roger akers – akers capital llc akers capital llc [email protected] 916-966-2236 funding...

TRANSCRIPT

Funding Entrepreneurs

Roger Akers – Akers Capital LLCRoger Akers – Akers Capital LLCAkers Capital LLCAkers Capital LLC

[email protected]@akerscapital.com916-966-2236916-966-2236

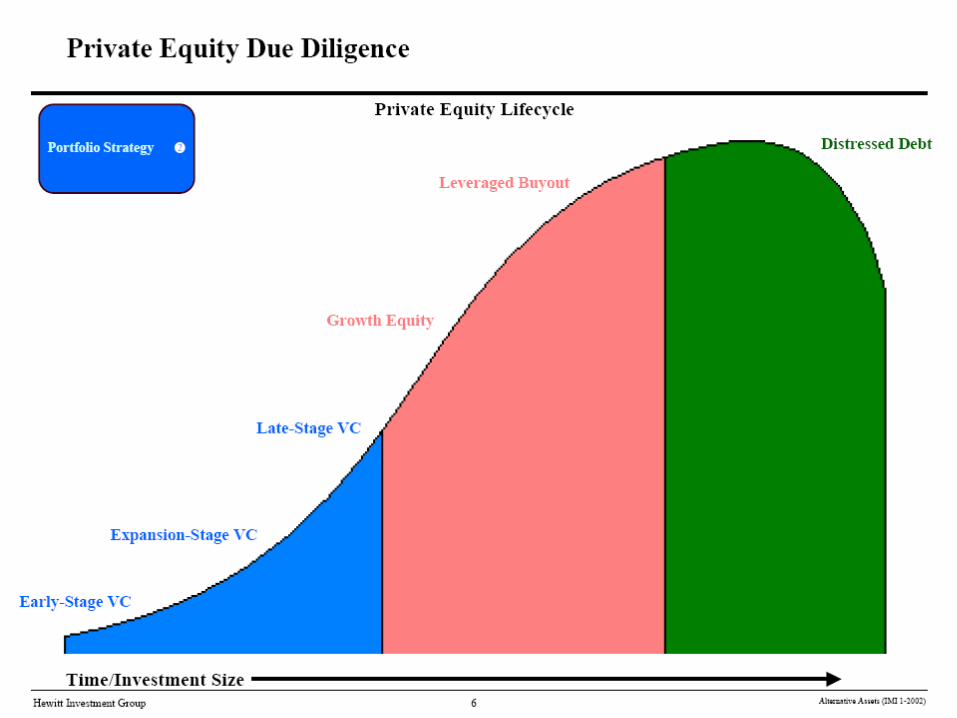

Financing Food ChainFinancing Food Chain

•Understanding the Financing Food Chain– Savings & Credit Cards– Friends & Family– Crowd Funding– Angels– Venture Capitalists

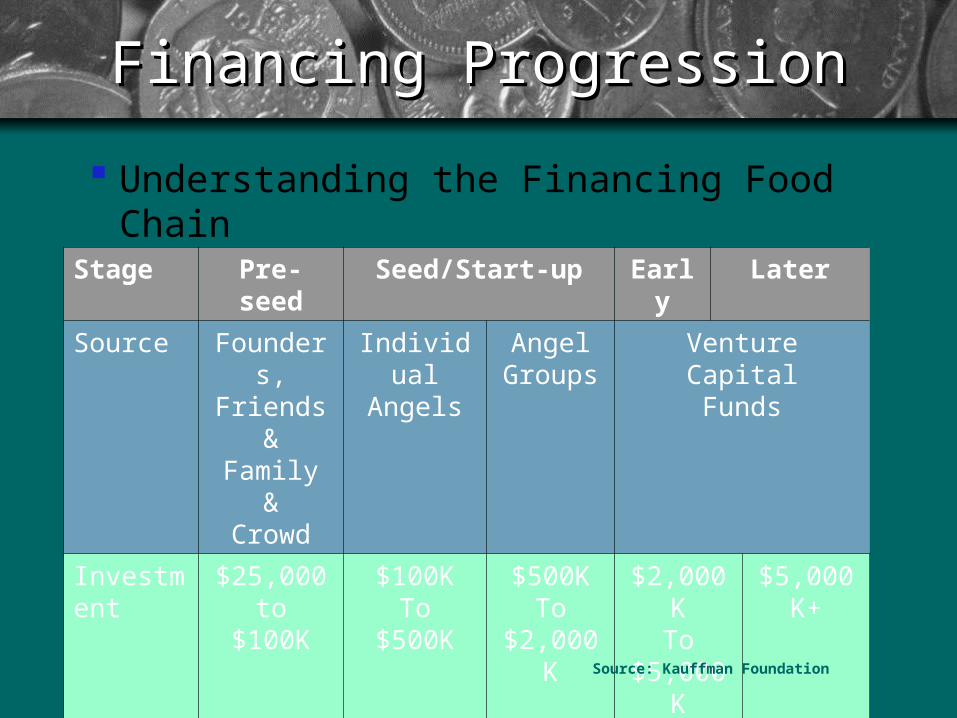

Financing ProgressionFinancing Progression

Stage Pre-seed

Seed/Start-up Early Later

Source Founders,

Friends &

Family&

Crowd

Individual

Angels

AngelGroups

VentureCapitalFunds

Investment

$25,000 to

$100K

$100KTo

$500K

$500KTo

$2,000K

$2,000KTo

$5,000K

$5,000K+

Source: Kauffman Foundation

Understanding the Financing Food Chain

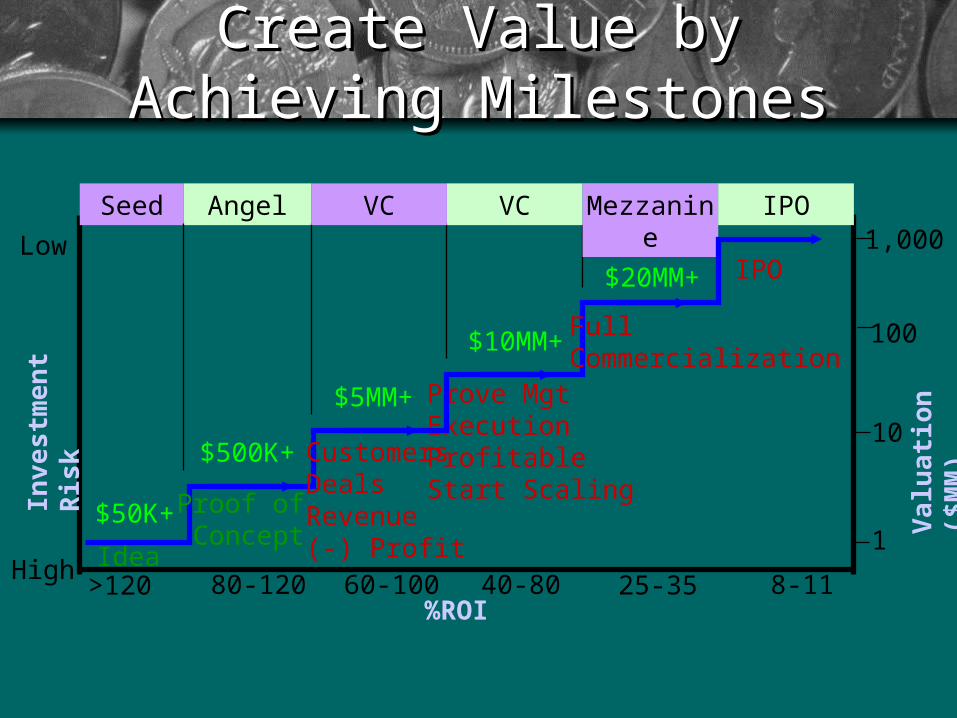

Create Value by Achieving Create Value by Achieving MilestonesMilestones

Va

lua

tio

n (

$M

M)

1

10

100

1,000

Inve

stm

en

t R

isk

High

Low

>120 80-120 60-100 40-80 25-35 8-11%ROI

VC

Full Commercialization

$10MM+

CustomersDealsRevenue(-) Profit

Angel

$500K+

VC

Prove MgtExecutionProfitableStart Scaling

$5MM+

Proof of Concept

Seed

Idea

$50K+

Mezzanine IPO

$20MM+ IPO

Size of Angel ActivitySize of Angel Activity

• Approx. 250,000 active angels in this country

• Invest approximately $30 billion annually most of it in seed, start-up and early stage

• 7 million accredited investors – qualified potential angels

• Informal investors; $92 billion, 3.3 mil companies

Expected ReturnsExpected Returns• Pre-seed stage Founders 20X in 7yrs

• The Crowd The masses Something?

• Angels 10X in 6yrs

• Early-stage Venture capital 10x in 6 yrs

• Mid-stage Venture capital(s) 3X in 3 yrs

• Late-stage Venture capital(s) 2X in 2 yrs

• Exit Investment banks 1.35X 1yr

WhereWhere

• “Use your own cash when you can”

• Friends, Family and Fools

• Crowd Funding

• Angels and Local Venture

• Local Venture and Syndication National /

Strategic Partner

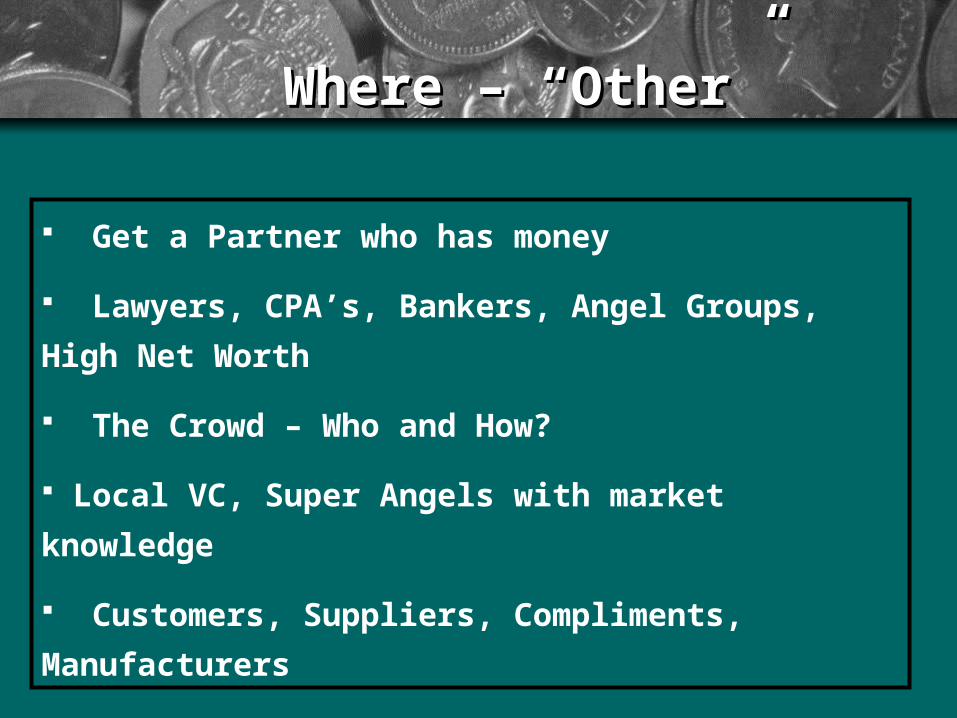

Where – “Other”Where – “Other”

Get a Partner who has money

Lawyers, CPA’s, Bankers, Angel Groups, High Net Worth

The Crowd – Who and How?

Local VC, Super Angels with market knowledge

Customers, Suppliers, Compliments, Manufacturers

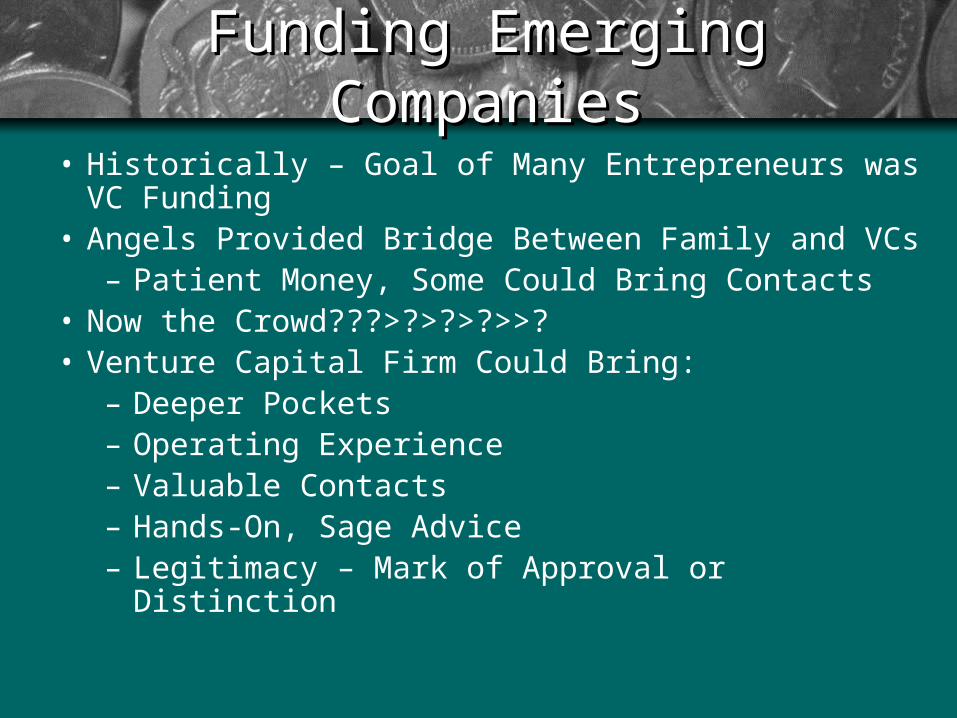

• Historically – Goal of Many Entrepreneurs was VC Funding

• Angels Provided Bridge Between Family and VCs– Patient Money, Some Could Bring Contacts

• Now the Crowd???>?>?>?>>?• Venture Capital Firm Could Bring:

– Deeper Pockets– Operating Experience– Valuable Contacts– Hands-On, Sage Advice– Legitimacy – Mark of Approval or Distinction

Funding Emerging Funding Emerging CompaniesCompanies

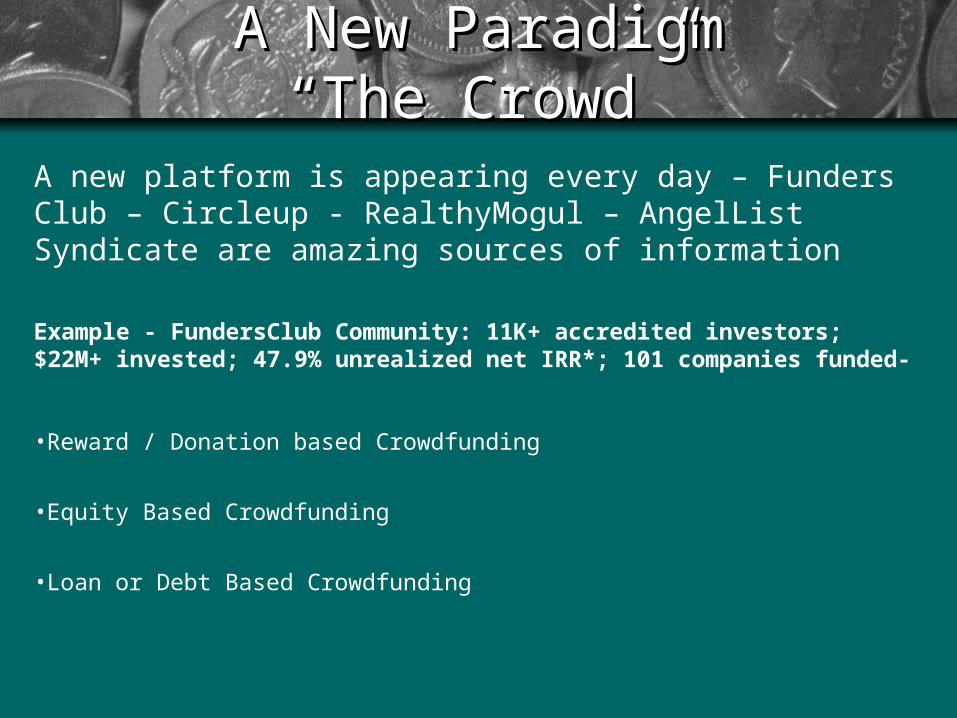

A New ParadigmA New Paradigm“The Crowd”“The Crowd”

A new platform is appearing every day – Funders Club – Circleup - RealthyMogul – AngelList Syndicate are amazing sources of information

Example - FundersClub Community: 11K+ accredited investors; $22M+ invested; 47.9% unrealized net IRR*; 101 companies funded-

•Reward / Donation based Crowdfunding

•Equity Based Crowdfunding

•Loan or Debt Based Crowdfunding

CrowdfundingCrowdfunding

• Initially, crowdfunding was limited to a reward or donation basis. By collecting incremental donations from hundreds or thousands of backers, sites pool the capital necessary to launch products and support ideas of various sizes. In return for backing products, funders receive prototypes, discounts, or special product packages, while those participating in donation-based funding do not expect or receive anything in return. Although these types of crowdfunding skyrocketed in popularity, growing by 524% from 2009 to 2012, their potential to benefit startups pales in comparison to that of equity crowdfunding.

Jobs ActJobs Act

• The goal of Title III is to level the playing field for everyday citizens looking to invest. Once enacted, Title III will allow issuers to advertise and extend investment opportunities to unaccredited investors, potentially causing the U.S. investing market to grow to $300 billion.

• According to Title III rules proposed by the SEC in October of 2013, transactions involving these unaccredited investors must meet specified requirements, such as: 1) The amount raised must not exceed $1,000,000 in a 12-month period, 2)

• Individual investments in a 12-month period cannot exceed the greater of $2,000 or 5% of net worth for those making less than $100,000 annually, and $10,000 or 10% of net worth for those making at least $100,000 annually, 3) These transactions must be conducted through an intermediary that is either a broker or a funding portal.

• With a less sophisticated investment audience comes more regulation. Thus, there is no effective date currently in place for Title III of the JOBS Act. To circumvent this issue, numerous states such as Indiana and Michigan have created their own exemptions to this regulation by passing less restrictive legislation. To date, nearly 15 states currently have intrastate crowdfunding regulations in place.

Benefits of Equity Versus Benefits of Equity Versus Reward CFReward CF

• In reward-based crowdfunding, a target amount and deadline are set for a project. Once a raise begins, promotional videos are usually released to generate and maintain interest in the project. Funders then pledge in certain tiers, receiving different rewards based on the amount donated. If the target amount is hit on or before the deadline, backers are charged the amount they pledged and are given the corresponding reward. This creates incentive for individuals to promote the project themselves through social media and other channels. However, if the target is not hit, none of the backers are charged or rewarded. Because of this process, rewards-based crowdfunding is an all-or-nothing approach.

• Though equity crowdfunding and reward-based crowdfunding provide support for up-and-coming projects and products, equity crowdfunding offers a greater reward for startups and investors who desire to back them. Equity crowdfunding allows individuals the opportunity to invest on a larger scale, raising 40 times more per company than any other type of crowdfunding today. This provides a middle ground between the $ average reward-based donation and the traditional five-figure minimum sum required to invest in a company.

• With reward-based crowdfunding, the bragging rights of those who donated at early stages grow with a company, but the reward remains the same. Conversely, equity crowdfunding allows the investor’s commitment to grow side-by-side with a startup, providing a growing revenue or profit-share.

Rewards / Donation BasedRewards / Donation Based

• Rewards Funders back products, arts, and other ideas – In exchange the receive Products, Discounts or incentives - See Kickstarter, RocketHub – 46,000 successful campaigns – 80% that raised 20% of goal were funded – 5% Fee – 56% fail

• Donation Funders Contribute to philanthropic

causes, expecting nothing in return – See Indiegogo, Crowdrise – Average raised $3700 – 80% fail – 4% - 9% Fee – Fixed or Flexible – To keep or not to keep – 80% fail

Equity Based – Pg1Equity Based – Pg1

• Equity crowdfunding allows backers to reap eventual financial returns on investments, and the investment scale for businesses and startups is typically much larger than donation-based crowdfunding campaigns. The experience of funding something for $25 to $50 on impulse is radically different from considering the long-term prospects of a business, and investing $1,000 to $10,000, or See Circleup, Crowdfunder.com,

• Solicitation began Sept 23rd, 2014 - General.

• Social Proof: Knowing who backs a campaign can help sway other potential investors

• Momentum: Initial funding can beget more funding• Validation: Having raised money online successfully can be a proof

point of its own• Customer Engagement: The people who fund you are also your

customers

Equity Based – Pg 2Equity Based – Pg 2

• As the overall crowdfunding market is expected to grow roughly at a rate of doubling year over year, it is set to rapidly expand with the more immediate kicking off of Title II (general solicitation and accredited investing activity online).

• Title III of the JOBS Act (non-accredited crowdfunding) is most likely to be proposed for commenting this Fall and put to a vote by the SEC Commissioners sometime at the end of the year or early 2015.

Loan or DebtLoan or Debt

• Funders loan money – AngelList, SeedCapital, Somolend, Prosper

• Securitized lending based on Assets including A/Rs, Real Property, etc.

1. Expecting income – Cash Flow

2. Return of their initial investment – 7-34% cost

3. Usually with some warrant or conversion capability – Maybe an equity kicker will happen someday

Size of Angel ActivitySize of Angel Activity

• Approx. 250,000 active angels in this country

• Invest approximately $30 billion annually most of it in seed, start-up and early stage

• 7 million accredited investors – qualified potential angels

• Informal investors; $92 billion, 3.3 mil companies

Changing Value Changing Value Proposition Of AngelsProposition Of Angels

• Value Proposition for Angels Has Changed:• Angels Can Be:

– Deep Pockets; Start Small Then Go Big– Willing to Fund Companies Through Later Stages– Bring Sage Advice and Contacts

•To Help Raise More $$•To Help Create More Sales•To Help Bring Employees and Consultants to the

Company– Not Seal of Approval for Company on Wall Street– But Maybe Legitimizes Management Competency

• Result: Angels Can Be a Viable Alternative to VCs in the Right Circumstances

VC Funding Has ChangedVC Funding Has Changed

• The Value Proposition for VCs Has Changed:– VCs Increasingly Looking Farther Up the Chain– Bigger Individual Investments– Less Time Spent Guiding Individual Portfolio Cos. – VCs Sometimes More Banker or Newly Minted

MBA Than Seasoned Manager– VC/Institutional Money Not Necessary Prerequisite

for Successful Liquidity Events– Wall Street Will Make Its Own Assessment of the

Quality of the Opportunity

Current Equity Capital Current Equity Capital Climate Climate

•The bad and good news:The bad and good news:

•Liquidity is still very difficult – Merger orientedLiquidity is still very difficult – Merger oriented

•VCs are at a crossroads relative to the pace of investingVCs are at a crossroads relative to the pace of investing

•Valuations still have downward pressureValuations still have downward pressure

•Subsequent rounds for VC-funded companies are not easySubsequent rounds for VC-funded companies are not easy

•Liquidity windows open and close with the economyLiquidity windows open and close with the economy

•VCs do have lots of money to investVCs do have lots of money to invest

•Better more complete companies are emerging from this periodBetter more complete companies are emerging from this period

•Expectations are much more realisticExpectations are much more realistic

•Those companies that succeed in raising $ have more board Those companies that succeed in raising $ have more board involvement, better resources, and less competitioninvolvement, better resources, and less competition

Words to the wiseWords to the wise

• Don’t burn bridges with investors

• Mitigate Risk / Maximize Return

• Take the smart money

• Don’t screw your old investors

• Incent the employees with good expectations and

personal growth

• Communicate often to your investors

• Keep your word – always

• You will lose control – Have great partners when you do

Reference MaterialsReference Materials

• MicroVentures.com, Forbes, Crowdfunding.com

• Some Useful Reference Materials– Inside Secrets to Venture Capital

•Brian E. Hill & Dee Power– The Art of the Start

•Guy Kawasaki– Term Sheets & Valuations: A Line by Line

Look at the Intricacies of Term Sheets & Valuations•Alex Wilmerding