smart cars: who has the head start? -...

TRANSCRIPT

See important disclosures, including any required research certifications, beginning on page 70

26 June 2015

Smart cars: who has the head start?

• Smart cars now look set to hit the roads from 2025 • Over time we foresee the auto OEMs integrating the smart-car

value chain, led by Toyota, then GM and Ford • In order, our preferred Pan-Asia smart-car plays today are

Toyota, Denso and Hyundai Mobis

Pan-Asia Autos

Consumer Discretionary / Pan Asia

How do we justify our view?How do we justify our view?

Pan-Asia Autos 26 June 2015

- 2 -

Contents

Smart cars: changing the landscape ............................................................................................ 8

What will be the next smart device? ........................................................................................ 8

Smart cars: the industry’s next response to consumer needs ................................................ 10

What is a smart car? ................................................................................................................ 11

When will self-driving cars take to the roads? ....................................................................... 13

Smart-car market outlook more promising than ever ........................................................... 15

Smart-car market: OEM-leading value chain established .................................................... 20

Korea’s smart-car industry: currently behind the curve ........................................................ 27

Korea’s smart-car industry: who are the major beneficiaries? ............................................. 29

Valuations and recommendations ......................................................................................... 30

Risks to our investment case ................................................................................................. 38

Appendices ............................................................................................................................. 39

Company Section

Toyota Motor ...........................................................................................................................41

Denso ......................................................................................................................................45

Hyundai Mobis ....................................................................................................................... 49

Hyundai Motor ........................................................................................................................ 53

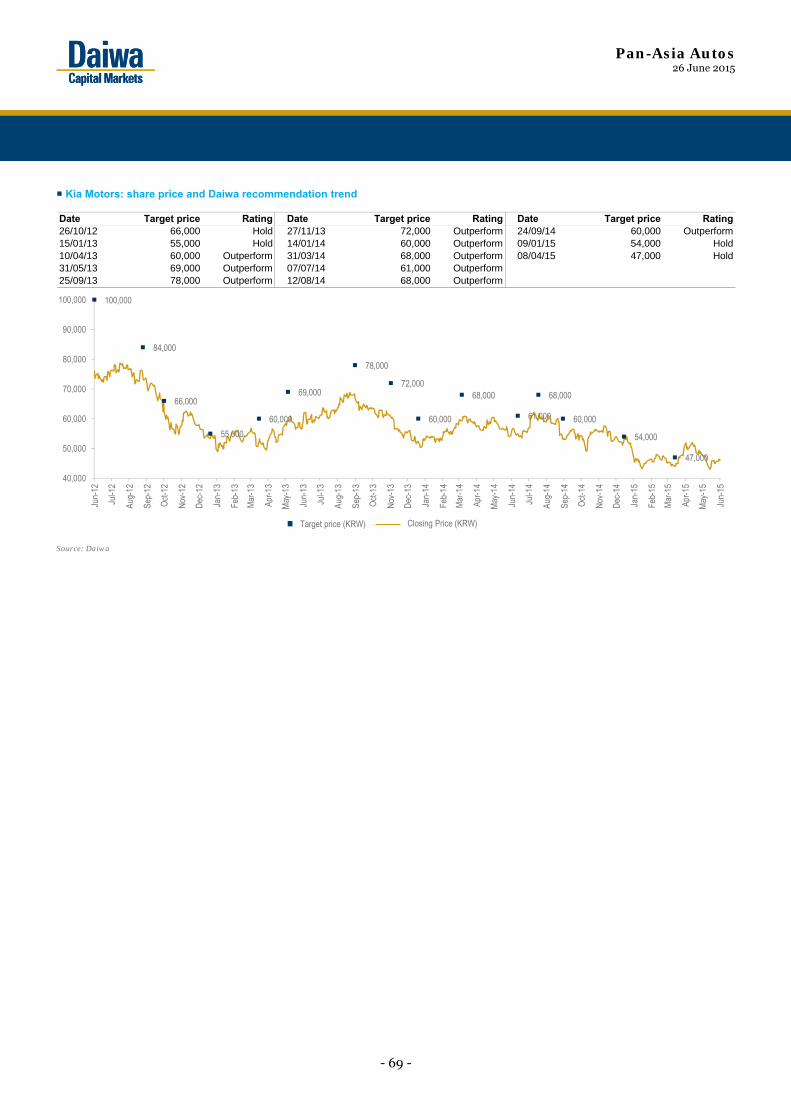

Kia Motors ...............................................................................................................................59

See important disclosures, including any required research certifications, beginning on page 70

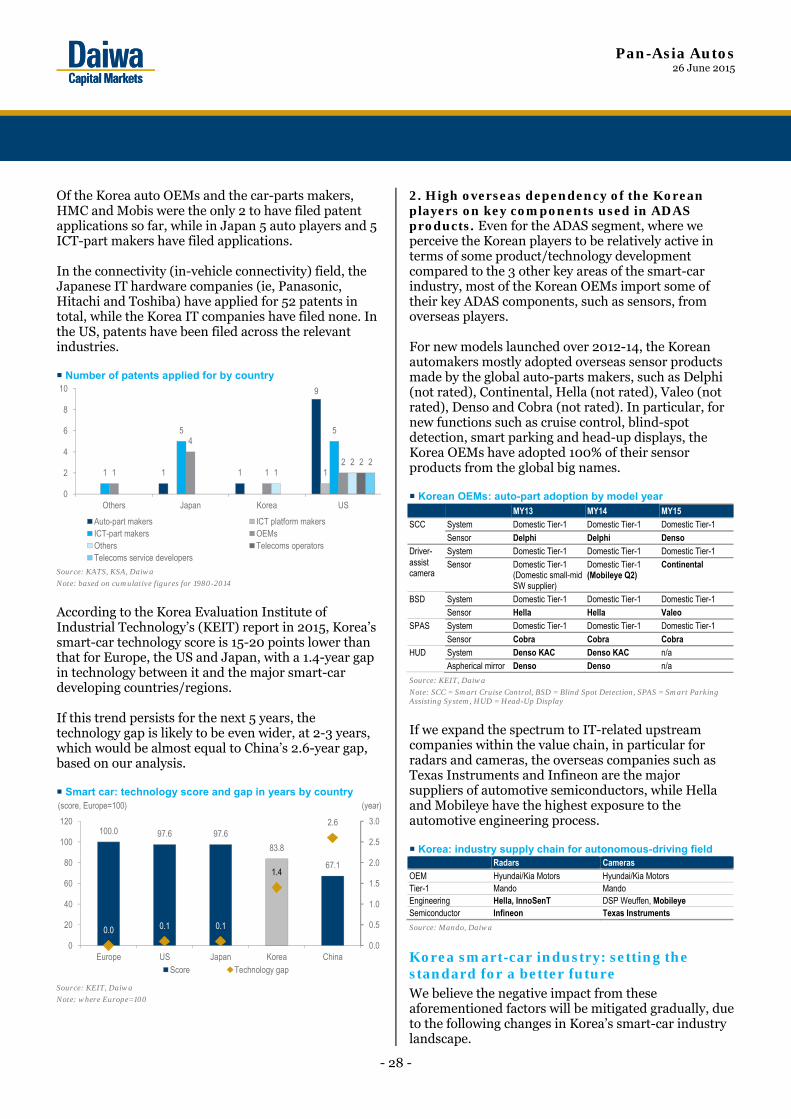

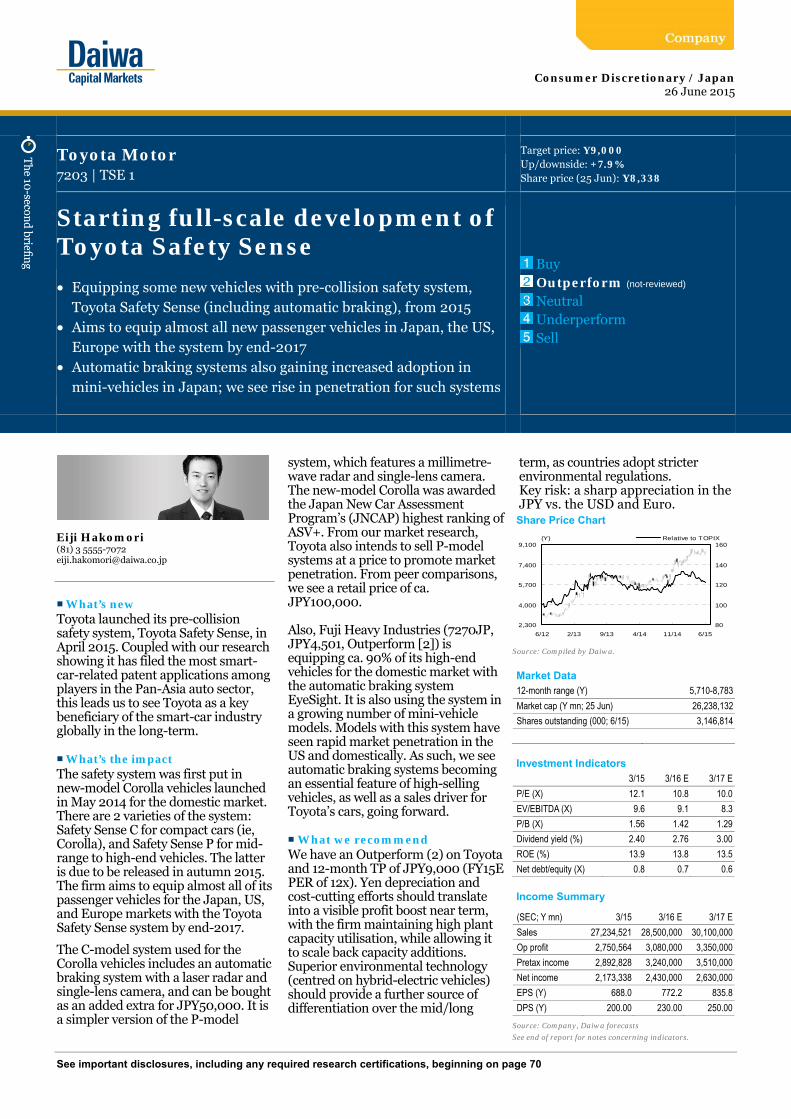

It’s been a year since our first report on the Advanced Driver Assistance market, and since then we have seen the global auto players (including the Pan-Asia auto OEMs and core-parts makers) unveil a slew of systems/parts/platforms and prototypes. In this report we assess which companies are the best placed to write the next chapters in the rapidly evolving smart-car story. ■ What's the impact We believe that cars are set to undergo dramatic changes akin to those seen in the smart-device segment since 2009. Allowing for technical hurdles to be overcome and tougher safety regulations to be met, we expect the smart-car market to see a CAGR of 11.5% over 2019-25E, reaching USD150.5bn in 2025. While Apple revolutionised smartphones in 2009 with its technologically more advanced iPhone, forming the grounds for today’s industry

landscape, we see the existing smart-car parts and auto makers as sufficiently well armed to withstand and ultimately defeat new entrants. Smart cars should have 4 key elements: 1) in-vehicle infotainment, 2) telematics, 3) vehicle-to-X communication, and 4) autonomous driving. To help the auto players tick these boxes, we expect even more cross-industry collaboration (eg, the auto OEMs and the ICT players) and government-led initiatives. In the run-up to 2025, we expect the auto-parts makers to set the pace in smart cars, backed by their overall competitive advantages in automotive electronics. Beyond that, we look for the auto OEMs to take the baton, as we expect them to integrate the smart-car value chain and absorb the requisite technology. ■ What we recommend Among our Pan-Asia coverage, we highlight 3 smart-car beneficiaries. First, we reiterate Toyota (7203 JP, JPY8,338, Outperform [2]) as our top pick on 12-month and 3-year views, as we believe: 1) it has a more favourable earnings-revision cycle and cash-management policy than the Korea automakers, and 2) it has a clear competitive edge in smart cars. Second, we like Denso (6902 JP, JPY6,310, Outperform [2]), which we foresee benefiting the most among the major auto-parts makers in the Pan-Asia region from the smart-car theme thanks to its prowess in sensors.

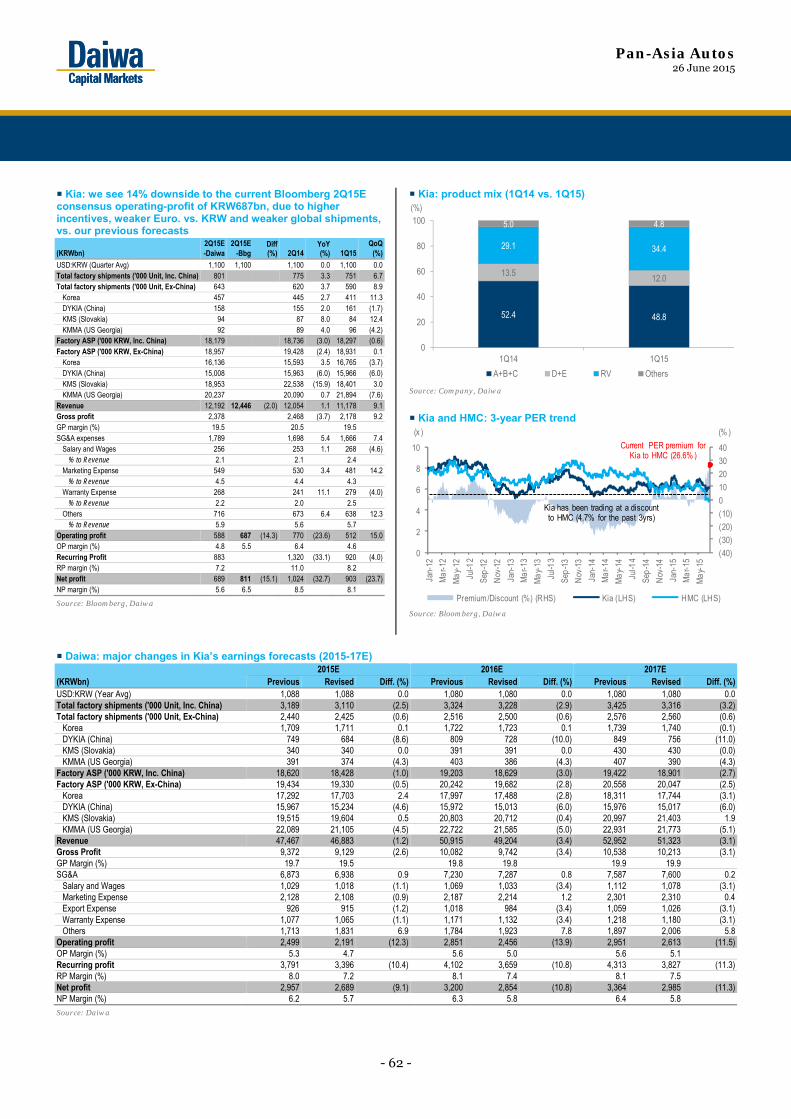

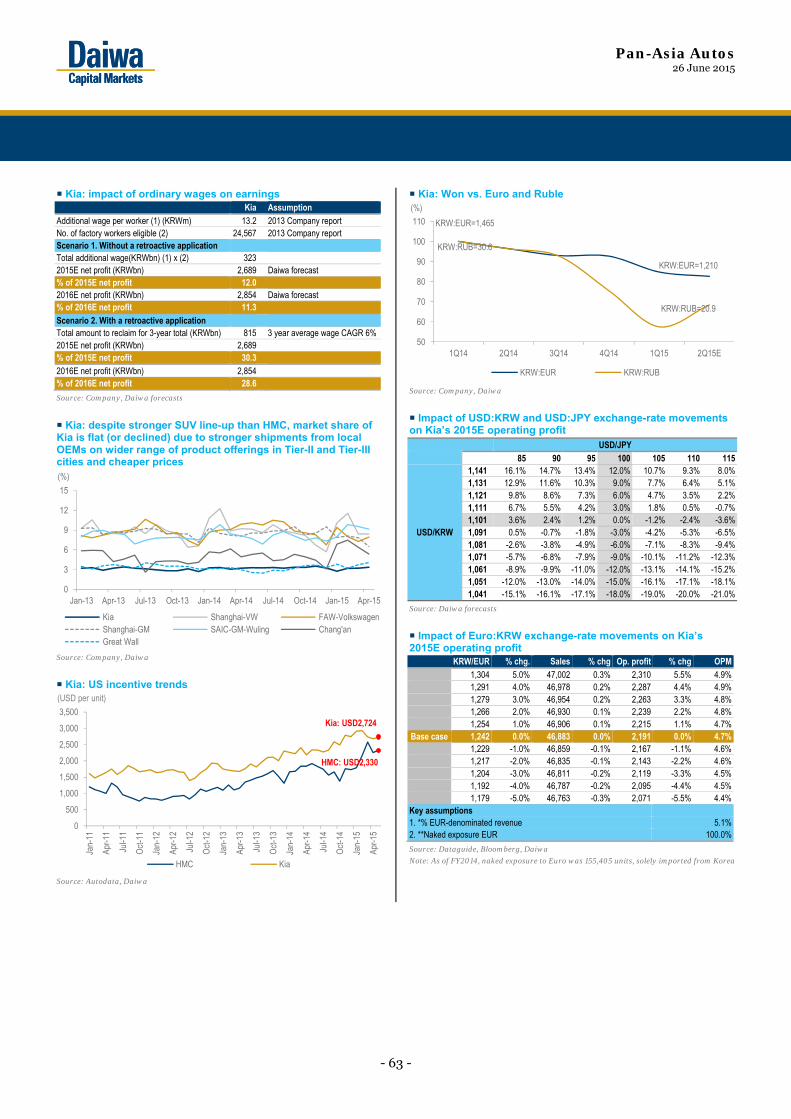

Third is Hyundai Mobis (Mobis; 012330 KS, KRW208,000, Buy [1]), for its more defensive nature relative to the Korea OEMs and its appealing valuation on a 12-month view. Its competitive edge in ADAS should be a big plus as the smart-car story unfolds. On the other hand, we lower our 12-month DCF/PER-based target prices for Hyundai Motor Company (HMC; 005380KS, KRW132,000, Outperform [2]) and Kia Motors (Kia; 000270KS, KRW45,950, Hold [3]) to KRW145,000 (from KRW150,000) and KRW43,000 (from KRW47,000), due to their weaker competitive advantage in smart cars relative to their global peers. For Kia, we revise down 2015-17E EPS to factor in higher incentives, global shipments and marketing expenses vs. our prior forecasts. ■ How we differ Reflecting our upbeat stance on Toyota and Denso, our FY15-16E EPS forecasts for both companies are higher than the consensus.

26 June 2015

Smart cars: who has the head start?

• Smart cars now look set to hit the roads from 2025 • Over time we foresee the auto OEMs integrating the smart-car

value chain, led by Toyota, then GM and Ford • In order, our preferred Pan-Asia smart-car plays today are

Toyota, Denso and Hyundai Mobis

Pan-Asia Autos

Eiji Hakomori (81) 3 5555-7072 [email protected]

Key stock calls

New Prev.

Toyota (7203 JP) RatingTarget Upside

Outperform 9,000

7.9%

Outperform9,000

Source: Daiwa forecasts.

Consumer Discretionary / Pan Asia

Sung Yop Chung(82) 2 787 [email protected]

Hyundai Mobis (012330 KS)Rating Buy BuyTarget 250,000 250,000Upside 20.2%

Hyundai Motor (005380 KS)Rating Outperform OutperformTarget 145,000 150,000Upside 9.8%

How do we justify our view?How do we justify our view?

Pan-Asia Autos 26 June 2015

- 4 -

How do we justify our view?

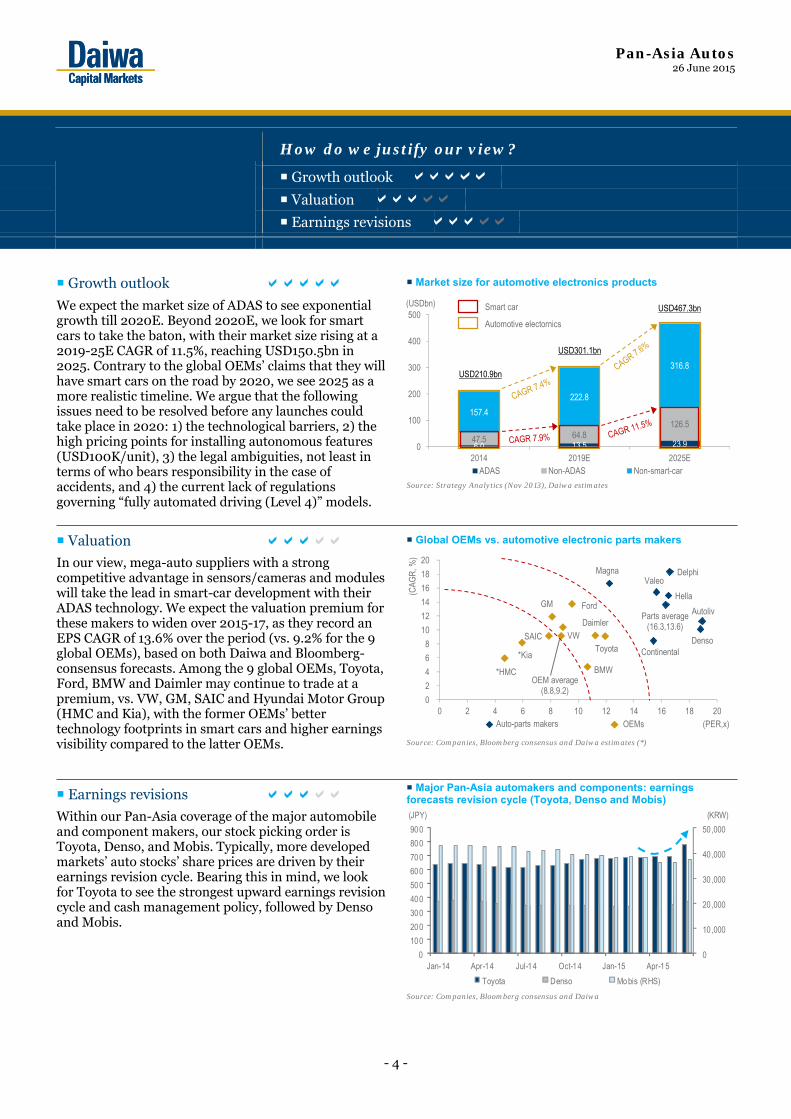

Growth outlook

Valuation

Earnings revisions

Growth outlook Market size for automotive electronics products

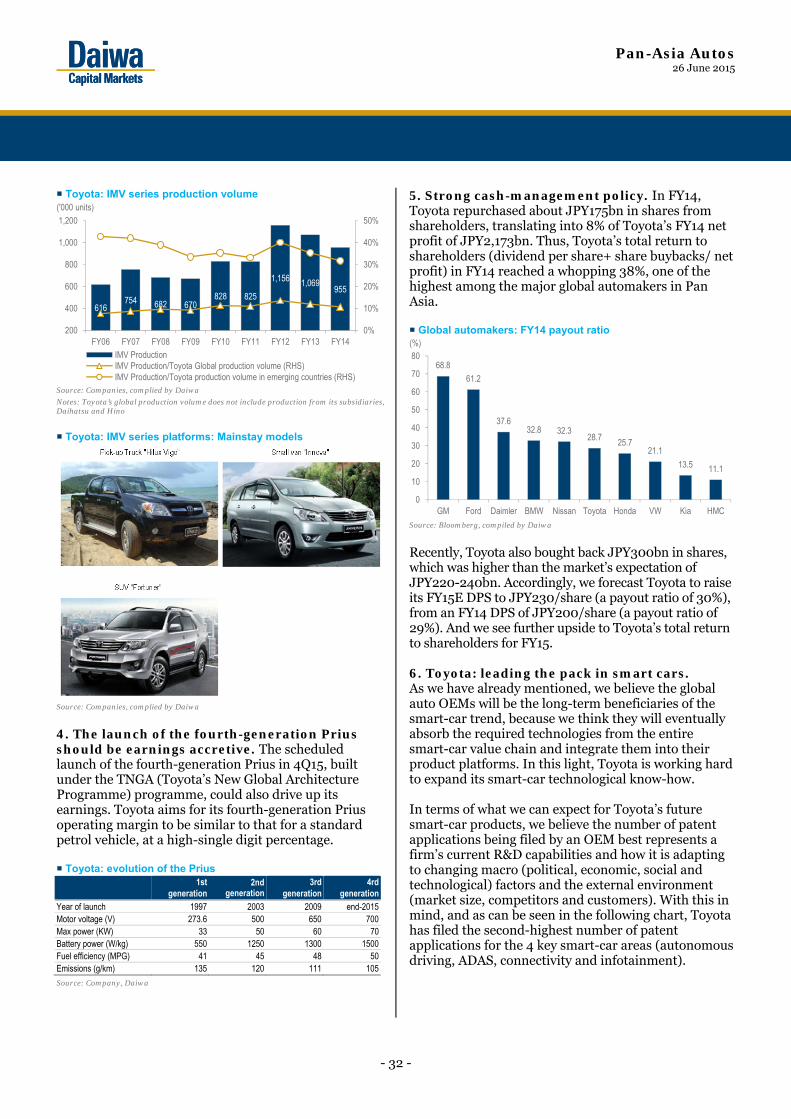

We expect the market size of ADAS to see exponentialgrowth till 2020E. Beyond 2020E, we look for smart cars to take the baton, with their market size rising at a 2019-25E CAGR of 11.5%, reaching USD150.5bn in 2025. Contrary to the global OEMs’ claims that they will have smart cars on the road by 2020, we see 2025 as a more realistic timeline. We argue that the following issues need to be resolved before any launches could take place in 2020: 1) the technological barriers, 2) the high pricing points for installing autonomous features (USD100K/unit), 3) the legal ambiguities, not least in terms of who bears responsibility in the case of accidents, and 4) the current lack of regulations governing “fully automated driving (Level 4)” models.

Source: Strategy Analytics (Nov 2013), Daiwa estimates

Valuation Global OEMs vs. automotive electronic parts makers

In our view, mega-auto suppliers with a strong competitive advantage in sensors/cameras and modules will take the lead in smart-car development with their ADAS technology. We expect the valuation premium for these makers to widen over 2015-17, as they record an EPS CAGR of 13.6% over the period (vs. 9.2% for the 9 global OEMs), based on both Daiwa and Bloomberg-consensus forecasts. Among the 9 global OEMs, Toyota, Ford, BMW and Daimler may continue to trade at a premium, vs. VW, GM, SAIC and Hyundai Motor Group (HMC and Kia), with the former OEMs’ better technology footprints in smart cars and higher earnings visibility compared to the latter OEMs.

Source: Companies, Bloomberg consensus and Daiwa estimates (*)

Earnings revisions Major Pan-Asia automakers and components: earnings forecasts revision cycle (Toyota, Denso and Mobis)

Within our Pan-Asia coverage of the major automobile and component makers, our stock picking order is Toyota, Denso, and Mobis. Typically, more developed markets’ auto stocks’ share prices are driven by their earnings revision cycle. Bearing this in mind, we look for Toyota to see the strongest upward earnings revision cycle and cash management policy, followed by Denso and Mobis.

Source: Companies, Bloomberg consensus and Daiwa

6.0 13.5 23.9 47.5 64.8 126.5

157.4

222.8

316.8

0

100

200

300

400

500

2014 2019E 2025EADAS Non-ADAS Non-smart-car

(USDbn)

USD210.9bn

USD301.1bn

USD467.3bnSmart car

Automotive electornics

FordGM

Daimler

BMW

VW

OEM average(8.8,9.2)

SAICToyota

*HMC

*Kia

Delphi

Autoliv

DensoContinental

MagnaValeo

Hella

Parts average(16.3,13.6)

0

2

4

6

8

10

12

14

16

18

20

0 2 4 6 8 10 12 14 16 18 20Auto-parts makers OEMs (PER,x)

(CAG

R, %

)

0

10 ,000

20,000

30,000

40,000

50,000

0

100

200

300

400

500

600

700

800

900

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15

Toyota Denso Mobis (RHS)

(JPY) (KRW)

Pan-Asia Autos 26 June 2015

- 5 -

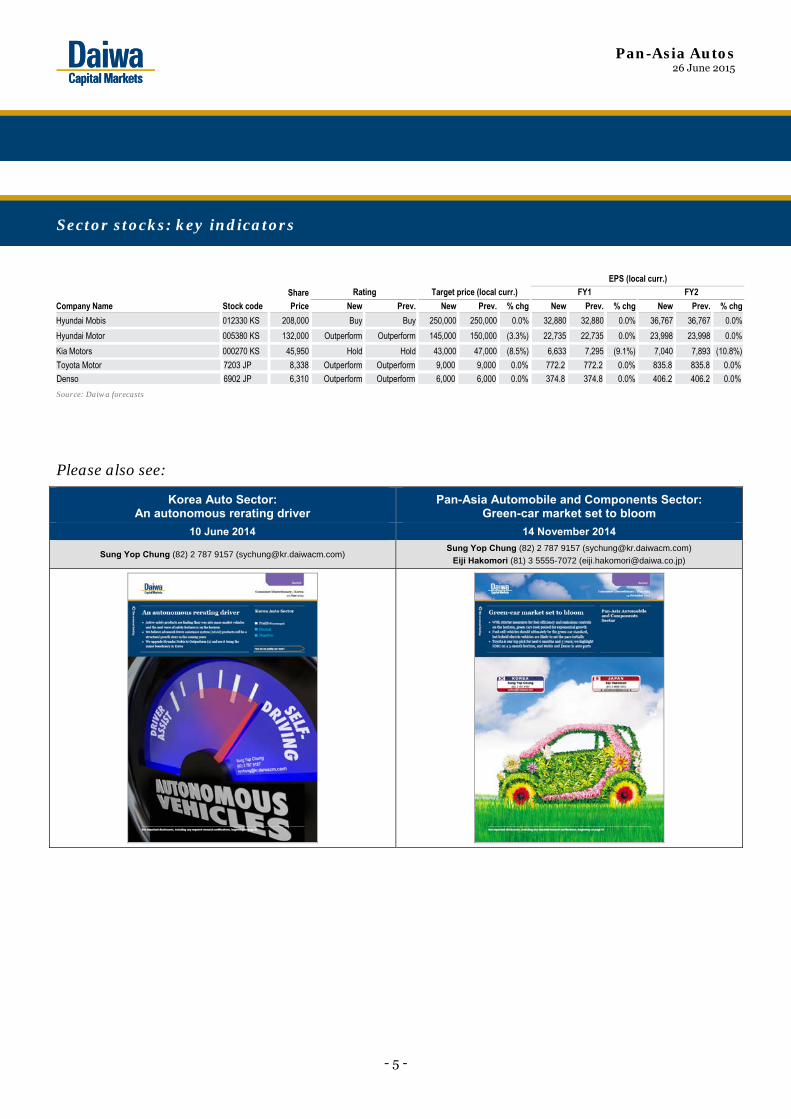

Toyota Motor 7203 JP 8,338 Outperform Outperform 9,000 9,000 0.0% 772.2 772.2 0.0% 835.8 835.8 0.0%

Denso 6902 JP 6,310 Outperform Outperform 6,000 6,000 0.0% 374.8 374.8 0.0% 406.2 406.2 0.0%

Source: Daiwa forecasts

Please also see:

Korea Auto Sector: An autonomous rerating driver

Pan-Asia Automobile and Components Sector: Green-car market set to bloom

10 June 2014 14 November 2014

Sung Yop Chung (82) 2 787 9157 ([email protected]) Sung Yop Chung (82) 2 787 9157 ([email protected])

Eiji Hakomori (81) 3 5555-7072 ([email protected])

Sector stocks: key indicators

Share

Company Name Stock code Price New Prev. New Prev. % chg New Prev. % chg New Prev. % chg

Hyundai Mobis 012330 KS 208,000 Buy Buy 250,000 250,000 0.0% 32,880 32,880 0.0% 36,767 36,767 0.0%

Hyundai Motor 005380 KS 132,000 Outperform Outperform 145,000 150,000 (3.3%) 22,735 22,735 0.0% 23,998 23,998 0.0%

Kia Motors 000270 KS 45,950 Hold Hold 43,000 47,000 (8.5%) 6,633 7,295 (9.1%) 7,040 7,893 (10.8%)

Rating Target price (local curr.) FY1

EPS (local curr.)

FY2

Pan-Asia Autos 26 June 2015

- 6 -

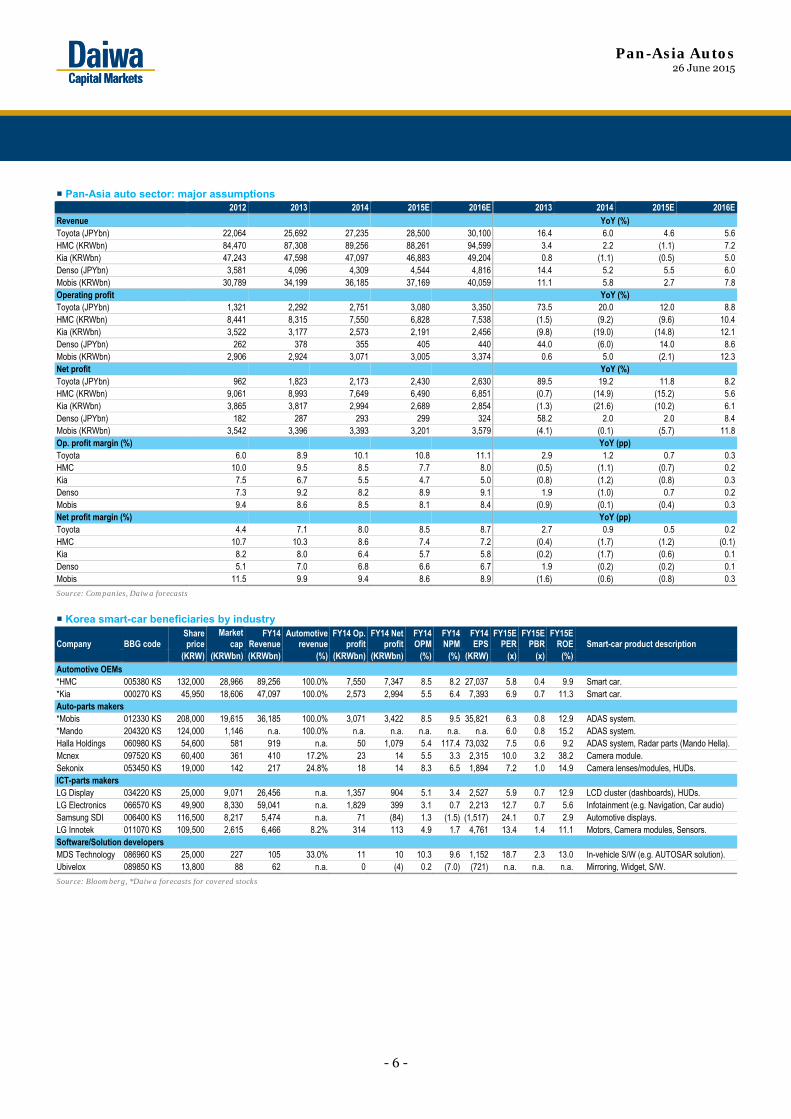

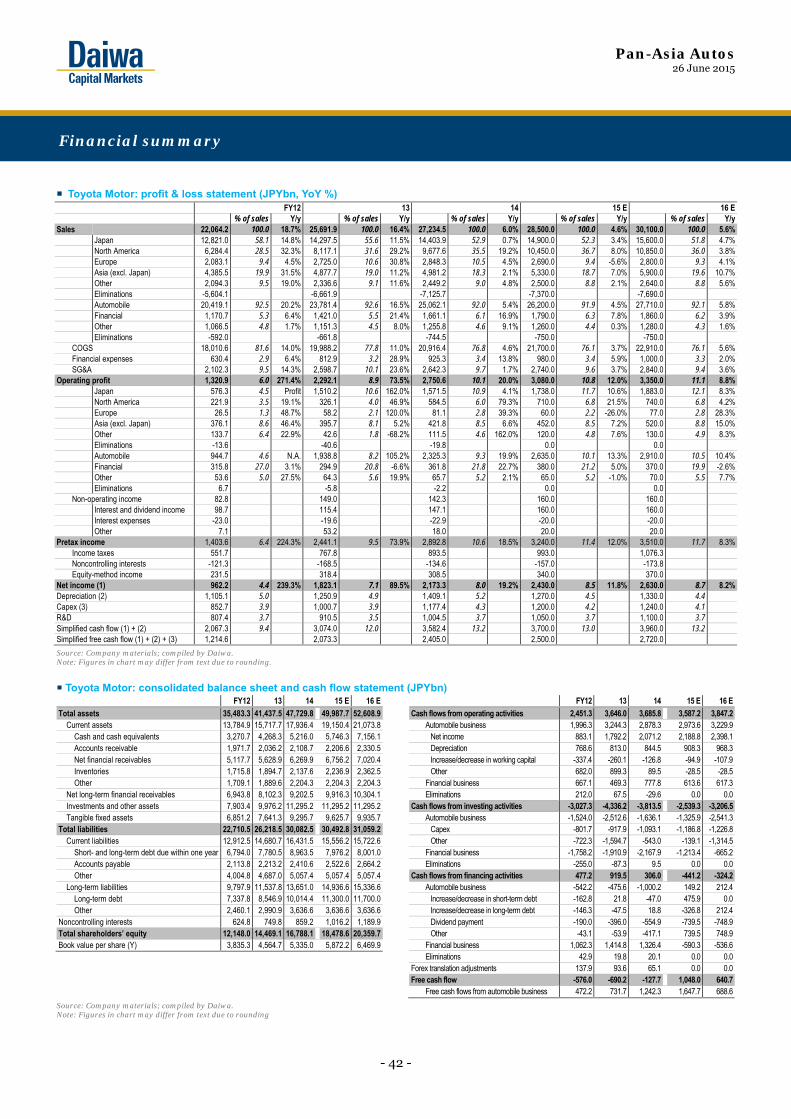

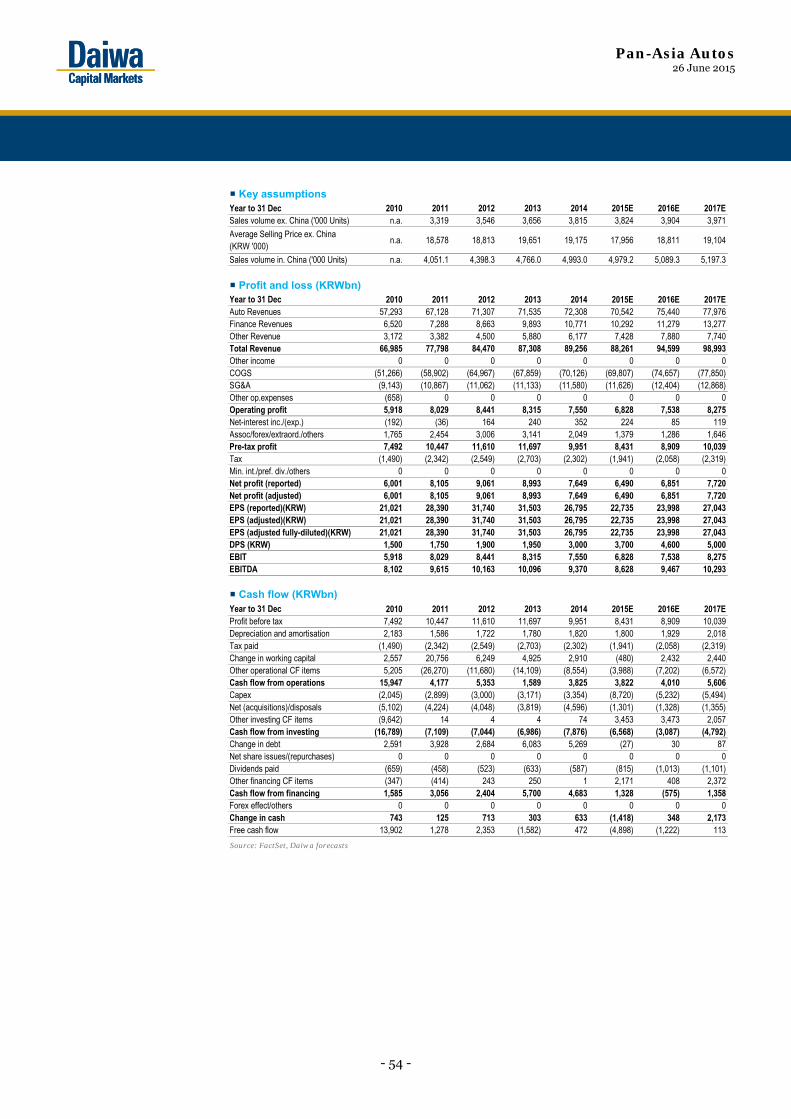

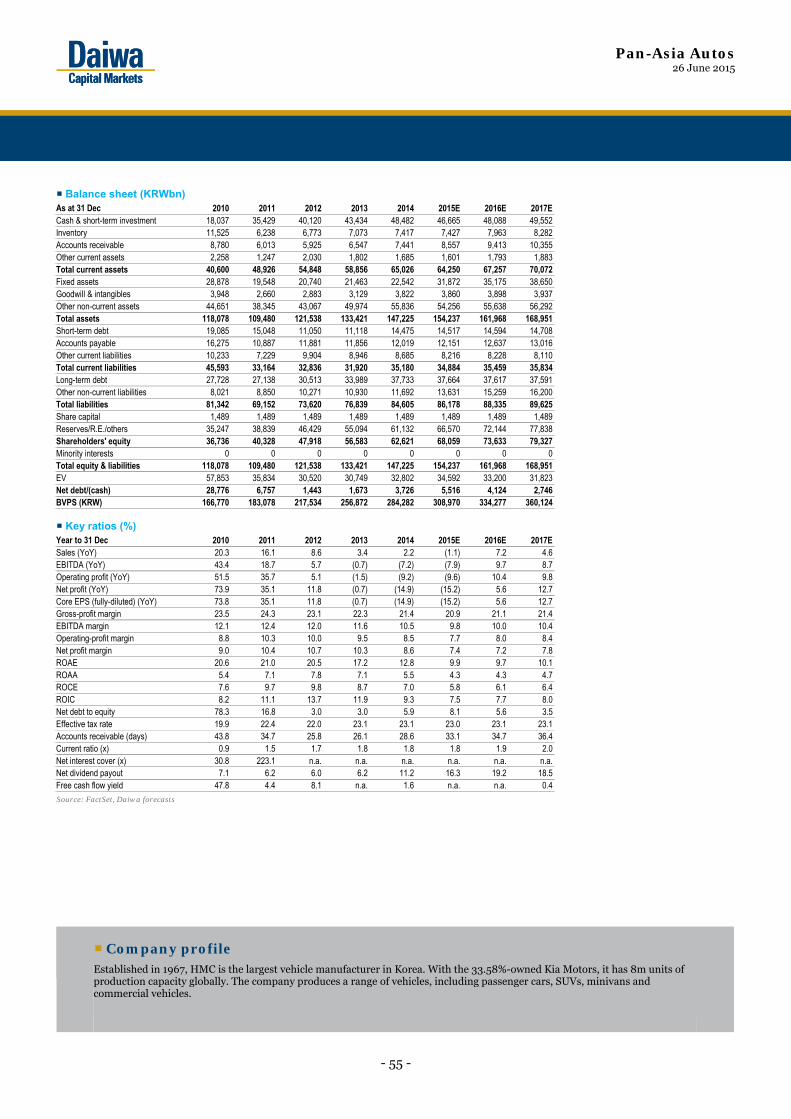

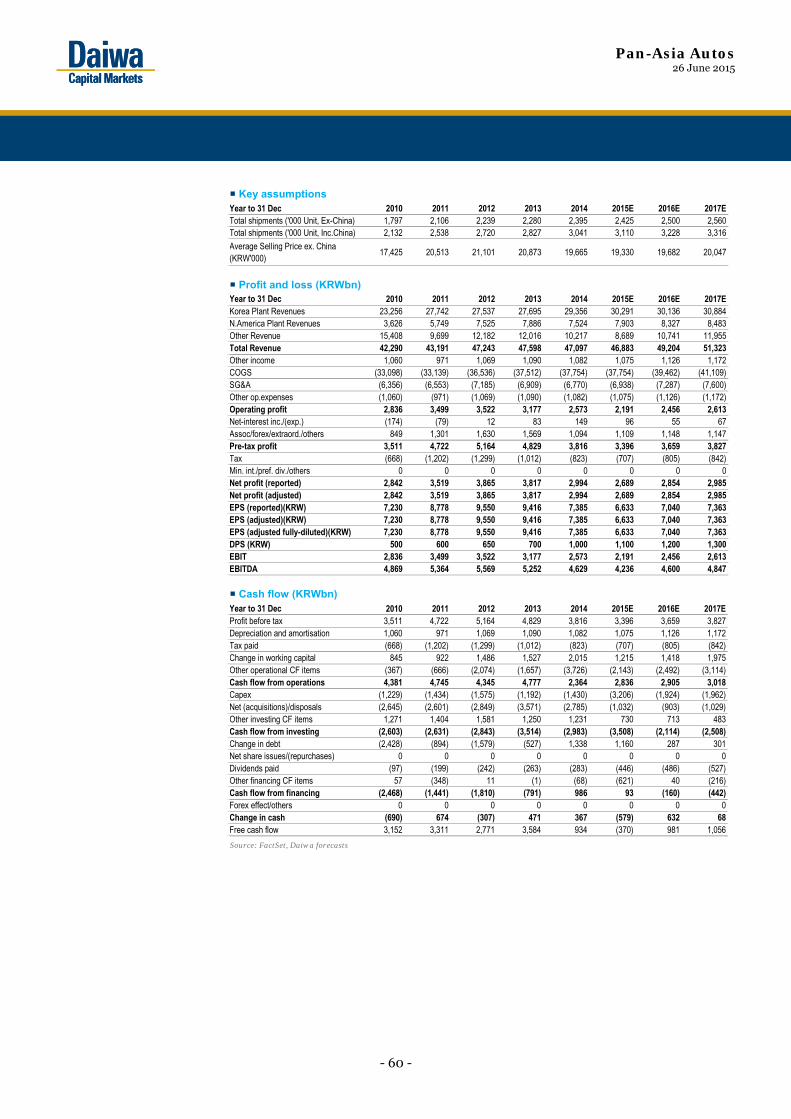

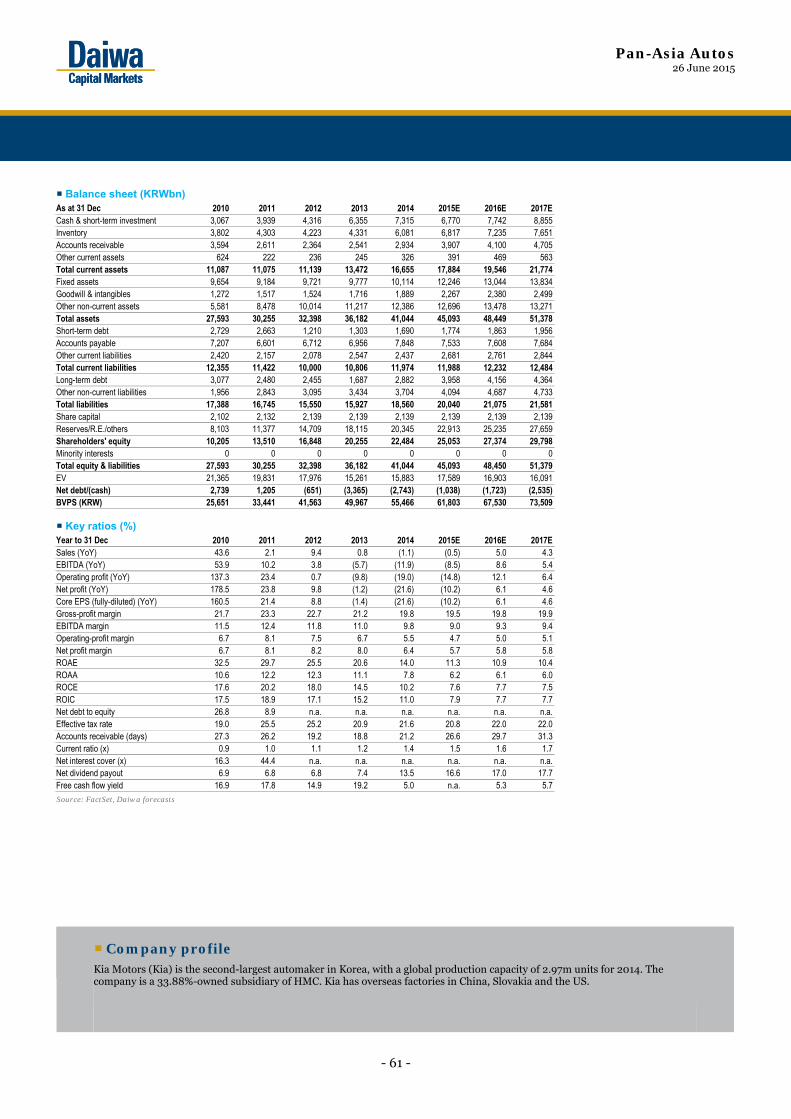

Pan-Asia auto sector: major assumptions 2012 2013 2014 2015E 2016E 2013 2014 2015E 2016ERevenue YoY (%) Toyota (JPYbn) 22,064 25,692 27,235 28,500 30,100 16.4 6.0 4.6 5.6 HMC (KRWbn) 84,470 87,308 89,256 88,261 94,599 3.4 2.2 (1.1) 7.2 Kia (KRWbn) 47,243 47,598 47,097 46,883 49,204 0.8 (1.1) (0.5) 5.0 Denso (JPYbn) 3,581 4,096 4,309 4,544 4,816 14.4 5.2 5.5 6.0 Mobis (KRWbn) 30,789 34,199 36,185 37,169 40,059 11.1 5.8 2.7 7.8 Operating profit YoY (%) Toyota (JPYbn) 1,321 2,292 2,751 3,080 3,350 73.5 20.0 12.0 8.8 HMC (KRWbn) 8,441 8,315 7,550 6,828 7,538 (1.5) (9.2) (9.6) 10.4 Kia (KRWbn) 3,522 3,177 2,573 2,191 2,456 (9.8) (19.0) (14.8) 12.1 Denso (JPYbn) 262 378 355 405 440 44.0 (6.0) 14.0 8.6 Mobis (KRWbn) 2,906 2,924 3,071 3,005 3,374 0.6 5.0 (2.1) 12.3 Net profit YoY (%) Toyota (JPYbn) 962 1,823 2,173 2,430 2,630 89.5 19.2 11.8 8.2 HMC (KRWbn) 9,061 8,993 7,649 6,490 6,851 (0.7) (14.9) (15.2) 5.6 Kia (KRWbn) 3,865 3,817 2,994 2,689 2,854 (1.3) (21.6) (10.2) 6.1 Denso (JPYbn) 182 287 293 299 324 58.2 2.0 2.0 8.4 Mobis (KRWbn) 3,542 3,396 3,393 3,201 3,579 (4.1) (0.1) (5.7) 11.8 Op. profit margin (%) YoY (pp) Toyota 6.0 8.9 10.1 10.8 11.1 2.9 1.2 0.7 0.3 HMC 10.0 9.5 8.5 7.7 8.0 (0.5) (1.1) (0.7) 0.2 Kia 7.5 6.7 5.5 4.7 5.0 (0.8) (1.2) (0.8) 0.3 Denso 7.3 9.2 8.2 8.9 9.1 1.9 (1.0) 0.7 0.2 Mobis 9.4 8.6 8.5 8.1 8.4 (0.9) (0.1) (0.4) 0.3 Net profit margin (%) YoY (pp) Toyota 4.4 7.1 8.0 8.5 8.7 2.7 0.9 0.5 0.2 HMC 10.7 10.3 8.6 7.4 7.2 (0.4) (1.7) (1.2) (0.1)Kia 8.2 8.0 6.4 5.7 5.8 (0.2) (1.7) (0.6) 0.1 Denso 5.1 7.0 6.8 6.6 6.7 1.9 (0.2) (0.2) 0.1 Mobis 11.5 9.9 9.4 8.6 8.9 (1.6) (0.6) (0.8) 0.3

Source: Companies, Daiwa forecasts

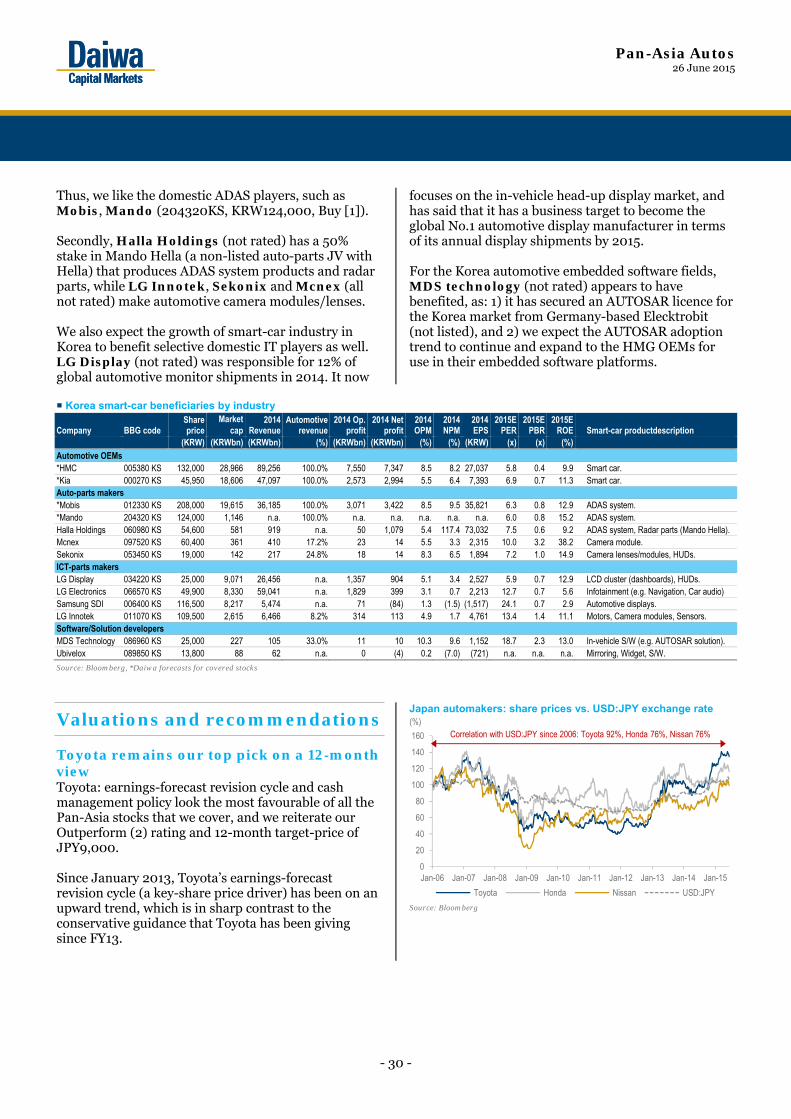

Korea smart-car beneficiaries by industry

Company BBG code Share price

Market cap

FY14 Revenue

Automotiverevenue

FY14 Op. profit

FY14 Net profit

FY14 OPM

FY14 NPM

FY14 EPS

FY15E PER

FY15EPBR

FY15E ROE Smart-car product description

(KRW) (KRWbn) (KRWbn) (%) (KRWbn) (KRWbn) (%) (%) (KRW) (x) (x) (%) Automotive OEMs *HMC 005380 KS 132,000 28,966 89,256 100.0% 7,550 7,347 8.5 8.2 27,037 5.8 0.4 9.9 Smart car. *Kia 000270 KS 45,950 18,606 47,097 100.0% 2,573 2,994 5.5 6.4 7,393 6.9 0.7 11.3 Smart car. Auto-parts makers *Mobis 012330 KS 208,000 19,615 36,185 100.0% 3,071 3,422 8.5 9.5 35,821 6.3 0.8 12.9 ADAS system. *Mando 204320 KS 124,000 1,146 n.a. 100.0% n.a. n.a. n.a. n.a. n.a. 6.0 0.8 15.2 ADAS system. Halla Holdings 060980 KS 54,600 581 919 n.a. 50 1,079 5.4 117.4 73,032 7.5 0.6 9.2 ADAS system, Radar parts (Mando Hella). Mcnex 097520 KS 60,400 361 410 17.2% 23 14 5.5 3.3 2,315 10.0 3.2 38.2 Camera module. Sekonix 053450 KS 19,000 142 217 24.8% 18 14 8.3 6.5 1,894 7.2 1.0 14.9 Camera lenses/modules, HUDs. ICT-parts makers LG Display 034220 KS 25,000 9,071 26,456 n.a. 1,357 904 5.1 3.4 2,527 5.9 0.7 12.9 LCD cluster (dashboards), HUDs. LG Electronics 066570 KS 49,900 8,330 59,041 n.a. 1,829 399 3.1 0.7 2,213 12.7 0.7 5.6 Infotainment (e.g. Navigation, Car audio) Samsung SDI 006400 KS 116,500 8,217 5,474 n.a. 71 (84) 1.3 (1.5) (1,517) 24.1 0.7 2.9 Automotive displays. LG Innotek 011070 KS 109,500 2,615 6,466 8.2% 314 113 4.9 1.7 4,761 13.4 1.4 11.1 Motors, Camera modules, Sensors. Software/Solution developers MDS Technology 086960 KS 25,000 227 105 33.0% 11 10 10.3 9.6 1,152 18.7 2.3 13.0 In-vehicle S/W (e.g. AUTOSAR solution). Ubivelox 089850 KS 13,800 88 62 n.a. 0 (4) 0.2 (7.0) (721) n.a. n.a. n.a. Mirroring, Widget, S/W.

Source: Bloomberg, *Daiwa forecasts for covered stocks

Pan-Asia Autos 26 June 2015

- 7 -

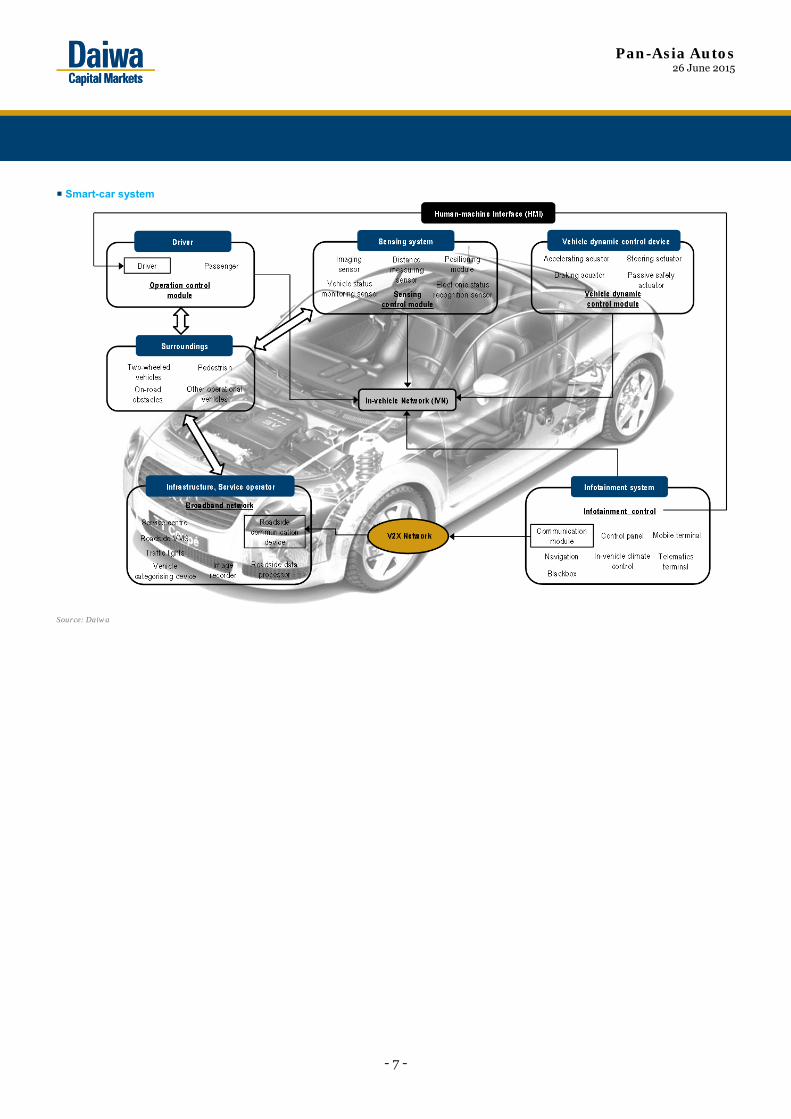

Smart-car system

Source: Daiwa

Pan-Asia Autos 26 June 2015

- 8 -

Smart cars: changing the landscape

What will be the next smart device?

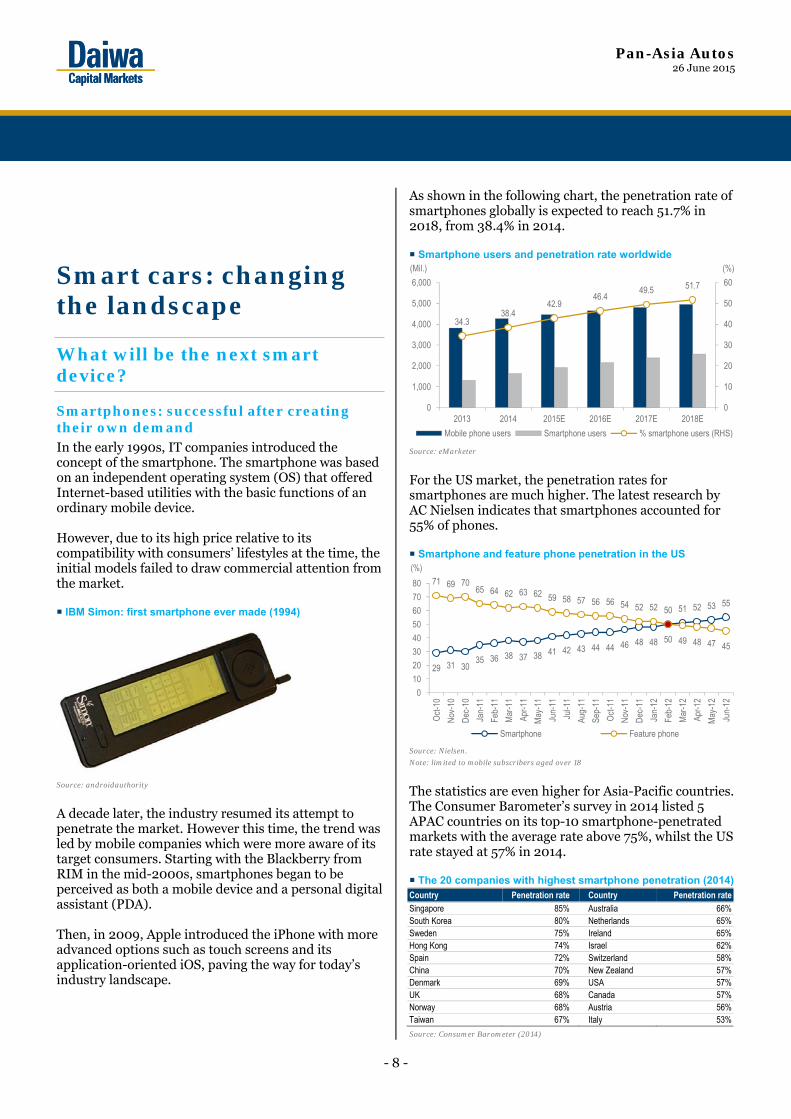

Smartphones: successful after creating their own demand In the early 1990s, IT companies introduced the concept of the smartphone. The smartphone was based on an independent operating system (OS) that offered Internet-based utilities with the basic functions of an ordinary mobile device. However, due to its high price relative to its compatibility with consumers’ lifestyles at the time, the initial models failed to draw commercial attention from the market. IBM Simon: first smartphone ever made (1994)

Source: androidauthority

A decade later, the industry resumed its attempt to penetrate the market. However this time, the trend was led by mobile companies which were more aware of its target consumers. Starting with the Blackberry from RIM in the mid-2000s, smartphones began to be perceived as both a mobile device and a personal digital assistant (PDA). Then, in 2009, Apple introduced the iPhone with more advanced options such as touch screens and its application-oriented iOS, paving the way for today’s industry landscape.

As shown in the following chart, the penetration rate of smartphones globally is expected to reach 51.7% in 2018, from 38.4% in 2014. Smartphone users and penetration rate worldwide

Source: eMarketer

For the US market, the penetration rates for smartphones are much higher. The latest research by AC Nielsen indicates that smartphones accounted for 55% of phones. Smartphone and feature phone penetration in the US

Source: Nielsen.

Note: limited to mobile subscribers aged over 18

The statistics are even higher for Asia-Pacific countries. The Consumer Barometer’s survey in 2014 listed 5 APAC countries on its top-10 smartphone-penetrated markets with the average rate above 75%, whilst the US rate stayed at 57% in 2014. The 20 companies with highest smartphone penetration (2014) Country Penetration rate Country Penetration rateSingapore 85% Australia 66%South Korea 80% Netherlands 65%Sweden 75% Ireland 65%Hong Kong 74% Israel 62%Spain 72% Switzerland 58%China 70% New Zealand 57%Denmark 69% USA 57%UK 68% Canada 57%Norway 68% Austria 56%Taiwan 67% Italy 53%

Source: Consumer Barometer (2014)

34.338.4

42.946.4

49.5 51.7

0

10

20

30

40

50

60

0

1,000

2,000

3,000

4,000

5,000

6,000

2013 2014 2015E 2016E 2017E 2018E

Mobile phone users Smartphone users % smartphone users (RHS)

(Mil.) (%)

29 31 3035 36 38 37 38 41 42 43 44 44 46 48 48 50

51 52 53 55

71 69 7065 64 62 63 62 59 58 57 56 56 54 52 52 50

49 48 47 45

0

10

20

30

40

50

60

70

80

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb-

11

Mar

-11

Apr-1

1

May

-11

Jun-

11

Jul-1

1

Aug-

11

Sep-

11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

Feb-

12

Mar

-12

Apr-1

2

May

-12

Jun-

12Smartphone Feature phone

(%)

Pan-Asia Autos 26 June 2015

- 9 -

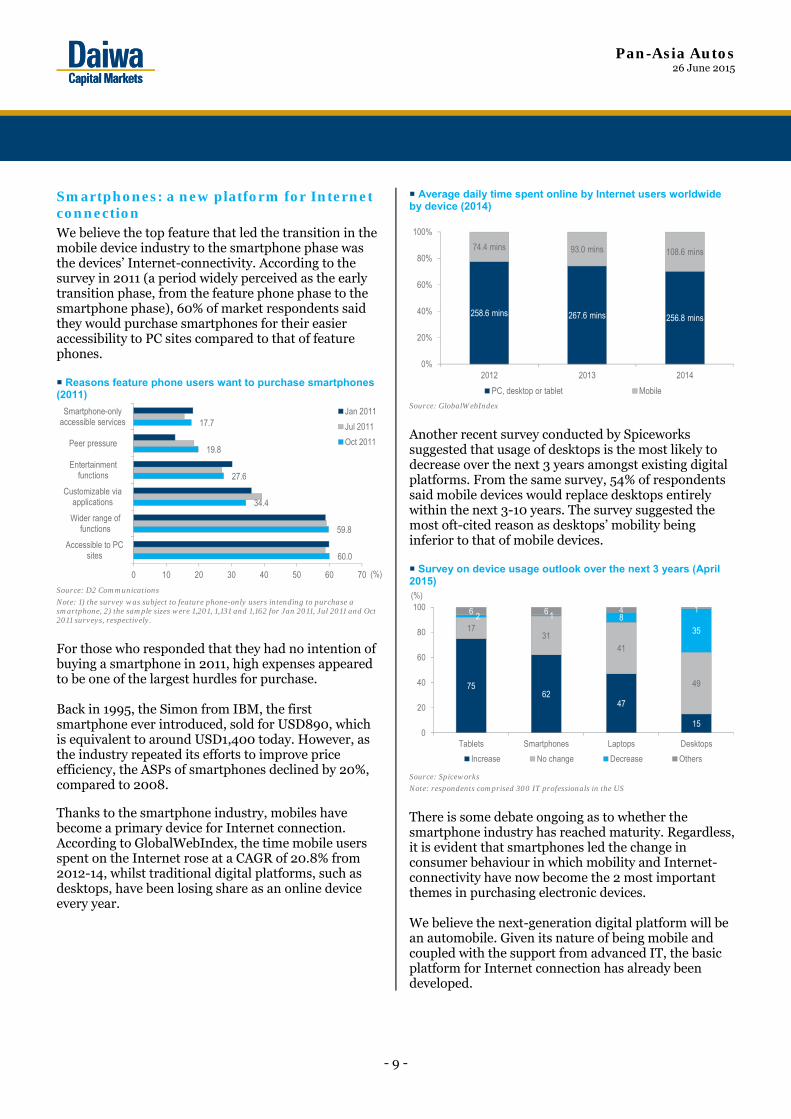

Smartphones: a new platform for Internet connection We believe the top feature that led the transition in the mobile device industry to the smartphone phase was the devices’ Internet-connectivity. According to the survey in 2011 (a period widely perceived as the early transition phase, from the feature phone phase to the smartphone phase), 60% of market respondents said they would purchase smartphones for their easier accessibility to PC sites compared to that of feature phones. Reasons feature phone users want to purchase smartphones (2011)

Source: D2 Communications

Note: 1) the survey was subject to feature phone-only users intending to purchase a smartphone, 2) the sample sizes were 1,201, 1,131 and 1,162 for Jan 2011, Jul 2011 and Oct 2011 surveys, respectively.

For those who responded that they had no intention of buying a smartphone in 2011, high expenses appeared to be one of the largest hurdles for purchase. Back in 1995, the Simon from IBM, the first smartphone ever introduced, sold for USD890, which is equivalent to around USD1,400 today. However, as the industry repeated its efforts to improve price efficiency, the ASPs of smartphones declined by 20%, compared to 2008.

Thanks to the smartphone industry, mobiles have become a primary device for Internet connection. According to GlobalWebIndex, the time mobile users spent on the Internet rose at a CAGR of 20.8% from 2012-14, whilst traditional digital platforms, such as desktops, have been losing share as an online device every year.

Average daily time spent online by Internet users worldwide by device (2014)

Source: GlobalWebIndex

Another recent survey conducted by Spiceworks suggested that usage of desktops is the most likely to decrease over the next 3 years amongst existing digital platforms. From the same survey, 54% of respondents said mobile devices would replace desktops entirely within the next 3-10 years. The survey suggested the most oft-cited reason as desktops’ mobility being inferior to that of mobile devices. Survey on device usage outlook over the next 3 years (April 2015)

Source: Spiceworks

Note: respondents comprised 300 IT professionals in the US

There is some debate ongoing as to whether the smartphone industry has reached maturity. Regardless, it is evident that smartphones led the change in consumer behaviour in which mobility and Internet-connectivity have now become the 2 most important themes in purchasing electronic devices. We believe the next-generation digital platform will be an automobile. Given its nature of being mobile and coupled with the support from advanced IT, the basic platform for Internet connection has already been developed.

60.0

59.8

34.4

27.6

19.8

17.7

0 10 20 30 40 50 60 70

Accessible to PCsites

Wider range offunctions

Customizable viaapplications

Entertainmentfunctions

Peer pressure

Smartphone-onlyaccessible services

Jan 2011

Jul 2011

Oct 2011

(%)

258.6 mins 267.6 mins 256.8 mins

74.4 mins 93.0 mins 108.6 mins

0%

20%

40%

60%

80%

100%

2012 2013 2014

PC, desktop or tablet Mobile

7562

47

15

1731

41

49

2 1 8

35

6 6 4 1

0

20

40

60

80

100

Tablets Smartphones Laptops Desktops

Increase No change Decrease Others

(%)

Pan-Asia Autos 26 June 2015

- 10 -

Smart cars: the industry’s next response to consumer needs

Internet connectivity is now a consideration in automobile purchases According to KPMG’s annual survey in 2015, fuel efficiency and enhanced vehicle lifespan remain the most significant factors in consumers’ automobile purchase decisions, with respondent rates of 67% and 53%, respectively. However, there has been a certain change in perception to other minor factors, especially with IT-related ones, over the past few years. In-car Internet connectivity seems to have been undervalued in the past, considering its rating increase to 24% in 2015, from 17% in 2013. Plug-in solutions for navigation, speech recognition and mobile Internet device also rose in its rating to 38% in 2015, from 20% in 2013. In an effort to explain the reasons for such changes in perception, KPMG said the younger generation in particular expects to enjoy the same range of services in their vehicles as they can get at home, in the office or on their smartphone. The services include music, telecommunications and Internet access, as well as a navigation system that integrates with broader traffic control systems to make their journey as efficient as possible. Importance of vehicle features to consumer purchase decisions until 2020 (Jan 2015)

Source: KPMG’s Global Auto Executive Survey 2015

Note: 1) figures are percentages of respondents that rated issues as ‘extremely important’ or ‘very important’, 2) dual responses were allowed in the survey

In addition to KPMG’s comments, we expect the abovementioned factors to optimise other key criteria such as fuel efficiency, as in-vehicle connection will be able to reroute vehicles to less-congested routes, thereby cutting some of their fuel usage, as well as drivers’ congestion charges. Thus, we believe the IT themes will be more appealing to consumers in their car purchase decisions over the next decade.

Connectivity appeals to automobile consumers but has raised safety concerns However, as much as the embedded connectivity in automobiles appeals to consumers, there are growing concerns as to whether in-vehicle entertainment will further distract drivers while a vehicle is moving. Surveys conducted in the US, UK and Germany said 65% of drivers believe further services in their cars would only increase the risk of an accident, as they pay less attention to traffic and steering. Respondent rate of those expecting potential threats from further services in cars (Feb 2015)

Source: Prophet

Note: the question was whether further services in the car will only distract from traffic and steering, thereby serving to increase the risk of an accident

A recent study on mental distraction in cars carried out by the American Automobile Association (AAA) also showed that the added complexity of in-vehicle systems can dangerously divert drivers’ attention, with voice-to-voice interactions such as Apple’s Siri seeming to be hugely distracting to drivers in general. Cognitive workload scale by task while driving (Oct 2014)

Source: AAA

Note: 1)*using hands-free voice commands while driving, 2)**version iOS7 at time of research, evaluated sending/receiving texts, updating Facebook/Twitter and checking calendar by using voice commands while driving, 3) distraction level by scale range is as follows: 1-2 = low;2-3 = medium; more than or equal to 3 = high

68

19

46 47

35

23 20 17 11 21

66

45 48

36 38 34 39

26 16 15

67

53 52 49 41 40 38

24 19 18

01020304050607080

Fuel

effic

ienc

y

Life

span

Safe

ty

Ergo

nom

ics

Eco-

frien

dlin

ess

Styl

ing

*Plu

g-in

solu

tions

Inte

rnet

conn

ectiv

ity

Tele

mat

ics

Alt.

fuel

tech

.

2013 2014 2015

(%)

23

42

28

7

19

48

27

6

20

41

31

8

21

44

29

7

0

10

20

30

40

50

60

Strongly agree Agree Disagree Strongly disagree

US UK Germany Average

(%)

1.00

1.882.18

3.082.83

3.674.15

0.00

1.00

2.00

3.00

4.00

5.00

Driving only Adjustingradio ortemp*

Listening tomessages*

Listening &composingmessages*

Navigatingsimplemenus*

Navigatingcomplexmenus*

Apple'sSiri**

HighDistraction

MediumDistraction

LowDistraction

Pan-Asia Autos 26 June 2015

- 11 -

For this reason, we believe the next commercial automobile must satisfy both advanced Internet connectivity and provide a full guarantee of safety to prevent any potential distractions from utilising the in-vehicle entertainment. For the latter, we believe autonomous driving, or self-driving technology, could meet the objective. Concept of a next-generation vehicle

Source: Daiwa

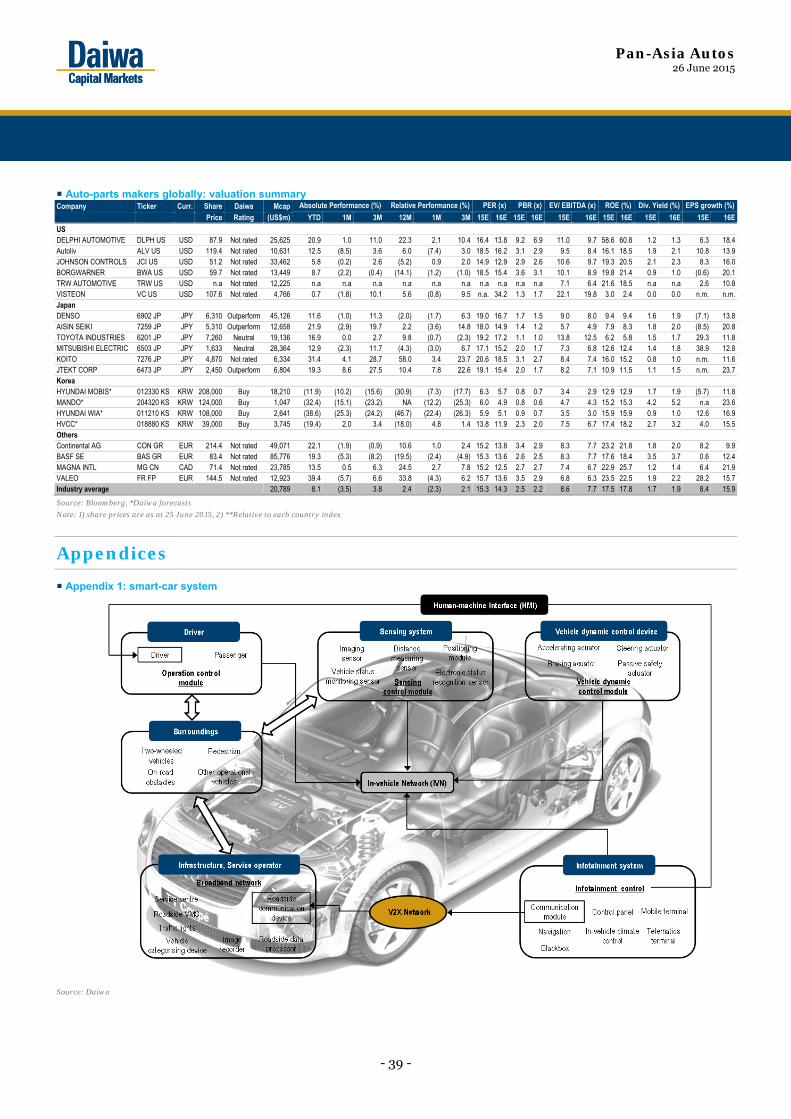

What is a smart car?

A connected, self-driving vehicle In the past, the term “smart car” simply meant an automobile equipped with advanced electronics. The definition is more specific nowadays. Now the term is generally accepted as referring to a vehicle in which Internet of Things (IoT) technology helps the auto to communicate with its surroundings in real time, thereby maximising safety and convenience for the driver. We believe there are 4 types of applications that define smart cars: 1) infotainment/media, 2) advanced telematics, 3) vehicle-to-X communications, and 4) autonomous driving capabilities (See Appendix 1). Smart-car features Features Details In-vehicle infotainment Web browsing

Media and entertainment Communication

Telematics Navigation Insurance Emergency services Diagnostics, prognostics

Vehicle-to-X communications Infrastructure (eg, toll plazas, traffic signals) Other vehicles (eg, crash avoidance)

Autonomous operation Cruise control Lane detection Auto-parking Collision avoidance Self-driving assistance

Source: Daiwa

1. In-vehicle infotainment (IVI) Infotainment refers to a type of media that combines information and entertainment. In turn, IVI is a collective term for the hardware/software products and systems that are built into vehicles to enhance the

driver and passenger experience. And as far as smart cars are concerned, the term encompasses such functions as web browsing, media and entertainment and consumption, and communications. Since the mid-2000s, automotive OEMs have been showing off models featuring IVI at auto fairs around the world. At the 2005 American International Auto show, Nissan demonstrated the Nissan Urge, which featured a Microsoft Xbox 360 game console to entertain the driver. Then, in 2006, GM added an option to install a 40gb hard drive in its Buick Terraza minivan which drivers could use to store digital files such as games, movies and music. Consumers’ expectations for IT-based functionality continue to grow, and it has become a major trend for the automotive OEM players to expand their IVI features. But, in order to do that, the global OEMs have had to enter into collaborative relationships with Information and Communication Technology (ICT) players. For example, in 2005, Chrysler showed off the fruits of its collaboration with Apple: vehicles in which an iPod could be controlled using the auto’s main control system. Global OEMs: cooperative development milestones with ICT companies Automotive ICT Description Ford Microsoft Launched SYNC, an in-vehicle voice-recognition technology BMW Intel Worked jointly on infotainment system development schedule Toyota Microsoft Launched EnTune, an in-vehicle multi-platform Microsoft Developed a cloud-computer-based telematics system Intel Announced results of its in-vehicle multi-system development

research HMC Microsoft Launched Bluelink Kia Microsoft Developed UVO HMC/Kia Intel C&S Developed an infotainment platform Tesla NVIDIA Announced plan to adopt Nvidia’s Tegra technology in MY15 model Audi NVIDIA Announced plans to adopt Nvidia’s Tegra 3 in Audi cars

Source: Daiwa

In 2010, Ford and Microsoft launched their proprietary IVI system, SYNC. Unlike previous in-vehicle embedded control systems, SYNC offered hands-free calls and the activation of mobile-based apps using only the driver’s voice. It also provided voice-based entertainment functions, including music, games, radio and news/weather updates. Toyota and Audi followed suit by announcing their own IVI platforms in 2011 (Entune) and 2013 (Connect), respectively.

Current commercial vehicle

Internetconnectiv ity

Full guaranteeof safety

Nextvehicle to be commercialised

+ +

Pan-Asia Autos 26 June 2015

- 12 -

Ford: SYNC (2010)

Source: Ford

After a few such collaborations, it became clear to both the auto companies and the ICT players that having standardised formats for IVI platforms would reduce development time and investment costs. We look briefly at these efforts to standardise platforms and illustrate why we think they will become a catalyst for the growth of smart-car industry globally (see “Cross-industry cooperation expected to accelerate smart-car development”). 2. Telematics Telematics refers to the convergence of telecommunications and information processing. In the context of autos, the term refers to automation, such as emergency warning systems, GPS navigation, and remote diagnostics. Concept of automotive telematics

Source: Car Tracking Device

To date there are basically 3 types of car connectivity solutions: 1) embedded, 2) tethered, and 3) integrated. Embedded solutions feature Internet connectivity whereby the underlying modems, UICC and automotive intelligence systems are installed in the vehicle itself. By contrast, integrated solutions work by allowing the vehicles to get connected via a smartphone interface only.

In the telematics fields, telecommunications operators have established collaborative relationships with the auto OEMs in much the same way as the ICT companies have done so. Car connectivity solutions

Source: Daiwa

Again, we look in more detail at in-vehicle telematics and IVI fields on “Cross-industry cooperation expected to accelerate smart-car development”. 3. Vehicle-to-X (V2X) communications This feature refers to vehicles being able to communicate automatically with each other, as well as with traffic infrastructure. Through the adoption of V2X systems in autos, all the data acquired by a vehicle’s on-board sensors, such as speed, position and driving direction, is made available to other traffic participants and infrastructure components (such as traffic lights and traffic guidance systems). In addition, vehicle systems can process this data and turn it into useful information for the driver, too, such as navigation advice, thereby optimising traffic flow and traffic safety at the same time. Continental: V2X landscape

Source: Continental

Pan-Asia Autos 26 June 2015

- 13 -

The above illustration showing a virtual landscape for V2X communication calls for technological advances across the board, including to such mainstay infrastructure as traffic lights, street lamps, and road signs. Hence, to bring such a system to fruition would require the active involvement and participation of government bodies and commercial entities. To date, US agencies have carried out 14 nationwide vehicle-to-infrastructure (V2I) programmes —one component of a fully featured V2X system — and successfully established WAVE-based V2I networks, including IntelliDrive, VSC, VII and CICAS. For V2X in particular, the US has conducted the Connected Vehicle Safety Pilot project and in 2012-13 it showcased 3,000 V2X-equipped vehicles driving in Ann Arbor. For its part, the EU has established its own CALM-based V2I networks, including VCIS and SAFESPOT, which are the product of around 60 V2I-related development programmes. And there has been an industry-led push among auto players globally to launch commercial vehicles with V2X functionality in the near future. In 2008, 9 automakers formed a non-profit organisation, the CAR 2 CAR Communication Consortium (C2C CC), with the goal of promoting car-to-car (C2C) strategies globally. In 2013, along other major names, such as GM and Ford, Daimler announced its Drive kit plus, an initial step towards a C2X project featuring a smartphone and the Digital DriveStyle app (developed by Mercedes-Benz), which together turn a vehicle into a simultaneous transmitter and receiver of information. Daimler plans to commercialise its system by 2015. 4. Autonomous driving Of all the smart features we have highlighted, we expect autonomous driving to be the biggest potential business catalyst for the auto industry globally. In our 10 June 2014 report (An autonomous rerating driver), we assessed the outlook for advanced driving assistance system (ADAS) products and their makers globally. In this report, we go a step further and look at autonomous driving schemes, as true smart cars must feature always-on online connectivity as well as flawless self-driving functionality. Previously, we defined ADAS as an advanced form of active-safety technology that could be applied to 3 categories: forward sensing, lane departure, and others. Among the early movers in ADAS products are

the tier-1 suppliers of safety parts, such as Autoliv (not rated), Continental (not rated), Bosch (not listed), TRW (not rated) and Denso. We retain our view that the worldwide adoption of ADAS products will unfold over the course of 2015-20. But, we now expect autonomous driving to become more apparent in 2025, rather than within 2015-20, given the need to overcome certain technological barriers. Mandatory active safety regulations in major countries Safety measure

2011 2012 2013 2014 2015

ESC USA, EU Japan, Korea TPMS USA Korea EURear-view camera USA Smart pedal USAAEB EU Japan Korea

Source: KART, KEIT, Daiwa

Note: ESC = Electronic stability control, TPMS = Tyre pressure monitoring system, AEB = Autonomous Emergency Braking

Roadmap for safety products

Stage 1 Stage 2 Stage 3 Stage 4 Passive safety Active safety ADAS Autonomous

driving Key technologies

Airbag Seatbelt

ABS ESC EPS

ACC, FCW LDW Blind-spot detection

Self-parking Highway steering

Key suppliers

Bosch Continental Delphi Denso Mobis, Mando

Autoliv Bosch Continental TRW Mobis, Mando

Bosch Continental Toyota Nissan GM

Timeframe for adoption

1981-98 1999-2015 2015-20 2025-

Source: Daiwa

Note: ABS = Antilock braking system, ESC = Electronic stability control, EPS = Electronic power steering, ACC = Adaptive cruise control, FCW = Forward collision warning, LDW = Lane-departure warning

When will self-driving cars take to the roads?

2020 is not a realistic target As shown in the following table, the US National Highway Traffic Safety Administration (NHTSA) defines autonomous driving in different stages.

Pan-Asia Autos 26 June 2015

- 14 -

NHTSA/SAE defined autonomous driving stages

NHTSA level

SAE level Name Narrative definition

Execution of steering/acceleration/deceleration

Monitoring of driving environment

Fall-back performance of dynamic driving task

System capability (driving models)

Human driver monitors the driving environment 0 0 No

automation The full-time performance by human driver of all aspects of the dynamic driving task, even when enhanced by warning or intervention system

Human driver Human driver Human driver n.a.

1 1 Driver assistant

The driving mode-specific execution by a driver assistance system of either steering or acceleration/deceleration using information about the driving environment and with the expectation that the human driver perform all remaining aspects of the dynamic driving task

Human driver and system

Human driver Human driver Some driving models

2 2 Partial automation

The driving mode-specific execution by one or more driver assistance system of both steering and acceleration/deceleration using information about the driving environment and with the expectation that the human driver perform all remaining aspects of the dynamic driving task

System Human driver Human driver Some driving models

Automated driving system ("system") monitors the driving environment 3 3 Conditional

automation The driving mode-specific performance by an automated driving system of all aspects of the dynamic driving tasks with the expectation that the human driver will respond appropriately to a request to intervene

System System Human driver Some driving models

4 4 High automation

The driving mode-specific performance by an automated driving system of all aspects of the dynamic driving task, even if a human driver does not respond appropriately to a request to intervene

System System System Some driving models

5 Full automation

The full-time performance by an automated driving system of all aspects of the dynamic driving task under all roadway and environmental conditions that can be managed by a human driver

System System System All driving models

Source: SAE, Daiwa

Among the various players working on autonomous driving, Google is targeting to reach Level 4, ie, “fully automated driving”, while global OEMs such as VW Group and GM aim to reach this stage by 2020. However, we believe it will be difficult for any player to reach Level 4 by 2020 because there are significant technological hurdles in the way. For this reason we consider 2025 to be a more realistic target. Various players’ targets to meet goal of offering fully automated driving Company Year expected to launch commercial model Audi 2020 (Level 4) Volkswagen 2020 (Level 4) GM 2016 (Level 3) Mercedes-Benz 2020 (Level 4) Google 2017 (Level 4) Renault 2016 (Level 2), 2020 (Level 4) Nissan 2020 (Level 4) Toyota 2016 (Level 3) Volvo 2017 (Level 3) HMC 2016 (Level 2), 2020 (Level 4)

Source: Daiwa

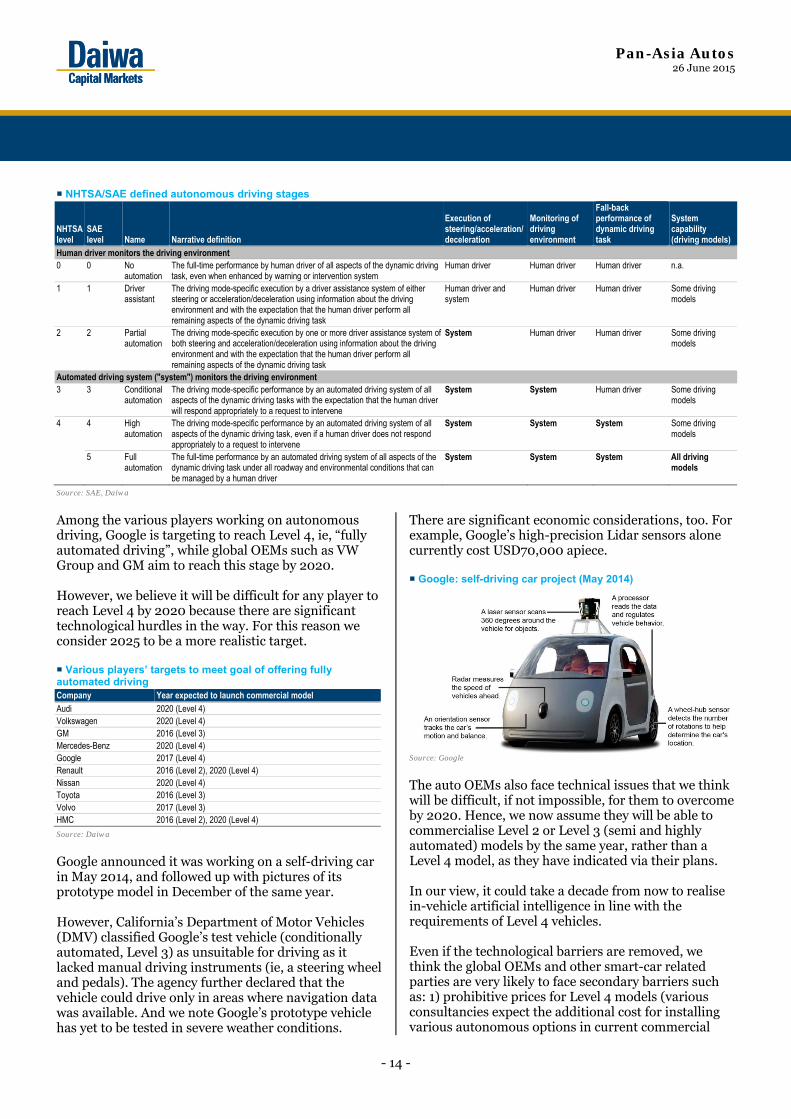

Google announced it was working on a self-driving car in May 2014, and followed up with pictures of its prototype model in December of the same year. However, California’s Department of Motor Vehicles (DMV) classified Google’s test vehicle (conditionally automated, Level 3) as unsuitable for driving as it lacked manual driving instruments (ie, a steering wheel and pedals). The agency further declared that the vehicle could drive only in areas where navigation data was available. And we note Google’s prototype vehicle has yet to be tested in severe weather conditions.

There are significant economic considerations, too. For example, Google’s high-precision Lidar sensors alone currently cost USD70,000 apiece. Google: self-driving car project (May 2014)

Source: Google

The auto OEMs also face technical issues that we think will be difficult, if not impossible, for them to overcome by 2020. Hence, we now assume they will be able to commercialise Level 2 or Level 3 (semi and highly automated) models by the same year, rather than a Level 4 model, as they have indicated via their plans. In our view, it could take a decade from now to realise in-vehicle artificial intelligence in line with the requirements of Level 4 vehicles. Even if the technological barriers are removed, we think the global OEMs and other smart-car related parties are very likely to face secondary barriers such as: 1) prohibitive prices for Level 4 models (various consultancies expect the additional cost for installing various autonomous options in current commercial

Pan-Asia Autos 26 June 2015

- 15 -

models to reach USD100,000/unit), 2) legal ambiguities, not least in terms of who bears responsibility in the case of accidents, 3) the danger of privacy invasion, and 4) the current lack of regulations governing “fully automated driving (Level 4)” models.

Smart-car market outlook more promising than ever

Ingredients for growth already secured Considering the high level of specialisation required for each feature in a smart car, we think the market can only expand in size if its corresponding markets expand in a similar manner. In 2010, automotive electronics accounted for 30% of the total cost of manufacturing a car. Given the encouraging growth of the electricity-reliant car market, including green cars, such as FCVs and HEVs (see our report “Green-car market set to bloom”, published on 17 November 2014), we see strong potential for the cost proportion of automotive electronics parts to reach 50% by 2030. Automotive electronics parts (% of manufacturing costs for cars)

Source: PwC analysis

As electronics parts have become more important in the automobile production process, the corresponding markets, such as automotive semiconductors/displays, have been in expansionary phases since the late-2000s. For example, the global automotive semiconductor market grew to USD29.0bn in 2014, in terms of revenue, from USD25.3bn in 2012, translating into a 2-year CAGR of 6.8%. Meanwhile, automotive semiconductor revenue as a proportion of the global top 5 companies’ total revenue increased to 30.5% in 2014, from 26.8% in 2012.

Thus, we think it is reasonable to expect the semiconductor companies to target the automotive market as their next potential revenue-growth driver. Global top-5 automotive semiconductor suppliers’ automotive revenue (2012-14)

Source: IHS

Note: *average percentage of global top 5 companies’ automotive semiconductor revenue compared to total revenue

As shown in the following chart, consultancy group IC Insights forecasts the automotive semiconductor market to record by far the strongest revenue growth among major industries from 2013-18E. CAGR of semiconductor market by end-user (2013-18E)

Source: IC Insights

The importance of in-vehicle embedded connectivity, alongside potential changes in safety regulations in major countries, is likely to underpin further growth in the automotive electronics market. For companies providing embedded connectivity, such as GM subsidiary On Star Corporation in the US and eCall in Europe, some governments, including the US, EU and Russia, have made it mandatory for new vehicles to ship with systems that automatically alert emergency services in the event of an accident. We note that smartphone-integration systems may not meet these requirements, since smartphones may run out of battery power before or even during accidents.

1 3 4

1015

20

3035

50

0

10

20

30

40

50

60

1950 1960 1970 1980 1990 2000 2010 2020F 2030F

(%)

1.7 1.8 2.11.5 1.6 1.9

3.4 2.9 3.0

2.2 2.42.7

1.9 2.02.1

26.8

28.4

30.5

26

27

28

29

30

31

0

2

4

6

8

10

12

14

2012 2013 2014

Freescale NXP Renesas Infineon ST Micro *% A/S revenue

(USDbn) (%)

USD10.6bn USD10.8bnUSD11.8bn

3.3

4.1

4.1

5.5

5.7

6.8

10.8

0 2 4 6 8 10 12

Computer

Government/Military

Consumer

Total

Industrial/Medical

Communication

Automotive

(%)

Pan-Asia Autos 26 June 2015

- 16 -

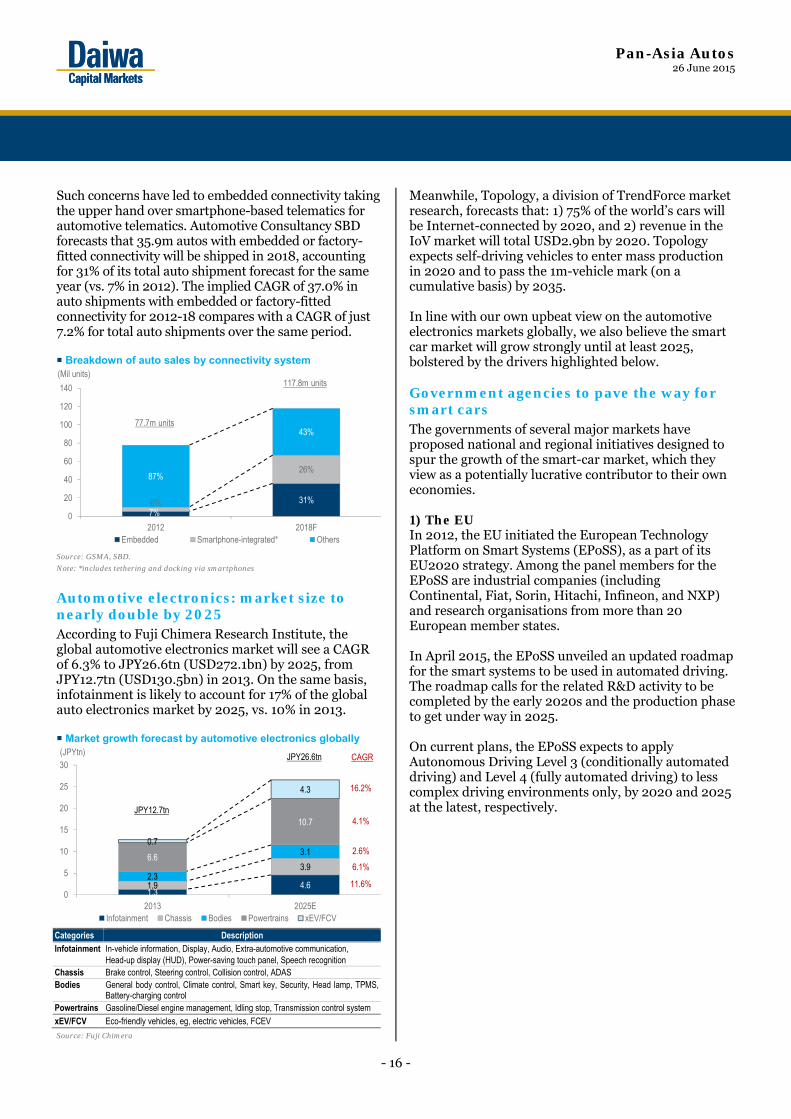

Such concerns have led to embedded connectivity taking the upper hand over smartphone-based telematics for automotive telematics. Automotive Consultancy SBD forecasts that 35.9m autos with embedded or factory-fitted connectivity will be shipped in 2018, accounting for 31% of its total auto shipment forecast for the same year (vs. 7% in 2012). The implied CAGR of 37.0% in auto shipments with embedded or factory-fitted connectivity for 2012-18 compares with a CAGR of just 7.2% for total auto shipments over the same period. Breakdown of auto sales by connectivity system

Source: GSMA, SBD.

Note: *includes tethering and docking via smartphones

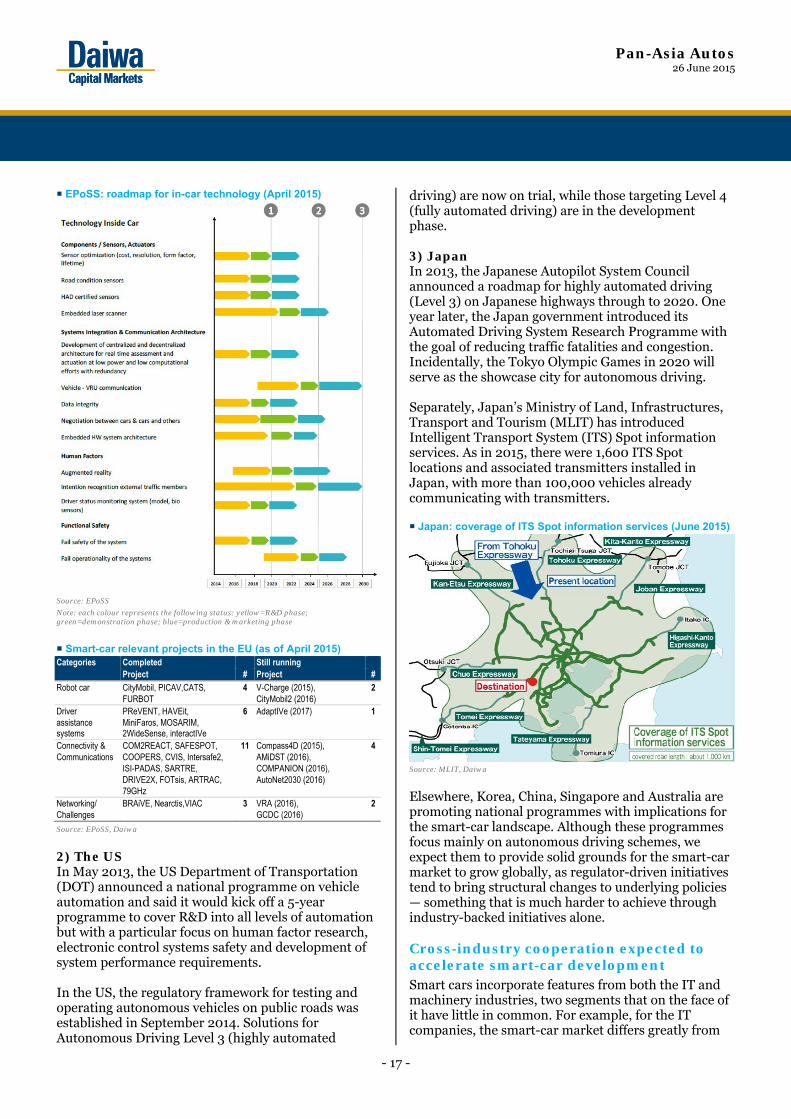

Automotive electronics: market size to nearly double by 2025 According to Fuji Chimera Research Institute, the global automotive electronics market will see a CAGR of 6.3% to JPY26.6tn (USD272.1bn) by 2025, from JPY12.7tn (USD130.5bn) in 2013. On the same basis, infotainment is likely to account for 17% of the global auto electronics market by 2025, vs. 10% in 2013. Market growth forecast by automotive electronics globally

Categories Description Infotainment In-vehicle information, Display, Audio, Extra-automotive communication,

Head-up display (HUD), Power-saving touch panel, Speech recognition Chassis Brake control, Steering control, Collision control, ADAS Bodies General body control, Climate control, Smart key, Security, Head lamp, TPMS,

Battery-charging control Powertrains Gasoline/Diesel engine management, Idling stop, Transmission control system xEV/FCV Eco-friendly vehicles, eg, electric vehicles, FCEV

Source: Fuji Chimera

Meanwhile, Topology, a division of TrendForce market research, forecasts that: 1) 75% of the world’s cars will be Internet-connected by 2020, and 2) revenue in the IoV market will total USD2.9bn by 2020. Topology expects self-driving vehicles to enter mass production in 2020 and to pass the 1m-vehicle mark (on a cumulative basis) by 2035. In line with our own upbeat view on the automotive electronics markets globally, we also believe the smart car market will grow strongly until at least 2025, bolstered by the drivers highlighted below. Government agencies to pave the way for smart cars The governments of several major markets have proposed national and regional initiatives designed to spur the growth of the smart-car market, which they view as a potentially lucrative contributor to their own economies. 1) The EU In 2012, the EU initiated the European Technology Platform on Smart Systems (EPoSS), as a part of its EU2020 strategy. Among the panel members for the EPoSS are industrial companies (including Continental, Fiat, Sorin, Hitachi, Infineon, and NXP) and research organisations from more than 20 European member states. In April 2015, the EPoSS unveiled an updated roadmap for the smart systems to be used in automated driving. The roadmap calls for the related R&D activity to be completed by the early 2020s and the production phase to get under way in 2025. On current plans, the EPoSS expects to apply Autonomous Driving Level 3 (conditionally automated driving) and Level 4 (fully automated driving) to less complex driving environments only, by 2020 and 2025 at the latest, respectively.

7%31%6%

26%87%

43%

0

20

40

60

80

100

120

140

2012 2018FEmbedded Smartphone-integrated* Others

(Mil units)

77.7m units

117.8m units

1.34.61.9

3.92.3

3.16.6

10.7

0.7

4.3

0

5

10

15

20

25

30

2013 2025EInfotainment Chassis Bodies Powertrains xEV/FCV

(JPYtn)

JPY12.7tn

JPY26.6tn CAGR

4.1%

2.6%

6.1%

11.6%

16.2%

Pan-Asia Autos 26 June 2015

- 17 -

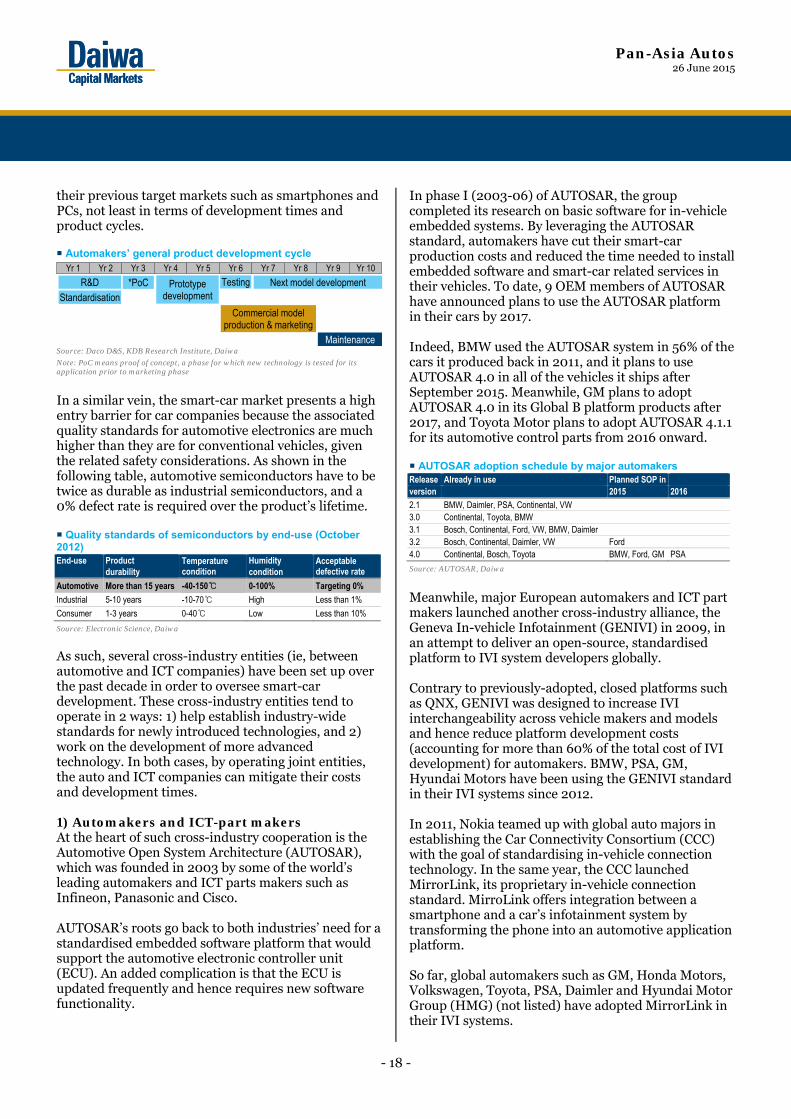

EPoSS: roadmap for in-car technology (April 2015)

Source: EPoSS

Note: each colour represents the following status: yellow=R&D phase; green=demonstration phase; blue=production & marketing phase

Smart-car relevant projects in the EU (as of April 2015) Categories Completed Still running

Project # Project # Robot car CityMobil, PICAV,CATS,

FURBOT 4 V-Charge (2015),

CityMobil2 (2016) 2

Driver assistance systems

PReVENT, HAVEit, MiniFaros, MOSARIM, 2WideSense, interactIVe

6 AdaptIVe (2017) 1

Connectivity & Communications

COM2REACT, SAFESPOT, COOPERS, CVIS, Intersafe2, ISI-PADAS, SARTRE, DRIVE2X, FOTsis, ARTRAC, 79GHz

11 Compass4D (2015), AMiDST (2016), COMPANION (2016), AutoNet2030 (2016)

4

Networking/ Challenges

BRAiVE, Nearctis,VIAC 3 VRA (2016), GCDC (2016)

2

Source: EPoSS, Daiwa

2) The US In May 2013, the US Department of Transportation (DOT) announced a national programme on vehicle automation and said it would kick off a 5-year programme to cover R&D into all levels of automation but with a particular focus on human factor research, electronic control systems safety and development of system performance requirements. In the US, the regulatory framework for testing and operating autonomous vehicles on public roads was established in September 2014. Solutions for Autonomous Driving Level 3 (highly automated

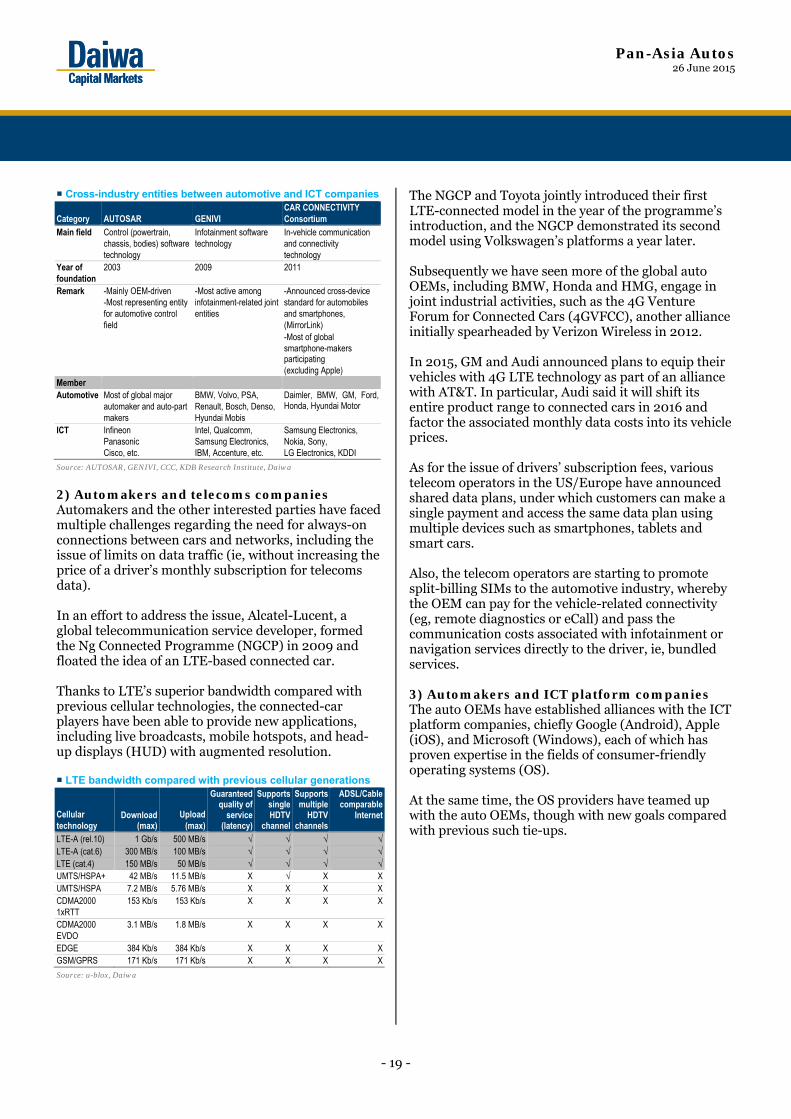

driving) are now on trial, while those targeting Level 4 (fully automated driving) are in the development phase. 3) Japan In 2013, the Japanese Autopilot System Council announced a roadmap for highly automated driving (Level 3) on Japanese highways through to 2020. One year later, the Japan government introduced its Automated Driving System Research Programme with the goal of reducing traffic fatalities and congestion. Incidentally, the Tokyo Olympic Games in 2020 will serve as the showcase city for autonomous driving. Separately, Japan’s Ministry of Land, Infrastructures, Transport and Tourism (MLIT) has introduced Intelligent Transport System (ITS) Spot information services. As in 2015, there were 1,600 ITS Spot locations and associated transmitters installed in Japan, with more than 100,000 vehicles already communicating with transmitters. Japan: coverage of ITS Spot information services (June 2015)

Source: MLIT, Daiwa

Elsewhere, Korea, China, Singapore and Australia are promoting national programmes with implications for the smart-car landscape. Although these programmes focus mainly on autonomous driving schemes, we expect them to provide solid grounds for the smart-car market to grow globally, as regulator-driven initiatives tend to bring structural changes to underlying policies — something that is much harder to achieve through industry-backed initiatives alone. Cross-industry cooperation expected to accelerate smart-car development Smart cars incorporate features from both the IT and machinery industries, two segments that on the face of it have little in common. For example, for the IT companies, the smart-car market differs greatly from

Pan-Asia Autos 26 June 2015

- 18 -

their previous target markets such as smartphones and PCs, not least in terms of development times and product cycles. Automakers’ general product development cycle

Source: Daco D&S, KDB Research Institute, Daiwa

Note: PoC means proof of concept, a phase for which new technology is tested for its application prior to marketing phase

In a similar vein, the smart-car market presents a high entry barrier for car companies because the associated quality standards for automotive electronics are much higher than they are for conventional vehicles, given the related safety considerations. As shown in the following table, automotive semiconductors have to be twice as durable as industrial semiconductors, and a 0% defect rate is required over the product’s lifetime. Quality standards of semiconductors by end-use (October 2012) End-use Product

durability Temperature condition

Humidity condition

Acceptable defective rate

Automotive More than 15 years -40-150℃ 0-100% Targeting 0%

Industrial 5-10 years -10-70℃ High Less than 1%

Consumer 1-3 years 0-40℃ Low Less than 10%

Source: Electronic Science, Daiwa

As such, several cross-industry entities (ie, between automotive and ICT companies) have been set up over the past decade in order to oversee smart-car development. These cross-industry entities tend to operate in 2 ways: 1) help establish industry-wide standards for newly introduced technologies, and 2) work on the development of more advanced technology. In both cases, by operating joint entities, the auto and ICT companies can mitigate their costs and development times. 1) Automakers and ICT-part makers At the heart of such cross-industry cooperation is the Automotive Open System Architecture (AUTOSAR), which was founded in 2003 by some of the world’s leading automakers and ICT parts makers such as Infineon, Panasonic and Cisco. AUTOSAR’s roots go back to both industries’ need for a standardised embedded software platform that would support the automotive electronic controller unit (ECU). An added complication is that the ECU is updated frequently and hence requires new software functionality.

In phase I (2003-06) of AUTOSAR, the group completed its research on basic software for in-vehicle embedded systems. By leveraging the AUTOSAR standard, automakers have cut their smart-car production costs and reduced the time needed to install embedded software and smart-car related services in their vehicles. To date, 9 OEM members of AUTOSAR have announced plans to use the AUTOSAR platform in their cars by 2017. Indeed, BMW used the AUTOSAR system in 56% of the cars it produced back in 2011, and it plans to use AUTOSAR 4.0 in all of the vehicles it ships after September 2015. Meanwhile, GM plans to adopt AUTOSAR 4.0 in its Global B platform products after 2017, and Toyota Motor plans to adopt AUTOSAR 4.1.1 for its automotive control parts from 2016 onward. AUTOSAR adoption schedule by major automakers Release Already in use Planned SOP in version 2015 2016

2.1 BMW, Daimler, PSA, Continental, VW 3.0 Continental, Toyota, BMW 3.1 Bosch, Continental, Ford, VW, BMW, Daimler 3.2 Bosch, Continental, Daimler, VW Ford 4.0 Continental, Bosch, Toyota BMW, Ford, GM PSA

Source: AUTOSAR, Daiwa

Meanwhile, major European automakers and ICT part makers launched another cross-industry alliance, the Geneva In-vehicle Infotainment (GENIVI) in 2009, in an attempt to deliver an open-source, standardised platform to IVI system developers globally. Contrary to previously-adopted, closed platforms such as QNX, GENIVI was designed to increase IVI interchangeability across vehicle makers and models and hence reduce platform development costs (accounting for more than 60% of the total cost of IVI development) for automakers. BMW, PSA, GM, Hyundai Motors have been using the GENIVI standard in their IVI systems since 2012. In 2011, Nokia teamed up with global auto majors in establishing the Car Connectivity Consortium (CCC) with the goal of standardising in-vehicle connection technology. In the same year, the CCC launched MirrorLink, its proprietary in-vehicle connection standard. MirroLink offers integration between a smartphone and a car’s infotainment system by transforming the phone into an automotive application platform. So far, global automakers such as GM, Honda Motors, Volkswagen, Toyota, PSA, Daimler and Hyundai Motor Group (HMG) (not listed) have adopted MirrorLink in their IVI systems.

Yr 2 Yr 3 Yr 4 Yr 5 Yr 6 Yr 7 Yr 8Yr 1 Yr 9 Yr 10

R&DStandardisation

*PoC Prototypedevelopment

Testing Next model development

Commercial model production & marketing

Maintenance

Pan-Asia Autos 26 June 2015

- 19 -

Cross-industry entities between automotive and ICT companies

Category AUTOSAR GENIVI CAR CONNECTIVITY Consortium

Main field Control (powertrain, chassis, bodies) software technology

Infotainment software technology

In-vehicle communication and connectivity technology

Year of foundation

2003 2009 2011

Remark -Mainly OEM-driven -Most representing entity for automotive control field

-Most active among infotainment-related joint entities

-Announced cross-device standard for automobiles and smartphones, (MirrorLink)

-Most of global smartphone-makers participating (excluding Apple)

Member Automotive Most of global major

automaker and auto-part makers

BMW, Volvo, PSA, Renault, Bosch, Denso, Hyundai Mobis

Daimler, BMW, GM, Ford, Honda, Hyundai Motor

ICT Infineon Panasonic Cisco, etc.

Intel, Qualcomm, Samsung Electronics, IBM, Accenture, etc.

Samsung Electronics, Nokia, Sony, LG Electronics, KDDI

Source: AUTOSAR, GENIVI, CCC, KDB Research Institute, Daiwa

2) Automakers and telecoms companies Automakers and the other interested parties have faced multiple challenges regarding the need for always-on connections between cars and networks, including the issue of limits on data traffic (ie, without increasing the price of a driver’s monthly subscription for telecoms data). In an effort to address the issue, Alcatel-Lucent, a global telecommunication service developer, formed the Ng Connected Programme (NGCP) in 2009 and floated the idea of an LTE-based connected car. Thanks to LTE’s superior bandwidth compared with previous cellular technologies, the connected-car players have been able to provide new applications, including live broadcasts, mobile hotspots, and head-up displays (HUD) with augmented resolution. LTE bandwidth compared with previous cellular generations

Cellular technology

Download (max)

Upload (max)

Guaranteed quality of

service (latency)

Supports single HDTV

channel

Supports multiple

HDTV channels

ADSL/Cable comparable

Internet

LTE-A (rel.10) 1 Gb/s 500 MB/s √ √ √ √LTE-A (cat.6) 300 MB/s 100 MB/s √ √ √ √LTE (cat.4) 150 MB/s 50 MB/s √ √ √ √UMTS/HSPA+ 42 MB/s 11.5 MB/s X √ X XUMTS/HSPA 7.2 MB/s 5.76 MB/s X X X XCDMA2000 1xRTT

153 Kb/s 153 Kb/s X X X X

CDMA2000 EVDO

3.1 MB/s 1.8 MB/s X X X X

EDGE 384 Kb/s 384 Kb/s X X X XGSM/GPRS 171 Kb/s 171 Kb/s X X X X

Source: u-blox, Daiwa

The NGCP and Toyota jointly introduced their first LTE-connected model in the year of the programme’s introduction, and the NGCP demonstrated its second model using Volkswagen’s platforms a year later. Subsequently we have seen more of the global auto OEMs, including BMW, Honda and HMG, engage in joint industrial activities, such as the 4G Venture Forum for Connected Cars (4GVFCC), another alliance initially spearheaded by Verizon Wireless in 2012. In 2015, GM and Audi announced plans to equip their vehicles with 4G LTE technology as part of an alliance with AT&T. In particular, Audi said it will shift its entire product range to connected cars in 2016 and factor the associated monthly data costs into its vehicle prices. As for the issue of drivers’ subscription fees, various telecom operators in the US/Europe have announced shared data plans, under which customers can make a single payment and access the same data plan using multiple devices such as smartphones, tablets and smart cars. Also, the telecom operators are starting to promote split-billing SIMs to the automotive industry, whereby the OEM can pay for the vehicle-related connectivity (eg, remote diagnostics or eCall) and pass the communication costs associated with infotainment or navigation services directly to the driver, ie, bundled services. 3) Automakers and ICT platform companies The auto OEMs have established alliances with the ICT platform companies, chiefly Google (Android), Apple (iOS), and Microsoft (Windows), each of which has proven expertise in the fields of consumer-friendly operating systems (OS). At the same time, the OS providers have teamed up with the auto OEMs, though with new goals compared with previous such tie-ups.

Pan-Asia Autos 26 June 2015

- 20 -

Cross-industry entities between automotive and ICT companies [2]

Google Apple Microsoft

Smart-car platform OAA CarPlay Window Automotive Concept Industrial alliance

seeking to develop Android-based automotive OS

Seeking to link its products to automobiles

Similar to CarPlay

Year of commercialisation

1H14 2H14 On progress

Automotive alliances

GM, Ford, FCA, Audi, Nissan, Honda, Hyundai/Kia Motors,

BMW, Toyota, Ford, Hyundai Motor

FCA

Characteristics Competing with OEM-developed OS

Seeking industrial cooperation with global OEMs

Less market-leading than Google/Apple

Source: OAA, Apple, Microsoft, KDB Research Institute, Daiwa

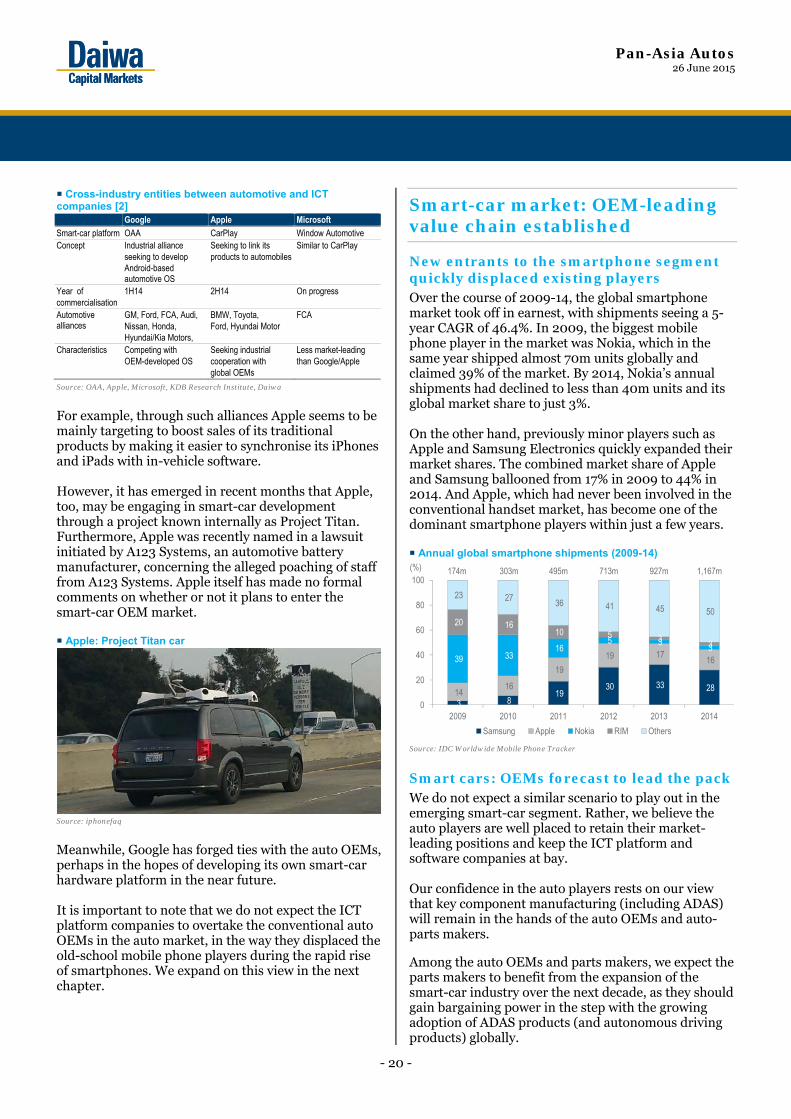

For example, through such alliances Apple seems to be mainly targeting to boost sales of its traditional products by making it easier to synchronise its iPhones and iPads with in-vehicle software. However, it has emerged in recent months that Apple, too, may be engaging in smart-car development through a project known internally as Project Titan. Furthermore, Apple was recently named in a lawsuit initiated by A123 Systems, an automotive battery manufacturer, concerning the alleged poaching of staff from A123 Systems. Apple itself has made no formal comments on whether or not it plans to enter the smart-car OEM market. Apple: Project Titan car

Source: iphonefaq

Meanwhile, Google has forged ties with the auto OEMs, perhaps in the hopes of developing its own smart-car hardware platform in the near future. It is important to note that we do not expect the ICT platform companies to overtake the conventional auto OEMs in the auto market, in the way they displaced the old-school mobile phone players during the rapid rise of smartphones. We expand on this view in the next chapter.

Smart-car market: OEM-leading value chain established

New entrants to the smartphone segment quickly displaced existing players Over the course of 2009-14, the global smartphone market took off in earnest, with shipments seeing a 5-year CAGR of 46.4%. In 2009, the biggest mobile phone player in the market was Nokia, which in the same year shipped almost 70m units globally and claimed 39% of the market. By 2014, Nokia’s annual shipments had declined to less than 40m units and its global market share to just 3%. On the other hand, previously minor players such as Apple and Samsung Electronics quickly expanded their market shares. The combined market share of Apple and Samsung ballooned from 17% in 2009 to 44% in 2014. And Apple, which had never been involved in the conventional handset market, has become one of the dominant smartphone players within just a few years. Annual global smartphone shipments (2009-14)

Source: IDC Worldwide Mobile Phone Tracker

Smart cars: OEMs forecast to lead the pack We do not expect a similar scenario to play out in the emerging smart-car segment. Rather, we believe the auto players are well placed to retain their market-leading positions and keep the ICT platform and software companies at bay. Our confidence in the auto players rests on our view that key component manufacturing (including ADAS) will remain in the hands of the auto OEMs and auto-parts makers.

Among the auto OEMs and parts makers, we expect the parts makers to benefit from the expansion of the smart-car industry over the next decade, as they should gain bargaining power in the step with the growing adoption of ADAS products (and autonomous driving products) globally.

3 8 19

30 33 28 14 16

19

19 17 16 39 33

16 5 3

3

20 16 10 5 3

3

23 27 36 41 45 50

0

20

40

60

80

100

2009 2010 2011 2012 2013 2014

Samsung Apple Nokia RIM Others

174m 303m 495m 713m 927m 1,167m(%)

Pan-Asia Autos 26 June 2015

- 21 -

However, if we extend our time horizon beyond a decade, we believe the auto OEMs have the potential to integrate all of the relevant platforms into the production chains. First, we examine how we expect the automotive players to protect their leading positions from non-automotive players in the smart-car industry. Automotive players: more patent applications, higher R&D spending As shown in the chart below, the software & Internet industry recorded the highest growth in R&D expenses in 2014 (vs. 2013) among major industries globally, according to Strategy & Analytics. Change in R&D spending by industry (2013-14)

Source: Strategy & Analysis, Daiwa

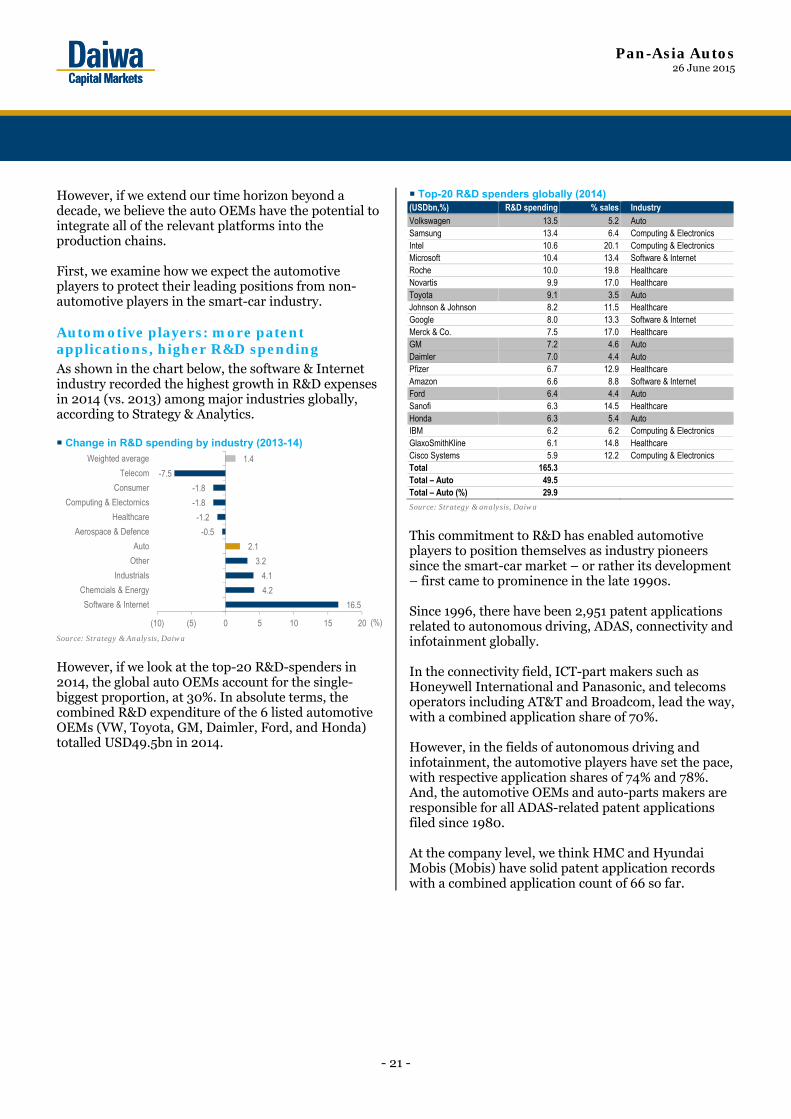

However, if we look at the top-20 R&D-spenders in 2014, the global auto OEMs account for the single-biggest proportion, at 30%. In absolute terms, the combined R&D expenditure of the 6 listed automotive OEMs (VW, Toyota, GM, Daimler, Ford, and Honda) totalled USD49.5bn in 2014.

Top-20 R&D spenders globally (2014) (USDbn,%) R&D spending % sales Industry Volkswagen 13.5 5.2 Auto Samsung 13.4 6.4 Computing & Electronics Intel 10.6 20.1 Computing & Electronics Microsoft 10.4 13.4 Software & Internet Roche 10.0 19.8 Healthcare Novartis 9.9 17.0 Healthcare Toyota 9.1 3.5 Auto Johnson & Johnson 8.2 11.5 Healthcare Google 8.0 13.3 Software & Internet Merck & Co. 7.5 17.0 Healthcare GM 7.2 4.6 Auto Daimler 7.0 4.4 Auto Pfizer 6.7 12.9 Healthcare Amazon 6.6 8.8 Software & Internet Ford 6.4 4.4 Auto Sanofi 6.3 14.5 Healthcare Honda 6.3 5.4 Auto IBM 6.2 6.2 Computing & Electronics GlaxoSmithKline 6.1 14.8 Healthcare Cisco Systems 5.9 12.2 Computing & Electronics Total 165.3 Total – Auto 49.5 Total – Auto (%) 29.9

Source: Strategy & analysis, Daiwa

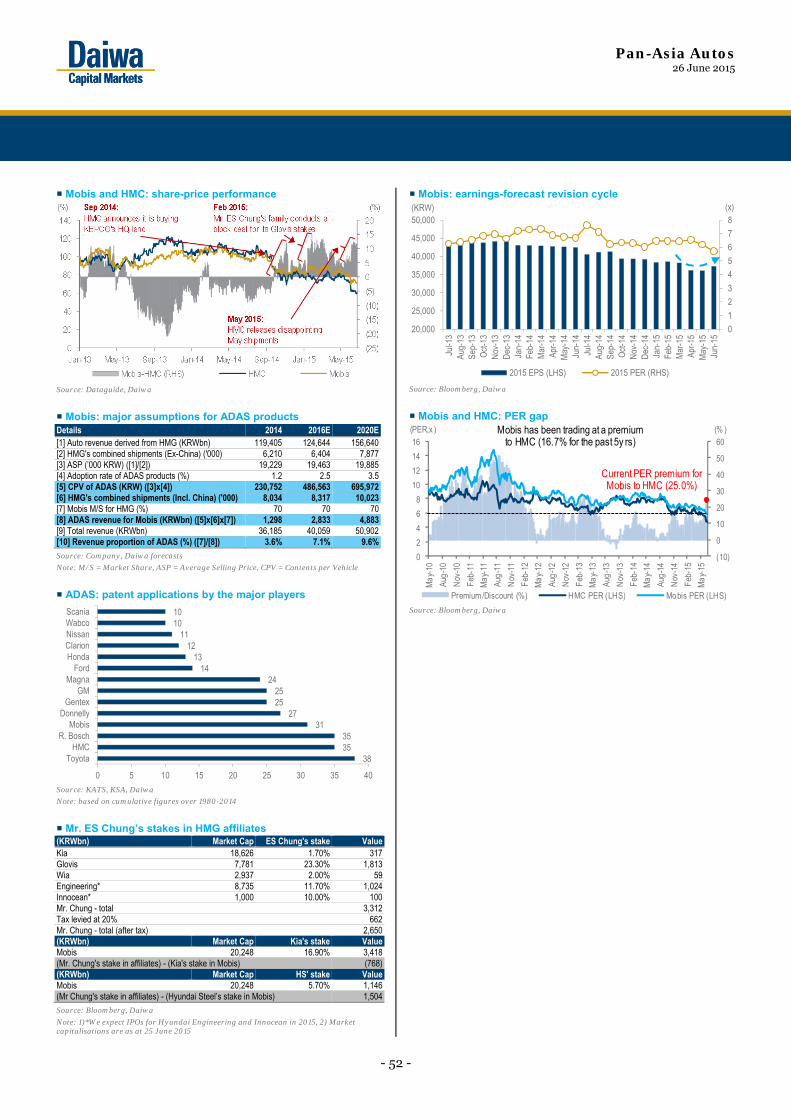

This commitment to R&D has enabled automotive players to position themselves as industry pioneers since the smart-car market – or rather its development – first came to prominence in the late 1990s. Since 1996, there have been 2,951 patent applications related to autonomous driving, ADAS, connectivity and infotainment globally. In the connectivity field, ICT-part makers such as Honeywell International and Panasonic, and telecoms operators including AT&T and Broadcom, lead the way, with a combined application share of 70%. However, in the fields of autonomous driving and infotainment, the automotive players have set the pace, with respective application shares of 74% and 78%. And, the automotive OEMs and auto-parts makers are responsible for all ADAS-related patent applications filed since 1980. At the company level, we think HMC and Hyundai Mobis (Mobis) have solid patent application records with a combined application count of 66 so far.

16.5

4.2

4.1

3.2

2.1

-0.5

-1.2

-1.8

-1.8

-7.5

1.4

(10) (5) 0 5 10 15 20

Software & Internet

Chemcials & Energy

Industrials

Other

Auto

Aerospace & Defence

Healthcare

Computing & Electornics

Consumer

Telecom

Weighted average

(%)

Pan-Asia Autos 26 June 2015

- 22 -

Patent application trend by smart-car features

Source: KATS, KSA, Daiwa

Note: *patents applied during 2013-14 are not fully disclosed yet

Patent application composition by candidate’s field

Source: KATS, KSA, Daiwa

Note: based on cumulative figures during 1980-2014

ADAS: auto-parts makers to take the lead As mentioned earlier, we view ADAS as the core component in the smart-car product market on the basis that autonomous driving will be front and centre in the rise of smart cars over the next decade. In 2010, according to the Strategy Analytics, the global ADAS market accounted for only 2.0% and 7.9% of the smart-car market and automotive electronics market, respectively (See Appendix 3 for category composition.) However, we expect ADAS to grow in its significance to the overall smart-car market, backed by: 1) new regulatory requirements mandated by major governments, including the US and the EU, 2) automakers adopting more ADAS features in order to differentiate themselves, and 3) potentially lower insurance costs as ADAS products are installed in vehicles.

US and EU: mandatory active safety regulations The US EU

Mandated NCAP IIHS Mandated NCAP 2013 FCW AEB FCW 2014 AEB, LKA 2015 AEB AEB 2016 AEB+PD 2017 FCW, LDW FCW, LDW

Source: Various press reports globally (ie, US NCAP, IIHS, EU NCAP), Daiwa

Note: PD = pedestrian detection

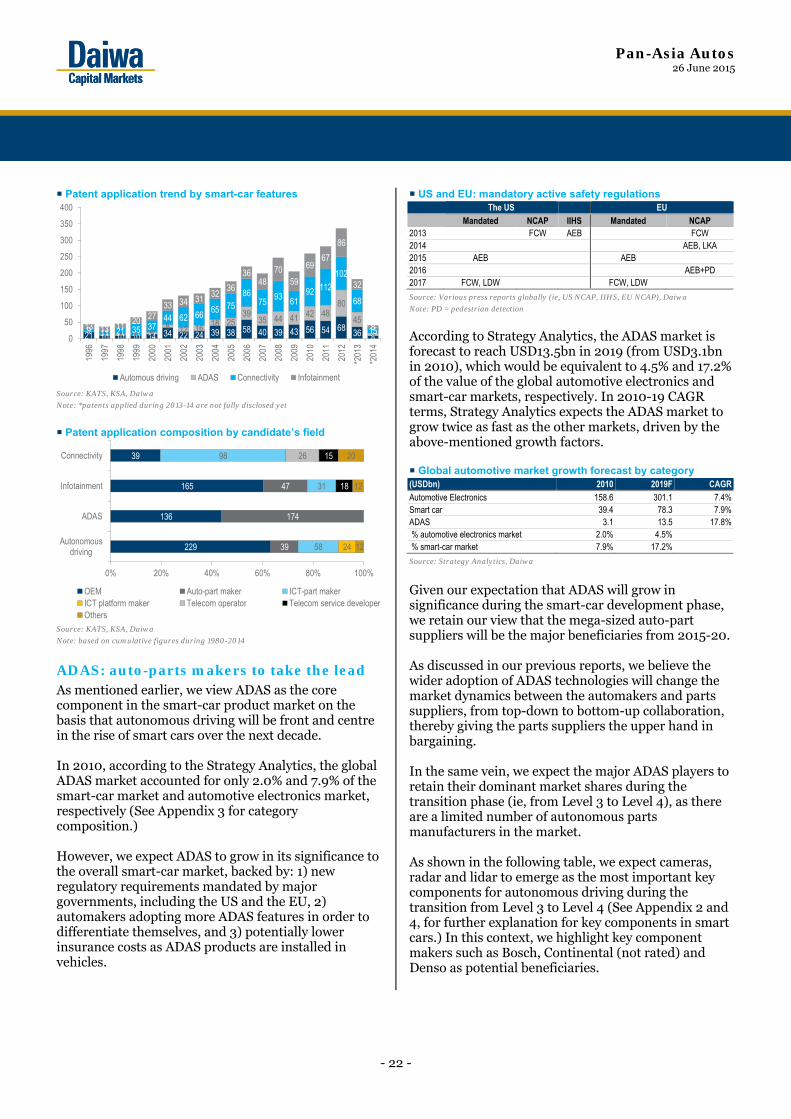

According to Strategy Analytics, the ADAS market is forecast to reach USD13.5bn in 2019 (from USD3.1bn in 2010), which would be equivalent to 4.5% and 17.2% of the value of the global automotive electronics and smart-car markets, respectively. In 2010-19 CAGR terms, Strategy Analytics expects the ADAS market to grow twice as fast as the other markets, driven by the above-mentioned growth factors. Global automotive market growth forecast by category (USDbn) 2010 2019F CAGRAutomotive Electronics 158.6 301.1 7.4%Smart car 39.4 78.3 7.9%ADAS 3.1 13.5 17.8% % automotive electronics market 2.0% 4.5% % smart-car market 7.9% 17.2%

Source: Strategy Analytics, Daiwa

Given our expectation that ADAS will grow in significance during the smart-car development phase, we retain our view that the mega-sized auto-part suppliers will be the major beneficiaries from 2015-20. As discussed in our previous reports, we believe the wider adoption of ADAS technologies will change the market dynamics between the automakers and parts suppliers, from top-down to bottom-up collaboration, thereby giving the parts suppliers the upper hand in bargaining. In the same vein, we expect the major ADAS players to retain their dominant market shares during the transition phase (ie, from Level 3 to Level 4), as there are a limited number of autonomous parts manufacturers in the market. As shown in the following table, we expect cameras, radar and lidar to emerge as the most important key components for autonomous driving during the transition from Level 3 to Level 4 (See Appendix 2 and 4, for further explanation for key components in smart cars.) In this context, we highlight key component makers such as Bosch, Continental (not rated) and Denso as potential beneficiaries.

21 10 10 10 14 34 22 24 39 38 58 40 39 43 56 54 68 36 81 2 3 0 5

8 12 16 18 2539

35 44 41 42 4880

45

99 11 21 35 3744 62 66

65 7586

7593 61

92 112

102

68

1513 13 11 20 2733 34 31

3236

3648

7059

6967

86

32

80

50

100

150

200

250

300

350

400

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

*201

3

*201

4Automous driving ADAS Connectivity Infotainment

229

136

165

39

39

174

47

58

31

98

24

26

18

15

12

12

20

0% 20% 40% 60% 80% 100%

Autonomousdriving

ADAS

Infotainment

Connectivity

OEM Auto-part maker ICT-part makerICT platform maker Telecom operator Telecom service developerOthers

Pan-Asia Autos 26 June 2015

- 23 -

Core systems for fully automated vehicles

Level of automation Assistance

(Lv. 1)

Semi-automated

(Lv. 2)

Highly Automated

(Lv. 3)

Fully Automated

(Lv. 4) Adaptive headlamp control Optional Optional Imperative Optional Radar Imperative Imperative Imperative Imperative Ultrasonic sensors Optional Imperative Imperative Imperative Forward-looking camera Imperative Imperative Imperative Imperative Rear-vision camera Optional Imperative Imperative Imperative Surround view camera Optional Imperative Imperative Imperative Night vision Optional Optional Imperative Imperative Lidar Optional Optional Imperative Imperative Map-supported ADAS Optional Optional Imperative Imperative Steering & braking automation Optional Imperative Imperative Imperative Artificial intelligence Optional Optional Optional Imperative Multiple redundancies Optional Optional Optional Imperative Self-healing systems Optional Optional Optional Imperative

Source: KATECH, Daiwa

Smart-car components: major manufacturers

Company 24Ghz radar

77Ghz radar

Lidar Laser scanner

IR sensor

Ultra-sonic

Mono. camera

Stereo camera

Bosch - √ - - √ √ √ √Continental √ √ √ - √ - √ √Denso - √ - - - √ √ √Delphi √ √ - - - - √ -TRW √ √ - - - - √ -Autoliv √ √ - - √ - √ √Valeo √ - - √ - √ √ -Hella √ - - - - - √ -

Source: Companies, Daiwa

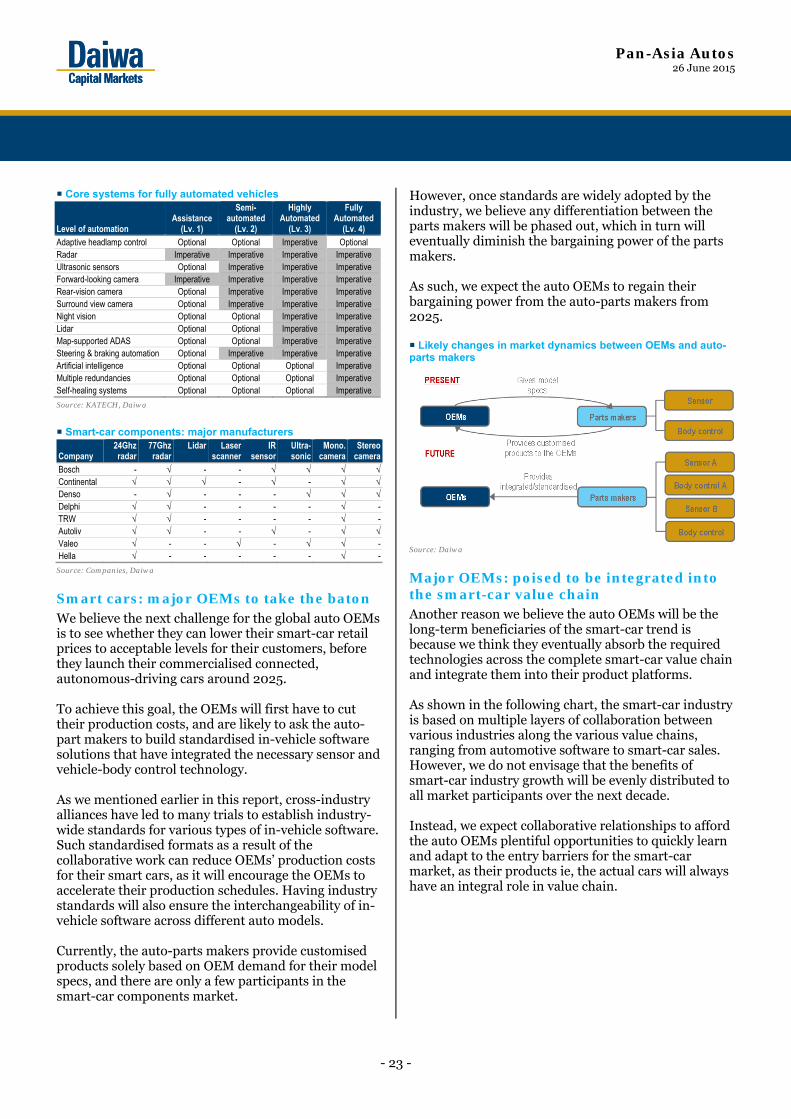

Smart cars: major OEMs to take the baton We believe the next challenge for the global auto OEMs is to see whether they can lower their smart-car retail prices to acceptable levels for their customers, before they launch their commercialised connected, autonomous-driving cars around 2025. To achieve this goal, the OEMs will first have to cut their production costs, and are likely to ask the auto-part makers to build standardised in-vehicle software solutions that have integrated the necessary sensor and vehicle-body control technology. As we mentioned earlier in this report, cross-industry alliances have led to many trials to establish industry-wide standards for various types of in-vehicle software. Such standardised formats as a result of the collaborative work can reduce OEMs’ production costs for their smart cars, as it will encourage the OEMs to accelerate their production schedules. Having industry standards will also ensure the interchangeability of in-vehicle software across different auto models. Currently, the auto-parts makers provide customised products solely based on OEM demand for their model specs, and there are only a few participants in the smart-car components market.

However, once standards are widely adopted by the industry, we believe any differentiation between the parts makers will be phased out, which in turn will eventually diminish the bargaining power of the parts makers. As such, we expect the auto OEMs to regain their bargaining power from the auto-parts makers from 2025. Likely changes in market dynamics between OEMs and auto-parts makers

Source: Daiwa

Major OEMs: poised to be integrated into the smart-car value chain Another reason we believe the auto OEMs will be the long-term beneficiaries of the smart-car trend is because we think they eventually absorb the required technologies across the complete smart-car value chain and integrate them into their product platforms. As shown in the following chart, the smart-car industry is based on multiple layers of collaboration between various industries along the various value chains, ranging from automotive software to smart-car sales. However, we do not envisage that the benefits of smart-car industry growth will be evenly distributed to all market participants over the next decade. Instead, we expect collaborative relationships to afford the auto OEMs plentiful opportunities to quickly learn and adapt to the entry barriers for the smart-car market, as their products ie, the actual cars will always have an integral role in value chain.

Pan-Asia Autos 26 June 2015

- 24 -

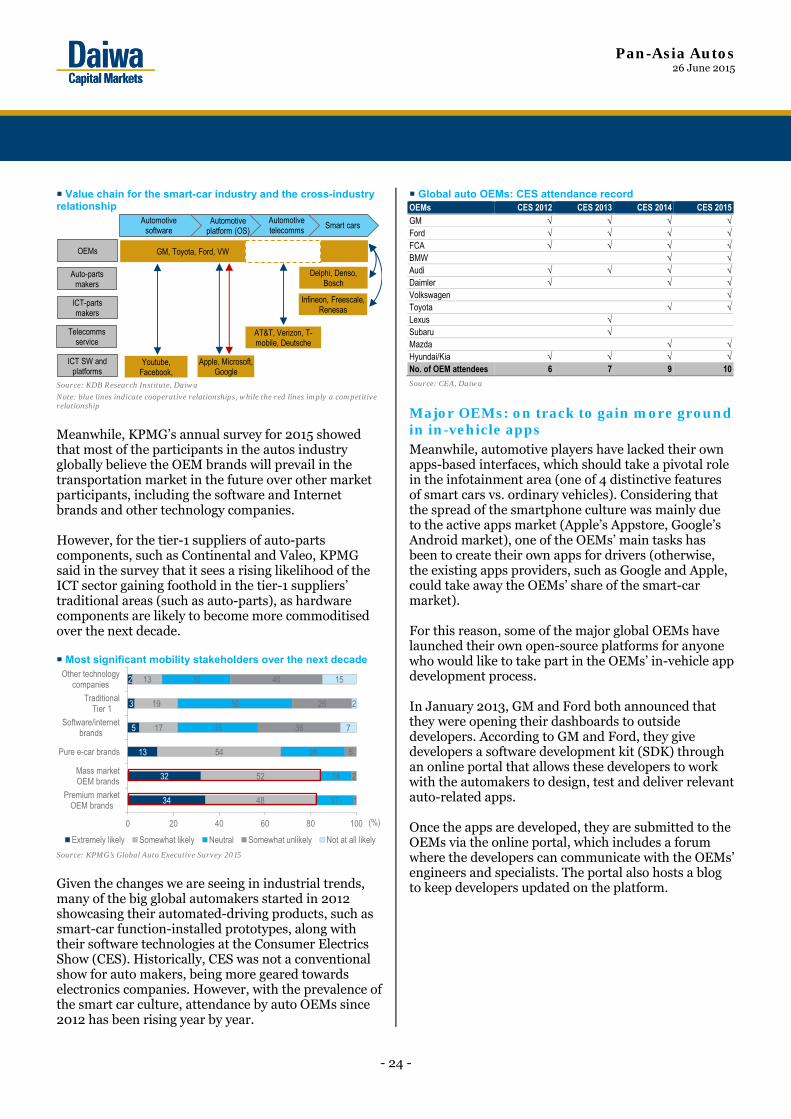

Value chain for the smart-car industry and the cross-industry relationship

Source: KDB Research Institute, Daiwa

Note: blue lines indicate cooperative relationships, while the red lines imply a competitive relationship

Meanwhile, KPMG’s annual survey for 2015 showed that most of the participants in the autos industry globally believe the OEM brands will prevail in the transportation market in the future over other market participants, including the software and Internet brands and other technology companies. However, for the tier-1 suppliers of auto-parts components, such as Continental and Valeo, KPMG said in the survey that it sees a rising likelihood of the ICT sector gaining foothold in the tier-1 suppliers’ traditional areas (such as auto-parts), as hardware components are likely to become more commoditised over the next decade. Most significant mobility stakeholders over the next decade

Source: KPMG’s Global Auto Executive Survey 2015

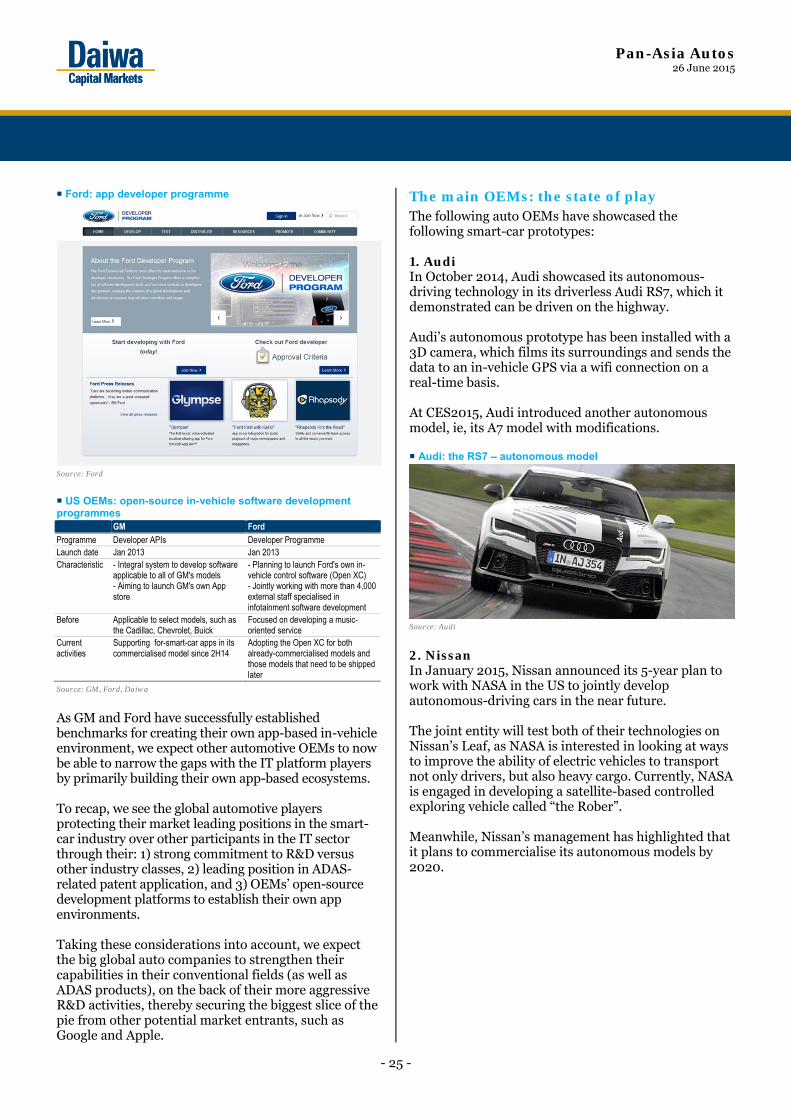

Given the changes we are seeing in industrial trends, many of the big global automakers started in 2012 showcasing their automated-driving products, such as smart-car function-installed prototypes, along with their software technologies at the Consumer Electrics Show (CES). Historically, CES was not a conventional show for auto makers, being more geared towards electronics companies. However, with the prevalence of the smart car culture, attendance by auto OEMs since 2012 has been rising year by year.

Global auto OEMs: CES attendance record OEMs CES 2012 CES 2013 CES 2014 CES 2015GM √ √ √ √Ford √ √ √ √FCA √ √ √ √BMW √ √Audi √ √ √ √Daimler √ √ √Volkswagen √Toyota √ √Lexus √ Subaru √ Mazda √ √Hyundai/Kia √ √ √ √No. of OEM attendees 6 7 9 10

Source: CEA, Daiwa