roundtable on natural gas vehicles in fleets · pdf fileroundtable on natural gas vehicles in...

TRANSCRIPT

Roundtable on Natural Gas Vehicles in FleetsNational Governors Association

August 28, 2015

What is NGVAmerica?

NGVAmerica is the national trade organization dedicated to the development of a growing, profitable, and sustainable market for vehicles powered by natural gas or renewable natural gas.

NGVAmerica represents the full value chain of the industry including more than 200 companies, environmental and government organizations interested in the promotion and use of natural gas as a transportation fuel.

NGVAmerica members produce, distribute, and market natural gas and renewable natural gas across the country; manufacture and service natural gas vehicles, engines, and equipment; and operate fleets powered by clean-burning gaseous fuels.

Who is NGVAmerica?

Corners of NGVAmerica’s Mission

Lead advocacy efforts with federal and state regulators and policymakers to advance the marketplace and level the playing field with other transportation fuels

Through education & communications be the most credible voice on NGVs and to support information sharing within the industry

Serve as forum for collaboration, discussion, & debate in the interest of developing common standards and best practices for the NGV marketplace

Be the convening authority for NGV industry leaders to gather and discuss issues with business peers, customers, technology experts, and thought leaders

What’s the Value Proposition?Natural Gas as a Transportation Fuel

ECONOMICSo Historically ~8:1 price advantage on Btu basiso $0.75 to $1 lower at the pump than dieselo Federal tax credit $0.50 per gallono Less costly emissions control systems

ENVIRONMENTAL BENEFITSo 20-29% lower GHG emissions than petroleum fuelso 15-21% lower GHG emissions on well to wheels basiso 90% lower GHG emissions with RNG/bio-methaneo 50% lower NOx emissionso Lower particulate matter compared to dieselo Quieter engines

ABUNDANCEo U.S. is now number one NG producer in the worldo Shale gas revolution = decades of affordable reserveso Shale gas basins provide increased access to NGo Production will increase by 56% between 2012 & 2040

ENERGY SECURITYo Almost all NG used in the United States is produced in

North Americao Exporting NG can bolster energy security of other

countrieso Domestic reserves uniquely make the US energy

independent

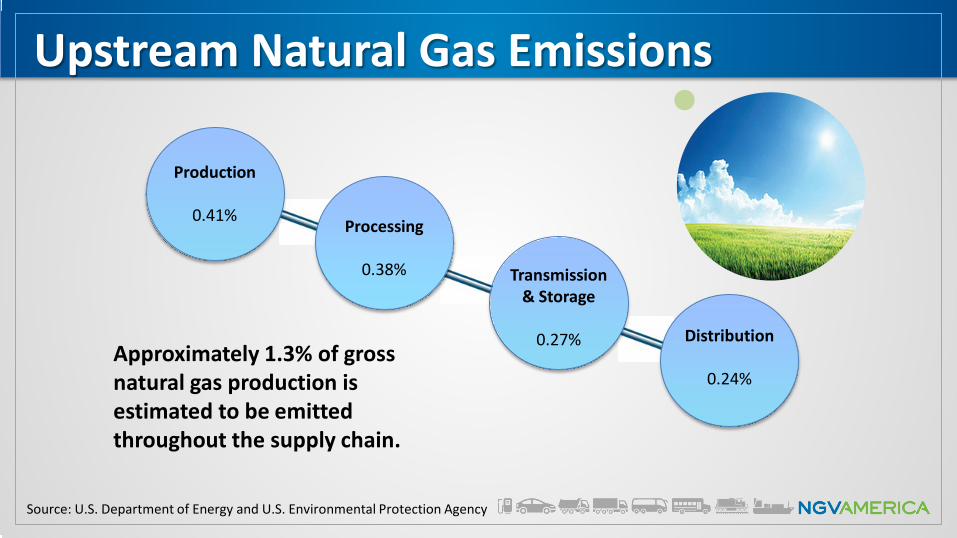

Upstream Natural Gas Emissions

Approximately 1.3% of gross natural gas production is estimated to be emitted throughout the supply chain.

Production

0.41% Processing

0.38% Transmission & Storage

0.27% Distribution

0.24%

Source: U.S. Department of Energy and U.S. Environmental Protection Agency

NG Methane Emissions vs. Production

Source: ANGA

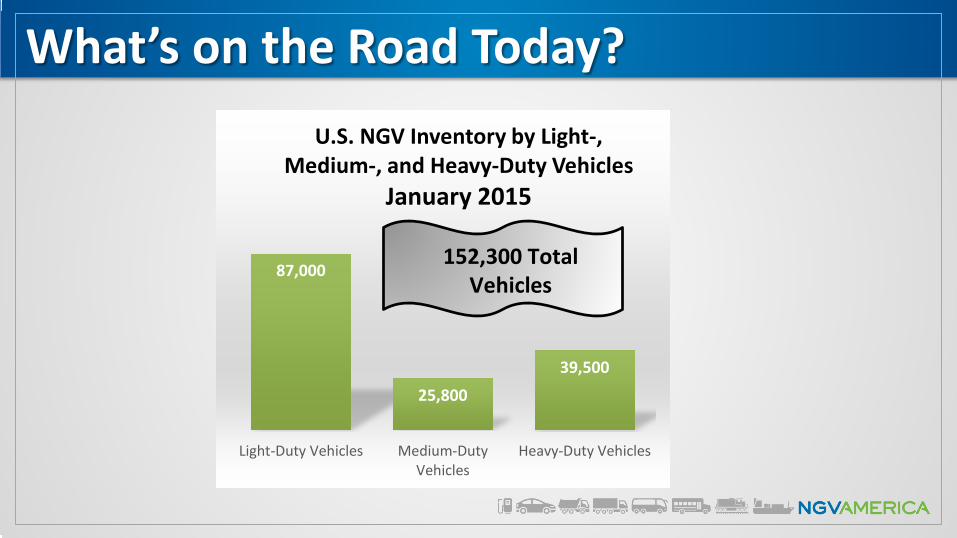

What’s on the Road Today?

87,000

25,80039,500

Light-Duty Vehicles Medium-DutyVehicles

Heavy-Duty Vehicles

U.S. NGV Inventory by Light-, Medium-, and Heavy-Duty Vehicles

January 2015

152,300 Total Vehicles

NGV Marketplace2014 Sales & Production:

NGV production and sales totaled just over 18,000 vehicles in 2014

Overall NGV production and sales fell by 6.5% in 2014 as compared to 2013

Heavy-duty market segment grew 30% Medium-duty market segment grew 24% Light-duty market segment fell 34%

Refuse & transit markets strong Heavy-duty continues solid growth Light-duty hurt by E&P & strong ‘12 & ‘13

10,150

2,175

6,7006,650

2,700

8,700

LIGHT-DUTY MEDIUM-DUTY HEAVY-DUTY

2013–2014 NGV Production and Sales

2013 2014

NGV Inventory by MD and HD Market Segments

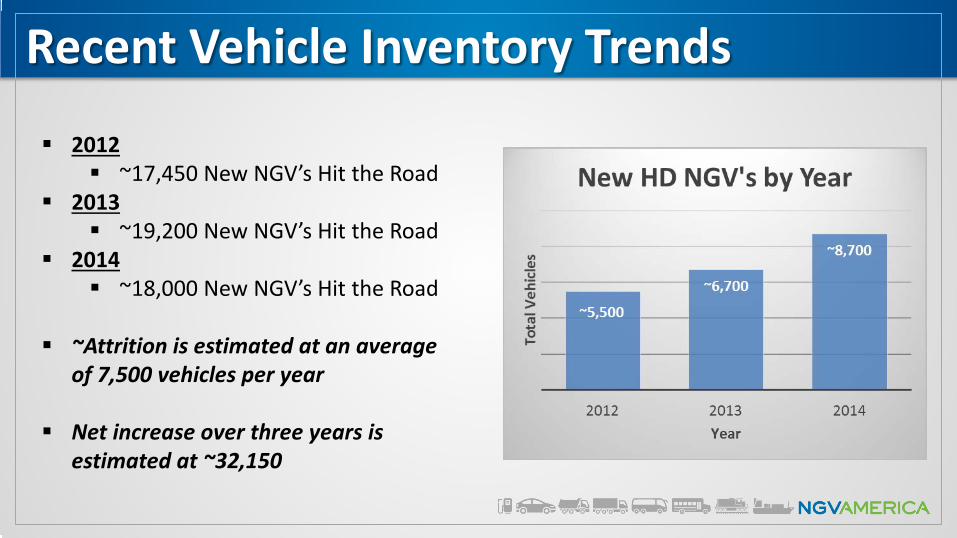

Recent Vehicle Inventory Trends

2012 ~17,450 New NGV’s Hit the Road

2013 ~19,200 New NGV’s Hit the Road

2014 ~18,000 New NGV’s Hit the Road

~Attrition is estimated at an average of 7,500 vehicles per year

Net increase over three years is estimated at ~32,150

Recent Vehicle Inventory Trends

Over 1,600 stations 15-20+ new per month, but

slowing

Multiple Stakeholders Natural gas retail fuel sellers LDCs Gas exploration & production Leasing companies Traditional fuel retailers C-Stores Truck Stops Grocery/Warehouse stores

Historical Price of Crude Oil

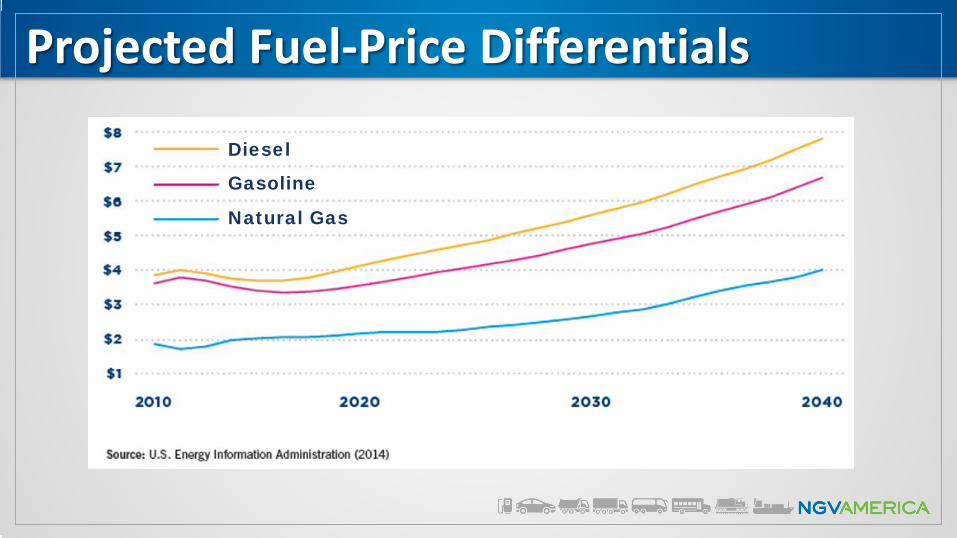

Projected Fuel-Price Differentials

Diesel

Gasoline

Natural Gas

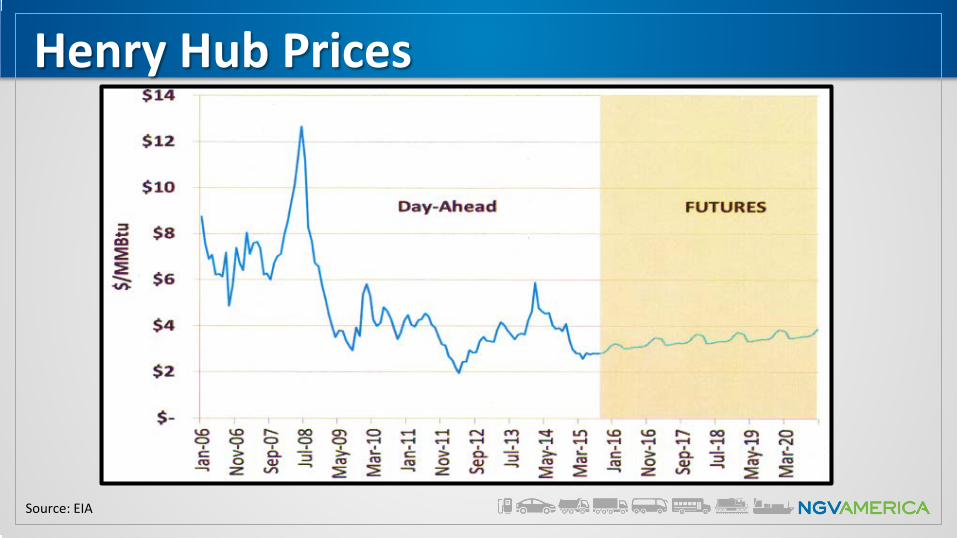

Henry Hub Prices

Source: EIA

U.S. Natural Gas Fuel Supply

Natural Gas Production

Source: EIA

Oil Price Volatility and the Continuing Case for Natural Gas

History shows that the decline in world oil prices and drop in gasoline and diesel prices are likely to be short-lived. Oil will increase as the world economy rebounds.

Diesel fuel is influenced by a variety of other factors that will likely keep upward pressure on prices over the long run.

On a Btu basis, natural gas still has a 3:1 price advantage over oil. At the pump, average CNG prices are $0.75 to $1 lower than diesel.

The long-term stability and low prices for natural gas relative to oil are likely to remain for many years – perhaps even decades – based on well-documented economic models.

Oil Price Volatility and the Continuing Case for Natural Gas

The long-term nature of fleet asset management suggests that it is prudent to continue to invest in transportation fuel portfolio diversification by transitioning more vehicles to natural gas.

Fleets that have already made the investment in vehicles and infrastructure will continue to benefit from the stability of natural gas prices and their continuing economic advantage.

State and federal policymakers are likely to continue to promote fuel diversity and policies that encourage use of natural gas as a transportation fuel on the road to energy security.

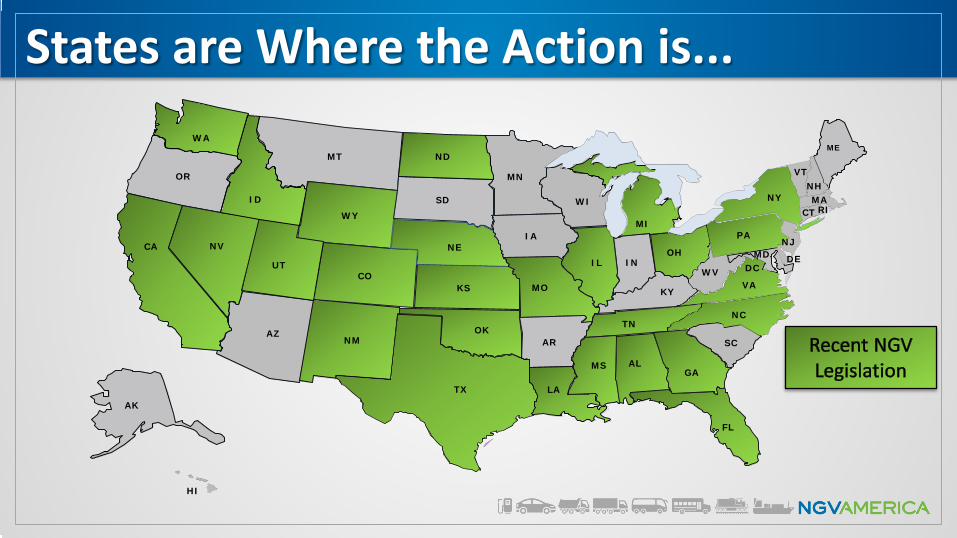

States are Where the Action is...

AZ

MT

WY

NM

CO

AL

FL

SC

TN

KY

INOH

NC

SD

KS

NE

MN

WI

IL

MO

AR

MS

OK

ND

OR

CA NV

WA

AK

ME

CT

WV

NJ

DE

RI

HI

MI

GA

NY

VTNH

PA

MA

MD

VA

IA

UT DC

TX LA

ID

States are Where the Action is...What can states to do promote NGVs? Vehicle purchase grants or tax incentives Fuel station grants or tax incentives Sales & use tax exemptions, registration fees Motor fuel tax preferential or equal treatment HOV lane access Method of sale Weight exemption Market participant

Federal Policies to Promote NGVs:

Extension of the fuel & infrastructure tax credits

Fix the LNG diesel tax penalty

Reduce the incremental FET on HD vehicles

Weight waiver for HD trucks on federal roads

Appropriations for NGV RD&D / Clean Cities program

Vehicle incentives for LD & HD

Washington Matters….

Technology, Codes, Standards & Best Practices

What are the industry’s critical safety & technology issues?

Tank Safety Best

Practices

Maintenance Facility C&S

Fire Marshall Training

Gas Quality

Home Refueling

Modern Fuel Station Monitoring

Others

The Road Ahead for NGVs…What elements are needed to grow the NGV marketplace?

Promote the value proposition as a transportation fuel – economics, environmental benefits, energy security, & abundance

MD and HD duty fleets / high fuel users are the near-term opportunity Light duty fleets remain key – infrastructure paves the way for consumers States must continue to lead the way – incentives, CMAQ, fuel taxes, etc. Innovation & technology – low NOx engines, RNG, tanks, home refueling Collaborative efforts across the value chain based on credible data

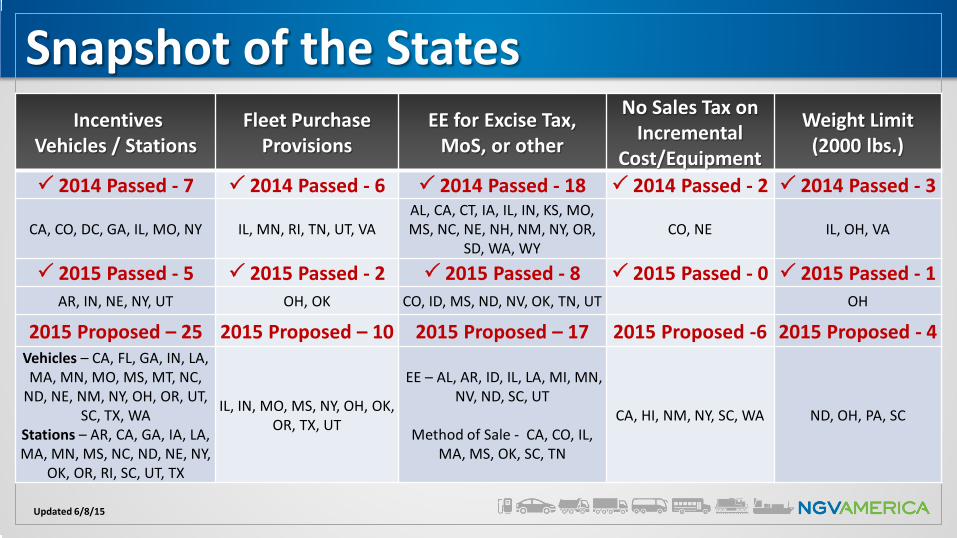

Snapshot of the StatesIncentives

Vehicles / StationsFleet Purchase

ProvisionsEE for Excise Tax,

MoS, or other

No Sales Tax on Incremental

Cost/Equipment

Weight Limit (2000 lbs.)

2014 Passed - 7 2014 Passed - 6 2014 Passed - 18 2014 Passed - 2 2014 Passed - 3

CA, CO, DC, GA, IL, MO, NY IL, MN, RI, TN, UT, VAAL, CA, CT, IA, IL, IN, KS, MO, MS, NC, NE, NH, NM, NY, OR,

SD, WA, WYCO, NE IL, OH, VA

2015 Passed - 5 2015 Passed - 2 2015 Passed - 8 2015 Passed - 0 2015 Passed - 1AR, IN, NE, NY, UT OH, OK CO, ID, MS, ND, NV, OK, TN, UT OH

2015 Proposed – 25 2015 Proposed – 10 2015 Proposed – 17 2015 Proposed -6 2015 Proposed - 4Vehicles – CA, FL, GA, IN, LA, MA, MN, MO, MS, MT, NC,

ND, NE, NM, NY, OH, OR, UT, SC, TX, WA

Stations – AR, CA, GA, IA, LA, MA, MN, MS, NC, ND, NE, NY,

OK, OR, RI, SC, UT, TX

IL, IN, MO, MS, NY, OH, OK, OR, TX, UT

EE – AL, AR, ID, IL, LA, MI, MN, NV, ND, SC, UT

Method of Sale - CA, CO, IL, MA, MS, OK, SC, TN

CA, HI, NM, NY, SC, WA ND, OH, PA, SC

Updated 6/8/15

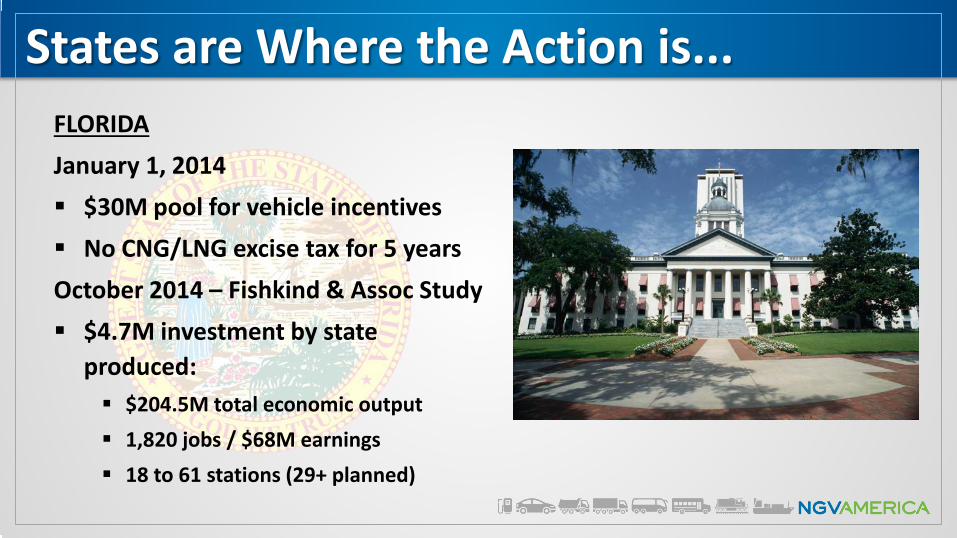

FLORIDAJanuary 1, 2014 $30M pool for vehicle incentives No CNG/LNG excise tax for 5 yearsOctober 2014 – Fishkind & Assoc Study $4.7M investment by state

produced: $204.5M total economic output 1,820 jobs / $68M earnings 18 to 61 stations (29+ planned)

States are Where the Action is...

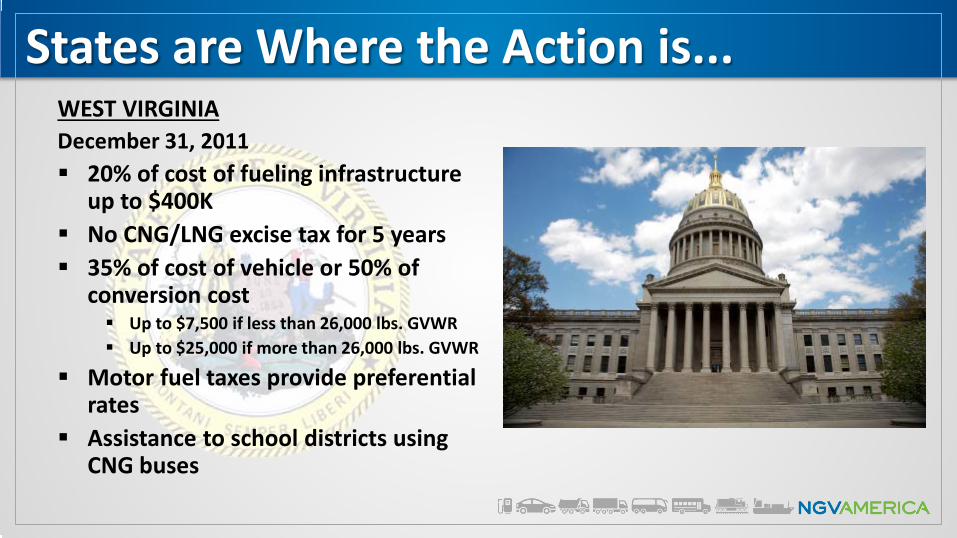

WEST VIRGINIADecember 31, 2011 20% of cost of fueling infrastructure

up to $400K No CNG/LNG excise tax for 5 years 35% of cost of vehicle or 50% of

conversion cost Up to $7,500 if less than 26,000 lbs. GVWR Up to $25,000 if more than 26,000 lbs. GVWR

Motor fuel taxes provide preferential rates

Assistance to school districts using CNG buses

States are Where the Action is...

TEXASJuly 1, 2011 Texas Clean Transportation Triangle $20M vehicle & station funding

March 2015 – San Antonio Express News $52.9M investment by state produced:

Additional $79.1M in gross state product 927 new full time jobs

April 2015 – Texas Railroad Commission Report 7,800 Vehicles have been

purchased/converted 130 Stations (77 public; 53 private; 42

planned)

States are Where the Action is...

WASHINGTONJuly 15, 2015 Tax credits for alternative fuel vehicles new

or converted 50% of incremental cost (varies by class) $6M annually to be available 2016 - 2020 Exemption from sales & use tax

Sales and use tax exemption for: Natural gas used as transportation fuel Equipment used to produce NG intended

for transportation use Utilities tax exemption for NG used in

transportation Emission inspection exemption for

dedicated NGVs and other AFVs

States are Where the Action is...