same problems better decisions - portland state university may 2016... · same problems – better...

TRANSCRIPT

page 1

Same Problems – Better Decisions Hans Nordby I CoStar Portfolio Strategy

page 2

• Old Big Data

• New Big Data

– Apartments

– Office

– Retail

– Industrial

Agenda

page 3

Big Data: It’s Here and In Use

Today – This Is Not 1999

page 4

Cap Rates, After Jackson Pollack

Institutional Grade Transaction Cap Rates

Portland

Source: CoStar Portfolio Strategy. Cap rates are shaded by distance from trailing average to identify trend.

Includes 2+ star-rated apartment assets selling for at least $5 million. As of May 2016

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Transaction Cap Rate

Apartment Transaction Cap Rate

page 5

Cap Rates, After Jackson Pollack

Institutional Grade Transaction Cap Rates

Portland

Source: CoStar Portfolio Strategy. Cap rates are shaded by distance from trailing average to identify trend.

Includes 2+ star-rated apartment assets selling for at least $5 million. As of May 2016

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Transaction Cap Rate Portland

Apartment Transaction Cap Rate

page 6

Cap Rates, After Jackson Pollack

Institutional Grade Transaction Cap Rates

Seattle

Source: CoStar Portfolio Strategy. Cap rates are shaded by distance from trailing average to identify trend.

Includes 2+ star-rated apartment assets selling for at least $5 million. As of May 2016

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Transaction Cap Rate Seattle

Apartment Transaction Cap Rate

page 7

Actionable Data

page 8

Retail

page 9

The Sum Of Many Sources

Buying Power Flows Into Shopping Center

page 10

Resident-Only Models Produce Uneven Results

Components Of Adjusted Buying Power

Sources: CoStar Portfolio Strategy; Census Bureau; Neustar As of 15Q4

$0

$500

$1,000

$1,500

$2,000

$2,500

World TradeCenter

San FranciscoCentre

RoyalHawaiian

Lenox Square The ForumShops AtCaesars

Mall ofAmerica

Residential

Adjusted Buying Power (Millions)

page 11

Accounting For Tourist Spending

Components Of Adjusted Buying Power

Sources: CoStar Portfolio Strategy; Census Bureau; Neustar As of 15Q4

$0

$500

$1,000

$1,500

$2,000

$2,500

World TradeCenter

San FranciscoCentre

RoyalHawaiian

Lenox Square The ForumShops AtCaesars

Mall ofAmerica

Residential Hotel

Adjusted Buying Power (Millions)

page 12

Daytime Population Contribution

Components Of Adjusted Buying Power

Sources: CoStar Portfolio Strategy; Census Bureau; Neustar As of 15Q4

$0

$500

$1,000

$1,500

$2,000

$2,500

World TradeCenter

San FranciscoCentre

RoyalHawaiian

Lenox Square The ForumShops AtCaesars

Mall ofAmerica

Residential Hotel Office

Adjusted Buying Power (Millions)

page 13

The Market Is Priced Efficiently

Adjusted Buying Power & Cap Rates

Source: CoStar Portfolio Strategy As of 15Q4

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

0 100 200 400 600 800 1,000 1,500

Average Cap Rate (2014-15)

Adjusted Buying Power ($, M)

page 14

Better Retail Is More Highly Occupied

Adjusted Buying Power & Occupancy Rates

100,000,000 200,000,000 300,000,000 400,000,000 500,000,000 600,000,000 700,000,000 800,000,000 900,000,000

1,000,000,000 1,100,000,000 1,300,000,000 1,500,000,000

5,000,000,000

Source: CoStar Portfolio Strategy As of 15Q4

91%

92%

93%

94%

95%

96%

97%

98%

0 200 400 600 800 1,000 1,200 1,400 1,600

Adjusted Buying Power ($, M)

Occupancy Rate

page 15

Retailers Pay A Premium To Be In The Best Areas

Adjusted Buying Power & Rents

050

100200300400500600700800900

1000125015001750

2,000,000,000

Source: CoStar Portfolio Strategy As of 15Q4

$0

$20

$40

$60

$80

$100

$120

0 200 400 600 800 1,000 1,200 1,400 1,600 1,800

Rent

Adjusted Buying Power ($, M)

page 16

Sources: Neustar; CoStar Portfolio Strategy As of 15Q1

0

50

100

150

200

250

300

350

400

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0

JCPenney Sears Barnes Noble

Number of Stores

3-Mile Buying Power ($B)

Tenant Risk

Tenant Store Count by Local Trade Area Demographics

page 17

Search New Stores Since 2013 In the CoStar Product and derive buying power

1,459,629,228

Sources: Neustar; CoStar Portfolio Strategy As of 15Q3

0

20

40

60

80

100

120

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0

Apple Nordstrom Rack H&M

Number of Stores

3-Mile Buying Power ($B)

H&M Median New Store 3-Mi. Buying Power:

Nordstrom Rack New Store3-Mi. Buying Power:

Apple New Store 3-Mi. Buying Power:

Tenant Risk

Tenant Store Count by Local Trade Area Demographics

page 18

Retail Growth Follows Apartment Construction

Adjusted Buying Power Change, 2015-20

Modeled Buying Power Increase Due To

Anticipated Apartment Deliveries &

Additional Locational Attributes In Seattle

page 19

Office

page 20

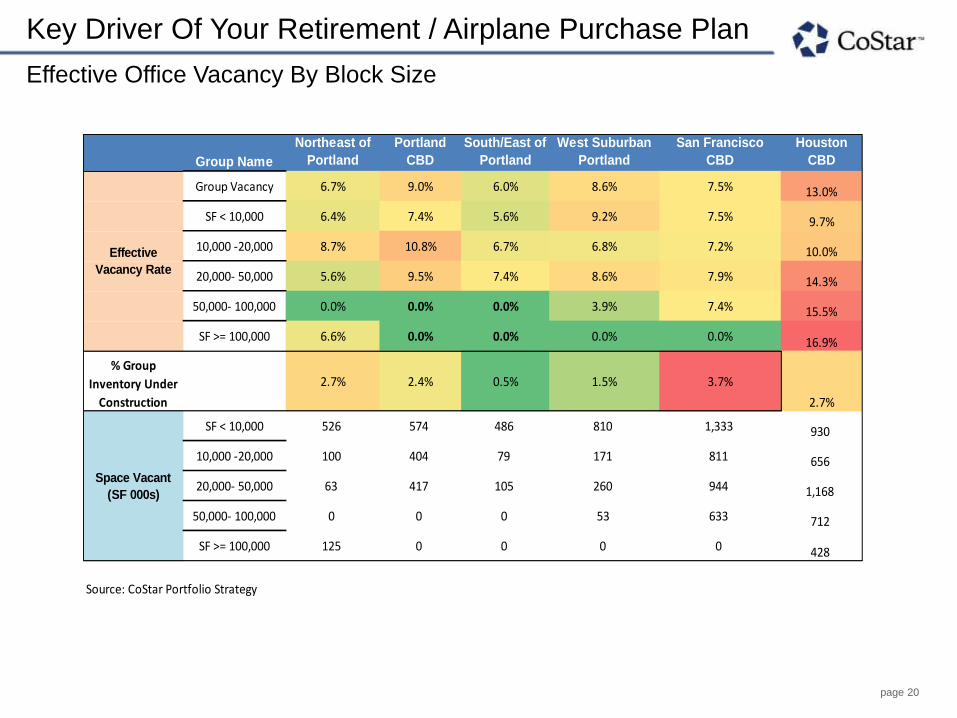

Key Driver Of Your Retirement / Airplane Purchase Plan

Effective Office Vacancy By Block Size

Group Name

Northeast of

Portland

Portland

CBD

South/East of

Portland

West Suburban

Portland

San Francisco

CBD

Houston

CBD

Group Vacancy 6.7% 9.0% 6.0% 8.6% 7.5% 13.0%

SF < 10,000 6.4% 7.4% 5.6% 9.2% 7.5% 9.7%

10,000 -20,000 8.7% 10.8% 6.7% 6.8% 7.2% 10.0%

20,000- 50,000 5.6% 9.5% 7.4% 8.6% 7.9% 14.3%

50,000- 100,000 0.0% 0.0% 0.0% 3.9% 7.4% 15.5%

SF >= 100,000 6.6% 0.0% 0.0% 0.0% 0.0% 16.9%

% Group

Inventory Under

Construction

2.7% 2.4% 0.5% 1.5% 3.7%

2.7%

SF < 10,000 526 574 486 810 1,333 930

10,000 -20,000 100 404 79 171 811 656

20,000- 50,000 63 417 105 260 944 1,168

50,000- 100,000 0 0 0 53 633 712

SF >= 100,000 125 0 0 0 0 428

Source: CoStar Portfolio Strategy

Effective

Vacancy Rate

Space Vacant

(SF 000s)

page 21

U.S. Apartment Market Review

page 22

Pockets Of Heavy Building

Growth In Inventory By Metro Through 2017Q4 (15Q4-17Q4)

Rank1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

Source: CoStar Portfolio Strategy As of 15Q4

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

South East Midwest West

New Supply (As % of Inventory)New Supply (Units)

page 23

Pockets Of Heavy Building

Growth In Inventory By Metro Through 2017Q4 (15Q4-17Q4)

Rank1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

Source: CoStar Portfolio Strategy As of 15Q4

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000N

ew

York

South East Midwest West

New Supply (As % of Inventory)New Supply (Units)

page 24

Pockets Of Heavy Building

Growth In Inventory By Metro Through 2017Q4 (15Q4-17Q4)

Rank1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

Source: CoStar Portfolio Strategy As of 15Q4

0%

2%

4%

6%

8%

10%

12%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000N

ew

York

Completions As A % Of InventorySouth East Midwest West

New Supply (As % of Inventory)New Supply (Units)

page 25

Pockets Of Heavy Building

Growth In Inventory By Metro Through 2017Q4 (15Q4-17Q4)

Rank1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

Source: CoStar Portfolio Strategy As of 15Q4

0%

2%

4%

6%

8%

10%

12%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000N

ew

York

Na

shvill

e

Completions As A % Of InventorySouth East Midwest West

New Supply (As % of Inventory)New Supply (Units)

page 26

Pockets Of Heavy Building

Growth In Inventory By Metro Through 2017Q4 (15Q4-17Q4)

Rank1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

Source: CoStar Portfolio Strategy As of 15Q4

0%

2%

4%

6%

8%

10%

12%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000N

ew

York

Na

shvill

e

Completions As A % Of InventorySouth East Midwest West

New Supply (As % of Inventory)New Supply (Units)

page 27

Pockets Of Heavy Building

Growth In Inventory By Metro Through 2017Q4 (15Q4-17Q4)

Rank1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

Source: CoStar Portfolio Strategy As of 15Q4

0%

2%

4%

6%

8%

10%

12%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000N

ew

York

Los A

ngele

s

Na

shvill

e

Completions As A % Of InventorySouth East Midwest West

New Supply (As % of Inventory)New Supply (Units)

page 28

Pockets Of Heavy Building

Growth In Inventory By Metro Through 2017Q4 (15Q4-17Q4)

Rank1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

Source: CoStar Portfolio Strategy As of 15Q4

0%

2%

4%

6%

8%

10%

12%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000N

ew

York

Los A

ngele

s

Na

shvill

e

Completions As A % Of InventorySouth East Midwest West

New Supply (As % of Inventory)New Supply (Units)

page 29

Where’s The Risk?

page 30

Multifamily Activity in Downtown LA

Source: CoStar Portfolio Strategy As of 15Q4

801 S Olive Street Multifamily Underwriting Report

page 31

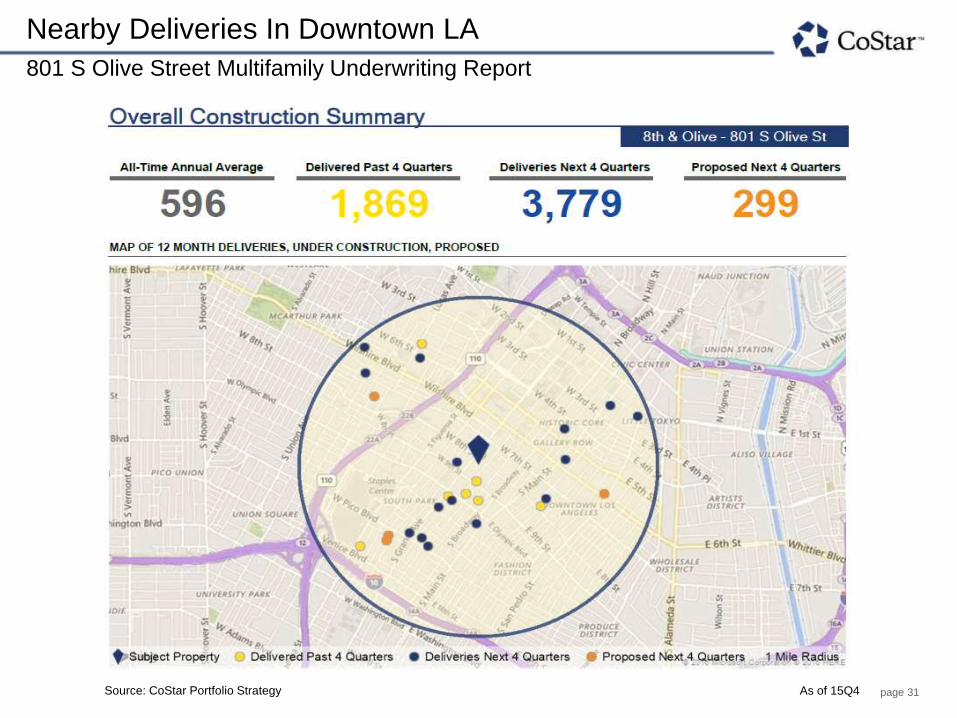

Nearby Deliveries In Downtown LA

Source: CoStar Portfolio Strategy As of 15Q4

801 S Olive Street Multifamily Underwriting Report

page 32

The Construction Pipeline Is Hot

Source: CoStar Portfolio Strategy As of 15Q4

801 S Olive Street Multifamily Underwriting Report

page 33

Many Properties Nearing Completion

Source: CoStar Portfolio Strategy As of 15Q4

801 S Olive Street Multifamily Underwriting Report

page 34

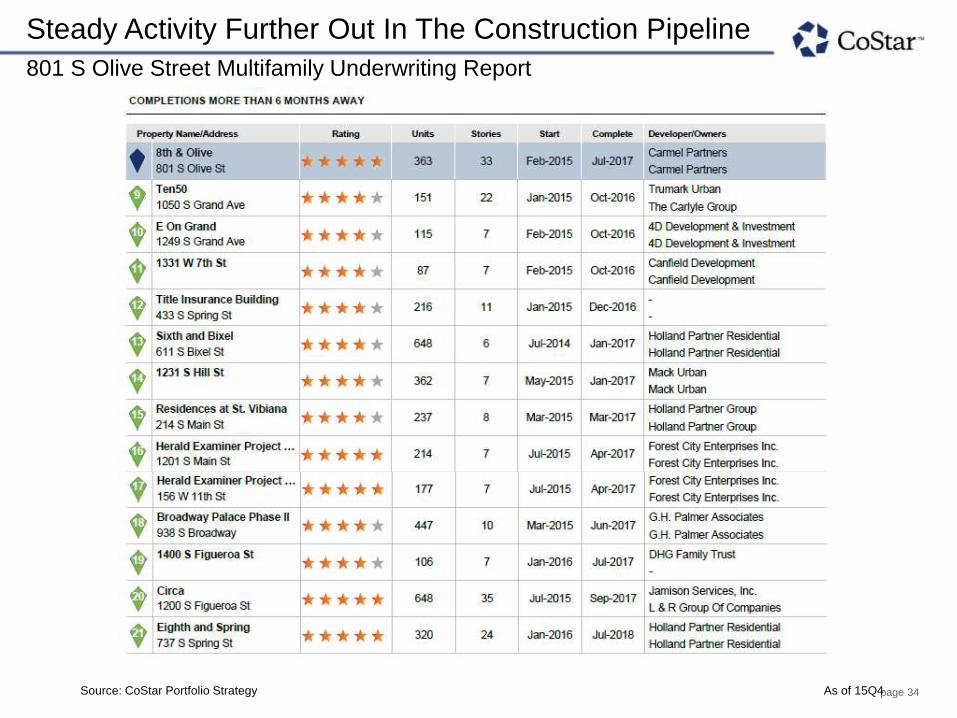

Steady Activity Further Out In The Construction Pipeline

Source: CoStar Portfolio Strategy As of 15Q4

801 S Olive Street Multifamily Underwriting Report

page 35

Industrial

page 36

Dallas: Don’t Forget About The Smaller Tenants

Vacant, Available UC, & Spaces Taken In Last 10 Years

Source: CoStar Portfolio Strategy As of 16Q1

1.4

2.4

2.2

0.0

0.5

1.0

1.5

2.0

2.5

3.0

30

20

10

0

10

20

30

40

100-250K 250-500K 500-1500K

Years of Supply Blocks Of Space

# Blocks Under Construction & Available

# Vacant Existing Blocks (Buildings Built Since 2000)

# Blocks Taken

# Years of Supply

page 37

These Costar Portfolio Strategy Materials Contain Financial And Other Information From A Variety of public and proprietary

sources. CoStar Group, Inc. and its affiliates (collectively, “CoStar”) have assumed and relied upon, without independent

verification, the accuracy and completeness of such third party information in preparing these materials.

The modeling, calculations, forecasts, projections, evaluations, analyses, simulations, or other forward-looking information

prepared by CoStar and presented herein (the “Materials”) are based on various assumptions concerning future events

and circumstances, which are speculative, uncertain and subject to change without notice. You should not rely upon the

Materials as predictions of future results or events, as actual results and events may differ materially. All Materials speak

only as of the date referenced with respect to such data and may have materially changed since such date. CoStar has no

obligation to update any of the Materials included in this document. You should not construe any of the data provided

herein as investment, tax, accounting or legal advice.

CoStar does not represent, warrant or guaranty the accuracy or completeness of the information provided herein and shall

not be held responsible for any errors in such information. Any user of the information provided herein accepts the

information “AS IS” without any warranties whatsoever. To the maximum extent permitted by law, CoStar disclaims any

and all liability in the event any information provided herein proves to be inaccurate, incomplete or unreliable.

© 2016 CoStar Realty Information, Inc. No reproduction or distribution without permission.

Hans Nordby, Managing Director