rx for medical practice operations - home - lewis & knopf

TRANSCRIPT

Rx for Medical Practice Operations

2012 Edition

5206 Gateway Centre | Suite 100 | Flint, MI 48507 | 810-238-4617 | 877-244-1787 | 810-238-5083 fax

5918 Meridian Blvd. | Suite 1 | Brighton, MI 48116 | 810-225-1808 | 810-225-1847 fax

104 South Adelaide Street | Fenton, MI 48430 | 810-629-1500 | 810-629-7441 fax

www.lewis-knopf.com

2

Rx for Medical Practice OperationsDeveloping and maintaining a successful medical practice can be a difficult task. Finding the right tools and advisors to best meet the unique needs of the medical practice is essential, allowing you to focus on the more important tasks at hand. To most healthcare professionals, their number one priority is to provide quality care to their patients. Consequently, their training focuses on their profession and not on running a business. The profit motive is a secondary, but necessary concern. We at Lewis & Knopf, CPAs, P.C. can provide invaluable service by utilizing our business knowledge to assist the physician in creating and maintaining a successful and quality healthcare practice. The services we provide are generally divided into two categories – practice services related to your business and personal services related to your business.

Being familiar with the operations of the physician’s office, we can provide valuable consulting services on a number of practice management issues. Lewis & Knopf, CPAs, P.C. has created this “Rx for Medical Practice Operations” to assist physicians contemplating entering into a private practice. This guide is in outline form for quick reference to the sections which interest you the most and relate to your individual concerns. You will find very helpful reference material to assist you in determining your exact needs and source references such as websites and vendor listings to fulfill those needs. Your time is very valuable and usually a “hot” commodity. We suggest taking advantage of the checklist at the beginning of the packet to get you started on the right track as soon as possible. Our goal for this guidebook is that your practice “hits the floor running” when you begin seeing patients.

Please feel free to contact Tom Shade, Steve Kidd, Anita Abrol or Dave Page at our office at (810) 238-4617 or toll-free (877) 244-1787 if you need any assistance or have any questions concerning the “Rx for Medical Practice Operations.” These four partners specialize in the healthcare industry and have extensive backgrounds in supporting numerous physicians within the Genesee, Livingston, Lapeer, and Oakland County areas with their business and personal needs. In addition, our team can introduce you to any number of attorneys, bankers, investment advisors, and/or insurance agents with experience dealing with the medical profession. Please enjoy this packet and do not hesitate to call us at your earliest convenience.

Please note: The material discussed in this publication is meant to provide general information and should not be acted on without obtaining professional advice appropriately tailored to your individual needs. Any tax information contained in the body of this guidebook is not intended or written to be used, and cannot be used, by the recipient for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code or applicable state or local tax law provisions.

3

Table of Contents

I. Business Startup Checklist .......................................................................... 4

II. Services Offered by Lewis & Knopf, CPAs, P.C. & Professional Profiles .... 6

III. Choice of Entity ......................................................................................... 8

IV. Billing Services ........................................................................................... 15

V. Sample Cash Flow Projection ..................................................................... 16

VI. Physician Compensation Planning .............................................................. 18

VII. Retirement Plans ........................................................................................ 20

VIII. Other Fringe Benefits ................................................................................. 27

IX. Business & Payroll Taxes ............................................................................ 28

X. Buy/Sell Agreements ................................................................................... 31

XI. Issues Concerning Setting Up a Practice:

A. Acquiring Medical Office Space .................................................. 32

B. Office Design and Layout ........................................................... 33

C. Furniture and Equipment ............................................................ 35

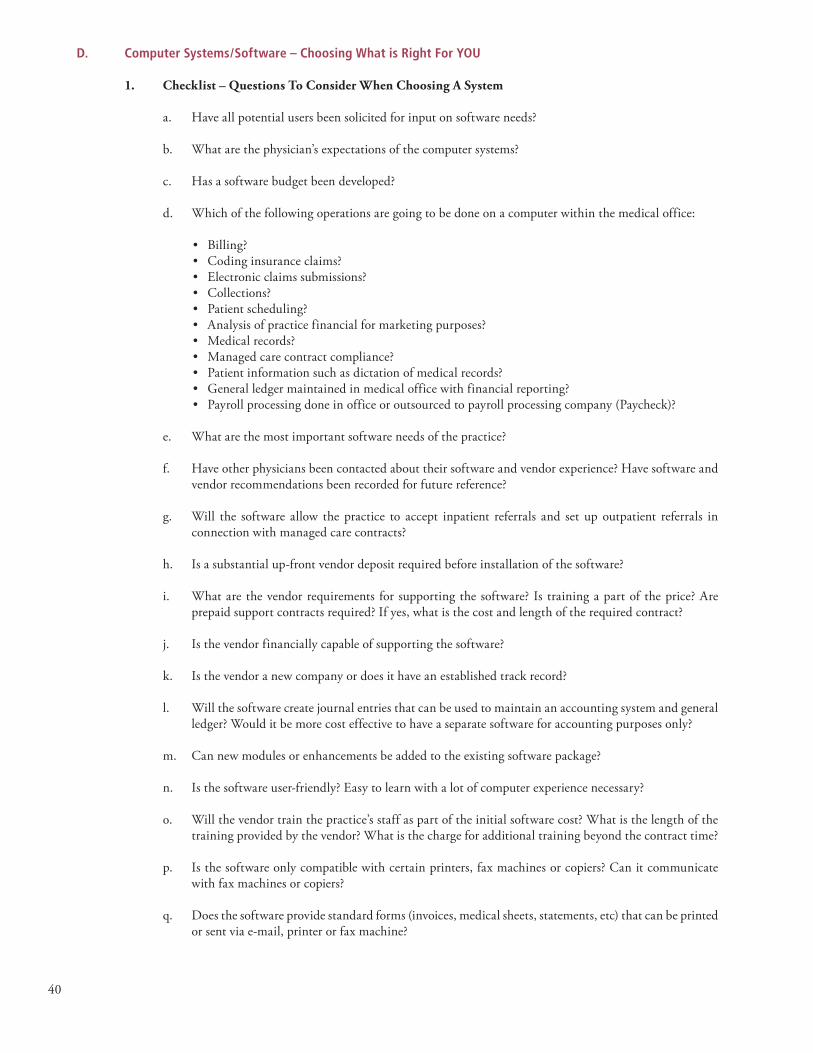

D. Computer Systems/Software ........................................................ 40

E. Suggested Approach for Buying Furniture and Equipment .......... 41

F. Equipment Buying vs. Leasing .................................................... 41

4

I. Business Start-Up Checklist For Healthcare ProfessionalsThis checklist is designed to help and inform you, the healthcare professional, about issues you should be considering when setting up your practice.

A. Select Your Business Advisors Lewis & Knopf, CPAs, P.C. would like to be your quarterback. We will provide you with a list of advisors that have

experience in the healthcare field.

B. Choice of Entity Select an entity that fits your needs. We recommend that you choose to be taxed as an “S corporation.” However,

please refer to Section III to find out more about the different types of entities available and the advantages and disadvantages of each.

C. Select your Billing Service Through our contacts at Lewis & Knopf, we can assist you in hiring a billing company who will focus on a number

of key issues critical to increasing billing collections. Often new physicians feel they cannot afford a billing service. We believe you cannot afford to not utilize a billing service. The information contained in this guidebook is worthless if you are not able to bill and collect timely from your patients.

D. Applications It is necessary that you apply to the various governmental entities to obtain identification numbers, licenses, and

PIN numbers for medical billing purposes. We can assist you in this process. Some examples of what is required are:

• Articles of Incorporation • Subchapter S Election Form (Form 2553) • Partnership (LLC) Operating Agreement • Federal Identification Number (SS-4)• Michigan Sales, Use, Withholding and Unemployment Registration• Hospital Privilege Applications • Drug Prescription Application• Credentialing (Pin Numbers)

E. Your Business Plan It is imperative that you develop a business plan including cash flow projections. The “plan” will be useful when

establishing banking relationships for financing purposes. In addition, we will give you an idea about your potential compensation level. Please refer to Section V for an example of a cash flow projection for the first three years of operations.

F. Physician Compensation Planning In practices with more than one doctor, it will become apparent that some physicians are more efficient than others

and, therefore, may generate more revenue. However, there are basic overhead expenses that occur regardless of how efficiently you can practice. We will help you design a compensation package that will be fair and equitable to all of the members of the practice. Please refer to Section VI.

G. Retirement Plans There are a variety of retirement plans available to our healthcare professionals. We will help you choose the right

plan at the right time. Please refer to Section VII for a detailed discussion on retirement plans.

H. Other Fringe Benefits As an employer, you will need to consider what kinds of fringe benefits you want to offer/provide to your employees.

Please see Section VIII for a detailed discussion.

5

I. Business and Payroll Tax Returns Healthcare professionals are concerned with patient care as they should be. As a result, we recommend that you

contract with a payroll service to prepare the payroll. They will deposit all of the taxes with the proper governmental authority, prepare the payroll returns, prepare the W-2’s for employees, etc. for a reasonable fee. However, if you choose to prepare your own payroll, see Section IX that describes the various deposit requirements for the different returns.

J. Buy/Sell Agreements It is important that a mechanism be in place that will resolve disputes that can and do arise in practices comprised

of more than one physician. We work closely with your attorney to design a buy/sell agreement that will work best for you. See Section X.

K. Purchase Adequate Insurance It is essential that you have adequate insurance coverage. You should consider at a minimum the following types of

coverage:

• “Malpractice Insurance” We can explain the importance of each one, how it will affect you, and recommend limits. (Don’t forget “tail coverage.”)

• General, Liability and Umbrella • Workmen’s compensation• Disability• Life• Fire• Employee dishonesty• Other

L. Issues Concerning Setting up a Practice Setting up a new office requires a great deal of time, but it does not have to be a painful experience. With the help

of our L&K Checklist, it will be a straight forward and simple task. Please refer to Section XI for a discussion on acquiring office space, equipment, etc., and a shopping list for your new practice. Congratulations!

6

II. Services Offered by Lewis & Knopf, CPAs, P.C. Managed care and the tenuous financial health of Medicare and Medicaid are changing the nature and business climate

of the entire healthcare industry. As a healthcare professional in the center of an industry driven by mergers of hospitals, physicians, other healthcare providers, and payers, you are experiencing the need to achieve economies to scale and attain cost efficiencies. These forces require professionals like you to clearly define your vision and future strategic direction, to organize and maximize both the financial return and cost effectiveness of your organization.

Considering the challenges and changes you face, you need business advisors experienced in serving professionals like yourself. We at Lewis & Knopf, CPAs, P.C. can assist you with all of your professional accounting, tax, and consulting needs. We have provided business and consulting services to healthcare professionals for over 70 years, keeping abreast of business and regulatory changes affecting providers in the medical field. This, combined with our years of experience and healthcare industry knowledge, allows us to help you achieve your goals.

Our Expert Consulting Capabilities Include:

• Annual Business Planning• Business Development• Business Valuations • Estate and Trust Planning• Financial Analyses, Budgeting, Projections and Forecasts• Individual Income Tax Planning• Management Compensation Planning• Mergers & Acquisitions• New Business/Start-up Planning• Organizational Structuring for Management and Corporations• Pension and Employee Welfare Benefits• Personal Financial Planning• Strategic Planning

We welcome the opportunity to serve you. L&K’s professionalism, experience, network of resources, dedication to personal service, and insight are yours to grasp!

7

Their areas of business specialty practice are:• Health Care Professionals• Income Tax Planning• Business Development and Growth

They provide tax planning and tax return preparation services to individuals and closely held businesses. Their services also include:• Accounting system reviews to improve operating efficiencies and internal controls• Researching the tax consequences of alternative business strategies• Tax planning for income and estate tax purposes

They are members of the American Institute of Certified Public Accountants and the Michigan Association of Certified Public Accountants.

David A. Page, CPA/ABV, CBA, AM, CFP, ChFC, is the principal in-charge of the firm’s valuation practice. He joined Lewis & Knopf in 2007 and has been a certified public accountant since 1984.

Dave specializes in valuation services for closely-held companies and medical practices. He also provides comprehensive

tax and accounting services to a variety of clients including real estate holding companies, construction companies, investment partnerships, healthcare practices, partnerships, trusts and high net worth individuals.

Dave graduated from Michigan State University with a Bachelor of Arts degree in history in 1974. He received his Bachelor in Business Administration in 1981 from University of Michigan Flint.

Stephen L. Kidd, CPA, is a principal with the firm. He joined Lewis & Knopf in 1978 and has been a certified public accountant since 1980

Steve is focused on facilitating growth for his entrepreneurial clients as they become more profitable business owners. He has helped clients return to profitability by

restructuring cost accounting systems. Steve has also been intricately involved in the negotiation of various company transitions of ownership.

Steve graduated from Ferris State College with a Bachelor of Science degree in accountancy in 1978.

Thomas K. Shade, CPA, is a principal of the firm. He joined Lewis & Knopf in 1979 and has been a certified public accountant since 1982.

As a member of the firm’s Professional Service Group, Tom specializes in serving professional service providers including physicians, dentists, pharmacists, and

attorneys. He also works with a variety of entrepreneurial industries, including auto dealerships, construction, and real estate.

Tom graduated from Alma College in 1979 with a Bachelor of Science degree in business administration with an emphasis in accounting. He is actively involved in both local and national professional organizations and currently serves on the Michigan Association of Certified Public Accountants Midsize Firm Advisory Council.

Anita Abrol, CPA, is the managing principal of the firm. She joined Lewis & Knopf in 1988 and has been a certified public accountant since 1990.

Anita specializes in healthcare, high net worth individuals, professional services, estates and trusts, and school districts. She has helped numerous physicians set

up their professional practices from scratch, including their billing systems, office procedures, and accounting cycle.

Anita is a 1984 graduate of the University of London, England with a Bachelor of Science degree in mathematics. She received a Certificate of Educational Achievement in estate planning from the American Institute of Public Accountants (AICPA) in 1997 and a Certified Specialist in Estate Planning designation from the National Institute for Excellence in Professional Education in 1999.

II. Lewis & Knopf, CPAs, P.C.’s Professional Profiles

8

III. Choice of Entity

A. S Corporations (Recommended by Lewis & Knopf, CPAs, P.C.)

S corporations are hybrid corporations that combine some of the tax advantages of a partnership with the liability protection of a corporation. Start-up businesses often consider S corporation status because profits and losses are passed through to the shareholders with no corporate tax imposed.

1. Advantages include:

a. The double taxation affecting most C corporations is avoided because income is passed through to the shareholders for tax purposes, increasing stock basis.

b. Owners have limited liability.

c. The tax rate on S corporation earnings, when passed through to the shareholder, may be lower than the applicable corporate tax rate. (In fact the top individual rate is currently equal to the top corporate rate of 35%).

d. Distributions from S corporations are exempt from the payroll tax system, assuming the corporation issues adequate compensation to those shareholders performing services for the corporation.

2. Disadvantages include:

a. The number of shareholders is limited to no more than 100.

b. They can have only one class of stock.

c. They cannot have corporate, partnership, certain trusts, or nonresident alien shareholders (other than a limited exception for one S corporation owning 100% of another S corporation).

d. They must choose a calendar year rather than a fiscal year (or prepay the tax that shareholders defer if electing to report on a fiscal year).

e. Shareholders owning more than 2% of the company must pay taxes on a wide range of employee fringe benefits that would be tax free to an employee of a C corporation.

f. The tax rate on S corporation earnings, when passed through to the shareholder, may be higher than the applicable corporate tax rate.

B. Corporations Corporations are business entities created under state law. They are characterized as artificial persons created for

the purpose of conducting business. As such, they can hire employees, enter into contracts, acquire assets, and incur liabilities. An important feature is that they generally enable their owners (shareholders) to limit their liability to the extent of their investment in the corporation.

1. Advantages include:

a. There is a practical method to raise capital (through the sale of capital stock).

b. Owners have limited liability.

c. Corporations have unlimited lives. d. It is relatively easy to transfer ownership interests.

9

e. They generally have more management resources.

f. When formed as S corporations, they have certain tax advantages because income is generally passed through to the owners and taxed at the individual level.

g. When formed as C corporations, owner-employees generally may receive the full array of employer-provided tax free fringe benefits.

2. Disadvantages include:

a. C corporations are subject to double taxation. Pretax income is taxed at the corporate level. Dividends are then taxed to the owners creating double tax on such distributions.

b. They have more administrative burdens.

c. They are more difficult to form, and dissolution can trigger taxable gains. d. Borrowing may be difficult without stockholder guarantees, which negates part of the advantage of

limited liability.

C. Proprietorships Proprietorships are the most basic and usually the simplest form of business organization. In a proprietorship, the

owner holds title to property, conducts business for profit, and is directly and personally liable for all obligations of the business. In most cases, the owner’s personal assets can be seized to satisfy proprietorship debts.

1. Advantages include:

a. They are easy to form. For example, they have few filings, elections, and registrations.

b. They are simple to operate. For example, the owner manages the business and reports to no one.

c. It is easy to sell the assets of the business.

d. There are few administrative burdens.

e. For tax purposes, income is generally passed through to the owner and taxed only at the personal level.

2. Disadvantages include:

a. They may have limited sources of capital.

b. There is no limited liability, as can be achieved with a corporation or limited liability company.

c. There is no structured continuity beyond the proprietor.

d. All business net income is subject to self-employment tax.

10

D. Limited Liability Companies Limited liability companies (LLCs) are business entities created under state law that can be used in all states.

Limited liability companies are owned by members and combine the tax advantages of a partnership with the liability protection of a corporation. As a result, the LLC structure is often compared to an S corporation. In many cases, LLCs are more flexible than S corporations. The major drawbacks of LLCs are that laws are new and relatively untested in nontax matters, and members of LLCs that conduct an active business will generally be subject to self-employment tax. Each state establishes its own LLC rules and characteristics.

1. Advantages include:

a. Members have limited liability.

b. The number of members is not limited.

c. Members may be individuals, corporations, trusts, partnerships, other LLCs, and other entities.

d. The double taxation affecting most C corporations is avoided. Income is passed through to the members for tax purposes under partnership principles.

e. Members can participate in managing the LLC.

f. Members generally are not personally liable for the LLC’s debt (although lenders often require personal guarantees of owners).

g. Distributions to members do not have to be directly proportional to the members’ ownership percentages as they do for S corporations.

h. They can have different classes of ownership.

2. Disadvantages include:

a. They may have limited life, often by termination on the death or bankruptcy of a member.

b. Transfer of interests is difficult. Although a member may transfer an equity interest in the LLC, the new owner does not necessarily possess all of the rights and attributes of a member.

c. Some industries or professions may not be permitted to use LLC status, and there is still one state, Massachusetts, that requires at least two members.

d. All states have enacted LLC laws, but the laws that have been enacted vary from state to state. Therefore, the LLC must determine how it will be treated for both tax and liability purposes in other states.

e. The various LLC laws are new and relatively untested in non-tax matters, such as their actual ability to limit member liability.

f. For tax purposes, the complex partnership rules generally apply.

g. Members will often be subject to self-employment tax.

E. General Partnerships General partnerships are associations of two or more persons as co-owners to carry on a business for profit. The

co-owners personally share the risks and rewards of all phases of the business. Because of tax rules and regulations, partnerships are increasingly complex entities. Each partner is jointly and severally liable for the partnership’s obligations. Like proprietorships, a partner’s personal assets can be seized to satisfy partnership debts.

11

1. Advantages include.

a. They have more sources of initial capital than proprietorships.

b. There generally are more management resources available than for proprietorships.

c. They have less administrative burdens than corporations.

d. For tax purposes, income is generally passed through to the partners and taxed only at the personal level. Income and loss allocations can be flexible (i.e., other than in proportion to partner capital accounts), and termination can generally occur without taxation.

2. Disadvantages include.

a. The transfer of interests is difficult.

b. Each partner is personally liable for all partnership obligations. There is no liability limitation unless the partnership is a limited liability partnership.

c. Generally, all business net income of a partnership is subject to self-employment tax, even if the partner is not personally active in the partnership.

d. Partnership income tax and basis adjustment rules can be very complex, particularly with respect to transactions between a partner and partnership.

e. Partners are entitled to very few of the tax deductible fringe benefits that are generally available to employees.

F. Limited Liability Partnerships Limited liability partnerships (LLPs) are a special type of partnership that exists under applicable state law. Relatively

new, they were enacted in response to the concern that a partner of a professional firm can be held liable for the malpractice of another partner in the same firm. LLPs are an alternative available in some states that do not allow professional firms to organize as LLCs.

In some states, LLP partners remain personally liable for the commercial and other obligations of the entity, their

own acts and omissions, and for the acts and omissions of persons under their supervision. However, LLP partners are generally not liable for acts and omissions by the other LLP partners and non-supervised employees (often referred to as “vicarious” liabilities). In states with this type of statute, LLPs provide less liability protection than LLCs, but more than general partnerships. In most states, the LLP statutes provide that LLP partners are not personally liable for the LLP’s contract liabilities unless the partners have personally guaranteed the debt. In such states, LLPs are similar to LLCs with regard to the issue of owner exposure to the entity’s liabilities.

1. Advantages include:

a. As partnerships, they have favorable pass-through taxation status.

b. They have flexibility to structure ownership interests.

2. Disadvantages. The main disadvantage of LLPs (in some states) is that the partners are liable for the debts and other obligations of the LLP (exclusive of liability for professional acts and omissions of others).

12

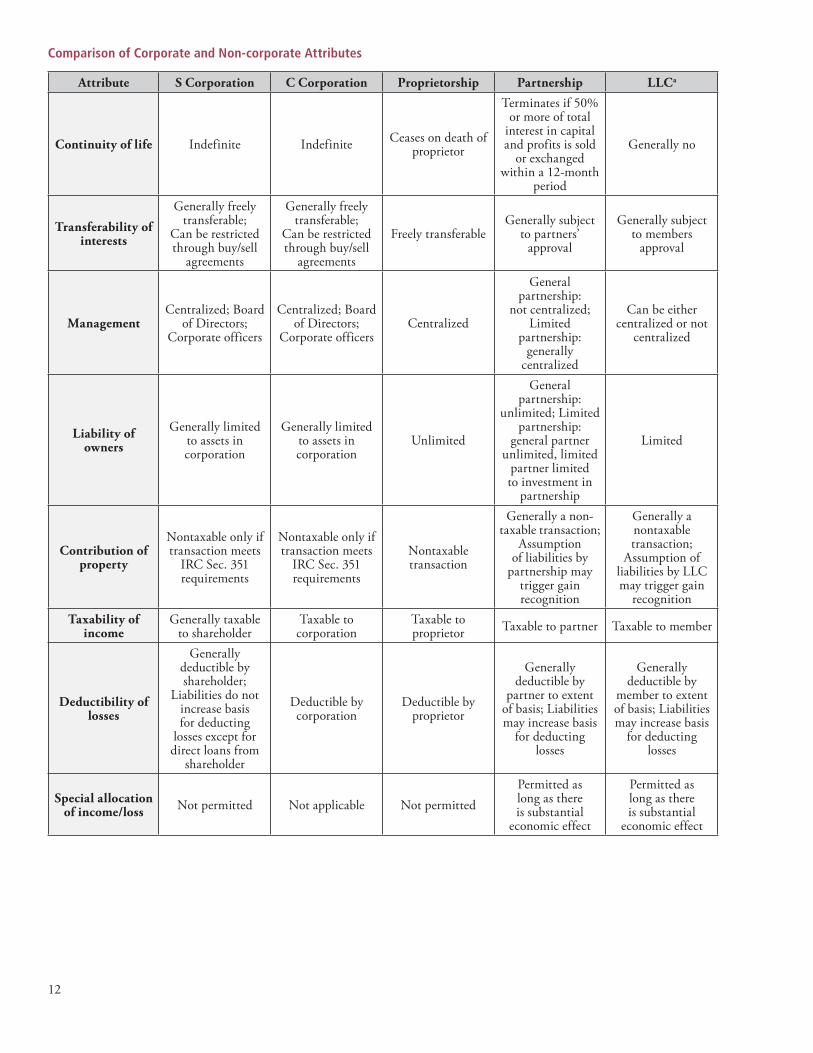

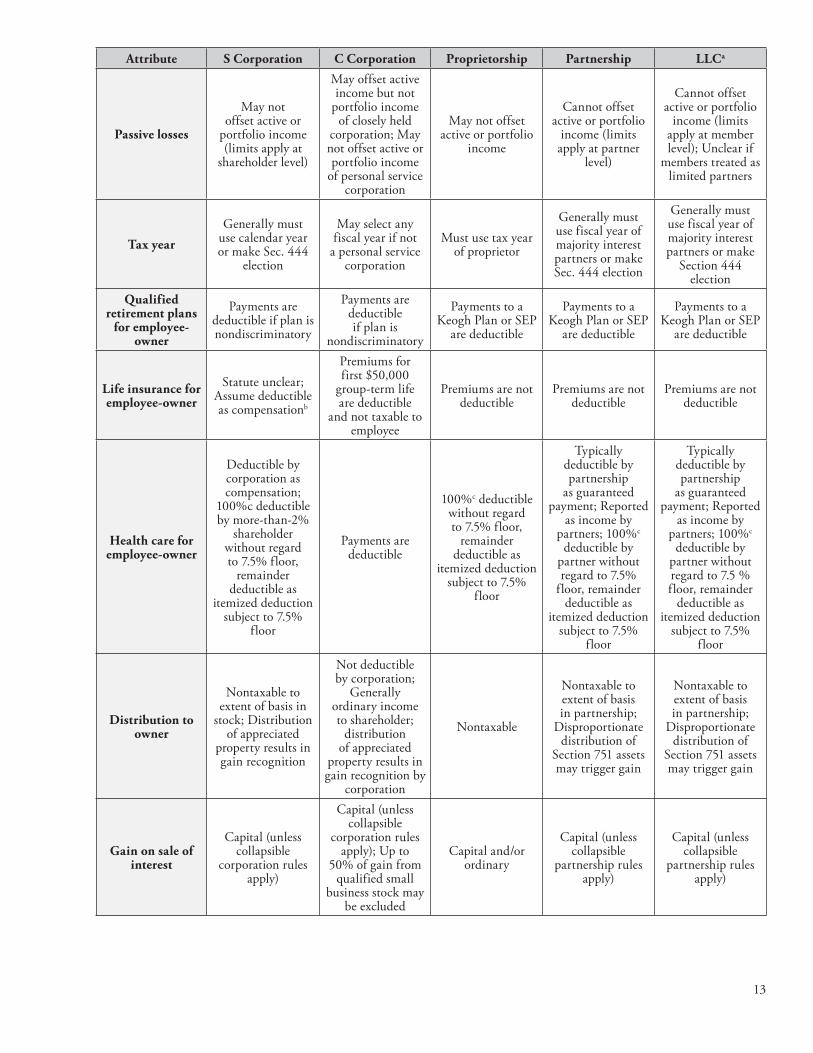

Comparison of Corporate and Non-corporate Attributes

Attribute S Corporation C Corporation Proprietorship Partnership LLCa

Continuity of life Indefinite Indefinite Ceases on death of proprietor

Terminates if 50% or more of total

interest in capital and profits is sold

or exchanged within a 12-month

period

Generally no

Transferability of interests

Generally freely transferable;

Can be restricted through buy/sell

agreements

Generally freely transferable;

Can be restricted through buy/sell

agreements

Freely transferableGenerally subject

to partners’ approval

Generally subject to members

approval

ManagementCentralized; Board

of Directors; Corporate officers

Centralized; Board of Directors;

Corporate officersCentralized

General partnership:

not centralized; Limited

partnership: generally

centralized

Can be either centralized or not

centralized

Liability of owners

Generally limited to assets in corporation

Generally limited to assets in corporation

Unlimited

General partnership:

unlimited; Limited partnership:

general partner unlimited, limited

partner limited to investment in

partnership

Limited

Contribution of property

Nontaxable only if transaction meets

IRC Sec. 351 requirements

Nontaxable only if transaction meets

IRC Sec. 351 requirements

Nontaxable transaction

Generally a non-taxable transaction;

Assumption of liabilities by

partnership may trigger gain recognition

Generally a nontaxable transaction;

Assumption of liabilities by LLC may trigger gain

recognitionTaxability of

incomeGenerally taxable

to shareholderTaxable to corporation

Taxable to proprietor Taxable to partner Taxable to member

Deductibility of losses

Generally deductible by shareholder;

Liabilities do not increase basis for deducting

losses except for direct loans from

shareholder

Deductible by corporation

Deductible by proprietor

Generally deductible by

partner to extent of basis; Liabilities may increase basis

for deducting losses

Generally deductible by

member to extent of basis; Liabilities may increase basis

for deducting losses

Special allocation of income/loss Not permitted Not applicable Not permitted

Permitted as long as there is substantial

economic effect

Permitted as long as there is substantial

economic effect

13

Attribute S Corporation C Corporation Proprietorship Partnership LLCa

Passive losses

May not offset active or

portfolio income (limits apply at

shareholder level)

May offset active income but not

portfolio income of closely held

corporation; May not offset active or portfolio income

of personal service corporation

May not offset active or portfolio

income

Cannot offset active or portfolio

income (limits apply at partner

level)

Cannot offset active or portfolio

income (limits apply at member level); Unclear if

members treated as limited partners

Tax year

Generally must use calendar year or make Sec. 444

election

May select any fiscal year if not

a personal service corporation

Must use tax year of proprietor

Generally must use fiscal year of majority interest partners or make Sec. 444 election

Generally must use fiscal year of majority interest partners or make

Section 444 election

Qualified retirement plans

for employee-owner

Payments are deductible if plan is nondiscriminatory

Payments are deductible if plan is

nondiscriminatory

Payments to a Keogh Plan or SEP

are deductible

Payments to a Keogh Plan or SEP

are deductible

Payments to a Keogh Plan or SEP

are deductible

Life insurance for employee-owner

Statute unclear; Assume deductible as compensationb

Premiums for first $50,000

group-term life are deductible

and not taxable to employee

Premiums are not deductible

Premiums are not deductible

Premiums are not deductible

Health care for employee-owner

Deductible by corporation as compensation;

100%c deductible by more-than-2%

shareholder without regard to 7.5% floor,

remainder deductible as

itemized deduction subject to 7.5%

floor

Payments are deductible

100%c deductible without regard to 7.5% floor,

remainder deductible as

itemized deduction subject to 7.5%

floor

Typically deductible by partnership

as guaranteed payment; Reported

as income by partners; 100%c

deductible by partner without regard to 7.5%

floor, remainder deductible as

itemized deduction subject to 7.5%

floor

Typically deductible by partnership

as guaranteed payment; Reported

as income by partners; 100%c

deductible by partner without regard to 7.5 % floor, remainder

deductible as itemized deduction

subject to 7.5% floor

Distribution to owner

Nontaxable to extent of basis in

stock; Distribution of appreciated

property results in gain recognition

Not deductible by corporation;

Generally ordinary income to shareholder;

distribution of appreciated

property results in gain recognition by

corporation

Nontaxable

Nontaxable to extent of basis in partnership;

Disproportionate distribution of

Section 751 assets may trigger gain

Nontaxable to extent of basis in partnership;

Disproportionate distribution of

Section 751 assets may trigger gain

Gain on sale of interest

Capital (unless collapsible

corporation rules apply)

Capital (unless collapsible

corporation rules apply); Up to

50% of gain from qualified small

business stock may be excluded

Capital and/or ordinary

Capital (unless collapsible

partnership rules apply)

Capital (unless collapsible

partnership rules apply)

14

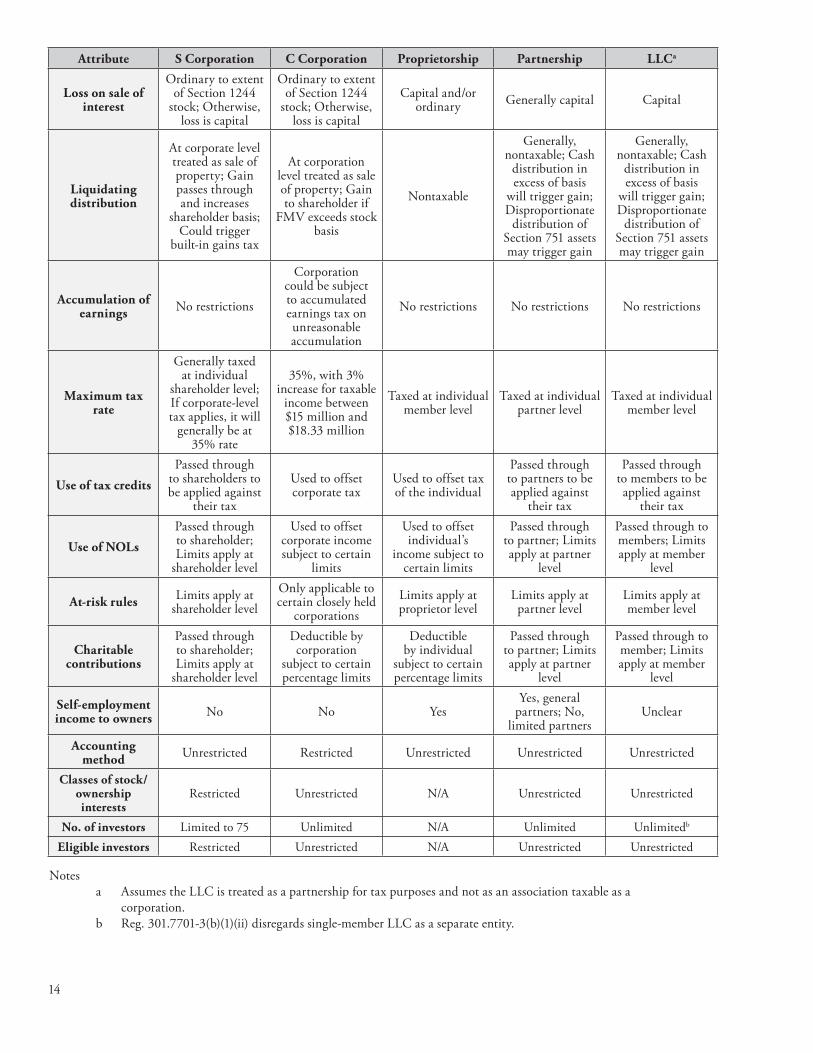

Attribute S Corporation C Corporation Proprietorship Partnership LLCa

Loss on sale of interest

Ordinary to extent of Section 1244

stock; Otherwise, loss is capital

Ordinary to extent of Section 1244

stock; Otherwise, loss is capital

Capital and/or ordinary Generally capital Capital

Liquidating distribution

At corporate level treated as sale of property; Gain passes through and increases

shareholder basis; Could trigger

built-in gains tax

At corporation level treated as sale of property; Gain to shareholder if

FMV exceeds stock basis

Nontaxable

Generally, nontaxable; Cash

distribution in excess of basis

will trigger gain; Disproportionate

distribution of Section 751 assets may trigger gain

Generally, nontaxable; Cash

distribution in excess of basis

will trigger gain; Disproportionate

distribution of Section 751 assets may trigger gain

Accumulation of earnings No restrictions

Corporation could be subject to accumulated earnings tax on unreasonable accumulation

No restrictions No restrictions No restrictions

Maximum tax rate

Generally taxed at individual

shareholder level; If corporate-level tax applies, it will

generally be at 35% rate

35%, with 3% increase for taxable

income between $15 million and $18.33 million

Taxed at individual member level

Taxed at individual partner level

Taxed at individual member level

Use of tax credits

Passed through to shareholders to be applied against

their tax

Used to offset corporate tax

Used to offset tax of the individual

Passed through to partners to be applied against

their tax

Passed through to members to be applied against

their tax

Use of NOLs

Passed through to shareholder; Limits apply at

shareholder level

Used to offset corporate income subject to certain

limits

Used to offset individual’s

income subject to certain limits

Passed through to partner; Limits apply at partner

level

Passed through to members; Limits apply at member

level

At-risk rules Limits apply at shareholder level

Only applicable to certain closely held

corporationsLimits apply at proprietor level

Limits apply at partner level

Limits apply at member level

Charitable contributions

Passed through to shareholder; Limits apply at

shareholder level

Deductible by corporation

subject to certain percentage limits

Deductible by individual

subject to certain percentage limits

Passed through to partner; Limits apply at partner

level

Passed through to member; Limits apply at member

level

Self-employment income to owners No No Yes

Yes, general partners; No,

limited partnersUnclear

Accounting method Unrestricted Restricted Unrestricted Unrestricted Unrestricted

Classes of stock/ownership interests

Restricted Unrestricted N/A Unrestricted Unrestricted

No. of investors Limited to 75 Unlimited N/A Unlimited Unlimitedb

Eligible investors Restricted Unrestricted N/A Unrestricted Unrestricted

Notesa Assumes the LLC is treated as a partnership for tax purposes and not as an association taxable as a

corporation.b Reg. 301.7701-3(b)(1)(ii) disregards single-member LLC as a separate entity.

15

IV. Billing Services

Billing can be a difficult and draining process for a medical practice.

In assessing the necessity of outsourcing your office’s billing department, ask yourself if you or your internal billers can answer these questions:

• How much do you re-bill each week? Does it exceed what you receive in rejections?• How many weeks of A/R do you have outstanding?• How many dollars were written off last month and why?• What does your billing department cost?

If not, or if the answers point to inefficiencies, it may be time to consider outsourcing your billing department.

Through our contacts at Lewis & Knopf, we can assist you in hiring a billing company who will focus on a number of key issues critical to increasing billing collections, including:

• Closely measuring and monitoring the volume of re-billing for the account• Challenging write-off amounts, aging and types of rejections• Making sure that there is a billing submission each week• Watching, questioning and challenging accounts over 90 days old• Implementing monthly meetings to review outstanding problems and issues• Tracking commercial carriers to deal with on a par or non-par basis• Alerting the front desk about patients who are delinquent so pro-active action can be taken• Managing HIPAA and OIG compliance issues

Please contact our service team at Lewis & Knopf at 810-238-4617.

16

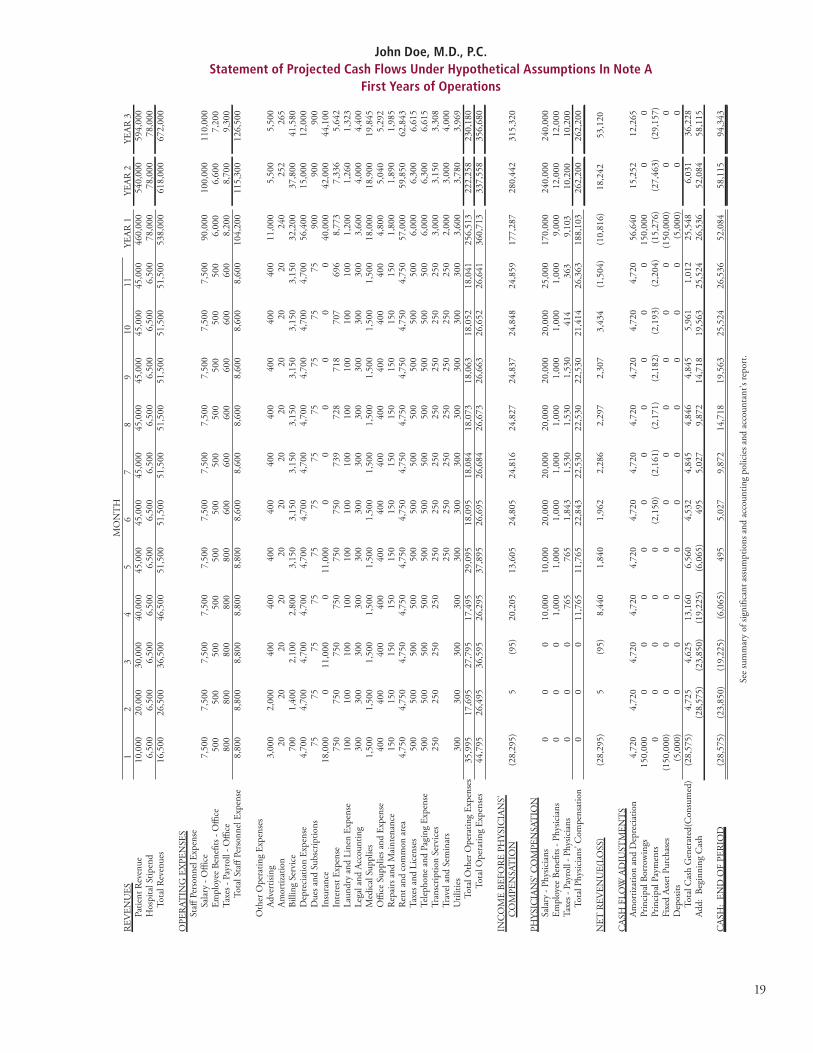

V. Sample Cash Flow Projection

DATE

John Doe M.D., PC

We have compiled the accompanying statement of projected cash flows for the first three years of operations of John Doe M.D., PC in accordance with attestation standards established by the American Institute of Certified Public Accountants. The accompanying projection was prepared for financial institutions to use in negotiating financing of the corporation’s start-up costs.

A compilation is limited to presenting in the form of projection information that is the representation of the owner and does not include evaluation of the support for the assumptions underlying the projection. We have not examined the projection and, accordingly, do not express an opinion or any other form of assurance on the accompanying statement or assumptions. Furthermore, even if the projected volume of billings is attained, the financing is obtained on the projected terms, and the physician compensation are as projected, there will usually be differences between the projected and actual results, because events and circumstances frequently do not occur as expected, and those differences may be material. We have no responsibility to update this report for events and circumstances occurring after the date of this report.

The accompanying projection and this report are intended solely for the information and use of John Doe M.D., PC and XYZ Bank and are not intended to be and should not be used by anyone other than these specified parties.

LEWIS & KNOPF, CPAs, P.C. CERTIFIED PUBLIC ACCOUNTANTS

17

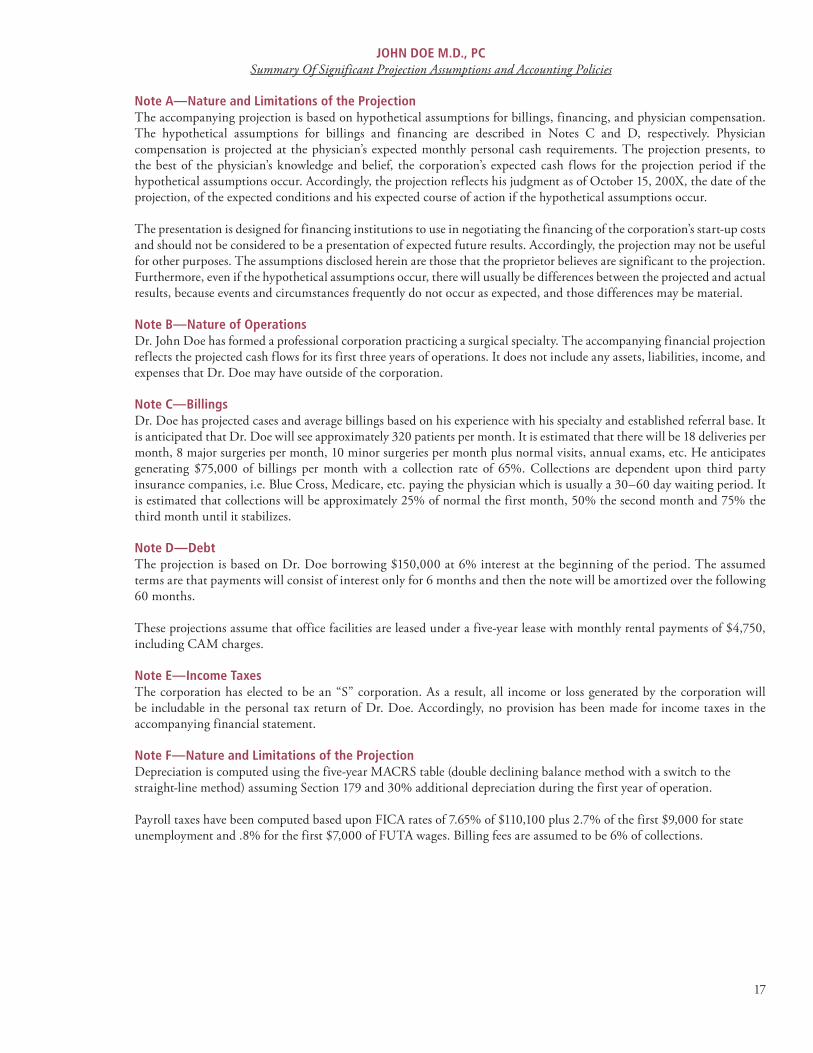

JOHN DOE M.D., PCSummary Of Significant Projection Assumptions and Accounting Policies

Note A—Nature and Limitations of the ProjectionThe accompanying projection is based on hypothetical assumptions for billings, financing, and physician compensation. The hypothetical assumptions for billings and financing are described in Notes C and D, respectively. Physician compensation is projected at the physician’s expected monthly personal cash requirements. The projection presents, to the best of the physician’s knowledge and belief, the corporation’s expected cash flows for the projection period if the hypothetical assumptions occur. Accordingly, the projection reflects his judgment as of October 15, 200X, the date of the projection, of the expected conditions and his expected course of action if the hypothetical assumptions occur.

The presentation is designed for financing institutions to use in negotiating the financing of the corporation’s start-up costs and should not be considered to be a presentation of expected future results. Accordingly, the projection may not be useful for other purposes. The assumptions disclosed herein are those that the proprietor believes are significant to the projection. Furthermore, even if the hypothetical assumptions occur, there will usually be differences between the projected and actual results, because events and circumstances frequently do not occur as expected, and those differences may be material.

Note B—Nature of OperationsDr. John Doe has formed a professional corporation practicing a surgical specialty. The accompanying financial projection reflects the projected cash flows for its first three years of operations. It does not include any assets, liabilities, income, and expenses that Dr. Doe may have outside of the corporation.

Note C—BillingsDr. Doe has projected cases and average billings based on his experience with his specialty and established referral base. It is anticipated that Dr. Doe will see approximately 320 patients per month. It is estimated that there will be 18 deliveries per month, 8 major surgeries per month, 10 minor surgeries per month plus normal visits, annual exams, etc. He anticipates generating $75,000 of billings per month with a collection rate of 65%. Collections are dependent upon third party insurance companies, i.e. Blue Cross, Medicare, etc. paying the physician which is usually a 30–60 day waiting period. It is estimated that collections will be approximately 25% of normal the first month, 50% the second month and 75% the third month until it stabilizes.

Note D—DebtThe projection is based on Dr. Doe borrowing $150,000 at 6% interest at the beginning of the period. The assumed terms are that payments will consist of interest only for 6 months and then the note will be amortized over the following 60 months.

These projections assume that office facilities are leased under a five-year lease with monthly rental payments of $4,750, including CAM charges.

Note E—Income TaxesThe corporation has elected to be an “S” corporation. As a result, all income or loss generated by the corporation will be includable in the personal tax return of Dr. Doe. Accordingly, no provision has been made for income taxes in the accompanying financial statement.

Note F—Nature and Limitations of the ProjectionDepreciation is computed using the five-year MACRS table (double declining balance method with a switch to the straight-line method) assuming Section 179 and 30% additional depreciation during the first year of operation.

Payroll taxes have been computed based upon FICA rates of 7.65% of $110,100 plus 2.7% of the first $9,000 for state unemployment and .8% for the first $7,000 of FUTA wages. Billing fees are assumed to be 6% of collections.

18

VI. Physician Compensation Planning

In practices consisting of more than one physician, disputes often arise. It is important that the group has a “meeting of the minds” as to how the profits are going to be split. Ideally, this would occur at inception so the players know the “rules of the game.” As human beings, we each have different interests. For instance, one doctor may enjoy belonging to a country club while the other enjoys driving a lavish car. These differences must be planned for to keep everyone happy.

We view these types of discretionary expenses as part of the physician’s compensation package. Thus, all of these additional expenses should be considered when the profits are allocated at the end of the year. We have helped hundreds of healthcare professionals design a compensation plan that will fit their specific wants and needs.

The profitability of the practice can be divided up several different ways. Factors that should at least be considered by the physicians are the following:

• Stock Ownership• Seniority• Night and Holiday Shift Work• Production of Each Physician

Below are some commonly used methods to divide profits. These examples are illustrated here to give you a starting point upon which you might consider when designing your own compensation plan.

A. Per Capita Basis In some practices the compensation is split up equally. This method is most common in hospital-based practices

such as those of anesthesiologists, pathologists, and radiologists. A slight variation to this method might take into account holiday and shift work performed.

B. Incentive Compensation Arrangements These types of arrangements are designed to reward based on attributes the group deems important. Often groups

recognize that a portion of the profits should be split on the per capita basis. Physicians then split the remaining profits based on net collections by physicians. This division recognizes that a core part of the profitability of the practice is attributable to each of the physicians equally just as they equally bear call and night shift duties while also recognizing that some physicians work harder or are more efficient. A slight variation to this method includes a “seniority portion” using a “points system.”

C. Remember A poor compensation plan, both real and/or perceived, destroys more physician relationships than any other issue

in the group. It is imperative that a method of splitting profits be devised that is fair to all concerned.

19

John Doe, M.D., P.C.Statement of Projected Cash Flows Under Hypothetical Assumptions In Note A

First Years of Operations

20

VII. Retirement PlansA. What Is a Defined Contribution Plan?

A defined contribution plan provides each participant with an individual account to which annual contributions are credited. The retirement benefit equals the amount contributed to the account, adjusted by any income, expenses, forfeitures, gains, and losses allocated to the account. The individual account feature makes these plans popular with employees because they can “see” what they are getting.

Depending on the plan type, the employer’s annual contributions can be either “fixed” (the amount determined by a plan formula) or “flexible” (the employer can annually determine the amount, if any, contributed). Plan earnings, gains, and losses are allocated to individual participant accounts, usually in proportion to participant account balances. Special allocation methods such as permitted disparity or an age-weighted formula can be used to maximize benefits to highly compensated employees.

Commonly used types of defined contribution plans are:

• Profit-sharing plans• 401(k) plans which are cash or deferral arrangement that are part of a profit sharing plan

These plans are described in the following paragraphs:

1. What is a Profit-sharing Plan?A profit sharing plan is a plan in which the employer agrees to make discretionary contributions. The contributions may be keyed to the company’s profits, although current or accumulated profits are not required for the company to make a contribution. However, the plan document governs, employers wanting flexibility in making contributions will also find a profit-sharing plan to be appealing. A profit-sharing plan that allows discretionary contributions enables an employer to decide on a year-to-year basis whether or not to contribute to the plan and, if so, what amount. That is, if the plan document states the contributions are dependent on profits, this is the rule for that particular plan. A contribution formula based on profits may be used by employers to encourage productivity. These plans must define profits to be used for contributions.

Contributions to profit-sharing plans must be “recurring and substantial.” This does not mean that contributions must be made each year, but it may preclude long periods without contributions particularly when the company has shown profits during those years. If the IRS determines that the contributions have not been recurring or substantial, it will generally rule that the plan is terminated in the year following the last significant contribution.

Once made, plan contributions are allocated to separate participant accounts the plan maintains for each employee. This allocation is made under the method as prescribed by the plan, usually based on the employee’s compensation relative to the compensation of all plan participants. Under IRS regulations, basing the allocation of plan contributions on factors that combine the participant’s age and compensation may be possible.

Because profit-sharing contributions can be flexible, these plans are suitable for start-up companies, companies in cyclical industries, or companies simply wanting flexibility and discretion in determining plan costs.

2. What is a Cash or Deferred Arrangement Plan [401(k) Plan]?A cash or deferred arrangement plan (CODA), usually known as a 401(k) plan, is a profit-sharing or stock bonus plan that also allows before-tax employee contributions. These 401(k) plans may also permit after-tax employee contributions in addition to before-tax amounts. Employee contributions, both before-tax and after-tax, and employer matching contributions are subject to limits the Internal Revenue Code imposes.

21

Although it is possible for 401(k) plans to be funded strictly from employee contributions, this is usually not the case because:

• The maximum percentage highly compensated employees (HCEs) (including owners) can contribute is limited by the average percentage contributed by non-highly compensated employees (NHCEs). Accordingly, to encourage plan participation among these employees, businesses generally match at least a portion of each employee’s contributions to the plan.

• If the plan is top-heavy, which many small plans are, a minimum employer contribution is required.

From a business’s perspective, the advantage of a 401(k) plan is that the employees share at least a portion of the annual contribution burden. This shared burden helps businesses with tight cash flow that could not establish a plan if they had to make the entire contribution on their own. Except for reasons of hardship, distributions of an employee’s pretax contributions cannot be made before retirement, death, disability, separation from service, or attainment of age 59 ½.

In addition to the regular 401(k) plans that have been around for many years, there are two additional types of 401(k) plans that should be considered for small employers. They are the safe harbor 401(k) plans, safe harbor Roth 401(k) plans, and SIMPLE 401(k) plans.

a. Safe Harbor Rules Provide Alternative to Nondiscrimination Testing. The first is actually “safe harbor” provisions that if complied with and elected by the employer may be

used to pass the nondiscrimination requirements for the plan. There are notice requirements and employer contributions required to satisfy these provisions.

Safe harbor 401(k) plans allow an employer to make certain contributions to a 401(k) plan as an alternate method of meeting the nondiscrimination requirements. Under this safe harbor, a plan passes the discrimination test if certain notice and vesting requirements are met (all safe harbor contributions and match amounts must be fully vested), the plan document specifies that the ADP safe harbor testing method is being used, and the employer provides any of the following:

1) A non-elective contribution of:

+ At least 3% for each eligible NHCE.

2) A basic matching formula of:

+ 100% of the employee’s elective contributions up to 3% of compensation, and

+ 50% of the employee’s elective contributions in excess of 3% but no greater than 5% of compensation, where the matching contribution rate for HCEs does not exceed that for the NHCEs.

3) An enhanced matching formula such that:

+ The rate of the employer’s matching contribution does not increase as an employee’s rate of elective contribution increases, and

+ The aggregate amount of matching contributions at any elective contribution rate is at least as much as the aggregate amount of matching contributions required under the basic matching formula (e.g., 100% of contributions up to 3% of compensation and 50% of contributions from 3% to 5% of compensation).

EGTRRA provides that matching or non-elective contributions under a safe harbor 401(k) plan may be taken into account in satisfying the top-heavy minimum contribution for plan years beginning after 2001.

22

b. SIMPLE 401(k) Plans Have Limited Appeal. SIMPLE 401(k) plans offer few advantages to employers. They are qualified plans and therefore must

comply with the reporting requirements and several of the other requirements for qualified plans. They are not subject to the nondiscrimination requirements.

c. Comparability Plans As with age-weighted plans, comparability plans are based on equivalent future benefits, rather than

equivalent contributions. Comparability or cross-tested plans are age-weighted by groups of employees, not by individuals.

New comparability and other defined contribution plans (such as age-weighted plans) that attempt to pass the nondiscrimination rules by cross-testing, work best when the average age of the employees the company wants to favor (normally the owners) is greater than the average age of the other employees.

d. Comparability Plans That Include a 401(k) Feature. The final regulations clarify some provisions related to comparability profit-sharing plans that include a

Section 401(k) feature. Any non-elective contributions, such as the 3% safe harbor employer contribution [for a safe-harbor 401(k) or a top heavy plan], will count toward the minimum allocation requirement needed to pass the gateway test. This allows (a) HCEs to make elective deferrals, without increasing the minimum required allocation and (b) any non-elective employer contributions to be included in satisfying the gateway minimum allocation requirement. These provisions, coupled with the EGTTRA changes that exclude 401(k) deferrals from being counted as part of the employer contribution and increase the deferral, contribution, and annual addition limits will significantly increase the possibilities for new comparability plans.

1) If there are a few younger owner-employees that are causing difficulty with the discrimination testing for a new comparability plan, consider adding 401(k) features to the plan and have only the younger owner-employees make deferrals along with the rank-and-file employees. This will help reduce their need for higher profit-sharing contributions.

2) If there are multiple owners who desire different contribution levels, a new comparability plan can be used to provide differing levels of contributions. For example, in the case of a group of physicians where the physicians cannot agree on the level for the profit-sharing contribution, consider establishing two groups for the physicians and one for the office staff. Allow the older physicians to have a $50,000 maximum contribution and the younger physicians (who have cash needs to buy out the older physicians, send children to college, etc.) to have a lower level of contribution. The contribution for the office staff will be calculated as the amount necessary to meet discrimination-testing requirements.

B. What is a Simplified Employee Pension Plan (SEP)?

A simplified employee pension plan (SEP) is a written arrangement that allows an employer to make contributions to individual retirement arrangements (referred to as SEP-IRAs) established by (or on the behalf of) each qualifying employee.

Although designed for small businesses, any employer (sole proprietorship, partnership, limited liability company, or corporation) regardless of its size or number of employees may generally establish and maintain an SEP. SEPs are established at the employer level, rather than the employee level. SEPs are relatively easy to establish and administer. They are not subject to the complex vesting, participation, nondiscrimination, reporting, and other rules applying to qualified plans. Furthermore, unlike a qualified plan, a SEP can be established after the employer’s year-end. However, to receive favorable tax benefits, SEPs must meet the following special requirements:

• Special participation requirements must be met. • Contributions must not discriminate in favor of highly compensated employees (HCEs). • Contributions must be made under a written allocation formula. • Contributions must be fully vested when made and withdrawals must be permitted.

23

What are the Participation Requirements? Employer contributions to a SEP are discretionary, and thus, may be made on a year-to-year basis. However, if employer

contributions are made for a year, they must be made on behalf of all eligible employees. Any employee who satisfies the requirements at any time during the year must be eligible to participate in the plan, including those who die or terminate employment during the year. An eligible employee is one who meets all of the following participation requirements:

• The Age Requirement. An employee who has attained age 21 has met this requirement.• The Service Requirement. An employee who has performed any services for the employer during at least

three of the preceding five years has met this requirement.• The Compensation Requirement. An employee who has received compensation as defined on an annual

basis by the IRS has met this requirement.

Leased employees, employees of commonly controlled businesses, owner-employees, and employees who have attained age 70½ must be considered when determining eligible employees.

C. What is a Savings Incentive Match Plan for Employees (SIMPLE) IRA Plan?

A SIMPLE IRA plan is a written salary reduction arrangement under which eligible employees can elect to have the employer make contributions to a SIMPLE IRA rather than receiving that amount in cash. Under such a plan, employees can elect to defer up to $11,500 ($14,000 if age 50 or older) of their compensation for 2012. Employers are required to either match this deferral (up to 3% of the employee’s compensation), or make a 2% contribution on behalf of all eligible employees (regardless of whether the employees elect to defer any of their own money). The SIMPLE IRA plan must be the only employer-sponsored retirement plan for the year and is only available to a small business (one with 100 or fewer employees when considering only those employees who earned at least $5,000 of compensation during the preceding year).

An employer can generally establish a SIMPLE IRA plan effective on any date between January 1 and October 1 of the year. However, if an employer (or predecessor employer) previously maintained a SIMPLE IRA plan, a new SIMPLE IRA plan can be established effective only on January 1. Also, a new employer that comes into existence after October 1 can establish a SIMPLE IRA plan effective between October 1 (keep on same line) and December 31 if the plan is established as soon as administratively feasible after the employer comes into existence.

Employer Contributions Once a SIMPLE IRA plan is established, employers are required to make contributions using one of the following two

contribution formulas:

1) Matching Contribution Formula. Under this formula, the employer must generally match employee contributions on a dollar-for-dollar basis, up to 3% of the employee’s compensation for the calendar year. However, in two out of every five years, the employer has the option of electing a matching percentage as low as 1% of each eligible employee’s compensation. For purposes of the matching contribution, compensation is not limited. Therefore, an employee who earns $300,000 could receive a $9,000 ($300,000 × 3%) match.

2) Non-elective Contribution Formula. In lieu of making matching contributions for a year, an employer may make a non-elective contribution of 2% of compensation for each eligible employee (regardless of whether the employees put any of their own money in the plan). The employer may, but is not required to, limit non-elective contributions to eligible employees who have at least $5,000 (or some lower amount selected by the employer) of compensation for the year. For this purpose, compensation of each eligible participant is limited to $250,000 for 2012, thus limiting the contribution to $5,000 per employee ($250,000 × 2%).

24

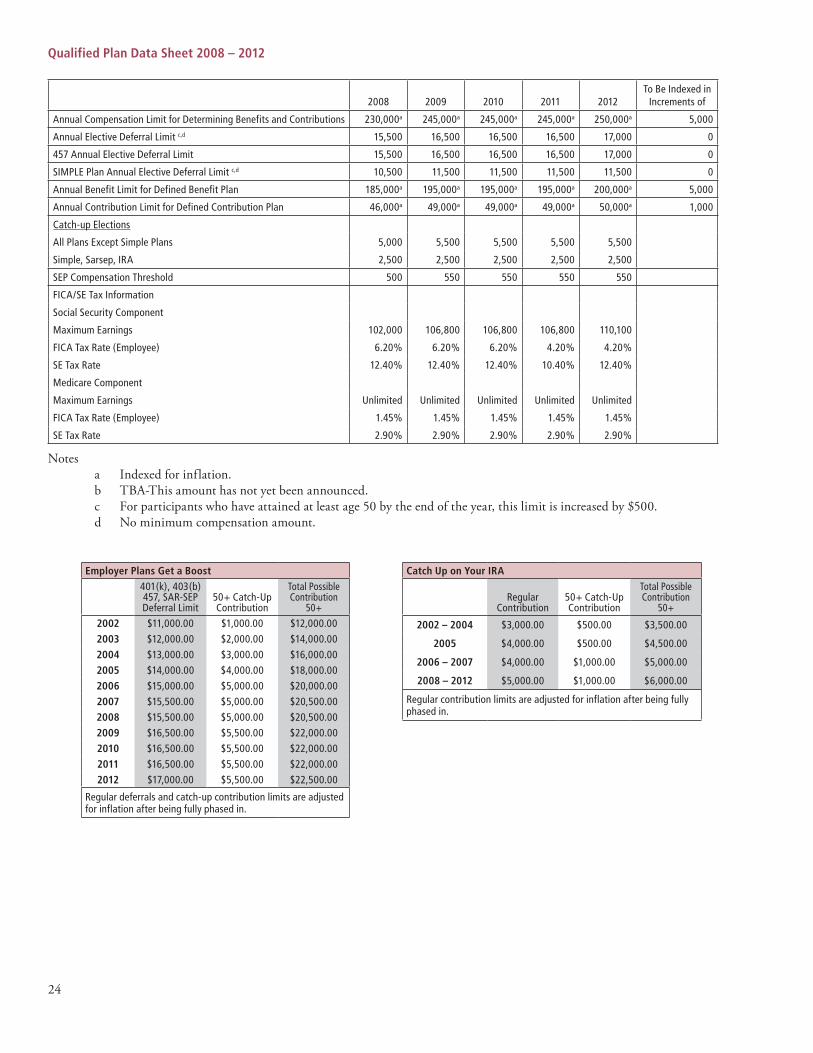

Qualified Plan Data Sheet 2008 – 2012

Notesa Indexed for inflation.b TBA-This amount has not yet been announced.c For participants who have attained at least age 50 by the end of the year, this limit is increased by $500.d No minimum compensation amount.

Employer Plans Get a Boost401(k), 403(b)457, SAR-SEP Deferral Limit

50+ Catch-Up Contribution

Total Possible Contribution

50+2002 $11,000.00 $1,000.00 $12,000.002003 $12,000.00 $2,000.00 $14,000.002004 $13,000.00 $3,000.00 $16,000.002005 $14,000.00 $4,000.00 $18,000.002006 $15,000.00 $5,000.00 $20,000.002007 $15,500.00 $5,000.00 $20,500.002008 $15,500.00 $5,000.00 $20,500.002009 $16,500.00 $5,500.00 $22,000.002010 $16,500.00 $5,500.00 $22,000.002011 $16,500.00 $5,500.00 $22,000.002012 $17,000.00 $5,500.00 $22,500.00

Regular deferrals and catch-up contribution limits are adjusted for inflation after being fully phased in.

Catch Up on Your IRA

Regular Contribution

50+ Catch-Up Contribution

Total Possible Contribution

50+

2002 – 2004 $3,000.00 $500.00 $3,500.00

2005 $4,000.00 $500.00 $4,500.00

2006 – 2007 $4,000.00 $1,000.00 $5,000.00

2008 – 2012 $5,000.00 $1,000.00 $6,000.00

Regular contribution limits are adjusted for inflation after being fully phased in.

2008 2009 2010 2011 2012To Be Indexed in

Increments of

Annual Compensation Limit for Determining Benefits and Contributions 230,000a 245,000a 245,000a 245,000a 250,000a 5,000

Annual Elective Deferral Limit c,d 15,500 16,500 16,500 16,500 17,000 0

457 Annual Elective Deferral Limit 15,500 16,500 16,500 16,500 17,000 0

SIMPLE Plan Annual Elective Deferral Limit c,d 10,500 11,500 11,500 11,500 11,500 0

Annual Benefit Limit for Defined Benefit Plan 185,000a 195,000a 195,000a 195,000a 200,000a 5,000

Annual Contribution Limit for Defined Contribution Plan 46,000a 49,000a 49,000a 49,000a 50,000a 1,000

Catch-up Elections

All Plans Except Simple Plans 5,000 5,500 5,500 5,500 5,500

Simple, Sarsep, IRA 2,500 2,500 2,500 2,500 2,500

SEP Compensation Threshold 500 550 550 550 550

FICA/SE Tax Information

Social Security Component

Maximum Earnings 102,000 106,800 106,800 106,800 110,100

FICA Tax Rate (Employee) 6.20% 6.20% 6.20% 4.20% 4.20%

SE Tax Rate 12.40% 12.40% 12.40% 10.40% 12.40%

Medicare Component

Maximum Earnings Unlimited Unlimited Unlimited Unlimited Unlimited

FICA Tax Rate (Employee) 1.45% 1.45% 1.45% 1.45% 1.45%

SE Tax Rate 2.90% 2.90% 2.90% 2.90% 2.90%

25

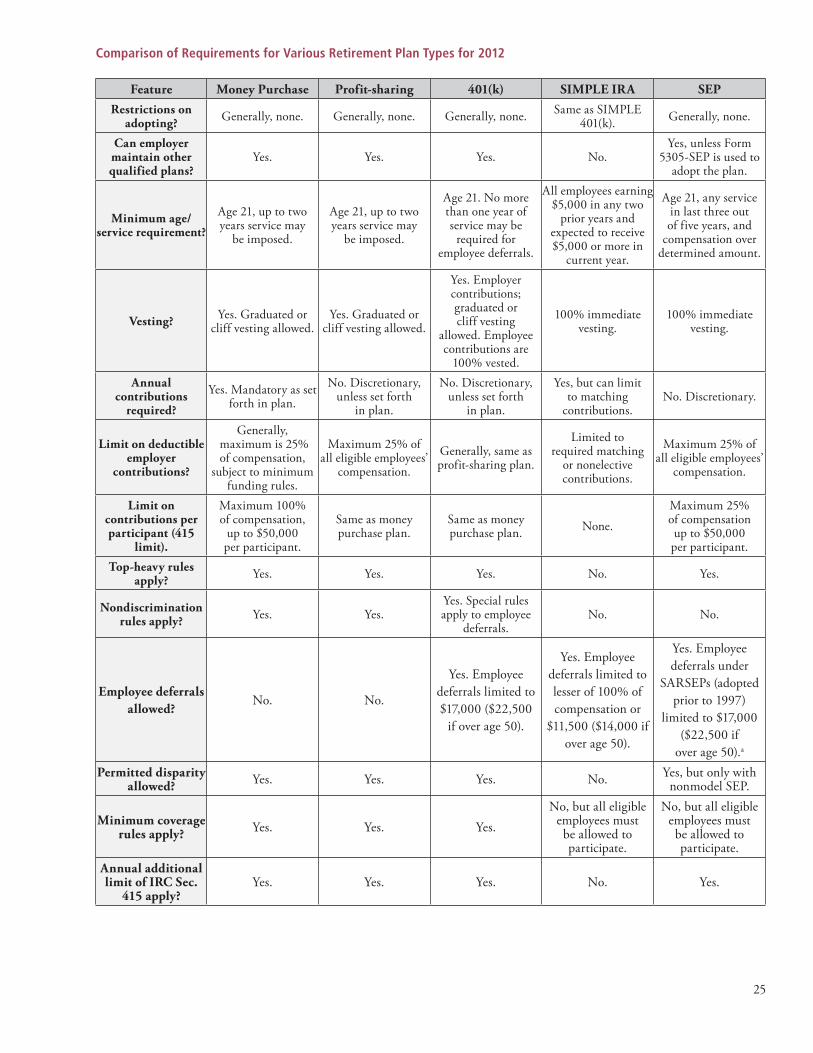

Comparison of Requirements for Various Retirement Plan Types for 2012

Feature Money Purchase Profit-sharing 401(k) SIMPLE IRA SEPRestrictions on

adopting? Generally, none. Generally, none. Generally, none. Same as SIMPLE 401(k). Generally, none.

Can employer maintain other qualified plans?

Yes. Yes. Yes. No.Yes, unless Form

5305-SEP is used to adopt the plan.

Minimum age/service requirement?

Age 21, up to two years service may

be imposed.

Age 21, up to two years service may

be imposed.

Age 21. No more than one year of service may be

required for employee deferrals.

All employees earning $5,000 in any two

prior years and expected to receive $5,000 or more in

current year.

Age 21, any service in last three out of five years, and

compensation over determined amount.

Vesting? Yes. Graduated or cliff vesting allowed.

Yes. Graduated or cliff vesting allowed.

Yes. Employer contributions; graduated or cliff vesting

allowed. Employee contributions are

100% vested.

100% immediate vesting.

100% immediate vesting.

Annual contributions

required?

Yes. Mandatory as set forth in plan.

No. Discretionary, unless set forth

in plan.

No. Discretionary, unless set forth

in plan.

Yes, but can limit to matching

contributions.No. Discretionary.

Limit on deductible employer

contributions?

Generally, maximum is 25% of compensation,

subject to minimum funding rules.

Maximum 25% of all eligible employees’

compensation.

Generally, same as profit-sharing plan.

Limited to required matching

or nonelective contributions.

Maximum 25% of all eligible employees’

compensation.

Limit on contributions per participant (415

limit).

Maximum 100% of compensation,

up to $50,000 per participant.

Same as money purchase plan.

Same as money purchase plan. None.

Maximum 25% of compensation up to $50,000 per participant.

Top-heavy rules apply? Yes. Yes. Yes. No. Yes.

Nondiscrimination rules apply? Yes. Yes.

Yes. Special rules apply to employee

deferrals.No. No.

Employee deferrals allowed?

No. No.

Yes. Employee deferrals limited to $17,000 ($22,500

if over age 50).

Yes. Employee deferrals limited to lesser of 100% of compensation or

$11,500 ($14,000 if over age 50).

Yes. Employee deferrals under

SARSEPs (adopted prior to 1997)

limited to $17,000 ($22,500 if

over age 50).a

Permitted disparity allowed? Yes. Yes. Yes. No. Yes, but only with

nonmodel SEP.

Minimum coverage rules apply? Yes. Yes. Yes.

No, but all eligible employees must be allowed to participate.

No, but all eligible employees must be allowed to participate.

Annual additional limit of IRC Sec.

415 apply?Yes. Yes. Yes. No. Yes.

26

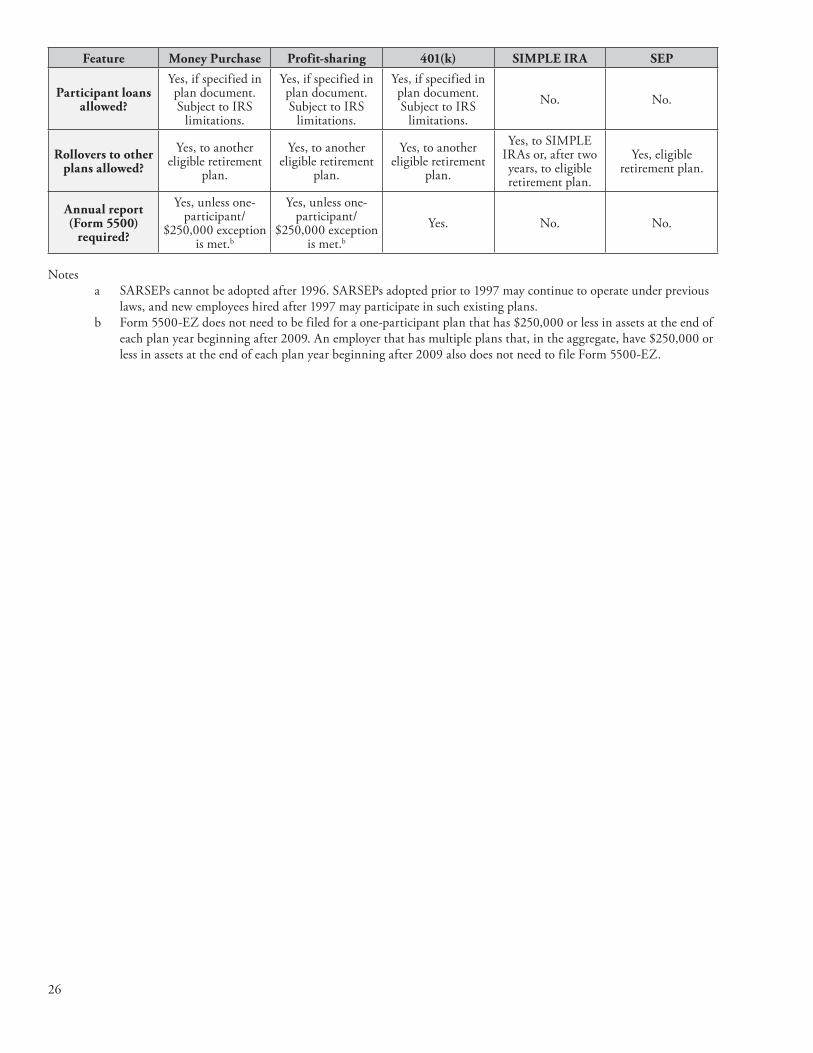

Feature Money Purchase Profit-sharing 401(k) SIMPLE IRA SEP

Participant loans allowed?

Yes, if specified in plan document. Subject to IRS

limitations.

Yes, if specified in plan document. Subject to IRS

limitations.

Yes, if specified in plan document. Subject to IRS

limitations.No. No.

Rollovers to other plans allowed?

Yes, to another eligible retirement

plan.

Yes, to another eligible retirement

plan.

Yes, to another eligible retirement

plan.

Yes, to SIMPLE IRAs or, after two years, to eligible retirement plan.

Yes, eligible retirement plan.

Annual report (Form 5500)

required?

Yes, unless one-participant/

$250,000 exception is met.b

Yes, unless one-participant/

$250,000 exception is met.b

Yes. No. No.

Notesa SARSEPs cannot be adopted after 1996. SARSEPs adopted prior to 1997 may continue to operate under previous

laws, and new employees hired after 1997 may participate in such existing plans.b Form 5500-EZ does not need to be filed for a one-participant plan that has $250,000 or less in assets at the end of

each plan year beginning after 2009. An employer that has multiple plans that, in the aggregate, have $250,000 or less in assets at the end of each plan year beginning after 2009 also does not need to file Form 5500-EZ.

27

VIII. Other Fringe Benefits There are a variety of fringe benefits available to the healthcare professional. You will hear all sorts of stories from fellow physicians in the lunchroom discussing all of the things they deduct through their corporation. Although it may be true, that does not necessarily mean it’s right. At Lewis & Knopf CPAs, we believe that you should run all expenses related to your business through your corporation. It is important that you remember that these business expenses must be documented. Below we have attempted to list a few of the items you should consider.

A. Health Insurance Health insurance costs are rising at an ever-increasing rate. We suggest that you contact an insurance broker to help

you find the plan that meets your needs at a reasonable cost. On a limited basis, you can discriminate in favor of the employer with respect to health insurance coverage.

B. Disability Insurance We at Lewis & Knopf CPAs believe that young physicians should buy as much disability coverage as the insurance

carrier will write. Statistically, the risk of disability is greater during the physician’s working lifetime than the risk of death. Once your financial responsibilities to your family decline later in life, you can decrease your coverage. There are several schools of thought on who should pay the premiums, the corporation or the individual. We believe that the individual should pay the premiums personally. If you become disabled, the disability benefits you collect will be tax-free.

C. Life Insurance There are many types of life insurance you can choose from. They include, but are not limited to, term life insurance,

whole life, universal life, and variable life. Term can provide the most coverage at the cheapest cost, however, the cost increases as the insured gets older. Discussion of other life insurance policies is beyond the scope of this book. Please see our list of recommended insurance agents who will work as part of the team to protect your future.

D. Automobiles Your automobile used for your business must be charged through the corporation. There are several record keeping

requirements that we would be glad to discuss with you. Believe it or not, a vehicle costing more than approximately $15,000 is considered to be a luxury automobile by the IRS! Consequently, your write-offs are limited. However, vehicles weighing more than 6,000 pounds, i.e. Chevy Tahoe/Suburban, GMC Yukon, Ford Expedition, etc., are not considered to be luxury automobiles. The write-offs of these vehicles are significantly greater. Leasing is also an option that you should consider (especially those vehicles weighing less than 6,000 pounds). REMEMBER—the personal use portion, (commuting from home to work and back to home is personal use), must be included in your annual compensation (W-2).

E. Country Club Memberships and Entertainment Expenses Dues for country clubs, health clubs, etc. are not deductible for tax purposes. However, they can still be paid

through the business. Entertainment expenses related to the business are deductible with some limitations. We would be happy to explain these rules to you.

F . Cafeteria Plans If you are interested in your employees sharing in the cost of providing fringe benefits to them, you should consider

a Section 125 plan otherwise known as a cafeteria plan. Employees can select from a menu of fringe benefits they want to have withheld from their paycheck. If you choose to be an “S corporation,” the owner physician will not be able to participate in this plan.

28

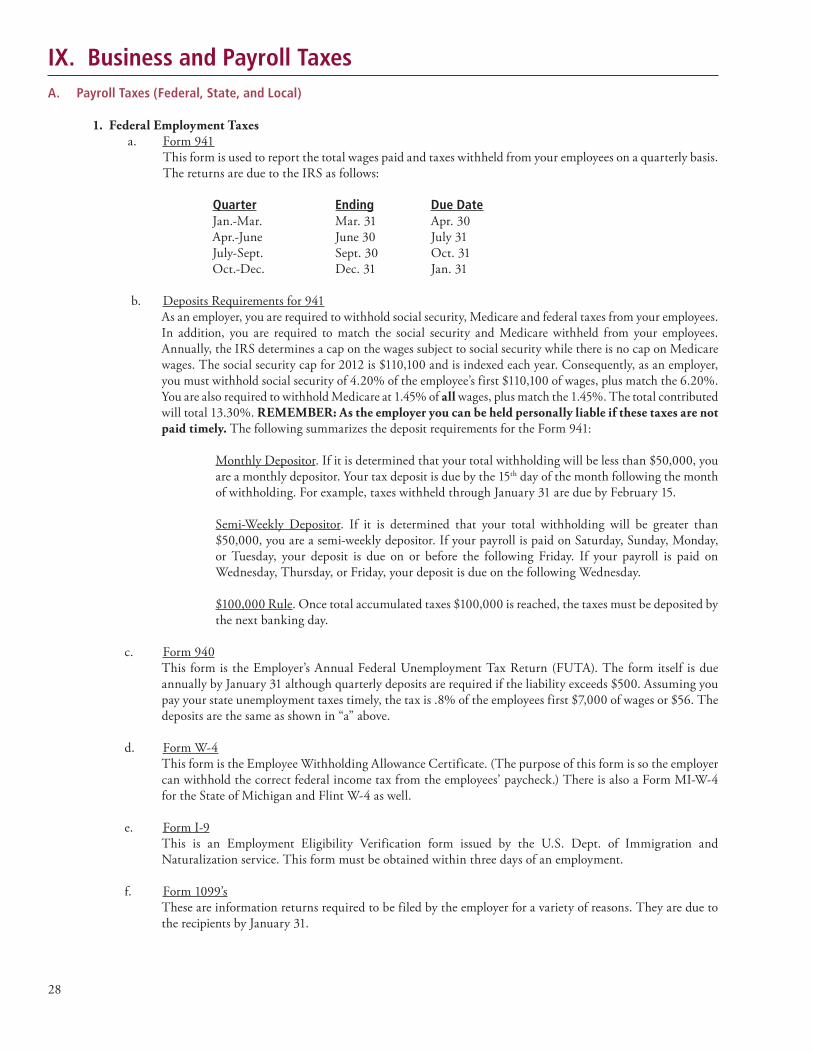

IX. Business and Payroll TaxesA. Payroll Taxes (Federal, State, and Local)

1. Federal Employment Taxes a. Form 941 This form is used to report the total wages paid and taxes withheld from your employees on a quarterly basis. The returns are due to the IRS as follows:

Quarter Ending Due DateJan.-Mar. Mar. 31 Apr. 30Apr.-June June 30 July 31July-Sept. Sept. 30 Oct. 31Oct.-Dec. Dec. 31 Jan. 31

b. Deposits Requirements for 941 As an employer, you are required to withhold social security, Medicare and federal taxes from your employees. In addition, you are required to match the social security and Medicare withheld from your employees. Annually, the IRS determines a cap on the wages subject to social security while there is no cap on Medicare wages. The social security cap for 2012 is $110,100 and is indexed each year. Consequently, as an employer, you must withhold social security of 4.20% of the employee’s first $110,100 of wages, plus match the 6.20%. You are also required to withhold Medicare at 1.45% of all wages, plus match the 1.45%. The total contributed will total 13.30%. REMEMBER: As the employer you can be held personally liable if these taxes are not paid timely. The following summarizes the deposit requirements for the Form 941:

Monthly Depositor. If it is determined that your total withholding will be less than $50,000, you are a monthly depositor. Your tax deposit is due by the 15th day of the month following the month of withholding. For example, taxes withheld through January 31 are due by February 15.

Semi-Weekly Depositor. If it is determined that your total withholding will be greater than $50,000, you are a semi-weekly depositor. If your payroll is paid on Saturday, Sunday, Monday, or Tuesday, your deposit is due on or before the following Friday. If your payroll is paid on Wednesday, Thursday, or Friday, your deposit is due on the following Wednesday.

$100,000 Rule. Once total accumulated taxes $100,000 is reached, the taxes must be deposited by the next banking day.

c. Form 940 This form is the Employer’s Annual Federal Unemployment Tax Return (FUTA). The form itself is due annually by January 31 although quarterly deposits are required if the liability exceeds $500. Assuming you pay your state unemployment taxes timely, the tax is .8% of the employees first $7,000 of wages or $56. The deposits are the same as shown in “a” above.

d. Form W-4 This form is the Employee Withholding Allowance Certificate. (The purpose of this form is so the employer can withhold the correct federal income tax from the employees’ paycheck.) There is also a Form MI-W-4 for the State of Michigan and Flint W-4 as well.

e. Form I-9 This is an Employment Eligibility Verification form issued by the U.S. Dept. of Immigration and Naturalization service. This form must be obtained within three days of an employment.

f. Form 1099’s These are information returns required to be filed by the employer for a variety of reasons. They are due to the recipients by January 31.

29

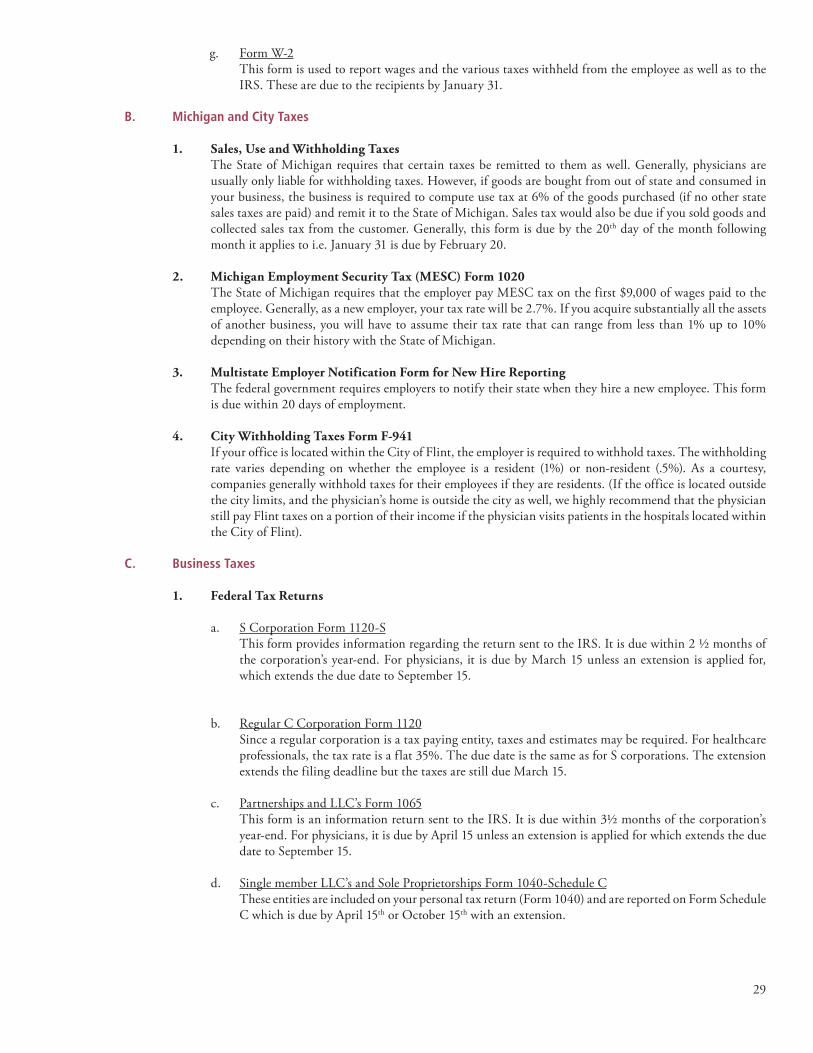

g. Form W-2 This form is used to report wages and the various taxes withheld from the employee as well as to the

IRS. These are due to the recipients by January 31.

B. Michigan and City Taxes

1. Sales, Use and Withholding Taxes The State of Michigan requires that certain taxes be remitted to them as well. Generally, physicians are

usually only liable for withholding taxes. However, if goods are bought from out of state and consumed in your business, the business is required to compute use tax at 6% of the goods purchased (if no other state sales taxes are paid) and remit it to the State of Michigan. Sales tax would also be due if you sold goods and collected sales tax from the customer. Generally, this form is due by the 20th day of the month following month it applies to i.e. January 31 is due by February 20.

2. Michigan Employment Security Tax (MESC) Form 1020 The State of Michigan requires that the employer pay MESC tax on the first $9,000 of wages paid to the

employee. Generally, as a new employer, your tax rate will be 2.7%. If you acquire substantially all the assets of another business, you will have to assume their tax rate that can range from less than 1% up to 10% depending on their history with the State of Michigan.

3. Multistate Employer Notification Form for New Hire Reporting The federal government requires employers to notify their state when they hire a new employee. This form

is due within 20 days of employment.

4. City Withholding Taxes Form F-941 If your office is located within the City of Flint, the employer is required to withhold taxes. The withholding

rate varies depending on whether the employee is a resident (1%) or non-resident (.5%). As a courtesy, companies generally withhold taxes for their employees if they are residents. (If the office is located outside the city limits, and the physician’s home is outside the city as well, we highly recommend that the physician still pay Flint taxes on a portion of their income if the physician visits patients in the hospitals located within the City of Flint).

C. Business Taxes

1. Federal Tax Returns

a. S Corporation Form 1120-S This form provides information regarding the return sent to the IRS. It is due within 2 ½ months of

the corporation’s year-end. For physicians, it is due by March 15 unless an extension is applied for, which extends the due date to September 15.

b. Regular C Corporation Form 1120 Since a regular corporation is a tax paying entity, taxes and estimates may be required. For healthcare

professionals, the tax rate is a flat 35%. The due date is the same as for S corporations. The extension extends the filing deadline but the taxes are still due March 15.

c. Partnerships and LLC’s Form 1065 This form is an information return sent to the IRS. It is due within 3½ months of the corporation’s

year-end. For physicians, it is due by April 15 unless an extension is applied for which extends the due date to September 15.

d. Single member LLC’s and Sole Proprietorships Form 1040-Schedule C These entities are included on your personal tax return (Form 1040) and are reported on Form Schedule

C which is due by April 15th or October 15th with an extension.

30

2. Michigan Tax Returns

a. Corporate Income Tax (CIT) The CIT takes effect January 1, 2012 and replaces the Michigan Business Tax (MBT). The CIT

applies only to entities taxed as C Corporations. Individuals and flow-through entities, including partnerships, LLC’s, and S Corporations are not subject to CIT. The CIT is equal to 6% of CIT tax base after allocation or apportionment.

b. Michican Business Tax - Prior to 2012 The Michigan Business Tax is comprised of two taxes one calculated on business income and the other

modified gross receipts, and a surcharge. This return is due the last day of the 4th month following your year-end. For physicians, it is due by April 30 unless an extension is applied for which extends the due date to December 31. The extension extends the filing deadline but the taxes are still due April 30. Estimates are required on a quarterly basis and are due April 15, July 15, October 15, and January 15.

c. Michigan Single Business Tax Form C-8000 - prior to 2008 This was a tax on business activity and was quite unusual. Fortunately, the tax expired December

31, 2007 and was replaced with the Michigan Business Tax. The tax rate was 1.9% of your adjusted business income.

d. Michigan Annual Report Form MAR This information form is required annually by the State of Michigan. The fee is $25 and is due by May 15.

3. City Tax Returns

a. Corporate Income Tax Return Form F-1120 This return is due on the last day of the 4th month following the year-end. Generally, this tax is minor

at best since healthcare practices pay out most of the profits to the doctor anyway. Estimates can be required and are due April 30, June 30, September 30, and January 31.

b. Partnership Tax Return Form F-1065 This return is due the last day of the 4th month following the year-end or April 30. Generally, it is an

information return although it can elect to pay the partner’s city tax on their behalf.

31

X. Buy/Sell Agreements There are many choices that must be made concerning the financial aspects of a physician entering or leaving a multi-