revenue recognition including construction contracts

TRANSCRIPT

Revenue recognition including construction contracts

Academic Resource Center

Revenue recognition including construction contracts Page 2

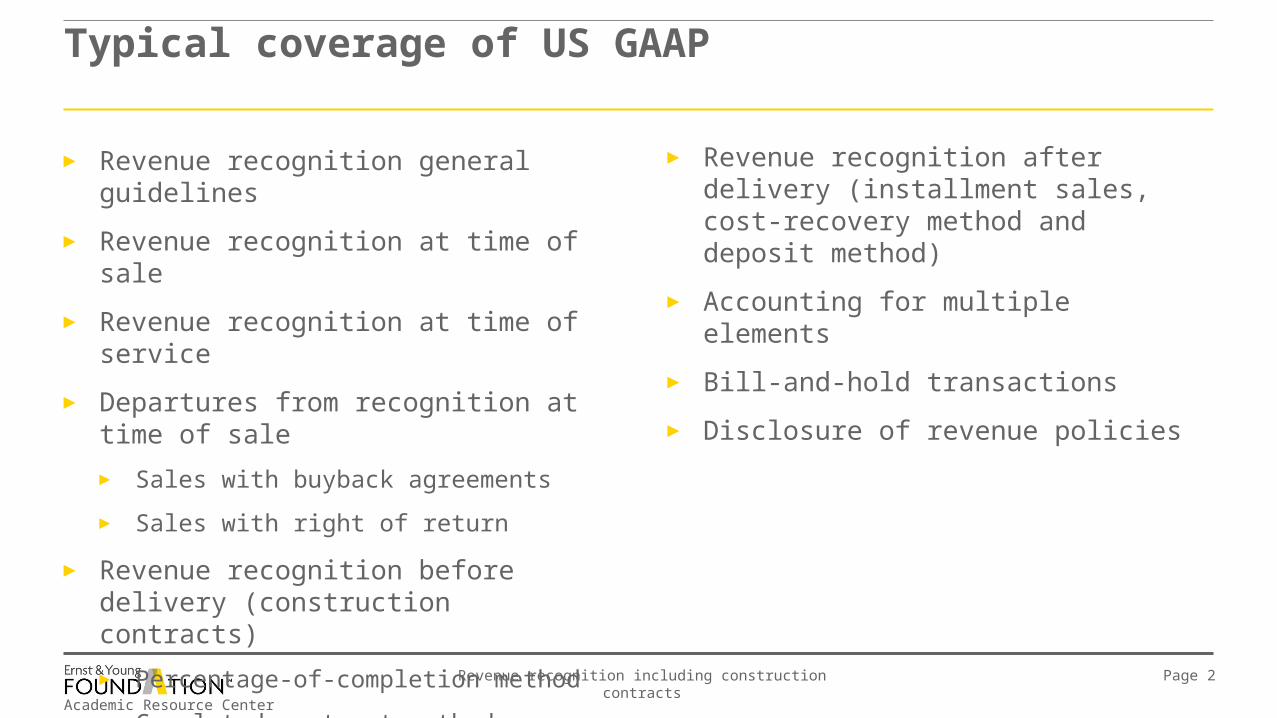

Typical coverage of US GAAP

► Revenue recognition general guidelines

► Revenue recognition at time of sale

► Revenue recognition at time of service

► Departures from recognition at time of sale

► Sales with buyback agreements

► Sales with right of return

► Revenue recognition before delivery (construction contracts)

► Percentage-of-completion method

► Completed-contract method

► Revenue recognition after delivery (installment sales, cost-recovery method and deposit method)

► Accounting for multiple elements

► Bill-and-hold transactions

► Disclosure of revenue policies

Academic Resource Center

Revenue recognition including construction contracts Page 3

Executive summary

► General:

► Under both IFRS and US GAAP, revenue is not recognized until it is both realized (realizable) and earned.

► The preponderance of the accounting guidance on revenue recognition for IFRS is contained in IAS 18 and IAS 11. Under US GAAP, there is a large volume of guidance on revenue recognition, including numerous industry standards. Although IAS 18 and IAS 11 contain the IFRS general guidance for revenue recognition, there is a lack of specific guidance in relation to industry-specific issues and multiple-element arrangements.

► Revenue recognition at the time of sale: under IFRS, there is no specific requirement that persuasive evidence of a sale must exist before revenue is recognized as there is under US GAAP.

► Revenue recognition at the time of service: IFRS allows the use of the percentage-of-completion model for service contracts. This model is prohibited for service contracts under US GAAP.

Academic Resource Center

Revenue recognition including construction contracts Page 4

Executive summary

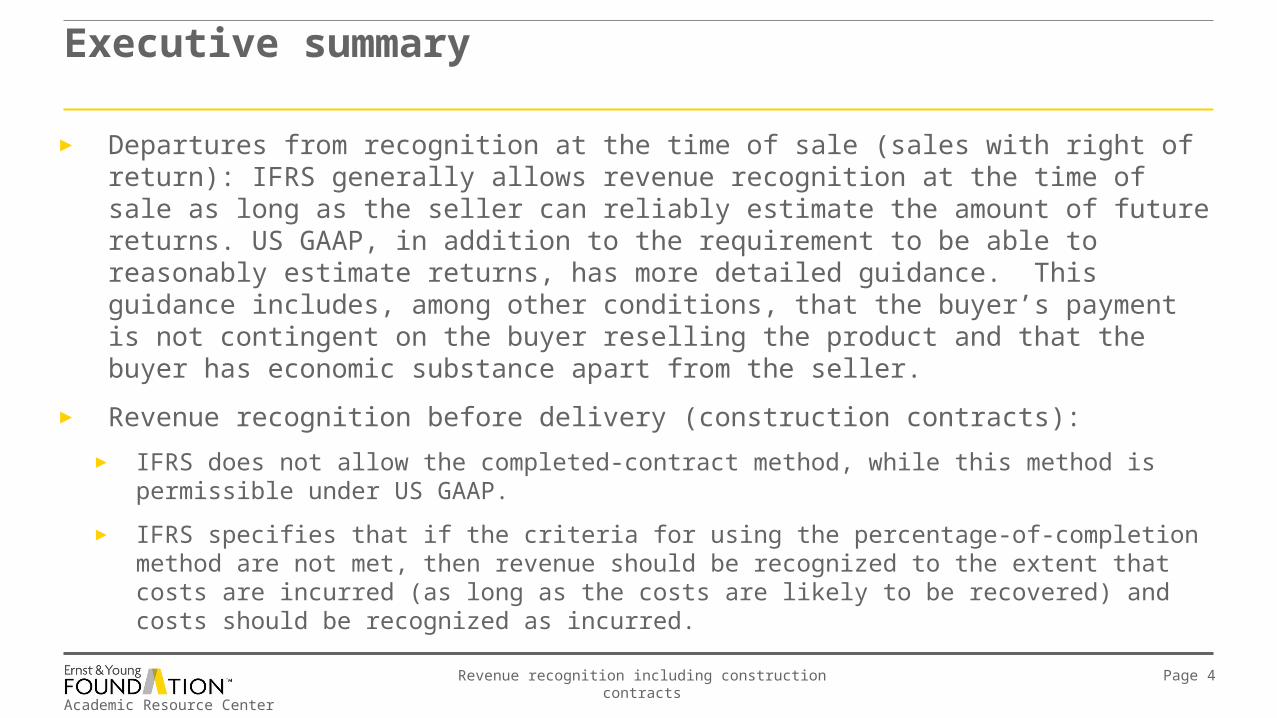

► Departures from recognition at the time of sale (sales with right of return): IFRS generally allows revenue recognition at the time of sale as long as the seller can reliably estimate the amount of future returns. US GAAP, in addition to the requirement to be able to reasonably estimate returns, has more detailed guidance. This guidance includes, among other conditions, that the buyer’s payment is not contingent on the buyer reselling the product and that the buyer has economic substance apart from the seller.

► Revenue recognition before delivery (construction contracts):

► IFRS does not allow the completed-contract method, while this method is permissible under US GAAP.

► IFRS specifies that if the criteria for using the percentage-of-completion method are not met, then revenue should be recognized to the extent that costs are incurred (as long as the costs are likely to be recovered) and costs should be recognized as incurred.

Academic Resource Center

Revenue recognition including construction contracts Page 5

Executive summary

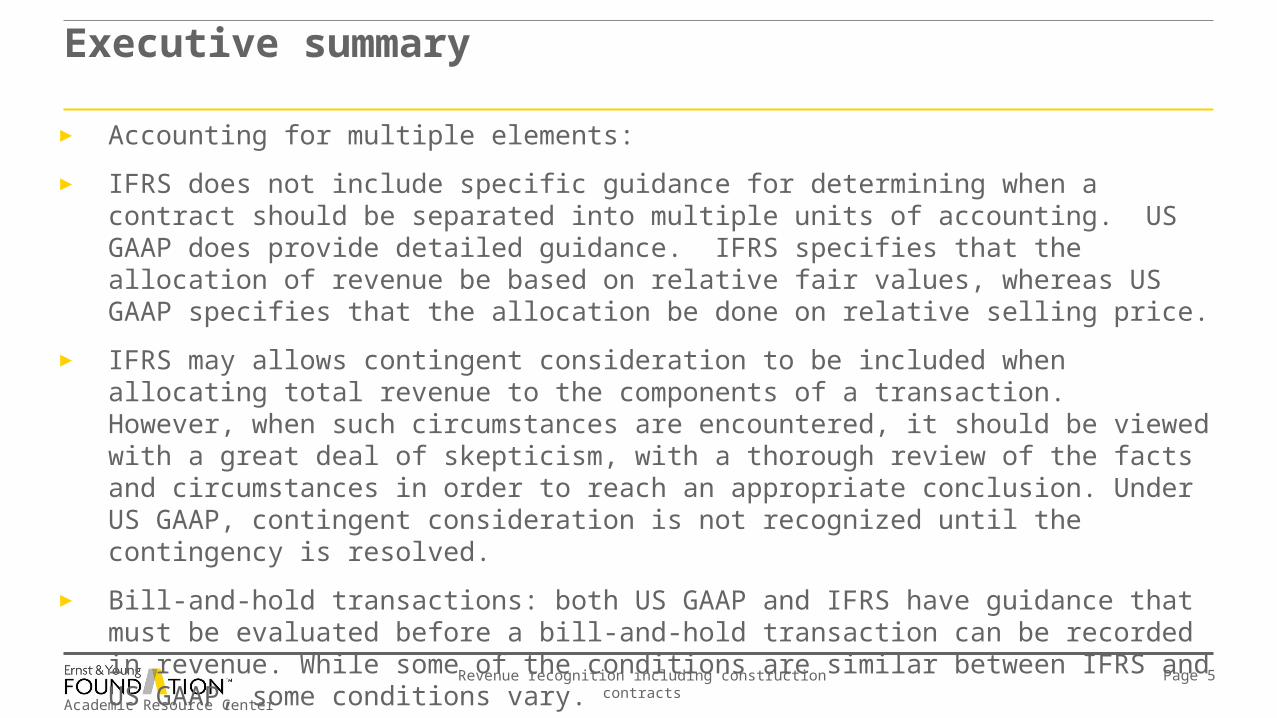

► Accounting for multiple elements:

► IFRS does not include specific guidance for determining when a contract should be separated into multiple units of accounting. US GAAP does provide detailed guidance. IFRS specifies that the allocation of revenue be based on relative fair values, whereas US GAAP specifies that the allocation be done on relative selling price.

► IFRS may allows contingent consideration to be included when allocating total revenue to the components of a transaction. However, when such circumstances are encountered, it should be viewed with a great deal of skepticism, with a thorough review of the facts and circumstances in order to reach an appropriate conclusion. Under US GAAP, contingent consideration is not recognized until the contingency is resolved.

► Bill-and-hold transactions: both US GAAP and IFRS have guidance that must be evaluated before a bill-and-hold transaction can be recorded in revenue. While some of the conditions are similar between IFRS and US GAAP, some conditions vary.

Academic Resource Center

Revenue recognition including construction contracts Page 6

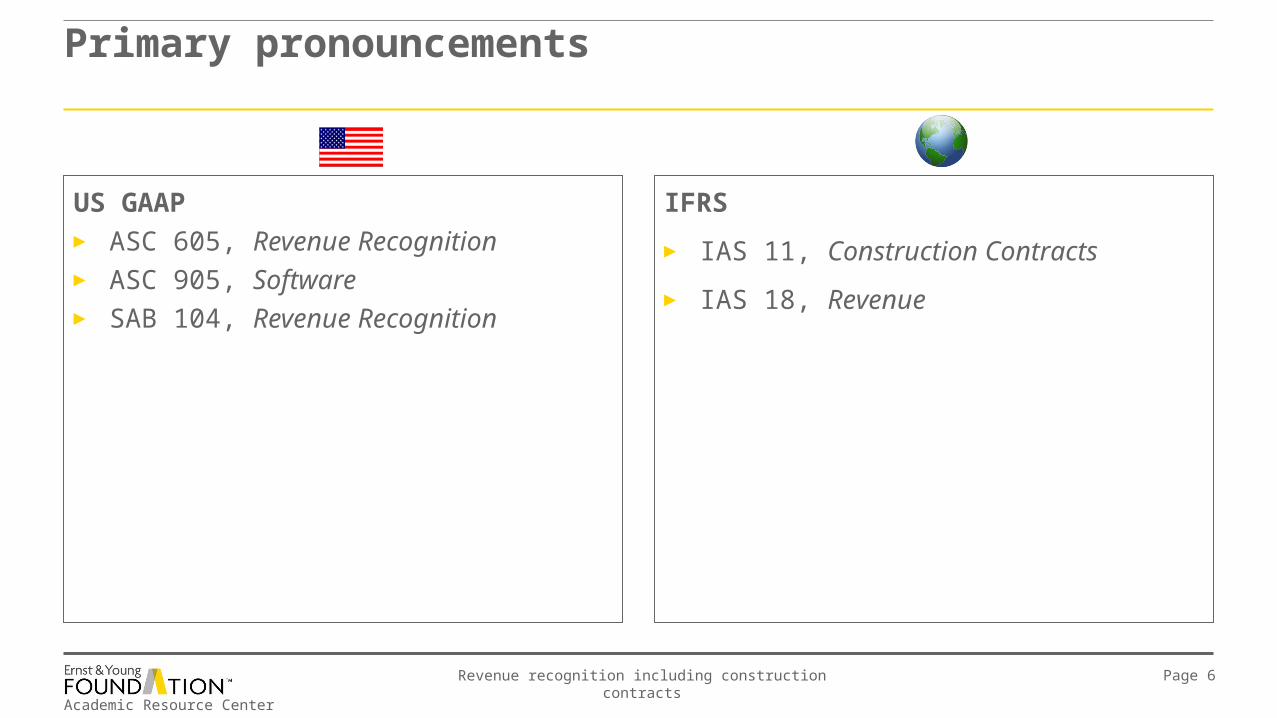

Primary pronouncements

US GAAP► ASC 605, Revenue Recognition► ASC 905, Software► SAB 104, Revenue Recognition

IFRS

► IAS 11, Construction Contracts

► IAS 18, Revenue

Academic Resource Center

Revenue recognition including construction contracts Page 7

Progress on convergence

► The Boards are currently conducting a joint project to develop concepts for revenue recognition and a standard based on those concepts.

► The Boards issued an Exposure Draft (ED), Revenue from Contracts with Customers, in June 2010 that describes a model to determine the appropriate amount, timing and uncertainty of revenue recognition consisting of the following steps:

1) Identify the contracts(s) with the customer

2) Identify the separate performance obligations in the contract

3) Determine the transaction price

4) Allocate the transaction price to the separate performance obligations

5) Recognize revenue when each performance obligation is satisfied.► ED public comments were due by October 22, 2010. In June 2011, the Boards

decided to issue a new ED for public comment because they made significant changes to the proposal during re-deliberations. The new ED is expected to be issued in the second half of 2011 with a 120 day comment period.

► The industries most likely to be impacted by the proposed guidance are software, entertainment, telecommunications, real estate, retail (depending on right of return) and construction.

Academic Resource Center

Revenue recognition including construction contracts Page 8

Revenue recognition general guidelines

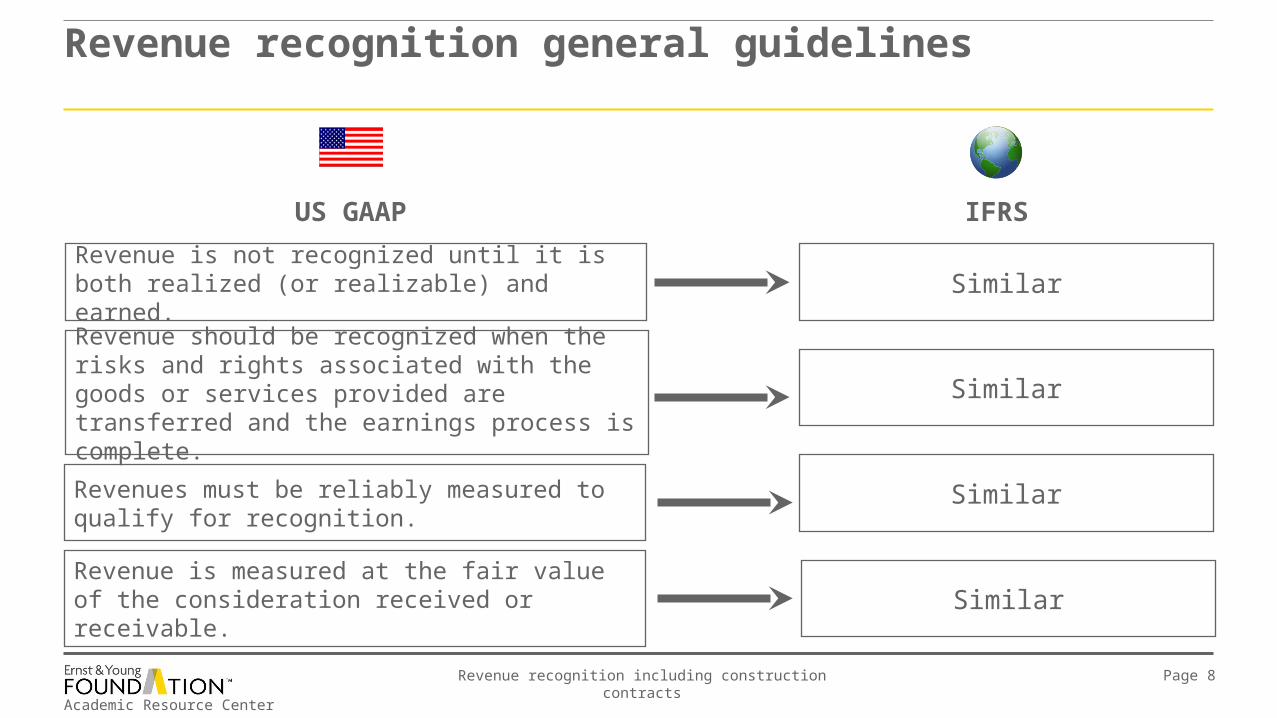

Revenue is not recognized until it is both realized (or realizable) and earned.

Revenue should be recognized when the risks and rights associated with the goods or services provided are transferred and the earnings process is complete.

Similar

Similar

IFRSUS GAAP

Revenues must be reliably measured to qualify for recognition.

Revenue is measured at the fair value of the consideration received or receivable.

Similar

Similar

Academic Resource Center

Revenue recognition including construction contracts Page 9

Revenue recognition general guidelines

IFRS

► Although IAS 18 and IAS 11 contain general guidance for revenue recognition, there is a lack of specific guidance in relation to industry-specific issues and multiple-element arrangements.

► As IFRS does not include as much guidance on specific transactions or events as US GAAP, some companies may choose to take advantage of the hierarchy set out in IAS 8, paragraph 11. This guidance allows companies to use other GAAP (e.g., US GAAP) to the extent it would not contradict guidance contained in IFRS. However, it is important to understand that the IAS 8 hierarchy does not require companies to refer to US GAAP.

► Based on the parameters for adopting IFRS, it is possible that a transaction or event will be accounted for differently under IFRS than when a company uses US GAAP.

US GAAP

► There is a large volume of guidance on revenue recognition, including numerous industry standards.

Academic Resource Center

Revenue recognition including construction contracts Page 10

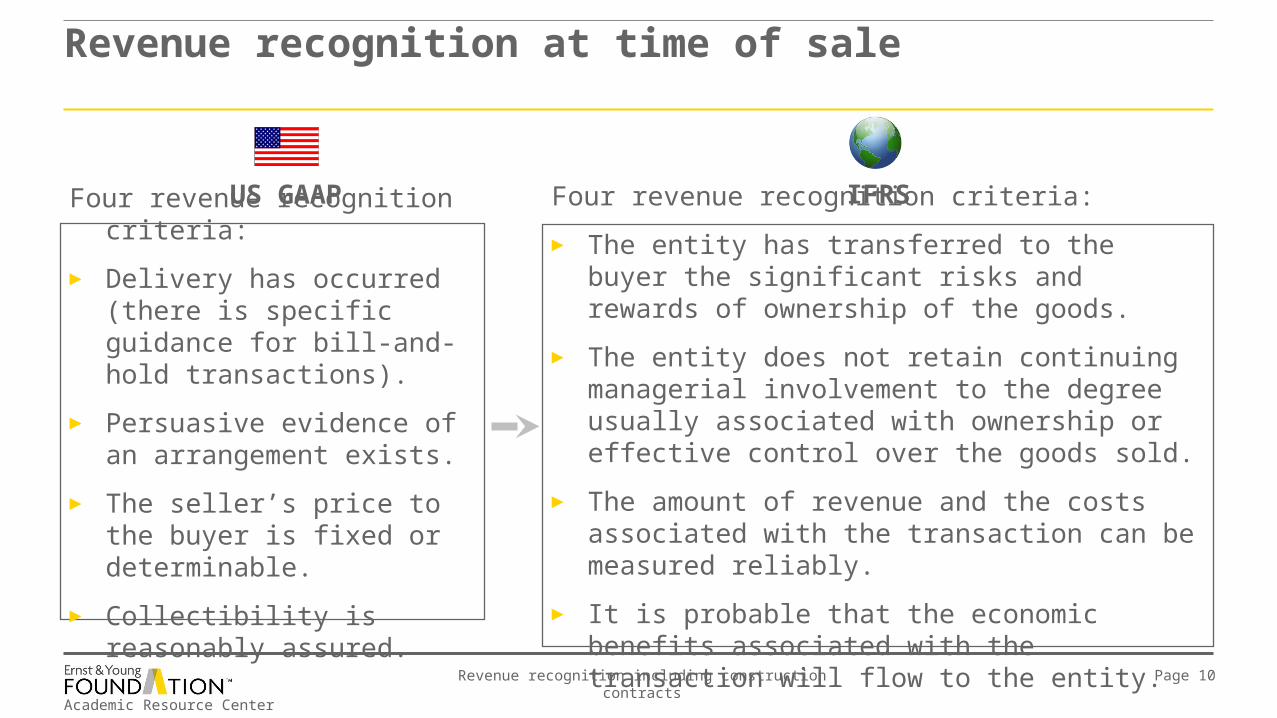

Revenue recognition at time of sale

Four revenue recognition criteria:

► Delivery has occurred (there is specific guidance for bill-and-hold transactions).

► Persuasive evidence of an arrangement exists.

► The seller’s price to the buyer is fixed or determinable.

► Collectibility is reasonably assured.

Four revenue recognition criteria:

► The entity has transferred to the buyer the significant risks and rewards of ownership of the goods.

► The entity does not retain continuing managerial involvement to the degree usually associated with ownership or effective control over the goods sold.

► The amount of revenue and the costs associated with the transaction can be measured reliably.

► It is probable that the economic benefits associated with the transaction will flow to the entity.

IFRSUS GAAP

Academic Resource Center

Revenue recognition including construction contracts Page 11

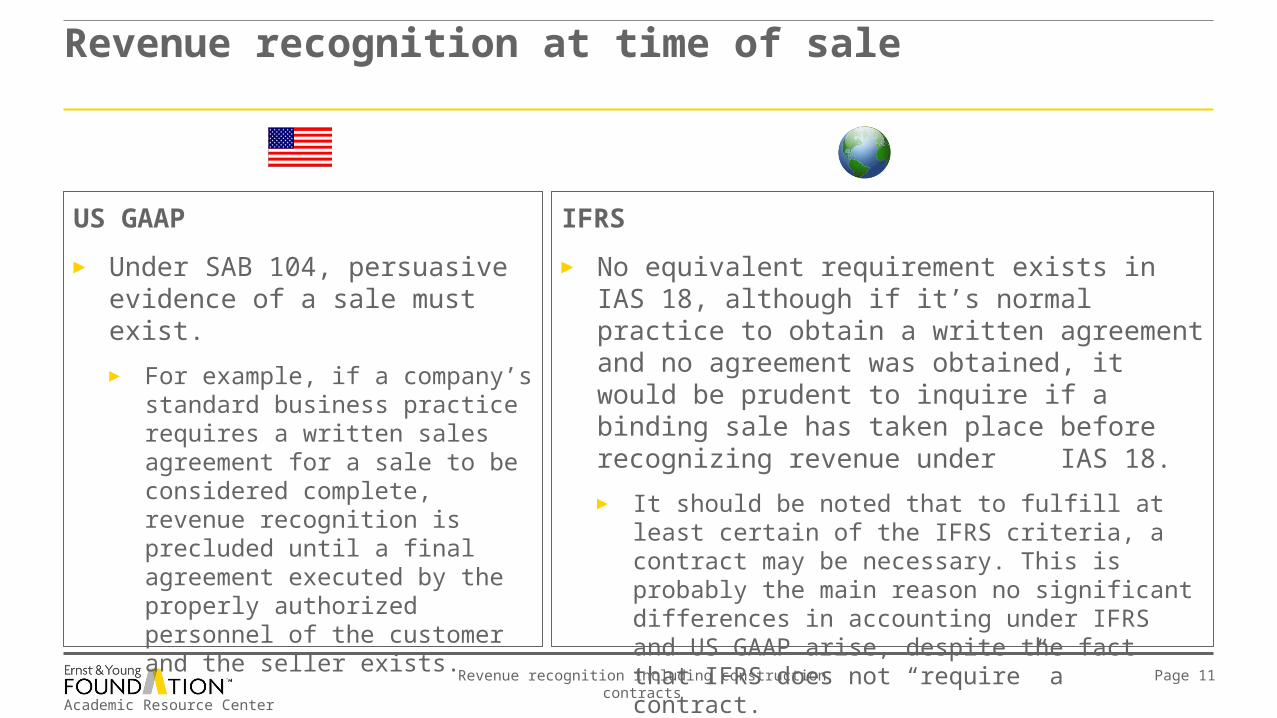

IFRS

► No equivalent requirement exists in IAS 18, although if it’s normal practice to obtain a written agreement and no agreement was obtained, it would be prudent to inquire if a binding sale has taken place before recognizing revenue under IAS 18.

► It should be noted that to fulfill at least certain of the IFRS criteria, a contract may be necessary. This is probably the main reason no significant differences in accounting under IFRS and US GAAP arise, despite the fact that IFRS does not “require” a contract.

US GAAP

► Under SAB 104, persuasive evidence of a sale must exist.

► For example, if a company’s standard business practice requires a written sales agreement for a sale to be considered complete, revenue recognition is precluded until a final agreement executed by the properly authorized personnel of the customer and the seller exists.

Revenue recognition at time of sale

Academic Resource Center

Revenue recognition including construction contracts Page 12

Example 1 – persuasive evidence of a sale

Car Company has operations in the US and Malaysia. Currently, the US operations require a written contract be signed when a car is sold. Car Company’s Malaysian operations only require an oral commitment to buy a car. It should be noted that Malaysians feel their word is binding and few cancellations have ever occurred. In December, the US operations delivered 200 cars for $30,000 each. Written contracts were received in December for 198 cars. Contracts on the remaining two cars were received in the first week of January. In December the Malaysian operations delivered 40 cars for $35,000 each. Before the end of December, it had oral acceptance commitments from all 40 buyers and actual written contracts with 30 of the buyers. The remaining 10 written contracts were received in the first week of January.

Persuasive evidence of a sale example

► Assuming the US operations report using US GAAP, show the required sales journal entries for December.

► Assuming the Malaysian operations report using IFRS, show the required sales journal entries for December.

► Assuming the consolidated group financials are based on US GAAP, show the required consolidated journal entries for December sales.

Academic Resource Center

Revenue recognition including construction contracts Page 13

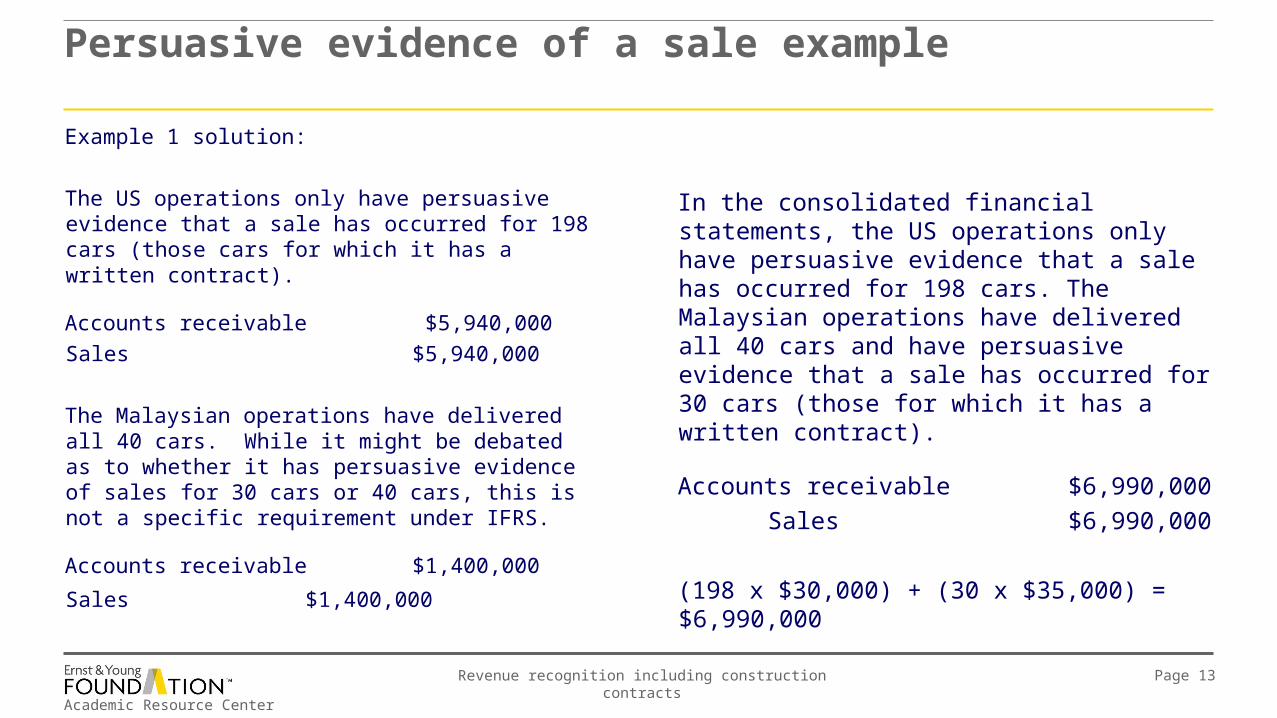

Example 1 solution:

The US operations only have persuasive evidence that a sale has occurred for 198 cars (those cars for which it has a written contract).

Accounts receivable $5,940,000

Sales $5,940,000

The Malaysian operations have delivered all 40 cars. While it might be debated as to whether it has persuasive evidence of sales for 30 cars or 40 cars, this is not a specific requirement under IFRS.

Accounts receivable $1,400,000

Sales $1,400,000

Persuasive evidence of a sale example

In the consolidated financial statements, the US operations only have persuasive evidence that a sale has occurred for 198 cars. The Malaysian operations have delivered all 40 cars and have persuasive evidence that a sale has occurred for 30 cars (those for which it has a written contract).

Accounts receivable $6,990,000

Sales $6,990,000

(198 x $30,000) + (30 x $35,000) = $6,990,000

Academic Resource Center

Revenue recognition including construction contracts Page 14

With respect to service contracts, the specific-performance method is allowed. Generally, under this approach, performance consists of the execution of a single act and revenue is recognized when that act takes place. In addition, if the services are performed by an indeterminate number of acts over a specified period of time, revenue can be recognized on a straight-line basis.

Similar

IFRSUS GAAP

Revenue recognition at time of service

Academic Resource Center

Revenue recognition including construction contracts Page 15

IFRS

► Costs with respect to service contracts may be expensed as incurred depending on a company’s policy for recognizing revenue for service contracts, but they could be deferred if the company is using the percentage-of-completion method.

US GAAP

► Costs with respect to service contracts are expensed as incurred. The percentage-of-completion model is prohibited by US GAAP under ASC 605-35.

Revenue recognition at time of service

Academic Resource Center

Revenue recognition including construction contracts Page 16

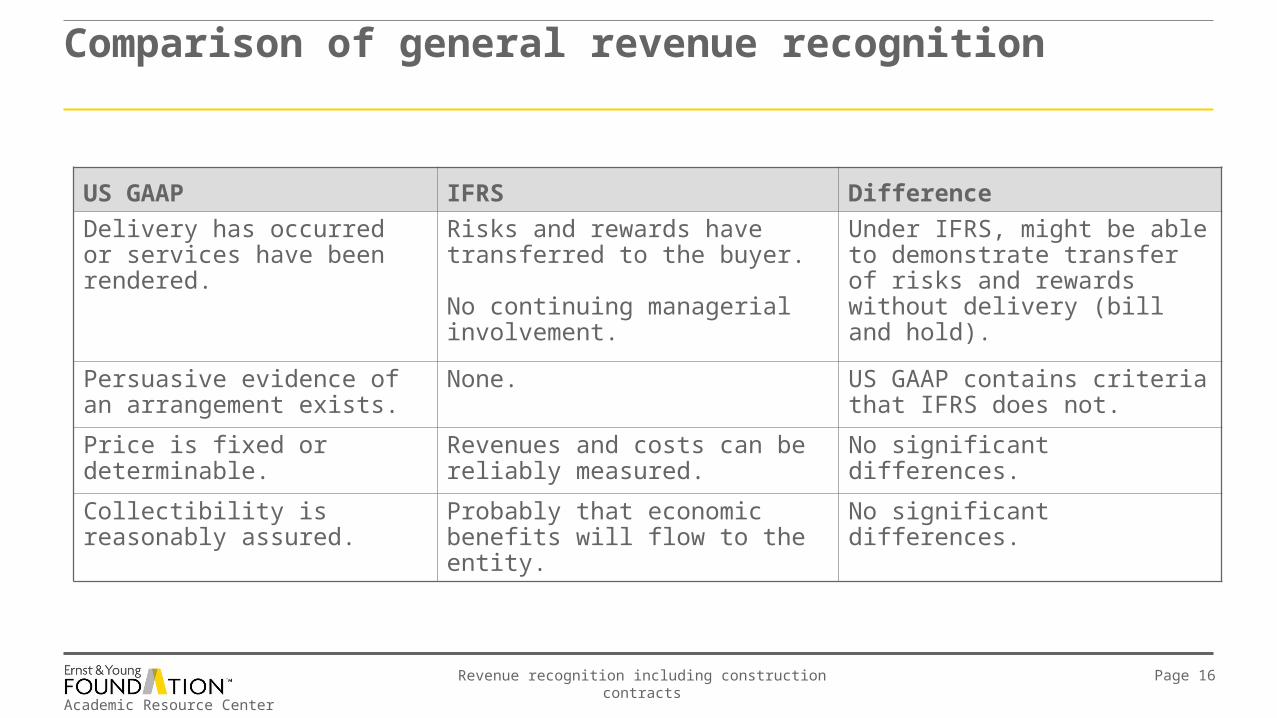

Comparison of general revenue recognition

US GAAP IFRS Difference

Delivery has occurred or services have been rendered.

Risks and rewards have transferred to the buyer.

No continuing managerial involvement.

Under IFRS, might be able to demonstrate transfer of risks and rewards without delivery (bill and hold).

Persuasive evidence of an arrangement exists.

None. US GAAP contains criteria that IFRS does not.

Price is fixed or determinable. Revenues and costs can be reliably measured.

No significant differences.

Collectibility is reasonably assured.

Probably that economic benefits will flow to the entity.

No significant differences.

Academic Resource Center

Revenue recognition including construction contracts Page 17

Example 2 – revenue recognition when rendering services

Advisco, a strategic advisory firm, contracted with Temple Manufacturing Company (Temple) on January 1, 2010, to provide services to help compare Temple’s business to peer groups, determine leading practices and develop strategic alternatives for performance improvements.

The services provided by Advisco will include subscription offerings that provide a mix of on-demand leading practice research, advisor access, benchmarking and business transformation services over a period of 18 months for a fixed fee of $180,000.

Advisco is unable to specify the type and number of items that will be delivered to Temple through its services as of January 1, 2010. However, based on past experience, Advisco can make reasonable estimates of the costs that will be incurred to fulfill its contractual obligations and each stage of completion. Advisco estimates that it will cost $144,000 to complete its obligations under this contract.

Revenue recognition when rendering services example

Academic Resource Center

Revenue recognition including construction contracts Page 18

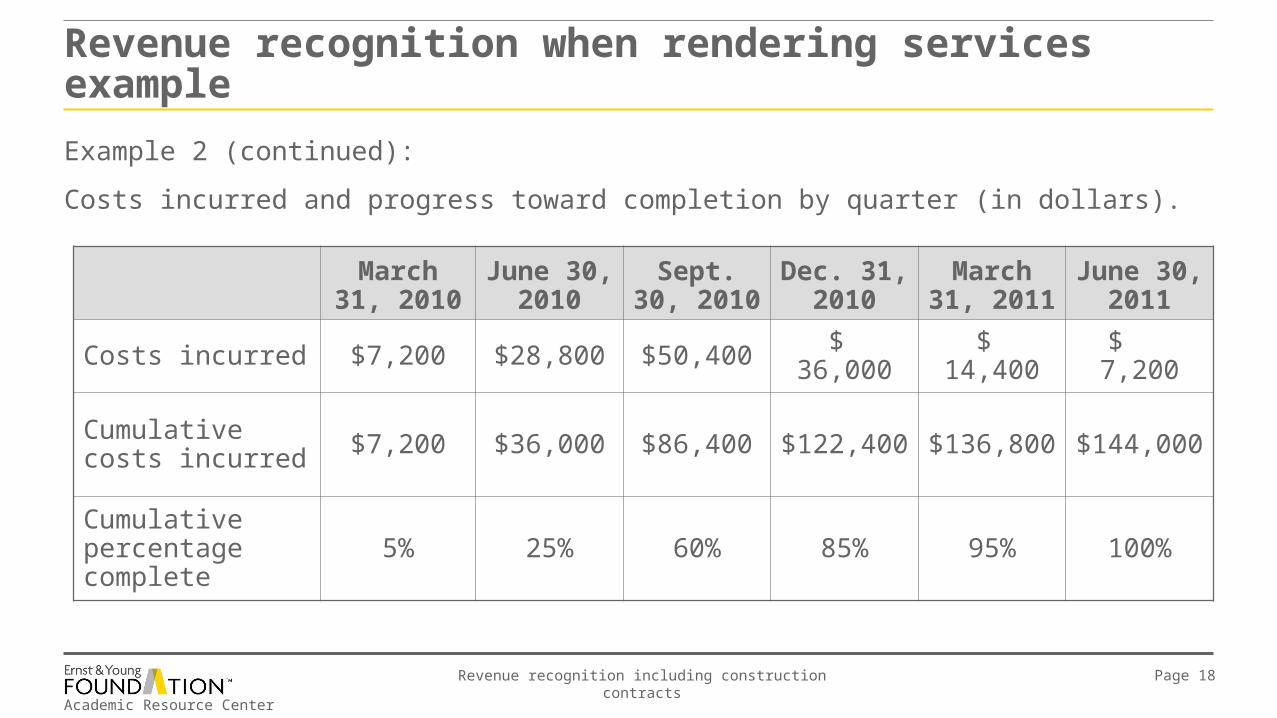

March 31, 2010

June 30, 2010

Sept. 30, 2010

Dec. 31, 2010

March 31, 2011

June 30, 2011

Costs incurred $7,200 $28,800 $50,400 $ 36,000 $ 14,400 $ 7,200

Cumulative costs incurred $7,200 $36,000 $86,400 $122,400 $136,800 $144,000

Cumulative percentage complete

5% 25% 60% 85% 95% 100%

Example 2 (continued):

Costs incurred and progress toward completion by quarter (in dollars).

Revenue recognition when rendering services example

Academic Resource Center

Revenue recognition including construction contracts Page 19

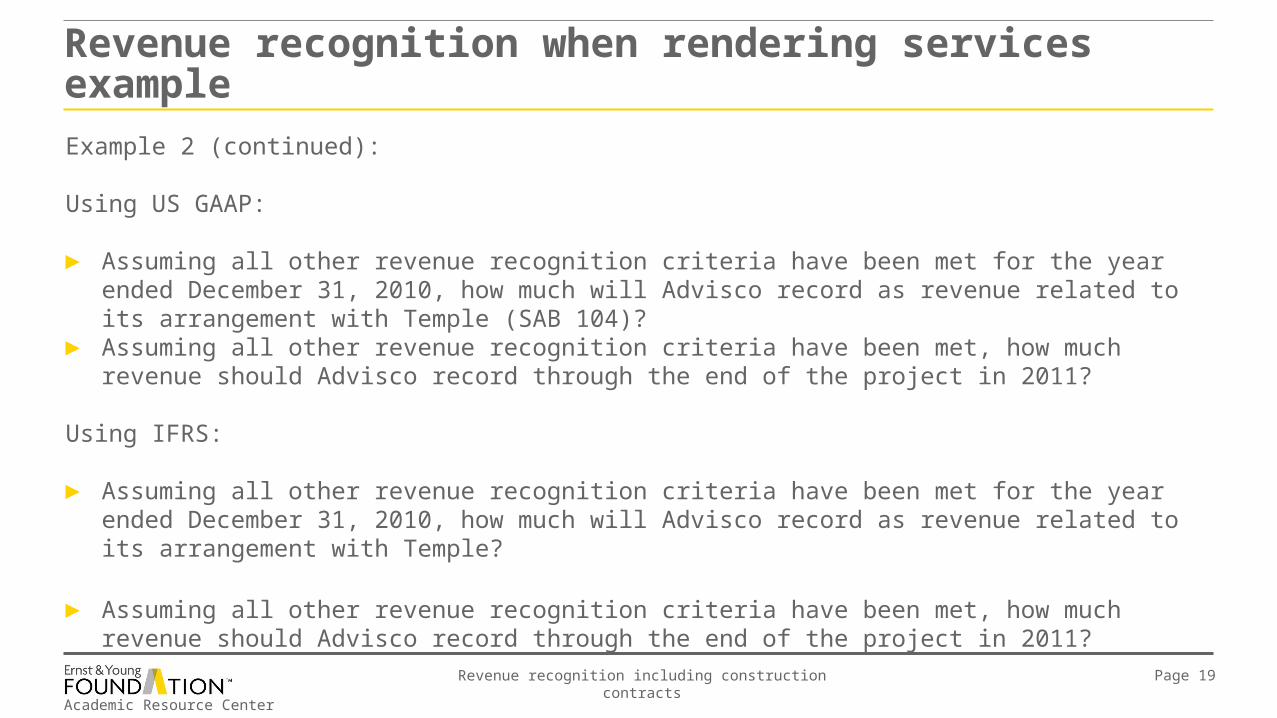

Example 2 (continued):

Using US GAAP:

► Assuming all other revenue recognition criteria have been met for the year ended December 31, 2010, how much will Advisco record as revenue related to its arrangement with Temple (SAB 104)?

► Assuming all other revenue recognition criteria have been met, how much revenue should Advisco record through the end of the project in 2011?

Using IFRS:

► Assuming all other revenue recognition criteria have been met for the year ended December 31, 2010, how much will Advisco record as revenue related to its arrangement with Temple?

► Assuming all other revenue recognition criteria have been met, how much revenue should Advisco record through the end of the project in 2011?

Revenue recognition when rendering services example

Academic Resource Center

Revenue recognition including construction contracts Page 20

Example 2 solution:

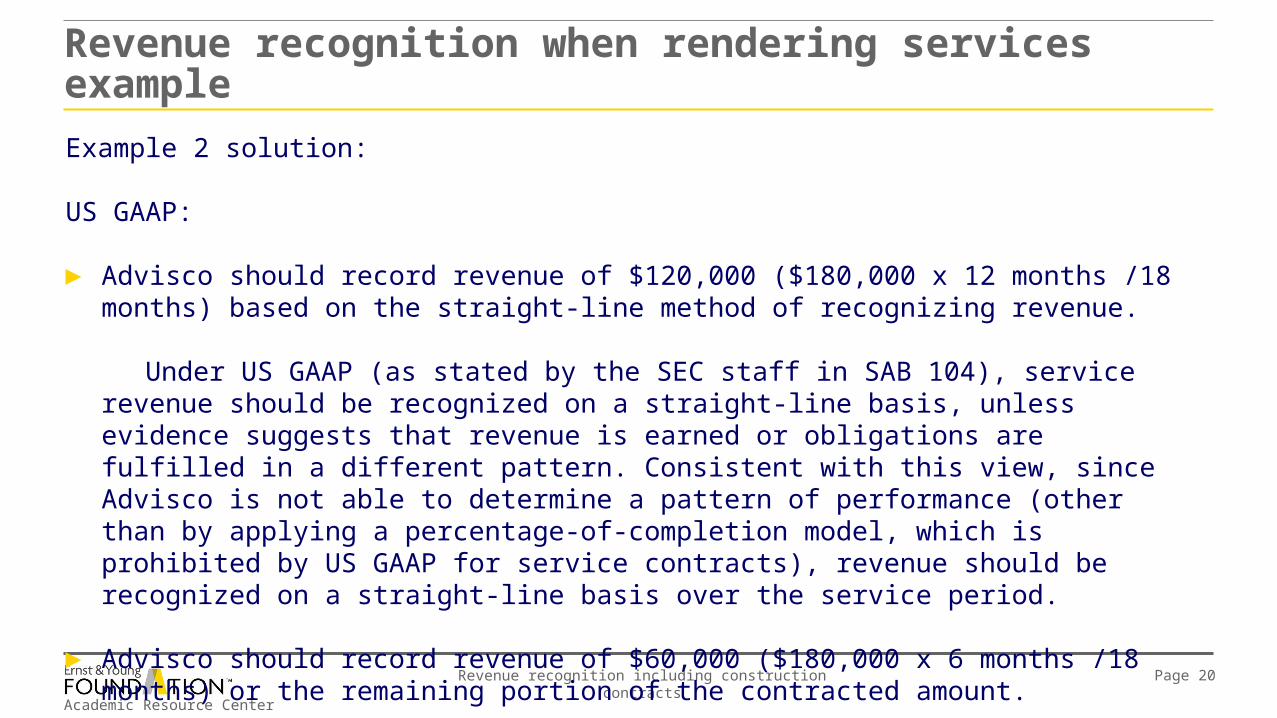

US GAAP:

► Advisco should record revenue of $120,000 ($180,000 x 12 months /18 months) based on the straight-line method of recognizing revenue.

Under US GAAP (as stated by the SEC staff in SAB 104), service revenue should be recognized on a straight-line basis, unless evidence suggests that revenue is earned or obligations are fulfilled in a different pattern. Consistent with this view, since Advisco is not able to determine a pattern of performance (other than by applying a percentage-of-completion model, which is prohibited by US GAAP for service contracts), revenue should be recognized on a straight-line basis over the service period.

► Advisco should record revenue of $60,000 ($180,000 x 6 months /18 months) or the remaining portion of the contracted amount.

Revenue recognition when rendering services example

Academic Resource Center

Revenue recognition including construction contracts Page 21

Example 2 solution (continued)

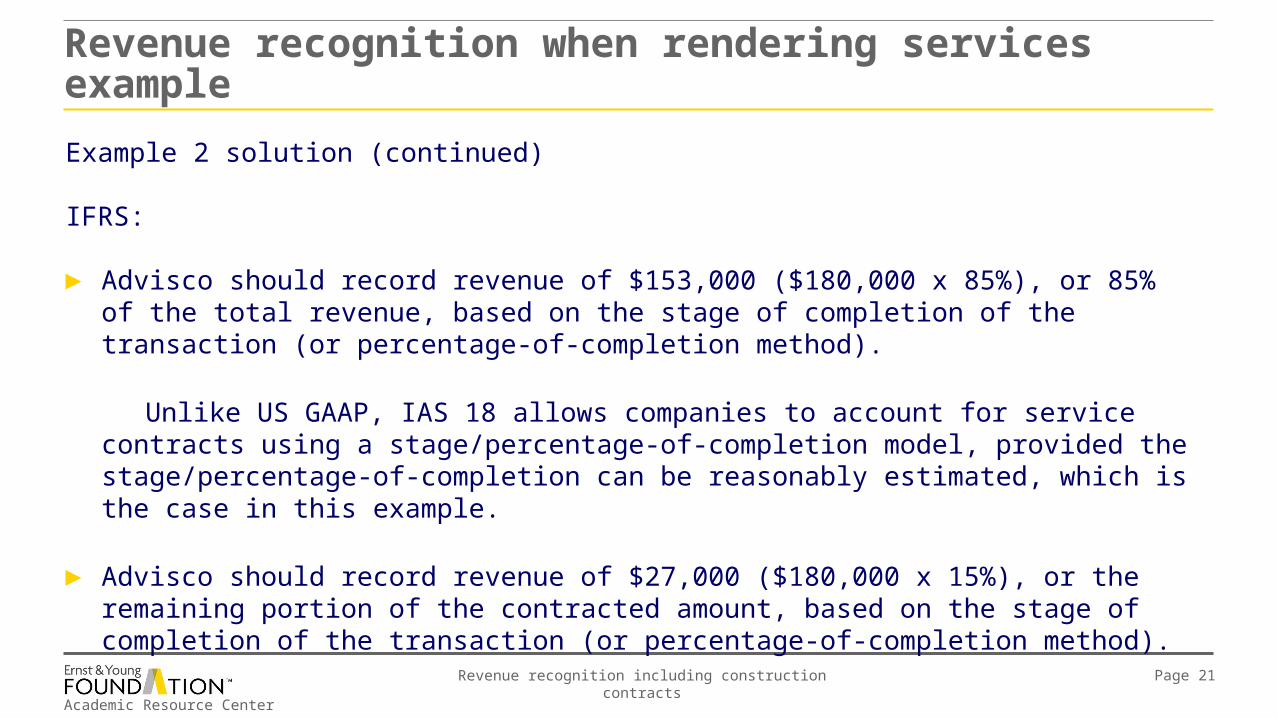

IFRS:

► Advisco should record revenue of $153,000 ($180,000 x 85%), or 85% of the total revenue, based on the stage of completion of the transaction (or percentage-of-completion method).

Unlike US GAAP, IAS 18 allows companies to account for service contracts using a stage/percentage-of-completion model, provided the stage/percentage-of-completion can be reasonably estimated, which is the case in this example.

► Advisco should record revenue of $27,000 ($180,000 x 15%), or the remaining portion of the contracted amount, based on the stage of completion of the transaction (or percentage-of-completion method).

Revenue recognition when rendering services example

Academic Resource Center

Revenue recognition including construction contracts Page 22

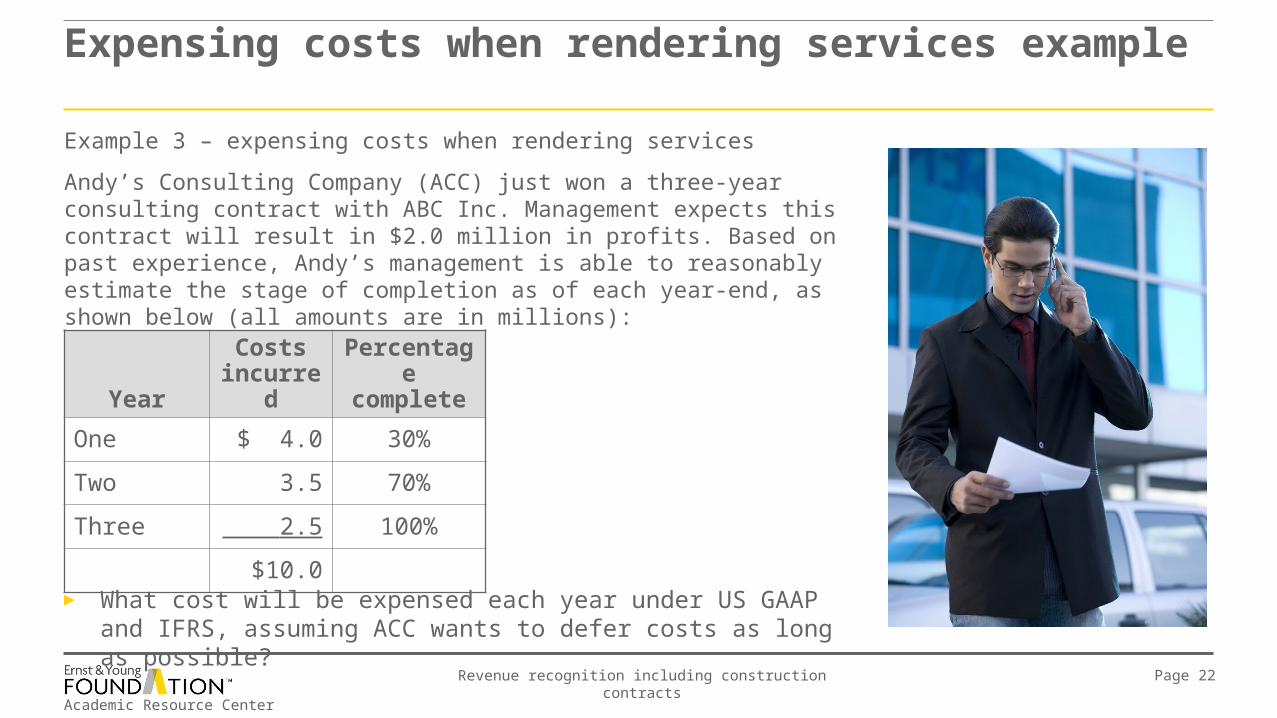

Example 3 – expensing costs when rendering services

Andy’s Consulting Company (ACC) just won a three-year consulting contract with ABC Inc. Management expects this contract will result in $2.0 million in profits. Based on past experience, Andy’s management is able to reasonably estimate the stage of completion as of each year-end, as shown below (all amounts are in millions):

Expensing costs when rendering services example

► What cost will be expensed each year under US GAAP and IFRS, assuming ACC wants to defer costs as long as possible?

YearCosts

incurredPercentage complete

One $ 4.0 30%

Two 3.5 70%

Three 2.5 100%

$10.0

Academic Resource Center

Revenue recognition including construction contracts Page 23

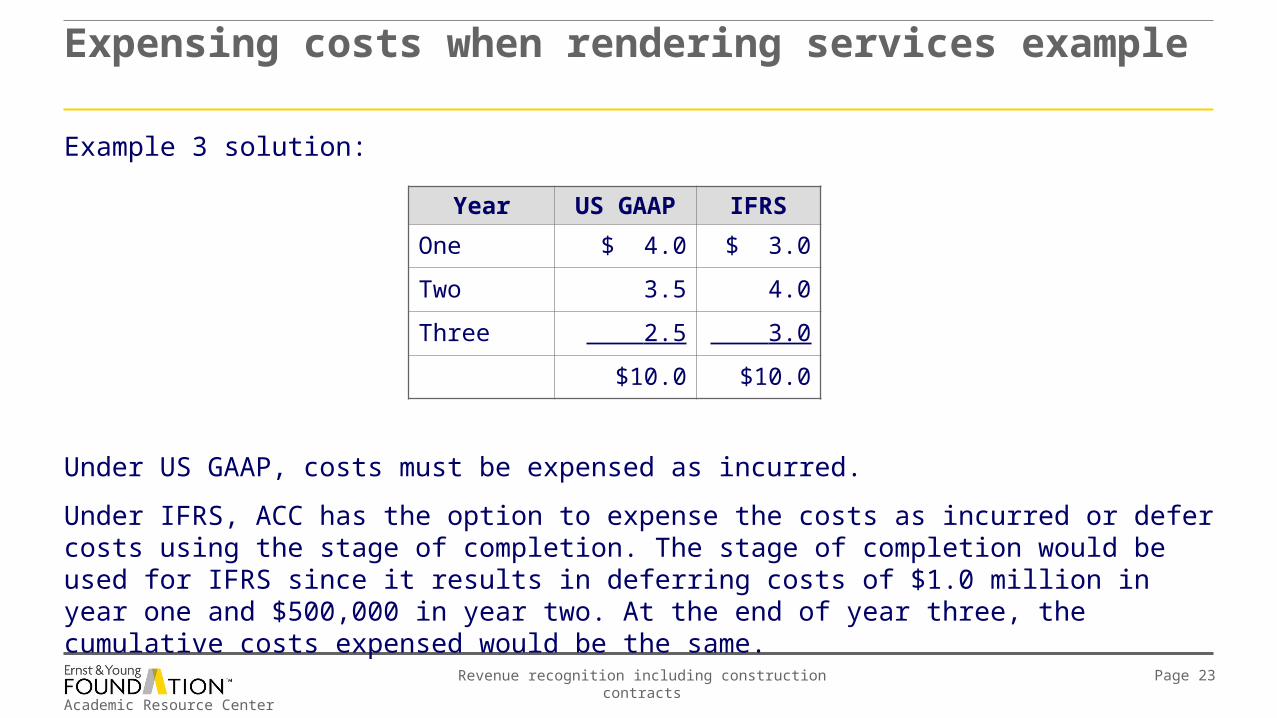

Example 3 solution:

Expensing costs when rendering services example

Year US GAAP IFRS

One $ 4.0 $ 3.0

Two 3.5 4.0

Three 2.5 3.0

$10.0 $10.0

Under US GAAP, costs must be expensed as incurred.

Under IFRS, ACC has the option to expense the costs as incurred or defer costs using the stage of completion. The stage of completion would be used for IFRS since it results in deferring costs of $1.0 million in year one and $500,000 in year two. At the end of year three, the cumulative costs expensed would be the same.

Academic Resource Center

Revenue recognition including construction contracts Page 24

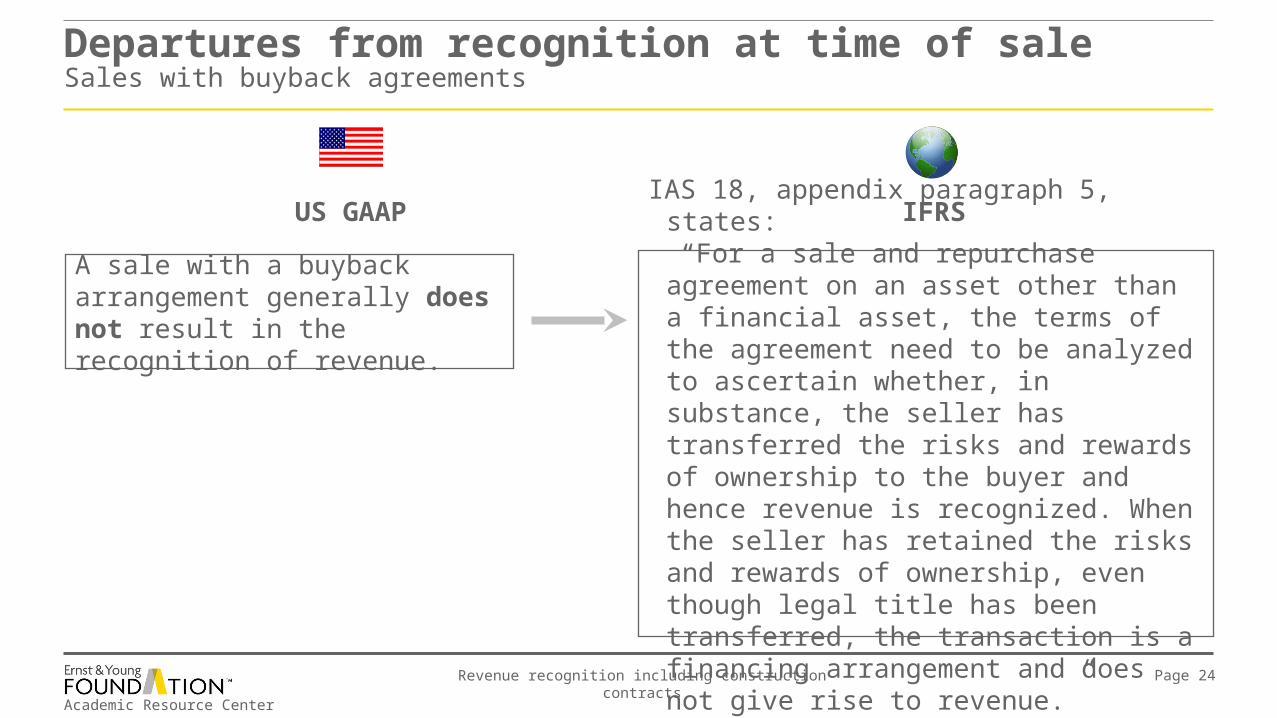

A sale with a buyback arrangement generally does not result in the recognition of revenue.

IAS 18, appendix paragraph 5, states: “For a sale and repurchase agreement on an

asset other than a financial asset, the terms of the agreement need to be analyzed to ascertain whether, in substance, the seller has transferred the risks and rewards of ownership to the buyer and hence revenue is recognized. When the seller has retained the risks and rewards of ownership, even though legal title has been transferred, the transaction is a financing arrangement and does not give rise to revenue.”

IFRSUS GAAP

Departures from recognition at time of saleSales with buyback agreements

Academic Resource Center

Revenue recognition including construction contracts Page 25

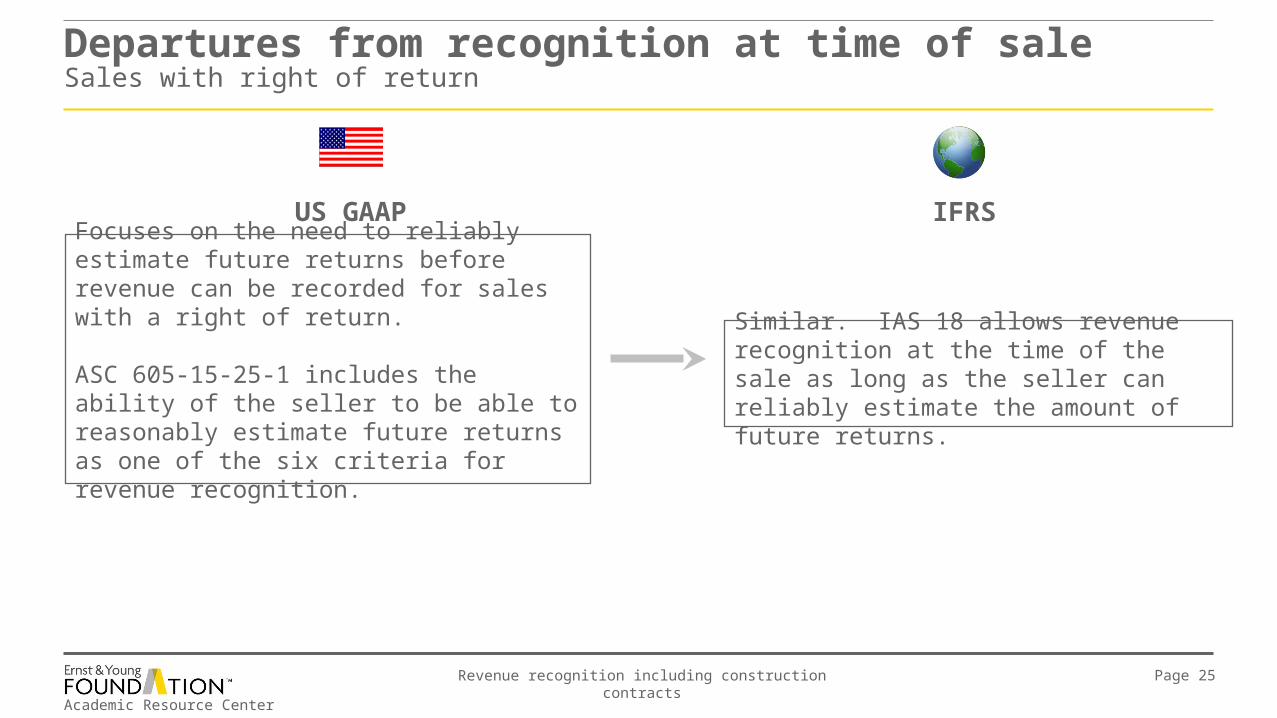

Focuses on the need to reliably estimate future returns before revenue can be recorded for sales with a right of return.

ASC 605-15-25-1 includes the ability of the seller to be able to reasonably estimate future returns as one of the six criteria for revenue recognition.

Similar. IAS 18 allows revenue recognition at the time of the sale as long as the seller can reliably estimate the amount of future returns.

IFRSUS GAAP

Departures from recognition at time of saleSales with right of return

Academic Resource Center

Revenue recognition including construction contracts Page 26

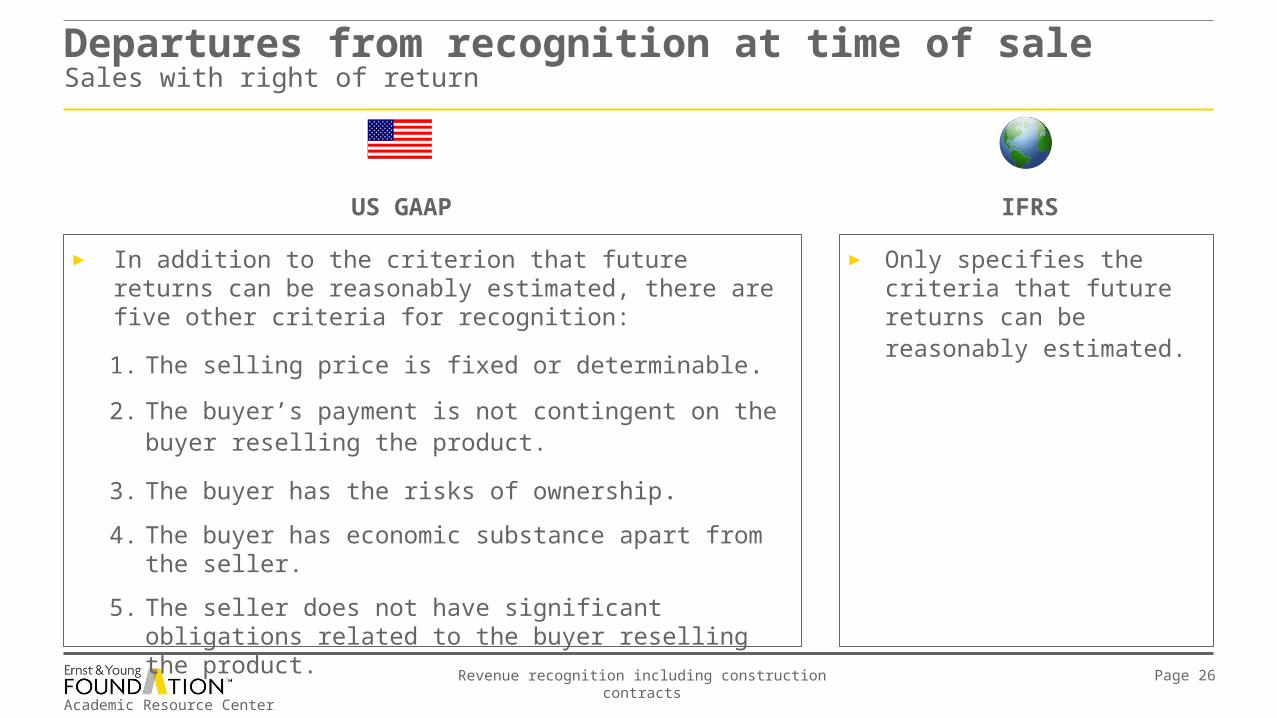

► Only specifies the criteria that future returns can be reasonably estimated.

► In addition to the criterion that future returns can be reasonably estimated, there are five other criteria for recognition:

1. The selling price is fixed or determinable.

2. The buyer’s payment is not contingent on the buyer reselling the product.

3. The buyer has the risks of ownership.

4. The buyer has economic substance apart from the seller.

5. The seller does not have significant obligations related to the buyer reselling the product.

Departures from recognition at time of saleSales with right of return

US GAAP IFRS

Academic Resource Center

Revenue recognition including construction contracts Page 27

Example 4 – revenue recognition when a right of return exists

Identify for which of the following situations, if any, it would be inappropriate to recognize revenue under US GAAP. Also, identify for which situations it would be inappropriate to recognize revenue under IFRS. Provide an explanation of your answers.

Revenue recognition when right of return exists example

► Company A introduced a new product that had sales of $1.0 million in the first month. Total returns in the first month were $200,000.

► Company B wanted to sell its product in Mexico. It contacted a local businesswoman in Mexico City and established a joint venture. Company B provided the initial financing and the businesswoman agreed to broker the product to local companies. In the first month, Company B sold $2.0 million of product to the joint venture to cover anticipated sales. Assume that Company B properly concluded that this is not a consignment sale. Company B has extensive experience selling its product and believes it can reliably estimate future returns.

► Company C has a long history of selling small motors to Company D. Company D mounts these motors on its lawn mowers and sells the completed lawn mowers to hardware stores. When Company D receives payment from the hardware stores it pays Company C for the motors. Company D has the right to return any unused motors at the end of the year. Historically, these returns have averaged 2% of sales.

Academic Resource Center

Revenue recognition including construction contracts Page 28

Example 4 solution: ► Company A — Because this is a new product, it is unlikely Company A could reliably estimate future

returns. Therefore revenue should not be recorded currently under either US GAAP or IFRS.

► Company B — Under US GAAP, the requirement that the buyer has economic substance separate from the seller does not appear to have been met so no revenue should be currently recorded. It is possible that under IFRS the conclusion might be to record the revenue since Company B can reliably estimate returns. The question that would need to be addressed is whether sales returns in Mexico will follow the same pattern as historical experience.

► Company C — It appears the buyer’s payment is dependent on the buyer selling the lawn mower. Therefore under US GAAP it would appear that revenue should not be currently recognized. Under IFRS at first glance it would appear that the revenue would be recorded because it is probable that the economic benefits from the sale of the motors will flow to the seller and the returns can be reliably determined. One of the specific criteria for revenue recognition under IAS 18 is that Company C has transferred to the buyer the significant risks and rewards of ownership of the goods. However since the payment for the motors is only made if Company D is able to sell its lawn mowers, it appears significant risk of ownership has been retained by Company C and, therefore, revenue should not be recognized.

Revenue recognition when right of return exists example

Academic Resource Center

Revenue recognition including construction contracts Page 29

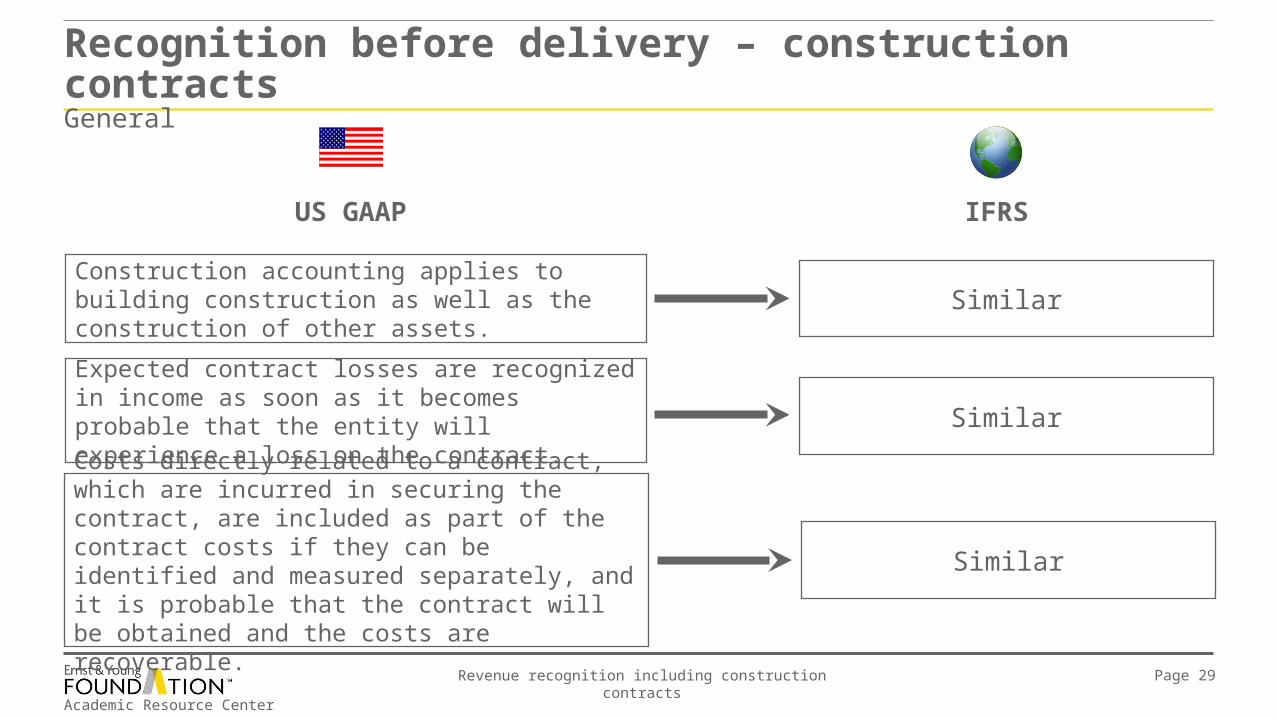

Recognition before delivery – construction contractsGeneral

Construction accounting applies to building construction as well as the construction of other assets.

Expected contract losses are recognized in income as soon as it becomes probable that the entity will experience a loss on the contract.

Similar

Similar

IFRSUS GAAP

Costs directly related to a contract, which are incurred in securing the contract, are included as part of the contract costs if they can be identified and measured separately, and it is probable that the contract will be obtained and the costs are recoverable.

Similar

Academic Resource Center

Revenue recognition including construction contracts Page 30

IFRS

► Contracts are classified as fixed-price or cost-plus contracts.

► Time-and-materials-type contracts would most likely be classified as cost-plus contracts.

► Units-of-production contracts would most likely be classified as fixed-price contracts.

► Contracts are segmented if certain criteria are met. These criteria are different from the criteria under US GAAP.

US GAAP

► Contracts can be classified as fixed-price, cost-plus, time-and-materials and units-of-production contracts.

► Contracts may be segmented if certain criteria are met, but it is not required.

Recognition before delivery – construction contractsGeneral

Academic Resource Center

Revenue recognition including construction contracts Page 31

Recognition before delivery – construction contractsPercentage-of-completion method

Both input and output methods are acceptable for determining the stage of completion of a given project.

Similar

IFRSUS GAAP

Academic Resource Center

Revenue recognition including construction contracts Page 32

IFRSUS GAAP

► The criteria for using the percentage-of-completion method (ASC 605-35-25-56 and 57) are as follows:

► The entity must have the “ability to make reasonably dependable estimates.” These estimates are defined as relating to “estimates of the extent of progress toward completion, contract revenues, and contract costs.”

► “Contracts executed by the parties normally include provisions that clearly specify the enforceable rights regarding goods or services to be provided and received by the parties, the consideration to be exchanged, and the manner and terms of settlement.”

Recognition before delivery – construction contractsPercentage-of-completion method

Academic Resource Center

Revenue recognition including construction contracts Page 33

IFRS

► Per IAS 11.22, the percentage-of-completion method can be used “when the outcome of the construction contract can be estimated reliably.” If the criteria for using the percentage-of-completion method are not met, then the entity recognizes revenue to the extent that costs are incurred (as long as the costs are likely to be recovered) and recognizes costs as incurred. The criteria of reliable estimation are defined differently, depending on the type of contract.

US GAAP

► Criteria, continued:

► “The buyer can be expected to satisfy all obligations under the contract.

► The contractor can be expected to perform all contractual obligations.”

Recognition before delivery – construction contractsPercentage-of-completion method

Academic Resource Center

Revenue recognition including construction contracts Page 34

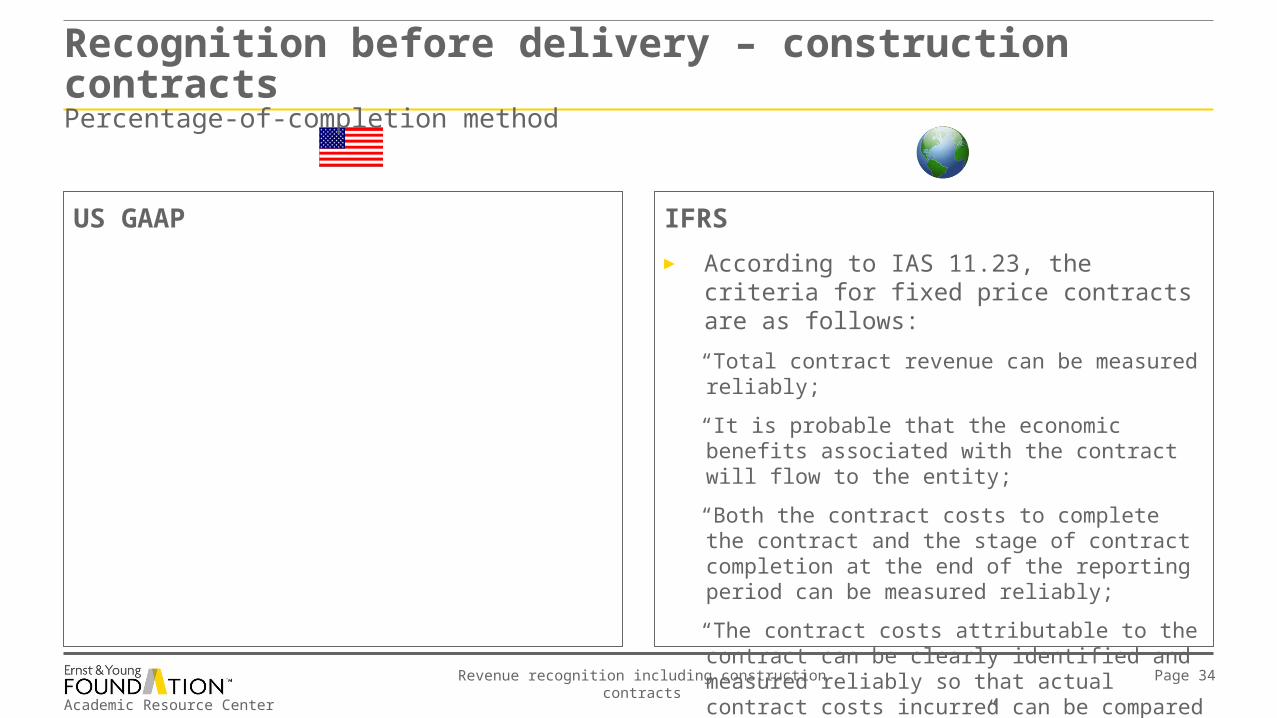

IFRS

► According to IAS 11.23, the criteria for fixed price contracts are as follows:

“Total contract revenue can be measured reliably;

“It is probable that the economic benefits associated with the contract will flow to the entity;

“Both the contract costs to complete the contract and the stage of contract completion at the end of the reporting period can be measured reliably;

“The contract costs attributable to the contract can be clearly identified and measured reliably so that actual contract costs incurred can be compared with prior estimates.”

US GAAP

Recognition before delivery – construction contractsPercentage-of-completion method

Academic Resource Center

Revenue recognition including construction contracts Page 35

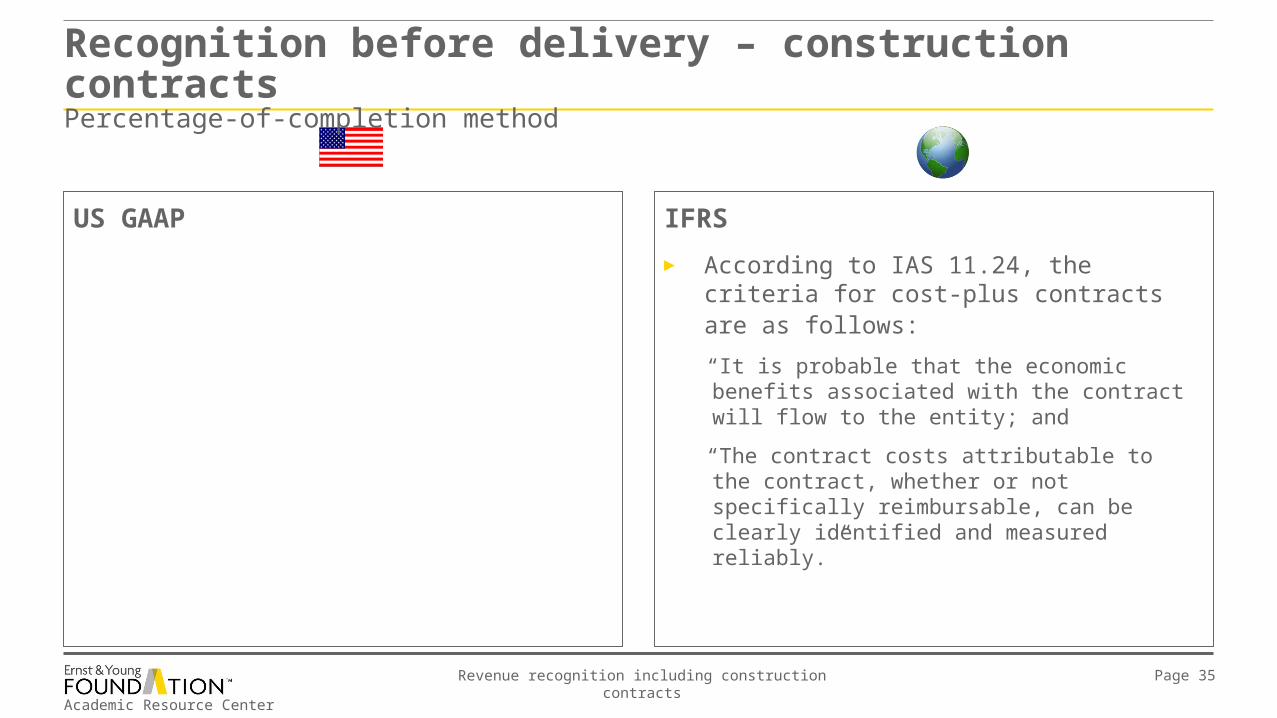

IFRS

► According to IAS 11.24, the criteria for cost-plus contracts are as follows:

“It is probable that the economic benefits associated with the contract will flow to the entity; and

“The contract costs attributable to the contract, whether or not specifically reimbursable, can be clearly identified and measured reliably.”

US GAAP

Recognition before delivery – construction contractsPercentage-of-completion method

Academic Resource Center

Revenue recognition including construction contracts Page 36

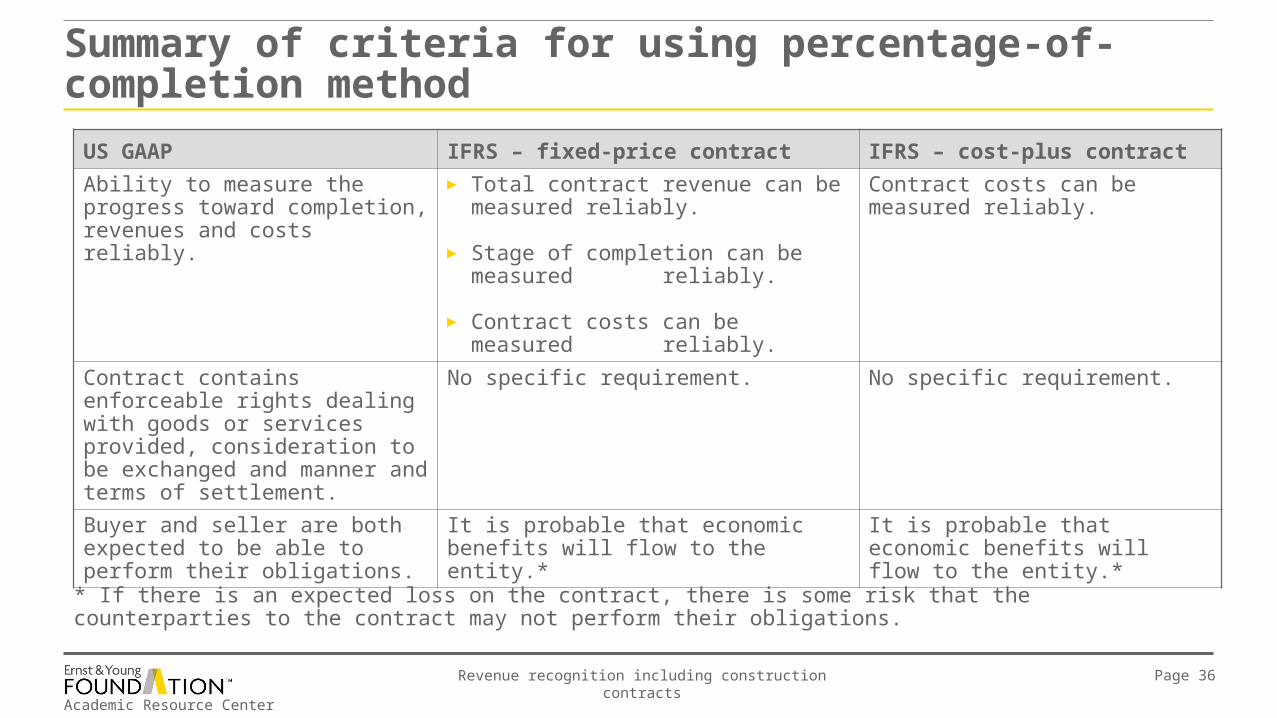

Summary of criteria for using percentage-of-completion method

US GAAP IFRS – fixed-price contract IFRS – cost-plus contract

Ability to measure the progress toward completion, revenues and costs reliably.

► Total contract revenue can be measured reliably.

► Stage of completion can be measured reliably.

► Contract costs can be measured reliably.

Contract costs can be measured reliably.

Contract contains enforceable rights dealing with goods or services provided, consideration to be exchanged and manner and terms of settlement.

No specific requirement. No specific requirement.

Buyer and seller are both expected to be able to perform their obligations.

It is probable that economic benefits will flow to the entity.*

It is probable that economic benefits will flow to the entity.*

* If there is an expected loss on the contract, there is some risk that the counterparties to the contract may not perform their obligations.

Academic Resource Center

Revenue recognition including construction contracts Page 37

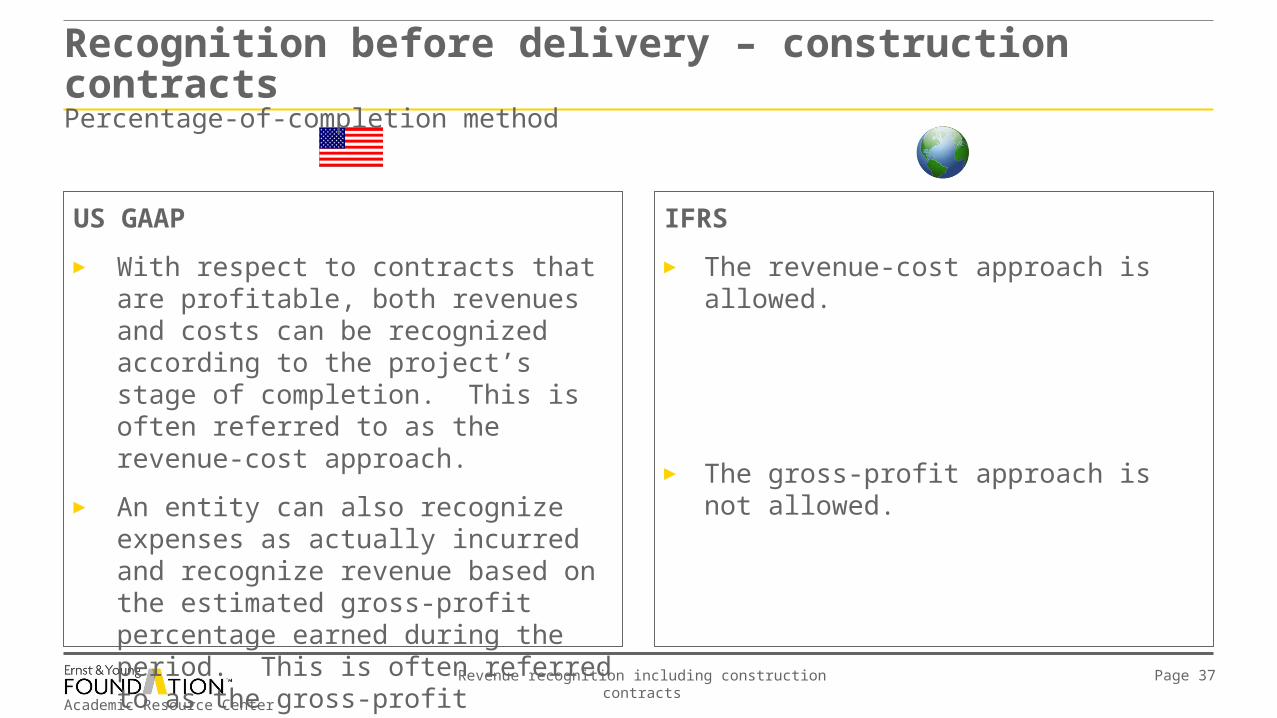

IFRS

► The revenue-cost approach is allowed.

► The gross-profit approach is not allowed.

US GAAP

► With respect to contracts that are profitable, both revenues and costs can be recognized according to the project’s stage of completion. This is often referred to as the revenue-cost approach.

► An entity can also recognize expenses as actually incurred and recognize revenue based on the estimated gross-profit percentage earned during the period. This is often referred to as the gross-profit approach.

Recognition before delivery – construction contractsPercentage-of-completion method

Academic Resource Center

Revenue recognition including construction contracts Page 38

Revenue-cost and gross-profit approach example

Example 5 – revenue-cost and gross-profit approach

A company enters into a contract with expected revenues of $5.6 million and expected costs of $4.9 million. The contract is 30% complete in the first year, 65% complete in the second year and 100% complete in the third year. The costs incurred for the three years are $1.4 million, $1.65 million and $1.85 million, respectively.

► Using the revenue-cost approach, compute the revenues and costs that will be recognized each year under US GAAP and IFRS.

► Using the gross-profit approach, compute the revenues and costs that will be recognized each year under US GAAP and IFRS.

Academic Resource Center

Revenue recognition including construction contracts Page 39

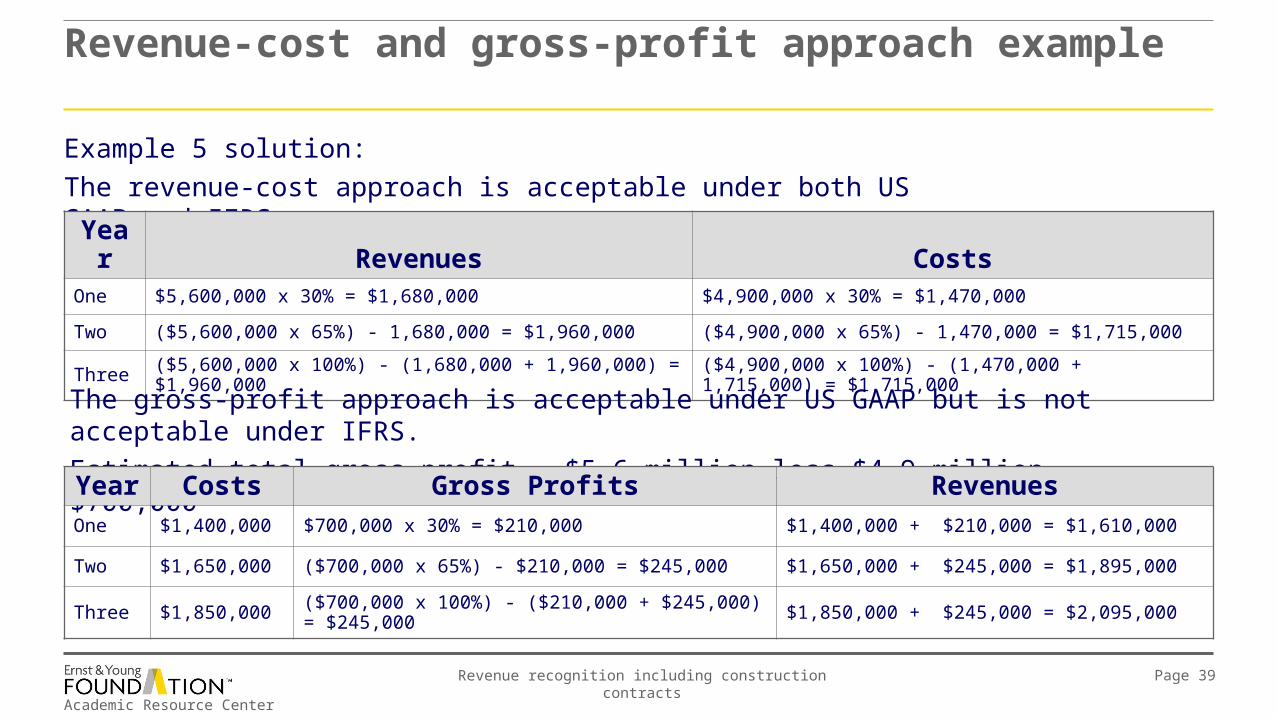

Revenue-cost and gross-profit approach example

Example 5 solution:

The revenue-cost approach is acceptable under both US GAAP and IFRS.

Year Revenues CostsOne $5,600,000 x 30% = $1,680,000 $4,900,000 x 30% = $1,470,000

Two ($5,600,000 x 65%) - 1,680,000 = $1,960,000 ($4,900,000 x 65%) - 1,470,000 = $1,715,000

Three ($5,600,000 x 100%) - (1,680,000 + 1,960,000) = $1,960,000 ($4,900,000 x 100%) - (1,470,000 + 1,715,000) = $1,715,000

The gross-profit approach is acceptable under US GAAP but is not acceptable under IFRS.

Estimated total gross profit = $5.6 million less $4.9 million = $700,000

Year Costs Gross Profits RevenuesOne $1,400,000 $700,000 x 30% = $210,000 $1,400,000 + $210,000 = $1,610,000

Two $1,650,000 ($700,000 x 65%) - $210,000 = $245,000 $1,650,000 + $245,000 = $1,895,000

Three $1,850,000 ($700,000 x 100%) - ($210,000 + $245,000) = $245,000 $1,850,000 + $245,000 = $2,095,000

Academic Resource Center

Revenue recognition including construction contracts Page 40

IFRS

► The completed-contract method is not permitted. If the criteria for using the percentage-of-completion method are not met, then the entity recognizes revenue to the extent that costs are incurred (as long as the costs are likely to be recovered) and recognizes costs as incurred.

US GAAP

► If the percentage-of-completion criteria aren’t met, then the completed-contract method is used.

► The AICPA Accounting Trends and Techniques for 2010 reported that of 500 companies sampled for 2009, 124 had long-term construction contracts. Of these 124 companies, 20 used completed-contract accounting.

Recognition before delivery – construction contractsCompleted-contract method

Academic Resource Center

Revenue recognition including construction contracts Page 41

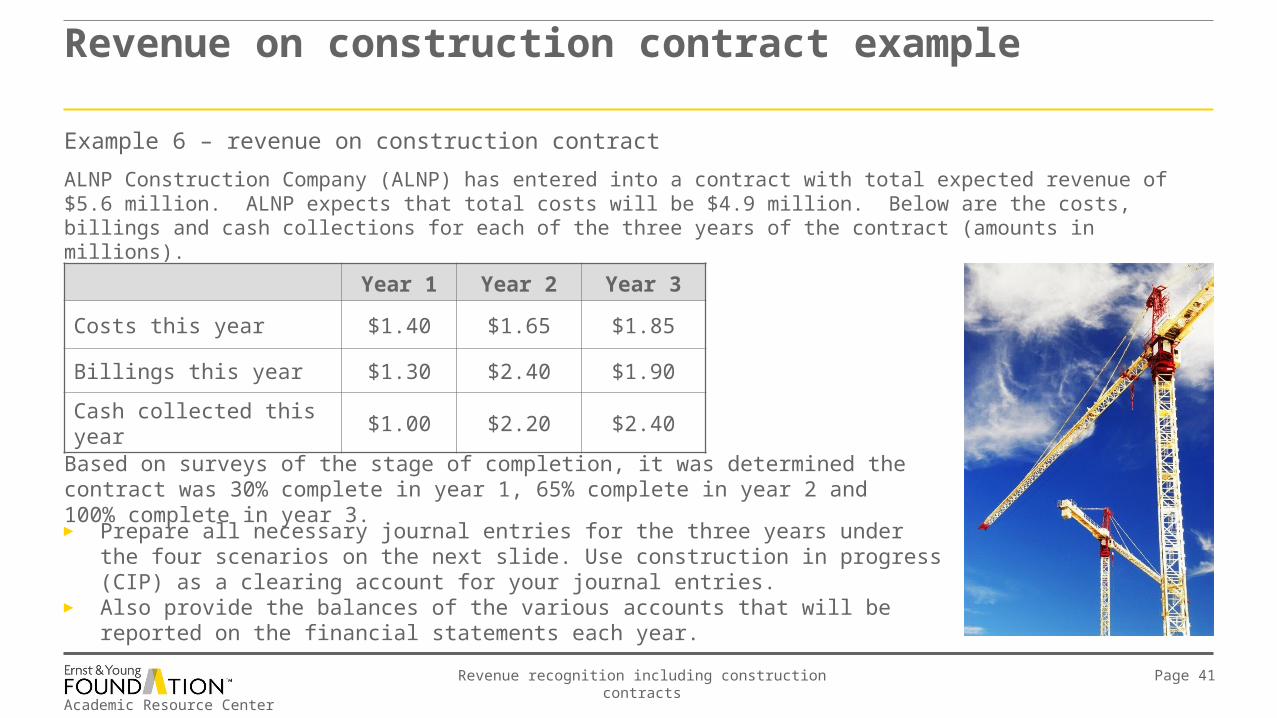

Example 6 – revenue on construction contract

ALNP Construction Company (ALNP) has entered into a contract with total expected revenue of $5.6 million. ALNP expects that total costs will be $4.9 million. Below are the costs, billings and cash collections for each of the three years of the contract (amounts in millions).

► Prepare all necessary journal entries for the three years under the four scenarios on the next slide. Use construction in progress (CIP) as a clearing account for your journal entries.

► Also provide the balances of the various accounts that will be reported on the financial statements each year.

Year 1 Year 2 Year 3

Costs this year $1.40 $1.65 $1.85

Billings this year $1.30 $2.40 $1.90

Cash collected this year $1.00 $2.20 $2.40

Revenue on construction contract example

Based on surveys of the stage of completion, it was determined the contract was 30% complete in year 1, 65% complete in year 2 and 100% complete in year 3.

Academic Resource Center

Revenue recognition including construction contracts Page 42

Revenue on construction contract example

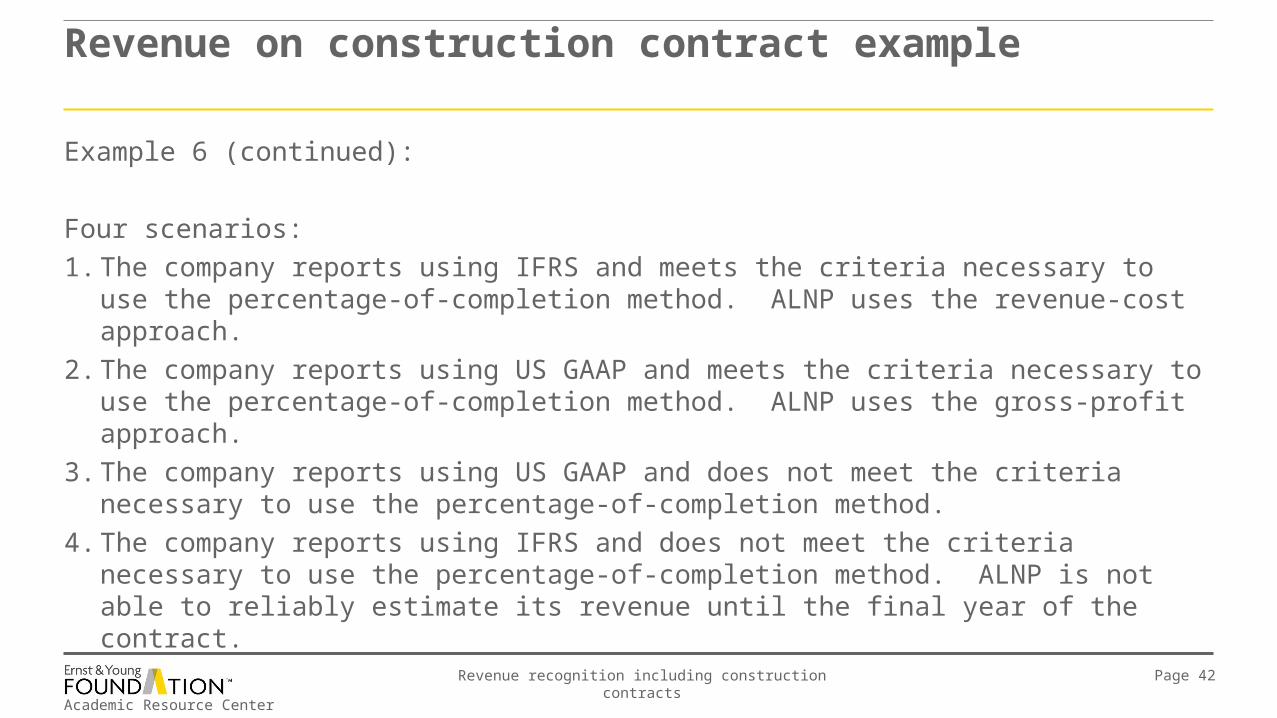

Example 6 (continued):

Four scenarios:

1. The company reports using IFRS and meets the criteria necessary to use the percentage-of-completion method. ALNP uses the revenue-cost approach.

2. The company reports using US GAAP and meets the criteria necessary to use the percentage-of-completion method. ALNP uses the gross-profit approach.

3. The company reports using US GAAP and does not meet the criteria necessary to use the percentage-of-completion method.

4. The company reports using IFRS and does not meet the criteria necessary to use the percentage-of-completion method. ALNP is not able to reliably estimate its revenue until the final year of the contract.

Academic Resource Center

Revenue recognition including construction contracts Page 43

Revenue on construction contract example

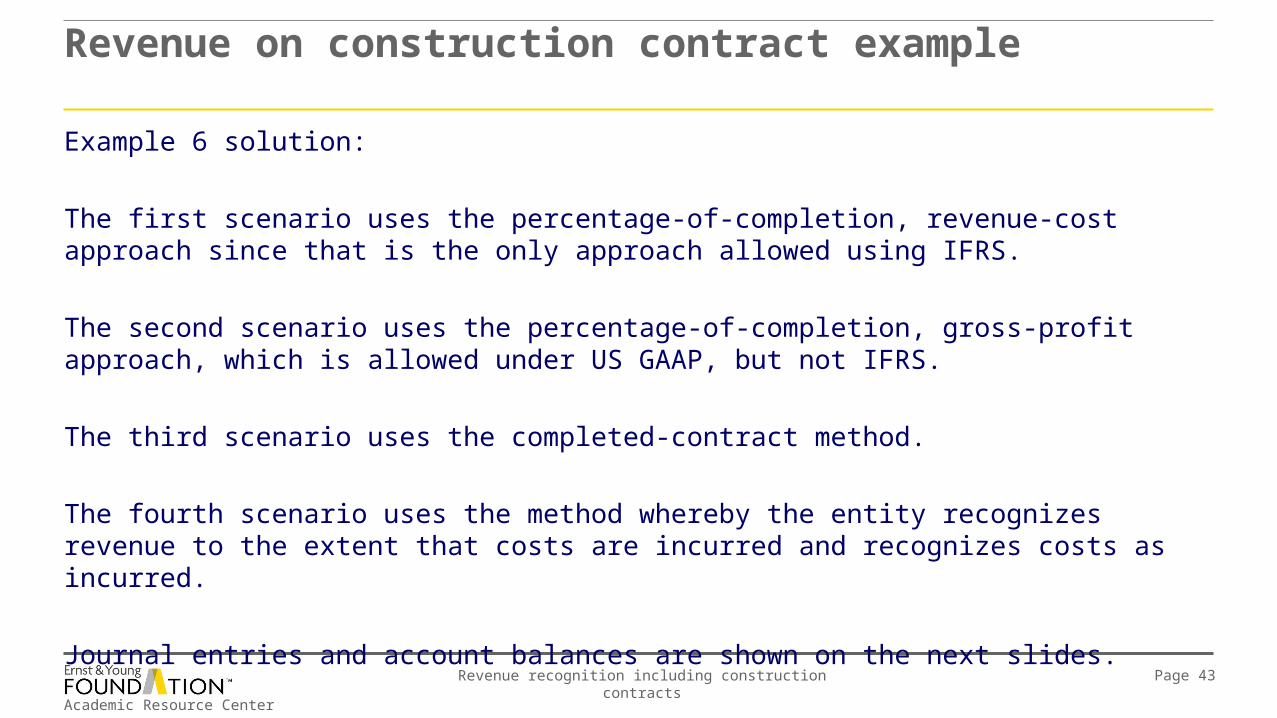

Example 6 solution:

The first scenario uses the percentage-of-completion, revenue-cost approach since that is the only approach allowed using IFRS.

The second scenario uses the percentage-of-completion, gross-profit approach, which is allowed under US GAAP, but not IFRS.

The third scenario uses the completed-contract method.

The fourth scenario uses the method whereby the entity recognizes revenue to the extent that costs are incurred and recognizes costs as incurred.

Journal entries and account balances are shown on the next slides.

Academic Resource Center

Revenue recognition including construction contracts Page 44

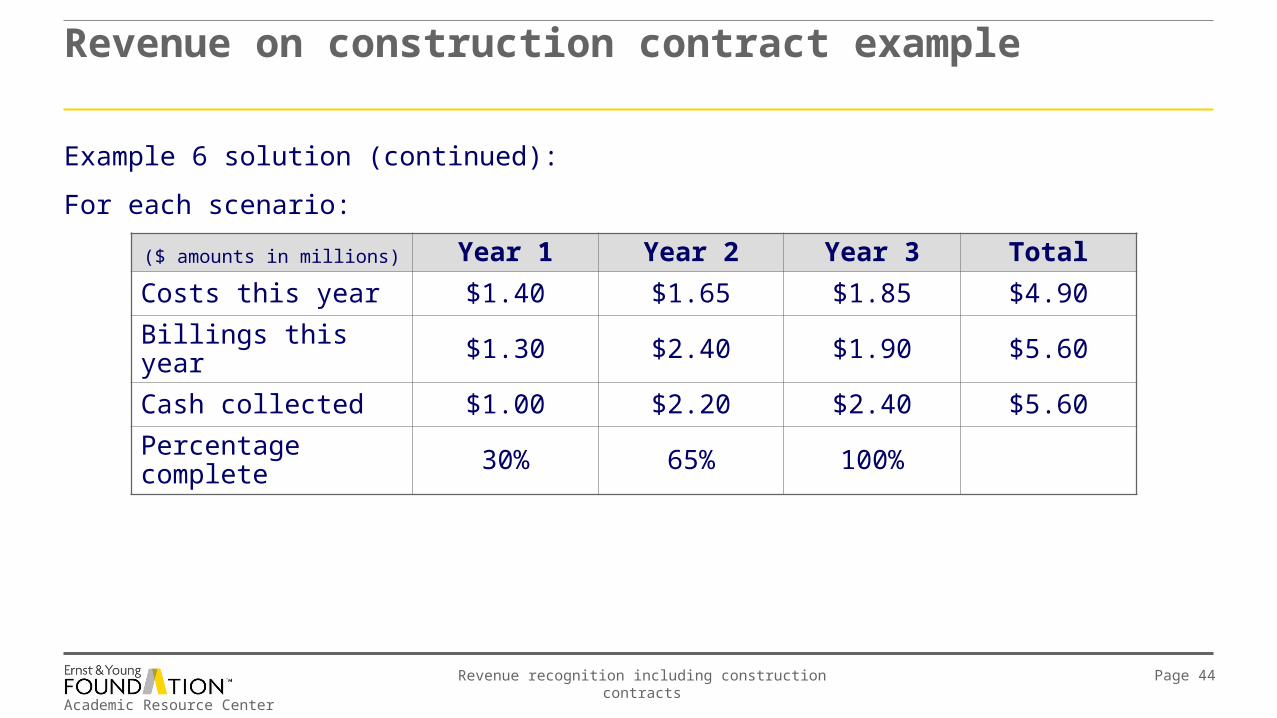

($ amounts in millions) Year 1 Year 2 Year 3 Total

Costs this year $1.40 $1.65 $1.85 $4.90

Billings this year $1.30 $2.40 $1.90 $5.60

Cash collected $1.00 $2.20 $2.40 $5.60

Percentage complete 30% 65% 100%

Revenue on construction contract example

Example 6 solution (continued):

For each scenario:

Academic Resource Center

Revenue recognition including construction contracts Page 45

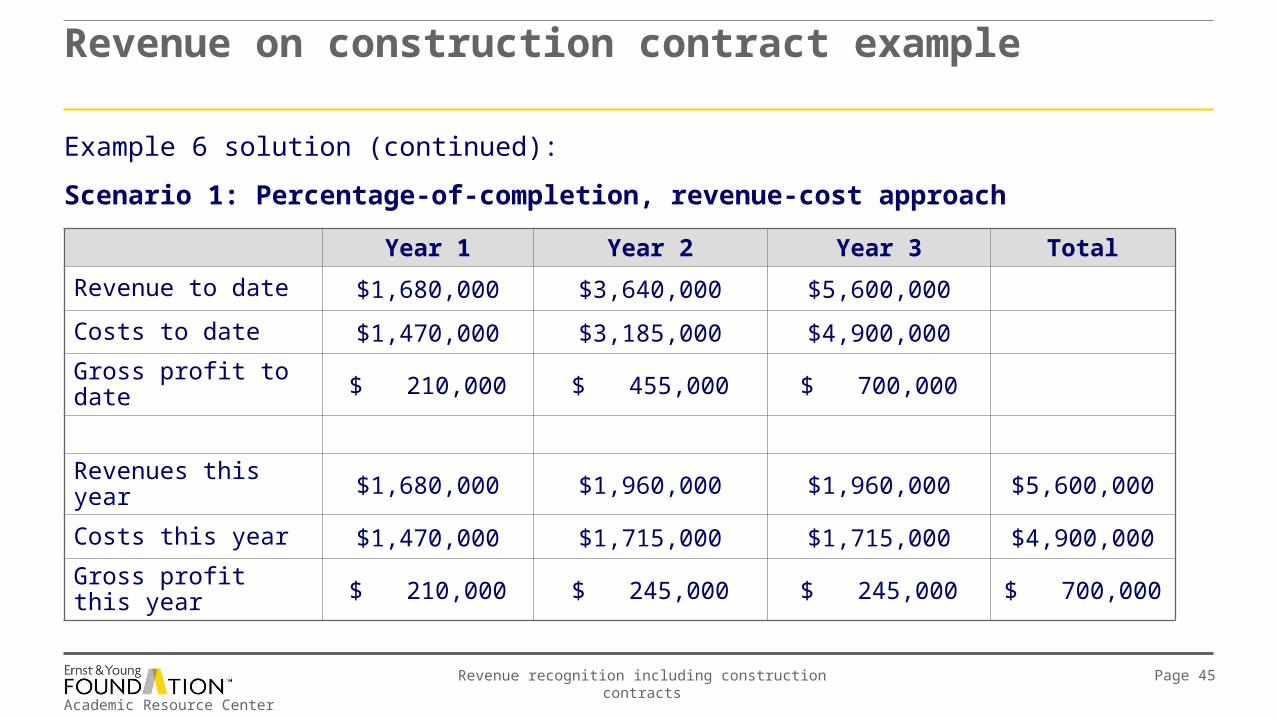

Example 6 solution (continued):

Scenario 1: Percentage-of-completion, revenue-cost approach

Year 1 Year 2 Year 3 Total

Revenue to date $1,680,000 $3,640,000 $5,600,000

Costs to date $1,470,000 $3,185,000 $4,900,000

Gross profit to date $ 210,000 $ 455,000 $ 700,000

Revenues this year $1,680,000 $1,960,000 $1,960,000 $5,600,000

Costs this year $1,470,000 $1,715,000 $1,715,000 $4,900,000

Gross profit this year $ 210,000 $ 245,000 $ 245,000 $ 700,000

Revenue on construction contract example

Academic Resource Center

Revenue recognition including construction contracts Page 46

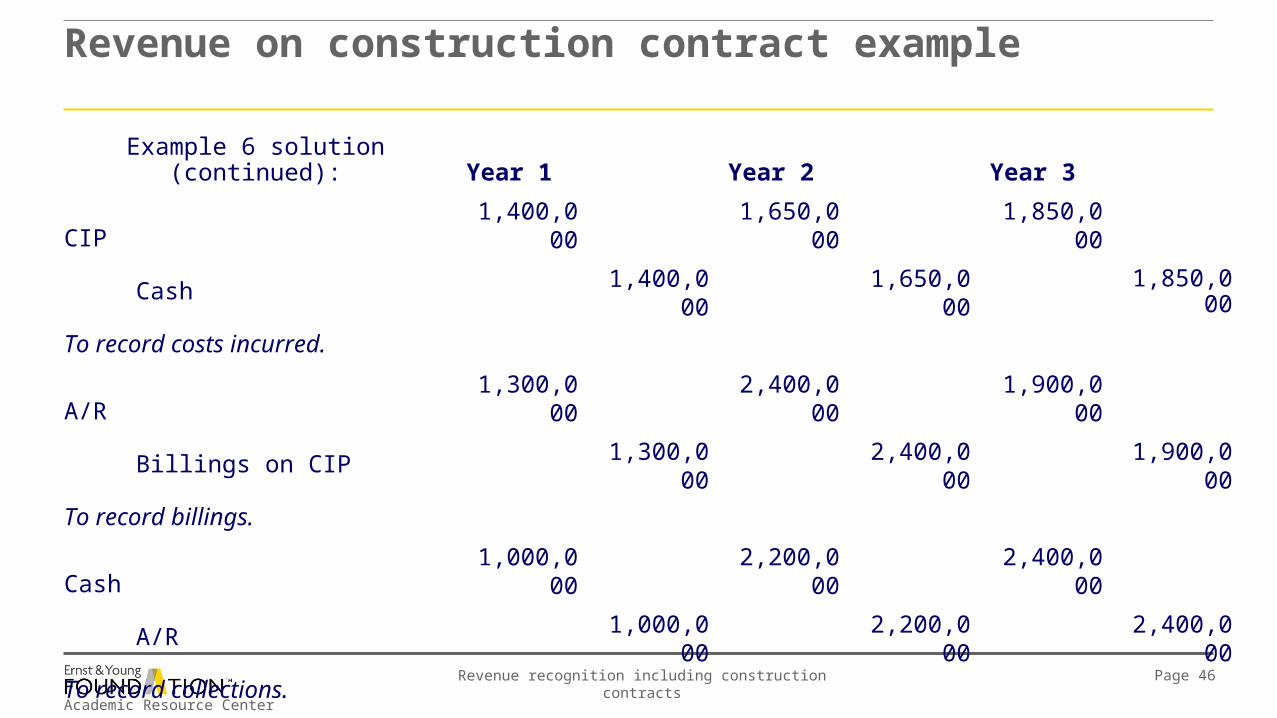

Example 6 solution (continued): Year 1 Year 2 Year 3

CIP 1,400,000 1,650,000 1,850,000

Cash 1,400,000 1,650,000 1,850,000

To record costs incurred.

A/R 1,300,000 2,400,000 1,900,000

Billings on CIP 1,300,000 2,400,000 1,900,000

To record billings.

Cash 1,000,000 2,200,000 2,400,000

A/R 1,000,000 2,200,000 2,400,000

To record collections.

Note: All amounts are in dollars.

Revenue on construction contract example

Academic Resource Center

Revenue recognition including construction contracts Page 47

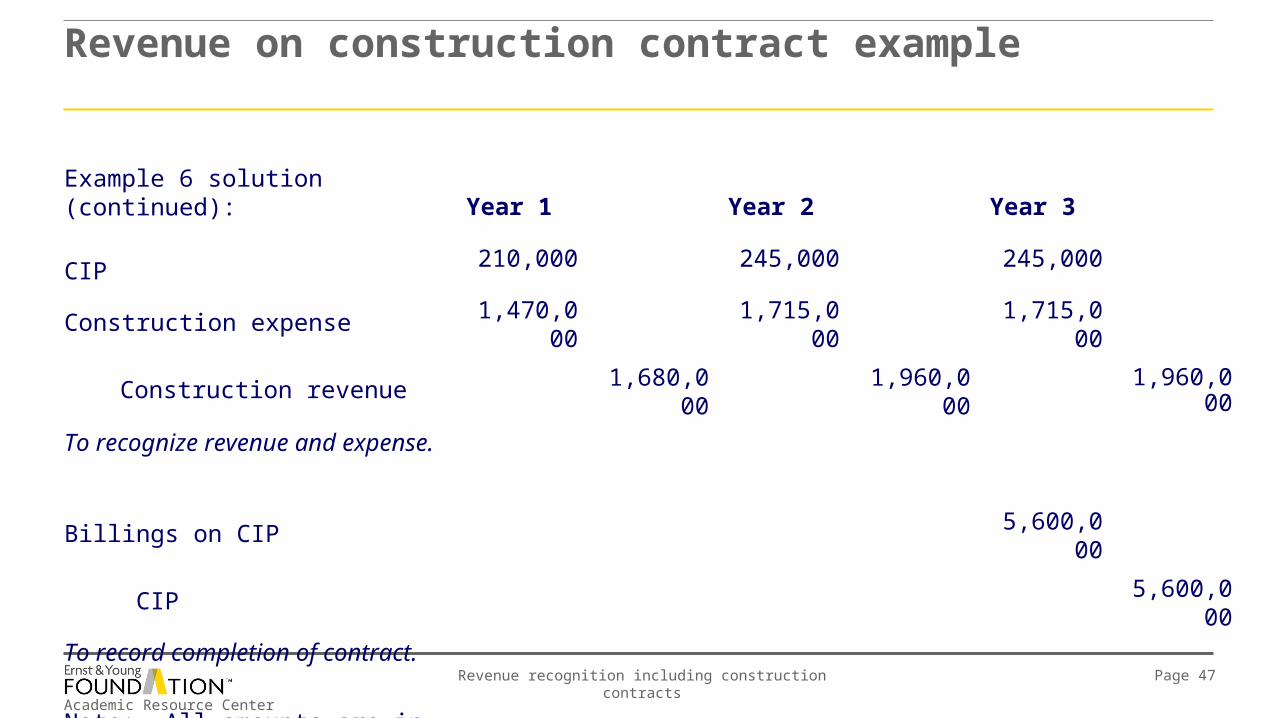

Example 6 solution (continued): Year 1 Year 2 Year 3

CIP 210,000 245,000 245,000

Construction expense 1,470,000 1,715,000 1,715,000

Construction revenue 1,680,000 1,960,000 1,960,000

To recognize revenue and expense.

Billings on CIP 5,600,000

CIP 5,600,000

To record completion of contract.

Note: All amounts are in dollars.

Revenue on construction contract example

Academic Resource Center

Revenue recognition including construction contracts Page 48

Balance sheet account balances at December 31

Year 1 Year 2 Year 3

Assets:

Cash $ (400,000) $ 150,000 $700,000

A/R 300,000 500,000

CIP 1,610,000 3,050,000

Billings on CIP (1,300,000) (3,700,000)

Costs and recognized profit in excess of billings 310,000

Liabilities:

Billing in excess of costs and recognized profits 195,000

Equity:

Retained earnings (ignoring effects of taxes) 210,000 455,000 700,000

Revenue on construction contract example

Example 6 solution (continued):

Academic Resource Center

Revenue recognition including construction contracts Page 49

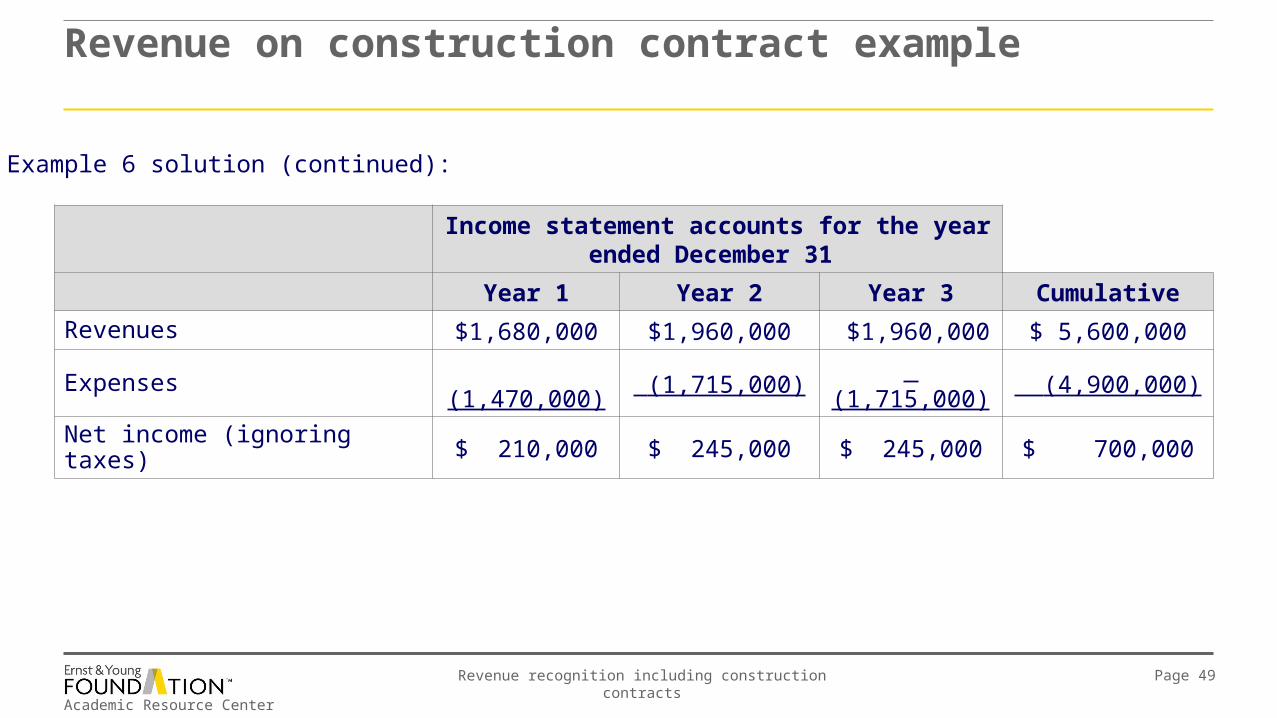

Income statement accounts for the year ended December 31

Year 1 Year 2 Year 3 Cumulative

Revenues $1,680,000 $1,960,000 $1,960,000 $ 5,600,000

Expenses (1,470,000) (1,715,000) (1,715,000) (4,900,000)

Net income (ignoring taxes) $ 210,000 $ 245,000 $ 245,000 $ 700,000

Revenue on construction contract example

Example 6 solution (continued):

Academic Resource Center

Revenue recognition including construction contracts Page 50

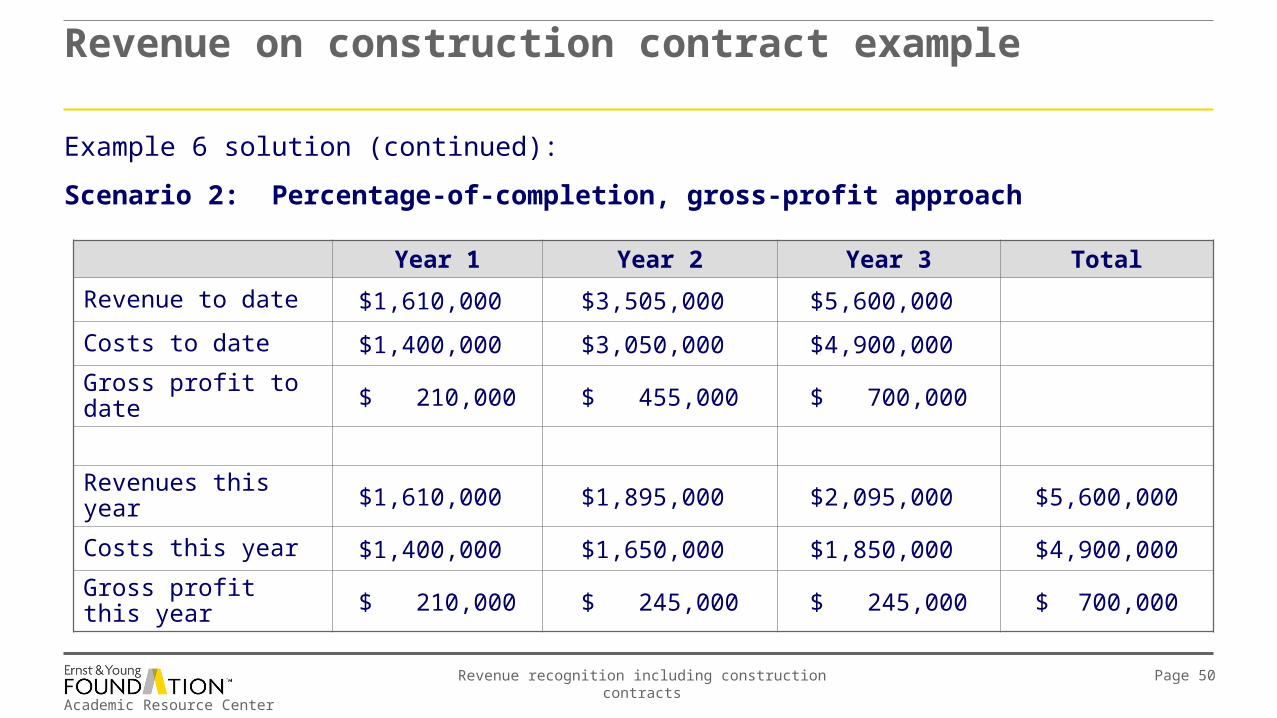

Example 6 solution (continued):

Scenario 2: Percentage-of-completion, gross-profit approach

Year 1 Year 2 Year 3 Total

Revenue to date $1,610,000 $3,505,000 $5,600,000

Costs to date $1,400,000 $3,050,000 $4,900,000

Gross profit to date $ 210,000 $ 455,000 $ 700,000

Revenues this year $1,610,000 $1,895,000 $2,095,000 $5,600,000

Costs this year $1,400,000 $1,650,000 $1,850,000 $4,900,000

Gross profit this year $ 210,000 $ 245,000 $ 245,000 $ 700,000

Revenue on construction contract example

Academic Resource Center

Revenue recognition including construction contracts Page 51

Example 6 solution (continued): Year 1 Year 2 Year 3

CIP 1,400,000 1,650,000 1,850,000

Cash 1,400,000 1,650,000 1,850,000

To record costs incurred.

A/R 1,300,000 2,400,000 1,900,000

Billings on CIP 1,300,000 2,400,000 1,900,000

To record billings.

Cash 1,000,000 2,200,000 2,400,000

A/R 1,000,000 2,200,000 2,400,000

To record collections.

Note: All amounts are in dollars.

Revenue on construction contract example

Academic Resource Center

Revenue recognition including construction contracts Page 52

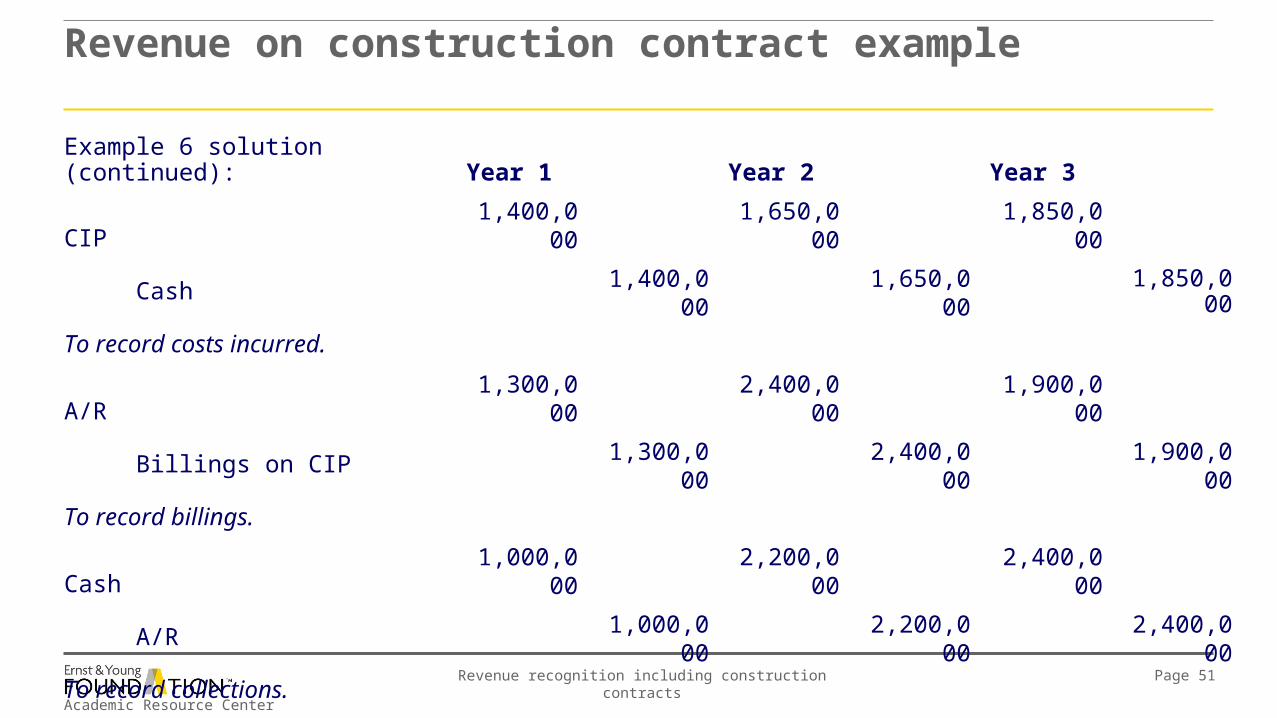

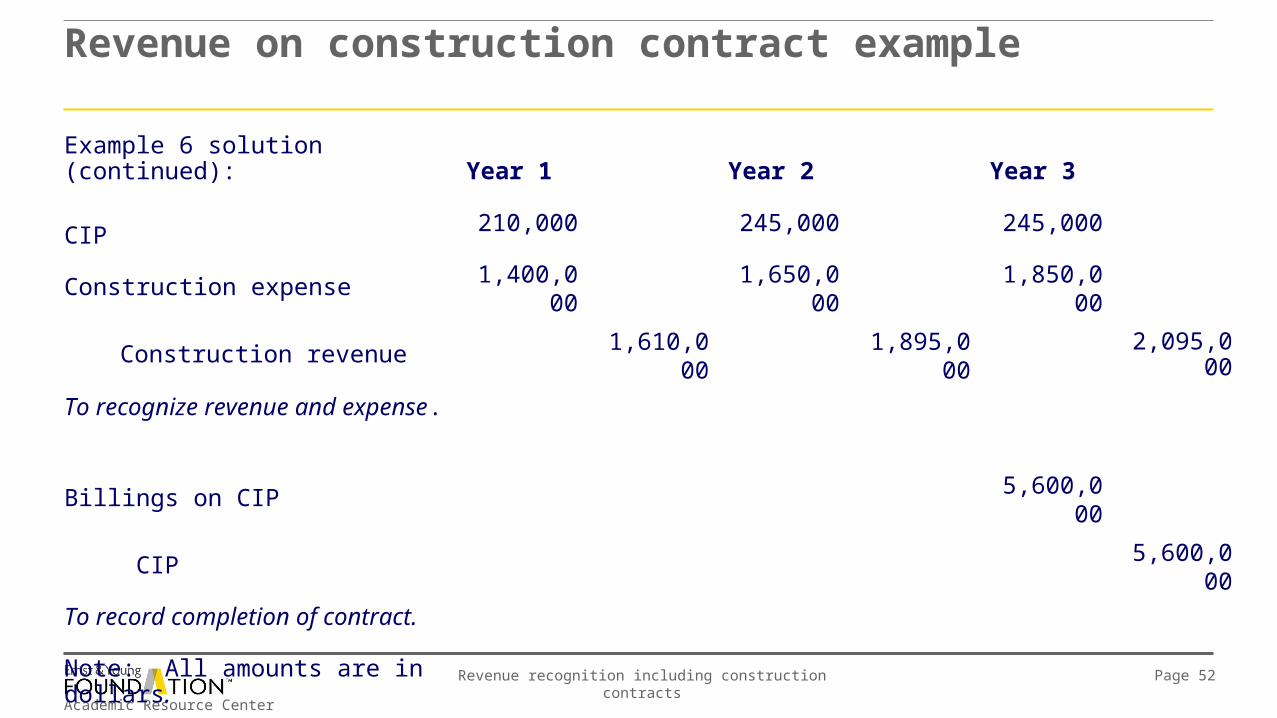

Example 6 solution (continued): Year 1 Year 2 Year 3

CIP 210,000 245,000 245,000

Construction expense 1,400,000 1,650,000 1,850,000

Construction revenue 1,610,000 1,895,000 2,095,000

To recognize revenue and expense.

Billings on CIP 5,600,000

CIP 5,600,000

To record completion of contract.

Note: All amounts are in dollars.

Revenue on construction contract example

Academic Resource Center

Revenue recognition including construction contracts Page 53

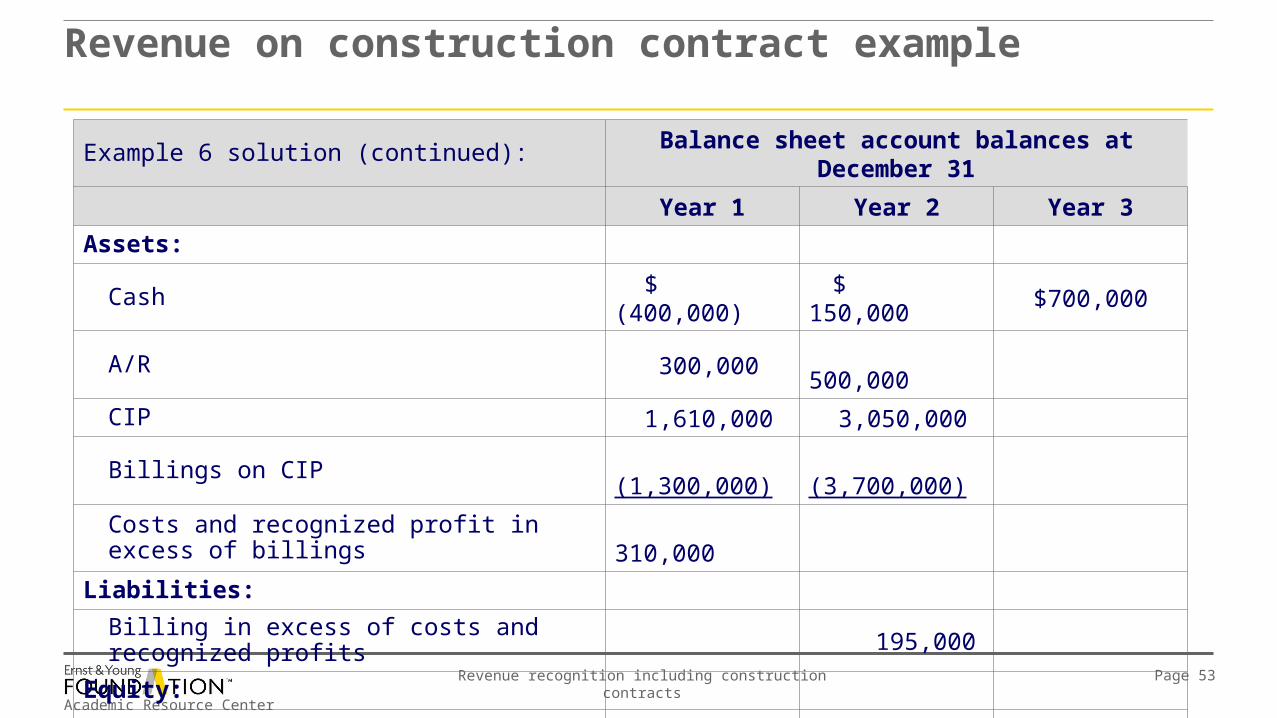

Revenue on construction contract example

Example 6 solution (continued): Balance sheet account balances at December 31

Year 1 Year 2 Year 3

Assets:

Cash $ (400,000) $ 150,000 $700,000

A/R 300,000 500,000

CIP 1,610,000 3,050,000

Billings on CIP (1,300,000) (3,700,000)

Costs and recognized profit in excess of billings 310,000

Liabilities:

Billing in excess of costs and recognized profits 195,000

Equity:

Retained earnings (ignoring effects of taxes) 210,000 455,000 700,000

Academic Resource Center

Revenue recognition including construction contracts Page 54

Income statement accounts for the year ended December 31

Year 1 Year 2 Year 3 Cumulative

Revenues $1,610,000 $1,895,000 $2,095,000 $ 5,600,000

Expenses (1,400,000) (1,650,000) (1,850,000) (4,900,000)

Net income (ignoring taxes) $ 210,000 $ 245,000 $ 245,000 $ 700,000

Revenue on construction contract example

Example 6 solution (continued):

Academic Resource Center

Revenue recognition including construction contracts Page 55

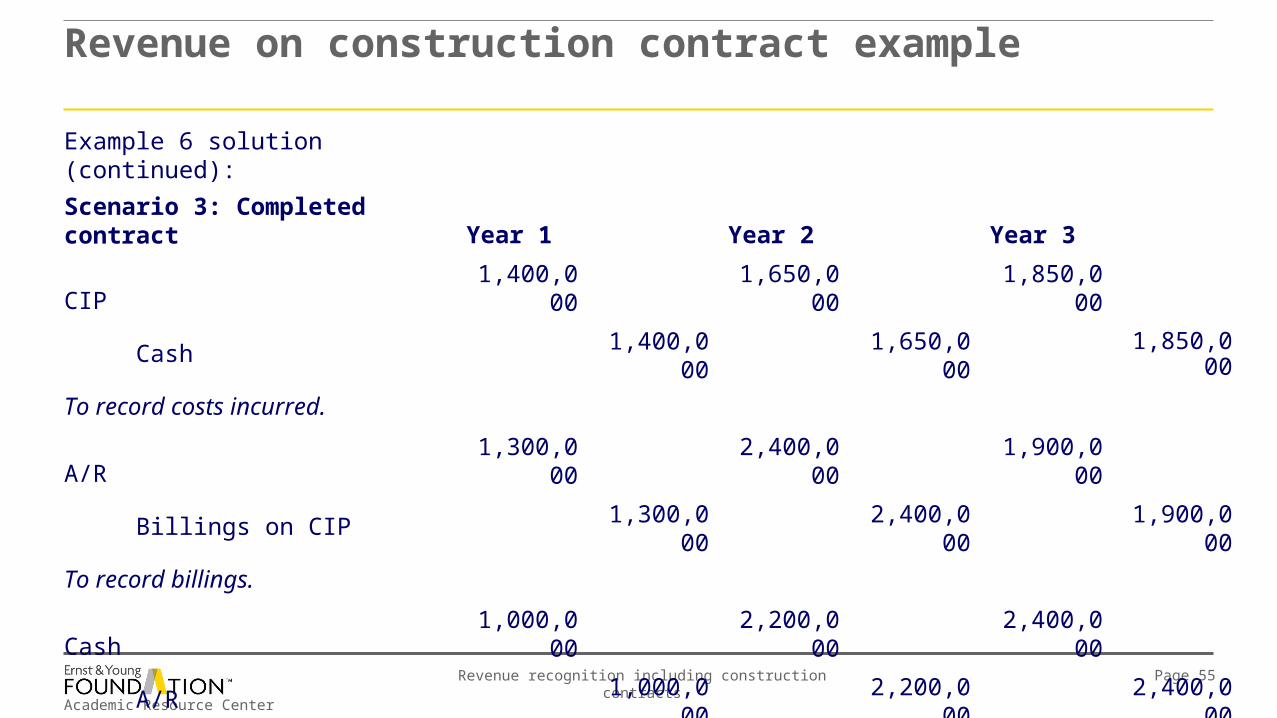

Example 6 solution (continued):

Scenario 3: Completed contract Year 1 Year 2 Year 3

CIP 1,400,000 1,650,000 1,850,000

Cash 1,400,000 1,650,000 1,850,000

To record costs incurred.

A/R 1,300,000 2,400,000 1,900,000

Billings on CIP 1,300,000 2,400,000 1,900,000

To record billings.

Cash 1,000,000 2,200,000 2,400,000

A/R 1,000,000 2,200,000 2,400,000

To record collections.

Note: All amounts are in dollars.

Revenue on construction contract example

Academic Resource Center

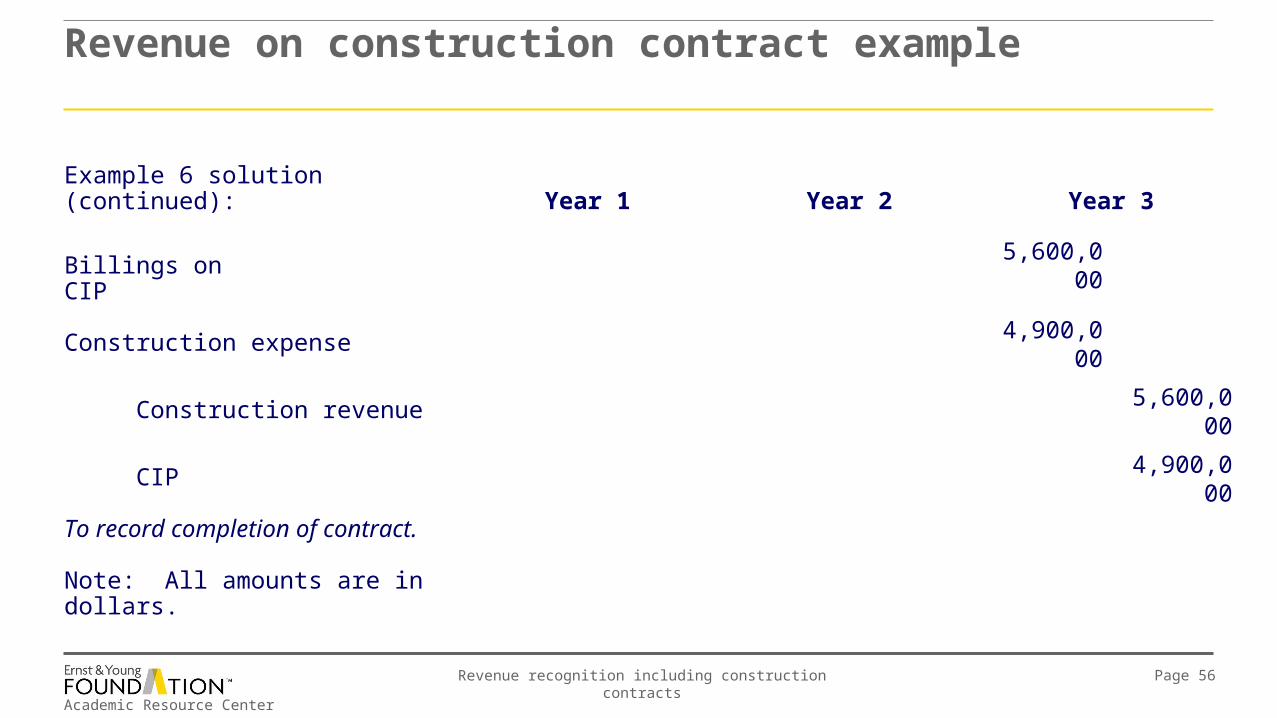

Revenue recognition including construction contracts Page 56

Example 6 solution (continued): Year 1 Year 2 Year 3

Billings on CIP 5,600,000

Construction expense 4,900,000

Construction revenue 5,600,000

CIP 4,900,000

To record completion of contract.

Note: All amounts are in dollars.

Revenue on construction contract example

Academic Resource Center

Revenue recognition including construction contracts Page 57

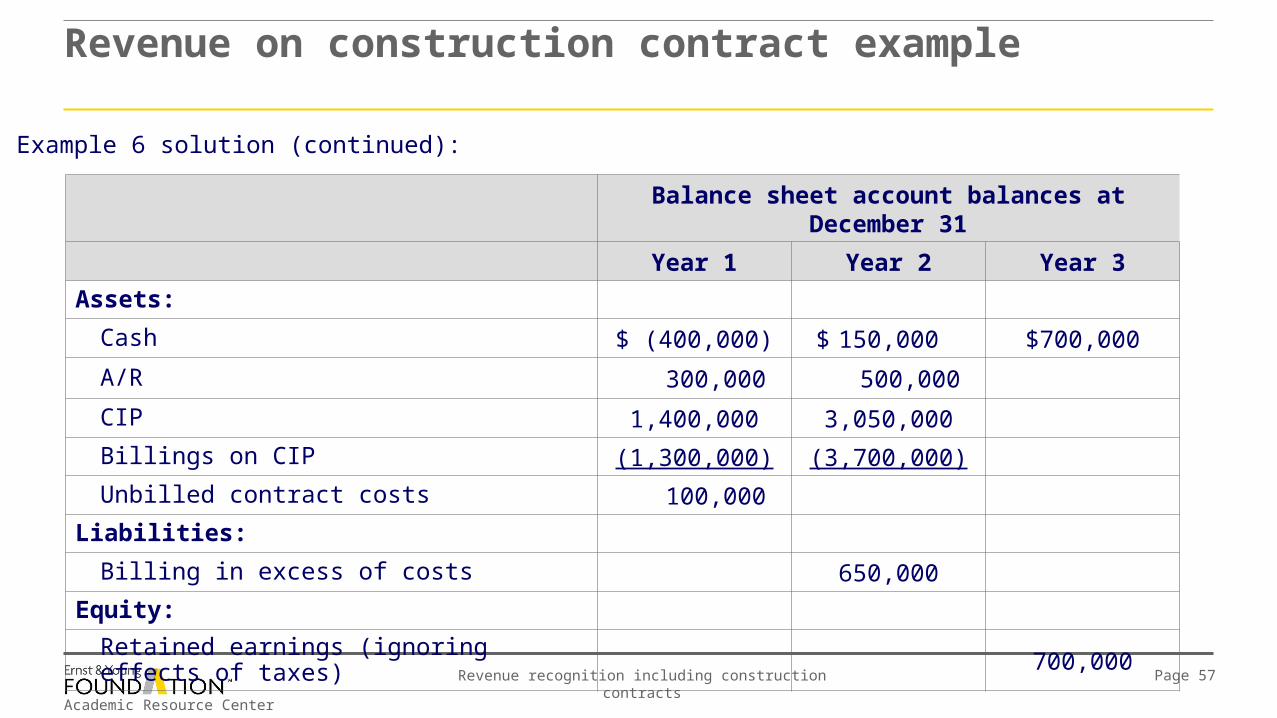

Balance sheet account balances at December 31

Year 1 Year 2 Year 3

Assets:

Cash $ (400,000) $ 150,000 $700,000

A/R 300,000 500,000

CIP 1,400,000 3,050,000

Billings on CIP (1,300,000) (3,700,000)

Unbilled contract costs 100,000

Liabilities:

Billing in excess of costs 650,000

Equity:

Retained earnings (ignoring effects of taxes) 700,000

Revenue on construction contract example

Example 6 solution (continued):

Academic Resource Center

Revenue recognition including construction contracts Page 58

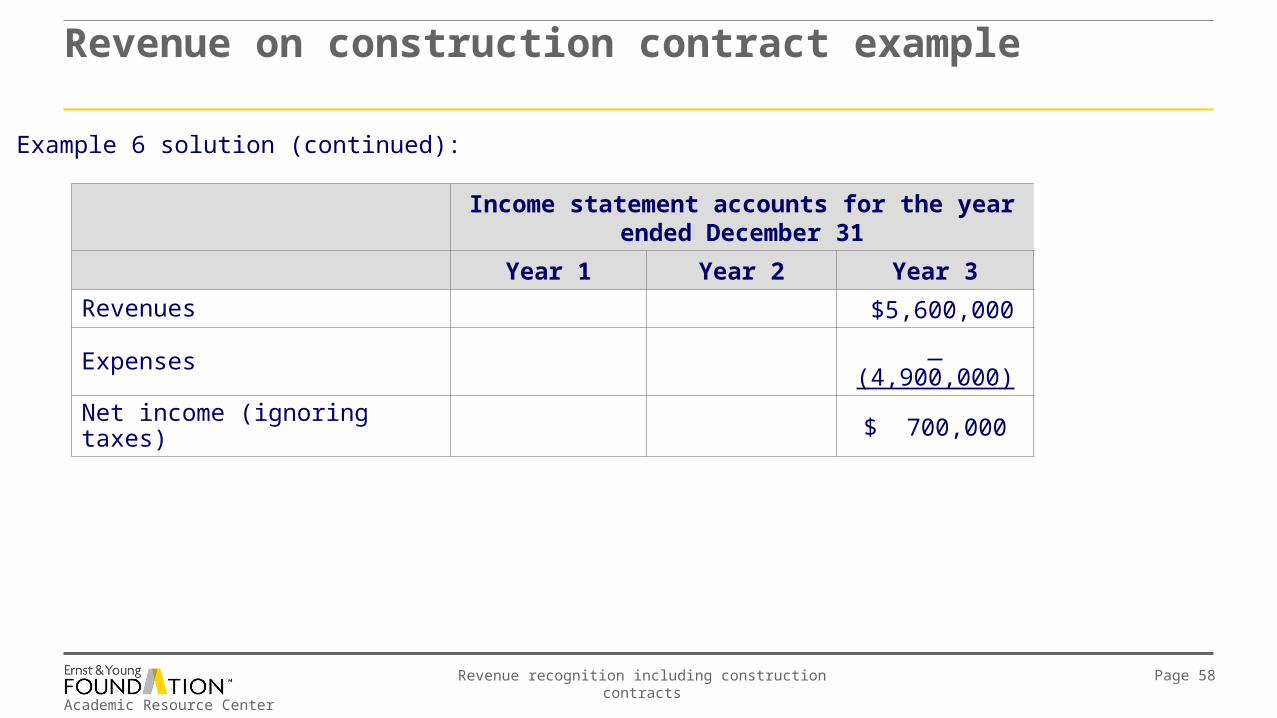

Income statement accounts for the year ended December 31

Year 1 Year 2 Year 3

Revenues $5,600,000

Expenses (4,900,000)

Net income (ignoring taxes) $ 700,000

Revenue on construction contract example

Example 6 solution (continued):

Academic Resource Center

Revenue recognition including construction contracts Page 59

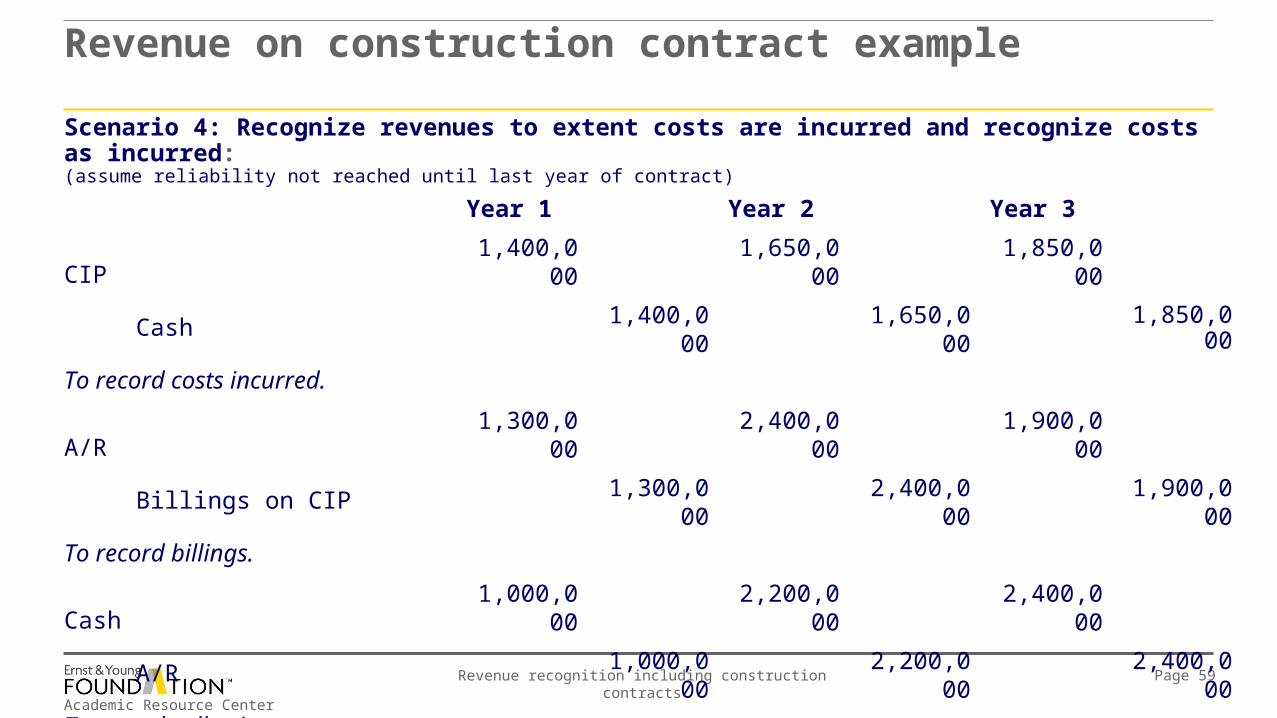

Scenario 4: Recognize revenues to extent costs are incurred and recognize costs as incurred: (assume reliability not reached until last year of contract)

Year 1 Year 2 Year 3

CIP 1,400,000 1,650,000 1,850,000

Cash 1,400,000 1,650,000 1,850,000

To record costs incurred.

A/R 1,300,000 2,400,000 1,900,000

Billings on CIP 1,300,000 2,400,000 1,900,000

To record billings.

Cash 1,000,000 2,200,000 2,400,000

A/R 1,000,000 2,200,000 2,400,000

To record collections.

Note: All amounts are in dollars.

Revenue on construction contract example

Academic Resource Center

Revenue recognition including construction contracts Page 60

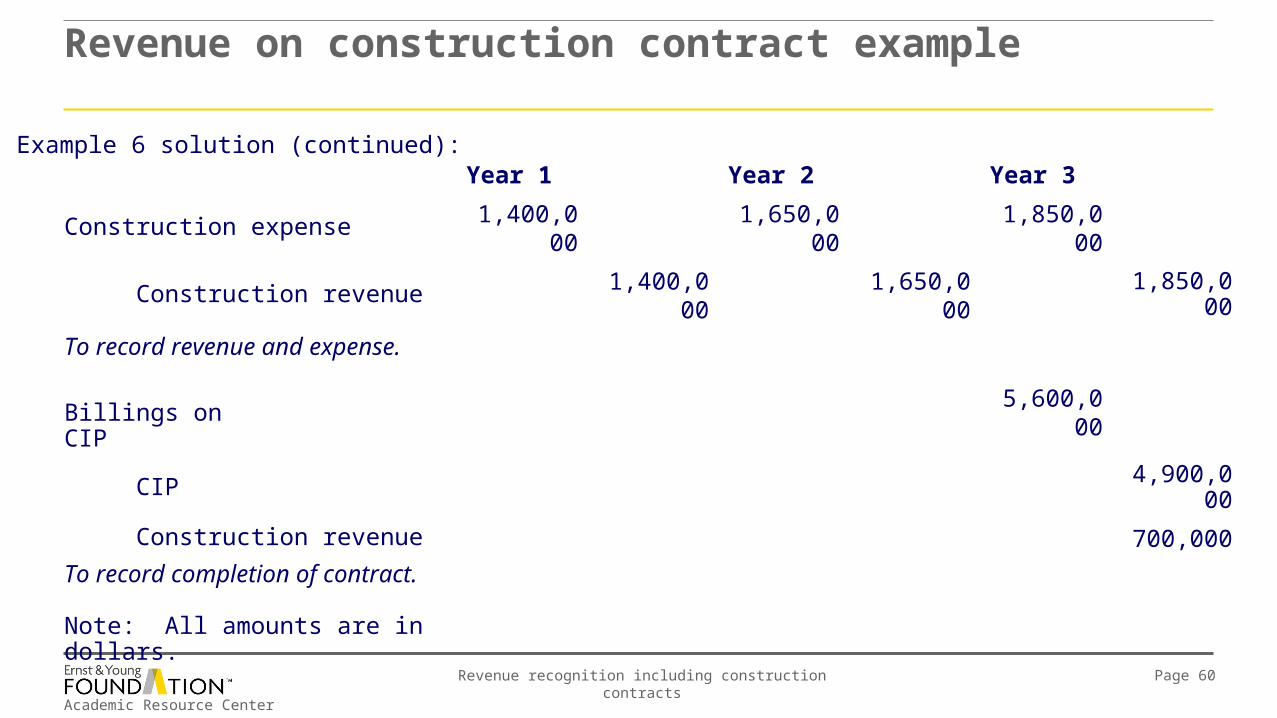

Year 1 Year 2 Year 3

Construction expense 1,400,000 1,650,000 1,850,000

Construction revenue 1,400,000 1,650,000 1,850,000

To record revenue and expense.

Billings on CIP 5,600,000

CIP 4,900,000

Construction revenue 700,000

To record completion of contract.

Note: All amounts are in dollars.

Revenue on construction contract example

Example 6 solution (continued):

Academic Resource Center

Revenue recognition including construction contracts Page 61

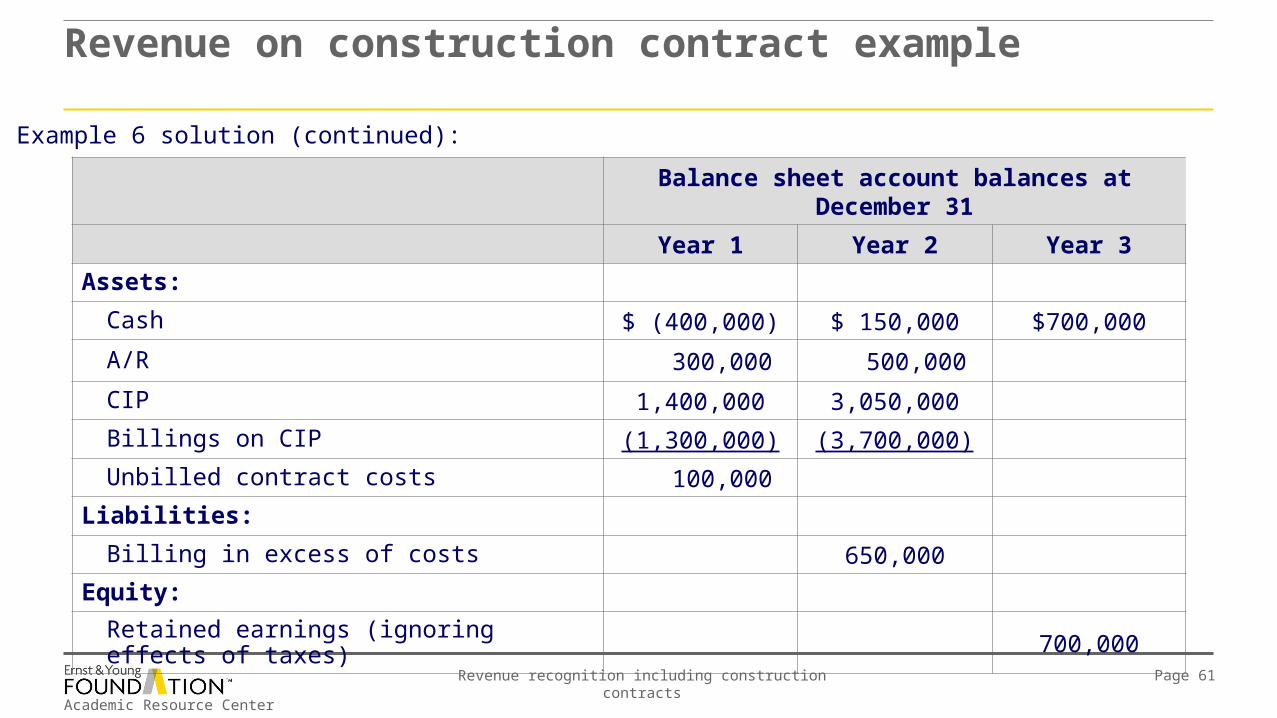

Balance sheet account balances at December 31

Year 1 Year 2 Year 3

Assets:

Cash $ (400,000) $ 150,000 $700,000

A/R 300,000 500,000

CIP 1,400,000 3,050,000

Billings on CIP (1,300,000) (3,700,000)

Unbilled contract costs 100,000

Liabilities:

Billing in excess of costs 650,000

Equity:

Retained earnings (ignoring effects of taxes) 700,000

Revenue on construction contract example

Example 6 solution (continued):

Academic Resource Center

Revenue recognition including construction contracts Page 62

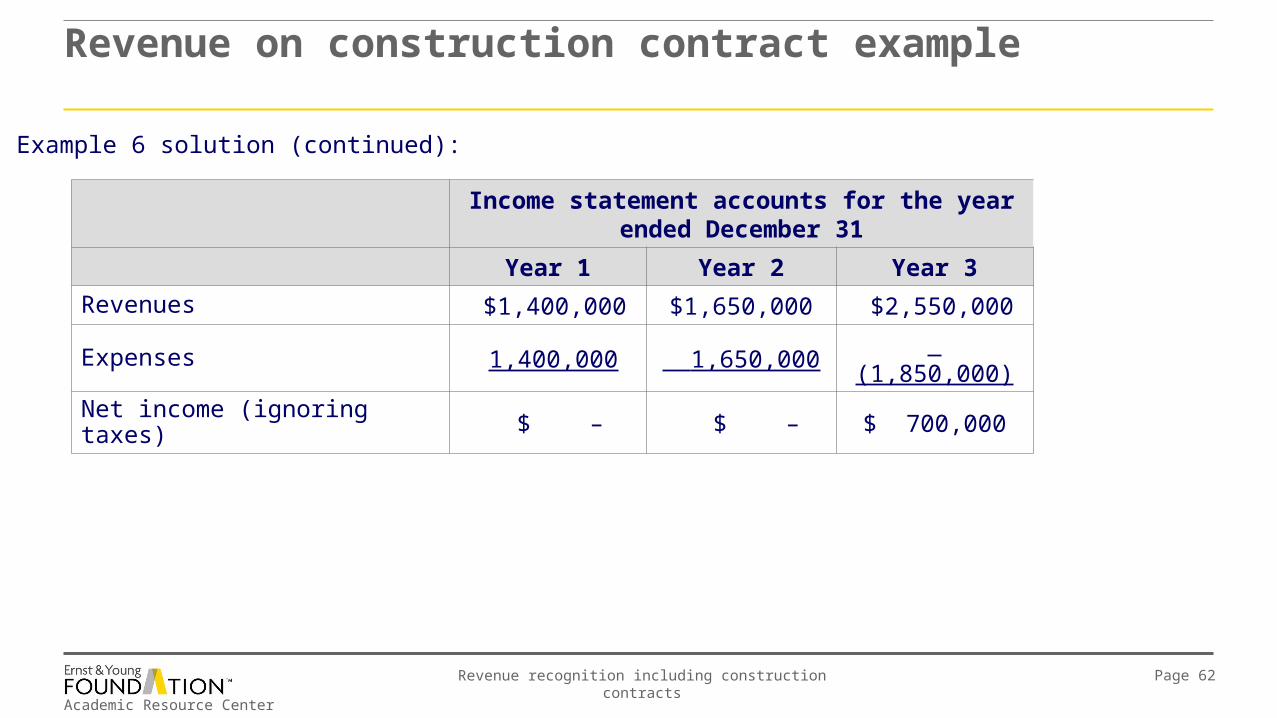

Income statement accounts for the year ended December 31

Year 1 Year 2 Year 3

Revenues $1,400,000 $1,650,000 $2,550,000

Expenses 1,400,000 1,650,000 (1,850,000)

Net income (ignoring taxes) $ – $ – $ 700,000

Revenue on construction contract example

Example 6 solution (continued):

Academic Resource Center

Revenue recognition including construction contracts Page 63

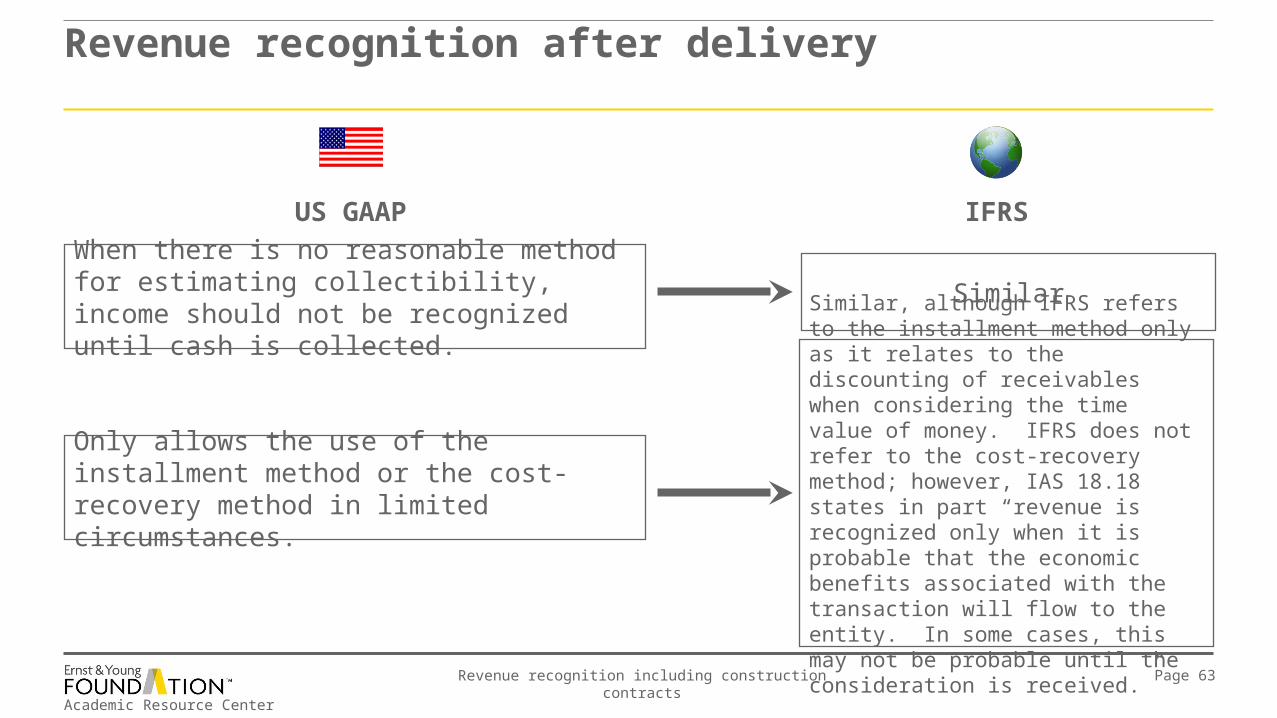

Revenue recognition after delivery

When there is no reasonable method for estimating collectibility, income should not be recognized until cash is collected.

Only allows the use of the installment method or the cost-recovery method in limited circumstances.

Similar

Similar, although IFRS refers to the installment method only as it relates to the discounting of receivables when considering the time value of money. IFRS does not refer to the cost-recovery method; however, IAS 18.18 states in part “revenue is recognized only when it is probable that the economic benefits associated with the transaction will flow to the entity. In some cases, this may not be probable until the consideration is received.”

IFRSUS GAAP

Academic Resource Center

Revenue recognition including construction contracts Page 64

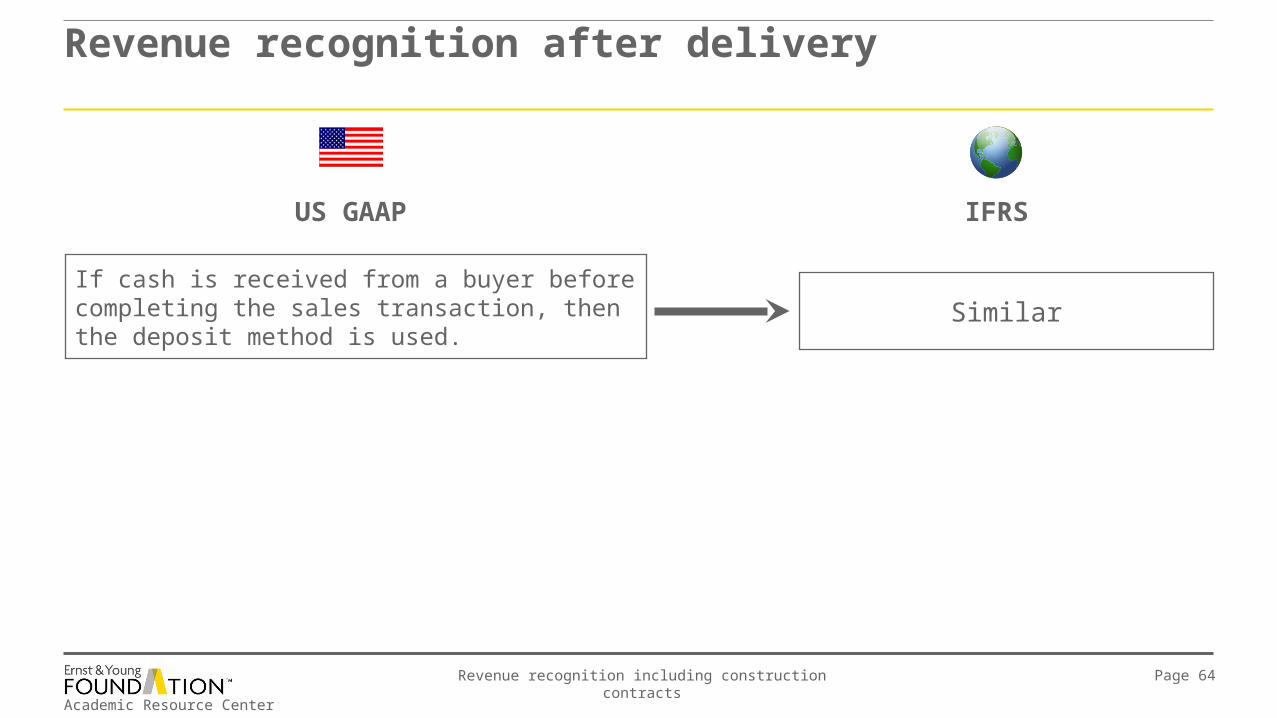

Revenue recognition after delivery

If cash is received from a buyer before completing the sales transaction, then the deposit method is used.

Similar

IFRSUS GAAP

Academic Resource Center

Revenue recognition including construction contracts Page 65

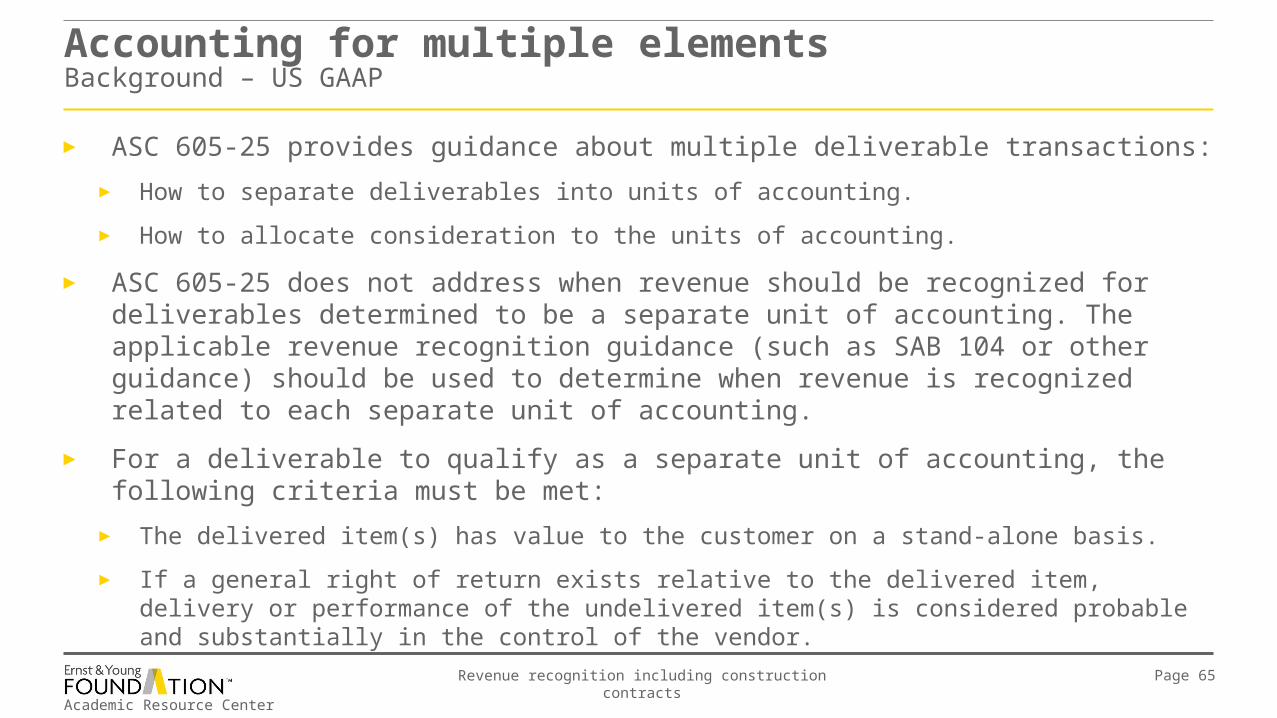

Accounting for multiple elementsBackground – US GAAP

► ASC 605-25 provides guidance about multiple deliverable transactions:

► How to separate deliverables into units of accounting.

► How to allocate consideration to the units of accounting.

► ASC 605-25 does not address when revenue should be recognized for deliverables determined to be a separate unit of accounting. The applicable revenue recognition guidance (such as SAB 104 or other guidance) should be used to determine when revenue is recognized related to each separate unit of accounting.

► For a deliverable to qualify as a separate unit of accounting, the following criteria must be met:

► The delivered item(s) has value to the customer on a stand-alone basis.

► If a general right of return exists relative to the delivered item, delivery or performance of the undelivered item(s) is considered probable and substantially in the control of the vendor.

Academic Resource Center

Revenue recognition including construction contracts Page 66

Accounting for multiple elementsBackground – US GAAP

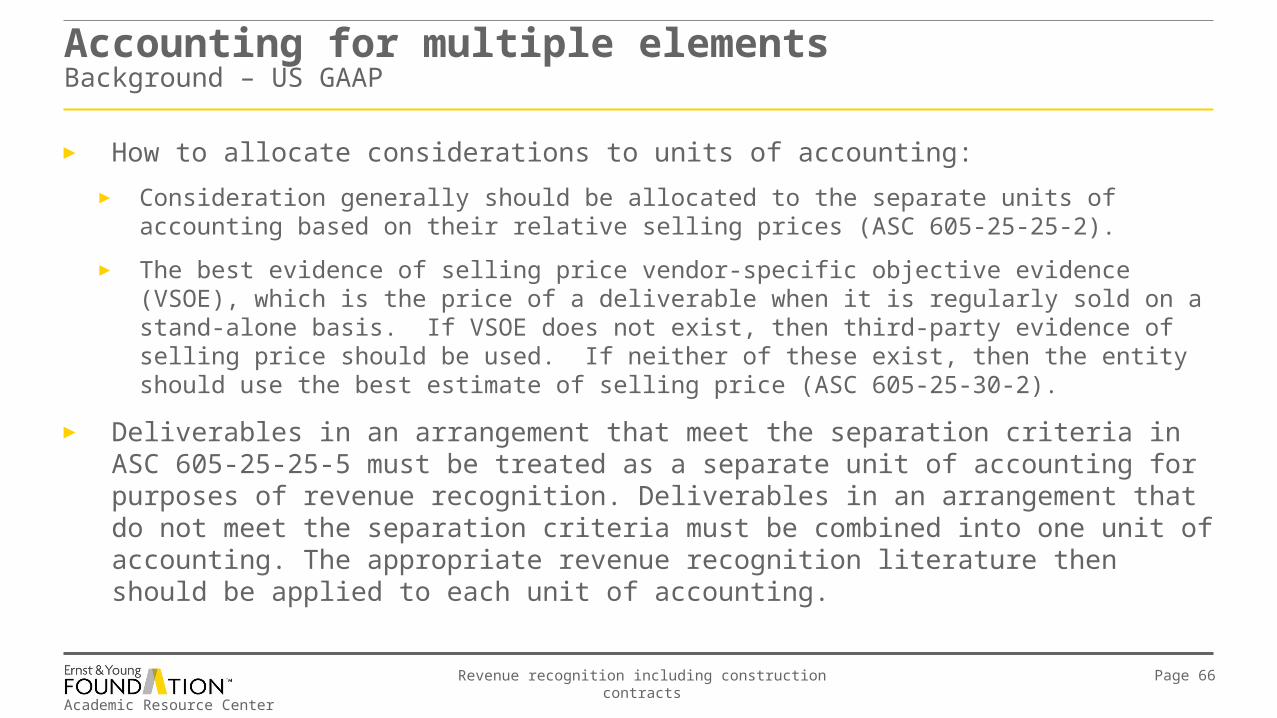

► How to allocate considerations to units of accounting:

► Consideration generally should be allocated to the separate units of accounting based on their relative selling prices (ASC 605-25-25-2).

► The best evidence of selling price vendor-specific objective evidence (VSOE), which is the price of a deliverable when it is regularly sold on a stand-alone basis. If VSOE does not exist, then third-party evidence of selling price should be used. If neither of these exist, then the entity should use the best estimate of selling price (ASC 605-25-30-2).

► Deliverables in an arrangement that meet the separation criteria in ASC 605-25-25-5 must be treated as a separate unit of accounting for purposes of revenue recognition. Deliverables in an arrangement that do not meet the separation criteria must be combined into one unit of accounting. The appropriate revenue recognition literature then should be applied to each unit of accounting.

Academic Resource Center

Revenue recognition including construction contracts Page 67

Accounting for multiple elementsBackground – US GAAP

► Although ASC 605-25-25 is silent as to what revenue recognition method should be applied to a combined unit of accounting, there is a rebuttable presumption that the revenue recognition model applicable to the final deliverable included in the arrangement is the model that should be followed for the combined unit of accounting.

► The final deliverable model dictates that revenue is recognized only once the last item has been delivered, or over a performance period if the last deliverable is a service, assuming the other revenue recognition criteria have been met.

► This presumption may be overcome in certain circumstances.

► Any contingent consideration is not included in the allocable arrangement consideration and is not recognized until the contingency is resolved.

Academic Resource Center

Revenue recognition including construction contracts Page 68

Accounting for multiple elementsBackground – IFRS

► IAS 18.13 states that the recognition criteria usually are applied separately to each transaction.

► It goes on to say that “in certain circumstances, it is necessary to apply the recognition criteria to the separately identifiable components of a single transaction to reflect the substance of the transaction.”

► This means that transactions have to be analyzed in accordance with their economic substance in order to determine whether they should be combined or segmented for revenue recognition purposes. The basic revenue recognition criteria are then applied to each component to determine when to record revenue.

► IAS 18, Appendix A.11 provides guidance on servicing fees included in the price of the product:

► “When the selling price of a product includes an identifiable amount for subsequent servicing (for example, after sales support and product enhancement on the sale of software), that amount is deferred and recognized as revenue over the period during which the service is performed. The amount deferred is that which will cover the expected costs of the services under the agreement, together with a reasonable profit on those services.”

Academic Resource Center

Revenue recognition including construction contracts Page 69

Accounting for multiple elements

Contracts executed concurrently or in close proximity are presumed to be one overall arrangement.

Similar: Parts of contracts are considered together when they are linked in such a way that the whole commercial effect cannot be understood without reference to the series of transactions as a whole.

IFRSUS GAAP

Academic Resource Center

Revenue recognition including construction contracts Page 70

Accounting for multiple elements

IFRS

► Does not provide detailed guidance.

US GAAP

► Provides detailed hierarchical guidance for determining when a contract should be separated into multiple units of accounting.

Academic Resource Center

Revenue recognition including construction contracts Page 71

Accounting for multiple elements

IFRS

► The total revenues are allocated to the components based on their relative fair value. IAS 18.7 contains the following definition: “Fair value is the amount for which an asset could be exchanged, or a liability settled, between knowledgeable, willing parties in an arm’s length transaction.”

► IFRS does not specify the method to determine fair value. However, IFRIC 13 provides guidance for measuring fair value for award credits that are being utilized in practice for multiple elements allocation, such as: (a) costs plus a reasonable profit margin, (b) third-party evidence and (c) VSOE (essentially the price for which the vendor has sold the goods on a stand-alone basis). From a practical standpoint, the use of these factors achieves the same results as under US GAAP.

US GAAP

► The total revenue is allocated to the units of account based on their relative selling prices. The best evidence of selling price is VSOE. If VSOE does not exist, then third-party evidence of selling price should be used. If neither of these exist, then the entity should use the best estimate of selling price.

Academic Resource Center

Revenue recognition including construction contracts Page 72

Accounting for multiple elements

IFRS

► Contingent amounts may be included when allocating total revenues to the components of the transaction. However, IAS 18.18 indicates that revenue is recognized only if it is probable that economic benefits of a transaction will flow to an entity and, in some cases, it may not be probable until an uncertainty is resolved. Therefore, when circumstances are encountered where contingent consideration is being allowed, it should be viewed with a great deal of skepticism and a thorough review of the facts and circumstances should be made in order to reach an appropriate conclusion.

US GAAP

► ASC 605-25-30-5 restricts the amount of revenue recognized, with respect to any component, to the amount that is not contingent on the delivery of additional items or other specific performance criteria. Contingent consideration is not recognized until the contingency is resolved.

Academic Resource Center

Revenue recognition including construction contracts Page 73

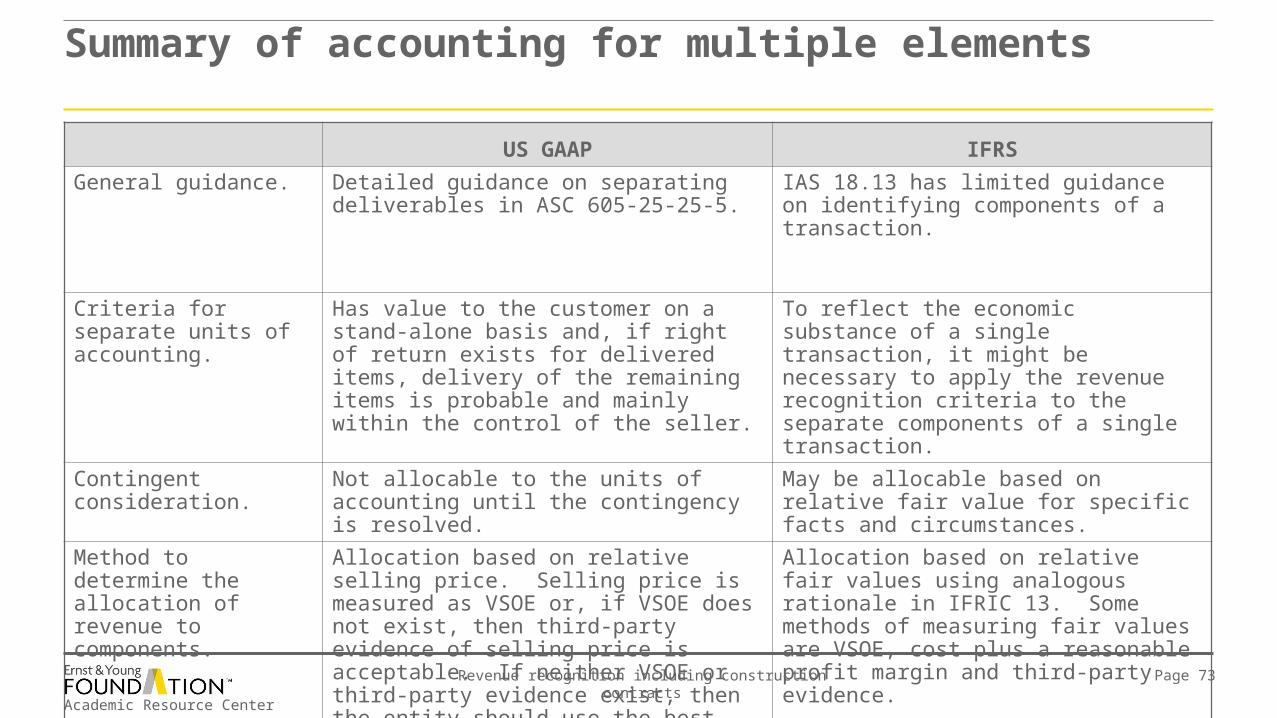

Summary of accounting for multiple elements

US GAAP IFRS

General guidance. Detailed guidance on separating deliverables in ASC 605-25-25-5.

IAS 18.13 has limited guidance on identifying components of a transaction.

Criteria for separate units of accounting.

Has value to the customer on a stand-alone basis and, if right of return exists for delivered items, delivery of the remaining items is probable and mainly within the control of the seller.

To reflect the economic substance of a single transaction, it might be necessary to apply the revenue recognition criteria to the separate components of a single transaction.

Contingent consideration.

Not allocable to the units of accounting until the contingency is resolved.

May be allocable based on relative fair value for specific facts and circumstances.

Method to determine the allocation of revenue to components.

Allocation based on relative selling price. Selling price is measured as VSOE or, if VSOE does not exist, then third-party evidence of selling price is acceptable. If neither VSOE or third-party evidence exist, then the entity should use the best estimate of selling price.

Allocation based on relative fair values using analogous rationale in IFRIC 13. Some methods of measuring fair values are VSOE, cost plus a reasonable profit margin and third-party evidence.

Academic Resource Center

Revenue recognition including construction contracts Page 74

Accounting for multiple elements example

Example 7 – accounting for multiple elements

On January 1, 2010, Robots Inc. (Robots) sold Wings Company (Wings) its packaging machine and other services for $500,000. The sales arrangement includes the packaging machine, installation services, training on the machine for a period of 18 months and three years of maintenance services.

The maintenance agreement is not separately priced and is not within the scope of paragraphs 1 through 6 of ASC 605-20-25 which deals with Accounting for Separately Priced Extended Warranty and Product Maintenance Contracts. The packaging machine is never sold without the related installation services; however, it is sold exclusive of training and maintenance services. In addition to being included in the original sales of the packaging machine, training contracts are sold on a stand-alone basis and maintenance contracts are sold on a stand-alone basis as renewals of existing contracts. The installation services do not have any stand-alone value as they are never sold separately and no other vendors provide these services.

Based on vendor-specific objective evidence, the selling price of the packaging machine, including installation services, is $420,000, the selling price of the training sessions is $60,000 and the selling price of three years of maintenance services is $120,000.

Academic Resource Center

Revenue recognition including construction contracts Page 75

Example 7 (continued):

The packaging machine was installed at Wings and operational on June 30, 2010, at which time the training services commenced. The training sessions are held weekly at Wings for the entire 18-month period. In addition, per the contract, the maintenance service period starts upon the completion of the installation (i.e., June 30, 2010). Management of Robots wants to report as much revenue as possible on the contract with Wings in 2010 so they earn their bonuses.

► Under US GAAP and IFRS, answer the following three questions:

1. How many units of accounting are included in this arrangement?

2. If there is more than one accounting unit, how should the $500,000 arrangement fee be allocated to the accounting units?

3. How much revenue for each accounting unit should be recorded as of December 31 of each year?

► How much total revenue would be reported in 2010 under IFRS compared to US GAAP?

Accounting for multiple elements example

Academic Resource Center

Revenue recognition including construction contracts Page 76

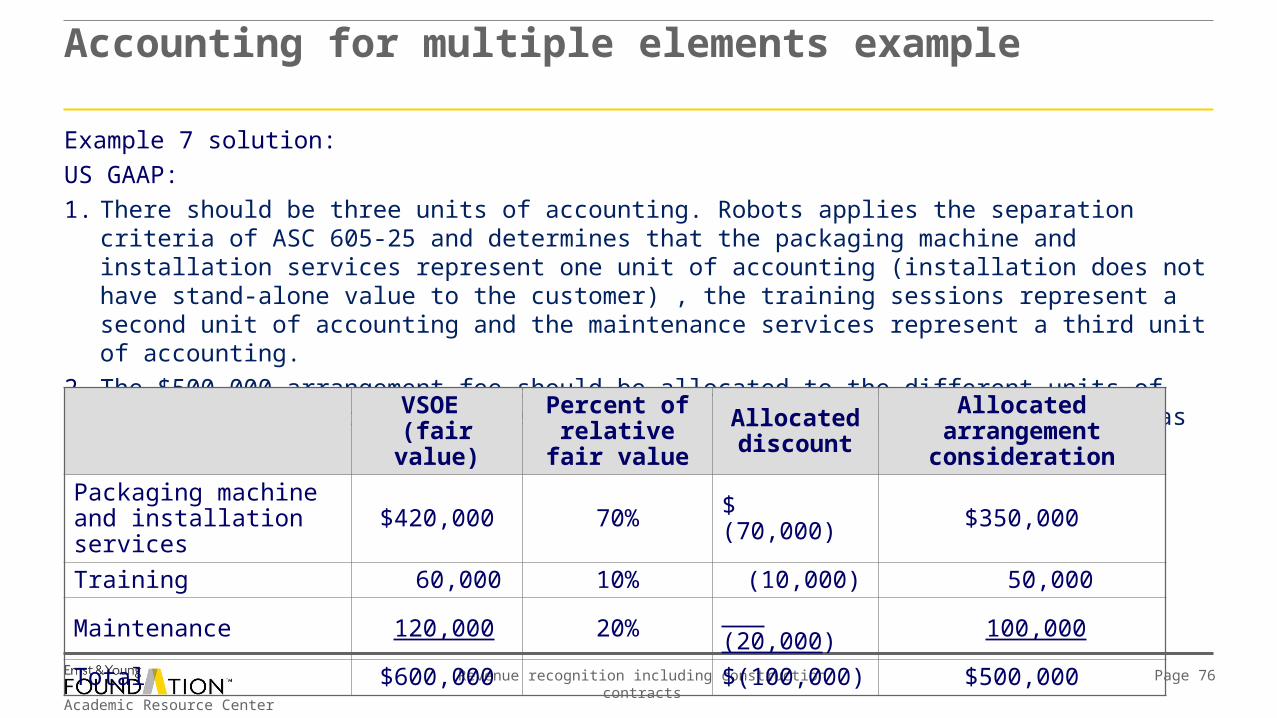

Example 7 solution:

US GAAP:

1. There should be three units of accounting. Robots applies the separation criteria of ASC 605-25 and determines that the packaging machine and installation services represent one unit of accounting (installation does not have stand-alone value to the customer) , the training sessions represent a second unit of accounting and the maintenance services represent a third unit of accounting.

2. The $500,000 arrangement fee should be allocated to the different units of accounting based on their selling price (VSOE). The allocation would be as follows:

Accounting for multiple elements example

VSOE (fair value)

Percent of relative fair

value

Allocated discount

Allocated arrangement consideration

Packaging machine and installation services $420,000 70% $ (70,000) $350,000

Training 60,000 10% (10,000) 50,000

Maintenance 120,000 20% (20,000) 100,000

Total $600,000 $(100,000) $500,000

Academic Resource Center

Revenue recognition including construction contracts Page 77

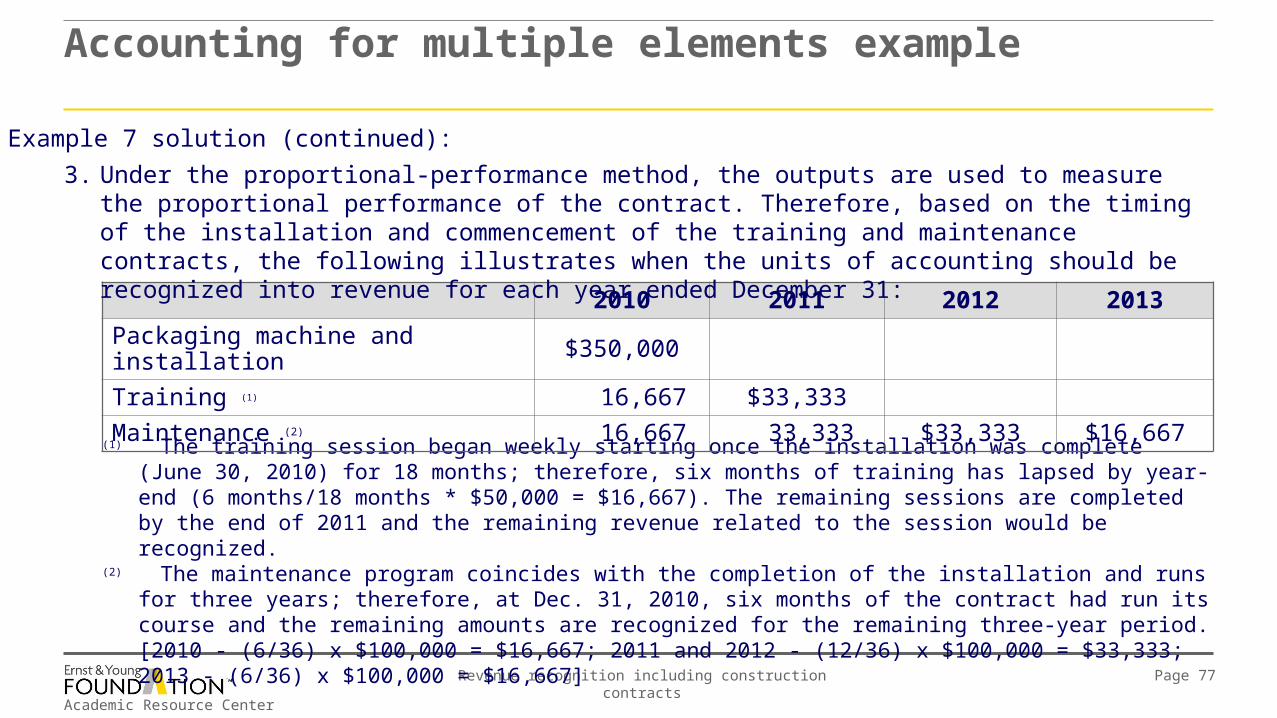

(1) The training session began weekly starting once the installation was complete (June 30, 2010) for 18 months; therefore, six months of training has lapsed by year-end (6 months/18 months * $50,000 = $16,667). The remaining sessions are completed by the end of 2011 and the remaining revenue related to the session would be recognized.

(2) The maintenance program coincides with the completion of the installation and runs for three years; therefore, at Dec. 31, 2010, six months of the contract had run its course and the remaining amounts are recognized for the remaining three-year period. [2010 - (6/36) x $100,000 = $16,667; 2011 and 2012 - (12/36) x $100,000 = $33,333; 2013 - (6/36) x $100,000 = $16,667]

Accounting for multiple elements example

2010 2011 2012 2013

Packaging machine and installation $350,000

Training (1) 16,667 $33,333

Maintenance (2) 16,667 33,333 $33,333 $16,667

3. Under the proportional-performance method, the outputs are used to measure the proportional performance of the contract. Therefore, based on the timing of the installation and commencement of the training and maintenance contracts, the following illustrates when the units of accounting should be recognized into revenue for each year ended December 31:

Example 7 solution (continued):

Academic Resource Center

Revenue recognition including construction contracts Page 78

Example 7 solution (continued):

IFRS:

The solution under IFRS is the same as for US GAAP. However, it should be noted that the standards under US GAAP are explicit and structured for determining allocation of multiple elements, while there is very limited guidance under IFRS. Likewise, IFRS does not provide guidance on how to determine fair value other than some analogous guidance contained in IFRIC 13, which is being used in practice for multiple element arrangements overall. The guidance in IFRIC suggests that some measures to determine fair value include: the amount for which items may be sold separately (selling price), amounts paid to third parties plus a reasonable profit margin (cost plus profit margin = selling price) or an estimated amount. This guidance is very similar to US GAAP with the end result being the same. However, students should be cautioned that a thorough analysis needs to be made for multiple-element arrangements under IFRS due to a lack of specific guidance, but generally there are no differences in accounting under either US GAAP or IFRS (excluding multiple-element arrangements for software).

Accounting for multiple elements example

Academic Resource Center

Revenue recognition including construction contracts Page 79

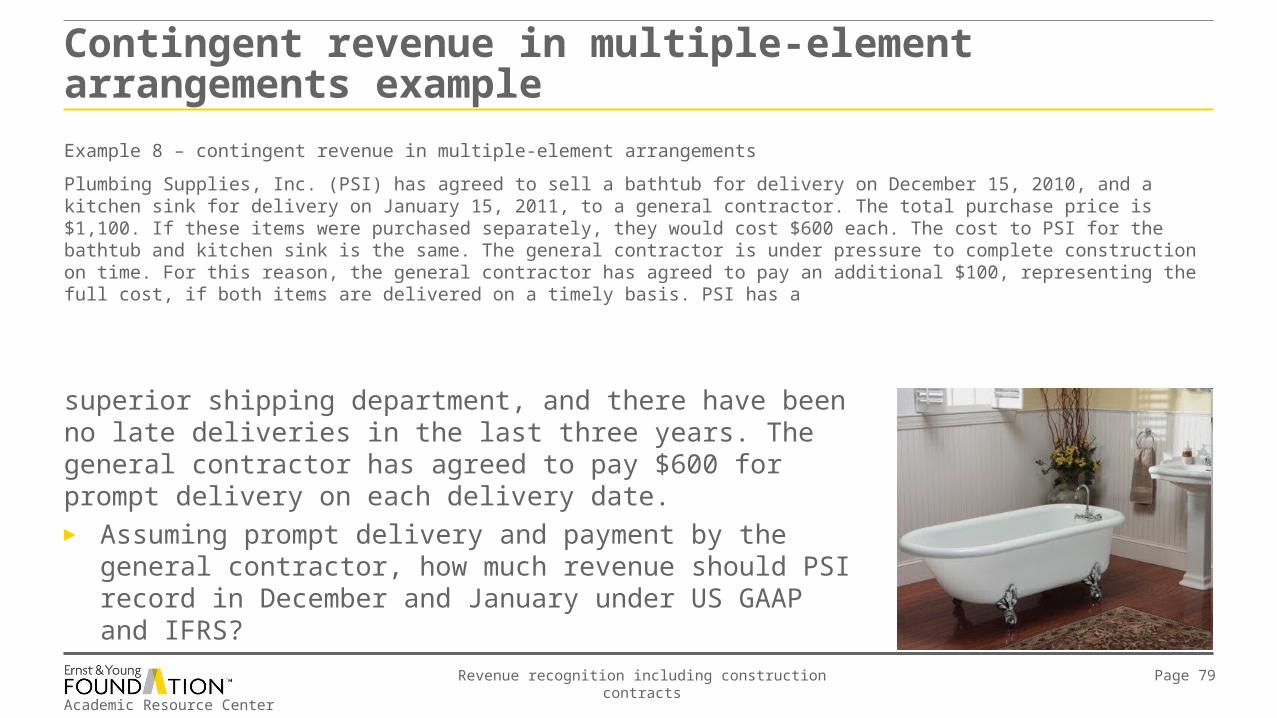

Example 8 – contingent revenue in multiple-element arrangements

Plumbing Supplies, Inc. (PSI) has agreed to sell a bathtub for delivery on December 15, 2010, and a kitchen sink for delivery on January 15, 2011, to a general contractor. The total purchase price is $1,100. If these items were purchased separately, they would cost $600 each. The cost to PSI for the bathtub and kitchen sink is the same. The general contractor is under pressure to complete construction on time. For this reason, the general contractor has agreed to pay an additional $100, representing the full cost, if both items are delivered on a timely basis. PSI has a

Contingent revenue in multiple-element arrangements example

► Assuming prompt delivery and payment by the general contractor, how much revenue should PSI record in December and January under US GAAP and IFRS?

superior shipping department, and there have been no late deliveries in the last three years. The general contractor has agreed to pay $600 for prompt delivery on each delivery date.

Academic Resource Center

Revenue recognition including construction contracts Page 80

Example 8 solution:US GAAP: None of the contingent consideration (the $100 potential revenue reduction) can be recorded until the contingency is fully resolved. Thus the amount to be allocated is $1,200 - $100 = $1,100. Therefore, revenue of $550 would be recorded in December and $650 in January ($550 allocated plus the $100 contingent amount).

IFRS: It is possible that two different answers may be reached under IFRS.

1. The same answer as determined for US GAAP. The logic in arriving at the same answer as US GAAP is that IAS 18.18 states “Revenue is recognized only when it is probable that the economic benefits associated with the transaction will flow to the entity. In some cases, this may not be probable until the consideration is received or until an uncertainty is removed.” Accordingly, until the second item is received, which doesn’t occur until after year-end, a contingency exists and a strict reading of the guidance would indicate that revenue would not be recognized.

2. The relative fair value of each delivery is $600 since the contingency is very remote. Thus, $600 could be recorded in both December and January.

Likewise, since the IFRS guidance is not definitive for all cases, if the answer in 2. above is used, it would be necessary to thoroughly review the facts and circumstances. In practice, this situation should and would raise the skepticism of accountants to make sure the appropriate conclusion was reached.

Contingent revenue in multiple-element arrangements example

Academic Resource Center

Revenue recognition including construction contracts Page 81

Bill-and-hold transactionsBackground

► In a bill-and-hold transaction, a customer agrees to purchase goods but the seller retains physical possession until the customer requests shipment to designated locations.

► Bill-and-hold transactions rarely result in up-front revenue recognition. In SAB 104, the SEC provided several conditions that must be met if a bill-and-hold transaction is to be recorded as a sale. These include:

“1. The risks of ownership must have passed to the buyer;

2. The customer must have made a fixed commitment to purchase the goods, preferably in written documentation;

3. The buyer, not the seller, must request that the transaction be on a bill-and-hold basis. The buyer must have a substantial business purpose for ordering the goods on a bill-and-hold basis;

4. There must be a fixed schedule for delivery of the goods. The date for delivery must be reasonable and must be consistent with the buyer's business purpose (e.g., storage periods are customary in the industry);

5. The seller must not have retained any specific performance obligations such that the earning process is not complete;

6. The ordered goods must have been segregated from the seller's inventory and not be subject to being used to fill other orders; and

7. The equipment [product] must be complete and ready for shipment.”

Academic Resource Center

Revenue recognition including construction contracts Page 82

Bill-and-hold transactionsBackground

► In addition, SAB 104 specifies that the following factors should be considered:“1. The date by which the seller expects payment and whether the seller has modified its normal billing and credit

terms for the buyer;

2. The seller's past experiences with and pattern of bill-and-hold transactions;

3. Whether the buyer has the expected risk of loss in the event of a decline in the market value of goods;

4. Whether the seller's custodial risks are insurable and insured;

5. Whether extended procedures are necessary in order to assure that there are no exceptions to the buyer's commitment to accept and pay for the goods sold (i.e., that the business reasons for the bill and hold have not introduced a contingency to the buyer's commitment).”

► The appendix to IAS 18, paragraph 1, provides that the seller recognize revenue on a bill-and-hold transaction once title passes to the buyer and the following requirements are met:

“(a) it is probable that delivery will be made;

(b) the item is on hand, identified and ready for delivery to the buyer at the time the sale is recognized;

(c) the buyer specifically acknowledges the deferred delivery instructions; and

(d) the usual payment terms apply.”

Academic Resource Center

Revenue recognition including construction contracts Page 83

Bill-and-hold transactions

The following criteria exist for recognizing revenue on a bill-and-hold transaction:

►Risk of ownership must pass to the buyer.

►There is a fixed commitment by the buyer and thus it is probable delivery will be made.

►The goods to be sold must be on hand and ready for shipment.

►The buyer acknowledges the delayed delivery instructions.

Similar

IFRSUS GAAP

** Because of the restrictive nature of the criteria, under both US GAAP and IFRS, bill-and-hold transactions rarely result in revenue recognition before the customer takes delivery of the goods (and even then, only if all of the other basic criteria for revenue recognition have been met).

Academic Resource Center

Revenue recognition including construction contracts Page 84

Bill-and-hold transactions

IFRS

► These requirements are not specifically included in IFRS guidance.

► IFRS does have a requirement that usual payment terms apply to the transaction (not specifically mentioned in SAB 104).

US GAAP

► SAB 104 requires a fixed delivery schedule and that the seller has not retained any performance obligations.

Academic Resource Center

Revenue recognition including construction contracts Page 85

Summary of criteria for bill and hold

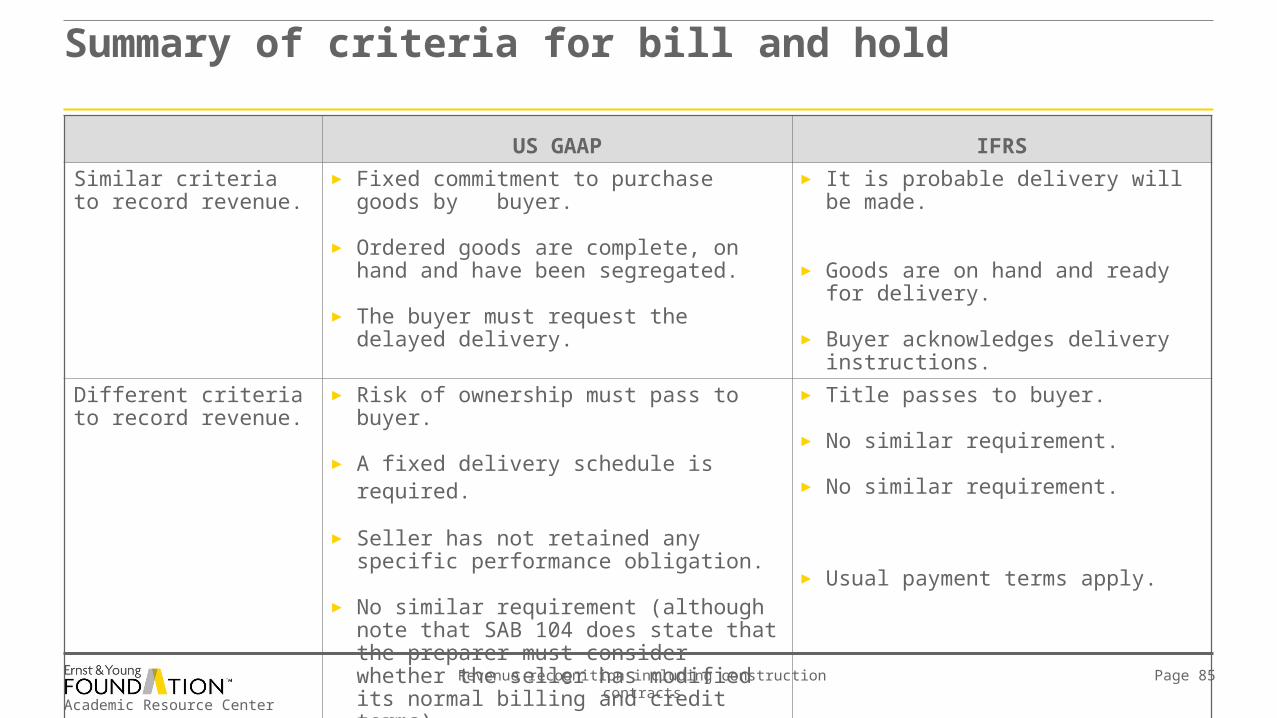

US GAAP IFRS

Similar criteria to record revenue.

► Fixed commitment to purchase goods by buyer.

► Ordered goods are complete, on hand and have been segregated.

► The buyer must request the delayed delivery.

► It is probable delivery will be made.

► Goods are on hand and ready for delivery.

► Buyer acknowledges delivery instructions.

Different criteria to record revenue.

► Risk of ownership must pass to buyer.

► A fixed delivery schedule is required.

► Seller has not retained any specific performance obligation.

► No similar requirement (although note that SAB 104 does state that the preparer must consider whether the seller has modified its normal billing and credit terms).

► Title passes to buyer.

► No similar requirement.

► No similar requirement.

► Usual payment terms apply.

Academic Resource Center

Revenue recognition including construction contracts Page 86

Example 9 – bill-and-hold transaction example

Paper Products Inc. (PPI) manufactures advertising material for billboards. PPI was contacted by a customer that wanted specific material prepared for a new sports product it expected to launch just before the World Series in October. In July, the customer placed a firm order for material for 1,000 billboards related to the launch of its new sports product. The order required delivery of the material during the third week in September, at which time $1.0 million would be due and payable.

In mid-September the customer contacted PPI and informed PPI that the introduction of the new sports product was delayed. PPI had already manufactured the material for the 1,000 billboards. After negotiations, it was decided that the

Bill-and-hold transaction example

► What, if any, revenue can be recognized in the year ended December for the undelivered billboards under US GAAP and IFRS?

customer would pay the $1.0 million due according to the contract. The customer hopes to launch the new sports product in conjunction with some future major league sporting event. PPI, in turn, agreed to store the billboard material in its warehouse until the launch of the new product. The customer agreed to separately purchase insurance on its billboard material stored in the warehouse. PPI’s fiscal year-end is December.

Academic Resource Center

Revenue recognition including construction contracts Page 87

Example 9 solution:

The customer has a commitment to take delivery of the billboard material and has already paid for it. It appears the customer has taken title to the billboard material as it is assuming the risk of ownership by purchasing insurance on this material. The billboard material is unique and can only be delivered to the customer introducing the new sports product. The customer is the party requesting the delayed delivery. It appears all the requirements for revenue recognition under IFRS have been met.

However, US GAAP also requires a fixed delivery schedule to be in place to recognize the revenue on this bill-and-hold transaction. Since the delivery date is uncertain, no revenue can be recorded until the billboard material is actually delivered. It should be noted that it could also be argued that PPI retained a performance obligation by agreeing to store the billboard material in its warehouse, which would also preclude revenue recognition until delivery of the billboard materials.

Bill-and-hold transaction example

Academic Resource Center

Revenue recognition including construction contracts Page 88

Disclosure of revenue policies

Requires disclosure of significant accounting policies. Similar

IFRSUS GAAP

Academic Resource Center

Revenue recognition including construction contracts Page 89

Disclosure of revenue policies

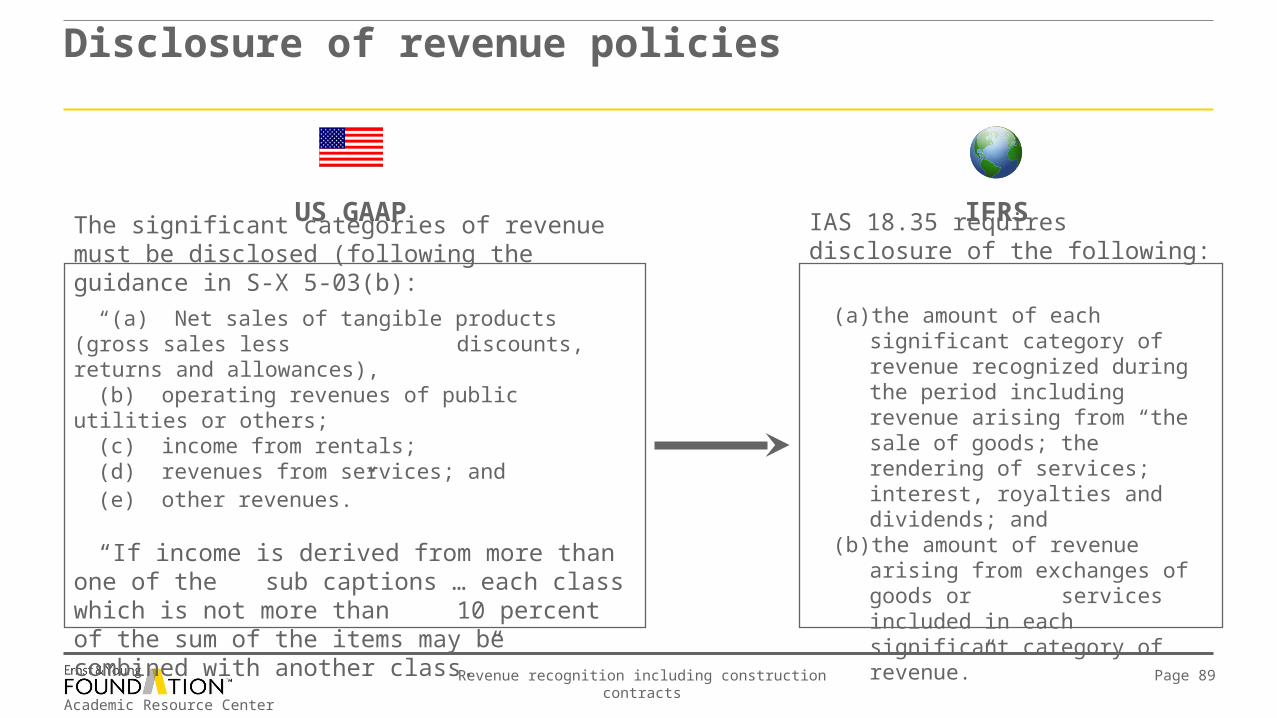

IAS 18.35 requires disclosure of the following:

(a) the amount of each significant category of revenue recognized during the period including revenue arising from “the sale of goods; the rendering of services; interest, royalties and dividends; and

(b) the amount of revenue arising from exchanges of goods or services included in each significant category of revenue.”

IFRSUS GAAP

The significant categories of revenue must be disclosed (following the guidance in S-X 5-03(b):

“(a) Net sales of tangible products (gross sales less discounts, returns and allowances),

(b) operating revenues of public utilities or others; (c) income from rentals; (d) revenues from services; and (e) other revenues.”

“If income is derived from more than one of the sub captions … each class which is not more than 10 percent of the sum of the items may be

combined with another class.”

Academic Resource Center

Revenue recognition including construction contracts Page 90

IFRS

► There is a general lack of detailed guidance regarding disclosures of revenue recognition policies.

► The determination of revenue recognition policies under IFRS requires significant professional judgment.

US GAAP

► There is significant guidance in various accounting pronouncements and industry guides regarding disclosures of revenue recognition policies.

Disclosure of revenue policies

Academic Resource Center

Revenue recognition including construction contracts Page 91

Ernst & Young LLP

Assurance | Tax | Transactions | Advisory

About Ernst & YoungErnst & Young is a global leader in assurance, tax, transaction and advisory services. Worldwide, our 141,000 people are united by our shared values and an unwavering commitment to quality. We make a difference by helping our people, our clients and our wider communities achieve their potential.

Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit www.ey.com.

Ernst & Young LLP is a client-serving member firm of Ernst & Young Global and of Ernst & Young Americas operating in the US.

© 2011 Ernst & Young Foundation (US). All Rights Reserved.All Rights Reserved.SCORE No. MM4092C.