q1 2003 results, may 8, 2003 - hugin onlinereports.huginonline.com/902758/117509.pdf · jun.92...

TRANSCRIPT

Q1 2003 results,

May 8, 2003

1

•Introduction

•Market update – outlook

•Corporate financial status

•Other

Agenda

2

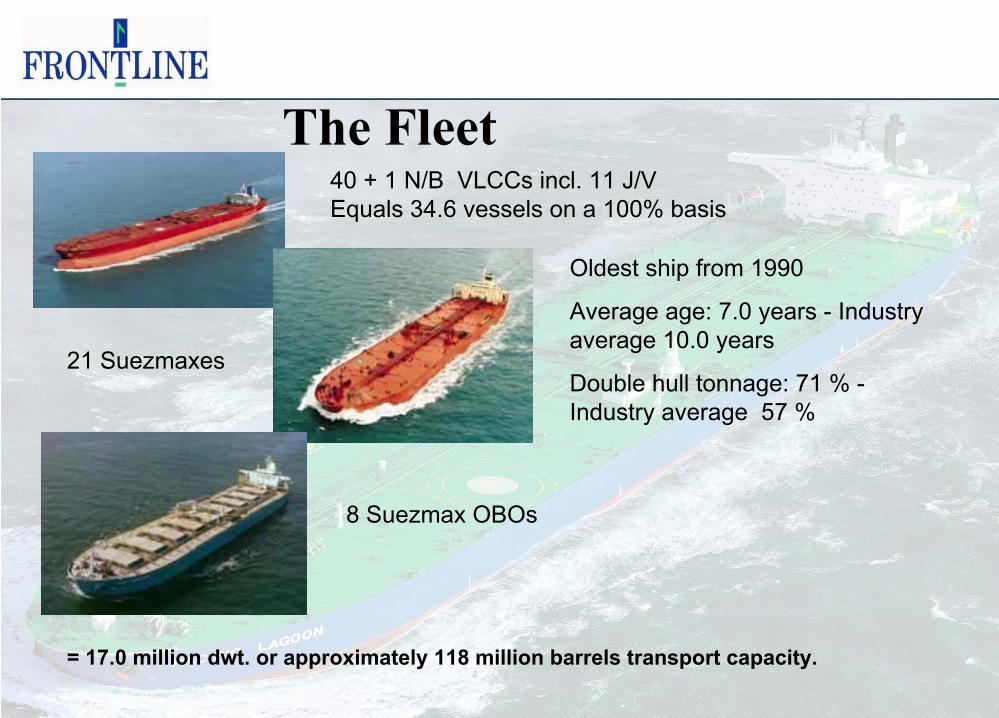

Oldest ship from 1990

Average age: 7.0 years - Industryaverage 10.0 years

Double hull tonnage: 71 % -Industry average 57 %

40 + 1 N/B VLCCs incl. 11 J/V Equals 34.6 vessels on a 100% basis

21 Suezmaxes

8 Suezmax OBOs

= 17.0 million dwt. or approximately 118 million barrels transport capacity.

The Fleet

Main events Q1 2003

4

•Frontline aquired the suezmax tankers Polytrader and Polytraveller,which were owned by Joint Ventures with Rasmussen in which Frontline had 40% and 35% respectively. The vessels weresubsequently sold in March 2003, with delivery of the second vessel taking place in April 2003,

•Frontline aquired 250,000 shares under the ESL with Nova Scotia, and as at March, 31 2003 a total of 2,945,000 shares are acquired pursuant to the existing Equity Swap Line facility at an average cost of $8.91 per share,

•A dividend of $0.15 per share paid out in late March

•$29.3 million in prepayment of debt in excess of scheduled repayments. Same for associated companies - $20.0 million (100% basis)

•The Board has adopted a strategy whereby the Company will seek to have a normalized future quarterly dividend target of $ 0.25 per share or $1.00 total per share per year which corresponds to a yield of 8.7 per cent based on current share price.

•In addition to the normalized quarterly dividend, each quarter the Board will evaluate how to utilize any potential earnings achieved in excess of the dividend break even level. Such earnings may be retained in the Company to strengthen the balance sheet, they may be used for capital investments, for repurchase of shares or paid out as additional dividend. The decision will be taken based on existing market conditions at the time, and will also take into consideration the need to have a large enough cash position to secure future ordinary dividends.

Dividend policy – “New deal”

5

Of whichVLCC's ULCC's*) Suezmaxes

Building year 200,000+ dw t 320,000 + dw t 120,000-200,000 dw t

1973 or earlier 2 01974-75 9 1 101976-77 26 9 141978-80 11 8 161981 or later 392 4 249Fleet as at May 7, 2003 440 22 289

On order2003 26 1 232004 28 24

2005+ 21 11Total on order 2003-2006 75 1 58

*) Each ULCC representing an average of 400,000 Dwt

Source: P.F.Bassøe

Supply VLCC’s / Suezmaxes(No. of vessels)

6

VLCC N/B, SH prices, parity and ratio

7

20,0

30,0

40,0

50,0

60,0

70,0

80,0

90,0

100,0

110,0

120,0

1990 1992 1994 1996 1998 2000 200250,0 %

55,0 %

60,0 %

65,0 %

70,0 %

75,0 %

80,0 %

85,0 %

90,0 %

95,0 %

100,0 %

Newbuilding (l.s.) 5 year old (l.s.) SH/NB ratio (r.s.) SH/NB parity

Trends in tanker valuesUSDm

Source: Bassøe, Clarkson, May 2, 2003

The macro trend

8

•A lower oil price, low inventories and increased focus on Middle East production after the Iraq war gives comfort on the demand side,

•The supply side is supported by the fact that, even in the current weak market, there is no material excess supply of ships and that very limited waiting time is being experienced on modern tonnage,

•Anticipated introduction of new EU legislation for tankers from July 1st 2003,

•Current acceleration of scrapping,

•Political unrest in several short haul production areas can create significant upside in the market

•Start up of nuclear power plant closures in Japan which requires substitution with fossil fuel for power generation have been delayed,

•High Natural gas prices

•Nigeria and Venezuela still not back to full production

Estimated oil demand/supply 2003

Avg. 02 Q103 Q203 Q303 Q403 Avg. 03

Demand* 76,9 78,8 76,6 77,5 79,5 78,1

Supply* 76,3 78,5 77,6 77,9 78,9 78,1

*)Based on JP Morgan estimates as of May 7, 2003

9

Oil production

10

Change 2000 2001 2002 2003 2000 - 2003

Canada 2,68 2,74 2,87 2,99 0,31Mexico 3,45 3,56 3,59 3,70 0,25USA 8,11 8,05 8,11 8,06Argentina 0,82 0,82 0,80 0,77Brazil 1,50 1,58 1,71 1,79 0,29Colombia 0,71 0,63 0,59 0,55 -0,16Ecuador 0,41 0,42 0,39 0,39Denmark 0,37 0,35 0,37 0,36Norway 3,35 3,42 3,33 3,26 -0,09UK 2,60 2,45 2,44 2,32 -0,28Oman 0,96 0,96 0,90 0,85Syria 0,54 0,55 0,55 0,54Yemen 0,54 0,46 0,46 0,46Australia 0,82 0,73 0,73 0,69 -0,13Brunei 0,20 0,20 0,19 0,19China 3,25 3,31 3,40 3,40 0,15India 0,79 0,78 0,76 0,76Malaysia 0,81 0,79 0,80 0,82Vietnam 0,32 0,35 0,32 0,30Angola 0,75 0,73 0,90 0,89 0,14Egypt 0,80 0,76 0,73 0,72Gabon 0,33 0,30 0,29 0,29Total 34,11 33,94 34,23 34,10

Other / smaller prod 2,43 2,48 2,53Refinery proc gain 1,76 1,79 1,83

Non OPEC supply ex FSU 38,13 38,50 38,46

Source: JPMorgan May 7, 2003

Oil production

11

Change 2000 2001 2002 2003 2000 - 2003

Russia 6,54 7,05 7,65 8,13 1,59Kazakhstan 0,75 0,83 0,95 1,04 0,29Other FSU 0,75 0,77 0,80 0,82FSU 8,04 8,65 9,40 9,99

OPEC NGL / Condensate 2,90 3,00 3,2Call on OPEC crude 26,80 25,90 26,4Stockbuild 0,40 -0,50 0,1OPEC crude 27,20 25,40 26,50

Source: JPMorgan May 7, 2003

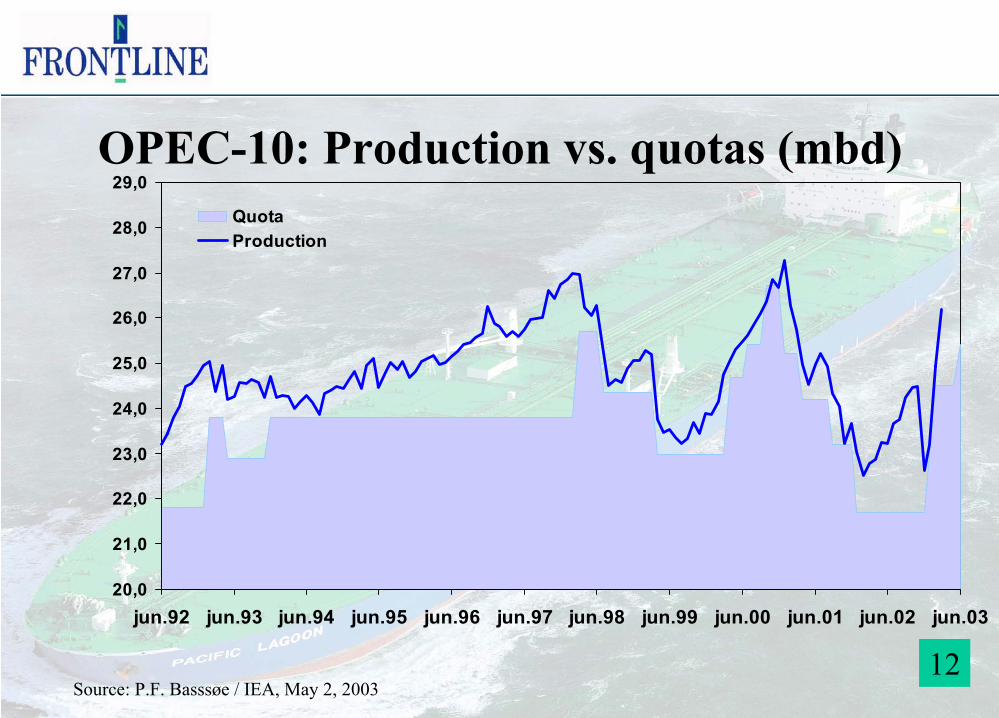

OPEC-10: Production vs. quotas (mbd)

12Source: P.F. Basssøe / IEA, May 2, 2003

20,0

21,0

22,0

23,0

24,0

25,0

26,0

27,0

28,0

29,0

jun.92 jun.93 jun.94 jun.95 jun.96 jun.97 jun.98 jun.99 jun.00 jun.01 jun.02 jun.03

QuotaProduction

13Source: RS Platou

14Source: RS Platou

Oil inventories, OECD and US, mb

15Source. P.F. Bassøe / IEA / DOE May 2, 2003

2 300

2 400

2 500

2 600

2 700

2 800

2 900

Jan Mar Mai Jul Sep Nov

Commercial inventories, OECD

850

900

950

1 000

1 050

1 100

1 150

Jan Mar Mai Jul Sep Nov

Commercial inventories, US

5-year high range

5-year low range

2002

2003

5-year high range

5-year low range

2002

2003

mblmbl

Oil inventories, Europe and Asia, mbCommercial inventories, OECD Europe Commercial inventories, OECD Asia

16Source. P.F. Bassøe / IEA / Euroilstock May 2, 2003

840

860

880

900

920

940

960

980

1 000

1 020

1 040

1 060

Jan Mar Mai Jul Sep Nov380390400410420430440450460470480490500510520530

Jan Mar Mai Jul Sep Nov

5-year high range

5-year low range

2002

2003

5-year high range

5-year low range

2002

2003

mblmbl

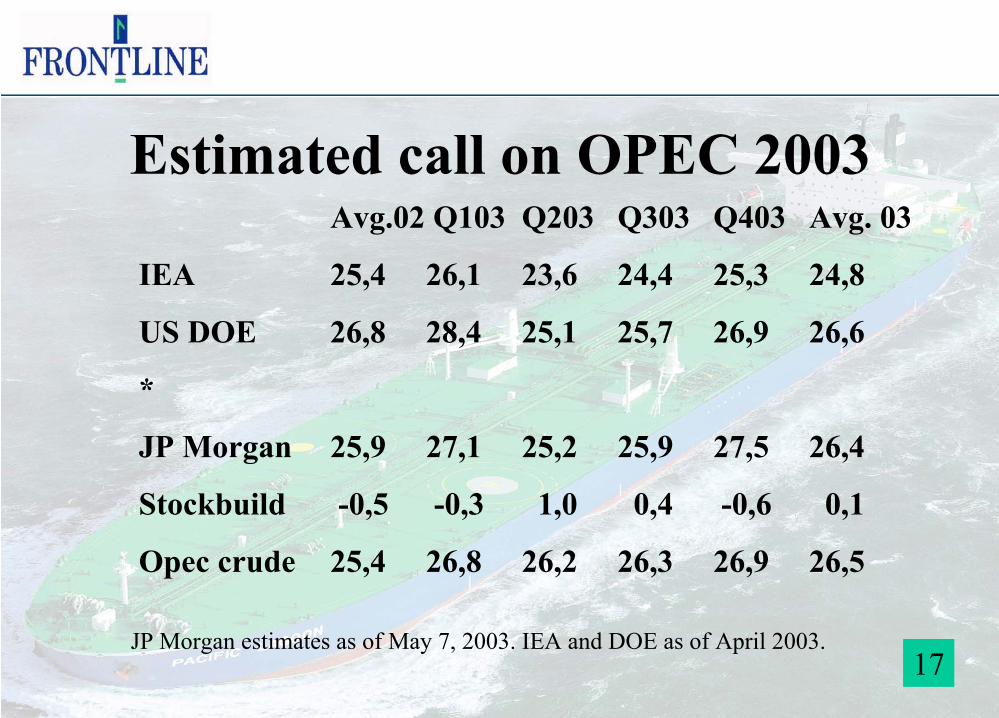

Avg.02 Q103 Q203 Q303 Q403 Avg. 03

IEA 25,4 26,1 23,6 24,4 25,3 24,8

US DOE 26,8 28,4 25,1 25,7 26,9 26,6

*

JP Morgan 25,9 27,1 25,2 25,9 27,5 26,4

Stockbuild -0,5 -0,3 1,0 0,4 -0,6 0,1

Opec crude 25,4 26,8 26,2 26,3 26,9 26,5

JP Morgan estimates as of May 7, 2003. IEA and DOE as of April 2003.

Estimated call on OPEC 2003

17

Oil production, Opec-10 and Iraq

18

20,0

22,0

24,0

26,0

28,0

30,0

32,0

jan.98 jul.98 jan.99 jul.99 jan.00 jul.00 jan.01 jul.01 jan.02 jul.02 jan.03 jul.03

Iraq (r.s.)Opec-10 (l. s.)

Estimate JPMorgan from Apr. 03

Source: P.F. Bassøe / IEA JPMorgan May 2, 2003

mbl

WTI-Brent Blend / Natural Gas

19

OILW TX2-OILBRNT 6/5/03

1998 1999 2000 2001 2002-0.50

0

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

OILWTX2-OILBRNT(P)

HIGH 4.08 10/3/03, LOW -0.14 21/1/02, LAST 2.17 5/5/03 Source: DATASTREAM

Natural Gas, Henry Hub $/MMBTUFROM 4/5/98 TO 5/5/03 WEEKLY

1998 1999 2000 2001 2002 20030

2

4

6

8

10

12

14

HIGH 12.2000 24/ 2/03 LOW 1.5750 7/12/98 LAST 5.2300Source: DATASTREAM

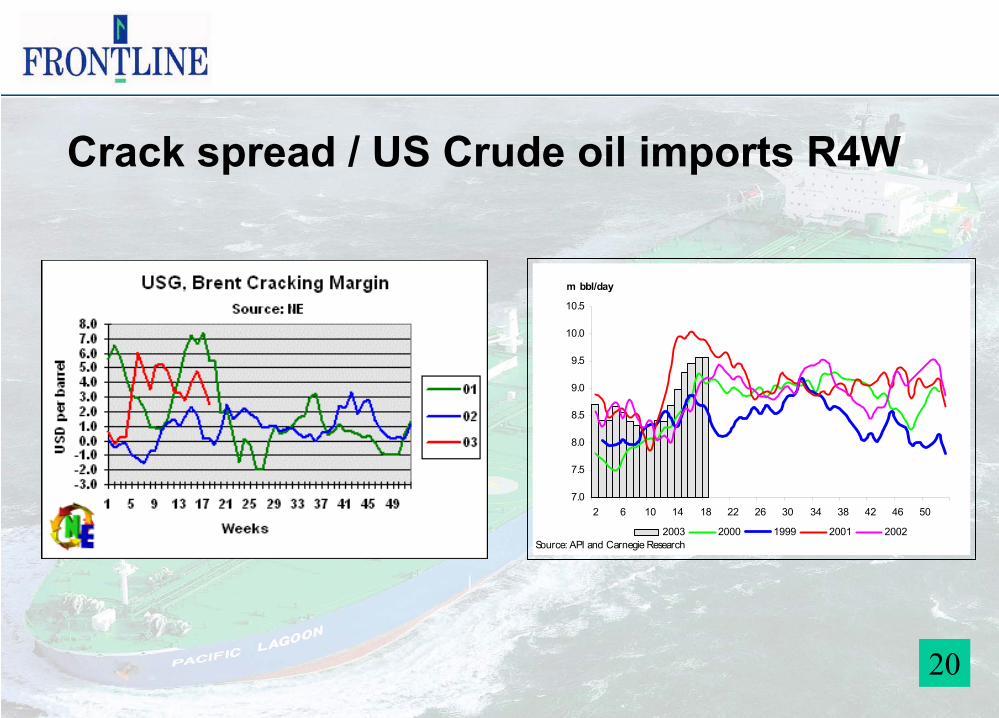

Crack spread / US Crude oil imports R4W

20

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

2 6 10 14 18 22 26 30 34 38 42 46 50

m bbl/day

2003 2000 1999 2001 2002Source: API and Carnegie Research

Correlation between production and VLCC rates

21Source: R.S. Platou

Profit & Loss

22

USD million Q1 03 Q1 02 2002

Net operating revenues 258,9 94,8 429,0Gain / loss on sale of vessels 0,5 0,0 -4,3Total expenses 53,7 39,0 187,1Operating profit before depreciation (EBITDA) 205,8 55,8 237,6Depreciation 36,2 34,0 139,9Operating profit (EBIT) 169,6 21,8 97,7Financial items 8,0 -7,8 -90,5Net profit (loss) before min. & taxes 177,6 14,0 7,2Taxes 0,0 0,0 0,0Cumulative effect of change in accounting principle - -14,1 -14,1Net profit (loss) 177,6 -0,1 -6,9

EPS before cumulative effect of change in accounting principle 2,32 0,18 0,09Cumulative effect of change in accounting principle - -0,18 -0,18EPS 2,32 - -0,09

Income on time charter basis

23

Q1 03 Q1 02 2002 2001

VLCC, spot , T/C and B/B vessels 55 400 21 600 22 500 40 800VLCC, spot 60 500 18 900 21 000 -VLCC, T/C and B/B vessels 35 600 28 300 27 900Suezmax 40 800 16 500 18 400 30 700Suezmax OBO 42 400 18 000 17 700 28 900

01000020000300004000050000600007000080000

Q197

Q2 Q3 Q4 Q198

Q2 Q3 Q4 Q199

Q2 Q3 Q4 Q100

Q2 Q3 Q4 Q101

Q2 Q3 Q4 Q102

Q2 Q3 Q4 Q103

USD

per d

ay

Ship operating expenses (USD/day)

24

Q1 03 2002 2001 2000 1999

VLCC 5 632 6 311 6 339 6 940 6 828Suezmax 5 138 5 597 5 706 5 476 5 976Suezmax OBO 5 473 5 711 8 996 6 246 6 385Drybulk 2 763 4 053

No. of vessels drydocked or expected to be

012345678

Q101

Q201

Q301

Q401

Q102

Q202

Q302

Q402

Q103

Q203

Q303

Q403

Ship operating expenses

0

2 000

4 000

6 000

8 000

10 000

12 000

Q199

Q299

Q399

Q499

Q100

Q200

Q300

Q400

Q101

Q201

Q301

Q401

Q102

Q202

Q302

Q402

Q103

VLCC Suezmax Suezmax OBO

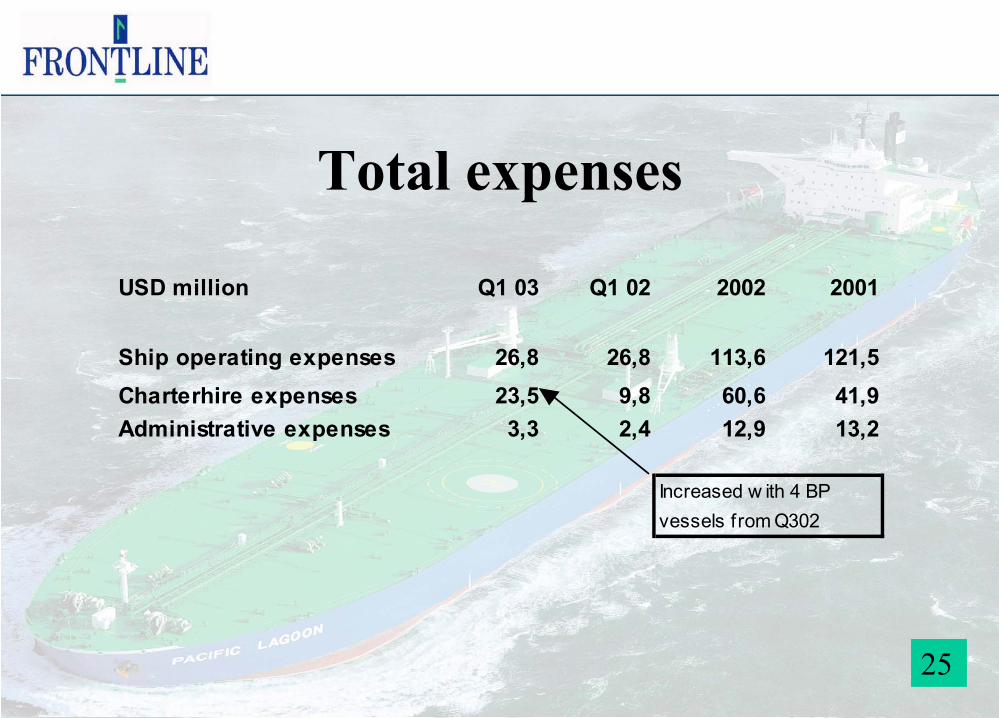

Total expenses

25

USD million Q1 03 Q1 02 2002 2001

Ship operating expenses 26,8 26,8 113,6 121,5Charterhire expenses 23,5 9,8 60,6 41,9Administrative expenses 3,3 2,4 12,9 13,2

Increased w ith 4 BPvessels from Q302

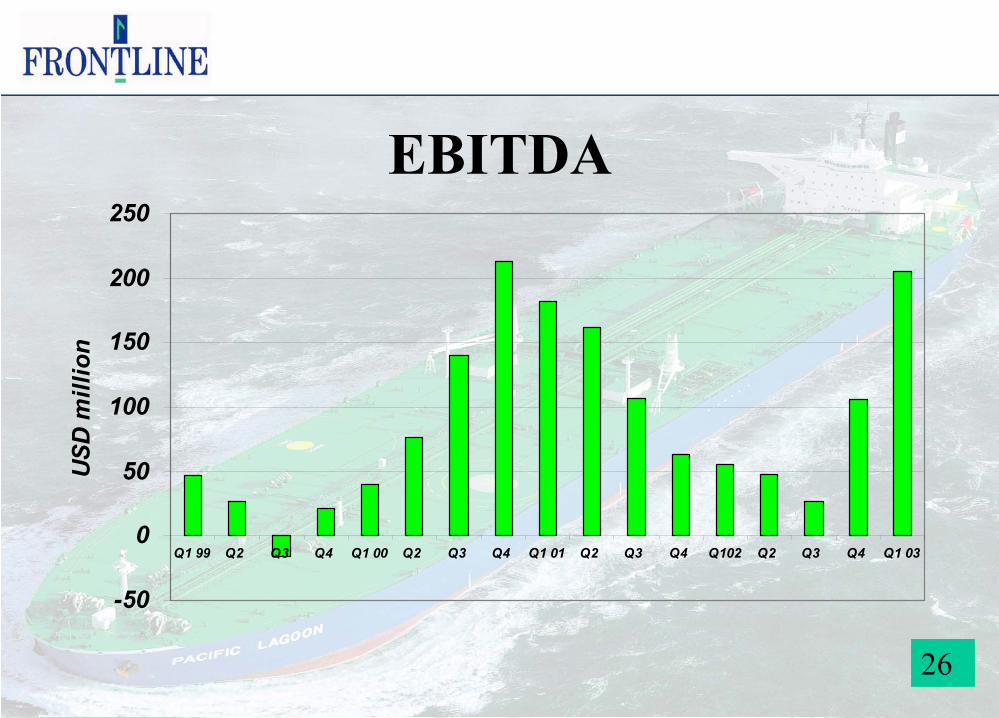

EBITDA

26

-50

0

50

100

150

200

250

Q1 99 Q2 Q3 Q4 Q1 00 Q2 Q3 Q4 Q1 01 Q2 Q3 Q4 Q102 Q2 Q3 Q4 Q1 03

USD

mill

ion

Financial items

27

USD million Q1 03 Q1 02 2 002

Net operating revenues 258,9 94,8 429,0Gain / loss on sale of vessels 0,5 0,0 -4,3Total expenses 53,6 39,0 187,1Operating profit before depreciation (EBITDA) 205,8 55,8 237,6Depreciation 36,2 34,0 139,9Operating profit (EBIT) 169,6 21,8 97,7Financial items 8,0 -7,8 -90,5Net profit (loss) before min. & taxes 177,6 14,0 7,2Taxes 0,0 0,0 0,0Cumulative effect of change in accounting principle 0,0 -14,1 -14,1Net profit (loss) 177,6 -0,1 -6,9

Interest income 2,7 2,5 13,1Interest expense -17,8 -17,7 -72,9Share of result in assoc 17,2 1,0 -10,7Other financial items 4,9 5,7 -6,6Foreign currency gain / loss 1,0 0,7 -13,3

Balance sheet - Assets

28

USD million Q1 03 Q1 02 2002

Short termCash and Bank deposits 149,4 81,6 100,3Other current assets 188,3 94,9 133,1

Long termNewbuildings 35,0 62,1 27,4Vessels and equipment, net 2 605,1 2 623,1 2 638,1Associated companies 136,7 116,6 119,3Goodwill - - -Deferred charges and other assets 18,4 16,5 17,7Total assets 3 132,9 2 994,8 3 035,9

Front Hawk 26.6 Oscilla 8.4

Trade rec./Voyages in progress 127.2Prepayment/inventory 44.6Other 16.4

29

0,0

50,0

100,0

150,0

200,0

250,0

300,0

Q199

Q299

Q399

Q499

Q100

Q200

Q300

Q400

Q101

Q201

Q301

Q401

Q102

Q202

Q302

Q402

Q103

Quarter

$mill

ion

Net working capital (excl. Cash) Net working capital (incl. Cash)Average net working capital Cash

Net working capital development

Associated companies

30

As at 31.03.03Debt

outstandingOur

shareGuarantee

liability

Our share of cash and net working capital

•Front Tobago (40%) partners OSG and Euronav 10,1 4,1 2,4 2,8•Ariake (33%), partners OSG and Euronav 45,8 15,3 4,2 2,1•Sakura (33%), partners OSG and Euronav 45,8 15,3 4,2 2,2•Ichiban (33%), partners OSG and Euronav 43,6 14,5 4,8 2,0•Tanabe (33%), partners OSG and Euronav 46,0 15,3 5,1 1,4•Hakata (33%), partners OSG and Euronav 48,3 16,1 5,4 2,0•Edinburgh (50,1%), partner OSG 23,6 11,8 3,5 2,4•Dundee (50,1%), partner OSG 23,6 11,8 3,5 2,4•Golden Fountain (50%) partner Euronav 29,3 14,6 29,3 3,7•New Circassia (50%) partners Ropner and Runciman 53,3 26,6 53,3 4,7•Pacific Lagoon (50%) partner Euronav 52,8 26,4 52,8 3,4

Total = 422,2 171,9 168,5 29,2

Yen denominated debt 116,7Our share 58,3

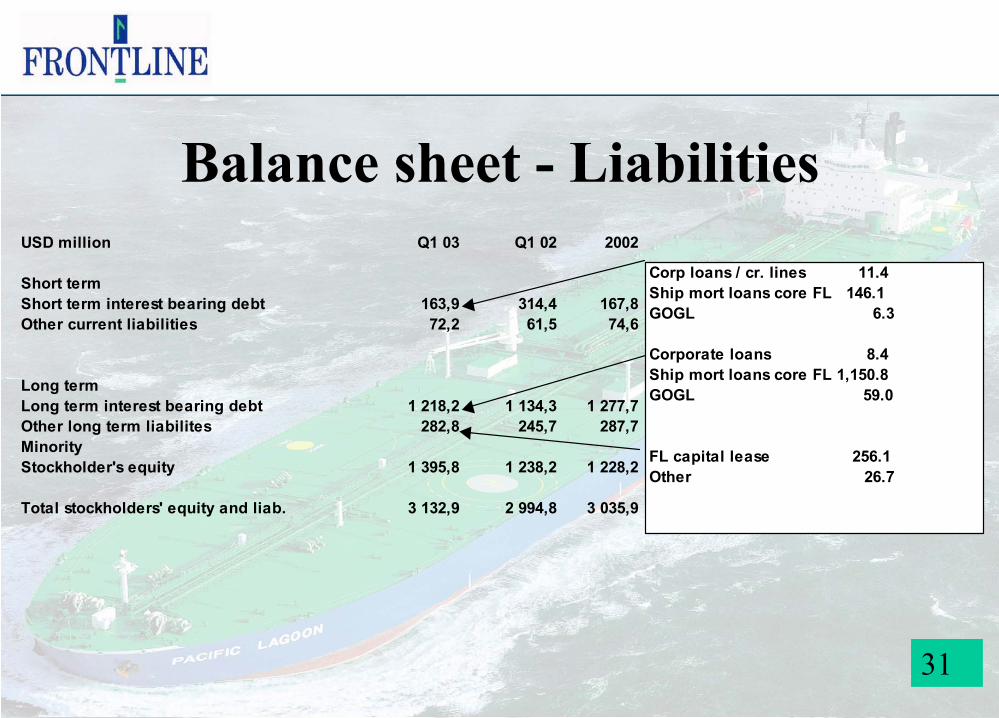

Balance sheet - Liabilities

31

USD million Q1 03 Q1 02 2002

Short termShort term interest bearing debt 163,9 314,4 167,8Other current liabilities 72,2 61,5 74,6

Long termLong term interest bearing debt 1 218,2 1 134,3 1 277,7Other long term liabilites 282,8 245,7 287,7MinorityStockholder's equity 1 395,8 1 238,2 1 228,2

Total stockholders' equity and liab. 3 132,9 2 994,8 3 035,9

Corp loans / cr. lines 11.4Ship mort loans core FL 146.1GOGL 6.3

Corporate loans 8.4Ship mort loans core FL 1,150.8GOGL 59.0

FL capital lease 256.1Other 26.7

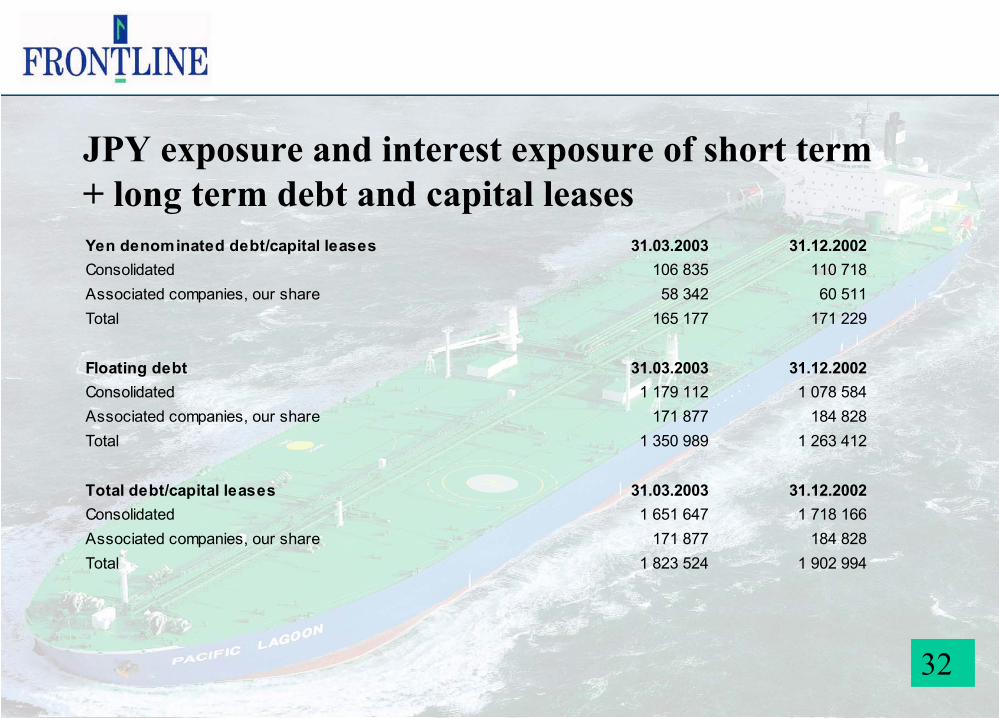

JPY exposure and interest exposure of short term + long term debt and capital leases

32

Yen denominated debt/capital leases 31.03.2003 31.12.2002Consolidated 106 835 110 718Associated companies, our share 58 342 60 511Total 165 177 171 229

Floating debt 31.03.2003 31.12.2002Consolidated 1 179 112 1 078 584Associated companies, our share 171 877 184 828Total 1 350 989 1 263 412

Total debt/capital leases 31.03.2003 31.12.2002Consolidated 1 651 647 1 718 166Associated companies, our share 171 877 184 828Total 1 823 524 1 902 994

Off balance sheet vessels

•Front Century

•Front Champion

•Front Warrior

•Golden Victory

33

Remaining N/B commitments

34

Q3 03Gross cap. ex 52Bank loan 47Equity financing 5

Statement of Cashflows

35

STATEMENT O F CASHFLO WS 2003 2002 2002

(in thousands of $) Jan-Mar Jan-Mar Jan-Dec

(restated)O PERATING ACTIVITIES

Net income (loss) 177,61 -112 -6,931

Adjustments to reconcile net income to net cash provided by operating activit ies

Depreciation and amortisation 36,638 34,086 142,149

Unrealised foreign currency exchange (gain) loss -1,258 -1,685 14,176

Gain or loss on sale of assets -493 - 4,337

Results from associated companies -17,165 -986 10,711

Change in accounting principle - 14,142 14,142

Adjustment of financial derivatives to market value -6,16 -5,116 7,495

Other 1,131 - -Change in operating assets and liabilities -53,379 -11,112 -34,816

Net cash provided by operating activities 136,924 29,217 151,263

INVESTING ACTIVITIES

Additions to newbuildings, vessels and equipment -14,314 -118,542 -376,844

Advances to associated companies, net 269 -5,541 -20,01

Purchase of minority interest - -5,652 -6,822

Proceeds from sale of assets 3,943 10,5 177,902

Net cash used in investing activities -10,102 -119,235 -225,774

FINANCING ACTIVITIES

Proceeds from long-term debt, net of fees paid -1,077 123,177 370,88

Repayments of long-term debt -62,103 -66,153 -341,784

Repayment of capital leases -3,156 -59,626 -24,671

Dividends paid -11,471 -15,294 -19,116

Issue of shares, net 52 223 223

Net cash used in financing activities -77,755 -17,673 -14,468

Net decrease in cash and cash equivalents 49,067 -107,691 -88,979

Cash and cash equivalents at start of period 100,298 189,277 189,277

Cash and cash equivalents at end of period 149,365 81,586 100,298

Breakeven rates (USD / day)

36

Cash Breakeven P/L Breakeven

VLCC 20 727 19 998Suezmax 13 545 12 440Suezmax OBO 13 351 13 666

Breakeven requirements are very low

37Source TCE: Clarksons

Average TCE VLCC’s in the period 1990 – May 2, 2003 is USD 29,355 per day, as compared to P&L B/E May 2003 of USD 19,998 per day and cash B/E of USD 20,727 per day.

VLCC TCE versus Cash Breakeven

0,00010,00020,00030,00040,00050,00060,00070,00080,00090,000

100,000

jan-

90

jan-

91

jan-

92

jan-

93

jan-

94

jan-

95

jan-

96

jan-

97

jan-

98

jan-

99

jan-

00

jan-

01

jan-

02

jan-

03

USD

/day

VLCC TCE Cash Breakeven May 2003 Average TCE in the period

Breakeven requirements are very low

38Source TCE: Clarksons

Average TCE Suezmax in the period 1990 – May 2, 2003 is USD 21,552 per day, as compared to P&L B/E May 2003 of USD 12,440 per day and cash B/E of USD 13,545 per day.

Suezmax TCE versus Cash Breakeven

0,000

10,00020,000

30,00040,000

50,000

60,00070,000

80,000

jan-

90

jan-

91

jan-

92

jan-

93

jan-

94

jan-

95

jan-

96

jan-

97

jan-

98

jan-

99

jan-

00

jan-

01

jan-

02

jan-

03

USD

/day

Suezmax TCE Cash Breakeven M ay 2003 Average TCE in the period

Appendixes

39

Income on time charter basis

40

USD'000s Q1 03 Q1 02 2 002 2 001

VLCC, spot 137 383 27 896 159 679 243 886VLCC, T/C and B/B vessels 20 896 17 015 57 889 -Suezmax 76 909 30 975 137 974 220 787Suezmax OBO 30 304 12 524 51 029 79 435

Trading days minus off hire Q1 03 Q1 02 2 002 2 001

VLCC, spot 2 271 1 477 7 586 5 973 VLCC, T/C and B/B vessels 587 602 2 078 -Suezmax 1 883 1 881 7 480 7 195Suezmax OBO 715 695 2 875 2 746

Newbuildings versus scrapping candidatesVL/ULCC fleet as of May 7, 2003

41Source: P.F. Bassøe

1 1 3 6

22

4 3 62 4 1 3 1 2

9 610

161318

26

39

19

2821

1113

32

41

26

37

16

26

28

1

20

05

1015202530354045

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

NO

. VS

LS

Order No. VslsFleet No. Vsls

Newbuildings versus scrapping candidates Suezmax fleet as of May 7, 2003

42Source: P.F. Bassøe

6 48 6 8

5 3 1 3 4 30 1

4 6

15

7

2227

139 8 9 11

2115

2317

23

23

24

10

10

5

10

15

20

25

30

3519

74

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

NO

VS

LS

Order No. VslsFleet No. Vsls

VLCC/ULCC fleet development

43Source: P.F. Bassøe

Change y/y Apr:+4,4%

Mill. dwt

116,0

118,0

120,0

122,0

124,0

126,0

128,0

130,0

132,0

134,0

136,0

apr.00 jul.00 okt.00 jan.01 apr.01 jul.01 okt.01 jan.02 apr.02 jul.02 okt.02 jan.03 apr.03

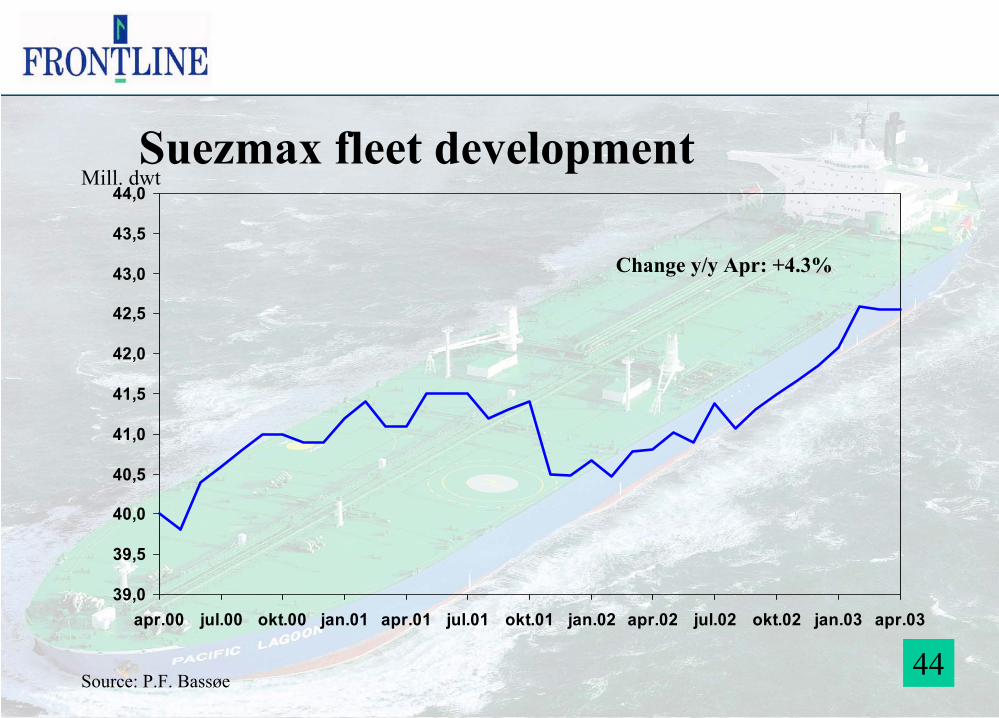

Suezmax fleet development

44Source: P.F. Bassøe

Change y/y Apr: +4.3%

Mill. dwt

39,0

39,5

40,0

40,5

41,0

41,5

42,0

42,5

43,0

43,5

44,0

apr.00 jul.00 okt.00 jan.01 apr.01 jul.01 okt.01 jan.02 apr.02 jul.02 okt.02 jan.03 apr.03