forecasting using - rob j hyndman 1exponential smoothing methods so far 2holt-winters’ seasonal...

TRANSCRIPT

Forecasting using

6. ETS models

OTexts.com/fpp/7/

Forecasting using R 1

Rob J Hyndman

Outline

1 Exponential smoothing methods so far

2 Holt-Winters’ seasonal method

3 Taxonomy of exponential smoothingmethods

4 Exponential smoothing state space models

Forecasting using R Exponential smoothing methods so far 2

Exponential smoothing methods

Simple exponential smoothing: no trend.ses(x)

Holt’s method: linear trend.holt(x)

Exponential trend method.holt(x, exponential=TRUE)

Damped trend method.holt(x, damped=TRUE)

Damped exponential trend method.holt(x, damped=TRUE, exponential=TRUE)

Forecasting using R Exponential smoothing methods so far 3

Exponential smoothing methods

Simple exponential smoothing: no trend.ses(x)

Holt’s method: linear trend.holt(x)

Exponential trend method.holt(x, exponential=TRUE)

Damped trend method.holt(x, damped=TRUE)

Damped exponential trend method.holt(x, damped=TRUE, exponential=TRUE)

Forecasting using R Exponential smoothing methods so far 3

Exponential smoothing methods

Simple exponential smoothing: no trend.ses(x)

Holt’s method: linear trend.holt(x)

Exponential trend method.holt(x, exponential=TRUE)

Damped trend method.holt(x, damped=TRUE)

Damped exponential trend method.holt(x, damped=TRUE, exponential=TRUE)

Forecasting using R Exponential smoothing methods so far 3

Exponential smoothing methods

Simple exponential smoothing: no trend.ses(x)

Holt’s method: linear trend.holt(x)

Exponential trend method.holt(x, exponential=TRUE)

Damped trend method.holt(x, damped=TRUE)

Damped exponential trend method.holt(x, damped=TRUE, exponential=TRUE)

Forecasting using R Exponential smoothing methods so far 3

Exponential smoothing methods

Simple exponential smoothing: no trend.ses(x)

Holt’s method: linear trend.holt(x)

Exponential trend method.holt(x, exponential=TRUE)

Damped trend method.holt(x, damped=TRUE)

Damped exponential trend method.holt(x, damped=TRUE, exponential=TRUE)

Forecasting using R Exponential smoothing methods so far 3

Outline

1 Exponential smoothing methods so far

2 Holt-Winters’ seasonal method

3 Taxonomy of exponential smoothingmethods

4 Exponential smoothing state space models

Forecasting using R Holt-Winters’ seasonal method 4

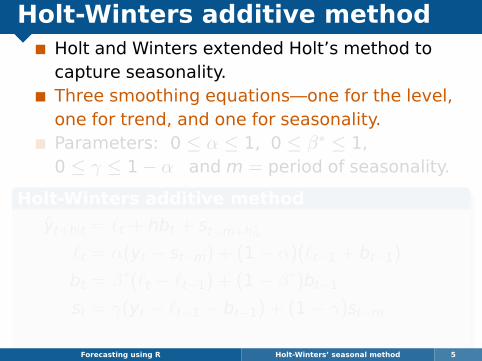

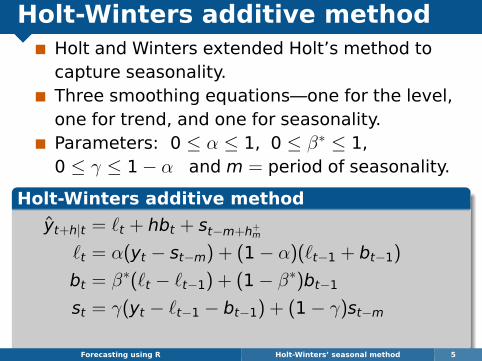

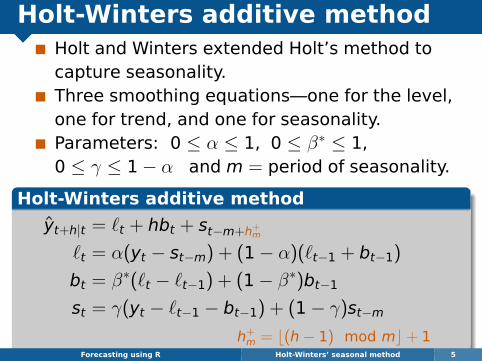

Holt-Winters additive methodHolt and Winters extended Holt’s method tocapture seasonality.Three smoothing equations—one for the level,one for trend, and one for seasonality.Parameters: 0 ≤ α ≤ 1, 0 ≤ β∗ ≤ 1,0 ≤ γ ≤ 1− α and m = period of seasonality.

Holt-Winters additive method

yt+h|t = `t + hbt + st−m+h+m

`t = α(yt − st−m) + (1− α)(`t−1 + bt−1)

bt = β∗(`t − `t−1) + (1− β∗)bt−1

st = γ(yt − `t−1 − bt−1) + (1− γ)st−m

Forecasting using R Holt-Winters’ seasonal method 5

Holt-Winters additive methodHolt and Winters extended Holt’s method tocapture seasonality.Three smoothing equations—one for the level,one for trend, and one for seasonality.Parameters: 0 ≤ α ≤ 1, 0 ≤ β∗ ≤ 1,0 ≤ γ ≤ 1− α and m = period of seasonality.

Holt-Winters additive method

yt+h|t = `t + hbt + st−m+h+m

`t = α(yt − st−m) + (1− α)(`t−1 + bt−1)

bt = β∗(`t − `t−1) + (1− β∗)bt−1

st = γ(yt − `t−1 − bt−1) + (1− γ)st−m

Forecasting using R Holt-Winters’ seasonal method 5

Holt-Winters additive methodHolt and Winters extended Holt’s method tocapture seasonality.Three smoothing equations—one for the level,one for trend, and one for seasonality.Parameters: 0 ≤ α ≤ 1, 0 ≤ β∗ ≤ 1,0 ≤ γ ≤ 1− α and m = period of seasonality.

Holt-Winters additive method

yt+h|t = `t + hbt + st−m+h+m

`t = α(yt − st−m) + (1− α)(`t−1 + bt−1)

bt = β∗(`t − `t−1) + (1− β∗)bt−1

st = γ(yt − `t−1 − bt−1) + (1− γ)st−m

Forecasting using R Holt-Winters’ seasonal method 5

Holt-Winters additive methodHolt and Winters extended Holt’s method tocapture seasonality.Three smoothing equations—one for the level,one for trend, and one for seasonality.Parameters: 0 ≤ α ≤ 1, 0 ≤ β∗ ≤ 1,0 ≤ γ ≤ 1− α and m = period of seasonality.

Holt-Winters additive method

yt+h|t = `t + hbt + st−m+h+m

`t = α(yt − st−m) + (1− α)(`t−1 + bt−1)

bt = β∗(`t − `t−1) + (1− β∗)bt−1

st = γ(yt − `t−1 − bt−1) + (1− γ)st−m

Forecasting using R Holt-Winters’ seasonal method 5

Holt-Winters additive methodHolt and Winters extended Holt’s method tocapture seasonality.Three smoothing equations—one for the level,one for trend, and one for seasonality.Parameters: 0 ≤ α ≤ 1, 0 ≤ β∗ ≤ 1,0 ≤ γ ≤ 1− α and m = period of seasonality.

Holt-Winters additive method

yt+h|t = `t + hbt + st−m+h+m

`t = α(yt − st−m) + (1− α)(`t−1 + bt−1)

bt = β∗(`t − `t−1) + (1− β∗)bt−1

st = γ(yt − `t−1 − bt−1) + (1− γ)st−m

Forecasting using R Holt-Winters’ seasonal method 5

Holt-Winters additive methodHolt and Winters extended Holt’s method tocapture seasonality.Three smoothing equations—one for the level,one for trend, and one for seasonality.Parameters: 0 ≤ α ≤ 1, 0 ≤ β∗ ≤ 1,0 ≤ γ ≤ 1− α and m = period of seasonality.

Holt-Winters additive method

yt+h|t = `t + hbt + st−m+h+m

`t = α(yt − st−m) + (1− α)(`t−1 + bt−1)

bt = β∗(`t − `t−1) + (1− β∗)bt−1

st = γ(yt − `t−1 − bt−1) + (1− γ)st−mh+m = b(h− 1) mod mc+ 1

Forecasting using R Holt-Winters’ seasonal method 5

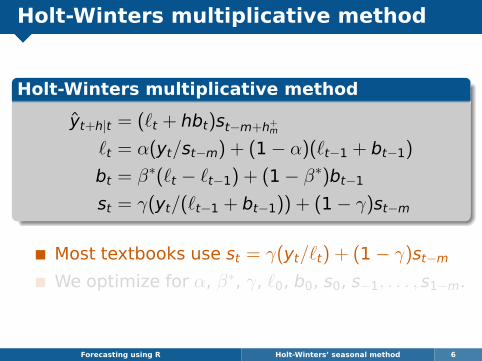

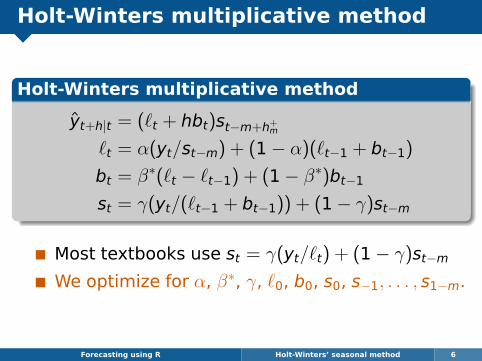

Holt-Winters multiplicative method

Holt-Winters multiplicative method

yt+h|t = (`t + hbt)st−m+h+m

`t = α(yt/st−m) + (1− α)(`t−1 + bt−1)

bt = β∗(`t − `t−1) + (1− β∗)bt−1

st = γ(yt/(`t−1 + bt−1)) + (1− γ)st−m

Most textbooks use st = γ(yt/`t) + (1− γ)st−mWe optimize for α, β∗, γ, `0, b0, s0, s−1, . . . , s1−m.

Forecasting using R Holt-Winters’ seasonal method 6

Holt-Winters multiplicative method

Holt-Winters multiplicative method

yt+h|t = (`t + hbt)st−m+h+m

`t = α(yt/st−m) + (1− α)(`t−1 + bt−1)

bt = β∗(`t − `t−1) + (1− β∗)bt−1

st = γ(yt/(`t−1 + bt−1)) + (1− γ)st−m

Most textbooks use st = γ(yt/`t) + (1− γ)st−mWe optimize for α, β∗, γ, `0, b0, s0, s−1, . . . , s1−m.

Forecasting using R Holt-Winters’ seasonal method 6

Damped Holt-Winters method

Damped Holt-Winters multiplicative method

yt+h|t = [`t + (1 + φ+ φ2 + · · ·+ φh−1)bt]st−m+h+m

`t = α(yt/st−m) + (1− α)(`t−1 + φbt−1)

bt = β∗(`t − `t−1) + (1− β∗)φbt−1

st = γ[yt/(`t−1 + φbt−1)] + (1− γ)st−m

This is often the single most accurateforecasting method for seasonal data.

Forecasting using R Holt-Winters’ seasonal method 7

A confusing array of methods?

All these methods can be confusing!

How to choose between them?

The ETS framework provides an

automatic way of selecting the best

method.

It was developed to solve the problem

of automatically forecasting

pharmaceutical sales across thousands

of products.Forecasting using R Holt-Winters’ seasonal method 8

A confusing array of methods?

All these methods can be confusing!

How to choose between them?

The ETS framework provides an

automatic way of selecting the best

method.

It was developed to solve the problem

of automatically forecasting

pharmaceutical sales across thousands

of products.Forecasting using R Holt-Winters’ seasonal method 8

A confusing array of methods?

All these methods can be confusing!

How to choose between them?

The ETS framework provides an

automatic way of selecting the best

method.

It was developed to solve the problem

of automatically forecasting

pharmaceutical sales across thousands

of products.Forecasting using R Holt-Winters’ seasonal method 8

A confusing array of methods?

All these methods can be confusing!

How to choose between them?

The ETS framework provides an

automatic way of selecting the best

method.

It was developed to solve the problem

of automatically forecasting

pharmaceutical sales across thousands

of products.Forecasting using R Holt-Winters’ seasonal method 8

Outline

1 Exponential smoothing methods so far

2 Holt-Winters’ seasonal method

3 Taxonomy of exponential smoothingmethods

4 Exponential smoothing state space models

Forecasting using R Taxonomy of exponential smoothing methods 9

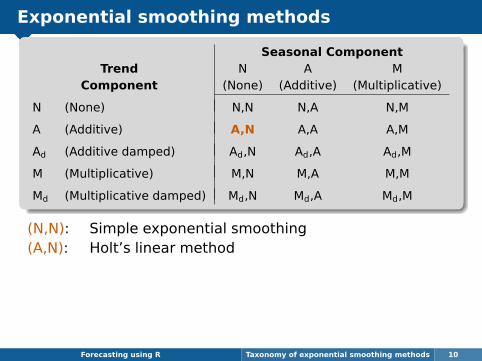

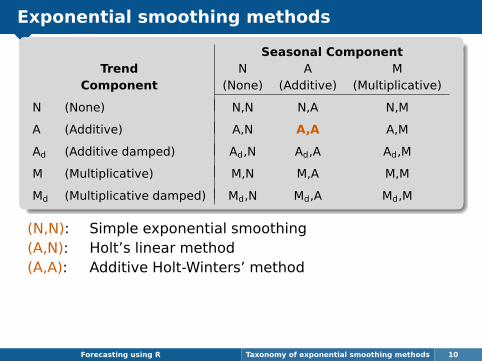

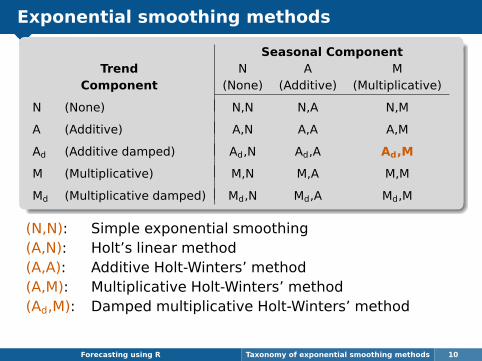

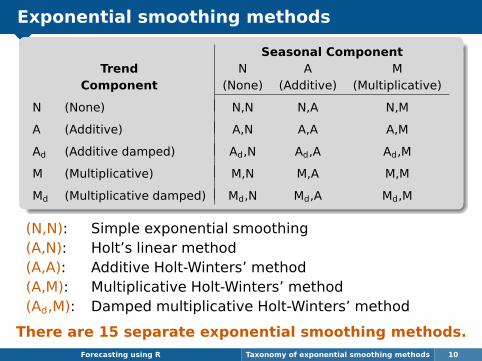

Exponential smoothing methods

Seasonal ComponentTrend N A M

Component (None) (Additive) (Multiplicative)

N (None) N,N N,A N,M

A (Additive) A,N A,A A,M

Ad (Additive damped) Ad,N Ad,A Ad,M

M (Multiplicative) M,N M,A M,M

Md (Multiplicative damped) Md,N Md,A Md,M

Forecasting using R Taxonomy of exponential smoothing methods 10

Exponential smoothing methods

Seasonal ComponentTrend N A M

Component (None) (Additive) (Multiplicative)

N (None) N,N N,A N,M

A (Additive) A,N A,A A,M

Ad (Additive damped) Ad,N Ad,A Ad,M

M (Multiplicative) M,N M,A M,M

Md (Multiplicative damped) Md,N Md,A Md,M

(N,N): Simple exponential smoothing

Forecasting using R Taxonomy of exponential smoothing methods 10

Exponential smoothing methods

Seasonal ComponentTrend N A M

Component (None) (Additive) (Multiplicative)

N (None) N,N N,A N,M

A (Additive) A,N A,A A,M

Ad (Additive damped) Ad,N Ad,A Ad,M

M (Multiplicative) M,N M,A M,M

Md (Multiplicative damped) Md,N Md,A Md,M

(N,N): Simple exponential smoothing(A,N): Holt’s linear method

Forecasting using R Taxonomy of exponential smoothing methods 10

Exponential smoothing methods

Seasonal ComponentTrend N A M

Component (None) (Additive) (Multiplicative)

N (None) N,N N,A N,M

A (Additive) A,N A,A A,M

Ad (Additive damped) Ad,N Ad,A Ad,M

M (Multiplicative) M,N M,A M,M

Md (Multiplicative damped) Md,N Md,A Md,M

(N,N): Simple exponential smoothing(A,N): Holt’s linear method(A,A): Additive Holt-Winters’ method

Forecasting using R Taxonomy of exponential smoothing methods 10

Exponential smoothing methods

Seasonal ComponentTrend N A M

Component (None) (Additive) (Multiplicative)

N (None) N,N N,A N,M

A (Additive) A,N A,A A,M

Ad (Additive damped) Ad,N Ad,A Ad,M

M (Multiplicative) M,N M,A M,M

Md (Multiplicative damped) Md,N Md,A Md,M

(N,N): Simple exponential smoothing(A,N): Holt’s linear method(A,A): Additive Holt-Winters’ method(A,M): Multiplicative Holt-Winters’ method

Forecasting using R Taxonomy of exponential smoothing methods 10

Exponential smoothing methods

Seasonal ComponentTrend N A M

Component (None) (Additive) (Multiplicative)

N (None) N,N N,A N,M

A (Additive) A,N A,A A,M

Ad (Additive damped) Ad,N Ad,A Ad,M

M (Multiplicative) M,N M,A M,M

Md (Multiplicative damped) Md,N Md,A Md,M

(N,N): Simple exponential smoothing(A,N): Holt’s linear method(A,A): Additive Holt-Winters’ method(A,M): Multiplicative Holt-Winters’ method(Ad,M): Damped multiplicative Holt-Winters’ method

Forecasting using R Taxonomy of exponential smoothing methods 10

Exponential smoothing methods

Seasonal ComponentTrend N A M

Component (None) (Additive) (Multiplicative)

N (None) N,N N,A N,M

A (Additive) A,N A,A A,M

Ad (Additive damped) Ad,N Ad,A Ad,M

M (Multiplicative) M,N M,A M,M

Md (Multiplicative damped) Md,N Md,A Md,M

(N,N): Simple exponential smoothing(A,N): Holt’s linear method(A,A): Additive Holt-Winters’ method(A,M): Multiplicative Holt-Winters’ method(Ad,M): Damped multiplicative Holt-Winters’ method

There are 15 separate exponential smoothing methods.Forecasting using R Taxonomy of exponential smoothing methods 10

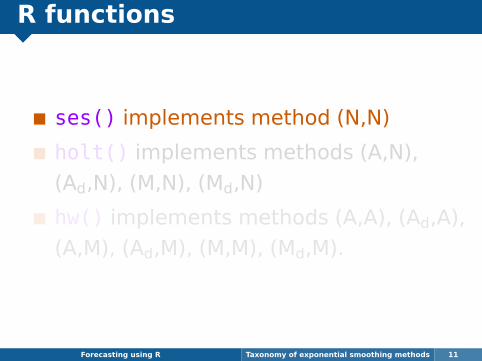

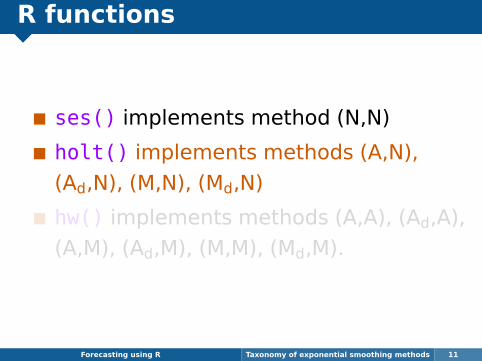

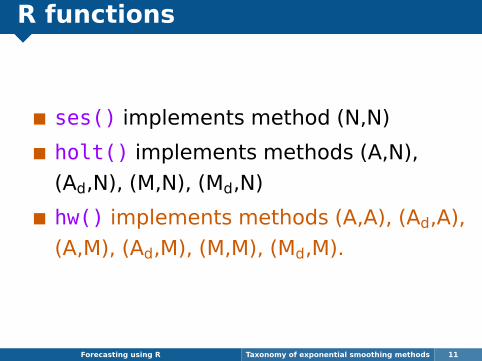

R functions

ses() implements method (N,N)

holt() implements methods (A,N),

(Ad,N), (M,N), (Md,N)

hw() implements methods (A,A), (Ad,A),

(A,M), (Ad,M), (M,M), (Md,M).

Forecasting using R Taxonomy of exponential smoothing methods 11

R functions

ses() implements method (N,N)

holt() implements methods (A,N),

(Ad,N), (M,N), (Md,N)

hw() implements methods (A,A), (Ad,A),

(A,M), (Ad,M), (M,M), (Md,M).

Forecasting using R Taxonomy of exponential smoothing methods 11

R functions

ses() implements method (N,N)

holt() implements methods (A,N),

(Ad,N), (M,N), (Md,N)

hw() implements methods (A,A), (Ad,A),

(A,M), (Ad,M), (M,M), (Md,M).

Forecasting using R Taxonomy of exponential smoothing methods 11

Outline

1 Exponential smoothing methods so far

2 Holt-Winters’ seasonal method

3 Taxonomy of exponential smoothingmethods

4 Exponential smoothing state space models

Forecasting using R Exponential smoothing state space models 12

Exponential smoothing

Until recently, there has been no stochasticmodelling framework incorporating likelihoodcalculation, prediction intervals, etc.

Ord, Koehler & Snyder (JASA, 1997) andHyndman, Koehler, Snyder and Grose (IJF,2002) showed that all ES methods (includingnon-linear methods) are optimal forecasts frominnovations state space models.

Hyndman et al. (2008) provides acomprehensive and up-to-date survey of area.

The forecast package implements the statespace framework.

Forecasting using R Exponential smoothing state space models 13

Exponential smoothing

Until recently, there has been no stochasticmodelling framework incorporating likelihoodcalculation, prediction intervals, etc.

Ord, Koehler & Snyder (JASA, 1997) andHyndman, Koehler, Snyder and Grose (IJF,2002) showed that all ES methods (includingnon-linear methods) are optimal forecasts frominnovations state space models.

Hyndman et al. (2008) provides acomprehensive and up-to-date survey of area.

The forecast package implements the statespace framework.

Forecasting using R Exponential smoothing state space models 13

Exponential smoothing

Until recently, there has been no stochasticmodelling framework incorporating likelihoodcalculation, prediction intervals, etc.

Ord, Koehler & Snyder (JASA, 1997) andHyndman, Koehler, Snyder and Grose (IJF,2002) showed that all ES methods (includingnon-linear methods) are optimal forecasts frominnovations state space models.

Hyndman et al. (2008) provides acomprehensive and up-to-date survey of area.

The forecast package implements the statespace framework.

Forecasting using R Exponential smoothing state space models 13

Exponential smoothing

Until recently, there has been no stochasticmodelling framework incorporating likelihoodcalculation, prediction intervals, etc.

Ord, Koehler & Snyder (JASA, 1997) andHyndman, Koehler, Snyder and Grose (IJF,2002) showed that all ES methods (includingnon-linear methods) are optimal forecasts frominnovations state space models.

Hyndman et al. (2008) provides acomprehensive and up-to-date survey of area.

The forecast package implements the statespace framework.

Forecasting using R Exponential smoothing state space models 13

Exponential smoothing

Until recently, there has been no stochasticmodelling framework incorporating likelihoodcalculation, prediction intervals, etc.

Ord, Koehler & Snyder (JASA, 1997) andHyndman, Koehler, Snyder and Grose (IJF,2002) showed that all ES methods (includingnon-linear methods) are optimal forecasts frominnovations state space models.

Hyndman et al. (2008) provides acomprehensive and up-to-date survey of area.

The forecast package implements the statespace framework.

Forecasting using R Exponential smoothing state space models 13

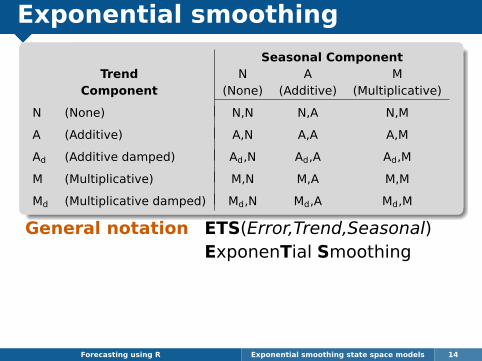

Exponential smoothing

Seasonal ComponentTrend N A M

Component (None) (Additive) (Multiplicative)

N (None) N,N N,A N,M

A (Additive) A,N A,A A,M

Ad (Additive damped) Ad,N Ad,A Ad,M

M (Multiplicative) M,N M,A M,M

Md (Multiplicative damped) Md,N Md,A Md,M

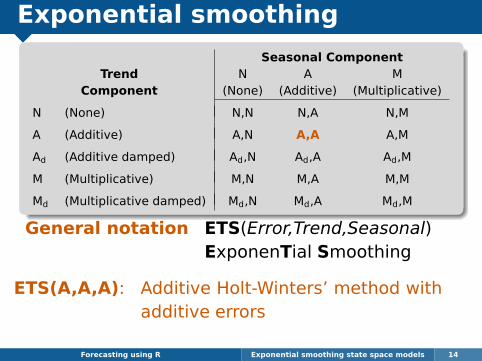

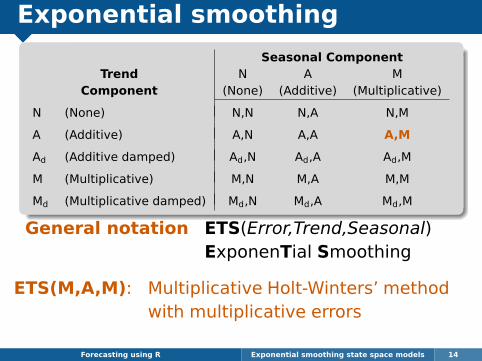

General notation ETS(Error,Trend,Seasonal)

Forecasting using R Exponential smoothing state space models 14

Exponential smoothing

Seasonal ComponentTrend N A M

Component (None) (Additive) (Multiplicative)

N (None) N,N N,A N,M

A (Additive) A,N A,A A,M

Ad (Additive damped) Ad,N Ad,A Ad,M

M (Multiplicative) M,N M,A M,M

Md (Multiplicative damped) Md,N Md,A Md,M

General notation ETS(Error,Trend,Seasonal)

Forecasting using R Exponential smoothing state space models 14

Exponential smoothing

Seasonal ComponentTrend N A M

Component (None) (Additive) (Multiplicative)

N (None) N,N N,A N,M

A (Additive) A,N A,A A,M

Ad (Additive damped) Ad,N Ad,A Ad,M

M (Multiplicative) M,N M,A M,M

Md (Multiplicative damped) Md,N Md,A Md,M

General notation ETS(Error,Trend,Seasonal)ExponenTial Smoothing

Forecasting using R Exponential smoothing state space models 14

Exponential smoothing

Seasonal ComponentTrend N A M

Component (None) (Additive) (Multiplicative)

N (None) N,N N,A N,M

A (Additive) A,N A,A A,M

Ad (Additive damped) Ad,N Ad,A Ad,M

M (Multiplicative) M,N M,A M,M

Md (Multiplicative damped) Md,N Md,A Md,M

General notation ETS(Error,Trend,Seasonal)ExponenTial Smoothing

ETS(A,N,N): Simple exponential smoothing withadditive errors

Forecasting using R Exponential smoothing state space models 14

Exponential smoothing

Seasonal ComponentTrend N A M

Component (None) (Additive) (Multiplicative)

N (None) N,N N,A N,M

A (Additive) A,N A,A A,M

Ad (Additive damped) Ad,N Ad,A Ad,M

M (Multiplicative) M,N M,A M,M

Md (Multiplicative damped) Md,N Md,A Md,M

General notation ETS(Error,Trend,Seasonal)ExponenTial Smoothing

ETS(A,A,N): Holt’s linear method with additiveerrors

Forecasting using R Exponential smoothing state space models 14

Exponential smoothing

Seasonal ComponentTrend N A M

Component (None) (Additive) (Multiplicative)

N (None) N,N N,A N,M

A (Additive) A,N A,A A,M

Ad (Additive damped) Ad,N Ad,A Ad,M

M (Multiplicative) M,N M,A M,M

Md (Multiplicative damped) Md,N Md,A Md,M

General notation ETS(Error,Trend,Seasonal)ExponenTial Smoothing

ETS(A,A,A): Additive Holt-Winters’ method withadditive errors

Forecasting using R Exponential smoothing state space models 14

Exponential smoothing

Seasonal ComponentTrend N A M

Component (None) (Additive) (Multiplicative)

N (None) N,N N,A N,M

A (Additive) A,N A,A A,M

Ad (Additive damped) Ad,N Ad,A Ad,M

M (Multiplicative) M,N M,A M,M

Md (Multiplicative damped) Md,N Md,A Md,M

General notation ETS(Error,Trend,Seasonal)ExponenTial Smoothing

ETS(M,A,M): Multiplicative Holt-Winters’ methodwith multiplicative errors

Forecasting using R Exponential smoothing state space models 14

Exponential smoothing

Seasonal ComponentTrend N A M

Component (None) (Additive) (Multiplicative)

N (None) N,N N,A N,M

A (Additive) A,N A,A A,M

Ad (Additive damped) Ad,N Ad,A Ad,M

M (Multiplicative) M,N M,A M,M

Md (Multiplicative damped) Md,N Md,A Md,M

General notation ETS(Error,Trend,Seasonal)ExponenTial Smoothing

ETS(A,Ad,N): Damped trend method with addi-tive errors

Forecasting using R Exponential smoothing state space models 14

Exponential smoothing

Seasonal ComponentTrend N A M

Component (None) (Additive) (Multiplicative)

N (None) N,N N,A N,M

A (Additive) A,N A,A A,M

Ad (Additive damped) Ad,N Ad,A Ad,M

M (Multiplicative) M,N M,A M,M

Md (Multiplicative damped) Md,N Md,A Md,M

General notation ETS(Error,Trend,Seasonal)ExponenTial Smoothing

There are 30 separate models in the ETSframework

Forecasting using R Exponential smoothing state space models 14

Innovations state space models

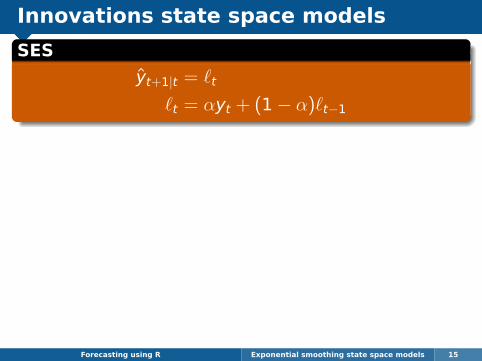

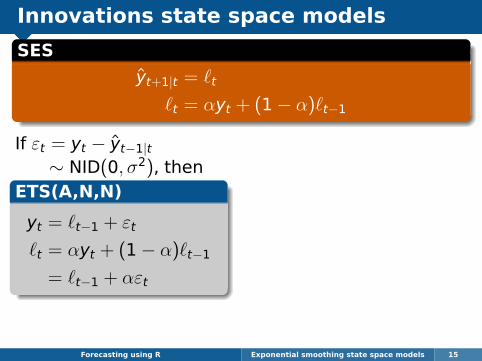

SES

yt+1|t = `t

`t = αyt + (1− α)`t−1

Forecasting using R Exponential smoothing state space models 15

Innovations state space models

SES

yt+1|t = `t

`t = αyt + (1− α)`t−1

Forecasting using R Exponential smoothing state space models 15

If εt = yt − yt−1|t∼ NID(0, σ2), then

ETS(A,N,N)

yt = `t−1 + εt

`t = αyt + (1− α)`t−1

= `t−1 + αεt

Innovations state space models

SES

yt+1|t = `t

`t = αyt + (1− α)`t−1

Forecasting using R Exponential smoothing state space models 15

If εt = yt − yt−1|t∼ NID(0, σ2), then

ETS(A,N,N)

yt = `t−1 + εt

`t = αyt + (1− α)`t−1

= `t−1 + αεt

If εt = (yt − yt−1|t)/yt−1|t∼ NID(0, σ2), then

ETS(M,N,N)

yt = `t−1(1 + εt)

`t = αyt + (1− α)`t−1

= `t−1(1 + αεt)

Innovations state space models

SES

yt+1|t = `t

`t = αyt + (1− α)`t−1

All exponential smoothing methods can be writtenusing analogous state space equations.

Forecasting using R Exponential smoothing state space models 15

If εt = yt − yt−1|t∼ NID(0, σ2), then

ETS(A,N,N)

yt = `t−1 + εt

`t = αyt + (1− α)`t−1

= `t−1 + αεt

If εt = (yt − yt−1|t)/yt−1|t∼ NID(0, σ2), then

ETS(M,N,N)

yt = `t−1(1 + εt)

`t = αyt + (1− α)`t−1

= `t−1(1 + αεt)

Innovations state space models

Example: Holt-Winters’ multiplicativeseasonal method

ETS(M,A,M)

yt = (`t−1 + bt−1)st−m(1 + εt)

`t = (`t−1 + bt−1)(1 + αεt)

bt = bt−1 + β(`t−1 + bt−1)εt

st = st−m(1 + γεt)

where β = αβ∗.

Forecasting using R Exponential smoothing state space models 16

Innovations state space models

All the methods can be written in this statespace form.

Prediction intervals can be obtained bysimulating many future sample paths.

For many models, the prediction intervals canbe obtained analytically as well.

Additive and multiplicative versions give thesame point forecasts.

Estimation is handled via maximizing thelikelihood of the data given the model.

Forecasting using R Exponential smoothing state space models 17

Innovations state space models

All the methods can be written in this statespace form.

Prediction intervals can be obtained bysimulating many future sample paths.

For many models, the prediction intervals canbe obtained analytically as well.

Additive and multiplicative versions give thesame point forecasts.

Estimation is handled via maximizing thelikelihood of the data given the model.

Forecasting using R Exponential smoothing state space models 17

Innovations state space models

All the methods can be written in this statespace form.

Prediction intervals can be obtained bysimulating many future sample paths.

For many models, the prediction intervals canbe obtained analytically as well.

Additive and multiplicative versions give thesame point forecasts.

Estimation is handled via maximizing thelikelihood of the data given the model.

Forecasting using R Exponential smoothing state space models 17

Innovations state space models

All the methods can be written in this statespace form.

Prediction intervals can be obtained bysimulating many future sample paths.

For many models, the prediction intervals canbe obtained analytically as well.

Additive and multiplicative versions give thesame point forecasts.

Estimation is handled via maximizing thelikelihood of the data given the model.

Forecasting using R Exponential smoothing state space models 17

Innovations state space models

All the methods can be written in this statespace form.

Prediction intervals can be obtained bysimulating many future sample paths.

For many models, the prediction intervals canbe obtained analytically as well.

Additive and multiplicative versions give thesame point forecasts.

Estimation is handled via maximizing thelikelihood of the data given the model.

Forecasting using R Exponential smoothing state space models 17

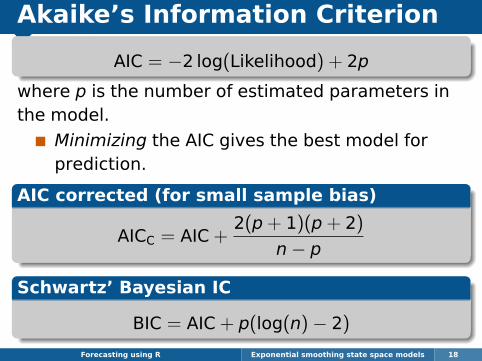

Akaike’s Information Criterion

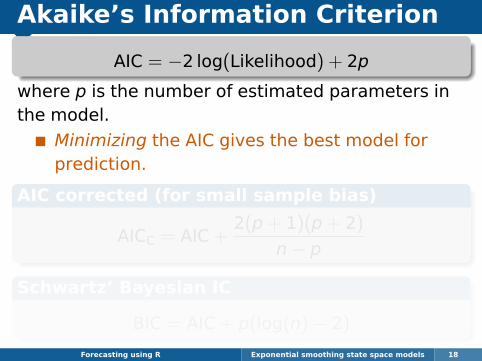

AIC = −2 log(Likelihood) + 2p

where p is the number of estimated parameters inthe model.

Minimizing the AIC gives the best model forprediction.

AIC corrected (for small sample bias)

AICC = AIC +2(p+ 1)(p+ 2)

n− p

Schwartz’ Bayesian IC

BIC = AIC + p(log(n)− 2)

Forecasting using R Exponential smoothing state space models 18

Akaike’s Information Criterion

AIC = −2 log(Likelihood) + 2p

where p is the number of estimated parameters inthe model.

Minimizing the AIC gives the best model forprediction.

AIC corrected (for small sample bias)

AICC = AIC +2(p+ 1)(p+ 2)

n− p

Schwartz’ Bayesian IC

BIC = AIC + p(log(n)− 2)

Forecasting using R Exponential smoothing state space models 18

Akaike’s Information Criterion

AIC = −2 log(Likelihood) + 2p

where p is the number of estimated parameters inthe model.

Minimizing the AIC gives the best model forprediction.

AIC corrected (for small sample bias)

AICC = AIC +2(p+ 1)(p+ 2)

n− p

Schwartz’ Bayesian IC

BIC = AIC + p(log(n)− 2)

Forecasting using R Exponential smoothing state space models 18

Akaike’s Information Criterion

AIC = −2 log(Likelihood) + 2p

where p is the number of estimated parameters inthe model.

Minimizing the AIC gives the best model forprediction.

AIC corrected (for small sample bias)

AICC = AIC +2(p+ 1)(p+ 2)

n− p

Schwartz’ Bayesian IC

BIC = AIC + p(log(n)− 2)

Forecasting using R Exponential smoothing state space models 18

Akaike’s Information Criterion

AIC = −2 log(Likelihood) + 2p

where p is the number of estimated parameters inthe model.

Minimizing the AIC gives the best model forprediction.

AIC corrected (for small sample bias)

AICC = AIC +2(p+ 1)(p+ 2)

n− p

Schwartz’ Bayesian IC

BIC = AIC + p(log(n)− 2)

Forecasting using R Exponential smoothing state space models 18

Akaike’s Information Criterion

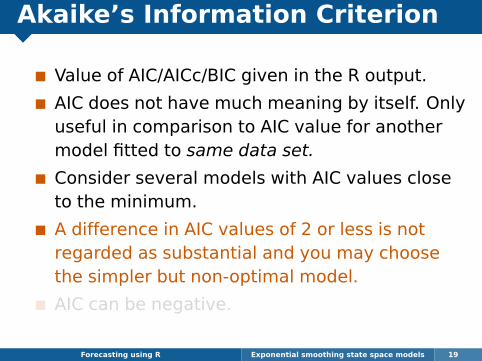

Value of AIC/AICc/BIC given in the R output.

AIC does not have much meaning by itself. Onlyuseful in comparison to AIC value for anothermodel fitted to same data set.

Consider several models with AIC values closeto the minimum.

A difference in AIC values of 2 or less is notregarded as substantial and you may choosethe simpler but non-optimal model.

AIC can be negative.

Forecasting using R Exponential smoothing state space models 19

Akaike’s Information Criterion

Value of AIC/AICc/BIC given in the R output.

AIC does not have much meaning by itself. Onlyuseful in comparison to AIC value for anothermodel fitted to same data set.

Consider several models with AIC values closeto the minimum.

A difference in AIC values of 2 or less is notregarded as substantial and you may choosethe simpler but non-optimal model.

AIC can be negative.

Forecasting using R Exponential smoothing state space models 19

Akaike’s Information Criterion

Value of AIC/AICc/BIC given in the R output.

AIC does not have much meaning by itself. Onlyuseful in comparison to AIC value for anothermodel fitted to same data set.

Consider several models with AIC values closeto the minimum.

A difference in AIC values of 2 or less is notregarded as substantial and you may choosethe simpler but non-optimal model.

AIC can be negative.

Forecasting using R Exponential smoothing state space models 19

Akaike’s Information Criterion

Value of AIC/AICc/BIC given in the R output.

AIC does not have much meaning by itself. Onlyuseful in comparison to AIC value for anothermodel fitted to same data set.

Consider several models with AIC values closeto the minimum.

A difference in AIC values of 2 or less is notregarded as substantial and you may choosethe simpler but non-optimal model.

AIC can be negative.

Forecasting using R Exponential smoothing state space models 19

Akaike’s Information Criterion

Value of AIC/AICc/BIC given in the R output.

AIC does not have much meaning by itself. Onlyuseful in comparison to AIC value for anothermodel fitted to same data set.

Consider several models with AIC values closeto the minimum.

A difference in AIC values of 2 or less is notregarded as substantial and you may choosethe simpler but non-optimal model.

AIC can be negative.

Forecasting using R Exponential smoothing state space models 19

Exponential smoothing

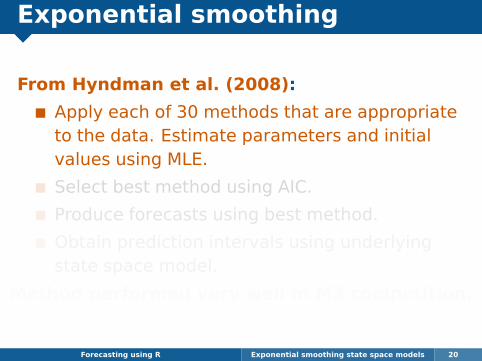

From Hyndman et al. (2008):

Apply each of 30 methods that are appropriateto the data. Estimate parameters and initialvalues using MLE.

Select best method using AIC.

Produce forecasts using best method.

Obtain prediction intervals using underlyingstate space model.

Method performed very well in M3 competition.

Forecasting using R Exponential smoothing state space models 20

Exponential smoothing

From Hyndman et al. (2008):

Apply each of 30 methods that are appropriateto the data. Estimate parameters and initialvalues using MLE.

Select best method using AIC.

Produce forecasts using best method.

Obtain prediction intervals using underlyingstate space model.

Method performed very well in M3 competition.

Forecasting using R Exponential smoothing state space models 20

Exponential smoothing

From Hyndman et al. (2008):

Apply each of 30 methods that are appropriateto the data. Estimate parameters and initialvalues using MLE.

Select best method using AIC.

Produce forecasts using best method.

Obtain prediction intervals using underlyingstate space model.

Method performed very well in M3 competition.

Forecasting using R Exponential smoothing state space models 20

Exponential smoothing

From Hyndman et al. (2008):

Apply each of 30 methods that are appropriateto the data. Estimate parameters and initialvalues using MLE.

Select best method using AIC.

Produce forecasts using best method.

Obtain prediction intervals using underlyingstate space model.

Method performed very well in M3 competition.

Forecasting using R Exponential smoothing state space models 20

Exponential smoothing

From Hyndman et al. (2008):

Apply each of 30 methods that are appropriateto the data. Estimate parameters and initialvalues using MLE.

Select best method using AIC.

Produce forecasts using best method.

Obtain prediction intervals using underlyingstate space model.

Method performed very well in M3 competition.

Forecasting using R Exponential smoothing state space models 20

Exponential smoothing

From Hyndman et al. (2008):

Apply each of 30 methods that are appropriateto the data. Estimate parameters and initialvalues using MLE.

Select best method using AIC.

Produce forecasts using best method.

Obtain prediction intervals using underlyingstate space model.

Method performed very well in M3 competition.

Forecasting using R Exponential smoothing state space models 20

Exponential smoothing

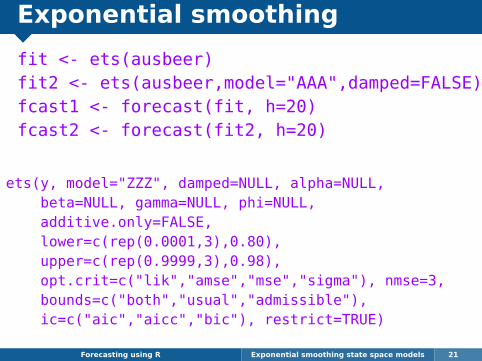

fit <- ets(ausbeer)fit2 <- ets(ausbeer,model="AAA",damped=FALSE)fcast1 <- forecast(fit, h=20)fcast2 <- forecast(fit2, h=20)

ets(y, model="ZZZ", damped=NULL, alpha=NULL,beta=NULL, gamma=NULL, phi=NULL,additive.only=FALSE,lower=c(rep(0.0001,3),0.80),upper=c(rep(0.9999,3),0.98),opt.crit=c("lik","amse","mse","sigma"), nmse=3,bounds=c("both","usual","admissible"),ic=c("aic","aicc","bic"), restrict=TRUE)

Forecasting using R Exponential smoothing state space models 21

Exponential smoothing

fit <- ets(ausbeer)fit2 <- ets(ausbeer,model="AAA",damped=FALSE)fcast1 <- forecast(fit, h=20)fcast2 <- forecast(fit2, h=20)

ets(y, model="ZZZ", damped=NULL, alpha=NULL,beta=NULL, gamma=NULL, phi=NULL,additive.only=FALSE,lower=c(rep(0.0001,3),0.80),upper=c(rep(0.9999,3),0.98),opt.crit=c("lik","amse","mse","sigma"), nmse=3,bounds=c("both","usual","admissible"),ic=c("aic","aicc","bic"), restrict=TRUE)

Forecasting using R Exponential smoothing state space models 21

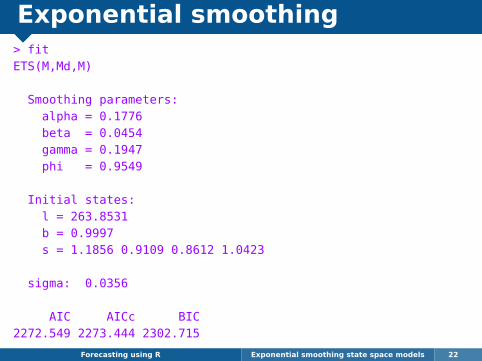

Exponential smoothing> fitETS(M,Md,M)

Smoothing parameters:alpha = 0.1776beta = 0.0454gamma = 0.1947phi = 0.9549

Initial states:l = 263.8531b = 0.9997s = 1.1856 0.9109 0.8612 1.0423

sigma: 0.0356

AIC AICc BIC2272.549 2273.444 2302.715

Forecasting using R Exponential smoothing state space models 22

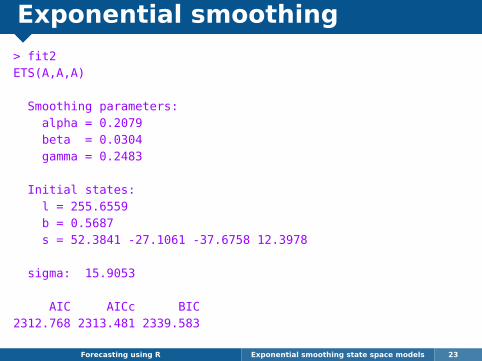

Exponential smoothing

> fit2ETS(A,A,A)

Smoothing parameters:alpha = 0.2079beta = 0.0304gamma = 0.2483

Initial states:l = 255.6559b = 0.5687s = 52.3841 -27.1061 -37.6758 12.3978

sigma: 15.9053

AIC AICc BIC2312.768 2313.481 2339.583

Forecasting using R Exponential smoothing state space models 23

Exponential smoothing

ets() function

Automatically chooses a model by default usingthe AIC, AICc or BIC.

Can handle any combination of trend,seasonality and damping

Produces prediction intervals for every model

Ensures the parameters are admissible(equivalent to invertible)

Produces an object of class ets.

Forecasting using R Exponential smoothing state space models 24

Exponential smoothing

ets() function

Automatically chooses a model by default usingthe AIC, AICc or BIC.

Can handle any combination of trend,seasonality and damping

Produces prediction intervals for every model

Ensures the parameters are admissible(equivalent to invertible)

Produces an object of class ets.

Forecasting using R Exponential smoothing state space models 24

Exponential smoothing

ets() function

Automatically chooses a model by default usingthe AIC, AICc or BIC.

Can handle any combination of trend,seasonality and damping

Produces prediction intervals for every model

Ensures the parameters are admissible(equivalent to invertible)

Produces an object of class ets.

Forecasting using R Exponential smoothing state space models 24

Exponential smoothing

ets() function

Automatically chooses a model by default usingthe AIC, AICc or BIC.

Can handle any combination of trend,seasonality and damping

Produces prediction intervals for every model

Ensures the parameters are admissible(equivalent to invertible)

Produces an object of class ets.

Forecasting using R Exponential smoothing state space models 24

Exponential smoothing

ets() function

Automatically chooses a model by default usingthe AIC, AICc or BIC.

Can handle any combination of trend,seasonality and damping

Produces prediction intervals for every model

Ensures the parameters are admissible(equivalent to invertible)

Produces an object of class ets.

Forecasting using R Exponential smoothing state space models 24

Exponential smoothing

ets objects

Methods: coef(), plot(), summary(),

residuals(), fitted(), simulate()

and forecast()

plot() function shows time plots of the

original time series along with the

extracted components (level, growth

and seasonal).

Forecasting using R Exponential smoothing state space models 25

Exponential smoothing

ets objects

Methods: coef(), plot(), summary(),

residuals(), fitted(), simulate()

and forecast()

plot() function shows time plots of the

original time series along with the

extracted components (level, growth

and seasonal).

Forecasting using R Exponential smoothing state space models 25

Exponential smoothing

Forecasting using R Exponential smoothing state space models 26

200

400

600

obse

rved

250

350

450

leve

l

0.99

01.

005

slop

e

0.9

1.1

1960 1970 1980 1990 2000 2010

seas

on

Time

Decomposition by ETS(M,Md,M) methodplot(fit)

Goodness-of-fit

> accuracy(fit)ME RMSE MAE MPE MAPE MASE

0.17847 15.48781 11.77800 0.07204 2.81921 0.20705

> accuracy(fit2)ME RMSE MAE MPE MAPE MASE

-0.11711 15.90526 12.18930 -0.03765 2.91255 0.21428

Forecasting using R Exponential smoothing state space models 27

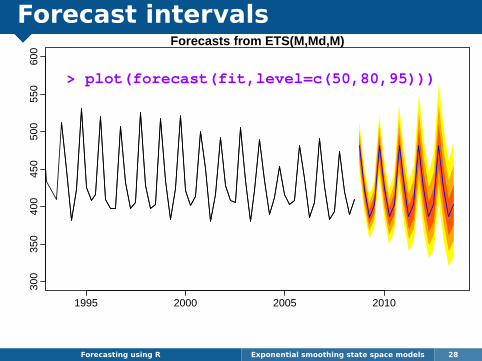

Forecast intervals

Forecasting using R Exponential smoothing state space models 28

Forecasts from ETS(M,Md,M)

1995 2000 2005 2010

300

350

400

450

500

550

600

> plot(forecast(fit,level=c(50,80,95)))

Forecast intervals

Forecasting using R Exponential smoothing state space models 28

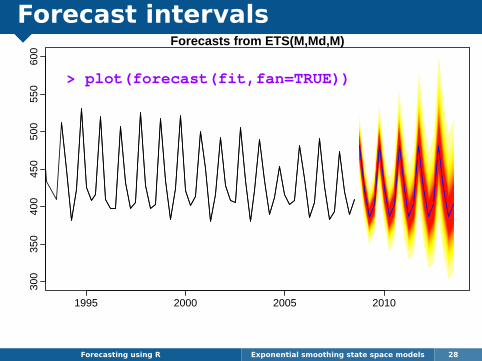

Forecasts from ETS(M,Md,M)

1995 2000 2005 2010

300

350

400

450

500

550

600

> plot(forecast(fit,fan=TRUE))

Exponential smoothing

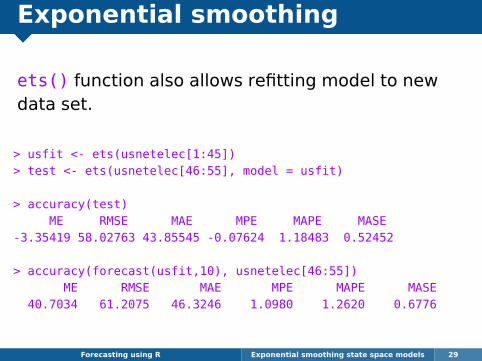

ets() function also allows refitting model to newdata set.

> usfit <- ets(usnetelec[1:45])> test <- ets(usnetelec[46:55], model = usfit)

> accuracy(test)ME RMSE MAE MPE MAPE MASE

-3.35419 58.02763 43.85545 -0.07624 1.18483 0.52452

> accuracy(forecast(usfit,10), usnetelec[46:55])ME RMSE MAE MPE MAPE MASE

40.7034 61.2075 46.3246 1.0980 1.2620 0.6776

Forecasting using R Exponential smoothing state space models 29

Unstable models

ETS(M,M,A)

ETS(M,Md,A)

ETS(A,N,M)

ETS(A,A,M)

ETS(A,Ad,M)

ETS(A,M,N)

ETS(A,M,A)

ETS(A,M,M)

ETS(A,Md,N)

ETS(A,Md,A)

ETS(A,Md,M)Forecasting using R Exponential smoothing state space models 30

Unstable models

ETS(M,M,A)

ETS(M,Md,A)

ETS(A,N,M)

ETS(A,A,M)

ETS(A,Ad,M)

ETS(A,M,N)

ETS(A,M,A)

ETS(A,M,M)

ETS(A,Md,N)

ETS(A,Md,A)

ETS(A,Md,M)Forecasting using R Exponential smoothing state space models 30

In practice, the modelswork fine for short- tomedium-term forecastsprovided the data arestrictly positive.

Forecastability conditions

ets(y, model="ZZZ", damped=NULL, alpha=NULL,beta=NULL, gamma=NULL, phi=NULL,additive.only=FALSE,lower=c(rep(0.0001,3),0.80),upper=c(rep(0.9999,3),0.98),opt.crit=c("lik","amse","mse","sigma"),nmse=3,bounds=c("both","usual","admissible"),ic=c("aic","aicc","bic"), restrict=TRUE)

Forecasting using R Exponential smoothing state space models 31

The magic forecast() function

forecast returns forecasts when applied to anets object (or the output from many other timeseries models).

If you use forecast directly on data, it willselect an ETS model automatically and thenreturn forecasts.

Forecasting using R Exponential smoothing state space models 32

The magic forecast() function

forecast returns forecasts when applied to anets object (or the output from many other timeseries models).

If you use forecast directly on data, it willselect an ETS model automatically and thenreturn forecasts.

Forecasting using R Exponential smoothing state space models 32