section ii: man made fibres -...

TRANSCRIPT

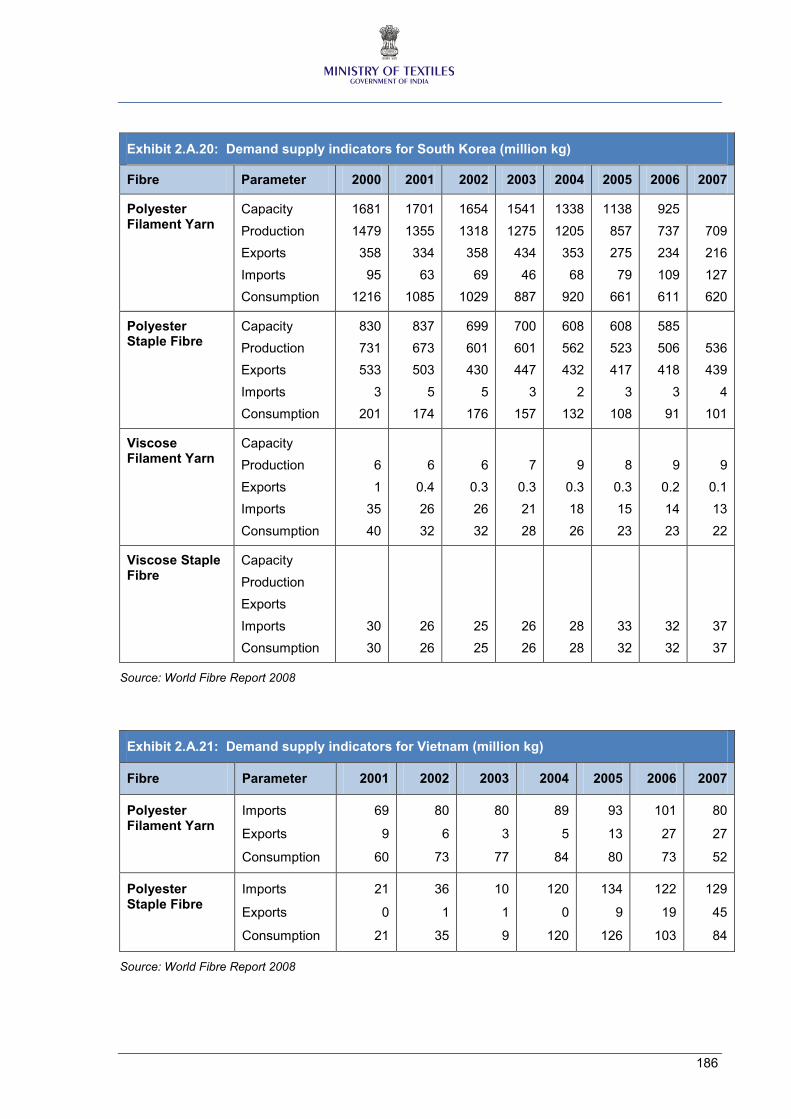

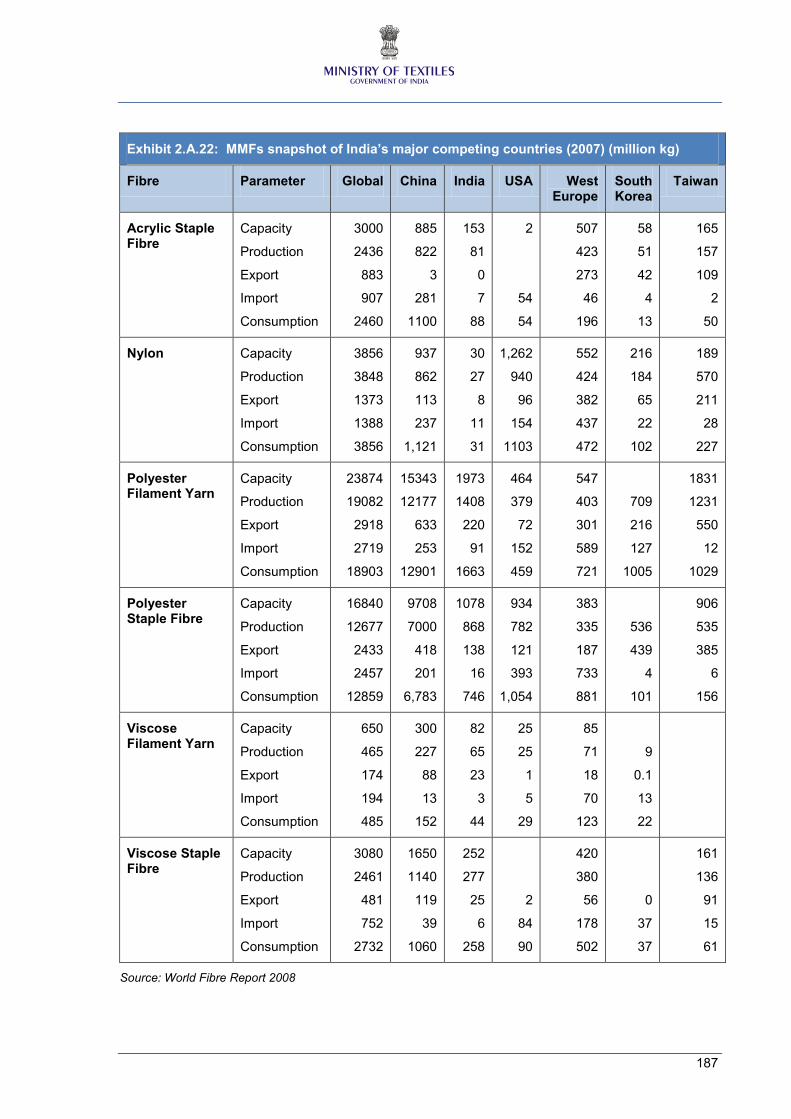

SECTION II: MAN MADE FIBRES

110

TABLE OF CONTENTS

SUMMARY – MAN MADE FIBRES ..................................................................................................... 112

2.1. INDIAN SCENARIO ...................................................................................................................... 120

IMPORTANT MMF PLAYER IN THE WORLD .............................................................................. 120

CHANGING FIBRE COMPOSITION ............................................................................................. 120

POLYESTER ACCOUNTS FOR LARGEST SHARE IN MMF ...................................................... 122

EXCESS CAPACITIES .................................................................................................................. 122

LIMITED NUMBER OF PLAYERS ................................................................................................. 123

RAW MATERIALS AVAILABILITY ................................................................................................. 123

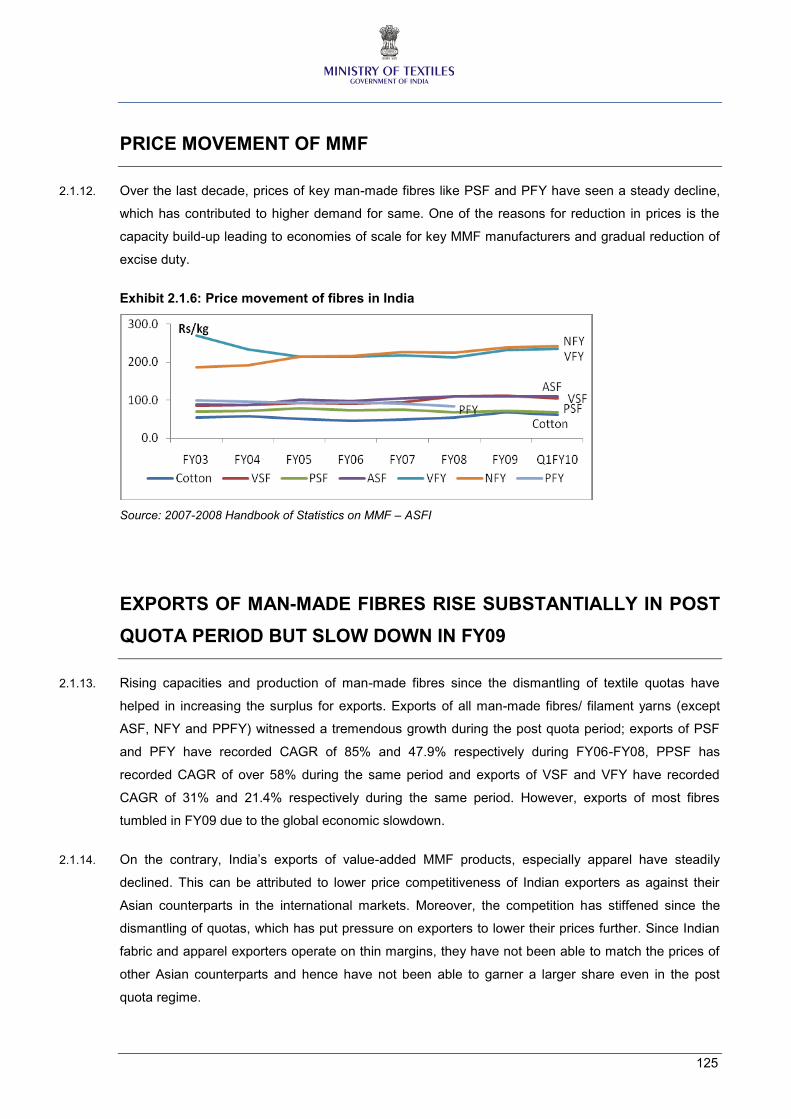

PRICE MOVEMENT OF MMF ....................................................................................................... 125

EXPORTS OF MAN-MADE FIBRES RISE SUBSTANTIALLY IN POST QUOTA PERIOD BUT

SLOW DOWN IN FY09 .................................................................................................................. 125

POLYESTER STAPLE FIBRE ....................................................................................................... 127

VISCOSE STAPLE FIBRE ............................................................................................................. 127

ACRYLIC STAPLE FIBRE ............................................................................................................. 128

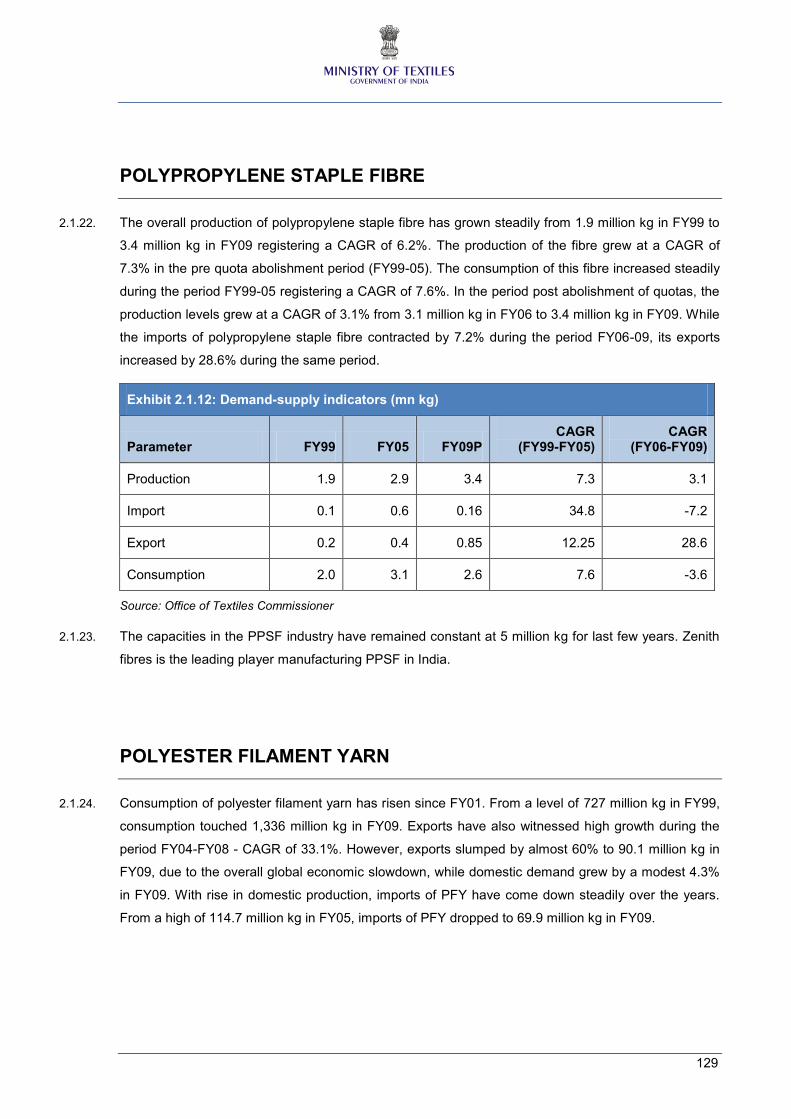

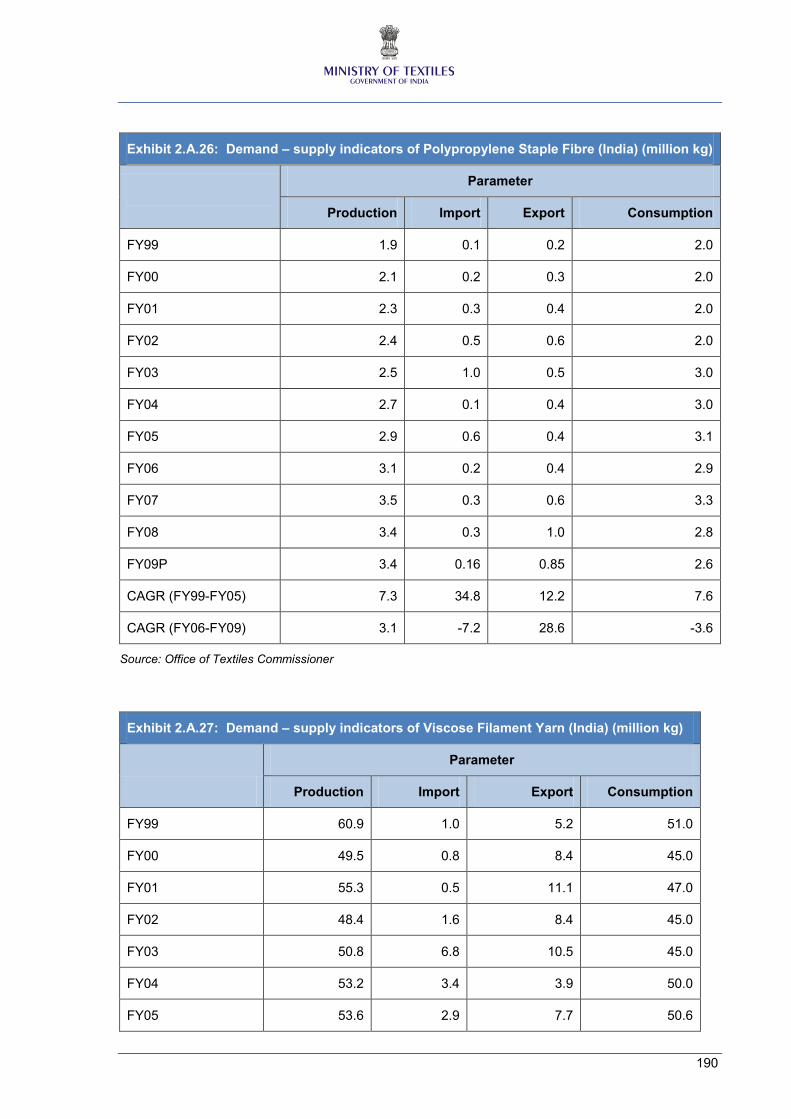

POLYPROPYLENE STAPLE FIBRE ............................................................................................. 129

POLYESTER FILAMENT YARN .................................................................................................... 129

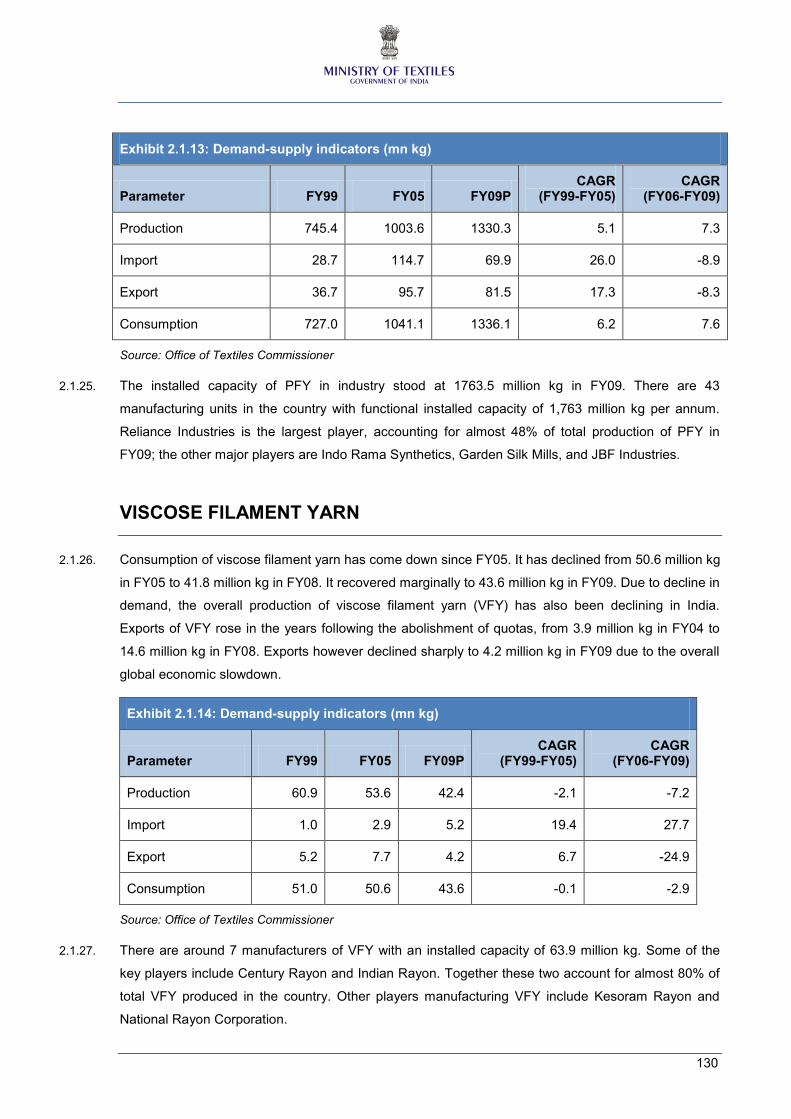

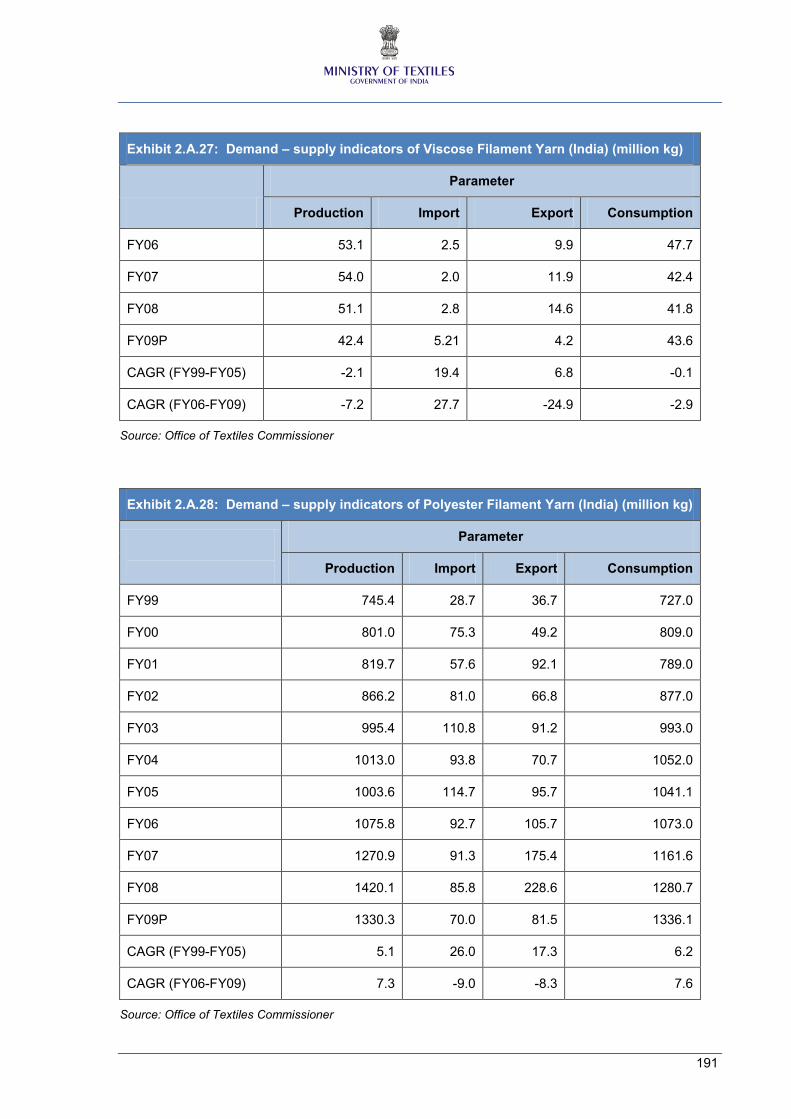

VISCOSE FILAMENT YARN ......................................................................................................... 130

NYLON FILAMENT YARN ............................................................................................................. 131

POLYPROPYLENE FILAMENT YARN .......................................................................................... 131

DYNAMICS OF VALUE ADDED MMF TEXTILES ........................................................................ 132

FUTURE DEMAND FOR MMF ...................................................................................................... 133

2.2. GLOBAL SCENARIO ................................................................................................................... 136

COMPOSITION OF MAN-MADE FIBRES ..................................................................................... 137

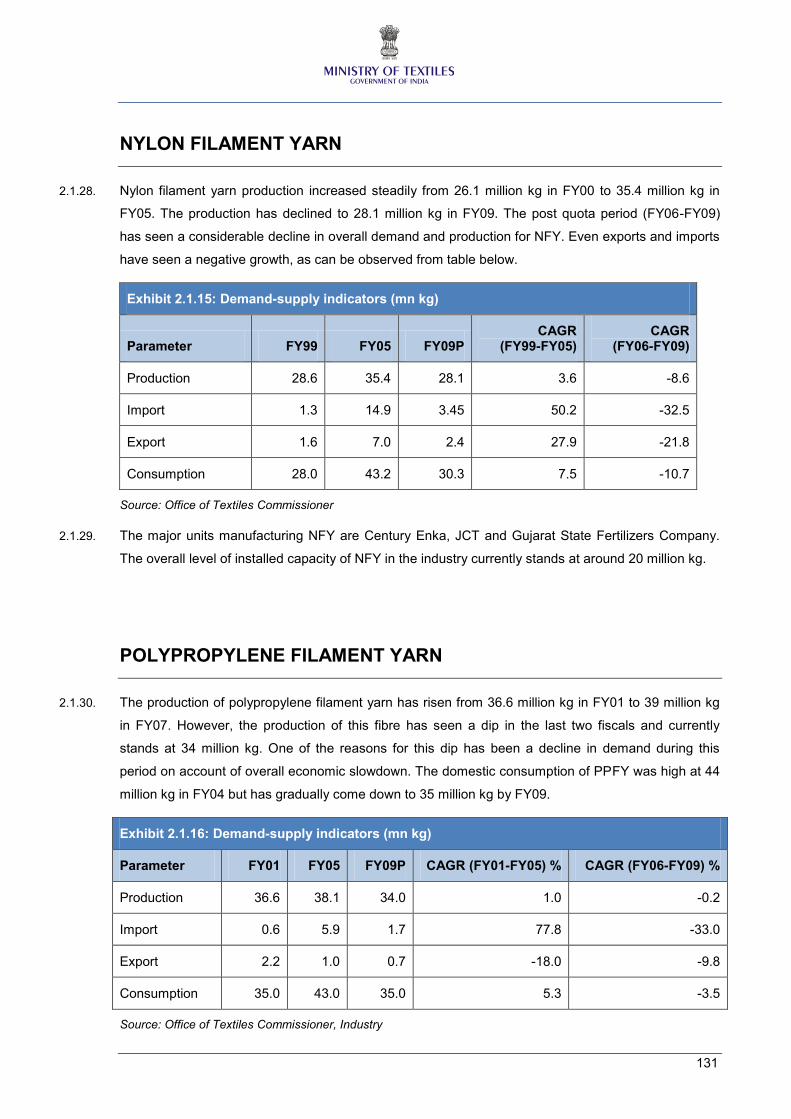

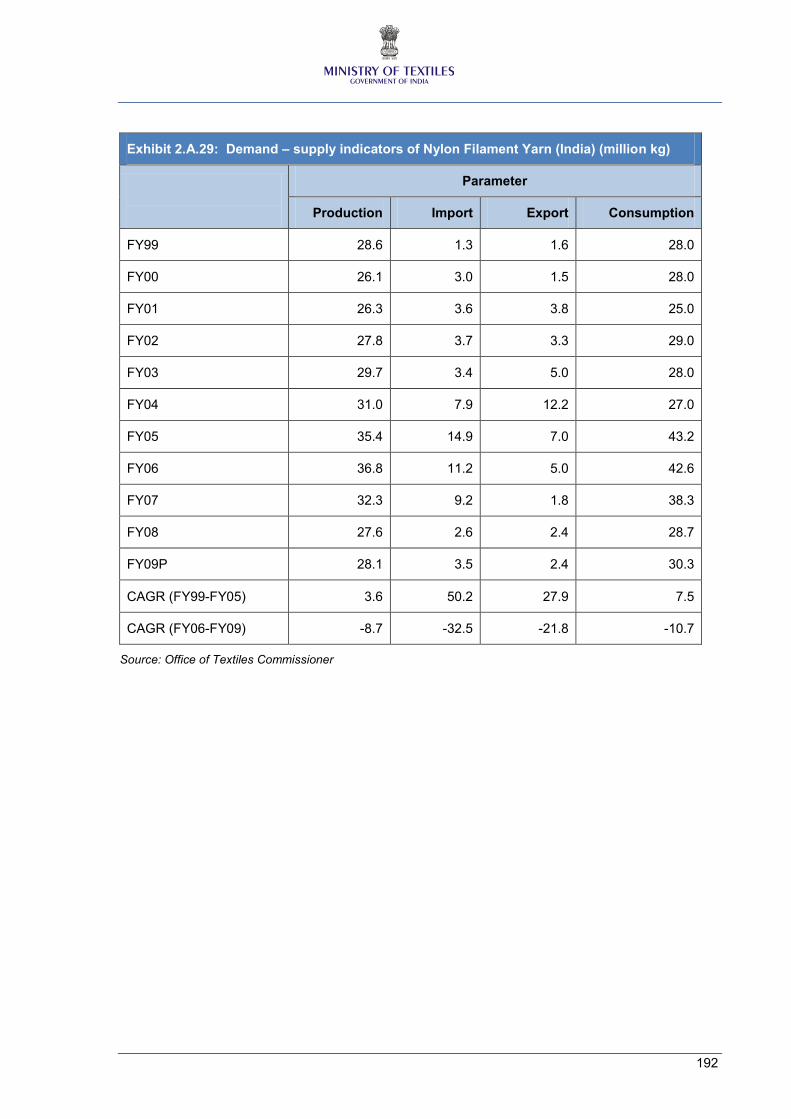

REGIONAL COMPOSITION .......................................................................................................... 138

2.3. ISSUES AND CONCERNS ........................................................................................................... 141

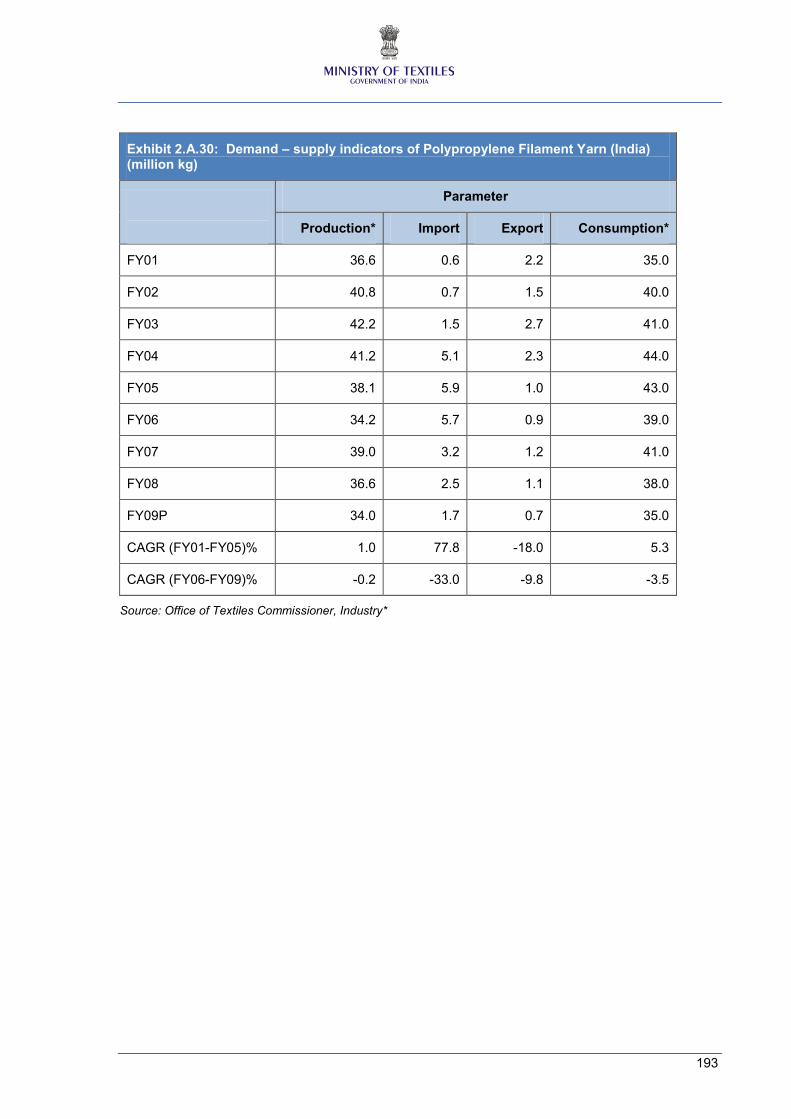

EXCISE DUTY ANOMALIES ......................................................................................................... 141

CUSTOMS DUTY ANOMALIES .................................................................................................... 142

DELAY IN GETTING DRAWBACK /EXCISE REBATE CLAIMS ................................................... 143

111

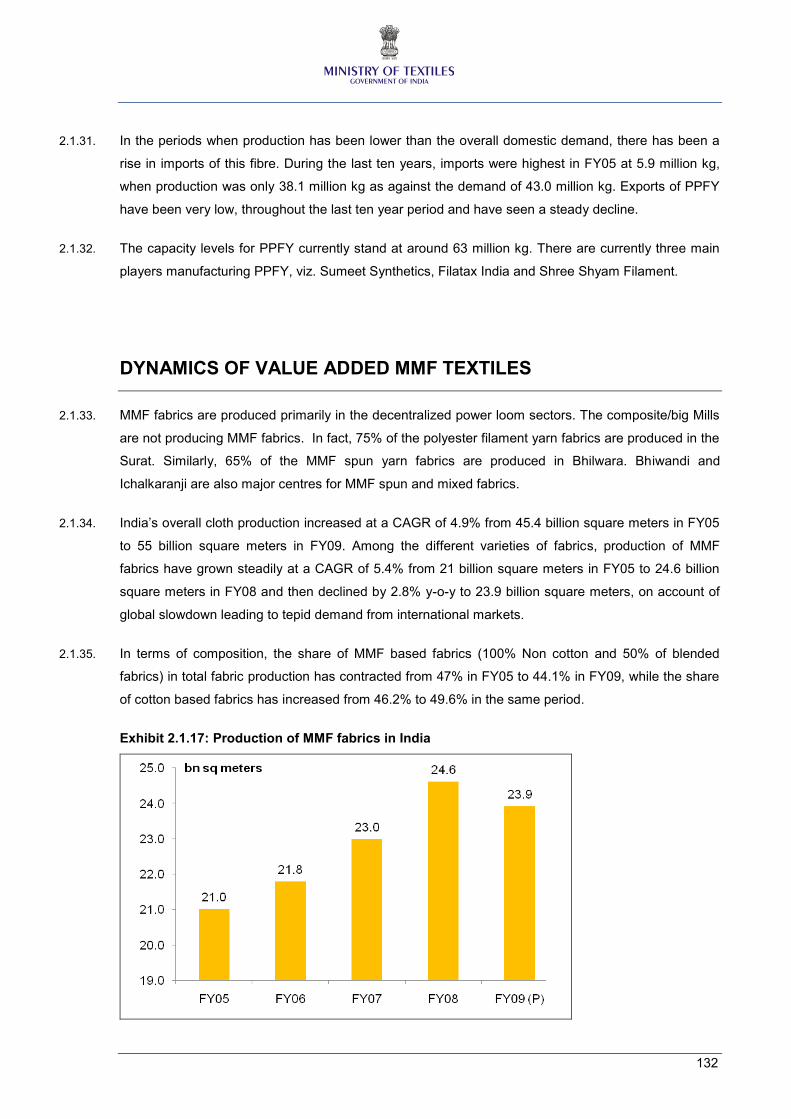

CONCERNS ABOUT ANTI DUMPING DUTIES............................................................................ 144

LOWER EXPORT BENEFITS FOR STANDALONE GARMENT MANUFACTURERS ................ 144

CONCERNS ABOUT GST ............................................................................................................. 145

NIL INDIGENOUS PRODUCTION OF SPECIALISED MMF ........................................................ 145

LIMITED NUMBER OF MMF PLAYERS ....................................................................................... 145

LACK OF COMPETITIVENESS IN EXPORTS ............................................................................. 147

EXPORTS DISADVANTAGE AGAINST COTTON TEXTILES ..................................................... 148

HIGHER EXPORT PRICES OF INDIAN EXPORTERS ................................................................ 150

LACK OF INCENTIVES FOR EXPANSION .................................................................................. 151

RAW MATERIAL AVAILABILITY ................................................................................................... 152

COST RELATED ISSUES ............................................................................................................. 153

HIGH TRANSACTION COSTS ...................................................................................................... 154

SUMMARY ..................................................................................................................................... 156

2.4. RECOMMENDATIONS ................................................................................................................. 157

FISCAL MEASURES ..................................................................................................................... 157

NON-FISCAL MEASURES ............................................................................................................ 161

2.A. ANNEXURE .................................................................................................................................. 164

TEXTILE OVERVIEW AND POLICIES IN MAJOR COUNTRIES ................................................. 164

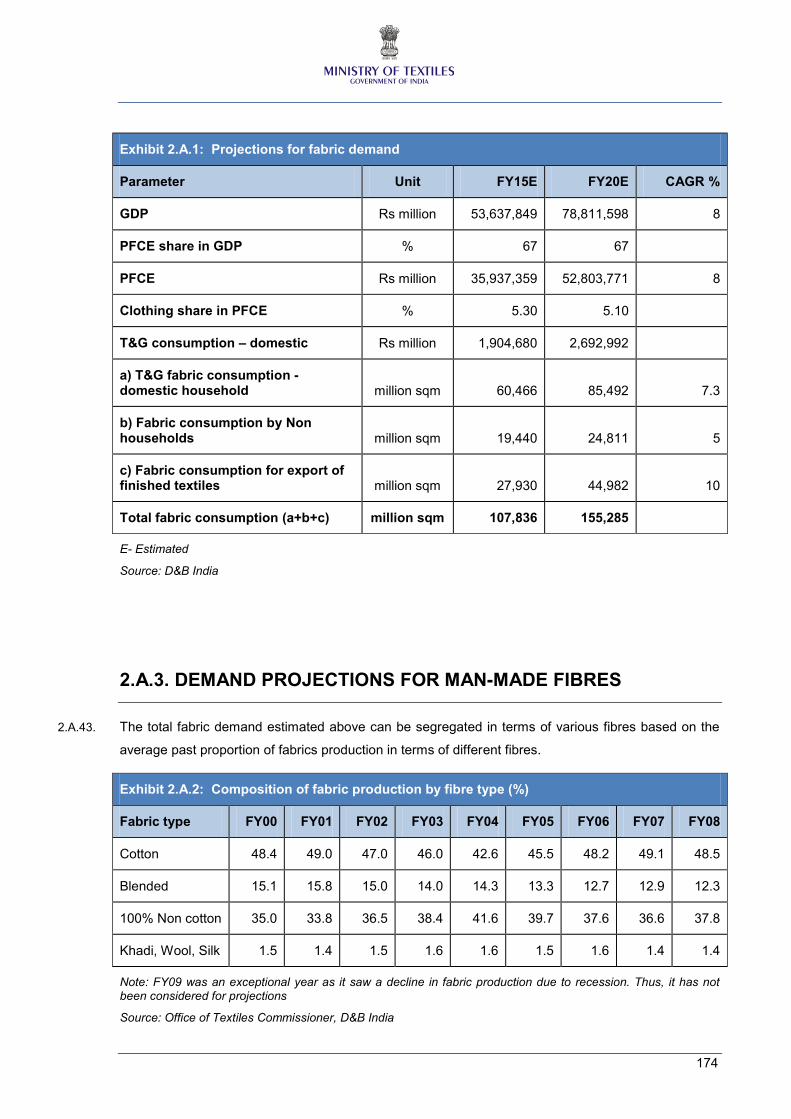

DEMAND PROJECTIONS ............................................................................................................. 172

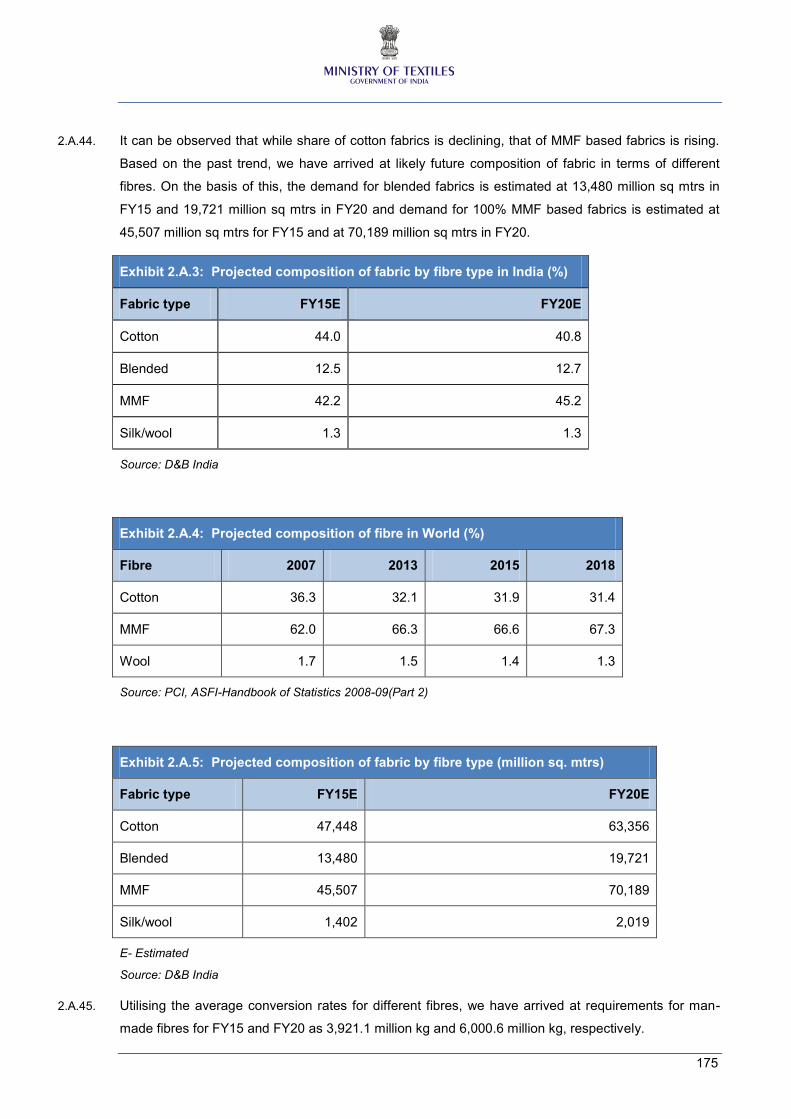

DEMAND PROJECTIONS FOR MAN-MADE FIBRES ................................................................. 174

FUTURE DEMAND PROJECTIONS VIS-À-VIS EXISTING CAPACITIES ................................... 177

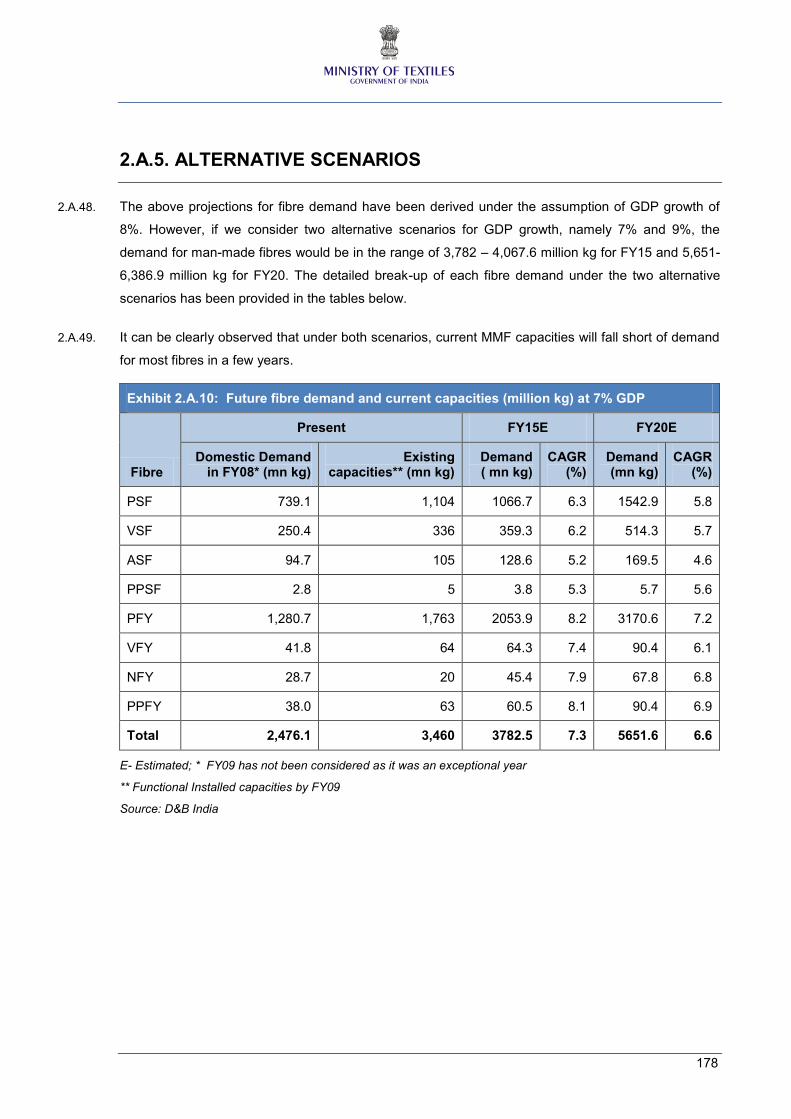

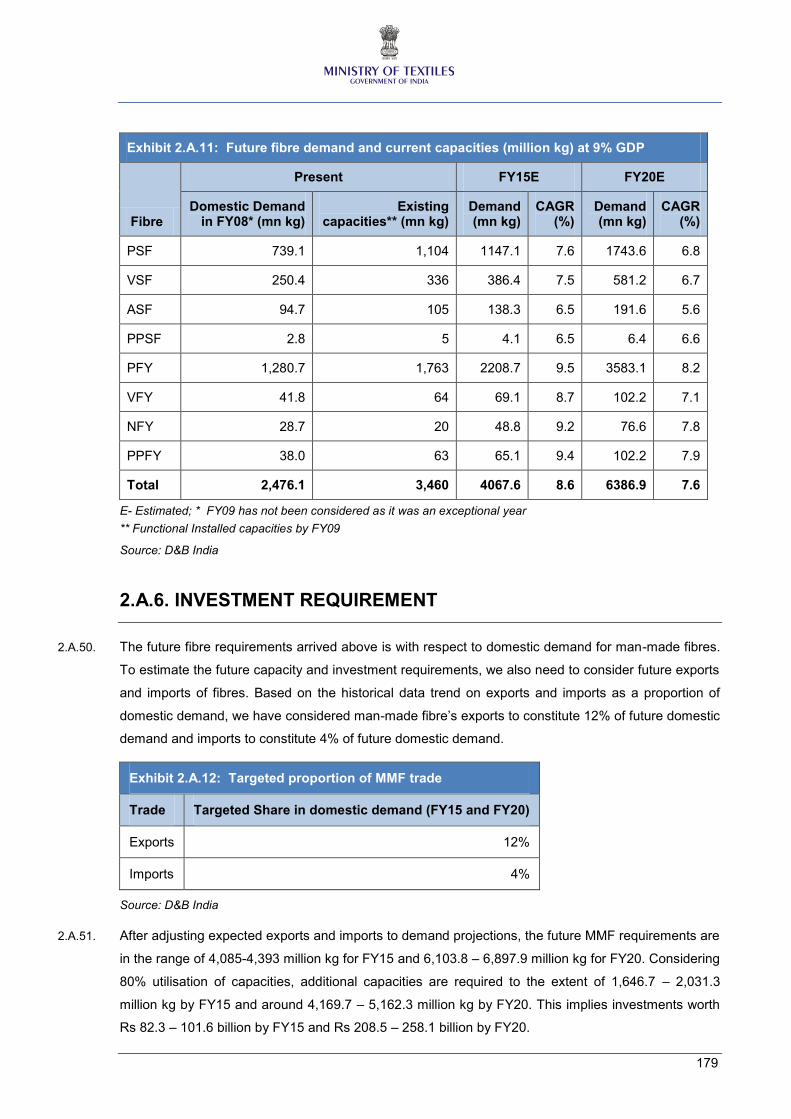

ALTERNATIVE SCENARIOS ........................................................................................................ 178

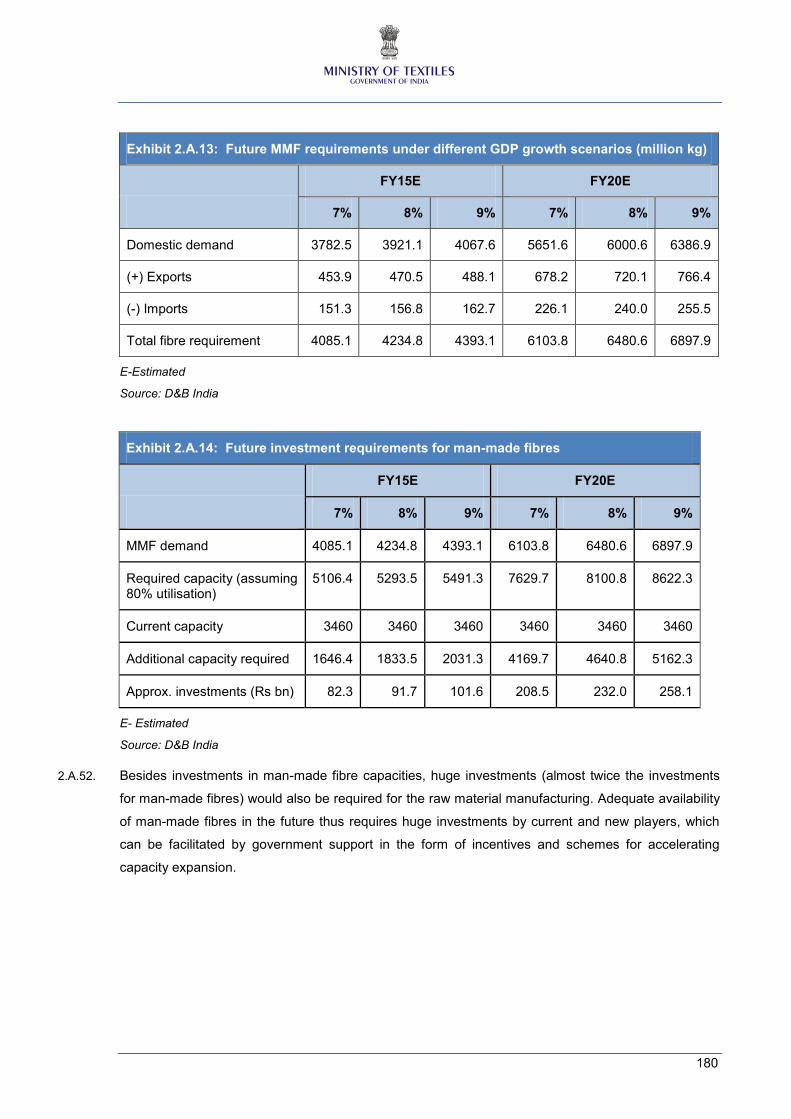

INVESTMENT REQUIREMENT .................................................................................................... 179

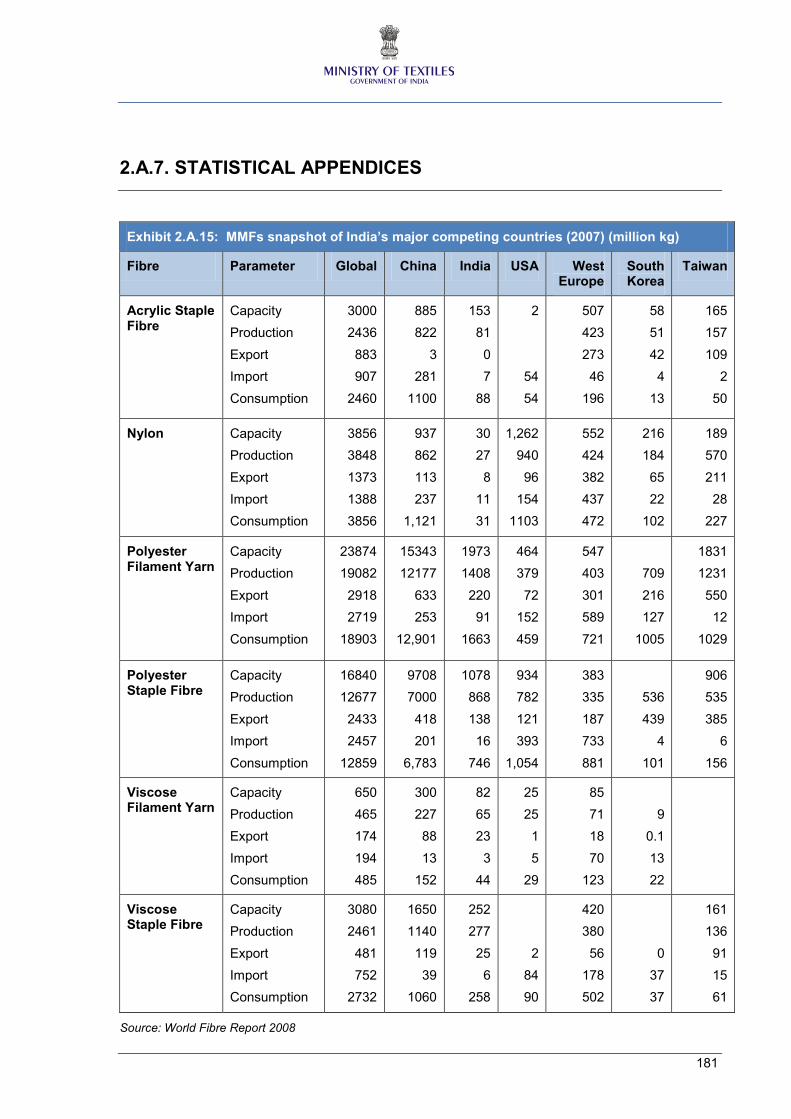

STATISTICAL APPENDICES ........................................................................................................ 181

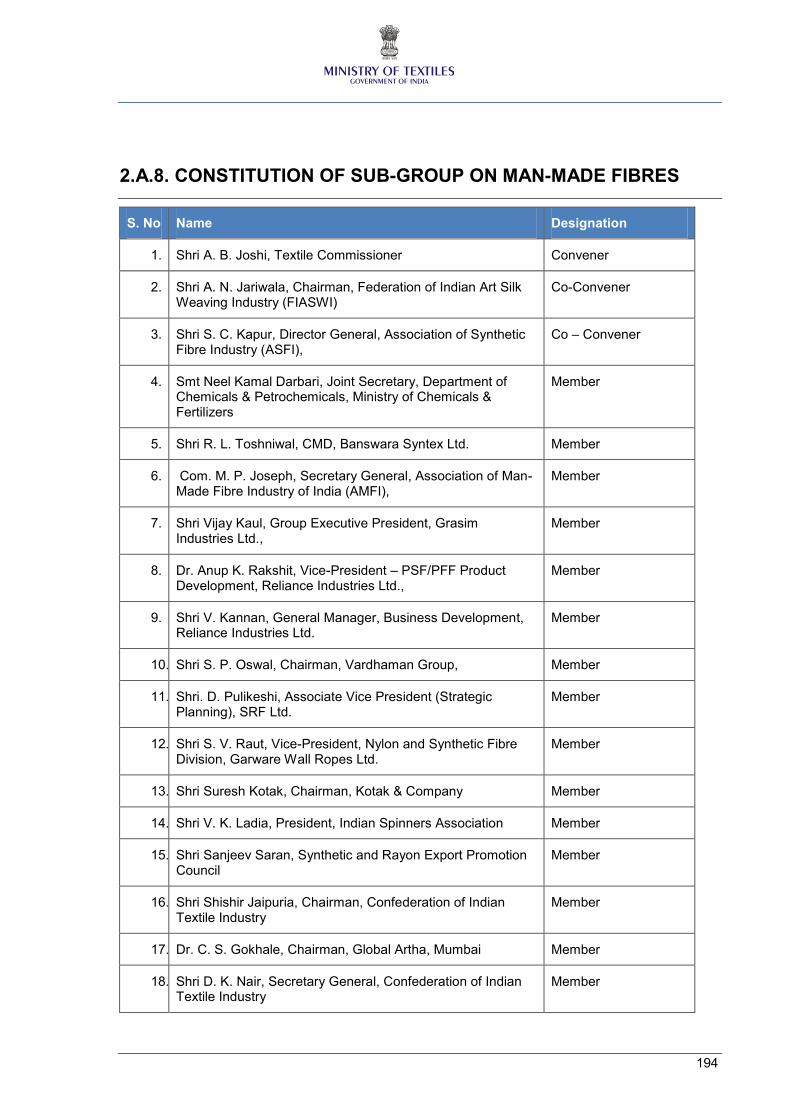

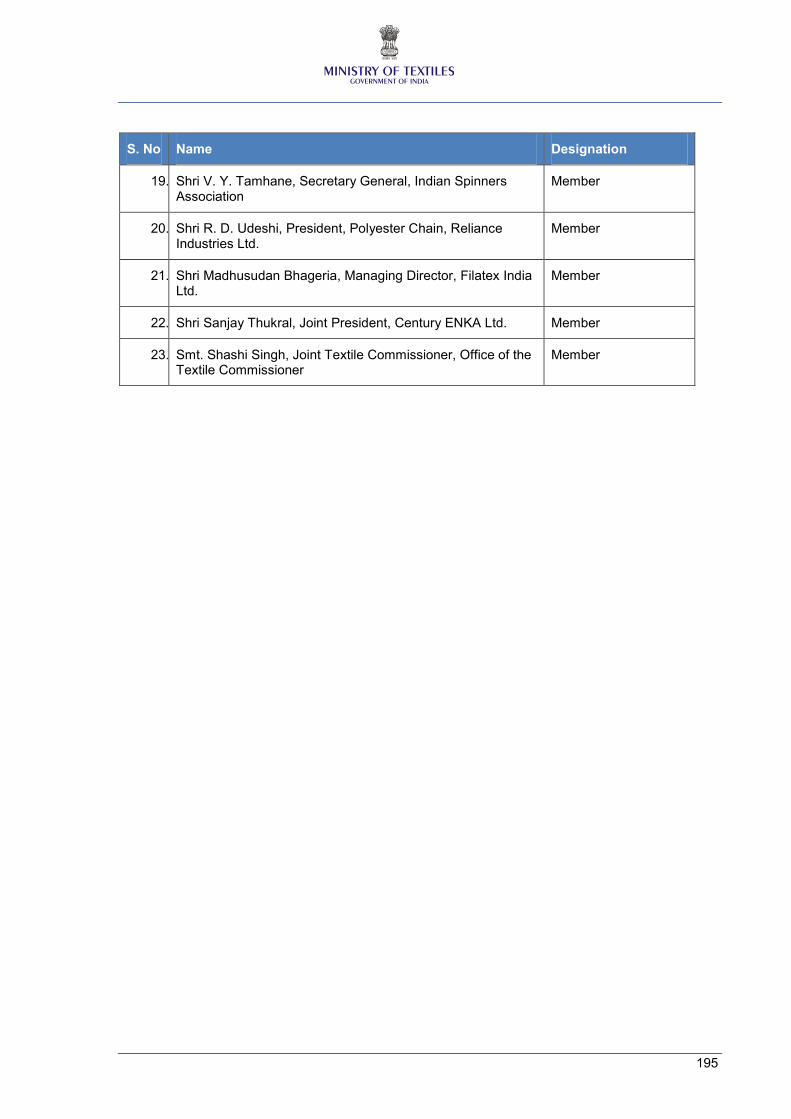

CONSTITUTION OF SUB-GROUP ON MAN-MADE FIBRES ...................................................... 194

112

SUMMARY – MAN MADE FIBRES

I. Ministry of Textiles, Government of India constituted a working group to formulate a Comprehensive

Fibre Policy for Textiles and Garments sector of India with a view to render Indian textiles and

garments sector competitive in the global market in the near, medium as well as long-term. One of the

sub-groups formulated under the working group was on synthetic fibres. The scope of the sub-group

was extended to “man-made fibres” as synthetic fibres would exclude cellulosic fibres like viscose.

Further, “Man-made fibre” was understood to include “filament yarn” along with staple fibres.

Speciality fibres for technical textiles have been excluded from consideration as a separate sub-group

is looking into the same.

II. The key objectives of the study done for the sub-group on Man-made fibres were:

i. To assess the reasons for consumption pattern of man-made fibres (MMF) in India being

different than the world trend

ii. To study the reasons for low consumption of MMF in domestic and export market

iii. To assess the demand-supply and projections for MMF for year 2015 and 2020

iv. Formulating policy interventions and recommendations

INTRODUCTION

III. India is the second largest producer of man-made fibres in the world (World Fibre Report 2008) with

presence of large plants having state-of-the art technology. MMF textiles constitute almost two-third of

the domestic textile market. However, India’s share in global exports of value-added textiles of man-

made fibres is miniscule at around 2.25% in 2008 (India’s MMF exports were US$ 3.3 billion as

against global exports of US$ 146.7 billion). Further, while textiles made of man-made fibres

constitute around 63% of the world trade, it is mere 16.4% (FY09) in case of India as Indian textiles

exports are predominantly cotton based.

IV. The domestic fibre consumption ratio in India at present is 41:59 (FY09) between man-made fibres

and cotton, while it is almost 60:40 globally. The global fibre consumption trend in future is likely to

further tilt in favour of man-made fibres as there is a limitation to growth of cotton on account of limited

availability of land for cotton cultivation. Moreover, the land available for cotton is gradually declining

on account of rise in cultivation of food crops. Given the future demand is expected to be largely in

favour of man-made fibre based textiles, special attention is required to boost the consumption and

production of man-made fibres in India.

113

V. Further, Indian textile industry is an export intensive industry, with almost one-third of domestic

production being exported. Thus, in order to maintain high growth of exports in future, India’s textiles

exports portfolio needs to have a balanced fibre mix in line with the global consumption pattern.

PRESENT SCENARIO

VI. India’s capacities for man-made fibres currently stand at 3.4 billion kg, which is around 6.6% of global

MMF capacities. India’s total production of man-made fibres stood at 2.5 billion kg in FY09, of which

exports constituted 10.3% at 0.25 billion kg. Domestic consumption for man-made fibres during FY09

stood at 2.4 billion kg, of which imports constituted roughly 5% at 0.12 billion kg. Indian man-made

fibre industry is largely polyester dominated, which constitutes over 83% of total man-made fibre

production. Further, production of man-made fibres in India is characterised by limited number of

players having a dominant share in the production of most of the man-made fibres and filament yarns.

VII. Although Indian players manufacture most of the man-made fibres (PSF, VSF, ASF, PPSF, PFY,

VFY, NFY, PPFY), the specialised man-made fibres like acetate fibre/ filament yarn, tri-acetate fibre/

filament yarn, cuprammonium filament yarn, nylon 66, nylon 11, spandex, PVA fibre and filament yarn,

PBT yarn, modacrylic staple fibres and PTET are not being manufactured in India.

VIII. While man-made fibre production is highly concentrated, with limited players engaged in

manufacturing of MMF, the value added MMF textiles are primarily being manufactured in the

decentralised sector, with presence of large number of small and medium enterprises. Production of

MMF fabrics has grown from 21 billion square meters in FY05 to 23.9 billion square meters in FY09.

While in the domestic market, MMF textiles and garments are dominant, cotton textiles are

predominant in the export markets; MMF garments are predominant to the extent of 65% (estimated)

in the domestic market, while in the export market cotton garments are predominant with over 80%

share.

FUTURE PROJECTIONS

IX. A top down approach has been followed to determine the future demand for man-made fibres in FY15

and FY20. Considering future GDP growth of 8%, the domestic demand for man-made fibres/ filament

yarns is estimated at 3.9 billion kg in FY15 and about 6 billion kg in FY20. Adjusting to this the likely

exports and imports of MMF, the overall MMF requirement is estimated at 4.2 billion kg for FY15 and

6.48 billion kg for FY20. This implies capacity additions of about 1.8 billion kg (FY15) and 4.6 billion kg

(FY20), which would require an investment of over Rs 90 billion (approximately US$ 2 billion) by FY15

and Rs 230 billion (approximately US$ 5.1 billion) by FY20.

114

ISSUES AND CONCERNS

A. Exclusively affecting MMF and MMF textiles

X. Excise duty discrimination: A major concern area has been the historical discrimination of man-

made fibres and textiles against cotton and cotton textiles in the form of higher excise duties. Although

there has been substantial reduction in excise duties on man-made fibres and textiles during the last

10 years, the current duties on MMF and MMF textiles are still high; while cotton is exempt from

excise duty, MMF attracts excise duty of 8%. Further, while MMF textiles attract a mandatory

CENVAT of 8%, cotton textiles have an optional CENVAT of 4%. Any reduction in excise duties on

MMF and MMF textiles will have a highly positive impact on the growth of MMF consumption.

XI. Lack of global competitiveness: Indian man-made fibres textile industry has not been able to create

a mark in the global textiles market post dismantling of textile quotas even though cotton textiles

industry has witnessed a substantial growth. Since dismantling of quotas (2005 onwards), Indian

cotton apparel exports to the world have grown at about 10.7% CAGR, while MMF apparel exports

have witnessed a decline.

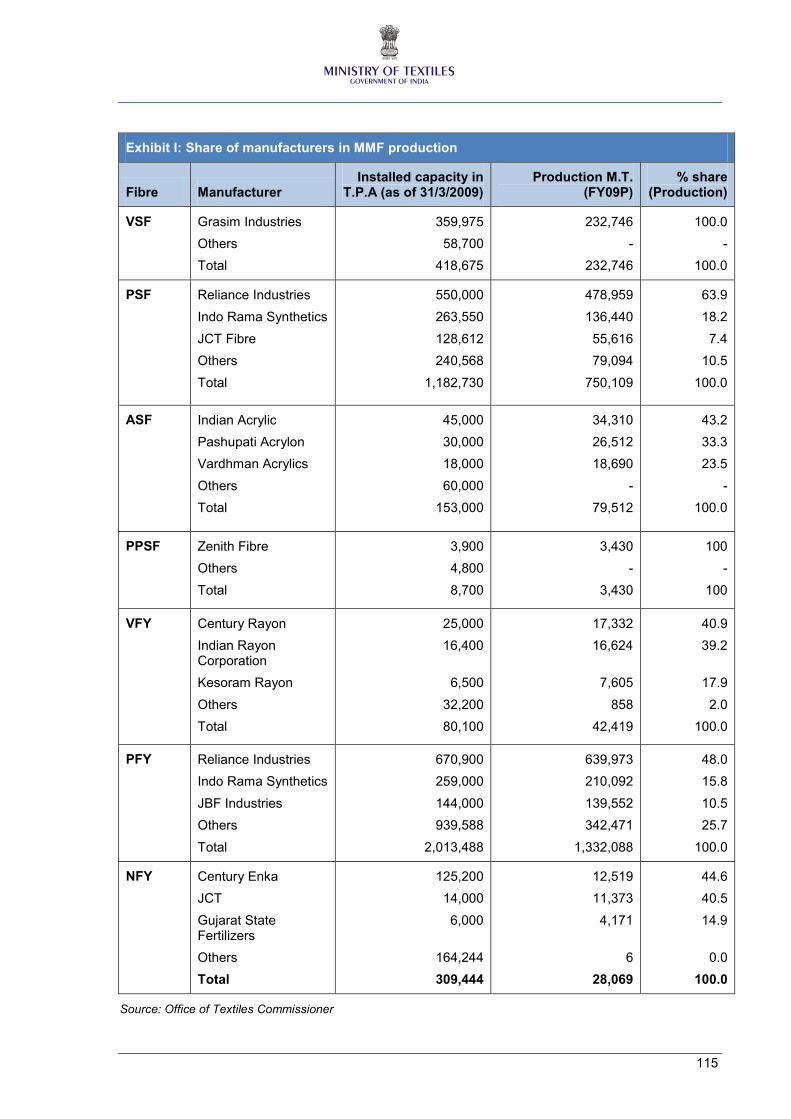

XII. Limited number of players: There are only a few big players manufacturing man-made fibres in

India. The industry follows a pricing policy on import parity basis at landed cost. User industry has

submitted that MMF producers export man-made fibres at lower prices than in the domestic market.

This submission is supported by SRTEPC exports data analysed by FIASWI in respect of polyester

fibre and yarn.

115

Exhibit I: Share of manufacturers in MMF production

Fibre Manufacturer Installed capacity in

T.P.A (as of 31/3/2009) Production M.T.

(FY09P) % share

(Production)

VSF

Grasim Industries

Others

Total

359,975

58,700

418,675

232,746

-

232,746

100.0

-

100.0

PSF

Reliance Industries

Indo Rama Synthetics

JCT Fibre

Others

Total

550,000

263,550

128,612

240,568

1,182,730

478,959

136,440

55,616

79,094

750,109

63.9

18.2

7.4

10.5

100.0

ASF

Indian Acrylic

Pashupati Acrylon

Vardhman Acrylics

Others

Total

45,000

30,000

18,000

60,000

153,000

34,310

26,512

18,690

-

79,512

43.2

33.3

23.5

-

100.0

PPSF

Zenith Fibre

Others

Total

3,900

4,800

8,700

3,430

-

3,430

100

-

100

VFY

Century Rayon

Indian Rayon Corporation

Kesoram Rayon

Others

Total

25,000

16,400

6,500

32,200

80,100

17,332

16,624

7,605

858

42,419

40.9

39.2

17.9

2.0

100.0

PFY

Reliance Industries

Indo Rama Synthetics

JBF Industries

Others

Total

670,900

259,000

144,000

939,588

2,013,488

639,973

210,092

139,552

342,471

1,332,088

48.0

15.8

10.5

25.7

100.0

NFY

Century Enka

JCT

Gujarat State Fertilizers

Others

Total

125,200

14,000

6,000

164,244

309,444

12,519

11,373

4,171

6

28,069

44.6

40.5

14.9

0.0

100.0

Source: Office of Textiles Commissioner

116

XIII. Levy of anti-dumping duties: Indian MMF textile manufacturers are also faced with higher fibre

prices as against their global counterparts on account of levy of anti-dumping duties on imports of

majority of man-made fibres. This in turn affects the availability of fibres to MMF textile manufacturers

at competitive prices.

XIV. Lack of indigenous production of specialized MMF: Various specialised man-made fibres (like

acetate/ tri-acetate, cuprammonium filament yarn, nylon 66, nylon 11, spandex, etc) are not being

manufactured in India despite having huge potential and thus have to be imported by the weavers.

XV. High customs duty: Another factor that has contributed to higher costs of man-made fibre

manufacturers and thus for man-made fibre textile manufacturers is the high customs duty on certain

raw materials required for man-made fibre industry. Certain raw materials and additives used in the

production of man-made fibres are necessarily imported on account of limited domestic production/

lack of requisite quality. Some of these raw materials and additives like rayon grade wood pulp (used

for manufacture of viscose fibre), titanium di-oxide and spin finish oil (used as additives for

manufacturing polyester) attract high customs duty, while the same are either exempted or have lower

customs duty in major competing countries. To enable a level-playing field with the global

counterparts in the international export markets and to reduce the key input costs of man-made fibre

manufacturers, it is desired that customs duty on such inputs are exempted. Since these items are

largely imported due to shortage in domestic market, reduction in import duties on same is not likely to

hurt the domestic manufacturers of these items.

XVI. High debt servicing cost: Another reason for relatively higher costs of man-made fibre/ filament yarn

manufacturers vis-à-vis the cotton textile manufacturers and global counterparts is the high debt

servicing costs of the former. The lending rates in India are in the range of 11% - 13.5% (IBA Website)

and are significantly higher in comparison to competing countries like China (5.04 – 6.12% ; Source :

Bank of Communication, China) and South Korea (5.72 – 6.33%), which contributes to much higher

interest costs for Indian MMF manufacturers vis-à-vis counterparts in competing countries. Further,

concessional schemes like TUFS is not applicable for manufacturing synthetic fibres, which puts this

capital intensive MMF industry at a great disadvantage vis-à-vis the cotton textile industry.

XVII. GST issues for textile industry: Major tax reforms are expected in the form of Goods and Services

Tax (GST), which is likely to be introduced next year. However, textile industry has a major concern

with respect to GST. The textiles industry involves a lot of inter-state transfers especially at the fabric

stage. Due to long supply chain in the textile industry involving traders in various cities, towns, etc, the

inter state transactions are likely to take place among the organised players who are above the

threshold limit for GST exemption and small decentralised traders who are exempted from payment of

GST. Consequently, the regular payee (one above threshold limit) would not get any credit for

purchases from small decentralised trader but shall have to pay full duty on the sale price. Thus, the

117

tax will multiply and the purpose of VAT principle would be broken. This would have serious cost

implications to the Indian textile industry, which is predominantly in the decentralised sector.

B. Industry neutral issues

XVIII. There are various other factors contributing to higher costs of Indian MMF and MMF textile

manufacturers vis-à-vis global counterparts, including high power costs and high transaction costs.

Indian industries (including textile industry) face a major disadvantage against countries like China

and countries in South East Asia in terms of power costs and availability. Moreover, Indian exporters

are faced with huge transaction cost burden in comparison with exporters in competing countries. For

instance, transaction costs for exports in India stands at US$ 945 per container as compared to US$

500 per container for China. The un-neutralised state taxes such as CST, VAT, Octroi, etc contribute

to higher transaction costs for Indian exporters. To mitigate the cost burden of Indian textile players, a

long term solution is required with respect to strengthening of physical infrastructure and introduction

of tax reforms.

RECOMMENDATIONS

XIX. To meet the objectives of attaining high growth and increasing the competitiveness of Indian textile

industry (including MMF textiles), the national fibre policy needs to lay a special emphasis on

improving the competitiveness of Indian man-made fibres and textiles industry as it can drive the

growth of the Indian textile industry in the future, both in domestic as well as export markets. This

requires addressing of issues and constraints faced by the industry at present and make suitable

provisions to avoid any foreseeable hurdles in the future.

XX. The key recommendations arrived from this study for incorporation in the National Fibre Policy are:

1. Have a fibre neutral excise policy; i.e. all textiles and fibres should attract the same excise

duty i.e. 4% optional

2. Excise duty and customs duty exemption for specialised MMF which are not produced

indigenously. Such specialised fibres are listed below:

a. Acetate fibre (HS code – 55049010)

b. Acetate filament yarn (HS code – 540342)

c. Tri-acetate fibre (HS code proposed - 55049011)

d. Tri-acetate filament yarn (HS code proposed - 54033310)

e. Cuprammonium filament yarn (HS code – 54033910)

f. Cuprammonium fibre (HS code proposed – 55049040)

g. Nylon 66 (HS code proposed – 55031110, 54025110)

h. Nylon 11 (HS code proposed – 55031120, 54025120)

118

i. Spandex fibre (HS code proposed- 55039030)

j. Spandex filament yarn (HS code – 54024400)

k. PVA fiber (HS code proposed – 55039030)

l. PVA filament yarn (HS code proposed - 54026960)

m. PBT yarn (HS code proposed– 54026970, 55039040)

n. Modacrylic staple fibres (HS code proposed - 55033010)

o. Modacrylic filament yarn (HS code proposed – 54026940)

p. PTET (HS code proposed – 54026980, 55039050)

3. Removal of 4% Special Additional Duty (SAD) on imports of man-made fibres to make the

same available to domestic consumers at competitive prices.

4. Customs duty exemption on certain raw materials and additives that are primarily imported

a. Customs duty on rayon grade wood pulp (HS Code 47020000) to be exempted (from

current 5%)

b. Customs duty on titanium di-oxide (Anatase grade) with HS code 283230030 to be

reduced to nil from current 11%.

c. Customs duty on Spin finish oil to be reduced to nil from current 8%. Specific HS

codes for Spin finish oil have already been proposed by the industry (HS code

34031200) and endorsed by the Department of Chemicals and Petrochemicals for

this purpose.

5. Export oriented incentives should be provided to manufacturers of MMF textiles and garments

for a limited period to neutralize the impact of cost-disadvantage vis-à-vis exporters in

competing countries. This could include higher drawback rates and inclusion of processed

fabrics, madeups and garments made of man-made fibres under the Focus Product Scheme.

(Currently, MMF garments and certain types of woven fabrics of MMF falling under HS Code

5512, 5513, 5514, 5515 and 5516 are covered under Market Linked Focus Product Scheme

for limited number of countries.). The proposed scheme is as follows:

a. A graduation scheme for three years can be introduced under the Focus product

scheme with benefits of 10% in first year, 7% in second year and 3% in third year.

b. This scheme may cover man-made textiles and garments. In case financial

implications do not permit coverage of textiles and garments then at least garments

sector should be incentivised as exports of these are currently very low in value

terms.

6. Textile industry should be kept out of GST for at least two years

7. Synthetic fibres should be covered under TUFS with fund support from their administrative

Ministry i.e. Department of Chemicals and Petrochemicals.

119

a. The machinery for manufacture of synthetic fibres post polymerisation may be

covered under TUFS. Since the processes upto polymerisation are primarily chemical

in nature polymerisation machineries may not be covered.

b. The post polymerisation machinery may be benchmarked by TAMC in consultation

with proposed advisory council on MMF.

c. To encourage setting up of small size units, particularly from chips the restriction on

term loan and also on capital cost may be fixed by IMSC in consultation with TAMC

and proposed advisory council.

8. Introduction of anti-dumping proceedings on man-made fibres should involve consultation

with the Ministry of Textiles

9. Introduction of an institutional mechanism wherein government support (financial and

otherwise) is made available to industry associations/ players to initiate and defend anti-

dumping proceedings, where necessary

10. A MMF advisory council with all the stakeholders may be set up to monitor that the excise

duty and other concessions have been passed on by the MMF manufacturers and also to

take on integrated approach to solving the problems of MMF producers and users of MMF

and to accelerate their growth

11. MMF manufacturing and processing units should be given a priority under the gas allocation

policy, at par with the power sector.

XXI. If the above recommendations are implemented, it would result in high growth of man-made fibres

and textiles industry, thereby contributing to higher revenues, increase in employment generation, and

higher foreign exchange earnings. Financial implications of these recommendations would be

balanced by the intangible benefits and cascading effect in the economy.

120

2.1. INDIAN SCENARIO

IMPORTANT MMF PLAYER IN THE WORLD

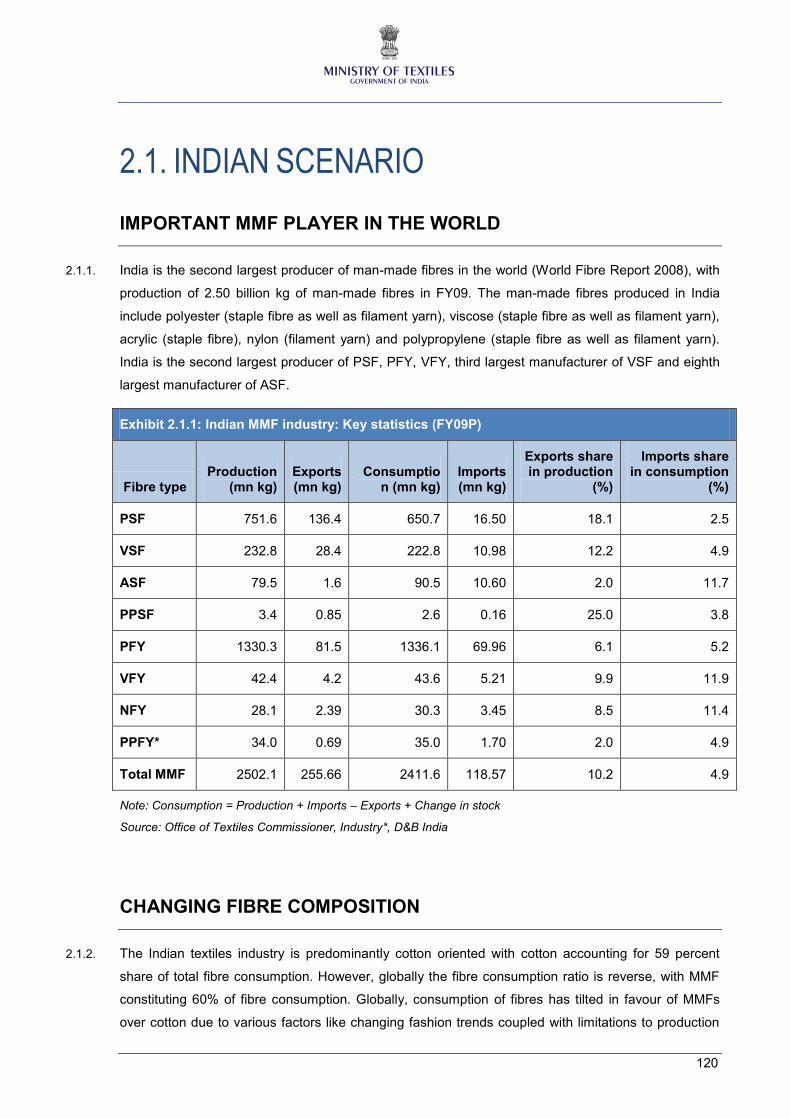

2.1.1. India is the second largest producer of man-made fibres in the world (World Fibre Report 2008), with

production of 2.50 billion kg of man-made fibres in FY09. The man-made fibres produced in India

include polyester (staple fibre as well as filament yarn), viscose (staple fibre as well as filament yarn),

acrylic (staple fibre), nylon (filament yarn) and polypropylene (staple fibre as well as filament yarn).

India is the second largest producer of PSF, PFY, VFY, third largest manufacturer of VSF and eighth

largest manufacturer of ASF.

Exhibit 2.1.1: Indian MMF industry: Key statistics (FY09P)

Fibre type Production

(mn kg) Exports (mn kg)

Consumption (mn kg)

Imports (mn kg)

Exports share in production

(%)

Imports share in consumption

(%)

PSF 751.6 136.4 650.7 16.50 18.1 2.5

VSF 232.8 28.4 222.8 10.98 12.2 4.9

ASF 79.5 1.6 90.5 10.60 2.0 11.7

PPSF 3.4 0.85 2.6 0.16 25.0 3.8

PFY 1330.3 81.5 1336.1 69.96 6.1 5.2

VFY 42.4 4.2 43.6 5.21 9.9 11.9

NFY 28.1 2.39 30.3 3.45 8.5 11.4

PPFY* 34.0 0.69 35.0 1.70 2.0 4.9

Total MMF 2502.1 255.66 2411.6 118.57 10.2 4.9

Note: Consumption = Production + Imports – Exports + Change in stock

Source: Office of Textiles Commissioner, Industry*, D&B India

CHANGING FIBRE COMPOSITION

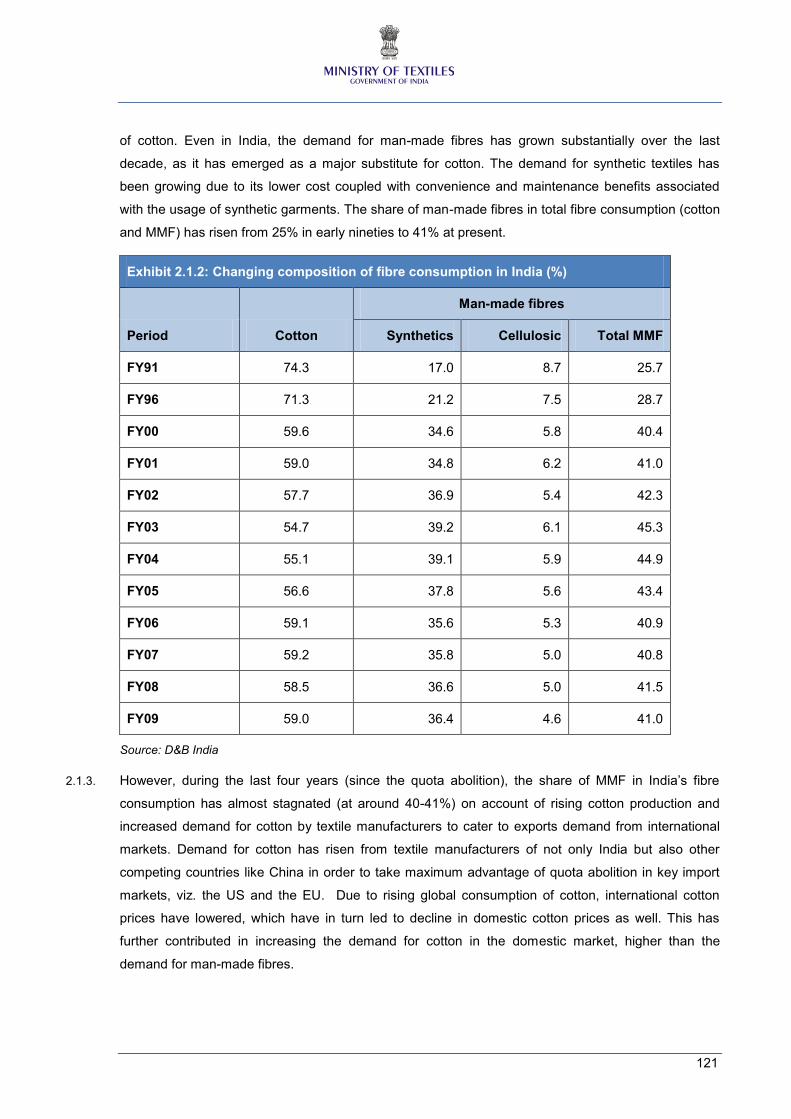

2.1.2. The Indian textiles industry is predominantly cotton oriented with cotton accounting for 59 percent

share of total fibre consumption. However, globally the fibre consumption ratio is reverse, with MMF

constituting 60% of fibre consumption. Globally, consumption of fibres has tilted in favour of MMFs

over cotton due to various factors like changing fashion trends coupled with limitations to production

121

of cotton. Even in India, the demand for man-made fibres has grown substantially over the last

decade, as it has emerged as a major substitute for cotton. The demand for synthetic textiles has

been growing due to its lower cost coupled with convenience and maintenance benefits associated

with the usage of synthetic garments. The share of man-made fibres in total fibre consumption (cotton

and MMF) has risen from 25% in early nineties to 41% at present.

Exhibit 2.1.2: Changing composition of fibre consumption in India (%)

Period Cotton

Man-made fibres

Synthetics Cellulosic Total MMF

FY91 74.3 17.0 8.7 25.7

FY96 71.3 21.2 7.5 28.7

FY00 59.6 34.6 5.8 40.4

FY01 59.0 34.8 6.2 41.0

FY02 57.7 36.9 5.4 42.3

FY03 54.7 39.2 6.1 45.3

FY04 55.1 39.1 5.9 44.9

FY05 56.6 37.8 5.6 43.4

FY06 59.1 35.6 5.3 40.9

FY07 59.2 35.8 5.0 40.8

FY08 58.5 36.6 5.0 41.5

FY09 59.0 36.4 4.6 41.0

Source: D&B India

2.1.3. However, during the last four years (since the quota abolition), the share of MMF in India’s fibre

consumption has almost stagnated (at around 40-41%) on account of rising cotton production and

increased demand for cotton by textile manufacturers to cater to exports demand from international

markets. Demand for cotton has risen from textile manufacturers of not only India but also other

competing countries like China in order to take maximum advantage of quota abolition in key import

markets, viz. the US and the EU. Due to rising global consumption of cotton, international cotton

prices have lowered, which have in turn led to decline in domestic cotton prices as well. This has

further contributed in increasing the demand for cotton in the domestic market, higher than the

demand for man-made fibres.

122

POLYESTER ACCOUNTS FOR LARGEST SHARE IN MMF

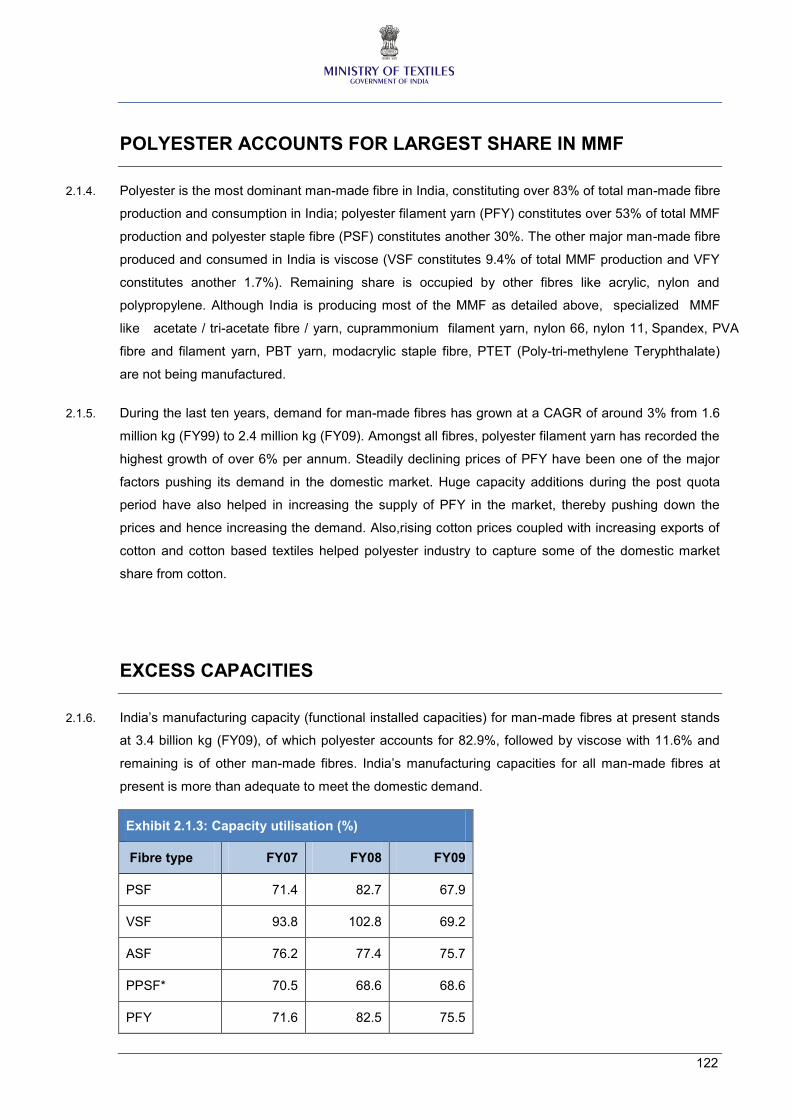

2.1.4. Polyester is the most dominant man-made fibre in India, constituting over 83% of total man-made fibre

production and consumption in India; polyester filament yarn (PFY) constitutes over 53% of total MMF

production and polyester staple fibre (PSF) constitutes another 30%. The other major man-made fibre

produced and consumed in India is viscose (VSF constitutes 9.4% of total MMF production and VFY

constitutes another 1.7%). Remaining share is occupied by other fibres like acrylic, nylon and

polypropylene. Although India is producing most of the MMF as detailed above, specialized MMF

like acetate / tri-acetate fibre / yarn, cuprammonium filament yarn, nylon 66, nylon 11, Spandex, PVA

fibre and filament yarn, PBT yarn, modacrylic staple fibre, PTET (Poly-tri-methylene Teryphthalate)

are not being manufactured.

2.1.5. During the last ten years, demand for man-made fibres has grown at a CAGR of around 3% from 1.6

million kg (FY99) to 2.4 million kg (FY09). Amongst all fibres, polyester filament yarn has recorded the

highest growth of over 6% per annum. Steadily declining prices of PFY have been one of the major

factors pushing its demand in the domestic market. Huge capacity additions during the post quota

period have also helped in increasing the supply of PFY in the market, thereby pushing down the

prices and hence increasing the demand. Also,rising cotton prices coupled with increasing exports of

cotton and cotton based textiles helped polyester industry to capture some of the domestic market

share from cotton.

EXCESS CAPACITIES

2.1.6. India’s manufacturing capacity (functional installed capacities) for man-made fibres at present stands

at 3.4 billion kg (FY09), of which polyester accounts for 82.9%, followed by viscose with 11.6% and

remaining is of other man-made fibres. India’s manufacturing capacities for all man-made fibres at

present is more than adequate to meet the domestic demand.

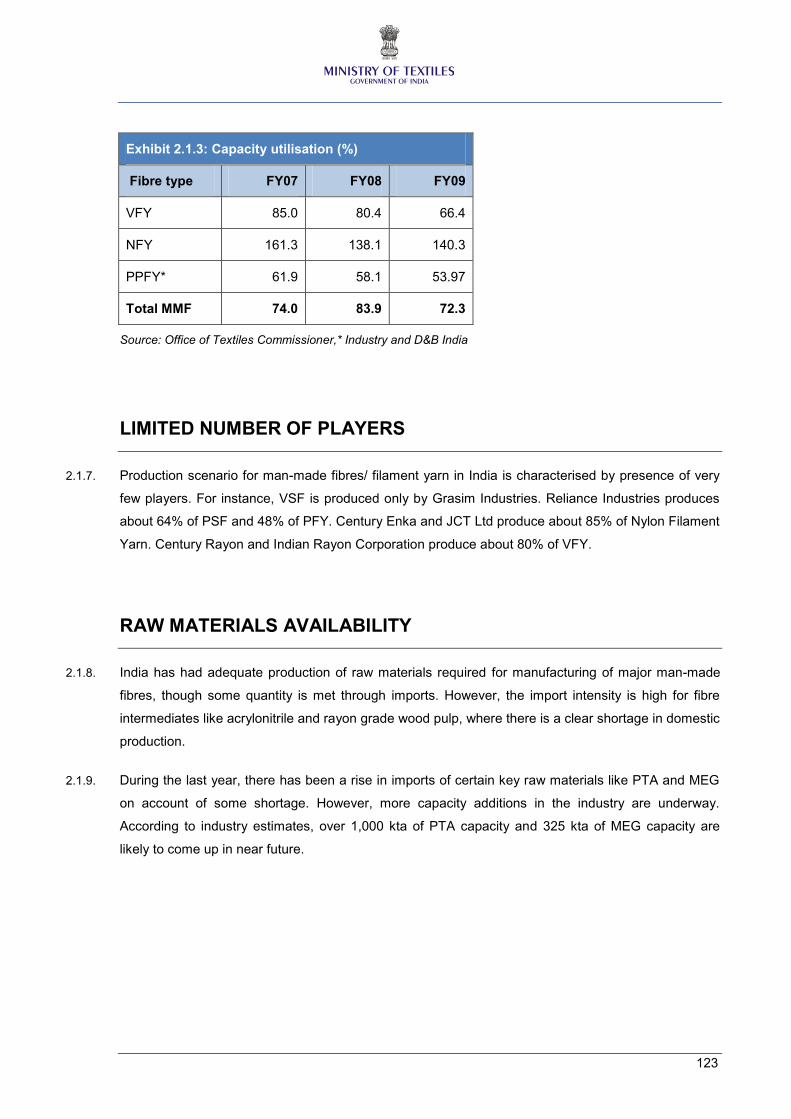

Exhibit 2.1.3: Capacity utilisation (%)

Fibre type FY07 FY08 FY09

PSF 71.4 82.7 67.9

VSF 93.8 102.8 69.2

ASF 76.2 77.4 75.7

PPSF* 70.5 68.6 68.6

PFY 71.6 82.5 75.5

123

Exhibit 2.1.3: Capacity utilisation (%)

Fibre type FY07 FY08 FY09

VFY 85.0 80.4 66.4

NFY 161.3 138.1 140.3

PPFY* 61.9 58.1 53.97

Total MMF 74.0 83.9 72.3

Source: Office of Textiles Commissioner,* Industry and D&B India

LIMITED NUMBER OF PLAYERS

2.1.7. Production scenario for man-made fibres/ filament yarn in India is characterised by presence of very

few players. For instance, VSF is produced only by Grasim Industries. Reliance Industries produces

about 64% of PSF and 48% of PFY. Century Enka and JCT Ltd produce about 85% of Nylon Filament

Yarn. Century Rayon and Indian Rayon Corporation produce about 80% of VFY.

RAW MATERIALS AVAILABILITY

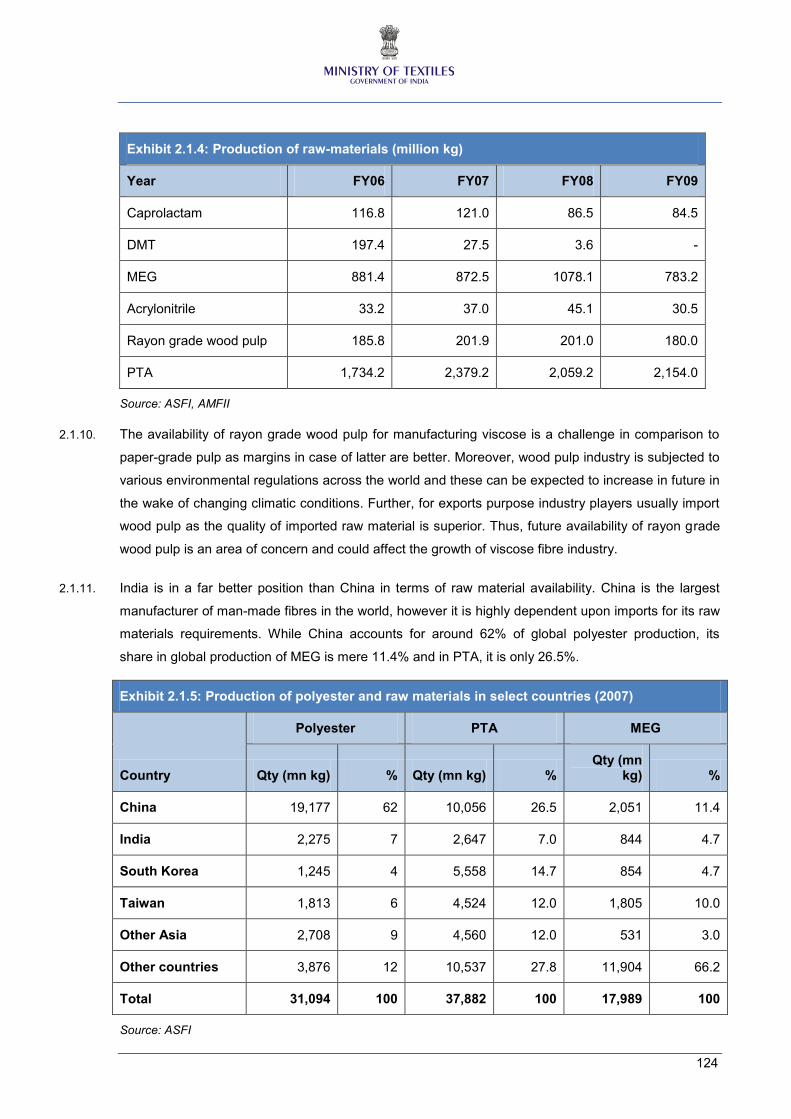

2.1.8. India has had adequate production of raw materials required for manufacturing of major man-made

fibres, though some quantity is met through imports. However, the import intensity is high for fibre

intermediates like acrylonitrile and rayon grade wood pulp, where there is a clear shortage in domestic

production.

2.1.9. During the last year, there has been a rise in imports of certain key raw materials like PTA and MEG

on account of some shortage. However, more capacity additions in the industry are underway.

According to industry estimates, over 1,000 kta of PTA capacity and 325 kta of MEG capacity are

likely to come up in near future.

124

Exhibit 2.1.4: Production of raw-materials (million kg)

Year FY06 FY07 FY08 FY09

Caprolactam 116.8 121.0 86.5 84.5

DMT 197.4 27.5 3.6 -

MEG 881.4 872.5 1078.1 783.2

Acrylonitrile 33.2 37.0 45.1 30.5

Rayon grade wood pulp 185.8 201.9 201.0 180.0

PTA 1,734.2 2,379.2 2,059.2 2,154.0

Source: ASFI, AMFII

2.1.10. The availability of rayon grade wood pulp for manufacturing viscose is a challenge in comparison to

paper-grade pulp as margins in case of latter are better. Moreover, wood pulp industry is subjected to

various environmental regulations across the world and these can be expected to increase in future in

the wake of changing climatic conditions. Further, for exports purpose industry players usually import

wood pulp as the quality of imported raw material is superior. Thus, future availability of rayon grade

wood pulp is an area of concern and could affect the growth of viscose fibre industry.

2.1.11. India is in a far better position than China in terms of raw material availability. China is the largest

manufacturer of man-made fibres in the world, however it is highly dependent upon imports for its raw

materials requirements. While China accounts for around 62% of global polyester production, its

share in global production of MEG is mere 11.4% and in PTA, it is only 26.5%.

Exhibit 2.1.5: Production of polyester and raw materials in select countries (2007)

Country

Polyester PTA MEG

Qty (mn kg) % Qty (mn kg) % Qty (mn

kg) %

China 19,177 62 10,056 26.5 2,051 11.4

India 2,275 7 2,647 7.0 844 4.7

South Korea 1,245 4 5,558 14.7 854 4.7

Taiwan 1,813 6 4,524 12.0 1,805 10.0

Other Asia 2,708 9 4,560 12.0 531 3.0

Other countries 3,876 12 10,537 27.8 11,904 66.2

Total 31,094 100 37,882 100 17,989 100

Source: ASFI

125

PRICE MOVEMENT OF MMF

2.1.12. Over the last decade, prices of key man-made fibres like PSF and PFY have seen a steady decline,

which has contributed to higher demand for same. One of the reasons for reduction in prices is the

capacity build-up leading to economies of scale for key MMF manufacturers and gradual reduction of

excise duty.

Exhibit 2.1.6: Price movement of fibres in India

Source: 2007-2008 Handbook of Statistics on MMF – ASFI

EXPORTS OF MAN-MADE FIBRES RISE SUBSTANTIALLY IN POST

QUOTA PERIOD BUT SLOW DOWN IN FY09

2.1.13. Rising capacities and production of man-made fibres since the dismantling of textile quotas have

helped in increasing the surplus for exports. Exports of all man-made fibres/ filament yarns (except

ASF, NFY and PPFY) witnessed a tremendous growth during the post quota period; exports of PSF

and PFY have recorded CAGR of 85% and 47.9% respectively during FY06-FY08, PPSF has

recorded CAGR of over 58% during the same period and exports of VSF and VFY have recorded

CAGR of 31% and 21.4% respectively during the same period. However, exports of most fibres

tumbled in FY09 due to the global economic slowdown.

2.1.14. On the contrary, India’s exports of value-added MMF products, especially apparel have steadily

declined. This can be attributed to lower price competitiveness of Indian exporters as against their

Asian counterparts in the international markets. Moreover, the competition has stiffened since the

dismantling of quotas, which has put pressure on exporters to lower their prices further. Since Indian

fabric and apparel exporters operate on thin margins, they have not been able to match the prices of

other Asian counterparts and hence have not been able to garner a larger share even in the post

quota regime.

126

Exhibit 2.1.7: India’s exports of MMF and MMF products (US$ million)

Item FY01 FY05 CAGR

(%) FY06 FY07 FY08 FY09 CAGR

(%)

MMF/ filament 265.3 377.9 9.2 405.7 641.4 841.0 686.6 19.2

MMF Spun Yarn 235.8 363.1 11.4 363.3 420.1 567.9 454.4 7.7

MMF Fabrics 496.1 1046.0 20.5 970.6 1013.7 1319.7 1630.0 18.9

MMF garments 744.8 489.0 -10.0 699.6 585.7 628.4 651.4 -2.4

Source: DGCI&S

2.1.15. As can be observed from the table below, the prices in last year have been much lower for Indian

exporters due to increased competition in the wake of global economic crisis. Further, since the

dismantling of quotas average export realisations in the US market have dropped from almost US$

2.9 per sqm in 2001 to just US$ 2.6 sqm in 2008. China has been able to garner almost 43% of USA’s

MMF garment imports on account of extremely low prices; the average price realisation for Chinese

exporters is only US$ 2.4 per sqm as against Indian exporters’ realisation of US$ 3.0 per sqm. India’s

export realisations are higher than the global average and also against other competing Asian

countries like Vietnam, Taiwan and South Korea.

Exhibit 2.1.8: Exports of MMF garments and realisations in USA for select countries

Country

2001 2005 2006 2008

Qty (mn sqm)

Price (US$/ sqm)

Qty (mn sqm)

Price (US$/ sqm)

Qty (mn sqm)

Price (US$/ sqm)

Qty (mn sqm)

Price (US$/ sqm)

World 6,564.3 2.9 8,199.4 2.5 8,165.1 2.6 8,252.9 2.6

India 129.5 3.2 149.6 3.3 119.4 3.5 98.3 3.0

China 453.4 4.8 2,596.6 2.2 2,824.7 2.4 3,536.3 2.4

Vietnam 7.5 1.5 409.0 2.7 433.8 2.8 641.6 2.9

Indonesia 317.6 3.4 404.0 3.1 466.6 3.2 451.1 3.2

Taiwan 470.1 2.6 289.3 2.5 259.0 2.5 170.6 2.7

South Korea 463.6 3.2 190.3 2.9 146.6 2.7 81.6 2.6

Source: OTEXA, D&B India

2.1.16. The industry dynamics for different man-made fibres and filament yarn have been discussed

hereunder.

127

POLYESTER STAPLE FIBRE

2.1.17. The production of polyester staple fibre (PSF) grew steadily from 522.7 million kg in FY99 to 644.2

million kg in FY05 registering a CAGR of 3.5%. The growth has been higher during the post quota

period (6.2% CAGR during FY06-FY09). Production of PSF has increased steadily and has always

been much higher that the domestic consumption, which has led to substantial growth in the exports

of this fibre.

Exhibit 2.1.9: Demand-supply indicators (mn kg)

Parameter FY99 FY05 FY09P CAGR

(FY99-FY05) CAGR

(FY06-FY09)

Production 522.7 644.2 751.6 3.5 6.2

Import 17.4 15.4 16.5 -2.0 1.5

Export 16.6 50.1 136.4 20.2 47.4

Consumption 494.0 623.0 650.7 3.9 2.1

Source: Office of Textiles Commissioner

2.1.18. The overall installed capacity levels of PSF currently stands at around 1104.3 million kg (FY09P). The

key players manufacturing PSF include Reliance Industries, Indo Rama and JCT Fibre. Reliance

Industries is the leading player with almost 64% of total production in the industry (FY09).

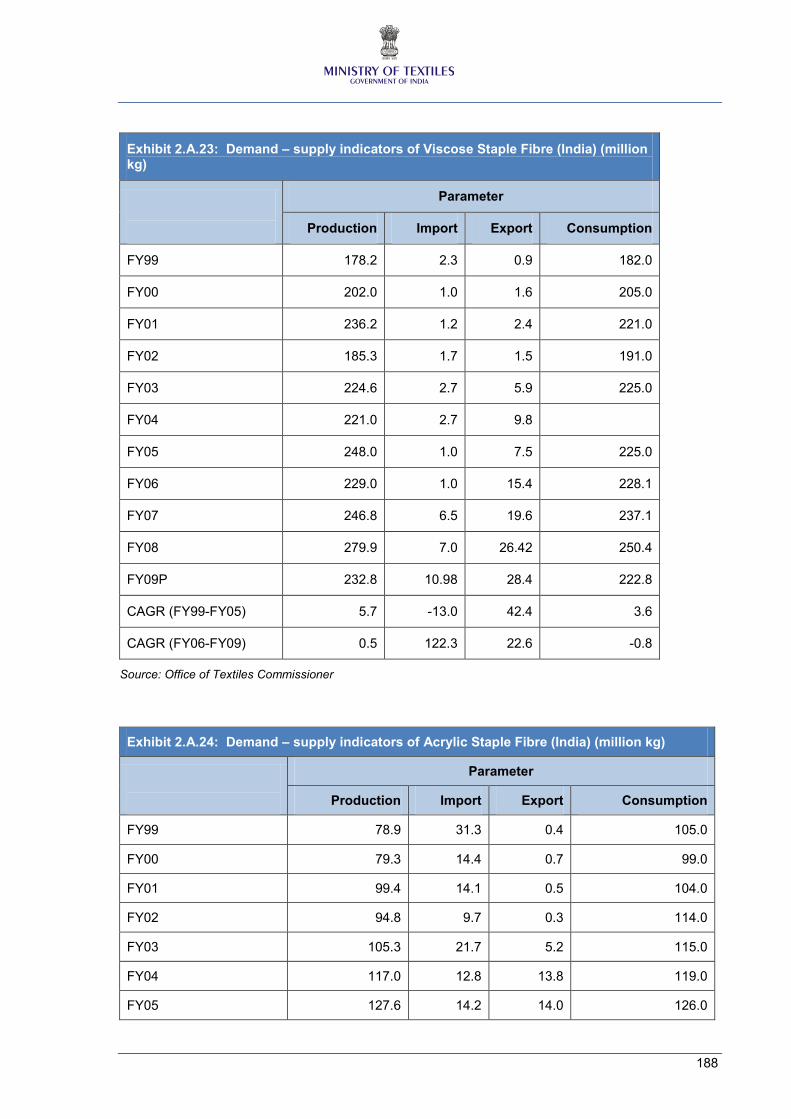

VISCOSE STAPLE FIBRE

2.1.19. The overall production of Viscose staple fibre (VSF) in India has grown at a CAGR of 2.7% from 178.2

million kg in FY99 to 232.8 million kg in FY09. While domestic production of VSF grew at a CAGR of

5.7% during the period FY99-05, the consumption grew at a CAGR of 22.8% during the same period.

However, production of VSF has fluctuated in the post quota period. There has been a rise in imports

during FY06-FY09 to cater to the domestic demand (CAGR of over 122%). The domestic

consumption of VSF grew from 228.1 million kg in FY06 to 250.4 million kg in FY08 registering a

CAGR of 4.8% during the same period. The installed capacity for VSF in the industry stood at 336.2

million kg in FY09. Grasim is the only manufacturer of VSF in India at present.

128

Exhibit 2.1.10: Demand-supply indicators (mn kg)

Parameter FY99 FY05 FY09P CAGR

(FY99-FY05) CAGR

(FY06-FY09)

Production 178.2 248.0 232.8 5.7 0.5

Import 2.3 1.0 10.98 -12.96 122.3

Export 0.9 7.5 28.4 42.39 22.6

Consumption 182.0 225.0 222.8 22.76 -0.8

Source: Office of Textiles Commissioner

ACRYLIC STAPLE FIBRE

2.1.20. A reverse trend can be observed in the overall production of acrylic staple fibre (ASF) wherein the

period before the abolishment of quotas saw production levels increase from 78.9 million kg in FY99

to 127.6 million kg in FY05 (registering a CAGR of 8.3%) while the production levels dropped by 9.7%

in the post quota period (FY06-09).

Exhibit 2.1.11: Demand-supply indicators (mn kg)

Parameter FY99 FY05 FY09P CAGR

(FY99-FY05) CAGR

(FY06-FY09)

Production 78.9 127.6 79.5 8.3 -9.7

Import 31.3 14.2 10.6 -12.3 -3.5

Export 0.4 14.0 1.6 80.9 -32.5

Consumption 105.0 126.0 90.5 3.1 -6.8

Source: Office of Textiles Commissioner

2.1.21. Dip in production levels in the period FY06-09 led to a 32.5% decrease in exports of the fibre. The

installed capacity of the acrylic staple fibre in India stood at 105 million kg in FY09. There are only

three key players manufacturing ASF at present, viz. Indian Acrylic Ltd, Pashupati Acrylon Ltd and

Vardhman Acrylic Ltd.

129

POLYPROPYLENE STAPLE FIBRE

2.1.22. The overall production of polypropylene staple fibre has grown steadily from 1.9 million kg in FY99 to

3.4 million kg in FY09 registering a CAGR of 6.2%. The production of the fibre grew at a CAGR of

7.3% in the pre quota abolishment period (FY99-05). The consumption of this fibre increased steadily

during the period FY99-05 registering a CAGR of 7.6%. In the period post abolishment of quotas, the

production levels grew at a CAGR of 3.1% from 3.1 million kg in FY06 to 3.4 million kg in FY09. While

the imports of polypropylene staple fibre contracted by 7.2% during the period FY06-09, its exports

increased by 28.6% during the same period.

Exhibit 2.1.12: Demand-supply indicators (mn kg)

Parameter FY99 FY05 FY09P CAGR

(FY99-FY05) CAGR

(FY06-FY09)

Production 1.9 2.9 3.4 7.3 3.1

Import 0.1 0.6 0.16 34.8 -7.2

Export 0.2 0.4 0.85 12.25 28.6

Consumption 2.0 3.1 2.6 7.6 -3.6

Source: Office of Textiles Commissioner

2.1.23. The capacities in the PPSF industry have remained constant at 5 million kg for last few years. Zenith

fibres is the leading player manufacturing PPSF in India.

POLYESTER FILAMENT YARN

2.1.24. Consumption of polyester filament yarn has risen since FY01. From a level of 727 million kg in FY99,

consumption touched 1,336 million kg in FY09. Exports have also witnessed high growth during the

period FY04-FY08 - CAGR of 33.1%. However, exports slumped by almost 60% to 90.1 million kg in

FY09, due to the overall global economic slowdown, while domestic demand grew by a modest 4.3%

in FY09. With rise in domestic production, imports of PFY have come down steadily over the years.

From a high of 114.7 million kg in FY05, imports of PFY dropped to 69.9 million kg in FY09.

130

Exhibit 2.1.13: Demand-supply indicators (mn kg)

Parameter FY99 FY05 FY09P CAGR

(FY99-FY05) CAGR

(FY06-FY09)

Production 745.4 1003.6 1330.3 5.1 7.3

Import 28.7 114.7 69.9 26.0 -8.9

Export 36.7 95.7 81.5 17.3 -8.3

Consumption 727.0 1041.1 1336.1 6.2 7.6

Source: Office of Textiles Commissioner

2.1.25. The installed capacity of PFY in industry stood at 1763.5 million kg in FY09. There are 43

manufacturing units in the country with functional installed capacity of 1,763 million kg per annum.

Reliance Industries is the largest player, accounting for almost 48% of total production of PFY in

FY09; the other major players are Indo Rama Synthetics, Garden Silk Mills, and JBF Industries.

VISCOSE FILAMENT YARN

2.1.26. Consumption of viscose filament yarn has come down since FY05. It has declined from 50.6 million kg

in FY05 to 41.8 million kg in FY08. It recovered marginally to 43.6 million kg in FY09. Due to decline in

demand, the overall production of viscose filament yarn (VFY) has also been declining in India.

Exports of VFY rose in the years following the abolishment of quotas, from 3.9 million kg in FY04 to

14.6 million kg in FY08. Exports however declined sharply to 4.2 million kg in FY09 due to the overall

global economic slowdown.

Exhibit 2.1.14: Demand-supply indicators (mn kg)

Parameter FY99 FY05 FY09P CAGR

(FY99-FY05) CAGR

(FY06-FY09)

Production 60.9 53.6 42.4 -2.1 -7.2

Import 1.0 2.9 5.2 19.4 27.7

Export 5.2 7.7 4.2 6.7 -24.9

Consumption 51.0 50.6 43.6 -0.1 -2.9

Source: Office of Textiles Commissioner

2.1.27. There are around 7 manufacturers of VFY with an installed capacity of 63.9 million kg. Some of the

key players include Century Rayon and Indian Rayon. Together these two account for almost 80% of

total VFY produced in the country. Other players manufacturing VFY include Kesoram Rayon and

National Rayon Corporation.

131

NYLON FILAMENT YARN

2.1.28. Nylon filament yarn production increased steadily from 26.1 million kg in FY00 to 35.4 million kg in

FY05. The production has declined to 28.1 million kg in FY09. The post quota period (FY06-FY09)

has seen a considerable decline in overall demand and production for NFY. Even exports and imports

have seen a negative growth, as can be observed from table below.

Exhibit 2.1.15: Demand-supply indicators (mn kg)

Parameter FY99 FY05 FY09P CAGR

(FY99-FY05) CAGR

(FY06-FY09)

Production 28.6 35.4 28.1 3.6 -8.6

Import 1.3 14.9 3.45 50.2 -32.5

Export 1.6 7.0 2.4 27.9 -21.8

Consumption 28.0 43.2 30.3 7.5 -10.7

Source: Office of Textiles Commissioner

2.1.29. The major units manufacturing NFY are Century Enka, JCT and Gujarat State Fertilizers Company.

The overall level of installed capacity of NFY in the industry currently stands at around 20 million kg.

POLYPROPYLENE FILAMENT YARN

2.1.30. The production of polypropylene filament yarn has risen from 36.6 million kg in FY01 to 39 million kg

in FY07. However, the production of this fibre has seen a dip in the last two fiscals and currently

stands at 34 million kg. One of the reasons for this dip has been a decline in demand during this

period on account of overall economic slowdown. The domestic consumption of PPFY was high at 44

million kg in FY04 but has gradually come down to 35 million kg by FY09.

Exhibit 2.1.16: Demand-supply indicators (mn kg)

Parameter FY01 FY05 FY09P CAGR (FY01-FY05) % CAGR (FY06-FY09) %

Production 36.6 38.1 34.0 1.0 -0.2

Import 0.6 5.9 1.7 77.8 -33.0

Export 2.2 1.0 0.7 -18.0 -9.8

Consumption 35.0 43.0 35.0 5.3 -3.5

Source: Office of Textiles Commissioner, Industry

132

2.1.31. In the periods when production has been lower than the overall domestic demand, there has been a

rise in imports of this fibre. During the last ten years, imports were highest in FY05 at 5.9 million kg,

when production was only 38.1 million kg as against the demand of 43.0 million kg. Exports of PPFY

have been very low, throughout the last ten year period and have seen a steady decline.

2.1.32. The capacity levels for PPFY currently stand at around 63 million kg. There are currently three main

players manufacturing PPFY, viz. Sumeet Synthetics, Filatax India and Shree Shyam Filament.

DYNAMICS OF VALUE ADDED MMF TEXTILES

2.1.33. MMF fabrics are produced primarily in the decentralized power loom sectors. The composite/big Mills

are not producing MMF fabrics. In fact, 75% of the polyester filament yarn fabrics are produced in the

Surat. Similarly, 65% of the MMF spun yarn fabrics are produced in Bhilwara. Bhiwandi and

Ichalkaranji are also major centres for MMF spun and mixed fabrics.

2.1.34. India’s overall cloth production increased at a CAGR of 4.9% from 45.4 billion square meters in FY05

to 55 billion square meters in FY09. Among the different varieties of fabrics, production of MMF

fabrics have grown steadily at a CAGR of 5.4% from 21 billion square meters in FY05 to 24.6 billion

square meters in FY08 and then declined by 2.8% y-o-y to 23.9 billion square meters, on account of

global slowdown leading to tepid demand from international markets.

2.1.35. In terms of composition, the share of MMF based fabrics (100% Non cotton and 50% of blended

fabrics) in total fabric production has contracted from 47% in FY05 to 44.1% in FY09, while the share

of cotton based fabrics has increased from 46.2% to 49.6% in the same period.

Exhibit 2.1.17: Production of MMF fabrics in India

133

2.1.36. Major items of MMF produced in the country are sarees, dress materials, shirting, suitings, home

textiles etc. In fact, 90% of the total sarees are now made of MMF. Cotton sarees are pre-dominantly

made in Handloom sector.

2.1.37. MMF textiles are cheaper vis a vis cotton and easy to maintain. Therefore, MMF fabrics and garments

are consumed mostly in rural, semi-urban and lower income segments in urban areas. There are

some local brands famous in the semi-urban, rural areas like Kumar, Cambridge etc. which enjoy

huge market share. In India, tailored garments have a huge market share and these are pre-

dominantly MMF fabrics based. The major MMF garment producing centres in the country are

Kolkata, Delhi and Indore.

2.1.38. There is a perception that in the domestic market cotton garments are predominant, but this not the

case. MMF products are predominantly consumed in the domestic market. MMF garments are

predominant to the extent of 65% in the domestic market, while in the export market cotton garments

are predominant to with over 80% share. The issues and concerns emanating out of imbalanced fibre

based T&G portfolio in India’s exports basket are discussed in detail in Chapter 3.

FUTURE DEMAND FOR MMF

2.1.39. Currently, India has excess capacities for many man-made fibres/ filament yarns and these are

adequate to meet the current and near future demand for man-made fibres. However, given the

changing consumer pattern in favour of man-made fibre based textiles, there is a need to assess the

medium term and long-term demand for man-made fibres in India. The demand for man-made fibres

depends upon the demand for yarns and fabrics, which in turn depends upon the consumption of

finished textiles viz. apparel and made-ups. Thus, in order to determine the future requirements for

man-made fibres/ filament yarns, we first need to assess demand for fabrics and finished textiles

made from man-made fibres, both for the domestic market as well as exports.

2.1.40. A top-down approach has been followed to determine the demand for man-made fibres in FY15 and

FY20. We have considered three scenarios, namely GDP growing at 7%, 8% and 9% respectively for

the next ten years. The share of private final consumption expenditure is taken as 67%, in line with

the average share over the past five years. The Eleventh five year plan report of the planning

commission for Textiles and Garments considers the share of textiles and clothing in PFCE to be

around 5.5% for FY08. It has been observed that over the past few years, the relative share of textiles

and clothing in total PFCE has come down due to increased private expenditure on transport and

communication, education, recreation, etc. Thus, we have considered the share of textiles and

clothing in the PFCE to be 5.3% for FY15 and 5.1% for FY20.

134

Exhibit 2.1.18: Demand projections for various man-made fibres/ filaments

Fibre

Current FY15E

Demand range (mn kg)

FY20E

Demand range (mn kg)

Domestic Demand*

(mn kg)

Existing capacities**

(mn kg)

PSF 739.1 1,104 1,066.7 – 1,147.1 1,542.9 – 1,743.6

VSF 250.4 336 359.3 – 386.4 514.3 – 581.2

ASF 94.7 105 128.6 – 138.3 169.5 – 191.6

PPSF 2.8 5 3.8 – 4.1 5.7 – 6.4

PFY@ 1,280.7 1,763 2,053.9 – 2,208.7 3,170.6 – 3,583.1

VFY 41.8 64 64.3 – 69.1 90.4 – 102.2

NFY# 28.7 20 45.4 – 48.8 67.8 – 76.6

PPFY 38.0 63 60.5 – 65.1 90.4 – 102.2

Domestic demand 2,476.1 3,460 3,782.5 – 4,067.6 5,651.6 – 6,386.9

Exports 453.9 – 488.1 678.2 – 766.4

Imports 151.3 – 162.7 226.1 – 255.5

Net demand/ requirement 4,085.1 – 4,393.1 6,103.8 – 6,897.9

E-Estimated, * -FY08 figures (FY09 has not been considered as it was an exceptional year with negative overall growth), ** - FY09 figures, @ Capacity under Board Banding scheme indicated against PFY,

# Exclusive capacity of NFY

Source: D&B India

2.1.41. Based on the above estimates, the demand for man-made fibres/ filament yarns in FY15 is projected

between 4,085 million kg and 4,393 million kg. Demand for man-made fibres/ filament yarns in FY20

is projected between 6,103.8 million kg and 6,897.9 million kg.

135

Exhibit 2.1.19: Future MMF requirements under different GDP growth scenarios (million kg)

FY15E FY20E

7% 8% 9% 7% 8% 9%

Domestic demand 3782.5 3921.1 4067.6 5651.6 6000.6 6386.9

(+) Exports 453.9 470.5 488.1 678.2 720.1 766.4

(-) Imports 151.3 156.8 162.7 226.1 240.0 255.5

Total fibre requirement 4085.1 4234.8 4393.1 6103.8 6480.6 6897.9

E- Estimated

Source: D&B India

2.1.42. The future fibre demand for different man-made fibres has been compared with existing capacities.

The current level of existing capacities of all man-made fibres would be insufficient to meet the future

demand and hence the above MMFs would require capacity additions by manufacturers. Detailed

explanation of demand projections is provided in annexure (Annexure 2.A.2).

136

2.2. GLOBAL SCENARIO

2.2.1. Global production of fibres has increased steadily at a CAGR of 4% from 35,438 million kg in 1990 to

68,669 million kg in 2007. The production of MMFs has grown at a faster rate as compared to natural

fibres. While production of MMFs has grown steadily at a CAGR of 6% (from 14,409 million kg in 1990

to 41,052 million kg in 2007), production of natural fibres has increased at a CAGR of 2% during the

same period.

Exhibit 2.2.1: Trend in production of fibres

Source: World Fibre Report 2008

2.2.2. The share of natural fibres in total production of fibres has rapidly deteriorated from 59% in 1990 to

40% in 2007, while that of man-made fibres has expanded rapidly from 41% in 1990 to the current

60%. This can be attributed to the higher growth of MMF production vis-à-vis cotton; while MMF

production recorded a CAGR of 6.6% during the ATC period (1994-2004).

Exhibit 2.2.2: Change in composition of fibres

MMF41%

Natural f ibres59%

1990

MMF60%

Natural f ibres40%

2007

Source: World Fibre Report 2008

137

Exhibit 2.2.3: Trend in global production of MMF

Source: World Fibre Report 2008

COMPOSITION OF MAN-MADE FIBRES

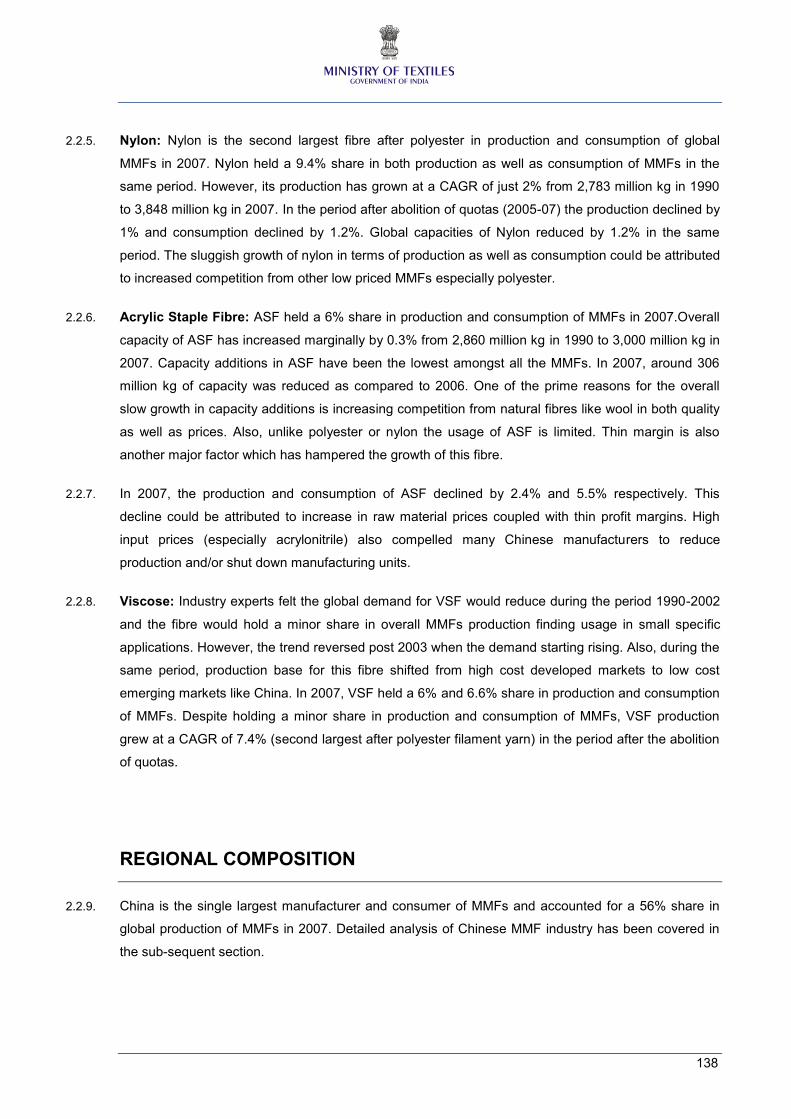

2.2.3. Globally, polyester is the most dominant man-made fibre, with a share of around 77% in total

production and consumption of man-made fibres. It is followed by nylon, with a share of 9.4% and

thereafter viscose, which constitutes roughly 7.7% share.

Exhibit 2.2.4: Composition of MMF’s production and consumption (2007)

ASF, 5.9

Nylon, 9.4

PFY, 46.5

PSF, 30.9

VFY, 1.1VSF, 6.0 Acetate, 0.2

Production

ASF, 6.0Nylon, 9.4

PFY, 45.9

PSF, 31.0

VFY, 1.2 VSF, 6.6

Consumption

Source: World Fibre Report 2008

2.2.4. Polyester: Polyester accounted for a major share of 77% in the production and consumption of MMFs

in 2007. This impressive performance of polyester can be attributed to a rapid increase in capacity of

this fibre. Overall capacity of polyester has increased at a CAGR of 8% from 10,837 million kg in 1990

to 40,724 million kg in 2007. The period after the abolition of quotas witnessed a 70.6% increase in

capacities of polyester to 36,376 million kg from 21,321 million kg in 2004. Among the varieties of

polyester fibre, production of PFY increased by 14.4% y-o-y while that of PSF grew by 12.3% in 2007.

138

2.2.5. Nylon: Nylon is the second largest fibre after polyester in production and consumption of global

MMFs in 2007. Nylon held a 9.4% share in both production as well as consumption of MMFs in the

same period. However, its production has grown at a CAGR of just 2% from 2,783 million kg in 1990

to 3,848 million kg in 2007. In the period after abolition of quotas (2005-07) the production declined by

1% and consumption declined by 1.2%. Global capacities of Nylon reduced by 1.2% in the same

period. The sluggish growth of nylon in terms of production as well as consumption could be attributed

to increased competition from other low priced MMFs especially polyester.

2.2.6. Acrylic Staple Fibre: ASF held a 6% share in production and consumption of MMFs in 2007.Overall

capacity of ASF has increased marginally by 0.3% from 2,860 million kg in 1990 to 3,000 million kg in

2007. Capacity additions in ASF have been the lowest amongst all the MMFs. In 2007, around 306

million kg of capacity was reduced as compared to 2006. One of the prime reasons for the overall

slow growth in capacity additions is increasing competition from natural fibres like wool in both quality

as well as prices. Also, unlike polyester or nylon the usage of ASF is limited. Thin margin is also

another major factor which has hampered the growth of this fibre.

2.2.7. In 2007, the production and consumption of ASF declined by 2.4% and 5.5% respectively. This

decline could be attributed to increase in raw material prices coupled with thin profit margins. High

input prices (especially acrylonitrile) also compelled many Chinese manufacturers to reduce

production and/or shut down manufacturing units.

2.2.8. Viscose: Industry experts felt the global demand for VSF would reduce during the period 1990-2002

and the fibre would hold a minor share in overall MMFs production finding usage in small specific

applications. However, the trend reversed post 2003 when the demand starting rising. Also, during the

same period, production base for this fibre shifted from high cost developed markets to low cost

emerging markets like China. In 2007, VSF held a 6% and 6.6% share in production and consumption

of MMFs. Despite holding a minor share in production and consumption of MMFs, VSF production

grew at a CAGR of 7.4% (second largest after polyester filament yarn) in the period after the abolition

of quotas.

REGIONAL COMPOSITION

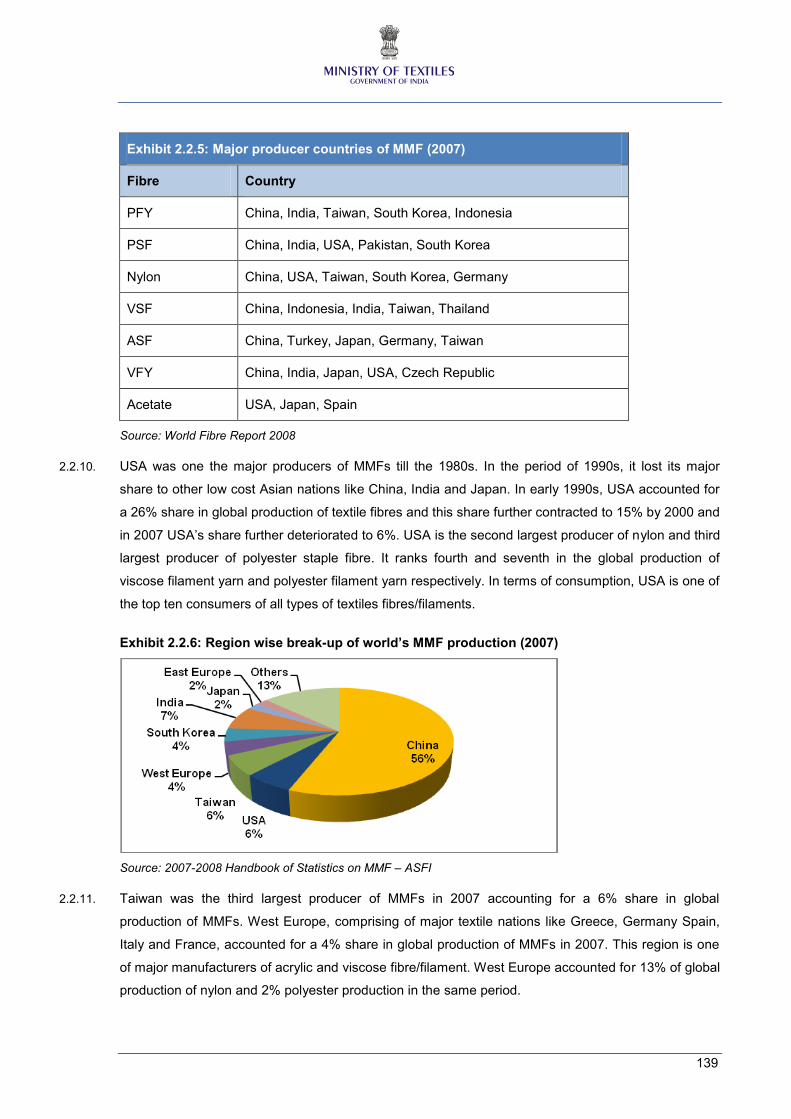

2.2.9. China is the single largest manufacturer and consumer of MMFs and accounted for a 56% share in

global production of MMFs in 2007. Detailed analysis of Chinese MMF industry has been covered in

the sub-sequent section.

139

Exhibit 2.2.5: Major producer countries of MMF (2007)

Fibre Country

PFY China, India, Taiwan, South Korea, Indonesia

PSF China, India, USA, Pakistan, South Korea

Nylon China, USA, Taiwan, South Korea, Germany

VSF China, Indonesia, India, Taiwan, Thailand

ASF China, Turkey, Japan, Germany, Taiwan

VFY China, India, Japan, USA, Czech Republic

Acetate USA, Japan, Spain

Source: World Fibre Report 2008

2.2.10. USA was one the major producers of MMFs till the 1980s. In the period of 1990s, it lost its major

share to other low cost Asian nations like China, India and Japan. In early 1990s, USA accounted for

a 26% share in global production of textile fibres and this share further contracted to 15% by 2000 and

in 2007 USA’s share further deteriorated to 6%. USA is the second largest producer of nylon and third

largest producer of polyester staple fibre. It ranks fourth and seventh in the global production of

viscose filament yarn and polyester filament yarn respectively. In terms of consumption, USA is one of

the top ten consumers of all types of textiles fibres/filaments.

Exhibit 2.2.6: Region wise break-up of world’s MMF production (2007)

Source: 2007-2008 Handbook of Statistics on MMF – ASFI

2.2.11. Taiwan was the third largest producer of MMFs in 2007 accounting for a 6% share in global

production of MMFs. West Europe, comprising of major textile nations like Greece, Germany Spain,

Italy and France, accounted for a 4% share in global production of MMFs in 2007. This region is one

of major manufacturers of acrylic and viscose fibre/filament. West Europe accounted for 13% of global

production of nylon and 2% polyester production in the same period.

140

2.2.12. South Korea is the fourth largest producer of nylon and polyester filament yarn, fifth largest

manufacturer of polyester staple fibre and sixth largest producer of viscose filament yarn. The region

accounted for a 4% share in global production of MMFs in 2007.

2.2.13. Japan, as per industry experts, is phasing out its production of MMFs. In early 1990, Japan accounted

for 12% share in global production of MMFs and this share contracted to 5% by 2000. Japan relies on

imports for its demand for MMFs. Despite Japan’s share fast contracting in supply of MMFs, the

regions remains one of the top ten suppliers and consumer of many MMFs. The region is third largest

producer of acrylic staple fibre and viscose filament yarn, sixth largest producer of viscose staple

fibre, eight largest in nylon, ninth largest producer of polyester staple fibre and tenth largest

manufacturer of polyester filament yarn.

2.2.14. The dynamics of man-made fibre industry for major countries and their policies are discussed in detail

in the annexure (Annexure 2.A.1).

141

2.3. ISSUES AND CONCERNS

EXCISE DUTY ANOMALIES

2.3.1. There exists a discrepancy in the duty charged on cotton vis-à-vis man-made fibres and textiles. For

instance, cotton is exempt from payment of excise duty whereas MMF manufacturers have to pay an

excise duty of 8%. MMF textiles also have a disadvantage vis-à-vis cotton textiles as the former

attract a mandatory CENVAT of 8% while the latter attracts only 4%, which is optional. Since cotton

does not attract any excise duty, most of the cotton yarn and fabric manufacturers prefer not to pay

any excise duty. Consequently, there is a disadvantage for MMF and MMF textiles’ manufacturers vis-

à-vis cotton and cotton textiles’ manufacturers.

Exhibit 2.3.1: Excise duty for 2009-10 (%)

Item Cotton Polyester Nylon Viscose Acrylic

Raw material Nil 8.24 8.24 Nil 8.24

Fibre/ filament - 8.24 8.24 8.24 8.24

Spun/ blended yarn 4.12* 8.24 8.24 8.24 8.24

Fabrics 4.12* 8.24 8.24 8.24 8.24

Garments 4.12* 8.24 8.24 8.24 8.24

Note: Excise duty includes 3% education cess on Basic Excise duty

* Optional Cenvat; if no Cenvat then nil duty

Source: Office of Textiles Commissioner

2.3.2. On the contrary, the excise duty structure in most of the other competing countries is uniform across

different fibres as well as the value chain. For instance, China levies a uniform VAT of 17% on all

fibres as well as textile products. Hence, there is a need to address this issue urgently and to make

the duty structure uniform for all fibres. 20

Exhibit 2.3.2: ExCross country duty rates comparison

India China * Indonesia Thailand

Cotton Nil 17% 10% 7%

Cotton yarn 4%/ Nil 17% 10% 7%

MMF 8% 17% 10% 7%

MMF yarn 8% 17% 10% 7%

Note: * - VAT rate Source: WTO, D&B India

142

CUSTOMS DUTY ANOMALIES

2.3.3. Historically, customs duty on man-made fibres had been very high. Over the last five years, customs

duties have been lowered substantially and currently prevail at about 5% for most man-made fibres.

However, the effective customs duty rate (after inclusion of SAD, CVD, etc) can be considered high

for certain fibres.

2.3.4. Certain raw materials for polyester such as Titanium di-oxide and spin finish oil attract a higher duty

than polyester fibres/ filaments. This is a clear case of inverted duty structure. According to industry

estimates, these additives constitute roughly 2-3% of total cost of production and are largely imported.

Thus, a high customs duty on these items increases the cost of production of man-made fibre

manufacturers.

Exhibit 2.3.3: Customs duty on MMF, raw materials and finished goods (2009-10)

Item Basic Custom duty (%)

Raw Materials

DMT, PTA, MEG 5.00

Acrylonitrile 5.00

Caprolactum 10.00

Propylene 5.00

Rayon grade wood pulp 5.00

Titanium Dioxide 10.00

Spin finish oil 7.50

Fibre/ Filament

PSF, ASF, VSF 5.00

PFY, VFY 5.00

NFY 10.00

Spun Yarn 5.00

Blended Yarn 10.00

Fabrics made of MMF 10.00 or Specific duty whichever is higher.

143

2.3.5. The customs duty in most competing countries do not have an inverted duty structure. For instance, in

South Korea, the customs duty on PTA and MEG is only 4.8% and 3% respectively and that on

polyester is higher at around 8%. In case of Thailand, there is no customs duty on basic raw materials

like PTA and MEG.

Exhibit 2.3.4: Duty structure on raw materials

Item India (FY10)

China (2008)

South Korea (2008)

Thailand (2007)

USA (2008)

PTA 5.0 6.5 4.8 Nil 6.5

MEG 5.0 5.5 3.0 Nil 5.5

Titanium di-oxide 11.0 5.5 Nil Nil 5.5

PSF 5.0 5.0 8.0 1.0 4.3

PFY 5.0 5.0 8.0 5.0 7.5

RGWP 5.0 Nil Nil Nil Nil

VSF 5.0 5.0 2.0 1.0 4.3

VFY 5.0 5.0 2.0 5.0 9.6

Source: WTO

DELAY IN GETTING DRAWBACK /EXCISE REBATE CLAIMS

2.3.6. At present, majority of MMF Textiles exporters are operating under Drawback/DEPB Scheme.

Appropriate Drawback Rates are crucial for growth in MMF Textiles Exports as it enables the players

to become competitive in the global markets. However, in FY09, there was a 4-5 percentage points

reduction in duty drawback rates for MMF without any changes in the duty rates.

Exhibit 2.3.5: Delay in reimbursement of drawback/excise rebate claims

Union Budget

Excise Duty On

MMF

Custom Duty On

MMF

Drawback Rates

Export Product Drawback Rates Effective

From

2007-08 8 % 5 % 14.8 %

17.5 %

MMF spun yarns (grey)

MMF spun yarns (dyed)

16-07-2007

2008-09 8 % 5 % 10.2 %

12.1 %

MMF spun yarns (grey)

MMF spun yarns (dyed)

01-09-2008

Source: SRTEPC

144

CONCERNS ABOUT ANTI DUMPING DUTIES

2.3.7. Anti-dumping duties are imposed to neutralise price differential between the normal value of the like

article in the domestic market of the exporting country and the export price of the product under

consideration. Currently, anti-dumping is levied on almost all man-made fibres, details of which are

as follows:

Import of POY from China, Taiwan, Indonesia, Malaysia and Thailand

Import of VFY from China

Import of NFY from China, Taiwan, Malaysia, Indonesia, Thailand and South Korea

Import of full drawn/fully oriented yarn/spin draw yarn/flat yarn of Polyester from

Indonesia, South Korea, Malaysia and Taiwan

Imports of Polypropylene

2.3.8. There is an argument by the spinning and weaving sectors that imposition of anti-dumping duties on

man-made fibres increases their input costs, rendering them uncompetitive in the global markets.

2.3.9. There is also apprehension amongst the user industry of man-made fibres about the mechanism

followed for levying anti-dumping duties; they believe that user community is not adequately consulted

while levying anti-dumping duties on man-made fibres/ filaments, which is their key raw material.

2.3.10. Secondly, the users of man-made fibre generally constitute small players who are not able to initiate

anti-dumping proceedings for their products, as it involves huge costs.

LOWER EXPORT BENEFITS FOR STANDALONE GARMENT

MANUFACTURERS

2.3.11. There are very few organised integrated players producing MMF fabrics and garments. Most of the

garment manufacturers have to procure MMF fabrics externally and are not able to get cenvat since

MMF fabrics producers are in the decentralised sector operating under optional cenvat route. Only

integrated organised players are able to get cenvat and DEPB which is more beneficial by 2-2.5% as

against stand alone RMG units which get only duty draw back or DEPB.

145

CONCERNS ABOUT GST

2.3.12. The Goods and Services Tax (GST) is to be introduced in the country from April 2010. It would be of

similar nature of VAT but would include other indirect taxes such as Cenvat, service tax. It would be

dual GST comprising of Central GST and State GST. GST would be destination based, while sales

tax and VAT for inter-state transactions are origin-based. On inter-state transactions of goods &

services, IGST (Integrated GST) would be applicable which would be equal to C-GST and S-

CST. The inter-state transactions would include sales of goods and services and inter-state depot

transfer of goods.

2.3.13. The textiles industry involves a lot of inter-state transfers especially at the fabric stage. Due to long

supply chain in the textile industry involving traders in various cities, towns, etc, the inter state

transactions are likely to take place among the organised players who are above the threshold limit for

GST exemption and small decentralised traders who are exempted from payment of GST.

Consequently, the regular payee (one above threshold limit) would not get any credit for purchases

from small decentralised trader but shall have to pay full duty on the sale price. Thus, the tax will

multiply and the purpose of VAT principle would be broken. This would have serious cost implications

on the exporters.

NIL INDIGENOUS PRODUCTION OF SPECIALISED MMF

2.3.14. MMF like acetate, cuprammonium filament yarn, nylon 66, nylon 11, spandex, PVA fiber and filament

yarn, which are required for manufacture of high end fashion garments, lingerie, swimming costumes,

Stockings, high end ladies garments are not produced indigenously and have to be imported by the

weavers. Thus, there is a need to have policy incentives in place to encourage domestic production of

such fibres in India.

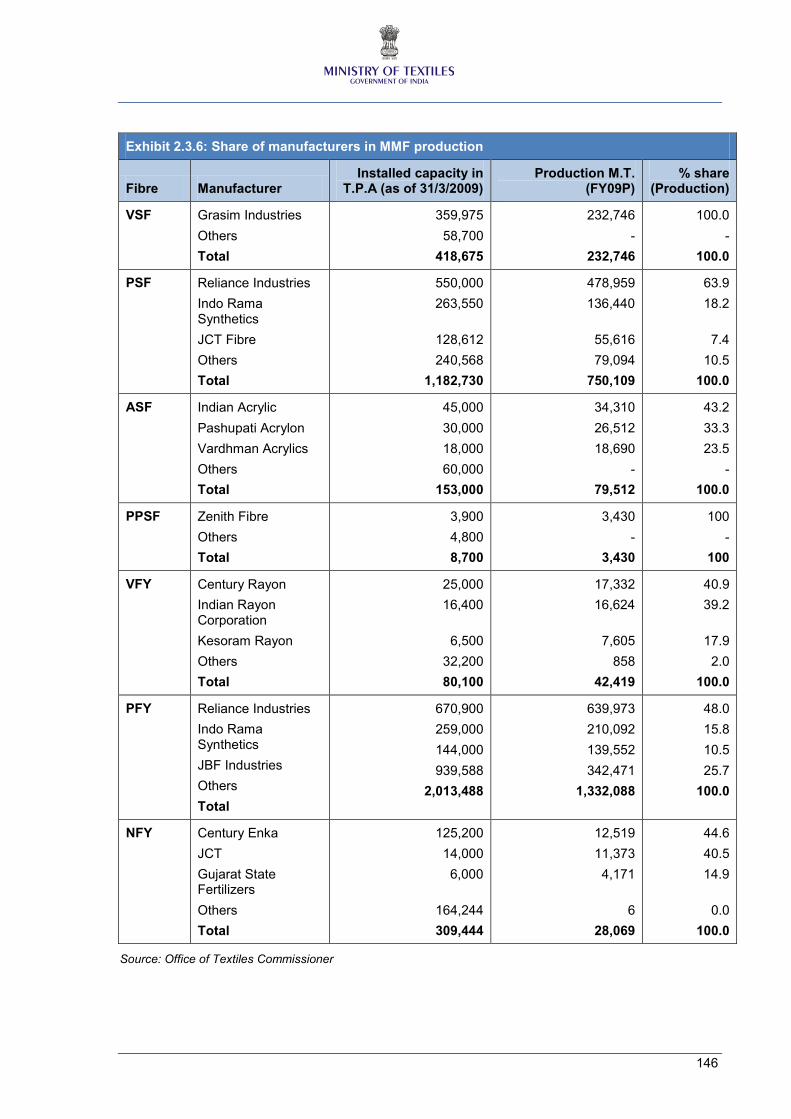

LIMITED NUMBER OF MMF PLAYERS

2.3.15. There are only a few big players manufacturing man-made fibres in India. The industry follows a

pricing policy on import parity basis at landed cost. User industry has submitted that MMF producers

export man-made fibres at lower prices than in the domestic market. This submission is supported by

SRTEPC exports data analysed by FIASWI in respect of polyester fibre and yarn.

146

Exhibit 2.3.6: Share of manufacturers in MMF production

Fibre Manufacturer Installed capacity in

T.P.A (as of 31/3/2009) Production M.T.

(FY09P) % share

(Production)

VSF

Grasim Industries

Others

Total

359,975

58,700

418,675

232,746

-

232,746

100.0

-

100.0

PSF

Reliance Industries

Indo Rama Synthetics

JCT Fibre

Others

Total

550,000

263,550

128,612

240,568

1,182,730

478,959

136,440

55,616

79,094

750,109

63.9

18.2

7.4

10.5

100.0

ASF

Indian Acrylic

Pashupati Acrylon

Vardhman Acrylics

Others

Total

45,000

30,000

18,000

60,000

153,000

34,310

26,512

18,690

-

79,512

43.2

33.3

23.5

-

100.0

PPSF

Zenith Fibre

Others

Total

3,900

4,800

8,700

3,430

-

3,430

100

-

100

VFY

Century Rayon

Indian Rayon Corporation

Kesoram Rayon

Others

Total

25,000

16,400

6,500

32,200

80,100

17,332

16,624

7,605

858

42,419

40.9

39.2

17.9

2.0

100.0

PFY

Reliance Industries

Indo Rama Synthetics

JBF Industries

Others

Total

670,900

259,000

144,000

939,588

2,013,488

639,973

210,092

139,552

342,471

1,332,088

48.0

15.8

10.5

25.7

100.0

NFY

Century Enka

JCT

Gujarat State Fertilizers

Others

Total

125,200

14,000

6,000

164,244

309,444

12,519

11,373

4,171

6

28,069

44.6

40.5

14.9

0.0

100.0

Source: Office of Textiles Commissioner

147

LACK OF COMPETITIVENESS IN EXPORTS

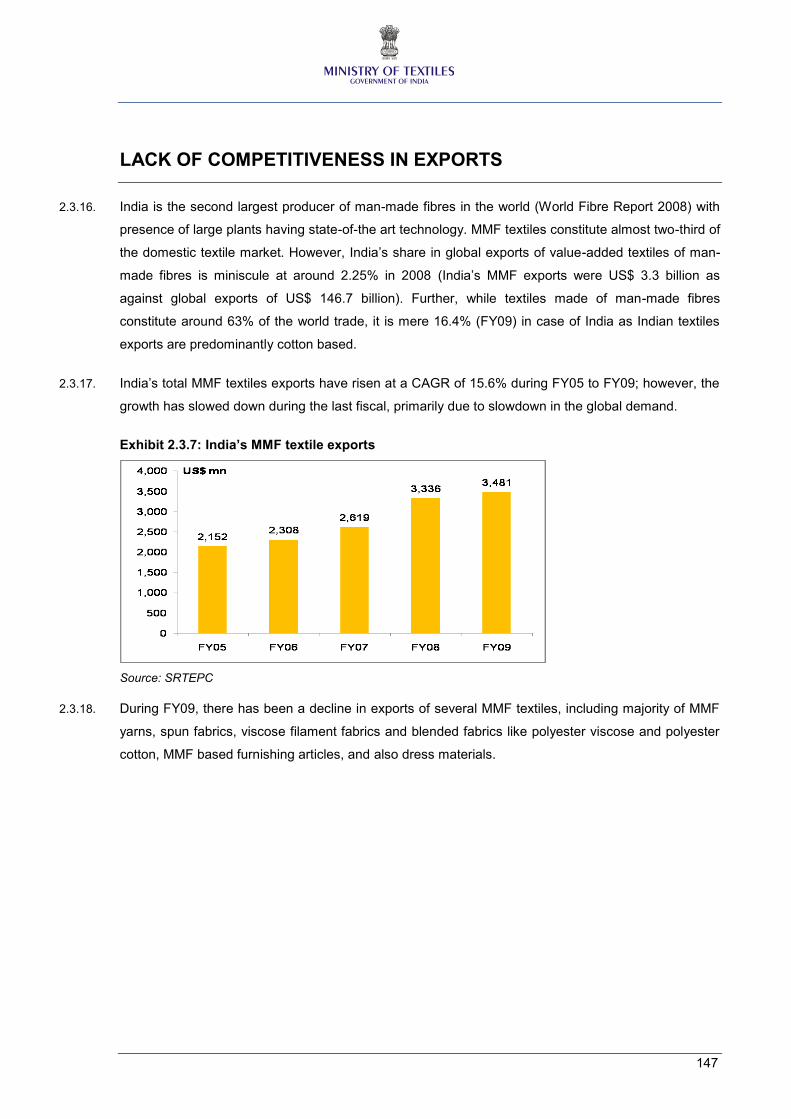

2.3.16. India is the second largest producer of man-made fibres in the world (World Fibre Report 2008) with

presence of large plants having state-of-the art technology. MMF textiles constitute almost two-third of

the domestic textile market. However, India’s share in global exports of value-added textiles of man-

made fibres is miniscule at around 2.25% in 2008 (India’s MMF exports were US$ 3.3 billion as

against global exports of US$ 146.7 billion). Further, while textiles made of man-made fibres

constitute around 63% of the world trade, it is mere 16.4% (FY09) in case of India as Indian textiles

exports are predominantly cotton based.

2.3.17. India’s total MMF textiles exports have risen at a CAGR of 15.6% during FY05 to FY09; however, the

growth has slowed down during the last fiscal, primarily due to slowdown in the global demand.

Exhibit 2.3.7: India’s MMF textile exports

Source: SRTEPC

2.3.18. During FY09, there has been a decline in exports of several MMF textiles, including majority of MMF

yarns, spun fabrics, viscose filament fabrics and blended fabrics like polyester viscose and polyester

cotton, MMF based furnishing articles, and also dress materials.

148

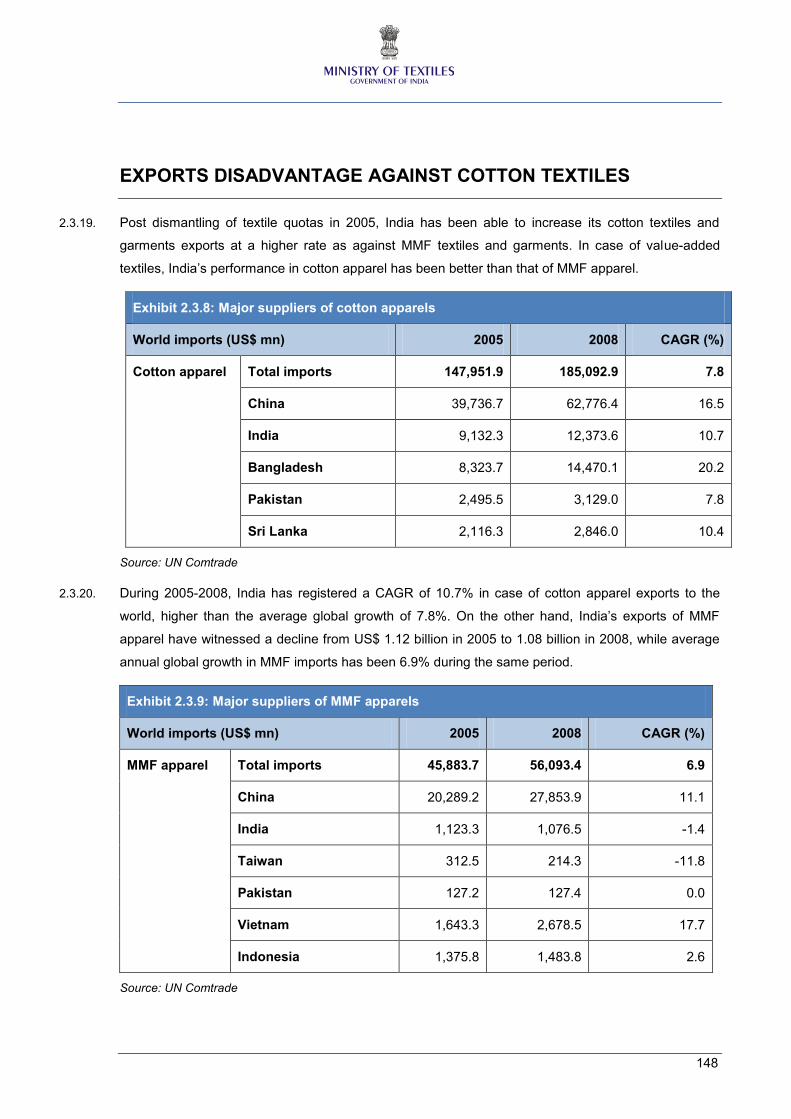

EXPORTS DISADVANTAGE AGAINST COTTON TEXTILES

2.3.19. Post dismantling of textile quotas in 2005, India has been able to increase its cotton textiles and

garments exports at a higher rate as against MMF textiles and garments. In case of value-added

textiles, India’s performance in cotton apparel has been better than that of MMF apparel.

Exhibit 2.3.8: Major suppliers of cotton apparels

World imports (US$ mn) 2005 2008 CAGR (%)

Cotton apparel Total imports 147,951.9 185,092.9 7.8

China 39,736.7 62,776.4 16.5

India 9,132.3 12,373.6 10.7

Bangladesh 8,323.7 14,470.1 20.2

Pakistan 2,495.5 3,129.0 7.8

Sri Lanka 2,116.3 2,846.0 10.4

Source: UN Comtrade

2.3.20. During 2005-2008, India has registered a CAGR of 10.7% in case of cotton apparel exports to the

world, higher than the average global growth of 7.8%. On the other hand, India’s exports of MMF

apparel have witnessed a decline from US$ 1.12 billion in 2005 to 1.08 billion in 2008, while average

annual global growth in MMF imports has been 6.9% during the same period.

Exhibit 2.3.9: Major suppliers of MMF apparels

World imports (US$ mn) 2005 2008 CAGR (%)

MMF apparel Total imports 45,883.7 56,093.4 6.9

China 20,289.2 27,853.9 11.1

India 1,123.3 1,076.5 -1.4

Taiwan 312.5 214.3 -11.8

Pakistan 127.2 127.4 0.0

Vietnam 1,643.3 2,678.5 17.7

Indonesia 1,375.8 1,483.8 2.6

Source: UN Comtrade

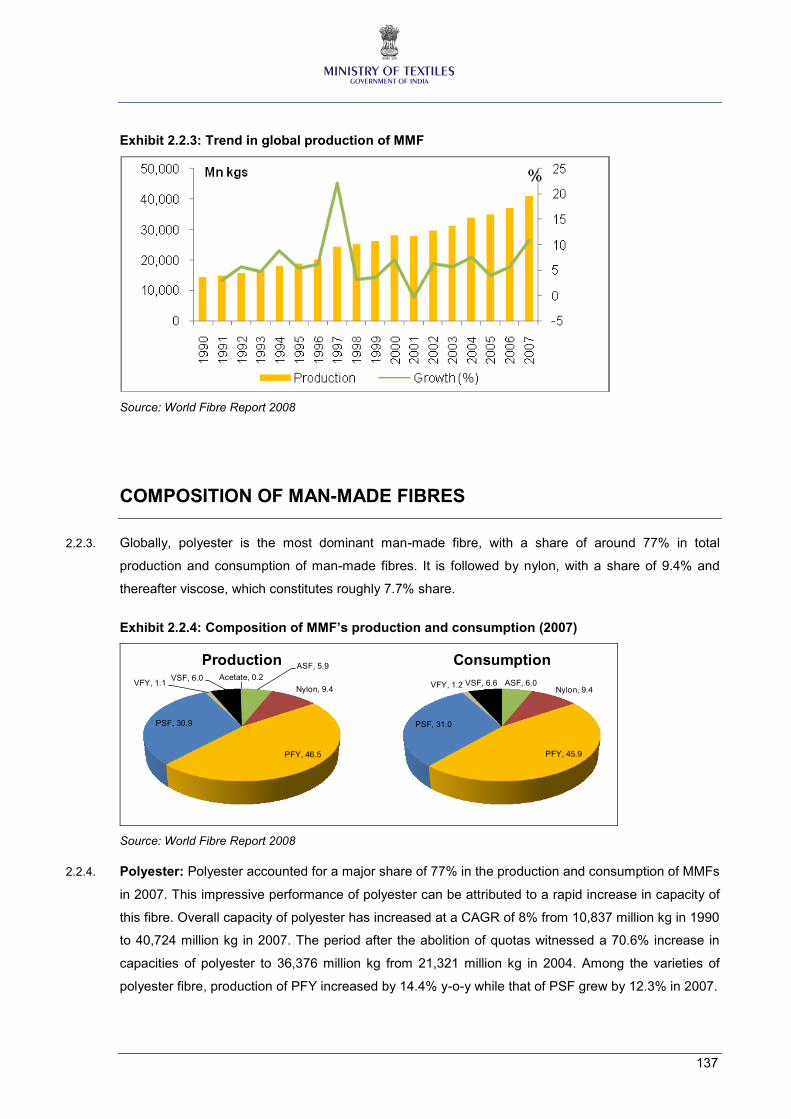

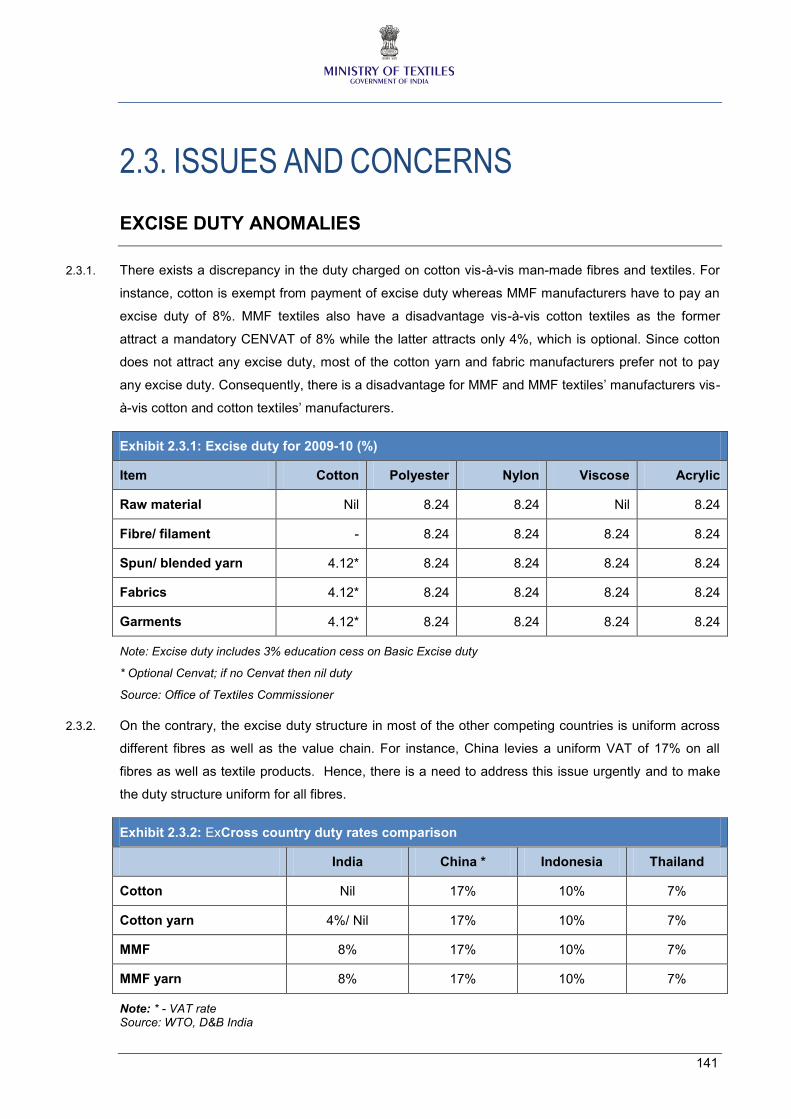

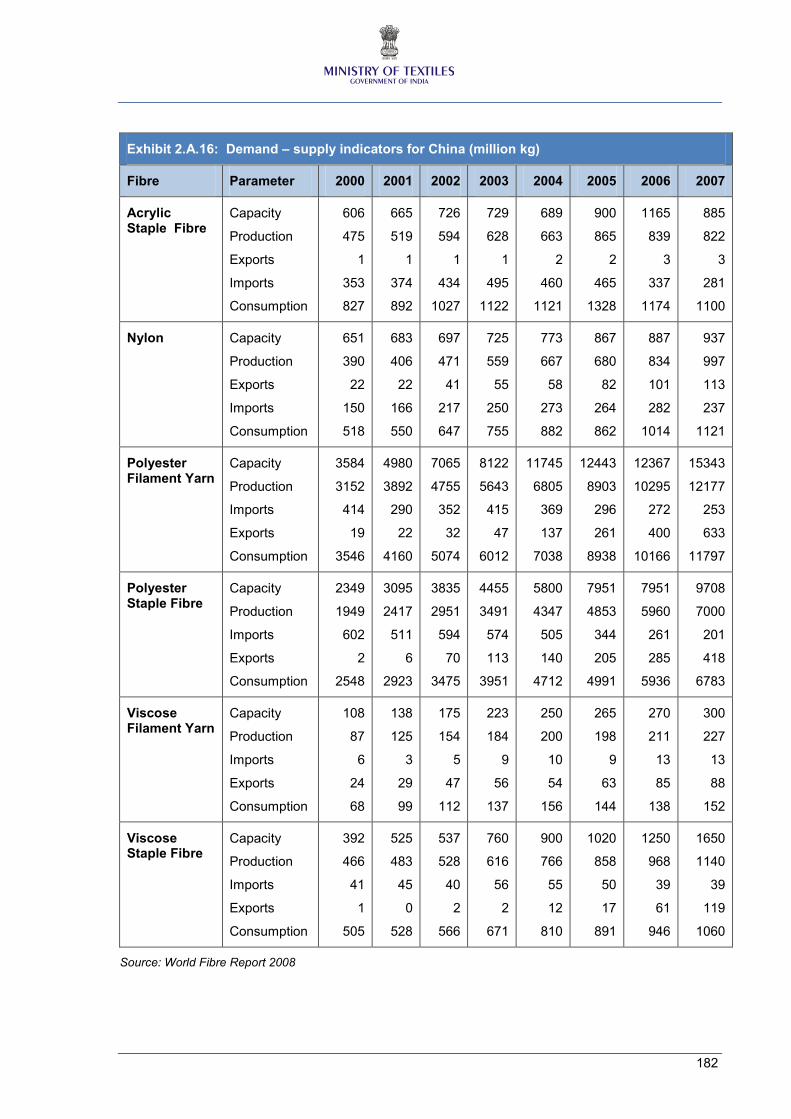

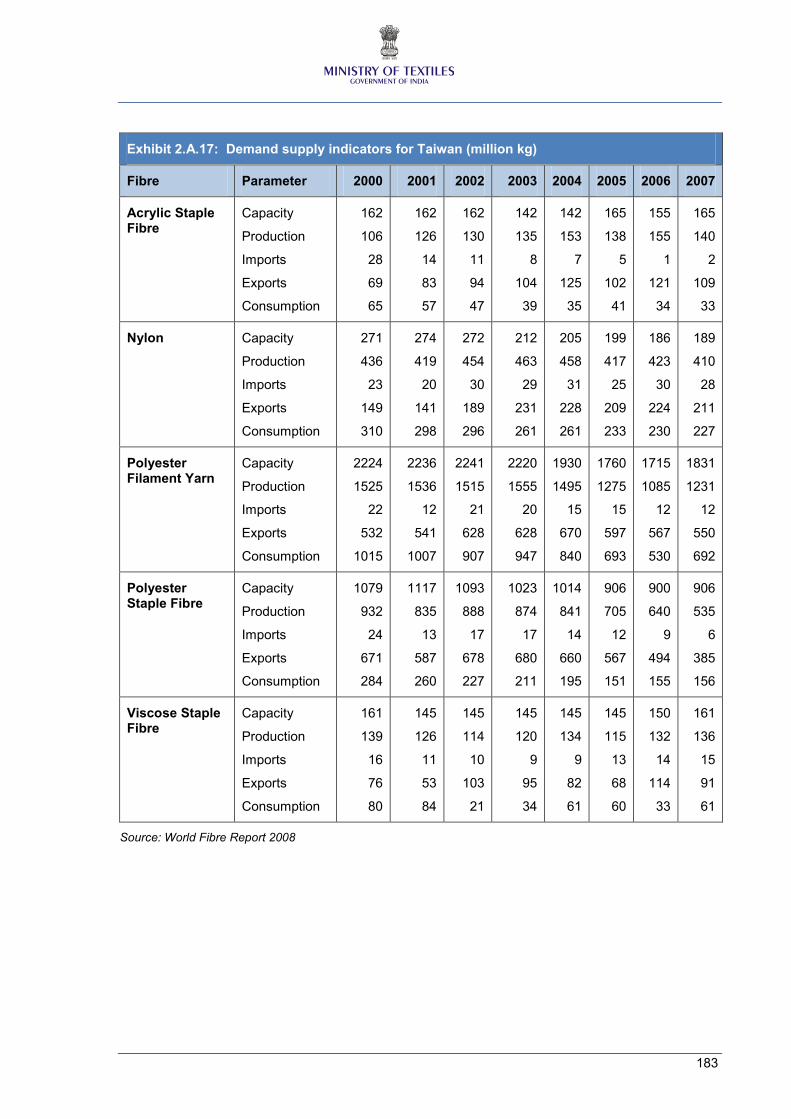

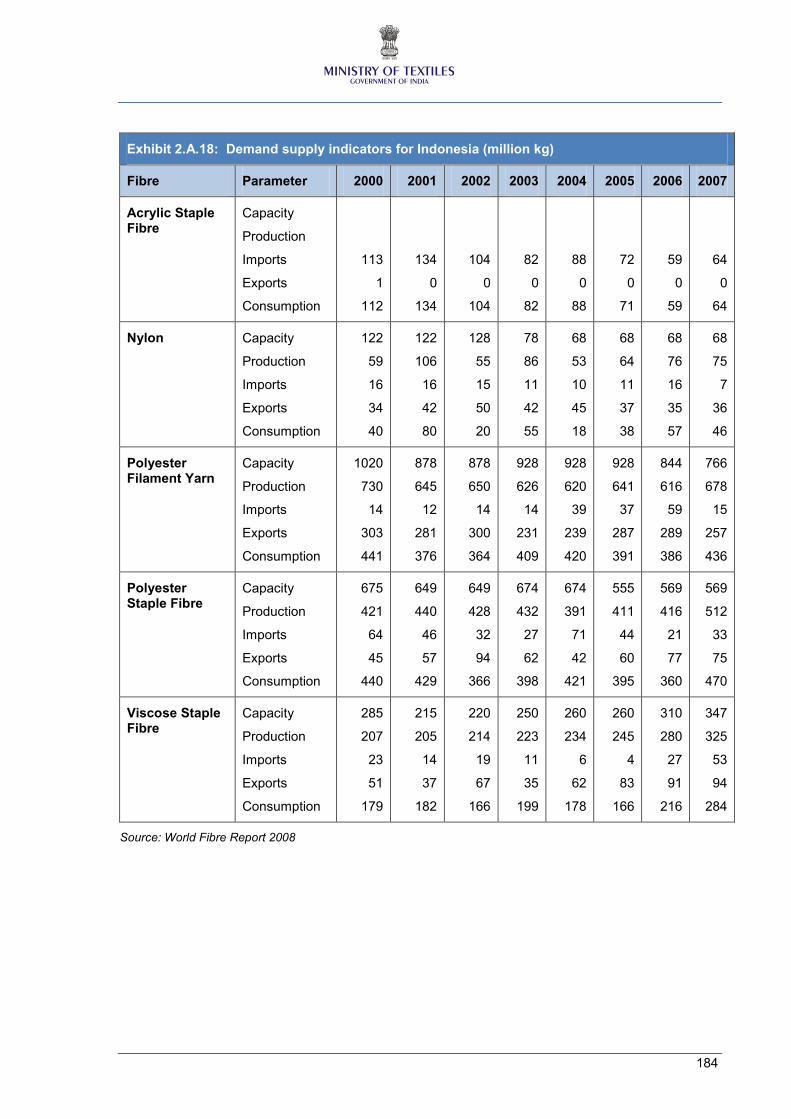

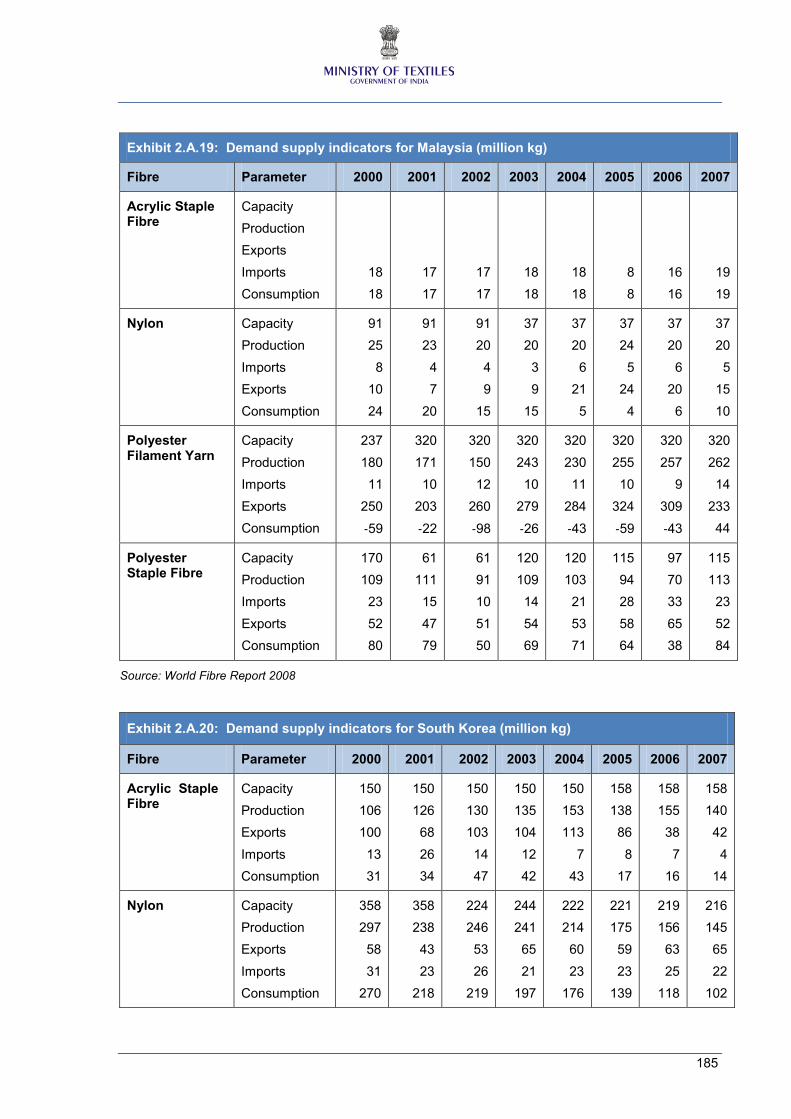

149