scm manual

DESCRIPTION

STRATEGIC COST MANAGEMENT.Improving Supply Chain - Competitiveness & Profitability in the 21st CenturyTRANSCRIPT

STRATEGIC COST MANAGEMENT

Improving Supply Chain Competitiveness & Profitability

in the 21st Century

Presented by

Anklesaria Group, Inc. 1172 Cuchara Drive

Del Mar, California 92014 Telephone: (858) 755-7119

Fax: (858) 755-2139 E-mail: [email protected]

Website: www.anklesaria.com

Copyright © 2001, Anklesaria Group, Inc. Del Mar, California

Part of this program is based on the book Zero Base Pricing™: Achieving World Class Competitiveness

Through Reduced All-in-Cost by

David N. Burt, Warren Norquist and Jimmy Anklesaria Byline Publishing

Zero Base Pricing™ is trademarked

by the Polaroid Corporation.

AIM & DRIVE is a registered servicemark by Jimmy Anklesaria

The material included in this Program Manual is copyrighted and may not be reproduced in whole or part

without the express written permission of Anklesaria Group, Inc., 1172 Cuchara Drive, Del Mar, California 92014.

Copyright © 2001, Anklesaria Group, Inc., Del Mar, California

All rights reserved

Code:010117

STRATEGIC COST MANAGEMENT TABLE OF CONTENTS

Page # The Anklesaria Group, Inc. Team 1 Firms That Have Participated in Anklesaria Group, Inc. Programs 3 Seminar Agenda and Objectives 4-5 Strategic Cost Management: The Concept 6-11 Cost and Price Management 12-42

Should Cost Models 16 Percentage of Sales Model 26 Price Discipline 30 Total Cost of Ownership Model 37

Implementing SCM 43-46 Exercises: 47-70 Case 1: Coating the Price 48 Case 2: Cable Connection 50 Case 3: Paying the Price 54 Case 4: Ace Incorporated 61 Case 5: The Collins Corporation 65 Optional Exercises: (Service Cases): 71-82 Case 1A: Price Maintenance 72 Case 3A: A Pricing Dilemma 74 Case 4A: A Temporary Solution 78 Appendix : 83-97 Appendix A: Economic Census 84 Appendix B: Pacific Bell Study - Overhead Rates 88 Appendix C: WageWeb Salary Data 89 Appendix D: Industry Financial Information 90 Appendix E: Producer Price Index 94 Appendix F: Bureau of Labor Statistics 96 Appendix G: Other Sources of data 99 Appendix H: International data sources 100 Appendix I: Present Value Interest Factor table 102

THE ANKLESARIA GROUP, INC. TEAM

JIMMY ANKLESARIA

Jimmy Anklesaria, F.C.A., LL.B. is the founder of Anklesaria Group, Inc. He is a Fellow Member of the Institute of Chartered Accountants, and holds a law degree and an M.B.A. Mr. Anklesaria is co-author of Zero Base Pricing™: Achieving World-Class Competitiveness Through Reduced All-In-Cost with David N. Burt and Warren E. Norquist. In January 1998 he founded Cost Management Solutions, LLC, which brings solutions to his various cost management programs through the use of sophisticated software. Mr. Anklesaria holds the international servicemark/patent for the AIM & DRIVE process. He has published several articles and cases in leading purchasing and financial journals and texts in the United States and abroad. One of America's most sought-after speakers on cost management, Mr. Anklesaria conducts seminars and workshops around the world. He has a unique ability to provide practical solutions to complex business problems. Mr. Anklesaria has been the keynote speaker for a number of organizations and companies. Mr. Anklesaria teaches a graduate level course in Strategic Cost Management at the University of San Diego, where he has been named Outstanding Professor of the Year. He is also a faculty member of the Certificate in International Business program in San Diego and is a guest lecturer at the University of Chicago, Graduate School of Business.

SANJIT MENEZES

Sanjit Menezes, CMA holds a Master of International Business degree from the University of San Diego. He is also a Certified Management Accountant. Mr. Menezes is currently the Anklesaria Group, Inc. Executive-in-Residence at the University of San Diego, where he teaches the undergraduate course in Strategic Cost Management/Contract Pricing. He was ranked among the top five instructors at the University of San Diego’s School of Business. Mr. Menezes has facilitated working sessions on cost management and conducted seminars for numerous firms around the world. He has developed a number case studies used to teach Strategic Cost Management and the AIM & DRIVE process. An enthusiastic and dynamic instructor, Mr. Menezes thinks quickly on his feet and has a natural ability to relate the material in the courses to real life situations. Mr. Menezes is currently responsible for the AGI Knowledge Center where he helps client companies bridge the knowing-doing gap. His expertise in "implementing" the Principles of Strategic Cost Management has saved clients millions of dollars.

PHIL KELLER

Phil Keller was with DuPont for 29 years and held positions in R&D, Sales, Marketing and for the past 20 years in many different line and management positions in procurement. His areas of expertise include Chemical raw materials, Specialty Chemicals, Capital Equipment and MRO supplies. Dr. Keller played a key role in developing DuPont's Strategic Sourcing Best Practice. He was instrumental in bringing both Strategic Cost Management and Managing the Cost of the Supply Chain

into DuPont. For the past 5 years he has facilitated Strategic Cost Management and mentored teams in applying cost management concepts. Dr. Keller's education includes a Bachelors degree and Ph.D in Chemistry from Temple University.

JOSEPH SANDOR

Joe Sandor, CPM, CPIM is one of America’s most respected Procurement visionaries. Prior to aligning with AGI, he was Chief Procurement Officer and Director of Corporate Purchasing and Logistics for the Sara Lee Corporation. Mr. Sandor currently is an adjunct professor of Supply Chain Management at the University of Chicago, Graduate School of Business. He brings over 24 years of Supply Management experience with Sara Lee, General Motors, NL Industries and Beatrice. Prior to joining Sara Lee, Mr. Sandor consulted for 3 years with companies such as, Sara Lee, RCA, Kraft, TRW, Hallmark Cards and others with emphasis on Materials Management strategy development. He holds an MBA from the University of Chicago, and is both a C.P.M. (Certified Purchasing Manager) and a CPIM (Certified in Production and Inventory Management).

M.P. “SID” SIDDHARTH

Sid Siddharth is an industrial marketing consultant specializing in competitive benchmarking, plant cost analysis, customer and supplier evaluations. He has a wide range of experience in the marketing consulting arena, including 10 years with Technomic Consultants, International. Providing in-depth analysis of supplier costs before a negotiation is one of his areas of expertise. He has consulted with several Fortune 500 firms in the areas of competitive cost analysis, new product introductions and acquisition/due diligence analyses. Mr. Siddharth has a Bachelor’s degree in Civil Engineering from Indian Institute of Technology, Madras, a Master’s in Civil Engineering from Vanderbilt University and an M.B.A. from Lehigh University.

JOHN STRIEBICH John Striebich has extensive knowledge and experience in corporate finance and accounting through his private and public sector work experience and academic preparation. He is an Adjunct Professor at Rochester Institute of Technology (R.I.T.) and the State University of New York at Geneseo, where he teaches courses in Finance and Economics. He has consulted with many small and medium-sized business in areas such as business plan development, venture capital acquisition and financial projections. Mr. Striebich holds an M.B.A. in Finance from R.I.T.

A partial list of firms that have participated in Anklesaria Group, Inc. programs

Abbot Laboratories Agilent Air Liquide Airborne Express Allen-Bradley Allied Signal Amana Electronics American Airlines American Express Amkor Electronics Amoco Chemicals Apple Computers Applied Materials Arizona Public Service ASM Int’l AVX Balzers Beitzell Bell Atlantic Bersdoff Extruders Bessin Corp. Bil Mar Foods Blackhawk Foundry Border States Burlington Air Exp. C-PAK Cadmus Capital One Financial Canon Casio Celestica Compact Industries Computer Task Group Conexant Chisso (Japan) Chevron Ciba-Geigy Conrail Columbia Gear Crenlo Cryovac Daichiyu Denshi Co. Dana Corporation Danzas Deco Tool Supply Deere & Co. Dewar Dewco Dexter Electronics DHL Dickey-John DISCO (Japan) Dow Chemical DNS DuPont EAC Plexus Eastman Chemical Eastman Kodak

Eaton Corp. Ebara Ecoplast Electrolux Emery Worldwide Faxon Federal Express FL Optics Flextronics Florida Power Fluor Daniel Fluorware FMC Corp. Ford Motor Co. Gem City General Dynamics General Electric Globe Machinery Grede Foundry Griffith Labs. GTI Hanover Direct Hamilton Standard Haraeus Harley Davidson Harris Corporation Hashimoto Hedwin Corp. Herman Miller Hewlett-Packard Hillshire Farm KLA-Tencor Kanto Hikari Photo Printing Hitachi Cable Hitachi Chemical Hoechst Celanese Honeywell, Inc. Reliant Energy IBM Iida Co. Ltd. Iomega Italtel Japan Energy Jimmy Dean Foods Kanto Japan Kelly Services KSK (Japan) Kuroda Electric Co. Kuwano (Japan) Kyocera Lam Research Litton Lockheed Lucent Maersk Manpower Matheson/Semi Gas

Maytag Mayville Engineering Medical Associates MEMC Menlo Logistics Mercury Aircraft Mercury Marine Mentor Graphics Mercedes-Benz Metalworks Incs. Metro Automation Millenium Petrochem. Milliken Mitsubishi Mitsui Metal Monona Tube Motorola Co. 3M N.A.P.M. Nalco Chemicals Nationway Transport NMC Nidec Nippon Nitto Novellus Nikon Norell Services NTK NSC Occidental Chemical Octel Network Ogilvy & Mather Oildyne Panalpina (Mexico) Parker Hannifin Partnership Works Philips Playtex Pratt & Whitney Praxair Probe Technologies PSEG Puget Plastics Qualcomm Quantum Rolls-Royce Rockwell Rohm Co., Ltd. Samsung Sandvik Sauer Sundstrand Sara Lee Schenker Eurocargo Scott Paper Sears Sequent Computer Sharp Corp.

Shell Oil Co. Shinetsu Shinkawa Shinko Shipley Signamax Signet Systems Soei (Japan) Solar Turbines Solectron Sony Corp. Southeast Freight SEH (America) Staples Star Manufacturing State of Illinois Steel Case Sumicarrier Sumitomo Chemical Superior Coffee TDK Takaki Tanaka Tandem Computers Teepak Tektronix Tennant Company Texas Instruments Tillotson Toppan (Japan) Tokyo Ohka Tokyo Seimitsu Tokyu Toshiba Triangle Plastics TRW UPS U.S. Marine Ushio UTC VDO Car Comm. VWR Waste Management Watanabe Watkins Johnson Co. Weber Seats Weyerhaeuser Wisconsin Label Xilinx Xyratex Yamadsa Yamashita Electric Yasuda Warehouse York International Young & Rubicam Z.F.Industries Zytec

Anklesaria Group, Inc. 2001

AGENDA

Day 1

u Introductionsu Strategic Cost Management: The Conceptu Anklesaria’s AIM & DRIVE® Process

Ø Case 1: Zero Base Pricing™

u Product Should Cost ModelsØ Case 2: Product Should Cost Model

u Service Should Cost ModelsØ Case 3: Service Should Cost Model

Anklesaria Group, Inc. 2001

AGENDA

Day 2u Cost Model: Percentage of Salesu Cost Model: Price Discipline™

Ø Case 4: Applying Price Discipline™

u Cost Model: Total Cost of Ownership (TCO)Ø Case 5: Applying TCO

u Profit Managementu Implementing SCM

Anklesaria Group, Inc. 2001

SEMINAR OBJECTIVES

u To gain a better knowledge of the cost structure of goods, equipment or services procured

u To differentiate between Zero Base Pricing™ and AIM & DRIVE®

u To distinguish between price and cost managementu To identify data sources and use market intelligence

in cost modelsu To use Price Discipline™ in long term contract

negotiationsu To apply the principles of TCO in sourcing decisions

Anklesaria Group, Inc. 2001

This slide is intentionally blank

STRATEGIC COST MANAGEMENT: THE CONCEPT

Anklesaria Group, Inc. 2001

It’s unwise to pay too much. But it’s worse to pay too little.

When you pay too much you lose a little money,that is all.

When you pay too little you sometimes lose everything, because the thing you bought was incapable of doing what it was bought to do.

The common law of business balance prohibits paying a little and getting a lot.

It can’t be done.

If you deal with the lowest bidder, it is well to add something for the risk you run.

And if you do that, you will have enough to pay for something better.

There is hardly anything in the world that someone can’t make a little worse and sell a little cheaper -- and people who consider price alone

are this man’s lawful prey.

John Ruskin(1819-1900)

Prices

Anklesaria Group, Inc. 2001

A HISTORICAL PERSPECTIVE

u The ‘50’s: Rebuilding the infrastructureu The ‘60’s: Decade of “catching up”u The ‘70’s: Emergence of global competitivenessu The ‘80’s: Quality, quality, qualityu The ‘90’s: Cost management & informationu 2000 & Beyond: Leveraging ideas over the

internet

Anklesaria Group, Inc. 2001

SUPPLY CHAIN COST FLOWA

cquisition Price

Conversion

GS&

A &

Profit

Revenue

Conversion

GS&

A &

Profit

Revenue

Acquisition P

rice

Acquisition P

rice

Supply Base Your Company

+ + = + + =

A1 A2 A3 A A B C X X

Cu

stomer

Drivers Drivers

$Money enters

the chain only once

Anklesaria Group, Inc. 2001

SELECTING YOUR STRATEGY

Time

Comparative

Costs $

This is where we generate real cost savings

•Jointly develop cost management strategies with suppliers (Cost Challenges)

•Execute strategies•Create knowledge base to leverage ideas

Breakthrough (AIM&DRIVE®)

•Leverage Volume•Price Analysis•Understand Costs•Price Discipline™

Negotiation (SCM)

Benchmark Competitor

Initial Cost Savings

Your Company

Anklesaria Group, Inc. 2001

USING COST DATA

Observations

Data

Understand the numbers

Manage Cost

Discussion

COST COOPERATION

Anklesaria Group, Inc. 2001

OVERCOMING BARRIERS TO COST SHARING

u Only request “relevant” datau Do not become an auditoru Sign a confidentiality agreement if

necessaryu Provide constructive feedbacku Communicate that cost knowledge is the

foundation for building a cost management strategy

Anklesaria Group, Inc. 2001

This slide is intentionally blank

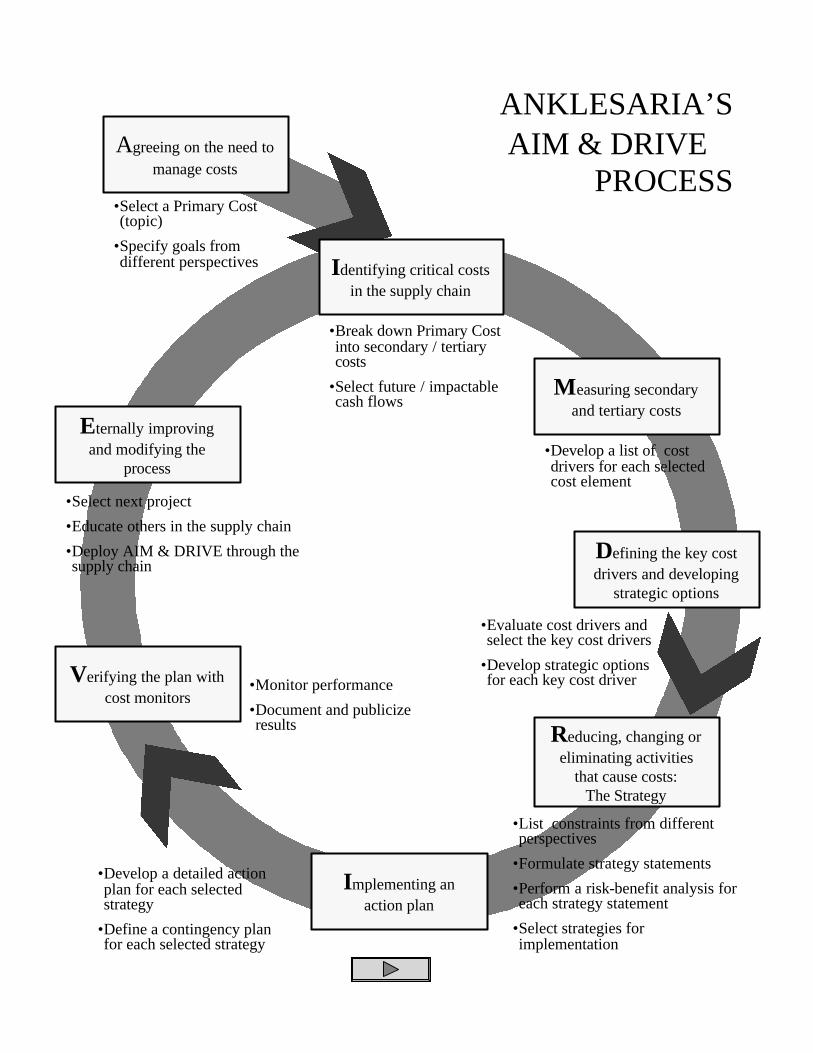

ANKLESARIA’S AIM & DRIVE

PROCESSAgreeing on the need to

manage costs

Implementing an action plan

Reducing, changing or eliminating activities

that cause costs:The Strategy

Defining the key cost drivers and developing

strategic options

Eternally improving and modifying the

process

Measuring secondary and tertiary costs

Identifying critical costs in the supply chain

Verifying the plan with cost monitors

•Select a Primary Cost (topic)

•Specify goals from different perspectives

•Break down Primary Cost into secondary / tertiary costs

•Select future / impactable cash flows

•Develop a list of cost drivers for each selected cost element

•Evaluate cost drivers and select the key cost drivers

•Develop strategic options for each key cost driver

•List constraints from different perspectives

•Formulate strategy statements

•Perform a risk-benefit analysis for each strategy statement

•Select strategies for implementation

•Develop a detailed action plan for each selected strategy

•Define a contingency plan for each selected strategy

•Monitor performance

•Document and publicize results

•Select next project

•Educate others in the supply chain

•Deploy AIM & DRIVE through the supply chain

PRICE AND COST MANAGEMENT

Anklesaria Group, Inc. 2001

PRICE ANALYSIS

u Evaluates and reviews only “bottom line” priceu Price analysis alone is useful when price is the

only variable that differentiates competing firmsu Can be used for standard products and servicesu Conducted through:

Ø Quote ComparisonsØ Internet cataloguesØ Historical Price ComparisonsØ Internet auction sitesØ Independent estimates

Anklesaria Group, Inc. 2001

COST ANALYSIS

u Initially evaluates each cost element that makes up the purchase price, including profit

u Later, extends to all other elements included in the “Total Cost of Ownership”

u Requires cost information from:Ø Supplier provided data (RFI/RFP/RFQ/survey)Ø Absolute Competitiveness Studies (benchmark

comparison)Ø Cost Models

u Can be used in single source or in competitive situations

Anklesaria Group, Inc. 2001

TYPES OF COST MODELS

uShould Cost ModelsØ Product Should CostØ Service Should Cost

uPercentage of Sales ModeluPrice Discipline™ Model

To evaluate Purchase Price:

*Note: The “Product Should Cost” approach was developed by Mark Cohen of Pacific Bell

To determine Life Cycle Costs:

uTotal Cost of Ownership Model

Anklesaria Group, Inc. 2001

THE POWER OF COST MODELS

u Educate the user in the cost structure of a product or service procured

u Engage a supplier that has not provided any cost information

u Ensure that cost discussions are based on facts and logic

u Build credibility and respect for well informed buyers

Anklesaria Group, Inc. 2001

SOME COST DEFINITIONS

Total of all cost elements

Profit before deduction of federal and state taxes

Costs incurred to keep the organization in operation (R&D, finance, procurement, mktg …)

Sub-total

Indirect costs associated with the conversion process (Depreciation, other plant costs, supervision, research support ...)

Product: Labor required to convert direct material into a finished product (production worker wages)

Service: Labor required to execute activities in the Statement of Work (SOW)

Bill of Materials (BOM)

Definition

PRICE=

Profit Before Tax+

Operating (GS&A)& Other Expenses

+

Cost of Goods Sold (COGS) or Cost of Sales (COS)

=

Manufacturing Overheador Service Overhead

+

Direct Labor+

Direct Material

Element

Anklesaria Group, Inc. 2001

AN INCOME STATEMENT APPROACH

NET PROFIT AFTER TAX=

TAXES (a percentage of Profit Before Tax)-

PROFIT BEFORE TAX=

OPERATING & OTHER EXPENSES-

GROSS PROFIT=

COST OF GOODS SOLD or COST OF SALES-

NET SALES (PRICE)

Element

Anklesaria Group, Inc. 2001

SHOULD COST MODEL

u Calculate a fair price for a product or service purchased

u Compare suppliers’ quotes to industry averages and to one another

u Extract cost information from suppliersu Identify key cost element/s for detailed

analysisu Estimate a target cost of a final product or

service

Application:

Anklesaria Group, Inc. 2001

SHOULD COST PHASES

u Development of a broad outline (framework)u Adjustments for:

a. Geographical locationb. Economic conditionsc. More current informationd. Other factors

u Use in negotiation

Anklesaria Group, Inc. 2001

PRODUCTSHOULD COST MODEL

Assumptions:

u Product purchased: Plastic housingu Supplier’s business: Fabricated Plastic Productsu Type of operation: Semi-automatedu Size of Supplier: $48 million in assets

Anklesaria Group, Inc. 2001

This slide is intentionally blank

Anklesaria Group, Inc. 2001

Step 1. Identification of product code and data sources:

BUILDING A PRODUCT SHOULD COST MODEL

Pacific Bell StudyData source for Overhead rates(See example on page 88 )

1.4

BOM, material or component suppliers, trade associations…

Data sources for Material costs1.2

US Census Bureau, Economic Census.

Data source for Labor costs(See example on page 85 )

1.3

RMA, Annual Statement Studies

Data source for financial ratios(See example on page 91 )

1.5

3089 / 308920Identify the SIC/NAICS code1.1

Step 2. Calculation of Direct Material (DM) costs:

= 5 * 2.00= $10.00

Calculate Direct Material costs2.3

$2.00 per lbObtain quotes on BOM elements2.2

5 lbs of resinBreak down the Bill of Materials (BOM)2.1

= 10.00 * 0.338= $3.38

Calculate Direct Labor costs(Direct Material * LM ratio)

3.2

= 8,951,204 / 26,503,716= 0.338

Using the Economic Census, Mfg. Series calculate the Labor/Material (LM) ratio(production worker wages / cost of materials, parts and containers consumed)

3.1

Step 3. Calculation of Direct Labor (DL) costs:

Anklesaria Group, Inc. 2001

Step 4. Calculation of Manufacturing Overhead (MOH):

Step 5. Calculation of Cost of Goods Sold (COGS) and Should Cost:

Step 6. Calculation of Operating & Other Expenses (O&O) and Profit:

PRODUCT SHOULD COST MODEL (CONTD)

= 4.2 / 100 * 25.39= $1.06

Calculate Profit Before Tax(PBT% * Should Cost)

6.2

= (18.1 + 1.7) / 100 * 25.39= $5.03

Calculate Operating & Other Expenses(O&O% * Should Cost)

6.1

= 19.30 / 0.76= $25.39

Estimate Should Cost(COGS$ / COGS%)

5.3

= 100.0 – 24.0= 76.0%

Using RMA, calculate COGS percentage(Net sales – Gross Profit)

5.2

= 10.00 + 3.38 + 5.92= $19.30

Calculate Cost of Goods Sold(DM + DL + MOH)

5.1

= 3.38 * 175= $5.92

Calculate MOH(Direct Labor * OH rate)

4.2

Plastic molding, semi-automatedaverage = 175%

Determine the applicable Overhead rate, based on type of operation and degree of automation

4.1

Anklesaria Group, Inc. 2001

PRODUCT SHOULD COST MODEL

SIC CODE 3089: MISC. PLASTIC PRODUCTS

BOM / quote from suppliers39.410.00Direct Material

100.025.39SHOULD COST

RMA, Annual Statement Studies4.21.06Profit Before Taxes

RMA, Annual Statement Studies19.85.03Operating & Other Exp.

RMA, Annual Statement Studies76.019.30Cost of Goods Sold

Pacific Bell Study23.35.92Manufacturing Overhead

Economic Census-Manufacturing Series13.33.38Direct Labor

Source%$Element

Anklesaria Group, Inc. 2001

PRODUCT SHOULD COST MODEL (ACTUAL)

BOM / quote from suppliers10.0010.00Direct Material

COGS $ / 0.7616.7425.39SHOULD COST

Should Cost * 0.0420.701.06Profit Before Taxes

Should Cost * 0.1983.325.03Operating & Other Exp.

Sub-total12.7219.30Cost of Goods Sold

Direct Labor * 32.045.92Manufacturing Overhead

Direct Labor / 50.683.38Direct Labor

SourceActualModelElement

A site visit indicated that the operation was fully automated. A fully automated machine was 5 time faster than a semi-automated one; actual OH was 300% of Direct Labor

Anklesaria Group, Inc. 2001

SERVICESHOULD COST MODEL

Assumptions:

u Service purchased: Design of mechanical toolu Supplier’s business: Engineering Servicesu Supplier location: Decatur, ILu Length of contract: 2 months

Anklesaria Group, Inc. 2001

This slide is intentionally blank

Anklesaria Group, Inc. 2001

Step 1. Identification of service code and data sources:

BUILDING A SERVICE SHOULD COST MODEL

Operations, HR departments of benchmark companies

Data sources for Statement of Work and bill-out ratio

1.4

IRS tables, Finance departmentData sources for corporate tax rate1.5

US Census Bureau, Economic Census, BLS Industry Occupation Matrix, Wageweb.com,

Data sources for Labor costs(See examples on pages 86, 57 & 89)

1.2

Dun & Bradstreet, Key Financial Norms and Ratios

Data sources for financial ratios(See example on page 92)

1.3

8711/541330Identify the SIC/NAICS code1.1

Anklesaria Group, Inc. 2001

SERVICE SHOULD COST MODEL (CONTD)

= 5.1 / (1 – 0.3)= 7.3%

Calculate Profit Before Tax %{PBT% = Net profit after tax% / (1 – tax rate)}

2.7

= 100 – (53.6 + 7.3)= 39.1%

Calculate O & O Expenses %{100 – (COS% + PBT%)}

2.8

= 53.6 – 32.2= 21.4%

Calculate Overhead %(COS% – DL%)

2.5

= 30%Using IRS tables, determine tax rate2.6

= 0.82 * 39.3= 32.2%

Calculate Direct Labor as a percentage of sales (DL% * Payroll%)

2.3

= 100- 46.4= 53.6%

Using D&B ratios, calculate Cost of Sales%(Net Sales% – Gross Profit%)

2.4

= 1,330,332 / 3,380,960= 39.3%

Using the Economic Census, Prof., Scientific and Tech. series, calculate Total Payroll as a percentage of sales(Annual Payroll / Total receipts)

2.2

= 82%

Using BLS IO matrix select Direct Labor items and determine Direct Labor $ as a percentage of Total Payroll

2.1

Step 2. Calculation of industry averages:

7.3Profit Before TaxE

100.0SHOULD COST (C+D+E)F

53.6Cost of Sales (A+B)C

39.1Operating & Other ExpensesD

21.4OverheadB

32.2Direct LaborA

Summary of industry averages (figures in %):

Anklesaria Group, Inc. 2001

Step 3. Calculation of Direct Labor Cost:

SERVICE SHOULD COST MODEL (CONTD)

Step 4. Calculation of Contract Price:

= 96,851 / 0.322= $300,779

Calculate contract price (CP)(Labor $ / Labor%)4.1

Step 5. Calculation of OH, COS, O&O and PBT Dollars:

= 300,779 * 0.073= $21,957

Calculate Profit Before Tax dollars(Contract price * PBT%)

5.4

= 300,779 * 0.391= $117,604

Calculate Operating & Other Exp. dollars(Contract Price * O&O%)

5.3

= 300,779 * 21.4= $64,367

Calculate Overhead dollars(Contract price * OH%)

5.2

= 300,779 * 0.536= $161,218

Calculate COS dollars(Contract price * COS%)

5.1

= 77,481 / 0.8= $96,851

Adjust Direct Labor cost for down-time (Direct Labor Cost / Billed time)3.4

80%, interview with ABC Co., T-Tech Inc.

Estimate percent of time billed out and document the source of this information

3.3

1 Supervisor @ $81,2755 engineers @ $64,1052 Technician @ $31,543Total = $464,886 / yearCost for 2 months:= 464,886 / 6= $77,481

Using data from Wageweb.com, calculate Direct Labor cost for contract term(salaries include Mean Avg. Max. Salary plus bonus)3.2

1 Supervisor5 Mechanical Engineers2 Technicians

Break down the Statement of Work and determine the labor requirements for the contract

3.1

Anklesaria Group, Inc. 2001

SERVICE SHOULD COST MODEL

SIC CODE 8711: Engineering Services

Labor $ / Labor %100.0300,779SHOULD COST

Dun & Bradstreet – Key Financial Ratios7.321,957Profit Before Taxes

Dun & Bradstreet – Key Financial Ratios39.1117,604Operating & Oth. Exp.

Dun & Bradstreet – Key Financial Ratios53.6161,218Cost of Sales

Cost of Sales - Labor21.464,367Overhead

Economic Census- Prof. Scientific, Tech Svcs – Geographic area series32.296,851Labor

Source%$Element

Anklesaria Group, Inc. 2001

SERVICE SHOULD COST MODEL (ACTUAL)

SIC CODE 8711: Engineering Services

Labor cost / 0.322343,748300,779SHOULD COST

Should cost * 0.07325,09421,957Profit Before Taxes

Should cost * 0.391134,405117,604Oper. & Other Exp.

Should Cost * 0.536184,249161,218Cost of Sales

Should cost * 0.21473,56264,367Overhead

96,851 * 0.8 / 0.7110,68796,851Labor

DetailsActualModelElement

Supplier indicated that engineers were billed out approximately 70% of the time

Anklesaria Group, Inc. 2001

PERCENTAGE OF SALES MODEL

Application:

u To understand the break-down of a supplier’s price, even when the price appears fair and reasonable

u To develop Price Discipline™ models in order to evaluate price-change requests over a period of time

u To engage a supplier that has not provided any cost information in a discussion on cost

Anklesaria Group, Inc. 2001

PERCENTAGE OF SALES MODEL

Assumptions:

u Product Purchased: Printed Materialu Supplier’s business: Commercial Printing,

Lithographicu Size of supplier: $30 million in salesu Supplier’s quote: $250 per 100 copies

Anklesaria Group, Inc. 2001

Step 1. Identification of product code and data sources:

Step 2. Calculation of Direct Material (DM) Cost:

Step 3. Calculation of Direct Labor (DL) Cost:

BUILDING A PERCENTAGE OF SALES MODEL

US Census Bureau, Economic Census, Manufacturing Series

Data source for Material costs(See example on page 87)

1.2

Economic Census, Manufacturing SeriesData source for Labor costs1.3

RMA, Annual Statement Studies

Data source for financial ratios(See example on page 93)

1.4

2752 / 323110Identify the SIC/NAICS code1.1

= 250.00 * 0.346= $86.50

Calculate Material costs(Material% * 250)

2.2

= 16,660,337 / (45,392,837+ 2,704,062)= 34.6%

Using the Economic Census, Mfg. Series, calculate Material as a % of Sales(Cost of material parts, containers etc. / {Primary products value of shipments + Secondary products value of shipments})

2.1

=250.00 * 0.18= $45.00

Calculate Direct Labor costs(Labor% * 250)

3.2

= 8,631,629 / (45,392,837+ 2,704,062)= 18.0%

Using the Economic Census, Mfg. Series calculate the Labor as a % of Sales(Production worker wages / {Primary products value of shipments + Secondary products value of shipments})

3.1

Anklesaria Group, Inc. 2001

Step 4. Calculation of COGS, O&O Expenses and Profit dollars:

Step 5. Calculation of Manufacturing Overhead (MOH) dollars:

PERCENTAGE OF SALES MODEL (CONTD)

= 250 * 0.043= $10.75

Calculate Profit Before Tax $(250 * PBT%)

4.5

= 4.3%Using RMA, determine Profit Before Tax%

4.4

= 250 * 0.214= $53.50

Calculate Operating & Other Exp. $(250 * O&O%)

4.3

= 19.4 + 2.0= 21.4%

Using RMA, determine Operating & Other Exp.% (Operating Exp. + Other Exp.)

4.2

= 100.0 – 25.7= 74.3%

Using RMA, calculate COGS%(COGS% = Net Sales% – Gross Profit%)

4.1

= 250 * 0.217= $54.25

Calculate Manufacturing Overhead $(250 * MOH%)

5.2

= 74.3 – {34.6 + 18.0}= 21.7%

Determine MOH as a % of Sales(MOH% = COGS% – {DM% + DL%})

5.1

Anklesaria Group, Inc. 2001

PERCENTAGE OF SALES MODELSIC Code 2752: Commercial Printing, Lithographic

Economic Census –Manufacturing series34.686.50Direct Material

100.0250.00SHOULD COST

RMA, Annual Statement Studies4.310.75Profit Before Taxes

RMA, Annual Statement Studies21.453.50Operating & Oth. Exp.

RMA, Annual Statement Studies74.3185.75Cost of Goods Sold

COGS – (DM = DL)21.754.25Manufacturing Overhead

Economic Census-Manufacturing Series18.045.00Direct Labor

Source%$Element

Anklesaria Group, Inc. 2001

This slide is intentionally blank

Anklesaria Group, Inc. 2001

PRICE DISCIPLINE MODEL

u Determines the reasonableness of a suppliers request for a change in price

u Uses a previous year’s price as a baseu Sets the structure for all future

discussions on priceu Useful in setting up LTA’s

Price Discipline™ involves an understanding that the various elements of cost are NOT directly correlated

Anklesaria Group, Inc. 2001

APPLYING PRICE DISCIPLINE™

ØFixed OH – Volume, inflation

ØVariable OH – InflationOverhead

ØRisk

ØValue added

ØWage rates

ØProductivity

ØMarket priceØTake Down Rate

ØVolume

Profit

ØSkill levels

ØSkill MixLabor

ØStability of ordersØMaterial yields

ØExchange ratesMaterial

SAMPLE FACTORSCOST

Make a list of the factors that impact each cost element, quantify the impact of each factor and adjust respective cost elements

Anklesaria Group, Inc. 2001

Step 2. Adjustment of Material Costs:

Step 1. Comparison of quotes

PRICE DISCIPLINE MODEL

See Percentage of Sales model

Build a Percentage of Sales model for the base year price

1.3

15,00024501

10,00025000

Vol..PriceYr

Compare current quote with base year quote1.2

2000Select a base year1.1

Take-down rates, Bench-marking studies

Supplier Competitive-ness

Quality auditsProductivity

PPIPrice

Track Mech.FactorList the factors that have impacted material costs over the given period and identify tracking mechanisms/indices to evaluate changes in each factor(see page 95)

2.3

Interviews with D Co., A Inc.Document all sources of information2.2

1.00Total

0.09Miscellaneous supplies4.

0.062893-23234Lithographic and offset ink (sheet)3.

0.152796-231Plates2.

0.702621-4Book paper, uncoated free sheet1.

WeightSIC CodeElement#

Break down the BOM into major elements, identify industry codes and assign weights for each. (For services, break down the SOW into activities, identify skill level requirements and assign weights based on time for each activity)

2.1

Anklesaria Group, Inc. 2001

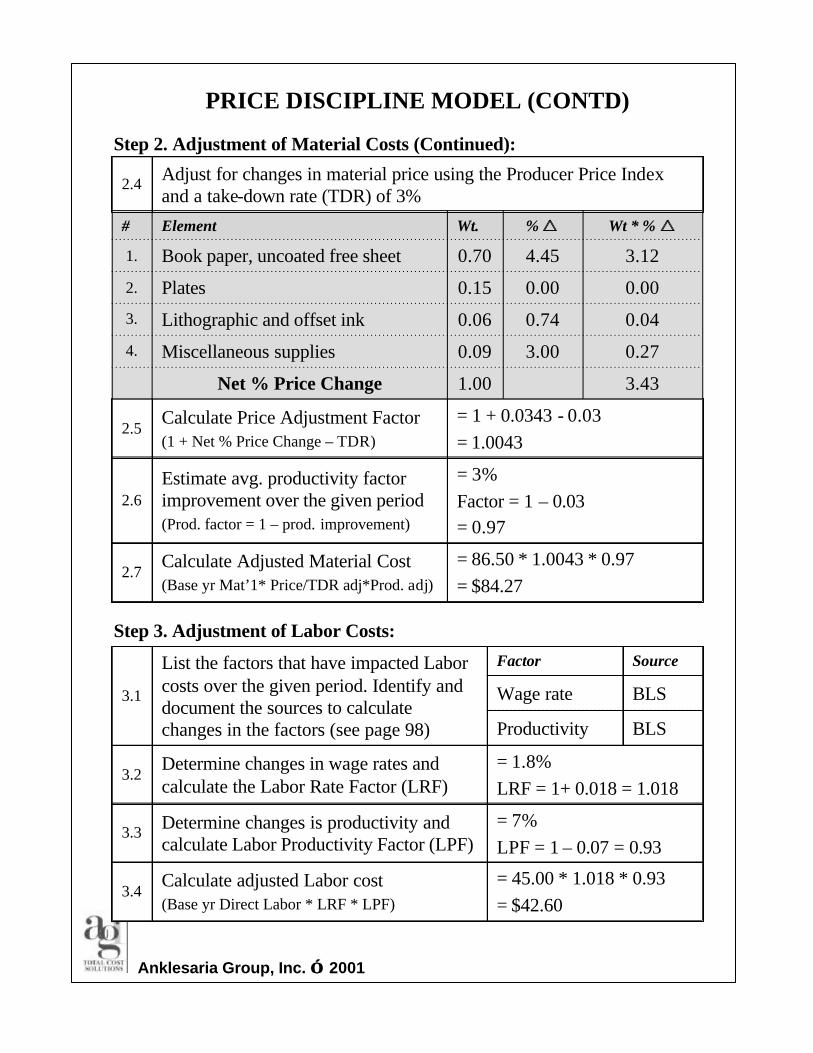

Step 2. Adjustment of Material Costs (Continued):

PRICE DISCIPLINE MODEL (CONTD)

= 86.50 * 1.0043 * 0.97= $84.27

Calculate Adjusted Material Cost(Base yr Mat’1* Price/TDR adj*Prod. adj)

2.7

= 3%Factor = 1 – 0.03= 0.97

Estimate avg. productivity factor improvement over the given period(Prod. factor = 1 – prod. improvement)

2.6

= 1 + 0.0343 - 0.03= 1.0043

Calculate Price Adjustment Factor(1 + Net % Price Change – TDR)

2.5

3.431.00Net % Price Change

0.273.000.09Miscellaneous supplies4.

0.040.740.06Lithographic and offset ink 3.

0.000.000.15Plates2.

3.124.450.70Book paper, uncoated free sheet1.

Wt * % rr% rrWt.Element#

Adjust for changes in material price using the Producer Price Index and a take-down rate (TDR) of 3%

2.4

Step 3. Adjustment of Labor Costs:

= 45.00 * 1.018 * 0.93= $42.60

Calculate adjusted Labor cost(Base yr Direct Labor * LRF * LPF)

3.4

= 7%LPF = 1 – 0.07 = 0.93

Determine changes is productivity and calculate Labor Productivity Factor (LPF)

3.3

= 1.8%LRF = 1+ 0.018 = 1.018

Determine changes in wage rates and calculate the Labor Rate Factor (LRF)

3.2

BLSProductivity

BLSWage rate

SourceFactorList the factors that have impacted Labor costs over the given period. Identify and document the sources to calculate changes in the factors (see page 98)

3.1

Anklesaria Group, Inc. 2001

Step 4. Adjustment of Manufacturing OH and Operating & Other Exp:

54.25

11.1810.85

43.40

(1.03)1

(1.03)1 29.80

1

10/15

Fixed 80%

Variable 20%

Base Yr OH

Adjusted Factory OH =

No volume adj

Volume (BV/CV)*Inflation adj.

Inflation adj

* * =

* * =

+

40.98* BV = Base Volume

CV = Current Volume

Manufacturing OH Adjustment

53.50

5.515.35

48.15

(1.03)1

(1.03)1 33.06

1

10/15

Fixed 90%

Variable 10%

Base Yr OH

Adjusted O & O Exp. =

No volume adj

Volume (BV/CV)*Inflation adj.

Inflation adj

* * =

* * =

+

38.57* BV = Base Volume

CV = Current Volume

Operating & Other Exp. Adjustment

PRICE DISCIPLINE MODEL (CONTD)

Adjust MOH and O&O Expenses as shown below4.3

= 3%Determine inflation rate for OH4.2

MOH = 80% F; 20% VO&O = 90 F; 10% VThis is a rule of thumb for Product Overhead

Determine the mix between Fixed and Variable OH for both Manufacturing Overhead and Operating & Other Expenses

4.1

Anklesaria Group, Inc. 2001

PRICE DISCIPLINE™

SIC Code 2752: Commercial Printing, LithographicSummary

Adjusted for price and productivity changes, and TDR 84.2786.50Direct Material

217.17250.00SHOULD COST

Profit $ kept constant10.7510.75Profit Before Taxes

Adjusted for inflation, Fixed OH for volume38.5753.50Operating & Oth. Exp.

167.85185.75Cost of Goods Sold

Adjusted for inflation, Fixed OH for volume40.9854.25Manufacturing OH

Adjusted for changes in wage rates and productivity42.6045.00Direct Labor

Source20012000Element

Anklesaria Group, Inc. 2001

BUILDING COST MODELS QUICKLY WITH

u Makes life easier for the procurement professionalu Provides a cost breakdown for any product or service in

minutes u Designed in Excel with user-friendly interface (buttons, pop-

up windows, menus, etc.)u Preloaded with:Ø SIC and NAICS codesØ Economic Census DataØ Industry Financial Ratios

u Direct hyperlinks to free web sites where buyers can retrieve relevant company-specific and industry data

Anklesaria Group, Inc. 2001

UNDERSTANDING OVERHEADTYPES OF COST

Based on Allocationu Direct Costs (Costs that can be traced to a product)u Indirect Costs (Costs that cannot be traced to a product)

Based on Behavior (reaction to volume changes)u FixedØConstant in total, vary per unit; as volume changes

ØCommittedã Costs committed for a period of time (building lease)

ØDiscretionaryã Amounts left to management discretion (advertising)

u VariableØConstant per unit, vary in total; as volume changes

Anklesaria Group, Inc. 2001

DETERMINING OVERHEAD RATES

Capacity = 1MM hrsUtilization = 80%

Overhead rate - $1.25/hr($1MM / 800,000)

OVERHEAD POOL (E.g. $1,000,000)

OVERHEAD BASE (E.g. LABOR HOURS – 800,000)

Product ALabor hrs = 3OH = $3.75

Product BLabor hrs = 8OH = $10.00

Product CLabor hrs = 5OH = $6.25

Product DLabor hrs = 4OH = $5.00

Anklesaria Group, Inc. 2001

ALLOCATING OVERHEAD

u Allocation of indirect costs using one or more allocation basesØ Job/Process CostingØ Standard CostingØ Activity Based CostingØ Process Based Costing

u Based on estimates made at the beginning of the year

u Markups on non-value-added activities is a cancer that is killing previously profitable companies

Anklesaria Group, Inc. 2001

No change in material costMOH = 200% of Direct LaborO&O Exp. = 25% of COGSProfit = 10% of Total Cost Wage Rate = $15 per hour

A $15 increase/decrease in labor of Supplier #1 magnifies to $117.00 for end customer

Assumptions:

MAGNIFICATION OF COST

$117.00$85.09$61.88Loaded Cost

10.647.745.63Profit

106.3677.3556.25Total Cost

21.2715.4711.25Operating & Other Exp.

85.0961.8845.00Cost of Goods Sold

N/CN/C30.00Manufacturing OH

N/CN/C$15.00Labor

$85.09$61.88N/CMaterial

Supplier#3Supplier#2Supplier#1

Anklesaria Group, Inc. 2001

TOTAL COST OF OWNERSHIP MODEL

Application:u Evaluate purchase optionsu Make effective sourcing decisionsu Make vs. Buy decisionsu Determine the overall financial impact of

changes in activityu Understand and measure all costs incurred over

the life of a purchased product/service

TCO: The Present value of all costs associated with a product/service, incurred over its expected life

Anklesaria Group, Inc. 2001

TOTAL COST OF OWNERSHIP

Total Cost of Ownership

Costs incurred in getting the product to customer site, incl. freight, admin costs

Costs incurred in converting purchased part/material into finished product and supporting it through its usable life

Costs incurred in the termination of products’ life, incl. disposal costs, winding down of project costs, etc.

Cost elements that make up the purchase price

Price is only a part of cost

Note: This breakdown is only a guideline. TCO

categories vary depending on the nature of the

product/service

Acquisition Costs

Purchase Price

Usage Costs

End of Life Costs

INHOUSE

COSTS

Anklesaria Group, Inc. 2001

TOTAL COST OF OWNERSHIP MODEL

Assumptions:

u Product Purchased: Desktop PC’su Product Life Cycle: 3 yearsu Volume: 1,000 PC’su Cost of Capital: 12%

Anklesaria Group, Inc. 2001

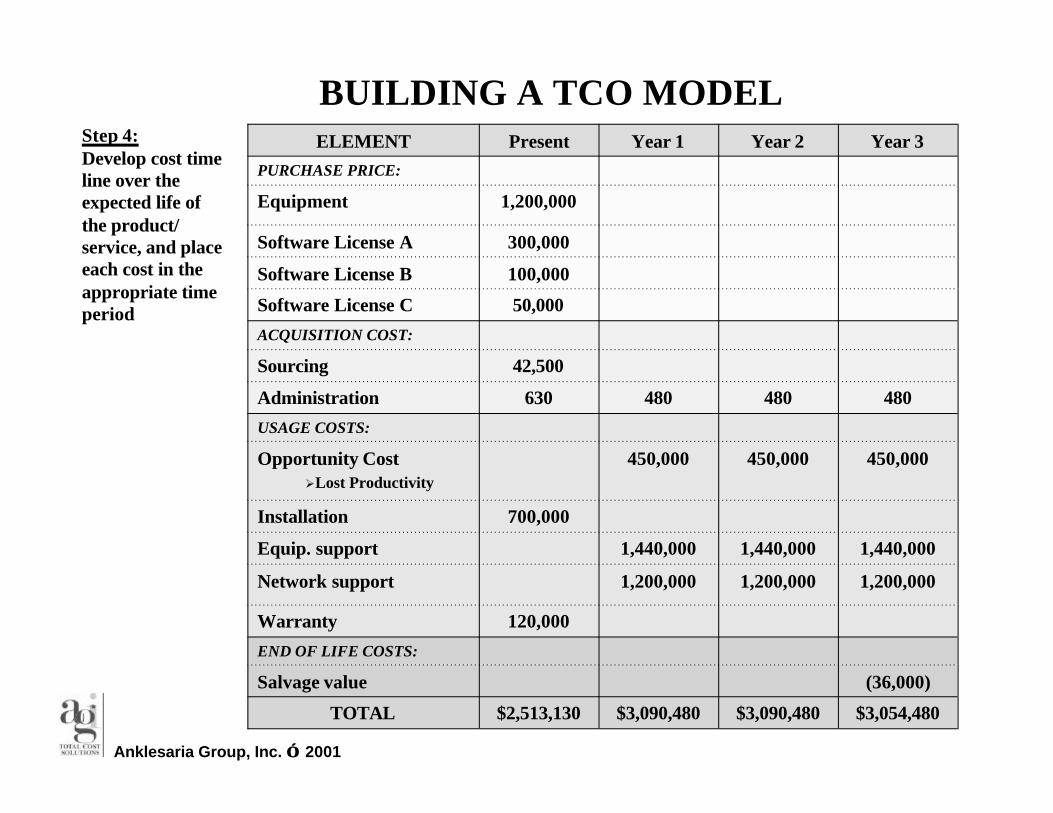

BUILDING A TCO MODEL

END OF LIFE COSTS

USAGE COSTS

ACQUISITION COST

PURCHASE PRICE

ØOpportunity CostØLost ProductivityØLost Sales

END OF LIFE COSTS:

USAGE COSTS:

ØInstallation

ØEquip. support

ØNetwork support

ØWarranty

ACQUISITION COST:

ØSourcing

ØAdministration

PURCHASE PRICE:

ØEquipment

ØSoftware A

ØSoftware B

ØSoftware C

ØSalvage value

Step 1: Construct a broad process map of the activities associated with “owning” the product/service and determine categories for the TCO

Step 2:List the cost elements under each category

Anklesaria Group, Inc. 2001

BUILDING A TCO MODEL

Downtime 15 hrs/PC per yr @ $30/hrRØOpportunity CostØLost Productivity

MEASURER/OELEMENT

ØSalvage value

END OF LIFE COSTS:

ØWarranty

ØNetwork support

ØEquipment support

ØInstallation

USAGE COSTS:

ØAdministration

ØSourcing

ACQUISITION COST:

ØSoftware License C

ØSoftware License B

ØSoftware License A

ØEquipment

PURCHASE PRICE:

O

O

R

R

O

R

R

O

O

O

O

$700/PC includes PC move, install and network

$120/month/PC – supplier quote

$100/month – supplier quote

$120/PC for 3 year warranty

2 FTE @ $70K and $120K for 3 months

1 PO @ $150 and 12 invoices @ $40 each

Supplier quote ($1,200 per PC)

Supplier quote ($300 per PC)

Supplier quote ($100 per PC)

Supplier quote ($150 per PC)

$36 per PC

Step 3:Determine if each cost element is recurring (R) or one-time (O) and identify how each element is to be measured

Anklesaria Group, Inc. 2001

BUILDING A TCO MODEL

450,000450,000450,000Opportunity CostØLost Productivity

$3,054,480$3,090,480$3,090,480$2,513,130TOTAL

120,000

700,000

630

42,500

50,000

100,000

300,000

1,200,000

Present

1,200,000

1,440,000

480

Year 1

1,200,000

1,440,000

480

Year 2

(36,000)

1,200,000

1,440,000

480

Year 3ELEMENT

Salvage value

END OF LIFE COSTS:

Warranty

Network support

Equip. support

Installation

USAGE COSTS:

Administration

Sourcing

ACQUISITION COST:

Software License C

Software License B

Software License A

Equipment

PURCHASE PRICE:

Step 4:Develop cost time line over the expected life of the product/ service, and place each cost in the appropriate time period

Anklesaria Group, Inc. 2001

BUILDING A TCO MODEL

$3,054,480$3,090,480$3,090,480$2,513,130TOTAL

Present Year 1 Year 2 Year 3Time

Step 5:Calculate Present Value Interest Factors (PVIF) for each year, using your firm’s Cost of Capital (12%)(See table on page 102)

0.7120.7970.8931

$2,174,790$2,463,113$2,759,799$2,513,130

Step 6:Calculate Present Values(Total * PVIF)

Step 7:Calculate Total Cost of Ownership(Sum of Present Values in Step 6) $9,910,832

Anklesaria Group, Inc. 2001

TOTAL COST OF OWNERSHIP EXAMPLE

Purchase Price 1,650K

Acquisition 44K

Usage 8,242K

EOL (26K)

Product life cycle

Source: Anklesaria Group, Inc.TCO for Desktop PC’s

Present values

Anklesaria Group, Inc. 2001

PROFITABILITY: THE KEY TO COMPETITIVENESS

u Acknowledge the need for suppliers to make a reasonable profit early in the process

u Profit should be discussed when it becomes a “critical” cost

u Profit should be based on risk and value addedu Select appropriate profit option:

Ø Current supplier profit marginØ Industry marginØ Industry margin plus premiumØ Current absolute per unit dollarsØ Current total dollars (ROIC)

IMPLEMENTING STRATEGIC COST MANAGEMENT

Anklesaria Group, Inc. 2001

IMPLEMENTATION

u Review material presented in this manualu Create an Intelligence Cellu Identify as many sources of data to build a cost

modelsu Communicate new strategy through the supply

chainu Reward suppliers that cooperateu Document & Publicize savings

Anklesaria Group, Inc. 2001

THE NEXT STEP

u Identify key suppliers/commoditiesu Engage in SCM techniquesu Determine readiness for strategy buildingu Establish initial team membersu Develop and deploy AIM&DRIVE®

strategies

Anklesaria Group, Inc. 2001

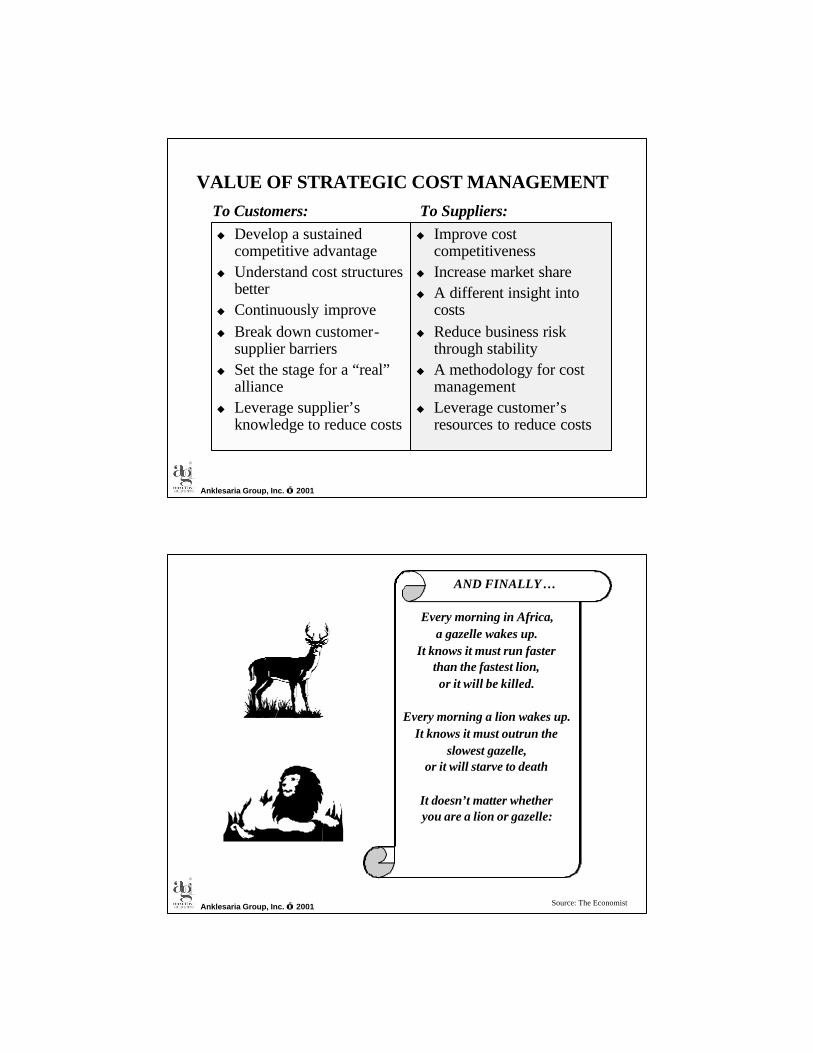

VALUE OF STRATEGIC COST MANAGEMENT

u Develop a sustained competitive advantage

u Understand cost structures better

u Continuously improveu Break down customer-

supplier barriers u Set the stage for a “real”

allianceu Leverage supplier’s

knowledge to reduce costs

u Improve cost competitiveness

u Increase market shareu A different insight into

costsu Reduce business risk

through stabilityu A methodology for cost

managementu Leverage customer’s

resources to reduce costs

To Customers: To Suppliers:

Anklesaria Group, Inc. 2001

AND FINALLY…

Every morning in Africa,a gazelle wakes up.

It knows it must run fasterthan the fastest lion,or it will be killed.

Every morning a lion wakes up.It knows it must outrun the

slowest gazelle,or it will starve to death

It doesn’t matter whether you are a lion or gazelle:

Source: The Economist

Anklesaria Group, Inc. 2001

WHEN THE SUN COMES UP

YOU HAD BETTER BE RUNNING

EXERCISES

Anklesaria Group, Inc. 2001

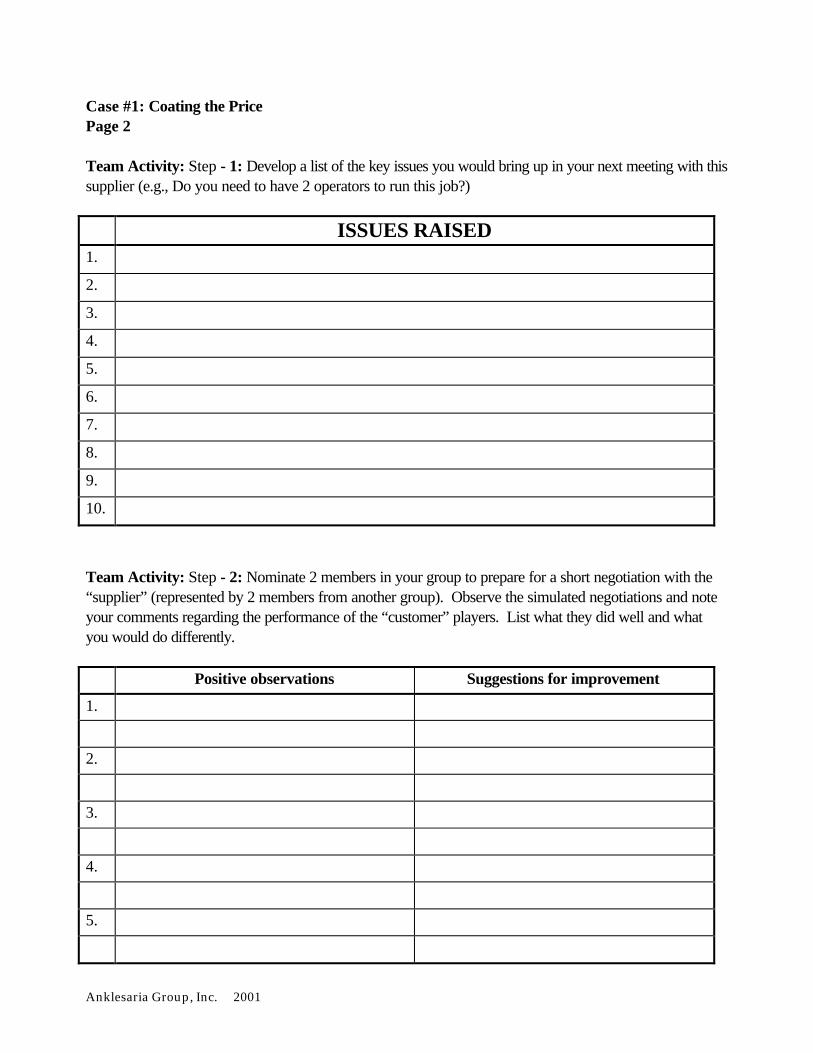

CASE #1 Coating the Price

A year ago, you entered into an indefinite quantity contract for coated plastic made to your specification. With experience you are now able to estimate, fairly accurately, that your requirement per month will be 4 million feet. The product that uses the plastic you are buying is doing very well in the market and is expected to have a life of at least three more years. However, customers are applying a lot of pressure on your salespeople to reduce the market price of the finished product to less than $275. This plastic is the main raw material used in the product and constitutes about 27 percent of the total selling price of $325. Hence the pressure is on the purchasing department to find ways to reduce the cost of raw material. You requested the current supplier to quote, together with supporting cost data, for a 12 month extension. The initial cost breakdown and data for the extension is shown below. The sales rep has pointed out that while costs have gone up in most cases, only $0.21, or 0.24%, has been passed on to you.

Cost Breakdown for coated plastic $ per thousand feet Current Proposed Raw Materials Plastic: $2.00/lb., 90% yield $ 57.00 $ 57.00 Coating: 90% yield 5.55 5.55 Total material cost $ 62.55 $ 62.55 Conversion Costs Labor (@10,500 feet/hr.) 2 operators x $20 (proposed labor: $21) 3.78 3.97 Machine Cost: $33.33/hour/10.5 3.17 3.17 Packaging .81 .81 Total conversion cost 7.76 7.95 Overhead Engineering 3.85 3.85 Manufacturing 1.15 1.15 General & Administrative 2.50 2.50 Selling 2.05 2.05 Total overhead 9.55 9.55 Profit 7.98 8.00 Selling Price (Total material + Conversion + Overhead + Profit) $ 87.84 $ 88.05 ====== ======

Anklesaria Group, Inc. 2001

Case #1: Coating the Price Page 2 Team Activity: Step - 1: Develop a list of the key issues you would bring up in your next meeting with this supplier (e.g., Do you need to have 2 operators to run this job?) ISSUES RAISED

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

Team Activity: Step - 2: Nominate 2 members in your group to prepare for a short negotiation with the “supplier” (represented by 2 members from another group). Observe the simulated negotiations and note your comments regarding the performance of the “customer” players. List what they did well and what you would do differently. Positive observations Suggestions for improvement

1.

2.

3.

4.

5.

Anklesaria Group, Inc. 2001

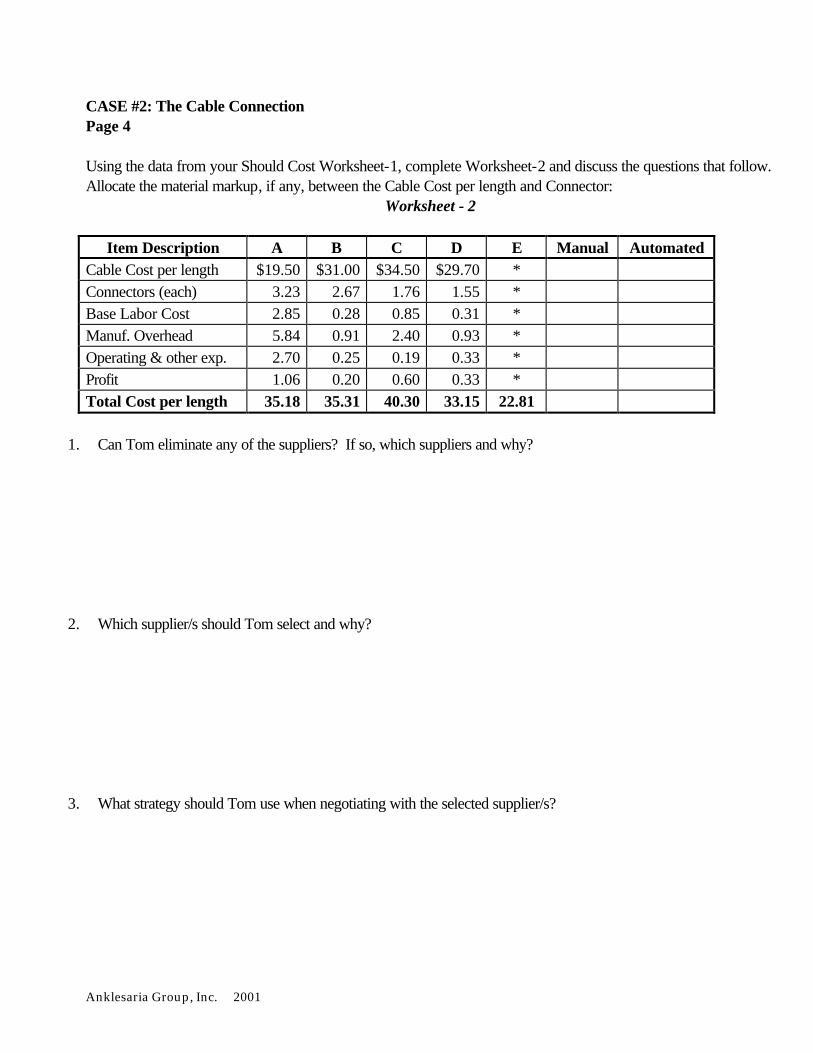

CASE #2 The Cable Connection: Should Cost Models

Tom Mazzone is a senior contract manager of Advanced Telecommunications. He had recently sent out a request for quotation for special connectorized cable. The cables are to be used in a very expensive and sophisticated switching system for a major telephone company. Success on this program could well mean many more such jobs for the company internationally. The selected supplier would need to be capable of meeting the increase in demand overseas as well as the inherent nuances of international business. Key points of the requirements are summarized below. Materials Cable A: 24.75 million feet, averaging 150 feet per length Male connector: one per length of cable Total number of connectors: 165,000 Specifications 25 pair cable; 24 g.a., ICC or equivalent Cable insulation: must have an oxygen index of 28% or better A week later, Tom received the following quotes, which are summarized below.

Item Description

Supplier A

Supplier B

Supplier C

Supplier D

Supplier E

Cable Cost per length $ 19.50 $ 31.00 $ 34.50 $ 29.70 * Connectors (each) 3.23 2.67 1.76 1.55 * Base Labor Cost 2.85 0.28 0.85 0.31 * Manuf. Overhead 5.84 0.91 2.40 0.93 * Operating & other exp. 2.70 0.25 0.19 0.33 * Profit 1.06 0.20 0.60 0.33 * Total Cost per length 35.18 35.31 40.30 33.15 22.81 * Supplier E quoted only a total cost per length. No breakdown was provided. In order to process the proposals, Tom decided to do a little homework. He first called one of the major suppliers of male connectors in Chicago and asked for a price based on 200,000 standard male connectors. The price quoted to him was $2.61 each on quantities below 100,000 pieces; $2.10 on quantities between 100,000 and 200,000; and $1.71 each on quantities of 200,000 or more. Tom realized that these prices could be further negotiated if he were a serious buyer. Besides, Tom feels that suppliers would purchase similar connectors for projects with other customers.

Anklesaria Group, Inc. 2001

CASE #2: The Cable Connection Page 2 Next, Tom called ICC, the country's leading manufacturer of this kind of cable. The prices provided were $0.1832 per foot. These prices were available to Advanced Telecommunication only because of the special relationship between the two companies. ICC usually charges a premium of 10 to 20 percent more to other companies, who in turn further add a markup of 2-15%, depending on the value added. Tom tried to get ICC to quote on the entire job, but was told that the company did not wish to take on that type of contract. ICC was willing to sell the cable to a selected supplier of Advanced at the preferred rate of $0.1832 per foot. However, the suppliers are not aware of this. In order to understand the labor contribution to cost, Tom called the engineer at Advanced, Margaret Teacher, who was familiar with the connectorization process. After reviewing the specifications, Margaret indicated that she knew of some studies that had been performed to evaluate the time standards for similar requirements. Her feeling was that the maximum time to connectorize 25 pair cable would be 15 minutes per cable (4 cables per hour). She pointed out that by using an automated system, the output could be improved to 1.5 minutes per cable (40 cables per hour). Referring to the Department of Labor Area Wage Surveys for the skill level required, Tom determined the labor to be $10.00 per hour. Next, Tom pulled out the files of the respective suppliers. In the past, all of them had dealt with Advanced Telecommunications without any major problem. Companies B, C and D were all large companies (between $40-50 million in asset size with around 750 to 1,000 production workers), while A and E, both between $15 and $20 million companies, had only recently diversified into cable assembly. These companies employed less than 250 production workers. Tom called Supplier E to verify if it really understood the requirement, and also to provide a cost breakdown. The sales representative said that she believed the quote was correct and that it was against company policy to share cost data. No samples were available to the customer for inspection. However, if Tom wished, he could purchase a minimum of 5,000 cable lengths at a price of $40 per length. If the full order of 165,000 cables were placed within 15 days, the $200,000 paid for the 5,000 cables would be adjusted against the full contract price of $22.81 per length. The hardware and software for the switching system is nearly complete and the cabling will have to be done within the next five weeks. An order would have to be placed fairly soon and the selected supplier would be given no more than three weeks to deliver the entire quantity. * This case is an adaptation of a case by Mark L. Cohen of Pacific Bell.

Anklesaria Group, Inc. 2001

CASE #2: The Cable Connection Page 3

Worksheet - 1

Based on the information above, develop a Should Cost model for special connectorized cable. The

information provided below the worksheet will help you in your calculations. Please note that this is a service should cost, so material costs have been calculated separately.

$ per length # Cost Element

Manual Automated 1 Direct Labor (Hourly wage rate ÷ # of cables per hr)

2 Overhead {see information (a) below}

3 Sub-total: Loaded labor Cost

4 GS&A {see information (b) below}

5 Sub-total: Total Cost (Loaded labor + GS&A)

6 Profit {see information (c) below}

7 Cost excluding mat’l (Total Cost + Profit)

8 Material Cost (ICC quote)

9 Connector (enquiry from Chicago)

10 Material Markup (Procurement OH) (use your discretion)

TOTAL SHOULD COST (Lines 7+8+9+10)

The following information has been obtained for SIC Code 3496 (misc. fabricated wire products):

a) Overhead as a percentage of direct labor (Pacific Bell study) for assembly Manual = 100% Semi-automated = 100-200% Automated = 225-400%

b) GS&A as a percentage of Loaded Labor Cost (RMA, 2000) $500K-2 mil. in assets = 35.3% $2-10 mil. in assets = 28.5% $10-50 mil. = 28%

c)Profit as a percentage of Total Cost (RMA, 2000) $500K-2 mil. in assets = 3.3% $2-10 mil. in assets = 5.4% $10-50 mil. = 8.7%

Anklesaria Group, Inc. 2001

CASE #2: The Cable Connection Page 4 Using the data from your Should Cost Worksheet-1, complete Worksheet-2 and discuss the questions that follow. Allocate the material markup, if any, between the Cable Cost per length and Connector:

Worksheet - 2

Item Description A B C D E Manual Automated Cable Cost per length $19.50 $31.00 $34.50 $29.70 * Connectors (each) 3.23 2.67 1.76 1.55 * Base Labor Cost 2.85 0.28 0.85 0.31 * Manuf. Overhead 5.84 0.91 2.40 0.93 * Operating & other exp. 2.70 0.25 0.19 0.33 * Profit 1.06 0.20 0.60 0.33 * Total Cost per length 35.18 35.31 40.30 33.15 22.81

1. Can Tom eliminate any of the suppliers? If so, which suppliers and why? 2. Which supplier/s should Tom select and why? 3. What strategy should Tom use when negotiating with the selected supplier/s?

Anklesaria Group, Inc. 2001

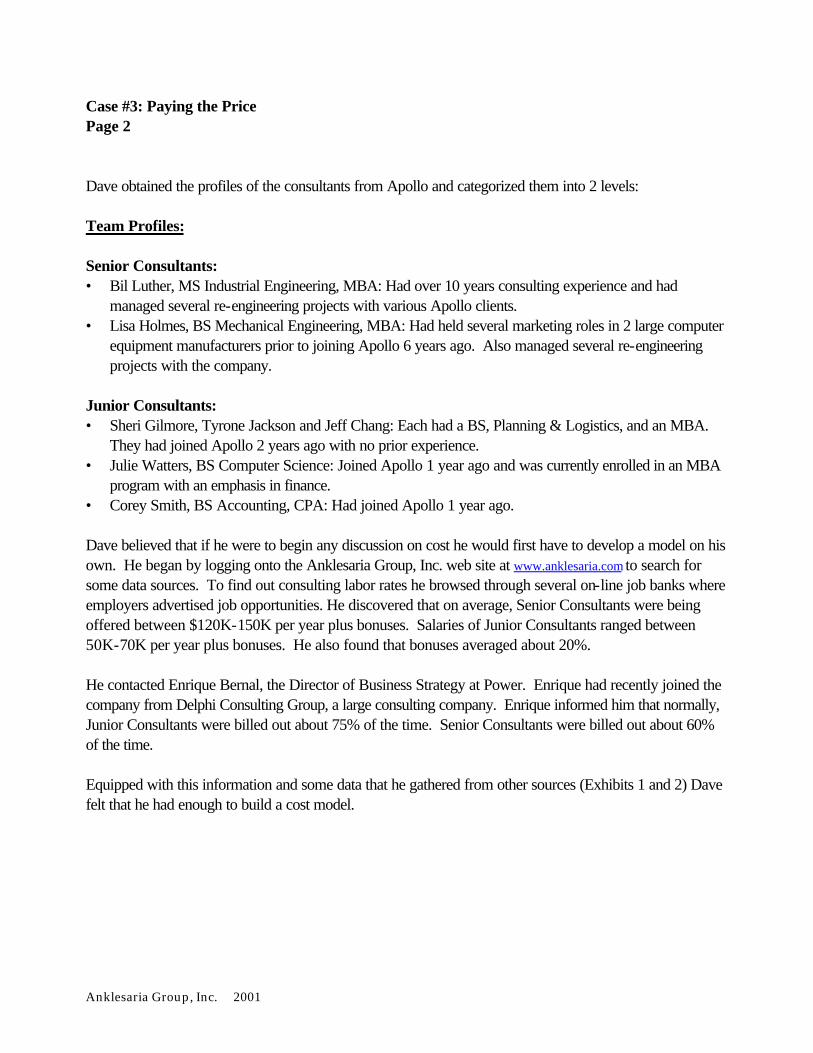

Paying the Price CASE # 3

Dave Matthews had recently joined Power Machine Corp., New York, as Senior Procurement Manager and was faced with a daunting task. He had been requested by Sandra Palmer, the Director of Marketing Operations, to help her obtain the services of a consultant to evaluate and re-engineer the company’s logistics department. There had been a significant reshuffle at the top and the incoming management team had established a 20% company-wide cost reduction target. Over the years Power had utilized the services of several consultants for various projects ranging from benchmarking studies to process re-engineering . Consulting contracts were traditionally put out to bid. On several occasions, Apollo Consulting, a large established management consulting firm headquartered in Chicago, IL had won the bid. Jan Thompson, Dave's predecessor had sent out several RFQ for the project prior to leaving. The responses Dave received were as follows: Supplier Days Contract Amount Apollo Consulting 30 600,000 Henderson Consulting 30 620,000 Carney & Co. 32 630,000 Aquarius Consulting 35 650,000 This was the first time Henderson, Carney and Aquarius had bid on a Power contract. Dave called Henry Dawson, the account manager at Henderson. Henry informed him that it would be impossible for him to lower the contract amount any further. He said that the project would involve a significant initial scope study. This would take about 6 days. It would involve a detailed evaluation of the company's existing organizational structure and operations, and would entail a round of in-depth interviews with several key business managers. Since this was the first time Henderson was involved with Power this would have to be done in great detail. Dave verified this with the account managers at Carney and Aquarius. Apollo had recently completed a large project for Power's manufacturing operation, which included a scope study and may not have to conduct another one. Dave then contacted Steve Lindsey, the Account Executive at Apollo. Steve provided him with the following breakdown team profiles: Project time – 30 days Resource requirements – 2 Senior Consultants, 5 Junior Consultants. Fee Structure: 2 Senior Consultants @ $4,000/day each = $240,000 5 Junior Consultants @ 2,400/day each = $360,000 TOTAL FEE: = $600,000

Anklesaria Group, Inc. 2001

Case #3: Paying the Price Page 2 Dave obtained the profiles of the consultants from Apollo and categorized them into 2 levels: Team Profiles: Senior Consultants: • Bil Luther, MS Industrial Engineering, MBA: Had over 10 years consulting experience and had

managed several re-engineering projects with various Apollo clients. • Lisa Holmes, BS Mechanical Engineering, MBA: Had held several marketing roles in 2 large computer

equipment manufacturers prior to joining Apollo 6 years ago. Also managed several re-engineering projects with the company.

Junior Consultants: • Sheri Gilmore, Tyrone Jackson and Jeff Chang: Each had a BS, Planning & Logistics, and an MBA.

They had joined Apollo 2 years ago with no prior experience. • Julie Watters, BS Computer Science: Joined Apollo 1 year ago and was currently enrolled in an MBA

program with an emphasis in finance. • Corey Smith, BS Accounting, CPA: Had joined Apollo 1 year ago. Dave believed that if he were to begin any discussion on cost he would first have to develop a model on his own. He began by logging onto the Anklesaria Group, Inc. web site at www.anklesaria.com to search for some data sources. To find out consulting labor rates he browsed through several on-line job banks where employers advertised job opportunities. He discovered that on average, Senior Consultants were being offered between $120K-150K per year plus bonuses. Salaries of Junior Consultants ranged between 50K-70K per year plus bonuses. He also found that bonuses averaged about 20%. He contacted Enrique Bernal, the Director of Business Strategy at Power. Enrique had recently joined the company from Delphi Consulting Group, a large consulting company. Enrique informed him that normally, Junior Consultants were billed out about 75% of the time. Senior Consultants were billed out about 60% of the time. Equipped with this information and some data that he gathered from other sources (Exhibits 1 and 2) Dave felt that he had enough to build a cost model.

Anklesaria Group, Inc. 2001

Case #3: Paying the Price Page 3 Exhibit 1: Source: Dun & Bradstreet Key Norms and Financial Ratios (1999-00): SIC 8742, Management Consulting Services

Item $ % Net Sales 1,500,000 100 Gross Profit 636,000 45.4 Net Profit After Tax 105,000 7.3 Exhibit 2: Source: U.S. Bureau of Census, 1997 Economic Census – Professional, Scientific & Tech. Services Geographical Area Series – Chicago, Illinois NAICS 541614 Process, physical distribution and logistics consulting services

Anklesaria Group, Inc. 2001

Case #3: Paying the Price Page 4 Exhibit 3:

Industry Total 1061240 100.00 20.45 21702358 100

Managerial & Administrative 223080 20.91 31.87 7109560 33% XFinancial Managers 21030 1.97 33.83 711445 3.28%Personnel, Training & Labor Relations Managers 7910 0.74 26.19 207163 0.95%Purchasing Managers 2480 0.23 21.45 53196 0.25%Marketing/Advertising/Public Relations Managers 23190 2.17 29.04 673438 3.10%Administrative Managers 22690 2.13 23.47 532534 2.45%Engineering, Mathematical & Natural Sciences Managers 10640 1.00 34.37 365697 1.69%Health Services Managers 660 0.06 27.88 18401 0.08%Industrial Production Managers 110 0.01 28.50 3135 0.01%Construction Managers 9210 0.86 28.72 264511 1.22%Communications/Transportation & Utilities Managers 480 0.05 30.47 14626 0.07%Food Service/Lodging Managers 780 0.07 22.74 17737 0.08%Other Services Managers 960 0.09 19.22 18451 0.09%General Managers & Top Executives 85280 8.00 38.06 3245757 14.96%All Other Managers & Administrators 37660 3.53 26.13 984056 4.53%

Professional/Paraprofessional & Technical Occupations 373180 34.96 23.38 8724948 40% XSales & Related Occupations 63580 5.96 17.35 1103113 5.08%Clerical & Administrative Support 246440 23.13 12.05 2969602 13.68%Service Occupations 65650 6.16 8.70 571155 2.63%Agricultural, Forestry, Fishing & Related 5770 0.54 9.98 57585 0.27%Product/Construct/Operate Maintenance/Material Handling 83540 7.70 13.90 1161206 5.35%

SIC Code - 874(Management & Public Relations) Industry-Occupation-Wage Matrix

Salary Dist

Direct LaborOccupation Title

No. of Employees

Mean Salary

Total Salary

Emp.Dist

Anklesaria Group, Inc. 2001

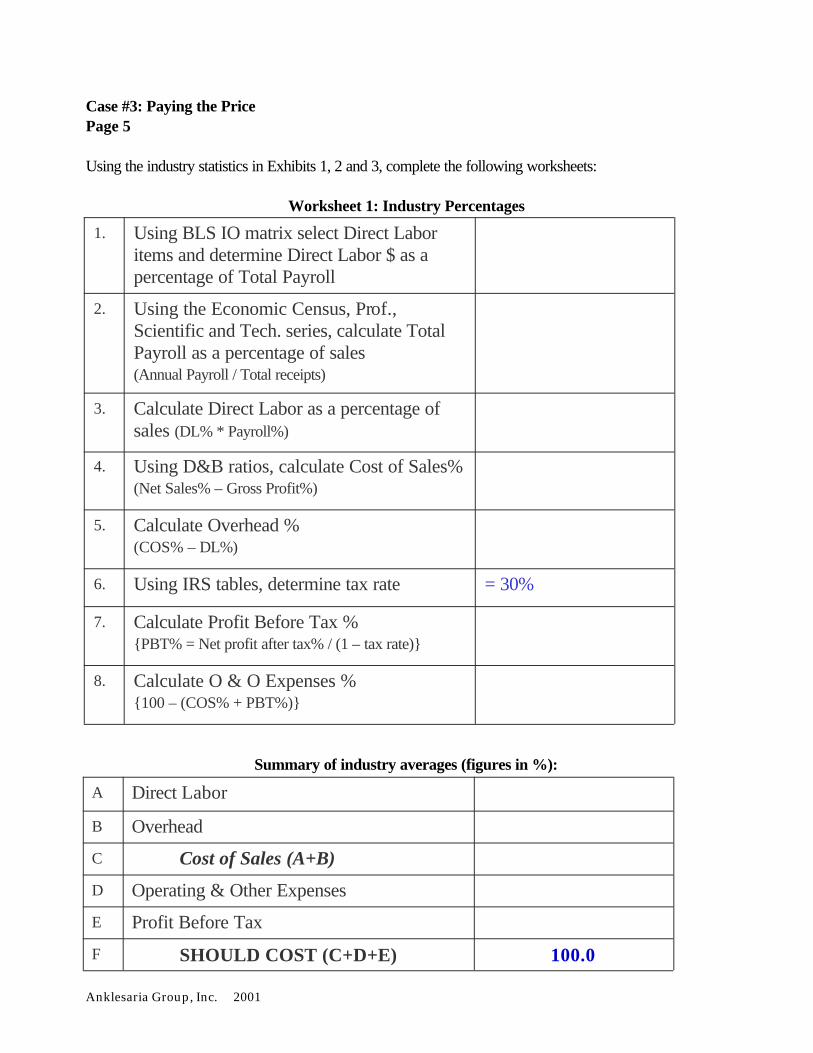

Case #3: Paying the Price Page 5 Using the industry statistics in Exhibits 1, 2 and 3, complete the following worksheets:

Worksheet 1: Industry Percentages

Summary of industry averages (figures in %):

Calculate Profit Before Tax % {PBT% = Net profit after tax% / (1 – tax rate)}

7.

Calculate O & O Expenses % {100 – (COS% + PBT%)}

8.

Calculate Overhead % (COS% – DL%)

5.

= 30% Using IRS tables, determine tax rate 6.

Calculate Direct Labor as a percentage of sales (DL% * Payroll%)

3.

Using D&B ratios, calculate Cost of Sales% (Net Sales% – Gross Profit%)

4.

Using the Economic Census, Prof., Scientific and Tech. series, calculate Total Payroll as a percentage of sales (Annual Payroll / Total receipts)

2.

Using BLS IO matrix select Direct Labor items and determine Direct Labor $ as a percentage of Total Payroll

1.

Profit Before Tax E

100.0 SHOULD COST (C+D+E) F

Cost of Sales (A+B) C

Operating & Other Expenses D

Overhead B

Direct Labor A

Anklesaria Group, Inc. 2001

Case #3: Paying the Price Page 6

Worksheet 2: Daily Direct Labor costs

Element Sr. Consultant Jr. Consultant

Base Annual Salary (use average)

Bonus

Total Annual Compensation

Percentage of time billed-out

Adjusted Annual Compensation

Number of billable hours in a year (default) 2080 2080

Hourly direct labor cost

Daily direct labor cost (use 8-hour workday)

Worksheet 3: Daily billing rate, using summary of industry averages

Element Sr. Consultant

$/day %

Jr. Consultant $/day

Daily direct labor cost

Overhead

COS (Daily rate + Overhead)

Operating & Other Expenses

Total Cost (COS + O&O Exp.)

Profit Before Taxes (PBT)

SHOULD COST (Total Cost + PBT) 100.0

Worksheet 4: Contract Amount

Resource # of

Consultants Daily billing

Rate

# days (less days for Co.

Evaluation) Total $

Senior Consultant

Junior Consultant

Contract Amount

Anklesaria Group, Inc. 2001

Case #3: Paying the Price Page 7 Questions: 1. What strategy should Dave use to negotiate the contract with Apollo? 2. Nominate two members from your team to participate in a negotiation with Apollo (two members from

another team). Note your observations on the negotiations below.

Anklesaria Group, Inc. 2001

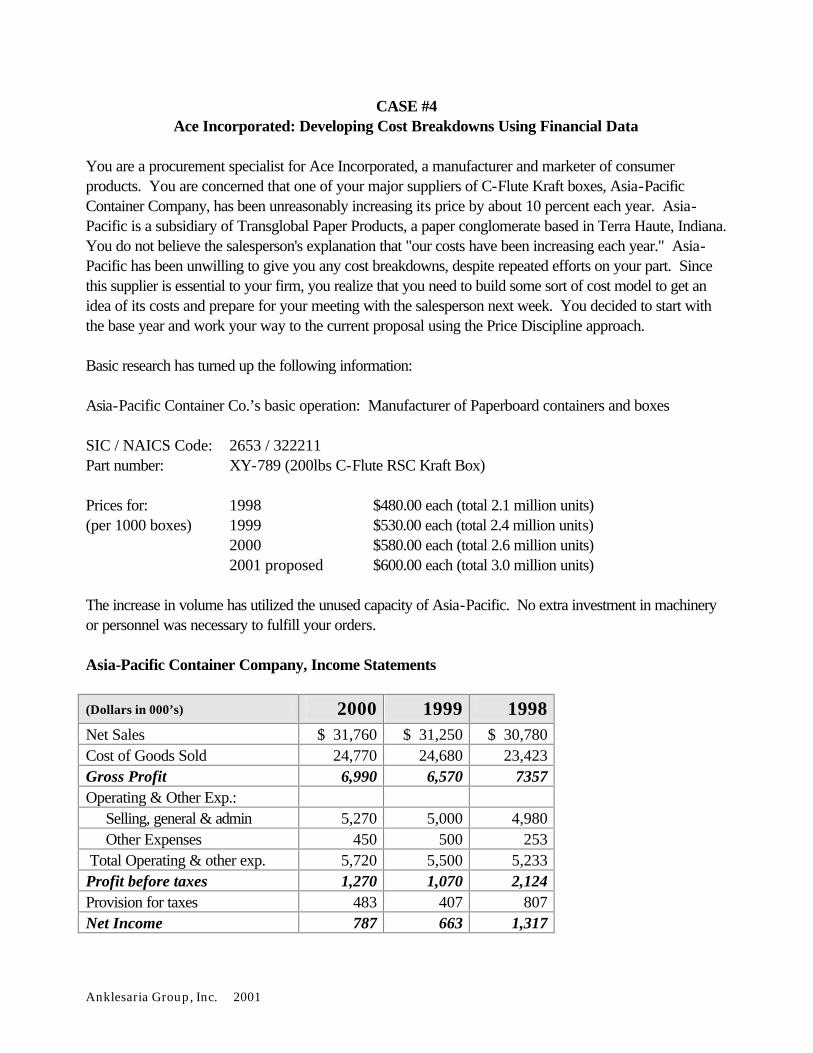

CASE #4 Ace Incorporated: Developing Cost Breakdowns Using Financial Data

You are a procurement specialist for Ace Incorporated, a manufacturer and marketer of consumer products. You are concerned that one of your major suppliers of C-Flute Kraft boxes, Asia-Pacific Container Company, has been unreasonably increasing its price by about 10 percent each year. Asia-Pacific is a subsidiary of Transglobal Paper Products, a paper conglomerate based in Terra Haute, Indiana. You do not believe the salesperson's explanation that "our costs have been increasing each year." Asia-Pacific has been unwilling to give you any cost breakdowns, despite repeated efforts on your part. Since this supplier is essential to your firm, you realize that you need to build some sort of cost model to get an idea of its costs and prepare for your meeting with the salesperson next week. You decided to start with the base year and work your way to the current proposal using the Price Discipline approach. Basic research has turned up the following information: Asia-Pacific Container Co.’s basic operation: Manufacturer of Paperboard containers and boxes SIC / NAICS Code: 2653 / 322211 Part number: XY-789 (200lbs C-Flute RSC Kraft Box) Prices for: 1998 $480.00 each (total 2.1 million units) (per 1000 boxes) 1999 $530.00 each (total 2.4 million units) 2000 $580.00 each (total 2.6 million units) 2001 proposed $600.00 each (total 3.0 million units) The increase in volume has utilized the unused capacity of Asia-Pacific. No extra investment in machinery or personnel was necessary to fulfill your orders. Asia-Pacific Container Company, Income Statements

(Dollars in 000’s) 2000 1999 1998 Net Sales $ 31,760 $ 31,250 $ 30,780 Cost of Goods Sold 24,770 24,680 23,423 Gross Profit 6,990 6,570 7357 Operating & Other Exp.: Selling, general & admin 5,270 5,000 4,980 Other Expenses 450 500 253 Total Operating & other exp. 5,720 5,500 5,233 Profit before taxes 1,270 1,070 2,124 Provision for taxes 483 407 807 Net Income 787 663 1,317

Anklesaria Group, Inc. 2001

CASE #4: Ace Incorporated Page 2 DATA FOR SIC /NAICS CODE 2653 / 322211 (Corrugated and Solid Fiber Boxes) Robert Morris Associates, 1998 Data sorted by $ sales (all numbers are in percent) Note: 1 MM = 1 Million

Income data 1-3MM 3-5MM 5-10MM 10-25MM > 25MM All Sizes

Net Sales 100.0 100.0 100.0 100.0 100.0 100.0 Gross Profit 27.9 28.1 28.1 27.5 25.0 27.5 Operating Exp 24.5 23.2 22.7 21.2 17.6 21.8 Other Expenses 1.7 1.3 0.9 1.0 1.4 1.1 Profit Before Tax 1.8 3.6 4.6 5.3 6.0 4.6

U.S. Bureau of Census, 1997 Economic Census – Manufacturing – Industry Series

Anklesaria Group, Inc. 2001

CASE #4: Ace Incorporated Page 3

Worksheet Step 1: Percentage of Sales (POS)

Using the POS approach, compute each cost element for 2001. To determine the industry averages, use the RMA and ASM data given at the end of the case. For Asia Pacific’s percentages, use the income statement provided in the case. In calculating the material, labor and factory overhead ratios for Asia Pacific, you may assume that the mix between these three costs is in line with the mix in the industry.

Cost Element 1998

Industry Avg (%) 1998

Asia Pacific (%) 1998

Asia Pacific ($) Material

Labor

Manufacturing Overhead

Sub-total (COGS)

Operating & other exp.

Profit

TOTAL 100% 100% $480.00

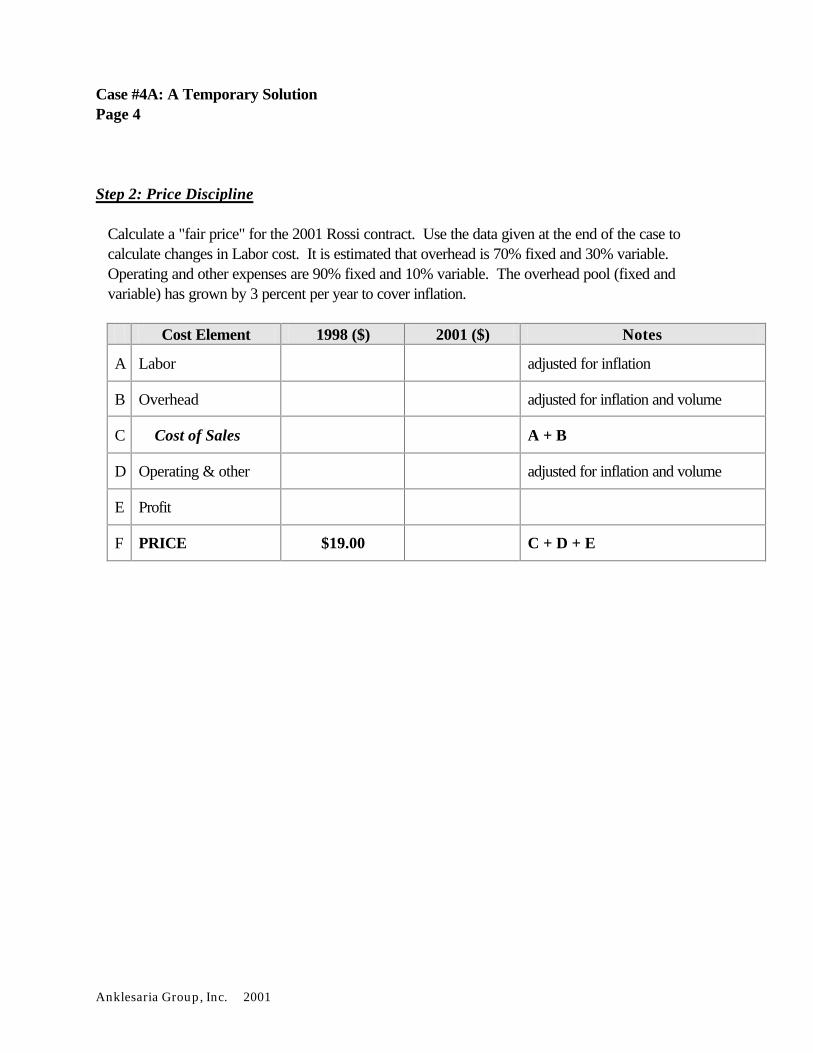

Step 2: Price Discipline

Using 1998 as the base, calculate a "fair price" for part #XY-789 for 2001. Reviewing the PPI for corrugated paperboard, you observed that Asia-Pacific’s raw material prices have increased by an average of 10.51% per year over the past 2 years. Labor rates have shown a 2% increase per year over the same period. You expect a 3% productivity improvement each year in material. The BLS Industry Productivity Index reveals that labor productivity improved by 6.84% per year over the same period. These trends in Material and Labor are expected to continue for the new contract period. It is estimated that manufacturing overhead is 80% fixed and 20% variable. Operating and other expenses are 90% fixed and 10% variable. The overhead pool (fixed and variable) has grown by 3 percent per year to cover inflation of some of the items in the pool.

Cost Element 1998 ($) 2001 ($) Notes 1 Material adjusted for inflation and productivity

2 Labor adjusted for inflation and productivity

3 Manufacturing OH adjusted for inflation and volume

4 Sub-total (COGS) 1 + 2 + 3

5 Operating & other adjusted for inflation and volume

6 Profit

7 TOTAL $480.00 4 + 5 + 6

Anklesaria Group, Inc. 2001

CASE #4: Ace Incorporated Page 4 Based on the results of the above worksheet, please answer the following questions: 1. How will you negotiate the 2001 contract with Asia-Pacific? 2. Assume Asia-Pacific has spare capacity over the short run and you have bought and paid for the 3

million units. You need 250,000 extra units, what price would you be willing to offer per extra unit? Explain. (Since prices are quoted to you per thousand units, do all calculations per thousand units.)

3. What price would you negotiate in case Asia-Pacific had to run the extra 250,000 units using

overtime? Assume that the firm operates only one shift and there is no spare capacity on that shift. Also, running overtime to fill your order will not affect the production schedule on regular runs in the near future.

Anklesaria Group, Inc. 2001

CASE #5 Techno, Inc.: Total Cost of Ownership

Liz Cooper sat at her desk gazing at the mounds of paper that had accumulated around her. She was the Capital Equipment buyer for Techno Inc.’s (TI) semiconductor division. The papers on her desk were all related to the responses she received to an RFP that was sent out to three of Techno’s capital equipment suppliers SeeMos, Inc., Applied Technologies and Trax Inc. A decision had been made to upgrade the Beam Tools that were used in the production of Techno’s highly successful Quasar product line. Sales had greatly exceeded initial expectations and were projected to grow rapidly over the next 5 years. The equipment that was currently being used was almost 5 years old and would not be able to sustain the expected market growth. Also this step of the production process was the one with the longest cycle time. The new machines had much faster throughput rates, which in turn would translate into increased production and sales. The RFP that was sent out to the three suppliers contained a detailed spec. Engineering had already examined the responses for functionality and were satisfied that all three suppliers met the stated requirements. It was now up to Liz to work the numbers out and determine the best option for Techno. This is where her problems began. She did not know how to proceed. She began by putting together a summary of the information she had. Her summary is below: General Information: Present Value Interest Factors @11%: • Purchase volume - 10 Machines Year 1 - 0.901 • Expected life – 5 years Year 2 - 0.812 • Techno’s cost of capital – 11% Year 3 - 0.731

Year 4 - 0.659 Year 5 - 0.593

Existing Equipment: No. of machines 10 Machine Throughput 67 units per hour Uptime 85% Current Total Annual Production 5,000,000 units Production time (maximum capacity) 24/7 (8760 hours a year) Disposal Costs $50,000 per machine Product Info (based on next year sales estimate of 9,900,000 units: Sales Price $23.50 Fixed Costs $7.25 Variable Costs $11.50 Profit $4.75

Anklesaria Group, Inc. 2001

Case Study # 5, page 2 New Equipment Product Summary (all information is per machine)

Details SeeMos, Inc Applied Technologies Trax, Inc. Model Name AC1 XRT-7 Trax 1000 Base Equipment $1,800,000 $1,300,000 $1,700,000 Discount 10% of Base Equipment cost, based on

order of 10 or more 12.5% of Base Equipment cost, based on order of 10 machines

8% of base price

Add-ons to meet TI spec: 1 Chamber $275,000 $220,000 Included Software $60,000 Included Included Drying system $25,000 $10,000 Included

Installation $25,000 $35,000 $25,000 Operating Costs Each machine would require 1.5 FTE

(Full time equivalent). The loaded cost is $100,000 per year

Each machine would require 2 FTE The loaded cost is $140,000 per year

Each machine would require 2 FTE The loaded cost is $120,000 per year

Training $7,500 for year 1 and $5,000 per year thereafter, for the life of the product.

$8,000 for year 1 and $4,000 per year thereafter, for the life of the product.

$9,000 for year 1 and $6,000 per year thereafter, for the life of the product.

Service/Maintenance $4,250 per month $5,750 per month $5,250 per month Freight to TI Included in equipment price $5,000 $7,500 Warranty 12 months parts and labor. Extended

Warranty of $200,000 for 5 years. This amount is due on delivery of the machines.

24 months parts and labor. Extended Warranty of $300,000 for 5 years. This amount is due on delivery of the machines.

24 months parts and labor. Extended Warranty of $250,000 for 5 years. This amount is due on delivery of the machines.

Delivery lead time 98 days 42 days 28 days Machine Uptime 93% 90% 90% Machine Throughput 122 units per hour 122 units per hour 120 units per hour Salvage value after 5 yrs $50,000 $50,000 $50,000

Anklesaria Group, Inc. 2001

Case Study # 5, page 3

Using the information Liz gathered, complete the following worksheets

Worksheet 1: SeeMos, Inc. - Total Cost of Ownership

Cost Element Year 0 (Now) Year 1 Year 2 Year 3 Year 4 Year 5

Acquisition Costs: Base Equip (less disc.) Additional chamber Software Drying system Freight Costs of Use: Disposal of current equip. Installation Training Operating costs Service/maintenance Extended warranty Opportunity costs (if any) End of Life Costs: Salvage value

TOTAL (sub-total of Acq costs, Cost of use, and EOL)

Present Value (enter the Present Value of each year’s total

in the appropriate box)

TCO: (Sum of all Present Values)

Anklesaria Group, Inc. 2001

Case Study # 5, page 4

Worksheet 2: Applied Technologies - Total Cost of Ownership

Cost Element Year 0 (Now) Year 1 Year 2 Year 3 Year 4 Year 5 Acquisition Costs: Base Equip (less disc.) Additional chamber Software Drying system Freight Costs of Use: Disposal of current equip. Installation Training Operating costs Service/maintenance Extended warranty Opportunity costs (if any) End of Life Costs: Salvage value

TOTAL (sub-total of Acq costs, Cost of use, and EOL)

Present Value (enter the Present Value of each year’s total

in the appropriate box)

TCO: (Sum of all Present Values)

Anklesaria Group, Inc. 2001

Case Study # 5, page 5 Worksheet 3: Trax, Inc. - Total Cost of Ownership

Cost Element Year 0 (Now) Year 1 Year 2 Year 3 Year 4 Year 5

Acquisition Costs: Base Equip (less disc.) Additional chamber Software Drying system Freight Costs of Use: Disposal of current equip. Installation Training Operating costs Service/maintenance Extended warranty Opportunity costs (if any) End of Life Costs: Salvage value

TOTAL (sub-total of Acq costs, Cost of use, and EOL)

Present Value (enter the Present Value of each year’s total

in the appropriate box)

TCO: (Sum of all Present Values)

Anklesaria Group, Inc. 2001

Case Study #5 Page 6 Questions: 1. Based on your TCO models, which supplier/s would you suggest Liz select? Explain your reasons 2. What points would you raise in your negotiations with the selected supplier?

OPTIONAL EXERCISES

Anklesaria Group, Inc. 2001

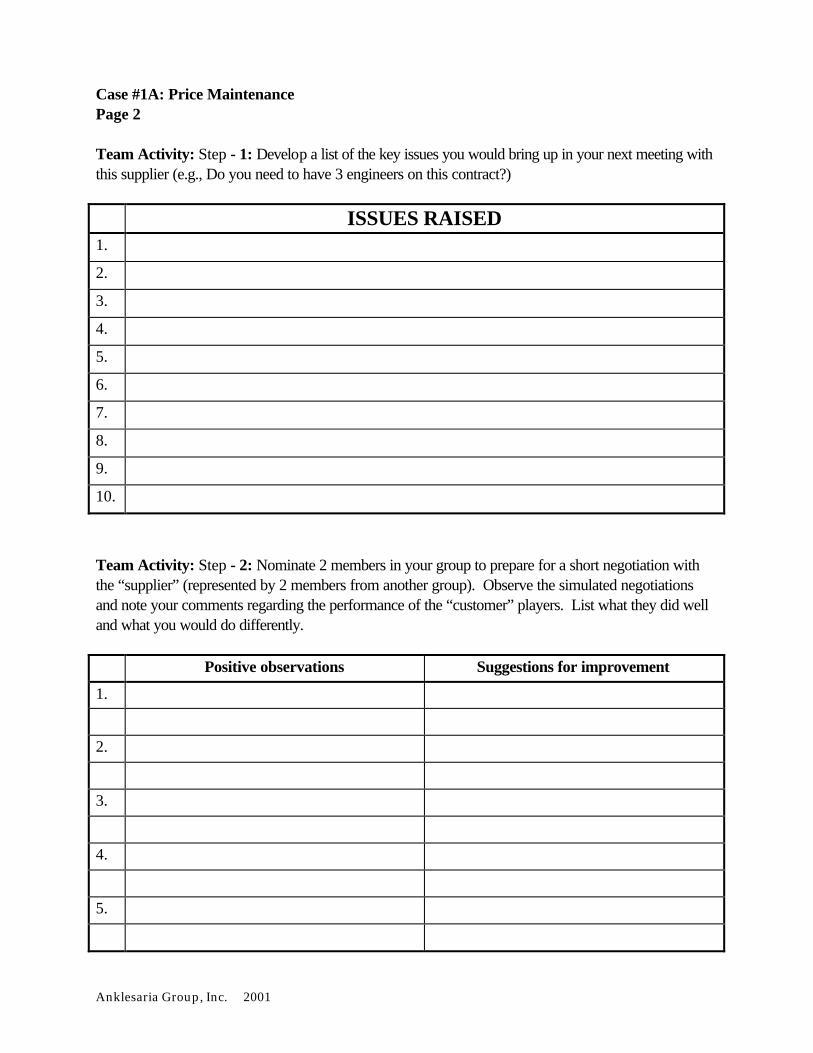

CASE #1A Price Maintenance

Three years ago you entered into a contract with Fluid Air, Inc. for the construction of a custom designed plant to manufacture Fluro dioxide. Fluro dioxide is used as a cleaning agent in the manufacture of integrated circuits (IC’s). The market for IC’s is currently exploding and is expected to continue to grow rapidly. The Fluro dioxide plant was constructed at a cost of $3.5 million and became operational a year after construction began. At that time, a 2-year maintenance contract was drawn up, whereby for a monthly fee of $60,000, Fluid Air would make sure that the plant remained fully operational. Fluid’s performance so far has met your expectations. The maintenance contract is now coming up for review. Fluid proposes to raise the maintenance fee to $65,800. You are aware that over the past two years, material prices have increased by 6% and labor rates have gone up by 10%. When reviewing Fluid’s cost breakdown for the current contract you notice that it had budgeted the labor hours for the 8 maintenance workers and 3 engineers based on routine maintenance, plus a 20% contingency factor for emergence repairs. There were no emergencies last year. Below is a comparison of the breakdowns for the current and proposed contracts.

Cost Breakdown for plant maintenance $ per month Current Proposed Raw Materials Oils, cleaners, tubing etc. 10,000.00 11,000.00 10,000.00 11,000.00 Labor: (Rates shown are current rates) 3 engineers @ $40/hr for 40 hrs. each 4,800.00 5,300.00 1 on site maintenance person @ $3,750/mth 3,750.00 4,000.00 8 maintenance workers @ $15/hr for 80 hrs. each 9,600.00 10,500.00 1 Project Coordinator 5,000.00 5,500.00 23,150.00 25,300.00 Overhead Engineering @ 300% of eng. labor 14,400.00 15,900.00 GS&A @ 25% of Materials and Labor 8,300.00 9,100.00 22,700.00 25,000.00 Profit 4,150.00 4,500.00 Monthly maintenance fee 60,000.00 65,800.00

Anklesaria Group, Inc. 2001

Case #1A: Price Maintenance Page 2 Team Activity: Step - 1: Develop a list of the key issues you would bring up in your next meeting with this supplier (e.g., Do you need to have 3 engineers on this contract?) ISSUES RAISED

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

Team Activity: Step - 2: Nominate 2 members in your group to prepare for a short negotiation with the “supplier” (represented by 2 members from another group). Observe the simulated negotiations and note your comments regarding the performance of the “customer” players. List what they did well and what you would do differently. Positive observations Suggestions for improvement

1.

2.

3.

4.

5.

Anklesaria Group, Inc. 2001