2014 kpmg global energy conference recap - il sole 24...

TRANSCRIPT

Day One

1 | © KPMG

2014 KPMG Global Energy Conference Recap

May 21–22, 2014

3. Women in Energy Breakfast: Women on Energy Boards – How to Develop

and Position Yourself for Success

5. Day One Opening Remarks: From John Kunasek, U.S. Sector

Leader for Energy & Natural Resources, and Regina Mayor,

U.S. Energy & Natural Resources Advisory Leader

6. General Session I: How New Oil and Gas Supply Is Changing Energy Policy

8. I-A Concurrent Session: Stemming the Retiring Workforce Brain Drain

10. I-B Concurrent Session: Disruptive Technologies Utilities Can’t Ignore

12. I-C Concurrent Session: BEPS: The Global Legislative Response to

Tax Minimization

14. Keynote Address: Remarks by Condoleezza Rice,

United States Secretary of State (2005–2009)

16. II-A Concurrent Session: Data & Analytics: The “Smart” Way to Enterprise

Asset Management

18. II-B Concurrent Session: New Utility Business Models for the 21st Century

20. II-C Concurrent Session: Cyber Security Evolution: From the Data Center

to the Boardroom

22. General Session II: Daniel Burrus, Founder and CEO, Burrus Research Associates

24. Day Two Opening Remarks: From John Kunasek, U.S. Sector

Leader for Energy & Natural Resources, and Regina Mayor,

U.S. Energy & Natural Resources Advisory Leader

25. Breakfast Panel: Evolving Opportunities and Challenges in Mexico and Sub-Saharan Africa

27. General Session III: The Development and Future of the U.S. Natural Gas Industry

29. III-A Concurrent Session: Information Strategies for Upstream Effectiveness

31. III-B Concurrent Session: Regulatory Trends That Are Changing the Power Industry

33. III-C Concurrent Session: The Developing Global LNG Market

35. IV-A Concurrent Session: Good, Bad, Ugly, and Good Again — JVs in the Energy Industry

37. IV-B Concurrent Session: Meeting the Energy Needs of the New Urban Society

39. IV-C Concurrent Session: Accounting and Reporting Update

41. Keynote Address: Why Not Your Best? NFL Legend Terry Bradshaw, Cohost and Analyst, FOX NFL Sunday

Contents

© KPMG | 2

Day One

3 | © KPMG

Women in Energy Breakfast Women on Energy Boards How to Develop and Posi-tion Yourself for Success

As appropriate for a session on leadership, the first event of the 2014 Global Energy Conference was an early morning breakfast for women on their way up in the energy industry. Regina Mayor, national Advisory industry leader for Energy & Natural Resources, KPMG LLP (U.S.), moderated a candid and wide-ranging discussion about board-level recruiting and how women can develop and position themselves for board membership.

Susan M. Cunningham, senior vice president of Gulf of Mexico, Africa, Frontier Ventures and Business Innovation, Noble Energy, addressed the question of how women should start preparing for possible board membership

Women in Energy Breakfast:

Women on Energy Boards How to Develop and Position Yourself for Success

Day One

© KPMG | 4

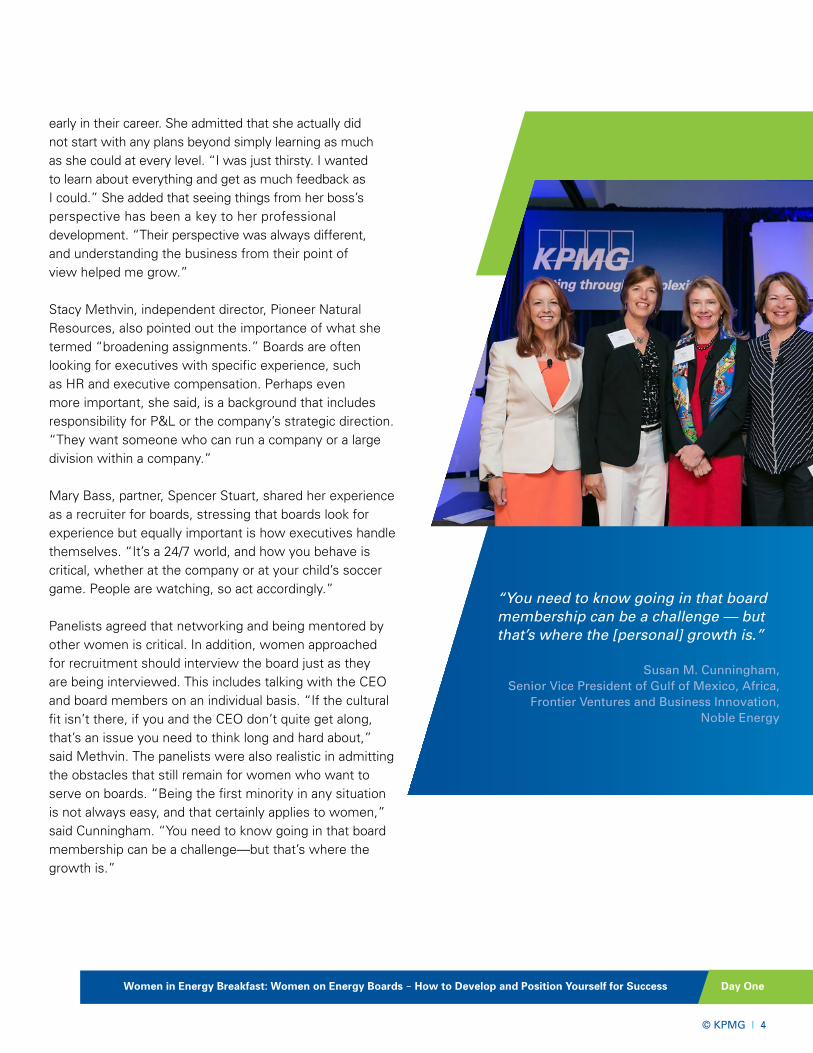

early in their career. She admitted that she actually did not start with any plans beyond simply learning as much as she could at every level. “I was just thirsty. I wanted to learn about everything and get as much feedback as I could.” She added that seeing things from her boss’s perspective has been a key to her professional development. “Their perspective was always different, and understanding the business from their point of view helped me grow.”

Stacy Methvin, independent director, Pioneer Natural Resources, also pointed out the importance of what she termed “broadening assignments.” Boards are often looking for executives with specific experience, such as HR and executive compensation. Perhaps even more important, she said, is a background that includes responsibility for P&L or the company’s strategic direction. “They want someone who can run a company or a large division within a company.”

Mary Bass, partner, Spencer Stuart, shared her experience as a recruiter for boards, stressing that boards look for experience but equally important is how executives handle themselves. “It’s a 24/7 world, and how you behave is critical, whether at the company or at your child’s soccer game. People are watching, so act accordingly.”

Panelists agreed that networking and being mentored by other women is critical. In addition, women approached for recruitment should interview the board just as they are being interviewed. This includes talking with the CEO and board members on an individual basis. “If the cultural fit isn’t there, if you and the CEO don’t quite get along, that’s an issue you need to think long and hard about,” said Methvin. The panelists were also realistic in admitting the obstacles that still remain for women who want to serve on boards. “Being the first minority in any situation is not always easy, and that certainly applies to women,” said Cunningham. “You need to know going in that board membership can be a challenge—but that’s where the growth is.”

Women in Energy Breakfast: Women on Energy Boards – How to Develop and Position Yourself for Success

“You need to know going in that board membership can be a challenge — but that’s where the [personal] growth is.”

Susan M. Cunningham, Senior Vice President of Gulf of Mexico, Africa,

Frontier Ventures and Business Innovation, Noble Energy

Day One

5 | © KPMG

Day One Opening Remarks

John Kunasek, U.S. sector leader for Energy & Natural Resources, KPMG LLP (U.S.), and Regina Mayor, U.S. Energy & Natural Resources Advisory leader, KPMG LLP (U.S.),opened the conference with a discussion of the issues framing the agenda. “We are in an unprecedented level of uncertainty and change for the industry,” Mayor said, referring to the economic, geopolitical, and regulatory uncertainty that the industry faces.

Kunasek noted that economic uncertainty comes from a slowing recovery. “What you see in recent statistics is that the recoveries are starting to moderate, and there’s some uncertainty included in that,” he said. Economies at different levels of development are also recovering at different rates, he said.

Recent events have contributed to increased geopolitical uncertainty. How tensions in the Middle East and between Ukraine and Russia will play out is unknown and a significant risk factor. In addition, economic and political policies in China and Japan could have a major impact on the global economy.

Kunasek and Mayor stressed that regulatory uncertainty is especially important. Climate change and sustainability, demand for increased access to affordable energy, and responses to the Fukushima Daiichi nuclear disaster in Japan are all contributing to regulatory changes. The possible actions of local regulators are perhaps the most important factor in regulatory uncertainty.

“Given this uncertainty, the fact that we can’t predict the future, we would put forward that the new core competence is an organization’s ability to anticipate and then respond,” Mayor said. She said technology, talent, risk, and delivery are the four things that companies need to get right. Technology is having a significant impact on the industry through the growing use of renewable energy, new technology to access oil wells previously deemed uneconomic, and breakthroughs in energy storage and distributive energy technology.

Energy companies also face a considerable challenge in the projected talent crisis. While the recent recession delayed many retirements, the industry now faces the confluence of an aging workforce, a significant number of retirements, and a new generation of workers.

Additionally, a new set of risk factors threatens the industry. Cybersecurity has increased in importance as this risk continues to grow. In the United States, aging infrastructure requires significant investment and has led to an increase in the number of significant power outages as well as increased vulnerability to weather.

Maintaining the energy delivery system will also be a growing challenge. The global urban population is expected to grow to two-thirds of the world’s population by 2050, and 90 percent of that increase is projected to come from underdeveloped regions.

While LNG could help in meeting growing energy demand, the global LNG industry will require approximately US $300 billion in investment and North America alone needs an estimated $200 billion

in investment in pipeline infrastructure.

“There are so many things that are going to change and we would put forward that our ability to anticipate and respond is going to be key.”

Regina Mayor, U.S. Energy & Natural Resources Advisory Leader,

KPMG LLP (U.S.)

Day One

6 | © KPMG

General Session I: How New Oil and Gas Supply is Changing Energy Policy

“You can’t just pick one aspect of free trade and free market and ignore all the other inhibitors to free trade and free market.”

Charles T. Drevna, President, American Fuel & Petrochemical Manufacturers

Day One

© KPMG | 7

General Session I: How New Oil and Gas Supply Is Changing Energy Policy

The increased supply of oil and natural gas from shale could lead to significant changes in energy policy, as some policymakers have proposed lifting the export ban on U.S. crude oil. John Gimigliano, principal, KPMG LLP (U.S.), led a panel discussion on whether the United States should lift this export ban. Panelists included Lee Fuller, vice president of Government Relations, Independent Petroleum Association of America; Kevin Book, managing director of Research, ClearView Energy Partners, LLC; and Charles T. Drevna, president, American Fuel & Petrochemical Manufacturers.

Book discussed the economic effects of the export ban. He noted that the United States became a net exporter of refined products in 2011, including increased exports to Canada. He said an additional 1.2 million barrels are going into inventory, and the supply glut on the Gulf Coast has pushed down the price of crude. Book also noted that forward pricing, a diversity of imports, and strategic oil reserves have contributed to a more secure market since the export ban was put in place during the 1960s and 1970s. “We’re much less concerned now about oil security and much more concerned about optimizing oil economics,” he said.

Fuller said producers are looking at the export ban from the standpoint that there is a certain price where it is no longer economical to keep producing oil. He also noted that the pace at which resources can be developed is dramatically faster than in the past. Fuller said the key is if the oil surplus can be assimilated into the U.S. system and exported to Canada at the same pace. “From that structure, it’s not that this industry sees exports as the primary approach that should be taken to utilize American crude, but, by the same token,

the desire to have the ability to export that crude when the U.S. capacity is incapable of managing all of it is a necessity that we think is important for the real potential for American production to grow at the pace that has been projected.”

Drevna said there was a misconception that U.S. refineries cannot take any more of the light sweet crude. “The problem is that our oil and gas system is turned on its head because of the shale revolution,” he said. He argued that the impact of increased U.S. exports on the world economy is unknown. Drevna described a “three-legged stool” of unprecedented production; the unknown of transportation, supply, and storage capacity; and the developing regulatory system.

Fuller argued that the ability of refiners to alter their operations to absorb shale was also unknown. He noted that exports of refined products are allowed and asked if refiners would change to produce more naphtha for export. “Those types of changes can deal with the volumes, but if the value to the producer isn’t high enough to keep production going then it’s not going to be that valuable from the production standpoint,” he said.

Panelists also discussed how a change to the export ban could happen. Book said the President can modify it by executive order, but he noted that since gasoline prices are not high and the crude glut has not cost jobs, then the political environment does not favor changing the policy. He noted that many politicians from both parties are not in favor of lifting the ban. Overall, all panelists were skeptical of Washington’s ability to act on this matter.

“1.8 million BPD ‘peak to trough’ change in net products for the U.S.”

Kevin Book, Managing Director of Research, Clearview Energy Partners, LLC

Day One

8 | © KPMG

Citing recent statistics that over 50 percent of the oil and gas professionals will be eligible for retirement by 2016, Zoe Thompson, principal, KPMG LLP (U.S.), set the stage for an in-depth discussion of what the energy industry can do to address the problem of an aging workforce. Barbara Heim, vice president, Human Resources, BG Group, described the problem as primarily a matter of being more proactive in finding the right people with the right technical skills. “We’ve known this problem was coming for a long time; we’ve just had our heads in the sand.” She pointed out that new hires need

extensive training to become qualified. In response, the industry must become more flexible in how it develops resources. “In the past, we had a checklist—five years at this job and five years at another. Now, companies are deciding to take more risks, and that’s healthy, especially with new grads.” She said that the key in hiring is ability rather than a specific set of proven skills. “I believe that if you hire for intellect, you’ll be able to train new people very quickly.” She cited a company program designed to bring in new grads with the promise of international assignments and continuous recruitment that have both helped meet their hiring goals.

Concurrent Session I-A:

Stemming the Retiring Workforce Brain Drain

Day One

© KPMG | 9

Stemming the Retiring Workforce Brain Drain

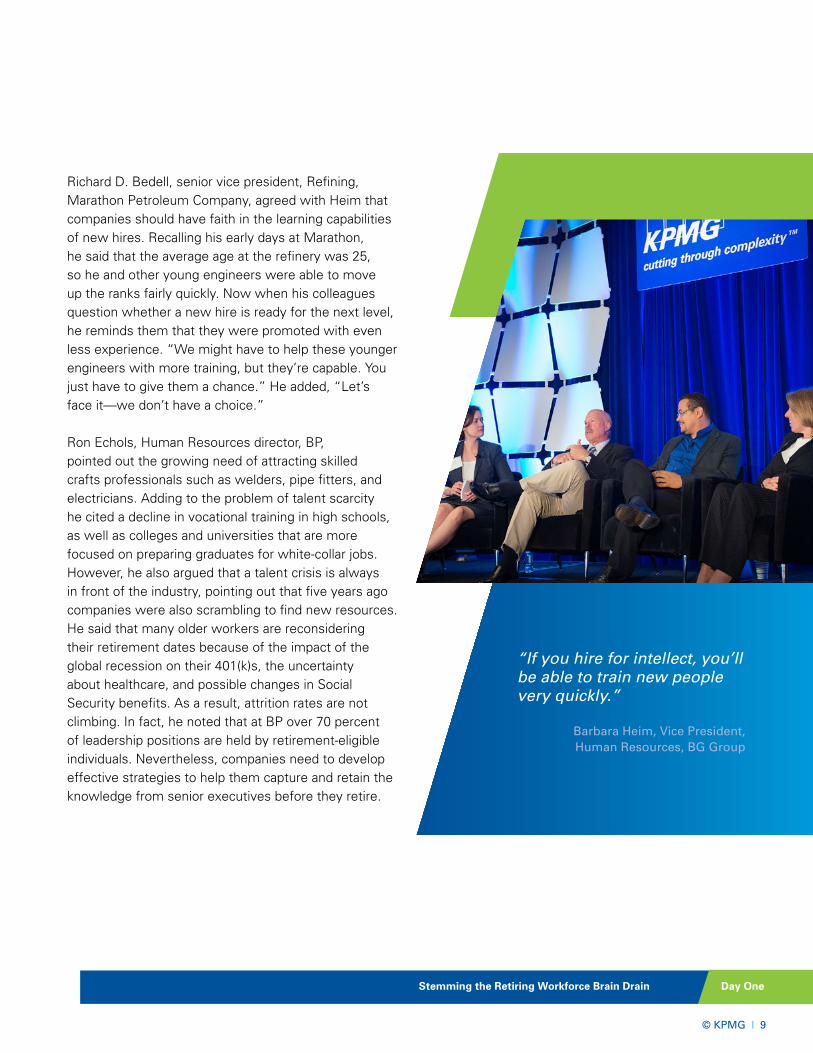

Richard D. Bedell, senior vice president, Refining, Marathon Petroleum Company, agreed with Heim that companies should have faith in the learning capabilities of new hires. Recalling his early days at Marathon, he said that the average age at the refinery was 25, so he and other young engineers were able to move up the ranks fairly quickly. Now when his colleagues question whether a new hire is ready for the next level, he reminds them that they were promoted with even less experience. “We might have to help these younger engineers with more training, but they’re capable. You just have to give them a chance.” He added, “Let’s face it—we don’t have a choice.” Ron Echols, Human Resources director, BP, pointed out the growing need of attracting skilled crafts professionals such as welders, pipe fitters, and electricians. Adding to the problem of talent scarcity he cited a decline in vocational training in high schools, as well as colleges and universities that are more focused on preparing graduates for white-collar jobs. However, he also argued that a talent crisis is always in front of the industry, pointing out that five years ago companies were also scrambling to find new resources. He said that many older workers are reconsidering their retirement dates because of the impact of the global recession on their 401(k)s, the uncertainty about healthcare, and possible changes in Social Security benefits. As a result, attrition rates are not climbing. In fact, he noted that at BP over 70 percent of leadership positions are held by retirement-eligible individuals. Nevertheless, companies need to develop effective strategies to help them capture and retain the knowledge from senior executives before they retire.

“If you hire for intellect, you’ll be able to train new people very quickly.”

Barbara Heim, Vice President,Human Resources, BG Group

Day One

10

Disruptive Technologies Utilities Can’t Ignore

Concurrent Session I-B:

10 | © KPMG

Day One

© KPMG | 11

Dale Williams, partner, KPMG LLP (U.K.), moderated a broad-ranging discussion about power-related technologies such as wind turbines, solar panels, mini-grids, smart grids, and demand management that are changing the energy landscape around the world. Matt Guyette, chief narketing and strategy officer, GE Power & Water, emphasized that plummeting costs have been the main driver of growth for alternative energy, a growth that is 20 times the pace of traditional

energy development. He pointed out that wind turbine generation has increased over 400 percent since 2004 while costs have dropped by two-thirds. As for solar, the world has seen more growth in the past two years than in the 40 years previously, with prices dropping by 50 percent in the past two years. “Even though solar presently makes up a tiny fraction of energy generation, it’s disruptive today, and it’s going to be more disruptive tomorrow.” He also noted the importance of new business models where homeowners can lease solar equipment, avoiding large front-end costs for their home installations. “Along with the development of shale gas,” he said, “the shift in the use of wind and solar, driven mainly by price, is causing an energy revolution across the United States and around the world.” Ben Wilson, CFO, Strategy & Regulation and Networks, UK Power, added that in the United Kingdom, incentives and subsidies are equally important, if not more so. With the recent end of government support for home-based solar generation, the solar industry has shifted to field-scale solar generation. “Fairly soon, we might see our East England network begin to meet minimum demand from distributed generation,” he said, “and it might even be a net exporter at certain times of the day to the national grid. That is a disruptive change.” Discussing incentives in U.S. states, Todd Durocher, managing director, KPMG LLP (U.S.), explained that states such as California and New Jersey offered significant rebate programs to encourage the development of solar for homeowners. This led to an increase in adoption, but these incentives have now been eliminated because the unplanned micro-generation by homeowners and businesses introduced uncertainty in terms of energy costs and availability across the grid. He suggested that perhaps micro-generation at the neighborhood level might be adopted to mitigate disruption to the grid and better support reliability. He also pointed out that solar micro-generation still has tremendous promise globally as an energy source for areas lacking access to power. “You can get power to people out in the desert, and that’s a development we in the industry want to support.”

Disruptive Technologies Utilities Can’t Ignore

“Even though solar presently makes up a tiny fraction of energy generation, it’s disruptive today,and it’s going to be moredisruptive tomorrow.”

Matt Guyette,Chief Marketing and Strategy Officer,

GE Power & Water

Day One

12 | © KPMG

International tax minimization through profit shifting and “stateless income” is a fundamental challenge to the way the global tax system operates. In response, the Organisation for Economic Co-operation and Development (OECD) and G20 leaders began the Base Erosion and Profit Shifting (BEPS) initiative. Chetan Vagholkar, partner, KPMG LLP (U.S.) moderated a panel that discussed current developments in BEPS. The panel included André Boekhoudt, partner, KPMG Meijburg & Co (Netherlands), and Michael Plowgian, principal, KPMG in the U.S.’s Washington National Tax.

Vagholkar outlined the three factors that have driven the BEPS initiation. First, the economic downturn reduced tax revenues. Second, there is a perception that multinational corporations are making significant profits and not paying their fair share of taxes. Third, many governments think multinational corporations are

shifting profits to low-tax jurisdictions. This has led the OECD to call for action in the form of BEPS. “It’s a pretty ambitious plan,” Vagholkar said, discussing the issue of how much corporations will have to report to different countries. “That’s going to be the biggest challenge in the next 12 to 18 months.”

Plowgian discussed the U.S. perspective and noted that the United States is concerned about these issues from profit shifting. He noted reform proposals from both U.S. political parties that include limiting interest expense reduction, dealing with payments to hybrid organizations, and strengthening the controlled foreign company (CFC) rules. “There’s surprising consistency between these proposals,” Plowgian said. Nonetheless, he noted that “the practicalities of getting that done in the short term seem to be pretty low.”

Concurrent Session I-C:BEPS: The Global Legislative Response to Tax Minimization

Day One

© KPMG | 13

BEPS: The Global Legislative Response to Tax Minimization

Boekhoudt discussed the different views at the EU level as well as from the individual countries in Europe. “I think the EU is reaching consensus in the transfer pricing master file,” Boekhoudt said. “As of 2016, companies need to show the value chain of all global revenues,” he said. “That’s a big change from the olden days.”

“There is a lack of cohesion in the EU on corporate income tax because we have a lot of tax competition between the countries,” Boekhoudt said. “There is a battle going on for attracting business, but business based on substance.” Companies will no longer be able to allocate profits to countries simply for tax purposes after 2016. He discussed the tension between EU countries and the U.S. tax system, which minimizes non-U.S. taxes and makes the U.S. levy on repatriated taxes as high as possible. “So it’s a battle mainly against U.S. corporations,” Boekhoudt said.

Plowgian said BEPS is driven by the politics of member governments and the leaders of the G20. He noted the tight time line of completing an agreement by September 2015. “It’s an unbelievable amount of work to get this done,” Plowgian said. He also discussed the importance of the OECD acting on this issue. “The OECD definitely feels the pressure that if they don’t act, then countries will act unilaterally, resulting in double taxation, and that’s exactly what the OECD has spent the past 50 years combating.”

Vagholkar noted that country-by-country reporting requirements will be required soon. “That, in my view, is a game changer, and companies need to start anticipating and of course responding to the country-by-country reporting action item,” he said. Boekhoudt discussed the dozens of items that companies will have to make available to a country’s tax authority. “Forget about spreadsheets, forget about PowerPoints; you need to set up a database-supported information structure around it,” Boekhoudt said. “What scares me is that I see a lot of multinational companies that think this is going to be a very manageable thing and are not starting to do it today,” he said.

“What scares me is that I see a lot of multinational companies that think this is going to be a very manageable thing and are not starting to do it today.”

André Boekhoudt, Partner, KPMG Meijburg & Co (Netherlands)

Day One

14 | © KPMG

In an hour-long discussion, Dr. Rice covered a wide range of topics from her advice on today’s energy companies to how we improve K-12 education, how to build women leaders, and how her views on domestic terrorism were shaped as a child growing up in segregated Birmingham. She offered insightful views and advice to women and developing leadership, tips on parenting in today’s world, and her thoughts on stability in different parts of the world of interest to energy companies.

As U.S. Secretary of State under the Bush administration, Dr. Rice gained a unique perspective on world affairs. She shared this perspective in an

astute overview of recent geopolitical events, their impact on the energy industry, and the role of the United States as a world leader. She characterized today’s international situation as “dangerous and chaotic.” This is not surprising, she argued, since the world has seen four “major shocks” since the beginning of the century. She listed the September 11th terrorist attacks, the financial crisis of 2008, the Arab Spring in 2010, and recent actions by Russia and other countries as events that are “rearranging the tectonic plates of the international system.”

Keynote Address:

Remarks by Condoleezza Rice U.S. Secretary of State, 2005 to 2009

“It must be that the most powerful country on the face of the Earth be generous, kind, and believing in human potential…”

Day One

© KPMG | 15

Remarks by Condoleezza Rice, U.S. Secretary of State, 2005 to 2009

“Great powers and great leaders can’t afford to be tired.”

What she called “great powers behaving badly” is perhaps the greatest cause for concern, arguing that the United States should maintain a clearly defined presence backed by military strength. She stated, “The instability of great powers is bad because by their very nature, they have the capacity of destabilizing the international system.“

“We need to get our defense policy right, and deep cuts in a period when great powers are behaving badly probably doesn’t make a lot of sense.”

At the same time, she emphasized the importance of oil and gas as a measure of national strength. “Energy is a very big part of the solution to these international problems,” she said.

“In fact, energy is geopolitics with a really big ‘G.’” She recalled the impact of crude oil prices in 2008. “When oil went to $147 a barrel, I never saw diplomacy affected so much,” she said, citing initiatives by Caesar Chavez, Vladimir Putin, and leaders across the Middle East. However, she pointed to the “extraordinary resources” available in North America that can help ensure energy security for the United States. “If we explore and exploit them sensibly and put them to work, this is going to change the energy profile of the international community in remarkable ways.”

“North America is a powerhouse in terms of energy,” she continued. “If we don’t use this energy, not only do we give up the possibility of economic growth in areas that have been depressed for a long time, but we give up the possibility of rearranging important elements of the geostrategic balance.” She cited the recent agreement between Russia and China for the sale of oil and gas to Chinese markets as an example of a major energy development that bypassed U.S. influence. Despite her concerns about international developments, Rice expressed optimism about the future of her country. “In history, the United States has been the very best in mobilizing human potential.” This strength is especially important, she argued, in a world where technical innovation and creativity are essential in addressing problems ranging from healthcare to energy supply. She also pointed to the openness of American society as a key advantage. “’We the people’ is an inclusive concept. We are not united by blood or ethnicity, by nationality or religion. Americans are united by a view that you can come from humble circumstances and do great things.”

Day One

16 | © KPMG

The energy sector is experiencing both increased complexity and increased capital intensity that is not proportionate to revenue growth. Oil and gas companies are deploying assets in remote locations for difficult projects, while power and utilities companies face a regulatory environment that often does not allow tariff increases or higher capital recovery needs. The energy industry, nonetheless, has an opportunity in technology, as the maturity of data management capability has increased significantly in recent years. Hiran Bhadra, principal, KPMG LLP (U.S.), moderated a panel on data & analytics in the energy industry that included Raymond E. Cline, Jr., department chair, Information and Logistics Technology, University of Houston; Martin Narendorf, senior director, Asset Planning and Optimization, CenterPoint Energy; and Rick Veague, chief technology officer, IFS North America. Narendorf discussed his organization’s data

transformation and said they focused on the value proposition of these investments. He noted that his company is achieving reliability improvements and increased efficiencies in operations. “We are expecting to capture great value to deliver to the marketplace and to the consumer,” he said.

Veague discussed the business benefits of these investments. He described how new technology such as the smart grid is changing the business landscape. “I think it’s very different than the traditional model,” he said. Veague said these technologies create a more dynamic environment and will have a profound impact on the business. He said the business benefit is in moving from a largely reactive model to a much more predictive and proactive model, which can lead to efficiencies and can also be used to exploit new opportunities.

Concurrent Session II-A:

Data & Analytics: The “Smart” Way to Enterprise Asset Management

Day One

© KPMG | 17

Data & Analytics: The “Smart” Way to Enterprise Asset Management

Cline discussed the increased maturity in how structured and unstructured data is handled. He predicted that the next level of maturity is to use it for closed-loop controls on a systems basis. “The holy grail is: how will it tie that back into my trading operations?” Cline said. He also discussed the challenge of finding the right people with data analytics skills and getting different roles to collaborate. “It’s not just the technology. It’s the people, process, and the technology,” he said.

The panelists discussed the types of skills that will be needed for this increased use of data analytics. Narendorf noted that companies need employees with both hard skills and business analytics skills. “It’s almost like the perfect person in the futureis going to be some sort of hybrid,” he said. Cline discussed the educational challenges and said students must come out of school with these needed skills. “One of the challenges that we have from a traditional education standpoint is are we going to water down the engineering degrees to put in IT,” he said.

Cybersecurity is an important topic on the minds of many executives. Cline said the risks are “very real.” He noted that companies must take into account the risks of having third parties handle their data, as they are legally responsible for security breaches by that third party.

The panelists also discussed the challenge of implementing data & analytics systems. Narendorf advised to include operations as part of the planning. Veague noted that implementation is a collaborative effort without a single solution, while Cline emphasized the importance of education and training for it to succeed.

“It’s not just the technology. It’s the people, process, and the technology.”

Raymond E. Cline, Jr., Department Chair, Information and Logistics Technology,

University of Houston

Concurrent Session II-A:

New Utility Business Models for the 21st Century

18 | © KPMG

Day One

© KPMG | 19

The critical interplay between technology and business in the energy industry was a major theme at this year’s conference. During the morning’s session on disruptive technologies, panelists discussed new global energy sources and distribution systems. In this session, the conversation focused on U.S. companies and how technical innovations might affect traditional business models for utilities. Bob Bergbauer, principal, KPMG LLP (U.S.), kicked off the discussion by asking about the impact of recent growth in solar energy. Stephanie McMichael, director, Strategic Planning, Arizona Public Service Company, pointed out that while market penetration is rapidly increasing, solar still provides only a small fraction of total energy

output. Pricing and reliability are the key challenges for solar technology. She also explained issues involving net metering for homeowners who offset electricity supplied by utilities with energy they generate themselves. The homeowners sell any net excess back to the utilities and avoid paying the fixed costs utilities incur to operate and maintain the distribution system. This creates a situation whereby nonsolar customers effectively subsidize those with solar panels. David K. Owens, executive vice president, Business Operations Group, Edison Electric Institute, agreed that net metering rate policies still need adjustment. “You can’t overcompensate the customer with rooftop panels,” he said. “You’ve got to make a contribution to the grid if you use it.” He proposed that utilities need to provide greater transparency in their billing so customers can better understand fixed cost recovery disparities and why they should not expect to sell electricity at the same price they buy it from the utilities. Citing recent court rulings involving EPA environmental regulation, Bergbauer then turned the discussion to the changing patterns of electric generation sources, chiefly coal and natural gas. Clint C. Freeland, executive vice president and chief financial officer, Dynegy, Inc., shared his experience with coal-fired power plants. “Not all coal plants are created equal,” he said, explaining that different plants use different types of coal and emission-reduction technologies, a distinction that is often overlooked in environmental debates. In addition, he acknowledged the importance of rapidly growing shale gas supplies, but noted that the existing gas pipeline infrastructure is still tied to traditional gas supply basins in the Gulf Coast and Rocky Mountain regions. Fully exploiting new gas reserves through fracking will require significant changes to this infrastructure, along with new storage facilities in the north and northeast. The panelists all felt that a diverse portfolio of energy sources is best for the utility industry. If natural gas becomes the overwhelming choice for new generation, that will only increase demand and lead to higher natural gas prices. The industry needs to consider what the right mix of energy sources might be, even while rewarding utilities for delivering affordable electricity on a reliable basis. “When it comes to energy sources,” said Owens, “what we need is a little bit of everything.”

New Utility Business Models for the 21st Century

“When it comes to energy sources, what we need is a little bit of everything.”

David K. Owens, Executive Vice President,

Business Operations Group, Edison Electric Institute

Day One

20 | © KPMG

Concurrent Session II-C:

Concurrent Session II-C:

Cyber Security Evolution: From the Data Center to the Boardroom

Who is attacking companies today? The better question might be who isn’t? This was one of many insights provided in a detailed discussion moderated by Greg Bell, principal, KPMG LLP (U.S.), about cybersecurity threats and defense strategies for energy companies. Michael Assante, director, SANS Institute, set the stage for the discussion. “In the last decade or two, our understanding of cybersecurity has always been lagging,” he explained. Cybersecurity used to be

considered as a business expense, and attacks were measured by the time and resources required to repair damage. However, hackers are now aware that cyber attacks can be monetized, while at the same time nations are using cyber tools to gather intelligence. As a result, cybersecurity professionals in the United States are still trying to catch up with a new generation of highly structured and directed attacks. “These days, companies have to operate under the assumption of breach,” he said, “and some of us haven’t yet made that change in thinking.”

Day One

© KPMG | 21

Cyber Security Evolution: From the Data Center to the Boardroom

Lisa Gauthier, vice president and chief information officer, Rowan Companies, agreed that cyber attacks in the energy industry have grown exponentially in size and complexity. “It’s not about protecting data anymore; it’s about protecting our core business,” she said. This includes employees and their safety, significant assets now under lock and key, and the environment that might be damaged if field operations are attacked. Cybersecurity is not just about networks and password protection but more about infected USB drives or employees who unknowingly click on an infected e-mail, she explained. “Part of my job is education about these threats, and that includes every employee as well as vendors outside the company.” Mark Thibodeaux, attorney, Sutherland Asbill & Brennan LLP, pointed out the legal ramifications of security. The government requires personnel records and medical information to be secure, he explained, so energy companies have taken steps to protect this information. But many companies are still at risk when it comes to other areas such as contracts, which usually include confidentiality agreements. In some cases, the information technology (IT) function is not alerted that

this content needs to be protected, especially if the contracts involve multinational operations. As a result, companies are unknowingly vulnerable to having this contractual confidentiality compromised by cyber attacks. Bell rounded out the discussion by listing six questions that energy companies should ask about cybersecurity: Do we have the right leadership in place to address cybersecurity, including but not limited to IT? Are we training all employees to recognize suspicious activity that might indicate a cyber threat? Do we know where our sensitive data resides? Do we have an effective plan to help us react to a cyber attack? Are we respectful of security laws in the United States and overseas? And do we have strong technology controls to defend the company from attack? Many companies focus only on the last question about technology, he said, but the other questions are equally important.

“These days, companies have to operate under the assumption of breach.”

Michael Assante, Director, SANS Institute

Day One

22 | © KPMG

“In the next five years, we will transform how we: market, sell, communicate, collaborate, innovate, and educate.”

General Session II:

Daniel Burrus, Founder and CEO Burrus Research Associates

Day One

© KPMG | 23

Daniel Burrus, Founder and CEO Burrus Research Associates

“Nobody can predict the future.” As a business forecaster and futurist, Daniel Burrus hears this a lot in his travels. During his keynote address, however, he argued that we can actually predict a great many things, especially if we can identify what he called “hard trends.” Hard trends, according to Burrus, are those trends we can extrapolate into the future with a high degree of certainty. We know for sure that smartphones will be smarter, that chips will get faster, and that storage capacities in devices will only increase, and these changes will affect how we use technology and conduct our businesses. “Once you get a smartphone, you’re not going back to a dumb one.” But this does not mean that the old technology will disappear; we will just be using the old technology differently. “If you want to see the future accurately, you have to understand the ‘both-and’ principle of technology. Mainframes and PCs are still around; we just use them differently. The key is how to bring the old and new together to create value that is greater than either one could create separately.”

Predicting the future is key for business success. “Things are changing and changing fast. Are you changing as fast as your customers are changing? Are you learning as fast as your customers are learning? If the answer is no, you’ve got trouble already.” Burrus noted that the younger generation is more familiar with new technology, citing visual communication tools like Skype as one example. This technology enables users to see “what others

are thinking, not just what they are saying.” We can better understand how others are feeling if we can watch their facial expressions and body language. “This helps us communicate better and that means better relationships.” Unfortunately, he said, many businesses have still not “seen the future” of this technology.

“If it can be done, it will be done and if you don’t, your competition will do it before you.” Even as he pointed out the importance of new technology, he explained that innovation by itself is not necessarily the key to success. “We have legacy technology, but that’s not the problem. It’s legacy thinking.” He advised everyone to take an hour every week to think about the future of their business. “The definition of your job is going to change. So are you going to change it—or will somebody change it for you?” He said that this time spent “unplugged from the present and plugged into the future” was critical even for hard-working professionals. “Yes, we’re all busy, but we can busy ourselves right out of business.” As he noted at the beginning, we can be certain about many things in the future, and nothing is more powerful in business than showing a customer something about their future which is obvious—once it is pointed out. “When you hear the future truth, you know it,” he said, “and that kind of certainty is the ultimate closing tool of any sale.”

“Energy is a secret ingredient that helps solve every major problem on Earth.”

Day One

24 | © KPMG

Day Two

Day Two Opening Remarks

John Kunasek and Regina Mayor opened the second day of the conference by highlighting the key themes and takeaways from the previous day’s sessions. They paid particular attention to the Day 1 keynote speakers Condoleezza Rice and Daniel Burrus.

Kunasek and Mayor also detailed the results of the 2014 KPMG Energy Industry Outlook. The survey revealed that the vast majority of energy executives are optimistic about the future, but they see emerging risks coming from energy costs, regulations, cybersecurity, and customer and employee mobility.

The opening session also included an interactive session that included real-time audience polls on several issues facing industry executives, including their outlook for oil and gas prices.

The majority of conference attendees expect oil prices to stay at more than $100/bl for the remainder of 2014.

Almost half (47 percent) of attendees also expected natural gas prices to stay in the range of $3.76–$4.50. Also, 74 percent of conference attendees think the United States could be energy independent by 2030, an increase from past years.

A surprising number of attendees said business model transformation will be a main focus for spending. Employee compensation and training, as well as managing the regulatory environment, were also significant areas of focus for energy companies.

Day One

25 | © KPMG

Day Two

Some of the most exciting new developments in the global energy industry are found in Mexico, East Africa, and West Africa. Andy Steinhubl, principal, KPMG LLP (U.S.), served as moderator for a discussion about key regulatory, prospectivity, and M&A trends that are creating both opportunities and challenges for U.S. oil and gas companies in these regions. Gilberto Alfaro, partner, KPMG in Mexico, provided an overview of recent activities around energy reform in Mexico, including the evolution of PEMEX—the

country’s national oil company—from a quasi-government agency responsible for energy security and operator of all in-country oil and gas projects to a state-owned, value-driven, enterprise. Alfaro was candid about the challenges facing the Mexican industry. “We need to develop new regulations to address transparency and corruption. We also need to build regulatory and other institutions necessary to support these imperatives. Stronger regulations will provide more authority and enable local and third parties from outside the country to work together

Breakfast Panel:

Evolving Opportunities and Challenges

in Mexico and Sub-Saharan Africa

Day Two

© KPMG | 26

for greater effectiveness.” He recognized the concern by investors that despite regulatory reform, PEMEX would retain a market advantage and not be subject to rules applied to other entities. At the same time, he saw opportunities for investors if they closely studied contract requirements, and considered opportunities for local partnering in their supply chains and potentially with PEMEX. Looking beyond current PEMEX capabilities, he anticipates early opportunities in high-potential areas in deep water and shales. For example, the highly productive Eagle Ford formation in the United States extends into Mexico, but as of yet it is undeveloped beyond the border. Dimeji Salaudeen, partner, KPMG in Nigeria, and head, Africa Oil & Gas, discussed improving prospects for energy companies in West Africa. “The potential in West Africa is not in what we have, but in what we see in front of us,” he said, pointing out that development is increasing due to significant offshore discoveries in Nigeria, Angola, and Ghana, improved geopolitical conditions, and greater economic stability. As well, Nigeria is restructuring its onshore industry, with multiple new operators and participation options expected to emerge. With oil and gas fields maturing in many parts of the world, Africa can be considered as one of the “last frontiers” for exploration and production. And, its location is advantaged to not only local markets, but to rapidly growing demand centers in SE Asia. “The opportunity is huge for foreign investors,” he said. As with any venture,

investors should do their due diligence and talk with players “on the ground” to better understand local conditions, but the companies that act today will be the winners tomorrow. “The time to come to Africa is now.” Richard Ndung’u, partner, KPMG in East Africa, conceded that East Africa has long envied West African oil and gas developments, but he argued that with substantial new reserves discovered in Tanzania, Rwanda, Uganda, and other countries, East Africa is on a path to matching, and potentially exceeding, supplies in the West. In fact, the same geological formations found in both West Africa and Brazil continue across East Africa, suggesting further discoveries in the future. He explained that foreign investors are using several models for engagement. These include bilateral agreements between local and foreign governments, although he conceded that political instability in Africa can put these agreements at risk. In the private sector, foreign companies are funding start-ups, buying local companies to operate as wholly owned subsidiaries, and entering into joint ventures with local or regional companies. On the whole, he said, the private sector presents more risk, but appears to offer sustainable opportunities for foreign investors entering the East African market. Like Salaudeen, he asserted that the time to enter is now, despite these risks, because the opportunities to assemble large positions and shape projects or infrastructure is higher today than probably later.

Evolving Opportunities and Challenges in Mexico and Sub-Saharan Africa

e

“The time to come to Africa is now.”

Dimeji Salaudeen, Partner, KPMG in Nigeria, and Head, Africa Oil & Gas

Day One

27 | © KPMG

Day Two

Robert Best, chairman of the board at Atmos Energy Corporation, offered his unique perspectives on the natural gas industry as well as on the importance of leadership. He discussed the factors behind Atmos Energy’s success as well as recent changes in the industry, and he shared the leadership principles that he has learned during his career.

Atmos has played an important role in the development of the U.S. natural gas industry, as it has grown from a small company to one of the largest gas pipeline businesses in the United States. Best discussed how

the success of Atmos came partly from its decision to focus on pipeline, distribution, and marketing only. He also discussed the firm’s growth strategy through acquisitions and noted the challenges that acquisitions can bring. “You have to have good continuity of leadership and good board support to do that,” he said.

Best stated that open transportation in buying and selling, deregulation at the well head, and fracking have all contributed to improving the natural gas industry over the years. He noted that in the past, there were concerns over the adequate supply of natural gas.

General Session III:

The Development and Future of the

U.S. Natural Gas Industry

Day Two

© KPMG | 28

“The greatest thing that’s happened to our industry today is that nobody talks about supply or lack thereof,” he said. Best outlined the impact that this increased supply has had on the economy. “Our manufacturing businesses have come back to natural gas.”

Best also discussed how natural gas will be needed as a backup for renewable energy sources and as a source of energy to meet the growing demand from urbanization and population growth. “Natural gas is going to play a very huge role for a very long time in this country,” he said.

Best argued that the political environment posed the biggest challenge to natural gas due to “anticarbon and antienergy” views. He noted opposition to fracking as well as to the Keystone pipeline as examples. Best also argued what the industry should do in response. “We have to do a better job of selling what we are and what we do.” He also predicted that the most successful companies will be those that can influence policymaking as well as use technology efficiently and effectively.

Best is passionate about leadership and shared his leadership principles. He said leaders must focus on the fundamentals and work to get people to understand their role as part of a team. Leaders must also get along because their attitudes affect the entire organization. He also noted that keeping employees in positions where they cannot be successful does not benefit them. Best also argued that good leaders must care more about the organization than they care about themselves. He said leaders should not stay too long for the wrong reasons, including for money and perks.

Best also discussed the importance of culture in a successful organization. “The reason you create a great culture is not so you can make everybody feel good,” he said. “It’s to create high performance.” This culture includes believing that employees are the heart of the company and creating trust between the company and the employees. “Culture trumps strategy,” he said.

The Development and Future of the U.S. Natural Gas Industry

“Culture trumps strategy.”

Day One

29 | © KPMG

Day Two

The “Intelligent Oilfield” has become a focus in recent years, and this panel of experts provided attendees with an overview of this concept as well as insight into barriers that have prevented it from being implemented faster in today’s oil and gas companies. Mark Tackley-Goodman, principal, KPMG LLP (U.S), moderated the panel and pointed out that even with the advent of shale gas, operating costs continue to

rise. Equally important, new regulations will require companies to demonstrate increasingly higher levels of operational effectiveness. He laid out the main components of the Intelligent Oilfield, which originally was simply a matter of asset-level instrumentation. The concept has broadened to encompass not just the technology, but also how the technology is being applied to make production processes faster, cheaper, and safer.

Concurrent Session III-A:

Information Strategies for Upstream Effectiveness

Day Two

© KPMG | 30

Pieter Kapteijn, managing director, FossilFuture, listed the capabilities required for implementing the Intelligent Oilfield and emphasized that the technology itself has already been developed. “Things are working at the lower level but not all the way across the organization. To realize the potential, it’s all about leadership that will enable a company to go to the next level.” Addressing employee turnover through retirement, Jim Crompton, managing director, Reflections Data Consulting LLC, said that today’s young professionals come to companies already comfortable with advanced technology. “They’re digital natives rather than digital immigrants.” He recalled that when he started working for energy companies in the 1970s, he was amazed at the technology made available to him. Now, he says, young professionals are often disappointed with company technology that can’t compare to their own devices. “We’re seeing a tension of expectations when it comes to Generation Y employees who want better and more sophisticated technology.” Danny Meyer, Global Exploration IT manager, Shell, said that in the past, companies focused only on earnings. Then the goal was to develop new technology to help improve operations. Now the challenge for many companies is to close the gap between earnings and technology through changes in behavior, leadership, and people who can understand the big picture. “We now have an opportunity to get smarter about what we’re doing, and that includes better wells, fewer dry holes, and more production.” He said oil and gas companies need to move the lessons learned in the field across the company so “every win can be an exponential win.”

Information Strategies for Upstream Effectiveness

“Leaders need to fullyunderstand IT. There’s no app for it.”

Pieter Kapteijn,Managing Director,

FossilFuture

“Culture trumps strategy."

Day One

31

Concurrent Session III-B:

Regulatory Trends That Are Changing

the Power Industry

31 | © KPMG

Day Two

© KPMG | 32

Major changes in regulation, enforcement, and market structures are changing the U.S. electric power industry. Glenn George, principal, KPMG LLP (U.S.), moderated a wide-ranging discussion on key industry topics such as capacity markets, infrastructure upgrades, customer demands for higher reliability, and disruptive technologies. Raymond Hepper, vice president, general counsel, and corporate secretary, ISO New England, outlined the main issues facing the New England region. “Capacity markets are the big nut we are all trying to crack,” he said. The concept introduces a radical change whereby resource performance and compensation in the marketplace are closely tied together. “That hasn’t really been done in a capacity market.” Nevertheless, he stated that capacity markets are the best way forward for utilities. During the past three to five years, ISO New England has seen some natural-gas-fired resources that don’t always have the needed gas, so the market relies on deteriorating oil units. “We don’t think an energy-only market will work. We think a capacity market is critical, and as we integrate more renewables, it will become even more critical.” Bohdan “Buck” Pankiw, chief counsel, Pennsylvania Public Utility Commission, listed several areas of importance for Pennsylvania electric utilities. One issue involved retail markets and uncapped rates that were introduced in 2011. When the Polar Vortex hit the region in January 2014, customers with variable rate programs saw their electricity bills soar by 100 to 200 percent.

Utilities responded with new efforts to educate customers about their variable rate plans and help them decide whether they want to accept the risks involved with a variable rate. Pankiw also discussed funding for maintaining the state’s aging infrastructure. The Public Utility Commission approved a mechanism for utility cost recovery of upgraded natural gas pipelines and other distribution components. This charge provides utilities with immediate capital recovery for infrastructure project costs. Thomas O’Neill, senior vice president, regulatory and energy policy and general counsel, ComEd, argued that the traditional regulatory model based on adequate reliability at least cost for volume sales is no longer relevant. Today’s commercial customers need “perfect” or premium power for their computer-based systems. “They won’t tolerate flickering lights anymore because all their systems trip offline and have to reboot.” At the same time, people use less energy today because of increased energy efficiency. This reduces energy demand and therefore impacts volume sales and revenues for utilities. In addition, customers now expect innovations like smart metering and self-healing grids to improve service and reduce outages. “In all these areas, the issue is really one of value,” he said. “What is the value of the electric grid to modern life?” Utilities need to move away from a least-cost discussion and help customers understand power more in terms of the measurable benefits that power provides to everyone.

Regulatory Trends That are Changing the Power Industry

“Capacity markets are the big nut we are all trying to crack.”

Raymond Hepper, Vice President, General Counsel, and Corporate Secretary, ISO

New England

Day One

33 | © KPMG

Day Two

The developing global LNG market could play a prominent role in meeting global energy demand. Mary Hemmingsen, Canada sector leader for Power and Utilities, KPMG LLP (Canada), led a panel discussion on the global LNG industry, including U.S. exports, an update on North American LNG projects under development, and an outlook for LNG demand in Asia. The panel included Renee Klimczak, president and chief executive officer, The Jarrah Group LLC; George O’Leary, vice president, Oil Service, E&C and LNG Research, Tudor, Pickering, Holt & Co.; and Mark Stubbe, senior vice president, Marketing and Trading, Cheniere Marketing LLC.

O’Leary discussed the projects under construction and explained that large exporters are now building regasification plants. He said the United States, Canada, and Mozambique are expected to provide the incremental supplies to the global market. Klimczak noted the significant and growing demand in global markets. “Currently the demand for global LNG is outpacing the supply, and this is largely due to the Fukushima impact from a few years ago,” she said. Klimczak said this could change by 2018–2020, when supply could exceed demand.

Concurrent Session III-C:

The Developing Global LNG Market

Day Two

© KPMG | 34

The panelists also discussed competitive differentiators for global LNG projects. O’Leary emphasized the importance of cost and discussed the significant arbitrage opportunity for U.S. gas suppliers. Stubbe stated that timing is everything for a strategic advantage and said the high number of proposed LNG projects drives competition and innovative thinking. “You have all this competition that’s built around the most integrated, flexible energy system in the world,” he said.

Klimczak noted that the United States has advantages from its liquid natural gas market, significant upstream resource base, integrated pipeline system, and export facilities. “Clearly, the risk out of the United States is much lower than these fully integrated projects,” she said. Klimczak said the brownfield projects will be completed and that some of the greenfield projects in the United States will likely be built before those in Canada and Africa. Klimczak predicted that about 25 percent of the proposed projects will be built. She said they will come online gradually and therefore won’t greatly impact the U.S. natural gas market.

O’Leary emphasized that proximity to Asia was an advantage for projects in Canada, Mozambique, and Tanzania. However, he explained that U.S. projects have a cost advantage in extraction and building liquefaction, which are the largest cost components.

The panelists also discussed the innovation of floating LNG plants. Klimczak outlined the benefits of floating LNG facilities in that they are cost effective, have a smaller environmental impact, and can be relocated if the market shifts. Stubbe added that floating LNG facilities increase competition.

The panelists also discussed the impact of shale natural gas on the global LNG market. O’Leary explained how natural gas liquids have driven shale production and how this has led to an oversupply of propane and ethane. He said NGLs and condensate make ongoing natural gas production economic despite the low natural gas prices. He also noted that the United States is projected to become a significant exporter of ethane and propane in the coming years.

In discussing the near future for the industry, O’Leary projected that regasification projects will continue to be built at a greater rate than liquefaction projects. In addressing the risks of overcapacity, he noted that the LNG market has weathered previous falls in demand. “It’s a resilient market, there is demand out there, you will see incremental projects built,” O’Leary said.

The Developing Global LNG Market

“It’s a resilient market, there is demand out there, you will see incremental projects built.”

George O’Leary, Vice President, Oil Service, E&C and LNG Research,

Tudor, Pickering, Holt & Co.

Concurrent Session IV-A:

Good, Bad, Ugly, and Good Again JVs in the Energy Industry

Day Two

© KPMG | 36

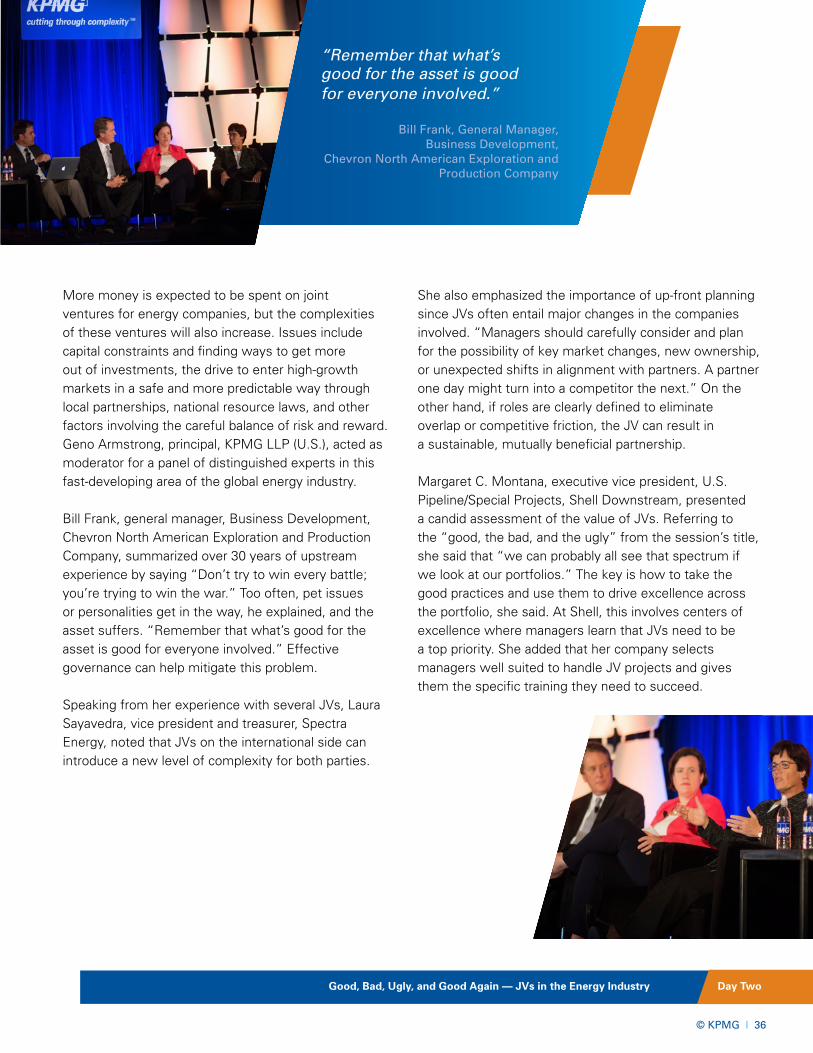

More money is expected to be spent on joint ventures for energy companies, but the complexities of these ventures will also increase. Issues include capital constraints and finding ways to get more out of investments, the drive to enter high-growth markets in a safe and more predictable way through local partnerships, national resource laws, and other factors involving the careful balance of risk and reward. Geno Armstrong, principal, KPMG LLP (U.S.), acted as moderator for a panel of distinguished experts in this fast-developing area of the global energy industry. Bill Frank, general manager, Business Development, Chevron North American Exploration and Production Company, summarized over 30 years of upstream experience by saying “Don’t try to win every battle; you’re trying to win the war.” Too often, pet issues or personalities get in the way, he explained, and the asset suffers. “Remember that what’s good for the asset is good for everyone involved.” Effective governance can help mitigate this problem. Speaking from her experience with several JVs, Laura Sayavedra, vice president and treasurer, Spectra Energy, noted that JVs on the international side can introduce a new level of complexity for both parties.

She also emphasized the importance of up-front planning since JVs often entail major changes in the companies involved. “Managers should carefully consider and plan for the possibility of key market changes, new ownership, or unexpected shifts in alignment with partners. A partner one day might turn into a competitor the next.” On the other hand, if roles are clearly defined to eliminate overlap or competitive friction, the JV can result in a sustainable, mutually beneficial partnership. Margaret C. Montana, executive vice president, U.S. Pipeline/Special Projects, Shell Downstream, presented a candid assessment of the value of JVs. Referring to the “good, the bad, and the ugly” from the session’s title, she said that “we can probably all see that spectrum if we look at our portfolios.” The key is how to take the good practices and use them to drive excellence across the portfolio, she said. At Shell, this involves centers of excellence where managers learn that JVs need to be a top priority. She added that her company selects managers well suited to handle JV projects and gives them the specific training they need to succeed.

Good, Bad, Ugly, and Good Again — JVs in the Energy Industry

“Remember that what’s good for the asset is good for everyone involved.”

Bill Frank, General Manager, Business Development,

Chevron North American Exploration and Production Company

Day One

37 | © KPMG

Day Two

Energy production, delivery, and use are essential to the growth and operation of many cities. With increasing urbanization, there is an urgent need for improved ways to integrate energy strategies into urban planning. Ron E. Clanton, partner, KPMG LLP (U.S.), moderated a panel on the challenges of urban planning and the variety of possible

solutions. The panel included Linda Head, associate vice chancellor, Workforce Education & Corporate Partnerships, Lone Star College; Raiford Smith, vice president of Corporate Development & Planning, CPS Energy; and Ken Geisler, vice president, Strategy, Smart Grid Division, Siemens.

Concurrent Session IV-B:

Meeting the Energy Needs of the New Urban Society

Day Two

© KPMG | 38

“It’s not just putting up fancy equipment and earning a rate of return; it is a meaningful impact to our customers’ lives and really to our economy.”

Raiford Smith, Vice President of Corporate Development & Planning,

CPS Energy

Head stated that the way the United States will remain competitive is to have a strong workforce pool. This includes identifying the job gaps, including those in the skilled trades. “Those jobs have changed. They’re technical,” she said. “We don’t have a huge pool of unskilled labor anymore.”

Geisler discussed how suburbanization grew with industrialization. Now, there’s reurbanization and redevelopment of downtown areas, and the infrastructure needs to follow it. Geisler said the top issues for utilities were reliability, efficiency, sustainability, and resiliency. “There is a movement with the move to urbanization and the need for resiliency and the desire for greater sustainability to decentralize.”

Smith discussed how utilities shifted from being developers of technology to being consumers of technology. Now, with the move toward new technologies like renewables and the smart grid, the industry has changed again from being consumers of technology to technological innovators.

Smith noted the three grids on which utilities depend: the electric grid, the telecomm grid, and the IT infrastructure grid. “All three of those different infrastructures are actually combining right now in our grid,” Smith said. He said that this requires a different workforce and a different way to solve problems. “I think it calls for a lot more partnerships than what we’re used to doing.”

Geisler said resilience issues are driving the issue of how to keep critical assets up and running in urban areas. “The truth of the matter is that the regulated business models needs to change,” he said. He explained how utilities designs will also have to change to accommodate renewables. “The fact of the matter is that it’s going to have to decentralize because it’s the only way you can get some of the economies and address some of the resiliency issues that we have and the fact that it’s going to involve the community at a fundamental level,” Geisler said.

Smith predicted that the energy grid will follow Metcalf’s law in which the value of the grid is proportional to the number of connected and communicating devices. He also discussed the implications of this for utilities. “Not only do you need to understand technology better, you need to change your underlying business model and you need to partner,” he said. “It’s not just putting up fancy equipment and earning a rate of return; it is a meaningful impact to our customers’ lives and really to our economy.”

Meeting the Energy Needs of the New Urban Society

Concurrent Session IV-C:

Accounting and Reporting Update

Day Two

© KPMG | 40

Many companies have not yet implemented a new plan in anticipation of the new FASB revenue recognition standard. Andrew Cabble, partner, KPMG LLP (U.S.), noted that industry has had a long wait for final issuance of this standard. Several distinguished panelists were able to add additional insight to this and other critical issues about new developments in accounting and reporting for the energy industry. Mark Bielstein, partner, KPMG LLP (U.S.), pointed out that the new revenue recognition standard would result in a number of changes—limited but still significant—that involve the transfer of control in terms of customer contracts, the performance obligations within the contract, the transaction price, price allocations, and recognizing revenue from the performance of the contractual obligations. Bielstein also discussed lease standards. The FASB has suggested a dual-model approach where capital leases are treated as the IASB model, recording the right of use, the asset, the liability, and the combination of the amortization of the asset, with the interest expense showing accelerated income statement recognition. For energy leases, however, the FASB proposes another amortization model where amortization and interest are presented as a single line item. Bielstein questioned whether this approach would eliminate the “bright line” between operating lease accounting and capital leases that now exists today.

Christopher Champion, partner, KPMG LLP (U.S.), provided an upstream perspective about the FASB revenue recognition standard and its possible impact on reporting. “The entitlements method is actually a creation from the 1990s, and it doesn’t seem to line up with the proposed standard,” he said, suggesting that further action would be required by the SEC. He also commented on FASB 144 and its relevance to discontinued operations. “My personal view is that this statement needed correcting a long time ago,” he said, adding, “where we are today with 144 is definitely where we need to be.” Darin Kempke, partner, KPMG LLP (U.S.), reviewed recent SEC comments that are relevant to power and utilities companies. These include matters related to impairments and goodwill; segments for companies and SEC questions addressed to companies when they change these segments; and joint venture accounting for utilities, especially in terms of new requirements to consolidate information between the two entities. He also discussed accounting issues involving utilities and their ability to have off-take agreements and SEC rules that make the off-taker consolidate the power plant, an approach that utility executives say makes little sense from a risk and reward perspective.

Accounting and Reporting Update

“Where we are today with 144 is definitely where we need to be.”

Christopher Champion, Partner,KPMG LLP (U.S.)

Day One

41 | © KPMG

Day Two

Keynote Address:

Why Not Your Best? NFL Legend

Terry Bradshaw Cohost and Analyst, FOX NFL Sunday

The 2014 Global Energy Conference ended on a high note with Terry Bradshaw, who shared the secrets of his success as football legend, gospel singer, actor, best-selling author, television broadcaster, and highly sought-after motivational speaker. Bradshaw has thought long and hard about how we should measure true success in our lives. “We can be happy if we’re smart, rich, and famous. But what really counts is joy, and joy is embedded in your spirit, your

soul. You can better deal with the tragic things in life if you have identified within yourself what brings you joy.”

Bradshaw said that joy can be a part of growing older. “As you go through the decades of your life, there’s a transformation—you understand that life is coming to an end. So you tell yourself—I’m not going to waste my time. I’m going to enjoy my life. Things might not make sense, but I’m going to enjoy every moment.”

Day Two

© KPMG | 42

Bradshaw also suggested that joy includes a strong measure of humility regardless of what we might accomplish in life. “If God called me to be a quarterback, why did I complete only 50 percent of my passes?” And despite being a member of the NFL Hall of Fame, he readily confessed that other quarterbacks have been better. “I’m no Staubach. I’m no Montana. I was never America’s quarterback.” He also praised Dallas Cowboys coach Tom Landry, even though he never played on Landry’s team. Landry was “the guy who could see stuff that nobody else could envision. He was a genius.”

For Bradshaw, humility is impossible without gratitude. “We accomplish nothing without saying thank-you to somebody else,” he said. “It’s important that we appreciate other people, that we learn how to be caring and kind and loving. It’s important that we tell our kids that we love them, tell our parents that we love them.” “The basics in life are all about people and heart and family. What truly makes us successful is that we become a family.”

“We accomplish nothing without saying thank-you to somebody else.”

Why Not Your Best? NFL Legend Terry Bradshaw, Cohost and Analyst, FOX NFL Sunday

Day One

43 | © KPMG

Day Two

Don’t Miss It! May 20–21, 2015

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act upon such information without appropriate professional advice after a thorough examination of the particular situation.

© 2014 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.