real estate competition - campus finalist

TRANSCRIPT

111

AN ACQUISTION OF THE PORTFOLIO

1

2

Table of Contents2 2

Strategic Overview3

5

6

7

9

10

11

National Market Overview

Portfolio Summary

West Loop Summary

Cutler Centre

San Diego Summary

Rivers Tower

Los Angeles Summary12

13

14

15

16

17

18

Bryant Plaza

Portfolio Recap

Valuation

Valuation of Debt

Valuation of Property

Assumptions

Recommendations19

20

21

22

23

24

25

Strategic Summary

Due Diligence

Acquisition of the Loans

Debt - Equity

Refinancing

Renovations

Cutler Centre - Upgrades26

27

28

29

30

31

32

Rivers Towers - Upgrade

Bryant Plaza - Upgrade

Exit & Sale

Risk

Recap

Overview & Summary

Expected Returns33

35

36

57

83

93

Appendix

Division 1 – Market Research

Division 2 – Strategic Research

Division 3 - Risk

Division 4 - Valuation

Summary34

33

After conducting appropriate

negotiations and due diligence, we

should move to purchase the

portfolio at a 75% discount to it’s

face value.

We should leverage our lein against

the borrowers equity and our

capacity to limit investor losses to

convert out mezzanine loans to a

proprietary interest in the properties

We should renovate all three

properties to maintain the Class A

classification of the properties.

We are pursuing a minimum multiple

on equity of 2.5x.

Our model indicates that the portfolio

will return a levered IRR of 22.28% and

a levered equity multiple of 4.11x

This exceeds the needs of Sun Rock

Capital’s fund.

Expected Returns

Strategic Overview

SWAPACQUIRE RENNOVATE

3

We believe that we will be in the

end of a strong bull real estate

market in 2018. Thus, we should

sell them

SELL

The current downturn in global real

estate market conditions creates the

opportunity for us to purchase quality

Real Estate assets at a substantial

objective discount.

Investment Thesis

3

We recommend pursuing loan-to-own strategy consistent with the funds targeted returns and overall strategy

444

PORTFOLIO & MARKET OVERVIEW – BUILDING AN ECONOMIC

NARRATIVE

4

5

• GFC-driven Yield spikes appear to have ended

• Research into the principles of mean reversion suggest yield will

compress slowly over the coming decade

Expected Growth Rates Yield Trends

US Property Market

Overview

• The recent decline in global market conditions

has caused a substantial shift in the

commercial real estate industry

• Interest rates are at all an time low – 0.25%

• Commercial prices are currently sitting at 2002-

2003 prices.

• The current interest rate environment is

expected to cause a gradual decrease in yields

over the coming 5-10 years

0.0

20.0

40.0

60.0

80.0

100.0

120.0

1997-12-01 1999-12-01 2001-12-01 2003-12-01 2005-12-01 2007-12-01 2009-12-01

Green Streets - Commercial Property Price Index

• Investors expect rent to grow at an increasing pace

• In the short term, it appears that rent growth will be

outstripped by expense growth and inflation

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

US Delinquency Rates

• Loan Delinquency rates appear to have peaked mid-

2009

• We expect rates to decrease slowly in line with current

interest rate conditions

Our analysis indicates that equity offers better

long-term risk adjusted returns than debt

5

6 A portfolio in context…

• The fund has diversified its

holdings well across major

American cities

• This limits our exposure to

localised disaster and regional

economic volatility

Geographic Diversity

The global financial crisis has forced us to target a minimum MOI of 2.5x

• 67% of used capital has been

deployed to purchase equity

• Current market conditions imply

that a weighting towards equity is

best practice

Investment Vehicle

Office52%

Industrial13%

Hotel16%

Retail19%

• Office buildings are less sensitive

to macroeconomic conditions

than retail or hotels

• This allows them to act as a

relative hedge to current financial

volatility

Building Kind

• 4 properties are expected to

make a loss

• This means that, in order to meet

the portfolio target MOI of 2x, the

remaining capital must be

invested at at least 2.5x

Projected MOI

67%Capital In Equity

1

3

1

3

1

2

1

<0.5 <1 <1.5 <2 <2.5 <3 <3.5

7

• West Loop is a former industrial

center that has experienced a

significant degree of urban

gentrification

• It’s central geographic position

creates an opportunity for high

reach retail businesses such as

bars and restaurants

• The decline of many of Chicago’s

outer suburbs creates substantive

demand for high-wealth,

developed inner-city property

West Loop

West Loop – A growth centre…The West Loop submarket is a substantial growth pocket that persists despite Chicago’s poor economic performance

4000000

4100000

4200000

4300000

4400000

4500000

4600000

4700000

4800000

Chicago Historical and Projected Unemployment Data - 2007-2011

Consumer17%

Services28%

Manufacturing

14%

Construction41%

Chicago

Industry

1641

935

855

730

622

520

494

487

New York

LA

Chicago

DC

Dallas

Atlanta

Houston

San…

Business Service Employers (‘000)

8

Copernicus Landsat 1984

West Loop - Growth and Development Trends

Copernicus Landsat 2010

We believe the fundamental geographic characteristics of the West Loop submarket will drive intrinsic demand growth. A comparison of

satellite imagery shows that the developmental boundaries of Chicago have expanded 200-300% over the past 25 years. This city growth is a

strong driver of demand for centralised real estate assets.

9

5400000

5600000

5800000

6000000

6200000

6400000

6600000

6800000

7000000

7200000

2011 2012 2013 2014 2015 2016 2017 2018

W Location: West Loop

Cutler Centre

• Cutler Centre is a 15-storey Class A office tower located in the West Loop submarket of Chicago.

• 240,000 square feet of office space consisting of well-diversified mix of tenants.

– 82% occupancy rate in office

– Currently in line with market, but was below-market last year

• 10,000 square feet of street-level retail space consisting of the Bank of America, convenience store, and clothing boutique.

– 100% occupancy rate

– Entire rental contract rolls over in 2018

• Rent roll unknown

• Loan structure consists of a senior loan and two mezzanines

Property Overview

SUMMARY

Cutler Towers can act as a lever to access growth in the growing West Loop submarket

NOI Projections

10

• San Diego has been considered a leading

area to launch a company

• San Diego is enclosed by the Laguna

Mountain Range. This creates a premium

for downtown real estate.

• San Diego has been designated a Foreign

Trade Zone. This creates opportunities to

leverage global trade trends

• Property sales reached an all time low of

2,142 in January 2008

• Currently, sales sit at around 3000 –

substantially lower than the historical

mean of 4,000-4,500

• Auction success rates are at an all time

low

Downtown San Diego

Downtown San Diego – Dense development

San Diego Property Sales 2000-10

0%

20%

40%

60%

80%

100%

120%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Auction Success Rates 2000-10

We can capitalize on poor market conditions to ride San Diego’s growing technology and trade industries

11

6400000

6600000

6800000

7000000

7200000

7400000

7600000

7800000

8000000

2011 2012 2013 2014 2015 2016 2017 2018

W Location: Downtown San Diego

Rivers Tower

• Rivers tower is a 20-storey Class A office

tower located in the San Diego CBD.

• 500,000 square foot of office space

consisting of a diversified tenant mix

– 75% occupancy rate

– Below-market

• No major capex has been invested and

no major renovations have been made

• Rent roll unknown

• Loan structure consists of a senior loan

and two mezzanines

Property Overview

SUMMARY

Rivers Tower will give us access to the Downtown San Diego submarket

NOI Projections

12

• The Los Angeles Property

Market appears to have

bottomed out

• Trade volumes, a major driver of

LA economic activity, are at

2003 levels

• Commercial yields have fallen by

over 2% over the past two years

• There has been a substantial

drop in the volume of Real

Estate transactions across the

city

• This indicates that liquidity has

dried up substantially over the

past 1-2 years

• We can leverage this in our debt-

equity swap

• This will also allow us to ride the

inevitable economic recovery

Downtown Los Angeles

Los Angeles – Leveraging a global trade fulcrum

0

2

4

6

8

10

12

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Volu

me (

Mill

ion T

EU

)

Port of Los Angeles Trade Volumes - 1990-2020

Poor Real Estate performance creates an opportunity to capture recovery-linked growth

Los Angeles Commercial Yields

Sales Volume

13

3700000

3800000

3900000

4000000

4100000

4200000

4300000

4400000

4500000

4600000

4700000

2011 2012 2013 2014 2015 2016 2017 2018

W Location: Downtown San Diego

Bryant Plaza

• Bryant Plaza is a 15-storey Class A office

tower located in downtown Los Angeles.

The building enjoys excellent visibility

and contains 300 on-site parking spaces.

• 275,000 square foot of office space

occupied by varied tenant groups

– 75% occupancy rate

– Below-market

• Building has undergone a significant

renovation in 2000.

• Loan structure consists of a senior loan

and a mezzanine loan

Property Overview

SUMMARY

Bryant Plaza will give us access to the Downtown Los Angeles submarket

NOI Projections

14

• Real Estate market cycles typical cycle over

between 7-11 years

• The last cycle ended in 2008-2009

• The portfolio could act as a vehicle to leverage

this trend

Fitting the portfolio together…

Economic

Recovery

Market Cycles

MARKETS

West Loop

Increasing

Rent & Yields

If purchase at the right price, the Portfolio may allow us to ride and profit from a global economic recovery

San Diego

Increasing

Rent & Yields

Los Angeles

Increasing

Rent & Yields

US Property Market Cycles

151515

VALUATION – QUANTIFYING VALUE

15

16

W

Valuation of the portfolio: Debt InstrumentsWe should purchase the debt instruments at a 75% discount to their implied value

Rivers Tower $30,851,197

Discount: 70.00%

Purchase Price: $9,255,359

Cutler Centre $20,776,748

Discount: 70.00%

Purchase Price: $6,233,024

Bryant Plaza $55,334,228

Discount: 90.00%

Purchase Price: $5,533,423

17

W

Valuation of the portfolio: Underlying PropertiesPerforming a debt to equity swap would allow us to access the underlying value of these properties

18

CAPITALISATION RATESGROWTH RATESDiscount Rate

9 9 9We have calculated a 9.85%

discount rate

Our rental growth rates are

predicted to grow 2-3% p.a.

We predict a 0.4% decline in

cap rates per year, leading to

an exit cap rate of 5.55%

Assumptions

Discount Rate Assumptions:

Loan Start Date: 01-June-2007

Loan End Date 01-June-2012

Discount Rate: 9.85%

10 Year US Treasury Rate: 3.85%

Real Estate Risk Premium: 6.00%

Rental Growth Rates Assumptions:

Cutler Center 1.2%

Post-Capex 3%

Rivers Tower 2%

Rivers Tower Post Capex 3.85%

Bryant Plaza 2%

Bryant Plaza Post Capex 3%

FRBSF Economic Letter 2011-29 September 19, 2011

2

Cap rates as an indicator of future price returns

The cap rate measures the ratio of net operating income to the price of a property. It can be interpreted

as the CRE equivalent of the price/earnings ratio in the stock market (see Campbell and Shiller 1988 for

the pricing implications of these valuation measures). According to theory, this rent/price ratio is largely

a function of interest rates and expected increases in the property’s price. Consider someone who wants

to use a real estate property for one year. This person can get the space in two ways. He or she could rent

the property for the year, which would cost a year of rent. The rent would appear as part of the property

owner’s net operating income. Alternatively, the person who wants to use the property could borrow

money, buy it, and hold it for a year. The cost of this ownership option, referred to as the user cost,

consists of interest payments on the purchase loan plus the expected change in the property’s price over

the holding period. In a well-functioning market with zero transactions costs, the price of these two

alternatives should be the same. If they were not—if rents were higher than the user cost, for example—

then all market participants would want to buy, bidding up prices until the rental option cost the same.

The important point here is the direct link between the net operating income of the rental option and

prices, ownership costs, and expected capital gains of the ownership option. When purchasing CRE,

market participants often link cap rates to expected future rental rates and vacancies. Expected increases

in rent or lower vacancies tend to lower the cap rate. If rents are expected to increase, then the property

has become more valuable and the owner will expect a higher capital gain, which will lead to a lower cap

rate. A similar argument can be made for falling vacancies.

Thus, expected price appreciation is ultimately a reflection of the outlook for fundamentals such as rents

and vacancies. However, there could also be unidentified nonfundamental reasons for changes in

expected price appreciation. For example, investor sentiment may improve and the discount rate applied

to cash flows from a property may fall, thereby lowering the cap rate. Indeed, investor sentiment could

become so exuberant that a bubble could form, in which expected appreciation soared and the cap rate

dropped sharply.

This link between cap rates, interest

rates, and expected price appreciation

is not merely theoretical. Using a

slightly different representation of the

cap rate, Ghysels, Plazzi, and Valkanov

(2007) show that it predicts CRE

returns. In our data we can see these

linkages in Figure 2, which compares

CRE cap rates with the interest paid on

loans to finance CRE transactions. We

focus here on the office market, but

other CRE asset classes have behaved

similarly. Ideally, the interest measure

should be the rate on new CRE loans,

but those are not readily obtainable.

Instead, we use as a proxy for CRE

purchase loans the yield on AAA-rated five-year commercial mortgage-backed securities (CMBS), which

finance a large share of CRE transactions.

Figure 2

Office building cap rates and CRE mortgage rates

Sources: CB Richard Ellis (CBRE) and Commercial Real Estate Direct.

0

1

2

3

4

5

6

7

8

9

10

0

2

4

6

8

10

12

14

16

18

20

2004 2005 2006 2007 2008 2009 2010 2011

Percent Percent

CMBS yield (left axis)

Office cap rate (right axis)

Summer2010

Our valuation is driven by a 9.85% discount rate, a 2-3% rent growth rate and a 0.4% Cap Rate compression each year

191919

OUR RECOMMENDATIONS AND ADVICE

19

20 Strategic SummaryWe propose purchasing the debt, swapping it to equity, renovating the properties and exiting at the peak of the market in 2018

• Conduct due diligence:

Property Condition

Owner’s Equity

Any binding

agreements

between HRC

Capital, senior debt

holders and owner

• Negotiate an interparty

agreement between owner

Debt to Equity

swap for the

ownership interest

in the property is

viable

Due Diligence

Interparty agreementPrior to Acquisition

• Purchase all Mezzanine

offered at a 75-90%

discount to its value

• Conduct a Debt to Equity

swap

Purchase Mezzanine Debt

• Owner will most likely

default in payments

Senior debt will

be compensated,

but mezzanine

debt may not be

We will not get

our money back

• Do not pursue investment

any further

Do not Purchase Mezzanine

Debt

SWAP

• Refinance the senior debts at a

lower interest rate

• Renovate the office buildings to -

Suit changing

contemporary economic

conditions

Appreciate underlying

value

Occupy Ownership Interest of the

Properties

Owner DefaultsBuy or Pass Exit Strategy

Contingencies

SE

LL

• Exit each office

building in year for a

total of $311M

• Offering a levered IRR

of 22.8%

Exit the Office Buildings

2010-2018

21

Borrowe

r

Senior

Debt

Mezz

Debt

Senior

Debt

Mezz

Debt

Senior

Debt

Bryant Plaza

Cutler Centre

Rivers TowerIs the purchase of the mezzanine loans UCC (Uniform Commercial Code) approved?

Negotiations and Due Diligence Questions

Will inter-creditor agreements interfere with either the purchase of the loan or the Debt-Equity Swap?

What upper-level debt agreements are the properties subject to?

What senior mortgage covenants and restrictions is the property subject to?

Is the borrower willing to swap the mezzanine loans for an equal proprietary interest in the building?

Do the terms of the current capital structure allow for us to refinance immediately?

Due Diligence & NegotiationsWe need to run a number of meetings and operate several due diligence checks before we proceed further…

2010

Due Diligence Checklist

Property & Markets

Borrower Position

Legal Structure & Documents

Other Creditors

Servicing History

22 Acquiring the loans…The debt on the portfolio matures after the next interest payment, thus there is a clear need to refinance

2010

CUTLER CENTRE

ACQUISITION

• Targeting a 70% discount to the

implied, risk free value of the loan.

• Reflective of the fact that the loan will

default as the property and capital

structure are distressed

• The fulcrum position of the loan with

respect to the capital stack as a whole

should allow us to pursue this discount

PURCHASE PRICE: $6.2M

RIVERS TOWER

ACQUISITION

• Target an identical 70% discount to the

implied risk free value of the loan

• Reflective of similar conditions to the

Cutler Centre

PURCHASE PRICE: $9.3M

BRYANT PLAZA

ACQUISITION

• Bryant Plaza’s NOI is two times lower

than their debt service requirements

• Therefore it is the most distressed out

of all three properties

• Thus, we are targeting a 90% discount

to the implied, risk free value of the

loan.

PURCHASE PRICE: $5.5<

THE PORTFOLIO

ACQUISITION

• Overall, we are targeting a weighted

discount of 75.26%

• This is the minimum discount required

to meet the 20% IRR requirement set

out by Sun Rock Capital

PURCHASE PRICE: $21M

23 Performing a debt to equity swapBy nature, mezzanine debt is a more effective vehicle for pursuing loan-to-own strategies

• Mezzanine are more flexible than senior debt

• A debt-equity swap would avoid the borrower public embarrassment

• Mezzanine debt cause a great deal of anxiety among borrowers for the following reasons

• Mezzanine Debt commands a higher interest rate than senior debt, therefore it has a higher chance of default

• If a borrower defaults on a mezzanine loan, the lender foreclose on the equity of the borrower rather than the property

• Estimates of cash flows indicate the borrower will default on their next interest payment

• This will allow the holder of the mezzanine to foreclose on the equity of the borrower

• As a result, a default would be catastrophic for the borrower

• A debt to equity swap would allow the borrower to avoid this issue

PERSUASIVE FACTORS

LEVERAGE

TERMS OF SWAP

TERMS

• We will swap our mezzanine debt at 1:1 ratio, i.e. 1% debt is converted into 1% equity

• We will take on the current obligations subject to the property and owed to senior and other mezzanine debt holders

• We will take management of the property in all areas, such to indicate that we are the sole equity partner and owner of the properties

Borrower

Senior

Debt

Mezzanine

Loan1

Mezzanine Loan

2

Senior

Debt

Mezzanine

Loan1

Owner (Sunrock

Capital)

2010

24 Refinancing the loansThe debt on the portfolio matures after the next interest payment, thus there is a clear need to refinance

2010

CURRENT CAPITAL STRUCTURE

CONDITIONS

Capital Structure Of Properties:

Cutler Center - Chicago

Senior Loan: $35,000,000

First Mezzanine: $30,000,000

Second Mezzanine: $20,000,000

Rivers Tower - San Diego

Senior Loan: $57,000,000

First Mezzanine: $25,000,000

Second Mezzanine: $30,000,000

Bryant Plaza - Los Angeles

Senior Loan: $45,000,000

Mezzanine: $51,000,000

Cutler Centre – Refinanced Capital Structure &

Conditions

Senior Loan:

Principal: $35,000,000

Loan Term (Years): 10

Rate: 4.50%

Amortisation (Years): 30.00

Payment: $2,148,704

First Mezzanine:

Principal: $30,000,000

Loan Term (Years): 7

Rate: 12.00%

Amortisation (Years): IO 7

Payment: $3,600,000

Rivers Tower – Refinanced Capital Structure

& Conditions

Senior Loan:

Principal: $57,000,000

Loan Term (Years): 10

Rate: 4.50%

Amortisation (Years): 30.00

Payment: $3,499,318

First Mezzanine:

Principal: $25,000,000

Loan Term (Years): 7

Rate: 12.00%

Amortisation (Years): IO 7

Payment: $3,000,000

Bryant Plaza – Refinanced Capital Structure &

Conditions

Senior Loan:

Principal: $45,000,000

Loan Term (Years): 10

Rate: 4.50%

Amortisation (Years): 30.00

Payment: $2,762,619

Loan

Structure

TARGETED CAPITAL STRUCTURE

STRUCTURE

We are targeting a 4.5% fixed interest rate

for senior debt. This is derived from similar

loans at the time, and the competing impact

of low interest rates and poor

macroeconomics

We target a 12% fully amortized structure

for mezzanine loans. This will compensate

investors for the risk they are taking.

25 Renovation as a defensive strategy…Renovation is necessary as a defensive move to lock in the Portfolio’s value in the heat of a strong bull market

2018

Renovation

Rationale

MARKET TRENDS

STRUCTURE

• As value and liquidity returns to the

market, competition will follow

• There will be strong growth in the

number and value of new property

projects

• In order to be competitive in this

environment, we need to keep our

property up to date

CONSUMER TRENDS

STRUCTURE

• At the peak of the market, there will be

a set of consumer demands which will

become standard for Class A

properties

• We must ensure that our properties are

sufficiently equipped to meet the

demands of both tenants in purchasers

in 2018

BUILDING CLASSIFICATION

STRUCTURE

• If we do not ensure sufficient Capex, it

is possible several properties may be

downgraded to Class B

26 Cutler Centre – Creating a luxury entertainment space…The retail space in the Cutler Centre can be renovated and upgraded to leverage market cycles

We propose upgrading and reconfiguring the

10,000sqft of retail space, with the following

proportions of rental space in mind;

• 40% of rental space dedicated towards

formal luxury dining

– This establishes a convenient platform for

office tenants to use as a meeting and

entertaining space

• 40% of rental space dedicated towards

casual dining

– This leverages the catering needs of office

space tenants

• 20% of rental space dedicated towards a

bar or other licensed facility

– This helps meet the entertainment and

social needs of tenants

Luxury Entertaining

UPGRADE

An analysis of large scale retail space

renovations indicates an average cost of

between $340-1200 sq ft. We believe our

renovations will cost roughly $5M

Costings

EVALUATION

Measuring Return

RESULTS

2013-2014

26

3%Post Value Add Growth Rate

1-1.5%Decrease in exit Cap Rate

27 Rivers Tower – Stronger communities…Updating shared spaces within the River Tower will drive down exit yields while increasing NOI

We propose renovating the

estimated 24,000 square feet of

lobby and shared space in Rivers

Tower. This will be critical to

decreasing the vacancy rates,

increasing rates and compressing

exit yields

• As we are aiming to sell at the

peak of the market in 2018 , we

believe it is critical to ensure the

building is designed well

– As such, we have allocated

capital towards graphic

design and architecture

Lobby & Shared Space Upgrades

UPGRADE

An analysis of large scale office space

renovations indicates an average cost of

between $200-300 sq. ft. We believe our

renovations will cost roughly $6M.

Costings

EVALUATION

Measuring Return

RESULTS

2013-2014

27

Post Value Add Growth Rate

1-1.5%Decrease in exit Cap Rate

2%

4.9-7M Value Add

28 Bryant Plaza – Changing the platformWe can elevate Bryant Plaza’s value by changing the way space is utilized and leveraging it’s geographic position

We are proposing two major changes to

Bryant Plaza

Rooftop Bar

• The excellent views offered by Bryant

Plaza create the opportunity for us to

build a rooftop bar

• This would drive up rent in 2018-19,

increasing the sale price

Underground Carpark

• Bryant Plaza’s access to motorways

creates an opportunity to generate

excess cash returns

• The Los Angeles population uses cars

heavily

Parking & Bars

UPGRADE

An analysis of large scale retail space

renovations indicates an average cost of

between $450 sqft. We believe our renovations

will cost roughly $6M

Costings

EVALUATION

Measuring Return

RESULTS

2013-2014

Generates 1.8 extra

revenue per annum

Present Value of

6.8M

29 Exiting the position - Selling and Profiting…The debt on the portfolio matures after the next interest payment, thus there is a clear need to refinance

2018

5.5%

Target Exit

Cap Rate

311.4

USD Exit

River

Tower

125.7M

USD

Bryant

Plaza

74.6M

USD

Cutler

Center

111M

USD

130M USD Levered

Free Cash Flow in Year

8

WHY SELL IN 2018?

Market Cycles

Our analysis indicates that the

market will peak between 2017 and

2020.

In order to be conservative and

avoid mistiming the market, we

believe 2018 is strong target sale

period

Capitalization Rates

We believe the current interest rate

environment will persist in general

terms for the next decade

This, along with the general

economic recovery, will compress

capitalisation rates and thus

increase our sale price

30

Increasing Likelihood

Incre

asin

g Im

pact

Strategic

Failure

Macroeconomic

Challenge

Tenant

Risk Matrix

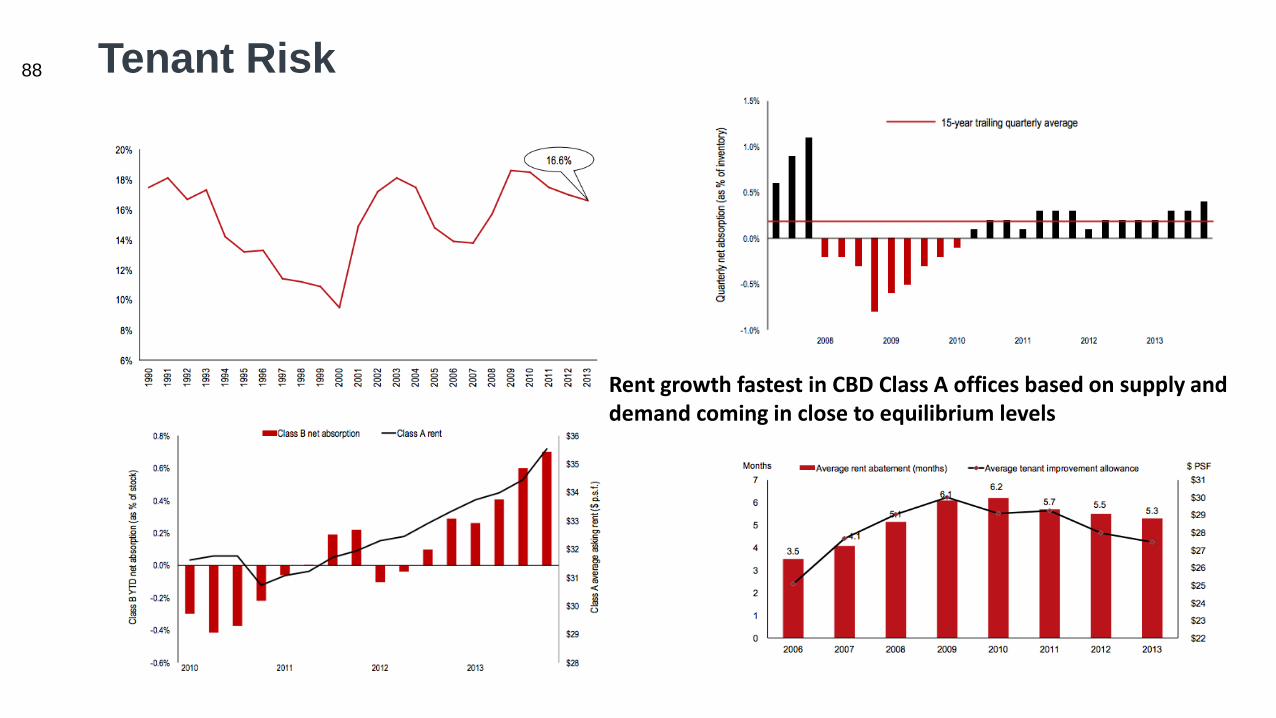

Overview: Commercial properties are

sensitive to market conditions.

Due to the post-recession environment,

unemployment rates and US office market

vacancy rates has increased steadily across

the nation.

We believe these factors may impact our

ability to find quality tenants when rents

rollover in 2012.

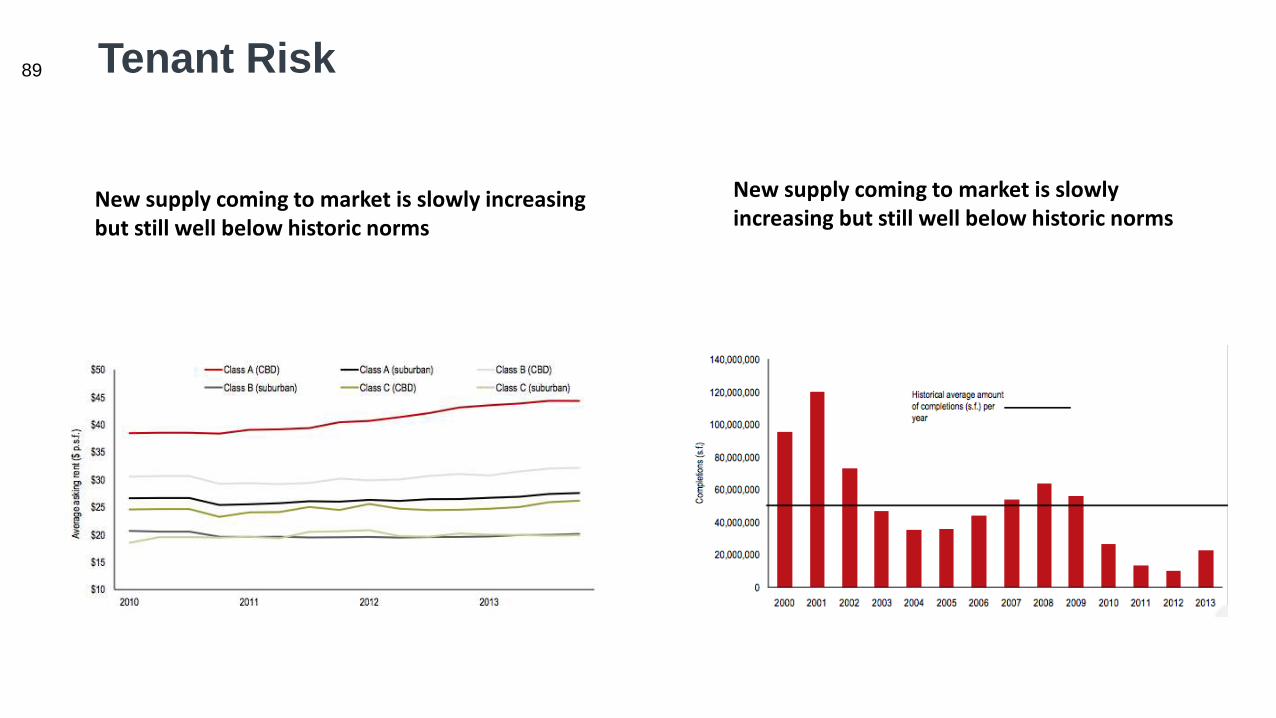

Overview: Delinquency rates of commercial

real estate loans are rising rapidly and the

market currently holds record levels of

outstanding commercial debt mortgage.

Rent growth and net absorption has also

experienced declines. We believe these

factors proposes a risk of tenants’ default on

lease repayments or loans.

Overview: We believe we will be exposed to

interest rate risks when we refinance our

loans.

Additionally, the presence of Mezzanine

loans on two of the properties, which will lein

on SunRock, need to managed carefully.

Strategic Risks Overview:

Exposure to senior debt risk.

Construction and renovation risks

due to impacted construction

industry.

Macroeconomic Risk

Tenant Risk

Financing Risk

Strategic Risk

Financing

Failure

Analysing Risk…The debt on the portfolio matures after the next interest payment, thus there is a clear need to refinance

31 Recapping our strategyWe believe that performing a debt to equity conversion will allow us to deliver results in line with our portfolio’s needs

21M USD

Purchase

Equity Injection

17M USD

130M USD

Free Cash Flow

Exit

27M USD

After conducting appropriate

negotiations and due diligence, we

should move to purchase the

portfolio at a 75% discount to it’s

face value.

We should leverage our lein against

the borrowers equity and our

capacity to limit investor losses to

convert out mezzanine loans to a

proprietary interest in the properties

We should renovate all three

properties to maintain their class A

classification.

SWAPACQUIRE

RENNOVATE

We believe that we will be in the

end of a strong bull real estate

market in 2018. Thus, we should

sell them

SELL

323232

SUMMARY AND OVERVIEW

32

33 Valuing our returnsWe believe that performing a debt to equity conversion will allow us to deliver results in line with our portfolio’s needs

Cutler Centre – West Loop, CH

Bryant Plaza, Downtown, LA

Rivers Tower – Downtown, SD The PortfolioProperty Returns

Unlevered IRR: 63.20%

Unlevered Equity Multiple: 13.70 x

Levered IRR: 22.69%

Levered Equity Multiple: 4.55 x

Property Returns:

Unlevered IRR: 48.12%

Unlevered Equity Multiple: 9.28 x

Levered IRR: 25.94%

Levered Equity Multiple: 4.41 x

Return Metrics

Unlevered IRR: 55.96%

Unlevered Equity Multiple: 11.47 x

Levered IRR: 22.28%

Levered Equity Multiple: 4.11 x

130M

Levered

Sale

27M Free Cash

Flow Equity

(excluding sale)

48M

Levered

Sale

6M Free Cash

Flow Equity

(excluding sale)

47M

Levered

Sale

2.68M Free Cash

Flow Equity

(excluding sale)

35.6M

Levered

Sale

17M Free Cash

Flow Equity

(excluding sale)

Property Returns:

Unlevered IRR: 56.61%

Unlevered Equity Multiple: 11.53 x

Levered IRR: 19.06%

Levered Equity Multiple: 3.56 x

34 Recapping our presentationWe believe that performing a debt to equity conversion will allow us to deliver results in line with our portfolio’s needs

Acquisition

and Due

Diligence

Debt-

Equity

Swap

Holding &

Renovation

Sale & Exit

Due Diligence Checklist

Property & Markets

Borrower Position

Legal Structure & Documents

Other Creditors

Servicing History

21M Portfolio Purchase

LEVERAGE

We believe that our

claim against the

borrowers equity

and said borrowers

poor financial

position will

persuade the

borrower to accept

our DIL

Persuasive Factors

UPGRADES

Renovations are

necessary as a

defensive move to

ensure that the

property remains

Class A and can

fully capture the

economic recovery

Defensive Renovations

BEGINNINGS RETURNS

Expected Returns

Return Metrics

Unlevered IRR: 55.96%

Unlevered Equity

Multiple: 11.47 x

Levered IRR: 22.28%

Levered Equity Multiple: 4.11 x

353535

APPENDIX

35

363636

APPENDIX DIVISION 1 – MARKET RESEARCH

36

37

W

US Property Market Information

CRE Index

• Moodys/REAL commercial property price index

• (CPPI) is based on actual repeat sales of a

large sample of CRE properties

• Transaction-based index (TBI) also uses sales

prices, but employs a different index

methodology and a smaller property sample.

• Figure 1 shows the behaviour of the

aggregated all-properties CPPI and TBI

indexes from 2004 and 2011

FRBSF ECONOMIC LETTER 2011-29 September 19, 2011

Cap Rates and Commercial Property Prices BY BART HOBIJN, JOHN KRAINER, AND DAVID LANG

Commercial real estate capitalization rates have been found to be good indicators of expected

returns in commercial properties. Recent declines in these cap rates appear to be signaling a

commercial real estate rebound, indicating improved investor expectations of price growth in

the market. Movements in national cap rates are the predominant drivers of changes in cap

rates in local markets. Therefore, the anticipated commercial real estate rebound is likely to be

widespread across many metropolitan areas.

The total value of U.S. private nonresidential structures, including office, industrial, and retail

properties, is about $11 trillion, according to the U.S. Commerce Department’s Bureau of Economic

Analysis. That compares with an estimated $17 trillion in the total value of residential structures in the

United States. Given the size of the market for commercial real estate (CRE), it is important to

understand CRE price movements. The Massachusetts Institute of Technology Center for Real Estate

publishes two widely used CRE price measures. The Moodys/REAL commercial property price index

(CPPI) is based on actual repeat sales of a large sample of CRE properties. The transaction-based index

(TBI) also uses sales prices, but

employs a different index methodology

and a smaller property sample. Figure

1 shows the behavior of the aggregated

all-properties CPPI and TBI indexes

from 2004 to 2011.

From the second quarter of 2007

through the fourth quarter of 2009,

both indexes dropped sharply, with the

CPPI falling 41% and the TBI 39%.

However, since the beginning of 2010,

these indexes have been painting very

different pictures. The CPPI indicates

that, since the end of 2009, CRE prices

have slid 7%. But the TBI indicates that

CRE prices have actually risen 19%

over that period. This unusual

deviation in these two indexes raises

the questions of whether CRE prices are currently recovering and how prices are likely to behave going

forward. To explore what may happen to these prices, we consider the capitalization rate, or cap rate for

short, as an alternative indicator of CRE valuations.

Figure 1

Two measures of commercial real estate prices

Sources: Moodys/MIT Center for Real Estate. Both indexes are based on

“all properties.”

50

60

70

80

90

100

110

2004 2005 2006 2007 2008 2009 2010 2011

Index

CPPI

TBI

38

W

Situational Overview

Context

Current date and location: North America Jan 1 2010

Unemployment topped 10% at end of 2009

Central business district offices fell about 53% from 2007 levels – this class is closely related to unemployment and hiring trends

Market may bottom out in 2010 – office vacancies touching 19% -any recovery for offices dependent on jobs

Some areas weathered the downturn better than others – location is important – focus on locations with educated workforces, strong population growth, prevalence of desirable industries such as IT

Deal activity going forward to be focused on modern, well leased, stable cash flow, well positioned assets – outside these markets, recovery will lag for some time

Overall delinquency rate (number of loans with delinquency payments/total number of loans held) has more than doubled since Aug 2008

Loans on properties in secondary markets are delinquent at about 2x the rate of those loans on primary market properties

Investor profile

SunRock Capital – opportunistic, global real estate investment management company

Core (Core plus): least risky because often target stabilised, fully leased, secure investments in core markets; well kept and require no improvements by owner; usually warrants low leverage acquisitions

Value add: seek to increase cash flow over time by making improvements to or reposition property; medium to high leverage used to acquire

Opportunistic: require significant rehabilitation; usually fully vacant upon acquisition or need to be developed from the ground up; offer highest level of return if successful; bears most risk as property has no in-place cash flow; usually high leverage acquisitions

HQ in NYC

Past strategies: high yield superior risk adjusted returns; significant renovations of properties, foreclosures (loan to own scenarios –acquisition of secured debt position to influence control and ultimately acquire ownership of target); asset repositioning where relevant

Most recent fund – SRC Capital VI

Closed in Q1 2009 with $1.5b in equity from pension funds, endowments, sovereign wealth funds, HNW individuals

Target gross returns of 20% IRR and 2x equity multiple on investment

MOI – multiple on investment

39

W

Situational Overview

The opportunity

Off market opportunity with another real estate private equity fund (HRC Capital)

Opportunity: Buy a portfolio of 3 loans on class A office buildings in 3 different North American cities

Classes reflect different risk and return – graded on location, physical characteristics, tenant levels, rental income etc.

Class A = highest quality building in the area and market; generally newer properties built within the last 15 years with top amenities, high income earning tenants and low vacancy rates; well located in the market and typically professionally managed; typicallydemand highest rent with little or no deferred maintenance issues

While HRC waits for our response, the loans will move between 60-90c on the dollar

Each loan is at the fulcrum point in the capital stack of the corresponding property

Capital fulcrum point – measures the annual % growth rate required from the underlying instrument for you to do equally well in terms of capital appreciation from its associated warrant (security that entitles the holder to buy the underlying stock of the issuing company at a fixed price called exercise price until the expiry date); the indifference point between buying a warrant rather than the stock in a company

Warrants are derivative instruments, are dilutive (Receive new stock when exercised), do not pay dividends or come with voting rights; traditional warrants are issued with bonds

ALL LOANS MUST BE PURCHASED IF THE DECISION IS BUY

40

W

Situational Overview

Portfolio & asset history

Loans originated from part of a larger office portfolio acquisition at the peak of the market in 2007

Sponsor expected to find easy refinancing for the Class A, iconic assets when loans matured in mid-2012, given the properties’ (now aggressive) underwriting and assumed steady property market increases

Properties are geographically dispersed

Portfolio relatively uniform in quality

The 3 buildings backing the loans are of a representative quality

Loans organised in complex structure

Debt was split and syndicated to multiple parties, including CMBS and mezzanine debt holders

Commercial mortgage backed securities (CMBS) – type of MBS secured by mortgages on commercial properties. CMBSs are a group of commercial loans on properties such as apartment complexes, factories, office buildings etc. that are bucketed into various tranches (usually 3-4). Tranches are ranked from senior (highest quality) to lowest quality

Mezzanine debt - occurs when a hybrid debt issue is subordinated to another debt issue from the same issuer. Mezzanine debt has embedded equity instruments attached, often known as warrants, which increase the value of the subordinated debt and allow greater flexibility when dealing with bondholders; enables firm to gain capital without offering any collateral, if business defaults on the loan, the lender can convert its loan into an ownership stake using options or warrants built into the deal; charges higher interest rate (usually 15-18%) due to

lack of due diligence, higher risk and is subordinate to higher forms of debt; The value of the warrant is a floating number based on the future value of the company

Mezzanine debt v senior debt: Mezzanine debt is a hybrid form of capital that is part loan and part investment. Senior debt is a loan from a bank. There are many differences between the two. Banks lend off of asset values so most senior loans are collateralized with assets. The bank loan is always secured and in the first position. Mezzanine debt is not collateralized by assets and is usually in the second position with assets. Mezzanine loans are made against the cash flow, not the assets of the business. Because of this feature, mezzanine debt providers use different criteria than banks in qualifying borrowers. They look closely at their EBITDA, their EBITDA margins, and the strength of their historical cash flow.

When market declined and office portfolio didn’t perform to underwritten projections, delinquencies weighed on the 3 loans in the portfolio

Sponsor worked with lenders on several strategies to consolidate loans and get them out of delinquency

After successfully bringing the loans up to date, holder of mezzanine pieces (HRC Capital) decided to market the loans

HRC offered a potential off market deal to SunRock before bringing the opportunity to more investors

HRC (the borrower) is an established private equity fund – specialises on owning and operating office assets across US (bulk of portfolio in top quality assets in major urban markets such as NYC and WDC)

41

W

US Property Market Information

• The Federal Reserve left the target range for its

federal funds rate unchanged at 1 percent to

1.25 percent during its July 2017 meeting and

said it will start reducing its USD 4.5 trillion

portfolio relatively soon.

• The committee considered near-term risks to

the economic outlook as roughly balanced, but

said it will closely monitor inflation

• Interest Rate in the United States averaged

5.78 percent from 1971 until 2017, reaching an

all time high of 20 percent in March of 1980

and a record low of 0.25 percent in December

of 2008.

42

W

US Property Market Information

Capitalisation Rates

• If rents are expected to increase

property has become more valuable

owner will expect a higher capital gain

lead to a lower cap rate

• During GFC, CRE prices dropped about

40% and the market for financing CRE

transactions was severely disrupted,

resulting in very high CMBS yields.

• Since summer 2010, yields on highly

rates CMBS have increased about

0.30%. However, cap rates have come

down 0.50%.

– Decline in cap rates despite the slight

increase in interest rates suggest that

investor expectations for CRE price

appreciation have strengthened

FRBSF Economic Letter 2011-29 September 19, 2011

2

Cap rates as an indicator of future price returns

The cap rate measures the ratio of net operating income to the price of a property. It can be interpreted

as the CRE equivalent of the price/earnings ratio in the stock market (see Campbell and Shiller 1988 for

the pricing implications of these valuation measures). According to theory, this rent/price ratio is largely

a function of interest rates and expected increases in the property’s price. Consider someone who wants

to use a real estate property for one year. This person can get the space in two ways. He or she could rent

the property for the year, which would cost a year of rent. The rent would appear as part of the property

owner’s net operating income. Alternatively, the person who wants to use the property could borrow

money, buy it, and hold it for a year. The cost of this ownership option, referred to as the user cost,

consists of interest payments on the purchase loan plus the expected change in the property’s price over

the holding period. In a well-functioning market with zero transactions costs, the price of these two

alternatives should be the same. If they were not—if rents were higher than the user cost, for example—

then all market participants would want to buy, bidding up prices until the rental option cost the same.

The important point here is the direct link between the net operating income of the rental option and

prices, ownership costs, and expected capital gains of the ownership option. When purchasing CRE,

market participants often link cap rates to expected future rental rates and vacancies. Expected increases

in rent or lower vacancies tend to lower the cap rate. If rents are expected to increase, then the property

has become more valuable and the owner will expect a higher capital gain, which will lead to a lower cap

rate. A similar argument can be made for falling vacancies.

Thus, expected price appreciation is ultimately a reflection of the outlook for fundamentals such as rents

and vacancies. However, there could also be unidentified nonfundamental reasons for changes in

expected price appreciation. For example, investor sentiment may improve and the discount rate applied

to cash flows from a property may fall, thereby lowering the cap rate. Indeed, investor sentiment could

become so exuberant that a bubble could form, in which expected appreciation soared and the cap rate

dropped sharply.

This link between cap rates, interest

rates, and expected price appreciation

is not merely theoretical. Using a

slightly different representation of the

cap rate, Ghysels, Plazzi, and Valkanov

(2007) show that it predicts CRE

returns. In our data we can see these

linkages in Figure 2, which compares

CRE cap rates with the interest paid on

loans to finance CRE transactions. We

focus here on the office market, but

other CRE asset classes have behaved

similarly. Ideally, the interest measure

should be the rate on new CRE loans,

but those are not readily obtainable.

Instead, we use as a proxy for CRE

purchase loans the yield on AAA-rated five-year commercial mortgage-backed securities (CMBS), which

finance a large share of CRE transactions.

Figure 2

Office building cap rates and CRE mortgage rates

Sources: CB Richard Ellis (CBRE) and Commercial Real Estate Direct.

0

1

2

3

4

5

6

7

8

9

10

0

2

4

6

8

10

12

14

16

18

20

2004 2005 2006 2007 2008 2009 2010 2011

Percent Percent

CMBS yield (left axis)

Office cap rate (right axis)

Summer2010

43

W

US Property Market Information

Terminology:

Net Absorption: Absorption is the amount of space

or units leased within a market or submarket over a

given period of time (usually one year).

Absorption considers both construction of new

space and demolition or removal from the market of

existing space. It represents the demand over a

specified period, contrasted with supply.

When supply is less than demand, vacancy

decreases and absorption is positive.

When supply is greater than demand, vacancy

increases and absorption is negative.

44

W

Chicago Property Market Information

Overall, the CBD remains a landlord’s market as

rent continues to increase across all building

classes and fewer concessions are granted. Limited

availability of quality high-rise space coupled with

continued corporate migration into the CBD has

solidified an advantageous environment for

landlords; however, tenants in a position to open

negotiations with landlords in 2017 will be looking at

a more tenant favourable market as approximately

2.3 million square feet are delivered in early 2017.

As this space is delivered to the market, landlords

will seek to avoid losing tenants to the new

developments, which will likely increase

concessions granted to tenants.

Investors see value in Chicago’s assets as they

offer a significant discount in pricing relative to

comparative properties on the coasts and believe

Chicago’s diverse economy and talented workforce

make for strong investments.

45

W

Chicago Property Market Information

• From 2009 – 2015, the vacancy rates

have continually dropped

– Total decline of 3.8%

• Period 2009 had a net absorption of -

1,614,937

– Oversupply of office properties

• Can be explained by the effect of the GFC

that caused a loss of jobs, a decline in real

income, a slowdown in industrial production

and manufacturing and a slump in

consumer spending

• From 2010 – 2011, economy began to

recover as vacancy rates declined and

net absorption levels became positive

again.

46

W

Chicago Property Market Information

• From 2009 – 2015, the vacancy rates

have continually dropped

– Total decline of 3.8%

• Period 2009 had a net absorption of -

1,614,937

– Oversupply of office properties

• Can be explained by the effect of the GFC

that caused a loss of jobs, a decline in real

income, a slowdown in industrial production

and manufacturing and a slump in

consumer spending

• From 2010 – 2011, economy began to

recover as vacancy rates declined and

net absorption levels became positive

again.

• The CBD’s overall vacancy decreased by 70

basis points over the past year, falling from

12.3 percent to 11.5 percent. Vacancy

decreased by at least 50 basis points across all

assets classes, with Class A leading the way

with an 80 basis point decrease during the

fourth quarter.

47

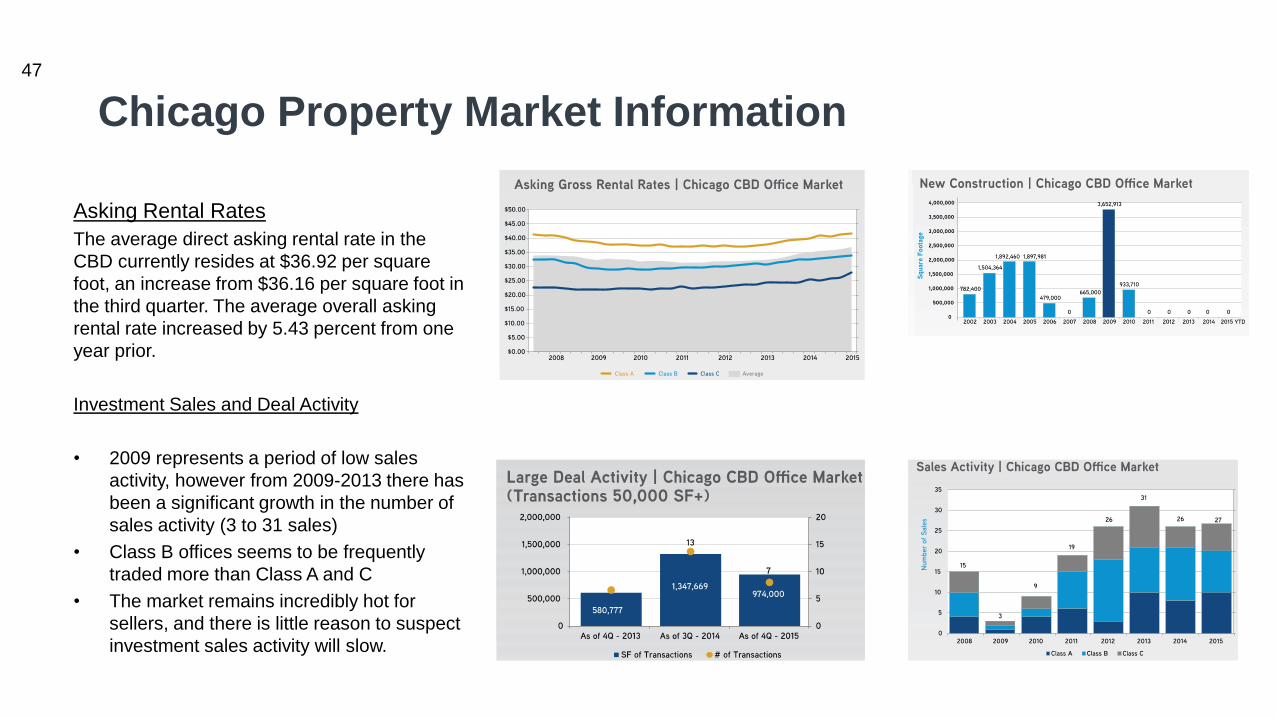

W

Chicago Property Market Information

Asking Rental Rates

The average direct asking rental rate in the

CBD currently resides at $36.92 per square

foot, an increase from $36.16 per square foot in

the third quarter. The average overall asking

rental rate increased by 5.43 percent from one

year prior.

Investment Sales and Deal Activity

• 2009 represents a period of low sales

activity, however from 2009-2013 there has

been a significant growth in the number of

sales activity (3 to 31 sales)

• Class B offices seems to be frequently

traded more than Class A and C

• The market remains incredibly hot for

sellers, and there is little reason to suspect

investment sales activity will slow.

48

Chicago Property Market Information

49

W

Los Angeles Property Market Information

• Net Absorption: The absorption rate is the rate at

which available properties are sold in a

specific real estate market during a given time

period. It is calculated by dividing the total number

of available homes by the average number of

sales per month.

cushmanwakefield.com I 5

MARKETBEAT

About Cushman & WakefieldCushman & Wakefield is a leading global real estate services firm that helps clients transform the way people work, shop, and live.

Our 43,000 employees in more than 60 countries help investors and occupiers optimize the value of their real estate by combining

our global perspective and deep local knowledge with an impressive platform of real estate solutions. Cushman & Wakefield is

among the largest commercial real estate services firms with revenue of $5 billion across core services of agency leasing, asset

services, capital markets, facility services (C&W Services), global occupier services, investment & asset management (DTZ

Investors), project & development services, tenant representation, and valuation & advisory. To learn more, visit

www.cushmanwakefield.com or follow @CushWake on Twitter.

Copyright © 2017 Cushman & Wakefield. All rights reserved. The information contained within this report is gathered from multiple

sources considered to be reliable. The information may contain errors or omissions and is presented without any warranty or

representations as to its accuracy.

Greater Los AngelesOffice Q1 2017

OFFICE SUBMARKETS

Cushman & Wakefield

601 S. Figueroa Street

47th Floor

Los Angeles, CA 90017

For more information, contact:

Eric Kenas, Market Director, Research

Tel: +1 213 955 6446

Vincent Chang, Senior Analyst

Tel: +1 213 955 5125

cushmanwakefield.com I 1

MARKETBEAT

Greater Los AngelesOffice Q1 2017

Economic Indicators

Market Indicators (Overall, All Classes)

Overall Net Absorption / Overall Asking Rent

4Q TRAILING AVERAGE

Overall Vacancy

Q1 16 Q1 1712-Month

Forecast

Los Angeles Employment 4.36M 4.44M

Los Angeles Unemployment 5.6% 4.9%

U.S. Unemployment 4.9% 4.8%

Q1 16 Q1 1712-Month

Forecast

Vacancy 14.4% 14.4%

YTD Net Absorption (SF) 1.4M 232K

Under Construction (SF) 1.8M 2.4M

Average Asking Rent* $2.84 $3.13

*Rental rates reflect gross asking $PSF/MO

EconomyU.S. job growth trend remains firmly in place and nonfarm payroll

employment has now increased for 78 consecutive months. Employment

growth in the first quarter of 2017 was solid—averaging 178,000 jobs

per month. The unemployment rate in Los Angeles County reached its

lowest level in 10 years, declining to 4.8% in February. In the last year,

nonfarm employment grew by 70,800, or +1.6%. Education and health

services listed the largest employment gains, adding 31,300 jobs. The

only sector with a reduction in jobs was manufacturing, influenced

primarily by the increasing weakness in the apparel industry.

Unemployment is expected to decline slowly over the next two years as

the county reaches full employment in 2018.

Market OverviewFirst quarter leasing activity of 2.7 million square feet (MSF) fell short of

the 3.5 MSF quarterly average in 2016. Activity was largely concentrated

in LA West with over 1.0 MSF of new leasing and also making up more

than half of the top key transactions. Net absorption was positive for the

14th consecutive quarter, but due to major construction completions in

each of the past four quarters, overall vacancy remained relatively flat

year-over-year (YOY) at 14.4%. New high-end product catering to the

rapidly evolving tenant demands has helped push overall average asking

rental rates to $3.13 per square foot per month (PSF/MO), for an

increase of 10.2% from a year ago. This was the first time since 2008

that there has been such a vigorous YOY increase in average asking

rental rates. Most of this rent growth was attributed to submarkets

outside of the CBD. LA Metro (non-CBD) overall average asking rents

have increased by over +9% YOY, whereas in the CBD they’ve

increased by +4.6%. In a sign of increased demand within the CBD,

prominent tenants are moving into the market and some CBD landlords

are now asking as high as almost $5.00 PSF/MO for premium space.

Investment sales volume by SF outpaced first quarter 2016 by +14%,

reaching 4.1 MSF. With 1.4 MSF or 34% of the transactions occurring in

TriCities, specifically the highest volume in Glendale. There are 3.4 MSF

of office developments in the Greater LA construction pipeline, with

nearly 2.0 MSF delivering by the end of 2017.

OutlookThe office sector is evolving as the definition of creative space broadens

and new tech innovations shape up the modern day workplace. These

new requirements are impacting nearly every submarket in Greater LA.

Office demand is driven by the labor market, and as we approach full

employment leasing should remain robust and continued rent growth is

expected. In 2017, new office supply catering to these demands may

cause vacancy to decline at a more tepid pace. Los Angeles is at the top

of list as an investment target market nationally and sales volume is

anticipated to exceed 2016 levels and with higher per square foot prices.

LOS ANGELES COUNTY

$2.25

$2.50

$2.75

$3.00

$3.25

-500

0

500

1,000

1,500

2012 2013 2014 2015 2016 2017

Net Absorption, KSF Asking Rent, $ PSF

10%

12%

14%

16%

18%

20%

2012 2013 2014 2015 2016 2017

5-Year Historical Average = 16.6%

cushmanwakefield.com I 1

MARKETBEAT

Greater Los AngelesOffice Q1 2017

Economic Indicators

Market Indicators (Overall, All Classes)

Overall Net Absorption / Overall Asking Rent

4Q TRAILING AVERAGE

Overall Vacancy

Q1 16 Q1 1712-Month

Forecast

Los Angeles Employment 4.36M 4.44M

Los Angeles Unemployment 5.6% 4.9%

U.S. Unemployment 4.9% 4.8%

Q1 16 Q1 1712-Month

Forecast

Vacancy 14.4% 14.4%

YTD Net Absorption (SF) 1.4M 232K

Under Construction (SF) 1.8M 2.4M

Average Asking Rent* $2.84 $3.13

*Rental rates reflect gross asking $PSF/MO

EconomyU.S. job growth trend remains firmly in place and nonfarm payroll

employment has now increased for 78 consecutive months. Employment

growth in the first quarter of 2017 was solid—averaging 178,000 jobs

per month. The unemployment rate in Los Angeles County reached its

lowest level in 10 years, declining to 4.8% in February. In the last year,

nonfarm employment grew by 70,800, or +1.6%. Education and health

services listed the largest employment gains, adding 31,300 jobs. The

only sector with a reduction in jobs was manufacturing, influenced

primarily by the increasing weakness in the apparel industry.

Unemployment is expected to decline slowly over the next two years as

the county reaches full employment in 2018.

Market OverviewFirst quarter leasing activity of 2.7 million square feet (MSF) fell short of

the 3.5 MSF quarterly average in 2016. Activity was largely concentrated

in LA West with over 1.0 MSF of new leasing and also making up more

than half of the top key transactions. Net absorption was positive for the

14th consecutive quarter, but due to major construction completions in

each of the past four quarters, overall vacancy remained relatively flat

year-over-year (YOY) at 14.4%. New high-end product catering to the

rapidly evolving tenant demands has helped push overall average asking

rental rates to $3.13 per square foot per month (PSF/MO), for an

increase of 10.2% from a year ago. This was the first time since 2008

that there has been such a vigorous YOY increase in average asking

rental rates. Most of this rent growth was attributed to submarkets

outside of the CBD. LA Metro (non-CBD) overall average asking rents

have increased by over +9% YOY, whereas in the CBD they’ve

increased by +4.6%. In a sign of increased demand within the CBD,

prominent tenants are moving into the market and some CBD landlords

are now asking as high as almost $5.00 PSF/MO for premium space.

Investment sales volume by SF outpaced first quarter 2016 by +14%,

reaching 4.1 MSF. With 1.4 MSF or 34% of the transactions occurring in

TriCities, specifically the highest volume in Glendale. There are 3.4 MSF

of office developments in the Greater LA construction pipeline, with

nearly 2.0 MSF delivering by the end of 2017.

OutlookThe office sector is evolving as the definition of creative space broadens

and new tech innovations shape up the modern day workplace. These

new requirements are impacting nearly every submarket in Greater LA.

Office demand is driven by the labor market, and as we approach full

employment leasing should remain robust and continued rent growth is

expected. In 2017, new office supply catering to these demands may

cause vacancy to decline at a more tepid pace. Los Angeles is at the top

of list as an investment target market nationally and sales volume is

anticipated to exceed 2016 levels and with higher per square foot prices.

LOS ANGELES COUNTY

$2.25

$2.50

$2.75

$3.00

$3.25

-500

0

500

1,000

1,500

2012 2013 2014 2015 2016 2017

Net Absorption, KSF Asking Rent, $ PSF

10%

12%

14%

16%

18%

20%

2012 2013 2014 2015 2016 2017

5-Year Historical Average = 16.6%

cushmanwakefield.com I 4

MARKETBEAT

Greater Los AngelesOffice Q1 2017

MARKETTOTAL

BUILDINGS

INVENTORY

(SF)

DIRECT

VACANCY

RATE

OVERALL

VACANCY

RATE

YTD

LEASING

ACTIVITY

(SF)

YTD

OVERALL NET

ABSORPTION

(SF)

UNDER

CONSTRUCTION

(SF)

OVERALL

AVERAGE

ASKING RENT

(ALL CLASSES)*

DIRECT

AVERAGE

ASKING RENT

(CLASS A)*

Los Angeles CBD 54 27,218,777 19.1% 19.9% 253,089 17,749 356,141 $3.42 $3.49

Los Angeles Central (Non-CBD) 140 20,315,970 14.3% 14.3% 128,374 378,046 334,201 $2.63 $2.75

Los Angeles West 416 52,797,801 11.3% 12.3% 1,011,384 (465,863) 1,171,175 $4.51 $4.64

Los Angeles North 407 31,332,528 10.6% 11.0% 506,752 36,897 355,000 $2.40 $2.50

Los Angeles South 249 30,182,254 15.5% 16.1% 447,561 349,126 159,087 $2.35 $2.68

TriCities 195 24,265,956 12.9% 13.8% 196,036 107,111 0 $2.96 $2.96

San Gabriel Valley 170 12,596,238 16.2% 16.5% 161,009 (190,860) 0 $2.15 $2.33

GREATER LOS ANGELES TOTALS 1,631 198,709,524 13.7% 14.4% 2,704,205 232,206 2,375,604 $3.13 $3.47

Key Lease Transactions Q1 2017

PROPERTY SF TENANT TRANSACTION TYPE SUBMARKET

222 W. Sixth Street / Topaz 99,343 Molina Healthcare New Lease Carson / San Pedro

5800 W. Sunset Boulevard / CUE 91,953 Netflix New Lease Hollywood

1299 Ocean Avenue / Wilshire Palisades 61,792 Wilshire & Associates Renewal Santa Monica

2425 Olympic Boulevard / Water Garden 60,772 Amazon New Lease Santa Monica

1000 S. Fremont Avenue / The Alhambra 50,525 Los Angeles Department of Health New Lease Alhambra / Monterey Park

12105 W. Waterfront Drive / The Brickyard 50,098 Loyola Marymount University New Lease Playa Vista

333 S. Grand Avenue / Wells Fargo – North 49,945 Convene New Lease Bunker Hill

2121 Avenue of the Stars / Fox Plaza 48,461 Fox New Lease Century City

8687 Melrose / Pacific Design Center 46,151 Cedars-Sinai New Lease West Hollywood

2000 Avenue of the Stars 44,898 Annenberg Foundation Renewal Century City

655 N. Central Avenue / Glendale Plaza 44,637 UNIM Renewal Glendale

Key Sales Transactions Q1 2017

PROPERTY OFFICE SF SELLER / BUYER PRICE / $PSF SUBMARKET

21271 & 21281 & 21301 Burbank Boulevard

5700 & 5820 Canoga Avenue898,044 Hines Securities / Oaktree Capital $235,500,000 / $262 Woodland Hills

655 N. Central Avenue 529,508 PGIM Real Estate / DivcoWest $179,000,000 / $338 Glendale

611 N. Brand Boulevard 381,841 LNR Partners / Onni Group $83,000,000 / $217 Glendale

100 N. Barranca Avenue / California State

Bank Tower225,920 LNR Partners / Sunny Hills Palladium $37,170,000 / $165 West Covina

10585 / 10635 Santa Monica Boulevard 171,450Alaska Permanent Fund Corporation /

Onni Group$40,700,000 / $237 West Los Angeles

2300 E. Imperial Highway 157,725 VCI Corp / Nant Health $52,000,000 / $330 El Segundo

200 S. Los Robles Avenue 131,807American Realty Advisors / Faring

Capital$46,000,000 / $349 Pasadena

2411 W. Olive Avenue / Buena Vista Plaza 115,130 TIER REIT / Menlo Equities $52,500,000 / $456 Burbank

3330 Cahuenga Boulevard / California Credit

Union Building103,710 Blackstone / 4M Investment Corp $36,000,000 / $347 Universal City / Studio City

520 N. Central Avenue / Central Building 93,644Prudential Investors / Lincoln Property

Company$19,600,000 / $290 Glendale

*Rental rates reflect gross asking $PSF/MO

cushmanwakefield.com I 2

MARKETBEAT

Greater Los AngelesOffice Q1 2017

Los Angeles CBDThe CBD office market improved moderately as overall vacancy rates

finished at 19.9%, representing a 10-basis point (BP) decrease YOY.

CBD overall asking rents are up +3.8% since this time last year,

reaching $3.42 PSF/MO ($41.04 PSF/YR). Class A direct asking rents

are up +1.7% over the quarter, increasing by $0.06 PSF/MO to $3.49

PSF/MO ($0.68 PSF/YR to $41.88 PSF/YR). First quarter leasing activity

of 253,089 SF fell short of the 2016 quarterly average. Increased

demand in Bunker Hill helped this submarket close four of the top five

largest CBD transactions. Convene, a conference and event hosting

firm, signed a lease for nearly 50,000 SF at Wells Fargo North Tower.

The Census Bureau and the State of California took space in Bunker Hill

for 36,000 SF and 24,000 SF, respectively. Overall net absorption was

minimal at 17,700 SF as the CBD mostly saw some intra-market

reshuffling and less in the way of expansions or new tenant migration.

Los Angeles WestThe Los Angeles West office market commands the highest asking

rental rates and continues to post the strongest rent growth. Over the

past year, asking rental rates have increased by +12.8% for all classes

and +13.3% for Class A. Most of this growth was in Playa Vista and

West Hollywood where asking rents are at $5.25 PSF/MO and $4.91

PSF/MO, respectively. This market has seen a growth in inventory as

major office developments delivered in the first quarter; with more to

come online throughout the year. Demand is strong as leasing volume

totaled over 1.0 MSF in the first quarter, over +7% higher than the

quarterly average in 2016. Construction completions in 2017 will bolster

asking rent growth even further, particularly for Class A product.

Although leasing remains healthy, it remains to be seen if the market will

be able to absorb 1.0 MSF of new office supply delivering in 2017.

TriCitiesOffice fundamentals remain solid in TriCities as direct vacancy rates

finished at 12.9%, making it the sixth consecutive quarter in which direct

vacancy rates stayed below 13%. With the addition of sublease space,

the overall vacancy rate finished at 13.8%, below the average vacancy

rate of 14% from the preceding five years. Overall asking rental rates in

TriCities increased by +2.3% over the quarter, finishing at $2.96

PSF/MO. Most of this growth was in Universal City/No. Hollywood where

asking rental rates increased by +6.7% over the quarter to $2.85

PSF/MO. Net absorption of 107,111 SF represented a +54.7% increase

over the strongest performing quarter in 2016. Burbank captured 76.4%

of TriCities’ first quarter net occupancy gains at 81,886 SF.

Direct Rental vs. Vacancy RateCENTRAL BUSINESS DISTRICT

Direct Rental vs. Vacancy RateTRICITIES

$2.9

2

$2.9

4

$3.1

9

$3.2

2

$3.3

7

$3.4

4

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

$0.00

$1.00

$2.00

$3.00

$4.00

2012 2013 2014 2015 2016 Q1 2017

PS

F/Y

R

DIRECT GROSS RENTAL RATE DIRECT VACANCY RATE

$2.6

7

$2.7

0

$2.6

6

$2.9

5

$2.8

9

$2.9

6

0.0%

5.0%

10.0%

15.0%

20.0%

$0.00

$1.00

$2.00

$3.00

$4.00

2012 2013 2014 2015 2016 Q1 2017

PS

F/M

O

DIRECT GROSS RENTAL RATE DIRECT VACANCY RATE

Direct Rental vs. Vacancy RateLOS ANGELES WEST

$3

.34

$3

.43

$3

.64

$4

.01

$4

.33

$4

.55

0.0%

5.0%

10.0%

15.0%

20.0%

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

2012 2013 2014 2015 2016 Q1 2017

PS

F/M

O

DIRECT GROSS RENTAL RATE DIRECT VACANCY RATE

50

W

Los Angeles Property Market Information

• Education and Unemployment

• The highest unemployment rates, in both the City of Los Angeles and Los Angeles County, exist for individuals with an educational attainment of high school or less (Exhibit E-6).

• Residents with a Bachelor’s degree or higher had an unemployment rate of 5.9 percent in the County (7.0 percent in the City) in 2013, roughly half the rate experienced by those at the opposite end of the spectrum—less than a high school education and high school diploma or equivalent reported unemployment rates of 10.1 percent

Executive Summary Los Angeles: People, Industry and Jobs 2014-2019

ii Institute for Applied Economics

Race and Ethnicity

The City of Los Angeles and Los Angeles County as a whole are racially and ethnically diverse. Approximately half of the resident population in both geographies identify as having Hispanic or Latino origins (Exhibit E-4).

Educational Attainment

Educational attainment is a key element in understanding challenges and opportunities present in the available workforce. For an individual, it is a factor in unemployment, earnings potential and poverty status, while from a business perspective, educational attainment of the resident population represents the quality of their labor pool. Areas with high rates of low educational attainment usually face challenges such as higher rates of unemployment and poverty and will therefore use higher levels of public services and resources. The city and county both have a large proportion of their resident population with low levels of educational attainment (Exhibit E-5). Almost 25 percent of the population has less than a high school education and high school graduates (or equivalent) account for an additional 20 percent. As an increased number of jobs require higher skill levels, a shortage of individuals with higher levels of education can result in fewer prospects for their employment, and consequently higher rates of unemployment.

Education and Unemployment

The highest unemployment rates, in both the City of Los Angeles and Los Angeles County, exist for individuals with an educational attainment of high school or less (Exhibit E-6). Residents with a Bachelor’s degree or higher had an unemployment rate of 5.9 percent in the County (7.0 percent in the City) in 2013, roughly half the rate experienced by those at the opposite end of the spectrum—less than a high school education and high school diploma or equivalent reported unemployment rates of 10.1 percent (9.6 percent) and 10.8 percent (11.6 percent) respectively.

48.3%

49.3%

27.0%

28.2%

13.9%

11.2%

8.0%

8.6%

2.2%

2.1%

0.3%

0.3%

0.2%

0.2%

0.2%

0.1%

LA County

City of LA

Exhibit E-4 Race and Ethnicity 2013

Hispanic White Asian

Black Two or More Other Race

Pacific Islander American Indian

Sources: 2013 ACS 1-year estimates

Less than HS

23.1%

Less than HS 25.4%

HS or equivalent

20.4%

HS or equivalent

19.4%

Some College 19.4%

Some College 17.9%

Associates 7.0%

Associates 6.0%

Bachelor's 19.7%

Bachelor's

20.9%

Masters

6.8%

Masters 6.6%

PhD or Prof'l 3.6%

PhD or Prof'l

3.9%

LA County

City of LA

Exhibit E-5 Educational Attainment Population 25 years and over

Population 25+ years: LA County: 6.6 million City of LA: 2.6 million

Source: 2013 ACS 1-year estimates

8.6% 9.2%

10.1% 9.6%

10.8% 11.6%

9.2% 10.0%

5.9%

7.0%

LA County City of LA

Exhibit E-6 Civilian Unemployment Rate by Educational Attainment 2013

Population 25 to 64 years Less than High School

High School or equiv Some college or Associate's Bachelor's or higher

Source: 2013 ACS 1-year estimates

Executive Summary Los Angeles: People, Industry and Jobs 2014-2019

iv Institute for Applied Economics

Exhibit E-12 Industry Employment Growth 2014-2019 in Los Angeles

Annual Average %

Growth

Δ Employment

(000s)

Total Nonfarm Payroll Employment 1.5% 322.0

Good Producing Industries: 0.5% 12.4

Natural Resources and Mining (1.4%) -0.3

Construction 1.8% 11.9

Manufacturing – Durable Goods 0.1% 2.1

Manufacturing – Nondurable Goods (0.0%) -1.2

Service Providing Industries 1.8% 287.6

Wholesale Trade 0.8% 8.6

Retail Trade 0.7% 14.7

Transportation, Warehousing, Utilities 0.7% 5.5

Information 1.4% 14.7

Financial Activities 1.2% 13.1

Professional and Business Services 2.1% 67.8

Educational and Health Services 2.7% 105.6

Leisure and Hospitality 2.3% 54.7

Other Services 0.5% 4.0

Government 0.8% 20.6

Sources: California Employment Development Department; LAEDC