salary trends in the gulf 2014

TRANSCRIPT

��������������������������������������������������������������������������������������

Introduction

1

Em

plo

ym

en

t and

jo

b c

rea

tio

n r

em

ain

the h

ott

est

issues in t

he M

idd

le E

ast,

inclu

din

g t

he s

ix c

ountr

ies o

f th

e G

ulf C

oo

pera

tio

n

Co

uncil

(GC

C)

This

researc

h r

ep

ort

, p

rod

uced

by o

nlin

e r

ecru

itin

g f

irm

, G

ulfT

ale

nt,

sum

marises t

he s

tatu

s o

f th

e e

mp

loym

en

t m

ark

et

and

fore

casts

ke

y t

ren

ds t

o b

e e

xp

ecte

d d

uring

2014

Pub

lished

annually

, “E

mp

loym

en

t a

nd

Sa

lary

Tre

nd

s in

th

e G

ulf

” is

the p

rem

ier

pub

licatio

n o

n e

mp

loym

ent

trend

s in

the G

ulf

reg

ion

© G

ulfT

ale

nt

2014. A

ll rig

hts

reserv

ed

.

Research M

ethodology

2

34,0

00 P

rofe

ssio

nals

800 E

xecutives &

HR

Manag

ers

60 S

enio

r E

xecutives

Em

plo

yed

by larg

e a

nd

med

ium

-siz

ed

firm

s in t

he G

CC

Ag

ed

22-6

0 y

ears

Annual i n

co

me in t

he r

ang

e

US

D 1

2,0

00 -

US

D 2

00,0

00

Em

plo

yin

g 5

0 t

o 2

0,0

00 s

taff

Acro

ss a

ll m

ajo

r in

dustr

ies

Mix

of

private

secto

r lo

cal and

i nte

rnatio

nal co

mp

anie

s

Acro

ss a

ll m

ajo

r in

dustr

ies

Based

in t

he 6

GC

C c

ountr

ies

( Saud

i A

rab

ia,

Qata

r, K

uw

ait,

Bahra

in, O

man a

nd

the U

AE

)

Rele

vant

rep

ort

s f

rom

the p

ress

and

new

s s

ourc

es a

cro

ss t

he

reg

ion

Macro

-eco

no

mic

so

urc

es

� ����� �����

� � ��� ����� �� � ��� � ����

� �� �� ���� ��� ��� ����

� �� �� ���� ��� � ��� �� ��

200+

Art

icle

s

Executive Summary

3

Ec

on

om

ic &

Po

liti

ca

l B

ac

kg

rou

nd

: T

he e

co

no

mie

s o

f th

e G

ulf c

ontinue t

o g

row

at

a h

ealthy p

ace, sup

po

rted

by c

ontinued

hig

h o

il p

rices a

nd

go

vern

ment

investm

ents

in infr

astr

uctu

re. T

he r

eg

ion is a

lso

gain

ing

inte

rnatio

nal p

rom

inence a

s Q

ata

r and

UA

E a

re p

rep

aring

to

ho

st

majo

r

inte

rnatio

nal events

in t

he n

ext

decad

e. P

olit

ical te

nsio

ns a

cro

ss t

he b

road

er

Mid

dle

East

co

ntinue t

o h

ave a

n im

pact

on t

he G

ulf,

with m

ore

peo

ple

and

cap

ital flo

win

g t

o t

he r

ela

tive s

tab

ility

of

the G

ulf.

Re

cru

itm

en

t: T

he r

eg

ion c

ontinues t

o c

reate

jo

bs w

ith S

aud

i A

rab

ia in t

he lead

, w

here

62%

of

co

mp

anie

s r

ep

ort

ed

incre

ased

head

co

unt

in

2013, fo

llow

ed

by t

he U

AE

. O

n a

secto

r b

asis

, healthcare

, te

leco

m a

nd

reta

il le

d jo

b g

row

th. M

eanw

hile

acro

ss t

he r

eg

ion, em

plo

yers

are

incre

asin

gly

und

er

pre

ssure

to

red

uce t

heir r

elia

nce o

n e

xp

atr

iate

tale

nt,

part

icula

rly in S

aud

i A

rab

ia. A

s g

row

th in A

sia

rem

ain

s s

tro

ng

,

exp

atr

iate

recru

itm

ent

fro

m t

ho

se m

ark

ets

, p

art

icula

rly Ind

ia,

co

ntinues t

o b

e c

halle

ng

ing

, b

ut

has b

enefite

d f

rom

recent

falls

in t

heir c

urr

ency

valu

es. T

he s

up

ply

of

Ara

b e

xp

atr

iate

tale

nt

has incre

ased

dra

stically

due t

o t

ensio

ns in E

gyp

t and

Syria.

Ho

wever,

incre

ased

vis

a r

estr

ictio

ns

on n

atio

nals

of

these c

ountr

ies in p

art

s o

f th

e G

CC

is p

reventing

em

plo

yers

fro

m h

irin

g t

hem

.

Mo

bilit

y:

The U

AE

has f

urt

her

str

eng

thened

its

po

sitio

n a

s t

he p

rim

e d

estinatio

n f

or

exp

atr

iate

s in t

he G

CC

, re

turn

ing

to

its

pre

-crisis

level o

f

po

pula

rity

. O

ptim

ism

ab

out

the c

ountr

y’s

futu

re h

as incre

ased

fo

llow

ing

Dub

ai’s e

co

no

mic

reco

very

and

its

successfu

l bid

fo

r th

e E

xp

o 2

020.

Dub

ai and

Ab

u D

hab

i are

the r

eg

ion’s

mo

st

att

ractive c

itie

s f

or

exp

atr

iate

s, fo

llow

ed

by D

oha.

Sa

lari

es &

Co

st

of

Liv

ing

: S

ala

ry r

ises in t

he p

rivate

secto

r are

sta

ble

at

aro

und

6%

but

rem

ain

well

belo

w p

re-r

ecessio

n levels

. O

man

co

ntinued

to

witness t

he r

eg

ion’s

hig

hest

avera

ge p

ay incre

ase in 2

013, fo

llow

ed

by S

aud

i A

rab

ia. S

ala

ry incre

ase w

as h

ighest

am

ong

acco

unting

and

fin

ance p

rofe

ssio

nals

. C

onstr

uctio

n s

aw

the larg

est

incre

ase a

mo

ng

secto

rs.

20

14

Fo

rec

ast:

Sala

ries a

re f

ore

cast

to r

ise a

t a h

igher

rate

in 2

014 in m

ost

of

the G

CC

, w

ith O

man a

nd

Saud

i A

rab

ia in t

he lead

. A

ll co

untr

ies

exp

ect

to s

ee a

net

incre

ase in jo

bs -

led

by Q

ata

r and

Saud

i A

rab

ia. F

acto

rs t

hat

can im

pact

the e

xp

ecte

d r

ate

of

gro

wth

inclu

de t

he o

il p

rice,

pace o

f d

evelo

pm

ent

of

infr

astr

uctu

re f

or

the W

orld

Cup

and

Exp

o 2

020, g

lob

al eco

no

mic

reco

very

, d

ete

rio

rating

co

nd

itio

n o

f em

erg

ing

mark

ets

and

reg

ional p

olit

ical d

evelo

pm

ents

.

Contents

4

Eco

no

mic

& P

olit

ical B

ackg

rou

nd

5

Recru

itm

en

t

10

Mo

bili

ty

18

Sala

ries &

Co

st

of

Liv

ing

2

3

20

14

Fo

recast

29

Ap

pen

dix

– U

sefu

l In

form

atio

n

35

5

Economic & Political Background

0.3

%

5.9

%

7.5

%

5.5

%

3.9

%

4.4

%

-2.3

%

4.1

%

2.7

%

2.1

%

2.0

%

2.7

%

2009

2010

2011

2012

2013

2014

Fo

recast

GC

C E

co

no

mic

Gro

wth

Wo

rld

Eco

no

mic

Gro

wth

6

Gulf Economic Growth

Gulf countries continue to enjoy higher economic growth

than the global average, thanks to high oil prices

Cru

de O

il P

rice

US

D p

er

Barr

el (B

rent)

So

urc

e: W

orld

Bank

GD

P G

row

th R

ate

2009-2

014

0

20

40

60

80

100

120

140

2009

2010

2011

2012

2013

2014

So

urc

e: E

co

no

mis

t In

telli

gence U

nit

7

In 2013, Qatar led economic growth in the region,

while Kuwait saw the lo

west growth

GC

C E

co

no

mic

Overv

iew

, 2013

Siz

e o

f E

co

no

my (U

SD

bn)

GD

P G

row

th E

stim

ate

K

ey F

acto

rs A

ffecting

Gro

wth

Gro

wth

in

no

n-o

il &

gas s

ecto

rs,

inclu

din

g c

on

str

uctio

n a

nd

ban

kin

g

20

6

Gro

wth

in

th

e t

ou

rism

& h

osp

italit

y s

ecto

r; r

eco

very

of

the r

eal esta

te s

ecto

r 4

04

Hig

h g

overn

men

t sp

en

din

g o

n in

frastr

uctu

re a

nd

welfare

8

2

Reco

very

of

oil

ou

tpu

t aft

er

tech

nic

al ch

alle

ng

es in

20

12

; u

nre

so

lved

po

litic

al te

nsio

ns

31

Go

vern

men

t in

vestm

en

t in

in

frastr

uctu

re;

gro

wth

in

th

e c

on

str

uctio

n, re

tail

an

d

tran

sp

ort

secto

rs;

slig

ht

dip

in

oil

ou

tpu

t

73

3

Weak g

row

th in

oil

pro

du

ctio

n

18

1

Economic Growth by Country

5.5

%

4.3

%

4.2

%

3.9

%

3.7

%

2.3

%

Qata

r

UA

E

Om

an

Bah

rain

Saud

i A

rab

ia

Ku

wait

So

urc

e: E

co

no

mis

t In

telli

gence U

nit,

Inte

rnatio

nal M

oneta

ry F

und

, G

ulfT

ale

nt

Inte

rvie

ws

8

Economic growth and employment are being affected by tensions in parts of the Arab world

Overt

hro

w o

f G

overn

ment

Pub

lic D

em

onstr

atio

ns

Arm

ed

Co

nflic

t

Str

ikes /

Ind

ustr

ial D

isp

ute

UA

E

Qata

r B

ahra

in

Saud

i A

rab

ia

Syria

Eg

yp

t

Yem

en

Om

an

Iraq

Kuw

ait

Jo

rdan

Leb

ano

n

Political D

evelopments

aq

Mid

dle

East

– K

ey H

ots

po

ts 2

013

9

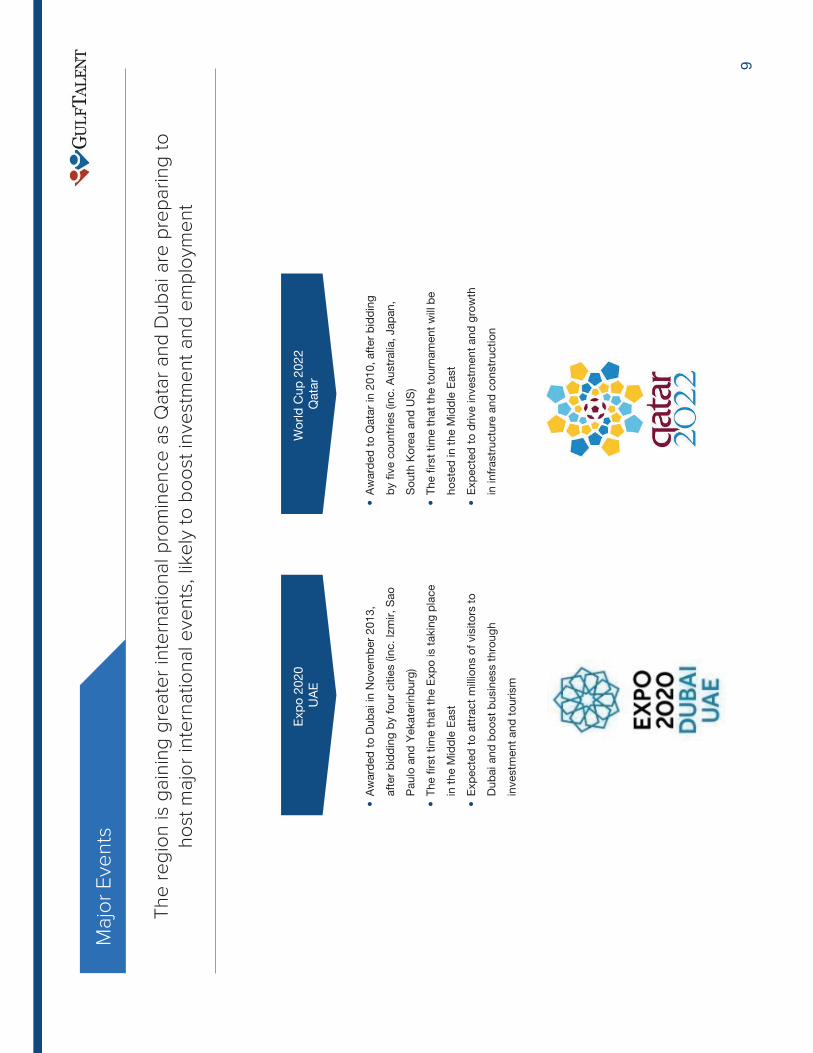

Major Events

The region is gaining greater international prominence as Qatar and Dubai are preparing to

host m

ajor international events, likely to boost investment and employment

Wo

rld

Cup

2022

Qata

r

Exp

o 2

020

UA

E

Aw

ard

ed

to

Qata

r in

20

10

, aft

er

bid

din

g

by f

ive c

ou

ntr

ies (in

c.

Au

str

alia

, Jap

an

,

So

uth

Ko

rea a

nd

US

)

Th

e f

irst

tim

e t

hat

the t

ou

rnam

en

t w

ill b

e

ho

ste

d in

th

e M

idd

le E

ast

Exp

ecte

d t

o d

rive in

vestm

en

t an

d g

row

th

in in

frastr

uctu

re a

nd

co

nstr

uctio

n

Aw

ard

ed

to

Du

bai in

No

vem

ber

20

13

,

aft

er

bid

din

g b

y f

ou

r citie

s (in

c.

Izm

ir,

Sao

Pau

lo a

nd

Yekate

rin

bu

rg)

Th

e f

irst

tim

e t

hat

the E

xp

o is t

akin

g p

lace

in t

he M

idd

le E

ast

Exp

ecte

d t

o a

ttra

ct

mill

ion

s o

f vis

ito

rs t

o

Du

bai an

d b

oo

st

bu

sin

ess t

hro

ug

h

investm

en

t an

d t

ou

rism

10

Recruitment

11

Saudi Arabia leads job creation in the Gulf, while Bahrain has the lo

west rate of job growth

Ob

serv

atio

ns

Em

plo

ym

ent

Gro

wth

by C

ountr

y:

Net

perc

enta

ge o

f firm

s w

hic

h incre

ased

head

co

unt

2012

2013

Sa

ud

i A

rab

ia h

ad

the h

ighest

rate

of

job

cre

atio

n a

mo

ng

all

GC

C

co

untr

ies w

ith 6

2%

of

co

mp

anie

s incre

asin

g h

ead

co

unt

Qa

tar

had

a s

ignific

antly lo

wer

rate

of

job

cre

atio

n c

om

pare

d t

o

2012 a

s p

roje

cts

ente

red

the e

xecutio

n p

hase late

r th

an

exp

ecte

d, p

ossib

ly r

esultin

g f

rom

uncert

ain

ty o

ver

the W

orld

Cup

and

the c

ountr

y’s

recent

lead

ers

hip

successio

n

Ba

hra

in’s

em

plo

yers

were

relu

cta

nt

to e

xp

and

their h

ead

co

unt

in

the f

ace o

f lo

w g

row

th a

nd

po

tential fu

rther

po

litic

al in

sta

bili

ty

57%

50%

31%

61%

44%

27%

Job Creation by Country 62%

51%

47%

41%

38%

9%

Saud

i A

rab

ia

UA

E

Ku

wait

Qata

r

Om

an

Bah

rain

So

urc

e: G

ulfT

ale

nt

Surv

ey o

f H

R M

anag

ers

31%

37%

34%

40%

22%

18%

15%

17%

20%

18%

20%

19%

16%

17%

20%

16%

4%

4%

5%

3%

3%

3%

4%

3%

4%

3%

2%

2%

2010

2011

2012

2013

12

The UAE, and particularly Dubai, have seen an increase in their share of

regional recruitment activity, while Qatar’s share declined in 2013

Recru

itm

ent

Vo

lum

e b

y L

ocatio

n:

Perc

enta

ge o

f vacancie

s a

dvert

ised

on G

ulfT

ale

nt

*

Dub

ai

UA

E

(Exclu

din

g D

ub

ai)

Saud

i A

rab

ia

Qata

r

Kuw

ait

Om

an

Bahra

in

Recruitment Volumes

* B

ased

on 1

00,0

00 v

acancie

s a

dvert

ised

by e

mp

loyers

and

recru

itm

ent

ag

encie

s o

n G

ulfT

ale

nt.

co

m o

ver

the s

pecifie

d p

erio

d

No

te: In

tern

et

penetr

atio

n a

nd

pre

vale

nce o

f o

nlin

e r

ecru

itm

ent

varies a

cro

ss t

he c

ountr

ies

So

urc

e: G

ulfT

ale

nt

13

Job Creation by Sector

The Healthcare sector witnesses the highest increase in headcount and Banking the lo

west

80%

67%

62%

60%

57%

50%

40%

33%

32%

Healthcare

Tele

co

ms &

IT

Reta

il

Ho

sp

italit

y

Oil

& G

as

Lo

gis

tics

Co

nstr

uctio

n

Real E

sta

te

Ban

kin

g

Ob

serv

atio

ns

Em

plo

ym

ent

Gro

wth

by S

ecto

r:

Net

perc

enta

ge o

f firm

s w

hic

h incre

ased

head

co

unt

in 2

013

He

alt

hc

are

enjo

yed

the h

ighest

incre

ase, as g

overn

ments

invest

heavily

in t

he s

ecto

r, w

hile

mo

re c

ountr

ies m

ake h

ealth insura

nce

mand

ato

ry f

or

em

plo

yers

Te

lec

om

s &

IT

’s h

igh incre

ase in h

ead

co

unt

was d

ue t

o

accele

rating

dem

and

, in

lin

e w

ith g

lob

al tr

end

s

Re

tail s

aw

hig

h g

row

th, d

riven b

y r

ap

id p

op

ula

tio

n g

row

th a

s

well

as incre

asin

g r

eta

il p

enetr

atio

n

Ba

nkin

g,

desp

ite a

healthy r

eco

very

fro

m t

he c

risis

, saw

the

low

est

em

plo

ym

ent

gro

wth

So

urc

e: G

ulfT

ale

nt

Surv

ey o

f H

R M

anag

ers

14

Nationalisation

Nationalisation of workforce remains a key challenge for companies,

especially in Saudi A

rabia and Oman

Natio

nalis

atio

n P

ressure

on E

mp

loyers

:

Perc

enta

ge o

f em

plo

yers

rep

ort

ing

natio

nalis

atio

n a

s a

key h

um

an

reso

urc

e c

halle

ng

e in 2

013

87%

81%

43%

38%

28%

21%

Saud

i A

rab

ia

Om

an

Bah

rain

Ku

wait

UA

E

Qata

r

Key G

overn

ment

Natio

nalis

atio

n M

easure

s in S

aud

i A

rab

ia

Str

ict

enfo

rcem

ent

of

Saud

isatio

n t

arg

ets

und

er

the ‘N

itaq

at’

syste

m D

ep

art

ure

of

1 m

illio

n e

xp

atr

iate

s d

uring

perio

d o

f am

nesty

C

rackd

ow

n o

n ille

gal m

igra

nt

wo

rkers

, re

sultin

g in d

ep

ort

atio

n

of

a f

urt

her

250,0

00 e

xp

atr

iate

s

Req

uirem

ent

for

dep

end

ents

of

exp

atr

iate

s t

o t

ransfe

r th

eir

sp

onso

rship

to

em

plo

yer

in o

rder

to b

e a

ble

to

wo

rk

Imp

ositio

n o

f a m

uch h

igher

annual fe

e o

n e

mp

loyers

fo

r

each e

xp

atr

iate

hire

So

urc

e: G

ulfT

ale

nt

Surv

ey o

f H

R M

anag

ers

15

Attracting W

estern nationals remains easier for Gulf employers, due to

high unemployment and wage stagnation in Europe

Private

Secto

r P

ay Incre

ase –

Glo

bal C

om

pariso

n

% 2

013

So

urc

e: A

on H

ew

itt,

Hay G

roup

, G

ulfT

ale

nt

Fra

nce

United

Kin

gd

om

Canad

a

Austr

alia

Global R

ecruitment Sources

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

2008

2009

2010

2011

2012

2013

10.2

%

6.7

%

5.9

%

3.8

%

3.0

%

2.9

%

2.9

%

Ind

ia

Phili

pp

ines

GC

C

Austr

alia UK

US

Canad

a

So

urc

e: E

co

no

mis

t In

telli

gence U

nit

Unem

plo

ym

ent

Rate

in W

este

rn C

ountr

ies

2008-2

013

16

Currency Movements

Recent currency movements have m

ade Gulf salaries more attractive for Asian professionals, while

reducing their value to Europeans

0.8

0.91

1.1 J

an

-13

Ap

r-1

3Ju

l-1

3O

ct-

13

Jan

-14

Ind

ian R

up

ee

British P

ound

Euro

Phili

pp

ine P

eso

* P

eg

ged

to

US

Do

llar

S

ourc

e: O

AN

DA

Fo

reig

n C

urr

encie

s vs. G

ulf C

urr

encie

s *

Chang

e in V

alu

e 2

013-2

014 (In

dexed

to

1 J

an.

2013)

17

“Eg

yp

tians a

re r

ead

y t

o w

ork

fo

r m

uch lo

wer

sala

ries

no

w, lo

okin

g f

or

peace o

f m

ind

and

security

.

HR

& A

dm

in M

anag

er,

Saud

i A

rab

ia

“The influx o

f cand

idate

s f

rom

Eg

yp

t and

Syria h

as

bro

ug

ht

the a

vera

ge s

ala

ry e

xp

ecta

tio

n d

ow

n a

s t

hey

are

read

y t

o w

ork

fo

r m

uch less.”

HR

Busin

ess P

art

ner,

UA

E

“Vis

as f

or

Eg

yp

tian, S

yrian, Jo

rdania

n a

nd

Leb

anese

cand

idate

s f

req

uently g

et

denie

d w

itho

ut

reaso

n,

part

icula

rly in t

he U

AE

, Q

ata

r and

Kuw

ait.”

HR

Busin

ess P

art

ner,

UA

E

“We h

ave f

ound

so

me r

eally

go

od

Syrian c

and

idate

s

keen t

o m

ove t

o G

CC

in t

he r

ecent

past,

but

gett

ing

vis

as f

or

them

pro

ved

to

be v

ery

difficult.”

HR

Manag

er,

UA

E

Impact of Arab Spring

The Arab Spring is driving m

ore Arab expats to the GCC, b

ut visa restrictions

have been increased against them

Incre

ased

vis

a r

estr

ictio

ns

Hig

h inte

rest

to r

elo

cate

to

GC

C

So

urc

e: G

ulfT

ale

nt

Inte

rvie

ws

18

Mobility

0%

10%

20%

30%

40%

50%

60%

70%

2008

2009

2010

2011

2012

2013

19

The UAE extends its lead over the other GCC countries as the

most popular destination for expatriates

Ob

serv

atio

ns

Att

ractio

n o

f E

xp

atr

iate

s:

Perc

enta

ge o

f G

CC

-based

exp

ats

outs

ide e

ach c

ountr

y w

ho

wis

h t

o r

elo

cate

into

it

The U

AE

has s

treng

thened

its p

ositio

n a

s t

he p

rim

e d

estinatio

n

for

exp

atr

iate

s, as o

ptim

ism

ab

out

its f

utu

re incre

ases f

ollo

win

g

Dub

ai’s s

uccessfu

l eco

no

mic

reco

very

and

co

ntinued

sta

bili

ty

desp

ite t

urm

oil

in t

he w

ider

reg

ion

Qa

tar

has d

rop

ped

heavily

fro

m its

2010 p

eak in p

op

ula

rity

,

driven b

y D

ub

ai’s r

e-b

ound

as w

ell

as t

he s

low

pace o

f new

pro

jects

Sa

ud

i A

rab

ia’s

heig

hte

ned

natio

nalis

atio

n m

easure

s a

re

dis

co

ura

gin

g e

xp

atr

iate

s f

rom

seekin

g e

mp

loym

ent

in t

he

kin

gd

om

Ba

hra

in r

em

ain

s t

he least

att

ractive d

estinatio

n a

s e

xp

atr

iate

s

co

ntinue t

o p

erc

eiv

e t

he c

ountr

y a

s u

nsafe

UA

E

Qata

r

Saud

i A

rab

ia

Om

an

Kuw

ait

Bahra

in

Popular Countries

So

urc

e: G

ulfT

ale

nt

Surv

ey

20

S

ourc

e: G

ulfT

ale

nt

Surv

ey

40%

19%

20%

7%

4%

3%

3%

3%

3%

1%

2%

1%

Popular Cities

Dubai remains the region’s m

ost attractive city, followed by Abu Dhabi and Doha

Rankin

g o

f G

ulf C

itie

s –

By A

ttra

ctio

n f

or

Exp

atr

iate

s:

Perc

enta

ge o

f G

CC

-based

exp

atr

iate

s o

uts

ide t

he c

ity w

ho

wis

h t

o r

elo

cate

into

it

48%

20%

16%

5%

3%

2%

2%

2%

2%

2%

1%

1%

Dub

ai

Ab

u D

hab

i

Do

ha

Jed

dah

Muscat

Ku

wait C

ity

Mad

ina

Riy

ad

h

Makkah

Sharjah

Dam

mam

Manam

a

2012

2013

21

43%

45%

47%

49%

60%

88%

Retention by Country

The UAE experiences a rise in retention rate, as the overw

helming m

ajority of

expatriates wish to stay in the country

Rete

ntio

n o

f E

xp

atr

iate

s:

Perc

enta

ge o

f exp

atr

iate

s w

ithin

the c

ountr

y w

ho

wis

h t

o r

em

ain

there

2012

2013

Ob

serv

atio

ns

The U

AE

’s a

pp

eal fo

r exp

atr

iate

s a

lread

y liv

ing

within

the

co

untr

y is d

ue t

o s

tab

ility

, in

frastr

uctu

re a

nd

op

tim

ism

ab

out

the

co

untr

y’s

eco

no

mic

develo

pm

ent

Qa

tar

co

ntinues t

o h

ave t

he lo

west

rete

ntio

n r

ate

within

the

GC

C,

main

ly a

s a

result o

f la

ws p

reventing

exp

atr

iate

s f

rom

chang

ing

jo

bs

Rete

ntio

n r

ate

s a

cro

ss m

ost

GC

C c

ountr

ies a

re f

alli

ng

, la

rgely

as a

result o

f th

e U

AE

’s a

ccele

rating

po

pula

rity

UA

E

Ku

wait

Bah

rain

Om

an

Sau

di A

rab

ia

Qata

r

83%

64%

50%

51%

49%

48%

So

urc

e: G

ulfT

ale

nt

Surv

ey

22

1.1

%

1.1

%

3.4

%

5.4

%

5.4

%

4.8

%

3.7

%

2007

2008

2009

2010

2011

2012

2013

Domestic Relocations

Fewer Dubai residents are now working in Abu Dhabi, following regulatory changes

in Abu Dhabi as well as an im

proving Dubai economy

Recessio

n c

auses

massiv

e jo

b

losses in D

ub

ai

Ab

u D

hab

i sta

te f

irm

s

ord

ere

d t

o s

top

ho

usin

g

allo

wan

ce t

o e

mp

loyees

livin

g o

uts

ide A

bu

Dh

ab

i

Dub

ai R

esid

ents

Wo

rkin

g in A

bu D

hab

i

As p

erc

enta

ge o

f all

wo

rkin

g p

rofe

ssio

nals

liv

ing

in D

ub

ai

So

urc

e: G

ulfT

ale

nt

Surv

ey

23

Salaries & Cost of Living

24

7.0

%

7.9

%

9.0

%

11.4

%

6.2

%

6.1

%

5.5

%

6.2

%

5.9

%

6.3

%

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Fo

recast

Salary Increases

Salary rises in the private sector are stable but remain below pre-recession levels

GC

C A

vera

ge S

ala

ry Incre

ase

2005 -

2014

Glo

bal financia

l crisis

hits t

he G

CC

So

urc

e: G

ulfT

ale

nt

Surv

ey

25

8.6

%

6.8

%

6.5

%

5.8

%

5.2

%

5.2

%

Salaries by Country

Oman continues to witness the region’s highest average pay increase

in the private sector, followed by Saudi Arabia

7.4

%

6.7

%

5.6

%

5.4

%

5.3

%

4.0

%

Om

an

Saud

i A

rab

ia

Qata

r

Ku

wait

UA

E

Bah

rain

Private

Secto

r S

ala

ry Incre

ase b

y C

ountr

y

2012

2013

Ob

serv

atio

ns

The U

AE

was t

he o

nly

co

untr

y t

hat

saw

a h

igher

avera

ge p

ay

incre

ase in 2

013 t

han t

he p

revio

us y

ear,

with m

ost

co

untr

ies

seein

g a

slo

wer

incre

ase

Om

an

had

the h

ighest

avera

ge s

ala

ry r

ise, fo

llow

ing

a 6

2%

ris

e

in n

atio

nal m

inim

um

wag

e a

nd

a f

urt

her

mand

ato

ry in

cre

ase f

or

natio

nals

em

plo

yed

in t

he p

rivate

secto

r

Ba

hra

in’s

sala

ry r

ise r

em

ain

ed

co

nserv

ative a

s m

any

busin

esses s

trug

gle

d t

o g

row

So

urc

e: G

ulfT

ale

nt

Surv

ey

26

5.3

%

5.6

%

7.4

%

6.7

%

5.4

%

4.0

%

3.2

%

3.7

%

2.8

%

1.3

%

1.1

%

3.1

%

Salaries and Inflation

Average pay rise adjusted for inflation was highest in Oman and the UAE

Real S

ala

ry Incre

ase b

y C

ountr

y, 2013 *

S

ala

ry R

ise

Inflatio

n

0.8

%

2.5

%

2.6

%

3.0

%

4.2

%

6.1

%

Bah

rain

Qata

r

Ku

wait

Saud

i A

rab

ia

UA

E

Om

an

Ob

serv

atio

ns

Om

an

and

the U

AE

enjo

yed

the h

ighest

real sala

ry incre

ase

with 6

.1%

and

4.2

% r

esp

ectively

due t

o lo

w inflatio

n r

ate

s

In S

au

di

Ara

bia

, K

uw

ait

and

Qa

tar,

hig

h inflatio

n led

to

co

mp

ara

tively

lo

w r

eal sala

ry r

ises

Ba

hra

in’s

alread

y lo

w a

vera

ge s

ala

ry incre

ase w

as a

lmo

st

entire

ly w

iped

out

by t

he h

igh r

ate

of

inflatio

n,

resultin

g in a

real

incre

ase c

lose t

o z

ero

* D

efined

as n

om

inal p

ay r

ise n

et

of

inflatio

n r

ate

S

ourc

e: G

ulfT

ale

nt

Surv

ey, E

co

no

mis

t In

telli

gence U

nit

27

Salaries by Segment

Salary increase was highest among Finance professionals. Among industry sectors, Construction saw

the largest average increase

Sala

ry Incre

ase b

y J

ob

Cate

go

ry

%, 2013

6.2

%

6.0

%

5.8

%

5.7

%

5.7

%

5.5

%

5.2

%

Fin

ance

Eng

ineering

HR

Ad

min

Mark

eting

Sale

s IT3.7

%

4.8

%

4.9

%

5.4

%

5.5

%

5.5

%

5.7

%

6.0

%

6.1

%

6.4

%

Ed

ucatio

n

Tele

co

ms &

IT

Lo

gis

tics

Real E

sta

te

Ho

sp

italit

y

Healthcare

Ban

kin

g

Reta

il

Oil

& G

as

Co

nstr

uctio

n

Sala

ry Incre

ase b

y Ind

ustr

y

%, 2013

So

urc

e: G

ulfT

ale

nt

Surv

ey

28

* A

vera

ge f

igure

. W

ide v

ariatio

ns b

ased

on lo

catio

n a

nd

qualit

y

S

ourc

e: G

ulfT

ale

nt

Surv

ey

Cost of Living

Cost of living saw the fastest rise in Saudi Arabia. In absolute term

s, however,

the UAE and Q

atar remain the m

ost expensive

Inflatio

n

Rent

for

Tw

o-b

ed

roo

m A

part

ment

US

D p

er

mo

nth

, 2013*

3.7

%

3.2

%

3.1

%

2.8

%

1.3

%

1.1

%

Saud

i A

rab

ia

Bah

rain

Qata

r

Ku

wait

Om

an

UA

E

2012

2013

2.9

%

4.1

%

3.0

%

3.1

%

1.1

%

1.9

%

1,9

10

1,8

90

1,7

00

1,1

40

1,0

50

1,0

50

950

830

780

740

720

670

Dub

ai

Do

ha

Ab

u D

hab

i

Ku

wait

Muscat

Manam

a

Sharjah

Dam

mam

Riy

ad

h

Jed

dah

Kh

ob

ar

Jub

ail

So

urc

e: E

co

no

mis

t In

telli

gence U

nit

29

2014 Forecast

30

7.4

%

6.7

%

5.6

%

5.3

%

5.4

%

4.0

%

Salaries by Country 2014

Salaries in m

ost Gulf countries are expected to rise at a higher rate in 2014

Exp

ecte

d A

vera

ge P

ay R

ise

%, 2014 F

ore

cast

2013

2014

8.0

%

6.8

%

6.7

%

5.9

%

5.8

%

3.9

%

Om

an

Saud

i A

rab

ia

Qata

r

UA

E

Ku

wait

Bah

rain

Ob

serv

atio

ns

Om

an

is f

ore

cast

to o

nce a

gain

enjo

y t

he h

ighest

avera

ge p

ay

rise in 2

014

UA

E c

om

panie

s p

lan t

o o

ffer

hig

her

sala

ry incre

ases t

han last

year,

driven b

y h

igher

exp

ecte

d inflatio

n a

s w

ell

as f

aste

r p

ace

of

gro

wth

Ba

hra

in’s

co

mp

anie

s r

em

ain

co

nserv

ative in t

heir s

ala

ry

decis

ions, d

esp

ite ind

icato

rs o

f an im

pro

vin

g e

co

no

mic

clim

ate

in 2

014

So

urc

e: G

ulfT

ale

nt

Surv

ey o

f H

R M

anag

ers

31

41%

62%

51%

38%

47%

9%

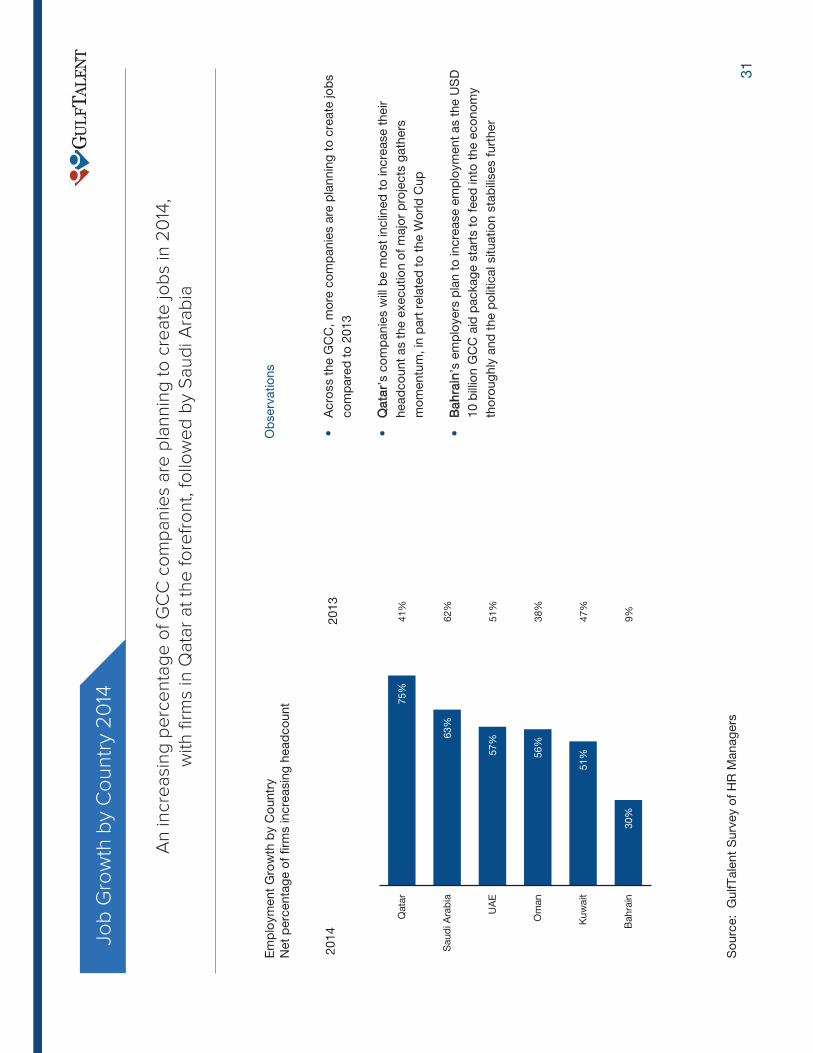

Job Growth by Country 2014

An increasing percentage of GCC companies are planning to create jo

bs in 2014,

with firms in Qatar at the forefront, followed by Saudi Arabia

Em

plo

ym

ent

Gro

wth

by C

ountr

y

Net

perc

enta

ge o

f firm

s incre

asin

g h

ead

co

unt

2013

2014

75%

63%

57%

56%

51%

30%

Qata

r

Saud

i A

rab

ia

UA

E

Om

an

Ku

wait

Bah

rain

Ob

serv

atio

ns

Acro

ss t

he G

CC

, m

ore

co

mp

anie

s a

re p

lannin

g t

o c

reate

jo

bs

co

mp

are

d t

o 2

013

Qa

tar’

s c

om

panie

s w

ill b

e m

ost

inclin

ed

to

incre

ase t

heir

head

co

unt

as t

he e

xecutio

n o

f m

ajo

r p

roje

cts

gath

ers

mo

mentu

m, in

part

rela

ted

to

the W

orld

Cup

Ba

hra

in’s

em

plo

yers

pla

n t

o incre

ase e

mp

loym

ent

as t

he U

SD

10 b

illio

n G

CC

aid

packag

e s

tart

s t

o f

eed

into

the e

co

no

my

tho

roug

hly

and

the p

olit

ical situatio

n s

tab

ilises f

urt

her

So

urc

e: G

ulfT

ale

nt

Surv

ey o

f H

R M

anag

ers