review package - midterm solution fall 2013 midterm ex… · review package - midterm solution fall...

TRANSCRIPT

ACCT1115

Review Package - Midterm

SOLUTION

Fall 2013

Part I Multiple Choice

1) How should you record the purchase of an expensive automobile?

a) Decrease cash, increase assets

b) Decrease cash, increase expenses c) Decrease cash, decrease net worth

d) Decrease cash, increase net worth

2) Which of the following businesses would be considered a service business?

a) Paper manufacturer

b) Retail store

c) Law firm

d) None of the available choices

3) Controls:

a) are a system of rules that govern international businesses

b) include procedures that are used to check and regulate business operations systematically

c) are financial goals that a business works towards

d) none of the choices

4) A business commences with owner's equity of $60,000 and a cash balance of $15,000 on September 1st. On the last day of September, the business prepays a maintenance contract of $12,000 for a one year service contract that will commence in October. The services will be delivered in equal amounts each month. Assuming no other transactions, what will be the value of cash and owners’ equity at the end of December?

a) Cash $3,000. Equity $57,000 b) Cash $13,000. Equity $60,000 c) Cash $3,000. Equity $45,000 d) Cash $13,000. Equity $57,000

5) Company ABC has not recognized $300 worth of prepaid insurance used at the end of its fiscal year. What happens to net income?

a) Net income would not be affected. b) Net income would be understated by $300.

c) It cannot be determined.

d) Net Income would be overstated by $300.

6) A typical accounting adjustment could be:

a) recognizing earned revenue

b) recognizing depreciation

c) recognizing prepaid expenses

d) all of the choices

7) Entries are recorded in the journal:

a) alphabetically

b) chronologically (by date)

c) in the order of account numbers used

d) randomly

8) The document which records the activities and balances of each specific account is called a:

a) journal

b) general Ledger

c) financial statement

d) trial balance

9) The trial balance lists:

a) all accounts in the general ledger and their balances

b) only income statement accounts

c) only balance sheet accounts

d) a summary of owner's equity

10) Which of the following accounts will NOT show on the post-closing trial balance?

a) Cash

b) Rent Expense

c) Accounts Payable

d) Owner's Equity

11) A post-closing trial balance contains:

a) assets and liabilities only

b) all zero balances

c) revenue and expenses only

d) assets, liabilities and owner’s equity

12) The Statement of Owner's Equity :

a) is used to determine the sources and uses of cash

b) is used to calculate ending Owners' equity so that it can be transferred to the income statement

c) reports any changes in equity over the reporting period

d) reflects increases due to losses and decreases due to profits

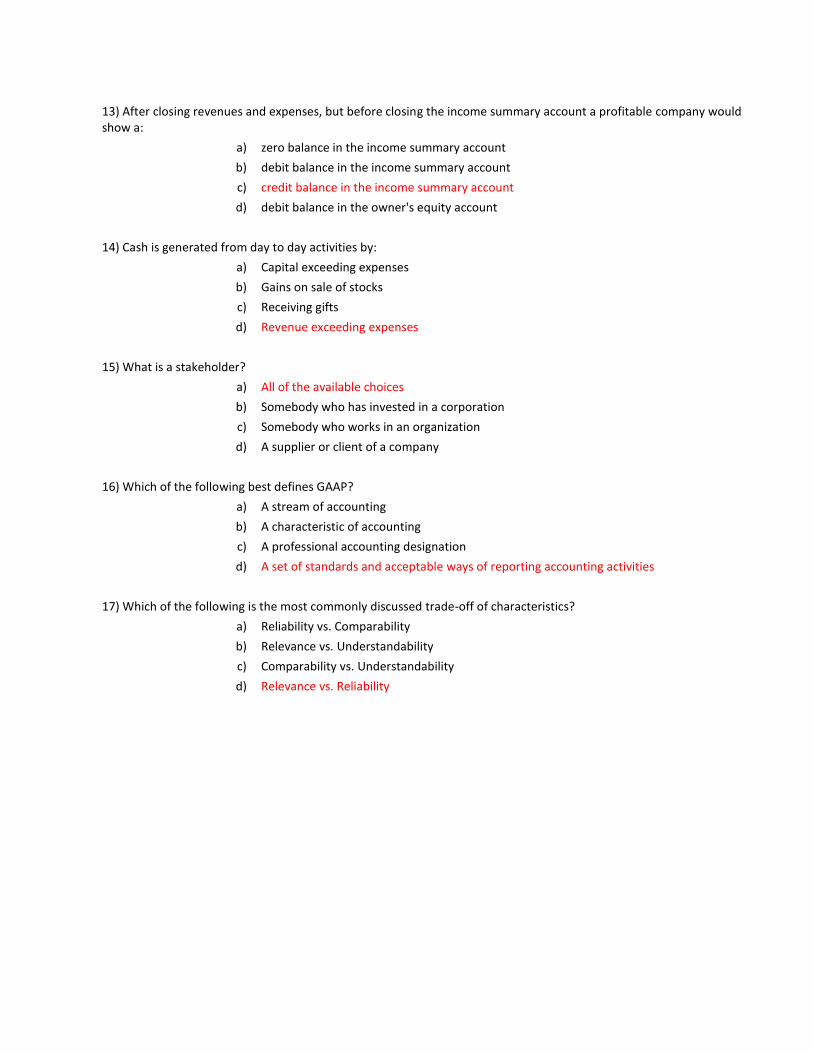

13) After closing revenues and expenses, but before closing the income summary account a profitable company would show a:

a) zero balance in the income summary account b) debit balance in the income summary account c) credit balance in the income summary account d) debit balance in the owner's equity account

14) Cash is generated from day to day activities by:

a) Capital exceeding expenses

b) Gains on sale of stocks

c) Receiving gifts

d) Revenue exceeding expenses

15) What is a stakeholder?

a) All of the available choices

b) Somebody who has invested in a corporation c) Somebody who works in an organization

d) A supplier or client of a company

16) Which of the following best defines GAAP?

a) A stream of accounting

b) A characteristic of accounting

c) A professional accounting designation

d) A set of standards and acceptable ways of reporting accounting activities

17) Which of the following is the most commonly discussed trade-off of characteristics?

a) Reliability vs. Comparability

b) Relevance vs. Understandability

c) Comparability vs. Understandability

d) Relevance vs. Reliability

Part II GAAP Principles

Match each of the following GAAP principles to the appropriate description in the table below.

A. Business entity principle

B. Going concern principle

C. Monetary unit principle

D. Objectivity principle

E. Cost principle

F. Conservatism principle

Corresponding Letter Description

F The accountant should exercise the option that results in a lower

balance of assets, lower net income or a higher balance of debt.

D

Accounting transactions should be recorded on the basis of verifiable evidence.

B Assumes that a business will continue to operate into the

foreseeable future.

C Financial reports should be expressed in a single currency.

A

Accounting for a business must be kept separate from the personal affairs of its owner or any other business.

E Accounting for purchases must be recorded at their cost on the date

of purchase.

Part III Transactions - Revenue & Expense

Complete the chart using the transactions below. Under the "Account Type" column, fill the cells with one of the following: Asset, Liability, Revenue or Expense. The first one has been done for you.

May 1 Paid cash for travel expenses incurred on this day $2,000 May 2 Paid cash for a one year insurance policy $1,800 May 12 Paid cash for telephone bill that was received and recorded last month $300 May 20 Received cash from a customer for service to be performed next month $800

May 25 Received a maintenance invoice for work completed in May which will be paid next month $400

Date Account Name Account Type Increase or Decrease Amount

May 1 Travel Expense Expense Increase $2,000

Cash Asset Decrease $2,000

May 2 Prepaid Expense Asset Increase $1,800

Cash Asset Decrease $1,800

May 12 Accounts Payable Liability Decrease $300

Cash Asset Decrease $300

May 20 Cash Asset Increase $800

Unearned Revenue Liability Increase $800

May 25 Maintenance Expense Expense Increase $400

Accounts Payable Liability Increase $400

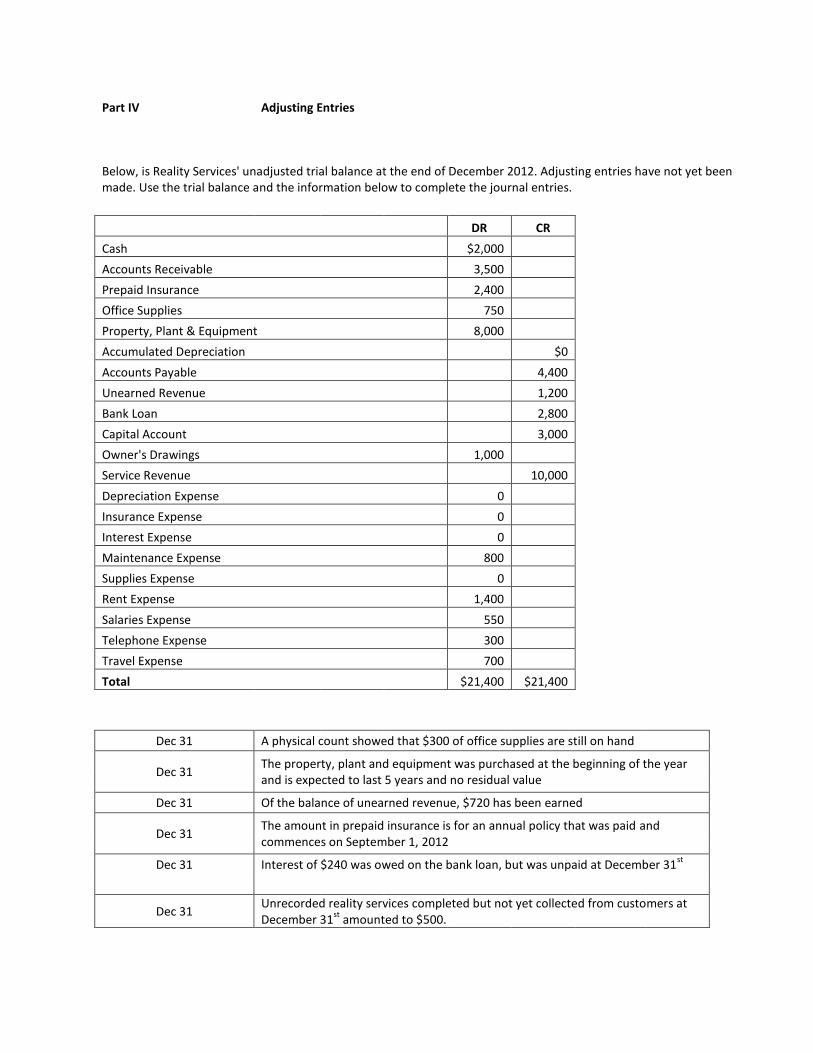

Part IV Adjusting Entries

Below, is Reality Services' unadjusted trial balance at the end of December 2012. Adjusting entries have not yet been made. Use the trial balance and the information below to complete the journal entries.

DR CR Cash $2,000 Accounts Receivable 3,500 Prepaid Insurance 2,400 Office Supplies 750 Property, Plant & Equipment 8,000 Accumulated Depreciation $0 Accounts Payable 4,400 Unearned Revenue 1,200 Bank Loan 2,800 Capital Account 3,000 Owner's Drawings 1,000 Service Revenue 10,000 Depreciation Expense 0 Insurance Expense 0 Interest Expense 0 Maintenance Expense 800 Supplies Expense 0 Rent Expense 1,400 Salaries Expense 550 Telephone Expense 300 Travel Expense 700 Total $21,400 $21,400

Dec 31 A physical count showed that $300 of office supplies are still on hand

Dec 31

The property, plant and equipment was purchased at the beginning of the year and is expected to last 5 years and no residual value

5

Dec 31 Of the balance of unearned revenue, $720 has been earned

Dec 31

The amount in prepaid insurance is for an annual policy that was paid and commences on September 1, 2012

Dec 31 Interest of $240 was owed on the bank loan, but was unpaid at December 31st

Dec 31

Unrecorded reality services completed but not yet collected from customers at December 31

st amounted to $500.

Journal

Date Account Title and Explanation DR CR Dec 31 Supplies Expense $450 Office Supplies $450 Adjust office supplies Dec 31 Depreciation Expense $1,600 Accumulated Depreciation $1,600 Depreciate PPE Dec 31 Unearned Revenue $720 Service Revenue $720 Adjust for revenue earned Dec 31 Insurance Expense $800 Prepaid Insurance $800 Adjust for 4 months of insurance Dec 31 Interest Expense $240 Interest Payable $240 To accrue for interest on bank loan Dec 31 Accounts Receivable $500

Service Revenue $500

Accrued for services provided.

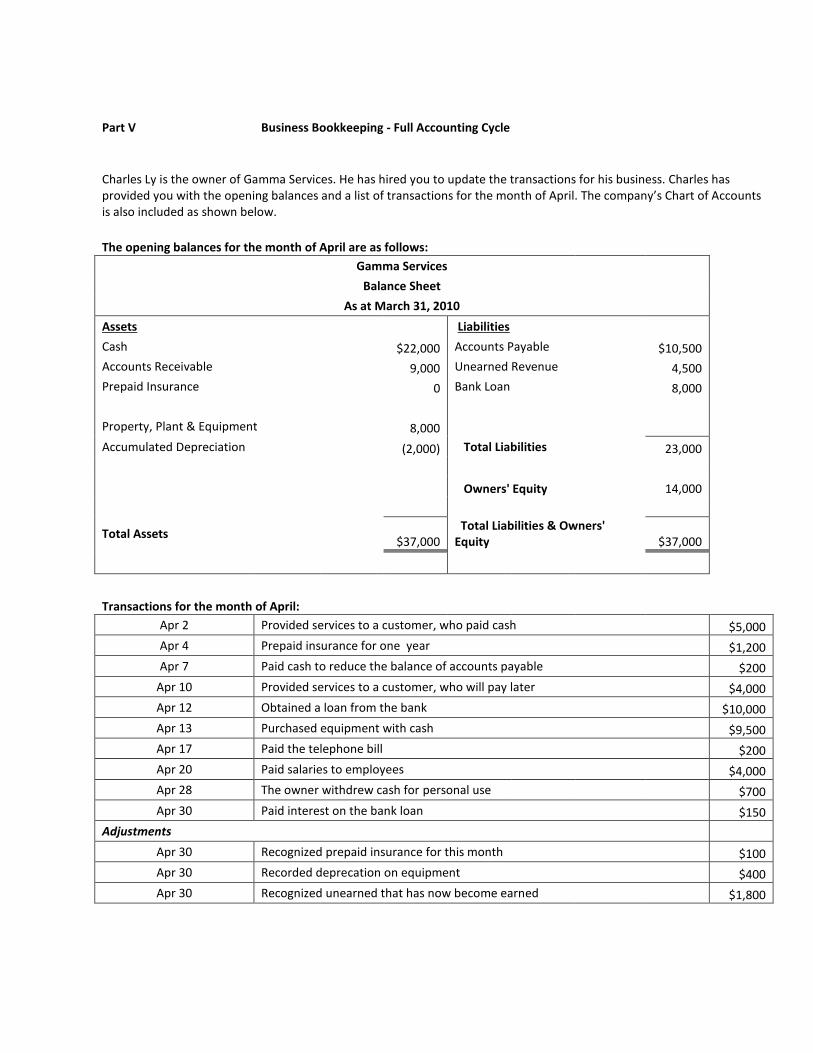

Part V Business Bookkeeping - Full Accounting Cycle

Charles Ly is the owner of Gamma Services. He has hired you to update the transactions for his business. Charles has provided you with the opening balances and a list of transactions for the month of April. The company’s Chart of Accounts is also included as shown below.

The opening balances for the month of April are as follows: Gamma Services

Balance Sheet

As at March 31, 2010

Assets Liabilities Cash $22,000 Accounts Payable $10,500 Accounts Receivable 9,000 Unearned Revenue 4,500 Prepaid Insurance 0 Bank Loan 8,000 Property, Plant & Equipment 8,000 Accumulated Depreciation (2,000) Total Liabilities 23,000

Owners' Equity

14,000

Total Assets

$37,000 Total Liabilities & Owners' Equity $37,000

Transactions for the month of April: Apr 2 Provided services to a customer, who paid cash $5,000

Apr 4 Prepaid insurance for one year $1,200 Apr 7 Paid cash to reduce the balance of accounts payable $200 Apr 10 Provided services to a customer, who will pay later $4,000 Apr 12 Obtained a loan from the bank $10,000 Apr 13 Purchased equipment with cash $9,500 Apr 17 Paid the telephone bill $200 Apr 20 Paid salaries to employees $4,000 Apr 28 The owner withdrew cash for personal use $700 Apr 30 Paid interest on the bank loan $150 Adjustments Apr 30 Recognized prepaid insurance for this month $100 Apr 30 Recorded deprecation on equipment $400 Apr 30 Recognized unearned that has now become earned $1,800

The Chart of Accounts (GL No.) is shown below:

Account Description Account

#

Account Description Account

# ASSETS

REVENUE

Cash 101

Service Revenue 400 Accounts Receivable 105

Interest Revenue 410

Prepaid Insurance 110

EXPENSES Property, Plant & Equipment 120

Advertising Expense 505

Accumulated Depreciation 130

Insurance Expense 510

Maintenance Expense 515

LIABILITIES

Professional Fees Expense 520 Accounts Payable 200

Rent Expense 525

Unearned Revenue 205

Salaries Expense 530 Bank Loan 210

Telephone Expense 535

Depreciation Expense 540 OWNER'S EQUITY

Interest Expense 545

Capital Account 300 Owner's Drawing 310 Income Summary 315

Required: a) Journalize the transactions.

b) Post the transactions to the General Ledger. c) Prepare the adjusted trial balance. d) Prepare the closing journal entries. Assume the company uses the income summary method.

e) Post the closing entries to the General Ledger. f) Prepare the post-closing trial balance.

Journal Date Account Title & Explanation PR DR CR

Apr 2 Cash 101 $5,000

Service Revenue 400 $5,000

Sold product to customer for cash

Apr 4 Prepaid Insurance 110 $1,200

Cash 101 $1,200

To record the prepayment of insurance

Apr 7 Accounts Payable 200 $200

Cash 101 $200

To record payment to reduce accounts payable

Apr 10 Accounts Receivable 105 $4,000

Service Revenue 400 $4,000

Sold product to a customer on account

Apr 12 Cash 101 $10,000

Bank Loan 210 $10,000

To record the loan from the bank

Apr 13 Property, Plant & Equipment 120 $9,500

Cash 101 $9,500

To record purchase of equipment

Apr 17 Telephone Expense 535 $200

Cash 101 $200

To record payment for telephone

Apr 20 Salaries Expense 530 $4,000

Cash 101 $4,000

To record payment for salaries

Apr 28 Owner's Drawing 310 $700

Cash 101 $700

To record owner's drawings

Apr 30 Interest Expense 545 $150

Cash 101 $150

To record payment of loan interest

Date Account Title & Explanation DR CR

Adjustments:

Apr 30 Insurance Expense 510 $100

Prepaid Insurance 110 $100

To adjust prepaid insurance

Apr 30 Depreciation Expense 540 $400

Accumulated Depreciation 130 $400

To record depreciation

Apr 30 Unearned Revenue 205 $1,800

Service Revenue 400 $1,800

To record earned revenue

Account: Cash GL No: 101 Date: 2010 Description PR DR CR Balance (DR or CR) Opening Balance $22,000 DR Apr 2 J1 $5,000 $27,000 DR

Apr 4 J1 $1,200 $25,800 DR

Apr 7 J1 $200 $25,600 DR

Apr 12 J1 $10,000 $35,600 DR

Apr 13 J1 $9,500 $26,100 DR

Apr 17 J1 $200 $25,900 DR

Apr 20 J1 $4,000 $21,900 DR

Apr 28 J1 $700 $21,200 DR

Apr 30 J1 $150 $21,050 DR

Account: Accounts Receivable GL No: 105 Date: 2010 Description PR DR CR Balance (DR or CR) Opening Balance $9,000 DR Apr 10 J1 $4,000 $13,000 DR

Account: Prepaid Insurance GL No: 110 Date: 2010 Description PR DR CR Balance (DR or CR) Opening Balance $0 DR Apr 4 J1 $1,200 $1,200 DR

Apr 30 To adjust prepaid insurance J1 $100 $1,100 DR

Account: Property, Plant & Equipment GL No: 120 Date: 2010 Description PR DR CR Balance (DR or CR) Opening Balance $8,000 DR Apr 13 J1 $9,500 $17,500 DR

Account: Accumulated Depreciation GL No: 130 Date: 2010 Description PR DR CR Balance (DR or CR) Opening Balance $2,000 CR Apr 30 To record depreciation J1 $400 $2,400 CR

Account: Accounts Payable GL No: 200 Date: 2010 Description PR DR CR Balance (DR or CR) Opening Balance $10,500 CR Apr 7 J1 $200 $10,300 CR

Account: Unearned Revenue GL No: 205 Date: 2010 Description PR DR CR Balance (DR or CR) Opening Balance $4,500 CR Apr 30 To record earned revenue J1 $1,800 $2,700 CR

Account: Bank Loan GL No: 210

Date: 2010 Description PR DR CR Balance (DR or CR) Opening Balance $8,000 CR

Apr 12 J1 $10,000 $18,000 CR

Account: Capital Account GL No: 300 Date: 2010 Description PR DR CR Balance (DR or CR) Opening Balance $14,000 CR

Apr 30 Clear income summary J1 $5,950 $19,950 CR

Apr 30 Clear income summary J1 $700 $19,250 CR

Account: Owner's Drawing GL No: 310 Date: 2010 Description PR DR CR Balance (DR or CR)

Apr 28 J1 $700 $700 DR

Apr 30 Clear income summary J1 $700 $0 DR

Account: Income Summary GL No: 315 Date: 2010 Description PR DR CR Balance (DR or CR) Apr 30 Clear the revenue account J1 $10,800 $10,800 CR

Apr 30 Clear the expense accounts J1 $4,850 $5,950 CR

Apr 30 Clear income summary J1 $5,950 $0 CR

Account: Service Revenue GL No: 400 Date: 2010 Description PR DR CR Balance (DR or CR) Apr 2 J1 $5,000 $5,000 CR

Apr 10 J1 $4,000 $9,000 CR

Apr 30 To record earned revenue J1 $1,800 $10,800 CR

Apr 30 Clear the revenue account J1 $10,800 $0 CR

Account: Advertising Expense GL No: 505 Date: 2010 Description PR DR CR Balance (DR or CR)

Account: Insurance Expense GL No: 510 Date: 2010 Description PR DR CR Balance (DR or CR) Apr 30 To adjust prepaid insurance J1 $100 $100 DR

Apr 30 Clear the expense accounts J1 $100 $0 CR

Account: Maintenance Expense GL No: 515

Date: 2010 Description PR DR CR Balance (DR or CR)

Account: Professional Fees Expense GL No: 520 Date: 2010 Description PR DR CR Balance (DR or CR)

Account: Rent Expense GL No: 525 Date: 2010 Description PR DR CR Balance (DR or CR)

Account: Salaries Expense GL No: 530 Date: 2010 Description PR DR CR Balance (DR or CR) Apr 20 J1 $4,000 $4,000 DR

Apr 30 Clear the expense accounts J1 $4,000 $0 DR

Account: Telephone Expense GL No: 535 Date: 2010 Description PR DR CR Balance (DR or CR) Apr 17 J1 $200 $200 DR

Apr 30 Clear the expense accounts J1 $200 $0 DR

Account: Depreciation Expense GL No: 540

Date: 2010 Description PR DR CR Balance (DR or CR) Apr 30 To record depreciation J1 $400 $400 DR

Apr 30 Clear the expense accounts J1 $400 $0 DR

Account: Interest Expense GL No: 545 Date: 2010 Description PR DR CR Balance (DR or CR) Apr 30 J1 $150 $150 DR

Apr 30 Clear the expense accounts J1 $150 $0 DR

Gamma Services

Adjusted Trial Balance

April 30, 2010

Account Titles DR CR DR CR DR CR

DR

Cash $21,050

$21,050

$21,050

Accounts Receivable 13,000

$13,000

13,000

Prepaid Insurance 1,100

$1,100

1,200

Property, Plant & Equipment 17,500

$17,500

17,500

Accumulated Depreciation $2,400

$2,400 Accounts Payable 10,300

$10,300

Unearned Revenue 2,700

$2,700 Bank Loan 18,000

$18,000

Capital Account 14,000

$14,000 Owner's Drawing 700

$700

Service Revenue 10,800

$10,800 Advertising Expense 0 $0

0

Insurance Expense 100 $100

0

Maintenance Expense 0 $0

0

Professional Fees Expense 0 $0

0

Rent Expense 0 $0

0

Salaries Expense 4,000 $4,000

4,000

Telephone Expense 200 $200

200

Depreciation Expense 400 $400

0

Interest Expense 150 $150

150

Totals $58,200 $58,200 $4,850 $10,800 $52,650 $48,100

$57,100

Net Profit (Loss)

$5,950

$5,950 Total $58,200 $58,200 $10,800 $10,800 $52,650 $54,050

Gamma Services

Income Statement

For the Month Ending April 30, 2010

Revenue

$10,800

Less Expenses

Advertising Expense $0

Insurance Expense 100

Salaries Expense 4,000

Telephone Expense 200

Depreciation Expense 400

Interest Expense 150

Total Expenses 4,850

Net Income $5,950

Gamma Services

Statement of Owner's Equity

For the Month Ending April 30, 2010

Opening Capital Account

$14,000

Add: Net Income $5,950 Less: Owner's Drawings (700) Ending Capital Account $19,250

Gamma Services Balance Sheet April 30, 2010 Assets Cash $21,050 Accounts Receivable 13,000 Prepaid Insurance 1,100 Property, Plant & Equipment $17,500 Accumulated Depreciation (2,400) 15,100 Total Assets

$50,250

Liabilities Accounts Payable $10,300 Unearned Revenue 2,700 Bank Loan 18,000

Total Liabilities

$31,000

Owner's Equity Capital Account

19,250

Liabilities + Owner's Equity $50,250

Closing Entries: Date Account Title & Explanation DR CR

Apr 30 Service Revenue $10,800 Income Summary $10,800 Clear the revenue account Apr 30 Income Summary $4,850 Insurance Expense $100 Salaries Expense $4,000 Telephone Expense $200 Depreciation Expense $400 Interest Expense $150 Clear the expense accounts Apr 30 Income Summary $5,950 Capital Account $5,950 Clear income summary Apr 30 Capital Account $700 Owner's Drawing $700 To close owner's drawings

Gamma Services Post-Closing Trial Balance April 30, 2010 Account DR CR Cash $21,050 Accounts Receivable 13,000 Prepaid Insurance 1,100 Property, Plant & Equipment 17,500 Accumulated Depreciation $2,400 Accounts Payable 10,300 Unearned Revenue 2,700 Bank Loan 18,000 Capital Account 19,250

Total $52,650 $52,650

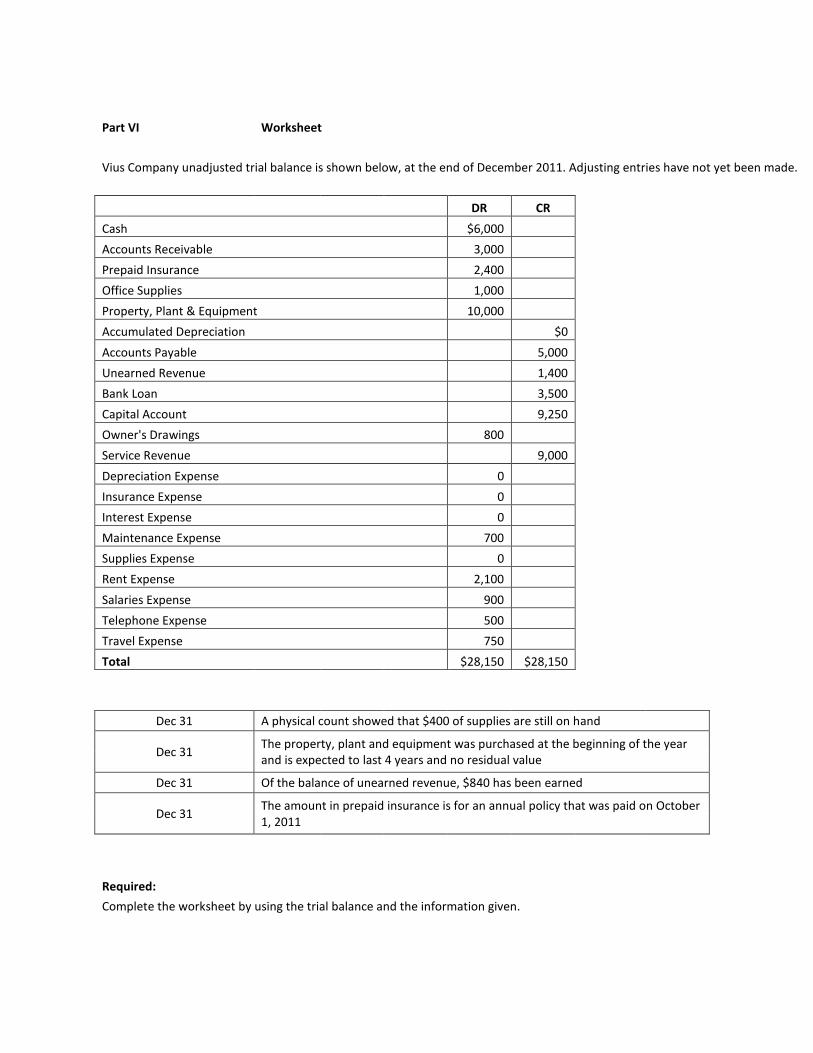

Part VI Worksheet

Vius Company unadjusted trial balance is shown below, at the end of December 2011. Adjusting entries have not yet been made.

DR CR Cash $6,000 Accounts Receivable 3,000 Prepaid Insurance 2,400 Office Supplies 1,000 Property, Plant & Equipment 10,000 Accumulated Depreciation $0 Accounts Payable 5,000 Unearned Revenue 1,400 Bank Loan 3,500 Capital Account 9,250 Owner's Drawings 800 Service Revenue 9,000 Depreciation Expense 0 Insurance Expense 0 Interest Expense 0 Maintenance Expense 700 Supplies Expense 0 Rent Expense 2,100 Salaries Expense 900 Telephone Expense 500 Travel Expense 750 Total $28,150 $28,150

Dec 31 A physical count showed that $400 of supplies are still on hand

Dec 31

The property, plant and equipment was purchased at the beginning of the year and is expected to last 4 years and no residual value

4

Dec 31 Of the balance of unearned revenue, $840 has been earned

Dec 31

The amount in prepaid insurance is for an annual policy that was paid on October 1, 2011

Required: Complete the worksheet by using the trial balance and the information given.

Vius Company

Worksheet

December 31, 2011

Unadjusted Trial

Balance Adjustments

Adjusted Trial Balance

Account Titles DR CR DR CR DR CR

Cash $6,000 $6,000

Accounts Receivable 3,000 3,000

Prepaid Insurance 2,400 600 1,800

Office Supplies 1,000 600 400

Property, Plant & Equipment 10,000 10,000

Accumulated Depreciation $0 2,500 $2,500

Accounts Payable 5,000 5,000

Unearned Revenue 1,400 840 560

Bank Loan 3,500 3,500

Capital Account 9,250 9,250

Owner's Drawings 800 800

Service Revenue 9,000 840 9,840

Depreciation Expense 0 2,500 2,500

Insurance Expense 0 600 600

Interest Expense 0 0

Maintenance Expense 700 700

Supplies Expense 0 600 600

Rent Expense 2,100 2,100

Salaries Expense 900 900

Telephone Expense 500 500

Travel Expense 750 750

Total $28,150 $28,150 $4,540 $4,540 $30,650 $30,650

Part VII Closing Entries

Below is the year-end trial balance for Serava Marketing :

Serava Marketing Trial Balance For the period ending December 31, 2012 Account # Account Title DR CR 101 Cash 20,000 105 Accounts Receivable 10,000 110 Prepaid Insurance 6,000 200 Accounts Payable 3,500 205 Unearned Revenue 3,000 300 Capital Account 30,000 305 Owner's Drawing 1,800 401 Service Revenue 6,000 510 Insurance Expense 2,400 520 Rent Expense 1,200 530 Depreciation Expense 1,100 Totals 42,500 42,500

Prepare the journal entries to close the appropriate accounts using the income summary.

Date Description DR CR Dec 31 Service Revenue $6,000 Income Summary $6,000 To close the revenue accounts Dec 31 Income Summary $4,700 Insurance Expense $2,400 Rent Expense $1,200 Depreciation Expense $1,100 To close the expense accounts Dec 31 Income Summary $1,300 Capital Account $1,300 To close the income summary account Dec 31 Capital Account $1,800 Owner's Drawing $1,800 To close the owner's drawing account

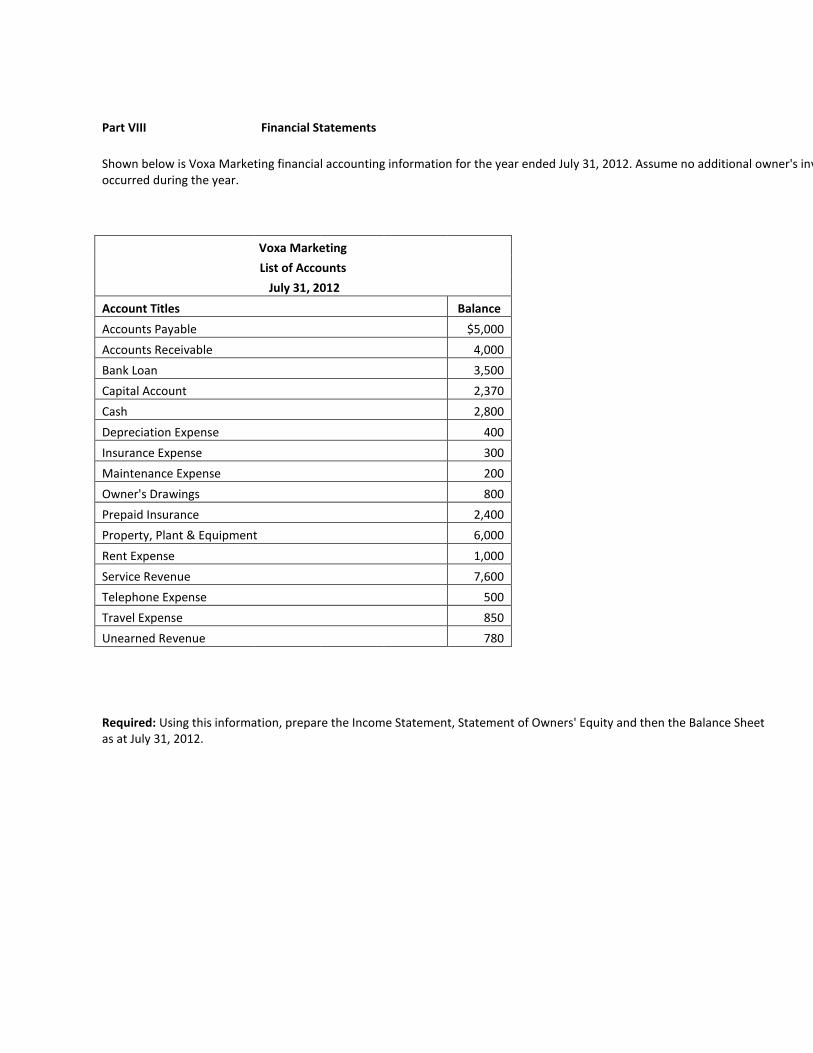

Part VIII Financial Statements

Shown below is Voxa Marketing financial accounting information for the year ended July 31, 2012. Assume no additional owner's investments occurred during the year.

Voxa Marketing

List of Accounts

July 31, 2012

Account Titles Balance Accounts Payable $5,000 Accounts Receivable 4,000 Bank Loan 3,500 Capital Account 2,370 Cash 2,800 Depreciation Expense 400 Insurance Expense 300 Maintenance Expense 200 Owner's Drawings 800 Prepaid Insurance 2,400 Property, Plant & Equipment 6,000 Rent Expense 1,000 Service Revenue 7,600 Telephone Expense 500 Travel Expense 850 Unearned Revenue 780

Required: Using this information, prepare the Income Statement, Statement of Owners' Equity and then the Balance Sheet as at July 31, 2012.

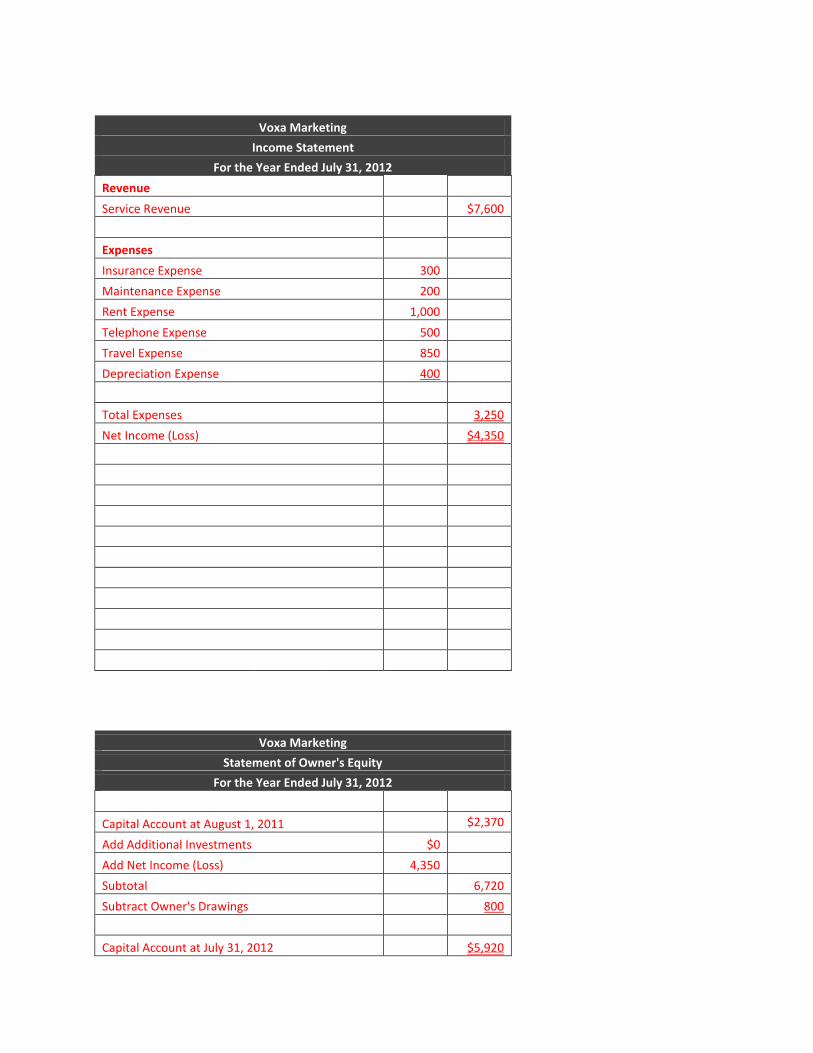

Voxa Marketing Income Statement For the Year Ended July 31, 2012 Revenue Service Revenue

$7,600

Expenses Insurance Expense 300 Maintenance Expense 200 Rent Expense 1,000 Telephone Expense 500 Travel Expense 850 Depreciation Expense 400

Total Expenses 3,250 Net Income (Loss)

$4,350

Voxa Marketing Statement of Owner's Equity For the Year Ended July 31, 2012 Capital Account at August 1, 2011 $2,370

Add Additional Investments $0 Add Net Income (Loss) 4,350 Subtotal 6,720 Subtract Owner's Drawings

800

Capital Account at July 31, 2012 $5,920

Voxa Marketing Balance Sheet As at July 31, 2012 Assets Cash $2,800 Accounts Receivable 4,000 Prepaid Insurance 2,400 Property, Plant & Equipment $6,400

Less: Accumulated Depreciation (400) 6,000

Total Assets $15,200 Liabilities Accounts Payable $5,000 Unearned Revenue 780 Bank Loan 3,500 Total Liabilities

$9,280

Owner's Equity

Capital Account 5,920

Total Liabilities & Owner's Equity $15,200