sidbi msfc

TRANSCRIPT

Roles and Function of SIDBI and

MSFC in Industrial Finance

SMALL INDUSTRIES

DEVELOPMENT BANK OF

INDIA

Introduction

The Government of India set up the SIDBI under aspecial Act of the Parliament in October 1989.

SIDBI commenced its operations from April 2, 1990with its head office in Lucknow.

SIDBI has been setup as a wholly owned subsidiaryof IDBI.

It is the apex institution which oversees, co-ordinates& further strengthens various arrangements forproviding financial and non-financial assistance tomeidum and small scale industries.

Objectives

Four basic objectives are set out in the SIDBI Charter.

Financing

Promotion

Development

Co-ordination

Functions

To promote and finance small scale industrial units

To implement government plans and projects concerned with development of small scale units

To provide seed capital and technical support to the start ups (SIDBI has a separate entity called SIDBI ventures set up for this purpose.)

To coordinate with other players for the promotion of specific sectors/regions (collaboration with World Bank on promotion of environment friendly industrial units, specific plans for poorest states of the country)

Business Domain of SIDBI

About 3.1 million small units, employing 17.2 million persons account for a share of 36 per cent of India's exports and 40 per cent of industrial manufacture.

In addition, SIDBI's assistance flows to the transport, health care and tourism sectors and also to the professional and self-employed persons setting up small-sized professional ventures.

Products & Services

Direct financeBills financeRefinance International financePromotional & Development activitiesFixed deposit schemeTechnology Up gradation & Modernization Fund

Scheme {TDMF}Venture Capital Fund Scheme Seed Money SchemesNational Equity Fund Scheme

Direct Finance

Since its beginning, SIDBI had been providing refinance to State Level Finance Corporations / State Industrial Development Corporations / Banks etc., against their loans granted to small scale units.

SIDBI’s direct finance schemes are:Scheme for expansion / diversification of

small scale units.Scheme for specialized marketing agencies.Scheme for unclearing / subcontract units.

Bills Finance Schemes

Bills Finance Scheme involves provision of medium and short-term finance for the benefit of the small-scale sector.

Bills Finance seeks to provide finance, to manufacturers of indigenous machinery, capital equipment, components sub-assemblies etc, based on compliance to the various eligibility criteria, norms etc. as applicable to the respective schemes.

To be eligible under the various bills schemes, one of the parties to the transactions to the scheme has to be an industrial unit in the small-scale sector.

Refinance Schemes

Under the scheme, SIDBI grants refinance againstterm loans granted by the eligible PLIs to industrialconcerns for setting up industrial projects in the smallscale sector as also for their expansion /modernisation / diversification.

Schemes of re-finance assistence:Scheme for SC-ST & physically handicraft personsComposite loan schemeEquipment refinance schemes.Schemes for small road transport operators.Special assistence to ex-servicemen.

International Finance Schemes

The main objective of the various InternationalFinance schemes is to enable small-scale industries toraise finance at internationally competitive rates tofulfill their export commitments.

The financial assistance is being offered in USDollars and Euro currencies. Assistance in Rupees isalso provided to the needy borrowers.

Need based limit, depending on the normal tradeterms and credit period given to overseas buyers byexporters not exceeding 180 days.

Fixed Deposit Scheme

The Interest Rate Structure for SIDBI Fixed Deposit Scheme of SIDBI are as under:

Time period

Revised Annual Interest

Rate %p.a. * w.e.f August

10, 2009

Interest (% p.a.)

12 months - 13 months 6.50

14 months - 36 months 7.00

14 months - 36 months 7.50

For Senior

Citizens

7.0

7.5

8.0

Promotional and Development

Activities

As an apex financial institution for promotion,

financing and development of industry in the small

scale sector, SIDBI meets the varied developmental

needs of the Indian SSI sector by its wide-ranging

Promotional and Developmental (P&D) activities.

The activities are as follows:

Entrepreneurship Development Programs.

Management Development Programs.

Technology Up gradation Programs.

Technology Up gradation &

Modernization Fund Scheme {TDMF}

This fund was setup in the year 1996 by the SIDBIwith an initial capital of 200 crores.

It was setup for the purpose of encouraging theexisting small scale industrial units to modernizeproduction facilities and adopt improved and updatedtechnology for strengthening export capabilities.

For availing benefits under this scheme the unit haveto prepare an estimate for modernization & submit itto SIDBI.

The sanction of funds is made depending upon theestimate submitted.

Venture Capital Fund Scheme

SIDBI is participating in the Venture capitalfund set by public sector institutions as well asprivate companies to the extent of Rs.50,00,000 of total capital of the fund required.

The fund should be dedicated to financingsmall industry preferably the most risky one.

Seed Money Schemes

One of the constraints faced by Entrepreneurs

is the lack of own resources to promote the

minimum promoter contribution.

Hence, SIDBI introduced seed money scheme

for the benefit of entrepreneurs.

Seed money is available through DIC{Direct

Industry Centre} to those entrepreneur who are

technically qualified but lack of own capital.

Maharashtra State Financial

Corporation (MSFC)

PROFILE

The Maharashtra State Financial Corporation(MSFC) has been set up under the ‘State FinancialCorporations (SFCs) Act 1951’.

The Corporation has been operating in the State ofMaharashtra since 1962 and in the State of Goa andthe Union Territory of Daman and Diu since 1964.

MSFC is a highly decentralized organization and hasnetwork of offices in all the districts of Maharashtraand Goa except Gadchiroli. MSFC has nine regionaloffices and twenty branch offices.

Functions and Objectives

The main function of MSFC is to meet the term loan

requirements of small and medium scale industries for

acquisition of fixed assets like land, building, machinery

and equipments.

The loans are given for setting up new industrial units as

well as for expansion and modernization of the existing

units.

The objective of the Corporation is to promote more

industries in backward and developing areas of

Maharashtra, Goa and Union Territory of Daman & Diu.

Eligible Industries

Most of the industrial activities such as

Manufacturing, Assembling, Servicing, Processing,

Preservation, Transportation, Setting - up Industrial

Estates, Road Construction etc.

Small Nursing Homes, Hotels, Restaurants, Tourism

Related Activities

Medical Practitioners, Qualified Professionals.

Major schemes

General Loan

Equipment Finance

Small Nursing Homes

Electro - Medical Equipment for Medical Practitioners

Hotels, Restaurants & Tourism Related Activities

Mahila Udyan Nidhi

National Equity Fund

Technology Development & Modernization

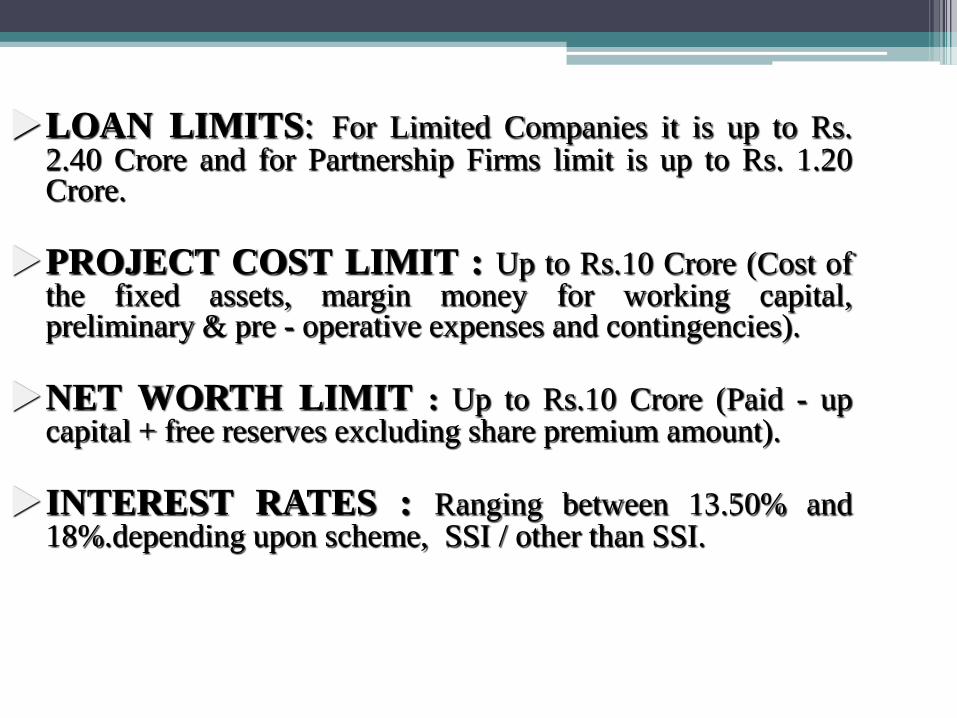

LOAN LIMITS: For Limited Companies it is up to Rs.2.40 Crore and for Partnership Firms limit is up to Rs. 1.20Crore.

PROJECT COST LIMIT : Up to Rs.10 Crore (Cost ofthe fixed assets, margin money for working capital,preliminary & pre - operative expenses and contingencies).

NET WORTH LIMIT : Up to Rs.10 Crore (Paid - upcapital + free reserves excluding share premium amount).

INTEREST RATES : Ranging between 13.50% and18%.depending upon scheme, SSI / other than SSI.

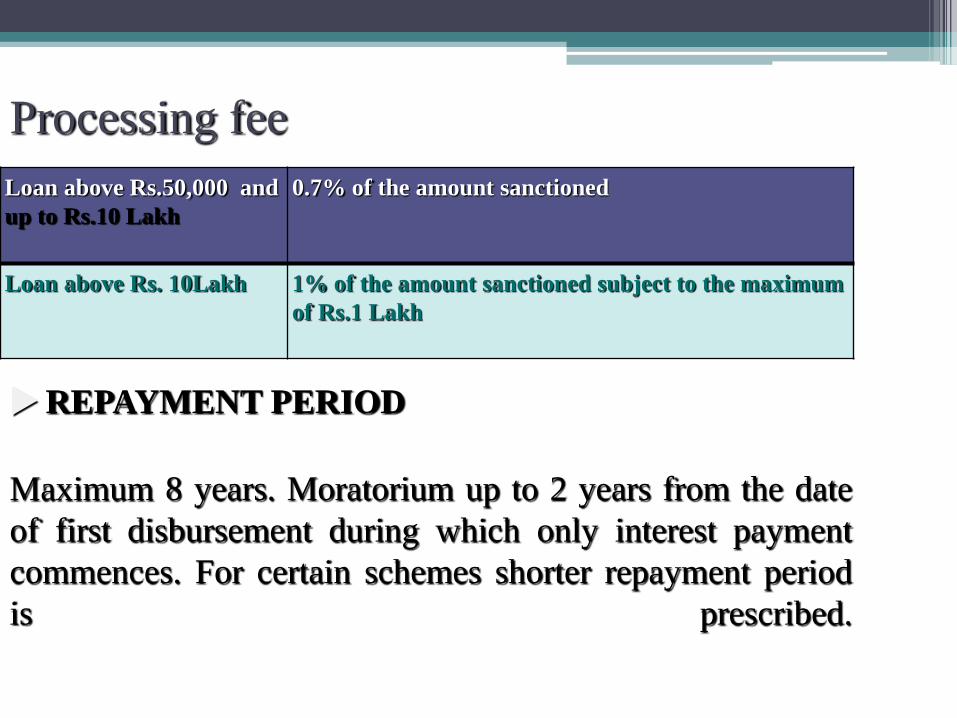

Processing fee

Loan above Rs.50,000 and

up to Rs.10 Lakh

0.7% of the amount sanctioned

Loan above Rs. 10Lakh 1% of the amount sanctioned subject to the maximum

of Rs.1 Lakh

REPAYMENT PERIOD

Maximum 8 years. Moratorium up to 2 years from the date

of first disbursement during which only interest payment

commences. For certain schemes shorter repayment period

is prescribed.

Special Features

No separate Interest Tax Guarantee Fee, ServiceCharge, Inspection Fee, Compulsory Purchase ofShares, etc.

Facility to pay the quarterly Interest within 15 daysfrom the date of calculation

Decentralization of Sanctioning & Disbursementpowers.

Need - based additional loans and facilities fordeserving units.

Longer Moratorium and Repayment Period.

References

http://agritech.tnau.ac.in/banking/crbank_sidbi%20-

%20intro.html#top

http://www.sidbi.com/

THANK YOU