seizing the small business rdc opportunity - mitek · seizing the small business rdc opportunity...

TRANSCRIPT

SEIZING THE SMALL BUSINESS RDC OPPORTUNITY NEW PRODUCTS ARE CHANGING EVERYTHING

Bob Meara June 2015

This report was prepared by Celent for Mitek Systems. Mitek has unlimited distribution rights, but had no input on the content of the analysis in the report. www.miteksystems.com

CONTENTS

Executive Summary ............................................................................................................ 1 Key Research Questions ................................................................................................. 1

Why Small Business RDC Matters ..................................................................................... 3 Opportunity Knocks ............................................................................................................. 8

A Product for Today ....................................................................................................... 12 Solution Landscape ........................................................................................................... 15

Vendor Listing ................................................................................................................ 17 Conclusion......................................................................................................................... 22 Leveraging Celent’s Expertise .......................................................................................... 23

Support for Financial Institutions ................................................................................... 23 Support for Vendors ...................................................................................................... 23

Related Celent Research .................................................................................................. 24

EXECUTIVE SUMMARY

KEY RESEARCH QUESTIONS

1 Why has small business RDC become more important to banks?

2 What has inhibited adoption historically? 3 How have new

vendor solutions changed things?

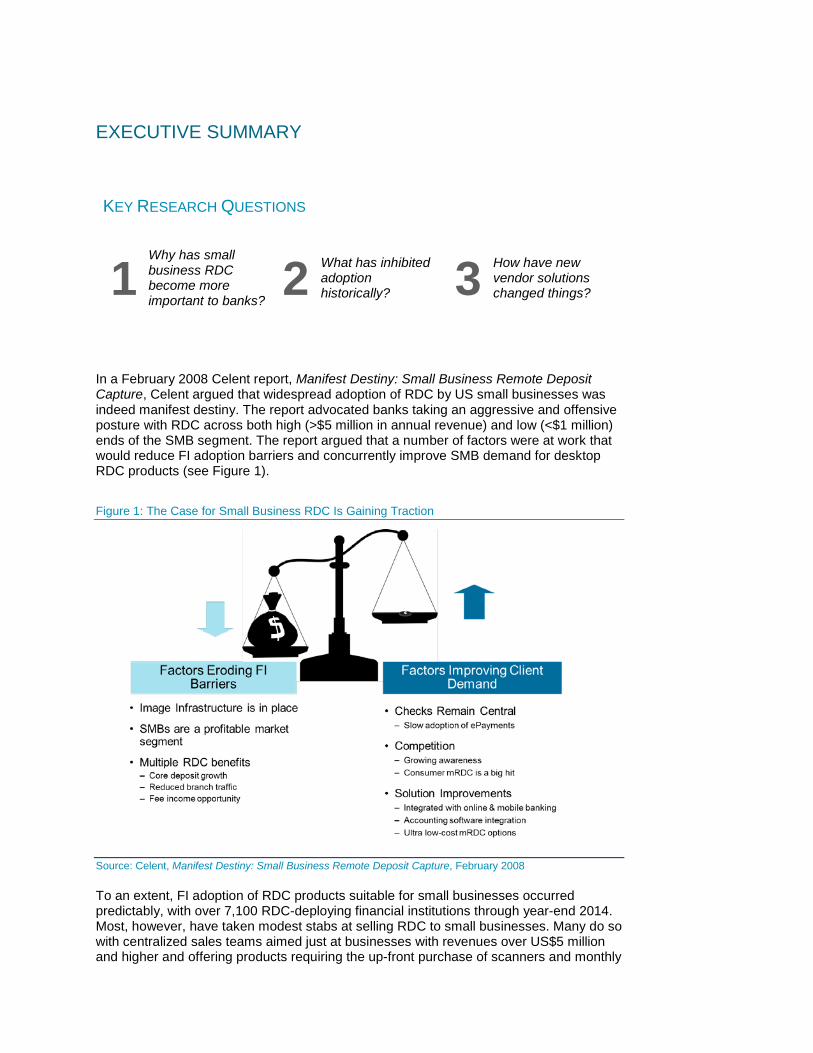

In a February 2008 Celent report, Manifest Destiny: Small Business Remote Deposit Capture, Celent argued that widespread adoption of RDC by US small businesses was indeed manifest destiny. The report advocated banks taking an aggressive and offensive posture with RDC across both high (>$5 million in annual revenue) and low (<$1 million) ends of the SMB segment. The report argued that a number of factors were at work that would reduce FI adoption barriers and concurrently improve SMB demand for desktop RDC products (see Figure 1).

Figure 1: The Case for Small Business RDC Is Gaining Traction

Source: Celent, Manifest Destiny: Small Business Remote Deposit Capture, February 2008

To an extent, FI adoption of RDC products suitable for small businesses occurred predictably, with over 7,100 RDC-deploying financial institutions through year-end 2014. Most, however, have taken modest stabs at selling RDC to small businesses. Many do so with centralized sales teams aimed just at businesses with revenues over US$5 million and higher and offering products requiring the up-front purchase of scanners and monthly

Cha

pter

: Exe

cutiv

e Su

mm

ary

2

fees exceeding US$30. The result has been tepid SMB adoption. But, newly available products from leading RDC vendors are poised to change things. These modern solutions are well-equipped to meet the needs of small businesses across the turnover spectrum, from the 84% of US SMBs with annual revenues of $1 million and less to the 16% of SMBs with revenues over $1 million.

Three primary use cases are apparent — and as check volumes continue their inexorable decline, mobile capture (mRDC) will become increasingly relevant to all three. Specifically:

1. Low check volume — these small businesses gladly accept checks and value being paid by check for their low perceived cost (e.g., no interchange), but receive a small number of items each week. Historic desktop RDC products were overkill for these SMBs and cost too much. Conversely, mRDC is a no-brainer, not for its mobility, but for its ultra-low solution cost.

2. Mobile capture — these small businesses (plumbers, electricians, HVAC contractors, etc.) receive payments on the road. In this use case, mRDC is compelling for its ability to reduce cost and accelerate funds availability. Oftentimes, these businesses also receive checks centrally. In those cases, a single RDC platform (with both desktop and mobile capture options) is the preferred solution.

3. Remittance capture — these SMBs, large and small, place significant value in the ability to capture, validate, and manage remittance information along with check payments in order to hasten cash application to open receivables. A core aspect of traditional desktop RDC products, remittance capture is absent in consumer mRDC products, making their use among SMBs ill-advised.

This report begins with an argument for why small business RDC matters — both for its ability to meet customer needs and for its ability to migrate branch transactions to digital channels. The report then looks at historic SMB RDC adoption barriers and how new solutions can dramatically change the market opportunity. A solution landscape section follows, offering a brief comparison of commercial mRDC solutions.

Cha

pter

: Why

Sm

all B

usin

ess

RD

C M

atte

rs

3

WHY SMALL BUSINESS RDC MATTERS

Small business RDC matters for two main reasons:

1. Check usage remains resilient, and small businesses welcome their use. Checks are preferred over most other payment methods because SMBs perceive them to be less expensive. With attractive product positioning and pricing, small business RDC is a slam-dunk.

2. These checks are needlessly showing up in bank branches. Migrating these branch deposits to RDC represents a significant cost take-out for many banks and is viewed by some as a prerequisite to large-scale branch redesign.

This is not entirely new news. Historically, though, most banks weren’t strategically focused on migrating branch transactions to self-service channels, and small business RDC adoption was so low that its use had only a small impact on branch footfall. But, that was then.

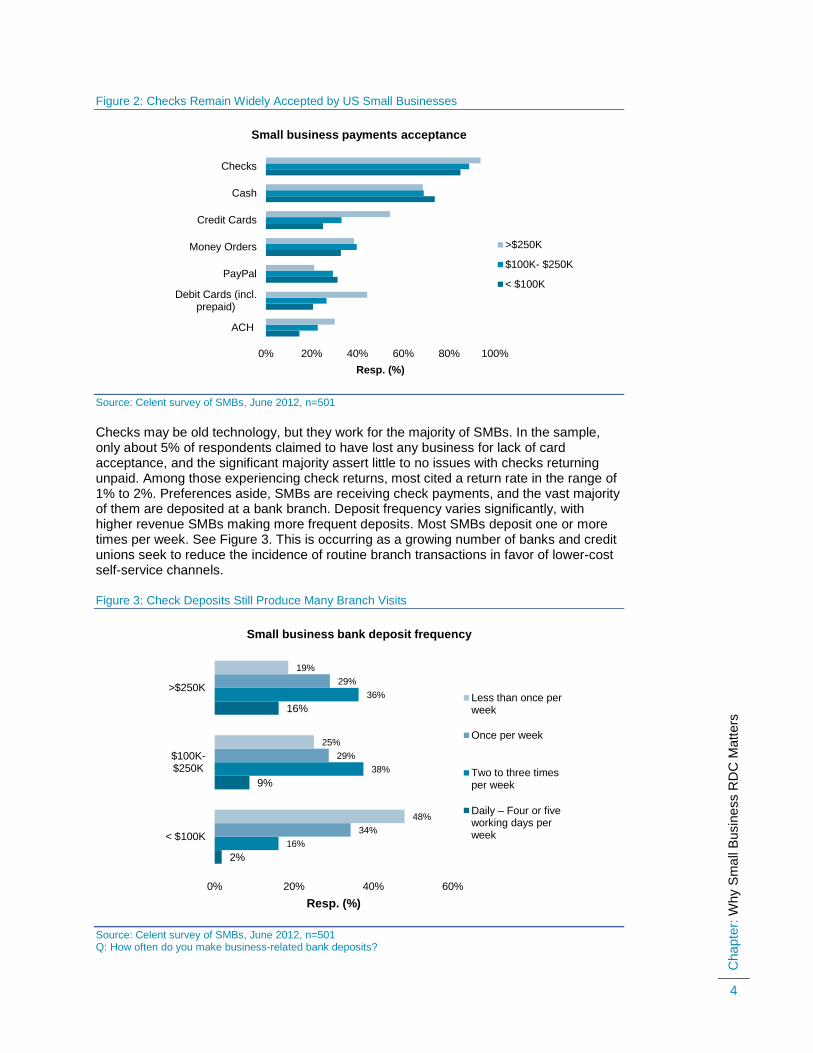

Checks Are Important to SMBs Celent conducted research among small and medium-size businesses (SMBs) in 2012 to examine aspects of accounts receivables. The surveys randomly sampled 500 business owners/managers with annual revenues less than US$5 million across multiple business segments and methods of service delivery and included a mix of business-to-consumer (B2C) and business-to-business (B2B) models. In short, the data supports longevity of check acceptance among SMBs and the viability of low-cost RDC solutions, particularly solutions that provide a one-stop shop for managing all noncash payments.

The first relevant insight is that checks remain widely accepted. Both cash and checks are the most widely accepted payment methods among SMBs for in-person and retail service delivery models (although few among the growing number of online businesses accept cash). Credit and debit card acceptance among SMBs pales in comparison to checks and cash — particularly among businesses with annual revenues less than US$250,000 (see Figure 2 on page 4).

Not only are checks widely accepted, but checks are preferred among SMBs compared to other forms of payment. In the survey, Celent asked SMB owners/managers, “If you could be paid the same way each time by every customer — how would you choose to be paid?” Businesses with in-person or brick-and-mortar delivery models overwhelmingly preferred checks to ACH, cards, or PayPal methods. Cash was a close second across all business models except online, which showed a strong preference for PayPal. The reasons cited for preferring check payments mostly had to do with perceived cost. After all, there’s no interchange associated with check deposits.

Key Research Question

1

Why has small business RDC become more important to banks?

Migrating small business branch deposits to RDC represents a significant cost take-out for many

banks and is viewed by some as a prerequisite to large-scale branch redesign.

Cha

pter

: Why

Sm

all B

usin

ess

RD

C M

atte

rs

4

Figure 2: Checks Remain Widely Accepted by US Small Businesses

Source: Celent survey of SMBs, June 2012, n=501

Checks may be old technology, but they work for the majority of SMBs. In the sample, only about 5% of respondents claimed to have lost any business for lack of card acceptance, and the significant majority assert little to no issues with checks returning unpaid. Among those experiencing check returns, most cited a return rate in the range of 1% to 2%. Preferences aside, SMBs are receiving check payments, and the vast majority of them are deposited at a bank branch. Deposit frequency varies significantly, with higher revenue SMBs making more frequent deposits. Most SMBs deposit one or more times per week. See Figure 3. This is occurring as a growing number of banks and credit unions seek to reduce the incidence of routine branch transactions in favor of lower-cost self-service channels.

Figure 3: Check Deposits Still Produce Many Branch Visits

Source: Celent survey of SMBs, June 2012, n=501 Q: How often do you make business-related bank deposits?

0% 20% 40% 60% 80% 100%

ACH

Debit Cards (incl.prepaid)

PayPal

Money Orders

Credit Cards

Cash

Checks

Resp. (%)

Small business payments acceptance

>$250K

$100K- $250K

< $100K

2%

9%

16%

16%

38%

36%

34%

29%

29%

48%

25%

19%

0% 20% 40% 60%

< $100K

$100K-$250K

>$250K

Resp. (%)

Small business bank deposit frequency

Less than once perweek

Once per week

Two to three timesper week

Daily – Four or five working days per week

Cha

pter

: Why

Sm

all B

usin

ess

RD

C M

atte

rs

5

Like frequency of deposit, the number of checks per deposit varies significantly by size and type of business. Half of businesses with annual revenues over US$250,000 make check deposits having six or more checks, whereas check deposits among smaller businesses typically contain less than 5 items. See Figure 4. Arguably, if businesses could deposit digitally, they would do so more often than they currently do at a branch, creating even smaller deposits. The obvious inference is that RDC solutions for these small businesses don’t have to accommodate large check volumes.

Figure 4: Larger Businesses Deposit More Checks

Source: Celent survey of SMBs, June 2012, n=501 Q: How many checks do you typically deposit each time?

These Checks are Costly to Banks Instead of seeking to maximize small business RDC as a way to migrate check deposits out of branch networks, most banks have viewed RDC through the strategic lens of fee income and to a lesser extent, deposit growth. In consecutive annual bank surveys from 2009 through 2013, banks’ top small business RDC priority was generating fee revenue growth (Figure 5 presents the most recent results).

Figure 5: Banks Have Historically Chased Fee Revenue with SMB RDC

Source: Celent financial institution survey, September 2013, n=266. Q: What is your institution's top small business RDC priority for the coming year?

4%

10%

80%

10%

15%

69%

28%

20%

51%

0% 20% 40% 60% 80% 100%

More than10

6 to 10

1 to 5

Resp. (%)

Small business checks per deposit

>$250K

$100K- $250K

< $100K

20%

29%

37%

58%

63%

0% 20% 40% 60% 80%

Improve regulatory compliance (e.g.,FFIEC, AML)

Improve risk management

Reduce cost

Increase client adoption for depositgrowth

Increase client adoption for feerevenue

Resp. (% Top 2-Box)

Top Small Business RDC Priority

Cha

pter

: Why

Sm

all B

usin

ess

RD

C M

atte

rs

6

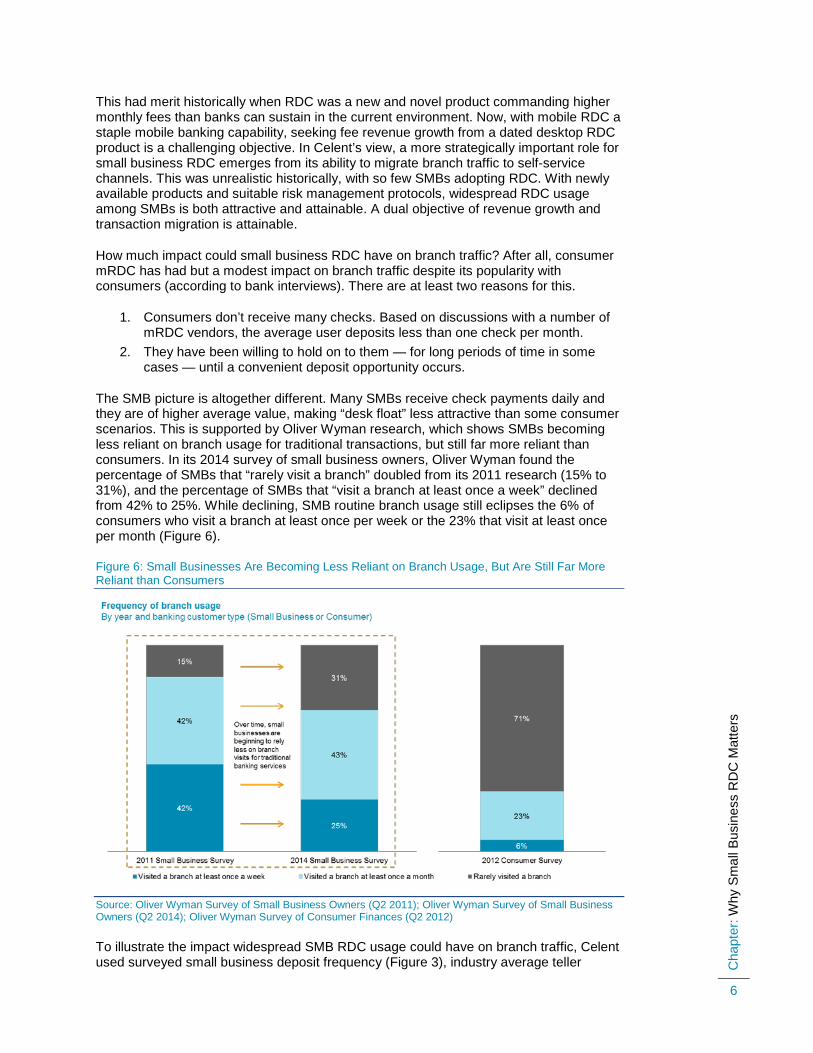

This had merit historically when RDC was a new and novel product commanding higher monthly fees than banks can sustain in the current environment. Now, with mobile RDC a staple mobile banking capability, seeking fee revenue growth from a dated desktop RDC product is a challenging objective. In Celent’s view, a more strategically important role for small business RDC emerges from its ability to migrate branch traffic to self-service channels. This was unrealistic historically, with so few SMBs adopting RDC. With newly available products and suitable risk management protocols, widespread RDC usage among SMBs is both attractive and attainable. A dual objective of revenue growth and transaction migration is attainable.

How much impact could small business RDC have on branch traffic? After all, consumer mRDC has had but a modest impact on branch traffic despite its popularity with consumers (according to bank interviews). There are at least two reasons for this.

1. Consumers don’t receive many checks. Based on discussions with a number of mRDC vendors, the average user deposits less than one check per month.

2. They have been willing to hold on to them — for long periods of time in some cases — until a convenient deposit opportunity occurs.

The SMB picture is altogether different. Many SMBs receive check payments daily and they are of higher average value, making “desk float” less attractive than some consumer scenarios. This is supported by Oliver Wyman research, which shows SMBs becoming less reliant on branch usage for traditional transactions, but still far more reliant than consumers. In its 2014 survey of small business owners, Oliver Wyman found the percentage of SMBs that “rarely visit a branch” doubled from its 2011 research (15% to 31%), and the percentage of SMBs that “visit a branch at least once a week” declined from 42% to 25%. While declining, SMB routine branch usage still eclipses the 6% of consumers who visit a branch at least once per week or the 23% that visit at least once per month (Figure 6).

Figure 6: Small Businesses Are Becoming Less Reliant on Branch Usage, But Are Still Far More Reliant than Consumers

Source: Oliver Wyman Survey of Small Business Owners (Q2 2011); Oliver Wyman Survey of Small Business Owners (Q2 2014); Oliver Wyman Survey of Consumer Finances (Q2 2012)

To illustrate the impact widespread SMB RDC usage could have on branch traffic, Celent used surveyed small business deposit frequency (Figure 3), industry average teller

Cha

pter

: Why

Sm

all B

usin

ess

RD

C M

atte

rs

7

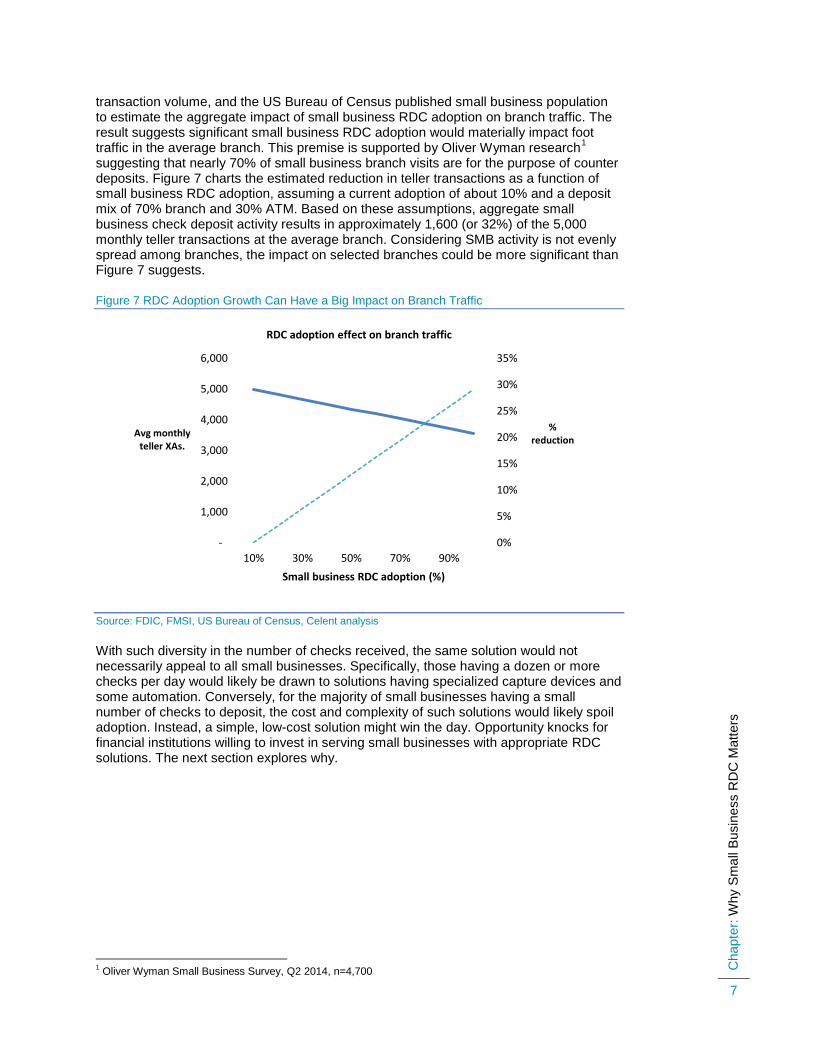

transaction volume, and the US Bureau of Census published small business population to estimate the aggregate impact of small business RDC adoption on branch traffic. The result suggests significant small business RDC adoption would materially impact foot traffic in the average branch. This premise is supported by Oliver Wyman research1 suggesting that nearly 70% of small business branch visits are for the purpose of counter deposits. Figure 7 charts the estimated reduction in teller transactions as a function of small business RDC adoption, assuming a current adoption of about 10% and a deposit mix of 70% branch and 30% ATM. Based on these assumptions, aggregate small business check deposit activity results in approximately 1,600 (or 32%) of the 5,000 monthly teller transactions at the average branch. Considering SMB activity is not evenly spread among branches, the impact on selected branches could be more significant than Figure 7 suggests.

Figure 7 RDC Adoption Growth Can Have a Big Impact on Branch Traffic

Source: FDIC, FMSI, US Bureau of Census, Celent analysis

With such diversity in the number of checks received, the same solution would not necessarily appeal to all small businesses. Specifically, those having a dozen or more checks per day would likely be drawn to solutions having specialized capture devices and some automation. Conversely, for the majority of small businesses having a small number of checks to deposit, the cost and complexity of such solutions would likely spoil adoption. Instead, a simple, low-cost solution might win the day. Opportunity knocks for financial institutions willing to invest in serving small businesses with appropriate RDC solutions. The next section explores why.

1 Oliver Wyman Small Business Survey, Q2 2014, n=4,700

0%

5%

10%

15%

20%

25%

30%

35%

-

1,000

2,000

3,000

4,000

5,000

6,000

10% 30% 50% 70% 90%

% reduction

Avg monthly teller XAs.

Small business RDC adoption (%)

RDC adoption effect on branch traffic

Cha

pter

: Opp

ortu

nity

Kno

cks

8

OPPORTUNITY KNOCKS

Opportunity knocks for financial institutions seeking to migrate routine branch deposits to RDC. At least three things stand in the way at most financial institutions, however.

1. Banks neglect to sell the majority (84%) of SMBs with revenues less than US$1 million, focusing mainly or exclusively on the 16% with higher annual revenues, perceiving them to be a more attractive business opportunity.

2. Banks underutilize branch resources for a variety of reasons. In Celent’s October 2013 survey, 44% of respondents indicated that less than 25% of SMB RDC sales leads came from branches, even though the majority of SMBs regularly made check deposits there.

3. The RDC products historically offered to small businesses were too complex and expensive.

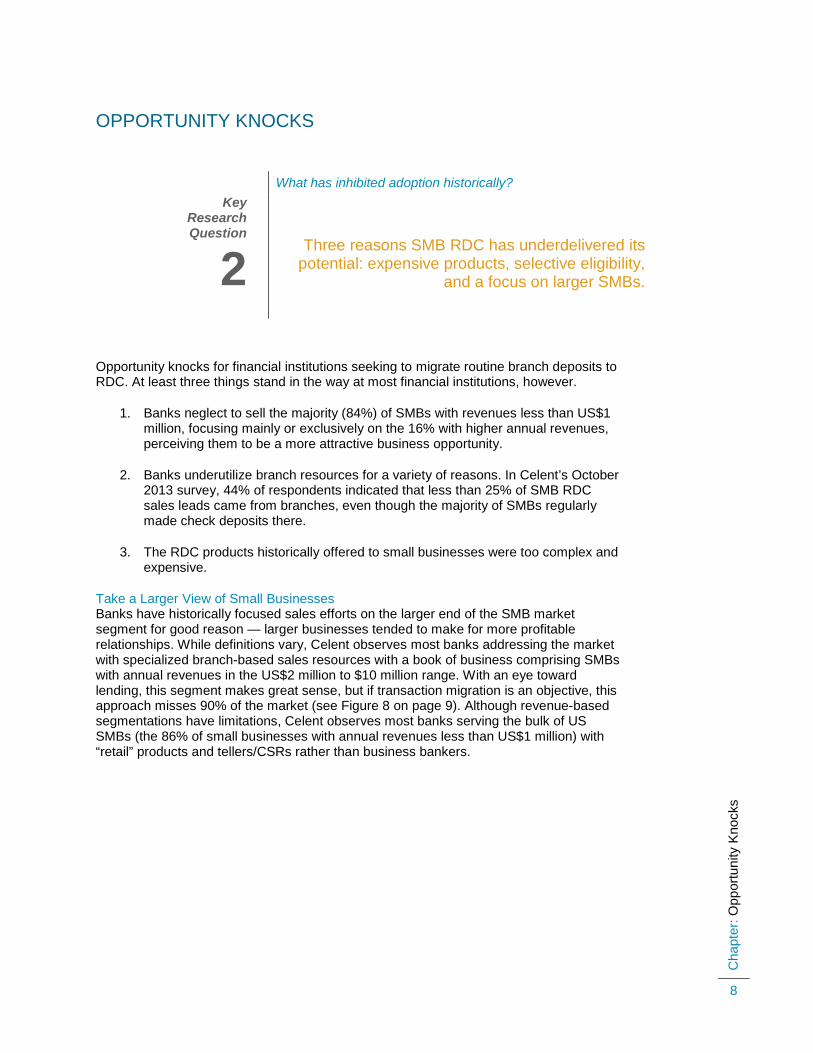

Take a Larger View of Small Businesses Banks have historically focused sales efforts on the larger end of the SMB market segment for good reason — larger businesses tended to make for more profitable relationships. While definitions vary, Celent observes most banks addressing the market with specialized branch-based sales resources with a book of business comprising SMBs with annual revenues in the US$2 million to $10 million range. With an eye toward lending, this segment makes great sense, but if transaction migration is an objective, this approach misses 90% of the market (see Figure 8 on page 9). Although revenue-based segmentations have limitations, Celent observes most banks serving the bulk of US SMBs (the 86% of small businesses with annual revenues less than US$1 million) with “retail” products and tellers/CSRs rather than business bankers.

Key Research Question

2

What has inhibited adoption historically?

Three reasons SMB RDC has underdelivered its potential: expensive products, selective eligibility,

and a focus on larger SMBs.

Cha

pter

: Opp

ortu

nity

Kno

cks

9

Figure 8: Most Attention Has Been Among Larger SMBs, Missing the Greater Opportunity

Source: US Bureau of Census, Celent analysis

Conversely, sales efforts devoted to a broader SMB target market would quickly realize diminishing returns and likely result in unprofitable investment of resources. Banks need products that can be easily sold by tellers, platform sales, and universal bankers, leaving the more lucrative opportunities to the SMB specialists. In other words, banks need SMB RDC products that effectively sell themselves and can be explained quickly and simply when the need arises. This hasn’t been the case with historic desktop small business RDC products.

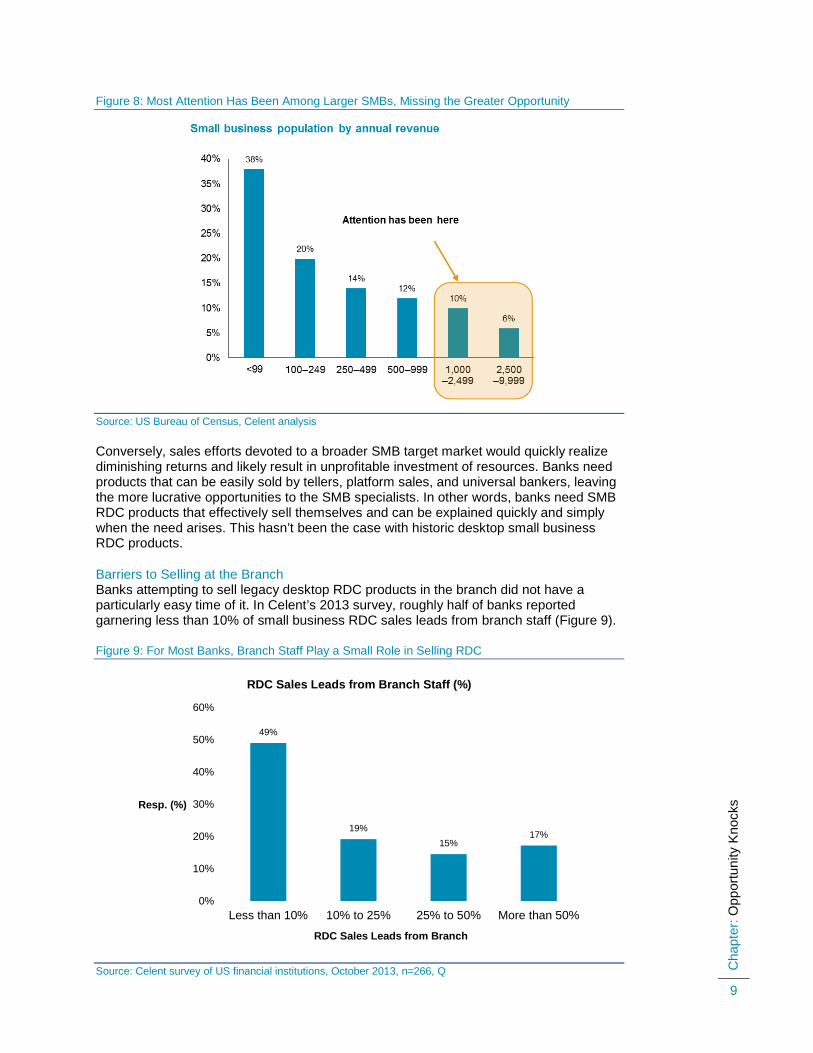

Barriers to Selling at the Branch Banks attempting to sell legacy desktop RDC products in the branch did not have a particularly easy time of it. In Celent’s 2013 survey, roughly half of banks reported garnering less than 10% of small business RDC sales leads from branch staff (Figure 9).

Figure 9: For Most Banks, Branch Staff Play a Small Role in Selling RDC

Source: Celent survey of US financial institutions, October 2013, n=266, Q

49%

19% 15%

17%

0%

10%

20%

30%

40%

50%

60%

Less than 10% 10% to 25% 25% to 50% More than 50%

Resp. (%)

RDC Sales Leads from Branch

RDC Sales Leads from Branch Staff (%)

Cha

pter

: Opp

ortu

nity

Kno

cks

10

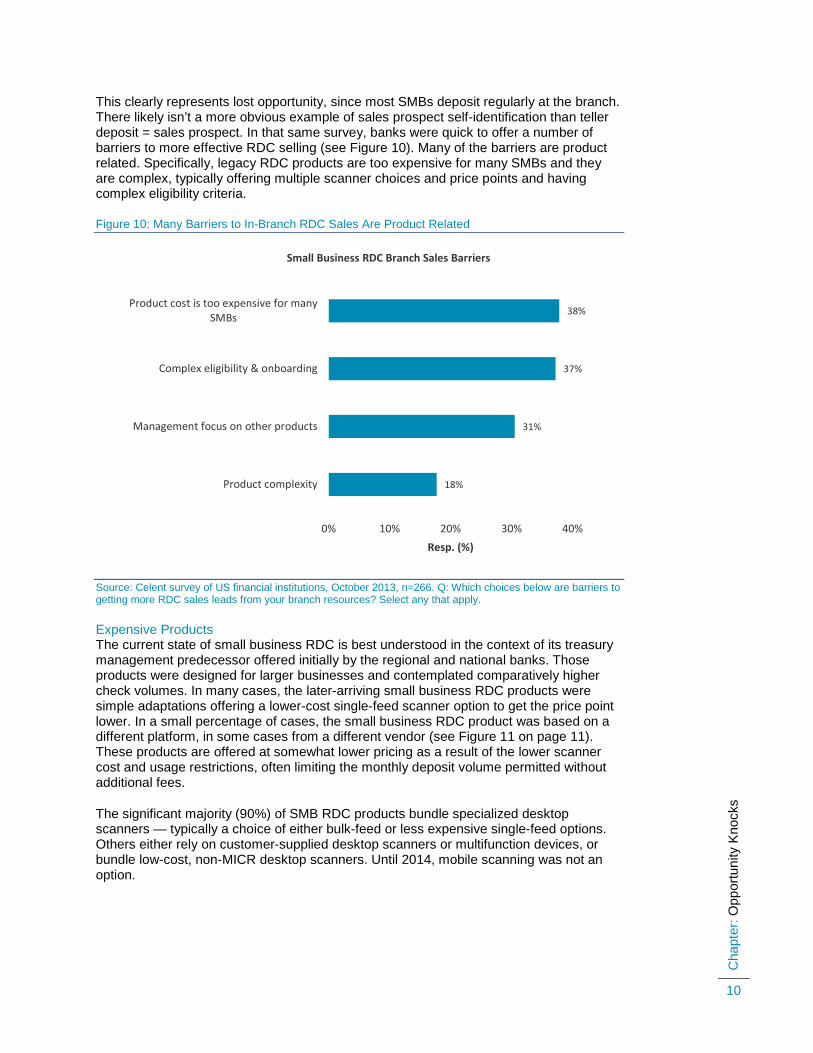

This clearly represents lost opportunity, since most SMBs deposit regularly at the branch. There likely isn’t a more obvious example of sales prospect self-identification than teller deposit = sales prospect. In that same survey, banks were quick to offer a number of barriers to more effective RDC selling (see Figure 10). Many of the barriers are product related. Specifically, legacy RDC products are too expensive for many SMBs and they are complex, typically offering multiple scanner choices and price points and having complex eligibility criteria.

Figure 10: Many Barriers to In-Branch RDC Sales Are Product Related

Source: Celent survey of US financial institutions, October 2013, n=266. Q: Which choices below are barriers to getting more RDC sales leads from your branch resources? Select any that apply.

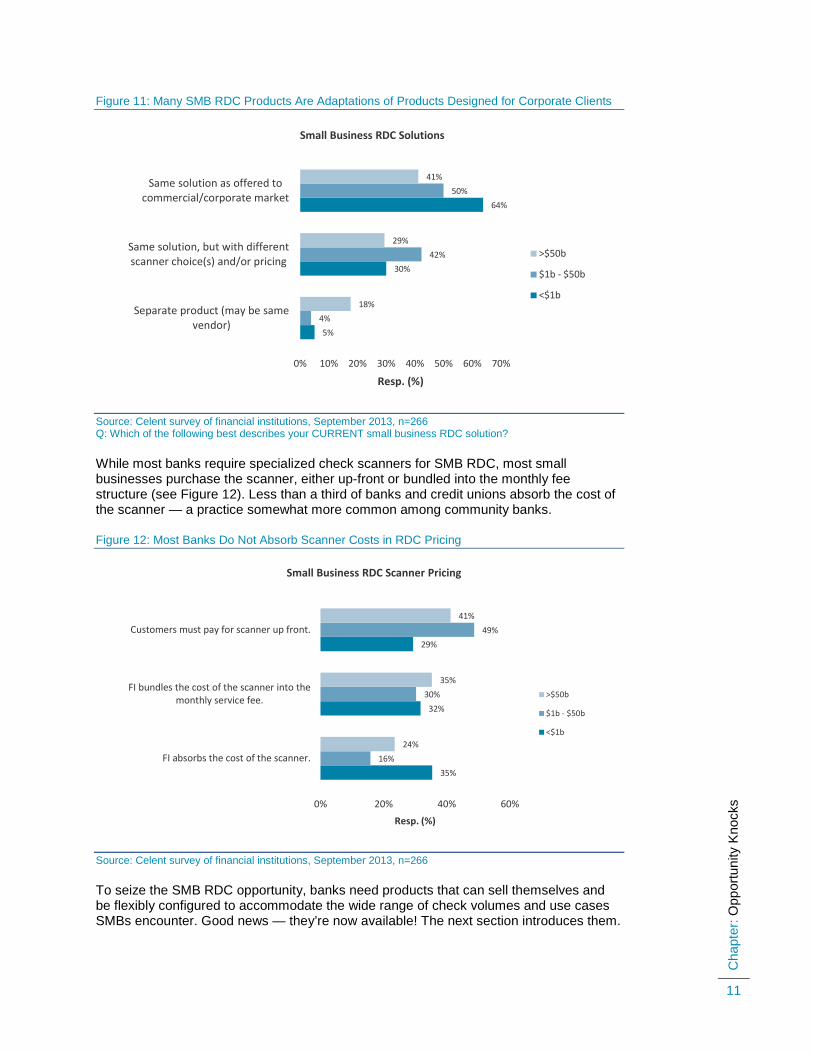

Expensive Products The current state of small business RDC is best understood in the context of its treasury management predecessor offered initially by the regional and national banks. Those products were designed for larger businesses and contemplated comparatively higher check volumes. In many cases, the later-arriving small business RDC products were simple adaptations offering a lower-cost single-feed scanner option to get the price point lower. In a small percentage of cases, the small business RDC product was based on a different platform, in some cases from a different vendor (see Figure 11 on page 11). These products are offered at somewhat lower pricing as a result of the lower scanner cost and usage restrictions, often limiting the monthly deposit volume permitted without additional fees.

The significant majority (90%) of SMB RDC products bundle specialized desktop scanners — typically a choice of either bulk-feed or less expensive single-feed options. Others either rely on customer-supplied desktop scanners or multifunction devices, or bundle low-cost, non-MICR desktop scanners. Until 2014, mobile scanning was not an option.

18%

31%

37%

38%

0% 10% 20% 30% 40%

Product complexity

Management focus on other products

Complex eligibility & onboarding

Product cost is too expensive for manySMBs

Resp. (%)

Small Business RDC Branch Sales Barriers

Cha

pter

: Opp

ortu

nity

Kno

cks

11

Figure 11: Many SMB RDC Products Are Adaptations of Products Designed for Corporate Clients

Source: Celent survey of financial institutions, September 2013, n=266 Q: Which of the following best describes your CURRENT small business RDC solution?

While most banks require specialized check scanners for SMB RDC, most small businesses purchase the scanner, either up-front or bundled into the monthly fee structure (see Figure 12). Less than a third of banks and credit unions absorb the cost of the scanner — a practice somewhat more common among community banks.

Figure 12: Most Banks Do Not Absorb Scanner Costs in RDC Pricing

Source: Celent survey of financial institutions, September 2013, n=266

To seize the SMB RDC opportunity, banks need products that can sell themselves and be flexibly configured to accommodate the wide range of check volumes and use cases SMBs encounter. Good news — they’re now available! The next section introduces them.

5%

30%

64%

4%

42%

50%

18%

29%

41%

0% 10% 20% 30% 40% 50% 60% 70%

Separate product (may be samevendor)

Same solution, but with differentscanner choice(s) and/or pricing

Same solution as offered tocommercial/corporate market

Resp. (%)

Small Business RDC Solutions

>$50b

$1b - $50b

<$1b

35%

32%

29%

16%

30%

49%

24%

35%

41%

0% 20% 40% 60%

FI absorbs the cost of the scanner.

FI bundles the cost of the scanner into themonthly service fee.

Customers must pay for scanner up front.

Resp. (%)

Small Business RDC Scanner Pricing

>$50b

$1b - $50b

<$1b

Cha

pter

: Opp

ortu

nity

Kno

cks

12

A PRODUCT FOR TODAY It is no wonder, then, that small businesses have been slow to adopt RDC over the past few years. The prospect of an up-front scanner purchase coupled with monthly service charges of $30 or more is a nonstarter for many businesses in the current economic environment.

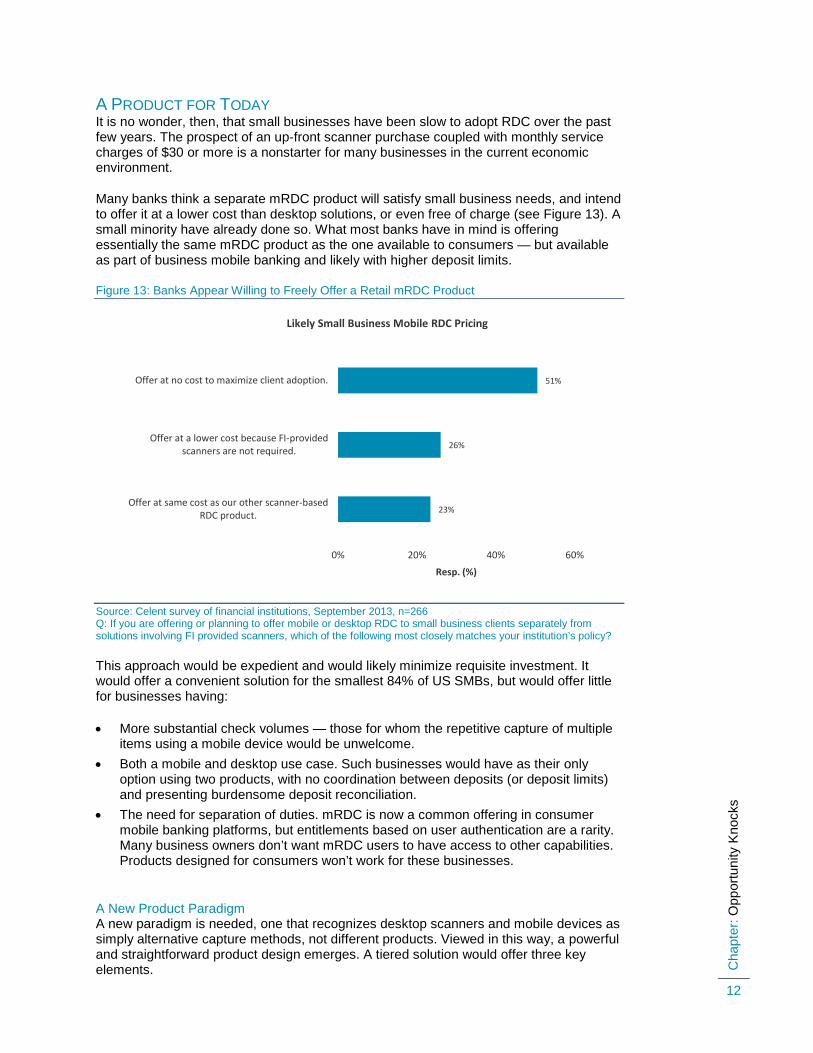

Many banks think a separate mRDC product will satisfy small business needs, and intend to offer it at a lower cost than desktop solutions, or even free of charge (see Figure 13). A small minority have already done so. What most banks have in mind is offering essentially the same mRDC product as the one available to consumers — but available as part of business mobile banking and likely with higher deposit limits.

Figure 13: Banks Appear Willing to Freely Offer a Retail mRDC Product

Source: Celent survey of financial institutions, September 2013, n=266 Q: If you are offering or planning to offer mobile or desktop RDC to small business clients separately from solutions involving FI provided scanners, which of the following most closely matches your institution’s policy?

This approach would be expedient and would likely minimize requisite investment. It would offer a convenient solution for the smallest 84% of US SMBs, but would offer little for businesses having:

• More substantial check volumes — those for whom the repetitive capture of multiple items using a mobile device would be unwelcome.

• Both a mobile and desktop use case. Such businesses would have as their only option using two products, with no coordination between deposits (or deposit limits) and presenting burdensome deposit reconciliation.

• The need for separation of duties. mRDC is now a common offering in consumer mobile banking platforms, but entitlements based on user authentication are a rarity. Many business owners don’t want mRDC users to have access to other capabilities. Products designed for consumers won’t work for these businesses.

A New Product Paradigm A new paradigm is needed, one that recognizes desktop scanners and mobile devices as simply alternative capture methods, not different products. Viewed in this way, a powerful and straightforward product design emerges. A tiered solution would offer three key elements.

23%

26%

51%

0% 20% 40% 60%

Offer at same cost as our other scanner-basedRDC product.

Offer at a lower cost because FI-providedscanners are not required.

Offer at no cost to maximize client adoption.

Resp. (%)

Likely Small Business Mobile RDC Pricing

Cha

pter

: Opp

ortu

nity

Kno

cks

13

• A choice of capture methods; desktop, mobile or both. • Support by a single admin and deposit review layer integrated to banks’ small

business Internet and mobile banking platforms. • Being operating system and device agnostic, supporting Android, iOS, and

Windows operating systems and able to run on mobile devices, phablets, tablets, laptops, or desktop hardware.

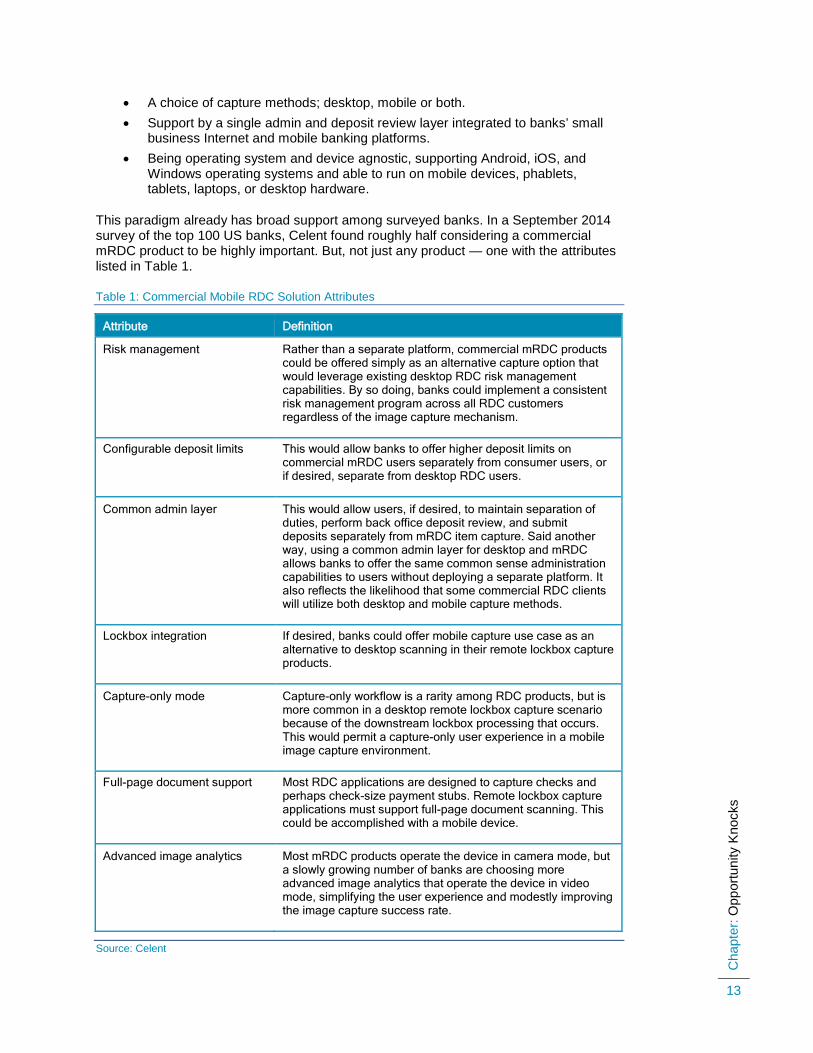

This paradigm already has broad support among surveyed banks. In a September 2014 survey of the top 100 US banks, Celent found roughly half considering a commercial mRDC product to be highly important. But, not just any product — one with the attributes listed in Table 1.

Table 1: Commercial Mobile RDC Solution Attributes

Attribute Definition

Risk management Rather than a separate platform, commercial mRDC products could be offered simply as an alternative capture option that would leverage existing desktop RDC risk management capabilities. By so doing, banks could implement a consistent risk management program across all RDC customers regardless of the image capture mechanism.

Configurable deposit limits This would allow banks to offer higher deposit limits on commercial mRDC users separately from consumer users, or if desired, separate from desktop RDC users.

Common admin layer This would allow users, if desired, to maintain separation of duties, perform back office deposit review, and submit deposits separately from mRDC item capture. Said another way, using a common admin layer for desktop and mRDC allows banks to offer the same common sense administration capabilities to users without deploying a separate platform. It also reflects the likelihood that some commercial RDC clients will utilize both desktop and mobile capture methods.

Lockbox integration If desired, banks could offer mobile capture use case as an alternative to desktop scanning in their remote lockbox capture products.

Capture-only mode Capture-only workflow is a rarity among RDC products, but is more common in a desktop remote lockbox capture scenario because of the downstream lockbox processing that occurs. This would permit a capture-only user experience in a mobile image capture environment.

Full-page document support Most RDC applications are designed to capture checks and perhaps check-size payment stubs. Remote lockbox capture applications must support full-page document scanning. This could be accomplished with a mobile device.

Advanced image analytics Most mRDC products operate the device in camera mode, but a slowly growing number of banks are choosing more advanced image analytics that operate the device in video mode, simplifying the user experience and modestly improving the image capture success rate.

Source: Celent

Cha

pter

: Opp

ortu

nity

Kno

cks

14

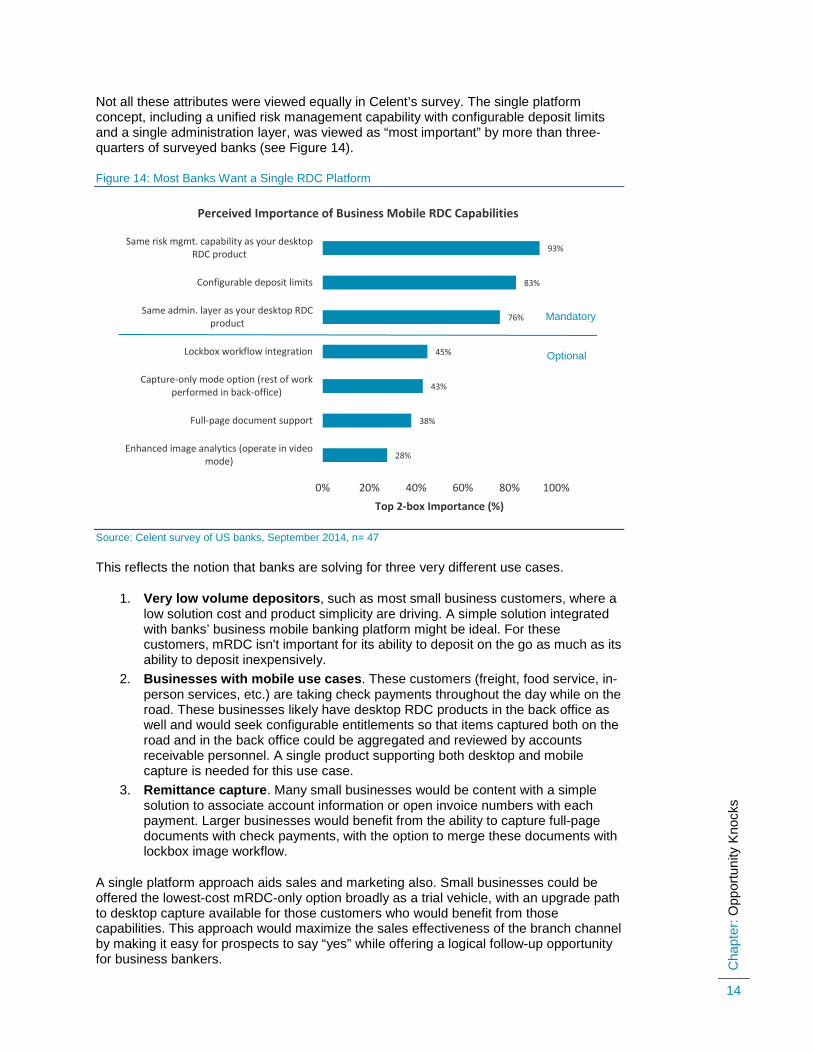

Not all these attributes were viewed equally in Celent’s survey. The single platform concept, including a unified risk management capability with configurable deposit limits and a single administration layer, was viewed as “most important” by more than three-quarters of surveyed banks (see Figure 14).

Figure 14: Most Banks Want a Single RDC Platform

Source: Celent survey of US banks, September 2014, n= 47

This reflects the notion that banks are solving for three very different use cases.

1. Very low volume depositors, such as most small business customers, where a low solution cost and product simplicity are driving. A simple solution integrated with banks’ business mobile banking platform might be ideal. For these customers, mRDC isn't important for its ability to deposit on the go as much as its ability to deposit inexpensively.

2. Businesses with mobile use cases. These customers (freight, food service, in-person services, etc.) are taking check payments throughout the day while on the road. These businesses likely have desktop RDC products in the back office as well and would seek configurable entitlements so that items captured both on the road and in the back office could be aggregated and reviewed by accounts receivable personnel. A single product supporting both desktop and mobile capture is needed for this use case.

3. Remittance capture. Many small businesses would be content with a simple solution to associate account information or open invoice numbers with each payment. Larger businesses would benefit from the ability to capture full-page documents with check payments, with the option to merge these documents with lockbox image workflow.

A single platform approach aids sales and marketing also. Small businesses could be offered the lowest-cost mRDC-only option broadly as a trial vehicle, with an upgrade path to desktop capture available for those customers who would benefit from those capabilities. This approach would maximize the sales effectiveness of the branch channel by making it easy for prospects to say “yes” while offering a logical follow-up opportunity for business bankers.

28%

38%

43%

45%

76%

83%

93%

0% 20% 40% 60% 80% 100%

Enhanced image analytics (operate in videomode)

Full-page document support

Capture-only mode option (rest of workperformed in back-office)

Lockbox workflow integration

Same admin. layer as your desktop RDCproduct

Configurable deposit limits

Same risk mgmt. capability as your desktopRDC product

Top 2-box Importance (%)

Perceived Importance of Business Mobile RDC Capabilities

Optional

Mandatory

Cha

pter

: Sol

utio

n La

ndsc

ape

15

SOLUTION LANDSCAPE

Not long ago, the RDC solution landscape was populated by thick client Windows applications, often adaptations of legacy check processing software platforms offered by those same vendors. These quickly gave way to more modern and easily deployed browser-based user interfaces. As demand for remote deposit capture migrated downmarket from its large corporate genesis, many vendors responded by architecting entirely new products. This trend continued with the advent of consumer RDC. Now, things are coming full circle, with a number of vendors launching or preparing to launch unified distributed capture platforms.

As common platform architectures across consumer, small business, and consumer products avail themselves, they will provide much needed flexibility for financial institutions and allow end users to treat mobile capture as simply a capture alternative, rather than a unique product with its own provisioning and entitlement requirements. Moreover, flexible customer provisioning in the current release of several vendor products eliminates the requirement for banks to provision users in the RDC application. This allows the bank to invite self-service provisioning — something attractive indeed if you’re a bank with a large SMB client base.

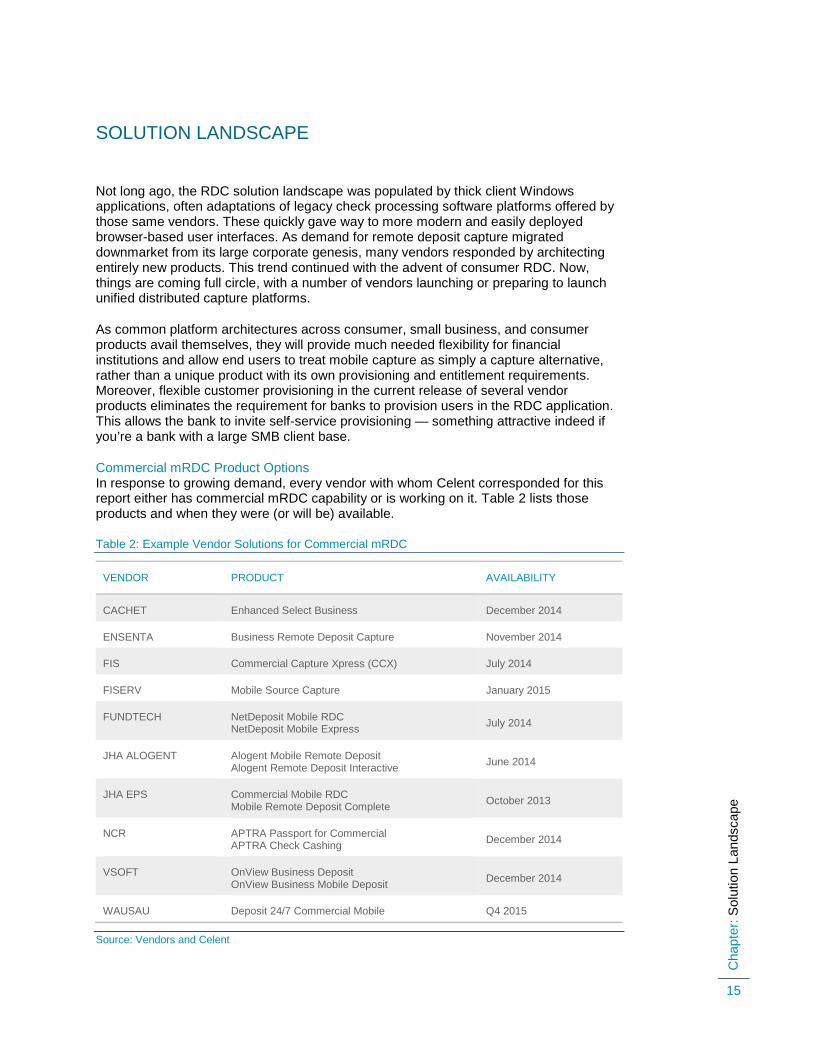

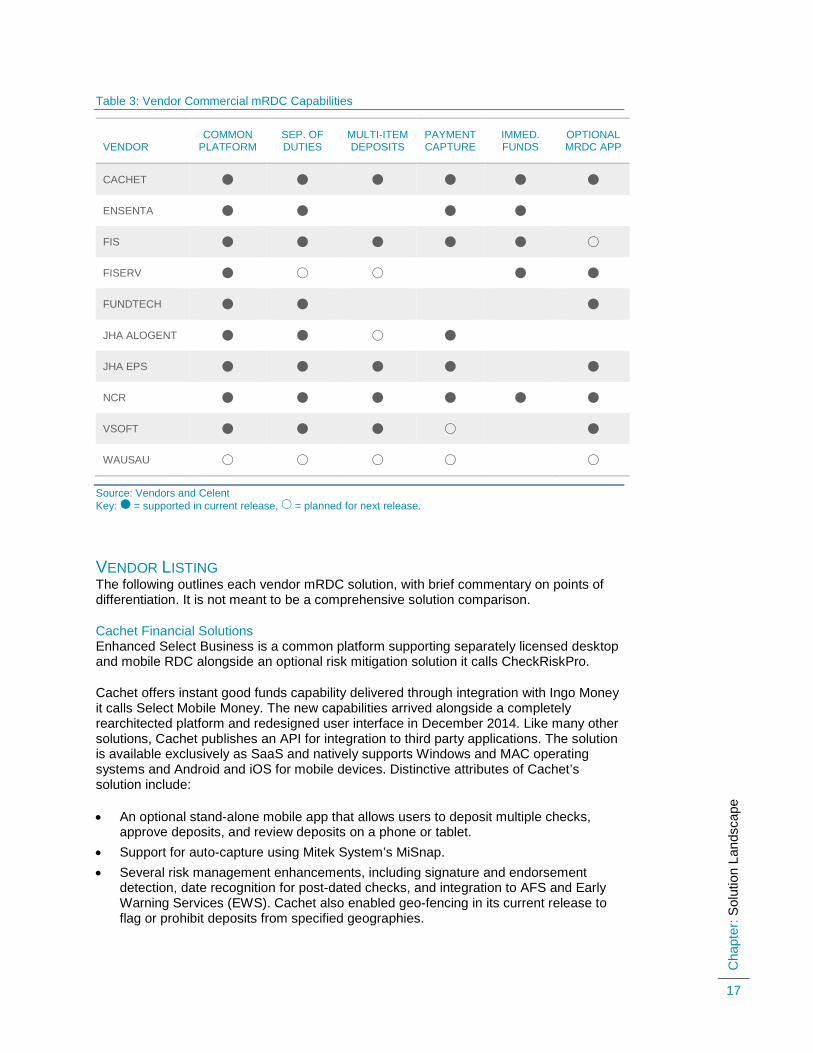

Commercial mRDC Product Options In response to growing demand, every vendor with whom Celent corresponded for this report either has commercial mRDC capability or is working on it. Table 2 lists those products and when they were (or will be) available.

Table 2: Example Vendor Solutions for Commercial mRDC

VENDOR PRODUCT AVAILABILITY

CACHET Enhanced Select Business December 2014

ENSENTA Business Remote Deposit Capture November 2014

FIS Commercial Capture Xpress (CCX) July 2014

FISERV Mobile Source Capture January 2015

FUNDTECH NetDeposit Mobile RDC NetDeposit Mobile Express July 2014

JHA ALOGENT Alogent Mobile Remote Deposit Alogent Remote Deposit Interactive June 2014

JHA EPS Commercial Mobile RDC Mobile Remote Deposit Complete October 2013

NCR APTRA Passport for Commercial APTRA Check Cashing December 2014

VSOFT OnView Business Deposit OnView Business Mobile Deposit December 2014

WAUSAU Deposit 24/7 Commercial Mobile Q4 2015

Source: Vendors and Celent

Cha

pter

: Sol

utio

n La

ndsc

ape

16

Celent observes some common attributes among commercial mRDC offerings. Here are some of the more obvious attributes that are delivered specifically to support commercial mRDC.

• Common platform. This implies a common admin layer and risk management controls across deposit channels/devices. In some cases, solutions aggregate deposit limits across channels.

• Separation of duties. This supports a common need to have configurable access to product capabilities across individual users. One user may be permitted only to capture items, while another user reviews and approves deposits.

• Multi-item deposits. Most products currently rely on the consumer mRDC end user workflow of single-item deposits. Post-capture, however, many products allow users to aggregate items into deposits as a separate step, typically as part of deposit review. A few solutions design a capture workflow that contemplates multiple items, but the capture process remains serial (e.g., front image, rear image, front image, rear image, etc.).

• Capturing payment information beyond check detail. Although not in widespread demand, many users want to associate remittance information with each check item. This capability has been supported broadly for years among desktop RDC products in the form of user-definable fields. A subset of products applied image analytics to automate data capture and validation. While there is some interest in image capture for archiving and workflow integration (wholesale lockbox, for example), most commercial mRDC solutions aren’t there.

• Immediate good funds. Banks are slowly embracing tiered funds availability for deposited items, with fees associated with immediate good funds. Several vendors offer such solutions preintegrated with one or more providers of risk scoring engines, such as FIS Certegy, Ingo Money, and Valid Systems. While this capability is often associated with check cashing or GPR prepaid reloading, it has emerged among several banks as a compelling and frequently used product for small businesses. Many are paid by check at the completion of a job and need to pay workers in cash immediately. For a detailed discussion of this solution space, see the Celent report Winning the Underbanked: How Banks Can Get an Omnichannel Upper Hand, April 2014.

• Optional stand-alone mobile app. While most agree mRDC capability is best integrated into a bank’s mobile banking app, there are some persistent reasons why a bank might like to offer a stand-alone mRDC app. One reason is time to market. Few banks have a small business mobile banking platform, for example. Many vendors don’t yet offer suitable solutions, and when they do, they will have to integrate with RDC vendors. A stand-alone app would hasten time to market for those banks. For larger businesses with a mobile use case, a stand-alone app for item capture may be preferred.

Table 3 compares a sampling of available solutions. These are important attributes of commercial mRDC, but they comprise just a small subset of overall solution considerations.

Cha

pter

: Sol

utio

n La

ndsc

ape

17

Table 3: Vendor Commercial mRDC Capabilities

VENDOR COMMON

PLATFORM SEP. OF DUTIES

MULTI-ITEM DEPOSITS

PAYMENT CAPTURE

IMMED. FUNDS

OPTIONAL MRDC APP

CACHET

ENSENTA

FIS

FISERV

FUNDTECH

JHA ALOGENT

JHA EPS

NCR

VSOFT

WAUSAU

Source: Vendors and Celent Key: = supported in current release, = planned for next release.

VENDOR LISTING The following outlines each vendor mRDC solution, with brief commentary on points of differentiation. It is not meant to be a comprehensive solution comparison.

Cachet Financial Solutions Enhanced Select Business is a common platform supporting separately licensed desktop and mobile RDC alongside an optional risk mitigation solution it calls CheckRiskPro.

Cachet offers instant good funds capability delivered through integration with Ingo Money it calls Select Mobile Money. The new capabilities arrived alongside a completely rearchitected platform and redesigned user interface in December 2014. Like many other solutions, Cachet publishes an API for integration to third party applications. The solution is available exclusively as SaaS and natively supports Windows and MAC operating systems and Android and iOS for mobile devices. Distinctive attributes of Cachet’s solution include:

• An optional stand-alone mobile app that allows users to deposit multiple checks, approve deposits, and review deposits on a phone or tablet.

• Support for auto-capture using Mitek System’s MiSnap. • Several risk management enhancements, including signature and endorsement

detection, date recognition for post-dated checks, and integration to AFS and Early Warning Services (EWS). Cachet also enabled geo-fencing in its current release to flag or prohibit deposits from specified geographies.

Cha

pter

: Sol

utio

n La

ndsc

ape

18

Ensenta Ensenta offers a single RDC platform for consumers and small businesses and across capture platforms — desktop and mobile. The platform supports consistent application of business rules and risk management across channels and offers support for check verification and guarantee for financial institutions pursuing check cashing or immediate funds availability options. Ensenta’s current release was generally available in late 2014. Distinctive attributes of Ensenta’s solution include:

• Instant Support — provides real-time information and access to captured images to bank support personnel so they might better assist customers having any difficulty making digital deposits.

• Early Warning Services (EWS) integration to provide banks the ability to leverage EWS at time of capture.

• Express Edit — the ability for back office personnel to make on-the-fly image modifications as part of the deposit review process.

FIS FIS offers multiple commercial RDC products. Its next release planned for late 2015, a substantial redesign, will result in fewer, more capable, and more flexible products. In its current lineup, commercial mRDC is enabled in Commercial Capture Express.

Direct Merchant (Smart Deposit and Web Deposit) includes both Smart Client and browser-based capture applications, used in tandem, and offered in both licensed and ASP models.

Commercial Capture Xpress (CCX) provides RDC for business and merchant use, utilizing MS SQL database and easy-to-use, browser-based user interface. CCX is operated in an FIS-managed ASP, with a full complement of implementation and support services. CCX offers a mobile API for integration with mobile banking platforms (since July 2014), but does not offer a stand-alone mRDC app in its current release. Users may capture multiple items in a single deposit and manually associate remittance information with each item.

VICOR Distributed Capture is a separate web-based solution designed for users of the VICOR RIDS Lockbox platform. The product offers capture of advanced remittance transactions, including full page invoices, coupons and associated artifacts, and downstream integration into the RIDS lockbox workflow. VICOR Distributed Capture does not support mRDC.

Fiserv Source Capture Solutions from Fiserv is a portfolio of web-based deposit gathering applications designed for all touchpoints, sharing a common back office processing platform and offered for both in-house and outsourced/ASP implementation. Products in the Source Capture product line include: Merchant Source Capture, Remittance Coupon Source Capture (for smaller billers wishing to automate coupon processing and expedite deposits), Mobile Source Capture (supporting mobile capture for both consumer and business end users), as well as Branch Source Capture, ATM Source Capture, and Teller Source Capture for deposit gathering within the bank infrastructure.

Available beginning in January 2015,Mobile Source Capture essentially integrates its consumer mRDC application with Mobiliti Business and Business Online channel applications which handle entitlements. In so doing, banks can offer commercial customers a single package to enable desktop RDC, mobile RDC, or both along with a straightforward administration layer to manage individual user configurations. Its current release, however, does not support batching multiple mRDC captured items into a single

Cha

pter

: Sol

utio

n La

ndsc

ape

19

deposit, and there is no support for payment capture for mobile users. Distinctive aspects of Mobile Source Capture include:

• Fiserv Mobile Source Capture is preintegrated into its Mobiliti Business mobile banking solution for SMBs, one of a relatively few offerings in the SMB specific digital banking platform space.

• Ability to offer low-risk immediate good funds through mRDC, ATM, and branch counter deposits through Fiserv’s separately licensed Immediate Funds product, leveraging a relationship with Valid Systems.

• Optional real-time check fraud detection in mRDC and other points of presentment through licensing Check Fraud Manager.

Fundtech Fundtech supports commercial mRDC on its NetDeposit Mobile RDC product through a published API for integration with mobile banking platforms. Fundtech also offers an optional stand-alone mobile app which it brands NetDeposit Mobile Express. The products have been available since July 2014 and have multiple financial institutions deploying the product.

Users have a choice of using desktop capture, mobile capture, or both with these products. Where both methods are in use, all transactions flow through a common deposit review and approval process, with velocity rules rolling up across all deposit channels. The mobile user experience is that of a single-item deposit, but users of the desktop portal can aggregate into a single deposit as desired.

D+H announced its planned acquisition of Fundtech in March 2015.

JHA Alogent Originally entirely separate products for commercial and retail remote deposit, Alogent now offers a single platform — the Alogent Remote Deposit Interactive — allowing any combination of Alogent Commercial Remote Deposit, Alogent Retail Remote Deposit, Alogent Mobile Remote Deposit, and Alogent Payment Web Services to coexist in a single install. Moreover, a single client entity can leverage any combination of commercial check scanners, flatbed or multifunction devices, and mobile devices to service its deposit-taking needs. All enjoy consistent application of business rules, automation, and risk mitigation techniques including entitlements and limits, deposit review, and duplicate detection.

Alogent’s solutions are targeted to large banks, those with both the inclination and capability to manage user interface design. As such, Alogent provides a Payments Web Services approach rather than a stand-alone mRDC App.

Alogent’s point of presentment capture solutions interface with Alogent Payments Gateway in the back office, providing a single, solution for the processing of image-based transactions received throughout the enterprise. Alogent Payments Gateway supports the collection of images and data across intrabank and interbank point of presentment applications. The Gateway enables image processing functions such as image assurance, validation, correction, and balancing, and routes transactions to the appropriate endpoints for final processing, clearing, and settlement. A separately licensed Enterprise Duplicate Detection application is also available. Distinctive aspects of the product include:

• Deposit review can be accomplished at a desktop or on a mobile device.

Cha

pter

: Sol

utio

n La

ndsc

ape

20

• Pre-Qualification — Alogent Mobile Remote Deposit allows financial institutions to pre-qualify transactions in advance of make deposit calls. Prequalification also helps financial institutions improve the customer experience (because doing so eliminates the transmission of images that will be rejected based on limits) and optimize costs associated with mobile remote deposit.

• Supports multiple mobile image analytics engines.

JHA EPS Commercial Mobile RDC has been a staple of the EPS Product Suite since October 2013. EPS’ commercial mobile RDC capabilities allow field reps or branch offices to capture items via smartphones or tablets in parallel with business efforts to scan bulk check receipts using traditional scanners. It provides full user and item management capabilities, funneling items captured via mobile devices and traditional scanners through EPS’ common processing, risk management and reporting service. Financial institutions are able to apply limits and velocity controls to each merchant’s comprehensive remote capture throughput, regardless of the source of capture for individual items.

Mobile Remote Deposit Complete is a business remote capture solution designed specifically for smartphones and tablets. SMBs can leverage RDC and mRDC concurrently, capturing items from mail and front counter sources in the operations area via traditional check scanners, while simultaneously allowing field agents to capture items onsite during client visits via their iPhone or iPad, or their Android or Windows phone, or tablet. Items from all capture methods flow into EPS’ consolidated processing and reporting engine, ensuring consistent handling of all items regardless of capture source. Mobile Remote Deposit Complete also provides a low-cost entry into remote deposit capture for small businesses with relatively low check volumes, providing a path to remote deposit capture without the cost of a check scanner. Distinctive aspects of the EPS product include:

• A web-based, multipayment platform that encompasses remote deposit, ACH origination, and card transaction processing.

• QuickBooks integration, supporting fast and effortless cash application for those users.

• SmartSight, an optional data visualization and analysis tool that helps financial institutions gain actionable insights from its payment information dashboard that allows users to drill down into key metrics to better understand customer behavior and usage patterns.

NCR Beyond a common desktop and mobile RDC platform, NCR offers a single distributed capture platform across all points of presence, including teller and ATM capture. The benefits of this approach are manifest. For commercial mRDC, APTRA Passport Commercial Mobile offers users the ability to create and manage deposits, input optional configurable fields, and validate information. Centrally, APTRA Passport Hub stores and validates deposits, supports export of data to external systems, and performs system administration tasks. Distinctive aspects of APTRA Passport include:

• A single, highly configurable deposit gathering platform that supports all channels, devices, and workflows.

• QuickBooks integration, supporting fast and effortless cash application for those users.

• Immediate good funds support via integration with several risk decisioning platforms: FIS Certegy, Ingo Money, and Valid Systems.

Cha

pter

: Sol

utio

n La

ndsc

ape

21

Vsoft Formally the Agile product line, Vsoft rebranded its distributed capture product line coincident with a significant modernization of its platform, which is now fully web-based with a Responsive HTML 5 user interface design supporting a variety of devices, browsers, and operating systems.

Vsoft offers a triumvirate of RDC applications that all utilize a common back office aggregation platform. OnView Business Deposit for Check Scanners is a web-based application supporting “traditional” desktop scanning workflow. A separate product, OnView Business Deposit, supports consumer and SMB low volume check deposit needs through the use of flatbed scanners or multifunction devices. A third product, OnView Business Mobile Deposit, is its new mobile merchant RDC application. Using the same platform as OnView Business Deposit for Check Scanners, users can easily support multi-item deposits across multiple devices and device types. Supporting separation of duties, individual roles can be tied to device types if desired. As well, deposit review and approval, if configured as a separate role, can take place on any device type. The product is available as a stand-alone app, or may be integrated to third party mobile banking platforms using its published API.

In its current release (6.0, December 2014), OnView Business Deposit supports customer-defined fields in the desktop use case only, with mobile to follow in the next release. This can be used to associate individual items or deposits with customer account numbers or open invoices.

Wausau WAUSAU offers a complete distributed capture product suite, including branch and teller capture and separate products for commercial, consumer desktop, and mobile RDC — in both in-house and ASP environments. Its stalwart desktop commercial RDC product, Deposit 24/7 Merchant, will be outfitted with mRDC capability in Q4 2015.

Deposit 24/7 Merchant — a web-client for commercial RDC, with configuration options designed to support both small business and larger corporate clients on a single platform. Deposit 24/7 Merchant offers an optional integration with QuickBooks using web services. The product also offers the ability to handle deposit and payment transactions as well as originate ACH transactions. Celent found this capability highly useful for select merchant segments as well as among RDC solutions.

Deposit 24/7 Commercial Mobile will provide mobile device image capture either stand-alone or in concert with desktop RDC. The product will support multi-item deposits, end user keying of flexibly defined fields with each item, and consolidated workflow through Risk Management and Deposit 24/7 Merchant. Wausau plans availability in Q3 2015 for corporate clients and later in 2015 for its bank clients. Distinctive aspects of the Deposit 24/7 suite include:

• QuickBooks API-level integration, supporting fast and effortless cash application for those users.

• Ability to capture multiple checks and non-check items within one capture session and integrate document image capture with Wausau’s retail and wholesale lockbox platforms.

Cha

pter

: Con

clus

ion

22

CONCLUSION

As check payments continue their inexorable usage decline, mobile RDC will become increasingly relevant — both as a matter of convenience and for its lower solution cost compared to scanner-based approaches. In large measure, mobile is the new scanner.

At the same time, banks are seeking a much needed step-change improvement in branch channel effectiveness. New branch designs are incompatible with heavy transaction-oriented foot traffic. Thus banks need to offer customers convenient ways to transact using digital channels. With roughly 70% of SMB branch visits tied to counter deposits, a low-cost and easy-to-sell mRDC solution appropriate for SMBs is the missing ingredient.

While historically available solutions were too expensive for most SMBs and too complex for branch staff to effectively sell and onboard, new single-platform products that support both desktop and mobile capture options fit the bill perfectly. These products can be sold using stand-alone apps to hasten time to market and eventually integrated into banks’ small business digital offerings when they come to market. Leveraging mRDC for both mobile and low-volume use cases benefits both banks and their SMB customers by offering:

• The lowest possible product cost (no scanner, lower cost license). • A straightforward upgrade path for higher-volume check depositors desiring the

speed and efficiency of desktop scanners.

Was this report useful to you? Please send any comments, questions, or suggestions for upcoming research topics to [email protected].

Key Research Question

3

How have new vendor solutions changed things?

mRDC is the path to both low solution cost and compelling SMB benefits and will be increasingly

relevant as check usage declines

Cha

pter

: Lev

erag

ing

Cel

ent’s

Exp

ertis

e

23

LEVERAGING CELENT’S EXPERTISE

If you found this report valuable, you might consider engaging with Celent for custom analysis and research. Our collective experience and the knowledge we gained while working on this report can help you streamline the creation, refinement, or execution of your strategies.

SUPPORT FOR FINANCIAL INSTITUTIONS Typical projects we support related to remote deposit capture include:

Vendor short listing and selection. We perform discovery specific to you and your business to better understand your unique needs. We then create and administer a custom RFI to selected vendors to assist you in making rapid and accurate vendor choices.

Business practice evaluations. We spend time evaluating your business processes, particularly in channel and lockbox platform integration. Based on our knowledge of the market, we identify potential process or technology constraints and provide clear insights that will help you implement industry best practices.

IT and business strategy creation. We collect perspectives from your executive team, your front line business and IT staff, and your customers. We then analyze your current position, institutional capabilities, and technology against your goals. If necessary, we help you reformulate your technology and business plans to address short-term and long-term needs.

SUPPORT FOR VENDORS We provide services that help you refine your product and service offerings. Examples include:

Product and service strategy evaluation. We help you assess your market position in terms of functionality, technology, and services. Our strategy workshops will help you target the right customers and map your offerings to their needs.

Market messaging and collateral review. Based on our extensive experience with your potential clients, we assess your marketing and sales materials—including your website and any collateral.

Cha

pter

: Rel

ated

Cel

ent R

esea

rch

24

RELATED CELENT RESEARCH

State of Remote Deposit Capture 2015: Mobile is the new scanner May 2015

Receivables in Motion: The Changing Game Plan to Grow Treasury Management Revenue November 2014

Winning the Underbanked: How Banks Can Get an Omnichannel Upper Hand April 2014

Remote Deposit Capture Solutions 2013: Vendor ABCD View January 2014

Repeat Performance? Things Canadian Banks Can Learn from the US Check 21 Experience February 2013

Imaging in the Retail Channel 2012: A Teller Capture Renaissance October 2012

State of Consumer RDC 2012: The Death of Desktop October 2012

State of Remote Deposit Capture 2012: A Replacement Market Emerges September 2012

Imaging in the Retail Channel 2011: Seventh Inning Stretch November 2011

State of Remote Deposit Capture 2011: Signs of a Maturing Market October 2011

Taking it to the Teller Line: Considerations for Implementing Teller Image Capture September 2011

The Future of Consumer RDC: Going Mainstream November 2010

State of Remote Deposit Capture 2010: Unintended Consequences October 2010

Imaging in the Retail Channel 2010: A Second Wind for Teller Capture October 2010

Mobile RDC: Self Service for the Masses? October 2009

State of Remote Deposit Capture 2009: New Markets, New Models October 2009

Imaging in the Retail Channel 2009: Retail Remote Deposit Capture Comes of Age October 2009

Deposit Gathering Using Remote Deposit Capture: Case Studies from A to Z February 2009

Copyright Notice

Prepared by

Celent, a division of Oliver Wyman, Inc.

Copyright © 2015 Celent, a division of Oliver Wyman, Inc. All rights reserved. This report may not be reproduced, copied or redistributed, in whole or in part, in any form or by any means, without the written permission of Celent, a division of Oliver Wyman (“Celent”) and Celent accepts no liability whatsoever for the actions of third parties in this respect. Celent and any third party content providers whose content is included in this report are the sole copyright owners of the content in this report. Any third party content in this report has been included by Celent with the permission of the relevant content owner. Any use of this report by any third party is strictly prohibited without a license expressly granted by Celent. Any use of third party content included in this report is strictly prohibited without the express permission of the relevant content owner This report is not intended for general circulation, nor is it to be used, reproduced, copied, quoted or distributed by third parties for any purpose other than those that may be set forth herein without the prior written permission of Celent. Neither all nor any part of the contents of this report, or any opinions expressed herein, shall be disseminated to the public through advertising media, public relations, news media, sales media, mail, direct transmittal, or any other public means of communications, without the prior written consent of Celent. Any violation of Celent’s rights in this report will be enforced to the fullest extent of the law, including the pursuit of monetary damages and injunctive relief in the event of any breach of the foregoing restrictions.

This report is not a substitute for tailored professional advice on how a specific financial institution should execute its strategy. This report is not investment advice and should not be relied on for such advice or as a substitute for consultation with professional accountants, tax, legal or financial advisers. Celent has made every effort to use reliable, up-to-date and comprehensive information and analysis, but all information is provided without warranty of any kind, express or implied. Information furnished by others, upon which all or portions of this report are based, is believed to be reliable but has not been verified, and no warranty is given as to the accuracy of such information. Public information and industry and statistical data, are from sources we deem to be reliable; however, we make no representation as to the accuracy or completeness of such information and have accepted the information without further verification.

Celent disclaims any responsibility to update the information or conclusions in this report. Celent accepts no liability for any loss arising from any action taken or refrained from as a result of information contained in this report or any reports or sources of information referred to herein, or for any consequential, special or similar damages even if advised of the possibility of such damages.

There are no third party beneficiaries with respect to this report, and we accept no liability to any third party. The opinions expressed herein are valid only for the purpose stated herein and as of the date of this report.

No responsibility is taken for changes in market conditions or laws or regulations and no obligation is assumed to revise this report to reflect changes, events or conditions, which occur subsequent to the date hereof.

For more information please contact [email protected] or:

Bob Meara [email protected] AMERICAS EUROPE ASIA

USA

200 Clarendon Street, 12th Floor Boston, MA 02116

Tel.: +1.617.262.3120 Fax: +1.617.262.3121

France

28, avenue Victor Hugo Paris Cedex 16 75783

Tel.: +33.1.73.04.46.20 Fax: +33.1.45.02.30.01

Japan

The Imperial Hotel Tower, 13th Floor 1-1-1 Uchisaiwai-cho Chiyoda-ku, Tokyo 100-0011

Tel: +81.3.3500.3023 Fax: +81.3.3500.3059

USA

1166 Avenue of the Americas New York, NY 10036

Tel.: +1.212.541.8100 Fax: +1.212.541.8957

United Kingdom

55 Baker Street London W1U 8EW

Tel.: +44.20.7333.8333 Fax: +44.20.7333.8334

China

Beijing Kerry Centre South Tower, 15th Floor 1 Guanghua Road Chaoyang, Beijing 100022

Tel: +86.10.8520.0350 Fax: +86.10.8520.0349

USA

Four Embarcadero Center, Suite 1100 San Francisco, CA 94111

Tel.: +1.415.743.7900 Fax: +1.415.743.7950

Italy

Galleria San Babila 4B Milan 20122

Tel.: +39.02.305.771 Fax: +39.02.303.040.44

China

Central Plaza, Level 26 18 Harbour Road, Wanchai Hong Kong

Tel.: +852.2982.1971 Fax: +852.2511.7540

Brazil

Av. Doutor Chucri Zaidan, 920 – 4º andar Market Place Tower I São Paulo SP 04578-903

Tel.: +55.11.5501.1100 Fax: +55.11.5501.1110

Canada

1981 McGill College Avenue Montréal, Québec H3A 3T5

Tel.: +1.514.499.0461

Spain

Paseo de la Castellana 216 Pl. 13 Madrid 28046

Tel.: +34.91.531.79.00 Fax: +34.91.531.79.09

Switzerland

Tessinerplatz 5 Zurich 8027

Tel.: +41.44.5533.333

Singapore

8 Marina View #09-07 Asia Square Tower 1 Singapore 018960

Tel.: +65.9168.3998 Fax: +65.6327.5406

South Korea

Youngpoong Building, 22nd Floor 33 Seorin-dong, Jongno-gu Seoul 110-752 Tel.: +82.10.3019.1417 Fax: +82.2.399.5534