revenue recognition for arrangements

TRANSCRIPT

1

Revenue Recognition Accounting For Arrangements: What You See (Or UCC) And What You Don’t See

Daniel V. Dooley* Revenue Recognition Accounting Sine Qua Non Staff Accounting Bulletin No. 101 The Securities and Exchange Commission (“SEC”) staff (“Staff”) has issued Staff Accounting Bulletin (“SAB”) No. 101 – Revenue Recognition in Financial Statements, which sets forth the Staff’s interpretation of generally accepted accounting principles (“GAAP”) governing accounting for revenue recognition in financial statements of SEC registrants.1 The guidance in SAB No. 101 principally sounds in contract law, that is to say – accounting for arrangements, creating express or implied contracts between sellers and buyers, for the exchange of consideration (usually goods and/or services for cash, cash equivalents, rights to receive cash, or other assets). The four basic revenue recognition criteria set forth in SAB No. 101 are:

Persuasive evidence of an arrangement exists.

Delivery has occurred or services have been rendered.

The seller’s price to the buyer is fixed or determinable.

Collectibility is reasonably assured. Thus, SAB No. 101 applies accounting principles or practices to elements of contract law, including: assent; reality of consent; agency; consideration; promises and covenants; and discharge and remedies. But, accounting recognition, under SAB No.101 does not necessarily follow legal recognition of contracts – as to timing, or the earning of consideration by seller, or the recognition of obligations to (or rights of) buyer. While framed in the context of business arrangements that sound in contract law, accounting rules do not always follow the legal rules. Generally Accepted Accounting Principles SAB No. 101 does not establish GAAP; rather, it provides the Staff’s views in applying GAAP to selected revenue recognition issues. In fact, SAB No. 101 expressly states:

* Daniel V. Dooley is a Partner in the firm of PricewaterhouseCoopers LLP and leads the firm’s Securities Litigation Consulting Practice. 1 17 CFR Part 211 (Amend.), Subpart B, Topics 13, 13-A and 8-A.

2

“This Staff Accounting Bulletin is not intended to change current guidance in the accounting literature.”2 Underlying U.S. GAAP is established by: the Financial Accounting Standards Board (“FASB”) or its predecessor, the Accounting Principles Board (“APB”); the American Institute of Certified Public Accountants (“AICPA”) and its Accounting Standards Executive Committee (“AcSEC”); and, the Emerging Issues Task Force (“EITF”) of FASB.3 The basic concept of revenue recognition is set forth in FASB Statement of Financial Accounting Concept (“CON”) No. 5, Recognition and Measurement in Financial Statements of Business Enterprises.4 CON No. 5, ¶ 83 states: “Revenue and gains of an enterprise during a period are generally measured by the exchange of values of the assets (goods or services) or liabilities involved, and recognition involves consideration of two factors, (a) being realized or realizable and (b) being earned ….

a. Realized or realizable. Revenues and gains are not recognized until realized or realizable. Revenues and gains are realized when products (goods or services), merchandise, or other assets are exchanged for cash or claims to cash. Revenues and gains are realizable when related assets received or held are readily convertible to known amounts of cash or claims to cash [e.g., accounts receivables] …

b. Earned. Revenues are not recognized until earned. An entity’s revenue-

earning activities involve delivering or producing goods, rendering services, or other activities that constitute its major or central operations, and revenues are considered to be earned when the entity has substantially accomplished what it must do to be entitled to the benefits represented by the revenues … .”

CON No. 5, ¶ 84 (a) states: “The two conditions (being realized or realizable and being earned) are usually met by the time the product or merchandise is delivered or services are rendered to customers, and revenues from manufacturing and selling activities and gains 2 See SAB No.101, Topic 8-B. 3 The hierarchy of GAAP is described in AICPA Statement on Auditing Standard (“SAS”) No. 69, The Meaning of Present Fairly in Conformity With Generally Accepted Accounting Principles in the Independent Auditor’s Report. See SAS No. 69 (AU§§ 411.05 (a)-(d), .07, and .11). 4 Statements of Financial Accounting Concepts are issued by FASB and establish a framework of accounting fundamentals and objectives. Unlike FASB Statements of Financial Accounting Standards (“SFAS”) or Accounting Principles Board Opinions or EITF Issues or AICPA Accounting and Auditing Guides (“AAG”), CONs do not establish standards prescribing accounting principles. Thus, CONs do not constitute authoritative pronouncements of GAAP unless there is an absence of higher GAAP authority, in which case CONs may constitute GAAP, as stated in AICPA SAS No. 69 ¶ 11: “In the absence of a pronouncement [e.g., SFAS, APB, EITF Issue or AAG] … the auditor of financial statements may consider other accounting literature … for example, FASB Statements of Financial Accounting Concepts …”

3

and losses from sales of other assets are commonly recognized at the time of sale (usually meaning delivery).” GAAP promulgates specific authoritative pronouncements that apply the conceptual guidance of CON No. 5, ¶¶ 83 and 84. Among these are:

AICPA Statement of Position (“SOP”) 97-2, Software Revenue Recognition.5

FASB SFAS No. 48, Revenue Recognition When Right of Return Exists.6

FASB SFAS No. 13, et seq., Accounting for Leases.

FASB SFAS No. 45, Accounting for Franchise Fee Revenue.

FASB SFAS No. 49, Accounting for Product Financing Arrangements.

FASB SFAS No. 66, Accounting for Sales of Real Estate.

Accounting Research Bulletin (“ARB”) No. 43, Restatement and Revision of Accounting Research Bulletins, (Ch. 1a) and ARB No. 45, Long-Term Construction-Type Contracts,7 and AICPA SOP 81-1, Accounting for Performance of Construction-Type and Certain Production-Type Contracts.8

FASB SFAS No. 91, Accounting for Nonrefundable Fees and Costs Associated

With Originating or Acquiring Loans and Initial Direct Costs of Leases.9

FASB SFAS No. 5, Accounting for Contingencies.10

5 An AICPA SOP is an authoritative pronouncement issued by AcSEC. 6 FASB SFAS No. 48 specifies how an enterprise should account for sales of its products in which the buyer has a right to return or exchange the product and in other circumstances when the seller’s price to the buyer may not (yet) be fixed or determinable. 7 Accounting Research Bulletins precursed APBs and also constitute GAAP when not superseded by any APB or FASB SFAS. 8 Collectively, ARB Nos. 43 (Ch. 1a) and 45 and AICPA SOP 81-1 establish the “percentage-of-completion,” “cost recovery,” and “completed contract” methods for accounting for long-term contracts involving construction, production and delivery of goods (or, in certain circumstances, services) over periods that usually exceed one year. 9 While FASB SFAS No. 91 nominally deals with revenue recognition in the financial services industry, in SAB No.101, the Staff have interpreted SFAS No. 91, as analogous GAAP, to apply to nonrefundable fee arrangements in all other industries, absent specific authoritative GAAP to the contrary. See SAB No. 101, Topic 13 (A) (3), “Delivery and Performance,” Question 5 and Interpretive Response. 10 FASB SFAS No. 5 is seminal GAAP that governs accounting for loss contingencies (e.g., allowance for doubtful accounts and sales returns allowances) which in turn implicates realizability under CON 5 and the revenue recognition criteria set forth in FASB SFAS No. 48 and AICPA SOP 97-2.

4

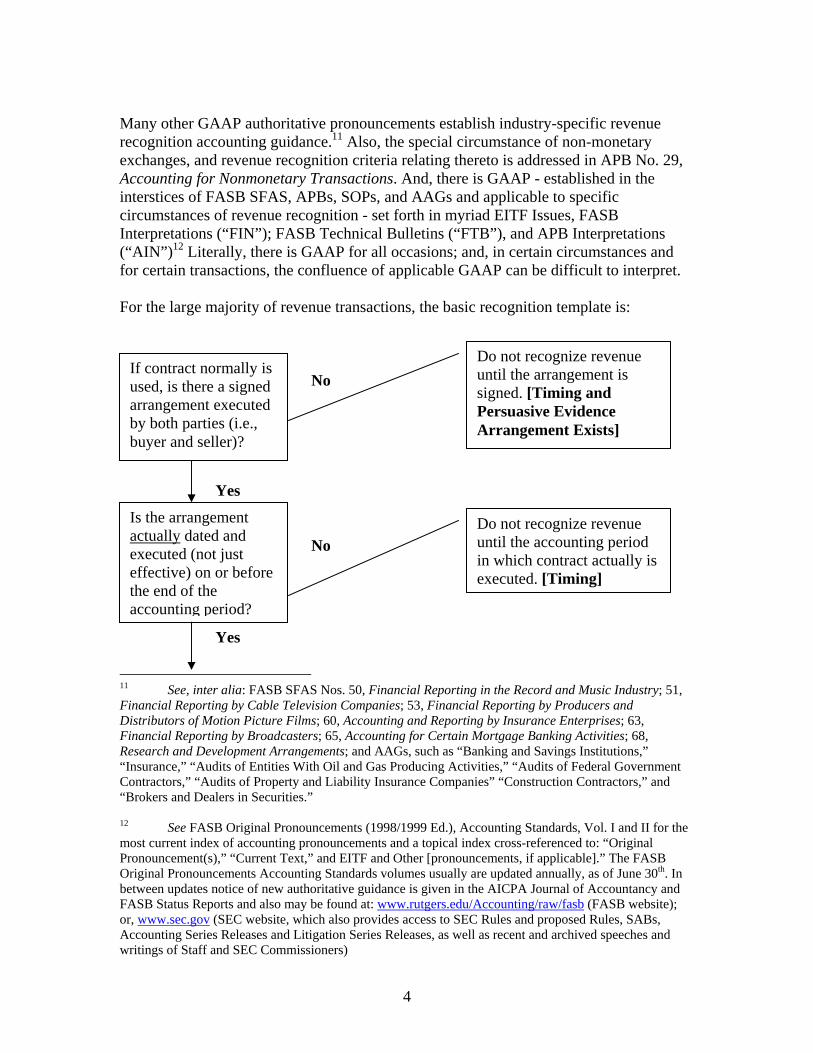

Many other GAAP authoritative pronouncements establish industry-specific revenue recognition accounting guidance.11 Also, the special circumstance of non-monetary exchanges, and revenue recognition criteria relating thereto is addressed in APB No. 29, Accounting for Nonmonetary Transactions. And, there is GAAP - established in the interstices of FASB SFAS, APBs, SOPs, and AAGs and applicable to specific circumstances of revenue recognition - set forth in myriad EITF Issues, FASB Interpretations (“FIN”); FASB Technical Bulletins (“FTB”), and APB Interpretations (“AIN”)12 Literally, there is GAAP for all occasions; and, in certain circumstances and for certain transactions, the confluence of applicable GAAP can be difficult to interpret. For the large majority of revenue transactions, the basic recognition template is: No

Yes

No Yes

11 See, inter alia: FASB SFAS Nos. 50, Financial Reporting in the Record and Music Industry; 51, Financial Reporting by Cable Television Companies; 53, Financial Reporting by Producers and Distributors of Motion Picture Films; 60, Accounting and Reporting by Insurance Enterprises; 63, Financial Reporting by Broadcasters; 65, Accounting for Certain Mortgage Banking Activities; 68, Research and Development Arrangements; and AAGs, such as “Banking and Savings Institutions,” “Insurance,” “Audits of Entities With Oil and Gas Producing Activities,” “Audits of Federal Government Contractors,” “Audits of Property and Liability Insurance Companies” “Construction Contractors,” and “Brokers and Dealers in Securities.” 12 See FASB Original Pronouncements (1998/1999 Ed.), Accounting Standards, Vol. I and II for the most current index of accounting pronouncements and a topical index cross-referenced to: “Original Pronouncement(s),” “Current Text,” and EITF and Other [pronouncements, if applicable].” The FASB Original Pronouncements Accounting Standards volumes usually are updated annually, as of June 30th. In between updates notice of new authoritative guidance is given in the AICPA Journal of Accountancy and FASB Status Reports and also may be found at: www.rutgers.edu/Accounting/raw/fasb (FASB website); or, www.sec.gov (SEC website, which also provides access to SEC Rules and proposed Rules, SABs, Accounting Series Releases and Litigation Series Releases, as well as recent and archived speeches and writings of Staff and SEC Commissioners)

If contract normally is used, is there a signed arrangement executed by both parties (i.e., buyer and seller)?

Do not recognize revenue until the arrangement is signed. [Timing and Persuasive Evidence Arrangement Exists]

Is the arrangement actually dated and executed (not just effective) on or before the end of the accounting period?

Do not recognize revenue until the accounting period in which contract actually is executed. [Timing]

5

No Yes No Yes No No Yes No Yes

Has delivery occurred?

Not only is evidence of shipment to the customer required, but also terms (e.g., FOB destination) may affect timing of recognition. Delivery to third parties, freight forwarders, and warehouses generally does not qualify. [Timing, Delivery and Acceptance]

Has customer accepted delivery, ownership and economic risk?

If “right of return” exists, have the criteria set forth in FASB SFAS No. 48, ¶ 6 (a) – (f) been met?

FASB SFAS No. 48, ¶ 6 revenue recognition criteria, when right of return exists, are: (a) seller’s price to buyer is substantially fixed or determinable at date of sale; (b) buyer has paid, or is obligated to pay, seller and the obligation is not contingent on resale of the product; (c) buyer’s obligation to pay would not change in the event of theft, physical destruction or damage of the product (economic/insurance risk has passed to buyer); (d) buyer has economic substance apart from that provided by seller; (e) seller does not have significant obligation for future performance to directly bring about resale of the product by the buyer; and (f) the amount of future returns can be reasonably estimated. If one or more of these criteria are not met, defer revenue recognition until right of return expires or all of the criteria are met. [Price Determinable and Contingency]

If right of return exists, and FASB SFAS No. 48, ¶ 6 (a) – (e) criteria are met, is the amount of future returns estimable under guidance set forth in FASB SFAS No. 5 and FASB SFAS No. 48, ¶¶ 7 and 8?

Allowance for sales returns and other “right of return” credits and adjustments must be reasonably estimable based on historical experience, evaluation of current events and likely future circumstances and other relevant facts – absent which, revenue recognition is deferred.

6

No Yes Yes No Yes No Yes No

If the arrangement provides for delivery of separate elements (i.e., of products or services), and such deliveries are not completed, or delivered to the customer, at date of sale, can the prices of such elements be separately fixed or determinable based upon vendor specific objective evidence?

Absent the ability to separately fix the price of multiple elements of the contractual consideration due buyer by seller, supported by competent VSOE subject to audit, revenue must be deferred and recognized either: (a) on a “percentage of completion” basis, if applicable under SOP 81-1 or SOP 97-2, or (b) ratably, over the term of the contract, or (c) when deliveries of all significant elements of products/services are made. [Price Fixed or Determinable]

If a credit sale, is receivable reasonably assured of collection (i.e., realizable) in the ordinary course and not due beyond twelve months of sale?

Sale does not meet the realizability criteria of CON No. 5, or SOP 97-2, or FASB SFAS No. 48, ¶ 6 (b) and (d), and recognition of revenue should be on the basis of cash received. [Realizability]

Does the arrangement constitute all, or in part, delivery of a “subscription” service (e.g., for license or content updates, for maintenance, etc.)

Account for ratably over the term of the arrangement. [Delivery and Continuing Obligation]

Does the arrangement include nonrefundable up-front fees paid to the seller?

Generally, under SAB No. 101, such fees may be required to be recognized ratably over the term of the arrangement. [Delivery, Continuing Obligation and Price Fixed and Determinable]

7

No Yes Yes No

Implications of SOP 97-2 For the Basic Revenue Recognition Template Although not fully acknowledged by SAB No. 101, the revenue recognition template that it adopts derives primarily from AICPA SOP 97-2, notwithstanding the fact that this SOP was promulgated only in respect of “when revenue should be recognized, and in what amounts, for licensing, selling, leasing or otherwise marketing computer software.”13 13 See AICPA SOP 97-2, ¶ 2, which also states: “It [AICPA SOP 97-2] does not apply, however, to revenue earned on products or services containing software that is incidental.”

Are costs properly accrued and matched with revenue in respect of any remaining obligation of seller?

In the case of significant continuing obligation, revenue may be required to be deferred. For “percentage-of-completion” accounting, revenue recognition requires that associated costs must be reasonably estimable and measurable. For insignificant remaining vendor obligations, revenue may be recognizable if such insignificant costs can be estimated and accrued. [Matching and Continuing Obligation]

Does the transaction involve non-monetary consideration from buyer to seller that does not meet the immediate recognition criteria of CON 5, ¶ 83 and APB No 29, ¶¶ 21 and 22? Defer revenue recognition

until asset(s) received are realizable (e.g., “sell-through” has occurred). [Realizability and Earned]

Recognize Revenue If, by this stage in the process, there is anything left to recognize at date of sale.

8

The Staff of the SEC interprets GAAP, as set forth in SAB No. 101, to apply the principles and practices promulgated in AICPA SOP 97-2 to revenue recognition accounting in other industries and in respect of other types of revenue, by use of “accounting transitivity,” direct invocation of relevant GAAP, and analogy, as follows:

Accounting transitivity. AICPA SOP 97-2 (or, “A”) is based upon accounting concepts and principles set forth in, inter alia: FASB CON No. 2, Qualitative Characteristics of Accounting Information; CON No. 5; FASB SFAS Nos. 5 and 48; ARB Nos. 43 and 45; and AICPA SOP 81-1 (collectively, “C”). Likewise, The Staff bases SAB No. 101 (or, “B”), in the main, on CON Nos. 2 and 5; FASB SFAS Nos.5 and 48; ARB Nos. 43 and 45; and AICPA SOP 81-1. By transitivity, if A = C and B = C, then A = B.

Direct invocation of relevant GAAP. Certain GAAP, particularly FASB SFAS

No. 48, overarches all revenue recognition accounting. Rights of return are not limited to sales of software, and as defined by FASB SFAS No. 48, a right of return includes any transaction where: “[A] product may be returned, whether as a matter of contract or as a matter of existing practice, either by the ultimate customer of by a party who resells the product to others. The product may be returned for a refund of the purchase price, for a credit applied to amounts owed or to be owed for other purchases, or in exchange for other products.”14 Under the broad principles established by FASB SFAS No. 48, this authoritative pronouncement creates seminal GAAP that underpins virtually every other authoritative pronouncement dealing with revenue recognition accounting.

Analogy. AICPA SAS No. 69, permits the use of “analogous GAAP” where no

specific GAAP can be found on point. This is the case, in SAB No. 101, where the Staff invokes FASB SFAS No. 91 – issued to address accounting for nonrefundable up-front fees by financial services entities – to apply to similar nonrefundable up-front fees in industries as diverse as: telecommunications, biotechnology, software, membership clubs and education services.

The fundamental principles of AICPA SOP 97-2 are exactly the same as those set forth in SAB No. 101, namely:15

Persuasive evidence of an arrangement exists.

Delivery has occurred.

The vendor’s fee is fixed or determinable.

Collectibility is probable.

14 See FASB SFAS No. 48, ¶ 3. 15 See AICPA SOP 97-2, ¶ 8.

9

Specific details of the revenue recognition criteria in AICPA SOP 97-2 cross over into SAB No.101 in a number of key areas, and the original intent of SEC interpretation in SAB No. 101 usually can be found in the guidance and background writings of AICPA SOP 97-2, as the following examples demonstrate. Both AICPA SOP 97-2 and SAB No. 101 mandate that persuasive evidence of an arrangement be a contract signed by both parties, where the vendor has a customary business practice of utilizing written contracts.16 Both condition revenue recognition on the occurrence of product delivery or the rendering of the services contracted for. Except in special circumstances, such delivery must be to the customer (either the ultimate user or the reseller).17 SAB No. 101 and AICPA SOP 97-2 interpret delivery to require that the customer has taken title and assumed the risks and rewards of ownership. SAB No. 101 also makes the point that where terms are “FOB destination” delivery has not occurred until the product is delivered to the customer’s delivery site, while for arrangements with terms of “FOB shipping point”, delivery typically occurs when the product actually is shipped to the customer.18

16 See id., at ¶ 16. Where a vendor operates in a manner that does not rely on signed contracts other forms of persuasive evidence are required to document the arrangement (e.g., a purchase order from a third party or on-line, E-commerce, authorization). 17 For the most part, delivery to intermediaries such as freight forwarders, warehouses or other third parties does not qualify as delivery under either AICPA SOP 97-2 or SAB No. 101. In SAB No. 101, the Staff recites the criteria established in Accounting and Auditing Enforcement Release (“AAER”) No 108 (August 5, 1986) for revenue recognition in “bill and hold” arrangements, where delivery has not occurred. These criteria are:

1. The risks of ownership must have passed to the buyer; 2. The customer must have made a fixed commitment to purchase the goods, preferably in writing; 3. The buyer, not the seller, must request that the transaction be on a “bill and hold” basis; and the

buyer must have a substantial business purpose for ordering the goods on a “bill and hold” basis; 4. There must be a fixed schedule for delivery of the goods; the date(s) for delivery must be

reasonable and consistent with the buyer’s business purpose (e.g., customary storage periods); 5. The seller must not have retained any specific performance obligations such that the earnings

process is not complete; 6. The ordered goods must be segregated from the seller’s inventory and not be subject to being used

to fill other orders; and, 7. The product must be completed and ready for shipment.

All of the above criteria must be met, as a threshold, for revenue recognition; however, the Staff advises that other criteria may be applicable, depending upon facts and circumstances, and even if such criteria are met, revenue recognition may not be appropriate. The practical implications of AAER No. 108 and SAB No. 101 are that revenue recognition for “bill and hold” transactions is a fool’s errand. Post hoc virtually any “bill and hold” arrangement can be found by the Staff of the Division of Enforcement of the SEC) to violate GAAP, generally, and one or more of the above criteria. 18 See SAB No. 101, Topic 13 (A) (3), Question 3 and Interpretive Response. Where multiple product elements are to be delivered, revenue recognition must be deferred for such elements to be delivered at later dates (until delivery actually has occurred), if the pricing of such elements can be fixed or determinable. Absent the ability to separately fix or determine the price of undelivered product elements, based upon VSOE, revenue recognition may require deferral until all elements are delivered.

10

In respect of customer acceptance, AICPA SOP 97-2 states: “After delivery, if uncertainty exists about customer acceptance of the software, license revenue should not be recognized until acceptance occurs.”19 SAB No. 101 restates the same requirement, and expands upon it to describe types of customer acceptance contractual provisions that the Staff would interpret as delaying revenue recognition (until acceptance has occurred or the provisions have lapsed), including customer rights to: (1) test the product; (2) require the seller to perform additional services subsequent to delivery (e.g., installation or activation); or (3) identify other work necessary to be done before accepting the product.20 Both AICPA SOP 97-2 and SAB No. 101 address the criteria of price fixed or determinable, but AICPA SOP 97-2 provides much more specific guidance regarding “multiple element” arrangements. This is because of the nature of many software licensing transactions where the arrangement s call for: (a) delivery of multiple elements of hardware, software, or both; (b) upgrade rights over the term of the arrangements (i.e., the right of the customer to receive subsequent versions or releases of the software); (c) “maintenance” services bundled with the initial software license; and/or (d) provision of other forms of post-contract support (“PCS”). AICPA SOP 97-2 describes a wide variety of PCS and multiple element terms typical to software arrangements, including:21

Vendor’s obligations for additional software deliverables and rights to exchange or return software.

Upgrade rights or buyer’s right to receive additional software, if and when,

developed.

Buyer’s rights to receive software maintenance and other PCS.

Bundled installation, training or integration services. The basic criteria of revenue recognition for such multiple element arrangements are: (a) ability to determine the respective pricing (i.e., fair value) of elements, based upon VSOE; (b) separate description of the services and other elements in the contract, so that the total price of the arrangement would be expected to vary based upon inclusions or exclusion of one or more of such elements; and (c) the fact that such services or other elements are not essential to the functionality of any other element(s) of the

19 See AICPA SOP 97-2, ¶ 20. 20 See SAB No. 101, Topic 13 (A) (3), supra. The Staff’s examples of customer acceptance contingencies are by no means exclusive. Other commonly found acceptance terms include: trial periods; acceptance dependant upon training, obtaining financing, “board approval,” or the product achieving stated performance measures. 21 See AICPA SOP 97-2, ¶¶ 34-66.

11

arrangement.22 Typically, objective evidence of the price for disaggregated, or unbundled, elements is based upon sales of such individual elements to third parties. For example, VSOE for maintenance might be determined by the prices charged the customer (or other) for separate maintenance contracts of the same type and providing similar coverage. AICPA SOP 97-2 notes that the fair value of separate elements may not necessarily be represented by individual prices for such elements that actually are stated in the contract. In the event of a failure to meet all of the criteria of AICPA SOP 97-2, ¶ 65, the entire fee arrangement should be recognized only as the service elements are performed, if a pattern of performance is discernable (e.g., by “milestones), or on a straight-line basis over the term of the services (or other elements’ delivery) obligation.23 Both SAB No. 101 and AICPA SOP 97-2 address the other major type of price fixed or determinable revenue recognition criteria – contingencies relating to vendor refunds, other express or implied rights of return granted to the buyer, customer cancellation privileges, or other circumstances in which buyer may not be obligated to pay the stated sales amount. Examples of such contingencies that might violate the criteria of price fixed or determinable include:

Unusually long credit terms.24

Cancellation rights.

Pricing and total amount of the transaction based upon the number units of product(s) distributed.

Other “variable-pricing” arrangements in which the buyer has the right to

allocate the arrangement fee (or sales amount) among different specified products, with different stated prices, covered by the arrangement.25

Uncertainties concerning buyer’s ultimate obligation created by volume rebate

terms, “most favored nation” price adjustment clauses, cooperative advertising or other marketing contribution clauses, etc.

22 See AICPA SOP 97-2, ¶ 65. 23 See id., at ¶ 67. 24 Usually, credit terms of over 12 months from date of sale preclude immediate revenue recognition. Such long terms imply that payment is dependent upon buyer’s ultimate resale of the product to third parties and/or that buyer’s are likely to return unsold product for credit against their payment obligations rather than make payment when the long-term receivable eventually comes due. 25 Because the actual mix of prices and quantities of products taken by the customer may not be known until delivery is complete for all products covered by the arrangement, prices of the multiple product elements may not be fixed or determinable.

12

Uncertainties, based upon business practice, buyer history, or other factors (e.g., channel capacity) which indicate a likelihood that buyer’s payment to seller is contingent on one or more future events (e.g., “sell-through”).

The realizability concept in FASB CON 5, ¶¶ 83 and 84, is applied in both SAB No. 101 and AICPA SOP 97-2 to mean, respectively: “Collectibility is reasonably assured,” and “Collectibility is probable.”26 In defining “probable,” the AICPA AcSEC refers to the same definition as used in FASB SFAS No. 5, which is: “The future event or events [i.e., collection of the account receivable arising from the sales transaction] are likely to occur.”27 In SAB No. 101, the Staff support the criteria of “reasonably assured by citing ARB No. 43 (Ch. 1a),28 APB NO. 10,29 and CON No. 5, ¶ 84 and AICPA SOP 97-2 (referred to above). However, nowhere in the literature cited by SAB No. 101 or AICPA SOP 97-2 is the conceptual criteria of realizability defined or established as an affirmative probability or assurance that collection will occur. Rather, the underlying accounting concept and GAAP express the criteria in negative terms of loss probability or doubt of collection. This nuance, though subtle, makes a substantial difference in meaning and application of both AICPA SOP 97-2 and SAB No. 101. If the burden falls on the side of proving that collection is probable, then it follows under that definition in FASB SFAS No. 5 (interpreted by EITF Issue No. 95-5) that collectibility must be judged likely, perhaps by odds of six, or seven, out of ten. But, if the burden falls on the side of proving that collection is doubtful, then it follows under the same definitions that non-collectibility must be judged likely, again perhaps by odds of six, or seven, out of ten. The interstices between affirmative or negative burdens well might represent a significant difference in weight of evidence required to meet these different burdens of proof.30 Accounting For Multiple-Element Arrangements Imagine a contractual arrangement to sell software and related services bundled together at one price. This is the common form of many software revenue recognition transactions, whether the multiple elements are express or implied obligations, under the

26 See SAB No. 101, Topic 13 (A) (1) and AICPA SOP 97-2, ¶ 8. 27 See AICPA SOP 97-2, n. 5, citing FASB SFAS No. 5, ¶ 3 (a). But, see also EITF Issue 93-5, Accounting for Environmental Liabilities, wherein the term “probable” is said to mean, in general practice, “more likely than not,” and is expressed quantitatively (e.g., 60%-75%). 28 See ARB No. 43 (Ch. 1a), ¶ 1: “Profit is deemed to be realized when a sale in the ordinary course of business is effected, unless the circumstances are such that collection of the sale price is not reasonably assured [emphasis added].” 29 See APB No. 10, ¶ 12, which only cites ARB No. 43 (Ch.1a), ¶ 1 as referenced in n. 29 above. 30 “Doubtful accounts” in the context of FASB CON No. 5, ¶ 84, means a loss accrual, reflecting allowance for uncollectible accounts receivable assets arising from sales, and as such is subject to the loss accrual criteria set forth in FASB SFAS No.5, ¶ 8 (a) and (b) and the proscription against “reserves for general contingencies” stated in FASB No. 5, ¶ 14. Thus, a reasonable case could be made for defining realizability (i.e., collectibility) as the absence of persuasive evidence that impairment of the account receivable is probable.

13

contract, to the customer. Now remember the second prong of the two-part revenue recognition test in CON No.5, ¶ 83: “… [R]evenues are considered to be earned when the entity has substantially accomplished what it must do to be entitled to the benefits represented by the revenues … [emphasis added].” What a seller must do may be spelled out in the contract, or it may be set forth in “side letters” to the contract, or it may obtain by oral promises made by the entity’s agent, acting with stated or apparent authority, or it may adhere through performance. If the arrangement calls for: (1) delivery of some product elements now; (2) delivery of some product elements later; (3) services provided for set-up, training, and testing; (4) integration and other services; (5) maintenance services over several years; (6) general, or specified up-grade rights, for free or at stated prices; and (7) in specific circumstances, rights of return or refund or price adjustment – then these are vendor’s obligations (or buyer’s rights) and “what [vendor] must do to be entitled to the benefits represented by the revenues.” Depending upon facts and circumstances, each of the aforementioned types of elements may require different accounting treatment – as to timing of revenue recognition, amounts to be recognized in respective accounting periods, and accounting method for accrual as revenue. In this hypothetical situation, assuming that functionality of any product element was not critically inter-dependent and assuming that all elements could be fair-valued and described separately, the following revenue recognition accounting might apply ($000):

Elements Key

1. Product, A Sys v2.0, GA and delivered at date of sale. 2. Product, B Sys v1.0, not GA for six months. 3. Set-up, training and testing, priced separately. 4. Integration of A Sys and B Sys into customer’s GL Sys, priced separately. 5. Maintenance services (not covering up-grades) for two years. 6. Upgrade rights for 2.1, if and when delivered, priced separately. 7. Right of refund of 20% of initial price of A Sys v.2.0 and, if customer buys

additional $1 million of product elements within next two years.

Recognize Revenue Estimated At Sale / When When/As Ratably When VSOE Delivery/ GA and Services Over Term Contingency Elements Fair Value Acceptance Delivered Rendered Obligated Expires*

1. $ 1,000 $1,000 2. 500 $500 3. 100 $100 4. 400 400 5. 600 $600 6. 100 100 7. <200> < 200> _____ _____ ____ $200

$ 2,500 $ 800 $600 $500 $600 ? * * If contingency expires, unused revenue may be recognized on unused refund credit.

14

Within one bundled contract, fair-valued at $2.5 to $2.7 million (depending upon whether the rebate will be earned by the buyer), seven different contractual and accounting elements obtain and require separate accounting treatments. What could be simpler? What could go wrong?

1. Regarding product delivered on or around date of sale, being recognized as revenue in the instant accounting period.

This product may not be separately priced or able to be priced separately,

requiring that revenue only be recognized when all other significant product elements are delivered (or ratably over the term of the arrangement).31

Functionality of this product may be critically dependant upon one or

more as yet undelivered product element(s), requiring that revenue recognition be deferred until delivery and acceptance has occurred.32

Acceptance (both de jure and de facto) must have taken place. Such

acceptance may be affected by:

Product return or sale cancellation periods;33 Contractual terms establishing “provisional acceptance” criteria; The term, and enforceability, of payment obligations;34 or, Performance, testing, or other acceptance criteria established by

contract.

The relative prices of the multiple elements may not be supportable by VSOE.

31 See AICPA SOP 97-2, ¶¶ 10, 12 and 65. 32 See Id., at ¶ 13: “[T]he delivery of an element is not considered to have occurred if there are undelivered elements that are essential to the functionality of the delivered element, because the customer would not have the full use of the delivered element.” 33 See Id., at ¶ 14: “No portion of the fee (including amounts otherwise allocated to delivered elements) meets the criteria of collectibility if the portion of the fee allocable to delivered elements is subject to forfeiture, refund or other concession if any of the undelivered elements are not delivered.” See also Id., at ¶ 26: “[I]f an arrangement includes (a) rights of return or (b) rights to refund without return of the software, FASB Statement No. 48 requires that conditions that must be met in order for the vendor to recognize revenue include that the amount of future returns or refunds can be reasonably be estimated.” 34 See Id., at ¶28: “[A]ny extended payment terms in a software licensing arrangement may indicate that the fee is not fixed or determinable. Further, if payment of a significant portion of the software licensing fee is not due until after expiration of the license or more than twelve months after delivery, the licensing fee should be presumed not to be fixed or determinable.” See also Id., at ¶ 27: “Because a product’s continuing value may be reduced due to the subsequent introduction of enhanced products by a vendor or its competitors, the possibility that the vendor still may provide a refund or concession to a creditworthy customer to liquidate outstanding amounts due under the original terms of the arrangement increases as payment terms become longer.”

15

Any cancellation period (other than obligations relating to warranties for defective software or similar obligations that are routine, short-term and relatively minor) must have lapsed, or been waived by the customer, before related license fees are considered to be fixed or determinable.35

2. Regarding product not yet GA, to be delivered subsequently:

If the product to be delivered is an up-graded version of the product delivered on or around date of sale (e.g., with enhanced functionality, new features, etc.), this begs the question, “Was the customer really buying (and intending to use) the earlier version?” Indications that customer acceptance actually is tied to subsequent delivery of the other (not yet GA) product may include:

Payment terms that extend beyond the promised delivery date for

the product up-grade; Absence of evidence of installation or use of the earlier version

of the product; Refund terms that forfeit substantially all of the amount of the

arrangement (or of the amount allocated to the delivered earlier version of the product) if delivery and acceptance of the up-graded version of the product does not occur.

The product to be delivered must not be critical to the functionality of the

product(s) delivered on or around date of sale, otherwise customer acceptance is deemed not to have occurred, and revenue recognition must be deferred until delivery and acceptance of all functionality-interdependent product elements.

The product is separately described, separately priced, and such price is

supported by VSOE.

The customer’s right to receive additional software is not in the nature of a subscription.36

The product is not actually part of PCS (which should be described and

priced separately, and should be supported by VSOE).

35 See FASB SFAS No. 5, ¶¶ 24-25. See also FASB SFAS No. 48, ¶¶ 3 and 6-8. 36 As part of a multiple-element software arrangement, a vendor may agree to deliver software currently and unspecified additional software products in the future (where such deliverables are not merely Post Contract Support, or “PCS,” upgrades, enhancements or minor “bug-fixes” relating to currently delivered products). Such an arrangement should be accounted under the subscription method; no allocation may be made among the current and potential future products in the arrangement, and generally, revenue should be recognized ratably over the term of the arrangement beginning with delivery of the first product.

16

3. In respect of service(s) element(s) for set-up, installation, training. 4. In respect of service(s) element(s) for system(s)’ integration.

Can the services be accounted for separately, under AICPA SOP 97-2, ¶ 65 (i.e., separately described, separately priced and supported by VSOE)?

Are the software elements of the arrangement, to which these services

apply, core or off-the-shelf?37

Are the services also available from other vendors?

Are the services primarily implementation services, such as implementation planning, loading of software, training of customer personnel, data conversion, building simple interfaces, running test data, and assisting in the development and documentation of procedures?38

Do the services carry any undue risk or unique acceptance criteria?

5. In connection with maintenance services. 6. In connection with PCS services and related obligations to provide up-grades,

“bug-fixes,” etc.

Services must be separately described, priced and supported by VSOE. 37 See AICPA SOP 97-2, ¶¶ 68-69: “Core software … is not sold as is because customers cannot use it unless it is customized to meet system objectives or customer specifications. Off-the-shelf software is software that is marketed as a stock item that can be used by the customer with little or no customization… Software should be considered off-the-shelf if it can be added to the arrangement with insignificant changes in the underlying code and it could be used by the customer for the customer’s purposes upon installation…. If significant modifications or additions to the off-the-shelf software are necessary to meet the customer’s purpose (for example changing or making additions to the software, or because it would not be usable in its off-the-shelf form in the customer’s environment), the software should be considered core software for purposes of that arrangement …. [and] no element of the arrangement would qualify for accounting as a service, and contract accounting [i.e., under AICPA SOP 81-1] should be applied to both the software and service elements of the arrangement. See also AICPA SOP 97-2, ¶ 70: “Factors indicating that the service element is essential to the functionality of the other elements of the arrangement, and consequently should not be accounted for separately, include the following.

• The software is not off-the-shelf software. • The services include significant alterations to the features and functionality of the off-the-shelf

software. • Building complex interfaces is necessary for the vendor’s software to be functional in the

customer’s environment. • The timing of payments for the software is coincident with performance of the services. • Milestones of customer-specific acceptance criteria affect the realizability (i.e., collectibility) of

the software-license fee.” 38 Such services would qualify for accounting as separate service element(s), assuming that they can be separately described, and separately priced (supported by VSOE), in accordance with AICPA SOP 97-2, ¶ 65. See AICPA SOP 97-2, ¶ 71.

17

Up-grades covered by PCS must not be separate, specifically identified products (i.e., with new functionality or features) that must be accounted for separately, when GA, delivered and accepted by customer.

Up-grades covered by PCS must not be unspecified rights to receive future

software products that should be accounted for on the subscription method.

Maintenance service fees should be recognized in accordance with the

pattern of activity, if discernable, or ratably over the term of the arrangement.

Vendor must have a record of having provided the subject PCS or

maintenance fee in order to support VSOE.

7. Regarding price adjustments, volume or activity credits and rebates or refunds.

Refunds arising from future sales of products, applied to outstanding receivables arising from prior arrangements may indicate that the price of the earlier arrangement was not fixed or determinable.

Price adjustments, volume or activity credits or rebates on “overlapping”

deals may indicate that the multiple elements should have been treated as one arrangement and the price(s) allocated accordingly.

The longer a receivable is outstanding – either by contractual term or in

practice – the more likely that subsequent price adjustments, volume or activity credits or rebates granted to that customer will be deemed to relate to the outstanding receivable balance and the arrangement giving rise to such receivable balance. This in turn may implicate whether the price of that arrangement actually was fixed or determinable.

Revenue Recognition Accounting Malefactions Accounting irregularities are distinguished from accounting errors in AICPA SAS No. 53, The Auditor’s Responsibility to Detect and Report Errors and Irregularities, as follows: “The term errors refers to unintentional misstatements or omissions of amounts or disclosures in financial statements. Errors may involve –

• Mistakes in gathering or processing accounting data from which financial statements are prepared.

• Incorrect accounting estimates arising from oversight or misinterpretation of facts.

18

• Mistakes in the application of accounting principles relating to amounts, classification, manner of presentation, or disclosure.”39

“The term irregularities refers to intentional misstatements or omissions of amounts or disclosures in financial statements. Irregularities include fraudulent financial reporting undertaken to render financial statements misleading, sometimes called management fraud …. Irregularities may involve acts such as the following:

• Manipulation, falsification, or alteration of accounting records or supporting documents from which financial statements are prepared.

• Misrepresentation or intentional omission of events, transactions, or other significant information.

• Intentional misapplication of accounting principles relating to amounts, classification, manner of presentation, or disclosure.”40

AICPA SAS No. 82, Consideration of Fraud in a Financial Statement Audit, states: “Fraud frequently involves the following: (a) pressure or an incentive to commit fraud and (b) a perceived opportunity to do so;” and, “Fraud may be concealed through falsified documentation, including forgery …. [and] Fraud also may be concealed through collusion among management, employees, or third parties.”41 Revenue recognition irregularities and financial usually involve both inclusive and exclusive fraud and acts of both commission and omission, as follows:

39 See AICPA SAS No. 53, ¶ 2 (AU§316). 40 See Id., at ¶ 3. 41 See AICPA SAS No. 82, ¶¶ 6-8 (AU§316, amended)

In Books and Records Legal and Economic Substance

Com

mission

Om

ission

1. False entries 2. Misstated contracts 3. Back-dating 4. Misrepresentations 5. Misapplication of

GAAP

1. Side Letters 2. Extra-contractual

promises 3. Actual dates, true

acceptance criteria, real rights and obligations

1. Overstated revenues 2. Mis-timing of recognition 3. Overstated receivables 4. Revenue not yet realizable 5. Mis-reported revenues and

earnings and trends

1. Remaining obligations 2. Material facts regarding the

arrangement 3. Allowances for returns 4. Contingencies 5. Violations of GAAP

19

Any time that a material amount of revenue intentionally is recognized when (a) the revenue is fictitious, (b) the timing of recognition is improper, (c) the amount being recognized has been improperly computed or estimated, and/or (d) GAAP has been misapplied, a false entry is recorded in the books and records of the entity. Generally, the purpose of such false entry is to overstate revenue in the current accounting period, either by recording an amount that is not realizable (i.e., fictitious revenue and corresponding receivable) or by recognizing revenue before it has been earned. In support of such a fraud, one or more of the following acts of commission (e.g., falsified documents and misrepresentations) or omissions (e.g., failure to disclose true terms of the arrangement) usually occurs. Existence of Arrangement Either the timing of the arrangement is misrepresented or the fact that a contract actually exists is falsified, by:

Back-dating documents or use of “as of” effective dating of documents.

Through collusion, arranging with a counter-party (i.e., customer representative) for a signed contract accompanied by an undisclosed: (a) side-letter providing cancellation rights to the buyer; (b) side-letter, contract amendment or other extra-contractual agreement providing executory contract contingencies, such as board approval, right of refusal by executive officers, or acceptance terms; or (c) “trial periods” or other contingencies affecting whether any arrangement actually is binding on the customer.

Carefully examine, with reasonable skepticism, all contracts received on or around period-end. Look for evidence contradicting contract dating, such as fax transmission dates, dating of accompanying correspondence, implausible sequence of events (e.g., shipping date, date of purchase order or invoice date vis-à-vis contract date), absence of prior contract negotiating history (i.e., “nick-of-time” and “out-of-the-blue” last minute contracts. Consider confirming with counter-party’s CFO, General Counsel, Controller, Chief Information Officer (“CIO”) and/or Purchasing Agent the terms and execution date of the arrangement.

Consider confirming nature and terms of arrangement with someone other (and preferably senior to) the counter-party signatory to the arrangement. Specifically inquire of counter-party and seller’s representative about existence of any undisclosed side-letters, contract amendments, or oral promises. Include language in all contracts prohibiting amendment by side-letter or extra-contractual agreement. Investigate the reason for any contractual provisions that grant abnormally long payment terms, or appear to allow cancellation, or that create right of return.

20

Improper period-end cut-off regarding: (a) receipt of contracts as of the close of business on the period-end date; (b) execution of received contracts by authorized representative(s) of seller; (c) non-delivery of product(s), under the terms of the arrangement (e.g., FOB shipping point or FOB destination), on or before period-end; and (d) incongruence of contract dating, authority and terms with antecedent documents such as request for proposal (“RFP”), purchase orders, and customer correspondence.

Delivery and acceptance Any delivery other than to the customer should be suspect and subject to investigation. Delivery should be supported by customary evidence of shipment and receipt; where delivery is effected by hand (e.g., seller’s sales representative), in advance of the contract date, through freight forwarders, to third party warehouses, or to sites other than the customer’s regular place(s) of business – beware! And, also watch for:

Arrangements executed immediately in advance of, or closely preceding, introduction of new versions of products, in which the current versions of the product are shipped.

Unusual acceptance criteria and any acceptance criteria with time periods that

carry over period-end.

Last minute, faxed, contracts or “letters of intent,” or arrangements drawn-up on non-standard forms should raise a heightened degree of professional skepticism. Arrangements must be executed by both parties, and last minute (or post-close) arrivals of customer-signed contracts beg the question, “How could seller have executed the final version of a contract not received from buyer until after the close of business on the period-end date?” Consider reviewing E-mail between seller representatives and buyer for support (or evidence to the contrary) of asserted timing of execution.

This naturally begs the question, “Why would the customer really want this soon-to-be obsolesced current version of the product(s)?” Often the answer is that the customer does not accept the current version because the terms of the arrangement, express or implied, within the contract or by side-letter, etc., provide for delivery of the new version when released. This in turn implicates acceptance, functionality and/or multiple element considerations before revenue may be recognized.

Any acceptance period that crosses over beyond the current accounting period may preclude revenue recognition in that accounting period. Unusual acceptance criteria (e.g., board approval, performance benchmarking, etc.) should be investigated.

21

Delivery to third-parties (e.g., value-added re-sellers, OEM’s, etc.) where the contract ultimately calls for acceptance by an end-user customer.

Any “bill and hold” arrangement.

Anomalies in documentation of delivery. For example, customer’s purchase order states, “FOB destination,” while vendor’s invoice and shipping documents reads, “FOB our dock,” and the contract is silent – if delivery occurs at or very near period-end, this disagreement between terms may affect revenue recognition. Or, packing slips show items not included in the arrangement (e.g., earlier versions of product) and do not reflect specified items (e.g., product versions ordered, equipment and peripheral items, etc.) – this may indicate incomplete delivery, only partial shipment, and lack of customer acceptance.

Price fixed or determinable The quickest way to “un-fix” a price, as an inducement to the customer to close a deal, is the use of a side-letter or contract amendment. But, any such alteration of the contract terms, if manifested in the legal and accounting documents (and if known), usually would

Such arrangements implicate whether the transaction is, in fact, a consignment sale, or whether collectibility ultimately depends upon the intermediary receiving payment from the end-user, or whether acceptance actually has occurred.

Rarely are such arrangements supportable under the strict criteria applied by the SEC. In practice, even the most carefully negotiated and executed “bill and hold” arrangement can be challenged. The revenue recognition risks far exceed any benefits; and, if the customer absolutely insists (and the transaction makes economic sense), consignment method accounting always is an option.

Other anomalies may include out-of-sequence shipping records (where waybills, bills of lading, etc. dated after period-end have identifying numbers earlier in sequence than the subject order represented as shipped on or before period-end. Or, when period-end falls on a weekend or holiday, shipment of equipment of product is claimed even though the shipping department (or customer’s receiving dock) normally is closed. Also, when delivery is represented as having been completed, but later (i.e., after period-close) E-mail, fax and written correspondence present contradictory evidence, delivery – in full – should be confirmed with the customer (preferably someone other than the contract signatory.

22

preclude revenue recognition until the sales contingency expired (or the terms of FASB SFAS No. 48, ¶¶ 6-8 could be met). Revenue recognition accounting irregularities involving exclusive fraud occur when material facts are omitted from documentation of the arrangement, by use of concealed side-letters, concealed contract amendments, or – in certain circumstances – by making oral promises. Concealment may occur through: (a) use of “separate” contracts or amendments to contracts (where the modifying documents intentionally are kept separate from the subject transaction’s contract documentation – in another file, or misrepresented as another arrangement); (b) use of undisclosed side-letters; (c) execution of a superseding, concealed, contract with modified terms; or use of intentionally ambiguous (or complex) terms, subject to differing interpretation, in the subject contract. In almost all cases, some degree of collusion exists on the part of the customer representative (negotiator and/or signatory), who has bargained for the contractual contingency. Typically, such contingencies involve one or more of the following:

Cancellation rights. In the matter of HBO & Company, one such concealed side-letter granting a right of cancellation was negotiated with a hospital operated by an order of nuns (raising the question, “Who can you trust these days?”). Cancellation rights may provide a “free trial” period, or a right of return if funding if not obtained or if board approval is not received. Such rights almost always indicate that the earnings process was not complete and the revenue was not yet (if ever) collectible.

Right of return (for product exchange or credit). In the case of sales to re-sellers

(e.g., wholesalers, distributors and retailers), rights of return are negotiated to obligate the seller to take back (either in exchange for new product or for credit) unsold goods. Such rights may be express or implied, and FASB SFAS No. 48 makes no distinction between the two forms. In the case of sales to end-users, rights of exchange for products of the same kind (e.g., similar functionality, same price) are not treated as rights of return, under FASB SFAS No. 48, ¶ 3. Similarly, platform transfer rights granted to end-users also may qualify as

Obviously, look for any such terms stated in the contract. Under both AICPA SOP 97-2 and SAB No. 101, fees from licenses that contain cancellation clauses are neither fixed nor determinable and revenue may not be recognized until the contingency expires. (AICPA SOP 97-2, ¶¶ 32-33 does provide for a possible exception in the circumstance of “fiscal funding clauses” often contained in contracts with government units). No internal control can be entirely effective in preventing a determined agent, officer or employee of a company from executing such a sales contingency and then concealing it. However, a regular program of confirming arrangement terms (particularly, confirming the absence of any cancellation clauses or any other rights of return not stated in the contract) can serve as a significant deterrent and can help to identify instances in which otherwise undisclosed sales contingencies do exist.

23

“exchanges” and not require accounting treatment as rights of return under FAS SFAS No. 48. However, rights to receive partial refund for undelivered products (either not currently GA or based upon arrangements to deliver in the future unspecified products) and rights to return (or receive partial credit for) product based upon “performance” clauses or other contractual contingencies are “rights of return” that fall within the ambit of FASB SFAS No. 48. Implied rights of return are, at once, both easy and hard to conceal. Because no express obligation exists there may be no documentation. However, the existence of such implied rights and obligations usually manifests itself through the behavior of the parties – as products are returned and/or credits are taken. Concealed express rights of return usually are created by side-letter or undisclosed contract amendment. As with other concealed contingencies, no internal control system can offer absolute assurance that concealment of sales contingencies will be prevented or detected.

Pricing involving volume credits, allocation among multiple products and other arrangements in which “fixed” payments may be allocated among various products. In arrangements involving products to be delivered, where such products involve different functionality or features, AICPA SOP 97-2, ¶ 46 requires that a portion of the arrangement fee should be allocated to the undelivered products. In arrangements in which the customer may allocate the arrangement fee to acquire different products (with different pricing and functionality), revenue may not be recognized until the amounts of such allocation are determinable. Accounting irregularities in this area most often involve attempts to misrepresent the arrangement so that elements to be delivered in the future are undervalued (thus inflating the amount of the arrangement qualifying for immediate revenue recognition)

Regular monitoring of collection, credits and returns activities (“looking-back,” post-sale, to determine if the amounts recorded were, in fact, realized) can identify the existence of implied or concealed express rights of return. Also, a regular program of confirming customers’ understanding of their arrangements – as to rights of return or any other contingencies – can serve as both a deterrent and a method of detection.

Front-loaded arrangements are easier to detect than to measure. VSOE must be credible and, regardless of contractually-stated prices, AICPA SOP 97-2, ¶ 10 states that: “Vendor-specific objective evidence of fair value [i.e., fair saleable value] is limited to the following:

• The price charged when the same element is sold separately • For an element not yet being sold separately, the price established

by management having relevant authority; it must be probable that the price, once established, will not change before the separate introduction of the product into the marketplace.”

24

Multiple-element arrangements (involving products and services). Again, the arrangement fee must be fixed or determinable and it must be allocable to the respective elements based upon VSOE supporting the fair values of such elements. Accounting irregularities (or, for that matter, errors) typically involve improper measurement and allocation of fair values among the elements in the arrangement – in order to front-load revenue. This in turn usually involves understating elements requiring deferral or accretion ratably over the term of the arrangement and overstating elements otherwise qualifying for immediate revenue recognition.

Realizability (i.e., collectibility) Revenue recognition accounting irregularities involving only timing improprieties may not always be detected by review of collections and receivables status (e.g., aging), especially if the irregularities are isolated and few. But, where the accounting irregularities involve sales contingencies, rights of return or credit, etc., such terms may lead to subsequent cancellation, credit issued against the receivable balance or return of amounts already collected. Or, the account receivable arising from the transaction simply grows older and older and never is collected. Eventually, such uncollectible receivables require allowance for doubtful accounts and, finally, write-off. Revenue also may be recognized improperly (or prematurely) for sales to customers that are not creditworthy (e.g., new enterprises or enterprises in rapidly changing and highly competitive industries, under-capitalized entities, companies with no, or poor, credit histories, etc.). Warning signs include:

Increased days’ sales outstanding (“DSO”), aging of receivables and allowances for doubtful accounts. If a vendors normal customer base is composed of well-established, steady, and financially sound customers, something is wrong. Such an adverse trend in DSO or aged receivables may indicate that the sales really were not earned or realizability (i.e., collectibility) was contingent on some future events that have not (or never) occurred.

There is no substitute for in-depth knowledge of: the products and their functionality; service elements and their nature, activities and obligations; pricing history; methods used to value products and services; and, pricing decisions to be made regarding products not yet delivered or GA. Pricing standards, based upon fair values supported by competent VSOE, should be developed; and any incongruities between such standards and prices stated in contracts (or the fair values used to allocate arrangement fees among such elements) should be investigated.

Study DSO and receivables trends carefully, and “drill-down” to find what accounts are causing the problem – and why.

25

Unusual credits. Receivables reduced by large or unusual credits, or accounts where long past-due balances suddenly are reduced should be investigated.

“Lapping” of payments or mis-applied payments. Payments made against current receivables may be mis-applied to reduce past-due balances, thus distorting DSO and aging statistics and masking the fact that older balances remain uncollectible.

Intervention in and corruption of confirmation of accounts receivables and

transaction terms with customers. Through collusion with customer representatives, misrepresentation of the terms and nature of arrangements or the amounts owed and conditions of payment can be obtained to deceive management, internal auditors or the company’s independent auditors.

Revenue Recognition - On the Qui Vive In order to be alert to potential revenue recognition accounting errors or irregularities, one must know what to look for and what questions to ask. The following list should be a starting point. Organizational

1. Who are the most “aggressive” (hard-charging, driven, etc.) sales and operational executives, management and key sales employees? Do you really know their business philosophy, culture, methods and what motivates them?

Such credits or changes in account balances long past due may indicate that an initially unrealizable sale and uncollectible receivable is being covered-up by additional accounting irregularities. Or, the initial sale may have contained cancellation clauses or other contingencies permitting the customer to avoid payment.

Other manipulation of the status of accounts receivables can include intervention and tampering with internal reports or write-off and re-creation of receivables designed to re-start the their aging and make the balances appear to be current.

Confirmations should be made on a “surprise” basis and strictly controlled. Also, confirmations should be addressed to, and followed-up with, persons other than the counter-party to the arrangements.

26

2. How are sales and revenue recognition linked to compensation? Will specific transactions be critical to individuals “making their numbers/”

3. Is there a permanent contract-review and audit function within then organization?

Is this function independent of the sales force and other operating parts of the business? Does this function have adequate resources (including legal and accounting personnel, access to all records, analytical programs, etc.) to be effective?

4. Does internal audit also examine: (a) controls, procedures and processes

surrounding the revenue recognition functions; (b) selected customer relationships and specific transactions; and (c) subsequent realization of sales amounts?

5. What is the tone at the top? Is that tone overly aggressive? Do senior management

and the directors properly and frequently communicate their insistence on adherence to high business and ethical standards and to compliance with GAAP Securities laws and SEC rules and regulations? Is the culture of the organization squarely aligned with such tone at the top?

6. Are there proper, well-designed and functioning compliance monitoring and

reporting systems in place. Are such systems designed to: (a) encourage participation and use; (b) provide for confidentiality and for due-process; (c) achieve appropriate follow-up; (d) enlist the aid of outside advisors where appropriate; and (e) report any significant matters to the appropriate levels within the organization (including the audit committee of the board of directors)?

Operational

7. Are accounting policies and procedures up-dated to conform to and comply with,

inter alia SAB No. 101, AICPA SOP 97-2, and any other relevant GAAP governing revenue recognition?

8. Are training programs designed to explain the accounting rules for revenue

recognition and educate management and employees regarding accounting rules and risks and more complex revenue recognition issues?

9. Are management and employees (particularly the sales force) required to

periodically: (a) confirm their understanding of company policies regarding revenue recognition, business ethics and compliance with GAAP, securities laws and SEC rules and regulations; (b) affirm their compliance with such policies; and (c) report any instances of the use of side-letters or any departures from contracting and sales guidelines?

27

Contracting

10. Are all (or a representative sample of) significant contracts executed on or around each period-end subject to careful scrutiny, and to confirmation with customers as to terms, delivery and acceptance, the absence of any contingencies, etc.?

11. Are contracts, amendments, side-letters and all related documentation maintained

together to facilitate review?

12. Do contracts contain language prohibiting use of side-letters unless such modifications are authorized and signed by specifically designated individuals?

13. Are levels of authority established to review and approve significant revenue

contracts? Are such individuals knowledgeable about the nature, terms and possible elements of such arrangements?

Accounting

14. What contracts have arrived in the final days of the period? Have these arrangements been scrutinized?

15. Have contracts been reviewed for execution, timing of execution, and any

apparent sales contingencies, cancellation clause, etc.?

16. Have significant arrangements been confirmed with customers?

17. Have the separate contract elements been identified and separately described?

18. Has VSOE supporting respective fair valuation of contract elements been validated?

19. Does affirmative evidence of realizability (i.e., collectibility) exist?

20. Stepping back, does the deal make sense and pass the “reasonableness test” for

accounting applied in recognizing revenue?