starting your career? here’s the last opportunity to build ... · here’s the last opportunity...

TRANSCRIPT

Starting your career? Here’s the last opportunity

to build wealth easily.

Distributed by:

Why is it the last opportunity to build wealth easily?

While we focus on getting a better

paying job, we seldom pay attention to

what we do with the money we get.

If you are smart about your savings and investments at this stage of life, you will be able to build wealth much more easily than in later stages.

Read on to find out how.

When you are young it can be difficult to

understand the reason for saving money. Most

of your friends and colleagues are most likely

spending on things like new smartphones,

on-trend clothes and eating out at the newest

jaunt.

Rather than spending all your disposable

income, you can start saving it from a young

age and set yourself up for a stable and secure

financial future. As soon as your monthly

salary comes into your hands, prepare a

budget and plan how much to save & spend.

Invest your savings immediately. As the adage

goes, tiny drops make an ocean. Little savings

started early can become significant sums later

in life.

11:50

11:50

11:50

11:50

11:50

11:50

11:50

Small savings add up to big money

Eyeing that new smartphone that’s just been launched? Even if it eats up your entire pay cheque? Think again!

0101

1 cola bottle 1 year45

Don't just save, invest to make it grow

Be smart with your money

You may think investing is something you don’t need to consider right now. But there’s a cost to keeping your money idle.

16,425

5 years

1,11,011

1 burger

Let’s take an amount of `45 that you spend on a bottle of cola and

burger every day. That adds up to a saving of `16,425 a year. If

you keep this money in your cupboard or locker or even a savings

account, its value will only decrease over time due to inflation.

Five years later, you will be able to buy a lot less with this money

than you can today. That’s because inflation reduces the

purchasing power of your money. The key is to invest in products

that give you returns higher than the rate of inflation.

Say you invest the amount monthly in an instrument that earns

12% a year, it would grow to `1,11,011 in 5 years. You could use

this money to plan a holiday or buy a two-wheeler. If you continue

investing, it will grow to `42,17,082 in 30 years. Now that’s called

putting your money to work for you.

02

Dreaming of designer wear or drooling over that machismo bike? You can save 35% and make it yours.

Plan for your goals

So if you’re dreaming of owning that high-performance bike that costs `1,50,000 and you take a loan for

3 years at the rate of 10% p.a. Thus, the total amount that you will pay in 3 years will be `1,74,243 with

a monthly EMI of `4,840.

On the other hand, you can make a monthly investment of `3,590 earning an interest of 10% and make it

yours in 3 years. This way you will invest `1,29,240 and earn `20,760. Now, that’s a whopping

difference of 35%* between the two costs. It is wiser to spend 35% less by making a monthly investment

towards the bike vis-a-vis taking a loan.

Or if you’re looking to buy a home in 5 years and need a down

payment of `15,00,000 you can invest towards your goal

by starting a monthly investment of `18,366 at an interest

rate of 12% to accumulate that amount.

*assuming that the cost of the bike remains the same over 3 years 03

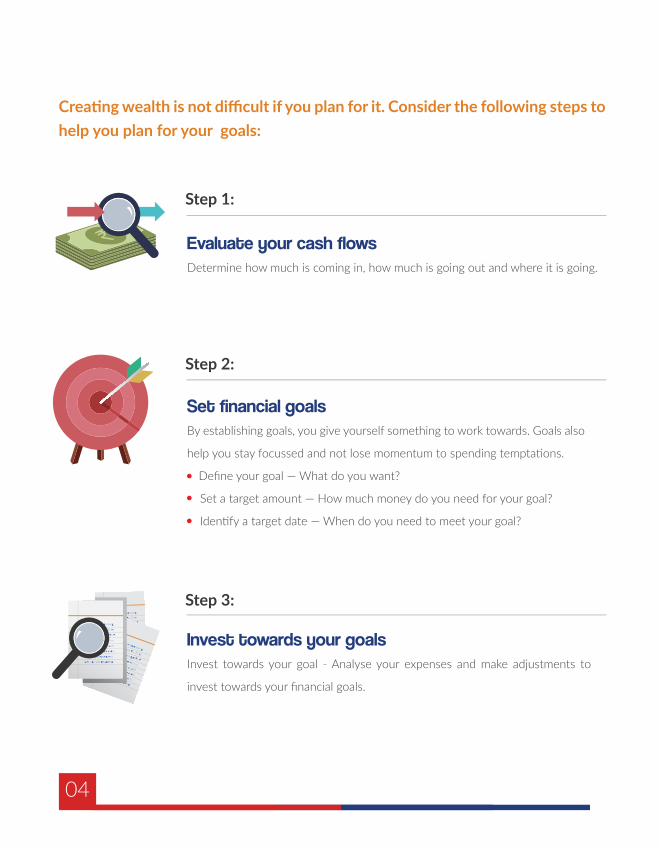

Creating wealth is not difficult if you plan for it. Consider the following steps to help you plan for your goals:

Evaluate your cash flows Determine how much is coming in, how much is going out and where it is going.

Set financial goals By establishing goals, you give yourself something to work towards. Goals also

help you stay focussed and not lose momentum to spending temptations.

Define your goal — What do you want?

Set a target amount — How much money do you need for your goal?

Identify a target date — When do you need to meet your goal?

Invest towards your goalsInvest towards your goal - Analyse your expenses and make adjustments to

invest towards your financial goals.

04

Step 1:

Step 2:

Step 3:

Be wise and plan for a rainy day

Before you invest…

Step 4:

Plan for emergencies and contingencies Start building a robust financial foundation by putting aside an emergency

fund of easily accessible savings. Keep aside 3 to 6 months of basic living

expenses to protect you from an unexpected job loss.

Invest in a pure protection insurance plan or term insurance. Such plans are

the most basic form of life insurance and enable you to secure your family

financially. Remember, the insurance amount that looks large now will begin

to look much smaller later. You should make the most by availing a high life

insurance cover for a relatively low premium payment when you’re young.

Step 5:

Plan your taxesLastly, understand the tax implications of your financial decisions and invest wisely to reduce your tax

burden. Equity Linked Savings Schemes (ELSS) of mutual funds are a good investment option as they offer

the dual-advantage of investment appreciation and tax savings. You can also invest in Retirement Funds that

are notified pension funds to save tax under Sec 80C.

05

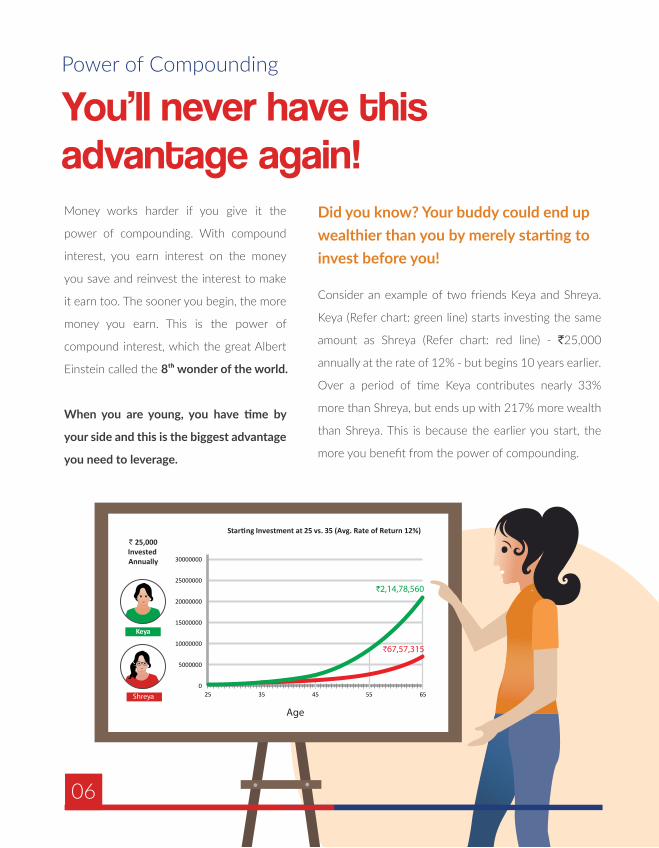

Starting Investment at 25 vs. 35 (Avg. Rate of Return 12%)

06

You’ll never have this advantage again!

Power of Compounding

Money works harder if you give it the

power of compounding. With compound

interest, you earn interest on the money

you save and reinvest the interest to make

it earn too. The sooner you begin, the more

money you earn. This is the power of

compound interest, which the great Albert

Einstein called the 8th wonder of the world.

When you are young, you have time by

your side and this is the biggest advantage

you need to leverage.

Consider an example of two friends Keya and Shreya.

Keya (Refer chart: green line) starts investing the same

amount as Shreya (Refer chart: red line) - `25,000

annually at the rate of 12% - but begins 10 years earlier.

Over a period of time Keya contributes nearly 33%

more than Shreya, but ends up with 217% more wealth

than Shreya. This is because the earlier you start, the

more you benefit from the power of compounding.

Did you know? Your buddy could end up wealthier than you by merely starting to invest before you!

Age

Keya

Shreya

` 25,000Invested Annually

`2,14,78,560

0

5000000

10000000

15000000

20000000

25000000

30000000

25 35 45 55 65

`67,57,315

Kickstart your investment plan with Mutual Funds

Benefits of Mutual Funds

Mutual funds are a great investment option for the young. They pool money from a number of people and use that money to buy government securities, stocks and bonds.

So, when you invest in a mutual fund, you

can invest in a diversified range of stocks,

bonds and government securities through

one single channel.

Mutual funds give you the benefit of diversification. They spread your risk across a wide variety

of investments vis-à-vis you putting all your money in one investment and losing it if it goes bad.

You benefit from diversification without requiring a large amount of money to spread

across investments.

Mutual funds can be used to invest towards a variety of short-, medium- and long-term goals.

Equity mutual funds are best suited to give you the advantage of beating inflation.

Mutual funds are regulated by the Securities & Exchange Board of India (SEBI) which means

mutual funds have to follow certain rules and provide the investor with relevant information.

07

08

15%` 27,56,561

When you are young, Mutual Funds are the best bet

Benefits of Mutual Funds

Even if you set aside `1000 every month and

invest it in a SIP earning a return of 15%*, you

will have `27,56,561, after 25 years. While you

have essentially invested only `3,00,000 you

would have earned a whopping `24,56,561 on

your investments. This is thanks to the power of

compounding as your returns are reinvested year

after year. A perfect example of money being put

to work for you.

You need not have a large amount to invest. You can invest a small amount regularly through a

monthly/quarterly investment. Such small investments are called Systematic Investment Plan (SIP) leading

to a significant investment over time.

Also, with a mutual fund investment you can weather the ups and downs of a storm better than

with a few individual stocks.

It is convenient to invest in mutual funds. if you want to invest your monthly savings in Mutual

Funds, all you need to do is register your SIP once and the money gets debited from your bank

account.

*The assumed rate of return is used only to explain the concept of Power of Compounding. It does not forecast or guarantee the returns given by any mutual fund scheme or any other investment instrument or asset class.

If you would like to read more to enhance your investment knowledge

and wealth creation opportunities, visit www.hdfcmfinvestwise.com

or contact your financial advisoror give a missed call on 92218 92218.

Mutual Fund investments are subject to market risks. Read all scheme related documents carefully.

cont

ent +

des

ign:

ww

w.ri

tekn

owle

dgel

abs.

comThe information provided herein is solely for creating awareness and educating investors. Whilst HDFC

Mutual Fund takes reasonable steps to ensure the accuracy of the information, it does not guarantee the

completeness, efficacy, accuracy or timeliness of such information. Readers are advised not to act purely

on the basis of this information but also seek professional advice from experts before taking any

investment decisions. Neither HDFC Mutual Fund nor HDFC Asset Management Company Limited nor

any person connected with them accepts any liability arising from the use of this information.