global energy institute – jakarta event - kpmg | us · global energy institute – jakarta event...

TRANSCRIPT

Global Energy Institute – Jakarta Event Cost Transparency Joint Ventures Best Practise

Global Energy & Natural Resources Institutes Global Energy Institute Global Mining Institute Global Chemicals Institute KPMG Singapore – ENR

Tim Rockell

Director

June 2015

3 © 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Thought Leadership FY 2013, 2014, 2015

Singapore Exploring Opportunities in Energy Value Chain (March 2013)

Shale Development: Global Update (July 2013)

The Energy Report Philippine- Growth and Opportunities in Philippine Electric Power Sector (October 2013)

Singapore Performance Optimisation in O&G Upstream (23 April 2013)

An emerging strategic energy relationship (January 2014)

Singapore Energy at Risk Cyber Security (April 2013)

Asia Pacific Energy Conference Summary (April 2013)

No paper chase: Transforming risk management at energy and natural resources companies (March 2014)

Nuclear Power: its role in shaping energy policies in Asia Pacific (May / June 2014)

Asia Pacific's Petrochemical Landscape: A Tale of Contrasting Regions (October 2014)

Future of Procurement: Keeping pace with change in the ENR Sector (February 2015)

Major LNG projects: Navigating the new terrain (September 2014)

Clarity on Commodities Trading: Transforming with agility (April 2015)

Commodity trading– Meeting the challenge of tax and regulatory change (January 2014) When one crisis meets another: Focusing on talent for the long term (April 2015)

Floating LNG: Revolution and evolution for the global industry? (March 2015)

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

4 © 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Global Energy Institute Webcasts FY 2014 and 2015

4

1) Optimizing Cost to sustain business value 2) Global Business Services – Revealed and De-Hyped 3) Global Business Services – Revealed and De-Hyped 4) Floating FLNG: Revolution & Evolution for the global industry 5) Commodity Trading: Changes affecting the O&G industry 6) Major LNG projects: Navigating the new terrain

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

5 © 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Global Energy Institute – Benefits of membership

As a Global Energy Institute (GEI) Member, you will obtain:

Invitation to the Global Energy Conference KPMG’s Global Energy Conference is a flagship regional event orchestrated by the GEI.

It aims to arm energy executives with new tools to better navigate the changes in the dynamic energy and natural resources sector.

Access to white papers, surveys and opinion pieces - Thought Leadership KPMG’s Thought Leadership initiatives comprise of white papers, survey and opinion pieces that provide compelling insights and the latest trends in the energy industry

Invitation to the Global Energy Institute Programs – Webcasts, Business Clubs and Seminars Part of GEI programs, webcasts, business clubs and seminars programs are an effective way for energy executives:

-Gather the latest information on trends affecting the industry. -Allow senior energy industry decision makers to network and obtain broader perspective in energy industry.

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

6 © 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Visit the KPMG Global Energy Institutes in Asia Pacific

The Global Energy Institute - ASPAC kpmg.com/energyaspac

The Global Mining Institute - ASPAC kpmg.com/miningaspac

The Global Chemicals Institute - ASPAC kpmg.com/chemicalsaspac

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

KPMG Cost Transparency KPMG Singapore - ENR

Mark Elia

Director

15 June 2015

8 © 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Background

Stages of Infrastructure Development Le

vel o

f act

ivity

Time

Evaluate risks and market opportunities

Search for commercially exploitable resources

Plant commissioning

Permit and licence applications

Commercial production begins

Expansion of refinery and plant Bankable feasibility study (BFS)

Land and infrastructure application

Feasibility study

Design + Definitive Economic Assessment

Design + Preliminary Economic Assessment

Construction of infrastructure and plant

Governance Performance

Strategy and Planning Project Execution and Management Operations and Performance

Growth

Design and implement market strategy

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

9 © 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Infrastructure Challenges

Key Considerations for JV / Large Scale Projects

Lifecycle Management

Corporate Program Social / Environment

Corporate Governance

Organization Setup

HR Strategies

Finance / Tax

Systems / Controls

Corporate Stakeholder

Governance

Program Stakeholder

Systems / Controls

Procurement

Delivery

Operation Readiness

Labour / Workforce

Security

Economic Impact

Social Effects

Environmental

Governance

JV Portfolio management

JV Strategy

Governance Committees

Roles and responsibilities

Performance Monitoring

Communications

Risk Management framework

Legal Management Framework Support

Processes

System and Technology

Reporting (including non standard KPI)

Board and Management Committees

Policies and Procedures

Capital allocation framework

Resource Planning

Code of conduct and ethics

HR and Performance management

Procurement

Change Management Processes

Wind down

Project Considerations

Operate Transact Establish JV

Operations and Performance Project Execution and Management Strategy and Planning

JV Considerations

10 © 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Infrastructure Challenges

Joint Venture challenges

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Setting clear Terms of reference for JV operations and appropriate Delegations of Authority for the JV board to work against. The establishment of committees that oversee current and future activities including Project Committee, HSE committee, Audit and Risk Committee.

Documented policies and procedures that reflect the spirit of the JV on Human Capital movement and compensation as determined by the intent and context of the JV.

Instill appropriate agreements and controls in managing expenses incurred during the course of construction phase including management of the Joint Account Schedules as at year end. Expense review and charge back mechanism set to remove ambiguity and compexity Alignment between cash calls and the JV agreement including the scheduling and amounts. Process of managing discrepancies / variations between cash call contribution and expense utilisation.

Framework and structured process for ensuring continuity of business operations in the event of JV related and / or environments related incident on the project progress

JV Board Matters Meeting Expectations

Key Appointments Compliance and Transparency

Expense Management Cost Control and Allocation

Cash Calls Working Capital / Cash scheduling

Business Continuity Managing Risk

Alignment

Compliance

Control

Risk

CHALLENGES JV IMPACT

Clarity

11 © 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Infrastructure Challenges

Project development challenges

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Construction and delivery of integrated infrastructure facilities to increase liquefaction capacity. Phased construction to stipulated timelines is intended to deliver to spec infrastructure within budgeted estimate

Management of a complex contracts environment in which multiple modules of infrastructure are delivered by different types of contractors who are required to function within the requirements of a Master Programme

Portfolio of projects are carried out under the umbrella of a Master Programme. Managing interdependencies and aligning the sequence of works to programme objectives is a key discipline in adhering to critical paths. Managing multiple stakeholders operating within the Programme and those with vested interest to ensure delivery is aligned to expectations and expectations are aligned to intent.

The largest constituent cause of cost and supply chain overruns by individual contractors on infrastructure projects is the sourcing and management of materials. Adopting innovative ways of monitoring bill of materials and consumption against progress mitigates risk and cost

Project Pressures Meeting Expectations

Contracts compliance Project efficiency

Programme dependencies Portfolio Management

Stakeholder Management Stakeholders Expectations

Managing materials Value contribution

Control Ratio

Efficiency of supply

Managing complexity

Innovation

CHALLENGES PROJECT IMPACT

Cross-functional collaboration

12 © 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Supporting Project Development

Pillars of project execution

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Project Scope Management

Risk Management

Quality Management

Project Schedule Management

Critical path management

Change Management

Governance

Administration

Communication

Project Engineering and Cost Management

Financial Management

Materials Management

Project Strategy

Cost and Financial

Management

Project Controls,

Quality and Risk

Management

Project Schedule

Management

Programme Management

Integrated Project Set Up

13 © 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Supporting Project Development

Structured framework for delivery

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

14 © 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Supporting Project Development

Focusing on Cost Management

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Mechanical Electrical Instrumentation Civil / Structural

Conceptual Design Evaluations / Approval Design Installation Handover

System Requirements

Functional Analysis

Detailed Analysis

Resource Requirements

Procurement Specifications

Engineering Evaluations

Management Approval

System Requirements

Functional Analysis

Detailed Analysis

Resource Requirements

Procurement Specifications

Purchasing

Procedures

Installation

Modifications

Testing

Functional Testing

Simulation Testing

Performance Testing

CONSTRUCTION: Work Category Breakdown

FEED FID Construction First Gas Operations

All support functions

EPCM

Contractor 1

Contractor 2

Contractor 3

Contractor 4

Costs occur: • Across Project phases • Between Project phases • Across categories of work • Between a number of contractors • Allocated to a number of JV partners • Between ongoing operations,

overheads and projects

15 © 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Supporting Project Development

Focusing on Cost Management

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Costs are incurred: • Services • Material • Equipment • Asset Components • Manpower • Across contracts

Project Cost Breakdown

Categories Sub-categories examples

■ Steel and Steel parts ■ Concrete/ Cement ■ Chemical stuff

Production Materials

■ Architecture and Engineering ■ Transportation/ Logistics ■ Infrastructure services

Subcontractor Services

■ Building extension ■ Civil engineering ■ Building shell

Subcontractor Construction

■ Construction machinery ■ Framework materials ■ Spare parts

Technical Procurement

■ Professional services ■ Marketing and PR ■ Utilities supply

Indirect Spend

27%

11%

26%

8%

29%

27%

11%

26%

8%

29%

16 © 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Supporting Project Development

Focusing on Cost Management / Allocation

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

A. Source B. Route C. Destination

A. WHERE are the costs coming from?

B. HOW do the costs travel?

C. WHERE do they land?

1. Cost pools: Analyse where costs are being accrued across various teams and activities

2. Cost framework: Review the ways costs are classified today and the materiality of certain cost objects/centres

$ 3. Cost allocation: Review the process and mechanics of allocating costs to end cost objects

4. JV environment: Review process to allocate costs to either Joint Venture (JV) projects or sole account (100% corporate)

5. Cost management: Review adherence to various cost management processes e.g: time writing, cost objects, AFE, POs etc

6. Assess your barriers: Identify and assess any barriers to improving your cost culture

7. Set principles: Agree a set of cost principles to shape a cost agenda

!

D. Compliance

D. WHAT are the ‘rules’ of cost allocation in your company?

Systematic approach to allocating costs

Joint Ventures – Best Practices and Current Trends

KPMG’s Global Joint Venture Practice

Brad Johnson

Director

15 June 2015

18 © 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Partnerships are increasing in number and complexity

Growth in revenue and value ■ Joint ventures and alliances make up over 35%

of corporate revenues ■ 100 largest joint ventures worth more than

$350bn revenue p.a.(2)

Relatively high failure rate ■ Average life of joint ventures is seven years(3)

■ Most joint ventures face serious management and/or financial difficulties in first two years(3)

■ Three-quarters of joint ventures end with one party buying out the other(3)

Potential growth Challenges

Growth in partnerships ■ An estimated 5,000 new joint ventures

established in the last five years(1)

■ JVs always popular in ENR, but increasingly they are formed with a strategic focus rather than necessity (e.g. unconventional energy, capability needs, syndicating capital and risk).

Source: (1) Allen & Overy, Trends in International JVs, March 2014, (2) Harvard Business Review, (3) Practical Law: analysis of various surveys of joint ventures in Europe, America and Japan

Inherently difficult governance structures ■ Traditional legal remedies struggle to address

commercial, political, culture and trust issues

■ Parents’ needs change, but the agreements are not flexible enough to change with them

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

19 © 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Topics for today

Best practice in joint ventures to protect value & manage risk

1

Recent trends regarding joint ventures focus & their use

2

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Topic 1: Best practice in joint ventures to protect value & manage risk

21 © 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Joint ventures and alliances should be used when appropriate

Source: Adapted from work by Gulati and Nickerson (2008); Powell (1990); Williamson (1991); Tjemkes et al. (2012)

Before concluding that a partnership is the right solution, it is important to consider alternative governance models, which provide alternative strategic options.

Make Buy Partner

Internal Growth Merger & Acquisition JVs and Alliances

Building and sustaining a competitive advantage

Market Transaction

Activities and resources developed

internally

Activities and resources internalised following a transaction

Activities and resources procured through the market

Access to activities and resources obtained

through collaboration with a third party

Full control Full control Full control Partial control

Hierarchy Hierarchy Price Relational

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

22 © 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Common pitfalls we see businesses encounter

Gets complex and consumes ‘too many’ resources

Partners disagree on respective investments

Different assumptions on standards and processes

Pre-deal operating model insufficiently detailed

JV devised without consultation of who will run it

Optimism bias at the beginning

Complexity of legal and compliance requirements

Diverse partners with diverging goals

Changing views on the uses of cash flow

Stability of key personnel and organisation

Failure to deliver forecast performance

Governance expensive and ineffective

Lack of transparency around costs and revenues

“Fix it on the go” mentality driven by deal deadlines

Setting up the JV Running the JV

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

23 © 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Decrease risk by considering non-traditional measurements

Traditional financial performance and responsiveness measures is usually where performance measurement stops. Unfortunately, they are internal and retrospective. Considering the broader picture can help forward looking risk mapping.

Indicators are more dramatic in joint ventures in which performance materially affects the parent.

The history between the joint venture participants can be significant indicator of future joint venture performance.

Partners with a history of joint ventures, who are familiar with joint ventures and who have a range in their portfolio tend to perform better in joint ventures than companies of which this is not normal repertoire.

The responsiveness of the joint venture to questions, concerns or calls for action by the joint venture participants. Responsiveness

Relativity

Relationship history

Regularity

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

24 © 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Focus on the operating model, then the ownership structure

Even the most sophisticated joint venture structure will fail without appropriate attention to operating model design and practicality.

The operating model is inherently linked to the deal structure, so design both with each in mind. Continually tie back to the vision of the partners.

Leave emotions at the door and consider who has what value to give to the joint venture to maximise your total returns.

Setting deal parameters without detailed work or discussion around the operational model restricts ability to design and create a robust joint venture (most famously, 50/50).

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

25 © 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Appoint neutral 3rd parties to assess JV risk and performance, and to optimise the JV when needed. Protect your relationship.

Design proactive management, rather than rely on reactive governance

Value is at risk of being destroyed at any time of the joint venture lifecycle. Manage the joint venture for what it is ... a partnership, not a subsidiary.

Take time to understand the risk profile of your partner and continue to monitor the JV for their risks as well as yours.

Incorporate flexibility into agreements to maintain relevance to both partners. Focus on relationship, not legal remedy, as path to correction.

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

26 © 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

The operating model is inherently linked to the deal structure, so design both with each in mind. Continually tie back to the vision of the partners and need of the market.

Relevance drives value within and outside of the joint venture

Parent interest tends to focus elsewhere over time, and joint ventures often become stale. Maintain the relevance to decrease risk and retain value.

Empower the management of the joint venture to constantly improve value, rather than allow parents to be overly prescriptive

The world changes, but legal agreements rarely do so themselves. Set regular refresh points in joint venture agreements to keep the joint venture relevant.

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Topic 2: Recent trends regarding joint venture focus & their use

28 © 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

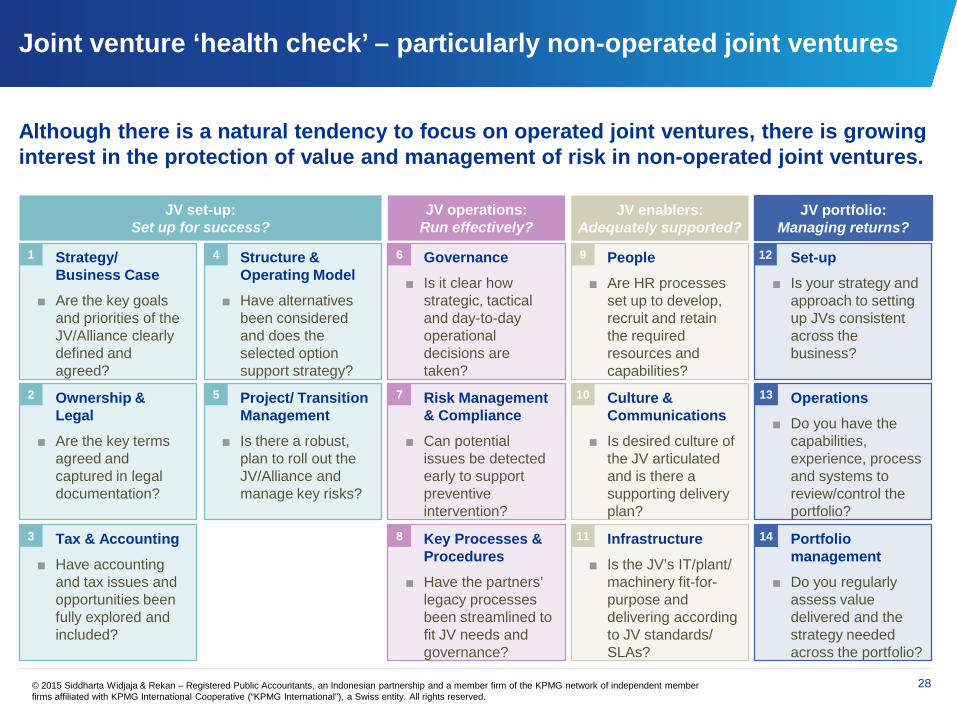

Joint venture ‘health check’ – particularly non-operated joint ventures

JV set-up: Set up for success?

JV operations: Run effectively?

JV enablers: Adequately supported?

Strategy/ Business Case

■ Are the key goals and priorities of the JV/Alliance clearly defined and agreed?

1

Ownership & Legal

■ Are the key terms agreed and captured in legal documentation?

2

Tax & Accounting ■ Have accounting

and tax issues and opportunities been fully explored and included?

3

Structure & Operating Model

■ Have alternatives been considered and does the selected option support strategy?

4

Project/ Transition Management

■ Is there a robust, plan to roll out the JV/Alliance and manage key risks?

5

Governance ■ Is it clear how

strategic, tactical and day-to-day operational decisions are taken?

6

Risk Management & Compliance

■ Can potential issues be detected early to support preventive intervention?

7

Key Processes & Procedures

■ Have the partners’ legacy processes been streamlined to fit JV needs and governance?

8

People ■ Are HR processes

set up to develop, recruit and retain the required resources and capabilities?

9

Culture & Communications

■ Is desired culture of the JV articulated and is there a supporting delivery plan?

10

Infrastructure ■ Is the JV’s IT/plant/

machinery fit-for-purpose and delivering according to JV standards/ SLAs?

11

Operations ■ Do you have the

capabilities, experience, process and systems to review/control the portfolio?

13

Portfolio management

■ Do you regularly assess value delivered and the strategy needed across the portfolio?

14

JV portfolio: Managing returns?

Set-up ■ Is your strategy and

approach to setting up JVs consistent across the business?

12

Although there is a natural tendency to focus on operated joint ventures, there is growing interest in the protection of value and management of risk in non-operated joint ventures.

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

29 © 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Joint venture ‘health check’ – sample of methodology

Strategy/Business Case - Are the key goals and priorities of the JV clear and agreed? 1

Status

1. Clear strategic rationale

2. Identified objectives and priorities

3. Clear, equitable “Win-Win”

4. Scope of activities agreed

5. Alternative partners considered

6. Rationale for selected partner clear, and communicated

7. Growth opportunities and required investment considered

8. Both/all partners agree on the “size of the prize”

9. Up- and downside risks considered in business case

10. Impact of JV on other parts of business assessed (through involvement of delivery lead)

11. Business case assumptions verified and evaluated

12. Assumed partner capabilities based on prior knowledge/experience

13. Key unknown partner capabilities tested/verified

14. Clear likely timeframe for life of Joint Venture

15. Joint Venture “end-game” clear

16. Business planning process clear and agreed

Relevance

Key: Most relevant Semi-relevant Least relevant

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

30 © 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Synergies from complementary assets or capabilities

Cost out focus: Operating with a partner who has similar market pressures

Cooperative mindset: Breadth, reach and scale, working together

Forward-thinking: Partnering with those not traditionally considered

Passionate: Shareholders as customers, but breaking the operator model

Value-adding: Commercialising the venture provides revenue opportunity

Capture back margin by creating industry solutions

In the struggle for improved margins, companies are starting to capture value by establishing joint ventures with multiple competitors and suppliers, to do tasks traditionally outsourced and not core to the business. They then look to commercialize the joint venture and create an industry solution.

© 2015 Siddharta Widjaja & Rekan – Registered Public Accountants, an Indonesian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.