reverse revenue sharing: a modest proposal

TRANSCRIPT

Reverse Revenue Sharing: A Modest ProposalAuthor(s): Dwight R. LeeSource: Public Choice, Vol. 45, No. 3 (1985), pp. 279-289Published by: SpringerStable URL: http://www.jstor.org/stable/30023766 .

Accessed: 15/06/2014 17:37

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

Springer is collaborating with JSTOR to digitize, preserve and extend access to Public Choice.

http://www.jstor.org

This content downloaded from 188.72.126.118 on Sun, 15 Jun 2014 17:37:08 PMAll use subject to JSTOR Terms and Conditions

Public Choice 45: 279-289 (1985). m 1985 Martinus Nijhoff Publishers, Dordrecht. Printed in the Netherlands.

Reverse revenue sharing: A modest proposal

DWIGHT R. LEE Center for Study of Public Choice, George Mason University, Fairfax, VA 22030

1. Introduction

The standard economic argument in favor of grants from the central government to local governments is straight-forward. Many goods and ser- vices provided by local governments generate positive spillovers to other political jurisdictions; education and public health measure are commonly cited examples. Local governments, it is argued, will finance such a public good only to the point where local benefit equals local cost at the margin, and thus less than the socially efficient amounts will be provided. The cen- tral government, with its broader taxing power and wider constituency, is in a position to share revenue with local jurisdiction in such a way that the local marginal costs of providing particular goods are reduced and the effi- cient quantity of public goods can be motivated.

This argument for intergovernmental grants would be a compelling one if government could be reasonably characterized as a benevolent despot; an organizational entity whose sole objective is to promote the public welfare and which is able to act effectively in pursuit of this objective. Though this is obviously a naive characterization of government, many policy recom- mendations made by economists make sense only under the benevolent despot assumption. It is common for economists to argue as if they believed their advice was being anxiously awaited by a government motivated only by the desire to improve general economic efficiency. How else can we ex- plain the widespread view among economists that market failure establishes the presumption that corrective government action is justified?'

A much more realistic model of government, and certainly one more con- sistent with the methodological approach of economics, consists of political decision-makers pursuing personal objectives within the constraints estab- lished by the prevailing government institutions. In this model, political out- comes are the unintended consequences of the self interested actions of con- strained political actors. Once this private interest model of government is taken seriously many recommendations that make sense is the benevolent despot, or public interest model are stood on their head, so to speak.

This content downloaded from 188.72.126.118 on Sun, 15 Jun 2014 17:37:08 PMAll use subject to JSTOR Terms and Conditions

280

A political arrangement that would facilitate efficiency in the public interest model would generate waste and inefficiency in the private interest model, and vice versa. Therefore the normative implications of the two models will often be in direct contradiction to each other. Interestingly, however, the positive implications of the two models may be identical.2

The purpose of this paper is to look at revenue sharing arrangements from the perspective of the private interest model of government. In the next sec- tion it will be argued that existing revenue sharing arrangements in which the central government's taxing authority has been extended in order to make grants to local governments can be explained by the private interest model. These arrangements can be seen as a means of facilitating special in- terest influence at the cost of economically inefficient outcomes. In Section 3 a fiscal structure quite the opposite of current revenue sharing arrange- ments, a fiscal structure best described as reverse revenue sharing, will be examined. Though a radical restructuring of current arrangements, it will be argued that reverse revenue sharing has the potential for alleviating many of the inefficiencies that are encouraged by the existing structure of inter- governmental grants. Section 4 provides a geometric analysis of some of the efficiency implication of reverse revenue sharing. Some brief concluding remarks are offered in a final section.

2. A private interest explanation of political centralization

There are several reasons why politically influential special interests will favor centralization political power and fiscal control. Any group benefiting from government transfers will generally find advantage in a move toward more centralized political control and financing of its program. If the group is concentrated geographically this advantage is immediately apparent. More centralized control increases the size of the exploitable population and thus reduces the per capita cost of transferring a given amount to the interest group. This will reduce the political resistance to additional transfers because it will increase the rational ignorance and apathy of those paying the bill. Even if the members of a special interest group are spread over several political jurisdictions, with consolidation under one political authority doing nothing to increase the exploitable population, the con- solidation will likely still favor the interest group and its transfer effort. Even though the cost per capita of the interest group's program will be the same after consolidation as before, consolidation will reduce the cost (saving) any one individual will suffer (realize) if the program is increased (reduced) a given amount. Consequently, the political resistance to an ex- pansion of the program will diminish.' So it can be expected that special in- terest groups will take advantage of every opportunity to push in favor of

This content downloaded from 188.72.126.118 on Sun, 15 Jun 2014 17:37:08 PMAll use subject to JSTOR Terms and Conditions

281

more centralization in the political authority over their respective programs. Because of considerations more pertinent to the revenue sharing theme of

this paper, those whose interests are tied to the expansion of state and local governments will, somewhat surprisingly, also see advantages in concen- trating more political power in the national government. Consider the ad- vantage state and municipal governments realize when the national govern- ment assumes increased responsibility for raising the tax revenues that will be used to finance local government (non-federal) programs. The higher the percentage of the total tax bill raised by the federal government, the smaller will be the regional differences in relative tax burdens, and the less will be the tax competition between states.4 Furthermore, the size of federal grants to local governments are commonly determined by formulas containing tax effort provisions which create incentives for recipient governments to main- tain their tax revenues rather than use federal funds as a substitute for these revenues. In effect, federal revenue sharing arrangements serve as a means of forming and enforcing a tax cartel that allows government, in aggregate, to extract more money from the public.5 Indeed, recent empirical evidence appears to support the view that consolidating taxing authority has in- creased the tax burden at all levels of government.6

Centralizing taxation obviously works to the advantage of those in the federal government. Those who work for the different agencies and depart- ments of the federal government have a vested interest in expanding the pro- grams their agencies help finance and administer. Through the control of tax revenues to be returned to local governments, those in the federal government can make programs, that they will be instrumental in pro- viding, more attractive to local governments. Matching and categorical grants increase the amount of federal services local governments will de- mand, and generate opportunities for federal involvement in areas that have traditionally been the sole responsibility of local governments. With local governments able to benefit from projects that are being paid for largely by others, the ever present temptation to free ride leads to excessive and ineffi- cient demands for government spending. The more centralized the taxing and spending authority becomes the more the political process, responding as it will to private interests, will reward local governments for pursuing pro- jects that are worth less than they cost, and the less it will reward them for implementing these projects in a cost conscious matter. But because these social inefficiencies advance the private interests of politically organized and influential groups, it is easy to understand the relentless pressure toward increased centralization of political authority.

Increased government concentration can be explained by either the public interest or private interest model of government. If one models government as a benevolent despot, one with both the ability and desire to promote the public interest, then increased concentration can be explained by the desire

This content downloaded from 188.72.126.118 on Sun, 15 Jun 2014 17:37:08 PMAll use subject to JSTOR Terms and Conditions

282

to unlease this force for social good from the restraints imposed by political decentralization. On the other hand, the private interest model, as discussed in this section, also provides an explanation of the increased centralization of government.

3. Reverse revenue sharing

While the public and private interest models of government may, from the perspective of positive analysis, point in the same direction, the normative implications of these two models are diametrically opposed. If the public in- terest model is used to inform policy, centralization of government power will be recommended as the way to promote efficiency. It is, however, a move back to the checks and balances created by a dispersion, or decen- tralization, of political authority that is recommended by the private interest model of government. Consider, for example, a structure of intergovern- mental grants that is suggested by the private interests model.

The proposal considered is a simple one. It is best described as reverse revenue sharing and harkens back to the fiscal federalism of the Articles of Confederation, with an important difference. Under the present proposal, as under the Articles of Confederations, all taxing authority will reside in the states. As opposed to the system established under the Articles, however, the central government's access to tax revenue will not depend on the voluntary contributions of the states. Each state will be required to give the central government some proportion of the tax revenue it raises (hence the description, reverse revenue sharing), with this proportion, given by 7, being uniform over all states.7

Given the discussion in the previous section, it should be apparent that several advantages would arise from the political incentives established by this reverse revenue sharing proposal. First, the tendency for the political process to respond to special interest demands by imposing costs on the general public would be countered. Shifting the tax authority back to the state level would reduce the political power of special interest groups for the same reason centralizing the tax authority increases this power. But even at the state level, if each dollar raised by the government could be spent by the government, there would remain a tendency for special interest programs to be funded into the range where the concentrated benefits are less than the diffused costs, at the margin. Under reverse revenue sharing this tendency would be countered since for each dollar the state spent it would have to ex- tract more than a dollar from its citizens in taxes. Indeed, for many values of y government programs, even those motivated by special interest pressure, will be underfunded as measured by the standard efficiency criterion. In the extreme case 7 = 1, for example, state governments could

This content downloaded from 188.72.126.118 on Sun, 15 Jun 2014 17:37:08 PMAll use subject to JSTOR Terms and Conditions

283

spend none of the tax revenue it raised and obviously state programs would be underfunded, as would centrally funded programs. In section 4 the criterion for, and implications of, choosing the best y will be examined.

The incentives established by the reverse revenue sharing fiscal structure would also reduce the tendency for the central government to become in- volved in the provision of those services that are more appropriately pro- vided by the state governments. Political decision-makers in the central government would be very reluctant to finance goods that provide primarily state specific benefits; goods that if cost effective would likely be provided by the benefiting state. To the extent that the central government finances such goods, the states will raise less tax revenue and central government will receive less tax revenue.8 The political advantage would be in the central government directing its attention toward the provision of genuinely na- tional public goods and leaving it to the states to provide themselves with those goods which provide more geographically focused benefits. Obvious- ly, there is little hope that the incentives established by reverse revenue sharing will lead to the efficiency of a 'perfect correspondence' in public good provision.9 But, unless one accepts an extreme version of the public interest model of government there is even less hope that the efficiency 'perfect correspondence' would provide will be realized by centralizing fiscal decisions. The advantage here with reverse revenue sharing is that, with a reasonable choice of y, it puts self interest on the side of moving toward a more efficient allocation of fiscal responsibility.

Political competition among the states would be clearly increased under reverse revenue sharing. The differences in state fiscal decisions would not be masked over by an overlay of centrally imposed taxes, and the state that did not provide a desirable mix of services at competitive tax prices would begin losing its tax base to those states that did. Furthermore, reverse revenue sharing would convert the motivation to free ride into a force for governmentaI efficiency, rather than inefficiency as it is under the current fiscal structure. With the central government concentrating its effort on providing public goods generating widespread benefits, each state would recognize that the centrally provided benefits it receives will be largely in- dependent of the contribution it makes to the central government. Conse- quently, each state would face a free-rider motivation to reduce its contribu- tion. Under reverse revenue sharing the only way a state could reduce its contribution to the central government without at the same time reducing the sevices it provides would be to provide these services more efficiently.

This content downloaded from 188.72.126.118 on Sun, 15 Jun 2014 17:37:08 PMAll use subject to JSTOR Terms and Conditions

284

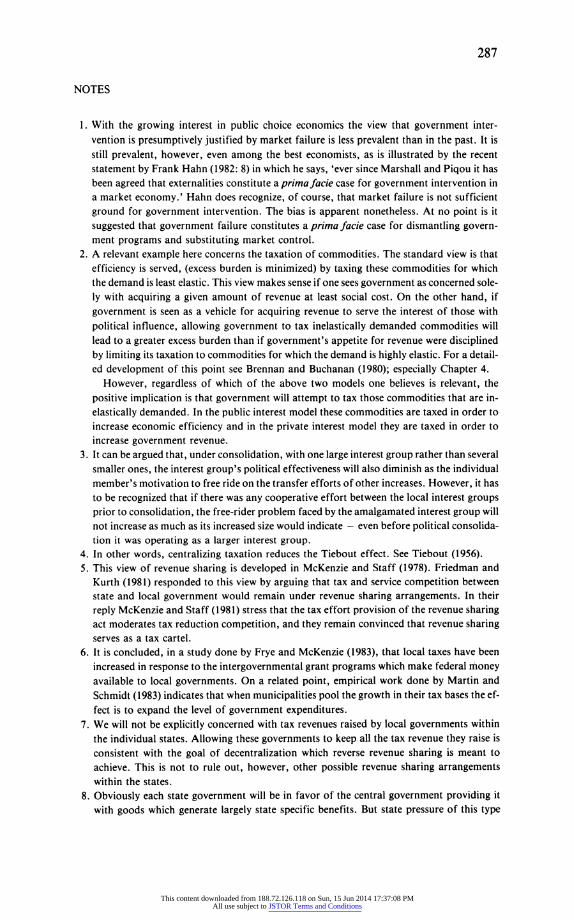

MB(y)

MC(y)

mci(y)

mb' (y)

y

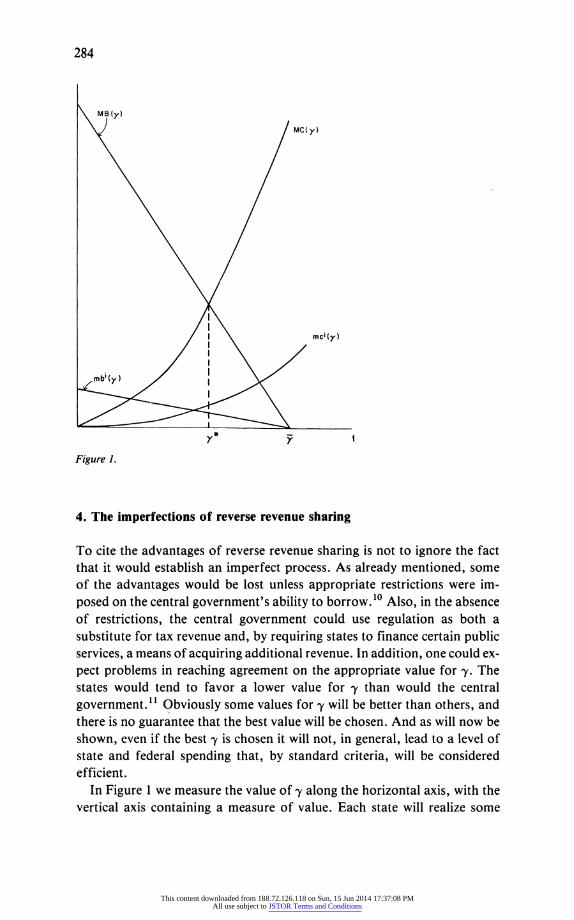

Figure 1.

4. The imperfections of reverse revenue sharing

To cite the advantages of reverse revenue sharing is not to ignore the fact that it would establish an imperfect process. As already mentioned, some of the advantages would be lost unless appropriate restrictions were im- posed on the central government's ability to borrow.'0 Also, in the absence of restrictions, the central government could use regulation as both a substitute for tax revenue and, by requiring states to finance certain public services, a means of acquiring additional revenue. In addition, one could ex- pect problems in reaching agreement on the appropriate value for y. The states would tend to favor a lower value for 7 than would the central government." Obviously some values for y will be better than others, and there is no guarantee that the best value will be chosen. And as will now be shown, even if the best y is chosen it will not, in general, lead to a level of state and federal spending that, by standard criteria, will be considered efficient.

In Figure 1 we measure the value of y along the horizontal axis, with the vertical axis containing a measure of value. Each state will realize some

This content downloaded from 188.72.126.118 on Sun, 15 Jun 2014 17:37:08 PMAll use subject to JSTOR Terms and Conditions

285

benefit at the margin from an increase in y as long as this increase generates additional central government revenue for providing goods and services to the states. The marginal benefit for state i is shown in Figure 1 as mb'(-y). This marginal benefit declines to zero for all states at y = y < 1, at which point tax revenue passed on to the central government is maximized. The national marginal benefit curve, MB(y), is shown as the vertical summation of the individual mbi(1y).12

The marginal cost that is imposed on state i when y is increased is given in Figure 1 by mc'(y). This marginal cost reflects two separate components: (1) the direct claim on real resources that state taxpayers have to relinquish to the central government, and (2) the allocative distortions that result from having to pay more than the marginal cost for state provided goods and ser- vices. Over some initial range for -y the distortion in (2) is a desirable counter to the political dominance of special interests over the broad taxpayers in- terest, and increasing y will improve the allocative efficiency of state fiscal decisions.13 Eventually, however, the additional distortion caused by in- creasing -y will more than offset the special interest distortion and both com- ponents (1) and (2) will represent positive marginal costs of increasing -y. The national marginal cost of increasing y is given by MC(y) in Figure 1 and is obtained by summing vertically the marginal cost curves of the individual states.

The 'efficient' value of y is determined by the conventional intersection between the marginal benefit and marginal cost schedule and is shown in Figure 1 as -y*. It is clear that, in the absence of side payments, disagreement will surround the choice of y. Some states will find the intersection between their mb'('y) and mc'(y) curves to the left of y* and they will prefer a -y < y*. On the other hand, other states will prefer a -y > y*. Those who identify their interest with the size of the central government would likely prefer -y = 7, the value that maximizes the central government's receipts. Presumably, however, under a reverse revenue sharing scheme it is the col- lective decisions of the states that will be controlling and a value for y in the neigborhood of -* will be chosen.

Even if y* is chosen, however, we will not satisfy all of the marginal con- ditions normally associated with efficiency. The requirement that the same -y apply to all states imposes a constraint that will, in general, prevent equalizing at all the margins normally considered relevant.14 In comparison to the ideal, for example, either too little or too much expenditure can be motivated at the state level when y is equal to y*,15 and similarly for expen- ditures of the central government. What is less obvious, but easily establish- ed, is that too little spending at the state level implies too little spending at the central level, and similarly, too much state spending implies too much central government spending."6

Assume, for example, that at y* too little is being spent at the state level;

This content downloaded from 188.72.126.118 on Sun, 15 Jun 2014 17:37:08 PMAll use subject to JSTOR Terms and Conditions

286

meaning that the value of the goods the states would provide, if the states were able to spend a marginally higher percentage of the tax revenues they raised, would be greater than the value of the private goods sacrificed. This implies that the distortion resulting from states having to raise more than a dollar for each dollar spent has more than offset the special interest distor- tion that pushes in the direction of excessive state spending. Of course, it is not desirable to reduce ' because at y* the marginal value of the centrally provided goods equals the marginal cost of providing them, this marginal cost reflecting the direct resource cost plus the positive distortion cost just mentioned. Clearly this implies that the value of the centrally provided goods is greater than the direct marginal resource cost of providing them, and thus by conventional standards too little is being spent by the central government. Similarly it can be argued that over provision at the state level will be accompanied by over provision at the central level.

Reverse revenue sharing is obviously an imperfect arrangement. In com- parison to public interest models of government in which centrally directed government grants are an effective means for internalizing fiscal exter- nalities, the reverse revenue sharing arrangement just outlined will have little to recommend it. But the argument here is not that reverse revenue sharing would be the appropriate fiscal structure for an ideal world. The more modest claim is that, in a world in which individuals are more concern- ed with private advantage than with public advantage, reverse revenue sharing offers significant advantages over present revenue sharing arrange- ments.

5. Conclusion

While no claim is made that reverse revenue sharing is, even from a private interest perspective, the best fiscal arrangement, it has been argued that it represents an improvement over current arrangements in important ways. Still, reverse revenue sharing surely will be seen by most as a rather extreme proposal. For some this will come from the fact that it is the public interest model of government that remains dominant in structuring their view of the political process. But even those who accept the private interest model of government will see the proposal as extreme in terms of its political in- feasibility. The very considerations that make the decentralization of the reverse revenue proposal desirable (i.e., reducing the power of political in- terest groups) make it unlikely that it will generate enthusiastic political sup- port. Indeed, few things would provide more compelling evidence that reverse revenue sharing is a badly flawed proposal than the formation of an effective coalition of political interests in favor of it. I conclude this paper with confidence that the case for reverse revenue sharing is completely safe from this damaging prospect.

This content downloaded from 188.72.126.118 on Sun, 15 Jun 2014 17:37:08 PMAll use subject to JSTOR Terms and Conditions

287

NOTES

1. With the growing interest in public choice economics the view that government inter- vention is presumptively justified by market failure is less prevalent than in the past. It is still prevalent, however, even among the best economists, as is illustrated by the recent statement by Frank Hahn (1982: 8) in which he says, 'ever since Marshall and Piqou it has been agreed that externalities constitute a primafacie case for government intervention in a market economy.' Hahn does recognize, of course, that market failure is not sufficient

ground for government intervention. The bias is apparent nonetheless. At no point is it

suggested that government failure constitutes a prima facie case for dismantling govern- ment programs and substituting market control.

2. A relevant example here concerns the taxation of commodities. The standard view is that

efficiency is served, (excess burden is minimized) by taxing these commodities for which the demand is least elastic. This view makes sense if one sees government as concerned sole-

ly with acquiring a given amount of revenue at least social cost. On the other hand, if

government is seen as a vehicle for acquiring revenue to serve the interest of those with

political influence, allowing government to tax inelastically demanded commodities will lead to a greater excess burden than if government's appetite for revenue were disciplined by limiting its taxation to commodities for which the demand is highly elastic. For a detail- ed development of this point see Brennan and Buchanan (1980); especially Chapter 4.

However, regardless of which of the above two models one believes is relevant, the

positive implication is that government will attempt to tax those commodities that are in-

elastically demanded. In the public interest model these commodities are taxed in order to increase economic efficiency and in the private interest model they are taxed in order to increase government revenue.

3. It can be argued that, under consolidation, with one large interest group rather than several smaller ones, the interest group's political effectiveness will also diminish as the individual member's motivation to free ride on the transfer efforts of other increases. However, it has to be recognized that if there was any cooperative effort between the local interest groups prior to consolidation, the free-rider problem faced by the amalgamated interest group will not increase as much as its increased size would indicate - even before political consolida- tion it was operating as a larger interest group.

4. In other words, centralizing taxation reduces the Tiebout effect. See Tiebout (1956). 5. This view of revenue sharing is developed in McKenzie and Staff (1978). Friedman and

Kurth (1981) responded to this view by arguing that tax and service competition between state and local government would remain under revenue sharing arrangements. In their

reply McKenzie and Staff (1981) stress that the tax effort provision of the revenue sharing act moderates tax reduction competition, and they remain convinced that revenue sharing serves as a tax cartel.

6. It is concluded, in a study done by Frye and McKenzie (1983), that local taxes have been increased in response to the intergovernmental grant programs which make federal money available to local governments. On a related point, empirical work done by Martin and Schmidt (1983) indicates that when municipalities pool the growth in their tax bases the ef- fect is to expand the level of government expenditures.

7. We will not be explicitly concerned with tax revenues raised by local governments within the individual states. Allowing these governments to keep all the tax revenue they raise is consistent with the goal of decentralization which reverse revenue sharing is meant to achieve. This is not to rule out, however, other possible revenue sharing arrangements within the states.

8. Obviously each state government will be in favor of the central government providing it with goods which generate largely state specific benefits. But state pressure of this type

This content downloaded from 188.72.126.118 on Sun, 15 Jun 2014 17:37:08 PMAll use subject to JSTOR Terms and Conditions

288

should be no greater under reverse revenue sharing than under current arrangements. Furthermore, under reverse revenue sharing, the effectiveness of state pressure for federal assistance would be limited not only by federal incentives, but also by a federal revenue constraint that is less yielding than is currently the case to the desire for more. The impor- tance of borrowing restrictions on the federal government is obviously relevant here. For a detailed discussion of the advantages of such restrictions, see Buchanan and Wagner (1977).

9. In order to realize a perfect correspondence, 'a structure of governments, in which the jurisdiction that determines the level of provision of each public good includes precisely the set of individuals who consume the good,' would be required. See Oates (1972: 34).

10. The appropriate constraint on central government borrowing may be less restrictive under reverse revenue sharing than under current arrangements (though more restrictive than is currently the case) in order to replace some of the fiscal flexibility given up with the power to tax.

11. This disagreement may not be as great as would first appear. Since -y is uniform over all states, no one state can free ride by attempting to get a lower -y for itself. Therefore the desirability of having centrally provided public goods will moderate state pressure for a lower 7. Also, the central government will recognize that its revenue will become a de- clining function of -y long before it reaches unity. Certainly at the constitutional level of decision-making this will temper upward pressure on y, although at the level of ordinary politics central government decision-makers may see short-run advantages in pushing y beyond long-run revenue maximizing limits. The problem here is analogous to the one discussed in Buchanan and Lee (1982). Clearly the advantage is in treating -y as a consti- tuentional variable; one that is insulated against the pressures of day to day politics.

12. This does not depend on the central government providing nothing but pure public goods that provide national benefits. Even if much of the central government's revenue goes to provide state specific goods, as long as there are no synergistic effects between the benefits received by the individual states, the vertical summation is appropriate.

13. It is conceivable that this allocative effect could more than offset the first component of cost (the direct resource cost) and result in a negative marginal cost to increases in -y. How likely this possibility is, however, is completely conjectural and also irrelevant to our analysis.

14. In a public interest world, it would make sense to discard this constraint and choose the most efficient y for each state. Allowing this possibility in a private interest world, however, may reduce efficiency. Each state would have a motivation to devote resources to the formation of unstable coalitions in favor of lowering selective y's. This not only diverts resources away from productive employments, it is not likely to result in choices of -y' that are even remotely efficient. This is a special case of the more general proposition that constitutional restraints on government seldom, if ever, make sense in a public interest model of government, but make a great deal of sense in a private interest model of government.

15. We are speaking here in a aggregate sense. Because of the uniform requirement on -, it is obviously possible that some states will be spending too much and others too little even when aggregate state expenditures is, say, too small.

16. Whether or not, relative to an efficiency norm, too much or too little government spending occurs under reverse revenue sharing, there can be little doubt that switching to such a fiscal arrangement would reduce government spending below those levels realized under current arrangements.

This content downloaded from 188.72.126.118 on Sun, 15 Jun 2014 17:37:08 PMAll use subject to JSTOR Terms and Conditions

289

REFERENCES

Brennan, G., and Buchanan, J.M. (1980). Thepower to tax: Analytical foundations of a fiscal constitution. Cambridge: Cambridge University Press.

Buchanan, J.M., and Lee, D.R. (1982). Politics, time, and the Laffer curve. Journal of Political Economy 90 (August): 816-819.

Buchanan, J.M., and Wagner, R.E. (1977). Democracy in deficit: The political legacy of Lord

Keynes. New York: Academic Press.

Friedman, D.D., and Kurth, M.M. (1981). Revenue sharing and monopoly government. Public Choice 37 (2): 365-370.

Frye, E.B., and McKenzie, R.B. (1983). Impact of federal aid on state and local taxes. Work-

ing Paper, Economics Department, Clemson University. Hahn, F. (1982). Reflections on the invisible hand. Lloyds Bank Review, No. 144 (April):

1-21.

Martin, D.T., and Schmidt, J.R. (1983). Expenditure effects of metropolitan tax base sharing: A public choice analysis. Public Choice 40 (2): 175-186.

McKenzie, R.B., and Staff, R.J. (1978). Revenue sharing and monopoly government. Public Choice 33 (3): 93-97.

McKenzie, R.B., and Staff, R.J. (1981). Revenue sharing and monopoly government: A Re-

ply. Public Choice 37 (2): 371-374.

Oates, W.E. (1972). Fiscal federalism. New York: Harcourt Brace Jovanovich.

Tiebout, C. (1956). A pure theory of local expenditures. Journal of Political Economy 64 (Oc- tober): 412-424.

This content downloaded from 188.72.126.118 on Sun, 15 Jun 2014 17:37:08 PMAll use subject to JSTOR Terms and Conditions