soa-soa experience study - iltciiltciconf.org/2015/index_htm_files/soa-soaexperiencestudy.pdf ·...

TRANSCRIPT

Actuarial

2000-2011 SOA LTC Intercompany

Experience StudyExperience StudyMarch 22, 2015

Jon Prince Great American Insurance GroupJon Prince, Great American Insurance GroupMatthew Morton, LTCG

Ben Williams, Towers Watson,

Agenda

• Introductions• Goals & Project PlanGoals & Project Plan• Data gathering

A t f D t• Assessment of Data• Morbidity experience• Experience table: Model build

SOA Experience Study 2

Introductions

Multi-faceted team• Society of Actuaries (sponsor)Society of Actuaries (sponsor)• Steering Committee

T W t• Towers Watson• LIMRA• MIB

SOA Experience Study 3

Goals and Project Plan

• Goals of this study:– Obtain, review and model morbidity Ob a , e e a d ode o b d y

experience for long term care insurance– Use the most complete datap– Provide aggregate databases to the industry– Build experience tableBuild experience table

SOA Experience Study 4

Data gathering

• Data gathering (Steering Committee)– Data request sent to top carriers in USa a eques se o op ca e s US– Conversations with carriers– Policy history filePolicy history file– Claim file– 22 companies submitted full or partial data– 22 companies submitted full or partial data– Exposure period: 2000-2011

Data scrubbing (MIB & LIMRA)• Data scrubbing (MIB & LIMRA)– Valid data fields

SOA Experience Study 5

Data Assessment

• Data Assessment (Towers Watson)– Created summariesC ea ed su a es

• Policy history• Policyholder characteristics• Benefit characteristics

– Confirmatory calls with participants– Identified key data items & find companies

with sufficient data quality to analyze

SOA Experience Study 6

Data Assessment

• For each morbidity component– Identified key data fields (approximately 12 de ed ey da a e ds (app o a e y

characteristics)– Participants with sufficient quality and complete p q y p

data were selected– Analyzed variety of remaining data to ensure

good mixture of policyholder and benefit characteristics

• Maximizing data while minimizing unknowns

SOA Experience Study 7

Morbidity Experience Review

• Reviewed each key morbidity experience metric– Incidencec de ce– Claim termination– Claim utilizationClaim utilization

• Reviewed for reasonableness & trendsC i t t d fi iti f i l i• Consistent definition of unique claim:– Payment made and– Multiple claims for single policyholder combined if

service dates are within 6 months

SOA Experience Study 8

Morbidity Experience Review

• Incidence– Active & total life incidencec e & o a e c de ce– Reviewed

• Rates in aggregategg g• Rates by age, gender, marital status, etc

– Analyzed results by company and y y p ycharacteristics

• Total exposure: 15 million life yearsp y• Claim count: over 200k

SOA Experience Study 9

Morbidity Experience Review

• Claim terminations– Total terminations & disabled mortalityo a e a o s & d sab ed o a y– 4 million years of disabled exposure– Claim counts: 200kClaim counts: 200k

• Claim utilizationGPO and unknown benefit inflation excluded– GPO and unknown benefit inflation excluded as benefit schedules were not providedResulting database has over $7 billion of– Resulting database has over $7 billion of claims paid

SOA Experience Study 10

Morbidity Experience Review

• Aggregate databases– Separate tables for each morbidity componentSepa a e ab es o eac o b d y co po e– Publicly available pivot tables that allow user to

manipulate data and analyze results at granular p y glevel

– Ability to view results more dynamically than static tables

– Confidentiality of data from participants– No manipulation to scale data

SOA Experience Study 11

Experience Table

• Goal: Develop experience table based on aggregated databases for:gg g– Incidence, claim termination, utilization

• Mixture ofMixture of – Predictive modeling: Generalized linear

modeling (GLM) used to determine baselinemodeling (GLM) used to determine baseline rate and factors

– Business knowledge: used to verify causalBusiness knowledge: used to verify causal relationships; feedback cycle with committee

SOA Experience Study 12

Experience Table

• Predictive modeling background:– Is the process of developing a model that estimates

the outcome of a given process– Uses statistical tests to determine the factors, and

which combinations of factors impact the processwhich combinations of factors, impact the process– Separates signal from noise in actual experience

• Predictive models are used to make• Predictive models are used to make projections of future results

SOA Experience Study 13

Experience Table

• GLM uses statistical methods to analyze data and determine relationshipsp

• Key metrics utilized include:– Chi-square:– Chi-square:– AIC (Akaike Information Criterion)

BIC (Bayesian Information Criterion)– BIC (Bayesian Information Criterion)

SOA Experience Study 14

Experience Table

• Claim incidence model:– Data drivena a d e– Multiplicative models

• Total lives• Active lives

– Base factor & vectors based on cell selection determine model output

SOA Experience Study 15

Experience Table

• Claim incidence model predictors:Incurred age Underwriting class– Incurred age

– Elimination periodBenefit period

– Underwriting class– Daily benefit

R i– Benefit period– Policy duration

M ti l t t

– Region– Tax Qualified status

C– Martial status– Underwriting type

– Coverage– Gender

SOA Experience Study 16

Experience Table

100

1.1Premium Class Relativities

801

1.05

es

40

60

0 9

0.95

Exps

oure

%

Rel

ativ

itie

200.85

0.9

00.8Preferred Standard Substandard

Premium Class

E Ob d R l ti iti

SOA Experience Study 17

Exposure Observed Relativities

Experience Table

100

1.1

Premium Class Relativities

80

1

1.05

s

40

60

0 9

0.95

Exps

oure

%

Rel

ativ

ities

200.85

0.9

00.8Preferred Standard Substandard

Premium Class

SOA Experience Study 18

Exposure Model Relativities

Experience Table

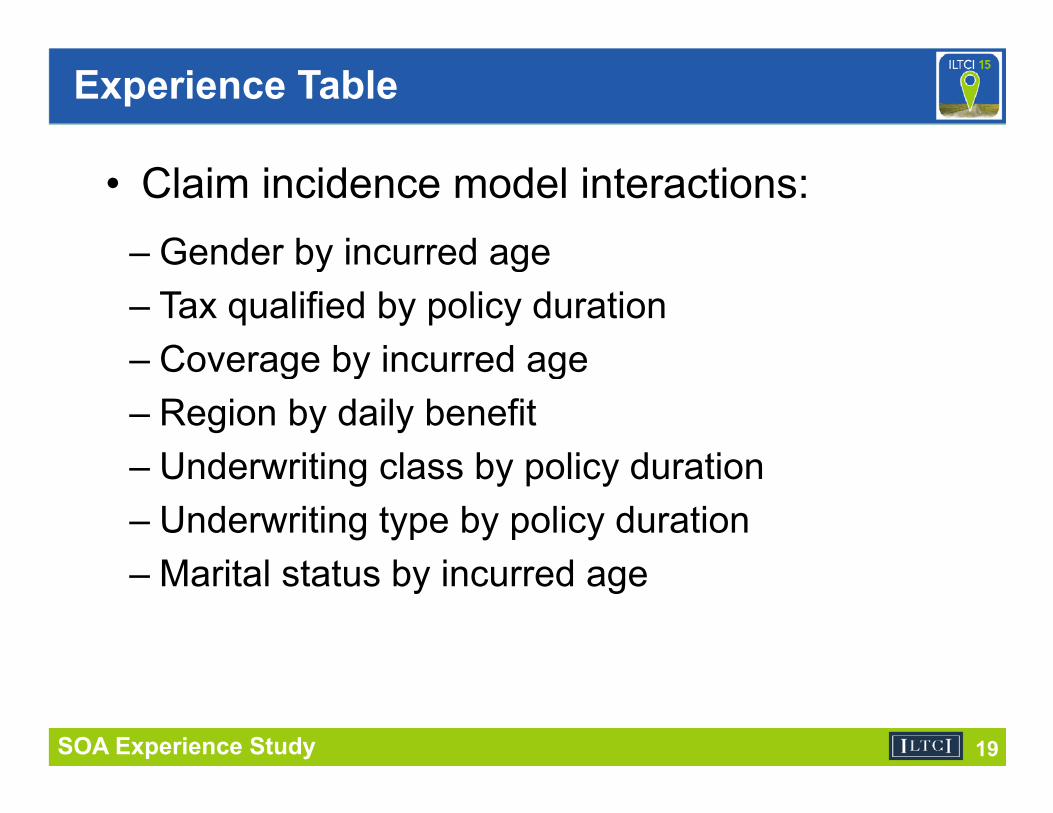

• Claim incidence model interactions:Gender by incurred age– Gender by incurred age

– Tax qualified by policy durationCoverage by incurred age– Coverage by incurred age

– Region by daily benefitU d iti l b li d ti– Underwriting class by policy duration

– Underwriting type by policy durationM it l t t b i d– Marital status by incurred age

SOA Experience Study 19

Experience Table

7

8

2.4

2.6Incurred Age interacted with Marital Status

5

6

7

1 8

2

2.2

es

3

4

1.4

1.6

1.8

Expo

sure

%

Rel

ativ

itie

1

2

0.8

1

1.2

00.6

35-

36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 9910

0+

Incurred Age

E M it l St t (M i d) M it l St t (Si l )

SOA Experience Study 20

Exposure Marital_Status (Married) Marital_Status (Single)

Experience Table

Example of model fit: by attained age8

Predicted Values - IncurredAge

6

7

9%

11%

4

5

5%

7%

2

3

1%

3%

0

1

-3%

-1%

5- 37 39 41 43 45 47 49 51 53 55 57 59 61 63 65 67 69 71 73 75 77 79 81 83 85 87 89 91 93 95 97 99

SOA Experience Study 21

35 3 3 4 4 4 4 4 5 5 5 5 5 6 6 6 6 6 7 7 7 7 7 8 8 8 8 8 9 9 9 9 9

Exposure Observed Average Fitted Average

Experience Table

Example of model fit: by policy duration

5%Predicted Values - DurYear

16

18

20

4%

5%

12

14

3%

6

8

10

1%

2% Exposure

Observed Average

Fitted Average

2

4

0%

SOA Experience Study 22

0-1%1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20+

Experience Table

Example of model fit: by issue age1414%

10

12

8%

10%

12%

6

8

4%

6%

8%

Exposure

4

6

0%

2%

4% Observed Average

Fitted Average

0

2

-4%

-2%

0%

- 7 9 3 5 7 9 3 5 7 9 3 5 7 9 3 5 7 9 3 +

SOA Experience Study 23

35-

37 39 41 43 45 47 49 51 53 55 57 59 61 63 65 67 69 71 73 75 77 79 81 83 85+

Experience Table

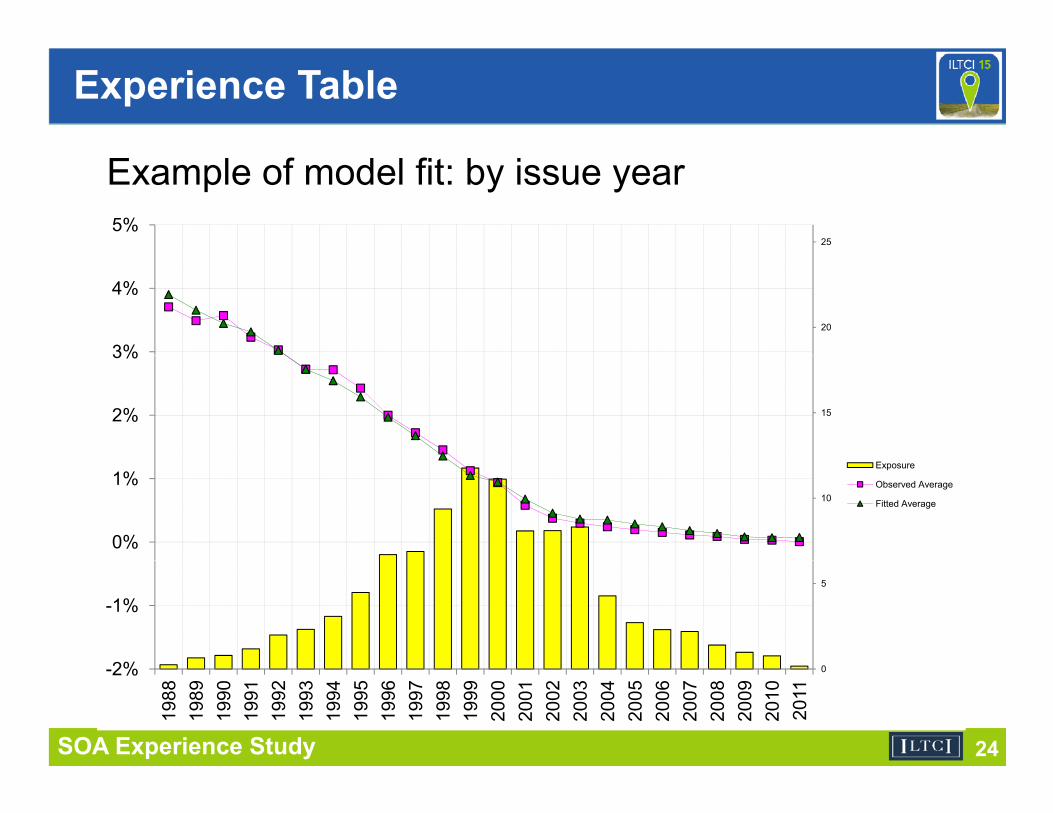

Example of model fit: by issue year25

5%

20

3%

4%

152%

3%

10

0%

1%Exposure

Observed Average

Fitted Average

5

2%

-1%

SOA Experience Study 24

0-2%

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

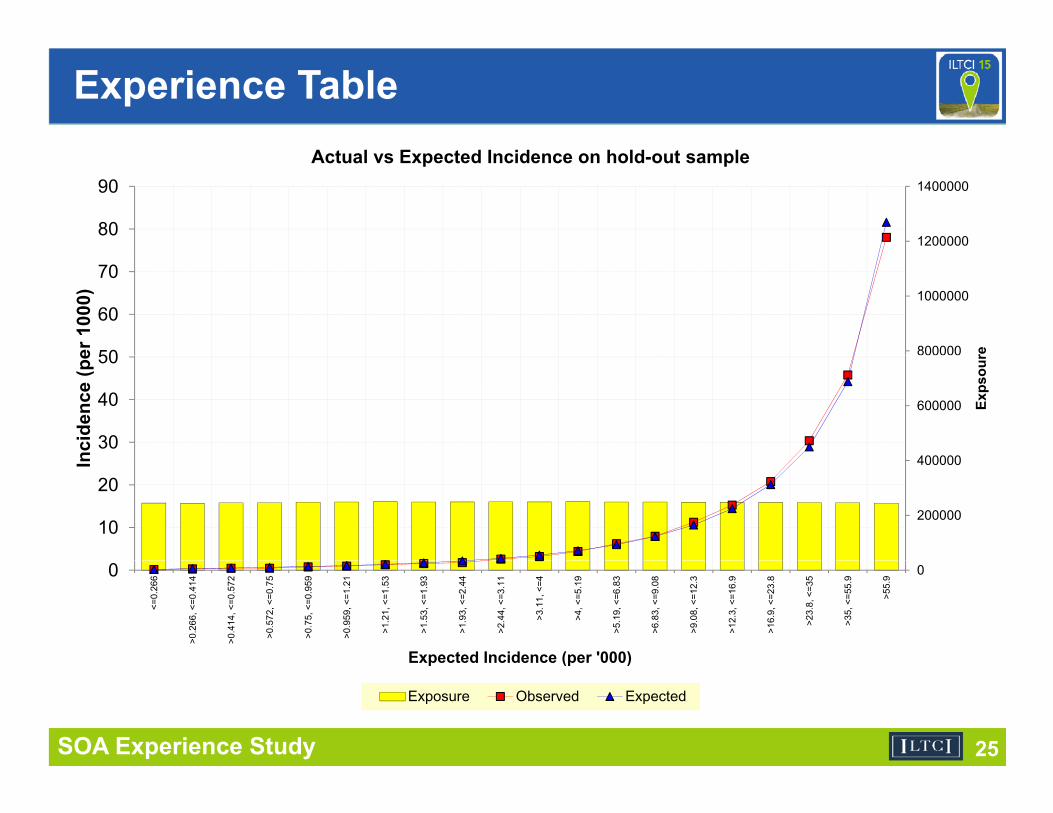

A t l E t d I id h ld t l

Experience Table

1200000

1400000

80

90Actual vs Expected Incidence on hold-out sample

800000

1000000

50

60

70

reer 1

000)

400000

600000

30

40

50

Exps

our

ncid

ence

(pe

200000

400000

10

20

In

00

<=0.

266

>0.2

66, <

=0.4

14

>0.4

14, <

=0.5

72

>0.5

72, <

=0.7

5

>0.7

5, <

=0.9

59

>0.9

59, <

=1.2

1

>1.2

1, <

=1.5

3

>1.5

3, <

=1.9

3

>1.9

3, <

=2.4

4

>2.4

4, <

=3.1

1

>3.1

1, <

=4

>4, <

=5.1

9

>5.1

9, <

=6.8

3

>6.8

3, <

=9.0

8

>9.0

8, <

=12.

3

>12.

3, <

=16.

9

>16.

9, <

=23.

8

>23.

8, <

=35

>35,

<=5

5.9

>55.

9

Expected Incidence (per '000)

SOA Experience Study 25

p (p )

Exposure Observed Expected

Experience Table

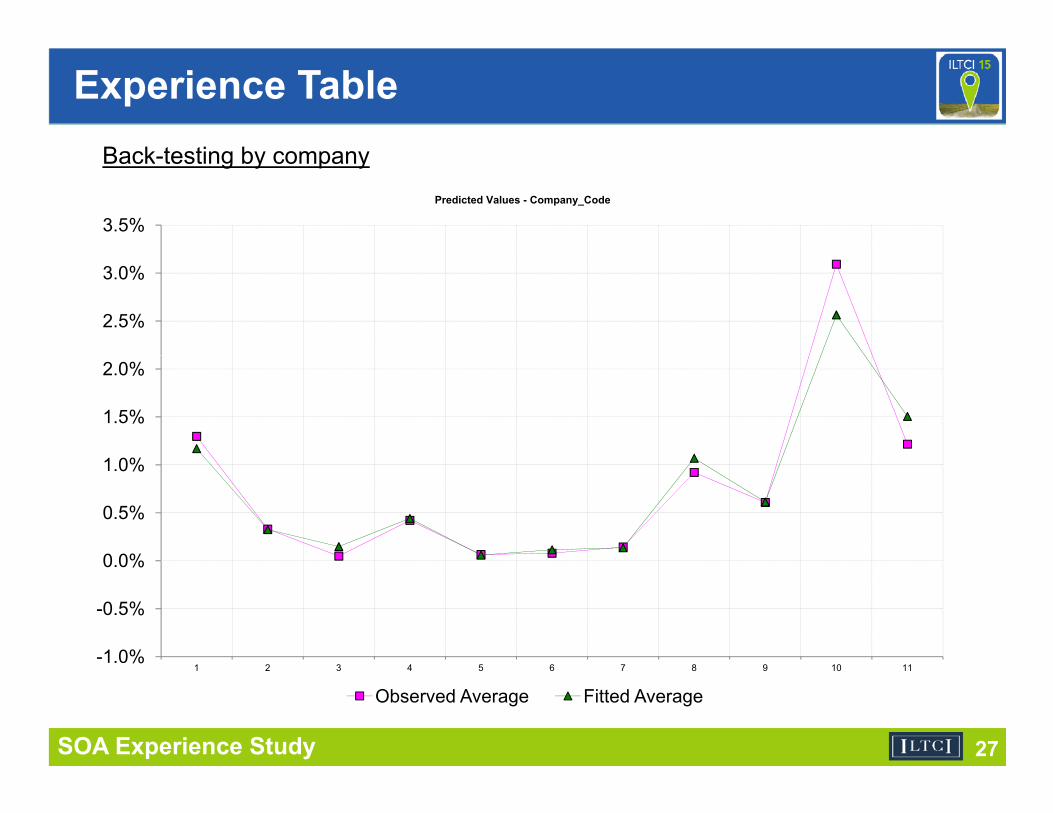

Back-testing by company• This graph shows a comparison of observed vs.

di t d i id t b i th t dpredicted incidence rates by company in the study• While the factor “company” is not in the model,

observed and predicted are closeobserved and predicted are close• This indicates that most differences between

observed incidence rates can be attributed to differences in composition of business (age, gender, marital status, duration, underwriting type etc.) among the companiesamong the companies

• Note that company codes have been anonymized

SOA Experience Study 26

Experience TableB k t ti b

3.5%Predicted Values - Company_Code

Back-testing by company

2.5%

3.0%

1 0%

1.5%

2.0%

0 0%

0.5%

1.0%

-1.0%

-0.5%

0.0%

SOA Experience Study 27

%1 2 3 4 5 6 7 8 9 10 11

Observed Average Fitted Average

Experience Table

Other models to be released• Claim terminationC a e a o

– Total termination with diagnosis & claim type– Total termination without diagnosis or claim type– Termination due to death with diagnosis & claim type– Termination due to death without diagnosis or claim type

• Claim utilization– With diagnosis & claim type

Wi h di i l i– Without diagnosis or claim type

SOA Experience Study 28

Benefit period factor analysis

• Impact of benefit period on incidence was inconsistent with expectation

• Slightly higher incidence for limited BP – (less than 1.5% for active life model)

• Significant discussion / investigation about relationship

• Note: for claim termination and claim utilization, – lifetime BP yields higher morbidity costs

SOA Experience Study 29

Benefit period factor analysis

70

80

5%

6%

50

60

4%

30

40

2%

3%

10

20

1%

2%

0-1%0-1 1-2 2-3 3-4 4-5 5-6 6+ Lifetime

E Ob d A Fitt d A

SOA Experience Study 30

Exposure Observed Average Fitted Average

Benefit period factor analysis

4.0%

4.5%

3.0%

3.5%

2.0%

2.5% Company 1Company 2Company 3C 4

1.0%

1.5%Company 4

0.0%

0.5%

SOA Experience Study 31

<3 3-4 4-5 5+ Lifetime

Benefit period factor analysis

8%

9%

10%

Limited vs Lifetime Incidence Rate

6%

7%

8% Limited vs Lifetime Incidence Rate by Attained Age

4%

5%

1%

2%

3%

0%

1%

65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91

Lif ti A t l Li it d A t l

SOA Experience Study 32

Lifetime Actual Limited Actual

Benefit period factor analysis

3.0%

3.5%

Limited vs Lifetime Incidence Rate

2.0%

2.5%

Limited vs Lifetime Incidence Rate by Policy Duration

1.5%

2.0%

0.5%

1.0%

0.0%1 2 3 4 5 6 7 8 9 10 11 12 13 14

Limited Actual Lifetime Actual

SOA Experience Study 33

Limited Actual Lifetime Actual

Benefit period factor analysis

3.0%

3.5%

Limited vs Lifetime Incidence Rate

2 0%

2.5%

Limited vs Lifetime Incidence Rate by Policy Duration

1.5%

2.0%

0.5%

1.0%

0.0%1 2 3 4 5 6 7 8 9 10 11 12 13 14

Limited Actual Limited Model Lifetime Actual Lifetime Model

SOA Experience Study 34

Limited Actual Limited Model Lifetime Actual Lifetime Model

Experience Table

Potential Drivers• Other factors account for differencesO e ac o s accou o d e e ces• Coding of BP data received (internal vs external)• Other factors not considered Examples couldOther factors not considered. Examples could

include:– Company sales distribution modelp y– Company specific underwriting guidelines– Mixture of companies included in study– etc

SOA Experience Study 35

Special Thanks

Steering Committee• Sheryl Babcock• Barry Koklefsky

Society of Actuaries• Cynthia MacDonald• Muz Waheedy y

• Susan Oberman Smith• Eric Perry• Eric Poirier

• Korrel Rosenberg• Erika Schulty

• Eric Poirier• Jon Prince• Steve Schoonveld

M Sh h• Maureen Shaughnessy• Bruce Stahl• Kevin Waterman• Perry Wiseblatt• Bob Yee

SOA Experience Study 36

Special Thanks - Participants

• Allianz• Berkshire Life

C lP

• United of Omaha• New York Life

N th t M t l• CalPers• Continental Casualty• Fortis

• Northwestern Mutual• Penn Treaty• PrudentialFortis

• Genworth Financial• John Hancock

Prudential• Senior Health• State Farm

• Lincoln Benefit Life• Mass Mutual

M Lif

• Thrivent AAL• Thrivent LB

T i A• MetLife• Mutual of Omaha

• Transamerica – Aegon• UNUM

SOA Experience Study 37

Wrap Up

• Questions?

Location of Aggregate Database Reporthttps://soa org/Research/Experience Study/Ltc/researchhttps://soa.org/Research/Experience-Study/Ltc/research-ltc-study-2000-11-aggregrated.aspx

SOA Experience Study 38