special comment moody’s-icra corporate finance · special comment moody’s-icra table of...

TRANSCRIPT

IAC ICRA Limited

Associate of Moody’s Investors Service

www.moodys.com

Corporate Finance Moody’s-ICRASpecial Comment

Table of Contents: Summary opinion 1

Importance of family-controlled companies in India 2 Moody’s-ICRA survey 3 Level of family shareholding 4 Checks and balances in Indian corporate environment 5 Governance strengths of Indian family-controlled corporates 6 Governance challenges for Indian family-controlled corporates 9 Moody’s Related Research 12 ICRA’s Related Research 12

Moody’s Contacts:

Mumbai 91.22.2422.3152

17 Chetan Modi Representative Director

New York 1.212.553.1653

0 Mark Watson Managing Director

Hong Kong 852.2916.1121

Jennifer Elliott Group Managing Director

Sydney 61.2.9270.8117

7 Brian Cahill Managing Director/Australia

ICRA Contacts:

Mumbai 91.22.3047.0006

17 Anjan Ghosh General Manager

Gurgaon 91.124.4545.370

0 Naresh Takkar Managing Director

October 2007

Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies India

Summary opinion

Family-controlled firms often have specific characteristics. Their strengths can include a long-term management perspective and a cautious approach to risk to avoid destroying family wealth – as well as an ability to act quickly. However, family control can also raise specific corporate governance concerns in areas including adaptability, leadership transition, checks and balances and transparency.

Family companies dominate India’s corporate landscape. Moody’s and ICRA have surveyed certain corporate governance practices of 32 Indian companies in 16 prominent family groups, covering a broad cross-section of Indian industry.

These companies have responded well to the opportunities available in the fast-growing and liberalizing economy of modern India. However, the lack of a meaningful “control group” of non-family controlled companies means that the survey has not been able to draw conclusions on how the family controlled-business model in India compares against one based on more widespread share ownership.

Although Indian corporate governance practices continue to improve, this largely reflects regulation of listed companies, particularly with regard to certain “checks and balances”. These include the composition of the board of directors and the operations of audit committees. Although there are material residual issues regarding checks and balances, these are generic to corporate India and not isolated to family companies – for example, the lack of activist shareholders and a business and cultural environment that does not permit hostile mergers and acquisitions.

2 October 2007 Special Comment Moody’s-ICRA Corporate Finance - Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

Special Comment Moody’s Corporate Finance

Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

Although a few notable companies are leading the way in emphasizing the importance of good governance and adopting global best practice, important governance issues persist. These potentially have negative credit implications, and typically effect issues not (or only partially) covered by regulations – including leadership transition, transparency on ownership/control and related-party transactions, and independence of directors.

The lack of board nomination sub-committees in most of the companies surveyed suggests that succession planning is not fully deliberated with appropriate involvement of independent directors.

Lack of clarity on ownership and the financial position of non-listed family-controlled holding companies (which may have raised significant amounts of debt to fund the group) are material credit weaknesses. Although the surveyed group is not excessively leveraged, in general the prospect remains of higher leverage as families try to avoid losing control while they implement their often aggressive growth plans.

Despite regulations regarding independent board directors, families retain significant control over listed companies – and sometimes appear to be acting primarily for the benefit of their group or family. As such, the difficulty in ascertaining the true independence of directors is a big corporate governance challenge.

Importance of family-controlled companies in India

The Indian corporate sector is dominated by companies controlled and managed by family groups. For example, 17 of the 30 Sensex1 companies are family-controlled.

Moody’s has observed globally that family-controlled companies can face specific corporate governance challenges. These include:

Comparatively fewer checks and balances on their actions

Leadership transition risks, and the emergence of conflicting visions and strategies

Limited transparency on matters such as ownership, control and related party transactions

Slowness to adapt, or respond to emerging business challenges

Propensity towards higher leverage.

Many Indian family-controlled groups have complex corporate structures. Furthermore, it is common to see inter-group cross-holdings of shares. In such cases and despite regulatory requirements to disclose promoter2 shareholding, it can be difficult to assess ownership and control – which factors potentially impact credit quality – on the basis of public information.3

Pyramid structures – where control of substantial operating companies can be achieved through ownership of 51% of a chain of holding companies – are not commonly observed in India. In addition, companies have generally not issued different classes of shares with differential voting rights.4

1 The Sensex is the common name for the Bombay Stock Exchange Sensitive Index, comprising the 30 largest and most actively traded stocks. The

balance 13 companies also includes banks and state-owned enterprises 2 Although the classification of Promoters may be subject to SEBI discretion, the concept typically covers the largest shareholders that control a

company. In this report, the word is used to mean the controlling family. 3 A number of private corporate bodies and investment firms may hold large stakes, classified both under ‘promoter holdings’ as well as under

‘others’ in the category of public shareholders. 4 Interestingly, dual classes of shares may emerge in future cases where companies issue convertible bonds, but want to avoid dilution of family

control should conversion occur. Both Tata Motors and Tata Steel have recently issued Convertible Alternate Reference Securities that are intended to convert into shares with different voting rights from common stock.

3 October 2007 Special Comment Moody’s-ICRA Corporate Finance - Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

Special Comment Moody’s Corporate Finance

Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

Although the lack of pyramid structures and different classes of shares in India are governance positives, their absence may be more reflective of the fact that families can maintain control without having to resort to such measures. This is possibly due to India’s business culture which lacks activist shareholders and does not permit hostile M&A activity, plus the blocking rights available to a 26% shareholder.5

Moody’s-ICRA survey

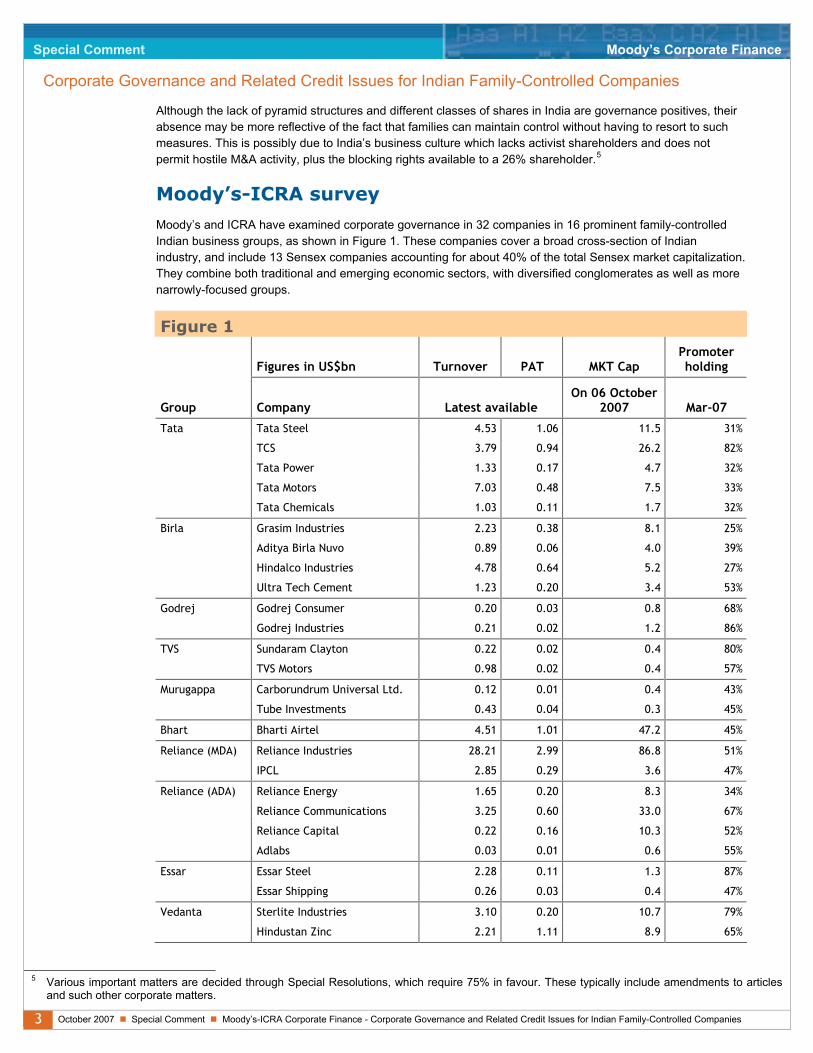

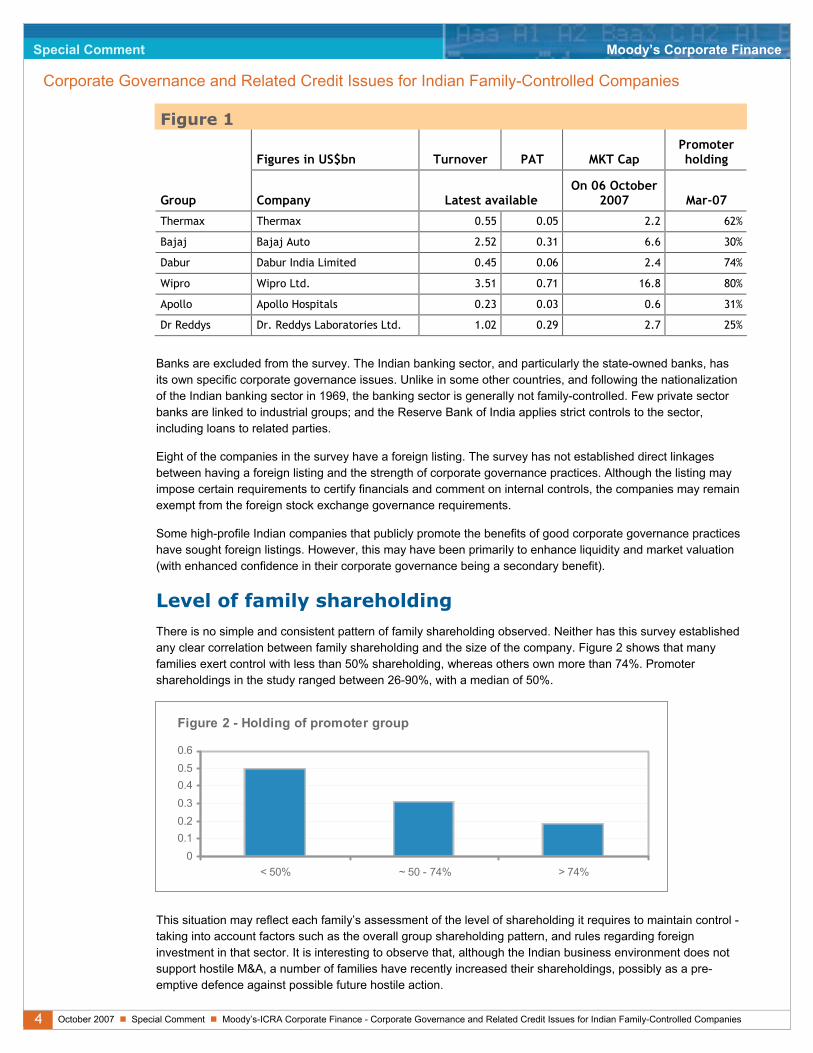

Moody’s and ICRA have examined corporate governance in 32 companies in 16 prominent family-controlled Indian business groups, as shown in Figure 1. These companies cover a broad cross-section of Indian industry, and include 13 Sensex companies accounting for about 40% of the total Sensex market capitalization. They combine both traditional and emerging economic sectors, with diversified conglomerates as well as more narrowly-focused groups.

Figure 1

Figures in US$bn Turnover PAT MKT Cap Promoter holding

Group Company Latest available On 06 October

2007 Mar-07

Tata Tata Steel 4.53 1.06 11.5 31%

TCS 3.79 0.94 26.2 82%

Tata Power 1.33 0.17 4.7 32%

Tata Motors 7.03 0.48 7.5 33%

Tata Chemicals 1.03 0.11 1.7 32%

Birla Grasim Industries 2.23 0.38 8.1 25%

Aditya Birla Nuvo 0.89 0.06 4.0 39%

Hindalco Industries 4.78 0.64 5.2 27%

Ultra Tech Cement 1.23 0.20 3.4 53%

Godrej Godrej Consumer 0.20 0.03 0.8 68%

Godrej Industries 0.21 0.02 1.2 86%

TVS Sundaram Clayton 0.22 0.02 0.4 80%

TVS Motors 0.98 0.02 0.4 57%

Murugappa Carborundrum Universal Ltd. 0.12 0.01 0.4 43%

Tube Investments 0.43 0.04 0.3 45%

Bhart Bharti Airtel 4.51 1.01 47.2 45%

Reliance (MDA) Reliance Industries 28.21 2.99 86.8 51%

IPCL 2.85 0.29 3.6 47%

Reliance (ADA) Reliance Energy 1.65 0.20 8.3 34%

Reliance Communications 3.25 0.60 33.0 67%

Reliance Capital 0.22 0.16 10.3 52%

Adlabs 0.03 0.01 0.6 55%

Essar Essar Steel 2.28 0.11 1.3 87%

Essar Shipping 0.26 0.03 0.4 47%

Vedanta Sterlite Industries 3.10 0.20 10.7 79%

Hindustan Zinc 2.21 1.11 8.9 65%

5 Various important matters are decided through Special Resolutions, which require 75% in favour. These typically include amendments to articles

and such other corporate matters.

4 October 2007 Special Comment Moody’s-ICRA Corporate Finance - Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

Special Comment Moody’s Corporate Finance

Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

Figure 1

Figures in US$bn Turnover PAT MKT Cap Promoter holding

Group Company Latest available On 06 October

2007 Mar-07

Thermax Thermax 0.55 0.05 2.2 62%

Bajaj Bajaj Auto 2.52 0.31 6.6 30%

Dabur Dabur India Limited 0.45 0.06 2.4 74%

Wipro Wipro Ltd. 3.51 0.71 16.8 80%

Apollo Apollo Hospitals 0.23 0.03 0.6 31%

Dr Reddys Dr. Reddys Laboratories Ltd. 1.02 0.29 2.7 25%

Banks are excluded from the survey. The Indian banking sector, and particularly the state-owned banks, has its own specific corporate governance issues. Unlike in some other countries, and following the nationalization of the Indian banking sector in 1969, the banking sector is generally not family-controlled. Few private sector banks are linked to industrial groups; and the Reserve Bank of India applies strict controls to the sector, including loans to related parties.

Eight of the companies in the survey have a foreign listing. The survey has not established direct linkages between having a foreign listing and the strength of corporate governance practices. Although the listing may impose certain requirements to certify financials and comment on internal controls, the companies may remain exempt from the foreign stock exchange governance requirements.

Some high-profile Indian companies that publicly promote the benefits of good corporate governance practices have sought foreign listings. However, this may have been primarily to enhance liquidity and market valuation (with enhanced confidence in their corporate governance being a secondary benefit).

Level of family shareholding

There is no simple and consistent pattern of family shareholding observed. Neither has this survey established any clear correlation between family shareholding and the size of the company. Figure 2 shows that many families exert control with less than 50% shareholding, whereas others own more than 74%. Promoter shareholdings in the study ranged between 26-90%, with a median of 50%.

Figure 2 - Holding of promoter group

00.10.20.30.40.50.6

< 50% ~ 50 - 74% > 74%

This situation may reflect each family’s assessment of the level of shareholding it requires to maintain control - taking into account factors such as the overall group shareholding pattern, and rules regarding foreign investment in that sector. It is interesting to observe that, although the Indian business environment does not support hostile M&A, a number of families have recently increased their shareholdings, possibly as a pre-emptive defence against possible future hostile action.

5 October 2007 Special Comment Moody’s-ICRA Corporate Finance - Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

Special Comment Moody’s Corporate Finance

Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

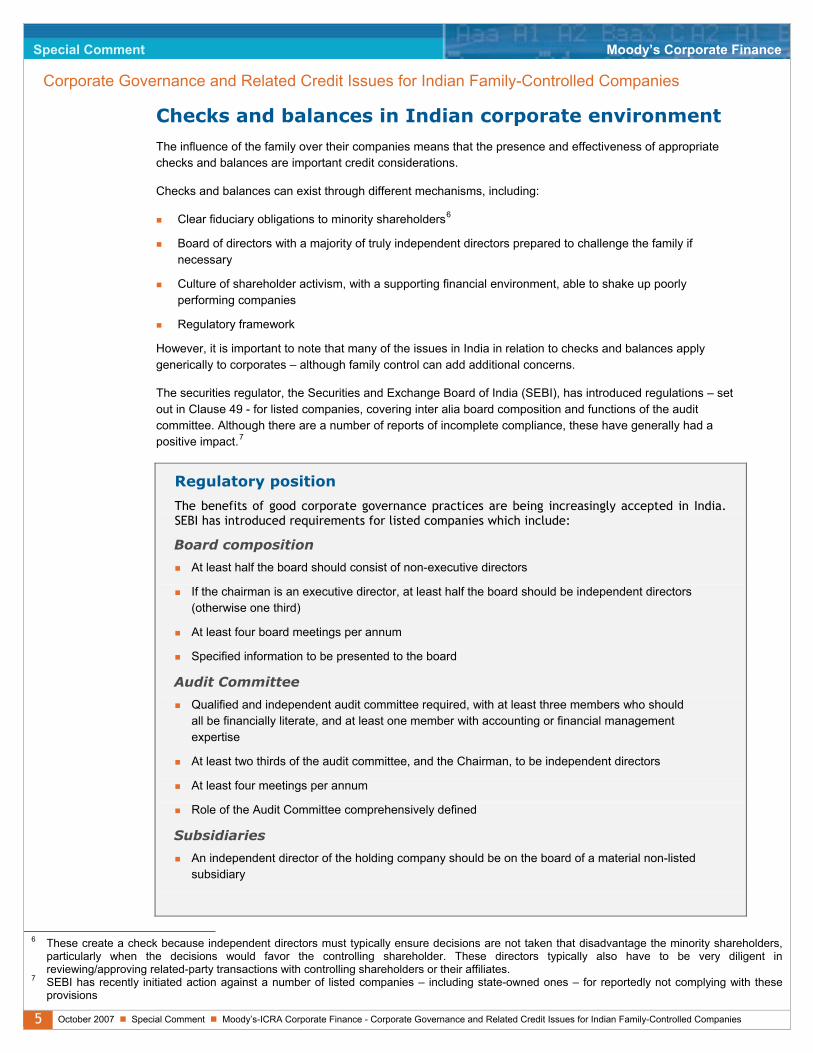

Checks and balances in Indian corporate environment

The influence of the family over their companies means that the presence and effectiveness of appropriate checks and balances are important credit considerations.

Checks and balances can exist through different mechanisms, including:

Clear fiduciary obligations to minority shareholders6

Board of directors with a majority of truly independent directors prepared to challenge the family if necessary

Culture of shareholder activism, with a supporting financial environment, able to shake up poorly performing companies

Regulatory framework

However, it is important to note that many of the issues in India in relation to checks and balances apply generically to corporates – although family control can add additional concerns.

The securities regulator, the Securities and Exchange Board of India (SEBI), has introduced regulations – set out in Clause 49 - for listed companies, covering inter alia board composition and functions of the audit committee. Although there are a number of reports of incomplete compliance, these have generally had a positive impact.7

Regulatory position

The benefits of good corporate governance practices are being increasingly accepted in India. SEBI has introduced requirements for listed companies which include:

Board composition

At least half the board should consist of non-executive directors

If the chairman is an executive director, at least half the board should be independent directors (otherwise one third)

At least four board meetings per annum

Specified information to be presented to the board

Audit Committee

Qualified and independent audit committee required, with at least three members who should all be financially literate, and at least one member with accounting or financial management expertise

At least two thirds of the audit committee, and the Chairman, to be independent directors

At least four meetings per annum

Role of the Audit Committee comprehensively defined

Subsidiaries

An independent director of the holding company should be on the board of a material non-listed subsidiary

6 These create a check because independent directors must typically ensure decisions are not taken that disadvantage the minority shareholders,

particularly when the decisions would favor the controlling shareholder. These directors typically also have to be very diligent in reviewing/approving related-party transactions with controlling shareholders or their affiliates.

7 SEBI has recently initiated action against a number of listed companies – including state-owned ones – for reportedly not complying with these provisions

6 October 2007 Special Comment Moody’s-ICRA Corporate Finance - Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

Special Comment Moody’s Corporate Finance

Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

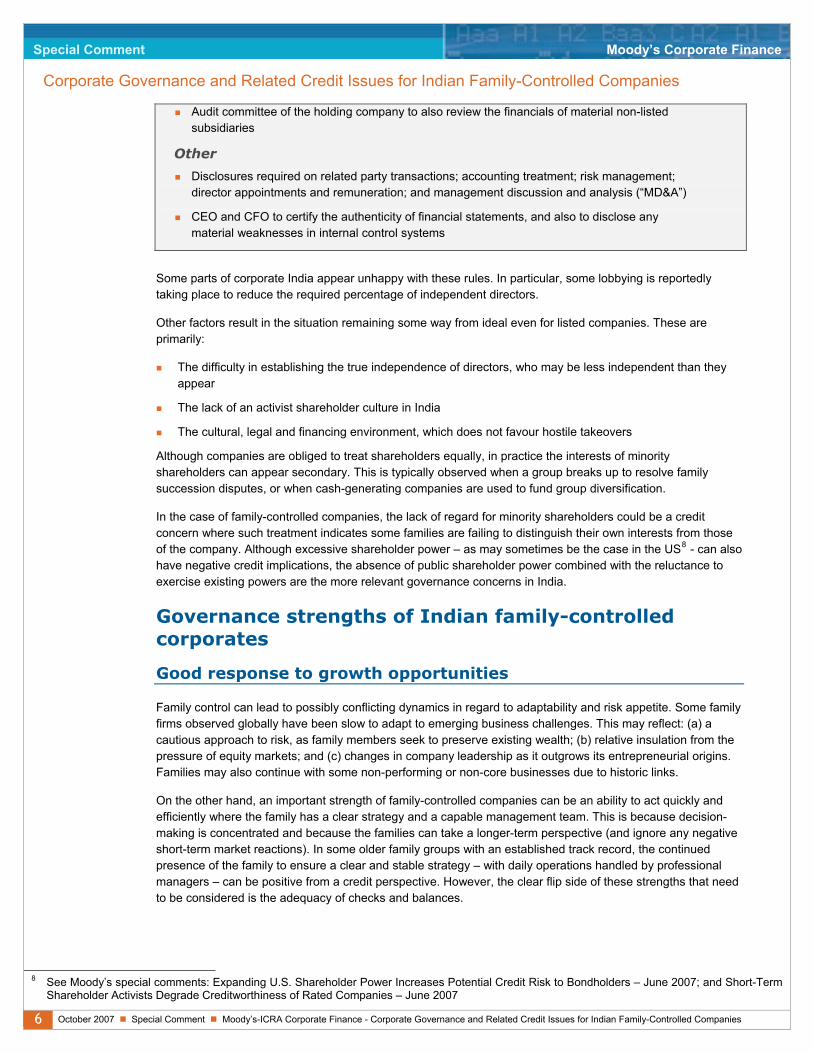

Audit committee of the holding company to also review the financials of material non-listed subsidiaries

Other

Disclosures required on related party transactions; accounting treatment; risk management; director appointments and remuneration; and management discussion and analysis (“MD&A”)

CEO and CFO to certify the authenticity of financial statements, and also to disclose any material weaknesses in internal control systems

Some parts of corporate India appear unhappy with these rules. In particular, some lobbying is reportedly taking place to reduce the required percentage of independent directors.

Other factors result in the situation remaining some way from ideal even for listed companies. These are primarily:

The difficulty in establishing the true independence of directors, who may be less independent than they appear

The lack of an activist shareholder culture in India

The cultural, legal and financing environment, which does not favour hostile takeovers

Although companies are obliged to treat shareholders equally, in practice the interests of minority shareholders can appear secondary. This is typically observed when a group breaks up to resolve family succession disputes, or when cash-generating companies are used to fund group diversification.

In the case of family-controlled companies, the lack of regard for minority shareholders could be a credit concern where such treatment indicates some families are failing to distinguish their own interests from those of the company. Although excessive shareholder power – as may sometimes be the case in the US8 - can also have negative credit implications, the absence of public shareholder power combined with the reluctance to exercise existing powers are the more relevant governance concerns in India.

Governance strengths of Indian family-controlled corporates

Good response to growth opportunities

Family control can lead to possibly conflicting dynamics in regard to adaptability and risk appetite. Some family firms observed globally have been slow to adapt to emerging business challenges. This may reflect: (a) a cautious approach to risk, as family members seek to preserve existing wealth; (b) relative insulation from the pressure of equity markets; and (c) changes in company leadership as it outgrows its entrepreneurial origins. Families may also continue with some non-performing or non-core businesses due to historic links.

On the other hand, an important strength of family-controlled companies can be an ability to act quickly and efficiently where the family has a clear strategy and a capable management team. This is because decision-making is concentrated and because the families can take a longer-term perspective (and ignore any negative short-term market reactions). In some older family groups with an established track record, the continued presence of the family to ensure a clear and stable strategy – with daily operations handled by professional managers – can be positive from a credit perspective. However, the clear flip side of these strengths that need to be considered is the adequacy of checks and balances.

8 See Moody’s special comments: Expanding U.S. Shareholder Power Increases Potential Credit Risk to Bondholders – June 2007; and Short-Term

Shareholder Activists Degrade Creditworthiness of Rated Companies – June 2007

7 October 2007 Special Comment Moody’s-ICRA Corporate Finance - Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

Special Comment Moody’s Corporate Finance

Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

Indian families have generally responded well to the changing business environment, and many have expanded successfully into new businesses in both traditional and new economic sectors. This may be because large Indian groups are best placed to exploit growth opportunities. They have greater access to capital and management than do local startups; and they have a more intimate knowledge of the operating environment and the key players than do foreign competitors.9

The groups surveyed have shown good recent financial performances, with mean compound revenue growth of 28% from 2001-02 through 2006-07, and mean compound post-tax profit growth of 47%. However, these results should be considered in the context of the multiple opportunities available in a populous country experiencing a high rate of growth. The lack of a “control group” of conglomerates with widespread shareholding, and without family control, means that the survey cannot draw any conclusions as to whether family companies perform better than non-family companies in India.

Furthermore, it remains to be seen how they will perform as the economic cycle changes. During the downturn of the late 1990s, some family groups experienced severe financial difficulties. Certain groups entered into debt restructuring schemes that were shareholder-friendly - where banks did not seize assets and the families were able to retain broad control until the economic cycle turned. However, this also to a large extent reflects the Indian business environment.

Financial and funding strategies

The Indian financial system is still developing a credit culture, and name recognition remains important to help raise funding. However, an important Indian governance positive is that the lack of family-controlled banks means that companies cannot fund themselves from a captive depositor base.

Family companies are generically susceptible to excessive indebtedness, as they seek to expand without diluting ownership or control. However, the companies studied have maintained conservative leverage, with average debt:equity staying at about 0.5x since 2001, although this is starting to change quickly. The study reveals no clear link between the degree of leverage and the age of the company.

Many Indian companies have issued Foreign Currency Convertible Bonds. The prevailing assumption in corporate India is that these instruments will convert to equity. Some companies are now looking to more creative solutions to prevent dilution of their control; though it remains to be seen whether family companies will eventually resort to a greater level of debt funding.

Intra-group support can be either a benefit or a disadvantage, depending on circumstances. In order to avoid loss of reputation or other damage arising from a default, companies connected via family ownership may support each other. This can benefit creditors of the troubled company, but at the expense of creditors of the supporting company.

Some board best practices

Appropriate size of boards

In Moody’s opinion, the optimum number of board members for most medium to large-sized companies is typically eight to twelve.10 With fewer members, it can be difficult to staff sub-committees and there may be insufficient diversity of opinion. With more members, board dynamics may suffer.

9 Domestic players have also benefited from regulations on foreign direct investment, plus the benefits perceived by foreign companies in

establishing joint ventures with local players. 10 See Moody’s special comment: Moody’s Findings on Corporate Governance in the United States and Canada: October 2004

8 October 2007 Special Comment Moody’s-ICRA Corporate Finance - Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

Special Comment Moody’s Corporate Finance

Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

Figure 3 shows that most boards in the study had between eight and twelve members, with a mean of 10.5.

Figure 3 - Average Board Size

0

0.2

0.4

0.6

0.8

< 8 8-12 12-15 > 15

Number of Board Members

Audit committees have important oversight responsibilities

The audit committee is the most important board sub-committee. It oversees the financial reporting process, accounting quality, risk management function and internal control systems.

The key functions of a listed Indian company’s audit committee are: Oversight of financial reporting process and the disclosure of financial information

Recommending to the board the appointment, re-appointment and fixing of audit fees; plus approving payments to statutory auditors for any non-audit services

Reviewing financial statements before submission to the board

Reviewing the performance of statutory and internal auditors; the adequacy of internal control systems; and the adequacy of the internal audit function

The companies surveyed averaged four members on their audit committees, against a minimum requirement of three. Many audit committees are now manned entirely by independent directors (with the CFO also invited to attend). The average number of meetings held was five, against a minimum requirement of four.

However, SEBI’s definition of “financially literate” is extremely broad – essentially the ability to read and understand basic financial statements. This may result in some audit committees not being technically equipped to perform their role adequately.

Executive pay linked to performance

The structure and level of executive pay is an important governance concern in the developed world, and has recently become an issue of public interest in India. Concerns about the extraction of wealth are particularly relevant in Indian family companies given the dominant role of the family.

Nearly all companies surveyed had a remuneration/compensation committee to determine senior management compensation, although this is not a regulatory requirement.11

In about 75% of the companies surveyed, the compensation of senior management for both external professionals and family members included a variable performance-linked component. The median variable component was 50%, rising to as high as 90% in some cases. This appears to link management remuneration to company performance, although, as details of compensation plans or process are not made public, it remains impossible to conclude whether compensation arrangements for family executives are appropriate.

11 SEBI suggests that commentary on this be included in the mandatory corporate governance section of the annual report

9 October 2007 Special Comment Moody’s-ICRA Corporate Finance - Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

Special Comment Moody’s Corporate Finance

Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

Global experience suggests that family firms can be relatively conservative on executive pay. The downside of this may be difficulty in attracting the highest quality executive talent – particularly if there is little prospect of the top jobs going outside the family. However, this may be less of a problem in India, at least for high-profile family companies. There is some evidence that the hunt for talent has led to very material increases in compensation packages; while at the same time, it remains prestigious for professional managers to work for such companies.

Governance challenges for Indian family-controlled corporates

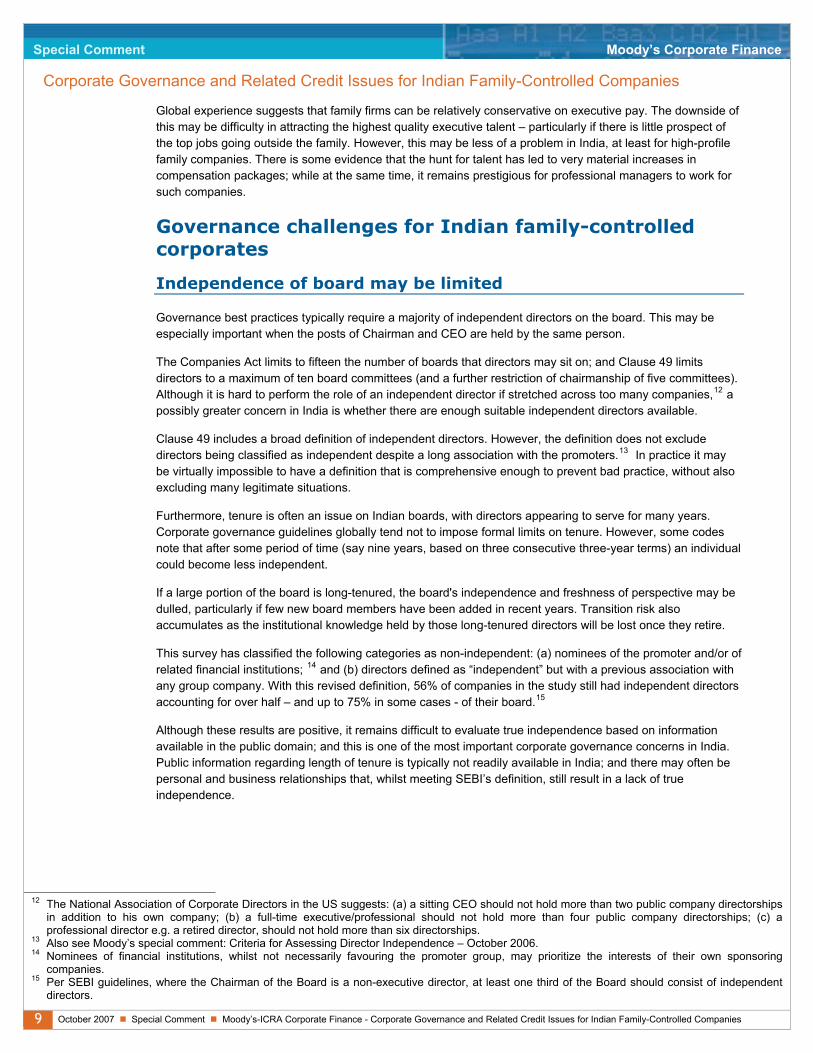

Independence of board may be limited

Governance best practices typically require a majority of independent directors on the board. This may be especially important when the posts of Chairman and CEO are held by the same person.

The Companies Act limits to fifteen the number of boards that directors may sit on; and Clause 49 limits directors to a maximum of ten board committees (and a further restriction of chairmanship of five committees). Although it is hard to perform the role of an independent director if stretched across too many companies,12 a possibly greater concern in India is whether there are enough suitable independent directors available.

Clause 49 includes a broad definition of independent directors. However, the definition does not exclude directors being classified as independent despite a long association with the promoters.13 In practice it may be virtually impossible to have a definition that is comprehensive enough to prevent bad practice, without also excluding many legitimate situations.

Furthermore, tenure is often an issue on Indian boards, with directors appearing to serve for many years. Corporate governance guidelines globally tend not to impose formal limits on tenure. However, some codes note that after some period of time (say nine years, based on three consecutive three-year terms) an individual could become less independent.

If a large portion of the board is long-tenured, the board's independence and freshness of perspective may be dulled, particularly if few new board members have been added in recent years. Transition risk also accumulates as the institutional knowledge held by those long-tenured directors will be lost once they retire.

This survey has classified the following categories as non-independent: (a) nominees of the promoter and/or of related financial institutions; 14 and (b) directors defined as “independent” but with a previous association with any group company. With this revised definition, 56% of companies in the study still had independent directors accounting for over half – and up to 75% in some cases - of their board.15

Although these results are positive, it remains difficult to evaluate true independence based on information available in the public domain; and this is one of the most important corporate governance concerns in India. Public information regarding length of tenure is typically not readily available in India; and there may often be personal and business relationships that, whilst meeting SEBI’s definition, still result in a lack of true independence.

12 The National Association of Corporate Directors in the US suggests: (a) a sitting CEO should not hold more than two public company directorships

in addition to his own company; (b) a full-time executive/professional should not hold more than four public company directorships; (c) a professional director e.g. a retired director, should not hold more than six directorships.

13 Also see Moody’s special comment: Criteria for Assessing Director Independence – October 2006. 14 Nominees of financial institutions, whilst not necessarily favouring the promoter group, may prioritize the interests of their own sponsoring

companies. 15 Per SEBI guidelines, where the Chairman of the Board is a non-executive director, at least one third of the Board should consist of independent

directors.

10 October 2007 Special Comment Moody’s-ICRA Corporate Finance - Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

Special Comment Moody’s Corporate Finance

Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

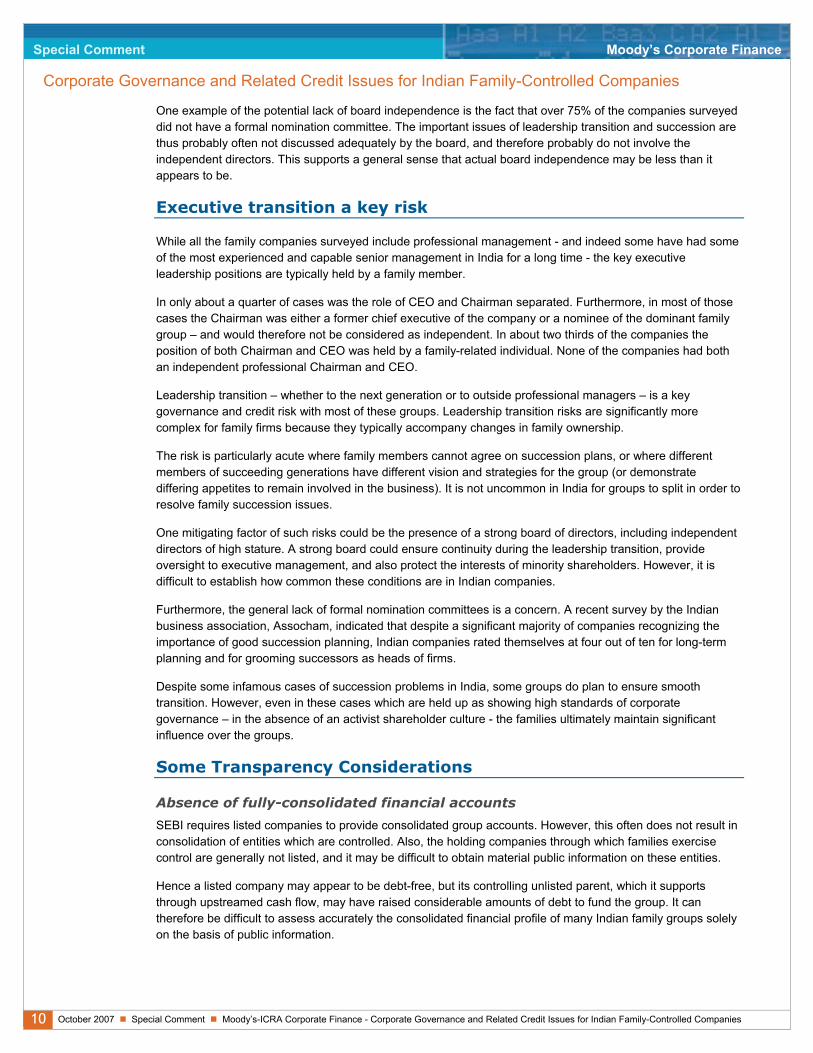

One example of the potential lack of board independence is the fact that over 75% of the companies surveyed did not have a formal nomination committee. The important issues of leadership transition and succession are thus probably often not discussed adequately by the board, and therefore probably do not involve the independent directors. This supports a general sense that actual board independence may be less than it appears to be.

Executive transition a key risk

While all the family companies surveyed include professional management - and indeed some have had some of the most experienced and capable senior management in India for a long time - the key executive leadership positions are typically held by a family member.

In only about a quarter of cases was the role of CEO and Chairman separated. Furthermore, in most of those cases the Chairman was either a former chief executive of the company or a nominee of the dominant family group – and would therefore not be considered as independent. In about two thirds of the companies the position of both Chairman and CEO was held by a family-related individual. None of the companies had both an independent professional Chairman and CEO.

Leadership transition – whether to the next generation or to outside professional managers – is a key governance and credit risk with most of these groups. Leadership transition risks are significantly more complex for family firms because they typically accompany changes in family ownership.

The risk is particularly acute where family members cannot agree on succession plans, or where different members of succeeding generations have different vision and strategies for the group (or demonstrate differing appetites to remain involved in the business). It is not uncommon in India for groups to split in order to resolve family succession issues.

One mitigating factor of such risks could be the presence of a strong board of directors, including independent directors of high stature. A strong board could ensure continuity during the leadership transition, provide oversight to executive management, and also protect the interests of minority shareholders. However, it is difficult to establish how common these conditions are in Indian companies.

Furthermore, the general lack of formal nomination committees is a concern. A recent survey by the Indian business association, Assocham, indicated that despite a significant majority of companies recognizing the importance of good succession planning, Indian companies rated themselves at four out of ten for long-term planning and for grooming successors as heads of firms.

Despite some infamous cases of succession problems in India, some groups do plan to ensure smooth transition. However, even in these cases which are held up as showing high standards of corporate governance – in the absence of an activist shareholder culture - the families ultimately maintain significant influence over the groups.

Some Transparency Considerations

Absence of fully-consolidated financial accounts

SEBI requires listed companies to provide consolidated group accounts. However, this often does not result in consolidation of entities which are controlled. Also, the holding companies through which families exercise control are generally not listed, and it may be difficult to obtain material public information on these entities.

Hence a listed company may appear to be debt-free, but its controlling unlisted parent, which it supports through upstreamed cash flow, may have raised considerable amounts of debt to fund the group. It can therefore be difficult to assess accurately the consolidated financial profile of many Indian family groups solely on the basis of public information.

11 October 2007 Special Comment Moody’s-ICRA Corporate Finance - Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

Special Comment Moody’s Corporate Finance

Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

Disclosure issues

Listed companies (possibly driven by SEBI’s regulations) have generally improved disclosures. SEBI has made the following mandatory for listed companies:

Related-party transactions

Appointment and remuneration of directors

MD&A

Quarterly results and presentations to be posted on the company’s web-site

Related-Party Transactions

Clause 49 requires that all related-party transactions must be considered by the company’s audit committee, and should also be disclosed in the annual report.

However, the adequacy of disclosure on such transactions, particularly for family businesses, is an important governance concern in India.

It can be difficult to truly know the level of promoter/family control, partly due to the complex group structures. This makes the extent of related-party transactions difficult to evaluate. A material difference between IFRS and Indian Gaap is the non-inclusion as a related party of entities in which either key management personnel or promoters exercise significant control or voting power.

12 October 2007 Special Comment Moody’s-ICRA Corporate Finance - Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

Special Comment Moody’s Corporate Finance

Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

Website

For additional information, please see the company’s websites: www.moodyscom, www.icraratings.com

MOODY’S has provided links or references to third party World Wide Websites or URLs (“Links or References”) solely for your convenience in locating related information and services. The websites reached through these Links or References have not necessarily been reviewed by MOODY’S, and are maintained by a third party over which MOODY’S exercises no control. Accordingly, MOODY’S expressly disclaims any responsibility or liability for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on any third party web site accessed via a Link or Reference. Moreover, a Link or Reference does not imply an endorsement of any third party, any website, or the products or services provided by any third party.

Moody’s Related Research

Special Comment: Family-Owned Corporates in the GCC – April 2007 (102897)

Criteria for Assessing Director Independence – October 2006 (100302)

Moody’s Findings on Corporate Governance in the United States and Canada – October 2004 (89113)

Expanding U.S. Shareholder Power Increases Potential Credit Risk to Bondholders – June 2007 (103598)

Short-Term Shareholder Activists Degrade Creditworthiness of Rated Companies – June 2007 (103433)

ICRA’s Related Research

Corporate Governance Methodology – July 2004

Corporate Governance Survey – February 2004

Emerging board practices – February 2005

To access any of these reports, click on the entry above. Note that these references are current as of the date of publication of this report and that more recent reports may be available. All research may not be available to all clients.

13 October 2007 Special Comment Moody’s-ICRA Corporate Finance - Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

Special Comment Moody’s Corporate Finance

Corporate Governance and Related Credit Issues for Indian Family-Controlled Companies

© Copyright 2007, Moody's Investors Service, Inc. and/or its licensors and affiliates including Moody's Assurance Company, Inc. (together, "MOODY'S") and/or ICRA Limited and/or its licensors and affiliates (together, "ICRA"). All rights reserved.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY COPYRIGHT LAW AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY'S AND ICRA'S PRIOR WRITTEN CONSENT. All information contained herein is obtained by MOODY'S and ICRA from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, such information is provided "as is" without warranty of any kind and MOODY'S and ICRA, in particular, make no representation or warranty, express or implied, as to the accuracy, timeliness, completeness, merchantability or fitness for any particular purpose of any such information. Under no circumstances shall MOODY'S or ICRA have any liability to any person or entity for (a) any loss or damage in whole or in part caused by, resulting from, or relating to, any error (negligent or otherwise) or other circumstance or contingency within or outside the control of MOODY'S or ICRA or any of their directors, officers, employees or agents in connection with the procurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any such information, or (b) any direct, indirect, special, consequential, compensatory or incidental damages whatsoever (including without limitation, lost profits), even if MOODY'S or ICRA are advised in advance of the possibility of such damages, resulting from the use of or inability to use, any such information. The credit ratings and financial reporting analysis observations, if any, constituting part of the information contained herein are, and must be construed solely as, statements of opinion and not statements of fact or recommendations to purchase, sell or hold any securities. NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY'S OR ICRA IN ANY FORM OR MANNER WHATSOEVER. Each rating or other opinion must be weighed solely as one factor in any investment decision made by or on behalf of any user of the information contained herein, and each such user must accordingly make its own study and evaluation of each security and of each issuer and guarantor of, and each provider of credit support for, each security that it may consider purchasing, holding or selling.

MOODY'S hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MOODY'S have, prior to assignment of any rating, agreed to pay to MOODY'S for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,400,000. Moody's Corporation (MCO) and its wholly-owned credit rating agency subsidiary, Moody's Investors Service (MIS), also maintain policies and procedures to address the independence of MIS's ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually on Moody's website at www.moodys.com under the heading "Shareholder Relations - Corporate Governance - Director and Shareholder Affiliation Policy."

ICRA is an associate of MOODY'S. MOODY'S has a minority share ownership stake in ICRA.

To order reprints of this report (100 copies minimum), please call 1.212.553.1658. Report Number: 105269

Authors Editor Senior Production Associate Chetan Modi Mark Watson Anjan Ghosh

Jonathan Barlow

Wing Chan