rapeseed/mustard seed - · pdf fileoilseeds and edible oil market. ... sea of india, nb...

TRANSCRIPT

Rapeseed/Mustard SeedCropSurvey & Analysis

2016

Rapeseed/Mustard SeedCropSurvey & Analysis

2016

OVERVIEW

DOMESTIC SCENARIO

Past Performance

Blame it on El-Nino, which ruffled the agro-climatic conditions in India, rendering a year of drought and

distress to the agriculture economy of India. The year 2015 was bad to the bone for the farm sector with reports

of crop losses pouring in from various quarters. On one side, our agro-trade deficit burgeoned while on the

other, the farmers were wailing over waiving agricultural loans. As it happened to be, many farmers were

unable to cover their losses, let alone make profits. The prices of essential goods skyrocketed due to the

widening demand-supply gap. Truly, the scenario was a downer.

Last year, we felt the heat of El-Nino which affected most of the agro-commodities in India and South-East Asia.

Amongst oilseeds, the production of soybean, which predominantly is a kharif, dropped to unpredicted levels

of around 7.5 million metric tonnes, a whopping decline of around 1.8 million metric tonnes from earlier

estimates. The dip in production witnessed prices rising to unprecedented levels. However a steep ascent was

arrested by the gloomy state of oil-meal exports and the declining profitability of oil mills. Also, the

burgeoning imports of edible oils spearheaded by palm oil from Malaysia and Indonesia choked the domestic

oilseeds and edible oil market.

Beginning the rabi season in October 2015, many turned down the possibilities of further climatic alterations

to a major extent. But, it seems that the rabi sowing hasn’t spread smiles on many a person. Lack of adequate

soil moisture, the variations of day and night atmospheric temperatures, relative humidity and precipitation,

has affected the plant growth in many regions in India –majorly the rain-fed regions of the country. The

oilseeds, especially Rape-Mustard (RM) seed witnessed a decline in sowing in major growing areas of India. As

per Nirmal Bang Commodity Research (NBCR), the decline in RM seed acreage was followed by an increase in

the acreage of pulses and coarse grains. Let us further delve into the details of the agro-climatic conditions

prevailing in the rabi oilseed areas of India. We’ll further look into the export-import scenario and the domestic

consumption as well.

Rapeseed/Mustard SeedCrop Survey & Analysis 2016

16 March, 2016th

Kunal Shah

Head - Commodity Research

Anish G

Research Associate

Agri-Commodities

During the past rabi season (Oct 2014 – Mar 2015), the crop output was lesser than expected due to unseasonal

rainfalls accompanied by strong winds. With the last year production of mustard seed standing at around 55

Lakh metric tonnes, the total available stock declined to 57.4 Lakh metric tonnes. The futures market prices

touched as high as Rs.5106 per 100 kg, while the spot prices witnessed Rs.5184 (per 100 kg) levels. The year

2015 witnessed bull trend for most of the edible oils as the El-Nino induced weather conditions continued to

threaten the crop yield.

The trade deficit arising from the import of edible oils and the export of oilmeals continued to widen, with

India losing the oil meal market to its Latin American counterparts. The disenchantment in the Chinese

economy and the continuing rattle over crude oil production also influenced the market to a considerable

extent.

2

A condiment and cooking oil, mustard has been serving the Indian palette for ages. From the traditional mortar-and-pestle

(ghani) pressers to latest refining machines, mustard oil has and continues to add flavor to Indian gourmet.

Basically a winter crop, RM seed cultivation begins in the month of October-November and is ready to be harvested by the

end of February. The crop calendar of Mustard seed is depicted below:

Crop Seasonality and Existing Climatic Conditions

Rapeseed/Mustard Seed Acreage - India

Source: NB Research

Source: SEA of India, NB Research

This season (2015-16 rabi), the sowing for mustard crop in India, was delayed due to delayed harvesting of kharif crop in

some of the regions and absence of adequate soil moisture. While some farmers switched to the rabi crops as early as first

week of October, others waited to step in at an appropriate stage. However, the climatic conditions didn’t rhyme well. Let

aside the precipitation measure, even the warm winters failed to set a proper stage for development of pods. In many regions

the plant growth was observed to be stunted, with pest infestation, the combined effect of which is likely to take a toll on

the yield of the crop.

As per the recent estimates of acreage released by Solvent Extractors’ Association (SEA) of India, the states of Rajasthan,

Madhya Pradesh, Uttar Pradesh, Bihar Chhattisgarh, Gujarat, Odisha are falling behind from their previous year numbers,

while Punjab, Haryana, West Bengal and Uttarakhand have exhibited an increase in the acreage. It is also notable that in

Jharkhand, the acreage increased by 142.5% compared to the previous season. The total sown area of rapeseed stands at

64.51 Lakh hectares, which is 1.01% less than the area sown last season.

Sr.

No

State

2015-16 2014-14 Sr.

No

State

2015-16 2014-15

1 2 3 4 5 6 7 8 9

Andhra Pradesh Telangana Arunachal Pradesh Assam Bihar Chhattisgarh Gujarat Haryana Himachal Pradesh

0.01 -- 0.3 2.11 1.23 1.26 1.9 5.8 0.04

-- 0.01 0.28 3.07 1.25 1.35 1.93 5.25 0.03

10 11 12 13 14 15 16 17 18

Jammu & KashmirJharkhand Madhya PradeshOdisha Punjab Rajasthan Uttar PradeshUttarakhandWest Bengal

0.31 1.94 6.25 0.96 0.4 25.44 11.23 0.19 4.76

0.3 0.8 6.63 1.1 0.3 26.4 11.42 0.18 4.74

Rapeseed/Mustard SeedCrop Survey & Analysis 2016

16 March, 2016th

3

Many of us will be acquainted with the fact that the global surface temperatures are on a rise, and India has

also witnessed the repercussions of the same. The winter in India was supposed to provide a cushion to the

farmers reeling under crisis. But, not many a farmer is contended. In the past few weeks, the temperatures have

been turning out to be favourable for the rabi crops, but the effects of the dwindling temperature and Relative

Humidity on the crop is yet to be ascertained. Our observations and analysis follows an extensive survey of the

standing crops conducted during its growing and maturity phases, in its major growing regions of India.

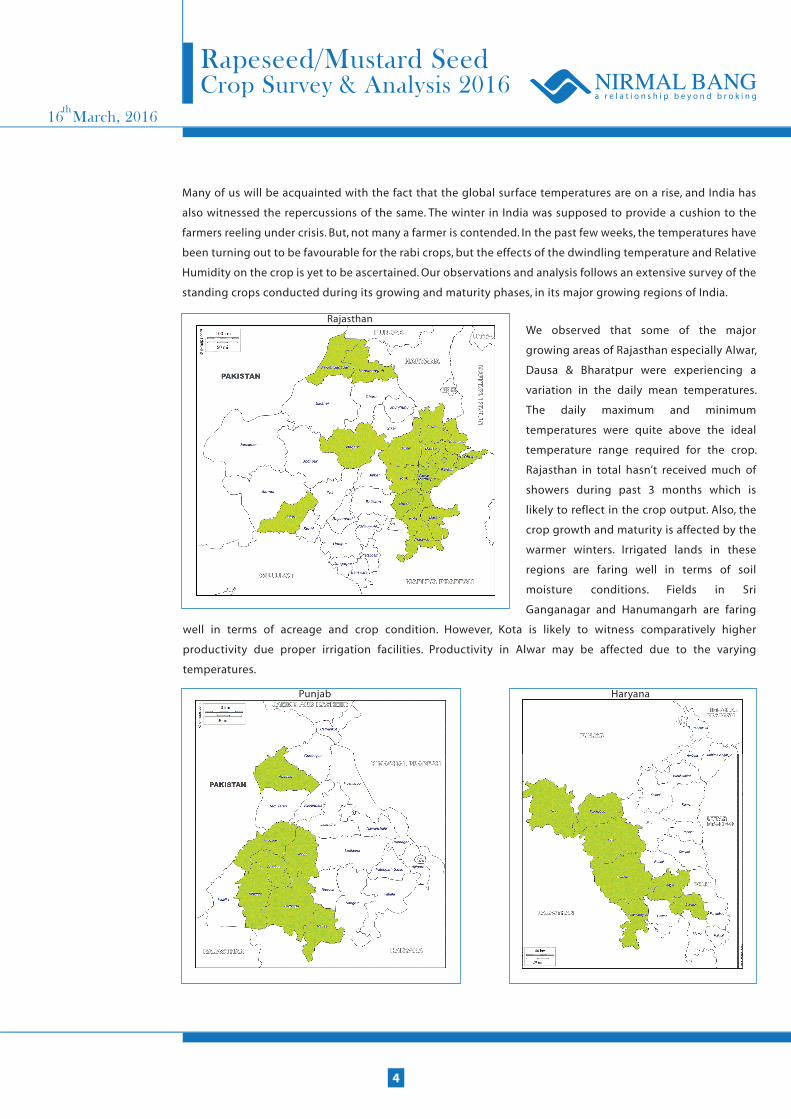

We observed that some of the major

growing areas of Rajasthan especially Alwar,

Dausa & Bharatpur were experiencing a

variation in the daily mean temperatures.

The daily maximum and minimum

temperatures were quite above the ideal

temperature range required for the crop.

Rajasthan in total hasn’t received much of

showers during past 3 months which is

likely to reflect in the crop output. Also, the

crop growth and maturity is affected by the

warmer winters. Irrigated lands in these

regions are faring well in terms of soil

moisture conditions. Fields in Sri

Ganganagar and Hanumangarh are faring

well in terms of acreage and crop condition. However, Kota is likely to witness comparatively higher

productivity due proper irrigation facilities. Productivity in Alwar may be affected due to the varying

temperatures.

Rajasthan

Punjab Haryana

Rapeseed/Mustard SeedCrop Survey & Analysis 2016

16 March, 2016th

4

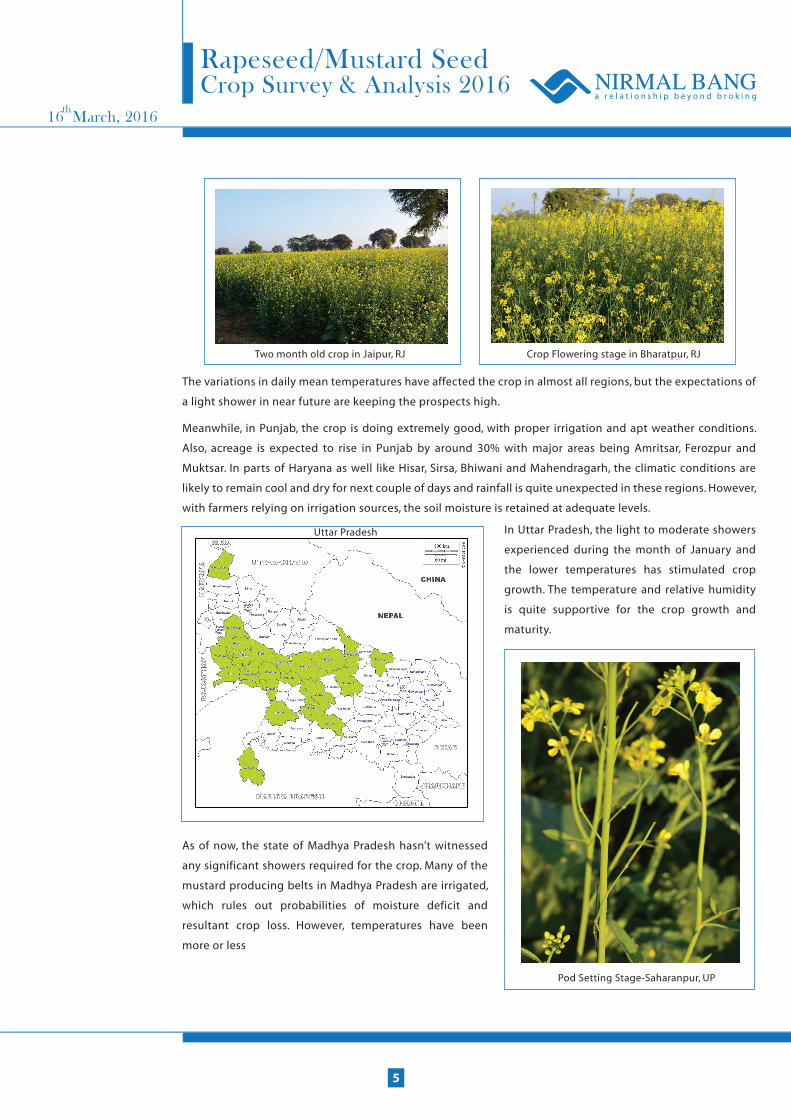

Two month old crop in Jaipur, RJ Crop Flowering stage in Bharatpur, RJ

Pod Setting Stage-Saharanpur, UP

The variations in daily mean temperatures have affected the crop in almost all regions, but the expectations of

a light shower in near future are keeping the prospects high.

Meanwhile, in Punjab, the crop is doing extremely good, with proper irrigation and apt weather conditions.

Also, acreage is expected to rise in Punjab by around 30% with major areas being Amritsar, Ferozpur and

Muktsar. In parts of Haryana as well like Hisar, Sirsa, Bhiwani and Mahendragarh, the climatic conditions are

likely to remain cool and dry for next couple of days and rainfall is quite unexpected in these regions. However,

with farmers relying on irrigation sources, the soil moisture is retained at adequate levels.

In Uttar Pradesh, the light to moderate showers

experienced during the month of January and

the lower temperatures has stimulated crop

growth. The temperature and relative humidity

is quite supportive for the crop growth and

maturity.

As of now, the state of Madhya Pradesh hasn’t witnessed

any significant showers required for the crop. Many of the

mustard producing belts in Madhya Pradesh are irrigated,

which rules out probabilities of moisture deficit and

resultant crop loss. However, temperatures have been

more or less

Uttar Pradesh

Rapeseed/Mustard SeedCrop Survey & Analysis 2016

16 March, 2016th

5

conducive to the growth of the plant.

Extremities in temperature are unlikely, and as

per preliminary reports, the region is likely to

receive light showers in the near term. In

Morena, light showers were experienced during

the 3rd week of January, 2016. However, the

temperatures are close to the ideal

requirement. Any major damages are not

reported as of now. However, Sehore region

hasn’t received good rains and the

temperatures are quite above the ideal

temperature requirements.

Pest Infestation-Chittorgarh Kota Belt, RJ Matured Pods-Kota Region, RJ

West Bengal contributes 5-6% of the total rapeseed production in India. It is notable that the acreage has

witnessed a minor surge and the current temperatures favour the pod development and maturity. The showers

experienced in the month of January have provided a fillip to the mustard crop, post which the temperatures

remained at favourable levels.

The major growing regions in Gujarat are facing risk from crop loss as the climatic conditions are weighing

heavy on the crop. Warmer winters are likely to pose a threat to the yield of the crop with probabilities of pest

infestation towards flowering and pod-setting stages. The minimum temperatures are hovering around 14°C

which is likely to be a detriment to the development and maturity of pods.

The recent showers and hailstorms in north-central belt of India have raised concerns on crop-loss

during the harvesting of major rabi crops. Considering the current scenario, we expect crop loss in major

mustard growing belts of India. However, it is too early to ascertain the losses at this point of time.

Madhya Pradesh

Rapeseed/Mustard SeedCrop Survey & Analysis 2016

16 March, 2016th

6

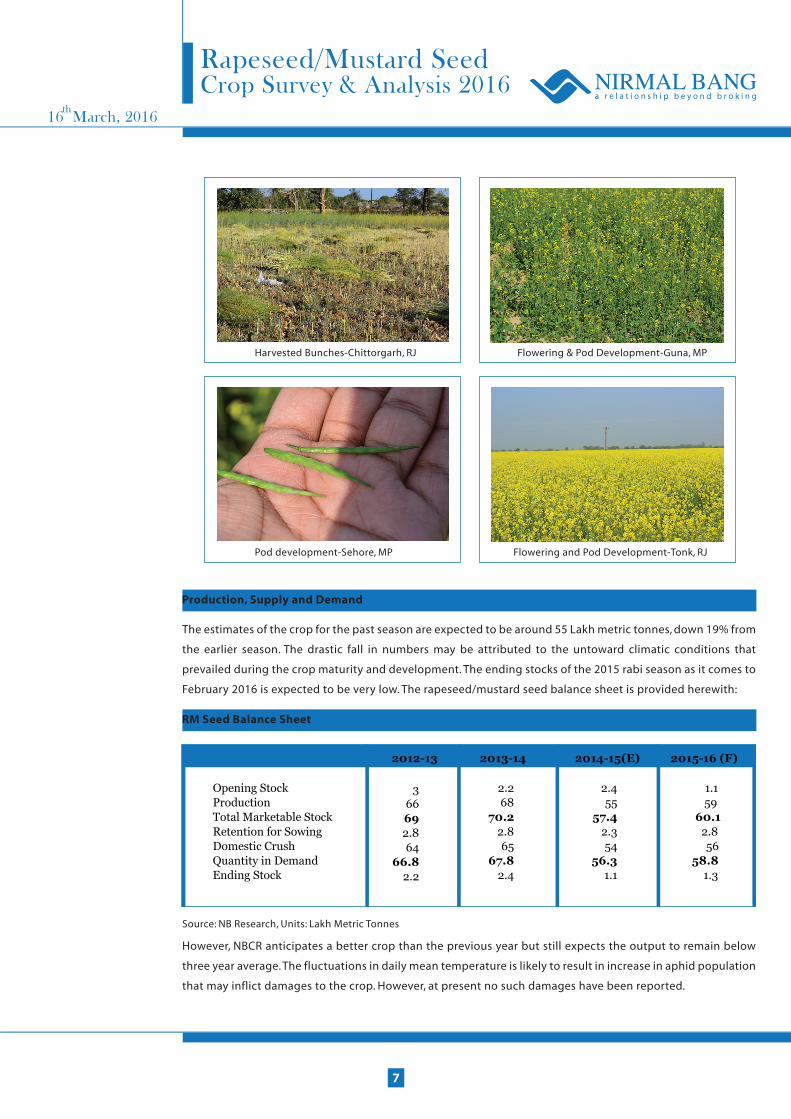

Production, Supply and Demand

RM Seed Balance Sheet

Harvested Bunches-Chittorgarh, RJ Flowering & Pod Development-Guna, MP

Pod development-Sehore, MP Flowering and Pod Development-Tonk, RJ

The estimates of the crop for the past season are expected to be around 55 Lakh metric tonnes, down 19% from

the earlier season. The drastic fall in numbers may be attributed to the untoward climatic conditions that

prevailed during the crop maturity and development. The ending stocks of the 2015 rabi season as it comes to

February 2016 is expected to be very low. The rapeseed/mustard seed balance sheet is provided herewith:

2012-13 2013-14 2014-15(E) 2015-16 (F)

Opening Stock Production Total Marketable StockRetention for Sowing Domestic Crush Quantity in Demand Ending Stock

3 66 69 2.8 64

66.8 2.2

2.2 68

70.2 2.8 65

67.8 2.4

2.4 55

57.4 2.3 54

56.3 1.1

1.1 59

60.1 2.8 56

58.8 1.3

Source: NB Research, Units: Lakh Metric Tonnes

However, NBCR anticipates a better crop than the previous year but still expects the output to remain below

three year average. The fluctuations in daily mean temperature is likely to result in increase in aphid population

that may inflict damages to the crop. However, at present no such damages have been reported.

Rapeseed/Mustard SeedCrop Survey & Analysis 2016

16 March, 2016th

7

Mustard Oil Balance Sheet

Source: NB Research, Units: Lakh Metric Tonnes

The average annual consumption of edible oils stands at 200 Lakh metric tonnes, which is evidently a figure to

worry about. NBCR estimates imports of rapeseed oil/canola oil to be consistent with the past year figures or

slightly lower at 2.8 Lakh metric tonnes.

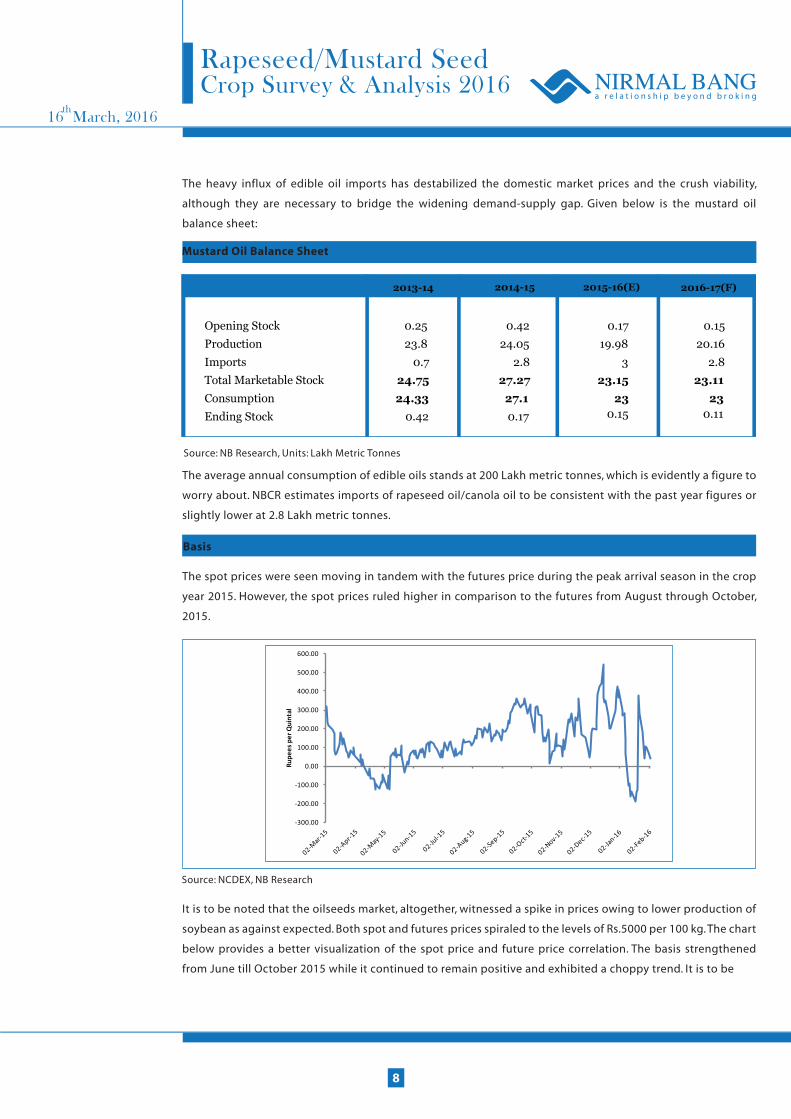

Basis

The spot prices were seen moving in tandem with the futures price during the peak arrival season in the crop

year 2015. However, the spot prices ruled higher in comparison to the futures from August through October,

2015.

It is to be noted that the oilseeds market, altogether, witnessed a spike in prices owing to lower production of

soybean as against expected. Both spot and futures prices spiraled to the levels of Rs.5000 per 100 kg. The chart

below provides a better visualization of the spot price and future price correlation. The basis strengthened

from June till October 2015 while it continued to remain positive and exhibited a choppy trend. It is to be

Source: NCDEX, NB Research

-300.00

-200.00

-100.00

0.00

100.00

200.00

300.00

400.00

500.00

600.00

Rupe

es p

er Q

uint

al

Rapeseed/Mustard SeedCrop Survey & Analysis 2016

16 March, 2016th

8

The heavy influx of edible oil imports has destabilized the domestic market prices and the crush viability,

although they are necessary to bridge the widening demand-supply gap. Given below is the mustard oil

balance sheet:

2013-14 2014-15

2015-16(E)

2016-17(F)

Opening Stock

Production

Imports

Total Marketable Stock

Consumption

Ending Stock

0.25

23.8

0.7

24.75

24.33

0.42

0.42

24.05

2.8

27.27

27.1

0.17

0.17

19.98

3

23.15

230.15

0.15

20.16

2.8

23.11

230.11

noted that the futures price remained subdued except for a brief period during the month of January-February

2016 where the futures ruled higher than spot owing to lesser stock and surging demand for edible oils.

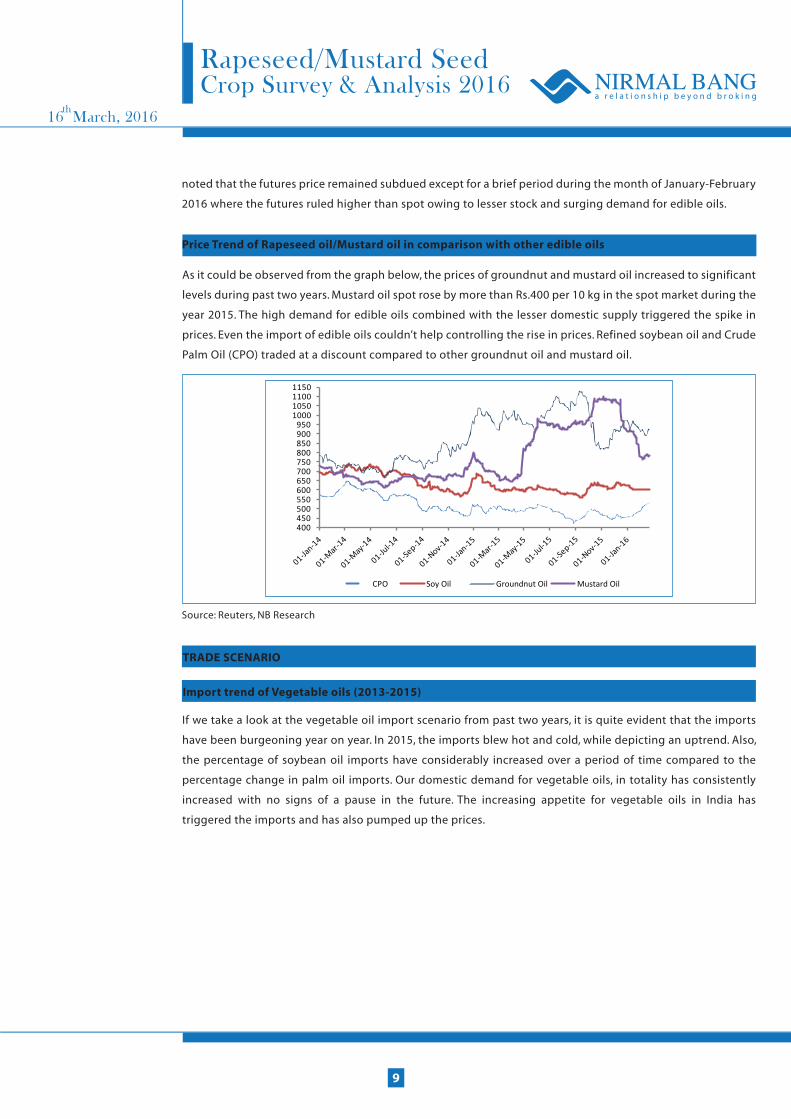

Price Trend of Rapeseed oil/Mustard oil in comparison with other edible oils

As it could be observed from the graph below, the prices of groundnut and mustard oil increased to significant

levels during past two years. Mustard oil spot rose by more than Rs.400 per 10 kg in the spot market during the

year 2015. The high demand for edible oils combined with the lesser domestic supply triggered the spike in

prices. Even the import of edible oils couldn’t help controlling the rise in prices. Refined soybean oil and Crude

Palm Oil (CPO) traded at a discount compared to other groundnut oil and mustard oil.

Source: Reuters, NB Research

400450500550600650700750800850900950

1000105011001150

CPO Soy Oil Groundnut Oil Mustard Oil

TRADE SCENARIO

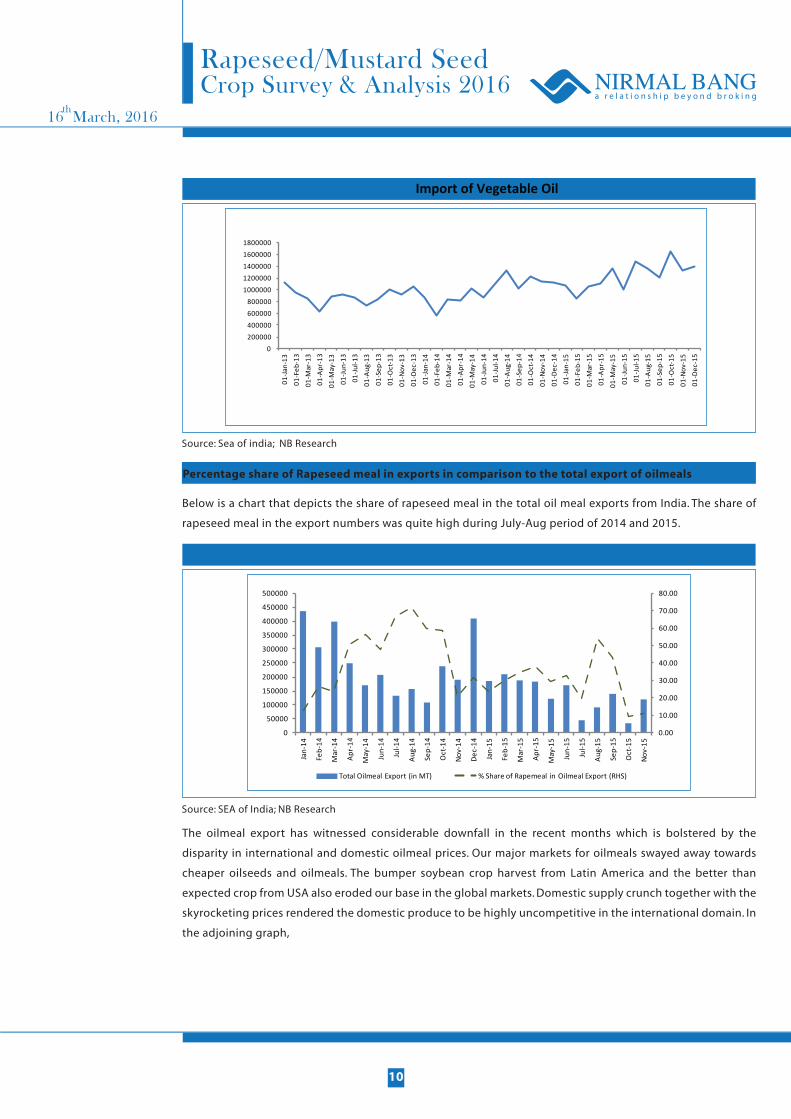

Import trend of Vegetable oils (2013-2015)

If we take a look at the vegetable oil import scenario from past two years, it is quite evident that the imports

have been burgeoning year on year. In 2015, the imports blew hot and cold, while depicting an uptrend. Also,

the percentage of soybean oil imports have considerably increased over a period of time compared to the

percentage change in palm oil imports. Our domestic demand for vegetable oils, in totality has consistently

increased with no signs of a pause in the future. The increasing appetite for vegetable oils in India has

triggered the imports and has also pumped up the prices.

Rapeseed/Mustard SeedCrop Survey & Analysis 2016

16 March, 2016th

9

Import of Vegetable Oil

Source: Sea of india; NB Research

Source: SEA of India; NB Research

Percentage share of Rapeseed meal in exports in comparison to the total export of oilmeals

Below is a chart that depicts the share of rapeseed meal in the total oil meal exports from India. The share of

rapeseed meal in the export numbers was quite high during July-Aug period of 2014 and 2015.

The oilmeal export has witnessed considerable downfall in the recent months which is bolstered by the

disparity in international and domestic oilmeal prices. Our major markets for oilmeals swayed away towards

cheaper oilseeds and oilmeals. The bumper soybean crop harvest from Latin America and the better than

expected crop from USA also eroded our base in the global markets. Domestic supply crunch together with the

skyrocketing prices rendered the domestic produce to be highly uncompetitive in the international domain. In

the adjoining graph,

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

500000

Jan-

14

Feb-

14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-1

4

Aug

-14

Sep-

14

Oct

-14

Nov

-14

Dec

-14

Jan-

15

Feb-

15

Mar

-15

Apr

-15

May

-15

Jun-

15

Jul-1

5

Aug

-15

Sep-

15

Oct

-15

Nov

-15

Total Oilmeal Export (in MT) % Share of Rapemeal in Oilmeal Export (RHS)

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1800000

01-J

an-1

3

01-F

eb-1

3

01-M

ar-1

3

01-A

pr-1

3

01-M

ay-1

3

01-J

un-1

3

01-J

ul-1

3

01-A

ug-1

3

01-S

ep-1

3

01-O

ct-1

3

01-N

ov-1

3

01-D

ec-1

3

01-J

an-1

4

01-F

eb-1

4

01-M

ar-1

4

01-A

pr-1

4

01-M

ay-1

4

01-J

un-1

4

01-J

ul-1

4

01-A

ug-1

4

01-S

ep-1

4

01-O

ct-1

4

01-N

ov-1

4

01-D

ec-1

4

01-J

an-1

5

01-F

eb-1

5

01-M

ar-1

5

01-A

pr-1

5

01-M

ay-1

5

01-J

un-1

5

01-J

ul-1

5

01-A

ug-1

5

01-S

ep-1

5

01-O

ct-1

5

01-N

ov-1

5

01-D

ec-1

5

Rapeseed/Mustard SeedCrop Survey & Analysis 2016

16 March, 2016th

10

Source: JCI China; Unit 1,000 MT; *Forecast for 2016-17

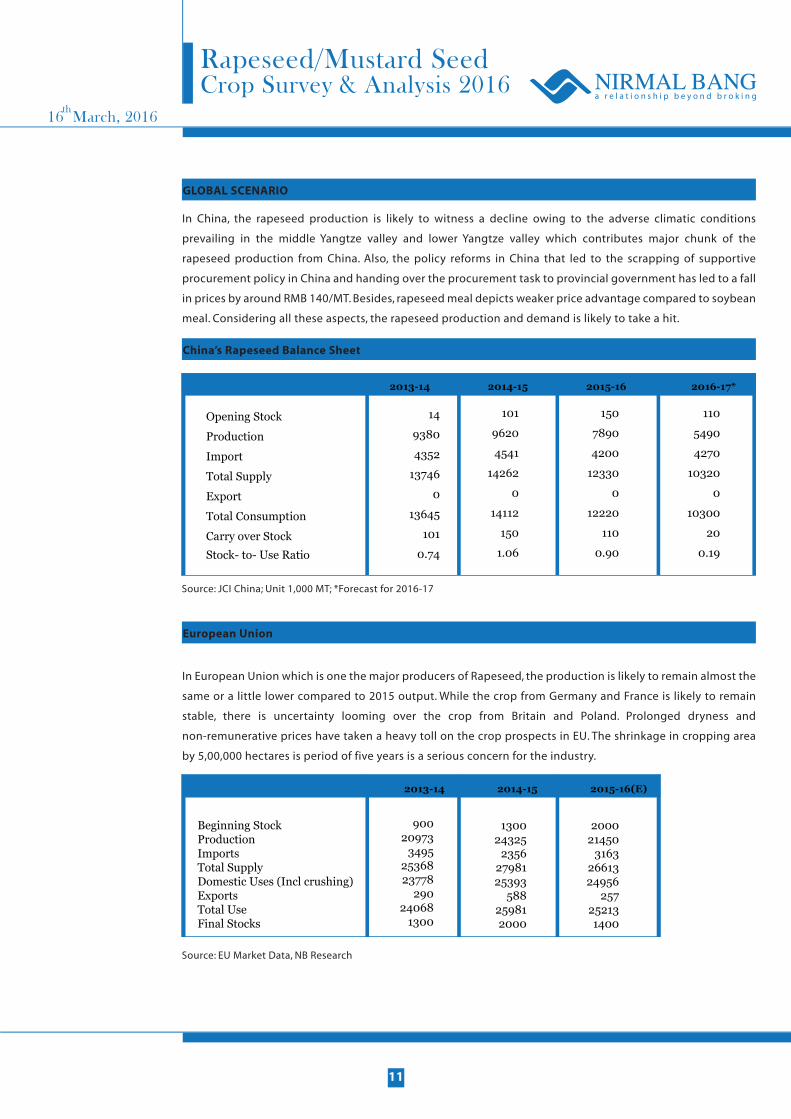

GLOBAL SCENARIO

China’s Rapeseed Balance Sheet

In China, the rapeseed production is likely to witness a decline owing to the adverse climatic conditions

prevailing in the middle Yangtze valley and lower Yangtze valley which contributes major chunk of the

rapeseed production from China. Also, the policy reforms in China that led to the scrapping of supportive

procurement policy in China and handing over the procurement task to provincial government has led to a fall

in prices by around RMB 140/MT. Besides, rapeseed meal depicts weaker price advantage compared to soybean

meal. Considering all these aspects, the rapeseed production and demand is likely to take a hit.

2013-14 2014-15 2015-16 2016-17*

Opening Stock

Production

Import

Total Supply

Export

Total Consumption

Carry over Stock

Stock- to- Use Ratio

14

9380

4352

13746

0

13645

101

0.74

90020973

34952536823778

29024068

1300

130024325

23562798125393

588259812000

200021450

31632661324956

257252131400

101

9620

4541

14262

0

14112

150

1.06

150

7890

4200

12330

0

12220

110

0.90

110

5490

4270

10320

0

10300

20

0.19

European Union

In European Union which is one the major producers of Rapeseed, the production is likely to remain almost the

same or a little lower compared to 2015 output. While the crop from Germany and France is likely to remain

stable, there is uncertainty looming over the crop from Britain and Poland. Prolonged dryness and

non-remunerative prices have taken a heavy toll on the crop prospects in EU. The shrinkage in cropping area

by 5,00,000 hectares is period of five years is a serious concern for the industry.

Rapeseed/Mustard SeedCrop Survey & Analysis 2016

16 March, 2016th

11

2013-14 2014-15 2015-16(E)

Beginning StockProductionImportsTotal SupplyDomestic Uses (Incl crushing)ExportsTotal UseFinal Stocks

Source: EU Market Data, NB Research

Ukraine

The climatic conditions are neutral for winter crops and it is expected that any significant increase of winterkill

is unlikely. In some regions the rapeseed crop requires favourable climate to recover from the brink of crop loss.

However, in the next few days, the climatic conditions are expected to show considerable improvement

Canada

The canola production is estimated to be 14.4 million tonnes in 2015, down 11.6% from 2014, as per the

government estimates. The lower harvested yields and decrease in the total acreage has resulted in the

decrease of total output of canola. Estimated average yields for 2015 are down 7.2% from 2014 to 32.6 bushels

per acre. Anticipated harvested acreage will be down 4.9% in 2015, which is another factor in the decrease in

the production estimate.

Global Outlook

At the global front, the rapeseed production scenario is bleak altogether. Non-remunerative prices of rapeseed

are likely to make it a less preferred crop amongst the farming community in China. Also, the acreage of

soybean is increasing in non-traditional regions lying in close proximity to the conventional areas in America.

Though rapeseed cultivation is expanding in few regions of Ukraine and EU, the climatic conditions do not

necessarily turn out to be favourable. The rapeseed future is likely to outperform that of soybean as the

production deficit is likely to provide a fillip to the prices. However, the enormous production of soybean and

the demand for soy derivatives is likely to cap the uptrend in rapeseed futures. Altogether, the oilseeds market

has been marred by the presence of humungous stockpiles of soybean and the enduring demand for the same.

Notwithstanding all the facts and figures, the Chinese appetite for oilmeals never ceases. With China giving

more emphasis to the hog market this year, it will definitely continue to reign as the top importer of oilseeds.

PRICE OUTLOOK

According to the outcome of the survey, NBCR expects the production of rapeseed to be higher than that of

the previous year, but we express our concerns regarding the oil content of the rapeseed/mustard seed. It is

quite possible that the oil content may fall in the range of 36-38% across the crops in various regions of the

country, rather than being in the optimal level of 42-45%. Shortage of water and unfavorable climatic

conditions are to be considered to be the prime reason for the same. Hence, even if the output seems better

than previous season, the oil yield is likely to be affected.

Due to the aforementioned reasons, NBCR expects the commodity to be moderately bullish and trade at

NCDEX in the range of ` 3850 - ` 4100 in the near term. A major downside is not expected due to the

sustained demand for edible oils. However, we expect the prices to ease to the levels of ` 3600 in the months

of March and April, which are the months of peak arrival. After the arrival pressure subsides, the market can

witness a price rally, and we may see rapeseed futures at NCDEX to trade at around ` 4500 within the months

of June-July 2016. So we recommend initiating a long position in NCDEX RM Seed futures contract at ` 3650 -

` 3750 with a target of `4450 - ` 4500.

Rapeseed/Mustard SeedCrop Survey & Analysis 2016

16 March, 2016th

12

COMMODITY & CURRENCY RESEARCH TEAM

Name Designation E-mail

Kunal Shah Research Head [email protected]

Devidas Rajadhikary Sr. Research Analyst [email protected]

Harshal Mehta Sr. Research Analyst [email protected]

Mohammed Azeem Research Analyst [email protected]

Ravi D'souza Research Analyst [email protected]

Nikhil Murali Research Associate [email protected]

Anish G Research Associate [email protected]

Smit Bhayani Research Associate [email protected]

This Document has been prepared by N.B. Commodity Research (A Division of Nirmal Bang Commodities Pvt. Ltd). The information, analysis

and estimates contained herein are based on N.B. Commodities Research assessment and have been obtained from sources believed to be

reliable. This document is meant for the use of the intended recipient only. This document, at best, represents N.B. Commodities Research

responsible for the contents stated herein. N.B. Commodities Research expressly disclaims any and all liabilities that may arise from

company mentioned in this document.

Address: Nirmal Bang Commodities Pvt. Ltd., B2, 301 / 302, 3rd Floor, Marathon Innova, Opp. Peninsula Corporate Park, Ganpatrao Kadam

Marg, Lower Parel (W), Mumbai - 400 013, India

Disclaimer

Rapeseed/Mustard SeedCrop Survey & Analysis 2016

16 March, 2016th

13