund the project out of his own resources.The redistributive properties of debt are neatly illustrated when the employees’share is calculated for D � D* :

Y(n) � L(n)iS � , (i � 2,...,n). (8)D* n � 1

is lower than , the employee’s payoff when no debt is raised (see (2)). Thus,i iS SD* 0

the entrepreneur borrows, and spends, the amount D* at t � 1, against a contractualrepayment equal to D* , which will be borne at time t � 2 by all those whoparticipate in production,that is, both the entrepreneur and the employees. Recentempirical findings support the claim that debt may work as a device to modify thedistribution of surplus. Garvey and Gaston (1997) show that unionization andcapital-intensity drive high leverage. Hanka (1998) finds that high-debt firms pay,ceteris paribus, significantly lower wages. Further, debt increases are associatedwith significant wage reductions. According to Hanka, these findings are consistentwith the ‘disciplinary or bargaining power effects’ of debt (279).

We can now reconsider the investment decision when the entrepreneur has theopportunity to borrow. As noticed in section 3, the employees’ ex post rent-seeking

262 A. Dalmazzo

behaviour discourages investment in efficient projects, leading to under-investment.When the entrepreneur can borrow, the relevant condition for investing is thatM(n,D*) must be positive. Since debt raises the profit level that can be obtainedby any type of project, the profitability requirement M(n,D*) � 0 is less restrictivethan the corresponding one in the absence of debt financing, M(n,0) � 0 (see (3)).Because the set of efficient projects that the entrepreneur is willing to implementbecomes larger, debt can effectively reduce under-investment. This property of debthas been emphasized by Dasgupta and Sengupta (1993) and Dalmazzo (1996).What is most interesting, however, is that debt can also affect the quality of theinvestment. Let us consider the choice of the project type. At t � 0, the entrepreneurmust choose n to maximise the profit expression (7).12 When the function (7) isconcave over [2,N], the entrepreneur will choose a project-type that satisfies thefollowing condition:

n � 1F.O.C. : [Y�(n) � I �(n)] � [I �(n) � L�(n)](D�D* ) 2

Y(n) � L(n)� � 0. (9)

n � 1

Note that the negative terms in the l.h.s. of (9) are smaller in size than the corre-sponding terms in (5). Thus, the strategic use of debt favours the adoption oftechnologies with higher levels of n, reducing under-sophistication. This resultdepends on two distinct mechanisms. As noted in sect. 3.1, higher levels of nincrease the sizeof the surplus (dY(n) /dn � 0), at the cost of a smaller share(d[1/n] /dn � 0), since the number of bargaining parties becomes larger. A debt-issuedoes not affect the gains from higher sophistication, dY(n) /dn � 0, but it implicitlyraises the number of bargaining parties from n to (n � 1) (the equilibrium debtrepayment D* equals the lender’s share in case of default). Since the share 1/n isdecreasing and convexin n, debt reduces the size of the additional cost due to agreater number of bargaining parties.13 The second mechanism through which debtdrives higher sophistication can be illustrated with reference to the term in I �(n) �L�(n) on the l.h.s. of (9). The (negative) impact of this term on the choice of n issmaller under debt financing than under self-financing (see (5)). When more so-phisticated technologies are financed through debt, their incremental cost is spreadthrough debt repayments over all the agents taking part in the production process.Thus, debt effectively reduces the ‘holdup’ problem even in its incrementalversion.This conclusion implies that complex production methods that require costly assets

12 The solution to the maximum problem in (7) is obviously only economically meaningful when thecondition M(n,D*(n)) � 0 holds for the optimal level of n.

13 Consider a simple example. Suppose that n � 2 and no debt is raised. The shift from a project oftype n � 2 to a project of type n � 3 implies a fall in the share of surplus appropriated equal to(0.5-0.33) � 0.17 (we abstract from liquidation values, here). Suppose, now, that n is still equal to2, but debt is raised. Passing from n � 2 to n � 3 will imply a fall in the share of surplus equalto (0.33-0.25) � 0.12, which is lessthan 0.17. Thus, debt reduces the cost of adopting more so-phisticated technologies.

Strategic debt 263

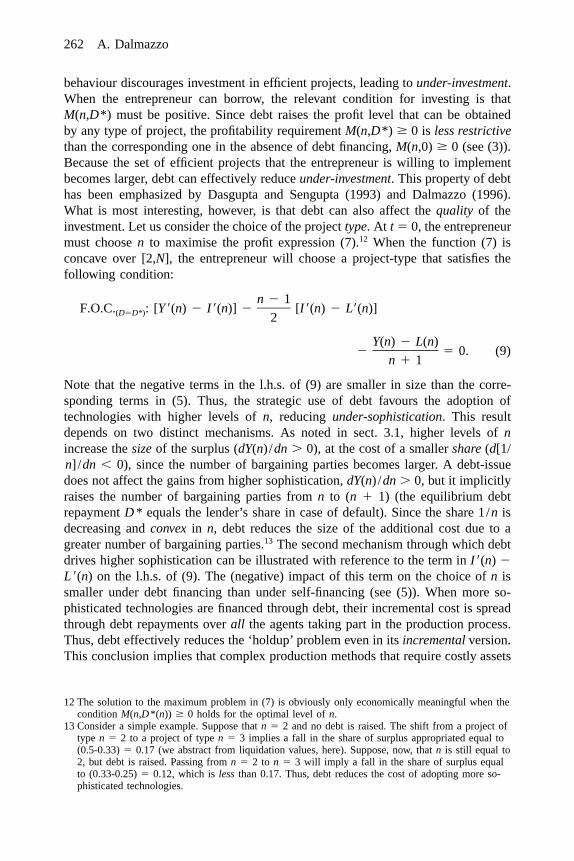

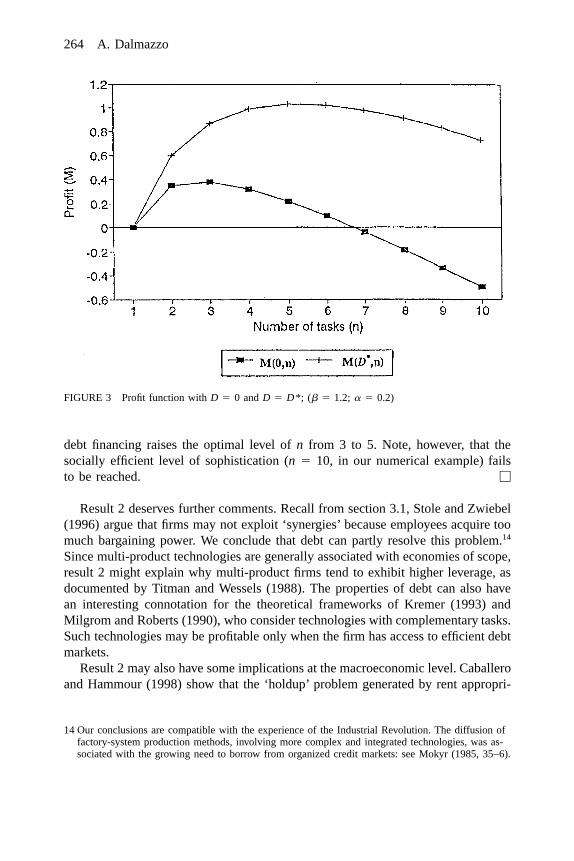

FIGURE 2 Profit function with D � 0 and D � D*; (� � 1; � � 0.2)

may be scarcely profitable when the entrepreneur cannot borrow. The positive cor-relation between leverage and expenditure in fixed assets is documented by Harrisand Raviv (1991) and, more recently, by Rajan and Zingales (1995). We summarizeour conclusions as follows:

RESULT 2. Strategic debt financing reduces under-investment and stimulates theentrepreneur to adopt more sophisticated investment projects.

Result 2 can be better understood by illustrating the effects of debt on the shapeof the profit function, M. The strategic use of debt raises the entrepreneur’s profitfunction for any level of n, and shifts its peak rightward. A simple example illus-trates this point.

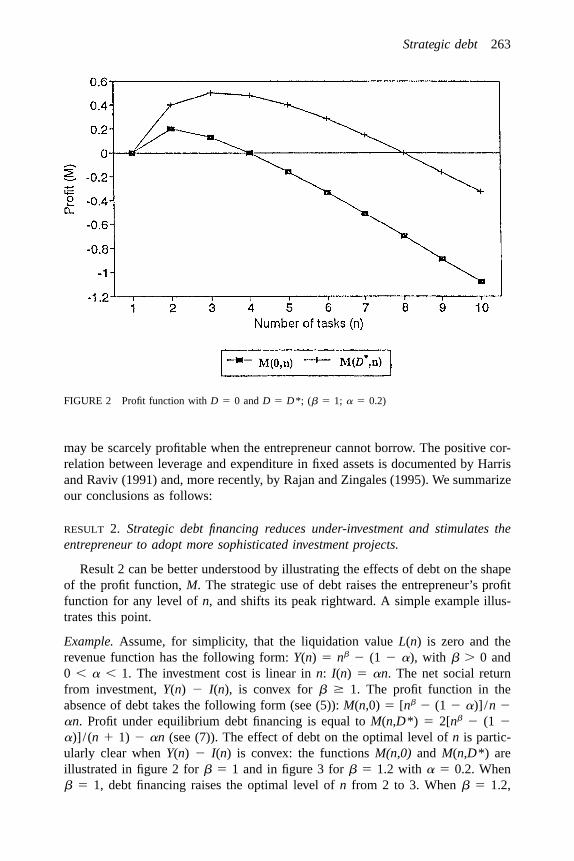

Example.Assume, for simplicity, that the liquidation value L(n) is zero and therevenue function has the following form: Y(n) � n� � (1 � �), with � � 0 and0 � � � 1. The investment cost is linear in n: I(n) � �n. The net social returnfrom investment, Y(n) � I(n), is convex for � � 1. The profit function in theabsence of debt takes the following form (see (5)): M(n,0) � [n� � (1 � �)] /n ��n. Profit under equilibrium debt financing is equal to M(n,D*) � 2[n� � (1 ��)] / (n � 1) � �n (see (7)). The effect of debt on the optimal level of n is partic-ularly clear when Y(n) � I(n) is convex: the functions M(n,0) and M(n,D*) areillustrated in figure 2 for � � 1 and in figure 3 for � � 1.2 with � � 0.2. When� � 1, debt financing raises the optimal level of n from 2 to 3. When � � 1.2,

264 A. Dalmazzo

FIGURE 3 Profit function with D � 0 and D � D*; (� � 1.2; � � 0.2)

debt financing raises the optimal level of n from 3 to 5. Note, however, that thesocially efficient level of sophistication (n � 10, in our numerical example) failsto be reached. �

Result 2 deserves further comments. Recall from section 3.1, Stole and Zwiebel(1996) argue that firms may not exploit ‘synergies’ because employees acquire toomuch bargaining power. We conclude that debt can partly resolve this problem.14

Since multi-product technologies are generally associated with economies of scope,result 2 might explain why multi-product firms tend to exhibit higher leverage, asdocumented by Titman and Wessels (1988). The properties of debt can also havean interesting connotation for the theoretical frameworks of Kremer (1993) andMilgrom and Roberts (1990), who consider technologies with complementary tasks.Such technologies may be profitable only when the firm has access to efficient debtmarkets.

Result 2 may also have some implications at the macroeconomic level. Caballeroand Hammour (1998) show that the ‘holdup’ problem generated by rent appropri-

14 Our conclusions are compatible with the experience of the Industrial Revolution. The diffusion offactory-system production methods, involving more complex and integrated technologies, was as-sociated with the growing need to borrow from organized credit markets: see Mokyr (1985, 35–6).

Strategic debt 265

ation can have pervasive macroeconomic consequences. In particular, the presenceof relationship-specific investments may cause several general-equilibrium pathol-ogies, such as under-investment, involuntary unemployment, and ‘sclerosis’ in thetechnological choice. Our results suggest that the strategic use of debt may alleviatethe problems generated by ‘specificity’ in the firm-worker relation and give anoriginal explanation as to why the presence of financial markets can stimulate highlevels of economic activity and growth.15 Financial markets might matter becausethey provide effective tools to redistribute the surplus created by specific firm-employee relationships.

We next consider two extensions to the basic model developed above. In section4, we will analyse the presence of multiple credit relationships. In section 5, wewill analyse employees’ investment in firm-specific skills, showing that strategicdebt can discourage employees to acquire specific competencies in the firm.

4. Multiple credit relationships

In section 3 we assumed that the entrepreneur borrowed from a single competitivelender. We now consider the more general case when the entrepreneur borrowsfrom X � 1 different lenders. All the existing debt has the same seniority. Shoulddefault occur at t � 2, each lender has the right to impose the liquidation of thefirm and get a fraction 1/X of the liquidation value L(n). If the firm is not liquidated,the X lenders will take part16 in a (n � X) � agents bargaining game over Y(n).The outside option of each lender is worth L(n) /X, while the entrepreneur’s andthe employees’ outside alternatives are zero. Hence, lender �’s payoff in the bank-ruptcy game over Y(n) will be

n�X1 L(n)Y(n) � (n � X � 1) � s�� �jn � X X j�1, j��

1 n� Y(n) � L(n) , (10)� �n � X X

where � � 1,2, . . ,X. Expression (10) defines , the maximum amount that each*D�

lender is willing to concede. Since the number of lenders is X, the firm’s debt-capacity is equal to X � . The profit expression Y(n) � (n � 1)[(Y(n) � ��D�)*D�

15 In several recent papers on finance and growth it has been shown that both the presence of devel-oped financial markets and their propensity to finance private entrepreneurship favour investmentand growth: see Levine (1997) for a comprehensive survey. On the basis of an international com-parison of firms, Rajan and Zingales (1998) find that industries that are more dependent on exter-nal finance grow relatively faster in countries with developed financial systems. In particular, theinvestment level in such industries is ‘disproportionately higher’ in financially developed countries.

16 As in Bolton and Scharfstein (1996), one may think that debt is secured to X complementary partsof the firm’s physical assets. Each of these X parts can be liquidated by a lender in case of de-fault.

266 A. Dalmazzo

/n] � I(n), calculated for the debt-capacity level, is equal to

1 � X n � 1*M(n,XD ) � Y(n) � L(n) � I(n). (11)� � � �� n � X n � X

Profit is increasing in X. Moreover, when the number of credit relations becomesarbitrarily large (X → �), the entrepreneur’s payoff tends to Y(n) � I(n), the socialobjective. In this case, the entrepreneur manages to capture the whole surplus ofthe project.

Consider the optimal choice of n when there are multiple credit relationships.By maximising (11), the following condition is obtained:

n � 1F.O.C. : [Y�(n) � I �(n)] � [I �(n) � L�(n)]*(D�XD )� X � 1

Y(n) � L(n)� � 0. (12)

X � n

The l.h.s. of (12) is increasing in X. Therefore, the higher the number of creditrelations, the higher the level of n chosen in equilibrium. In particular, when X isarbitrarily large, the private criterium for choosing n will coincide with the sociallyoptimal rule, Y�(n) � I �(n) � 0. These implications are summed-up in the follow-ing result.

RESULT 3. The larger the number of credit relationships, the higher the profit level,and the higher the level of n chosen in equilibrium. For X→ �, private investmentis socially efficient.

The presence of multiple credit relations further reduces the impact of ex postbargaining on the ex ante investment decision. As the number of credit relationsrises, the number of claims over the firm’s surplus also increases. As a consequence,the employees’ share in the bargaining game played at t � 2 is reduced. Result 3is consistent with the observation that large and complex corporations generallyhave multiple credit relationships.

The discussion about the number of credit relationships also depends on thenature of the lender. When X is seen as the number of banks lending to the firm,this number is likely to be quite small (due, e.g., to the presence of ‘restrictivecovenants’; see Brealey and Myers (1991, 601–602)). Moreover, the assumption –common to Hart and Moore (1994) – that lenders are ready to renegotiate in caseof default is more suitable for institutions such as banks, since empirical evidencesuggests that bankruptcy negotiations are more likely to fail with dispersed debt-holders (see Gilson, Kose, and Lang 1990).17 The risks of inefficient liquidation

17 In Rajan’s words: ‘bank debt is easily renegotiated, because the bank is a monolithic, readily ac-cessible creditor. However, a typical arm’s-length creditor like the bondholder receives only publicinformation. It is hard to contact these dispersed bondholders and any renegotiation suffers frominformation and free-rider problems’ (1992, 1369).

Strategic debt 267

caused by dispersed creditors have been analysed in several papers.18 Bolton andScharfstein (1996) show that a high number of creditors makes asset liquidationmore costly to stop; for this reason, arm’s-length debt seems to be particularlyeffective to discourage voluntarydefault (the kind of default considered here).

Notwithstanding the possibility of liquidation, many firms place relevant partsof their debt directly. Although this fact can be explained differently,19 our modelsuggests that public debt is issued because it is a powerful instrument to redistributesurplus. Suppose that the presence of dispersed debtholders always leads to inef-ficient liquidation in case of default.20 Since liquidation implies that the entrepre-neur and the employees will receive nothing, default will be avoided as long as thecondition [Y(n) � D] /n � 0 holds. Thus, the maximum amount of debt a firm canraise through public issues is equal to the value of returns, which is D**(n) �Y(n). Neither the entrepreneur nor the employees will ever trigger bankruptcy, sincedefault on publicly issued debt forces the firm into liquidation. Evaluating the profitfunction for D �D**(n) yields

Y(n) � D**M(n,D**) � Y(n) � (n � 1) � I(n) � Y(n) � I(n). (13)

n

As the entrepreneur’s objective in (13) coincides with the social one, publicly issueddebt eliminates both under-investmentand under-sophistication. Hence,

RESULT 4. If default on publicly issued debt leads to liquidation, the entrepreneur’sinvestment decision will be efficient.

The implication of result 4 holds only when employees are not required to makeany firm-specific human capital investment. As shown by the simple example de-veloped in the next section, the consideration of firm-specific investment in humancapital can lead to very different conclusions on the efficiency-enhancing role ofdebt.

5. Employees’ firm-specific investment

Similarly to Hart (1995, 59–61), it can be supposed that the project yields a returnequal to Y(n;h*) only if each employee makes a specific human capital investmenth* � 0 when hired at t � 1. The employee’s utility function is U(x,h) � x � c(h),

18 See, among others, Bulow and Shoven (1978), Gertner and Scharfstein (1991), Detragiache andGarella (1996).

19 Public-debt issues can reduce managerial opportunism in the lending relation: see Bolton andScharfstein (1996). Rajan (1992) argues that public debt can be issued at lower rates than privatedebt, when banks have a monopoly rent over the firm.

20 Similar conclusions about the effects of public debt will also hold when a bankrupt firm is liqui-dated with probability � � (0,1], where � � � (X) and ��(X) � 0. In this case, the entrepreneurwill not default on debt repayments XD� when the condition [Y(n) � XD�] / (n � 1) � � � 0 �(1 � �)[Y(n) / (X � n)] holds. It is easy to show that debt capacity XD� is increasing in �. Thecase considered in the text corresponds to � � 1.

268 A. Dalmazzo

where x denotes income, and c(h) the (non-verifiable) investment disutility, withc(0) � 0, c� � 0, c� � 0. At t � 1, each employee has to decide whether to makethe specific investment, knowing that the entrepreneur can raise some debt. If theentrepreneur were not expected to issue any debt, each employee would invest inspecific human capital whenever the condition Y(n,h*)/n � c(h*) holds. If theentrepreneur is expected to borrow, each employee will invest only if the conditionY(n,h*) / (n � 1) � c(h*) holds. Thus, debt can destroy the incentive to invest inspecific human capital by diluting the employees’ share.21 In this case debt ‘holdsup’ the employees.22

The negative effect of debt on employees’ incentives can be neutralized. Ar-rangements such as ‘partnerships’ or ‘joint ownership’23 may devoid debt of itsredistributive effects. When the entrepreneur fragments the control on the firm,including control on financial decisions, among those who participate in production,all the n agents will have some rights over the funds raised through debt-issues.As a consequence, debt will lose its redistributive role.24 In general, the entrepre-neur will prefer to commit to avoid strategic debt whenever his employees have tomake some specific investment. This implication might help to interpret some ex-isting evidence. For instance, Garvey and Gaston (1997) find that the greater thevalue of specific human capital investment, the lower the level of debt. It is alsocommonly observed that high-growth firms, as well as firms spending much inR&D, exhibit low leverage (see Harris and Raviv 1991; Rajan and Zingales 1995).Since growing and innovative firms are more likely to rely on their employees’human capital investments, we expect that such firms avoid the strategic use ofdebt.

6. Conclusions

When the employees have specific skills in the task they perform and bindinglabour contracts cannot be written, an entrepreneur will have an incentive to investin projects that exhibit low levels of technological sophistication. We have shownthat this inefficiency is reduced when the entrepreneur can borrow. Our model isvery stylized and abstracts from many relevant issues in the theory of corporatefinance. Its strength lies in giving an original perspective on the role of debt. Inparticular, a well-functioning debt market can redistribute surplus away from the

21 This problem is even more evident when there are public debt issues (see sect. 4).22 The possibility that ‘large investors,’ such as large equity-holders or debt-holders, may expropriate

the rents from managers’ and employees’ firm-specific human capital investments is discussed byShleifer and Vishny (1997). Gertner, Scharfstein, and Stein (1994) emphasize the merits of inter-nal financewhen issues such as project monitoring, management’s incentive, and so forth are ex-plicitly considered.

23 For some examples where partnerships or joint ownership reduce the holdup problem, see Hart(1995, 53, 69).

24 This conclusion, reached from the point of view of control on capital-budgeting decisions, bearssome similarity to the main result of Hart and Moore (1990), where the property rights on assetsshould go to those agents that make crucial firm-specific investments.

Strategic debt 269

labour share and thus encourage the adoption of sophisticated technologies that,although efficient, would have been unprofitable otherwise.

References

Baldwin, Carliss Y. (1983) ‘Productivity and labor unions: an application of the theory ofself-enforcing contracts,’ Journal of Business56, 155–85

Bolton, Patrick, and David S. Scharfstein (1996) ‘Optimal debt structure and the numberof creditors,’ Journal of Political Economy104, 1–25

Brander, James A., and Tracy R. Lewis (1986) ‘Oligopoly and financial structure: the lim-ited liability effect,’ American Economic Review76, 956–70

Brealey, Richard A., and Stewart C. Myers (1991) Principles of Corporate Finance4thed. (New York: McGraw-Hill)

Bronars, Stephen G., and Donald R. Deere (1991) ‘The threat of unionization, the use ofdebt and the preservation of shareholder wealth,’ Quarterly Journal of Economics106,231–54

Bulow, Jeremy I., and John B. Shoven (1978) ‘The bankruptcy decision,’ Bell Journal ofEconomics9, 437–56

Caballero, Ricardo, and Mohammad Hammour (1998) ‘The macroeconomics of specific-ity,’ Journal of Political Economy106, 724–67

Chatterjee, Kalyan, Bhaskar Dutta, Debraj Ray, and Kunal Sengupta (1993) ‘A noncooper-ative theory of coalitional bargaining,’ Review of Economic Studies60, 463–77

Dalmazzo, Alberto (1992) ‘Outside options in a bargaining model with decay in the sizeof the cake,’ Economics Letters40, 417–21

–– (1996) ‘Debt and wage negotiations: a bankruptcy-based approach,’ Scandinavian Jour-nal of Economics98, 351–64

Dasgupta, Sudipto, and Kunal Sengupta (1993) ‘Sunk investment, bargaining and thechoice of capital structure,’ International Economic Review34, 203–20

Detragiache, Enrica, and Paolo Garella (1996) ‘Debt restructuring with multiple creditorsand the role of exchange offers,’ Journal of Financial Intermediation5, 305–36

Garvey, Gerald, and Noel Gaston (1997) ‘Getting tough with workers? More on the strate-gic role of debt,’ mimeo, University of British Columbia

Gilson, Stuart C., Kose John, and Larry H.P. Lang (1990) ‘Troubled debt restructuring: anempirical study of private reorganization of firms in default,’ Journal of Financial Eco-nomics27, 315–53

Gertner, Robert, and David S. Scharfstein (1991) ‘A theory of workouts and the effects ofreorganization law,’ Journal of Finance46, 1189–222

Gertner, Robert, David S. Scharfstein, and Jeremy C. Stein (1994) ‘Internal versus exter-nal capital markets,’ Quarterly Journal of Economics109, 1211–30

Grout, Paul A. (1984) ‘Investment and wages in the absence of binding contracts: a Nashbargaining approach,’ Econometrica52, 449–60

Hanka, Gordon (1998) ‘Debt and the terms of employment,’ Journal of Financial Eco-nomics48, 245–82

Harris, Milton, and Artur Raviv (1991) ‘The theory of capital structure,’ Journal of Fi-nance46, 297–355

Hart, Oliver (1995), Firms Contracts and Financial Structure(Oxford: Oxford UniversityPress)

Hart, Oliver, and John Moore (1990) ‘Property rights and the nature of the firm,’ Journalof Political Economy98, 1119–58

–– (1994) ‘A theory of debt based on the inalienability of human capital,’ Quarterly Jour-nal of Economics109, 841–79

Horn, Henrik, and Asher Wolinsky (1988) ‘Workers substitutability and patterns of unioni-sation,’ Economic Journal98, 484–97

270 A. Dalmazzo

Kremer, Michael (1993) ‘The O-Ring theory of economic development,’ Quarterly Journalof Economics108, 551–75

Levine, Ross (1997) ‘Financial development and economic growth: views and agenda,’Journal of Economic Literature35, 688–726

Mayer, Colin (1988) ‘New issues in corporate finance,’ European Economic Review32,1167–89

Milgrom, Paul, and John Roberts (1990) ‘The economics of modern manufacturing: tech-nology, strategy, and organization,’ American Economic Review80, 511–28

–– (1995) ‘Complementarities and fit, strategy, structure, and organisational change inmanufacturing,’ Journal of Accounting and Economics19, 179–208

Mokyr, Joel (1985) ‘The Industrial Revolution and the new economic history,’ in The Eco-nomics of Industrial Revolution, ed. Joel Mokyr (London: George Allen)

Osborne, Martin J., and Ariel Rubinstein (1990) Bargaining and Markets(San Diego, CA:Academic Press)

Perotti, Enrico C., and Kathryn E. Spier (1993) ‘Capital structure as a bargaining tool: therole of leverage in contract renegotiation,’ American Economic Review83, 1131–41

Rajan, Raghuram (1992) ‘Insiders and outsiders: the choice between informed and arm’s-length debt,’ Journal of Finance47, 1367–400

Rajan, Raghuram, and Luigi Zingales (1995) ‘What do we know about capital structure?Some evidence from international data,’ Journal of Finance50, 1421–60

–– (1998) ‘Financial dependence and growth,’ American Economic Review88, 559–86Rubinstein, Ariel (1982) ‘Perfect equilibrium in a bargaining model,’ Econometrica50,

97–109Sarig, Oded H. (1988) ‘Bargaining with a corporation and the capital structure of the bar-

gaining firm,’ mimeo, Tel Aviv UniversityShleifer, Andrei, and Robert W. Vishny (1997) ‘A survey of corporate governance,’ Jour-

nal of Finance52, 737–83Stole, Lars A., and Jeffrey Zwiebel (1996) ‘Organizational design and technology choice

under intrafirm bargaining,’ American Economic Review86, 195–222Sutton, John (1986) ‘Non-cooperative bargaining theory: an introduction,’ Review of Eco-

nomic Studies53, 709–24Titman, Sheridan, and Roberto Wessels (1988) ‘The determinants of capital structure

choice,’ Journal of Finance43, 1–19Williamson, Oliver (1975) Market and Hierarchies: Analysis and Antitrust Implications

(New York: Free Press)Williamson, Oliver (1988) ‘Corporate finance and corporate governance,’ Journal of Fi-

nance43, 567–91Zechner, Josef (1996) ‘Financial market-product market interactions in industry equilib-

rium: implications for information acquisition decisions,’ European Economic Review40, 883–96