regulatory treatment of accounting provisions - ey.com · definitions, based on the eba’s...

TRANSCRIPT

Regulatory treatment of accounting provisions

O verview 1

Capital impacts of IFRS 9/CECL: Standardised and Internal Ratings-Based Approaches 2

Standardised Approach 2

Internal Ratings-Based Approach 2

Consultative document: interim approach 3

Immediate impact for general and specific provisions 3

A potential “ transitional” model 3

Impact studies 7

Discussion paper: longer-term regulatory treatment 8

Contacts 9

Contents

W hat you need to know ► The Basel Committee on Banking Supervision (BCBS) has issued a Consultative

Document (CD) on an interim approach and transitional adjustments for the

regulatory treatment of Expected Credit Loss (ECL) accounting provisions

under IFRS 9 Financial Instruments and the U S Current Expected Credit Loss

(CECL) model.

► The CD appreciates that accounting provisions under ECL models will be higher

than under the current incurred loss models. The document proposes to amortise

the capital impact of increased provisions under ECL models over three to five

years from the point of transition. BCBS has presented three potential approaches

in its CD based on amortisation over three years.

► BCBS has also issued a Discussion Paper (DP) on the longer-term regulatory

treatment of accounting provisions. The committee is currently considering four

possible options.

► BCBS welcomes comments on both the CD and the DP by 13 January 2017.

O verview

The BCBS issued a CD, Regulatory treatment of accounting provisions — interim approach and transitional arrangements1 on Tuesday, 11 O ctober. Additionally, BCBS has issued a DP on policy options for the longer-term regulatory treatment of provisions under the new ECL standards, Regulatory treatment of accounting provisions.2 For both documents, the BCBS seeks comments from the public by 13 January 2017.

BCBS continues to support the use of the ECL impairment model under IFRS 9 and the CECL approach to be required by the FASB. BCBS “ encourages their application in a manner that will achieve earlier recognition of credit losses than incurred loss models while also providing incentives for banks to follow sound credit risk management practices.” This is in line with its earlier G uidance on Credit Risk and Accounting for Expected Credit Losses (G -CRAECL) publication.3

BCBS recognises that the IFRS 9 ECL and FASB CECL models will likely lead to higher provisions than the Basel expected losses capital requirement, as the Basel requirement of Probability of Default (PD) is based only on a 12– month time horiz on. In contrast, IFRS 9 requires a 12-month ECL only for Stage 1 exposures and lifetime ECLs for Stages 2 and 3 exposures, whereas under CECL, all ECLs are based on lifetime estimates. For equivalent loans, banks applying CECL will be affected more than those applying IFRS 9 as CECL provisions will be higher.

The difference in PD between the accounting requirements and the Basel expected losses capital requirement will be partially offset as Basel Loss G iven Default (LG D) and Exposure At Default (EAD), estimates are based on loss severity experienced during economic downturn conditions while, under IFRS 9 and CECL, LG D and EAD each represent a neutral estimate based on forward-looking economic conditions.

The issue of transitional impact on capital is also more pressing for IFRS reporting banks, as the IFRS 9 model will be applied two years earlier than the CECL model.

Provisions under ECL models will likely be higher than 12–month Basel expected losses, with IFRS 9 impairment provisions based on 12-month ECLs for Stage 1 and lifetime ECLs for Stages 2 and 3. Under CECL, all provisions are based on lifetime ECLs.

3 “ Publications” , Bank for International Settlements website, http: //www.bis.org/bcbs/publ/d350.pdf, December 2015

1R e g u l at ory t re at m e n t of accou n t i n g prov i s i on s

1 " Publications" , Bank for International Settlements website, http: //www.eba.europa.eu/documents/10180/359972/EBA-RTS-2013-04-draft_ RTS_ on_ Credit_ Risk_Adjustments.pdf, O ctober 2016

2 “ Publications” , Bank for International Settlements website, http: //www.bis.org/bcbs/publ/d385.pdf, O ctober 2016

Capital impacts of IFRS 9/CECL: Standardised and Internal Ratings-Based Approaches

Before addressing the CD directly, it is important to understand the ways in which the Day 1 implementation of IFRS 9/CECL will impact upon a bank’ s capital position, with key differences driven by whether the bank employs either a Standardised Approach (SA) or an Internal Ratings-Based (IRB) Approach to the measurement of credit risk capital requirements.

S t an d ard i s e d Approach

The Common Equity Tier 1 (CET1) ratios of banks on the SA are likely to be affected more than IRB banks on Day 1 IFRS 9/CECL implementation, due to the adverse impact of impairment provisions on accounting reserves flowing directly to CET1 capital resources. This can be partially offset via a decrease in Risk-W eighted Assets (RW As), but only where additional impairment provisions recognised on Day 1 are classed as Specific Provisions (SPs) and netted off against accounting exposures prior to risk-weighting. The value of the offset is likely to be less than 10% of the impact on CET1 capital resources, with a significant portion of the newly recognised impairment provisions expected to meet the criteria for G eneral Provisions (G Ps) which are added back to Tier 2 capital resources, subject to a 1.25% cap of credit risk RW As calculated under the SA. This is, however, relevant since Tier 2 and total capital resources will become increasingly important for banks when deciding the volume of additional issuance required to meet the gone concern resolution requirements of Total Loss Absorbing Capacity (TLAC) and M inimum Requirements for own funds and Eligible Liabilities (M REL).

I n t e rn al R at i n g s - B as e d Approach

For IRB banks, the existing CET1 deduction of the excess of regulatory expected losses over accounting provisions, when made, should absorb at least a portion of the Day 1 IFRS 9/CECL increase in provisions before affecting CET1 capital levels. W here provisions, and other allowable value adjustments, exceed the regulatory expected losses they may be added back to Tier 2 capital, subject to a 0.6% cap of credit risk RW As calculated under the IRB. The split between G Ps and SPs will be important for IRB banks where certain of their portfolios follow the SA. It should also be noted that IRB banks may be required to perform full SA RWA calculations if an IRB capital floor is introduced, as has been previously proposed.

The IFRS 9/CECL Day 1 increase in provisions is likely to affect the CET1 ratios of Standardised banks more than those banks applying an Internal Ratings-Based Approach.

2 R e g u l at ory t re at m e n t of accou n t i n g prov i s i on s

Consultative document: interim approach

The headline proposal is the retention of the current regulatory treatment for provisions as applied under the SA and IRB approaches for an interim period following implementation.

The CD notes that ‘ banks should be prepared to absorb a ‘ modest’ decrease in CET1 capital upon initial application of ECL accounting’ . The CD also observes that banks should have considered ECLs as part of their capital planning in the run-up to the earliest required effective date. N evertheless, BCBS considers the implications for regulatory capital and identifies a number of reasons why it may be appropriate to introduce a transitional arrangement for the impact of ECLs on regulatory capital.

Immediate impact for general and specific provisions

The CD encourages jurisdictions to extend their existing approaches to categorising provisions as either GPs or SPs to the ECL accounting model. The significance of this is that under the SA, SPs are netted off against exposures prior to risk-weighting, whereas G Ps are added back to Tier 2 capital, up to a maximum of 1.25% of SA RW As. IFRS 9 implementation is likely to introduce additional complexity for European-based banks applying the SA as, under IAS 39, the European Banking Authority (EBA) has stated that no provisions can be categorised as a G Ps.4 It will be challenging to map the G Ps and SPs definitions, based on the EBA’s technical standard, to the stages of IFRS 9 impairment.5 In particular, it is possible that Stage 2 impairment provisions will be considered to contain a mixture of G Ps and SPs, with robust processes and governance being required to ensure an accurate split. BCBS encourages the regulators to provide guidance as soon as possible on the alignment of the 3 stages of IFRS 9 provisions with the regulatory definitions of G Ps and SPs.

A pot e n t i al “ t ran s i t i on al ” m od e l

The CD explores the possibility of a transitional model upon IFRS 9/CECL implementation. It outlines three possible methods that the BCBS may adopt, with a preference expressed for Approach 1. It should be noted that BCBS has not yet committed to provide any transitional relief and will decide whether to do so in part based on the results of its Q uantitative Impact Study (Q IS) assessment.

The European Commissions’ (EC) proposed amendments to the Capital Requirements Regulation (CRR), issued on 23 N ovember 2016, include a methodology similar to Approach 1. The proposed amendments to the CRR regulation require amortising the incremental provision requirement under IFRS 9 over a period of five years to mitigate the impact on institutions’ capital.

The portion of the IFRS 9/CECL accounting provisions not deducted from CET1 capital due to the transitional arrangement will not be subject to other regulatory adjustments. It will not be treated as G Ps or SPs for Tier 2 add-back or risk-weighting purposes. It will also not reduce the total exposure measure in the leverage ratio. Further, any deferred tax asset associated with such a non-deducted allowance should not be subject to deduction from CET1 capital and risk-weighting.

5 Paragraph 60 of Basel III defines the general provision as ‘provisions or loan losses reserves held against future, presently unidentified losses … ‘ These are eligible for inclusion within Tier 2. However, it further notes that ‘identified deterioration of particular assets or known liabilities, whether individually or grouped, should be excluded … ‘

Regulators will need to provide guidance on categorising ECL provisions as general or specific provisions for regulatory purposes.

4 " Press room" , EBA website, http: //www.eba.europa.eu/documents/10180/359972/EBA-RTS-2013-04-draft_ RTS_ on_ Credit_ Risk_ Adjustments.pdf, 26 July 2013

3R e g u l at ory t re at m e n t of accou n t i n g prov i s i on s

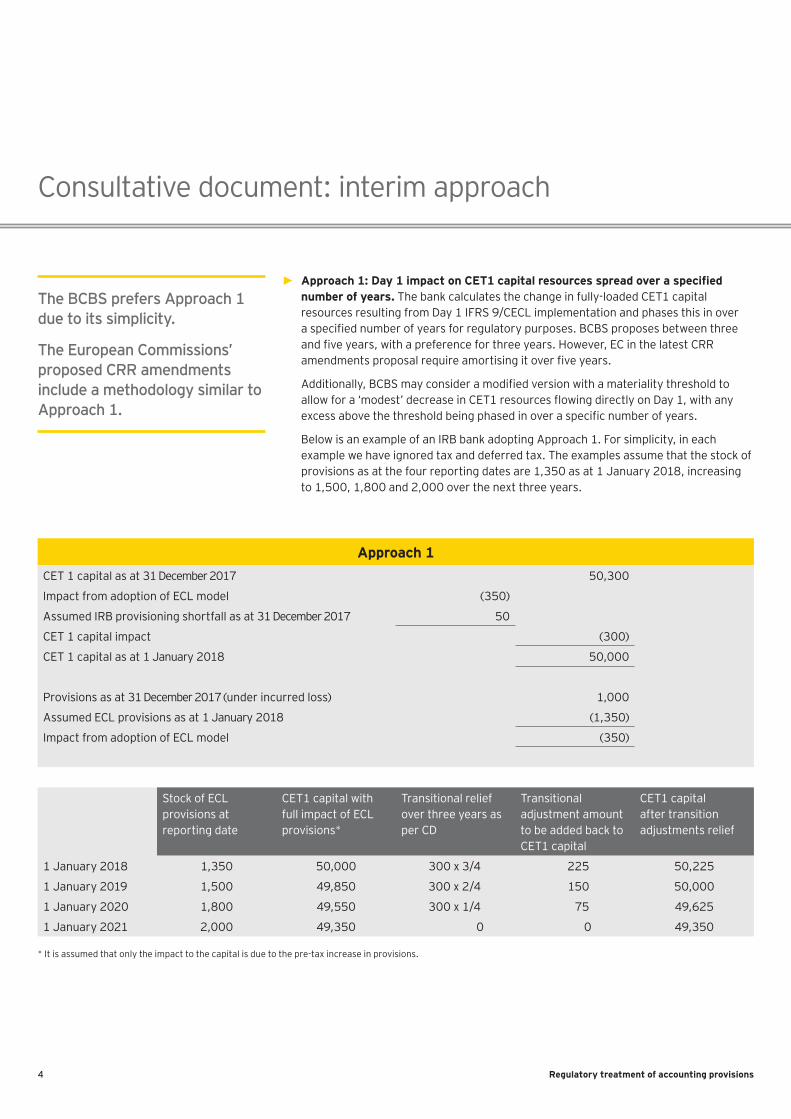

► Approach 1: Day 1 impact on CET1 capital resources spread over a specified n u m b e r of y e ars . The bank calculates the change in fully-loaded CET1 capital resources resulting from Day 1 IFRS 9/CECL implementation and phases this in over a specified number of years for regulatory purposes. BCBS proposes between three and five years, with a preference for three years. However, EC in the latest CRR amendments proposal require amortising it over five years.

Additionally, BCBS may consider a modified version with a materiality threshold to allow for a ‘modest’ decrease in CET1 resources flowing directly on Day 1, with any excess above the threshold being phased in over a specific number of years.

Below is an example of an IRB bank adopting Approach 1. For simplicity, in each example we have ignored tax and deferred tax. The examples assume that the stock of provisions as at the four reporting dates are 1,350 as at 1 January 2018, increasing to 1,500, 1,800 and 2,000 over the next three years.

Approach 1CET 1 capital as at 31 December 2017 50,300

Impact from adoption of ECL model (350)

Assumed IRB provisioning shortfall as at 31 December 2017 50

CET 1 capital impact (300)

CET 1 capital as at 1 January 2018 50,000

Provisions as at 31 December 2017 (under incurred loss) 1,000

Assumed ECL provisions as at 1 January 2018 (1,350)

Impact from adoption of ECL model (350)

Stock of ECL provisions at reporting date

CET1 capital with full impact of ECL provisions*

Transitional relief over three years as per CD

Transitional adjustment amount to be added back to CET1 capital

CET1 capital after transition adjustments relief

1 January 2018 1,350 50,000 300 x 3/4 225 50,225

1 January 2019 1,500 49,850 300 x 2/4 150 50,000

1 January 2020 1,800 49,550 300 x 1/4 75 49,625

1 January 2021 2,000 49,350 0 0 49,350

* It is assumed that only the impact to the capital is due to the pre-tax increase in provisions.

Consultative document: interim approach

The BCBS prefers Approach 1 due to its simplicity.

The European Commissions’ proposed CRR amendments include a methodology similar to Approach 1.

4 R e g u l at ory t re at m e n t of accou n t i n g prov i s i on s

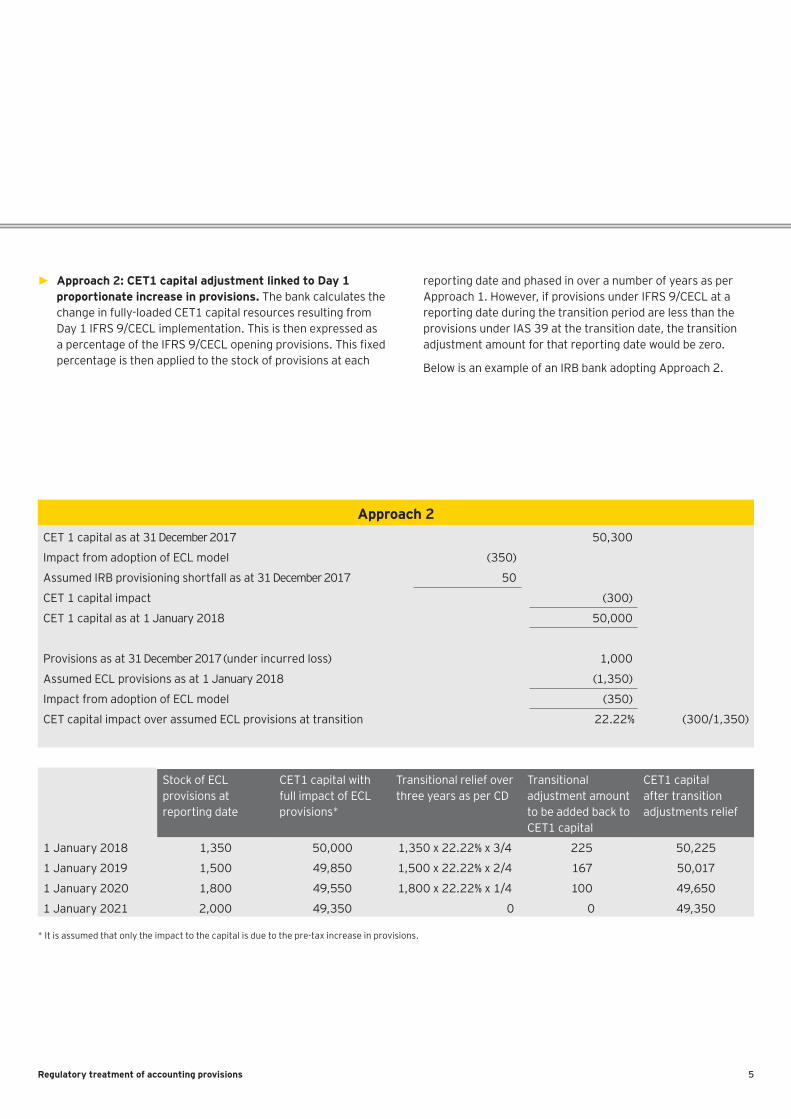

► Approach 2 : C E T 1 capi t al ad j u s t m e n t l i n k e d t o D ay 1 proport i on at e i n cre as e i n prov i s i on s . The bank calculates the change in fully-loaded CET1 capital resources resulting from Day 1 IFRS 9/CECL implementation. This is then expressed as a percentage of the IFRS 9/CECL opening provisions. This fixed percentage is then applied to the stock of provisions at each

reporting date and phased in over a number of years as per Approach 1. H owever, if provisions under IFRS 9/CECL at a reporting date during the transition period are less than the provisions under IAS 39 at the transition date, the transition adjustment amount for that reporting date would be z ero.

Below is an example of an IRB bank adopting Approach 2.

Approach 2CET 1 capital as at 31 December 2017 50,300

Impact from adoption of ECL model (350)

Assumed IRB provisioning shortfall as at 31 December 2017 50

CET 1 capital impact (300)

CET 1 capital as at 1 January 2018 50,000

Provisions as at 31 December 2017 (under incurred loss) 1,000

Assumed ECL provisions as at 1 January 2018 (1,350)

Impact from adoption of ECL model (350)

CET capital impact over assumed ECL provisions at transition 22.22% (300/1,350)

Stock of ECL provisions at reporting date

CET1 capital with full impact of ECL provisions*

Transitional relief over three years as per CD

Transitional adjustment amount to be added back to CET1 capital

CET1 capital after transition adjustments relief

1 January 2018 1,350 50,000 1,350 x 22.22% x 3/4 225 50,225

1 January 2019 1,500 49,850 1,500 x 22.22% x 2/4 167 50,017

1 January 2020 1,800 49,550 1,800 x 22.22% x 1/4 100 49,650

1 January 2021 2,000 49,350 0 0 49,350

* It is assumed that only the impact to the capital is due to the pre-tax increase in provisions.

5R e g u l at ory t re at m e n t of accou n t i n g prov i s i on s

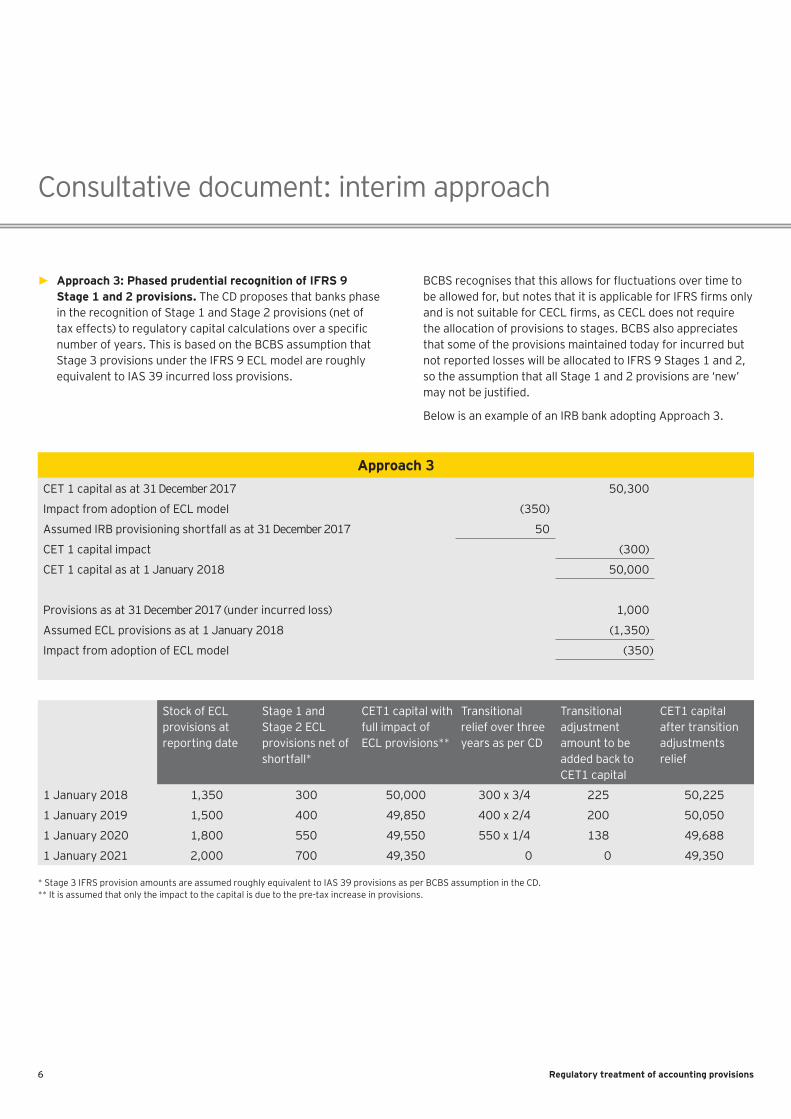

► Approach 3: P has e d pru d e n t i al re cog n i t i on of I F R S 9 S t ag e 1 an d 2 prov i s i on s . The CD proposes that banks phase in the recognition of Stage 1 and Stage 2 provisions (net of tax effects) to regulatory capital calculations over a specific number of years. This is based on the BCBS assumption that Stage 3 provisions under the IFRS 9 ECL model are roughly equivalent to IAS 39 incurred loss provisions.

BCBS recognises that this allows for fluctuations over time to be allowed for, but notes that it is applicable for IFRS firms only and is not suitable for CECL firms, as CECL does not require the allocation of provisions to stages. BCBS also appreciates that some of the provisions maintained today for incurred but not reported losses will be allocated to IFRS 9 Stages 1 and 2, so the assumption that all Stage 1 and 2 provisions are ‘ new’ may not be justified.

Below is an example of an IRB bank adopting Approach 3.

Approach 3CET 1 capital as at 31 December 2017 50,300

Impact from adoption of ECL model (350)

Assumed IRB provisioning shortfall as at 31 December 2017 50

CET 1 capital impact (300)

CET 1 capital as at 1 January 2018 50,000

Provisions as at 31 December 2017 (under incurred loss) 1,000

Assumed ECL provisions as at 1 January 2018 (1,350)

Impact from adoption of ECL model (350)

Stock of ECL provisions at reporting date

Stage 1 and Stage 2 ECL provisions net of shortfall*

CET1 capital with full impact of ECL provisions**

Transitional relief over three years as per CD

Transitional adjustment amount to be added back to CET1 capital

CET1 capital after transition adjustments relief

1 January 2018 1,350 300 50,000 300 x 3/4 225 50,225

1 January 2019 1,500 400 49,850 400 x 2/4 200 50,050

1 January 2020 1,800 550 49,550 550 x 1/4 138 49,688

1 January 2021 2,000 700 49,350 0 0 49,350

* Stage 3 IFRS provision amounts are assumed roughly equivalent to IAS 39 provisions as per BCBS assumption in the CD.** It is assumed that only the impact to the capital is due to the pre-tax increase in provisions.

Consultative document: interim approach

6 R e g u l at ory t re at m e n t of accou n t i n g prov i s i on s

Any bank applying the approach would be expected to disclose it publically, including the capital position before and after the transitional adjustment.

I m pact s t u d i e s

BCBS observes that the impact of an ECL approach ‘ could be significantly more material than currently expected’ and may lead

to a capital shock. The CD also notes that the BCBS intends to collect evidence of the potential impact of each approach through a Q IS survey.

The EBA conducted a Q IS to quantity the impact of IFRS 9 on banks in the EU in January 20166 with the intention to carry out a second Q IS in the near-future.

6 See press release, “ Press room” , EBA website, https: //www.eba.europa.eu/-/eba-launches-an-impact-assessment-of-ifrs-9-on-banks-in-the-eu, 17 January 2016

7R e g u l at ory t re at m e n t of accou n t i n g prov i s i on s

BCBS is considering the following options for a longer-term approach for the regulatory treatment of accounting provisions.

► The first option is to continue with the current regulatory treatment of provisions as a permanent approach, with the national regulator deciding how to distinguish between G Ps and SPs. The drawback is, there will be a different interpretation of G Ps and SPs across jurisdictions, resulting in different treatment of exposures and Tier 2 regulatory capital. M eanwhile, there will also be differences depending on whether banks apply the SA or IRB approaches.

► The second option is to retain the distinction between G Ps and SPs for regulatory purposes. BCBS would create a common definition of GPs and SPs with the aim of reducing variations across juridictions. The challenge would remain for banks of how to classify, operationally identify and track ECL provisions as G Ps or SPs.

► The third option is to introduce a standardised regulatory EL component to the SA for credit risk. This approach is similar to the current IRB approach as it does not distinguish between G Ps and SPs. Any excess of ECLs over and above the expected loss capital requirement would be added back to Tier 2 capital subject to the 0.6% of credit RW As.

► The fourth option for BCBS is to develop an approach based on comments received on the DP.

H ow w e s e e i t

► It is important for regulators to provide guidance on distinguishing between general and specific provisions under IFRS 9/CECL soon. This determination could be a challenging and complex area for banks to address, with sufficient time for implementation being critical.

► Banks should continue to review their capital plans, with reference to the proposed transitional arrangements, to ensure they maintain robust capital ratios through IFRS 9/CECL implementation. This may have wider impacts on strategic decision making and choices as to the markets in which they operate and the products they offer.

► W e expect that stakeholders, such as analysts and investors will focus predominantly on the fully loaded capital position, even if transition adjustments are made.

Discussion paper: longer-term regulatory treatment

8 R e g u l at ory t re at m e n t of accou n t i n g prov i s i on s

Contacts

T ara K e n g l a Partner

T: + 44 20 7951 3054 E: tkengla@ uk.ey.com

T on y C l i f f ord Partner

T: + 44 20 7951 2250 E: aclifford@ uk.ey.com

R i chard B row n Partner

T: + 44 20 795 15564 E: rbrown2@ uk.ey.com

D ou g V i ck Director

T: + 44 131 777 2329 E: dvick@ uk.ey.com

S al m an Af t ab Senior Manager

T: + 44 131 777 2122 E: saftab@ uk.ey.com

J an a W ä hri s ch Partner

T: + 49 6196 6996 23072 E: jana.waehrisch@ de.ey.com

C at ri on a E arl y Manager

T: + 44 20 7951 0249 E: cearly@ uk.ey.com

9R e g u l at ory t re at m e n t of accou n t i n g prov i s i on s

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2016 EYGM Limited. All Rights Reserved.

EYG No. 04451-164Gbl

EY-000014837.indd (UK) 12/16. Artwork by Creative Services Group Design.

ED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com

EY | Assurance | Tax | Transactions | Advisory