report on working capital loan (prime bank)

TRANSCRIPT

Report on Working Capital Loan

Working Capital Management (FIN 340) Submitted to Muntasir Alam

Submitted by

Rashadat Anowar Chowdhury

ii

Letter of Transmittal 12-12-2011 Muntasir Alam School of Business North South University Dhaka Dear Sir, I am delighted to present you the “Report on Working Capital Loan”. The report includes different aspects, policies, procedures and principles regarding working capital loan. It also includes recommendation based on the analysis of current situation of working capital credit of Bangladesh. Your instructions where followed as strictly as possible during the course of making the report to deliver a vivid picture of working capital loan scenario of Bangladesh. Yours Sincerely Rashadat Anowar Chowdhury 0930101020

Report on Working Capital Loan

iii

Index

Preface iv Procedure for Obtaining a Working Capital Loan for a Textile Firm

6

Prime Bank’s Method of Determining the Maximum Limit for a Working Capital Loan

9

Problem Face by Prime Bank When They Sanction Working Capital Loan

12

Process of Adjusting Working Capital Loan by Prime Bank 15 Role of Different Ratio in Determining Working Capital Loan 16 Types of Loan Sanctioned by Prime Bank 18 Kind of Securities Accepted by Bank for Sanctioning Working Capital Loan by Prime Bank

20

Recommendation and Suggestion 23 Appendix Procedure of Sanctioning Working Capital Loan of Prime Bank Appendix I Prerequisites for a Business Loan Appendix II Checklist for Obtaining Working Capital Loan Appendix III

Report on Working Capital Loan

iv

Preface This report primarily focuses on current situation of working capital loan of Bangladeshi commercial banks. Prime Bank was taken as a model of bank and Textile industry was chosen as an i ndustry model. Information provided in the report may vary by bank and industry. In addition, this report offers a complete picture of procedures faced by a t extile firm to obtain a working capital loan from Prime Bank. As well as it describes what factors Prime Bank takes into account to judge or evaluate a firm’s short term credit request and its size. Formula and equation mentioned and used in this report may not be uniform, since different financial institution follows different model and guideline. The report mentioned many problems and dilemma’s faced by Prime Bank regarding working capital loan. Those problems were stated by employees of Prime Bank based on their personal and practical experience. Based on a nalysis of available information number of recommendation were made in the report.

Report on Working Capital Loan

Procedure for Obtaining a Working Capital Loan for a Textile Firm

o obtain a working capital loan or any kind of loan a firm must open an account with the respective bank, from which they are seeking or want to take a l oan. A bank generally offers two kinds of bank account such as Savings Account and Current

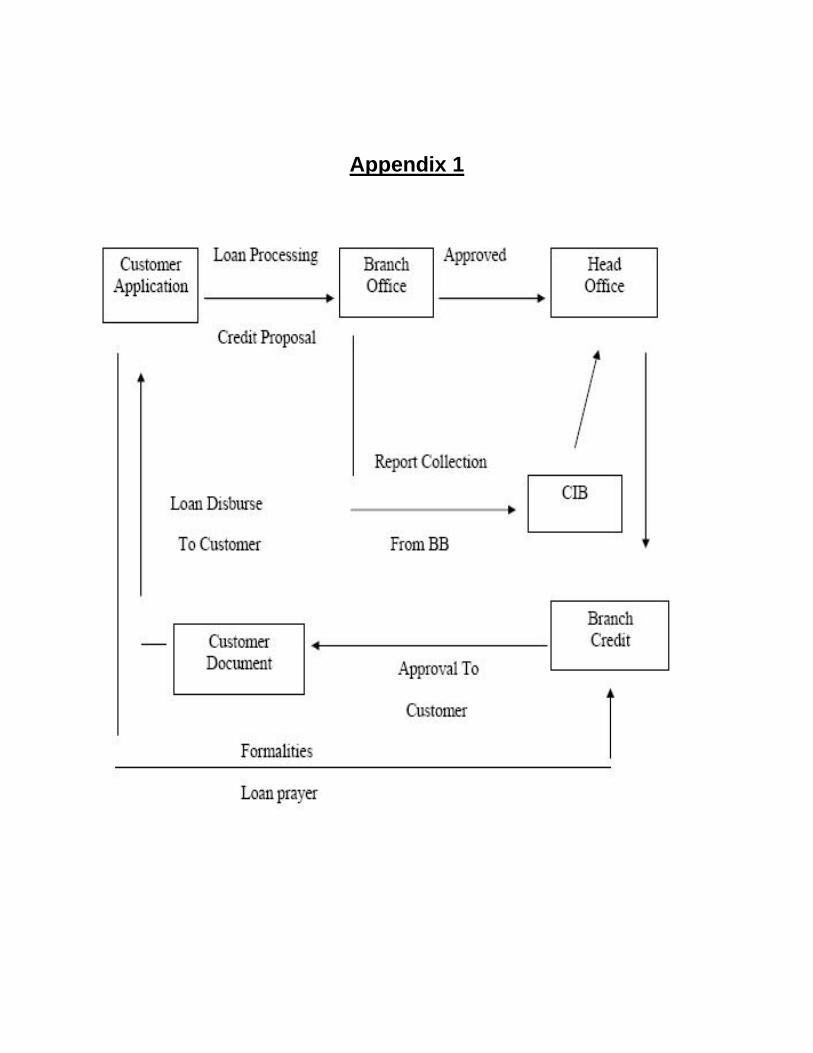

Account. In terms of firm or any business organization a current account is mandatory to have in order to obtain a bank account. There are several stages of credit approval which are done bot h at the corporate and branches office level. Below we will have a v ivid picture of steps followed by bank to provide loan to interested firm. (see appendix 1) Step 1: A loan procedure starts with a loan application from a client who must have an account with the Bank. At first it starts from the branch level. Branch receives application from client for a loan facility. In the application client mention what type of credit facility the company wants from the bank including firm’s corporate profile and financial information. Branch Manager or the Officer-in-charge of the credit department conducts the initial interview with company representative. (see appendix 2) Step 2: After receiving the loan application from the client, the bank sends a letter to Credit Information Bureau of Bangladesh Bank for obtaining a c redit inquiry report of the customer from there. This report is called CIB (Credit Information Bureau) report. This report is usually collected the credit information of customer. The purpose of this report is to be informed that whether or not the borrower has taken loans and advances from any other bank and if so, what is the status of those loans and advances i.e. whether those loans are classified or not. Step 3: If Credit information bureau (CIB) sends positive report on that particular borrower and if the Bank thinks that the prospective borrower is safe to grant loan, then the bank will examine the documents.

• Financial documents of the company for the last three to five years. Annual report and audit reports provide essential information of a firm’s financial performance and condition. In some case, the bank is allowed to analyze and audit the firm by external professional if the size of fund is huge. If the company is a new one, projected financial data for the same duration is required.

• In this stage, the bank will require whether the documents are properly filled up and

duly signed. Credit in charge of the relevant branch is responsible enquire about the in and out of the firm’s representative.

T

Report on Working Capital Loan 6

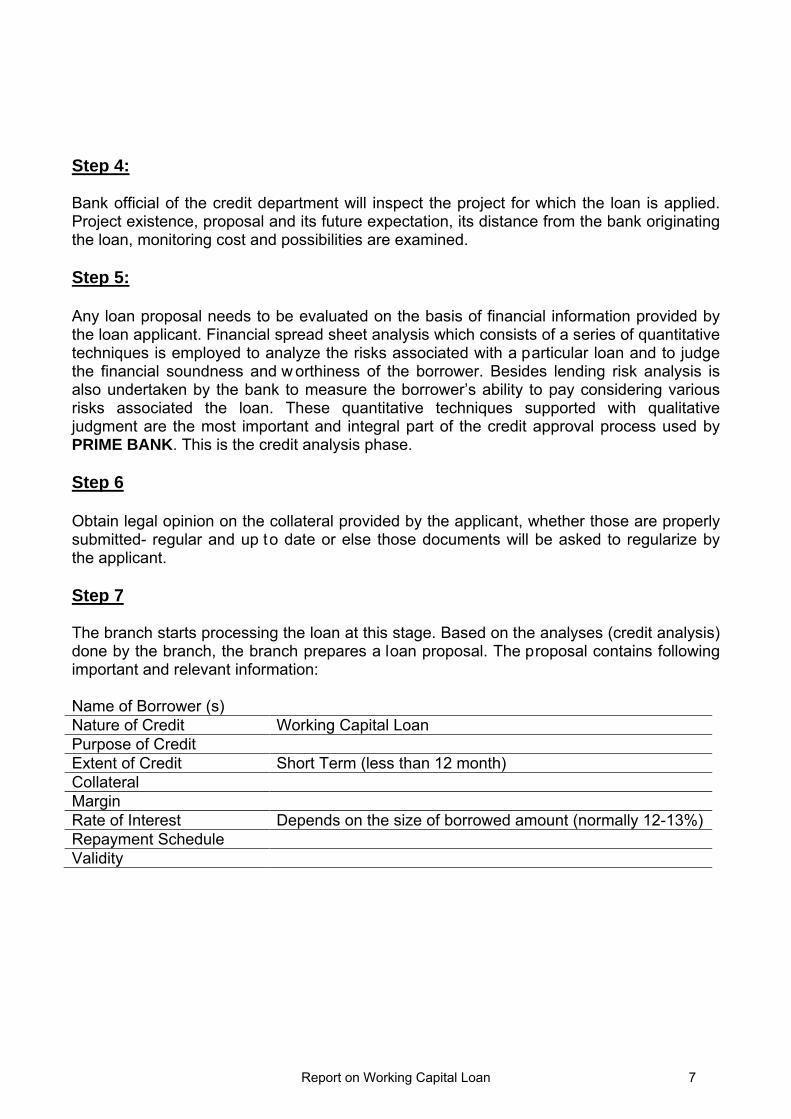

Step 4: Bank official of the credit department will inspect the project for which the loan is applied. Project existence, proposal and its future expectation, its distance from the bank originating the loan, monitoring cost and possibilities are examined. Step 5: Any loan proposal needs to be evaluated on the basis of financial information provided by the loan applicant. Financial spread sheet analysis which consists of a series of quantitative techniques is employed to analyze the risks associated with a particular loan and to judge the financial soundness and w orthiness of the borrower. Besides lending risk analysis is also undertaken by the bank to measure the borrower’s ability to pay considering various risks associated the loan. These quantitative techniques supported with qualitative judgment are the most important and integral part of the credit approval process used by PRIME BANK. This is the credit analysis phase. Step 6 Obtain legal opinion on the collateral provided by the applicant, whether those are properly submitted- regular and up to date or else those documents will be asked to regularize by the applicant. Step 7 The branch starts processing the loan at this stage. Based on the analyses (credit analysis) done by the branch, the branch prepares a loan proposal. The proposal contains following important and relevant information: Name of Borrower (s) Nature of Credit Working Capital Loan Purpose of Credit Extent of Credit Short Term (less than 12 month) Collateral Margin Rate of Interest Depends on the size of borrowed amount (normally 12-13%) Repayment Schedule Validity

Report on Working Capital Loan 7

Step 8 If the proposal meets PRIME BANK’s lending criteria and is within the manager’s discretionary power, the credit line is approved. The manager and t he sponsoring officer sign the credit line proposal and issue a sanction letter to the client. If the value of the credit line is above the branch manager’s limit then it is send to head office or zonal office for final approval with detailed information regarding the client (s), credit analysis and security papers. Step 9 Head office processes the credit proposal and afterwards puts forward an office notice if the loan is within the discretionary power of the head office credit committee or board memorandum if the loan requires approval from the board of directors. Step 10 If the zonal office, credit committee of the head of fice or the board as the case may be approves the credit line, an approval letter is sent to the branch. The branch then issues a sanction letter to the borrower with a duplicate copy. The duplicate copy duly signed by the borrower is returned to the branch of the bank. Step 11 After issuing the sanction advice, the bank will collect necessary charge documents. Charge documents vary on the basis of types of facility, types of collateral. (see appendix 3) Step 12 Finally loan is disbursed by the branch through a loan account in the name of the borrower and monitoring of the loan starts formally.

Report on Working Capital Loan 8

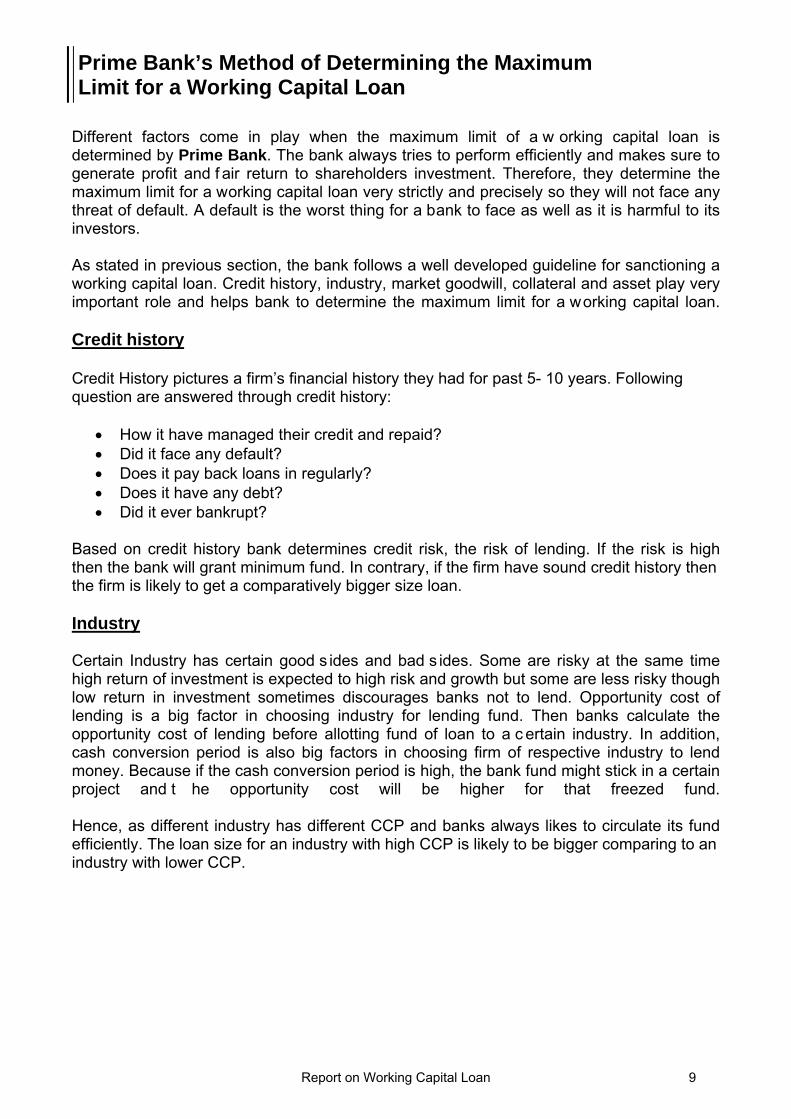

Prime Bank’s Method of Determining the Maximum Limit for a Working Capital Loan

Different factors come in play when the maximum limit of a w orking capital loan is determined by Prime Bank. The bank always tries to perform efficiently and makes sure to generate profit and f air return to shareholders investment. Therefore, they determine the maximum limit for a working capital loan very strictly and precisely so they will not face any threat of default. A default is the worst thing for a bank to face as well as it is harmful to its investors. As stated in previous section, the bank follows a well developed guideline for sanctioning a working capital loan. Credit history, industry, market goodwill, collateral and asset play very important role and helps bank to determine the maximum limit for a working capital loan. Credit history Credit History pictures a firm’s financial history they had for past 5- 10 years. Following question are answered through credit history:

• How it have managed their credit and repaid? • Did it face any default? • Does it pay back loans in regularly? • Does it have any debt? • Did it ever bankrupt?

Based on credit history bank determines credit risk, the risk of lending. If the risk is high then the bank will grant minimum fund. In contrary, if the firm have sound credit history then the firm is likely to get a comparatively bigger size loan. Industry Certain Industry has certain good s ides and bad s ides. Some are risky at the same time high return of investment is expected to high risk and growth but some are less risky though low return in investment sometimes discourages banks not to lend. Opportunity cost of lending is a big factor in choosing industry for lending fund. Then banks calculate the opportunity cost of lending before allotting fund of loan to a c ertain industry. In addition, cash conversion period is also big factors in choosing firm of respective industry to lend money. Because if the cash conversion period is high, the bank fund might stick in a certain project and t he opportunity cost will be higher for that freezed fund. Hence, as different industry has different CCP and banks always likes to circulate its fund efficiently. The loan size for an industry with high CCP is likely to be bigger comparing to an industry with lower CCP.

Report on Working Capital Loan 9

Market Goodwill Market goodwill plays an important role in determining the size of loan for bank. Every firm in market has to maintain a sound and positive corporate gesture through its performance. Performance not only refers to its provided service or manufactured product but also its responsibilities towards the well-being of society and nation. If a firm is contributing to noble causes for example empowering women entrepreneurship, helping people under poverty line or providing free primary education to street children etc. It directly helps firm to establish a sound status in the market. It is nearly impossible to calculate the market goodwill of a firm, but it helps banks to judge the size of loan can be granted to that firm. If a firm has better market goodwill, it will always seek to maintain it consequently there is a constant pressure on them to pay back their debt to avoid any financial dilemma or worst case, a bankruptcy. Thus, based on market goodwill a bank can determine the size of a working capital loan is making available to a firm. Collateral Collateral is a borrower's pledge of specific property to a lender, to secure repayment of a loan. The collateral serves as protection for a lender against a borrower's default. The value of collateral helps bank to assess the maximum limit for a working capital loan. The value of collateral must be greater than the maximum limit of loan. Since there is always a chance of default no matter how precise and sophisticated the credit assessment procedure is used. Bank will not risk losing its investment at any cost. We have discussed about collateral in “Kind of Securities Accepted by Bank for Sanctioning Working Capital Loan by Prime Bank” Asset The most important factor of determining the maximum limit for a working capital loan is asset. Asset consist cash balance, fixed asset, account receivables, equipment etc. Asset reflects a firm’s ability to repay the loan as well as equity. Cash balance is the most liquid asset. Based on the size of cash balance, a bank determines the size of loan to be sanctioned. It has been seen to avoid tax, firms sometimes prefers to take loan by keeping their cash balance intact. Though it is a risky policy but firm become profitable through this policy and day by day it is becoming popular. Accordingly, if a f irm asks for a loan though they have sufficient fund of their own. Bank seeks the amount of cash balance the firm has. The loan size is likely to be smaller than the cash balance the firm has. Therefore, in case of default, the bank do not loses its investment since the firm cash balance is greater than the size of loan. In addition, account receivables also helps bank to determine the size of loan alike the cash balance. Thus, the bank always tries to verify the value of security which helps them to assess the possible size of loan can be offered to firm.

Report on Working Capital Loan 10

Calculation:- The formula or model for calculating the maximum limit of working capital loan defers from bank to bank. In addition Bangladesh Bank does provide a guideline to manage credit risk for bank but it do not provide any model or procedure to calculate the maximum limit of working capital loan. The regulator of bank in case of Bangladeshi banking sector, Bangladesh Bank don’t provide any specific model to determine the maximum limit of working capital loan and there is no u niform model followed by banks to determine maximum working capital loan limit. Since, banks reject to share such model for research purpose. The model shown below consist basic elements which helps to determine the maximum limit of working capital loan. It must be added that models are developed and revised with the need of financial institutions for making the loan system more secured, safe and efficient for both borrowers and lenders. Working Capital Requirement = Current Asset – Current Liabilities. Generally, a w orking capital loan is taken by a f irm when it’s current asset < current liabilities that mean working capital requirement is negative. We can use company balance sheet as reference for current asset and current liabilities of a firm. Current assets are any cash or asset that can be quickly turned into cash which includes prepaid expenses, accounts receivable, most securities and your inventory. Current liabilities are a l iability in the immediate future which includes wages, taxes, and accounts payable. By calculating the negative difference between current asset and current liabilities banks can compute working capital requirement of a f irm. In addition, banks considered future value of collaterals to make its investment safe and s ecure in case of default. Thus different banks use different method to asses or determine the maximum limit of working capital loan. Here I have discussed on perspective Prime Bank for determining the loan limit. In must be said that the financial sector is developing and changing day by day to provide better, efficient and ha ssle free financial and trading facility to its consumer. Factor’s mentioned above were based on the practical experience faced by bank employees while determining a credit application.

Report on Working Capital Loan 11

Problem Face by Prime Bank When They Sanction Working Capital Loan

Generally after sanctioning a w orking capital loan, Prime Bank generally monitors the activity of firm and m akes sure that the firm is not involving into any risky investment or activity which might or will harm the investment of bank. But it is possible and i t does happen that firm’s involves in risky investment without the bank know about it and in some cases they face default. So, bank always makes sure that their investment is sound and s afe and i t is their maximum concern after sanctioning a loan or working capital loan. In addition, bank faces varies kinds of problem while sanctioning working capital loan. Generally following assessment dilemmas are face by bank while sanctioning working capital loan: -

• Intention of Client

• Sources of Loan Repayment

• Value and Durability of Collateral

• Outcome of Investment

Intention of Client Every client comes to bank for working capital loan with a common reason that is they need funds to continue their firm’s regular operation and in almost every case banks accept client’s request. But it is tough for banks to determine the honesty, truth and pure intention of client to take working capital loan. It is possible that borrowers might use the loan fund for more riskier investment which might cause default or bank have different policy and scheme for such investment and i t has been seen that clients asking for working capital loan for such investment activity were proposed to other loan scheme which consist higher interest rate, more complex procedure and policy for credit sanction. But acceptance rate of those loan scheme are not as high as working capital loan and it must be said that those loan scheme requires more valuable collateral and processing time is greater than working capital loan. However, borrowers do not want to get into such complex and time consuming procedure beside long term loan scheme charges higher interest rate and borrowers always prefers to choose schemes, which charges comparatively low interest rate. Therefore borrowers seek working capital loan and investment in non working capital activity which might be r ated highly risky investment by bank if they analyze it.

Report on Working Capital Loan 12

Source of Loan Repayment During analyzing a c redit request of firm, one of the important factor bank analyses very precisely is the source of loan repayment. If the source of loan repayment is not clear or transparent to bank than it could cause a major setback for approving loan request. As a result, firm’s shows strong sales figure and other asset balance through balance sheet and other financial statements. Bank uses financial statements as reference to evaluate the credit request of a f irm. In some cases the bank might ask for an independent audit if requires, which ensures that the financial stability and performance of the firm is good for investment. In contrary, financial statement also might not picture the actual situation of a firm. It might be developed to grab the attention investor. But it is not possible for bank to find out the exact flow of fund from the source of loan repayment. Source might fail to perform as expected and in cases of default it might disappear as well. Value and Durability of Collateral Value of collateral helps bank to determine the size of loan. But what if the value of collateral is overstated? There is a pos sibility that value of collateral fluctuates. In some cases, it might be seen that value of land which was kept as collateral has increases but in different cases it might be obs erved that value of that had s everely fall due to a nat ural disaster. As a result, while sanctioning working capital loan, it faces difficulty to assess the value of collateral and in this case they have to consider the whole economy and its future aspect as well. If the economy faces a recession, the value of collateral such as land or building is likely to fall. This will endanger the investment of bank. On the other hand, account receivables and third party guarantee are used as collateral as well. It is normal for business to face profit and lose. We can expect a bus iness to make profit all the time. But bank do not accept this fact. Bank has a target, maximizing the wealth of shareholders and m aking a pr ofitable return to investors for their investment. Account receivables and third party guarantee might fail as collateral. A chain reaction is observed in every market. As Suppliers relies on their buyer, buyers to rely on suppliers as well. So if one business fails it will affect others as well. Therefore, durability of collateral is another difficulty bank face to asses. Thus bank faces though time to evaluate the collateral’s value and durability. They cannot determine these factors precisely. Therefore, they always provide less amount working capital loan comparing to respective collateral.

Report on Working Capital Loan 13

Outcome of investment We can predict the outcome of investment but we cannot ensure the outcome of investment. A firm, which is achieving record sales in last year, might go bankrupt this year due to better competition, lack of development, fall of consumption or shock event. In other word, we can say that we can ensure success through numbers and f inancial statements because success and failure depend on countless factors. Bank faces tough time to determine the outcome of investment and t his problem can be solved only if the market is control by bank itself. Hence, we have highlighted the problems faced by bank while sanctioning working capital loan. These problems are generally faced by bank and now a day’s via development of banking sectors and human resource. Analyst has become more mature and efficient to justify these problems and makes sure the bank investment is safe and secure.

Report on Working Capital Loan 14

Process of Adjusting Working Capital Loan by Prime Bank

Prime Bank provides loan adjustment facilities to its borrowers. It has been seen that borrower’s faces trouble to pay back their loan due to lack of slow flow of fund they expect while taking the loan. A loan adjustment is a c hange to the loan terms that is agreed to by and bet ween the bank and the loaner. The bank will modify the existing loan(s) in order to work with the borrower because of a hardship. The purpose is to help make the loan(s) more affordable. Usually loan adjustments are in the form of a r ate reduction and/or fixing the rate for a c ertain period of time and/or even lowering the principal balance in extreme cases. Loan adjustments are only utilized when a borrower is delinquent and suffered a hard ship such as a adverse effect on business operation, loss, shock fall in sale, or failure to provide expected cash flow. Prime Bank follows a l ess complicated and ef ficient loan adjustment procedure for working capital loan:- Adjustment of working capital loan depends on different factors. These factors are same factors which helps banks to determine the maximum amount of loan can be sanctioned to a specific loaner.

Step 1 Whenever a firm found tough to maintain the burden of working capital loan, it discuss about problems with bank. And bank always try to avoid default for its own benefit. If the bank takes the situation into consideration, it consults with firm’s representative to find out the best loan adjustment possible. Step 2 After finding out a be st solution, bank verifies the tough situation by analyzing recent financial statement, credit history and other important aspects which are essential for finding out the problem as well as proving the security that adjustment of working capital loan will help the firm to achieve its goal. Step 3 Following the Important analysis of different factors, bank again meet the firm’s representative, share their views and analysis with them. In this stage, bank negotiates with firm about the possible outcome of adjustment. This negotiation continues until mutually acceptable decision is made. Step 4 Finally , when a mutually acceptable decisions is made, bank approve the loan adjustment of working capita loan and the firm comes under the adjusted working capital loan to reach its goal and payback the loan as well. Process of working capital loan adjustment varies by the preference of bank and clients. For some client it might take few days to approve but for other it might take weeks. Firm’s performance and future aspect plays key part in approving the adjustment of loan.

Report on Working Capital Loan 15

Role of Different Ratio in Determining Working Capital Loan We discussed before that bank uses different factor to evaluate a credit request of a firm. In some cases bank do evaluate them by using certain ratio. Ratio analysis helps bank to establish financial healthy and stability of a f irm for 5-10 fiscal year. Below we discuses about some important ratios which helps bank to evaluate a working capital credit request: Days Sales Outstanding Day’s sales outstanding is a calculation used by a company to estimate their average collection period. A low number of days indicate that the company collects its outstanding receivables quickly. Typically, Days sales outstanding are calculated monthly. Bank uses DSO to asses a firm’s ability to collects its receivables. If it has high DSO then bank might suggest firm’s management to increase its collection. In addition, if a f irm chooses account receivables as collateral than DSO will play a v ery important role to determine the working capital loan. Days Inventory Held Days inventory held ratio is used to determine how quickly a company is converting their inventory into sales. A slower turnaround on sales indicates than the firm is not active or efficient enough to convert its inventory into sale. In some cases, inventories are not durable enough which might harm firm financially well due to a slow turnaround on sale. Bank uses DIH ratio to asses a f irm’s ability to turnaround its inventory into sale. If it is having a s low turnaround that bank might suggest firm’s management to increase its turnaround. Operating Cycle Operating cycle is the summation of day’s inventory held and day’s sales outstanding. This ratio reflects how efficiently the firm is operating itself. The greater the operating cycle of a firm, the greater inefficient it is. Operating cycle generally shows the fund used for operational purpose by a firm and its flow. Bank uses operating cycle ratio to asses a firm’s flow of operation fund. If OC is small than the firm to good enough to provide a working capital loan cause it is efficient, if OC is big than its can cause a big setback for having a w orking capital loan.

Report on Working Capital Loan 16

Cash Conversion Period Cash conversion period is the difference between operating cycle and day’s payable outstanding. The greater the cash conversion period, the greater financial strain on the firm and the less liquid it is. A long cash conversion period can absorb a significant amount of liquidity during a per iod of growing sales and t herefore it must be m anaged carefully. In terms as factors for bank to evaluate a working capital credit request, this ratio helps bank to understand the liquidity and f inancial flexibility of the firm. As mentioned above, if the firm has greater CCP than it struggles to pay its obligations. In other word, financially the firm is inefficient and lacks of liquidity might fail the firm to pay loan repayment on time. Role of Ratios in Reality If bank considers all factors to determine a w orking capital credit request then it will be difficult for firm’s to get loan. Though in some cases, bank considers CCP and DSO cause these two ratios are directly related to important factors such as liquidity, financial flexibility and account receivables collection of a firm. Flow of fund within firm’s operation and flow of repayment from source concerns bank while sanctioning or analyzing a w orking capital loan. Thus, ratios do play important role while evaluating a working capital credit request.

Report on Working Capital Loan 17

Types of Loan Sanctioned by Prime Bank Prime Bank offers different kind of financial products including loan, different types of account. It primarily focuses on five (5) different kind of banking such as Retail Banking, Corporate Banking, Islamic Banking, SME Banking and Agricultural Banking. Retail Banking :-

Home Loan CNG Conversion Loan Marrige Loan Household Durable Loan Education Loan Any Purpose Loan Doctor’s Loan Travel Loan Hospitalization Loan Loan Against Salary

Corporate Banking:-

General Credit Unit (GCU)

Short Term Finance Long Term Finance Real Estate Finance Import Finance / Trade Finance Work Order Financing

Export Finance Unit (EFU) Project Loan

Working Capital Loan Structured Finance Unit (SFU) Project Finance Acquisition Finance Securitization Advisory Investment Procedure

Lease Finance Unit (LFU) Agricultural Banking :-

Crop Loan Farm / Non Crop Loan

Report on Working Capital Loan 18

Islamic Banking:-

Investment Home Investment Auto Investment

Household Durable Investment Medical Investment

Hire Purchase under Shirkatul Melk concept Bai Mechanism Hire Purchase / Ijara SME Banking :-

Easy Loan Capital Loan Working Capital Loan Seasonal Loan Double Loan

Women Entrepreneurs Loan

Report on Working Capital Loan 19

Kind of Securities Accepted by Bank for Sanctioning Working Capital Loan by Prime Bank Prime Bank has a strict and c omplex set of policy in terms of preferring security or collateral for sanctioning working capital loan. Though in some case, the bank doesn’t ask for security if the borrower has sound credit history and goo dwill in market. List of collateral are given below:-

• Account Receivables

• Stock

• Government Bond

• Third Party Guarantee

• Fixed Asset

Account Receivables Accounts receivable represents money owed by entities to the firm on the sale of products or services on credit. In most business entities, accounts receivable is typically executed by generating an invoice and either mailing or electronically delivering it to the customer, who, in turn, must pay it within an established timeframe, called credit terms or payment terms. Direct sale of accounts receivable is called factoring. A loan from a ba nk secured or collateralized against accounts receivable is known as a di scount, where the borrower draws against a l ine of credit that is less than the full value of the trade credits. Accounts receivable financing is a flexible way of obtaining credit, and borrowers’ financing costs are related directly to their business cycle. In a general assignment, all receivables can serve as collateral, with new receivables substituted for those collected. In a specific assignment, the parties involved can specify who will receive collection, whether customers will be notified of the arrangement, and which accounts are to be collateralized. Accounts receivable factoring is different from using accounts receivable as loan collateral because borrower sell the receivables to a factor at a di scount. In this case a f actor is referred as Prime Bank. The factor then collects the debt and b orrower doesn’t have to worry about loan repayments When a loan is obtained from a bank with receivables as collateral, there are rather more formal guidelines. Bank and finance companies insist on weekly reports on s ales, collections, and i neligibility analysis, as well as internally generated financial statements with detailed accounts receivable and accounts payable information. The amount borrowed is then repaid within a specified short-term period as the receivables are collected.

Report on Working Capital Loan 20

Stock The capital stock (or just stock) of a business entity represents the original capital paid into or invested in the business by its founders. It serves as a security for the creditors of a business since it cannot be w ithdrawn to the detriment of the creditors. Stock is different from the property and the assets of a business which may fluctuate in quantity and value. Loan taken by using stock as collateral are knows as stock loan. It is an advance of cash based on the value of stock that is held by a person or company. When a stockholder in a company is in need of assistance and does not wish to sell his or her shares, holding on to them as a c rucial investment, then the stockholder can find lending companies that will issue stock loans, using the stocks as collateral. Sometimes, within a company, the holding company may even issue an advance to stockholders, negating the need to put up shares as collateral to an outside party. There are many reasons that a stockholder may want to borrow money against his or her held stocks. Sometimes getting this funding may save an investor from complete liquidation and by not selling the stocks, there will be no sales taxes involved with the transactions. Though using stock as collateral has a good side and a bad side. Good side is it has value but the price of stock fluctuates a lot at the same time. Government Bond Government bond o r T-Bills are the safest bond f ound in an independent economy. Generally these kinds of bonds are issue by Central Bank or Federal Reserve of a country. They have maturity of 3, 6 or 12 months and pay a stated amount at maturity, but sell for less than that (at a discount), effectively paying some rate of interest. All debt issued by the Government are considered default free. Whenever, a Government issues new bond, it call for auction for it. Corporation and firms with huge capital and liquid cash get attracted to such investments. Since it is a default free investment and pay’s a decent interest rate of 6-7% firm’s purchase these bonds for future security so they can use it has collateral or create Repo whenever they need fund. Repurchase Agreements (Repos) are short-term loans secured by T-Bills. The bor rowers sell the lender a T-Bill with an explicit agreement to buy it back within a short period of time at a higher price. So the T-bill is collateral for the loan and the higher buyback price implies some interest rate.

Report on Working Capital Loan 21

Third Party Guarantee For businesses that cannot provide sufficient collateral to secure a s hort term loan, a complex and multi-level approach to structuring the transaction makes it possible to successfully receive venture capital funding, without any collateral from the client. This category of capital procurement requires extensive inside financial industry knowledge, legal and negotiating expertise, and di rect, active professional support. Using third party guarantee is popular among newly started business who seeks working capital loan. Since they lacks fund as well as other securities to use as collateral for a loan a third party comes into the play and guarantees to pay all obligations against the borrowers in case of a default. If the borrowing firm fails to pay back loan then bank will ask the third party, who guaranteed the safety of bank’s investment to pay back the loan. Fixed Asset Fixed assets or property, plant, and equipment are assets and property which cannot easily be converted into cash. Moreover, a fixed can also be defined as an asset not directly sold to a firm's consumers. These are items of value which the organization has bought and will use for an extended period of time; fixed assets normally include items such as land, building, motor vehicles, furniture, office equipment, computers, fixtures and f ittings, and pl ant and machinery. Fixed assets are very popular when it is used as collaterals. They are durable, well valued and tangible. Bank’s prefers fixed asset as collateral because these collateral outcomes are easily predictable. Beside it has been seen borrowers who keeps fixed asset as collateral has regular loan repayment and avoid defaults. Therefore, bank always favors applicants with fixed collateral whenever credit request are submitted. Hence, Prime Bank uses primarily these types of collateral while sanctioning working loan capital and choosing collateral makes important impacts on loan repayment and outcome of loan as well.

Report on Working Capital Loan 22

Recommendation and Suggestion

Working Capital Loan is a k ind of loan scheme which enriches and nurtures the development of different trading sector. It is a very useful debt instrument and day by day it is becoming very popular among traders of all sectors. It requires less security and charges less interest rate. So, trader’s takes risk by taking working capital loan to make their operation more efficient. Thou gh it must be said the current scenario of working capital loan of Bangladesh still has room for development. Now a day s, SME and m icro credit scheme have become very popular as well among small or medium trader of different sector. As a result in near future businesses might become discourage to take working capital loan. In addition, as I have mentioned in this report, bank faces different dilemma while sanctioning a working capital loan. Since these types of loans are easy to get, comparing to other long term loan. Based on my perspective and analysis I would like to recommend following things for making working capital loan more secured, efficient and po pular for both banks and businesses.

• Introduce sophisticated software for calculating credit risk score. • Improve the skill of credit analyst

• Upgrade the credit analysis model on annual basis.

• More Information about collateral should be provided to bank.

• Bank should be provided more authority over investigating collateral.

• Outcome of investment should be predicted for precisely.

• Bangladesh Bank should build an uni form model for all banks to calculate the

maximum limit for a loan.

• Valuation of collateral should be done by taking the economic satiation of the country under consideration.

• Monitoring procedure of a loan taker should be done properly

I believe recommendation present above will make the working capital loan system more protected, well-organized and profitable.

Report on Working Capital Loan 23

Appendix 1

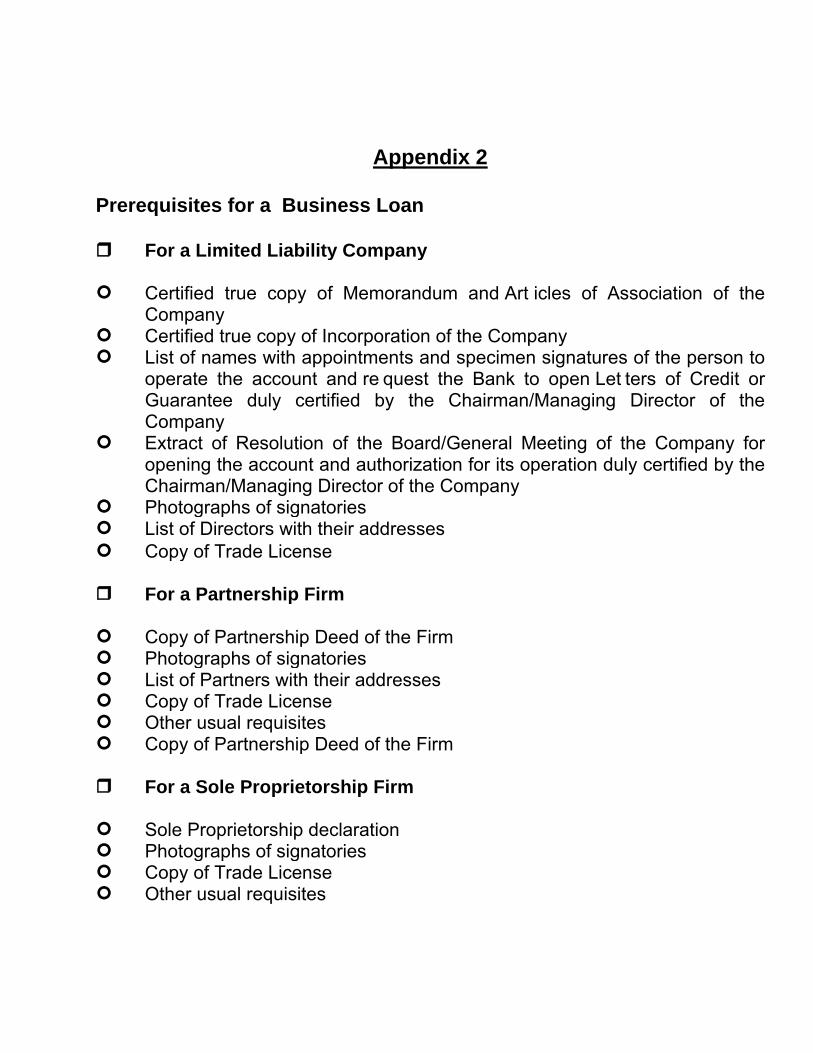

Appendix 2

Prerequisites for a Business Loan For a Limited Liability Company Certified true copy of Memorandum and Art icles of Association of the

Company Certified true copy of Incorporation of the Company List of names with appointments and specimen signatures of the person to

operate the account and re quest the Bank to open Let ters of Credit or Guarantee duly certified by the Chairman/Managing Director of the Company

Extract of Resolution of the Board/General Meeting of the Company for opening the account and authorization for its operation duly certified by the Chairman/Managing Director of the Company

Photographs of signatories List of Directors with their addresses Copy of Trade License For a Partnership Firm Copy of Partnership Deed of the Firm Photographs of signatories List of Partners with their addresses Copy of Trade License Other usual requisites Copy of Partnership Deed of the Firm For a Sole Proprietorship Firm Sole Proprietorship declaration Photographs of signatories Copy of Trade License Other usual requisites

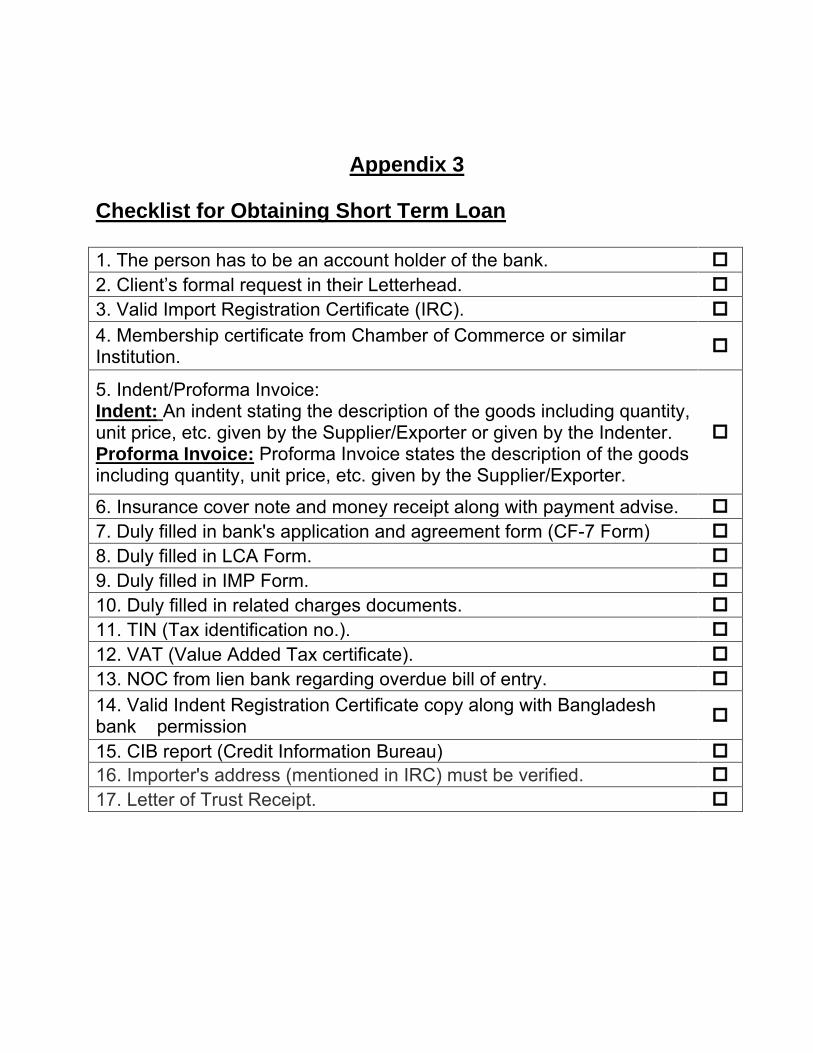

Appendix 3

Checklist for Obtaining Short Term Loan 1. The person has to be an account holder of the bank. 2. Client’s formal request in their Letterhead. 3. Valid Import Registration Certificate (IRC). 4. Membership certificate from Chamber of Commerce or similar Institution.

5. Indent/Proforma Invoice: Indent: An indent stating the description of the goods including quantity, unit price, etc. given by the Supplier/Exporter or given by the Indenter. Proforma Invoice: Proforma Invoice states the description of the goods including quantity, unit price, etc. given by the Supplier/Exporter.

6. Insurance cover note and money receipt along with payment advise. 7. Duly filled in bank's application and agreement form (CF-7 Form) 8. Duly filled in LCA Form. 9. Duly filled in IMP Form. 10. Duly filled in related charges documents. 11. TIN (Tax identification no.). 12. VAT (Value Added Tax certificate). 13. NOC from lien bank regarding overdue bill of entry. 14. Valid Indent Registration Certificate copy along with Bangladesh bank permission

15. CIB report (Credit Information Bureau) 16. Importer's address (mentioned in IRC) must be verified. 17. Letter of Trust Receipt.