residential real estate report

DESCRIPTION

RealestateTRANSCRIPT

4th Quarter and Year End Report 2009 Residential Real Estate in Austin, Texas

Clay Byrne, Broker

4700 N. Capital of Texas Highway #511 Austin, Texas 78746

(512) 431‐4342 [email protected]

(Information taken from Austin Board of Realtors MLS and National Association of Realtors)

My Thoughts…

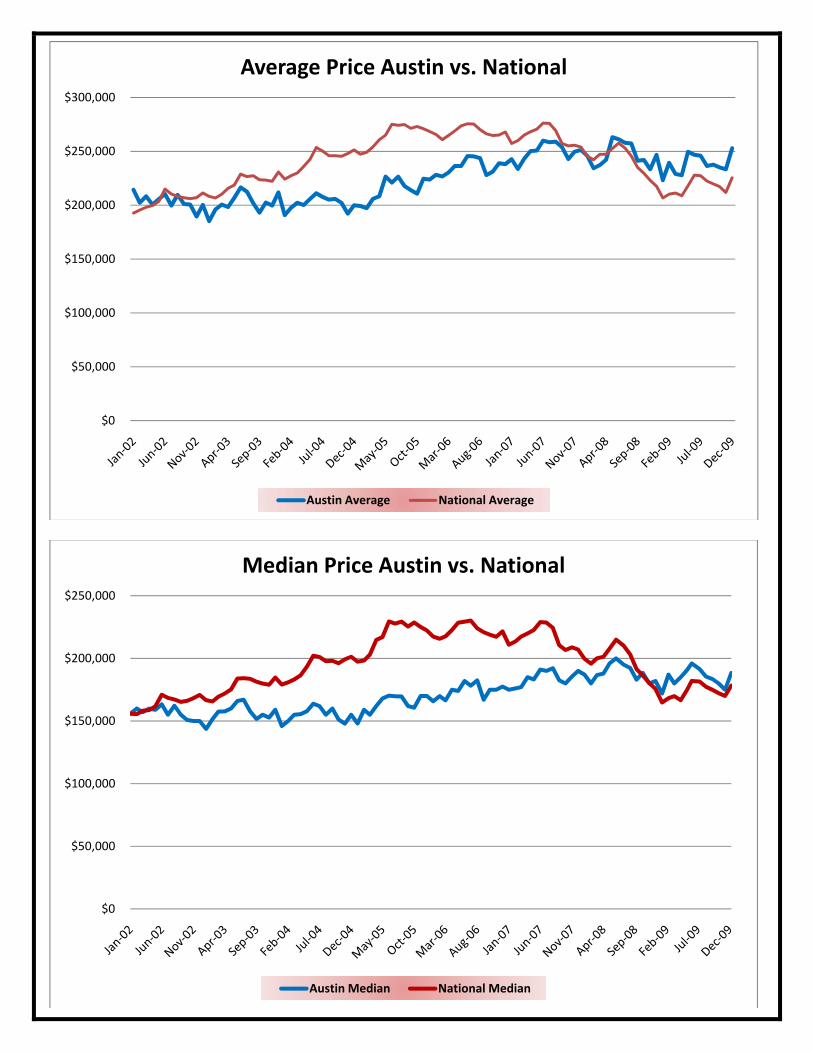

Goodbye 2009, we will not miss you! Real estate in Austin fell back to nearly the same number of transactions that we saw in 2003 which was right after the Tech Bust. The Austin Board of Realtors added 3 or 4 counties since 2003, too. So really, it was much worse in 2009. Money that was available to borrowers was almost impossible to find, foreclosures were sky high and unemployment kissed 10% last year. And, Austin was one of the best markets in the United States! Imagine being anywhere else but Austin. The end of 2009 was one of the worst winters I’ve seen as far as transactions, attitude and confidence in what was going to happen in near future. If you look at the charts in this report, it’s hard to believe we are at the bottom or bouncing along the bottom.

But… Since I’m getting this out so late this quarter, I’m going to go ahead and talk about what has been going on the last 3 months. Someone turned on the light switch on January 1, 2010. I am as busy as I have been in 3 years. The tax credits that are available are certainly part of the equation right now. I also think that people are tired of feeling ‘stuck’ like they have been the past few years. The stock market (DOW) has recovered a fair amount since its year and half long slide, hitting 7,062 at the beginning of 2009, managing to rebound and sustain around 10,000 for the last 5‐6 months. This has given some people a better feeling about their finances and with housing prices and interest rates being at the lowest they’ve been in years, they are buying homes. While the market is not robust and a full on recovery, there are homes being purchased in all price ranges.

The best part about what is going now is that several, and I mean several, of my unemployed contacts have landed high paying/highly skilled jobs not just in this quarter but starting at the end of last quarter. Jobs are the backbone of the economy as far as real estate is concerned. Most of the jobs have been in Austin and surrounding areas with some of my contacts getting multiple job offers from across the United States. My human resource associates in the larger companies based in Austin are telling me they are hiring highly skilled employees in Texas, US and Internationally. This is exactly what we need.

Don’t expect rapid appreciation or anything like that. Banks still have inventory (foreclosures) they are going put into the market and there is still some uncertainty in the market. Rates are low but banks still have very tight requirements. As you’ll read on the next page from Noelle Harris, there is a significant change in the money supply side of real estate about to take place. All I can tell you is that I am encouraged, and working, and so are a lot of people I know that haven’t been in several months.

Mortgage News

The Mortgage market has been through sweeping changes over the last 2 years. Undoubtedly we have all seen the headlines about Mortgage Fraud, and the damage it has caused to the banking industry and the economy at large. The lending industry has tightened lending guidelines to help safeguard against more losses. While mortgage applications continue to be steady many consumers have held off in moving forward with home purchases or refinances. A closer look at the current climate of lending may help to clarify the situation. While credit and lending guidelines are certainly tighter we are still experiencing a steady volume of new loans. The number of purchase and refinance applications have been high. This steady rate of mortgage applications can be linked to the Homebuyer’s Tax Credit, and the historically low interest rates. Consumers have been enjoying these low rates due to many reasons, but there are two factors in particular that are driving this benefit. First of all, it is important to note that interest rates are tied to the Federal Funds rate, which is set by the Federal Reserve. The Federal Funds rate is currently sitting at 0 ‐ .25%, and is keeping interest rates at a market‐driven minimum. This is in place to help stimulate the economy by keeping the cost of credit at an all‐time low. As the economy begins to recover the threat of inflation will rise. Inflation is not friendly to interest rates. Future comments from the economic world regarding inflation threats will cause the Federal Reserve to raise the Federal Funds rate, which, in turn, causes interest rates to rise. At this time the comments from the Fed regarding policy are to keep the Fed Funds rate low for an “extended time”. Should future comments not contain this “extended time” verbiage we can begin to expect that the Federal Funds rate will be raised. In addition to the Federal Funds rate being watched closely, it is important to keep a watchful eye on March 31, 2010. On this date the Federal Reserve will cease their program to purchase Mortgage Backed Securities (MBS). Each week the Fed is purchasing MBS to keep interest rates down. This program has been in place since January 2009, and has been keeping interest rates unnaturally low. As this program comes to a halt we will begin to see interest rates rise. In summary, it would seem to be a good time to move forward with purchases and refinances, as interest rates are historically low. Additionally the Federal Reserve policies put in place to keep interest rates low and stimulate the economy will be changing in the near future. As we see these policies change the interest rates will rise. Those who have been sitting on the fence would be well advised to research their lending possibilities and take advantage of the current low rates that are being offered.

Noelle Harris Barton Hills Mortgage Residential Lending, TXS&ML # 15414 Voice 512.699.8700 Fax 512.692.1973 [email protected] Apply Online: www.noelleharris.com

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

Average Price Austin vs. National

Austin Average National Average

$0

$50,000

$100,000

$150,000

$200,000

$250,000

Median Price Austin vs. National

Austin Median National Median

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

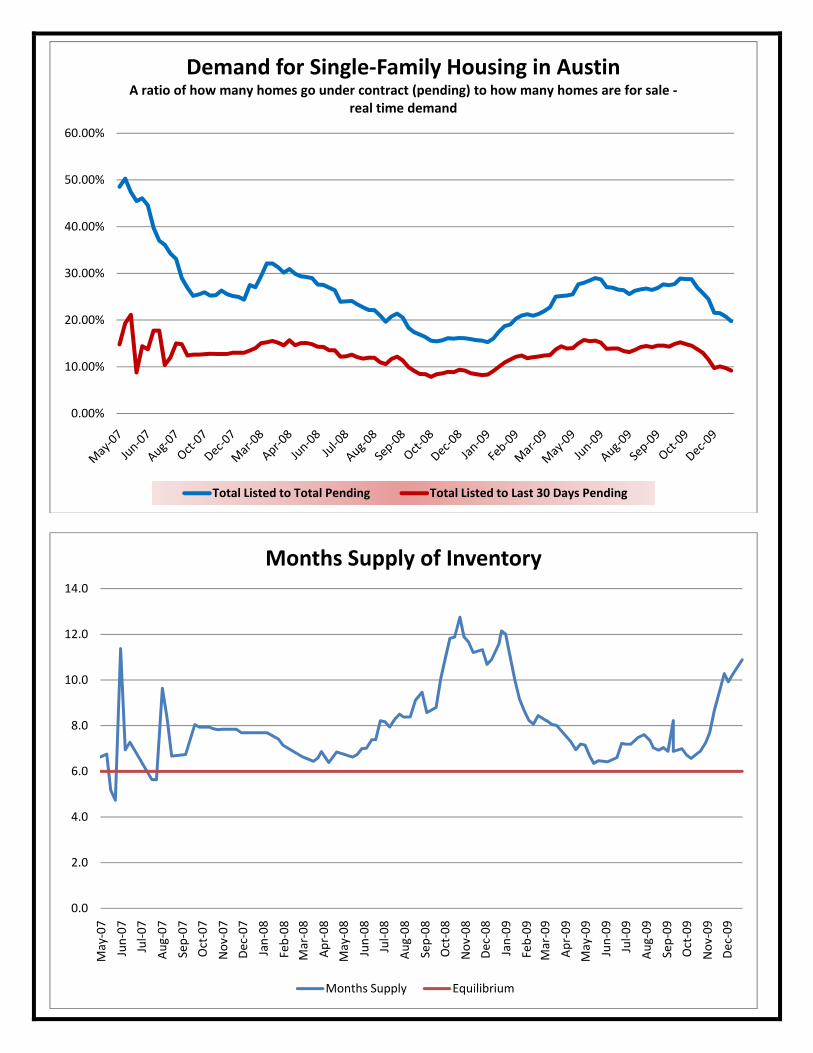

Demand for Single‐Family Housing in AustinA ratio of how many homes go under contract (pending) to how many homes are for sale ‐

real time demand

Total Listed to Total Pending Total Listed to Last 30 Days Pending

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

May‐07

Jun‐07

Jul‐0

7Au

g‐07

Sep‐07

Oct‐07

Nov‐07

Dec‐07

Jan‐08

Feb‐08

Mar‐08

Apr‐08

May‐08

Jun‐08

Jul‐0

8Au

g‐08

Sep‐08

Oct‐08

Nov‐08

Dec‐08

Jan‐09

Feb‐09

Mar‐09

Apr‐09

May‐09

Jun‐09

Jul‐0

9Au

g‐09

Sep‐09

Oct‐09

Nov‐09

Dec‐09

Months Supply of Inventory

Months Supply Equilibrium

0

10

20

30

40

50

60

70

80

90Jan‐02

Jun‐02

Nov‐02

Apr‐03

Sep‐03

Feb‐04

Jul‐0

4

Dec‐04

May‐05

Oct‐05

Mar‐06

Aug‐06

Jan‐07

Jun‐07

Nov‐07

Apr‐08

Sep‐08

Feb‐09

Jul‐0

9

Dec‐09

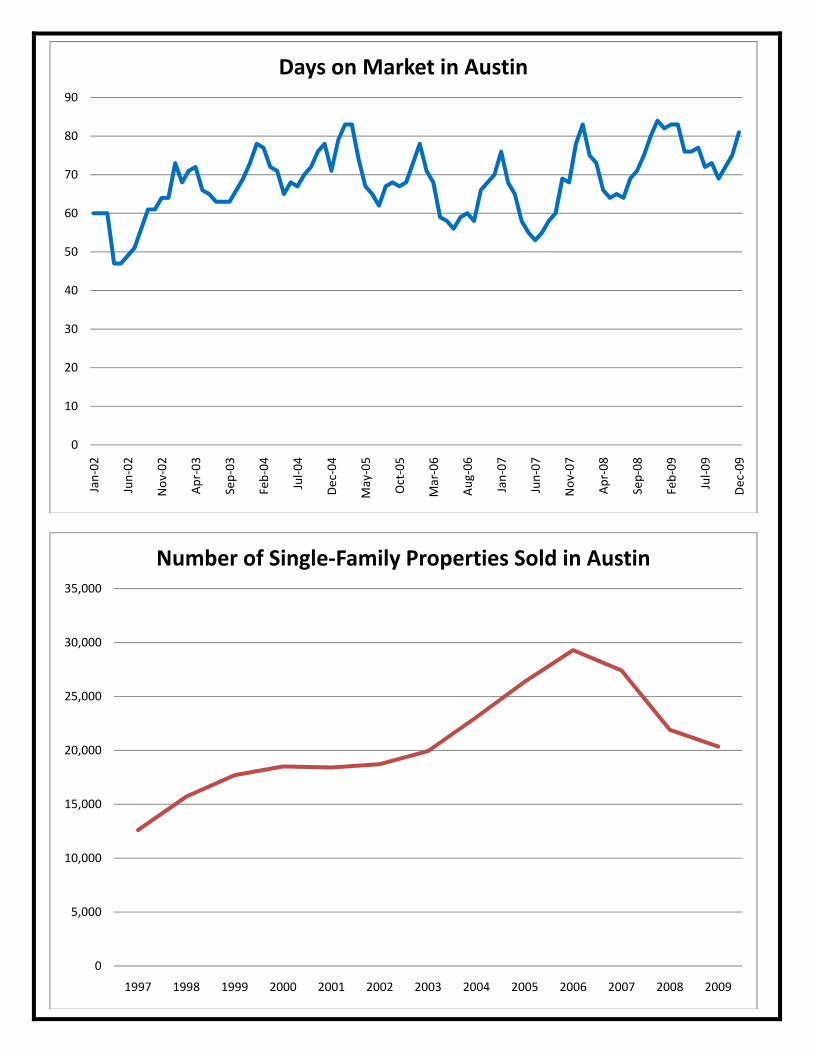

Days on Market in Austin

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Number of Single‐Family Properties Sold in Austin

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

Jan‐02

Jun‐02

Nov‐02

Apr‐03

Sep‐03

Feb‐04

Jul‐0

4

Dec‐04

May‐05

Oct‐05

Mar‐06

Aug‐06

Jan‐07

Jun‐07

Nov‐07

Apr‐08

Sep‐08

Feb‐09

Jul‐0

9

Dec‐09

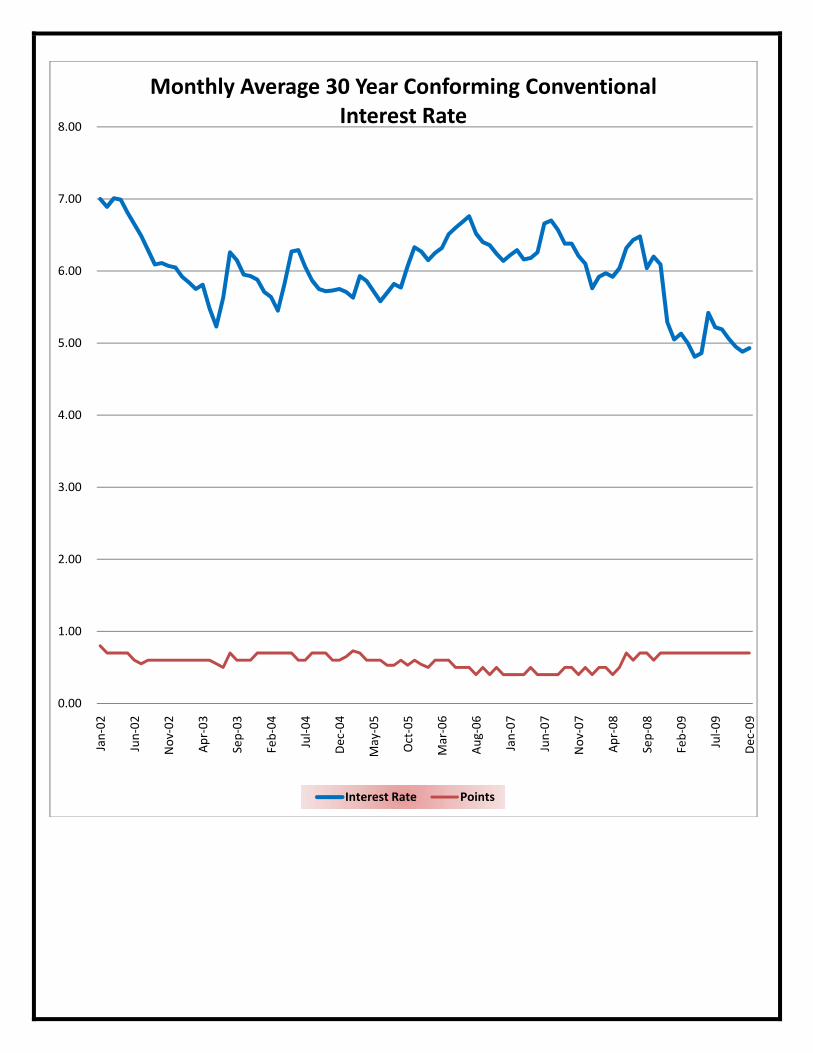

Monthly Average 30 Year Conforming Conventional Interest Rate

Interest Rate Points