remedies for distress - aciclaw.org · restructuring plan to serve their best interest positioning...

TRANSCRIPT

ACIC Annual Fall MeetingOctober 20 – 21, 2016

Remedies for Distress: Nuances of the 363 Sale Process

Paul Ferdinands, King & Spalding LLPLarry Halperin, Chapman and Cutler LLPJay Jacquin, Guggenheim Partners LLCJeffrey Manning, CohnReznick Capital Market Securities

DanfurnManagement

LLC

100%

Danfurn LLC

Danfurn Stores LLC

Danfurn Manufacturing

LLC

Danfurn Organizational Structure

- 1 -

LBO Debt Financing Structure

TrancheBorrowing Entity

Amount($ millions) Rate Maturity Relevant Covenants Guarantee

M&L Senior Secured Revolving Loan

Danfurn LLC 15.0 LIBOR+ 425

March 2016 Maintenance-based limitations on the incurrence of additional indebtednessand liens, payment of dividends,repurchases of capital stock, sales ofassets, and changes in control. Financialcovenants include: consolidatedadjusted EBITDA must exceed $8.5million; capital expenditures cannot exceed $3.0 million.

Danfurn Management LLC

M&L Senior Secured Term B Loan

Danfurn LLC 85.0 LIBOR+ 450

March 2017 Maintenance-based limitations on the incurrence of additional indebtednessand liens, payment of dividends,repurchases of capital stock, sales ofassets, and changes in control. Financialcovenants include: consolidatedadjusted EBITDA must exceed $8.5million; capital expenditures cannot exceed $3.0 million.

Danfurn Management LLC

10.345% Senior Mezzanine Notes + Equity Warrants

Danfurn Management LLC

30.0 10.35% August 2017 Incurrence-based restrictions onadditional indebtedness and liens andchanges in control. Notes also containcross-acceleration and cross-defaultprovisions tied to the Senior CreditFacilities.

None

- 2 -

* Excludes bad debt charges.

2010 2011 2012 2013 2014Net sales $ 294,321 $ 454,905 $ 503,295 $ 425,706 $ 332,843Cost of sales 191,309 309,335 339,724 303,954 241,977Gross profit 103,012 145,570 163,571 121,752 90,866

Selling, general, and administrative expenses excluding bad debt and notes receivable valuation charges 92,858 129,648 142,432 117,495 90,200Bad debt charges (1,549) (2,135) 11,769 15,205 6,567Profit (Loss) from operations 11,704 18,057 9,369 (10,948) (5,901)Interest expense (125) (232) (9,084) (7,722) (7,516)Loss before income taxes 11,579 17,825 285 (18,670) (13,417)Income tax benefit (provision) (4,052) (6,239) (100) 6,534 4,696

Net gain (loss) $ 7,526 $ 11,586 $ 186 $ (12,135) $ (8,721)

Depreciation & amortization 9,253 9,089 8,089 6,604 5,966EBITDA* 19,408 25,011 29,227 10,861 6,632Capital expenditures (net of sales of PP&E) (5,202) (2,743) (2,698) (967) 2,234

Danfurn Management LLCConsolidated Statement of Operations(in thousands of dollars)

- 3 -

2014 2013 2014 2013Assets Liabilities and Stockholders’ EquityCurrent assets Current liabilitiesCash and cash equivalents $ 6,017 $ 10,574 Accounts payable $ 15,786 $ 11,523Accounts receivable 33,621 38,225 Accrued compensation and benefits 6,322 6,157Inventories 41,810 33,388 Other accrued liabilities 14,983 11,730Other current assets 6,969 13,312 Current portion of bank loan 2,200 2,500

Total current assets 88,417 95,499 Total current liabilities 39,291 31,910

Long-term assets Long-term liabilitiesProperty and equipment, net 65,950 70,636 Post-employment benefit obligations 5,920 4,328Retail real estate 27,513 28,793 Bank debt 90,895 95,595Other 3,465 3,034 10.345% senior mezzanine notes 30,000 30,000

Total long-term assets 96,928 102,463 Other long-term liabilities 3,256 8,877

Total assets $ 185,345 $ 197,962 Total long-term liabilities 130,071 138,800

Commitments and Contingencies

Stockholders’ equityCommon stock 15,733 15,733Retained earnings 199 8,920Additional paid-in capital 478 481Accumulated other comprehensive income (loss) (427) 2,118

Total stockholders’ equity 15,983 27,252

Total liabilities and stockholders’ equity $ 185,345 $ 197,962

Danfurn Management LLCConsolidated Balance Sheet(in thousands of dollars)

- 4 -

RecoveryLow Case Mid Case High Case Notes($ in USD millions)

Run Rate EBITDA EBITDA Multiple

$10.0 5.5x

$15.0 8.0x

$20.0 9.5x

$55.0 $120.0 $190.06.0 6.0 6.0

$61.0 $126.0 $196.0(3.7) (3.7) (3.7)

TEVPlus: Cash

From Cap IQ Comp Range

Distributable Value TEV + CashLess: Administrative Claims Assume: 3% of 2010 Debt

Residual Value Available for Secured Creditors $57.3 $122.3 $192.3 Distributable Value - Admin ClaimsSecured Debt Revolver $8.1 $8.1 $8.1TLB 85.0 85.0 85.0 Amt. Outstanding

Total Secured Debt $93.1 $93.1 $93.1Recovery Rate for Secured Creditors 61.6% 100.0% 100.0% Value available to secured holders

as a % of Total Secured DebtResidual Value Available for Unsecured Creditors $0.0 $29.2 $99.2 less Total Secured Debt.Unsecured Debt Amt. OutstandingSr 10.375% Notes $30.0 $30.0 $30.0 From Case exhibitsAccounts Payable 15.8 15.8 15.8 From Case exhibitsOther General Unsecured Creditors 15.0 15.0 15.0

Total Unsecured Debt $60.8 $60.8 $60.8 Value available to secured holdersRecovery Rate for Unsecured Creditors 0.0% 48.1% 100.0% as a % of Total Unsecured Debt

Value available to unsecured holdersResidual Value Available for Equity Holders $0.0 $0.0 $38.5 less Total Unsecured Debt.

Danfurn Management LLCPreliminary Waterfall Model as of 2015

5- 5 -

Section 363 Creates Three Statutory Requirements

I. Requirements of a 363 Sale

§ Assets being sold must be “Property of the Estate.”

§ Sale must be outside the ordinary course of business.

§ There must be notice and a hearing culminating in the Bankruptcy Court approving the sale.

6- 6 -

§ “Property of the estate” includes all legal or equitable interests of the debtor in property as of the date that the bankruptcy case is commenced. 11 U.S.C. § 541(a).

§ Unless a particular federal interest requires a different result, property interests are created and defined by state law.

§ Property becomes property of the estate only to the extent of the debtor’s interest – bankruptcy does not create any new rights or property interests. If ownership is disputed, court must first determine ownership prior to authorizing a sale.

I. Requirements of a 363 Sale (continued)

What’s Being Sold Must Be “Property of the Estate”

7- 7 -

I. Requirements of a 363 Sale (continued)

§ Most courts apply both a “horizontal” and a “vertical” dimension in determining whether a transaction is in the ordinary course of business:

- Horizontal Test – a/k/a the “industry-wide test” – whether the transaction is of a kind commonly undertaken by companies in that industry based on an industry-wide perspective.

- Vertical Test – analysis of the transaction from a creditor’s perspective – is this the type of transaction this particular debtor regularly engaged in pre-petition.

§ A sale in the ordinary course of business does not require bankruptcy court approval or notice.

Must Be “Outside the Ordinary Course of Business”

- 8 -

§ The “typical” M&A process doesn’t effectively serve distressed companies that are facing unique and challenging corporate finance issues often found in distressed sales, including:

II. Should the Company Be Sold In or Out of a Bankruptcy?

Business Considerations

Timing - Liquidity constraints and creditor imposed deadlines require accelerated timelines

Multiple Constituencies

- Various creditors often have conflicting agendas and will attempt to influence the Company’s restructuring plan to serve their best interest

Positioning - The marketing process should be carefully crafted to:• Mitigate buyers’ concerns about the Company’s historical performance• Focus buyers to the left-side of the balance sheet and de-emphasize existing liabilities

Creditors as Buyers - Proliferation of “loan to own” investors warrants considering an in-court process to appropriately monitor Credit Bids and still run a fair, open, and competitive process

Multiple Transactions - Potential ability to unlock value through a “sum-of-the-parts” approach resulting in multiple, concurrent sale processes

Means of Implementation

- In-court process provides multiple value enhancing elements to ultimately increase valuations, including stalking horse benefits and live auction dynamics

- The re-marketing phase and live auction provides a “second-chance” opportunity to maximize value to the debtor’s estate

Court Approval - Court approval is required to formally:• Retain professionals; approve bid procedures; and ratify the sale

- Benefit of acquiring assets free and clear of liens afforded by the Court

9- 9 -

II. Should the Company Be Sold In or Out of a Bankruptcy? (continued)

Business Considerations (continued)

Advantages to 363 Sales§ Typically much faster and less expensive than confirming a plan

§ Secured lienholders have the ability to credit bid

§ Plan or solicitation of votes not required when converting assets to cash in sale process

§ Standard for Bankruptcy Court approval is generally easily satisfied per business judgement standard

§ Highly transparent process that provides recourse through the court system if the sale process was not conducted in a manner consistent with the procedures approved by the court

§ Buyer purchases the assets free and clear of all liens

§ Certainty, protection, and compensation benefits for a stalking horse bidder

§ Ability to unlock working capital value by only acquiring assets without accompanying liabilities

§ Ability to shed burdensome leases or contracts provides incentive for contract counterparties to negotiate with Seller

363 Sales vs. Healthy Transactions§ All cash bids are most common forms of consideration

§ Generally an asset sale transaction

§ Good faith deposit – stalking horse bidder usually required to provide a deposit of ~10% of the proposed consideration

§ Purchase agreements contain limited reps and warranties with none surviving post-closing as well as no post-closing indemnification – essentially an “As-is, Where-is” transaction

§ Limited closing conditions – no financing or due diligence contingencies or MACs

§ Auction participants adhere to bidding procedures approved by the court and are granted certain protections

- 10 -

II. Should the Company Be Sold In or Out of a Bankruptcy? (continued)

§ Timing; Burn Rate§ Types of Liabilities to be shedded

- Environmental - Product Liability- Pension and Union obligations- Litigation

§ Successor liability§ Court Order

§ Automatic Stay§ Consents

- Assignment clauses- Termination provisions- Change of control - Regulatory consents- Secured creditors

§ Fraudulent Transfer

Legal Considerations

- 11 -

II. Should the Company Be Sold In or Out of a Bankruptcy? (continued)

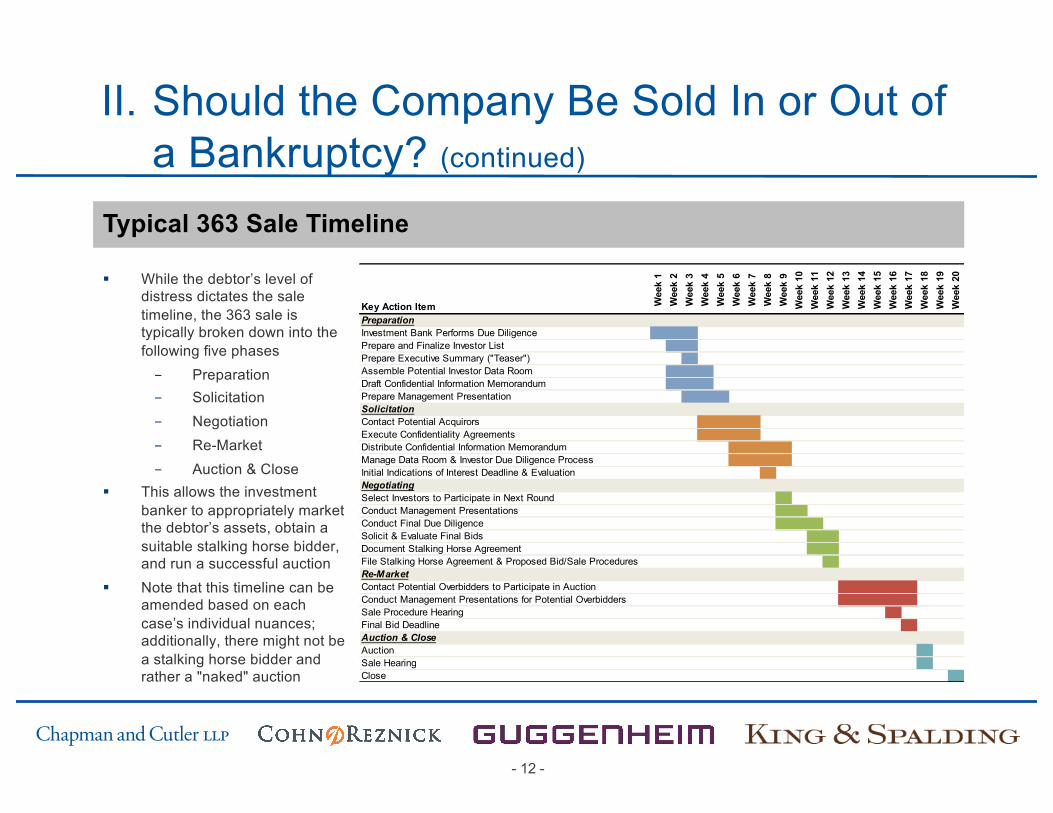

Typical 363 Sale Timeline

Key Action Item Wee

k 1

Wee

k 2

Wee

k 3

Wee

k 4

Wee

k 5

Wee

k 6

Wee

k 7

Wee

k 8

Wee

k 9

Wee

k 10

Wee

k 11

Wee

k 12

Wee

k 13

Wee

k 14

Wee

k 15

Wee

k 16

Wee

k 17

Wee

k 18

Wee

k 19

Wee

k 20

PreparationInvestment Bank Performs Due DiligencePrepare and Finalize Investor ListPrepare Executive Summary ("Teaser")Assemble Potential Investor Data RoomDraft Confidential Information MemorandumPrepare Management PresentationSolicitationContact Potential AcquirorsExecute Confidentiality AgreementsDistribute Confidential Information MemorandumManage Data Room & Investor Due Diligence ProcessInitial Indications of Interest Deadline & EvaluationNegotiatingSelect Investors to Participate in Next RoundConduct Management PresentationsConduct Final Due DiligenceSolicit & Evaluate Final BidsDocument Stalking Horse AgreementFile Stalking Horse Agreement & Proposed Bid/Sale ProceduresRe-MarketContact Potential Overbidders to Participate in AuctionConduct Management Presentations for Potential OverbiddersSale Procedure HearingFinal Bid DeadlineAuction & CloseAuctionSale HearingClose

§ While the debtor’s level of distress dictates the sale timeline, the 363 sale is typically broken down into the following five phases- Preparation- Solicitation- Negotiation- Re-Market- Auction & Close

§ This allows the investment banker to appropriately market the debtor’s assets, obtain a suitable stalking horse bidder, and run a successful auction

§ Note that this timeline can be amended based on each case’s individual nuances; additionally, there might not be a stalking horse bidder and rather a "naked" auction

- 12 -

III.Diligence Process: How Does Diligence Differ Whether In or Out of Bankruptcy?

§ Non-Disclosure Agreements- Scope and “use clause”

§ Sensitive Information- Dealing with a competitor or creditor

§ Ability to analyze the debtor’s assets to create a “menu” of desired assets and excluded liabilities

§ Need to review financial situation pre- and post-bankruptcy filing to determine the business’ true operating and financial situation

§ Careful diligence is necessary because typically there are no post-closing reps and warranties as well as indemnifications

- 13 -

IV. 363 Sale Process – Stalking Horse Bidder

§ Will you conduct a sale without a stalking horse bidder?§ What is a stalking horse bidder?

§ A “stalking horse bidder” is a party who agrees to purchase the debtor’s assets in advance, thus establishing a floor for the debtor’s assets.

§ Having a stalking horse bidder is not mandated by Bankruptcy Code but is very common.

§ Why have a stalking horse bidder?§ To attract or retain an initial bid§ To establish bid minimum and provide certainty to the debtor at a

given value§ To attract additional bidders§ To designate a baseline purchase agreement with specific

contractual terms for other bidders to follow

- 14 -

Stalking Horse Role in 363

- 15 -

Empowerment from Fulcrum Securities

Conducting Preliminary Due Diligence The Auction

Closing

Structuring and Pricing the “Stalking Horse” Bid

Post-Petition Validationof Due Diligence

External DueDiligenceResources

FinancialPartners

Public Relations /Public Market

Overbid

= Go/No Go Decision Point

Start Date ? Or Break Up Fee

“Stalking Horse” M&A Process

Month 1

Bankruptcy Filing Sales Hearing & Plan

Bidding & Auction Dynamics

Debtor

• Wants “certainty”• “Highest & Best”• Contracts assumed/rejected• Leases assumed/rejected• Material deposit• No escrow• No financing contingency• No due diligence contingency• Resolve employee issues• Short closing window• Sale “As Is/Where Is” – No

Reps

Buyer

• Stalking Horse• High break-up fee, plus

Expense reimbursement• “Serial” due diligence

• Postpone tough decisions• Keep financing open

• Not the Stalking Horse• Quality of Information• Multiple phases• Longer closing window

- 16 -

Stalking Horse Bidders – Bidding ProtectionsIn return for serving as the stalking horse bidder, debtors typically grant the stalking horse bidder certain benefits. These often include:

§ Break-Up Fee – a fee paid by the debtor to the stalking horse bidder if the contemplated transaction fails to be consummated – most likely – the debtor’s acceptance of a competing bid. Ordinarily, courts will approve a break up fee that is between 1 to 4 percent of the proposed purchase price.

§ Expense Reimbursement – reimbursement of stalking horse bidder’s out of pocket costs of due diligence and attorneys’ fees.

§ Minimum Bid Increments – requirements in bidding procedures that competing bids can only be in pre-arranged incremental amounts.

§ Terms of Sale Restrictions – requiring that competing bids be substantially similar to that of the stalking horse’s bid – such provisions usually regard the assets being sold, the treatment of management and timing and conditions of the closing.

- 17 -

Stalking Horse Bidders – Benefits of Bidding§ Gains a significant “First Mover Advantage” due to compressed timing

and degree of control over sale process.

§ Can negotiate and influence the sale process, including the bidding procedures, the terms of the asset purchase agreement, the sale’s timeframe and the assets to be purchased.

§ Receives a break-up fee payable if the sale is made to another bidder to compensate the stalking horse bidder for:

- Lost opportunity cost

- Setting a floor value for the assets

§ Also receives expense reimbursements up to a specified amount to cover out-of-pocket diligence expenses.

§ A stalking horse bidder could provide DIP financing, affording additional process control and oversight

- 18 -

363 Sale Process – Bid ProceduresBankruptcy sales, particularly those involving substantial property values, typically proceed according to a two-step Bankruptcy Court approval process:

§ First, the debtor must obtain the Court’s approval of a Bidding Procedures Motion. The Bidding Procedures Motion will typically provide, among other things:

- The date and location of a proposed auction;

- Procedures regarding disclosure of competing bids;

- Rules regarding participation in the auction by phone or email;

- Qualifications required for alternative bidders or “Qualified Bids”;

- Requirements concerning the form of any alternative bid;

- 19 -

363 Sale Process – Bid Procedures (continued)

- Minimum over-bid increments, if any;

- Credit-bid procedures for secured creditors;

- Terms regarding the timing of the purchase;

- Rules for valuing different forms of consideration (i.e. cash vs equity bids); and

- Terms regarding acceptance or requirement of back-up bids.

§ If there is a stalking horse bidder, the proposed asset purchase agreement will typically be included with the bidding procedures motion. The terms of the stalking horse bidder’s bid will be public. This is the bid other bids will be assessed against. The Stalking Horse bid and all fees and bidding protection must be approved by the Bankruptcy Court.

- 20 -

Qualified Bids

§ Prior to any auction, debtors will market assets and solicit bids for the assets from potential purchasers.

§ Only if there are multiple “Qualified Bids” will there be an auction.§ Typically, “Qualified Bids” must contain:

- evidence of financing;- a bid deposit; - a letter submitting an irrevocable bid and evidence of corporate

authority to enter into the transaction, and - a markup of the asset purchase agreement showing any changes

from the stalking horse bidder’s asset purchase agreement. § At the end of the auction, the debtor selects what it considers to be the

“highest and best” offer (generally with purchase price as the most important factor) and, in many cases assuming one has already been formed, consults with the creditors’ committee to determine a winner.

- 21 -

Auction§ The purpose of the auction is to obtain the highest and best price for the

debtor's assets. The investment banker typically runs the auction, as their valuation expertise is essential when comparing competing bids.

§ The debtor must balance its two key objectives: (1) maximizing value to the estate and (2) certainty of closing; therefore the highest bid is not always the best bid

§ All aspects of the bid will be analyzed, evaluated and discounted appropriately:- Consideration (cash, stock, notes, liabilities assumed); and- Contractual terms (representations and warranties, closing conditions,

holdbacks, offers for less than all the assets, purchase price adjustments, and other provisions)

§ Bids must be analyzed on an apples-to-apples basis to appropriately compare bidders’ contracts

§ After the bids have been appropriately valued, qualified bidders will bid against one other, subject to the bidding procedures.

- 22 -

Credit Bidding

§ The Bankruptcy Code specifically provides in section 363(k) for credit bidding by a secured lender at a 363 sale. Section 363(k) provides that:

- [a]t a sale under subsection (b) of this section of property that is subject to a lien that secures an allowed claim, unless the court for cause orders otherwise the holder of such claim may bid at such sale, and, if the holder of such claim purchases such property, such holder may offset such claim against the purchase price of such property.

Credit Bidding by Secured Creditors is Guaranteed Under Section 363(k)

- 23 -

Credit Bidding (continued)

§ The right to credit bid by secured creditors enables such secured creditors to protect themselves against the debtor selling the collateral at a price that the secured creditor thinks is inadequate or under market.

§ The secured creditor may bid its secured claim as if it was cash and reduce the purchase price of the assets on a dollar-for-dollar basis by the amount of the claim.

§ If purchased for less than the amount of the secured claim, the deficiency remains a claim against the debtor’s estate.

§ “Chilling” of bidding§ Specter of a credit bid may dissuade bidder participation as bidders are

reluctant to enter into an auction with uncertainties.

Benefits of Credit Bidding

Disadvantages of the Process

- 24 -

Credit Bidding (continued)

§ The secured creditor is permitted to bid the full face amount of its claim, not just the economic value of the collateral underlying the claim.

§ It’s important to recognize that other bidders do not necessarily know how deep the credit bid claim will go.

Full Amount of Claim May Be Bid

- 25 -

Credit Bidding (continued)

§ Because 363(k) is only applicable to 363 sales, there have previously been questions as to whether credit bidding was permitted with respect to sales conducted in connection with a chapter 11 plan.

§ A split on this issue had developed among the various circuits. CompareIn re Philadelphia Newspapers 599 F.3d 298 (3d Cir. 2010) and In re Pacific Lumber Co., 584 F.3d 229 (5th Cir. 2009) (each denying the right of secured creditors to credit bid) with River Road Hotel Partners, LLC v. Amalgamated Bank, 651 F.3d 642 (7th Cir. 2011) (declining to follow Philadelphia Newspapers and upholding secured lender’s right to credit bid in a sale under a chapter 11 plan).

Credit Bidding in Sales Pursuant to a Chapter 11 Plan

- 26 -

Credit Bidding (continued)

§ In both Pacific Lumber and Philadelphia Newspaper, the respective courts raised the question of whether a pre-petition lender had an absolute right to credit-bid the face value of its pre-petition claim in an asset sale if the sale was accomplished as part of a reorganization plan under § 1129(b) (as compared to a sale pursuant to a § 363(k) process). Both courts answered “no” because the statute’s clear language did not incorporate § 363(k) in all circumstances.

§ The Supreme Court reversed both Pacific Lumber and Philadelphia Newspapers, finding in a unanimous decision (Justice Kennedy recused) that debtors may not sell their property free and clear of liens under a plan of reorganization without allowing lienholders to credit bid. RadLAXGateway Hotel LLC v. Amalgamated Bank.

Credit Bidding in Sales Pursuant to a Chapter 11 Plan (continued)

- 27 -

Credit Bidding (continued)

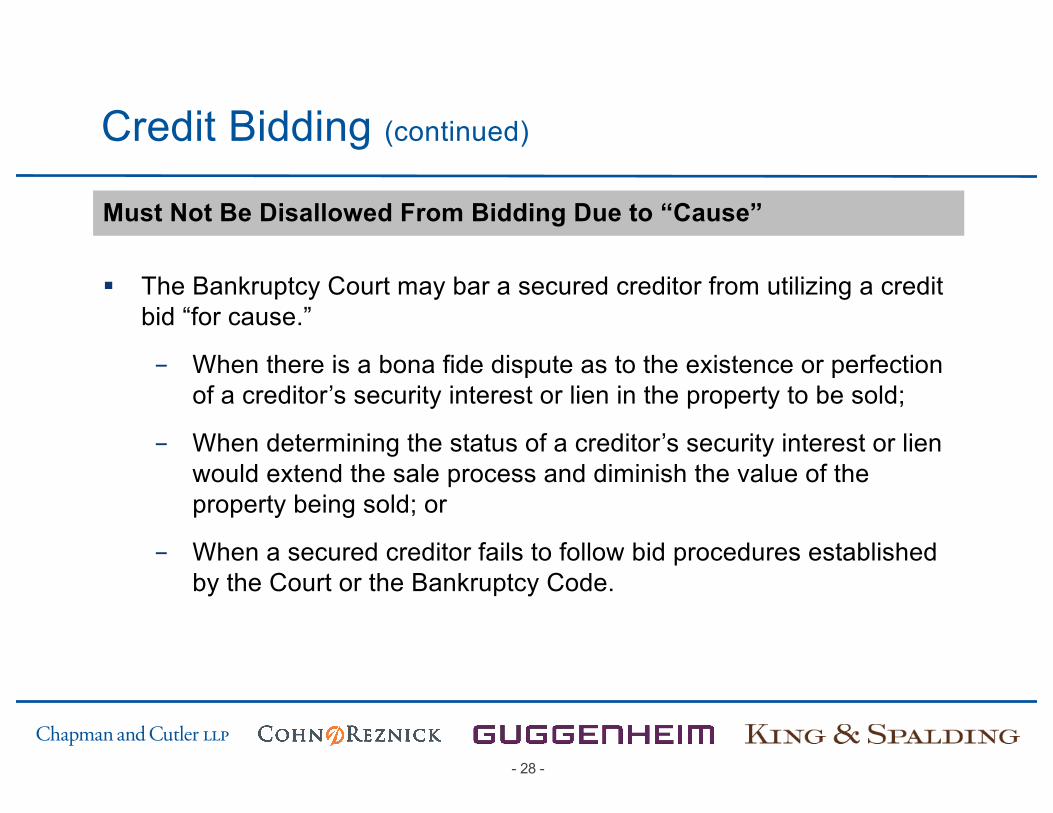

§ The Bankruptcy Court may bar a secured creditor from utilizing a credit bid “for cause.”

- When there is a bona fide dispute as to the existence or perfection of a creditor’s security interest or lien in the property to be sold;

- When determining the status of a creditor’s security interest or lien would extend the sale process and diminish the value of the property being sold; or

- When a secured creditor fails to follow bid procedures established by the Court or the Bankruptcy Code.

Must Not Be Disallowed From Bidding Due to “Cause”

- 28 -

Credit Bidding (continued)

§ In Fisker Automotive, the Senior Secured Creditor purchased approximately $169 million of Secured Claim for $25 million. The Unsecured Creditors Committee argued that credit bidding would chill bidding. Bankruptcy Court held that “cause” exists under sect. 363(k) of the Bankruptcy Code for two reasons (1) the desire to further a competitive bidding process and concern raised by the committee regarding the extent and validating of the Secured Creditor’s liens. The Court capped the Senior Secured Creditors’ right to bid to $25 million.

§ In Free Lance-Star, the Bankruptcy Court limited a Secured Creditor’s right to credit bids its $39 million claim to $13.9 million. The Bankruptcy Court concluded that the the secured creditor’s less than fully secured lien status, the secured creditor’s overly zealous loan to own strategy; and the negative impact of secured creditor’s misconduct has had on the auction process has created the perfect storm, requiring curtailment of secured creditor’s credit bid rights.

Must Not Be Disallowed From Bidding Due to “Cause” (continued)

- 29 -

Credit Bidding (continued)

§ Loan Documents control. Generally, syndicated loan transactions are structured to limit individual lender activity to avoid gridlock in diffusely-held transactions.

§ Purpose of syndicated financing structures is to provide “unified action,” and avoid chaos and prevent a single lender from being preferred over others.

§ Under most credit agreements, the Agent is permitted to credit bid the full amount of the loans outstanding thereunder upon the consent of lenders holding 50.1% of the outstanding loans. Individuals agreement terms may vary.

Who Can Credit Bid – Issues with Regard to Syndicated Loans

- 30 -

Credit Bidding (continued)

§ Whether an individual member of a syndicated loan may bid is determined by the underlying loan documents. This is a fact specific issue. Some examples:

- In re GWLS Holdings, Inc., Case No. 08-12430, 2009 WL 453110 (Bankr. D. Del. Feb. 23, 2009) (Bankruptcy Court held that, as a matter of contract law, agent could credit bid full amount of the outstanding loans over the objection of a minority lender).

- In re Chrysler LLC, 405 B.R. 84 (Bankr. S.D.N.Y. 2009) (Court held that a lender group holding approximately 7.5% of the outstanding debt that objected to proposed sale of substantially all of Chrysler’s assets had “contracted away their right to act inconsistently with the determination of the Required Lenders” and that their dissatisfaction with the ultimate outcome was not justification for disregarding the express provisions of the agreements).

Who Can Credit Bid – Issues with Regard to Syndicated Loans (continued)

- 31 -

- In re Delphi Corp., No. 05-44481 (Bankr. S.D.N.Y.) (Court overruled objection of minority DIP lenders who objected to entry into “Accommodation Agreement”, providing for forbearance from exercising remedies under the DIP agreement and order, holding that based on the express terms of the DIP Agreement, the agent has the exclusive right to exercise remedies, to compromise or forbear with respect to such remedies).

- In re Metaldyne Corp., 409 B.R. 671 (Bankr. S.D.N.Y. 2009) (Court overruled minority lender who objected to credit bid and found that under the loan documents, the agent did not need unanimous consent to credit bid and that it was authorized to submit a credit bid for the full amount outstanding).

Credit Bidding (continued)

Who Can Credit Bid – Issues with Regard to Syndicated Loans (continued)

- 32 -

Highest and Best Offer

§ The overriding goal of the 363 sale process is to maximize value to the debtor’s estate.

§ Bankruptcy Courts provide debtor’s with significant latitude when determining the highest and best offer as long as the decision is consistent with sound business judgement.

§ Typical considerations when evaluating bids:

- Consideration offered

- Contract terms

- Timing of sale’s closing

- Ability to finance the transaction as proposed

- Certainty to close

- Other externalities (jobs created, community and environmental issues, and governmental preferences)

§ After reviewing the bids on a apple-to-apples basis, the debtor selects the “highest and best” offer and motions for the sale of the assets.

- 33 -

Sale Motion§ Following approval of the Bidding Procedures Motion and completion of

any auction, the debtor will move for approval of the proposed sale of the property in the Sale Motion. The sale must then proceed according to the procedures approved in the Bidding Procedures Motion and Sale Motion.

§ Each of the Bidding Procedures Motion and Sale Motion will be subject to separate objection deadlines and hearing dates. This can lead to multiple objections from the same party, holding up the sale process.

- 34 -

Hot Issues at the Approval Hearing

• How does the Estate measure the Value of a Lien? – Value of Collateral vs. Amount of the Claim

• Existence of Conflicting Authorities – PBGC vs. EPA?

• Credit Bidding of a Lien by Secured Creditor

• Bona Fide Dispute – is there an Objective Factual or Legal Basis to Dispute the Interest? Courts may not Resolve Disputes on a commercially reasonable timeframe.

• Good Faith Purchaser Status – Establish Lack of Misconduct, Collusive Bidding, or Unfair Advantage Over Other Bidders

• Standing to Object and Appeal – Disgruntled Bidders

35- 35 -

Section 363(f) – “Free and Clear” of Liens or Interests

Section 363(f) permits bankruptcy estate property to be sold “free and clear of any interest in such property” (including a properly perfected lien) if:

§ applicable non-bankruptcy law permits sale of such property free and clear of such interest;

§ such entity consents;

§ such interest is a lien and the price at which such property is to be sold is greater than the “aggregate value of all liens on the property;”

§ such interest is in bona fide dispute; or

§ such entity could be compelled, in a legal or equitable proceeding, to accept a money satisfaction of such interest.

- 36 -

Section 363(f) – “Free and Clear” of Liens or Interests (continued)

Pursuant to section 363(f)(3), the Court may approve a sale – even over the objection of the secured party – if the secured party’s interest is a lien, and the price at which the property is to be sold is greater than the “aggregate value of all liens” on such property.

§ Conflict exists over whether the “aggregate value of all liens” means the face amount of the liens or if this language means the economic value/sale price.

§ The Ninth Circuit, in Clear Channel Outdoor, Inc. v. Knupfer (In re PW, LLC), 391 B.R. 25 (9th Cir. BAP 2008) (“Clear Channel”), interpreted “value” to refer to the face amount of the liens.

- 37 -

Section 363(f) – “Free and Clear” of Liens or Interests (continued)

§ However, in other districts, such as the Southern District of New York, the courts have held that interpreting this phrase to mean face value would prohibit any non-consensual sales. See In re Boston Generating, LLC, Case No. 10-14419, 2010 Bankr. LEXIS 4335 (Bankr. S.D.N.Y. Dec. 3. 2010). Instead, such courts have held that the “economic value” determined by the sale price governs.

§ Boston Generating and similar decisions have the effect of swinging the pendulum of leverage in a chapter 11 case for pre-confirmation section 363 sales decidedly away from the undersecured lender and toward the debtor and potential acquirers.

- 38 -

This document has been prepared by Chapman and Cutler LLP attorneys for informational purposes

only. It is general in nature and based on authorities that are subject to change. It is not intended as

legal advice. Accordingly, readers should consult with, and seek the advice of, their own counsel with

respect to any individual situation that involves the material contained in this document, the application

of such material to their specific circumstances, or any questions relating to their own affairs that may

be raised by such material.

© 2016 Chapman and Cutler LLP

This document has been prepared by Chapman and Cutler LLP attorneys for informational purposes

only. It is general in nature and based on authorities that are subject to change. It is not intended as

legal advice. Accordingly, readers should consult with, and seek the advice of, their own counsel with

respect to any individual situation that involves the material contained in this document, the application

of such material to their specific circumstances, or any questions relating to their own affairs that may

be raised by such material.

© 2016 Chapman and Cutler LLP

- 39 -