regulation, institutional logics and capital structure: … · regulation, institutional logics and...

TRANSCRIPT

1

Regulation, Institutional Logics and

Capital Structure: An Assessment

Sumit K. Majumdar

University of Texas at Dallas

October 1, 2015

2

Regulation, Institutional Logics and

Capital Structure: An Assessment

Abstract

The impact of transition from a rate of return to incentive regulation on firm leverage

levels in the United States telecommunications industry has been examined for the years

1988 to 2001. Overall, price cap regulated firms have had 43 percent lower leverage levels

than firms regulated by the rate of return method. Diffusion of price cap regulation between

1996 and 2001 has had larger negative impact than between 1988 and 1995. Price cap

regulated firms have had 23 percent lower leverage between 1988 and 1995, while price cap

regulated firms have had 78 percent lower leverage between 1996 and 2001. Leverage decline

after price caps introduction would be motivated by efficiency considerations, but after TA

1996 firms would not only cut costs but send signals that low leverage would provide

financial muscle to fight competitive battles and aggressively protect markets.

Key words: capital structure; debt; incentive regulation; institutional logics; leverage; price

caps; rate of return regulation; strategic behavior.

3

Introduction

There are three sets of issues, from several literatures, that matter for understanding

of firm behavior. First, in the regulation and firm behavior literature, financing questions

have been important. Regulated entities, such as electricity, financial services and

telecommunications firms, in the United States, have had high leverage (Barclay, et al 2003;

Besley and Bolten, 1990; Bowen, et al 1982; Bradley, et al 1984; Hagerman and Ratchford,

1978; Taggart, 1981). In regulated industries, with regulated output prices, that firms subject

to rate of return regulation would choose high leverage, because interest costs would be

included in the rate base for calculating firms’ allowable returns (Dasgupta and Nanda, 1993;

Meyer, 1976; Rao and Moyer, 1994; Sherman, 1977; Spiegel, 1996), has been an idea holding

sway.

The business environment that regulators create permits high leverage, because

regulators are not going to let firms die (Taggart, 1985). Regulators have had incentives to

set high regulated prices to lower the probability of regulated firms becoming financially

distressed, allowing interest costs to pass-through to customers and permitting higher

leverage (Spiegel and Spulber, 1994). Limited empirical work (Klein, et al 2002; Taggart,

1981, 1985) has highlighted the existence of price regulations in output markets as providing

regulated firms with incentives to utilize higher debt to finance their operations. Recent

evidence (Bortolotti, et al 2011; Cambini and Rondi, 2012) has examined causality between

regulation and leverage, finding that leverage positively affects regulated rates but causality

the other way around is not established.

4

An important dimension of contemporary business environments has been the world-

wide occurrence of regulatory changes. With such changes in the institutional environment, a

shift in risk, from a firm’s customers to its shareholders, can follow from changes in pricing

regulations, such as from a rate of return to an incentive regulation scheme such as price cap

regulation (Laffont and Tirole, 1993; Lewellen and Mauer, 1993; Majumdar, 2011a).

These institutional changes alter the nature of agency costs regulators face, and

trigger changes in firms’ incentives for reducing costs (Majumdar, 1997; Sappington, 2002),

as a result of which firms may reduce debt to reduce interest burdens. Hence, a shift away

from a rate of return regime, to alternative incentive regulation schemes, can influence debt

levels in affected firms. This issue is relatively unexplored, and only one work (Ovtchinnikov,

2010) has shown the introduction of regulatory innovations to have induced firms to lower

leverage.

Second, in the corporate finance and strategy literature, financing and strategic

behavior questions have been closely interrelated,1 given the relationships between a firm’s

capital structure and strategy,2 because types of financing of firms impacts their strategic

behavior (Hall, 2002Majumdar, 2011b; Mayer, 1990).3 Capital structure has been measured

as the ratio of debt to total capital (Zingales, 1998). Debt is an important type of funds

1 The literature (Balakrishnan and Fox, 1993; Barton and Gordon, 1987; Bettis, 1983;

Bromiley, 1990; Oviatt, 1988) finds numerous such interrelationships. 2 The literature (Brown, et al 2009; Campello, 2003; Kochhar and Hitt, 1996;

Kovenock and Phillips, 1997) has described the possible cause and effect linkages.

3 The additional literature (Bencivenga and Smith, 1991; Cantor, 1990; Hao and Jaffe,

1993; King and Levine, 1993; Lang, et al 1996; O’Brien, 2003) supports evidence that

different financing types influence strategic behavior.

5

source (Corbett and Jenkinson, 1997); the defining feature of two components in a firm’s

capital structure, debt and equity, are the differential rights of providers (La Porta, et al

1998), relative levels debt impact firms’ behavior and increased debt held by firms softens

aggressive strategic behavior.4

The financial structure decision is equally strategic (Myers, 1977).5 Because of agency

(Jensen and Meckling, 1976), signaling (Ross, 1977) and information asymmetry issues

(Myers and Majluf, 1984), considerable heterogeneity exists between firms in financing

decisions (Cantillo and Wright, 2000; Denis and Mihov, 2003; Houston and James, 1996;

Krishnaswami, et al 1999). The issues of whether to have debt, and how much, are important

(Grundy, 1996; Grinblatt and Titman, 2001), and the taking-on of debt is an important

endogenous strategic choice firms make (McKay and Phillips, 2005; Parsons and Titman,

2008; Titman and Wessels, 1988).

Third, in the strategy literature, the role of institutional logics is important

(Thornton, 2004; North, 2005). Firms are embedded within an institutional context that

prescribe appropriate responses (North, 2005; Thornton and Ocasio, 2008). Strategic actions

are responses to institutional features (Greenwood, et al 2014). Institutions are generative

context-defining forces for firms (de Figueiredo, 2002), and influence strategic decision-

making because their logics shape behavior via effects on individuals’ perceptions (Thornton

4 The literature (Anderson and Makhija, 1999; Chevalier, 1995; Chirinko and Elston,

2006; David, et al 2008; Khanna and Tice, 2000; Lambrecht, 2001; Phillips, 1995; Titman,

1984) establishes this.

5 While an early piece (Modigliani and Miller, 1958) had showed that debt to equity

ratios did not matter, a literature has emerged that shows these postulates to be irrelevant

(Parsons and Titman, 2008).

6

and Ocasio, 2008; North, 2005). Yet, there is inadequate evidence as to how institutional

changes affect the actual strategies of firms (Short and Tofell, 2010).

Government regulators exercise power over key economic sectors (Earle, 1997), and,

in regulated environments, government agencies use institutional rules to intervene in and

constrain day-to-day firm operational activities (Evans, 1995). Such contextual constraints

influence social interactions by providing incentives for regularity of behavior (Greif, 1998).

Institutional changes alter incentives, such as on property rights (North and Thomas, 1973),

and variations in firms’ behavior and strategy occur due to the influences of different

institutional regimes (Fukuyama, 2011).

Motivations of firms differ across time (Nelson, 2007), and firms scan the environment

(Nelson and Winter, 1982). Strategic behavior is influenced by incentives, and these vary

according to institutional contexts (North, 1990). Institutional changes alter institutional

logics, and motivate firms to change strategic behaviors, as scanning, searching and sense-

making outcomes impact incentives (Thornton, et al 2012). Altered institutional logics lead

to changes in interpretations of environmental contingencies (Ocasio and Joseph, 2005),

engender new approaches to address these contingencies (Rao, et al 2003), and strategic

changes occur in rapidly-changing environments (Teece, et al 1997; Teece, 2007).

Issue Assessed: Summing up briefly, first literature highlights that regulatory

considerations have an impact on leverage levels or the strategic leverage decision. The

second literature highlights leverage decisions to be a strategic choice of firms. The third

literature highlights the role of institutional changes as influencing strategic decisions.

Putting the key ideas from the three literatures together, this paper evaluates the question as

7

to whether, as institutional environments change, leading to changes in institutional logics,

and how regulatory norms can be interpreted within these different eras, firms decisions on

leverage levels are affected by the explicit regulatory changes that may have occurred in

each era when a differing institutional logic might have prevailed.

Specifically, the article reports on an evaluation of the impact of the transition from a

rate of regulation scheme to an incentive regulation scheme on the leverage strategy of firms

in the United States telecommunications industry. A form of detailed operational regulation

in the telecommunications sector has been over pricing behavior, so that the monopoly

incumbent local exchange companies (ILECs) do not compromise consumer welfare through

high prices (Sappington, 2002).

Price regulation has been based on two extremes (Sappington and Weisman, 1996).

The standard approach has, historically, been rate of return (ROR) based pricing regulation.

Firms have been allowed to set prices allowing them to earn a pre-determined return on their

capital base. This has been a, by now famous, “cost plus” model of regulation.

Given disquiet about the “cost plus” approach, incentive-based approaches, such as

the price cap regulation (PCR) model, have been derived (Sappington, 2002). The PCR

approach has been a “price minus” model of regulation. Introduced in the United States

telecommunications sector in 1990, by 2001 over 40 states had implemented price cap

regulations. In 1985, there were 50 states with rate of return regulatory schemes. By 2001,

the number was 6. The other states had variants of the two schemes.

Hypotheses Examined: How changes in pricing regulations affect the leverage of

telecommunications firms is examined over the years 1998 to 2001, and for two specific eras

8

in that overall period. The assessment is contextualized and conducted for two unique

institutional eras in which sector regulatory and competitive conditions changed. The

institutional environments have differed before and after passage of the Telecommunications

Act of 1996 (TA 1996) in the telecommunications industry. Differences in pre- and post-

legislation periods will have differently impacted firms’ leverage strategies.

The first period data are for the years 1988 to 1995, when a ‘regulated public utility’

logic was in place before TA 1996. A ‘competitive entity’ logic came into play after TA 1996.

The second period data relate to the 1996 to 2001 period. Two hypotheses are examined with

the data. First, a hypothesis relates the relative extent of l everage as a function of pricing

regulation regime changes. Second, a hypothesis posits that the relative impact of how

pricing regulation changes influence the extent of leverage will be a function of changing

institutional logics over the two time periods evaluated.

This article makes important contributions to the literatures by integrating ideas

across literatures to present a framework with which to assess how regulatory changes may

affect firm behavior, because of changes in institutional logic across time periods. While there

is now an emerging body of writing on the topic of institutional logics (North; 2005;

Thornton and Ocasio, 2008; Thornton, et al 2012), there is no articulation as to how, as

historical contingencies and institutional logics alter, and firms strategic pre-dispositions

change, changing regulations also affect firms’ strategic decisions differently over time.

Pricing Regulations and Leverage

In regulated environments, where a ‘cost plus’ mental framework, underlying the rate

of return regulatory regime, had driven the regulatory approach, the cost figure for a firm’s

9

operations, would be considered as constant or it could rise. Lack of cost and market

pressures would lead to inefficient strategic choices (Weisman, 1993). The regulated firm

would not need to appreciate market conditions as its focus would be on internal or political

matters. Such a firm would be concerned about just producing the mandated output. Given

the available outputs, whether customers might demand them or not would be

inconsequential.

Specifically, a rate of return culture would lead firms to inflate their capital base with

inappropriate items and waste resources (Averch and Johnson, 1962; Bailey and Coleman,

1971; Baumol and Klevorick, 1970), limit innovation on cost reduction activities (Biglaiser

and Riordan, 2001), and obfuscate costs as risks were transferred to consumers because of

‘cost pass-through’ by inefficient firms (Joskow, 1974). In such circumstance, regulated firms

would inflate their debt base because interest costs would be included in the rate base for the

passing-through of all costs to consumers within the structure of regulated prices (Dasgupta

and Nanda, 1993; Spiegel, 1994; Spiegel and Spulber, 1994).

An impact of price cap introduction would be cost reductions, as this would be a

“price minus” regulatory regime. In such a regulatory environment, with capped prices, a

firm’s question would be that given a price ceiling, being the maximum received sum for

service provision, how would it make a profit? In a price-capped environment, the price

figure would be constant; while the cost figure would have to be variable. If the profit per

unit were to rise, then the cost per unit would have to move down. That would imply cost

savings coming from all possible sources, including making savings on interest costs. In such

10

a setting, the incentives would be to lower debt levels so as to save on the costs of financing

borrowed funds.

The “price minus” approach of a price cap scheme would focus the firm’s attention on

the market, because it would have to establish the market for a service with a specific price,

and it would not be in the firm’s interest to argue for a higher price during a review. Lower

prices, generally, would lead to higher volumes, and marginal cost reductions would provide

larger reductions in total cost and larger increases in profit. With output prices fixed, the

lowering of costs, including that of interest costs through lowered borrowings, would trigger a

downward, and not upward, revisions of prices that would then further enhance demand for

firms’ outputs.

Regulated firms would also be free to put in the relevant capability packages to help

generate the required volumes of services. In addition, firms would have the full freedom and

flexibility to implement whatever organizational mechanism would be necessary to meet

internal profit volume targets. Hence, an important characteristic of the price cap model

would be enhanced autonomy for strategic actions and flexibility in organizational routines

for implementation.

The enhanced demand for outputs could also trigger increases in the level of demand

for other types of capital, such as human capital and other technological capital that would

augment firms’ dynamic capabilities (Majumdar, 2013). Hence, a transition to a price caps

regime would, in general, be associated with a decline in relative debt levels. Accordingly, it is

hypothesized that:

11

Hypothesis 1: A transition from a rate of return regulatory regime to a price caps regulatory

regime will be associated with relative lower levels of debt in the firms that have made the

transition.

Institutional Change in the United States Telecommunications Industry

Historical Background: The Communications Act of 1934 had formalized the United

States telecommunications industry as a collection of regulated public utilities. Given

institutional logics, local telephone companies acquired a regulated public utility mindset.

The 1934 Act directed the newly created Federal Communications Commission (FCC) to

regulate interstate communications to provide telecommunications services at "just, fair and

reasonable prices." The Act, however, did not specify as to how to obtain the goal. The means

to do so were left open.

In addition, the Act presumed the existence of a monopoly supplier of long distance

services, and the fostering of competition was not a stated goal of the 1934 Act (Spiller,

2005). The ethos then was of universal access and cheap service. In the late 1950s, the FCC

started a process of partially and selectively deregulating the long distance and customer

equipment industry segments. The deregulatory process eventually led to the break-up of the

Bell system in 1984.

The main change of the 1980s, the break-up of the Bell system, came about as a result

of a settlement of a Department of Justice antitrust suit against AT&T, rather than

legislation or regulation. The regulated public utility monopoly model, in which the ILECs

were regulated monopolists, was not dismantled for many more years. A decade later, the

1982 AT&T litigation settlement, the Modified Final Judgment (MFJ), was likely to be

12

reversed by the Supreme Court. In the early 1990s, the United States Congress codified many

restrictions of the settlement into legislation while opening local exchange markets for

competition and providing ILECs’ owners the ability to enter into long distance markets.

This legislation became TA 1996.

Telecommunications Act of 1996: Historical contingencies altered as fundamental

structural changes occurred in the telecommunications sector after TA 1996. After the issue

of a MFJ in 1982, and pursuant to a consent decree, in 1984 the Bell system had divested its

ILECs, called the Bell Operating Companies (BOCs), and retained long distance services. In

1984, 22 BOCs owned by 7 Regional Holding Companies (RHCs) were in existence, and 161

local access and transport areas (LATAs) were created. The BOCs were permitted to carry

calls originating and terminating in one LATA. Between 1984 and 1996 regulatory fiat was

still the prevalent logic.

Twelve years after the 1984 divestiture, the promulgation of TA 1996 (Public Law

104-104, 110 Stat. 56, codified at 47 U.S.C. 151, et seq.), recast industry structure to make it

competitive (Cave, et al 2002). The TA 1996 legislation was intended to change industry

structure and bring in competition. Convergence, inter-modal facility provision and

competition became norms. The emergence of inter-modal competition, from alternative high

speed and wireless carriers, within local markets of the firms studied, was profound (Loomis

and Swann, 2005). In this milieu, the institutional logics altered completely. Firms would be

guided by a competitive entity mindset as a character archetype (Thornton and Ocasio,

2008), driven by the making of continuous adaptations to changing market conditions and

providing customers with numerous choices.

13

Institutional Logic Changes, Pricing Regulations and Leverage

Institutional logics encompass assumptions about meaningful firm actions (Thornton,

et al 2012), and changes in logics perpetrate changes in individuals’ perceptions to influence

their actions on strategic decisions (Glynn, 2008). If the institutional logics of an era defined

by a regulated utility mindset transitioned to a an era where a competitive entity mindset

was to be in place, then perceptions about how to act in an era of different institutional

logics, and interpret environmental signals, would also alter.

The objectives of TA 1996 were: ‘To promote competition and reduce regulation in order

to secure lower prices and higher quality services for American telecommunications consumers and

encourage the rapid deployment of new telecommunications technologies.’ This structure-

changing legislation was intended to bring contestability and competition into a monopol ized

sector. The impact of this legislation would be vital in altering institutional logics of

incumbents from a regulated public utility to a competitive entity mindset.

The TA 1996 deregulated the industry make it competitive (Cave, et al 2002). The

policies after 1996 involved creating a new industry structure, encouraging the deployment of

alternate infrastructures and enhancing customer choices. The structure-changing legislation

would have induced competition in incumbents’ markets and made the environment

dynamic and unpredictable (Hazlett, 2000). The institutional ethos would have shifted from

maximizing universal access to enhancing customer choices.

Enhanced market contestability would increase customer choosiness (Fernandes,

2006). In the presence of competitor entry, with progressively increasing choices available to

customers, higher demand elasticities would result as customers’ consumption patterns would

14

change and switching between alternate suppliers become possible because of open markets.

The rewards or penalties for price changes would rise. Efficient firms could capture a greater

market share through price decreases, while high cost levels, and substantial high prices,

could lead to a substantial market share loss for the firms concerned, and the presence of

organizational slack in firms would be equally costly for inefficient firms (Scharfstein, 1988).

In the process of strategic adaptation to institutional change, because of changes in

the institutional logics, market-opening and structure-changing policies could trigger

important behavioral changes in firms (Barley and Tolbert, 1997). The presence of high costs

would lead to lower profits, increase fiscal distress, act as an inducement to improve internal

efficiencies (Schmidt, 1997) and motivate search for cost reductions (Majumdar, 1995). Even

if firms had hitherto been cost-conscious, such levels of cost-consciousness would rise and all

feasible sources of slack in firms would be cut. Firms would reduce their levels of leverage

further, so as to further reduce the quantum of borrowed funds on which interest would have

to be paid.

As noted earlier, a transition from a “cost-plus” to a “price-minus” regulatory

framework would, in general, be associated with a lower level of leverage; however, the

intensity of the relationship associated with such a transition to a lower level of leverage

would be greater in an era where a competitive entity mindset prevailed , since the need for

cost savings, in such a setting, would have increased by an order of magnitude because of of

emergent market contestability, over a regulated public utility mindset. Hence, it is

hypothesized that:

15

Hypothesis 2: While a transition from a rate of return to a price caps regulatory regime will

be associated with relative lower levels of debt in the firms that have made the transition, the size of

such an impact will be larger in an institutional era characterized by a competitive entity mindset

relative to an institutional era characterized by a regulated public utility mindset.

Empirical Analysis

Data and Dependent Variables: The forty ILECs studied have been the unit of

analysis, for the empirical assessment, with each of them having operations in one or more

states. The impact of regulatory change on relative leverage patterns has been evaluated for

each of the ILECs over the course of the 1988 to 2001 period, and separately for the two

different eras: 1998 to 1995 and 1996 to 2001.

Data for the firms have been obtained from the Statistics of Communications Common

Carriers (SCCC) for the period 1988 to 2001. These companies have accounted for ninety nine

percent of the United States telecommunications fixed-line infrastructure. The data have

been extensively used for other similar analyses (Majumdar, 2011a, 2013; Majumdar, et al

2010, 2014). A balanced panel data model has been used, with the dependent variable

measuring leverage, or debt ratio, denoted as Debt. It has been measured as the long term

debt over total assets ratio (Cornett and Tehranian, 1992). The primary explanatory variable

is changes in the nature of price regulation faced by each of firms over time.

Background Details of Price Cap Schemes: In the telecommunications sector, starting

with the United Kingdom, where price caps were implemented to regulate British Telecom in

1984, the implementation of price caps have become ubiquitous. Almost all of the States

within the United States have adopted some form of incentive regulation, the most popular

16

being price caps. The popularity of price caps have seen them being adopted world-wide.

Price cap regulation has been employed in recent years in Belgium, Bolivia, France,

Germany, Honduras, Hong Kong, Ireland, Italy, Japan, Mexico, The Netherlands, Panama

and Peru (Weisman and Pfeifenberger, 2003).

For the United States telecommunications sector, after the first studies providing

evidence for the ideas that price caps lead to higher technology diffusion (Taylor, et al, 1992;

Greenstein, et al, 1995) and increased efficiency (Majumdar, 1997), a number of pieces (Ai

and Sappington, 2003; Gasmi, et al, 2002; Sappington, 2002) have borne out the positive

behavioral and performance consequences of price caps.

Principal Regulation Explanatory Variable: The regulation variable, Regulation, is a

dummy variable; 1 denotes the presence of price caps or another form of incentive regulation;

0 denotes the presence of rate of return regulation. The diffusion of price caps scheme has

varied over time. Introduced in 1990, by 2001 over 40 states had implemented price cap

regulations. The decline in rate of return regulation has been steady. In 1985 there were 50

states with rate of return schemes. By 2001, it was 6. There was no straight transition from

rate of return to price cap regulation. There were other schemes, falling under the rubric

incentive regulation, also implemented (Sappington, 2002).

The data on regulatory changes in the United States telecommunications industry

have been used in other work (Majumdar, 2011a). For the firms, the regulatory regime in

each period, an incentive scheme or rate of regulation, has been coded as a 1, 0 variable. Over

time, if the regulatory regime an observation experiences has changed, the 1 and 0 coding

17

picks up the change. Hence, relative to itself, a comparison of regulatory regimes for each

observation has been feasible.

Estimation Approach: To evaluate the first hypothesis, treatment effects modelling of

the relationship between regulatory transition and leverage is undertaken for all of the firms

for the full period between 1988 and 2001. Subsequently, the data are split into two parts:

the first part for the years 1988 to 1995, and the second part for the years 1996 to 2001.

Models are estimated for each such separate data set. The differences between the estimates

for the Regulation variable for each part are statistically evaluated to enable a reaching of a

conclusion on the second hypothesis.

Also, a firm- and location specific regulatory change will be endogenous because

regulators will have taken numerous firm-specific factors into account while putting through

the change regime. In addition, there will be an element of self-selection by firms into a price

cap regime, from a rate of return regulation situation, as, in many cases, they would have

attempted to influence regulators to make the transition. Hence, the regulatory change

variable is treated as endogenous and modeled appropriately using a treatment effect model.

Treatment Effects Modeling: The literature has dealt with issues of endogeneity. The

analysis of historical micro-econometric causality helps ascertain factors influencing higher a

transition to price cap regulation, given that regulatory change can influence leverage. In

historical micro-econometric causality analysis, endogeneity concern is tackled using the

treatment effects approach, in which a dummy explanatory variable denotes the existence,

or otherwise, of the endogenous phenomenon the impact of which is evaluated on an outcome

18

variable (Abbring and Heckman, 2008; Angrist and Krueger, 2001; Dehejia and Wahba,

1999; Heckman, 2005; Heckman and Vytlacil, 2005).

Firms that experience price cap regulation subject themselves to a treatment. The

treatment occurrence is given by the transition from the rate of return scheme to price cap

regulation. Its outcome is evaluated in terms of resulting relative leverage levels. The

prospect of experiencing a treatment is endogenous, involving a selection bias, since not all

firms will have engaged in such a regulatory transition but just a selected set of firms. The

treatment effects approach (Heckman, 1976; 1979) helps assess how regulatory transition

influences firms’ subsequent leverage, and a treatment effect is the average causal effect of a

variable on an outcome such as leverage.

A treatment effects model consists of an outcome and a selection equation. The price

cap variable is a covariate influencing leverage, in an outcome equation, after the price cap

variable has been modeled as a dummy endogenous variable influenced by other exogenous

variables, in a selection equation. Selection bias arises because treated firms differ from non-

treated firms for reasons other than the treatment status, per-se. The process of regulatory

transition affecting a particular firm, in a particular territory and in a particular time, can be

conditioned by several factors, as self-selection into treatment may be at play.

Treatment effect models (Heckman, et al 1998; Hirano, et al 2003; Rubin, 1974)

permit natural experiments to be assessed (Angrist, 1998), where a response function,

identifying strategic behavior, in this case of firms leverage outcome, embodies the effect of

interest after the onset of an internal decision or institutional policy (White, 2011). Natural

19

experiments are identifiable discrete shifts in within- or outside-firm environments such that

there is a behavior change (Angrist and Krueger, 2001).

The treatment effects modeling approach is described in Cameron and Trivedi (2005),

Guo and Fraser (2010) and Wooldridge (2010). The selection models permit treatment effects

modeling and pre- and post-event evaluations of variables of interest. Given a binary

dependent variable, selection models are easier ways of dealing with sample selection bias

than instrumental variable regressions (Bascle, 2008; Hamilton and Nickerson, 2003).

Firm- and Industry-Related Variables in the Outcome Equation: The literatures cited

have dealt with the importance of debt in capital structure, and why debt is an important

strategic variable. The extent of firms’ leverage indicates expectations about earnings

capacities and the abilities to repay debts. Yet, on what factors actually drive leverage levels,

there is no universal set of covariates determining leverage (Myers, 2003). Factors relevant in

explaining leverage variations are contingent on time and place specificities (Simerly and Li,

2000), industry factors (Vincente-Lorente, 2001), and firm-specific attributes (Kayhan and

Titman, 2007; Kochhar, 1996; Morellec, 2004).

Three relevant surveys on the determinants of leverage (Harris and Raviv, 1991;

Rajan and Zingales, 1995; Frank and Goyal, 2009) highlight the key covariates that

influence leverage. Leverage increases with fixed assets, non-debt tax shields, growth

opportunities, and firm size; it decreases with volatility, spending on intangible assets and

superior economic performance (Harris and Raviv, 1991). Others (Rajan and Zingales, 1995)

highlight firm size, profitability, possession of tangible assets and firm growth opportunities

as variables significantly impacting leverage. Frank and Goyal (2009) find that: firms in

20

industries where the median firm has high leverage have high leverage; firms with greater

tangible assets have higher leverage; firms with higher profits have lower leverage; larger

firms have higher leverage; and firms with higher market-to-book ratios have lower leverage.

Based on the literature, along with the regulation variable, Regulation, the following are

included as firm-related explanatory variables in the selection equation for Leverage: sales

growth (Growth), firm size (Size) measured as the log of total assets, financial performance

(Performance) which is an asset utilization ratio, an important profitability driver, measured

as the ratio of operating revenues to total tangible assets, and the ratio of total long term

assets to total assets (Assets). To control for industry-related factors, an intensity of relative

competition (Relative Competition) variable is used. The variable is the number of possible

competitors given a license to operate in each firm’s specific territory relative to the average

number of competitors per territory in the industry as a whole. The competition data are

collected from the FCC Competition in Telecommunications Industry reports.

Financial Market Variables in the Outcome Equation: The structure of interest rates

predicts real economic activity (Fama, 1986). An issue is, do the levels of interest rates

influence borrowings by firms? Monetary policies influence real sector activities (Friedman

and Schwartz, 1963), and short-term interest rates have been used to influence the cost of

capital and fixed investment spending (Bernanke and Gertler, 1995). Monetary policy

changes lead to balance sheet restructuring, including that of leverage (Adrian and Shin,

2010; Kashyap, et al 1993). Financial policies propagate shocks. These constraints affect

firms’ leverage decisions (Gomes, 2001; Korajczyk and Levy, 2003). In assessing macro-

economic factors impacting firm level financial decisions, financial market controls are used

21

and the variable used is the interest rate on 30-year long term U. S. Treasury bonds (Interest

Rate).

Variables in the Selection Equation: The price caps literature (Sappington, 2002;

Majumdar, 2011a; 2013) highlights key variables that can determine a transition from a rate

of return to a price caps regime. The size (Size) variable is the log of total output, a standard

measure in the literature. A control for the nature of interconnection regimes is necessary,

since they have been important, for fiscal reasons, in the sector (Armstrong, 2002). In the

absence of a finer or granular measure over the full time period, the relative access cost,

computed as the ratio of access costs to total operating revenues (Access), proxies for

interconnection regimes.

Key environmental factors are urbanization and the extent of business lines (Sharkey,

2002). The urban population ratio (Urban) is the weighted average ratio of urban population

to total population in each firm’s territory. This ratio is weighted by the fraction of lines that

the firm has operating rights to in specific states. The business lines construct (Business) is

measured by the ratio of total business lines to total access lines for each firm.

A technology investment measure used as a control has been the ratio of total fiber

kilometers to total cable kilometers (Fiber), as fiber has been an important technology

providing connectivity and generating efficiency. An advertising variable used has been the

ratio of advertising expenses to total expenses (Advertising). A market share variable

(Market Share) has been constructed by taking the ratio of a firm’s lines in its operating

territory relative to the total lines in the territory. The use of market share constructs as

22

controls proxy for market presence, though in regulated industries a high market share does

not imply monopoly power (Spulber, 2002).

Four measures of firms’ economic performance have been used. Following Christensen

and Montgomery (1981) and Cornett and Tehranian (1992), the following variables, cash flow

over assets (Cash Flow) and growth in sales (Growth), have been used as measures of

financial performance. The cash flow over assets variable has been calculated as the ratio of

total operating revenues to total assets (Cornett and Tehranian, 1992). An efficiency measure

has been a plant efficiency ratio (Efficiency); while a relative performance used has been the

ratio of the cash flow to total assets for each firm relative to the average cash flow to total

assets for all the firms as a whole (Industry Performance).

Results

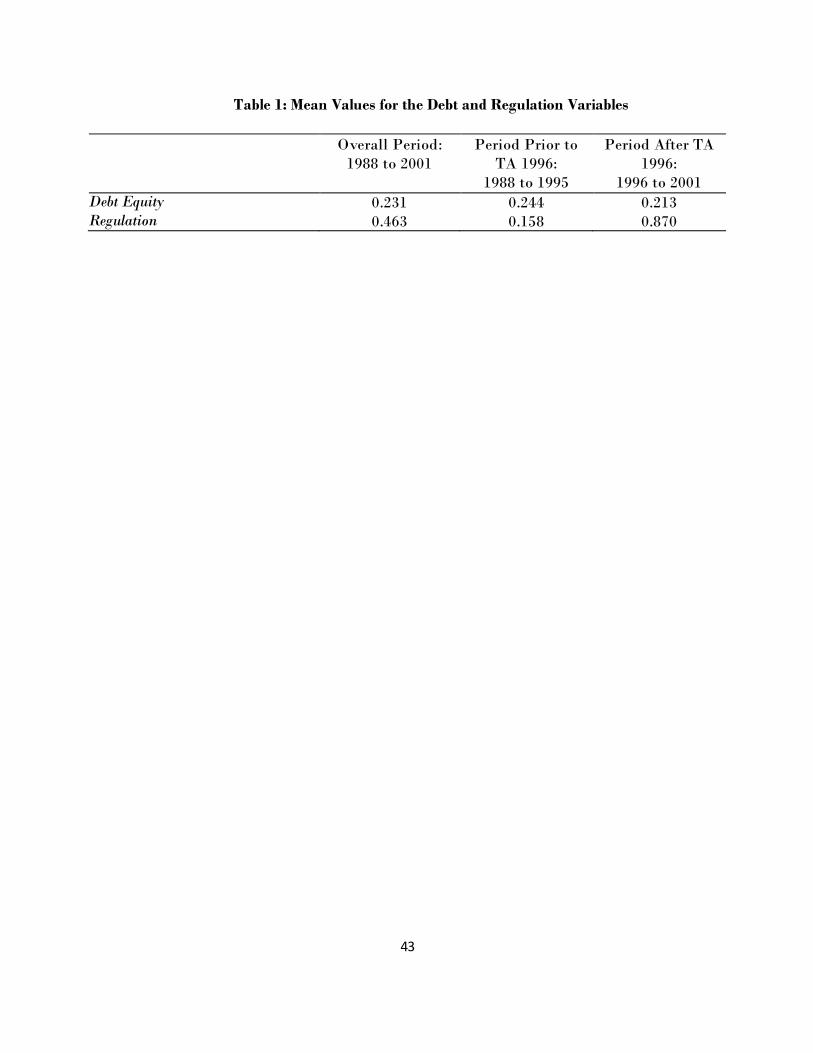

Mean Values: The mean values for the Debt and Regulation variables are given in

table 1. The average ratio of long term debt to total assets has been 0.23, in proportion terms,

or 23 percent, for the entire period. When the data are split into two separate periods, the

ratio for the 1988 to 1995 period has been 0.24, and over time there has been a decline since

the ratio has been 0.21 for the 1996 to 2001 period. Over time, equity financing has become

slightly more important for the firms.

The values of the Regulation variable are also given in table 1; recollect that this has

been a 1, 0 variable, with 1 denoting the presence of a price caps regime. For the entire

period, between 1998 and 2001, the ratio has been 0.46 denoting that the regulatory change

had occurred in just under half of the observations. That would, however, portray a

somewhat inaccurate picture since the diffusion of the regulatory innovation has been

23

steadily rising over the time period. The average value of the variable for the 1988 to 1995

period was about 0.16, denoting that the regulatory change had occurred in just under a

sixth of the observations. For the 1996 to 2001 period, the mean value of the variable of 0.87

has denoted that the regulatory change had occurred in about six-sevenths of the

observations.

1******************** INSERT TABLE 1 HERE ********************

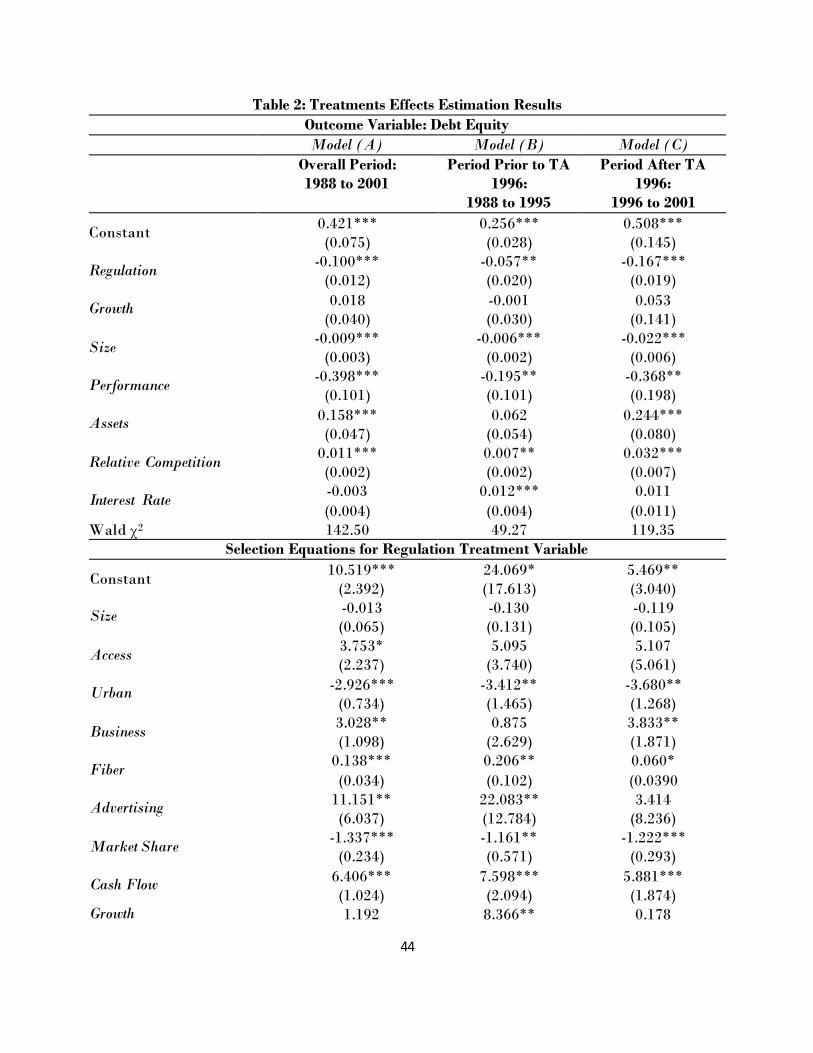

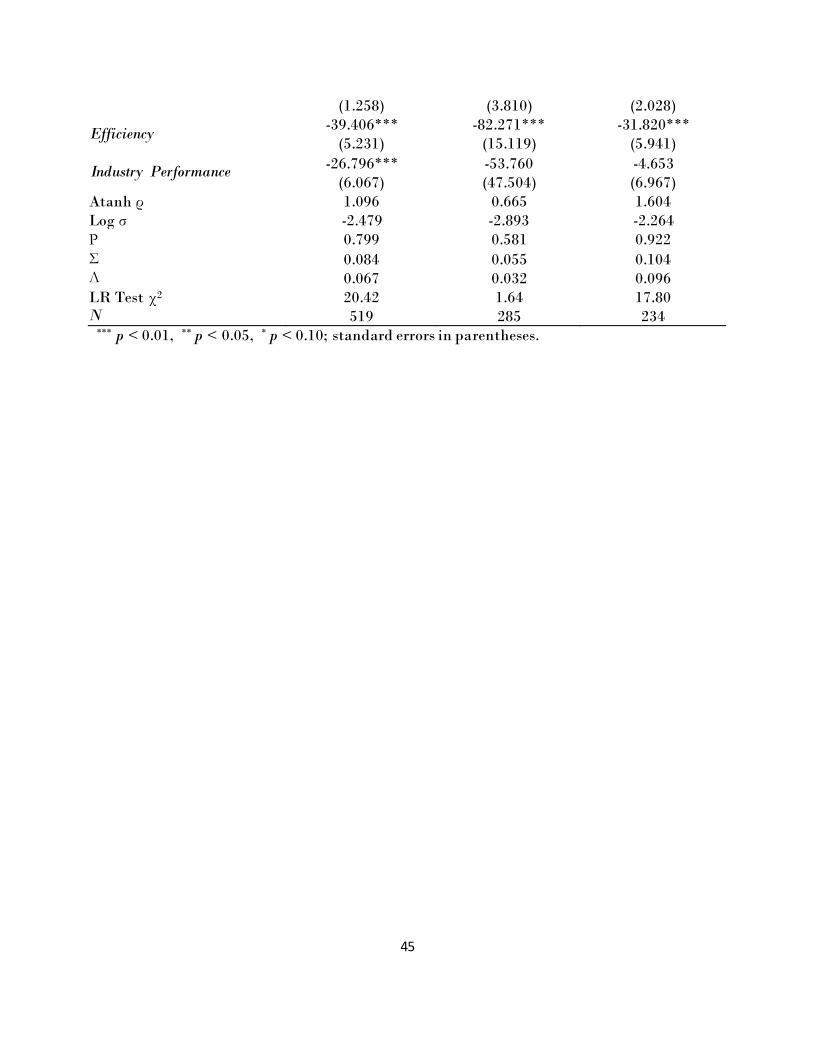

Tests for Hypothesis 1: The results of the estimations are given in table 2. Results for

the entire period, between 1998 and 2001, and for when the data are split into two separate

periods, the 1988 to 1995 period, when a regulated public utility entity mindset was in place,

and the 1996 to 2001 period, when a competitive entity mindset came into effect, are also

given in table 2. The estimates for the Regulation variable in the outcome equations for Debt

are -0.100, -0.057 and -0.167 for the entire period, for the 1988 to 1995 period and for the

1996 to 2001 period, respectively. All of the estimates are significant, at values of p < 0.01.

Hence, a transition from rate of return to price caps regulation has led the firms experiencing

such a transition to lower their levels of indebtedness, as measured by the Debt variable.

The impact of a transition in regulatory regimes on leverage levels is evaluated next.

Given average leverage ratios of 0.231, 0.244 and 0.213 for the Debt variable for the entire

period, and the 1988 to 1995 and 1996 to 2001 periods, the Regulation size estimates imply:

first, for the entire period, a transition to a price caps regulatory regime has been associated

with 43 percent lower leverage for the firms experiencing the regulatory transition; for the

period between 1998 to 1995, a transition to a price caps regime has been associated with 23

percent lower leverage for firms experiencing the transition; and for the period between 1996

24

to 2001 a transition to a price caps regime has been associated with 78 percent leverage ratio

for firms experiencing the regulatory transition.

Overall, these results support the first hypothesis that the transition away from a rate

of return regulatory regime to a price caps regulatory regime will be associated with relative

lower levels of debt. Additional unreported results suggest consistency across specifications.

The results for the 1988 to 1995 and 1996 periods show that, in both periods assessed

separately, the impact of a price caps regulatory scheme is to lower debt levels in firms. The

second hypothesis, however, has posited that the relationship for the 1996 to 2001 period, an

era characterized by a competitive entity mindset among the firms, will be larger than that

for the 1998 to 1995 period, an era characterized by a regulated public utility mindset.

******************** INSERT TABLE 2 HERE ********************

Tests for Hypothesis 2: A test to statistically establish the validity of the second

hypothesis is to apply a standard test comparing the estimates from two specifications. The

results of such a procedure, significant at p < 0.01, show that the negative relationship

between Regulation and Debt is of larger magnitude for the 1996 to 2001 period relative to the

1988 to 1995 period.

Such a test validates the second hypothesis that, given a negative relationship

between price cap regulation and debt, the size of such a relationship will be larger in an

institutional era characterized by a competitive entity mindset relative to an institutional era

characterized by a regulated public utility mindset.

Discussion

25

Contribution: The article is a contribution across several streams of literature in that a

theoretical framework of how institutions, via their underlying logics, have shaped the

heterogeneous action of firms in responding to regulatory changes and impacted on a key

dimension of strategy, the leverage choice, has been developed. Structures of financing, such

as the leverage ratio, significantly impacts firms’ strategic behavior (Hall, 2002; Hao and

Jaffe, 1993; King and Levine, 1993; Mayer, 1990; O’Brien, 2003). In many industries, the

types of regulation firms experience significantly impact their leverage decision (Dasgupta

and Nanda, 1993; Spiegel, 1996). Such impacts may further vary across unique institutional

time periods, because historical contingencies have altered (Thornton and Ocasio, 2008).

The data analysis results support the two hypotheses. Further discussions of the

results are based on applying institutional logics ideas to the context as well as extending

them. Institutional logics incorporate assumptions about what might be meaningful firm

actions (Glynn and Lounsbury, 2005; Thornton, et al 2012). While these are embedded in

individuals’ perceptions, influencing actions (Pahnke, et al 2015) and responses to

environmental stimuli (Almandoz, 2014), such institutional logics fit together (Glynn, 2000)

for firms to develop norms (Thornton, et al 2012) influencing strategy choices (Glynn, 2008).

Within each of the two epochs assessed, the extant regulated public utility and

competitive entity institutional logics have had central roles in influencing firm behavior.

The cost-reduction reasons as to why a change from rate of return regulation to price cap

regulation would be associated with lower leverage, and vice-versa, have been articulated.

There have been standard arguments in the literature on firm regulation on this issue, but

evidence has not been forthcoming so far.

26

Additionally, though, even within a regulated public utility environment, there could

be intra-organizational consequences arising from the particular regulatory transition

evaluated. A characteristic of such transitions are enhancements of autonomy and flexibility,

as regulatory micro-management is removed and firms are free to meet goals and targets

(Majumdar, 2013). This permits firms to put in relevant capability packages to achieve goals.

Firms have the freedom to implement necessary strategies. The impacts of such autonomy

and flexibility would result in superior performance. In such circumstances, managers and

shareholders would seek to enhance their ownership investments in increasingly-profitable

ventures and, to do so, reduce the proportion of debt in the firm’s financial structure.

Institutional Influences: The additional context-specific for cost-cutting, motivated by

institutional logics changes are discussed next. The TA 1996 impacted competitive entry.

After 1996, a number of possible competitors entered the territories of the ILECs. These

competitive local exchange carriers (CLECs) were defined as incumbents' rivals that entered

local phone markets after divestiture. The TA 1996 and the 1996 FCC Report and Order led

such firms to enter the local telecommunications market in three ways. First, CLECs could

purchase a local service at wholesale rates and re-sell it to the end users. These CLECs were

classified as resellers. Second, they could lease various unbundled elements of ILECs’

network through co-location. These CLECs were classified as service providers. Third, they

could set up their own networks as facilities-based competitors.

The TA 1996 mandated that parts of the ILECs’ infrastructure, including the last

mile of copper wires that ran to homes and businesses, be accessible to competitive providers

of services. These parts were called the unbundled network elements (UNE), and the ILECs

27

were to open their network in exchange for a chance to offer long distance services. The

legislation required that the firms classified as Regional Bell Operating Companies (RBOCs)

meet requirements, under Section 271 of the TA 1996, before they could enter inter-state long

distance markets. After TA 1996, competition in the sector dramatically increased.

A CLEC could even lease an entire network at unbundled rates, this being known as

the UNE platform, or UNE-P. By exploiting UNE-P, entrants could purchase downstream

services for a fraction of the incumbents’ retail prices. Details of how CLECs could lease

elements of an incumbents’ infrastructure, piece by piece, on very favorable terms would be

important as these factors will have influenced ILECs’ behavior. These rules disaggregated

ILECs’ upstream capital elements, and allowed entrants to make or buy each piece of their

network infrastructures as they saw fit with the aid of these elements.

The UNE rates were derived from total element long-run incremental costs

(TELRIC). The TELRIC method, which the incumbents had protested against, was upheld

by the United States Supreme Court in 2002. The approach estimated efficient long-run unit

costs for each network element, assuming that the latest technologies were in place,

effectively ignoring the fact that ILECs possessed legacy networks, built up expensively over

many years, which might have had different cost structures.

Introducing UNE and TELRIC into the downstream market was intended to

encourage entry and induce ILECs to upgrade networks. Yet, the costing and pricing rules

would easily motivate cost reductions in various areas, such as interest costs by the reduction

of debt levels, so as to generate financial savings and resources if the CLEC entrants were to

28

gain access to ILECs’ networks at a fraction of the cost incurred by the ILECs. These cost-

cutting necessities would motivate lower leverage levels after TA 1996 went into force.

Impact on Emergent Strategic Logic: In a strategic sense, the extent of leverage in a

firm would be dependent on what the future competitive and strategic impact of such

leverage might be. The impact of leverage on aggressiveness in strategic behavior is based on

the long purse argument (Telser, 1966). Per this argument, having ready access to capital

would allow a firm to sustain losses until it succeeded in eliminating competition. A firm with

low leverage levels could raise more debt, as it would have slack capacity to undertake grater

leverage. This contingency would enable it to behave aggressively, vis-à-vis its rivals, leading

to eventual competitive success.

Conversely, a firm with higher leverage could be vulnerable to competitors’ aggressive

behavior, and increased debt held by firms would soften aggressive strategic behavior

(Anderson and Makhija, 1999; David, et al 2008). The presence of high leverage in incumbent

firms would provide opportunities for rivals to weaken them financially by aggressive

strategies. Highly-leveraged firms would not respond similarly, since the resulting financial

outcomes could be quite negative. The converse would be true.

It was apparent that after TA 1996 the competitive environment had altered ,

exposing the ILECs to substantial threats (Economides, 1999; Koski and Majumdar, 2002).

Given a negative relationship between price cap regulation and leverage, motivated in part

by desires to augment endogenous capabilities in a price cap environment, post-TA 1996

competitive entity institutional logics would enhance the intensity of this relationship. Firms

would not only be motivated to cut costs, and use the savings to build capabilities, but also

29

send clear signals to competitors that they had the financial muscle, engendered by low

leverage levels, to fight strenuous and intense competitive battles and engage in aggressive

strategies to protect their markets and retaliate to competitors’ actions.

Conclusion

Leverage decisions being strategic choices of firms, regulatory considerations have a

major impact on the leverage levels of firms, and institutional changes influence strategic

decisions. In this paper, the question assessed has been whether, given dramatically-changing

institutional environments, with changes in institutional logics leading to interpretation

differences in regulatory norms, firms decisions on leverage levels have been affected by the

regulatory changes occurring in each era when differing institutional logics prevailed.

Specifically, the impact of the transition from a rate of regulation to an incentive

regulation scheme in the United States telecommunications industry on firm leverage levels

has been examined for the years 1998 to 2001, and within that period for two separate unique

eras in which competitive conditions changed, with the institutional environments differing

before and after passage of the Telecommunications Act of 1996 (TA 1996). Between the

years 1988 to 1995, a ‘regulated public utility’ logic prevailed, while a ‘competitive entity’ logic

prevailed for the years 1996 to 2001. Overall, the introduction of price cap regulation has led

to a decline in leverage.

Firms regulated by the price cap method have had 43 percent lower leverage than

firms regulated by the rate of return method. When data for two separate periods have been

analyzed, the diffusion of price cap regulation in the 1996 to 2001 period has had a larger

negative impact, on leverage, than the diffusion of price cap regulation between 1988 and

30

1995. Firms regulated by the price cap method have had 23 percent lower leverage than

others, in the 1988 to 1995 period, while firms regulated by the price cap method have had 78

percent lower leverage than others in the 1996 to 2001 period.

The results support the idea of the institutional logics literature that as institutional

logics alter, firms strategic pre-dispositions change, and hence changing regulations also

impact strategic decisions differently over time. The overall decline in leverage after price

caps introduction might be motivated by efficiency considerations, but after TA 1996 firms

would not only be motivated to cut costs, and build capabilities, but also send signals to

competitors that low leverage levels would provide the financial muscle and depth to fight

intense competitive battles and engage in aggressive market-protection strategies.

31

References

Abbring, J. H. and Heckman, J. J. (2008): Dynamic Policy Analysis, in L. Matyas and P.

Sevestre, Eds., Econometrics of Panel Data, Dordrecht: Kluwer, Third Edition.

Adrian, T. and H. S. Shin (2010): Liquidity and Leverage, Journal of Financial

Intermediation, 19, 418-437

Ai, C. and Sappington, D. (2002): The impact of state incentive regulation on the U.S. telecommunications industry. Journal of Regulatory Economics, 22, 2, 133-159.

Almandoz, J. (2014): Founding Teams as Carriers of Competing Logics: When Institutional Forces Predict Banks’ Risk Exposure, Administrative Science Quarterly, 59, 442-473.

Anderson, C. W. and Makhija, A. K. (1999): Deregulation, disintermediation, and agency costs of debt: Evidence from Japan. Journal of Financial Economics, 51, 309-339.

Angrist, J. (1998): Using Social Security Data on Military Applications to estimate the effect of Voluntary Military Service on Earnings, Econometrica, 66, 249-288

Angrist, J. and Krueger, A. (2001): Instrumental variables and the search for identification: from supply and demand to natural experiments. Journal of Economic Perspectives, 15,

4, 69–85.

Armstrong, M. (2002): The Theory of Access Pricing and Interconnection, in Handbook of

Telecommunications Economics, M. E. Cave, S. K. Majumdar and I. Vogelsang, Eds.,

Amsterdam: North Holland.

Averch, H. and Johnson, L. (1962): Behaviour of the firm under regulatory constraint, American Economic Review, 52, 1053-1069.

Bailey, E. and Coleman, R. (1971): The effect of lagged regulation in an Averch-Johnson model, Bell Journal of Economics, 2, 278-292.

Balakrishnan, S. and Fox, I. (1993): Asset Specificity, Firm Heterogeneity and Capital

Structure. Strategic Management Journal, 14: 3-16.

Barclay, M. J., L. Marx and C. Smith (2003): The Joint Determination of Leverage and Maturity, Journal of Corporate Finance, 9, 149–167.

Barley, S. R. and Tolbert, P. S. (1997): Institutionalization and Structuration: Studying the Links between Action and Institution, Organization Studies, 18, 1, 93–117.

32

Barton, S. and Gordon, P. (1987): Corporate Strategy: Useful Perspective for the Study of Capital Structure? Academy of Management Review, 12, 67-75.

Bascle, G. (2008): Controlling for endogeneity with instrumental variables in strategic management research. Strategic Organization, 6, 3, 285-327

Baumol, W. and Klevorick, A. K. (1970): Input Choices and Rate of Return Regulation: An Overview of the Discussion, Bell Journal of Economics and Management Science, 1:2

169-190.

Bencivenga, V. R. and B. D. Smith (1991): Financial Intermediation and Endogenous Growth, Review of Economic Studies, 58, 195-209.

Bernanke, B. S. and M. Gertler (1995): Inside the black box: The credit channel of monetary

policy transmission, Journal of Economic Perspectives, 9, 4, 27–48.

Besley, S. and E. Bolten (1990): What Factors Are Important in Establishing Mandated Returns? Public Utilities Fortnightly, 125, 26–30.

Bettis, R. A. (1983): Modern Finance Theory, Corporate Strategy and Public Policy: Three Conundrums. Academy of Management Review, 8, 406-415.

Biglaiser, G. and Riordan, M. (2001): Dynamics of price regulation, RAND Journal of

Economics, 31, 4, 744–767.

Bortolotti, B., C. Cambini, L. Rondi and Y. Spiegel (2011): Capital Structure and Regulation: Do Ownership and Regulatory Independence Matter? Journal of

Economics and Management Strategy, 20, 2, 517-564.

Bowen, R. M., L. A. Daley and C. Huber (1982): Evidence on the Existence and

Determinants of Inter-Industry Differences in Leverage, Financial Management, 1, 4,

10–20.

Bradley, M., Jarrell, G. A. and Kim, E. H. (1984): On the Existence of an Optimal Capital Structure: Theory and Evidence, Journal of Finance, 39, 3, 857-878.

Bromiley, P. (1990): On the Use of Financial Theory in Strategic Management, in P. Shrivastava and R. Lamb, Eds. Advances in Strategic Management, 6, 71-98.

Brown, J. R., S. M. Fazzari and B. C. Petersen (2009): Financing innovation and growth:

Cash flow, external equity, and the 1990s R&D boom. Journal of Finance, LXIV, 1,

151-185.

33

Cambini, C. and L. Rondi (2012): Capital structure and investment in regulated network utilities: Evidence from EU Telecoms, Industrial and Corporate Change, 21, 1, 31-71.

Campello, M. (2003): Capital Structure and Product Market Interactions: Evidence from Business Cycles. Journal of Financial Economics, 68, 353-378.

Cantillo, M. and Wright, J. (2000): How Do Firms Choose Their Lenders? An Empirical Investigation, Review of Financial Studies, 13, 155-189.

Cantor, R. (1990): Effects of Leverage on Corporate Investment and Hiring Decisions, Federal Reserve Bank of New York Quarterly Review, 15, 31-41.

Cave, M. E., Majumdar, S. K. and Vogelsang, I. (2002): Structure, Regulation and

Competition in the Telecommunications Industry, in M. E. Cave, S. K. Majumdar and

I. Vogelsang, Eds. Handbook of Telecommunications Economics, Amsterdam: North-

Holland, 1-40.

Chevalier, J. A. (1995): Capital structure and product-market competition: Empirical evidence from the supermarket industry. American Economic Review, 85, 415-435.

Chirinko, R. and J. A. Elston (2006): Finance, Control and Profitability: The Influence of German Banks. Journal of Economic Behaviour and Organisation, 59, 1, 69-88.

Christensen, H. and C. Montgomery (1981): Corporate Economic Performance:

Diversification Strategy versus Market Structure, Strategic Management Journal, 2,

327-343

Corbett, J. and Jenkinson, T. (1997): How is investment financed? A study of Germany, Japan, the United Kingdom and the United States, Manchester School, Supplement,

69-93.

Cornett, M. M. and Tehranian, H. (1992): Changes in Corporate Performance Associated with Bank Acquisitions, Journal of Financial Economics, 31, 211-234

Dasgupta, S. and Nanda, V. (1993): Bargaining and Brinkmanship: Capital Structure Choice

by Regulated Firms, International Journal of Industrial Organization, 11, 475-497

David, P., O’Brien, J. and Yoshikawa, T. (2008): The implications of debt heterogeneity for R&D investment and firm performance, Academy of Management Journal, 51: 165-

181.

de Figueiredo, J. M. (2002): Lobbying and Information in Politics, Business and Politics, 4, 2,

125-129.

34

Dehejia, R. and Wahba, S. (1999): Causal effects in nonexperimental studies: reevaluating the evaluation of training programs. Journal of the American Statistical Association,

94, 1053–1062.

Denis D. J. and Mihov, V. T. (2003): The Choice among Bank Debt, Non-bank Private Debt, and Public Debt: Evidence from New Corporate Borrowings, Journal of Financial

Economics, 70, 3-28

Earle, T. (1997): How Chiefs Come to Power. Stanford: Stanford University Press.

Economides, N. (1999): The Telecommunications Act of 1996 and its Impact, Japan and the

World Economy, 11, 4, 455-483

Evans, P. (1995): Embedded Autonomy: States and Industrial Transformation, Princeton:

Princeton University Press.

Fama, E. (1986): Term premiums and default premiums in money markets, Journal of

Financial Economics, 17, 175-196.

Fernandes, L. (2006): India’s New Middle Classes: Democratic Politics in an Era of Economic

Reform, Minneapolis: University of Minnesota Press

Frank, M. Z. and V. K. Goyal (2009): Capital structure decisions: Which factors are reliably

important? Financial Management, 38, 1-37

Friedman, M. and A. J. Schwartz (1963): A Monetary History of the United States, 1867-1960.

Princeton, N.J.: Princeton University Press.

Fukuyama, F. (2011): The Origins of Political Order, New York: Farrar, Straus and Giroux

Gasmi, F., Kennett, D. M., Laffont, J-J and Sharkey, W. W. (2002): Cost Proxy Models and

Telecommunications Policy, Cambridge, MA: MIT Press.

Glynn, M. A. (2000): When cymbals become symbols: Conflict over organizational identity

within a symphony orchestra, Organization Science, 11, 3, 285–298.

Glynn, M. A. (2008): Beyond Constraints: How Institutions Enable Identities. in R. Greenwood, C. Oliver, K. Sahlin-Andersson, and R. Suddaby, Eds., Handbook of

Organizational Institutionalism, Thousand Oaks, CA: Sage, 413-430

35

Glynn, M. A. and M. Lounsbury (2005): From the Critics’ Corner: Logic Blending, Discursive Change and Authenticity in a Cultural Production System, Journal of Management

Studies, 42, 5, 1031–1055.

Gomes, J. F. (2001): Financing investment, American Economic Review, 91, 1263-1285

Greenstein, S., McMaster, S. and Spiller, P. (1995): The Effect of Incentive Regulation on

Infrastructure Modernisation: Local Exchange Companies' Deployment of Digital

Technology, Journal of Economics and Management Strategy, 4, 187-236

Greenwood, R., C. R. Hinings and D. Whetten (2014): Rethinking Institutions and Organizations, Journal of Management Studies, 51, 7, 1206-1220

Greif, A. (1998): Historical and comparative institutional analysis, American Economic

Review, 88, 2, 72-74.

Grinblatt, M. and Titman S. (2001): Financial markets and corporate strategy, New York:

McGraw-Hill.

Grundy, A. (1996): Corporate strategy and financial decisions, London: Kogan Page.

Hagerman. L. and B. T. Ratchford (1978): Some Determinants of Allowed Rates of Return on Equity to Electric Utilities. Bell Journal of Economics, 9, 46-55.

Hall, B. H. (2002): The Financing of Research and Development, Oxford Review of Economic

Policy, 18, 1, 35-51.

Hamilton, B. H. and Nickerson, J. A. (2003): Correcting for Endogeneity in Strategic Management Research. Strategic Organization, 1, 1, 51-78

Hao, K. Y. and A. B. Jaffe (1993): Effect of Liquidity on Firms’ R&D Spending, Economics

of Innovation and New Technology, 2, 275-282.

Harris, M. and A. Raviv (1991): The theory of capital structure, Journal of Finance, 46, 297-

356.

Hazlett, T. (2000): Economic and Political Consequences of the 1996 Telecommunications Act, Regulation, 23, 3, 36-45

Heckman, J. (1976): The common structure of statistical models of truncation, sample

selection, and limited dependent variables and a simple estimator for such models. Annals of Economic and Social Measurement, 5, 475–492.

36

Heckman, J. J. (1979): Sample selection bias as a specification error. Econometrica, 47, 153–

161.

Heckman, J. J. (2005): The scientific model of causality, Sociological Methodology, 35, 1-97

Heckman, J. J., H. Ichimura and P. Todd (1998): Matching as an Econometric Evaluation Exercise, Review of Economic Studies, 65, 261-294.

Heckman, J. J. and E. Vytlacil (2005): Structural Equations, Treatment Effects, and Econometric Policy Evaluation, Econometrica, 73, 669-738

Hirano, K. G., G. Imbens and G. Ridder (2003): Efficient Estimation of Average Treatment Effects using the estimated Propensity Score, Econometrica, 71, 1161-1189

Houston, J. and James, C. (1996): Bank Information Monopolies and the Mix of Private and Public Debt Claims, Journal of Finance, 51, 1863-1889.

Jensen, M. and W. Meckling (1976): Theory of the firm: managerial behaviour, agency costs

and ownership structure. Journal of Financial Economics. 3. 305-360.

Joskow, P. (1974): Inflation and environmental concern: Structural change in the process of public utility price regulation, Journal of Law and Economics, 17, 291-327.

Kashyap, A. K., Stein, J. C. and Wilcox, D. W. (1993): Monetary Policy and Credit Conditions: Evidence from the Composition of External Finance. American Economic

Review, 83, 1, 78–98

Kayhan, A. and S. Titman (2007): Firms' histories and their capital structures, Journal of

Financial Economics, 83, 1-32.

Khanna, N. and Tice, S. (2000): Strategic Response of Incumbents to New Entry: The Effect of Ownership Structure, Capital Structure and Focus, Review of Financial Studies, 13,

749-779.

King, R. G. and R. Levine (1993): Finance and Growth: Schumpeter Might be Right. Quarterly Journal of Economics, 108, 3, 717-737.

Klein, R., R. Phillips, and W. Shiu (2002): The Capital Structure of Firms Subject to Price Regulation: Evidence from the Insurance Industry, Journal of Financial Services

Research, 22, 1–2, 79–100.

37

Kochhar, R. (1996): Explaining firm capital structure: the role of agency theory vs. transaction cost economics. Strategic Management Journal, 17, 9, 713–728.

Kochhar, R. and Hitt, M. (1998): Linking corporate strategy to capital structure: diversification strategy, type and source of financing, Strategic Management Journal,

19, 601-610

Korajczyk, R.A. and A. Levy (2003): Capital structure choice: Macroeconomic conditions

and financial constraints,” Journal of Financial Economics 68, 75-109.

Koski, H. A. and S. K. Majumdar (2002): Paragons of Virtue? Competitor Entry and the Strategies of Incumbents in the US Local Telecommunications Industry, Information

Economics and Policy, 14, 4, 453-480

Kovenock, D. and G. M. Phillips (1997): Capital structure and product market behavior: An examination of plant exit and investment decisions. Review of Financial Studies, 10,

767-803.

Krishnaswami, S., Spindt, P. A. and Subramaniam, V. (1999): Information Asymmetry,

Monitoring and the Placement Structure of Corporate Debt, Journal of Financial

Economics, 51, 407-434.

Laffont, J-J. and Tirole, J. (1993): A Theory of Incentives in Procurement and Regulation.

Cambridge, MA: MIT Press.

Lambrecht, B. (2001): The Impact of Debt Financing on Entry and Exit in a Duopoly, Review of Financial Studies, 14, 765-804.

Lang, L. H. P., Ofek, E. and R. M. Stulz (1996): Leverage, Investment, and Firm Growth, Journal of Financial Economics, 40, 3-29.

La Porta, R., F. Lopez-de-Silanes, A. Shleifer and R. W. Vishny (1998): Law and Finance. Journal of Political Economy, 106, 6, 1113-1155.

Lewellen, W. G. and Mauer, D. C. (1993): Public Utility Valuation and Risk under Incentive

Regulation. Journal of Regulatory Economics, 5, 263-287.

Loomis, D. G. and C. M. Swann (2005): Inter-modal Competition in Local Exchange Markets. Information Economics and Policy, 17, 97-113.

MacKay, P. and Phillips, G. M. (2005): How Does Industry Affect Firm Financial Structure? Review of Financial Studies, 18, 4, 1433-1466

38

Majumdar, S. K. (1995): X-efficiency in Emerging Competitive Markets: The Case of U.S. Telecommunications, Journal of Economic Behavior and Organization, 26, 1, 129-144

Majumdar, S. K. (1997): Incentive Regulation and Productive Efficiency in the U.S. Telecommunications Industry, Journal of Business, 70, 4, 547-576 (1997)

Majumdar, S. K. (2011a): Does Incentive Compatible Mechanism Design Induce Competitive Entry? Journal of Competition Law and Economics, 7, 2, 427-453

Majumdar, S. K. (2011b): Retentions, Relationships and Innovations: The Financing of R&D in India, Economics of Innovation and New Technology, 20, 3, 233-257

Majumdar, S. K. (2013): Appropriate Mechanism Design, Regulations and Wages, Industrial

and Corporate Change, 22, 5, 1373-1408

Majumdar, S. K., R. Moussawi and U. Yaylacicegi, (2010): Mergers, Jobs and Wages in the United States Telecommunications Industry, Human Relations, 63, 10, October, 1611-

1636

Majumdar, S. K., R. Moussawi and U. Yaylacicegi, (2014): Do Incumbents’ Mergers Influence Entrepreneurial Entry? An Evaluation, Entrepreneurship Theory and Practice, 38, 3,

601-633

Mayer, C. (1990): Financial Systems, Corporate Finance and Economic Development, in R.

G. Hubbard, Ed. Asymmetric Information, Corporate Finance and Investment, Chicago:

University of Chicago Press.

Meyer, R. A. (1976): Capital Structure and the Behavior of the Regulated Firm under Uncertainty. Southern Economic Journal, 42, 600-609.

Morellec, E. and A. Zhdanov (2005): The dynamics of mergers and acquisitions, Journal of

Financial Economics, 77, 649–672

Myers, S. C. (1977): Determinants of Corporate Borrowing, Journal of Financial Economics,

5, 147-175.

Myers, S. C. (2003): Financing of corporations, in G. Constantinides, M. Harris, and R. Stulz, Eds., Handbook of the Economics of Finance: Corporate Finance Vol 1A, Amsterdam:

North Holland, 215-253

Myers, S. and N. Majluf (1984): Corporate Financing and Investment Decisions when Firms Have Information Investors Do Not Have, Journal of Financial Economics, 131, 187-

221.

39

Modigliani, F. and Miller, M. (1958): The Cost of Capital, Corporation Finance and the Theory of Investment. American Economic Review, 48, 3, 261–297

Nelson, R. R. (2007): Universal Darwinism and Evolutionary Social Science, Biology and

Philosophy, 22, 73-94

Nelson R. R. and S. G. Winter (1982): An Evolutionary Theory of Economic Change.

Cambridge, MA: Harvard University Press:

North, D. C. (1990): Institutions, Institutional Change and Economic Performance, New York:

Cambridge University Press.

North, D. C. (2005): Understanding the Process of Economic Change, Princeton: Princeton

University Press

North, D. C. and R. P. Thomas (1973): The Rise of the Western World, New York: Cambridge

University Press.

O'Brien, J. (2003): The capital structure implication of pursuing a strategy of innovation. Strategic Management Journal, 24: 415-431.

Ocasio, W. and J. Joseph (2005): Cultural adaptation and institutional change: The evolution of vocabularies of corporate governance, 1972–2002, Poetics, 33, 163-178

Oviatt, B. M. (1988): Agency and Transaction Cost Perspectives on the Manager–Shareholder Relationship: Incentives for Congruent Interests. Academy of

Management Review, 13, 214–225.

Ovtchinnikov, A. (2010): Capital Structure Decisions: Evidence from Deregulated Industries,

Journal of Financial Economics, 95, 2, 249-274.

Pahnke, E. C., Katila, R. and Eisenhardt, K. M. (2015): Who Takes You to the Dance? How Funding Partners Influence Innovative Activity in Young Firms, Administrative

Science Quarterly, forthcoming

Parsons, C. and Titman, S. (2008): Capital Structure and Corporate Strategy, Handbook of

Corporate Finance: Empirical Corporate Finance, Volume 2, Ed. B. Espen Eckbo,

Amsterdam: North-Holland, 203-234

Phillips, G. M. (1995): Increased debt and industry product markets: An empirical analysis. Journal of Financial Economics, 37, 189-238.

40

Rajan, R. G. and L. Zingales (1995): What Do We Know about Capital Structure? Some Evidence from International Data, Journal of Finance, 50, 5, 1421–1460.

Rao, H., P. Monin and R. Durand (2003): Institutional Change in Toque Ville: Nouvelle Cuisine as an Identity Movement in French Gastronomy, American Journal of

Sociology, 108, 4, 795–843

Rao, R. and Moyer, C. R. (1994): Regulatory Climate and Electrical Utility Capital Structure

Decisions, Financial Review, 29, 97-124

Ross, S. (1977): The determination of financial structure: the incentive signaling approach, Bell Journal of Economics, 8, 1-32

Rubin, D. (1974): Estimating Causal Effects of Treatments in Randomized and Non-

randomized Studies, Journal of Educational Psychology, 66, 688-701

Sappington, D. (2002): Price Regulation, in Handbook of Telecommunications Economics, M.

E. Cave, S. K. Majumdar and I. Vogelsang, Eds., Amsterdam: North Holland

Sappington, D. and Weisman, D. (1996): Designing incentive regulation for the

telecommunications industry, Cambridge, MA: MIT Press.

Scharfstein, D. (1988): Product-market Competition and Managerial Slack. RAND Journal

of Economics, 19, 147-155.

Schmidt, K. (1997): Managerial Incentives and Product Market Competition, Review of

Economic Studies, 64, 191-213.

Sharkey, W. W. (2002): Representation of Technology and Production, in Handbook of

Telecommunications Economics, M. E. Cave, S. K. Majumdar and I. Vogelsang, Eds.,

Amsterdam: North Holland.

Sherman, R. (1977): Ex-Ante Rates of Return for Regulated Utilities, Land Economics, 53,

172-184

Short, J. L and M. W. Toffel (2010): Making Self-regulation more than Merely Symbolic: The Critical Role of the Legal Environment, Administrative Science Quarterly, 55, 361-396

Simerly, R. L. and Li, M. (2000): Environmental dynamism, capital structure and performance: a theoretical integration and an empirical test. Strategic Management

Journal, 21, 1, 31–49

41

Spiegel, Y. (1996): The Choice of Technology and Capital Structure under Rate Regulation, International Journal of Industrial Organization, 15, 191–216.

Spiegel, Y. and Spulber, D. F. (1994): The Capital Structure of a Regulated Firm, Rand

Journal of Economics, 25, 424-440

Spiller, P. T. (2005): Institutional Changes in Emerging markets: Implications for the Telecommunications Sector, in Handbook of Telecommunications Economics, Volume

2, S. K. Majumdar, I. Vogelsang and M. E. Cave, Eds., Amsterdam: North Holland

Spulber, D. (2002): Competition Policy in Telecommunications, in Handbook of

Telecommunications Economics, M. E. Cave, S. K. Majumdar and I. Vogelsang, Eds.,

Amsterdam: North Holland

Taggart, R. A. (1981): Rate of Return Regulation and Utility Capital Structure Decision, Journal of Finance, 36, 2, 383-393.

Taggart, R. A. (1985): Effects of Regulation on Utility Financing: Theory and Evidence, Journal of Industrial Economics, 33, 257-276.

Taylor, W., Zarkadas, C. and Zona, J. D. (1992): Incentive regulation and the diffusion of

new technology in telecommunications, Mimeo, National Economic Research

Associates.

Teece, D. J. (2007): Explicating dynamic capabilities: The nature and microfoundations of (sustainable) enterprise performance. Strategic Management Journal, 28, 1319-1350.

Teece, D. J., G. Pisano and A. Shuen (1997): Dynamic capabilities and strategic management. Strategic Management Journal, 18, 509-533.

Telser, L. G. (1966): Cutthroat competition and the long purse. Journal of Law and

Economics 9, 259–277.

Thornton, P. (2004): Markets from Culture: Institutional Logics and Organizational Decisions

in Higher Education Publishing. Stanford, CA: Stanford University Press

Thornton, P. and W. Ocasio (2008): Institutional Logics, in R. Greenwood, C. Oliver, K. Sahlin-Andersson, and R. Suddaby, Eds., Handbook of Organizational

Institutionalism, Thousand Oaks, CA: Sage, 99-129.

Thornton, P., W. Ocasio and M. Lounsbury (2012): The Institutional Logics Perspective: A

New Approach to Culture, Structure and Process. Oxford: Oxford University Press.

42

Titman, S. (1984): The effect of capital structure on a firm's liquidation decision, Journal of

Financial Economics, 13, 137-151.

Titman, S. and Wessels, R. (1988): The Determinants of Capital Structure Choice, Journal of

Finance, 43, 1-19.

Vincente-Lorente, J. D. (2001): Specificity and opacity as resource-based determinants of

capital structure: evidence for Spanish manufacturing firms. Strategic Management

Journal, 22, 2, 157–177

Weisman, D. (1993): Superior regulatory regimes in theory and practice, Journal of

Regulatory Economics, 5, 355-366.

Weisman, D and J. Pfeifenberger (2003): Efficiency as a Discovery Process: Why Enhanced Incentives Outperform Regulatory Mandates, Electricity Journal, 16, 1, 52-68.

White, H. (2011): Time Series Estimation of the Effects of Natural Experiments, Journal of

Econometrics, 135, 527-566

Zingales, L. (1998): Survival of the fittest or the fattest? Exit and financing in the trucking industry. Journal of Finance, 53, 905-938.

43

Table 1: Mean Values for the Debt and Regulation Variables

Overall Period: