seizing opportunities and confronting challenges in ... · pdf fileseizing opportunities and...

TRANSCRIPT

Seizing Opportunities and Confronting Challenges in Accountancy; Lessons and

Experiences from ICAI

PRESENTATION BY

CA. (Dr.) DEBASHIS MITRAM.Com, LL.B, F.C.A, A.C.M.A, A.C.S, DISA (ICA), Ph.D.

Central Council Member, ICAI

The Institute of Chartered Accountants of India

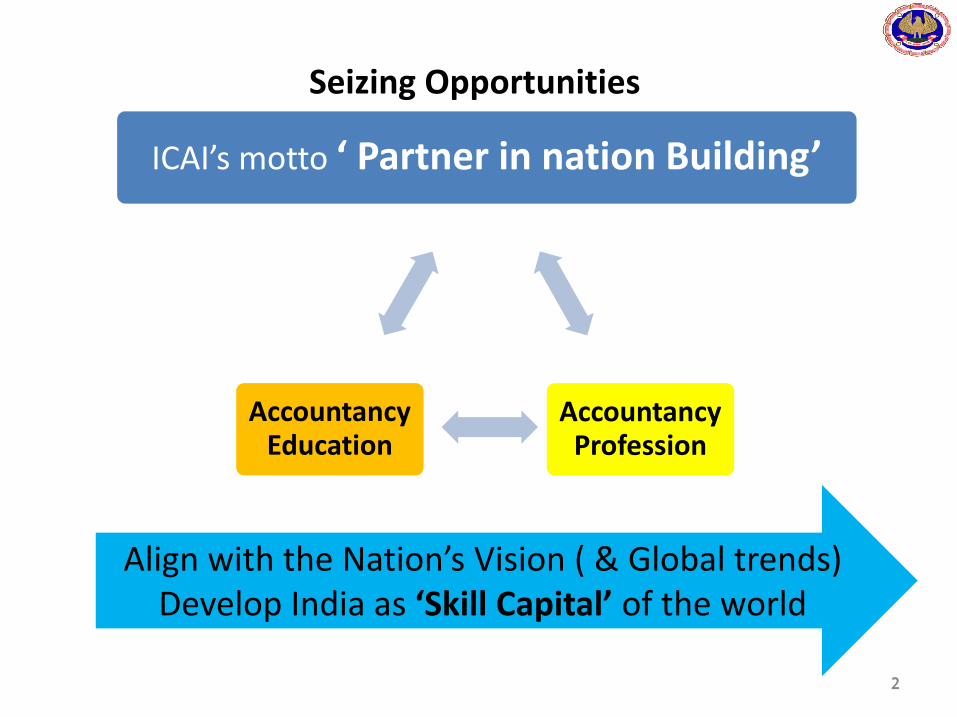

Seizing Opportunities

ICAI’s motto ‘ Partner in nation Building’

22

Accountancy Profession

Accountancy Education

Align with the Nation’s Vision ( & Global trends) Develop India as ‘Skill Capital’ of the world

ICAI’s Role

• ICAI was set up in 1949 under the Chartered Accountants Act,1949.

• Over a period of time the ICAI has achieved recognition as apremier accounting body not only in the country but also globally,for maintaining highest standards in technical, ethical areas andfor sustaining stringent examination and education standards.for sustaining stringent examination and education standards.

• In view of changing legal and economic environment, ICAI hasalways endeavoured to cater the changing needs of the professionand its members.

• ICAI acts as ‘Partner in Nation Building’ and intend to remainconverged with high quality accounting framework that is globallyaccepted.

33

ICAI’s Role (Contd..)

• Regulate the profession of Accountancy• Formulation of Accounting Standards• Prescription of Standard Auditing Procedures• Laying down Ethical Standards• Education and Examination of Chartered Accountancy

CourseCourse• Continuing Professional Education of Members• Conducting Post Qualification Courses• Monitoring Quality through Peer Review• Ensuring Standards of performance of Members• Exercise Disciplinary Jurisdiction• Financial Reporting Review• Input on Policy matters to Government

ICAI’s Role (Contd..)

Apart from the above, ICAI also endeavorsprofessional development:

• Identifying Role of Profession in emerging areas• Developing Practice Areas• Developing Practice Areas• Upgrading and updating the knowledge and skill

sets• Developing technical material to facilitate

practice in new areas• Considered as critical in the changed Scenario

Enabling ‘Financial Reporting Discipline’ …..

Financial reporting is an integral and important part ofgood corporate governance.

In order to make sound financial reporting, it isimperative that there are sound, reliable and highimperative that there are sound, reliable and highquality financial reporting structure in the country.

With globalisation, it has become essential that therewould be a single set of high quality accountingstandards to appreciate the differences in GAAPrequirements of various countries.

66

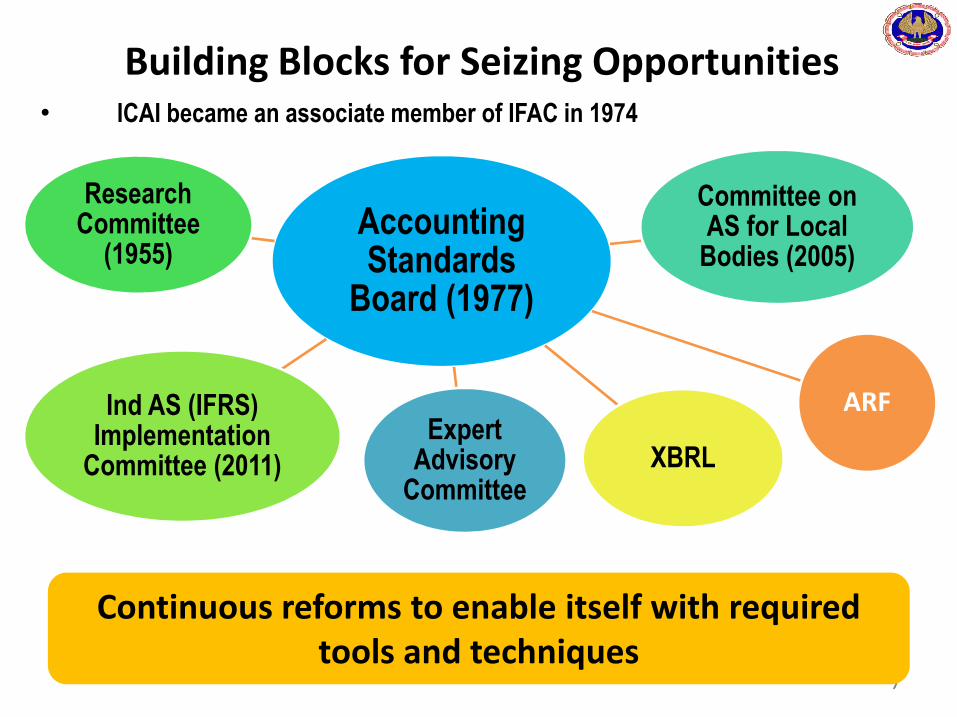

Building Blocks for Seizing Opportunities• ICAI became an associate member of IFAC in 1974

Accounting Standards

Board (1977)

Committee on AS for Local

Bodies (2005)

Research Committee

(1955)

77

Expert Advisory

Committee

Ind AS (IFRS) Implementation

Committee (2011) XBRL

ARF

Continuous reforms to enable itself with required tools and techniques

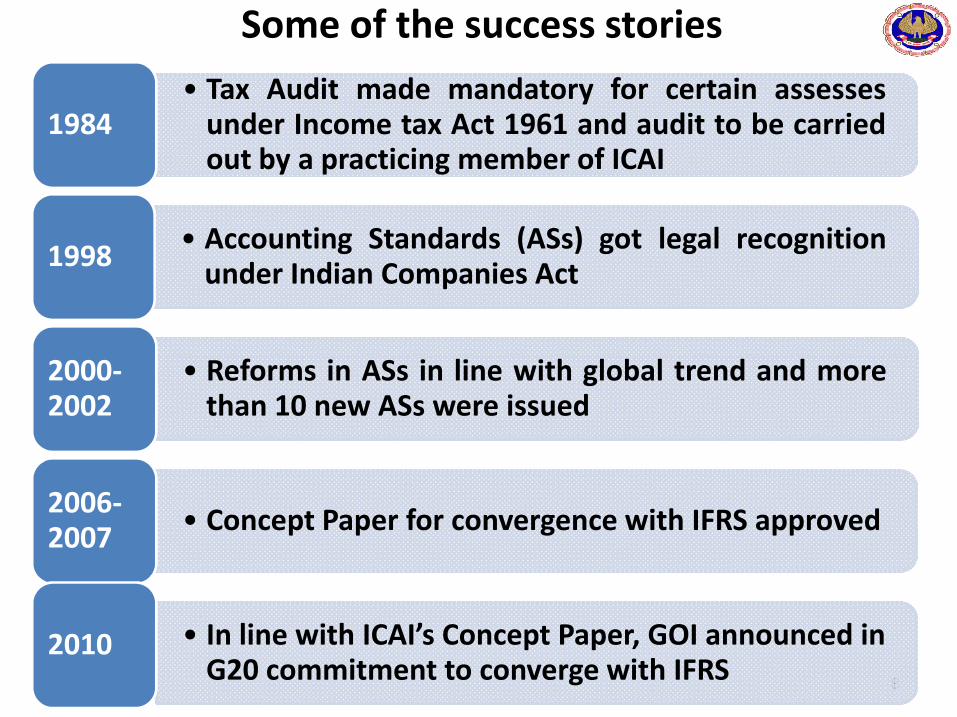

Some of the success stories

• Tax Audit made mandatory for certain assessesunder Income tax Act 1961 and audit to be carriedout by a practicing member of ICAI

1984

• Accounting Standards (ASs) got legal recognitionunder Indian Companies Act

1998

• Reforms in ASs in line with global trend and more2000-

88

• Reforms in ASs in line with global trend and morethan 10 new ASs were issued

2000-2002

• Concept Paper for convergence with IFRS approved2006-2007

• In line with ICAI’s Concept Paper, GOI announced inG20 commitment to converge with IFRS

2010

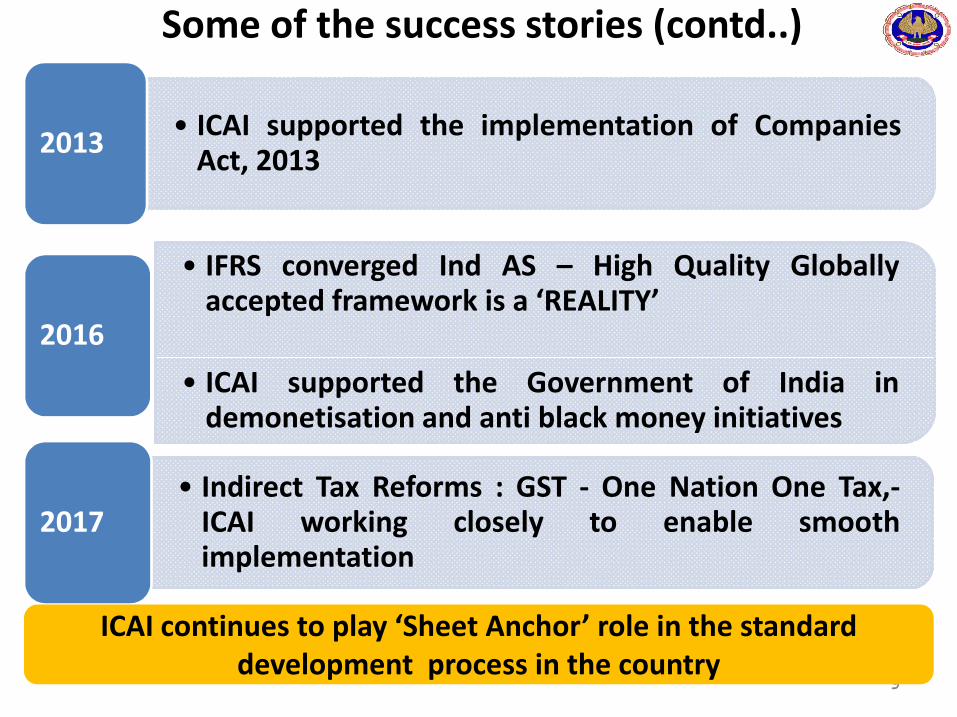

Some of the success stories (contd..)

• ICAI supported the implementation of CompaniesAct, 2013

2013

• IFRS converged Ind AS – High Quality Globallyaccepted framework is a ‘REALITY’

2016

99

• ICAI supported the Government of India indemonetisation and anti black money initiatives

• Indirect Tax Reforms : GST - One Nation One Tax,-ICAI working closely to enable smoothimplementation

2017

ICAI continues to play ‘Sheet Anchor’ role in the standard development process in the country

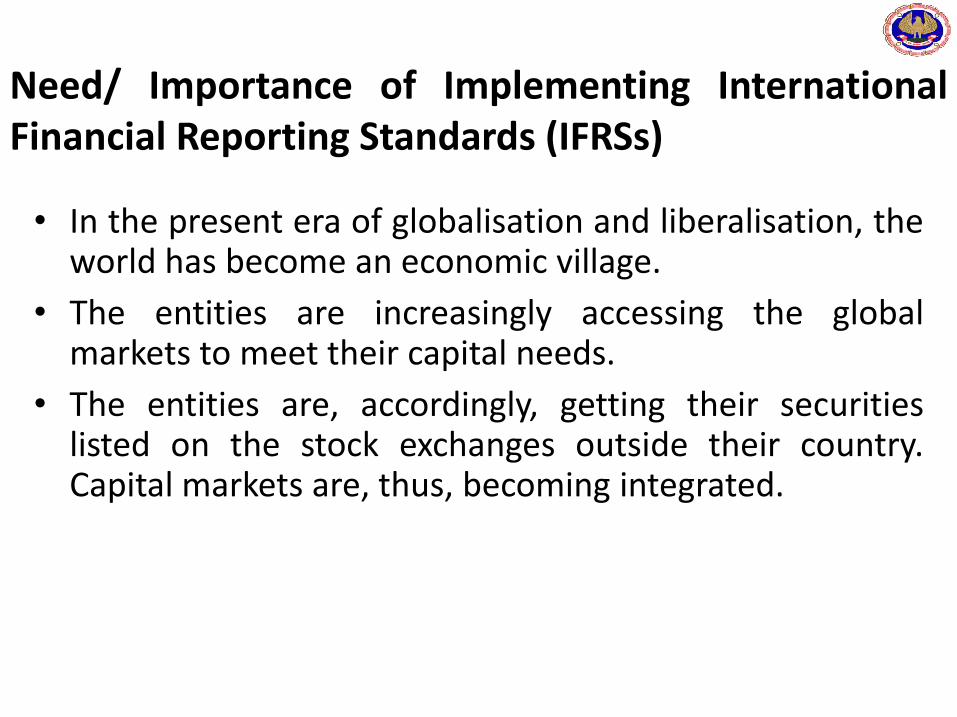

Need/ Importance of Implementing InternationalFinancial Reporting Standards (IFRSs)

• In the present era of globalisation and liberalisation, theworld has become an economic village.

• The entities are increasingly accessing the globalmarkets to meet their capital needs.markets to meet their capital needs.

• The entities are, accordingly, getting their securitieslisted on the stock exchanges outside their country.Capital markets are, thus, becoming integrated.

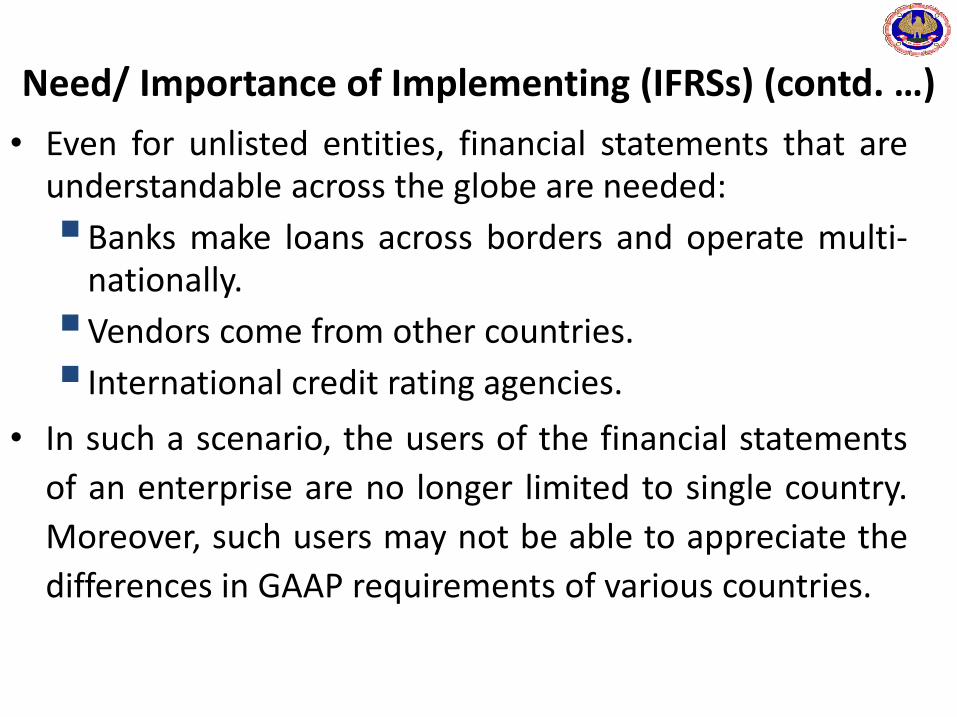

Need/ Importance of Implementing (IFRSs) (contd. …)

• Even for unlisted entities, financial statements that areunderstandable across the globe are needed:

Banks make loans across borders and operate multi-nationally.

Vendors come from other countries.

International credit rating agencies.

• In such a scenario, the users of the financial statements

of an enterprise are no longer limited to single country.

Moreover, such users may not be able to appreciate the

differences in GAAP requirements of various countries.

Need/ Importance of Implementing (IFRSs) (contd. …)

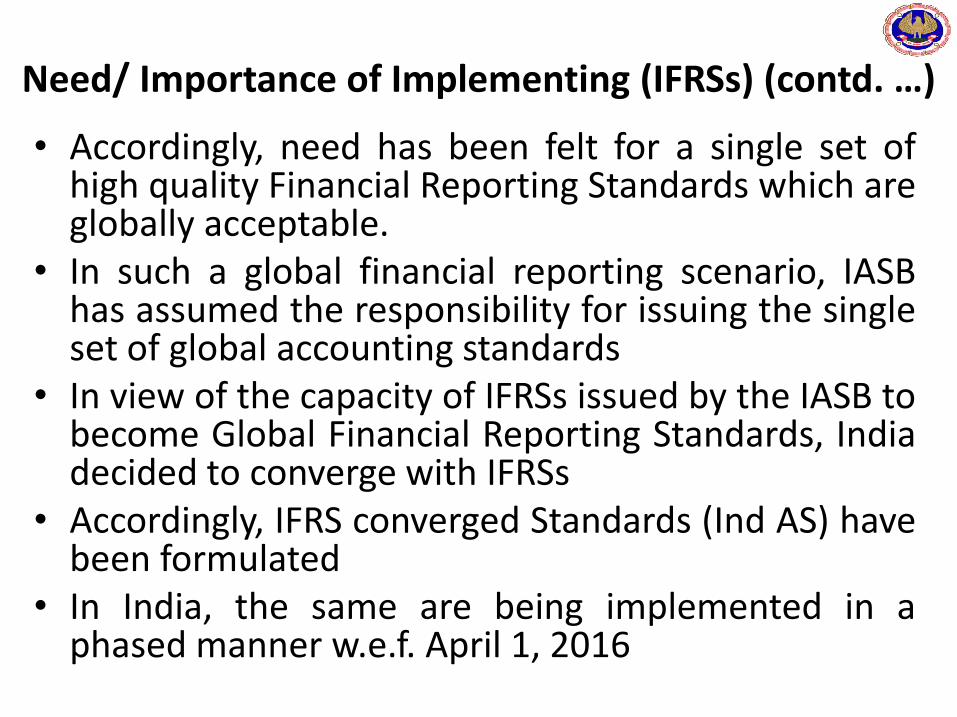

• Accordingly, need has been felt for a single set ofhigh quality Financial Reporting Standards which areglobally acceptable.

• In such a global financial reporting scenario, IASBhas assumed the responsibility for issuing the singleset of global accounting standardsset of global accounting standards

• In view of the capacity of IFRSs issued by the IASB tobecome Global Financial Reporting Standards, Indiadecided to converge with IFRSs

• Accordingly, IFRS converged Standards (Ind AS) havebeen formulated

• In India, the same are being implemented in aphased manner w.e.f. April 1, 2016

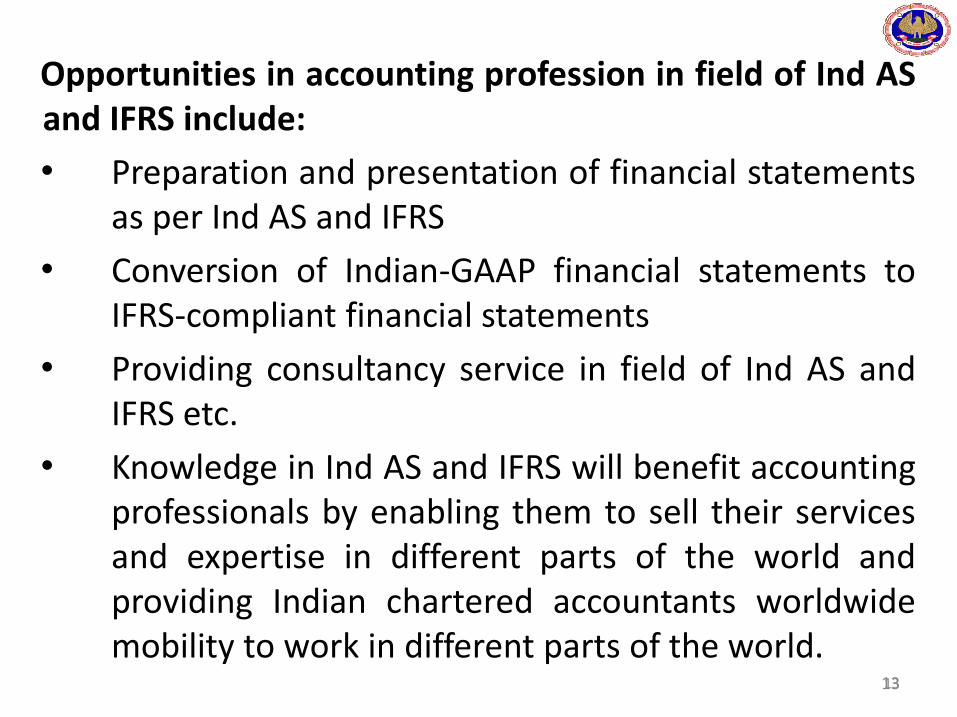

Opportunities in accounting profession in field of Ind ASand IFRS include:

• Preparation and presentation of financial statementsas per Ind AS and IFRS

• Conversion of Indian-GAAP financial statements toIFRS-compliant financial statements

• Providing consultancy service in field of Ind AS and• Providing consultancy service in field of Ind AS andIFRS etc.

• Knowledge in Ind AS and IFRS will benefit accountingprofessionals by enabling them to sell their servicesand expertise in different parts of the world andproviding Indian chartered accountants worldwidemobility to work in different parts of the world.

1313

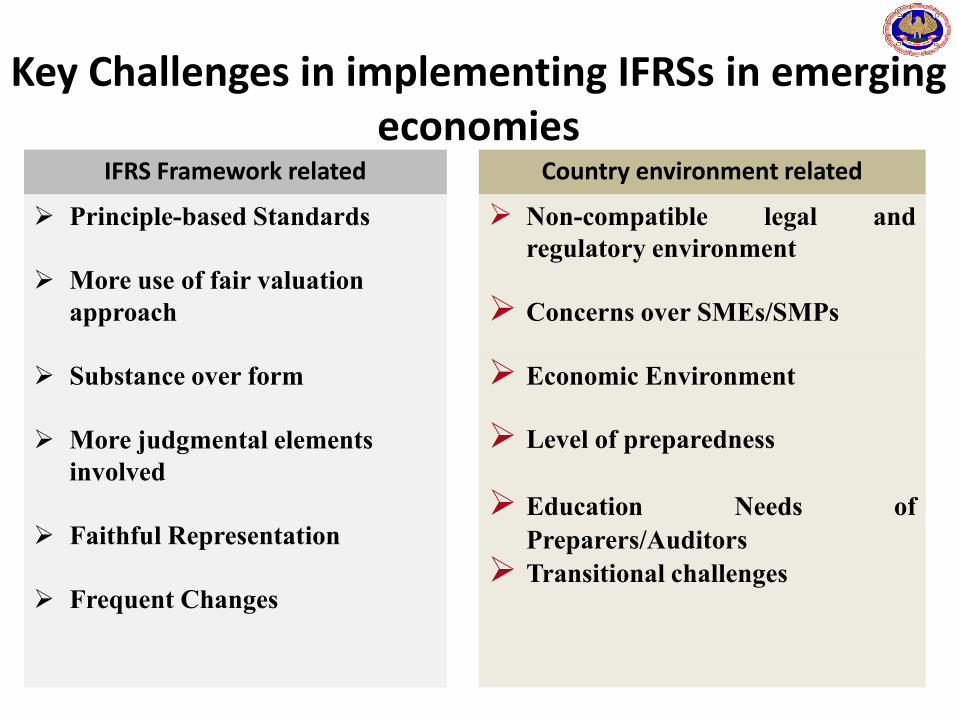

Key Challenges in implementing IFRSs in emerging economies

IFRS Framework related Country environment related

Principle-based Standards

More use of fair valuation approach

Non-compatible legal andregulatory environment

Concerns over SMEs/SMPs

Substance over form

More judgmental elements involved

Faithful Representation

Frequent Changes

Economic Environment

Level of preparedness

Education Needs of

Preparers/Auditors

Transitional challenges

Key Challenges in implementing IFRSs in emerging economies (Contd. …)

SME Concerns

Such entities face problems in implementing IFRSs

because of:

Scarcity of resources and expertise with the SMEs to Scarcity of resources and expertise with the SMEs to

achieve compliance with IFRSs

Cost of compliance with IFRSs not commensurate with

the expected benefits

Key Challenges in implementing IFRSs in emerging economies (Contd. …)

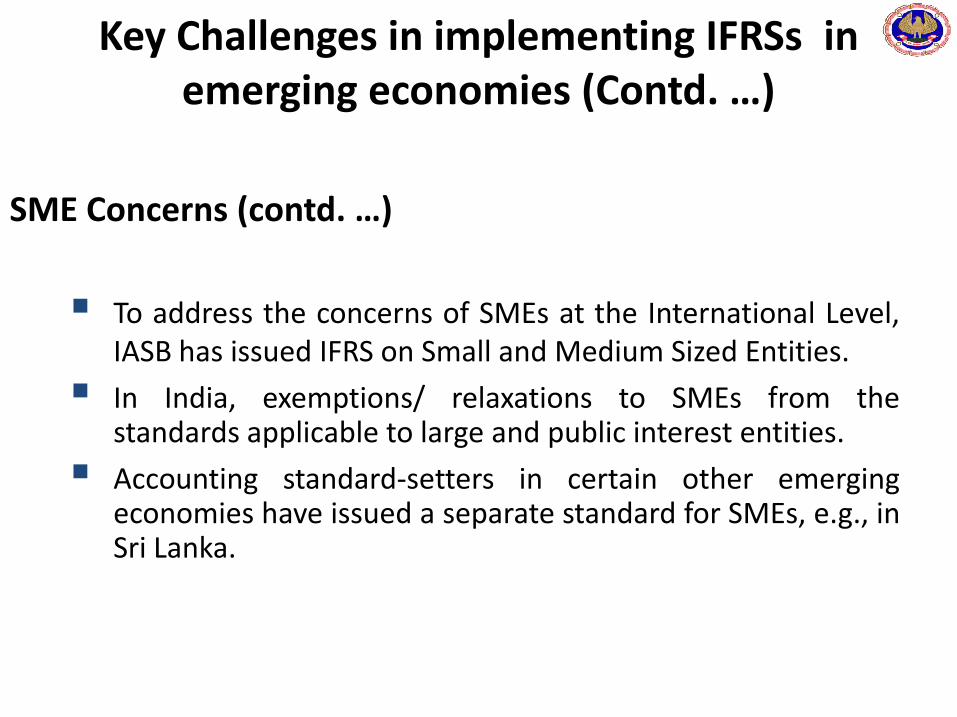

SME Concerns (contd. …)

To address the concerns of SMEs at the International Level,IASB has issued IFRS on Small and Medium Sized Entities.IASB has issued IFRS on Small and Medium Sized Entities.

In India, exemptions/ relaxations to SMEs from thestandards applicable to large and public interest entities.

Accounting standard-setters in certain other emergingeconomies have issued a separate standard for SMEs, e.g., inSri Lanka.

Key Challenges in implementing IFRSs in emerging economies (Contd.…)

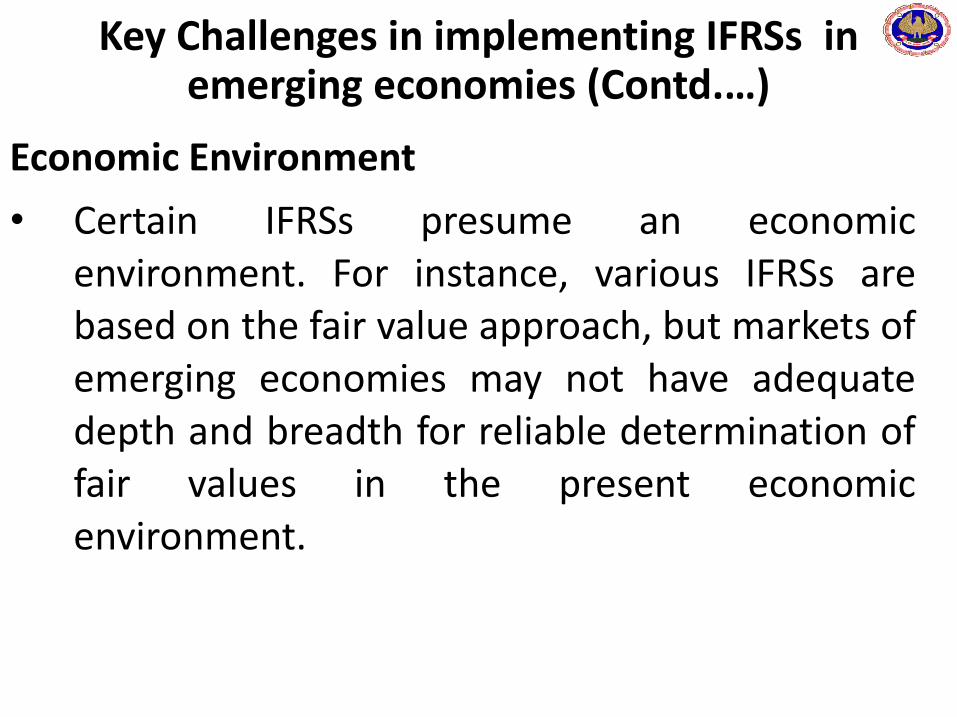

Economic Environment

• Certain IFRSs presume an economicenvironment. For instance, various IFRSs arebased on the fair value approach, but markets ofemerging economies may not have adequateemerging economies may not have adequatedepth and breadth for reliable determination offair values in the present economicenvironment.

Key Challenges in implementing IFRSs in emerging economies (Contd. …)

Level of Preparedness

• In a few cases, practical difficulties are perceivedin implementation of certain IFRSs in countrieswith emerging economies, considering the levelof preparedness in these countries.of preparedness in these countries.

• Accounting Standard-setters in such countries arerequired to consider these difficulties and makeappropriate changes in the corresponding IFRSfor the time being till preparedness is achieved.

Key Challenges in implementing IFRSs in emerging economies (Contd.…)

Education Needs of Preparers/ Auditors

Some IFRSs are very complex

Countries with Emerging Economies have also adopted/ adapted theabove IASs or are in the process of doing so.

above IASs or are in the process of doing so.

It is felt that proper implementation of such IFRSs requires extensiveeducation of preparers/ auditors in such countries.

There is a need to bring more educational material on such complexIFRSs.

To address the education needs, Accounting Standard-setters inemerging economies may organise joint seminars/ work-shops forsharing their experiences in implementation of IFRSs.

Key Challenges in implementing IFRSs in emerging economies (Contd. …)

Frequent Changes to the IFRSs Frequent changes and complexity of those changes has also been

the important hurdle in the adoption of IFRSs

If accounting standards are to be incorporated in the law as incase of India, it is very difficult to amend the law again and againcase of India, it is very difficult to amend the law again and againwith every change in IFRSs

IASB should try to strike a balance between the need to improvethe IFRSs and the practical issue of providing time to countries inimplementation of the revised standard

Key Challenges in implementing IFRSs in emerging economies (Contd. …)

Transition to IFRS

• Transition to IFRS involves huge efforts, hence, any transition of this size & nature comes with its own set of challenges.

• Transition brings in significant changes in the accounting withimplications on Taxation of entities. Therefore, needs big co-ordination with Tax Authorities.ordination with Tax Authorities.

• IFRSs are principle based standards with ‘substance over form’ askey fundamental driver. This entails extensive use of professionaland management judgement.

• Transition brings in many changes in the way the transactions arecurrently accounted, which in turn will require many changes tothe entities policies and processes and of course, changes to ITsystems.

ICAI’s experience in confrontingchallengesThe Institute of Chartered Accountants of India hasrecognised challenges at early stage and is making everypossible effort in this direction.

• ICAI being regulator of accounting profession in India,apart from helping in smooth transition to Ind AS, has aICAI being regulator of accounting profession in India,apart from helping in smooth transition to Ind AS, has arole of ensuring that these Ind AS are implemented inthe same spirit in which these have been formulated.

• ICAI is also ensuring that members have the right skillsto serve global markets which are regularly updatedand are relevant in the changing economic scenario.

ICAI’s experience in confronting challenges• ICAI is working to provide holistic education, effective practical training and

continuous professional development to ensure that the knowledge base of theprofession keeps pace with emerging global practices and innovations

• Ind AS (IFRS) Implementation Committee has been constituted by ICAI which isundertaking various initiatives to facilitate smooth transition and implementationof Ind AS, such as, issuing Educational Materials on Ind AS, clarifications by way ofInd AS Transition Facilitation Group bulletins.

• There are regular interactions with staff of IASB by the ASB• Play active role in various international forums of IFRS Foundation- Emerging

Economies Group (EEG), Asia-Oceanic Standard-setters Group (AOSSG),International Federation of Standard-setters (IFASS) and so on.

• ICAI is in continuous dialogue with key regulators, such as, Reserve Bank of India(RBI), Insurance Regulatory and Development Authority of India (IRDA), Ministry ofCorporate Affairs (MCA), etc., to address issues involved in Ind ASimplementation.

ICAI’s experience in confronting challengesInd AS (IFRS) Implementation Committee constituted by ICAI whichundertakes following initiatives to facilitate smooth transition andimplementation of Ind AS:

• Issuing Educational Materials covering FAQs

• Formation of Ind AS Transition Facilitation Group to address Ind AS implementation issues on urgent basis.

• Formation of Ind AS support desk

• Conducting 12-days certificate course on IFRS to impart knowledge about • Conducting 12-days certificate course on IFRS to impart knowledge about IFRS and Ind AS.

• Developing E-learning modules

• Organising training programmes on Ind AS for various regulators, organisations and corporate houses are also organised, etc.

Issues which need to be discussed with International Accounting StandardsBoard (IASB) are also taken up by the ASB

ICAI’s experience in confronting challengesInd AS successfully implemented in India

• In Phase I, approximately 600 listed companies excluding their subsidiarieshave implemented Ind AS.

• In Phase II, approximately 10,000 companies will be implementing Ind AS.

• In case of Banks and Insurance Companies, their Sectoral Regulators viz.RBI & IRDA have taken keen interest in implementing Ind AS. SectoralRegulators have issued instructions for conducting parallel runs by theentities.

• ICAI is also playing a proactive role to smoothen the transition process

• As major sector of Indian industry is transitioning to Ind AS, ICAI hasenabled them to realise benefits of globally accepted high qualityaccounting framework.

Way-Forward

• In our national role as ‘Partner in Nation Building’, weintend to remain converged with high quality accountingframework that is globally accepted. For the purpose ofremaining at par with IFRS, Ind AS are amended from timeto time in line with the amendments taking place in IFRS.

• Going forward, we have intention to remove the carve-outsmade in Ind AS.

• We also see this convergence as an opportunity to servethe global community by providing highly skilledaccountants. This is in line with our national vision todevelop India into ‘Skill Capital’ of the world.

THANK YOUTHANK YOUContact for more details : [email protected]

Follow ICAI on Social Media - http://www.icai.org/followus