retirement and investing b = c + i - e. overview basic retirement math benefits = contributions +...

TRANSCRIPT

RETIREMENT AND INVESTING

B = C + I - E

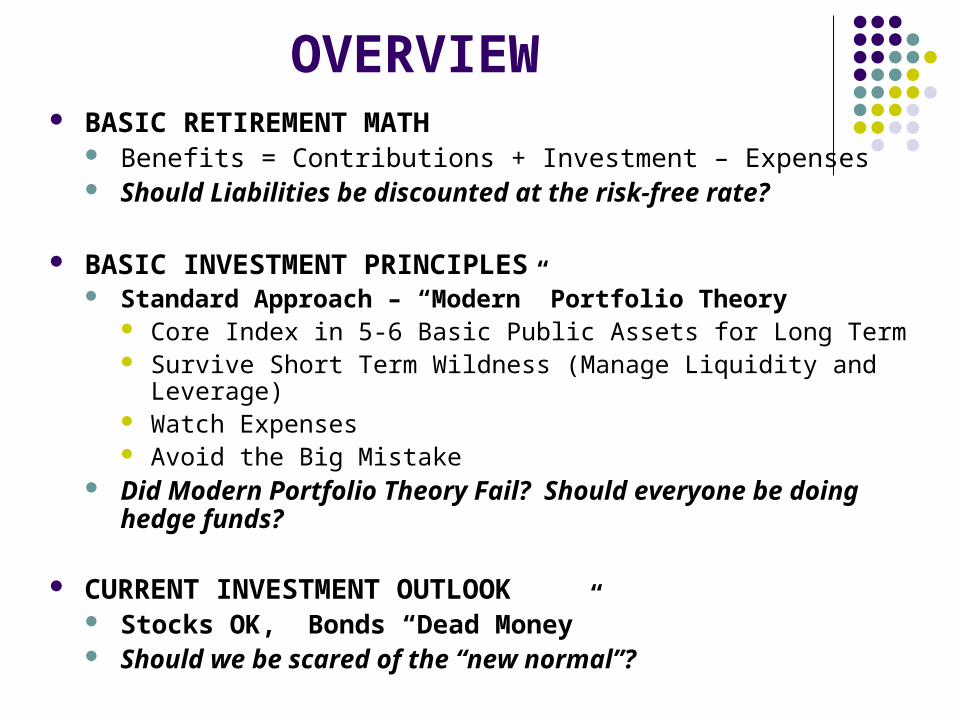

OVERVIEW BASIC RETIREMENT MATH

Benefits = Contributions + Investment – Expenses Should Liabilities be discounted at the risk-free rate?

BASIC INVESTMENT PRINCIPLES Standard Approach – “Modern” Portfolio Theory

Core Index in 5-6 Basic Public Assets for Long Term Survive Short Term Wildness (Manage Liquidity and Leverage) Watch Expenses Avoid the Big Mistake

Did Modern Portfolio Theory Fail? Should everyone be doing hedge funds?

CURRENT INVESTMENT OUTLOOK Stocks OK, Bonds “Dead Money” Should we be scared of the “new normal”?

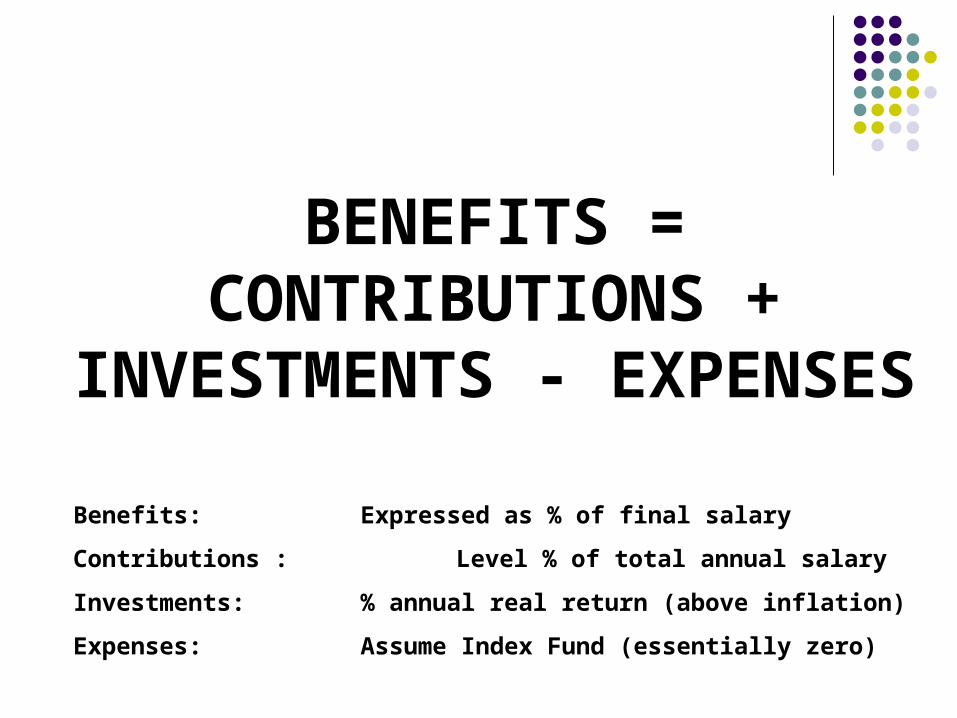

BENEFITS = CONTRIBUTIONS +

INVESTMENTS - EXPENSES

Benefits: Expressed as % of final salary

Contributions : Level % of total annual salary

Investments: % annual real return (above inflation)

Expenses: Assume Index Fund (essentially zero)

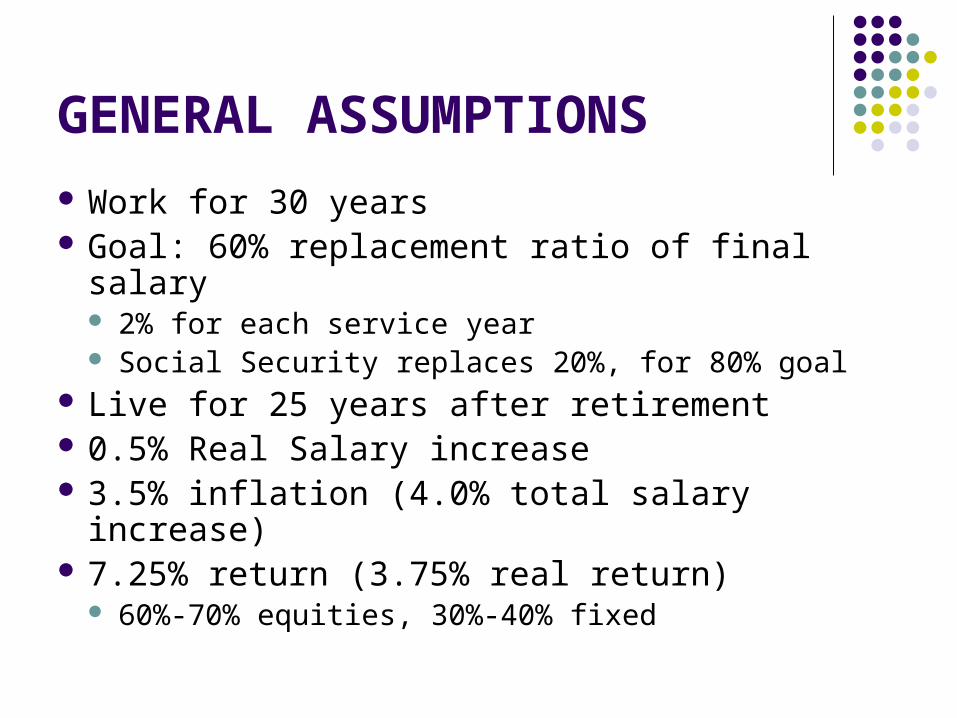

GENERAL ASSUMPTIONS

Work for 30 years Goal: 60% replacement ratio of final salary

2% for each service year Social Security replaces 20%, for 80% goal

Live for 25 years after retirement 0.5% Real Salary increase 3.5% inflation (4.0% total salary increase) 7.25% return (3.75% real return)

60%-70% equities, 30%-40% fixed

AMOUNTS NEEDED FOR EACH $100 OF ENDING SALARY100% Replacement, No inflation, No real salary increase, No COLA

30/30 $3,000

30/25 $2,500

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

-29

-27

-25

-23

-21

-19

-17

-15

-13

-11 -9 -7 -5 -3 -1 1 3 5 7 9 11 13 15 17 19 21 23 25 27 29

Years from retirement

Cu

mu

lati

ve $

nee

ded

in e

nd

ing

yea

r $

30/30 30/25 Level % of Total Salary

50%

45.5%

B = C BENEFITS = CONTRIBUTIONS

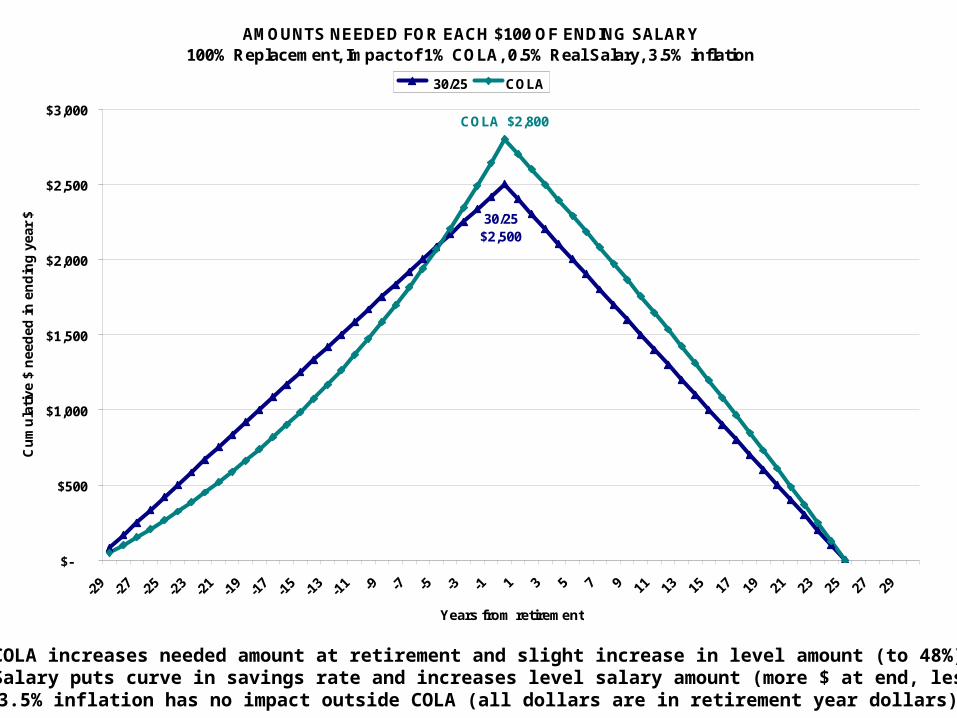

1% COLA increases needed amount at retirement and slight increase in level amount (to 48%). 0.5% Real Salary puts curve in savings rate and increases level salary amount (more $ at end, less $ early)

3.5% inflation has no impact outside COLA (all dollars are in retirement year dollars)

AMOUNTS NEEDED FOR EACH $100 OF ENDING SALARY100% Replacement, Impact of 1% COLA, 0.5% Real Salary, 3.5% inflation

30/25 $2,500

COLA $2,800

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

-29

-27

-25

-23

-21

-19

-17

-15

-13

-11 -9 -7 -5 -3 -1 1 3 5 7 9 11 13 15 17 19 21 23 25 27 29

Years from retirement

Cu

mu

lati

ve $

nee

ded

in e

nd

ing

ye

ar $

30/25 COLA Level % of Total Salary

61%

45.5%

B = C ASSUME NO INVESTMENTS BENEFITS = CONTRIBUTIONSDropping 100% replacement to 60% brings savings rate back to 50%

AMOUNTS NEEDED FOR EACH $100 OF ENDING SALARY3.5% inflation, 0.5% real salary increase, 1% COLA

60% replacement $1,800

100% replacement $2,800

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

-29

-27

-25

-23

-21

-19

-17

-15

-13

-11 -9 -7 -5 -3 -1 1 3 5 7 9 11 13 15 17 19 21 23 25

Years from retirement

Cu

mu

lati

ve $

nee

ded

in e

nd

ing

yea

r $

Level % of Total Salary

50%

61%

B = C + I ASSUME 7.25% NOMINAL RETURN 3.75% REAL RETURN

AMOUNTS NEEDED FOR EACH $100 OF ENDING SALARY3.5% inflation, 0.5% real salary increase, 1% COLA

3.75% real $838

60% replacement $1,800

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

-29

-27

-25

-23

-21

-19

-17

-15

-13

-11 -9 -7 -5 -3 -1 1 3 5 7 9 11 13 15 17 19 21 23 25

Years from retirement

Cu

mu

lati

ve $

nee

ded

in e

nd

ing

yea

r $

Level % of Total Salary

14%

50%

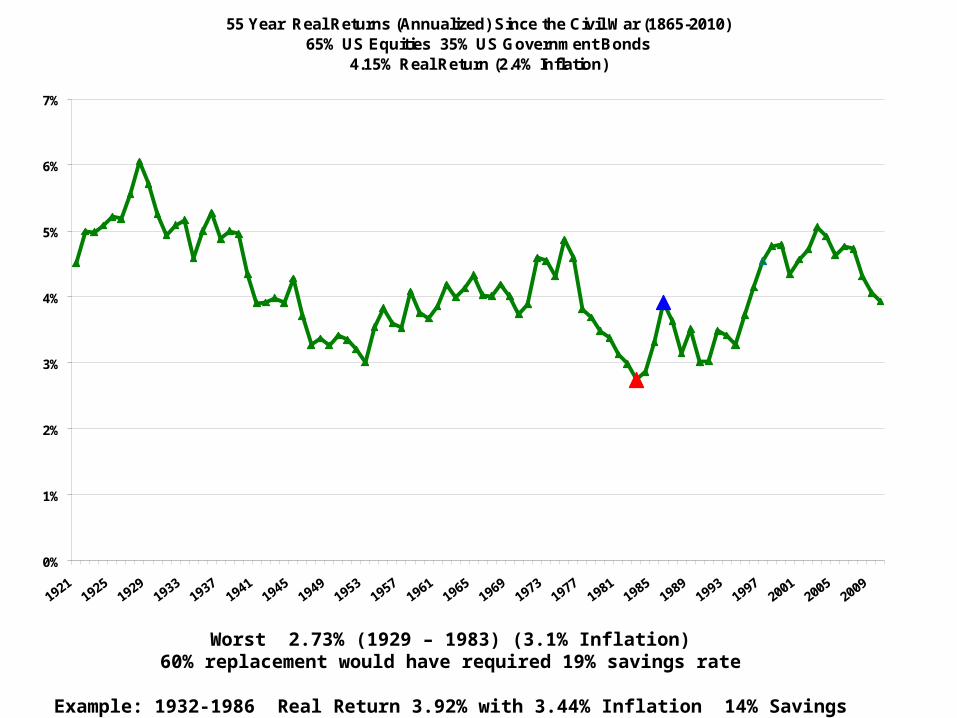

Worst 2.73% (1929 – 1983) (3.1% Inflation)60% replacement would have required 19% savings rate

Example: 1932-1986 Real Return 3.92% with 3.44% Inflation 14% Savings

55 Year Real Returns (Annualized) Since the Civil War (1865-2010)65% US Equities 35% US Government Bonds

4.15% Real Return (2.4% Inflation)

0%

1%

2%

3%

4%

5%

6%

7%

19211925

19291933

19371941

19451949

19531957

19611965

19691973

19771981

19851989

19931997

20012005

2009

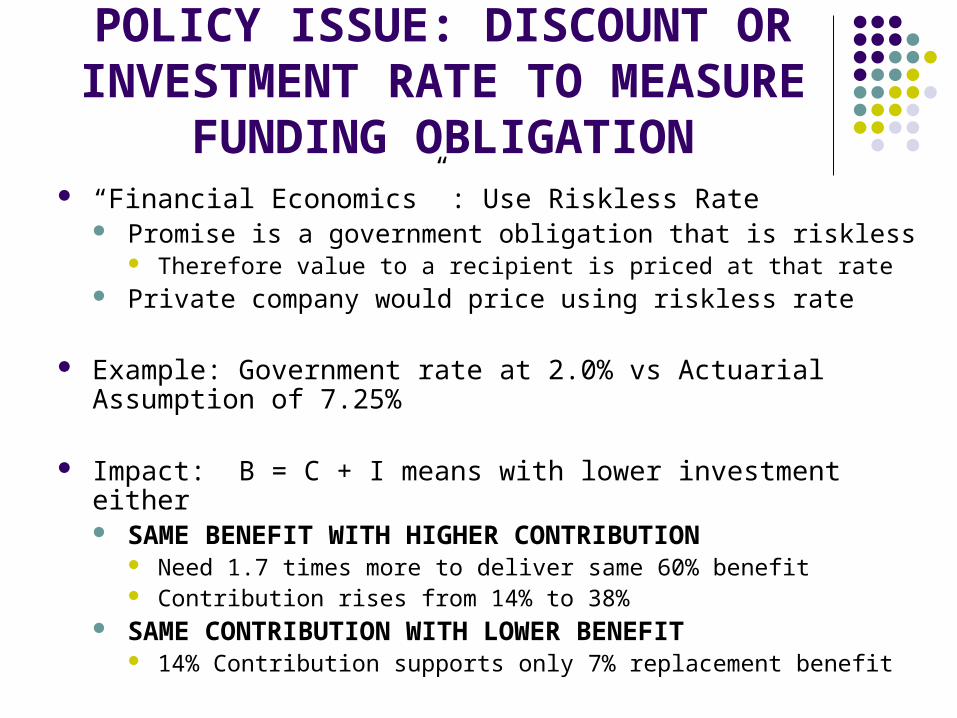

POLICY ISSUE: DISCOUNT OR INVESTMENT RATE TO MEASURE

FUNDING OBLIGATION “Financial Economics” : Use Riskless Rate

Promise is a government obligation that is riskless Therefore value to a recipient is priced at that rate

Private company would price using riskless rate

Example: Government rate at 2.0% vs Actuarial Assumption of 7.25%

Impact: B = C + I means with lower investment either SAME BENEFIT WITH HIGHER CONTRIBUTION

Need 1.7 times more to deliver same 60% benefit Contribution rises from 14% to 38%

SAME CONTRIBUTION WITH LOWER BENEFIT 14% Contribution supports only 7% replacement benefit

IMPACT OF INVESTING AT 2% TREASURY (OR DISCOUNT AT TREASURY)Increase needs by 1.7 times

Option 1: increase contributions by almost 3X

AMOUNTS NEEDED FOR EACH $100 OF ENDING SALARY3.5% inflation, 0.5% real salary increase, 1% COLA

3.75% real $838

2% Treasury $1,413

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

-29

-27

-25

-23

-21

-19

-17

-15

-13

-11 -9 -7 -5 -3 -1 1 3 5 7 9 11 13 15 17 19 21 23 25

Years from retirement

Cu

mu

lati

ve $

nee

ded

in e

nd

ing

ye

ar $

Level % of Total Salary

14%

38%

OPTION 2: REDUCE BENEFITS FROM 60% REPLACEMENT TO 7%

FINANCIAL ECONOMICS: 14 % CONTRIBUTION 2% TREASURY RETURNS60% REPLACEMENT DROPS TO 7% REPLACEMENT

3.75% real 60% replacement $838

2% Treasury 7% Replacement

$365

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

-29

-27

-25

-23

-21

-19

-17

-15

-13

-11 -9 -7 -5 -3 -1 1 3 5 7 9 11 13 15 17 19 21 23 25

Years from retirement

Cu

mu

lati

ve $

nee

ded

in e

nd

ing

yea

r $

Level % of Total Salary

14%

14%

WOULD GREECE HAVE A LOWER FUNDING NEED?

Financial economics equates “value” or “price” with “funding obligation”

Riskier obligor would have perceived lower funding obligation for same benefit A bonding rate of 34% would value liabilities at near 0, while

government pensions would be large

Shifting obligations from government to individuals would say tiny retirement need – but obviously not true

Should that drive behavior in investing for retirement?

Worst 2.73% (1929 – 1983) (3.1% Inflation)60% replacement would have required 19% savings rate

Example: 1932-1986 Real Return 3.92% with 3.44% Inflation 14% Savings

55 Year Real Returns (Annualized) Since the Civil War (1865-2010)65% US Equities 35% US Government Bonds

4.15% Real Return (2.4% Inflation)

0%

1%

2%

3%

4%

5%

6%

7%

19211925

19291933

19371941

19451949

19531957

19611965

19691973

19771981

19851989

19931997

20012005

2009

INDIVIDUAL ISSUES PRACTICAL: BEHAVIOR

Saving Enough DC Plans put half needed contribution levels

7.5% vs 14% Making Enough

DC Participant returns 2%-4% lower Higher costs and fees Poor portfolio construction and management

THEORETICAL: RISK Mortality Risk Increased Market Risk (particularly in retirement)

DB Plans pool and reduce Mortality and Market risk

Individual needs to save around 5% more to insure against risks

3.5% inflation, 0.5% real salary increase, 1% COLA

AVERAGE 401k EXPERIENCE: 7.5% CONTRIBUTION 2% LOWER RETURNS60% REPLACEMENT DROPS TO 11% REPLACEMENT

3.75% real 25% replacement $411

3.75% real 60% replacement $838

1.75% Real 11% Replacement

$299

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

-29

-27

-25

-23

-21

-19

-17

-15

-13

-11 -9 -7 -5 -3 -1 1 3 5 7 9 11 13 15 17 19 21 23 25

Years from retirement

Cu

mu

lati

ve $

nee

ded

in e

nd

ing

yea

r $

Level % of Total Salary

14%

7.5%

7.5%

Worst 2.73% (1929 – 1983) (3.1% Inflation)60% replacement would have required 19% savings rate

Example: 1932-1986 Real Return 3.92% with 3.44% Inflation 14% Savings

55 Year Real Returns (Annualized) Since the Civil War (1865-2010)65% US Equities 35% US Government Bonds

4.15% Real Return (2.4% Inflation)

0%

1%

2%

3%

4%

5%

6%

7%

19211925

19291933

19371941

19451949

19531957

19611965

19691973

19771981

19851989

19931997

20012005

2009

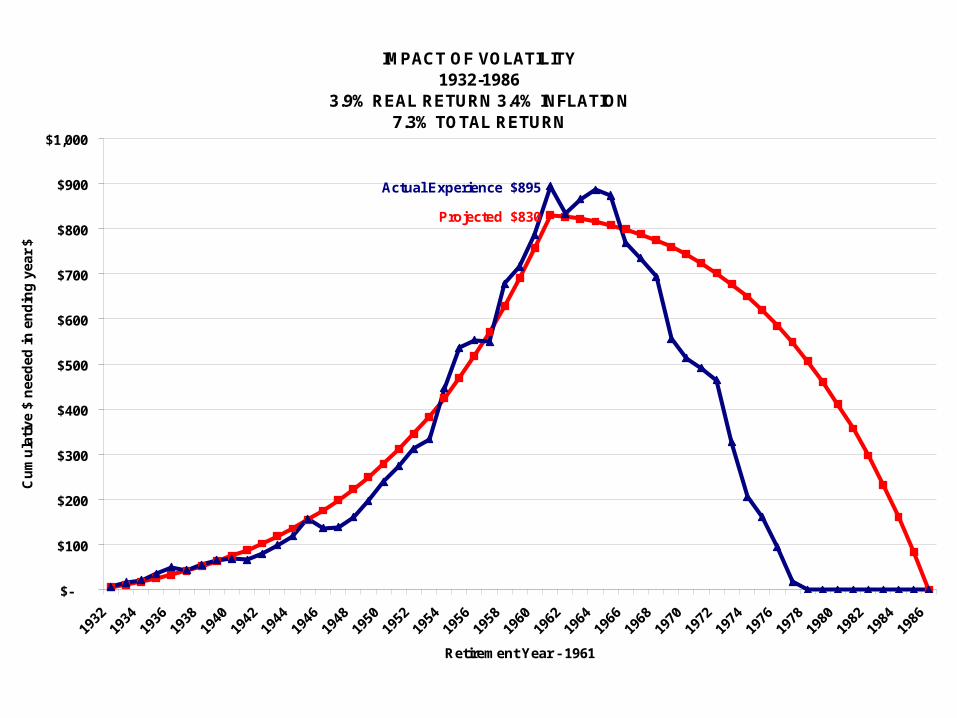

IMPACT OF VOLATILITY1932-1986

3.9% REAL RETURN 3.4% INFLATION 7.3% TOTAL RETURN

Projected $830

Actual Experience $895

$-

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

1932

1934

1936

1938

1940

1942

1944

1946

1948

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

Retirement Year - 1961

Cu

mu

lati

ve $

nee

ded

in e

nd

ing

yea

r $

Level % of Total Salary

14%14%

Expected Return for 1932-1978 : 7.3% Actual Return: 5.8% (2.5% real)

INDIVIDUAL (AND CLOSED PLAN) FUNDS RAN OUT BEFORE GREAT YEARS

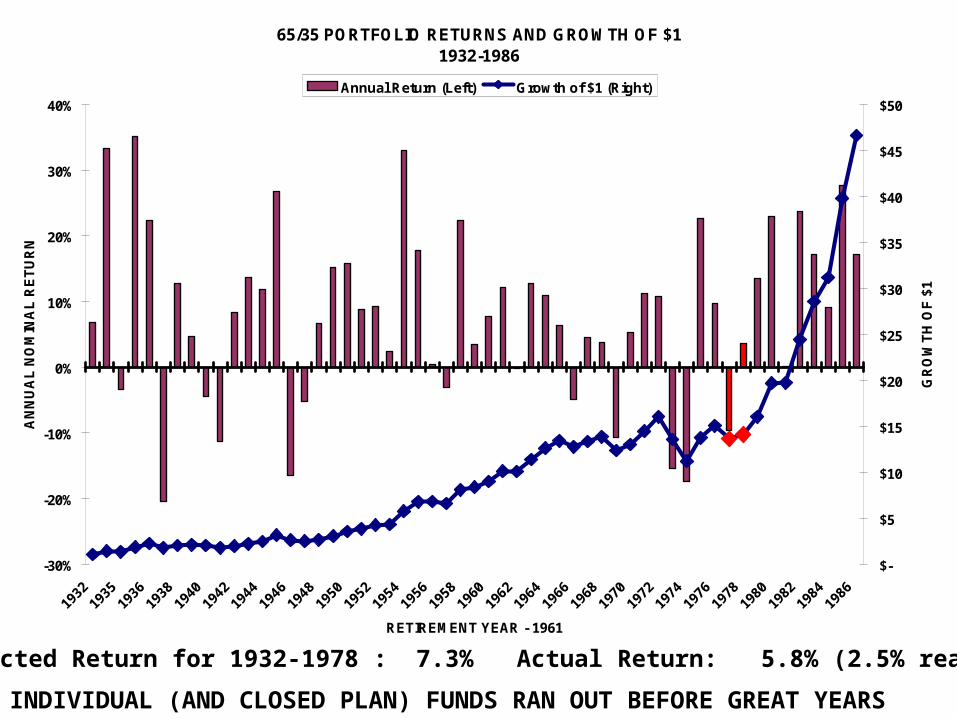

65/35 PORTFOLIO RETURNS AND GROWTH OF $11932-1986

-30%

-20%

-10%

0%

10%

20%

30%

40%

1932

1935

1936

1938

1940

1942

1944

1946

1948

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

RETIREMENT YEAR - 1961

AN

NU

AL

NO

MIN

AL

RE

TU

RN

$-

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

GR

OW

TH

OF

$1

Annual Return (Left) Growth of $1 (Right)

0.5% Real Salary Increase 1% COLA

IMPACT OF VOLATILITY1932-1986

NEEDED SAVINGS RATE - 19%NEEDED END ACCOUNT PER $100 FINAL SALARY: $1,281

Projected $830 Actual Experience $895

Needed $1,281

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

1932

1934

1936

1938

1940

1942

1944

1946

1948

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

Retirement Year - 1961

Cu

mu

lati

ve $

nee

ded

in e

nd

ing

yea

r $

Level % of Total Salary

14%

14%

19%

IS MODERN PORTFOLIO THEORY DEAD?

Daily S&P Price Movem ents 1950-2010

-1 0%

- 8%

- 6%

- 4%

- 2%

0%

2%

4%

6%

8%

1 0%

Jan-

00

May

-00

Sep-

00

Jan-

01

May

-01

Sep

-01

Jan-

02

May

-02

Sep-

02

Jan-

03

May

-03

Sep-

03

Jan-

04

May

-04

Sep

-04

Jan-

05

May

-05

Sep-

05

Jan-

06

May

-06

Sep-

06

Jan-

07

May

-07

Sep-

07

Jan-

08

May

-08

Sep-

08

Jan-

09

May

-09

Sep-

09

Jan-

10

May

-10

BASIC MPT PRINCIPLES Start with Long-Term (5-10 year +) time frame

Modern Portfolio Theory 5-6 Asset Types

US Equities, International Equities, REITS, Emerging Market Equities, US Investment Grade Bonds, TIPS

Core Index

Adjust for Short Term Wildness Survive: Attend to Liquidity Control Leverage Keep Broad Diversification

AVOID THE BIG MISTAKE In order to get market returns, need to be in the markets

Avoid tactical asset allocation NEVER make a major move in the middle of a crisis

Add investments where think have advantage or insight, if any Be careful with active management and fees Beware turnover and related costs KNOW WHAT YOU OWN

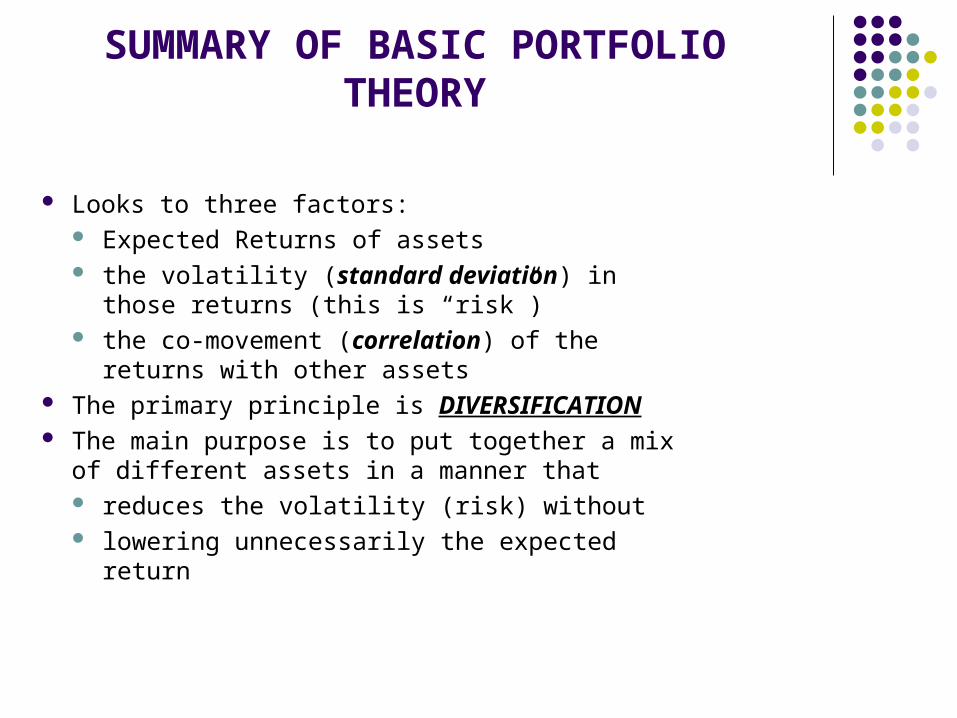

SUMMARY OF BASIC PORTFOLIO THEORY

Looks to three factors: Expected Returns of assets the volatility (standard deviation) in those

returns (this is “risk”) the co-movement (correlation) of the returns

with other assets The primary principle is DIVERSIFICATION The main purpose is to put together a mix of

different assets in a manner that reduces the volatility (risk) without lowering unnecessarily the expected return

ASSUMPTIONS OF MPT:“NORMAL” MARKETS IN LONG TERM

Return is generally linearly related to risk (volatility) Higher returns associated with higher volatility or risk

Returns normally (coin-tossing) random Bell shaped curve – “Gaussian” Allows Standard deviation to be a generally accurate

representation of risk (volatility)

DIVERSIFICATION REDUCES RISK Correlations or co-movements aren’t in lockstep

Holds for long-term (5-10 year rolling time frames)

HISTORIC RETURNS AND RISKS 1926 - 20101 Standard Deviation

49.3%

32.3%

11.2%6.8%

16.7%11.9%

5.5% 3.7%

-15.9%

-8.5%

-0.2% 0.6%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Small Stocks32.6%

S&P 50020.4%

Cash3.1%

Bonds5.7%

RETURN GENERALLY FOLLOWS RISK

Large Stocks

Small Stocks

Long GovInt Gov

T-Bills

Long Corp

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0% 5% 10% 15% 20% 25% 30% 35%

RISK (Annual Volatility)

RE

TU

RN

(A

rith

me

tic

)

Ibbotsen SBBI 2010 Classic YearbookAnnual Returns

27

Source: Yale University Professor Robert Shiller’s website, as of 12/31/08Past performance is not a guarantee of future results.Rolling periods represent a series of overlapping, smaller time periods within a single, longer-term time period. A hypothetical example is the 20-year time period from 12/31/82 through 12/31/02. This long-term period consists of 16 smaller five-year “rolling” segments. The first segment is the five-year period from 12/31/82 to 12/31/87. The next rolling segment is the five-year period from 12/31/83 to 12/31/88, and so on.

Expected vs Actual Frequency of Annual Returns5 Year Rolling Returns 1871-2008 (log)

0%

5%

10%

15%

20%

25%

30%

-20% -15% -10% -5% 0% 5% 10% 15% 20% 25% 30% 35% 40%

Annual Return (log)

Fre

qu

ency

0%

5%

10%

15%

20%

25%

30%

Expected Actual

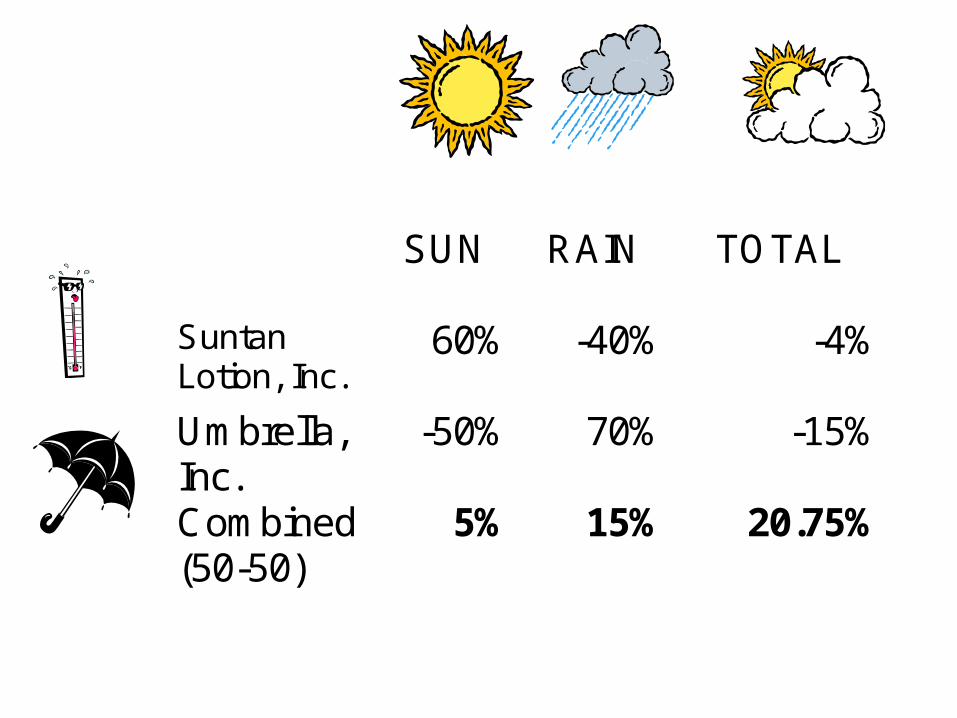

SUN RAIN TOTAL

Suntan Lotion, Inc.

60% -40% -4%

SUN RAIN TOTAL

Suntan Lotion, Inc.

60% -40% -4%

Umbrella, Inc.

-50% 70% -15%

SUN RAIN TOTAL

Suntan Lotion, Inc.

60% -40% -4%

Umbrella, Inc.

-50% 70% -15%

Combined (50-50)

5% 15% 20.75%

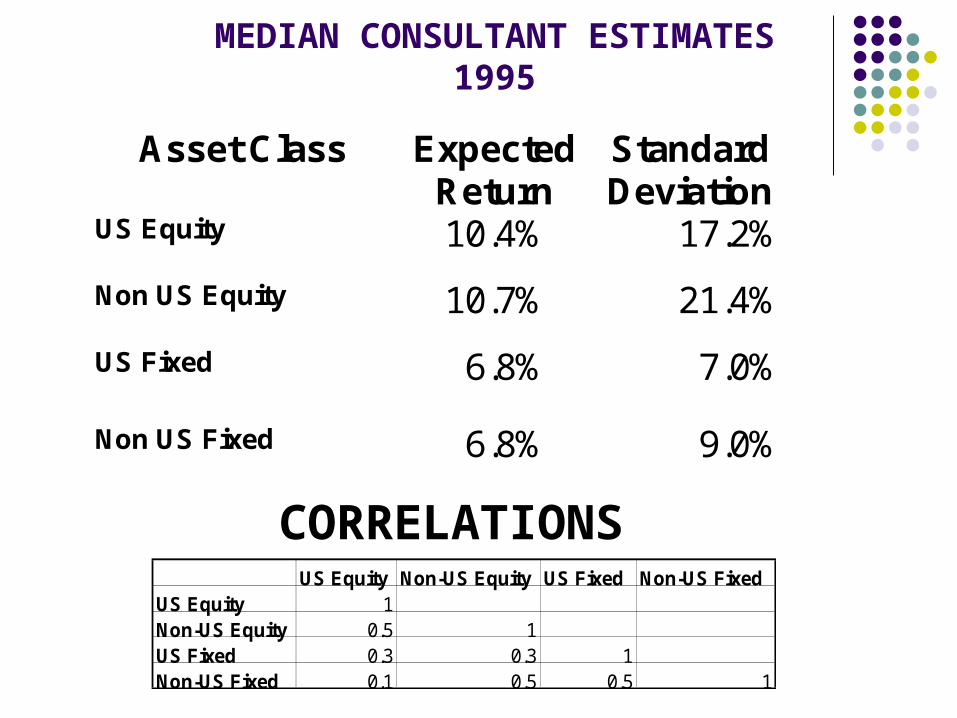

MEDIAN CONSULTANT ESTIMATES1995

Asset Class Expected Return

Standard Deviation

US Equity 10.4% 17.2%

Non US Equity 10.7% 21.4%

US Fixed 6.8% 7.0%

Non US Fixed 6.8% 9.0%

US Equity Non-US Equity US Fixed Non-US FixedUS Equity 1Non-US Equity 0.5 1US Fixed 0.3 0.3 1Non-US Fixed 0.1 0.5 0.5 1

CORRELATIONS

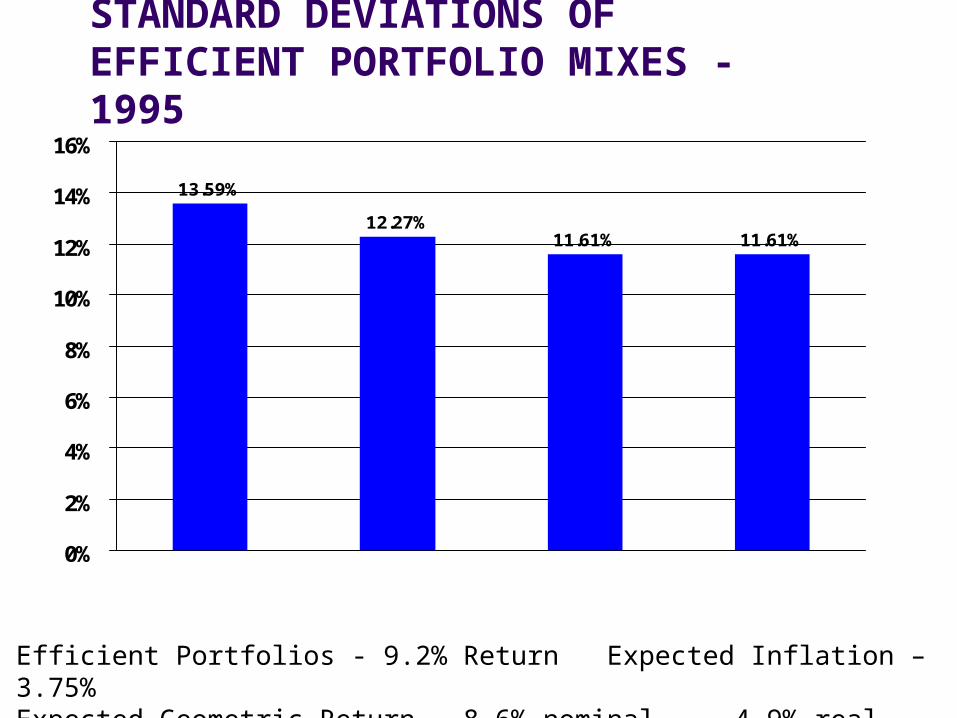

STANDARD DEVIATIONS OFEFFICIENT PORTFOLIO MIXES - 1995

13.59%

12.27%11.61% 11.61%

0%

2%

4%

6%

8%

10%

12%

14%

16%

78% US Stocks

22% Cash

46% US Stocks25% US Bonds

19% EAFE10% Non$Bonds

44% US Stocks35% US Bonds

21% EAFE

66% US Stocks34% US Bonds

Efficient Portfolios - 9.2% Return Expected Inflation – 3.75%Expected Geometric Return – 8.6% nominal 4.9% real

Growth of $1 January 1995 – June 201144% R3000, 21% EAFE, 35% Aggregate8.4% return 10.3% Standard Deviation

Oct-07 $3.34

Apr-11 $3.52

$3.45

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

Jan-9

5

Jan-9

6

Jan-9

7

Jan-9

8

Jan-9

9

Jan-0

0

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

FY 2009 - 16.6%FY 2010 12.0%FY 2011 21.7%

2.5% Inflation 7.8% Geometric 5.3% Real

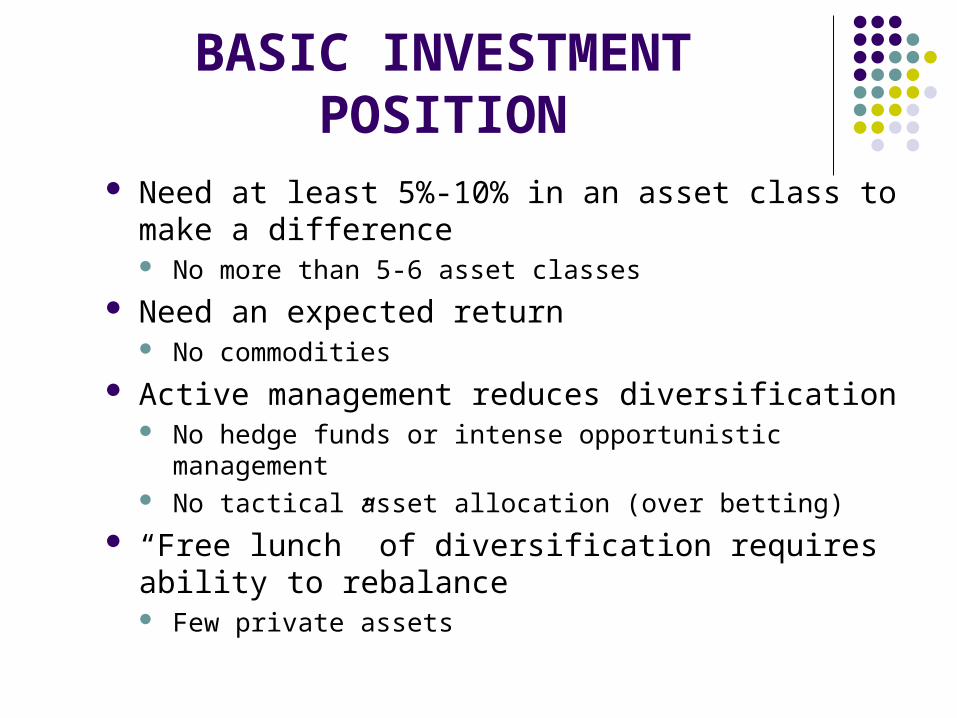

BASIC INVESTMENT POSITION

Need at least 5%-10% in an asset class to make a difference No more than 5-6 asset classes

Need an expected return No commodities

Active management reduces diversification No hedge funds or intense opportunistic management No tactical asset allocation (over betting)

“Free lunch” of diversification requires ability to rebalance Few private assets

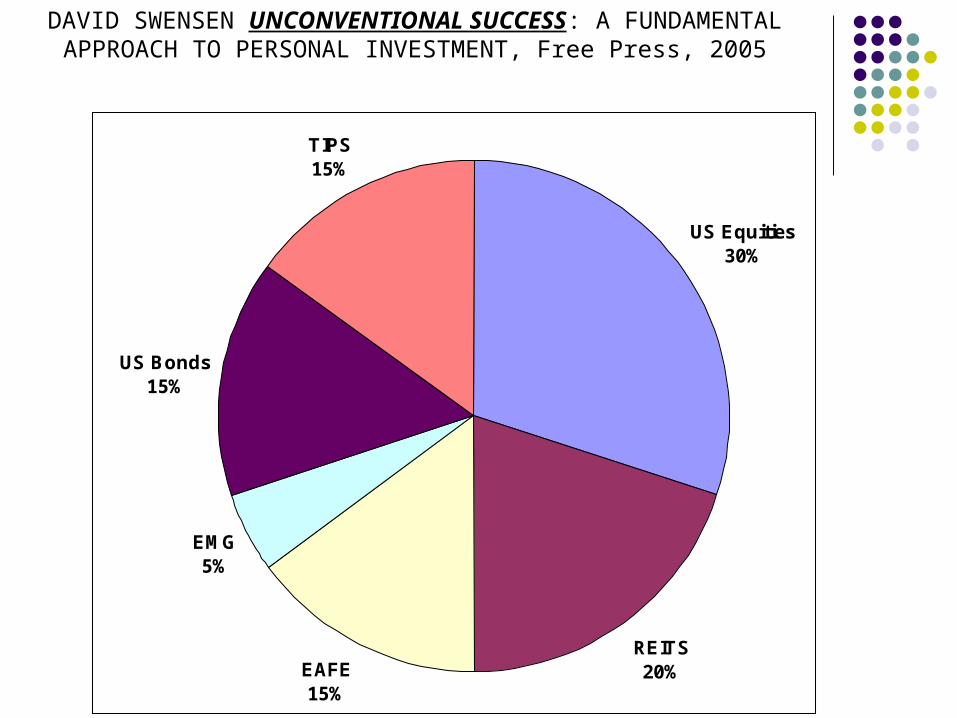

US Equities30%

REITS20%EAFE

15%

EMG5%

US Bonds15%

TIPS15%

DAVID SWENSEN UNCONVENTIONAL SUCCESS: A FUNDAMENTAL APPROACH TO PERSONAL INVESTMENT, Free Press,

2005

44/21/35 Swensen ExpectedGeometric 7.8% 8.9% 8.6%Real 5.3% 6.4% 4.9%

Growth of $1 from January 1995 to June 20118.4% Return 10.32% SD (44/21/35) 9.7% Return 11.39% SD (Swensen) 9.2% Return 11.61% SD (Expected)

44-21-35 $3.45

Swensen $4.12

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

Jan-9

5

Jan-9

6

Jan-9

7

Jan-9

8

Jan-9

9

Jan-0

0

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

44/21/35 Swensen YaleFY 2009 - 16.6% -22.1% -24.6%FY 2010 12.0% 13.0% 8.9%FY 2011 21.7% 24.2% 21.9%3 Year 13.7% 16.6% 0.1%

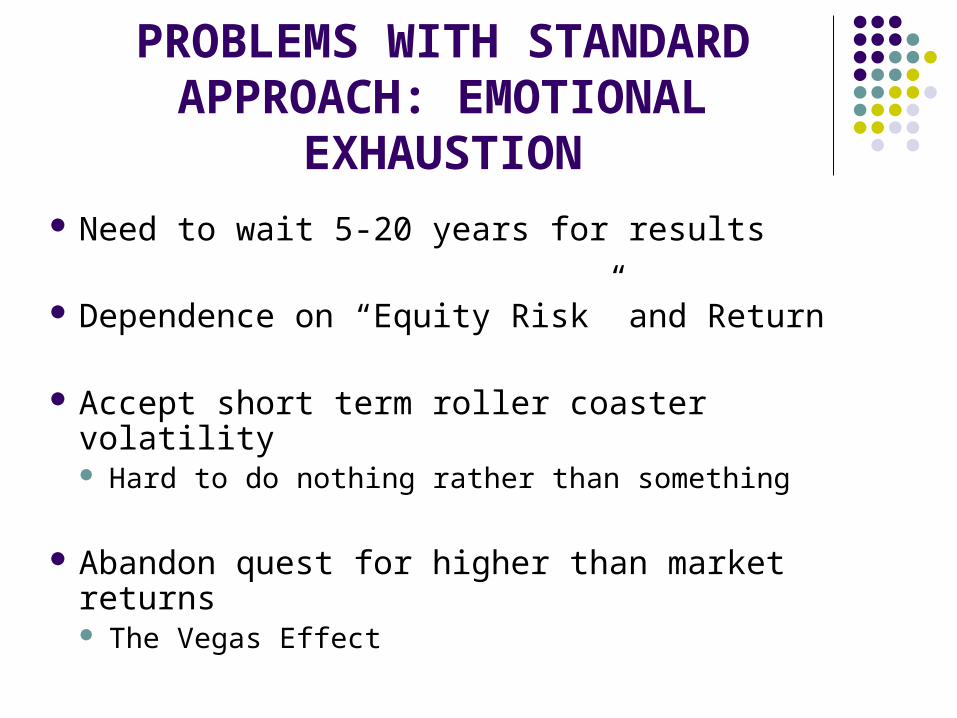

PROBLEMS WITH STANDARD APPROACH: EMOTIONAL

EXHAUSTION

Need to wait 5-20 years for results

Dependence on “Equity Risk” and Return

Accept short term roller coaster volatility Hard to do nothing rather than something

Abandon quest for higher than market returns The Vegas Effect

WHO NEEDS MORE? When Market returns are not enough

Liability needs are more than 3%-5% real Endowments with higher education inflation Pension funds in too big a whole

When 1-5 year “normal” volatility still too high Corporations with quarterly earnings reports Pension funds “near the edge”

If have short term attention span – “CNBC disease” Rotating Boards, CIO’s, Politics, etc.

If have special insight or advantage over others

SHORT TERM “Danger Will Robinson”

The Abnormal is “Normal”

Expect not only the unexpected, but also the impossible

Daily S&P Price Movements 1950-2010

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Ja

n-0

0

Ma

y-0

0

Se

p-0

0

Ja

n-0

1

Ma

y-0

1

Se

p-0

1

Ja

n-0

2

Ma

y-0

2

Se

p-0

2

Ja

n-0

3

Ma

y-0

3

Se

p-0

3

Ja

n-0

4

Ma

y-0

4

Se

p-0

4

Ja

n-0

5

Ma

y-0

5

Se

p-0

5

Ja

n-0

6

Ma

y-0

6

Se

p-0

6

Ja

n-0

7

Ma

y-0

7

Se

p-0

7

Ja

n-0

8

Ma

y-0

8

Se

p-0

8

Ja

n-0

9

Ma

y-0

9

Se

p-0

9

Ja

n-1

0

Ma

y-1

0

Daily S&P Price Movements 2002-2010

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Jan

-02

Ap

r-02

Jul-

02

Oct

-02

Jan

-03

Ap

r-03

Jul-

03

Oct

-03

Jan

-04

Ap

r-04

Jul-

04

Oct

-04

Jan

-05

Ap

r-05

Jul-

05

Oct

-05

Jan

-06

Ap

r-06

Jul-

06

Oct

-06

Jan

-07

Ap

r-07

Jul-

07

Oct

-07

Jan

-08

Ap

r-08

Jul-

08

Oct

-08

Jan

-09

Ap

r-09

Jul-

09

Oct

-09

Jan

-10

Ap

r-10

Jul-

10

Dai

ly P

rice

Mo

vem

ent

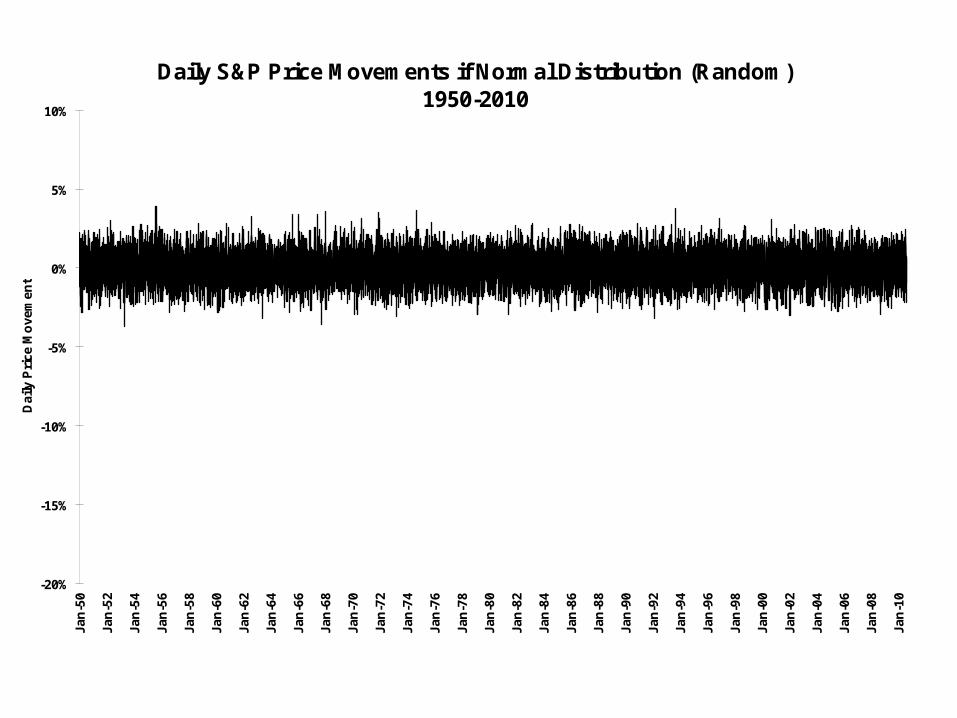

Daily S&P Price Movements if Normal Distribution (Random)1950-2010

-20%

-15%

-10%

-5%

0%

5%

10%

Jan

-50

Jan

-52

Jan

-54

Jan

-56

Jan

-58

Jan

-60

Jan

-62

Jan

-64

Jan

-66

Jan

-68

Jan

-70

Jan

-72

Jan

-74

Jan

-76

Jan

-78

Jan

-80

Jan

-82

Jan

-84

Jan

-86

Jan

-88

Jan

-90

Jan

-92

Jan

-94

Jan

-96

Jan

-98

Jan

-00

Jan

-02

Jan

-04

Jan

-06

Jan

-08

Jan

-10

Dai

ly P

rice

Mo

vem

ent

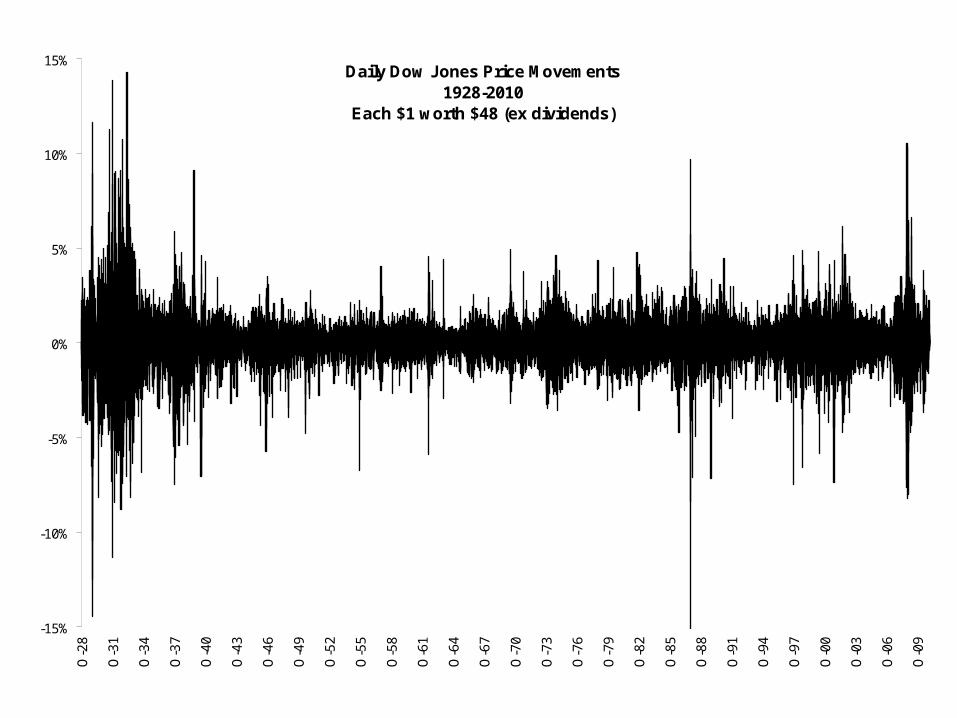

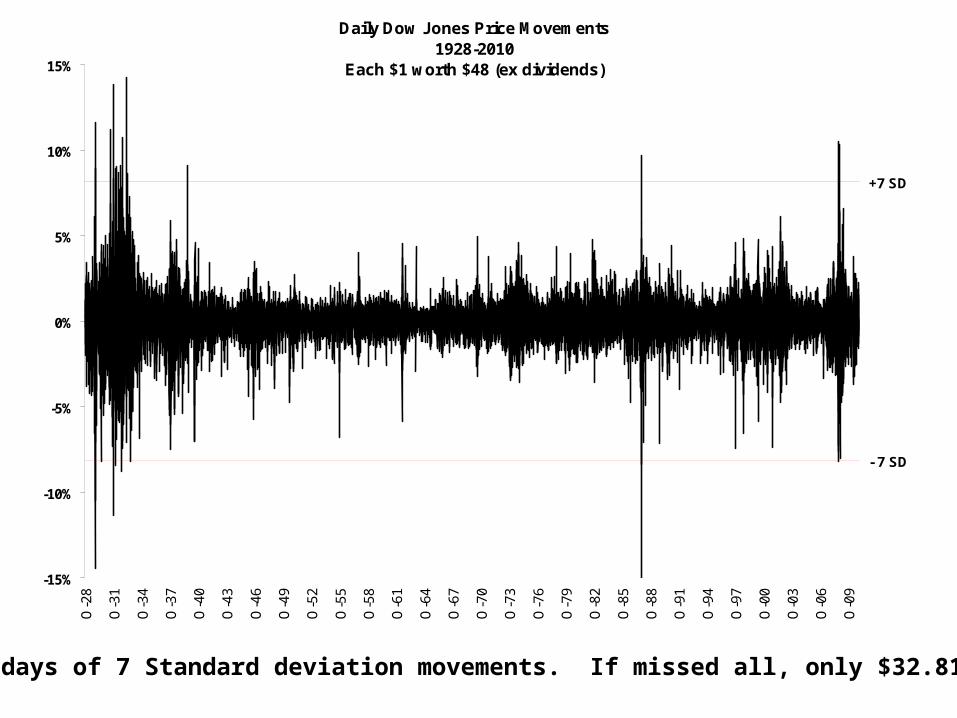

Daily Dow Jones Price Movements1928-2010

Each $1 worth $48 (ex dividends)

-15%

-10%

-5%

0%

5%

10%

15%

O-2

8

O-3

1

O-3

4

O-3

7

O-4

0

O-4

3

O-4

6

O-4

9

O-5

2

O-5

5

O-5

8

O-6

1

O-6

4

O-6

7

O-7

0

O-7

3

O-7

6

O-7

9

O-8

2

O-8

5

O-8

8

O-9

1

O-9

4

O-9

7

O-0

0

O-0

3

O-0

6

O-0

9

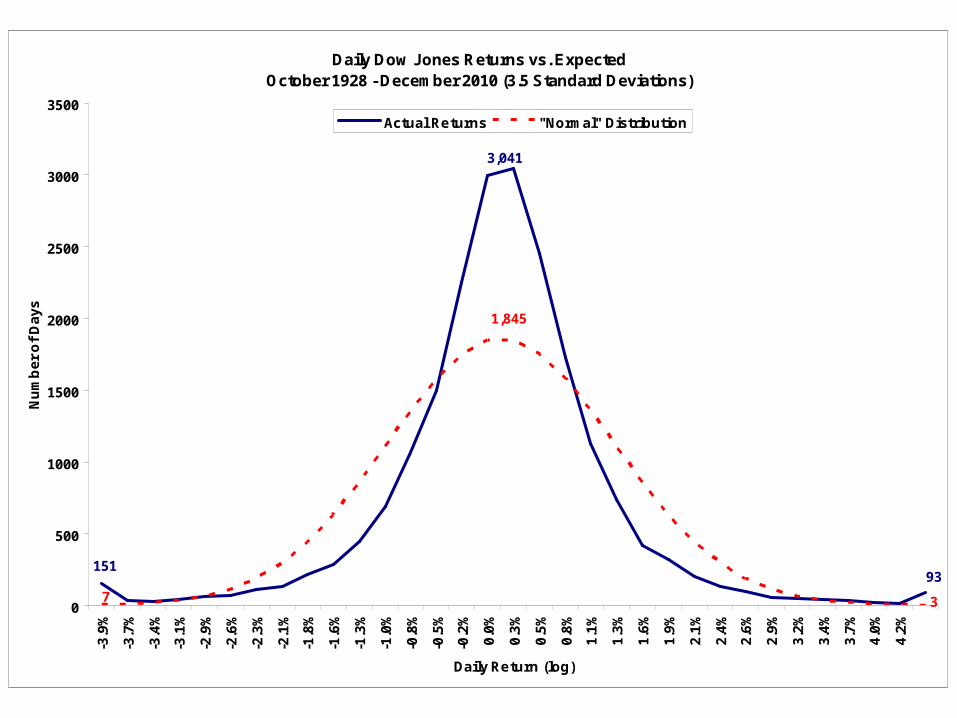

Daily Dow Jones Returns vs. ExpectedOctober 1928 - December 2010 (3.5 Standard Deviations)

93151

3,041

7 3

1,845

0

500

1000

1500

2000

2500

3000

3500-3

.9%

-3.7

%

-3.4

%

-3.1

%

-2.9

%

-2.6

%

-2.3

%

-2.1

%

-1.8

%

-1.6

%

-1.3

%

-1.0

%

-0.8

%

-0.5

%

-0.2

%

0.0

%

0.3

%

0.5

%

0.8

%

1.1

%

1.3

%

1.6

%

1.9

%

2.1

%

2.4

%

2.6

%

2.9

%

3.2

%

3.4

%

3.7

%

4.0

%

4.2

%

Daily Return (log)

Nu

mb

er

of

Da

ys

Actual Returns "Normal" Distribution

Daily Dow Jones Price Movements1928-2010

Each $1 worth $48 (ex dividends)

+7 SD

- 7 SD

-15%

-10%

-5%

0%

5%

10%

15%

O-2

8

O-3

1

O-3

4

O-3

7

O-4

0

O-4

3

O-4

6

O-4

9

O-5

2

O-5

5

O-5

8

O-6

1

O-6

4

O-6

7

O-7

0

O-7

3

O-7

6

O-7

9

O-8

2

O-8

5

O-8

8

O-9

1

O-9

4

O-9

7

O-0

0

O-0

3

O-0

6

O-0

9

27 days of 7 Standard deviation movements. If missed all, only $32.81

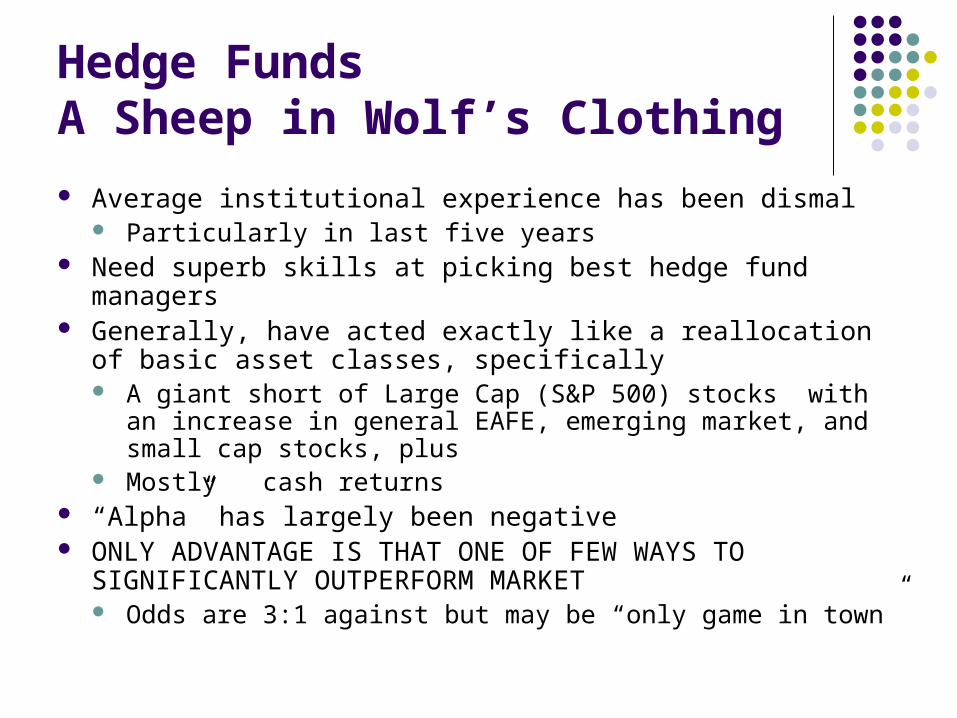

Hedge FundsA Sheep in Wolf’s Clothing

Average institutional experience has been dismal Particularly in last five years

Need superb skills at picking best hedge fund managers Generally, have acted exactly like a reallocation of basic asset

classes, specifically A giant short of Large Cap (S&P 500) stocks with an increase in

general EAFE, emerging market, and small cap stocks, plus Mostly cash returns

“Alpha” has largely been negative ONLY ADVANTAGE IS THAT ONE OF FEW WAYS TO

SIGNIFICANTLY OUTPERFORM MARKET Odds are 3:1 against but may be “only game in town”

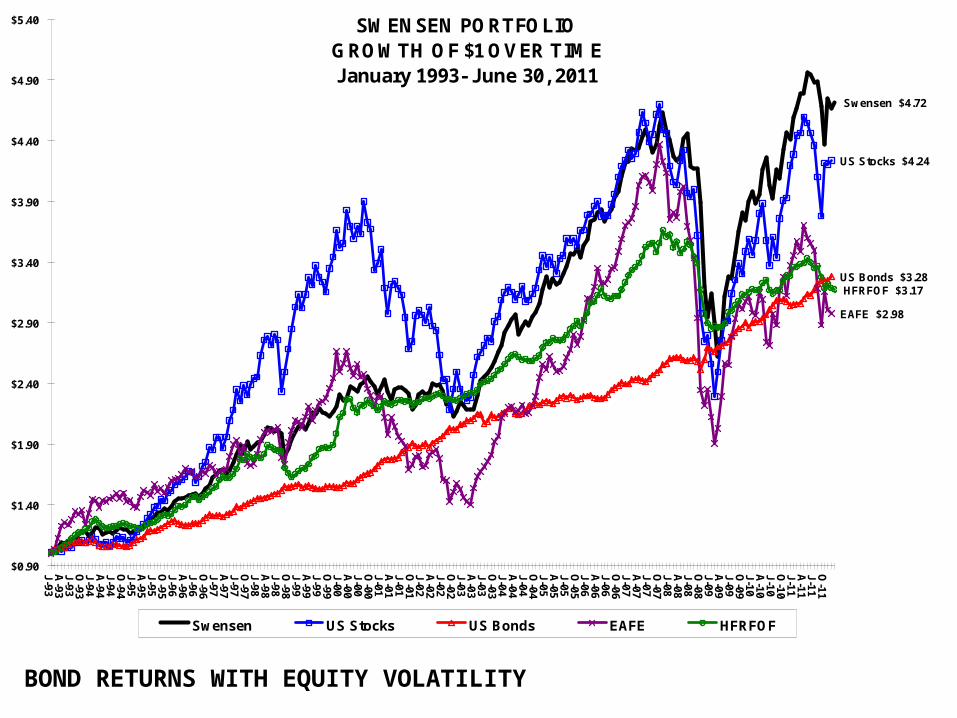

BOND RETURNS WITH EQUITY VOLATILITY

SWENSEN PORTFOLIOGROWTH OF $1 OVER TIMEJanuary 1993- June 30, 2011

Swensen $4.72

US Stocks $4.24

US Bonds $3.28

EAFE $2.98

HFRFOF $3.17

$0.90

$1.40

$1.90

$2.40

$2.90

$3.40

$3.90

$4.40

$4.90

$5.40

J-93A

-93J-93O

-93J-94A

-94J-94O

-94J-95A

-95J-95O

-95J-96A

-96J-96O

-96J-97A

-97J-97O

-97J-98A

-98J-98O

-98J-99A

-99J-99O

-99J-00A

-00J-00O

-00J-01A

-01J-01O

-01J-02A

-02J-02O

-02J-03A

-03J-03O

-03J-04A

-04J-04O

-04J-05A

-05J-05O

-05J-06A

-06J-06O

-06J-07A

-07J-07O

-07J-08A

-08J-08O

-08J-09A

-09J-09O

-09J-10A

-10J-10O

-10J-11A

-11J-11O

-11

Swensen US Stocks US Bonds EAFE HFRFOF

Excess Returns to 55% Russell 3000 / 15% EAFE / 30% AggregateHFR Fund of Funds vs S&P 500

1993-2011

HFR Excess -79%

S&P Excess 23%

-100%

-50%

0%

50%

100%

150%

Jan-9

3

Jan-9

4

Jan-9

5

Jan-9

6

Jan-9

7

Jan-9

8

Jan-9

9

Jan-0

0

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

HFR Excess S&P Excess

GROWTH OF $1 OVER PAST FIVE YEARS

HFRXGL, $0.87

PERSI $1.19

HFRXM $0.92

HFRXAR $0.85

HFRXEH $0.77

$0.50

$0.60

$0.70

$0.80

$0.90

$1.00

$1.10

$1.20

$1.30

Mar

-07

Jun-0

7

Sep-0

7

Dec-0

7

Mar

-08

Jun-0

8

Sep-0

8

Dec-0

8

Mar

-09

Jun-0

9

Sep-0

9

Dec-0

9

Mar

-10

Jun-1

0

Sep-1

0

Dec-1

0

Mar

-11

Jun-1

1

Sep-1

1

Dec-1

1

HFRXGL PERSI HFRXM HFRXAR HFRXEH

GROWTH OF $1 OVER PAST FIVE YEARS

HFRXGL, $0.87

PERSI, $1.19

R3000, $1.09

EAFE, $0.88

AGG $1.36

$0.50

$0.60

$0.70

$0.80

$0.90

$1.00

$1.10

$1.20

$1.30

$1.40

$1.50

Mar

-07

Jun-0

7

Sep-0

7

Dec-0

7

Mar

-08

Jun-0

8

Sep-0

8

Dec-0

8

Mar

-09

Jun-0

9

Sep-0

9

Dec-0

9

Mar

-10

Jun-1

0

Sep-1

0

Dec-1

0

Mar

-11

Jun-1

1

Sep-1

1

Dec-1

1

HFRXGL PERSI R3000 EAFE AGG

WORLD REBALANCING Great Deleveraging continues

World is Restructuring US Debt reduction and consolidation Europe fiscal integration China and developing world rebalancing

economies between exports and consumption

Process will take years, not months

BASIC CAPITAL MARKET CONCEPTS EXPECTATIONS

Not Current Conditions Current Expectations Moderate

PROFITS Not general economy Good balance sheets, lean operating conditions,

growth overseas (x Europe), little pressure on labor costs

RELATIVE VALUE Not absolute value in itself What are people willing to pay for expected earnings Current alternative – bonds -- unattractive

Current and Expected Yield Curves in 5 Yrs

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

Current TIPS -0.8% -0.8% -0.9% -1.0% -1.0% -0.9% -0.8% -0.6% -0.4% -0.2% -0.1% 0.6% 0.8%

Current Treasury 0.0% 0.1% 0.1% 0.3% 0.4% 0.6% 0.9% 1.4% 1.6% 1.8% 2.0% 2.7% 2.9%

TIPS in 5 -0.2% -0.2% -0.1% 0.0% 0.3% 0.5% 0.6% 0.7% 0.7% 0.7% 0.8% 1.1% 1.1%

Treasury in 5 2.5% 2.6% 2.7% 2.8% 2.9% 2.9% 3.0% 3.1% 3.1% 3.1% 3.1% 3.1% 3.0%

3M 6M 1Y 2Y 3Y 4Y 5Y 7Y 8Y 9Y 10Y 20Y 30Y

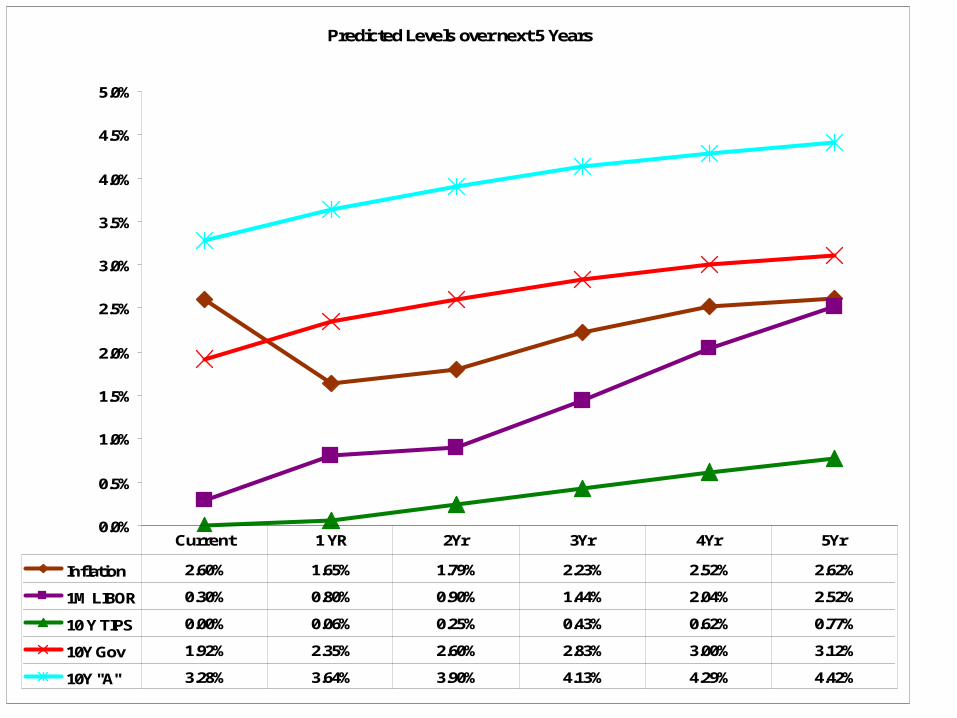

Predicted Levels over next 5 Years

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

Inflation 2.60% 1.65% 1.79% 2.23% 2.52% 2.62%

1M LIBOR 0.30% 0.80% 0.90% 1.44% 2.04% 2.52%

10 Y TIPS 0.00% 0.06% 0.25% 0.43% 0.62% 0.77%

10Y Gov 1.92% 2.35% 2.60% 2.83% 3.00% 3.12%

10Y "A" 3.28% 3.64% 3.90% 4.13% 4.29% 4.42%

Current 1 YR 2Yr 3Yr 4Yr 5Yr

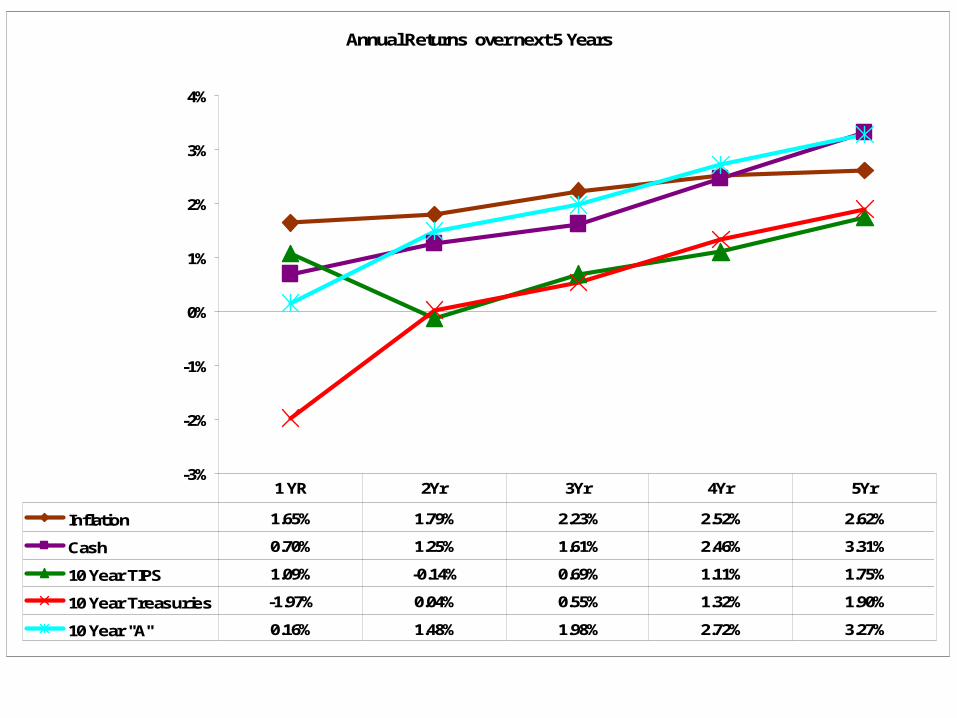

Annual Returns over next 5 Years

-3%

-2%

-1%

0%

1%

2%

3%

4%

Inflation 1.65% 1.79% 2.23% 2.52% 2.62%

Cash 0.70% 1.25% 1.61% 2.46% 3.31%

10 Year TIPS 1.09% -0.14% 0.69% 1.11% 1.75%

10 Year Treasuries -1.97% 0.04% 0.55% 1.32% 1.90%

10 Year "A" 0.16% 1.48% 1.98% 2.72% 3.27%

1 YR 2Yr 3Yr 4Yr 5Yr

Expected 10 Year Stock Return and Sources(Assumes Current P/E and Corp Profit Share of GDP remains the same)

2.1%2.6%

2.1% 2.4%

9.3%

10.8%

13.3%

0%

2%

4%

6%

8%

10%

12%

14%

Real GDP Inflation Dividend Buy Back Total WAC Equty 4Y Growth&Div

Current P/E Ratio (13.1) will probably riseCorporate Profit Share of GDP (12.9%) will probably drop

5 Year Expected Returns to Assets (Annualized)

2.4%

1.0%0.4%

-0.6%-0.9%

10.8%

-2%

0%

2%

4%

6%

8%

10%

12%

Inflation Cash 10 Year TIPS 10 YearTreasuries

10 Year "A" Equity

Expected Geometric Returns Expected 70/30 Return: 7.6% Nominal 5.2% Real

US GDP

(Billions)

Profits

(Billions)

S&P 500 EPS

S&P 500 Price

P/E Ratio

2001

(1/1)

$10,130 $ 790 $54.44 1320 24.3

2011

(9/30)

$15,181 $1,977 $94.81 1131 11.9

% CHANGE 2001-2011

50%

150%

74%

-14%

-51%

-100%

-50%

0%

50%

100%

150%

200%

US GDP CorporateProfits

S&P 500EPS

S&P 500Price

S&P 500P/E