rev. 16.1 finc 655, week 1 1 - pepperdine...

TRANSCRIPT

FINC 655, week 1 1

FINC 655 Managerial Finance

Week 1–Ratio analysis, financial forecasting and use of financial

statements

© Michael D. Kinsman, Ph.D.

Rev. 16.1 FINC 655, week 1 1

FINC 655, week 1

Welcome to FINC 655, Managerial Finance!

• This week, we will– Introduce the class– Introduce each of us– Discuss what you learned in accounting– Talk about and use ratio analysis– Discuss and use forecasting

Rev. 16.1 2

FINC 655, week 1

Who is the professor?• Dr. Michael Kinsman goes by the name

Mike. If you’ve gotta, Dr. Kinsman is fine.– Ph.D. in finance, Stanford University.– MBA in finance, Stanford University.– BA, math and econ, Claremont Men’s College

(now Claremont McKenna College)

Rev. 16.1 3

FINC 655, week 1 2

FINC 655, week 1

Who is the professor?– Practicing CPA in Laguna Beach.– At Pepperdine since 1975.– Formerly at UCI for 12 years.– Former systems programmer for General

Electric.– Former manager at Pacific Telephone.

Rev. 16.1 4

FINC 655, week 1

How can I reach him?

• In person: Before class here or at my office which is on the fourth floor in the far corner. I tend to get there about 45 minutes before class.

• By e-mail: [email protected]• By phone: (949) 223-2533.

Rev. 16.1 5

FINC 655, week 1

Why do you teach?

• I teach because I love it. I enjoy working with students and helping them learn. I really get excited as you can do new things. More than that, when you have become a success, and that happens a lot, I get pretty happy seeing your name in the paper.

Rev. 16.1 6

FINC 655, week 1 3

FINC 655, week 1

What is the book for the class?• Brigham, et. al, Financial Management:

Theory and Practice, current edition. This is a standard text. It is generally a good read, with a few problem spots. It’s the best of what’s out there, in my view.

Rev. 16.1 7

FINC 655, week 1

Materials for the class• Cases which I will supply, like the one you

got for tonight.• These cases are “Harvard-type” cases–

many are used in classrooms there, at Stanford, and nationally.

• Cases have no “right” answers, usually.• Cases are not easy–they are filled with

ambiguity.

Rev. 16.1 8

FINC 655, week 1

Do I really have to do the cases?

• Yes, you do. Cases are hard. I’ll be the first to admit that. And they are the closest to real life situations I can give you without it costing you a lot of money.

• You may believe you are the only person who “doesn’t get a case.” You believe wrong.

• Work in a group of 3 to 5 people. It helps.Rev. 16.1 9

FINC 655, week 1 4

FINC 655, week 1

Materials for the class• A financial calculator. As you saw in my

letter to you, that’s a requirement of the class.

• Access to your Pepperdine email account.

Rev. 16.1 10

FINC 655, week 1

Who are you?

• Name?• Undergraduate school and major?• Where do you work?• What do you do there?

Rev. 16.1 11

FINC 655, week 1

Please fill out a 3x5 card

• Use the landscape direction, please!• At the top right corner, FINC655• Name• Address• Office phone• Home phone• E-mail address

(If any of this is secret, write secret and I won’t divulge it. Else, I’ll show it to anyone in my classes who asks for you.)

Rev. 16.1 12

FINC 655, week 1 5

FINC 655, week 1

E-mail address

• If you did not get an email from me, please e-mail me your e-mail address. Do not make the assumption I will copy it from your card. I will not. Then you will not get “the secret stuff” I send out.

• You want to get “the secret stuff!”

Rev. 16.1 13

FINC 655, week 1

Syllabus• Each week is listed separately. • The syllabus is also on the Web. Go to: <http://luna.pepperdine.edu/faculty/mkinsman/mdkhome1.html>

to find it. • If there are updates, I will put them on the web. You

should also download class notes each week.

Rev. 16.1 14

FINC 655, week 1

A helpful hint on notetaking

• Also on the web pages (go back to my home page) is Taking Notes in Graduate School. It might be useful.

• Some profs won’t allow you to tape record classes. I encourage it, although you may want to use the oral notes instead. We’ll talk about them later. It lets you hear what’s going on again. And a lot is going on in this class.Rev. 16.1 15

FINC 655, week 1 6

FINC 655, week 1

How will I be graded?• There’s a handout at the back of your syllabus

that shows:– Exam 1 at week 5: About 25% of the total points.– Exam 2 at week 10: About 25% of the total points.– Written class project at week 11: 15% of the total

points.– Oral class project (week 11 or 12): 10% of the total

points.– Final exam: About 25% of the total points.

Rev. 16.1 16

FINC 655, week 1

Participation

• Participation will count. At the end of class, I will figure out the “participators” and the “non-participators.” That will affect your grade by at most one sign, and only for a couple of you in the class–see the handout for details.

Rev. 16.1 17

FINC 655, week 1

This class runs on your questions!

• I make the assumption that you understand the material unless you indicate otherwise. It is really important that you ask questions as you have them.

• I admit it. I can’t teach. I can only help you learn. Let me help you!

Rev. 16.1 18

FINC 655, week 1 7

FINC 655, week 1

You didn’t cover it on the night it was assigned!

• There are times that I will not cover the assigned reading on the night it was assigned. I will cover that assigned reading, but sometimes I “get out of phase.”

• There are usually good reasons for that, though I try to stay in phase.

• Bear with me. We’ll cover it all, and, honest, there are good reasons for being out of sync. It isn’t “just bad planning!”

Rev. 16.1 19

FINC 655, week 1

Weird stuff• I do weird stuff. For example:

– I really care if you get the content of the class.– I start the class on time right at 6:00. I really

appreciate your efforts to be here on time.– I call breaks for weird times like 9 minutes.

Why? We all know that 10 minutes is 15. But 9 minutes is 9. When I call a 9 minute break, I start nine minutes later.

– I call on people who don’t have their hands raised.

Rev. 16.1 20

FINC 655, week 1

My expectations

• My expectation is that you are here to learn as much finance as you can, so that you can use that material in the world.

• I push people to learn. That’s off-putting for people who want me to be nice and let them sit in the back of the room and just take notes. But this is a participation class.

Rev. 16.1 21

FINC 655, week 1 8

FINC 655, week 1

What will you do in class?• I am going to ask you questions you don’t

know the answers to. And I’m going to expect you to try to answer.

• “Why? If I don’t know it, I don’t know it.”• You know from experience that there are

lots of things both of us don’t know. Trying to figure them out is what separates you as a manager from the people who won’t advance.

Rev. 16.1 22

FINC 655, week 1

I heard four people died last time you taught this class

• I don’t know how these rumors get started. It was only 2.

• Understand that what I am doing is trying to get you as far as you can go. Each of you is different. I try to accommodate those differences.

• If you think I’m picking on you more than others, let’s talk about it outside of class. Rev. 16.1 23

FINC 655, week 1

What’s finance all about?

• ??????????

Rev. 16.1 24

FINC 655, week 1 9

FINC 655, week 1

What’s finance all about?• Finance is the study of what assets are

worth.• Sure, that other stuff is important:

• We look at the stock and bond markets.• We manage cash.• We run companies.

But the reason we do all that is to increase the value of the company–to make the asset worth more. That’s the focus of the class.Rev. 16.1 25

FINC 655, week 1

Where does finance fit in?

• Finance is one of the social sciences

Social sciences

And is part of economics

Microeconomics Macroeconomics

Rev. 16.1 26

FINC 655, week 1

Where does finance fit in?

• Economics is divided into two halves:

Microeconomics is the study of pricing and resource allocation

Macroeconomics is the study of how the government screws up the economy, according to at least one local economist

Rev. 16.1 27

FINC 655, week 1 10

FINC 655, week 1

Where does finance fit in?

• Finance is a subset of economics

Finance is wholly contained in economics

As is accounting

Rev. 16.1 28

FINC 655, week 1

Finance, accounting and econ

• Finance and accounting use micro-economics to look at individual firms and their pricing and allocation issues.

• Finance and accounting use macro-economics because the economy as a whole affects firms, their reporting, and their methods of raising capital.

Rev. 16.1 29

FINC 655, week 1

How does finance tie to accounting?

• First, they are different subjects, but joined at the financial statements.

• Remember that the major financial statements are the balance sheet, the income statement, and the statement of cash flows.

Rev. 16.1 30

FINC 655, week 1 11

FINC 655, week 1

A balance sheet view of finance

Current Assets

Long term assets

Current liabilities

Long term liabilities

Equity

The balance sheet

Rev. 16.1 31

FINC 655, week 1

A balance sheet view of finance

Current assets

Long term assets

Current liabilities

Long term liabilities

Equity

The balance sheet

Current assets minus current liabilities is net working capital

Rev. 16.1 32

FINC 655, week 1

A balance sheet view of finance

Net working capital

Long term assets

Long term liabilities

Equity

The balance sheet

The investing decision(capital budgeting)

Decisions about working capital and solvencyThe capital

structure and dividend decisions

Rev. 16.1 33

FINC 655, week 1 12

FINC 655, week 1

We will study these sequentially

❶ First we will go back to the accounting roots that you set in a previous trimester.– This will include reading financial statements,

budgeting, and ratio analysis.❷ Then we will study capital budgeting.

– This will include present value analysis and decisions about buying assets.

Rev. 16.1 34

FINC 655, week 1

We will study these sequentially

❸ Then we will study capital structure and dividends– How do we raise the money to buy the projects

we want to do?❹ Then we will study working capital.

– How do we stay solvent? How do we run our business?

Rev. 16.1 35

FINC 655, week 1

We will study these sequentially

❺ Finally, we will study the financial markets in which the financial instruments a firm sells are traded.

Rev. 16.1 36

FINC 655, week 1 13

FINC 655, week 1

Goals of the firm

• What are the goals of the firm?– Maximize owner’s wealth is the goal we will

assume and work with.– Maximize manager’s security is often true.

Rev. 16.1 37

FINC 655, week 1

Goals of the firm

• In fact, the overall goal of a firm–and of you as you invest–should be to maximize value to the person who will receive that value.

• Although that sounds simple, often we anguish over how to accomplish that because our “crystal balls” are cloudy.

Rev. 16.1 38

FINC 655, week 1

Less than perfect certainty–�get used to it!

• Uncertainty is a fact of life in finance–we make estimates (guesses) about the future.

• There are some people who freeze when faced with uncertainty–much like a deer in the headlights on a county road.

• Like the deer, if you don’t make a decision you will be run over.

• You must estimate value in finance.Rev. 16.1 39

FINC 655, week 1 14

Howmuch

Howsoon

Howrisky

Valuedependson3things

$value

Rev. 16.1 FINC 655, week 1 40

“How much” is about cash flows–how much is each of your future cash flows (both in and out) from the project. We love getting cash! We hate paying it.

Rev. 16.1 FINC 655, week 1 41

Howmuch

Howsoon

Howrisky

Valuedependson

$value

“How soon” asks when the cash flows occur–we like getting money soon,

and paying it out later.Rev. 16.1 FINC 655, week 1 42

Howmuch

Howsoon

Howrisky

Valuedependson

$value

FINC 655, week 1 15

“How much” and “How soon” come from our budgeted cash flows–they are estimates

(guesses) about the future of our flows. You studied this in accounting, and we will

discuss it again here in finance.Rev. 16.1 FINC 655, week 1 43

“How risky” is a measure of certainty–if we are very sure of getting the money on time,

our project is not too risky. If there’s a lot of uncertainty, we must recognize that.

Rev. 16.1 FINC 655, week 1 44

“How risky” comes from a comparison of our project to other projects available

to us and to the market.Rev. 16.1 FINC 655, week 1 45

FINC 655, week 1 16

“How risky” is reflected in the cost of capital (interest rate) we use in evaluating the

project. This is a subject we will discuss in several parts of this course.

Rev. 16.1 FINC 655, week 1 46

FINC 655, week 1

Remember that in the �preceding slides, we are �talking about cash flows �

• And more particularly, we are talking about after-tax cash flows–what you get to spend.

• Some things in a project use cash, such as investments in equipment and other balance sheet accounts like increasing receivables and inventory.

Rev. 16.1 47

FINC 655, week 1

Remember that in the �preceding slides, we are �talking about cash flows �

• Some things in a project provide cash, such as dis-investments in equipment, new loans, and other balance sheet accounts like increasing accounts payable.

Rev. 16.1 48

FINC 655, week 1 17

FINC 655, week 1

Remember that in the �preceding slides, we are �talking about cash flows �

• Obviously, if receivables or inventory go down, we have turned them into cash. If accounts payable goes down, we used cash to pay them off. If loans go down, we used cash to pay them off.

Rev. 16.1 49

FINC 655, week 1

The other source of cash flow• Finally, your after tax income is a cash flow

to you–you (or your company) get to keep the income after paying taxes.

• However, tax based income may be different from that reported on the firm’s financial statements.

• Which leads us to. . .

Rev. 16.1 50

FINC 655, week 1

Something your accounting prof may have forgotten to teach you!• I frequently ask students what they learned

in accounting, and among the things they learned was “depreciation.”

Rev. 16.1 51

FINC 655, week 1 18

FINC 655, week 1

Something your accounting prof may have forgotten to teach you!

• In finance, since we are interested primarily in after tax cash flows, we don’t care about “book” depreciation much, even though that is the basis of financial statement reported income.

• Instead, we use tax depreciation–MACRS–to (re)calculate the company’s tax liability, and therefore its after tax cash flow from income.

Rev. 16.1 52

FINC 655, week 1

MACRS (tax) depreciationYear 3 year 5 year 7 year

1 33.33 20.00 14.29 2 44.45 32.00 24.49 3 14.81 19.20 17.49 4 7.41 11.52 12.49 5 11.52 8.93 6 5.76 8.92 7 8.93 8 4.46

3 year property: R&D equipment and certain animals5 year property: Wheeled vehicles (with limits); computers; electronic office equipment, telephone central office equipment7 year property: Property not otherwise defined; office furniture.27.5 year (330 month) property (SL monthly): Residential real property39 year (468 month) property (SL monthly): Non-residential real property

Rev. 16.1 53

FINC 655, week 1

To use MACRS

• For 3, 5 and 7 year property, take the cost of the item (for example, a $5,000 computer system).

• Figure out what number of years it is (5 in the case of a computer).

• Multiply the cost times the annual factor in the table (20% x $5,000) to get your depreciation for that year ($1,000).

• It’s that easy!Rev. 16.1 54

FINC 655, week 1 19

FINC 655, week 1

To use MACRS• For 330 month and 468 month property, divide

the life in months into the depreciable basis of the property. That gives you the depreciation for one month.

• Multiply the depreciation for one month times the number of months you have held the asset this year. That is your depreciation for this year.

• Remember, land is not depreciable.

Rev. 16.1 55

FINC 655, week 1

Skipped material• In your book, there is some very good

introductory material on pages 11 through the end of chapter 1.

• We will cover that material in detail in later parts of the course, when we will specifically discuss trading in securities and types of securities.

• For now, please do read the material as general background. Recognize that it is general in nature, and we will look in more depth later.

Rev. 16.1 56

FINC 655, week 1

Skipped material• Recognize, also, that the authors of the book have

points of view that they express. Others have different views on the politics of the economy and markets.

• Their view may paint a picture that is different from the one you believe is “true and appropriate.”

Rev. 16.1 57

FINC 655, week 1 20

FINC 655, week 1

Skipped material• Do not be off-put if you disagree with the

authors’ points of view. Think critically about what they say, whether you agree or disagree with what they say.

• Consider their viewpoints, do your own research, and come to your own conclusions.

• That is, after all, both your right and also something very important to do as you move up in management.

Rev. 16.1 58

FINC 655, week 1

Ratio analysis

• When you go to the doctor, the doctor takes your blood pressure and checks certain other vital signs to check your physical health.

• We are going to check the “money pressure” and certain other vital signs of companies to check their fiscal health.

Rev. 16.1 59

FINC 655, week 1

What are we looking for?

• Like the doctor, we are looking for unexplained difference.

• Explainable differences may be just fine–our management may simply be managing differently or there is another difference.

• Unexplained difference gives us a list of potential problems.

Rev. 16.1 60

FINC 655, week 1 21

FINC 655, week 1

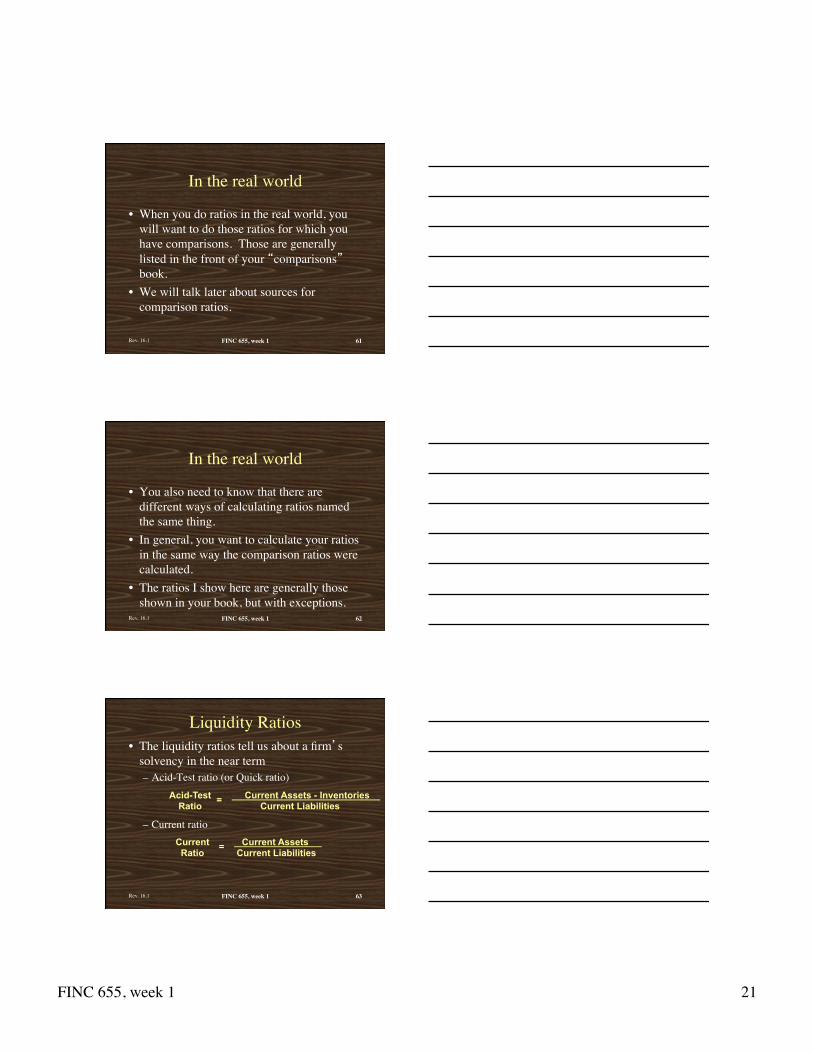

In the real world

• When you do ratios in the real world, you will want to do those ratios for which you have comparisons. Those are generally listed in the front of your “comparisons” book.

• We will talk later about sources for comparison ratios.

Rev. 16.1 61

FINC 655, week 1

In the real world

• You also need to know that there are different ways of calculating ratios named the same thing.

• In general, you want to calculate your ratios in the same way the comparison ratios were calculated.

• The ratios I show here are generally those shown in your book, but with exceptions.

Rev. 16.1 62

FINC 655, week 1

Liquidity Ratios• The liquidity ratios tell us about a firm’s

solvency in the near term– Acid-Test ratio (or Quick ratio)

– Current ratio

Current Assets - Inventories Current Liabilities = Acid-Test

Ratio

Current Assets Current Liabilities = Current

Ratio

Rev. 16.1 63

FINC 655, week 1 22

FINC 655, week 1

Asset management ratios

• Inventory turnover ratio Inventory turnover = Sales/Year end inventories

• Days’ Sales Outstanding (Average Collection Period)

Days’ Accounts Receivable Sales = Outstanding Net Sales

* 365

Rev. 16.1 64

FINC 655, week 1

Asset management ratios

• Fixed asset turnover ratio

• Total asset turnover ratio

Fixed asset turnover ratio

= Sales

Net fixed assets

Total asset turnover ratio

= Sales

Total assets Rev. 16.1 65

FINC 655, week 1

Another asset management ratio

• Days’ Stock on Hand Days’ Ending Inventory Stock = on Hand Cost of Goods Sold

* 365

Rev. 16.1 66

FINC 655, week 1 23

FINC 655, week 1

Long-Term Risk and Capital Structure

• Debt Ratio

• Times Interest Earned

Total Liabilities = Total Assets

Debt Ratio

Times Income Before Interest and Taxes Interest = Earned Interest Expense

Rev. 16.1 67

FINC 655, week 1

Profitability Ratios

• Profit Margin on sales

• Return on total assets

Profit margin on sales

Net Income Net revenues =

Return on Total Assets

Net Income Total assets =

Rev. 16.1 68

FINC 655, week 1

Profitability Ratios

• Return on Common EquityReturn on Common Equity

Net Income - Preferred Dividends Common Equity =

Rev. 16.1 69

FINC 655, week 1 24

FINC 655, week 1

Market value ratios

• Price Earnings Ratio

• Dividend yield ratio

• Market to book ratio

Price/Earnings Ratio

Market Price Per Share Earnings Per Share =

Dividend Yield

Annual Dividends Per Share Market Price Per Share =

Market/Book Ratio

Market Price Per Share Book Value Per Share =

Rev. 16.1 70

FINC 655, week 1

Additional analysis

• In addition to the traditional ratio analysis, we may want to do common sized income statements or balance sheets or trend or other analysis of a company’s financial statements.

Rev. 16.1 71

FINC 655, week 1

Common-Size Comparative Statements

• Common-size comparative statements use percentages to express the relationship of individual components to a total.– Net sales is usually expressed as 100% on the

income statement.– Total assets is usually expressed as 100% on

the balance sheet.

Rev. 16.1 72

FINC 655, week 1 25

FINC 655, week 1

Trend Analysis

The purpose of trend analysis is to identify a pattern or trend over a

long time span - usually five or more years.

Rev. 16.1 73

FINC 655, week 1

Trend Analysis

100

110

120

130

140

150

19X1 19X2 19X3 19X4 19X5

Sales

Often, trend percentages are used to construct a graph so we can see the trend

over time.

Rev. 16.1 74

FINC 655, week 1

So what?

• Once we have done our analyses, we are still left with the “so what” question.

• A company must be compared to something before we can make judgments about it.

• Comparisons may be subjective or objective.

Rev. 16.1 75

FINC 655, week 1 26

FINC 655, week 1

Subjective Standards �of Comparison

• Acquired from past experiences: – In this company, sales per square foot are never

below $300!

Rev. 16.1 76

FINC 655, week 1

Subjective Standards �of Comparison

• Acquired from past experiences.• Rule-of-thumb standards:

– 3 is a good current ratio.

Rev. 16.1 77

FINC 655, week 1

Objective Standards �of Comparison

• Published standards– Ratios and turnovers of competing companies in

the same industry:• Our competitor has six times turns on his financial

statement. Why can’t we!

Rev. 16.1 78

FINC 655, week 1 27

FINC 655, week 1

Objective Standards �of Comparison

• Published standards– Ratios and turnovers of competing companies in

the same industry.– Published ratios:

• Our trade association shows that firms like us spend 13 percent on R&D.

Rev. 16.1 79

FINC 655, week 1

Objective Standards �of Comparison

• Published standards– Ratios and turnovers of competing companies in

the same industry.– Published ratios.– Standards or average ratios and turnovers for the

industry: • I went to the library (or the WWW) and checked out the

industry standards. They were...Rev. 16.1 80

FINC 655, week 1

Forecasting

• Why do we bother to forecast?– So that we can tell about the future.– So that we can turn the future to our advantage.– So we can avoid problems in the future.

Rev. 16.1 81

FINC 655, week 1 28

FINC 655, week 1

How do we forecast?

• There are lots of different ways to forecast.– We can do “percent of sales” increases.– We can do specific pro-forma statement

forecasts.– We can use regression analysis or other

statistical tools for forecasting.

Rev. 16.1 82

FINC 655, week 1

Percent of sales example

• Suppose a company anticipates that its sales will increase from $500,000 this year to $800,000 next.

• The firm’s balance sheet is shown on the next slide.

• The firm is using all assets to capacity.• What amount of new capital will it have to

raise to support this increase in sales?Rev. 16.1 83

FINC 655, week 1

Percent of sales exampleAmount Pe r cen t Amount Pe r cen t

($ k) of sales ($ k) of salesCash 10 0.02 Accounts payable 50 0.10 Accounts receivable 85 0.17 Accrued taxes 25 0.05 Inventories 100 0.20 Mortgage bonds 70 0.14 Fixed assets 150 0.30 Common stock 100 0.20

Retained earnings 100 0.20

Total 345 0.69 345 0.69

Each item in the balance sheet was divided by $500,000 to get the percent of sales.

Rev. 16.1 84

FINC 655, week 1 29

FINC 655, week 1

What balance sheet items will automatically increase as sales

increases?• Assets: We would expect all the assets to

increase automatically–we are, after all, at capacity and are dramatically increasing sales. We need 69¢ of new assets per dollar of sales increase.

Rev. 16.1 85

FINC 655, week 1

What balance sheet items will automatically increase as sales

increases?• Liabilities: We would not expect the bank

to come to us to offer more money; nor will our shareholders. Only the first two are automatic increases. We will get 15¢ per dollar of sales increase from our vendors.

Rev. 16.1 86

FINC 655, week 1

Our financial need

• The financial need of the company–the amount of new capital it will have to raise–is

(Increase in assets - Increase in liabilities)* Increase in sales = Need =

(69¢ - 15¢) * $300,000 = $162,000• We need to find $162,000 in new financing to

be able to operate at the level projected.

Rev. 16.1 87

FINC 655, week 1 30

FINC 655, week 1

Are there limits to the analysis?

• Sure. We haven’t factored in any management decision making. For example, we might operate a second shift; or change our level of receivables or payable; or decide that cash is too high or too low. Each of those needs to be considered in this example.

• However, this is a good first cut at the need.Rev. 16.1 88

FINC 655, week 1

Forecasting

• We will do significantly more in the area of forecasting, including some fairly sophisticated forecasts, in future classes.

• For now, you have one method for doing a forecast “first cut.”

Rev. 16.1 89

FINC 655, week 1

John’s Really Terrible Day

• Your job is to tell me what firm is what, and why you came to that conclusion!

Rev. 16.1 90

FINC 655, week 1 31

That finishes what we’re going to do tonight.

Thanks for your patience. We will review some of this next week. Come with questions, and homework!

Rev. 16.1 FINC 655, week 1 91