stopanska banka ad - skopje financial … banka skopje 2007 a...stopanska banka ad – skopje 3...

TRANSCRIPT

STOPANSKA BANKA AD - SKOPJE

Financial Statements and Independent Auditors’ Report for the year ended December 31, 2007

STOPANSKA BANKA AD - SKOPJE

CONTENTS Page Independent Auditors’ Report 1 - 2 Income Statement 3 Balance Sheet 4 Statement of Changes in Equity 5 Statement of Cash Flows 6 - 7 Notes to the Financial Statements 8 – 60

STOPANSKA BANKA AD – SKOPJE

2

INDEPENDENT AUDITORS’ REPORT TO THE MANAGEMENT AND SHAREHOLDERS OF STOPANSKA BANKA AD - SKOPJE We have audited the accompanying financial statements (page 3 to 60) of Stopanska Banka AD - Skopje (hereinafter referred to as the “Bank”), which comprise the balance sheet as of December 31, 2007 and the income statement, statement of changes in equity and cash flow statement for the year then ended, and a summary of significant accounting policies and other explanatory notes to the financial statements.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with the accounting standards applied in the Republic of Macedonia. This responsibility includes: designing, implementing and maintaining internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Auditors’ Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with Audit Law of the Republic of Macedonia and International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the preparation and fair presentation of the financial statements of the Bank in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Bank’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the financial statements of the Bank present fairly, in all material respects the financial position of Stopanska banka AD - Skopje as of December 31, 2007, and its financial performance, changes in equity and its cash flows for the year then ended in accordance with accounting standards applied in the Republic of Macedonia and accounting policies presented in Notes 2 and 3 to the financial statements.

Deloitte DOOEL Lidija Nanush Biljana Nasteska Chartered Accountant Chartered Accountant Manager Skopje January 25, 2008

STOPANSKA BANKA AD – SKOPJE

3

INCOME STATEMENT Year ended December 31, 2007 (Expressed in thousands of Denars) Note 2007 2006 Interest income 3.1, 5 3,362,413 2,565,016 Interest expense 3.1, 5 (1,194,464) (756,341) Net interest income

2,167,949 1,808,675

Fee and commission income 3.1, 6 969,173 833,590 Fee and commission expense 3.1, 6 (50,886) (43,541) Net fee and commission income

918,287 790,049

Dividend income 7,892 1,977 Foreign exchange gains, net 3.2 111,976 94,810 Net trading income 7 614 842 Impairment losses, net 8 (495,388) (477,455) Other operating income 9 121,176 124,330 Other operating expenses 10 (1,713,792) (1,559,463) PROFIT BEFORE TAXATION 1,118,714 783,765 Income tax 11 (11,587) (8,638) NET PROFIT 1,107,127 775,127

The accompanying notes are an integral part of these financial statements. The financial statements were approved by the management of the Bank on January 24, 2008 and shall be proposed on approval by the Bank’s Board of Directors. Signed on behalf of Stopanska banka AD - Skopje: Mr. Gligor Bishev Mr. Georgios Papanastasiou First General Manager Second General Manager

STOPANSKA BANKA AD – SKOPJE

4

BALANCE SHEET At December 31, 2007 (Expressed in thousands of Denars) Note 2007 2006 ASSETS Cash and cash equivalents 12 4,722,680 4,664,562 Treasury and other eligible bills 13 5,232,175 2,426,260 Financial instruments held for trading 14 253,301 147,765 Financial instruments available for sale 14 123,123 107,354 Financial instruments held to maturity 14 3,838,602 4,391,916 Placement with, and loans to, banks 15 5,443,514 6,001,414 Loans to customers 16 32,917,403 21,659,311 Other receivables 17 1,021,369 1,023,626 Investment property 18 110,334 153,987 Leasehold improvements 19 20,268 20,754 Intangible assets 20 89,589 149,853 Property and equipment 21 1,134,954 1,162,151 Deferred tax assets 11 1,789 2,102 Total assets 54,909,101 41,911,055 LIABILITIES AND EQUITY LIABILITIES Deposits from banks and financial institutions 22 3,750,252 2,232,155 Deposits from customers 23 43,280,888 32,962,368 Loans payable 24 320,207 377,980 Subordinated debt 25 1,224,032 1,223,482 Preferred shares obligations 26 90,978 90,978 Other liabilities 27 740,141 578,426 Income tax payable 11 2,747 8,929 Deferred tax liabilities 11 1,307 - Obligations toward employees 14,908 - Total liabilities 49,425,460 37,474,318 EQUITY 28 Share capital 3,511,242 3,511,242 Reserves 252,977 147,555 Retained earnings 612,295 2,813 Net profit for the year 1,107,127 775,127 Total equity 5,483,641 4,436,737

Total liabilities and equity 54,909,101 41,911,055 Commitment and contingencies 31 10,639,454 6,938,483

The accompanying notes are an integral part of these financial statements.

STOPANSKA BANKA AD – SKOPJE

5

STATEMENT OF CHANGES IN EQUITY Year ended December 31, 2007 (Expressed in thousands of Denars)

Share Capital

Revalued Reserve

Statutory Reserve

Special Fund

Retained Earnings

Total

Balance, January 1, 2006 3,511,242 22,610 1,911 1,083 124,764 3,661,610 Transfer to statutory reserve - - 121,951 - (121,951) - Profit for the year - - - - 775,127 775,127 Balance, December 31, 2006 3,511,242

22,610 123,862 1,083 777,940 4,436,737

Balance, January 1, 2007 3,511,242 22,610 123,862 1,083 777,940 4,436,737 Transfer to statutory reserve - - 116,269 - (116,269) - Paid dividends - - - - (71,986) (71,986) Transfer of revalued reserve to retained earnings -

(22,610) - - 22,610 -

Revalued reserve from reassessment of equity securities -

11,763 - - - 11,763

Profit for the year - - - - 1,107,127 1,107,127 Balance, December 31, 2007 3,511,242 11,763 240,131 1,083 1,719,422 5,483,641

The accompanying notes are an integral part of these financial statements.

STOPANSKA BANKA AD – SKOPJE

6

STATEMENT OF CASH FLOWS Year ended December 31, 2007 (Expressed in thousands of Denars) 2007 2006 Profit before taxation 1,118,714 783,765 Adjustments for: Depreciation and amortization of: - Property and equipment 149,700 170,014 - Intangible assets 68,948 69,055 - Investment property 3,919 4,608 - Leasehold improvements 4,819 1,230 Capital gain: - Sale of property and equipment (41,513) (67,939)Interest income (3,362,413) (2,565,016)Interest expense 1,194,464 756,341 Net trading income (614) (842)Write-offs - 6,933 Impairment losses 879,381 993,293 Impairment losses for: - Investment property 7,117 11,741 - Assets acquired through foreclosure procedure 39,294 - Release of impairment for balance sheet items (383,993) (428,279)Impairment/(release) of impairment for off-balance sheet items - (87,559)Interest receipts 3,309,409 2,553,276 Interest paid (1,134,860) (737,045) Operating profit before changes in operating assets: 1,852,372 1,463,576 (Increase)/decrease of operating assets: Purchase of bonds held-for-trading (102,325) (73,535)Placements with, and loans to, banks 10,134 7,835 Loans to customers (11,732,446) (6,050,935)Increase/(decrease) in other assets 55,248 129,100 Increase/(decrease) in other liabilities: Deposits from banks and financial institutions 1,517,234 166,012 Deposits from customers 10,242,646 5,746,738 Other liabilities 159,663 135,780 Net cash flows from operating activities before income tax 2,002,526 1,524,571 Income tax paid (8,527) (1,811)Net cash flows from operating activities 1,993,999 1,522,760

STOPANSKA BANKA AD – SKOPJE

7

STATEMENT OF CASH FLOWS (Continued) Year ended December 31, 2007 (Expressed in thousands of Denars) 2007 2006 Cash flows from investing activities Acquisition of property and equipment (202,969) (215,983)Acquisition of intangible assets (8,714) (16,998)Acquisition of investment property - (1,007)Net proceeds from investments 575,128 114,922 Proceeds from sale of property and equipment 55,780 219,612 Proceeds from sale of investment property 39,446 37,204 Investments in leasehold improvements (9,540) (16,851)Net cash flows from investing activities 449,131 120,899 Cash flows from financing activities Net decries/increase of borrowings (65,011) 531,253 Payment of dividend (71,986) - Subordinated debt - 1,223,482 Net cash flows from financing activities (136,997) 1,754,735 Net increase of cash and cash equivalents 2,306,133 3,398,394 Cash and cash equivalents, beginning of year 13,092,236 9,693,842 Cash and cash equivalents, end of year 15,398,369 13,092,236 Cash and cash equivalents, end of year: Cash and cash equivalents, end of year (Note 12) 4,722,680 4,664,562 Treasury bills and other eligible bills (Note 13) 5,232,175 2,426,260 Deposits with banks placed for up to 30 days (Note 15) 5,443,514 6,001,414 15,398,369 13,092,236

The accompanying notes are an integral part of these financial statements.

STOPANSKA BANKA AD – SKOPJE

8

1. PRINCIPAL ACTIVITIES

Stopanska banka AD - Skopje (further referred as “the Bank”) was established as a shareholding bank on December 29, 1989. The Bank is registered as universal type of commercial bank in accordance with Macedonian laws. The principal activities of the Bank are as follows:

- Collecting deposits and other recurrent sources of funds; - Financing in the country and abroad, including factoring and financing commercial transactions; - Issuance and administration of payment instruments (cards, checks, bills of exchange); - Domestic and international payment operations, including purchase/sale of foreign currency

funds; - Fast money transfer - Trading in instruments at the money market (bills of exchange, deposit certificates); - Trading in foreign currency funds, securities and financial derivatives; - Financial leasing; - Foreign exchange operations; - Purchase/sale, guaranteeing and placement of securities issue; - Economic and financial consulting; - Providing services in collection of invoices, keeping records; - Issuing payment guarantees, backing guarantees and other forms of security; - Managing assets and securities portfolio at order and for account of clients; - Rendering services to custody bank; - Intermediating in concluding agreements for loans and borrowings and in selling insurance

policies; - Providing services of renting safe deposit boxes, depositories and depot; - Other financial services defined by law which can be performed only by a bank.�

On December 21, 1999, Share Purchase Agreement (“the Agreement”) was signed between the Bank, National Bank of Greece, International Finance Corporation (“IFC”), and the European Bank for Reconstruction and Development (“EBRD”) (“the Investors”) from one side and the Bank Rehabilitation Agency of the Republic of Macedonia and the Ministry of Finance of the Republic of Macedonia on the other side. Pursuant to the Agreement, the investors acquired ordinary shares in the Bank in a total amount equal to 85% of the Bank’s issued and outstanding shareholders’ capital in the following proportion: National Bank of Greece 65%, IFC 10% and EBRD 10%. The total number of Bank’s employees as of December 31, 2007 is 1,080.

2. BASIS OF PRESENTATION OF FINANCIAL STATEMENTS AND COMPARISON DATA

The Bank maintains its accounting records and prepares its financial statements in compliance with the Banking Law and by-laws prescribed by the National Bank of the Republic of Macedonia (“NBRM”), Company Law (Official Gazette of the Republic of Macedonia no. 28/2004 and no. 84/2005) and the Rules on Accounting Management (Official Gazette of the Republic of Macedonia nos. 94/2004, 11/2005 and 116/2005). According to these Rules, the accounting standards applied in the Republic of Macedonia are the International Accounting Standards (IAS) dated 2003 as prescribed by the International Accounting Standards Board (IASB). The supplement to these Rules dated February 10, 2005, refers to the application of the International Financial Reporting Standard (IFRS) 1, as well as the supplement dated December 29, 2005, for application of IFRS 2, 3, 4, 5, 6, and 7.

2. BASIS OF PRESENTATION OF FINANCIAL STATEMENTS AND COMPARISON DATA (Continued)

STOPANSKA BANKA AD – SKOPJE

9

In the beginning of October 2007, several enactments from the scope of work of the National Bank of the Republic of Macedonia (NBRM) were published as follows:

1. Decision on the chart of accounts of banks; 2. Decision on the Methodology of Recording and Evaluating accounting entries and on the

preparation of financial statements; and 3. Instructions on the types and contents of financial statements of the banks.

Pursuant to the provisions of these enactments, the Bank is obliged to:

1.1. Perform a reposting of the balance on 31st December 2008 from the accounts determined by the Regulation and Decision for analytical accounts in the chart of accounts of banks, savings banks and other financial organizations to the accounts prescribed with the decision on the chart of accounts of banks;

2.1. Submit to the NBRM a detailed Methodology Implementation Plan, not later than 10th January 2008;

2.2. Harmonize the internal enactments with the requirements in the Methodology and the Chart of accounts of banks not later than 31st August 2008 and to accordingly notify NBRM until 10th September 2008;

2.3. Harmonize the IT systems with the Methodology requirements not later than 31st October 2008 and to accordingly notify NBRM until 10th November 2008;

3.1. Prepare initial Balance sheet and fill in the relevant notes related to the items in the Balance sheet, as at 1st January 2008 and submit them to NBRM not later than 20th November 2008, along with the opinion on the initial financial statements prepared by the audit company.

For the purpose of more efficient performance of assignments and proper implementation of obligations, the Bank established a Committee for management with the project for implementing chart of accounts and methodology for recording and assessment of accounting items and for preparing financial statements, as well as a Committee to supervise this project. In accordance with item 2 and sub-items 2.1., 2.2. and 2.3., the Committee for project management prepared and submitted to NBRM a plan that contains the following:

� Organization of the process of harmonization with the requirements in the Methodology for Recording and Evaluating the accounting entries and on the preparation of financial statements;

� Allocation of human resources that will work on implementing the Methodology; � Time schedule for harmonization of the Bank’s internal enactments with the requirements of

the Methodology and the Chart of accounts of banks; � Time schedule for harmonization of the Bank IT systems with the Methodology requirements,

with a special attention to the application systems, including the defined period for their testing.

On December 31, 2006, the Bank has a 100% ownership in Stoba Trejd Skopje (“the Entity”). In the course of 2007 (November 21, 2007), in compliance with the modifications to the Banking Law, the Bank passed a Decision on closing of and initiation of liquidation of the Entity.

The financial statements of the Bank are prepared in accordance with the accounting policies disclosed in Note 3 to the financial statements. The presented financial statements are expressed in thousands of Macedonian Denars.

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

STOPANSKA BANKA AD – SKOPJE

10

3.1. Income and Expenses Recognition

Interest income and expense is recognized in the income statement for all interest-bearing instruments on a calculation basis, hence taking into account the unrepaid principal and using the method of effective interest rate based on amortized cost. Interest income involve as well coupons acquired on the basis of trading securities and securities held to maturity and calculated discount and premium on treasury bills and other discount bearing instruments. Fee and commission, except fee on approval of loans, is generally recognized on a calculation basis in the period of service rendering. Fees relating to loan origination are deferred and amortized to over the life of the loan using the effective interest rate method.

3.2. Foreign Exchange Translation

Transactions denominated in foreign currencies have been translated into Denars at rates set by the National Bank of the Republic of Macedonia (NBRM), which is the Central Bank of the Republic of Macedonia, at the dates of the transactions. Assets and liabilities denominated in foreign currencies are translated into Denars at the balance sheet date using official rates of exchange ruling on that date. Net foreign exchange gains or losses resulting from foreign currency translation are included in the income statement in the period in which they arose.

3.3. Loans originated by the Bank and allowances for Losses on Impairment and Uncollectability

Loans originated by the Bank are initially recognized at cost, when cash is advanced to customers. They are subsequently measured at amortized cost using the effective interest rate. Loans to customers and financial institutions are stated as net amount reduced by loss on impairment and uncollectability. Allowances for losses on impairment and uncollectability are determined if there are objective proofs that the Bank cannot collect all mature amounts upon receivables as per original agreed conditions. Allowance for losses on impairment and uncollectability is presented as reduction of carrying value of the claim in the balance sheet, while, regarding off-balance sheet items, such as financial liabilities, the allowance is presented within the other liabilities. Concurrently, allowances for losses on impairment and uncollectability are presented as well in the income statement as losses on impairment and uncollectability. The allowances for losses on impairment and uncollectability are determined on the basis of the degree (size) of the risk of uncollectability or specific country risk on the basis of the following principles: 3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) 3.3. Loans originated by the Bank and allowances for Losses on Impairment and

Uncollectability (continued)

STOPANSKA BANKA AD – SKOPJE

11

- Separate loan exposures (risks) are assessed on the basis of the type of loan applicant, his/her/its overall financial position, resources and payment records and recoverable value of collaterals. Allowances for losses on impairment and uncollectability are measured and determined for the difference between the carrying value of the loan and its estimated recoverable amount, which is, in fact, the present value of expected cash flows, including as well recoverable amounts from guarantees and collateral, discounted by effective loan interest rate.

- If there are objective proofs on uncollectability of loans in the loan portfolio that may not be identified

on a specific basis, the allowances for losses on impairment and uncollectability are determined at level of risk for overall loan portfolio. These losses are determined on the basis of historical data on loan classification of borrowers and express the current economic environment of the borrowers.

- Losses on impairment and uncollectability is termination of the calculation of interest income as per

agreed terms and conditions, while the loan is classified as non-performing since the contractual liabilities for payment of the principal and/or interest are on default, i.e. uncollected for a period longer than 90 days. All allowances for losses on impairment and uncollectability are reviewed and tested at least once a year, and any further changes in amounts and time of expected future cash inflows in comparison to previous assessments result in changes in allowances for losses on impairment and uncollectability recorded as debit/credit of losses on impairment and uncollectability recorded in the income statement.

- The loan which is believed that is impossible to be collected is written off against relevant allowance

for losses on impairment and uncollectability. Further collections are recorded as reduction of losses on impairment and uncollectability in the income statement.

- In case of granted loan to borrowers in countries with increased risk of difficulties for servicing

external debt, the political and economic circumstances are assessed and additional allowances for country risk are allocated.

In compliance with the Decision on modifying the Decision on classification of balance sheet and off-balance sheet asset positions of banks as per their risk degree risk published on June 29, 2006 (Official Gazette of the Republic of Macedonia no. 80/2006), starting as of March 31, 2007, the Bank allocates special reserve for potential losses at 1% of total loan exposure classified into risk category “A”.

STOPANSKA BANKA AD – SKOPJE

12

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) 3.4. Securities held for trading

Securities held for trading which comprise securities issued in local currency by the Ministry of Finance are securities included in the portfolio which is intended for realization of short-term profit. Securities held for trading are initially recognized at cost and are subsequently recognized as per their fair value on the basis of their market price. All of the respective realized and unrealized gains and losses are included under net trading income. Interest, if realized during management of securities held for trading, is recorded as interest income. The sale of securities held for trading is recognized on trading date, which is the date when the Bank obliges to buy/sell the asset.

3.5. Securities available for sale

Available for sale securities are those financial assets that are not classified as financial assets held for trading or held-to-maturity investments. This portfolio comprises quoted and unquoted equity investments in shares of banks and other financial institutions and enterprises, where the Bank does not exercise control. Available for sale financial assets are subsequently re-measured at fair value based on quoted prices or amounts derived from cash flow models.

Unrealized gains and losses arising from changes in fair value are recognized directly in equity, until the share is disposed of or is determined to be impaired, at which time the cumulative gain or loss previously recognized in equity is included in net profit or loss for the period.

3.6. Investments in associates

An associate is an enterprise over which the Bank is in a position to exercise significant influence, but not control, through participation in the financial and operating policy decisions of the investee.

Investments in associates comprise unquoted equity investments in shares that are stated at equity method. The Bank’s management believes that the carrying amount of this investment is a reasonable estimate of their market value.

3.7. Held-to-maturity securities

Held-to-maturity investments are financial assets with fixed or determinable payments and fixed maturity that the Bank has the positive intent and ability to hold to maturity. This portfolio comprises government bonds from old savings deposits, denationalization, government securities received in exchange for the Bank’s non-performing receivables as well as bonds issued by the Government of the Republic of Macedonia. These securities are measured at amortized cost using the effective interest rate method.

STOPANSKA BANKA AD – SKOPJE

13

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) 3.8. Property, equipment and intangible assets

Property and equipment and intangible assets are recognized at cost or revalued amount reduced by accumulated depreciation. Before January 1, 2006, property and equipment and intangible assets were revalued in past years at end of year by application of ratios of growth of prices of industrial products of cost or revalued amount, as well as value adjustment. The revaluation effect was recorded into revaluation reserve. As per Paragraph 44 (b) of the announced IAS 8 Net gain or loss for the period, basic omissions and changes in accounting policies (Official Gazette of the Republic of Macedonia no. 94/2004), revalued amounts of intangible and tangible assets are treated as revaluation in compliance with IAS 16 or IAS 38, but not as change in accounting policy. As at December 31, 2007, in compliance with letter from NBRM no. 91 dated January 8, 2008, this revalued reserve was transferred to retained earnings. Expenditure incurred to replace a component of an item of property and equipment that is accounted for separately is capitalized. Other subsequent expenditure is capitalized only when it increases the future economic benefits embodied in the item of property and equipment. All other expenditures are recognized in the income statements as an expense. Depreciation of property and equipment and intangible assets is computed on the straight-line basis so that to write off the cost or revalued amount of assets in the course of their estimated useful life. No depreciation is provided on construction in progress until the constructed assets are put into use. The annual depreciation rates are as follows:

Applied annual rates 2007-2006 Buildings 2.5% -5% Furniture and equipment 10% - 25% Intangible assets 20%

When assets subject to depreciation are put out of use, or, in any other way, are sold, the relevant revalued cost amount and adjustment of value are off-posted from relevant accounts. Capital gain or loss realized at sale is recorded as other income, i.e. other expense.

3.9. Investment property

Investment property includes buildings owned by the Bank with the intention of earning rentals or for the capital appreciation or both, and is initially recorded at cost, which includes transaction costs. The classification of the investment property is based on the criteria that the property is mostly held to earn rentals when compared to the property used by the Bank for own needs. Subsequent to the initial recognition, investment property is stated at cost less accumulated depreciation and any accumulated impairment losses. Such value represent the fair value of investment property at the date of balance sheet.

The depreciation of investment property is calculated on straight-line basis in a way to write off the cost value of assets over the estimated useful lives, which approximates the useful life of similar assets included in property, plant and equipment. The estimated annual depreciation rate is 2.5%. Rental income from investment property is recognized in the income statements on a straight-line bases over the term of the lease.

STOPANSKA BANKA AD – SKOPJE

14

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

3.10. Assets acquired through foreclosure procedures

In compliance with the Decision on the accounting and regulatory treatment of foreclosed assets (land, buildings, equipment and the like) published in the Official Gazette of the Republic of Macedonia no. 79/2007 dated June 26, 2007, the Bank is obligated to allocate special reserve for foreclosed assets, including as well the current foreclosed assets. On the foreclosure date, the foreclosed asset is recognized in the Bank’s financial statements at initial carrying value. The initial carrying value is the lower amount than the appraised value reduced by the expected sales costs to the debit of the Bank and the cost value of the foreclosed asset. The appraised value is determined by an authorized appraiser on the date of asset foreclosure, while the cost value is the value stated in an enactment passed by a competent body from where the legal grounds for acquiring ownership arises. If the appraised value is lower than the cost value, the Bank shall be obligated to present impairment loss (IAS 36) in the income statement in an amount of determined difference between both values. At least once a year in a period of 12 months, the Bank is obligated to provide appraisal of the value of foreclosed asset by three authorized appraisers, at least two of which are external appraisers not working for the Bank. Hence, the amount of the lowest appraisal out of the three ones is considered to be appraised value. Upon exception, the Bank may provide appraisal of the value of foreclosed assets by only one authorized appraiser if the initial carrying value of the foreclosed asset reduced by the total amount of impairment loss does not exceed MKD 2,000,000. If, as per the conducted appraisal, the appraised value reduced by the sales costs is lower than the amount of initial carrying value reduced by the total amount of impairment loss, the Bank is obligated to recognize in the income statement the additional impairment loss up to the amount of appraised value. When the appraised value is higher than the amount of initial carrying value reduced by the total amount of impairment loss, the Bank must not recognize this difference in the income statement. If the Bank fails to sell the foreclosed asset within 5 years following the foreclosure date, it is obligated to conduct full write-off of such asset, i.e. to bring its value down to zero. The Bank, within 3 months following the date of this decision’s enactment (26.07.2007), is obligated to provide appraisal of the value of current foreclosed assets. Hence, the date of this Decision’s enactment is considered the date of foreclosure of the current assets. If the appraised value is lower than the value upon which the foreclosed asset has been recorded until the date of this Decision’s enactment, the Bank is obliged to recognize in the income statement the impairment loss up to the amount of appraised value.

3.10. Cash and Cash Equivalents

Cash and cash equivalents include cash and nostro accounts, which represent unrestricted demand deposits and placements with other banks and financial institutions, with maturity up to three months, as well as unrestricted account balances with the NBRM.

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

STOPANSKA BANKA AD – SKOPJE

15

3.11 Managed Funds

Assets managed on a fee basis on behalf of legal entities and citizens are included in the balance sheets on a net basis. Net asset or liability position as reported in the balance sheet reflects timing difference in collection of receivables or settlement of liabilities on behalf of the clients.

3.12. Employment Benefits

In accordance with local regulations, the Bank is obligated to pay pension and social security contributions for its employees to the Pension & Social Security Fund calculated by applying the specific percentages stipulated under the relevant regulations. These contributions are recognized as expenses in the income statement at the moment of their generation. In accordance with the local regulations the employee is entitled to receive benefits upon retirement of at least two average monthly salaries paid to the employee in the Republic of Macedonia within the period of three preceding months. In addition, according to the collective agreement with the Bank’s employees, the employees are entitled to receive benefits of two average salaries paid to the employee in the Republic of Macedonia within the period of three preceding months. These benefits are considered defined pension benefit plans. The retirement benefit obligations is recognized in the balance sheet on the basis of actuary assessment and represents the present value of the defined benefit obligation to employees as adjusted for all unrecognized actuarial gains and losses less unrecognized past service cost.

3.13 Income Tax

Income tax is calculated in accordance with the provisions of the relevant legislation of the Republic of Macedonia based on the profit or loss recognized in the income statement prepared pursuant to Macedonian fiscal regulations. The estimated tax on monthly profit is paid in advance as determined by the tax authorities. Final taxes on profit of 12% are payable based on the annual profit shown in the statutory profit and loss account. Deferred income taxes if any are provided using the balance sheet liability method for temporary differences arising between the tax bases of assets and liabilities and their carrying values for financial reporting purposes. Currently enacted tax rates are used to determine deferred income tax. A deferred tax liability is recognized for all taxable temporary differences unless it arises from the initial recognition of an asset or liability in a transaction, which at the time of the transaction affects neither accounting profit nor taxable profit (tax loss). Deferred tax assets are recognized for all deductible temporary differences to the extent that it is probable that taxable profit will be available against which the deductible temporary difference can be utilized, unless the deferred asset arises from the initial recognition of an asset or liability in a transaction, which at the time of the transaction, affects neither accounting profit nor taxable profit (tax loss).

3.14. Fair Value

The accompanying financial statements are prepared on a cost basis and subsequently reduced in order to obtain their estimated recoverable amounts.

4. FINANCIAL INSTRUMENTS 4.1. Financial risk management

STOPANSKA BANKA AD – SKOPJE

16

The Bank’s activities expose it to a variety of financial risks and those activities involve the analysis, evaluation, acceptance and management of some degree of risk or combination of risks. Taking risk is core to the financial business, and the operational risks are an inevitable consequence of being in business. The Bank’s aim is therefore to achieve an appropriate balance between risk and return and minimize potential adverse effects on the Bank’s financial performance.

The Bank’s risk management policies are designed to identify and analyze these risks, to set appropriate risk limits and controls, and to monitor the risks and adherence to limits by means of reliable and up-to-date information systems. The Bank regularly reviews its risk management policies and systems to reflect changes in markets, products and emerging best practice.

The Bank’s risk management organization structure ensures existence of clear lines of responsibility, efficient segregation of duties and prevention of conflicts of interest at all levels, including the Board of Directors, Executive and Senior Management, as well as between SB and the NBG Group, its customers and any other stakeholders. Within the Bank, risk management activities broadly take place at the following levels:

• Strategic level encompasses risk management functions performed by the Supervisory Board. These include the approval of risk and capital strategy, ascertaining the Bank’s risk definitions, profile and appetite, as well as, the risk reward profile and other high-level risk related policies and internal guidelines.

• Tactical level encompasses risk management functions performed by the Board of Directors, Executive and Senior Management. These include the approval of risk policies and procedure manuals for managing specific risks and establishing adequate systems and controls to ensure that the overall risk and reward relation remains within acceptable levels. Generally, the risk management activities performed by the Risk Management department of SB, as well as, other critical support functions fall into this category.

• Operational (business line) level – It involves management of risks at the point where they are actually created. The relevant activities are performed by individuals who undertake risk on the organization’s behalf. Risk management at this level is implemented by means of appropriate controls incorporated into the relevant operational procedures and guidelines set by the management.

The most important types of risk are credit risk, liquidity risk, market risk and operational risk.

4.2. Credit risk

The Bank takes on exposure to credit risk, which is the risk to earnings arising from an obligor’s failure to meet the terms of any contract with the bank or otherwise fail to perform as agreed. Credit risk is the most important risk for the Bank’s business; management therefore carefully manages its exposure to credit risk. Credit exposures arise principally in lending activities that lead to loans and advances. There is also credit risk in off-balance sheet financial instruments, such as loan commitments, letters of guarantees and credits.

4. FINANCIAL INSTRUMENTS (continued) 4.2. Credit risk (continued)

STOPANSKA BANKA AD – SKOPJE

17

4.2.1. Credit risk measurement, limits and mitigation policies

Initially, when approving loans and loan commitments, different Credit Committees assess creditworthiness of the clients depending on the type and size of the exposure. The credit risk management, which encompasses measurement, monitoring and control of credit risk, is performed by Risk Management Committee and Committee for classification of assets and provisioning for potential losses, commitments and contingencies and it is mainly based on reports and analyses prepared by Research, Statistics and Risk Management Division. The Board of Directors is regularly informed concerning the credit risk that Bank is exposed to. The Bank monitors compliance with the legally and internally established limits and controls concentrations of credit risk. Credit risk limits regarding an individual borrower, internal persons, shareholders with over 5% of the voting shares, firms in which SB owns capital share as well as large exposures are set in the SB Risk Strategy which is approved and revised by the Board of Directors, and are in line with the regulatory requirements. The Bank structures the levels of credit risk that undertakes towards domestic and foreign banks by placing limits on the amount of risk accepted subject to an annual or more frequent review, when considered necessary. The concentration risk is monitored regularly for product, geographical and industry segments.

The Bank employs a range of practices to mitigate credit risk. Common practice is accepting suitable collateral for approved loans. The main collateral types for loans and other credit exposures are:

• Mortgages over residential properties; • Charges over business assets such as premises, inventory and accounts receivable; • Charges over financial instruments such as debt securities and equities.

4.2.2. Impairment and provisioning policies

The internal rating systems focus more on credit-quality mapping from the inception of the lending and investment activities. In contrast, impairment provisions are recognised for financial reporting purposes only for losses that have been incurred at the balance sheet date based on objective evidence of impairment.

The impairment provision shown in the balance sheet at year-end is derived from each of the five internal rating grades. However, the majority of the impairment provision comes from the bottom two gradings. The table below shows the Bank’s credit rating categories:

STOPANSKA BANKA AD – SKOPJE

18

4. FINANCIAL INSTRUMENTS (continued) 4.2. Credit risk (continued) 4.2.2. Impairment and provisioning policies (continued)

Credit rating Criteria Mapping Risk category A Debtor not likely to default and who repays on time, or with delay of

15 days. Credit exposure secured by first-class collateral. Satisfactory risk

Risk category B Debtor who repays its obligation with a delay of 30 days, occasionally 31-90 days. Regardless the temporary weak financial position, no signs of further deterioration.

Watch list

Risk category C Debtor who repays its obligation with a delay of 31-90 days, occasionally 91-180 days. Debtor is assessed to have inadequate cash flows to fulfilled its obligations.

Watch list

Risk category D Debtor who repays its obligation with a delay of 91-180 days, occasionally 181-365 days. Debtor is illiquid and insolvent, and have acceptable collateral.

Substandard

Risk category E Debtor who repays its obligation with a delay of more than 365 days or do not repay its obligation at all. Usually credit exposure to debtor under bankruptcy or liquidation procedure. Without or with bad collateral.

Substandard

The internal rating tool assists management to determine whether objective evidence of impairment exists under IAS 39, based on the following criteria set out by the Bank:

Delinquency in contractual payments of principal or interest:

• Cash flow difficulties experienced by the borrower (e.g. equity ratio, net income percentage of

sales);

• Breach of loan covenants or conditions;

• Initiation of bankruptcy proceedings;

• Deterioration of the borrower’s competitive position; and Deterioration in the value of collateral

The Bank’s policy requires the review of individual financial assets that are above materiality thresholds at least annually or more regularly when individual circumstances require. Impairment allowances on individually assessed accounts are determined by an evaluation of the incurred loss at balance-sheet date on a case-by-case basis, and are applied to all individually significant accounts.

The assessment normally encompasses collateral held (including re-confirmation of its enforceability) and the anticipated receipts for that individual account.

Collectively assessed impairment allowances are provided for portfolios of homogenous assets that are individually below materiality thresholds.

4. FINANCIAL INSTRUMENTS (continued)

STOPANSKA BANKA AD – SKOPJE

19

4.2. Credit risk (continued) 4.2.3. Maximum exposure to credit risk before collateral held or other credit enhancements

Maximum exposure in thousands

denars

31 December

2007 31 December

2006 Credit risk exposure relating to on balance sheet Treasury bills 5,232,175 2,426,260 Loans and advances to banks 5,443,514 6,001,414 Trading securities 253,301 147,765 Loans and advances to customers 32,917,403 21,659,311 Investment securities- available for sale 123,123 107,354 Investment securities- held to maturity 3,838,602 4,391,916 Other assets 329,562 230,681 Credit risk exposure relating to off -balance sheet Financial guarantees 2,019,165 1,619,601 Standby letters of credits 1,001,711 696,623 Commitments to extend credits 7,332,304 4,303,044 Total credit risk exposure 58,490,860 41,583,969

Deposit, property, cars, government bonds, pledge over machines and other movables are accepted as collateral in order to secure the credit exposures.

Mortgages and consumer loans in the amounts over EUR 5.000 are fully secured by property (residential and business premises) with LTV up to 75%. Also, deposits and government bonds are accepted as valid collateral.

Auto loans (included in category-consumer loans) are secured by cars.

The corporate loans and small business lines are secured with different types of collaterals: residential mortgage, commercial premises, cars, pledge over machines and other movables, L/Gs from first-class banks, corporate L/Gs and personal bills of exchange taking into consideration the quality of the collateral and the LTV ratio.

4. FINANCIAL INSTRUMENTS (continued) 4.2. Credit risk (continued)

STOPANSKA BANKA AD – SKOPJE

20

4.2.4. Loans and advances

Loans and advances are summarised below:

Neither past due

nor impaired

Past due but not

individually impaired

Individually impaired

Total Gross

Allowance for

individually impaired

loans

Allowance for

collectively impaired

loans

TOTAL Allowance for impairment

Total net

31 December

2007

Cards 1,519,095 406,184 - 1,925,279 - (61,504) (61,504) 1,863,775 Consumer 10,455,370 2,515,643 - 12,971,013 - (490,334) (490,334) 12,480,679 Mortgage 2,500,311 821,733 - 3,322,044 - (62,018) (62,018) 3,260,026 Small Business Loans 3,909,233 2,215,964 1,941,339 8,066,536 (1,517,340) - (1,517,340) 6,549,196 Corporate Loans 5,555,020 3,024,479 4,138,081 12,717,580

(3,953,853) - (3,953,853) 8,763,727

Total 23,939,029 8,984,003 6,079,420 39,002,452 (5,471,193) (613,856) (6,085,049) 32,917,403 Due from banks 5,392,146 77,435 - 5,469,581 - (26,067) (26,067) 5,443,514 29,331,175 9,061,438 6,079,420 44,472,033 (5,471,193) (639,923) (6,111,116) 38,360,917

4. FINANCIAL INSTRUMENTS (continued) 4.2. Credit risk (continued) 4.2.4. Loans and advances (continued)

Neither past due

nor impaired

Past due but not

individualy impaired

Individually impaired

Total Gross

Allowance for

individually impaired

loans

Allowance for

collectively impaired

loans

TOTAL Allowance for impairment

Total net

31 December 2006 Cards 1,001,630 277,272 - 1,278,902 - (31,772) (31,772) 1,247,130 Consumer 5,168,387 2816,803 - 7,985,190 - (381,404) (381,404) 7,603,786 Mortgage 1,576,416 880,773 - 2,457,189 - (15,819) (15,819) 2,441,370 Small Business Loans 2,061,894 2,839,958 2,030,337 6,932189 (1,583,395) - (1,583,395) 5,348,794 Corporate Loans 3,867,931 638,364 4,826,604 9,332,899 (4,314,668) - (4,314,668) 5,018,231

Total 13,676,258 7,453,170 6,856,941 27,986,369

(5,898,063) (428,995) (6,327,058) 21,659,311 Due from banks 5,949,205 89,010 - 6,038,215 - (36,801) (36,801) 6,001,414

19,625,463 7,542,180 6,856,941 34,024,584 (5,898,063) (465,796) (6,363,859) 27,660,725

STOPANSKA BANKA AD – SKOPJE

21

(a) Loans and advances neither past due or impaired

Satisfactory

risk Watch list Substandard Total

31 December 2006 Cards 1,001630 - - 1,001,630 Consumer 5,168,387 - - 5,168,387 Mortgage 1,576,416 - - 1,576,416 Small Business Loans 2,061,894 - - 2,061,894 Corporate Loans 3,867,931 - - 3,867,931 Total 13,676,258 - - 13,676,258 Due from banks 5,949,205 - - 5,949,205 19,625,463 - - 19,625,463

(b) Loans and advances past due but not individually impaired

Loans and advances which are past due 90 days doesn’t have a impaired treatment, except when exist nformation which is opposite. Gross amount of the loans are summarised bellow. 4. FINANCIAL INSTRUMENTS (continued) 4.2. Credit risk (continued) 4.2.4. Loans and advances (continued)

(b) Loans and advances past due but not individually impaired (continued)

Satisfactory risk

Watch list Substandard Total

31 December 2007 Cards 1,519,095 - - 1,519,095 Consumer 10,455,370 - - 10,455,370 Mortgage 2,500,311 - - 2,500,311 Small Business Loans 3,909,233 - - 3,909,233 Corporate Loans 5,555,020 - - 5,555,020 Total 23,939,029 - - 23,939,029 Due from banks 5,392,146 - - 5,392,146 29,331,175 - - 29,331,175

STOPANSKA BANKA AD – SKOPJE

22

Past due

up to 30 days

Past due 31-60 days

Past due 61-90 days

Past due 91-180 days

Past due 180-365

days

Past due 1-2 years

Past due over 2 years

Total

31 December 2007 Cards 295,992 46,674 10,743 52,775 - - - 406,184 Consumer 1,413,448 370,391 189,390 283,450 159,307 99,657 - 2,515,643 Mortgage 545,417 147,659 35,316 70,824 1,957 - 20,560 821,733 Small Business Loans 1,510,646 473,205 232,113 - - - - 2,215,964 Corporate Loans 2,332,594 265,340 426,545 - - - - 3,024,479 Total 6,098,097 1,303,269 894,107 407,049 161,264 99,657 20,560 8,984,003 Due from banks - - - - - - 77,435 77,435 6,098,097 1,303,269 894,107 407,049 161,264 99,657 97,995 9,061,438 Past due

up to 30 days

Past due 31-60 days

Past due 61-90 days

Past due 91-180 days

Past due 180-365

days

Past due 1-2 years

Past due over 2 years

Total

31 December

2006 Cards 179,330 35,105 8,572 54,265 - - - 277,272 Consumer 1,915,977 274,197 160,473 200,136 116,561 149,459 - 2,816,803 Mortgage 654,706 100,029 81,581 26,002 18,455 - - 880,773 Small Business Loans 2,369,436 330,612 139,490 420 - - - 2,839,958 Corporate Loans - - 638,364 - - - - 638,364 Total 5,119,449 739,943 1,028,480 280,823 135,016 149,459 - 7,453,170 Due from banks - - - - - - 89,010 89,010 5,119,449 739,943 1,028,480 280,823 135,016 149,459 89,010 7,542,180 4. FINANCIAL INSTRUMENTS (continued) 4.2. Credit risk (continued) 4.2.4. Loans and advances (continued)

(b) Loans and advances past due but not individually impaired (continued)

STOPANSKA BANKA AD – SKOPJE

23

The fair value of collateral is based on valuation techniques which are used for similar assets. Total fair value of collateral for consumer loans is: 7.103.970 thousands denars (2006-4.769.612 thousands denars), while for mortgage s8.529.484 thousands denars (2006-6.558.566 thousands denars)

The fair value of collateral for corporate portfolio is summarised bellow:

2007 2006 Cash and balances with central banks

297,633

217,619

Financial guarantees 2,719,217 2,850,350 Movable property 8,573,319 6,261,905 Real estate 28,621,092 22,000,474 Total 40,211,261 31,330,348

4.2.5. Foreclosed assets during the year During 2007, the Bank engaged two external appraisal companies in order to determine the fair value of the foreclosed assets. In this period, the Bank sold 30 assets at total value of MKD 121,124 thousand, whereas it foreclosed 10 facilities at total value of MKD 18,987 thousand. Activities have been undertaken for preparing the assets foreclosed during 2007 for sale because the general policy of the Bank is these facilities to be sold within a period of 3 years. The Bank utilizes such facilities for its own activities very rarely.

STOPANSKA BANKA AD – SKOPJE

24

4. FINANCIAL INSTRUMENTS (continued) 4.2. Credit risk (continued) 4.2.6. Concentration of risks of financial assets with credit risk exposure

(a) Geographical sectors The following table breaks down the Bank’s main credit exposure at their carrying amounts, as categorized by geographical region as of 31 December 2007. For this table, the Bank has allocated exposures to regions based on the country of domicile of the counterparties.

Greece

Macedonia

West

European countries

United States

and Canada

SE Europe

Australia

and Japan

Total

Treasury bills - 5,232,175 - - - - 5,232,175 Loans and advances to banks 5,075 45 4,028,047 510,741 236,034 663,572 5,443,514 Trading securities - 226,690 - - 26,611 - 253,301 Loans and advances to customers - 32,917,403 - - - - 32,917,403 Investment securities- available for sale - 92,066 31,057 - - - 123,123 Investment securities- held to maturity - 3,838,602 - - - - 3,838,602 Other assets - 329,562 - - - - 329,562 31 December 2007 5,075 42,636,543 4,059,104 510,741 262,645 663,572 48,137,680 31 December 2006 3,687 30,968,667 2,948,538 371,002 190,787 482,020 34,964,701

STOPANSKA BANKA AD – SKOPJE

25

4. FINANCIAL INSTRUMENTS (continued) 4.2. Credit risk (continued) 4.2.6. Concentration of risks of financial assets with credit risk exposure (continued)

(b) Industry sector The following table breaks down the Group’s main credit exposure at their carrying amounts, as categorised by the industry sectors of the counterparties.

Financial Institutions

Tobacco, food and beverage industry

Trade

Steel

Industry

Building Industry

Clothing Industry

Agriculture, Fishery

and Mining engeneerig industry

Transport

Services

Electricity

Public sector

Retail

Other

Total

Treasury bills 5,232,175 - - - - - - - - - - - - 5,232,175 Loans and advances to banks 5,443,514 - - - - - - - - - - - - 5,443,514 Trading securities 26,611 - - - - - - - - - 226,690 - - 253,301 Loans and advances to customers 451 1,754,913 3,861,295 1,975,969 1,038,436 691,738 675,861 641,516 - 1,199,157 504,226 17,466,151 3,107,690 32,917,403 Investment securities-

available for sale 72,016 - 2,919 6,728 - 14,742 - 227 - - - - 26,491 123,123 Investment securities-

held to maturity - - - - - - - - - - 3,838,602 - - 3,838,602 Other assets - - 148,515 - 22,389 - 20,125 - 43,177 - 62 82,759 12,535 329,562 31 December 2007 10,774,767 1,754,913 4,012,729 1,982,697 1,060,825 706,480 695,986 641,743 43,177 1,199,157 4,569,580 17,548,910 3,146,716 48,137,680

31 December 2006 7,826,804 1,274,771 2,914,851 1,440,234 770,585 513,188 505,565 466,163 31,364 871,069 3,319,349 12,727,282 2,303,477 34,964,702

STOPANSKA BANKA AD – SKOPJE

26

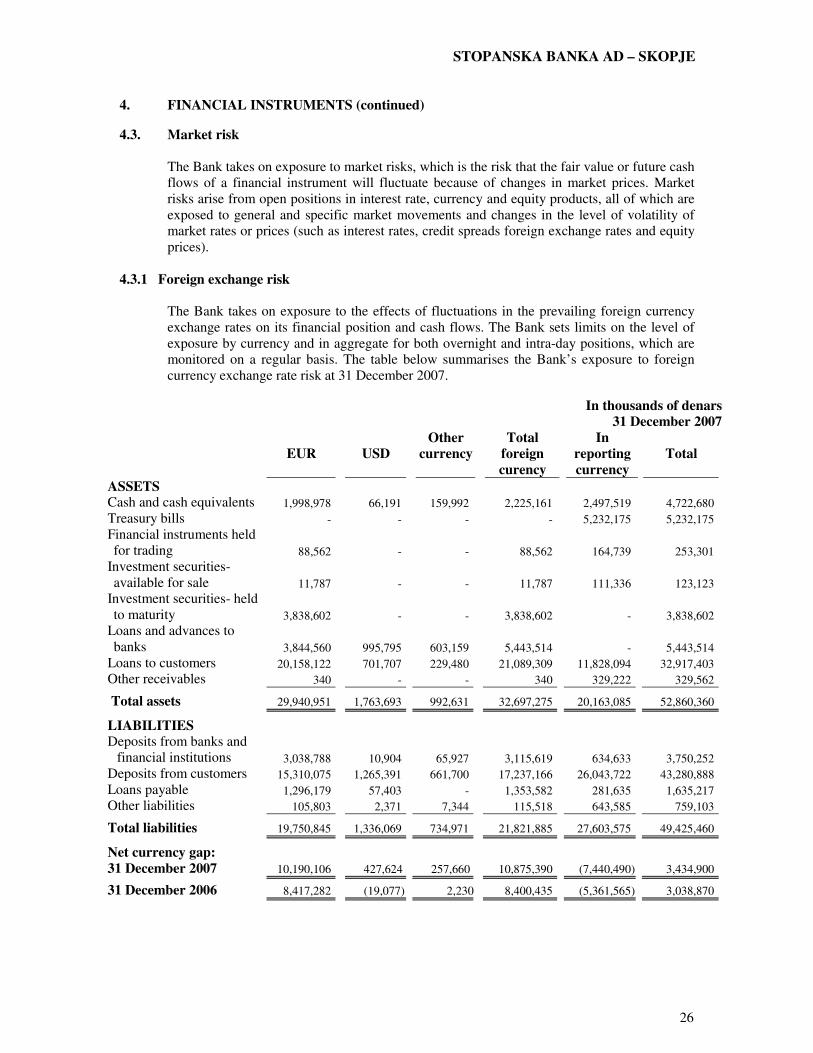

4. FINANCIAL INSTRUMENTS (continued) 4.3. Market risk

The Bank takes on exposure to market risks, which is the risk that the fair value or future cash flows of a financial instrument will fluctuate because of changes in market prices. Market risks arise from open positions in interest rate, currency and equity products, all of which are exposed to general and specific market movements and changes in the level of volatility of market rates or prices (such as interest rates, credit spreads foreign exchange rates and equity prices).

4.3.1 Foreign exchange risk

The Bank takes on exposure to the effects of fluctuations in the prevailing foreign currency exchange rates on its financial position and cash flows. The Bank sets limits on the level of exposure by currency and in aggregate for both overnight and intra-day positions, which are monitored on a regular basis. The table below summarises the Bank’s exposure to foreign currency exchange rate risk at 31 December 2007.

In thousands of denars

31 December 2007

EUR

USD Other

currency Total

foreign curency

In reporting currency

Total

ASSETS Cash and cash equivalents 1,998,978 66,191 159,992 2,225,161 2,497,519 4,722,680 Treasury bills - - - - 5,232,175 5,232,175 Financial instruments held for trading 88,562 - - 88,562 164,739 253,301

Investment securities- available for sale 11,787 - - 11,787 111,336 123,123

Investment securities- held to maturity 3,838,602 - - 3,838,602 - 3,838,602

Loans and advances to banks 3,844,560 995,795 603,159 5,443,514 - 5,443,514

Loans to customers 20,158,122 701,707 229,480 21,089,309 11,828,094 32,917,403 Other receivables 340 - - 340 329,222 329,562 Total assets 29,940,951 1,763,693 992,631 32,697,275 20,163,085 52,860,360 LIABILITIES Deposits from banks and

financial institutions 3,038,788 10,904 65,927 3,115,619 634,633 3,750,252 Deposits from customers 15,310,075 1,265,391 661,700 17,237,166 26,043,722 43,280,888 Loans payable 1,296,179 57,403 - 1,353,582 281,635 1,635,217 Other liabilities 105,803 2,371 7,344 115,518 643,585 759,103 Total liabilities 19,750,845 1,336,069 734,971 21,821,885 27,603,575 49,425,460 Net currency gap: 31 December 2007 10,190,106 427,624 257,660 10,875,390 (7,440,490) 3,434,900 31 December 2006 8,417,282 (19,077) 2,230 8,400,435 (5,361,565) 3,038,870

STOPANSKA BANKA AD – SKOPJE

27

4. FINANCIAL INSTRUMENTS (continued) 4.3. Market risk (continued) 4.3.1. Foreign exchange risk (continued)

At 31 December 2007 and 2006, loans approved to customers, accrued interest and other assets due to banks and customers and other liabilities denominated according exchange rate denars/eur are presented as assets and liabilities in EUR.

4.3.2. Interest rate risk

The Bank is exposed to various risks associated with the effects of fluctuations in the prevailing levels of market interest rates on its financial position and cash flow.

Interest margins may increase as a result of such changes but may reduce or create losses in the event that unexpected movements arise. The Board of Directors sets limits on the level of mismatch of interest rate re-rating that may be undertaken and monitors this on a regular basis. In general, the Bank is assets sensitive because of the majority of the interest-bearing assets and liabilities and the Bank has right simultaneously to change the interest rates. The Bank strives to maintain the interest margin at the same level. However, the actual effect will depend on various factors, including stability of the economy, environment and level of the inflation.

The table below summarises the Bank’s interest bearing and non-interest bearing assets and liabilities as of 31 December 2007.

In thousands of denars 31 December 2007

Interest bearing Non Interest

bearing Total ASSETS Cash and cash equivalents 2,372,070 2,350,610 4,722,680 Treasury bills 5,232,175 5,232,175 Financial instruments held for trading 226,421 26,880 253,301 Investment securities- available for sale - 123,123 123,123 Investment securities- held to maturity 3,838,602 - 3,838,602 Loans and advances to banks 5,443,514 - 5,443,514 Loans to customers 32,917,403 - 32,917,403 Total assets 50,030,185 2,500,613 52,530,798 LIABILITIES Deposits from banks and financial

institutions 3,750,252 - 3,750,252 Deposits from customers 43,280,888 - 43,280,888 Loans payable 1,474,115 161,102 1,635,217 Total liabilities 48,505,255 161,102 48,666,357 Net interest gap: 31 December 2007 1,524,930 2,339,511 3,864,441 31 December 2006 148,418 2,234,010 2,382,428

STOPANSKA BANKA AD – SKOPJE

28

4. FINANCIAL INSTRUMENTS (continued) 4.3. Market risk (continued) 4.3.2. Interest rate risk (continue)

The table bellow summarizes interest rates on the major financial instruments.

In foreign currency In Denars Assets Obligatory reserve held with Central Bank - 2% Treasury bills - 5.47%-5.82% Held-for trading securities - 2%-9% Placements with, and loans to, banks 3.54%-6.18% 4.15% Short-term loans:

- enterprises

8.75%-11.5% 9.75% - 1 � EURIBOR

+5.5%-6.25% - retail customers 11,5%-14.5% 13.5%-16.5% Long-term loans: - enterprises 9.5%-17.9% 9.75%-14.5% - retail customers 5.5%-14.5% 12%-16.5% Government bonds - 2%-8.89% Liabilities Demand deposits from banks 0.001%-1% 0.4% Short-term deposits from banks 1.6%-3.61% 4%-6.35% Demand deposits: - enterprises 0.001%-1% 0.4% - retail customers 0.001%-1.7% 0.65%-1% Short-term deposits: - enterprises 0.001%-5.71% 4%-7.23% - retail customers 0.75%-4.3% 5.5%-7.76% Long-term deposits: - enterprises 6.5%-8.85% 0.001%-5.57% - retail customers 1.75%-4.5% 8%-8.58% Loans payable 3.9%-6.73% 3.9% Subordinated debt 3� EURIBOR +0.85% -

4.4. Liquidity risk

Liquidity risk is defined as the current or prospective risk to earnings and capital arising from the institution’s inability to meet its liabilities when they come due without incurring unacceptable losses. The consequence may be the failure to meet obligations to repay depositors and fulfil commitments to lend.

4.4.1. Liquidity risk management process

The Bank’s liquidity risk management process encompasses:

� Appliance of operating standards relating to the Bank’s liquidity risk, including appropriate policies, procedures and resources for controlling and limiting liquidity risk.

� Maintenance of stock of liquid assets appropriate for the cash flow profile of the Bank which can be readily converted into cash without incurring undue capital losses.

� Measurement, control and scenario testing of funding requirements, as well as access to funding sources.

STOPANSKA BANKA AD – SKOPJE

29

4. FINANCIAL INSTRUMENTS (continued) 4.4. Liquidity risk (continued) 4.4.1. Liquidity risk management process (continued)

� Preparing contingency plans of the Bank for handling liquidity disruptions by means of the ability to fund some or all activities in a timely manner and at a reasonable cost.

� Monitoring liquidity risk limits and ratios (e.g. maturity mismatch ratio, liquid asset ratio) taking into account the Bank’s risk appetite and profile.

The basic tool for measuring, monitoring and evaluating liquidity needs and liquidity sources is the cash flow gap report. Cash flow or liquidity gap reports reflect the liquidity provided by cash inflows and the liquidity needed to fund cash outflows. They incorporate cash flows associated with assets and liabilities into time buckets.

The monitoring of the SB’s liquidity is performed by the Liquidity Department. The Liquidity Department reconciles all inflows and/or outflows in all currencies along with money orders, checks, bank transfers and account transfers.

In thousands of denars

31 December 2007

Up to 1 month

From 1 to 3 months

From 3 months to 1

year From 1 to 5

years

Over 5 years

Total

ASSETS Cash and cash equivalents 4,722,680 - - - - 4,722,680 Treasury bills 4,894,572 337,603 5,232,175 Financial instruments held for trading 253,301 - - - - 253,301 Investment securities- available for sale 123,123 - - - - 123,123 Investment securities- held to maturity - 212,064 745,617 2,873,138 7,783 3,838,602 Placement with, and loans to, banks 5,443,514 - - - - 5,443,514 Loans to customers 9,482,223 1,706,348 5,970,088 11,030,008 4,728,736 32,917,403

�������������� � 308,234 - 11,195 10,133 691,807 1,021,369 Investment property - - - - 110,334 110,334 Leasehold improvements - - - - 20,268 20,268 Intangible assets - - - - 89,589 89,589 Property and equipment - - - - 1,134,954 1,134,954 Deferred tax assets - - - - 1,789 1,789 Total assets 25,227,647 2,256,015 6,726,900 13,913,279 6,785,260 54,909,101 LIABILITIES AND EQUITY Deposits from banks and financial

institutions 3,296,311 350,310 82,604 21,027 - 3,750,252 Deposits from customers 21,906,393 11,084,920 9,255,696 933,703 100,176 43,280,888 Loans payable 34,955 2,892 18,345 85,727 1,493,298 1,635,217 Other payable 758,459 644 - - - 759,103 Equity - - - - 5,483,641 5,483,641 Total liabilities and equity 25,996,118 11,438,766 9,356,645 1,040,457 7,077,115 54,909,101 Net liquidity gap December 31, 2007 (768,471) (9,182,751) (2,629,745) 12,872,822 (291,855) - December 31, 2006 (8,510,259) (3,715,788) 2,901,196 9,671,684 (346,833) -

STOPANSKA BANKA AD – SKOPJE

30

4. FINANCIAL INSTRUMENTS (continued) 4.4. Liquidity risk (continued) 4.4.1. Liquidity risk management process (continued)

The structure of the Bank’s assets and liabilities as classified into their relevant maturities as of December 31, 2007. Indicates the existence of a significant discrepancy in the period from 1 years. The primary reason for the aforementioned unreconciled amounts lies in the fact that the short-term sources of funds with maturities from 3 months have been committed for longer periods of time.

According to the management estimation, based on the different analysis based on evaluation of the deposit level on corporate and retail, there is a deposit core in the amount of Denar 28,020,000 thousand (2006 – Denar 21,181,000 thousand) which helps the liquidity gap to be overcome. Items with indefinite maturities are included in the over five year’s category.

STOPANSKA BANKA AD – SKOPJE

31

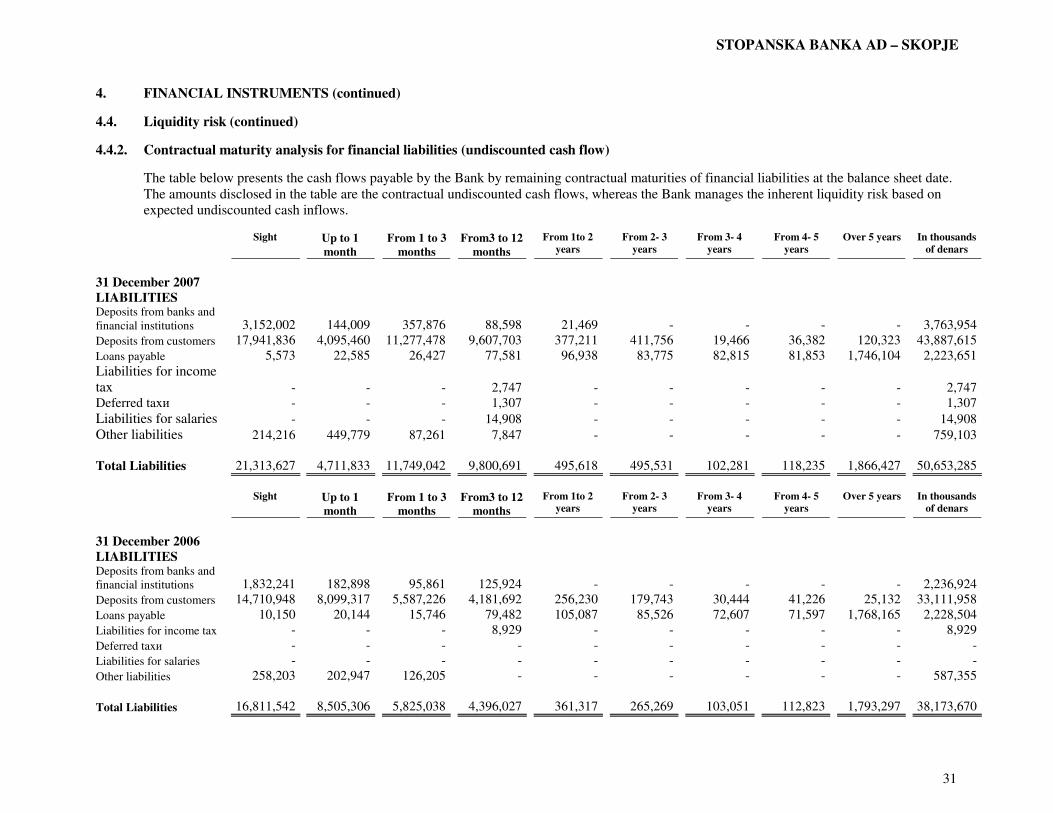

4. FINANCIAL INSTRUMENTS (continued) 4.4. Liquidity risk (continued) 4.4.2. Contractual maturity analysis for financial liabilities (undiscounted cash flow)

The table below presents the cash flows payable by the Bank by remaining contractual maturities of financial liabilities at the balance sheet date. The amounts disclosed in the table are the contractual undiscounted cash flows, whereas the Bank manages the inherent liquidity risk based on expected undiscounted cash inflows.

Sight Up to 1

month From 1 to 3

months From3 to 12

months From 1to 2

years From 2- 3

years From 3- 4

years From 4- 5

years Over 5 years In thousands

of denars

31 December 2006 LIABILITIES Deposits from banks and financial institutions 1,832,241 182,898 95,861 125,924 - - - - - 2,236,924 Deposits from customers 14,710,948 8,099,317 5,587,226 4,181,692 256,230 179,743 30,444 41,226 25,132 33,111,958 Loans payable 10,150 20,144 15,746 79,482 105,087 85,526 72,607 71,597 1,768,165 2,228,504 Liabilities for income tax - - - 8,929 - - - - - 8,929 Deferred tax� - - - - - - - - - - Liabilities for salaries - - - - - - - - - - Other liabilities 258,203 202,947 126,205 - - - - - - 587,355 Total Liabilities 16,811,542 8,505,306 5,825,038 4,396,027 361,317 265,269 103,051 112,823 1,793,297 38,173,670

Sight Up to 1 month

From 1 to 3 months

From3 to 12 months

From 1to 2 years

From 2- 3 years

From 3- 4 years

From 4- 5 years

Over 5 years In thousands of denars

31 December 2007 LIABILITIES Deposits from banks and financial institutions 3,152,002 144,009 357,876 88,598 21,469 - - - - 3,763,954 Deposits from customers 17,941,836 4,095,460 11,277,478 9,607,703 377,211 411,756 19,466 36,382 120,323 43,887,615 Loans payable 5,573 22,585 26,427 77,581 96,938 83,775 82,815 81,853 1,746,104 2,223,651 Liabilities for income tax - - - 2,747 - - - - - 2,747 Deferred tax� - - - 1,307 - - - - - 1,307 Liabilities for salaries - - - 14,908 - - - - - 14,908 Other liabilities 214,216 449,779 87,261 7,847 - - - - - 759,103 Total Liabilities 21,313,627 4,711,833 11,749,042 9,800,691 495,618 495,531 102,281 118,235 1,866,427 50,653,285

STOPANSKA BANKA AD – SKOPJE

32

4. FINANCIAL INSTRUMENTS (continued) 4.3. Liquidity risk (continued) 4.3.3. Off-balance sheet items

(a) Commitments to extend credit

The commitments to extend credits are summarised in the table below.

(b) Financial guarantees and other financial facilities

Financial guarantees are also included below based on the earliest contractual maturity date. Sight Up to 1

month From 1 to 3

months From3 to 12

months From 1to 2

years From 2- 3

years From 3- 4

years From 4- 5

years Over 5

years In thousands

of denars

31 December 2007 Commitments to extend credits

7,332,304 -

-

-

-

-

-

-

-

7,332,304

Financial guarantees 5,447 165,286 620,908 1,148,748 160,912 811,885 101,320 - 6,370 3,020,876 Total 7,337,751 165,286 620,908 1,148,748 160,912 811,885 101,320 - 6,370 10,353,180

Sight Up to 1 month

From 1 to 3 months

From3 to 12 months

From 1to 2 years

From 2- 3 years

From 3- 4 years

From 4- 5 years

Over 5 years

In thousands of denars

31 December 2007 Commitments to extend credits 4,303,044 - - - - - - - - 4,303,044 Financial guarantees 4,110 515,138 418,011 871,072 295,389 27,208 5,019 71,044 109,233 2,316,224 Total 4,307,154 515,138 418,011 871,072 295,389 27,208 5,019 71,044 109,233 6,619,268

STOPANSKA BANKA AD - SKOPJE

33

4. FINANCIAL INSTRUMENTS (continued) 4.5. Fair value of financial assets and liabilities

Carrying amount Fair value 2007 2006 2007 2006 Financial Assets Placement with, and loans to, banks 5,443,514

6,001,414

5,443,375

6,001,398

Loans to customers 32,917,403 21,659,311 32,917,403 21,659,311 Investment securities- available for sale 123,123

107,354

123,123

107,354

Investment securities- held to maturity 3,838,602

4,391,916

3,838,602

4,391,916

Financial Liabilities Deposits from banks and financial institutions 3,750,252

2,232,155

3,750,252

2,232,155

Deposits from customers 43,280,888 32,962,368 43,285,866 32,962,460 Loans payable 1,635,217 1,692,440 1,635,217 1,692,440

(a) Placement with, and loans to, banks

In 2007, the overnight deposits represent the major part of this position, i.e. MKD 4,096,833 (2006 – null). The fair value of the overnight deposits and sight placements to banks is their carrying amount. The remain fixed interest bearing deposits are time deposits from 7 to 90 days. The estimated fair value of such deposits is based on discounted cash flow using interest rates for similar placements.

(b) Loans to customers

Loans are net of provision for impairment. The major part of the loans to customers is with floating interest rate (over 95%). The remaining part of the loans with fixed interest rate relates to “teaser loans”, for which the fair value is estimated based on the discounted cash flow.

(c) Financial instruments available for sale

Available for sale financial assets are measured at fair value based on quoted prices or amounts derived from cash flow models. Consequently, the fair value is their carrying amount.

(d) Financial instruments held to maturity

Held-to-maturity investments are financial assets with fixed or determinable payments and fixed maturity that the Entity has the positive intend and ability to hold to maturity. This portfolio comprises government bonds from old savings deposits, decentralization, government securities received in exchange for the Bank’s non-performing receivables as well as bonds issued by the Government of the Republic of Macedonia. Taking into consideration the nature of these instruments, as well as the existing market information, the management’s opinion is that the fair value of such instruments approximates their carrying amount.

4. FINANCIAL INSTRUMENTS (continued)

STOPANSKA BANKA AD - SKOPJE

34

4.5. Fair value of financial assets and liabilities (continued)

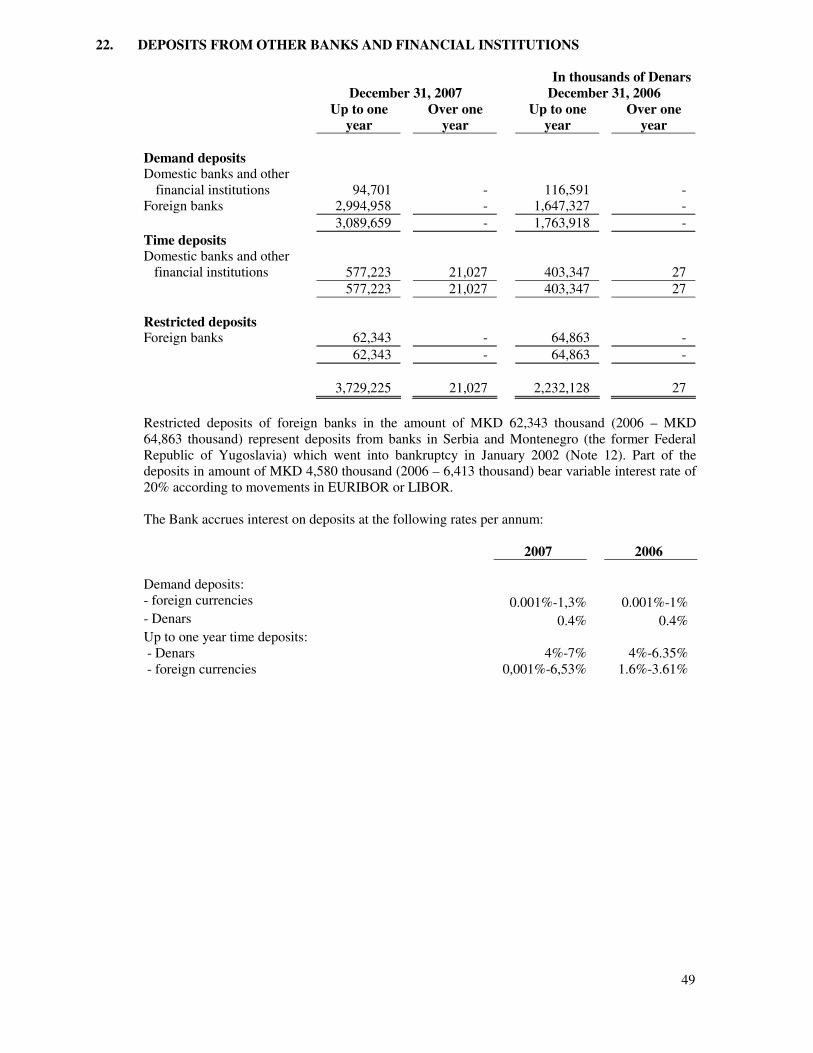

(e) Deposits from banks and other financial institutions The fair value of the sight deposits to banks and other financial institutions, i.e. MKD 3,089,659 (2006 – MKD 1,763,918), as well as the fair value of the deposits with floating interest rate is their carrying amount. The remaining part of these deposits represents restricted deposits (Note 22).

(f) Deposits from customers

The fair value of the sight deposits and the deposits with floating interest rate is their carrying amount. The estimated fair value of the deposits with fixed interest rate is based on discounted cash flows using the interest rate for similar deposits with similar maturity.

(g) Loans payable

Subordinated debt in amount of MKD 1,224,032 (2006 – MKD 1,223,482) represents the major part of this position. This loan is with floating interest rate. The remaining part relates to the loans from specific sources for which the market interest rate can not be reliably determined, taking into consideration the fact that there are no similar instruments on the market.

4.6. Capital management

The Bank’s objectives when managing capital, which is a broader concept than the ‘equity’ on the face of balance sheets, are:

• To comply with the capital requirements set by the regulator; • To safeguard the Bank’s ability to continue as a going concern so that it can continue to provide returns for shareholders and benefits for other stakeholders; and • To maintain a strong capital base to support the development of its business.

Capital adequacy and the use of regulatory capital are monitored regularly by the Bank’s management, employing techniques based on the directives required by the regulator, for supervisory purposes. The required information is filed with the NBRM on a quarterly basis.

The Bank’s regulatory capital is divided into two tiers:

• Tier 1 capital: share capital (net of any book values of the treasury shares), retained earnings

and reserves created by appropriations of retained earnings. The bank’s uncovered loss from previous years, the current loss, the book value of goodwill are deducted in arriving at Tier 1 capital; and

• Tier 2 capital: qualifying subordinated loan capital, cumulative preferred shares and premium from cumulative preferred shares sold revaluation reserves from fixed assets, hybrid capital instruments. Investments in financial institutions are deducted from Tier 1 and Tier 2 capital to arrive at the regulatory capital.

The risk-weighted assets are measured by means of a hierarchy of four risk weights classified according to the nature of – and reflecting an estimate of credit risk associated with – each asset and counterparty, taking into account any eligible collateral or guarantees. A similar treatment is adopted for off-balance sheet exposure, with some adjustments to reflect the more contingent nature of the potential losses.

4. FINANCIAL INSTRUMENTS (continued)

STOPANSKA BANKA AD - SKOPJE

35

4.7. Sensitivity analysis 4.7.1. Sensitivity analysis (foreign currency)

The currency risk management, performed by monitoring the assets and liabilities in foreign currencies, is supplemented by conducting sensitivity analysis of the Bank’s foreign currencies assets and liabilities. Therefore, appropriate scenario (change of the exchange rates by +10% i.e. -10%, with respect to the MKD) is used.

In thousands denars 2007 Change in exchange rate Total 10% -10% ASSETS Cash and cash equivalents 4,722,680 222,516 (222,516) Treasury bills 5,232,175 - - Financial instruments held for trading 253,301 8,856 (8,856) Investment securities- available for sale 123,123 1,179 (1,179) Investment securities- held to maturity 3,838,602 383,860 (383,860) Placement with, and loans to, banks 5,443,514 544,351 (544,351) Loans to customers 32,917,403 2,108,931 (2,108,931) Other receivables 329,562 34 (34) Total assets 52,860,360 3,269,727 (3,269,727) LIABILITIES 3,750,252 311,562 (311,562) Deposits from banks and financial institutions

Deposits from customers 43,280,888 2,222,831 (2,222,831) Loans payable 1,635,217 135,358 (135,358) Other liabilities 759,103 11,552 (11,552) Total liabilities 49,425,460 2,681,303 (2,681,303) Net currency gap: 31 December 2007 588,424 (588,424) 31 December 2006 840,044 (840,044)

At 31 December2007, if MKD had weakened 10% against the EUR (and all other currencies) with all other variables held constant, the profit for the year would have been MKD 588,425 thousands higher (2006, MKD 840,044 thousands). Conversely, if the MKD had strengthened 10% against the EUR (and all other currencies) with all other variables held constant, the profit for the year would have been MKD 588,425 thousands millions lower (2006, MKD 840,044 thousands). The lower sensitivity of SB’s assets and liabilities in case of change in foreign exchange rates compared to the previous year is a result of the lower open currency position as at end of 2007.

4.7.2. Sensitivity analysis (interest rates)

As a part of interest rate risk management, the Bank analyzes the sensitivity of the balance sheet items. The sensitivity analysis is performed taking into account assets and liabilities with floating interest rates. Hence, it was tested what would happen, if MKD and foreign currencies interest rates decreased/increased by 0.4 b.p. and 0.3 b.p respectively. The assumptions concerning the above mentioned changes are based on the volatility of the Central Bank bills’ interest rates (for the MKD) and the volatility of the one month EURIBOR (for the foreign currencies) during 2007.

. 4. FINANCIAL INSTRUMENTS (continued)

STOPANSKA BANKA AD - SKOPJE

36

4.7. Sensitivity analysis (continued) 4.7.2. Sensitivity analysis (interest rates) (continued)

If interest rates had been 0.4 b.p. for MKD and 0.3 b.p. for foreign currencies higher with all other variables held constant, taking into account the average balances of assets and liabilities for 2007, profit for the year would have been MKD 15,131 thousands lower. Conversely, if the interest rates had been 0.4 b.p. for MKD and 0.3 b.p. for foreign currencies lower with all other variables held constant, profit for the year would have been MKD 15,131 thousands higher. Such an effect arises as a result of higher sensitivity of liabilities compared to the sensitivity of the assets when experiencing a change of the interest rates

In thousands of denars Net effect over IS as result of interest rates change

ASSETS

Total 31.12.2007

+0.4 bp MKD IR

+0.3 bp FX IR

-0.4 bp MKD IR

-0.3 bp FX IR

Cash and cash equivalents Treasury bills 4,722,680 - - Financial instruments held for trading 5,232,175 15,259 (15,259) Investment securities- available for sale 253,301 - - Investment securities- held to maturity 123,123 Placement with, and loans to, banks 3,838,602 12,343 (12,343) Loans to customers 5,443,514 17,156 (17,156) Total assets 32,917,403 78,925 (78,925) 52,530,798 123,684 (123,684) LIABILITIES Deposits from banks and financial institutions Deposits from customers 3,750,252 2,537 (2,537) Loans payable 43,280,889 132,606 (132,606) Total liabilities 1,635,217 3,671 (3,671) 48,666,358 138,815 (138,815) Net interest rates gap: 31 December 2007 (15,131) 15,131

STOPANSKA BANKA AD - SKOPJE

37

5. INTEREST INCOME AND EXPENSES

Interest income and expense can be analyzed by the sectors to which loans and advances have been granted, and the related sources of deposits or borrowings obtained, as follows:

In thousands of Denars Year ended Year ended December 31, 2007 December 31, 2006 Income Expense Income Expense

- Citizens 1,709,537 702,908 1,325,467 404,658 - Enterprises 1,018,906 384,052 692,670 318,987 - Investments securities 244,859 - 210,379 - - Due from other banks 174,985 442 165,587 19,957 - Treasury bills and other Eligible bills 176,321 -

142,739 -

- Balances with central bank 37,805 - 28,174 - - Other - 80,470 - 12,739 3,362,413 1,194,464 2,565,016 756,341

6. FEE AND COMMISSION INCOME AND EXPENSES