public disclosure authorizeddocuments.worldbank.org/curated/en/... · public disclosure authorized...

TRANSCRIPT

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

MICROFINANCEHANDBOOK

MICROFINANCEHANDBOOKAn Institutional and Financial Perspective

Joanna Ledgerwood

T H E W O R L D B A N K

W A S H I N G T O N , D . C .

SUSTAINABLE BANKING with the POOR

Copyright © 1999The International Bank for Reconstructionand Development/THE WORLD BANK1818 H Street, N.W.Washington, D.C. 20433, U.S.A.

All rights reservedManufactured in the United States of AmericaFirst printing December 1998Second printing July 1999Third printing July 2000

The findings, interpretations, and conclusions expressed in this paper are entirely those of theauthor and should not be attributed in any manner to the World Bank, to its affiliated organiza-tions, or to members of its Board of Executive Directors of the countries they represent. TheWorld Bank does not guarantee the accuracy of the data included in this publication and acceptsno responsibility for any consequence of their use.

The boundaries, colors, denominations, and other information shown on any map in this volumedo not imply on the part of the World Bank Group any judgment on the legal status of any terri-tory or the endorsement or acceptance of such boundaries.

The material in this publication is copyrighted. Requests for permission to reproduce portions ofit should be sent to the Office of the Publisher at the address shown in the copyright notice above.The World Bank encourages dissemination of its work and will normally give permission prompt-ly and, when the reproduction is for noncommercial purposes, without asking a fee. Permission tocopy portions for classroom use is granted through the Copyright Clearance Center, Inc., Suite910, 222 Rosewood Drive, Danvers, Massachusetts 01923, U.S.A.

Joanna Ledgerwood is consultant to the Sustainable Banking with the Poor Project, World Bank,for Micro Finance International, Toronto, Canada.

Library of Congress Cataloging-in-Publication Data

Ledgerwood, Joanna.Microfinance handbook: an institutional and financial perspective/Joanna Ledgerwood.p. cm.—(Sustainable banking with the poor)

Includes bibliographical references and index.ISBN 0-8213-4306-81. Microfinance. 2. Financial institutions. I. Title.

II. Series.HG178.2.L43 1998 98–21754332.1—dc21 CIP

Contents

Foreword xv

Preface xvi

Introduction 1

PART I—ISSUES TO CONSIDER WHEN PROVIDING MICROFINANCE 9

Chapter 1 Understanding the Country Context 11Suppliers of Financial Intermediation Services 12Existing Microfinance Providers 14What Role Do Donors Play in Microfinance? 16

Financial Sector Policies and Legal Enforcement 17Interest Rate Policies 18Government Mandates for Sectoral Credit Allocations 19Legal Enforcement of Financial Contracts 19

Financial Sector Regulation and Supervision 20When Should MFIs Be Subject to Regulation? 21Considerations When Regulating MFIs 23Country Approaches to Regulating MFIs 25

Economic and Social Policy Environment 26Economic and Political Stability 26Poverty Levels 28Investment in Infrastructure and Human Resource Development 28Government View of the Microenterprise Sector 29

Appendix 1. Risks in the Microfinance Industry 30Sources and Further Reading 31

Chapter 2 The Target Market and Impact Analysis 33Objectives of the Microfinance Institution 33Direct and Indirect Targeting 34The Importance of Adequate Cash Flow and the Capacity to Service Debt 35

v

vi C O N T E N T S

Minimal Equity Requirement 36Moral Hazard 36Market Size 36

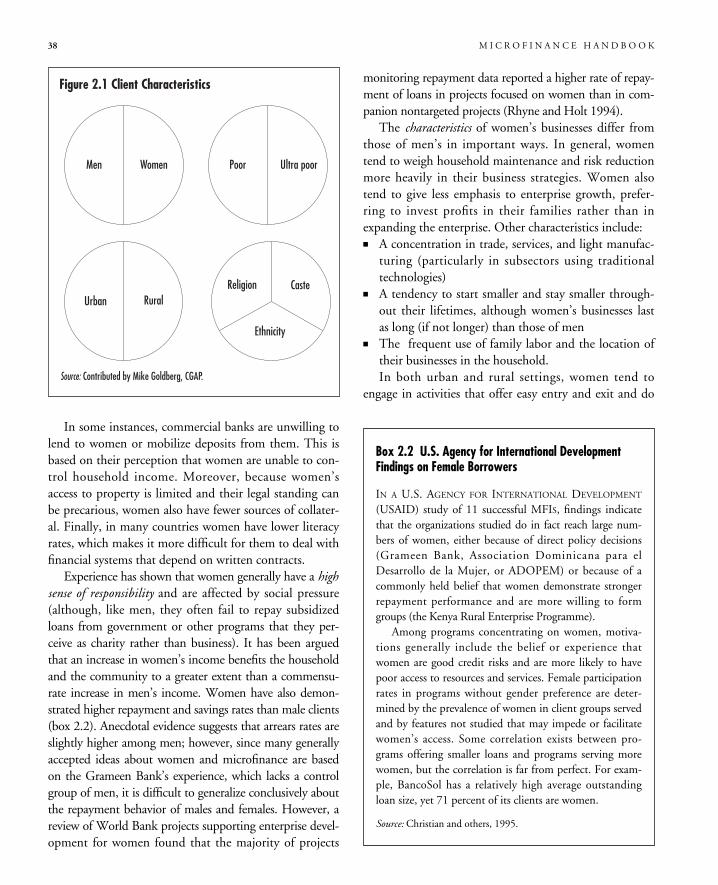

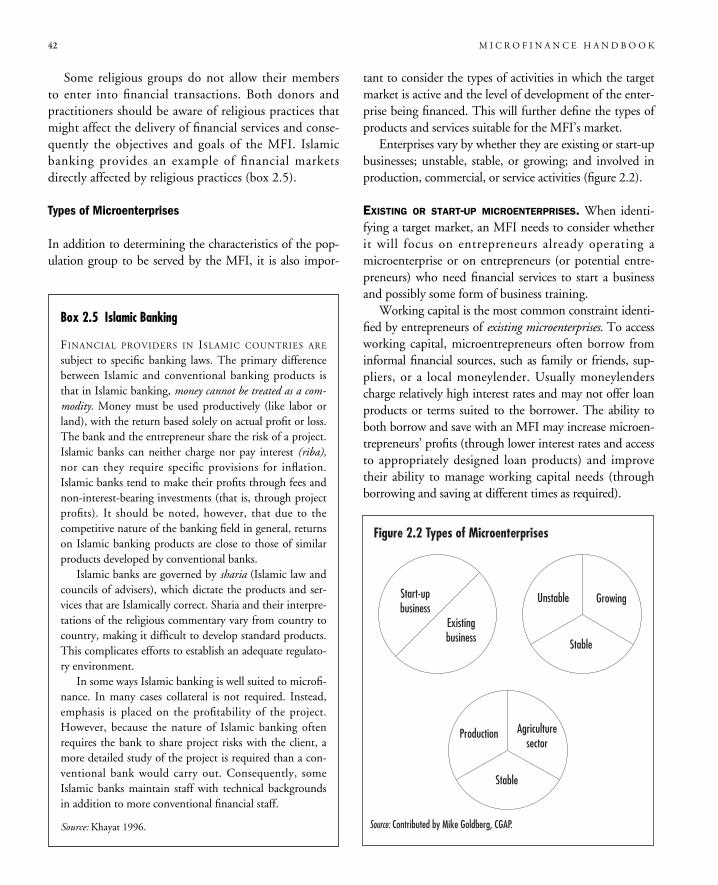

Identifying the Target Market 37Characteristics of the Population Group 37Types of Microenterprises 42

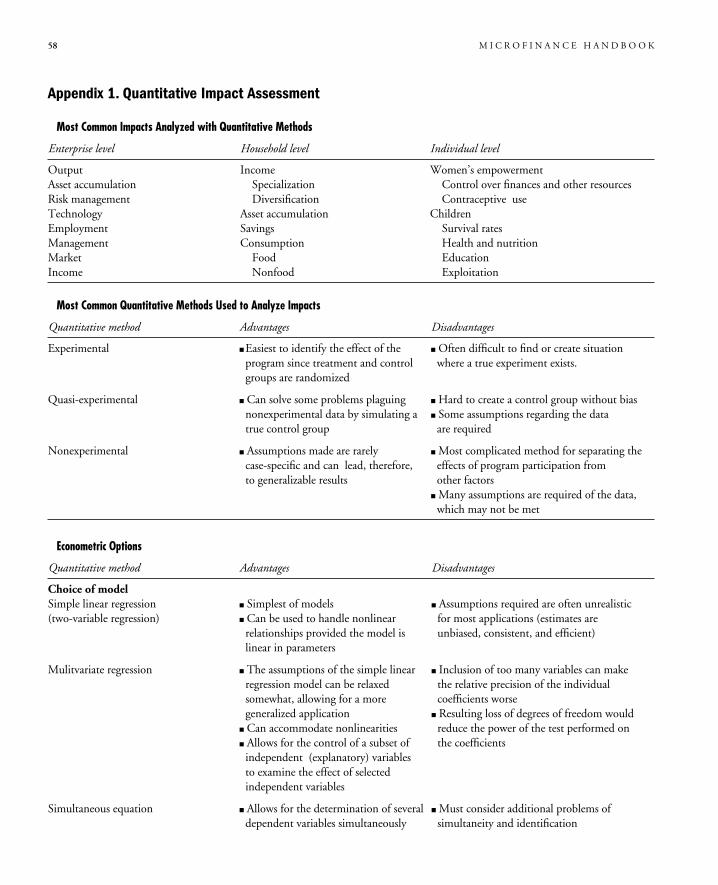

Impact Analysis 46Kinds of Impacts 47What Kinds of Impacts Have We Seen with Microfinance? 48Impact Proxies 49Client-Oriented Impact Analysis 49When Should Impact Be Assessed? 52Methods of Impact Assessment 53Fundamental Characteristics of Qualitative Approaches 53Fundamental Characteristics of Quantitative Approaches 54Comparisons of Quantitative and Qualitative Approaches 56Integrating Methodologies 56The Choice of Unit of Analysis 56

Appendix 1. Quantitative Impact Assessment 58Sources and Further Reading 59

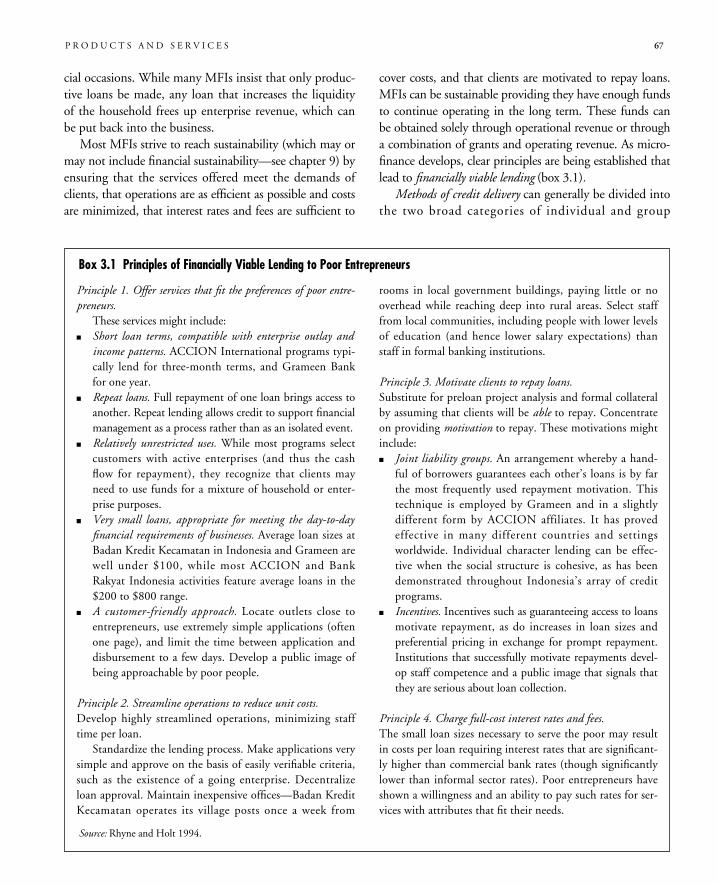

Chapter 3 Products and Services 63The Systems Framework 64Microfinance Institutions—Minimalist or Integrated? 65Financial Intermediation 66Credit 66Savings 71Insurance 74Credit Cards and Smart Cards 74Payment Services 75

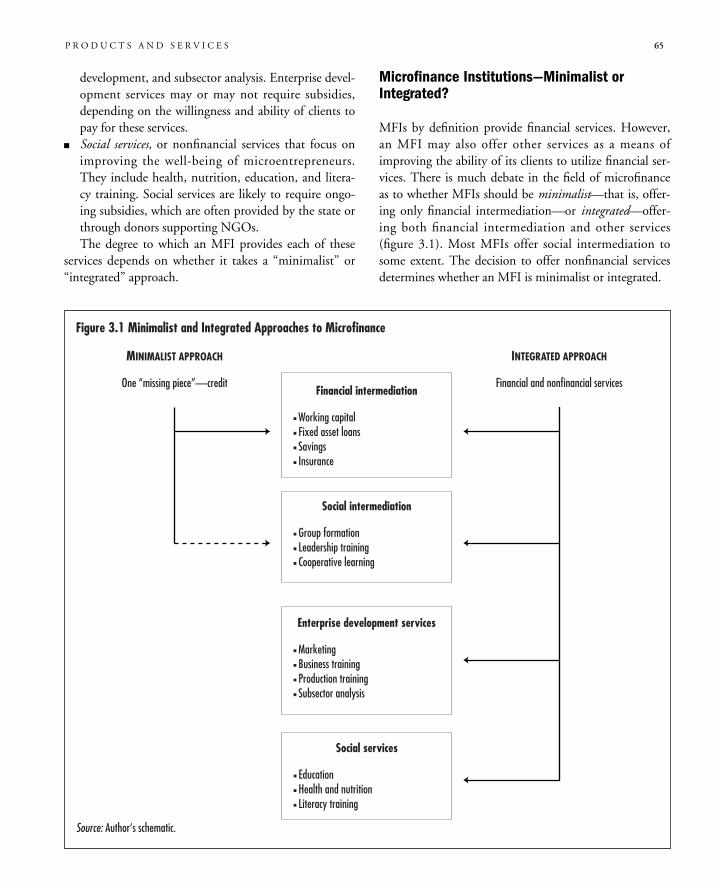

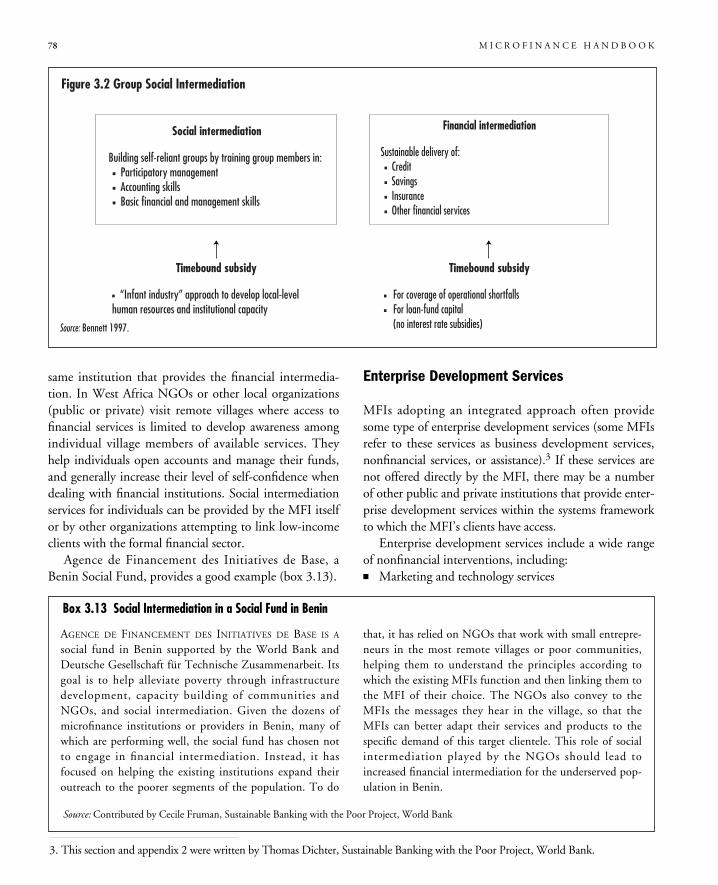

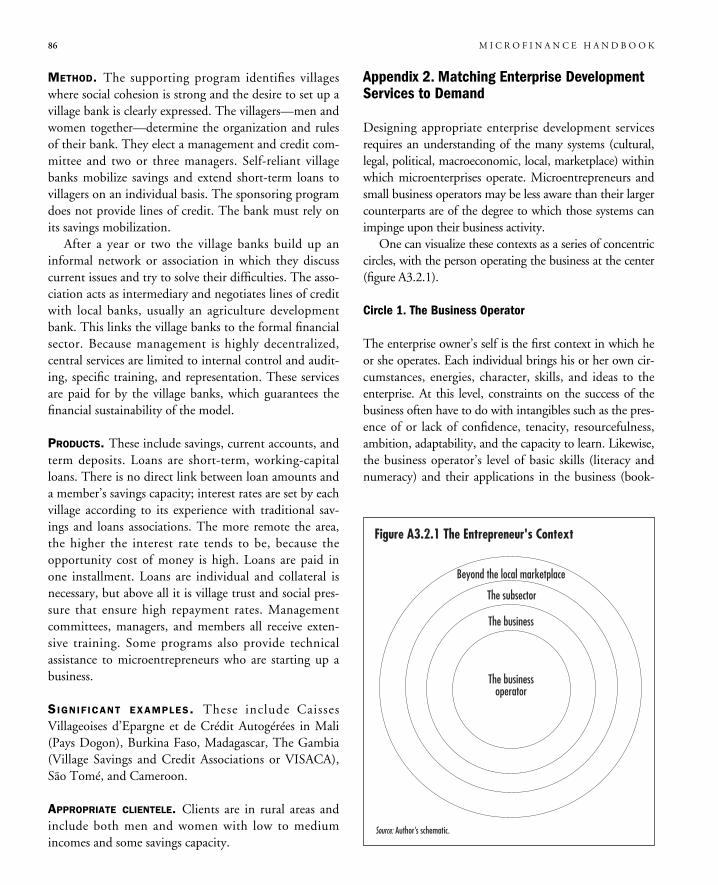

Social Intermediation 76Enterprise Development Services 78Social Services 81Appendix 1. Microfinance Approaches 82Appendix 2. Matching Enterprise Development Services to Demand 86Sources and Further Reading 90

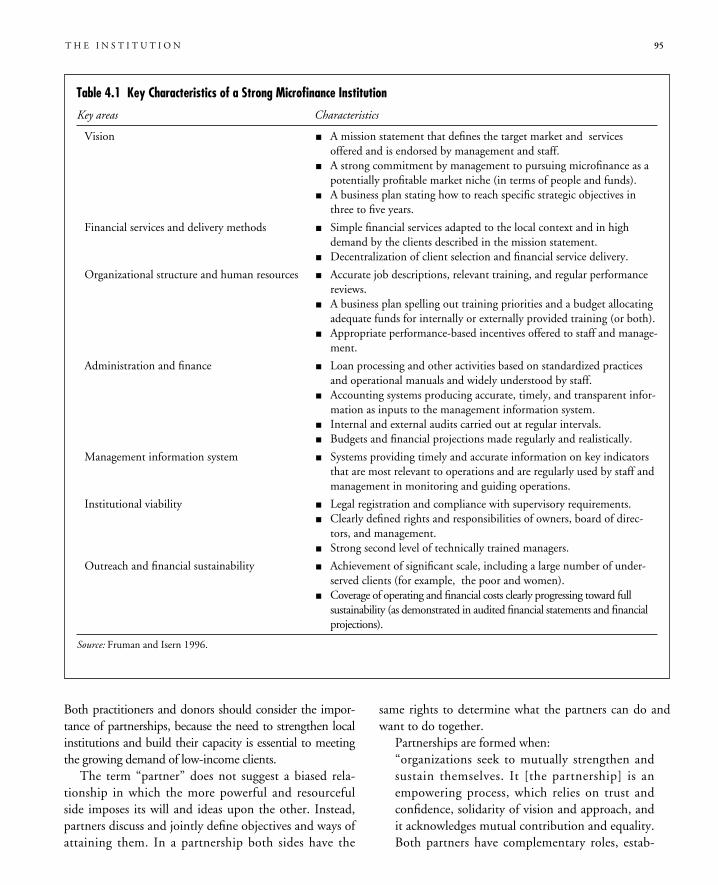

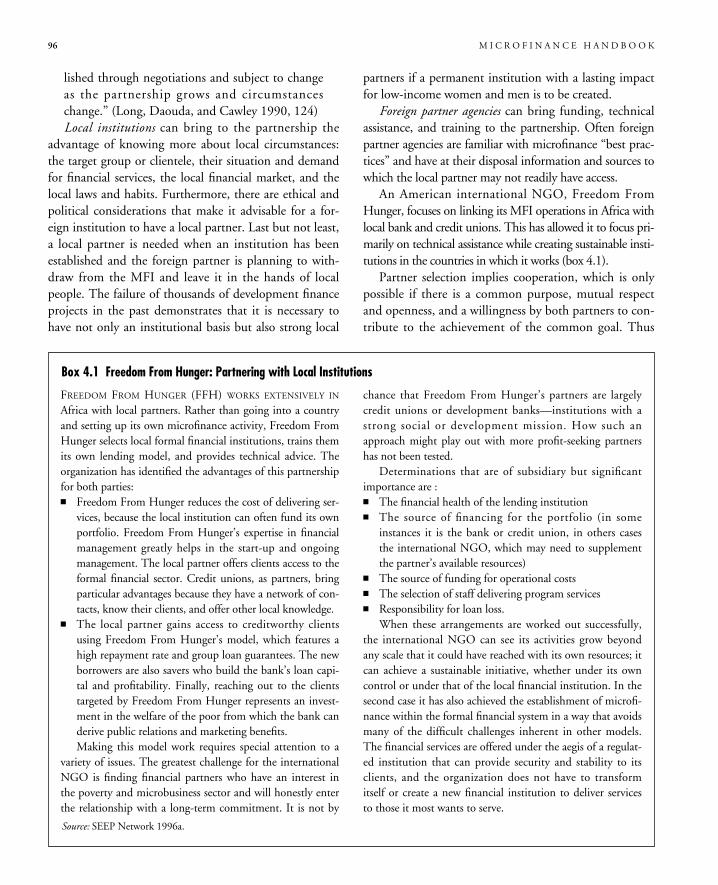

Chapter 4 The Institution 93The Importance of Institutions 93Attributes of a Good Institution 94The Importance of Partner Institutions 94

Institutional Types 97Formal Financial Institutions 97Semiformal Financial Institutions 101Informal Financial Providers 104

C O N T E N T S vii

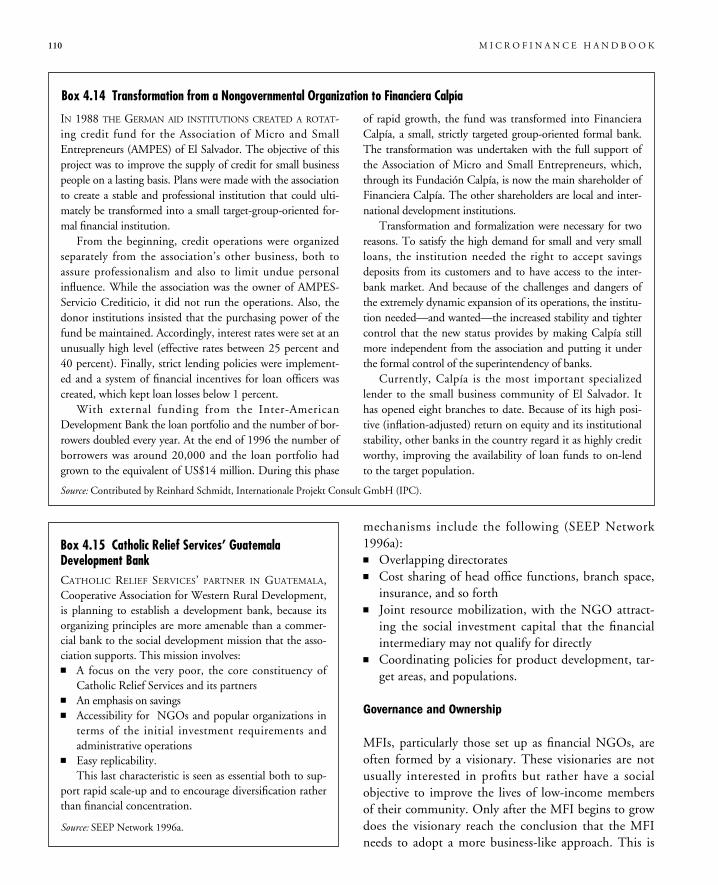

Institutional Growth and Transformation 106Expansion Within an Existing Structure 106Creating an Apex Institution 106Creating a Formal Financial Intermediary 109Governance and Ownership 110Accessing Capital Markets 113

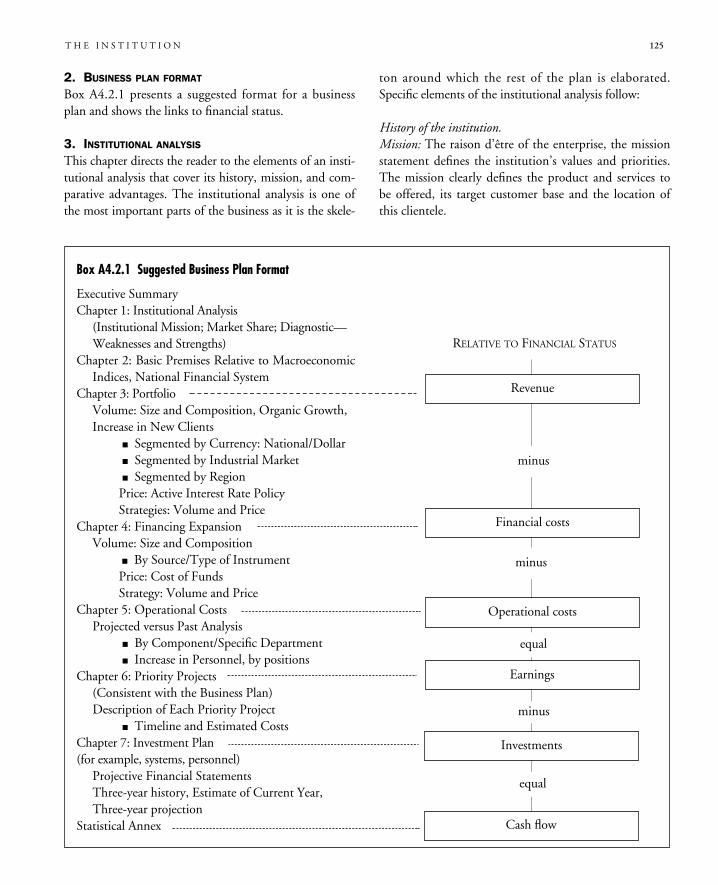

Institutional Capacity Building 117Appendix 1. MFI Operational Review 118Appendix 2. Manual for Elaboration of a Business Plan 123Sources and Further Reading 128

PART II—DESIGNING AND MONITORING FINANCIAL PRODUCTS AND SERVICES 131

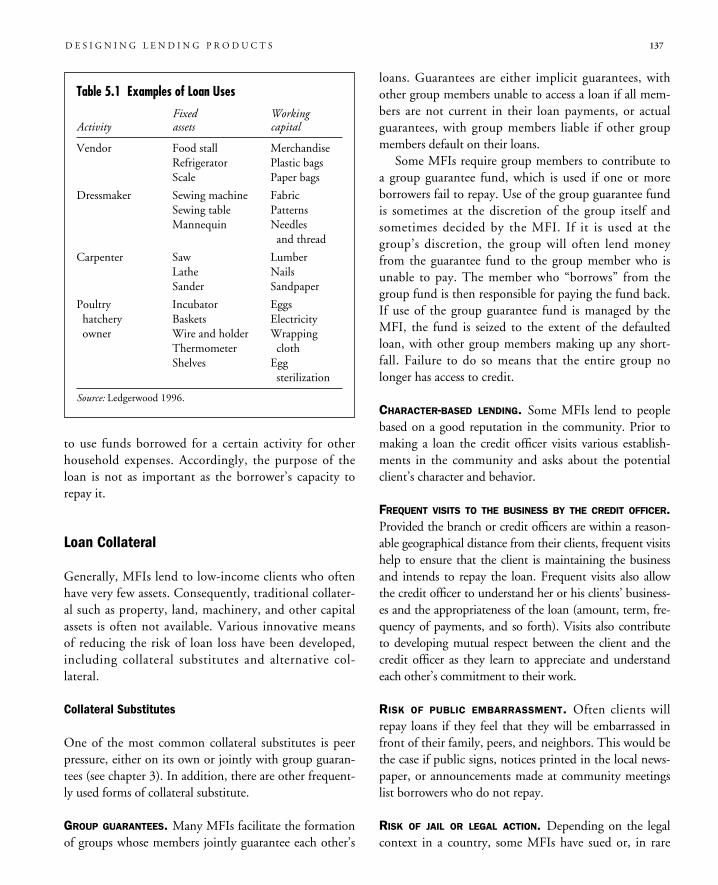

Chapter 5 Designing Lending Products 133Cash Patterns, Loan Terms, and Payment Frequency 133Client Cash Patterns and Loan Amounts 133How Does the Loan Term Affect the Borrower’s Ability to Repay? 134Frequency of Loan Payments 136Working Capital and Fixed Asset Loans 136

Loan Collateral 137Collateral Substitutes 137Alternative Forms of Collateral 138

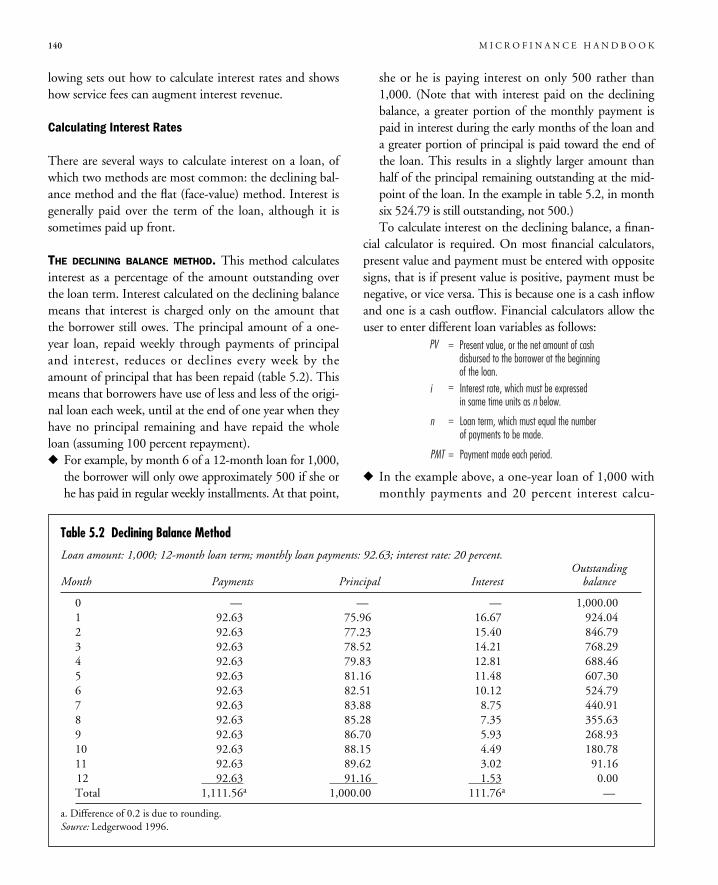

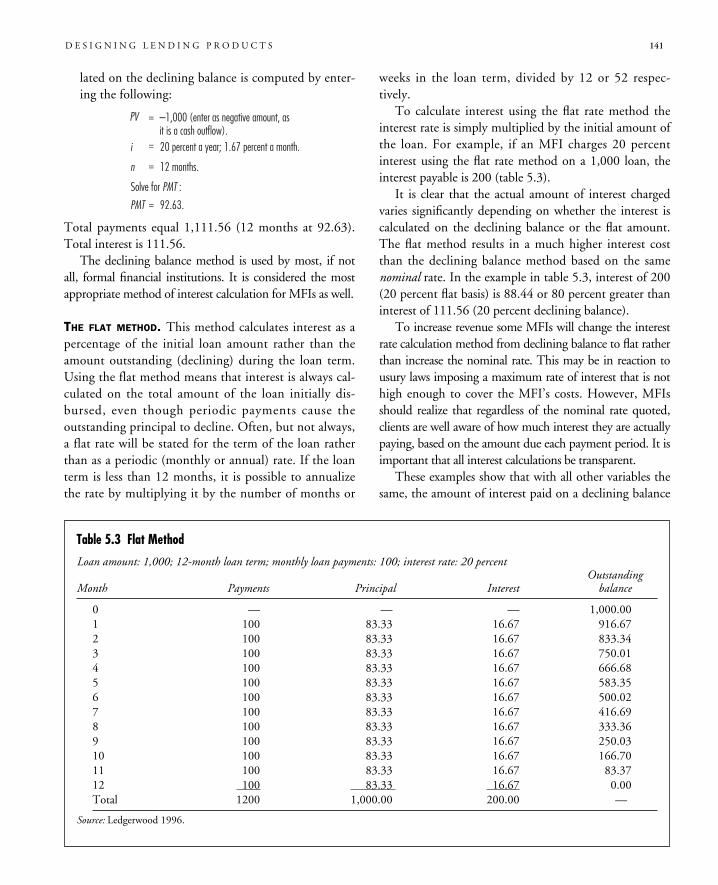

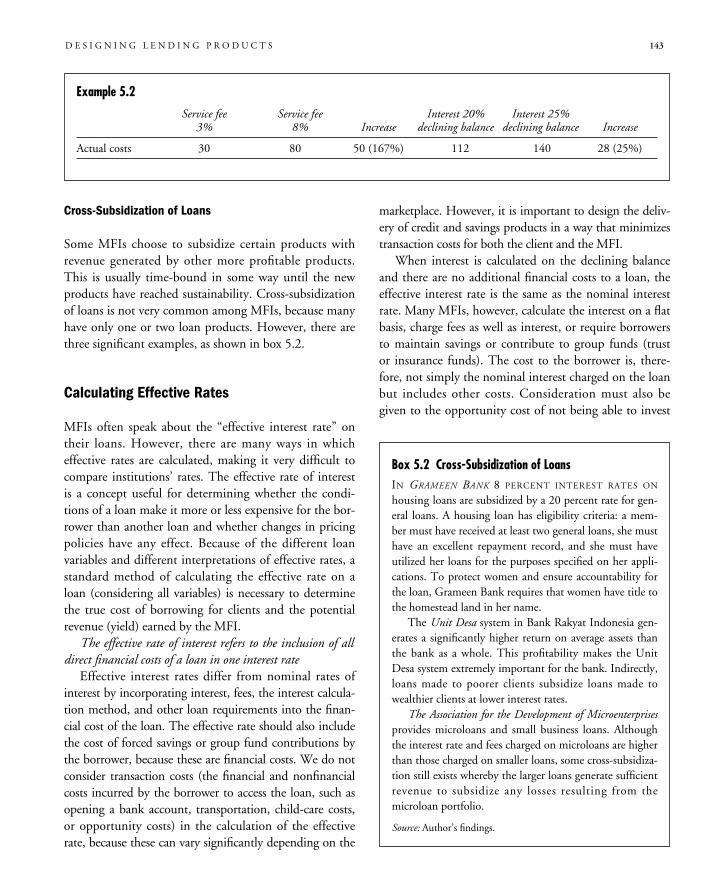

Loan Pricing 138Calculating Interest Rates 140How Do Fees or Service Charges Affect the Borrower and the MFI? 142Cross-Subsidization of Loans 143

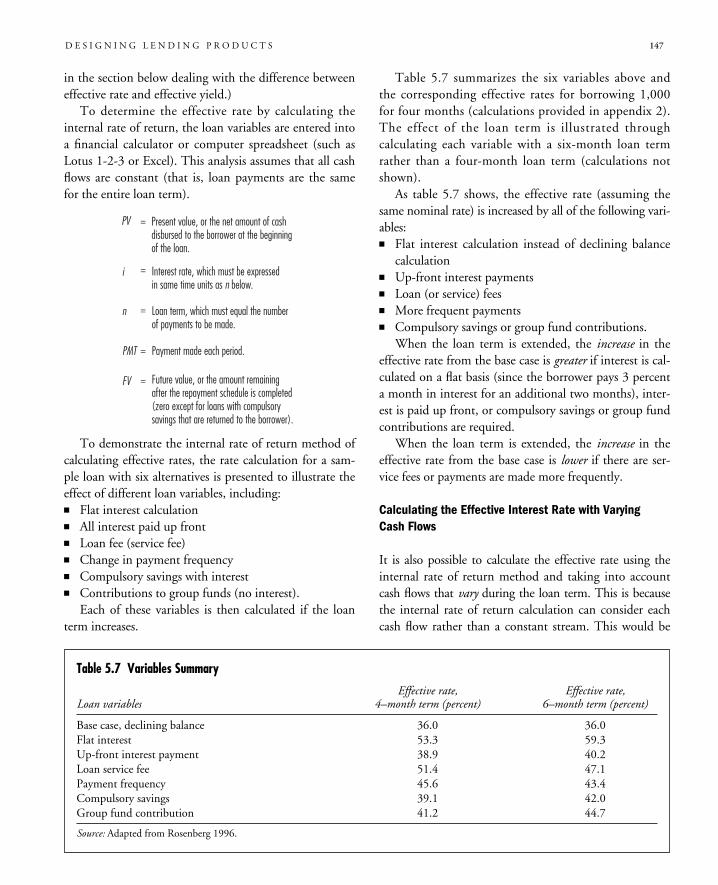

Calculating Effective Rates 143Estimating the Effective Rate 144Calculating the Effective Interest Rate with Compulsory Savings or Other Loan Variables 146Calculating the Effective Interest Rate with Varying Cash Flows 147How Does the Effective Cost for the Borrower Differ from the Effective Yield to the Lender? 148

Appendix 1. How Can an MFI Set a Sustainable Rate on Its Loans? 149Appendix 2. Calculating an Effective Interest Rate Using the Internal Rate of Return Method 150Appendix 3. Calculating the Effective Rate with Varying Cash Flows 152Sources and Further Reading 153

Chapter 6 Designing Savings Products 155Demand for Savings Services 156Is There an Enabling Environment? 157Legal Requirements for Offering Voluntary Savings Services 157Deposit Insurance 158

Does the MFI Have the Necessary Institutional Capacity to Mobilize Savings? 160Ownership and Governance 160Organizational Structure 160Human Resources 161Marketing 162Infrastructure 163

viii C O N T E N T S

Security and Internal Controls 163Management Information Systems 163Risk Management and Treasury 163

Sequencing the Introduction of Savings Services 164Types of Savings Products for Microentrepreneurs 164Liquid Accounts 165Semiliquid Accounts 165Fixed-Term Deposits 166

Costs of Mobilizing Voluntary Savings 166Pricing Savings Products 167Sources and Further Reading 168

Chapter 7 Management Information Systems 169An Overview of Issues Related to Management Information Systems 170Three Areas of Management Information Systems 171Accounting Systems 171Credit and Savings Monitoring Systems 172Client Impact Tracking Systems 178

Installing a Management Information System 178Institutional Assessment 178Configuration 178Software Modifications 179Testing 179Data Transfer 179Training 180Parallel Operations 180Ongoing Support and Maintenance 180

Appendix 1. Overview of Commercial Management Information System Software Packages 180Appendix 2. Criteria for Evaluating Loan Tracking Software 183Sources and Further Reading 183

PART III—MEASURING PERFORMANCE AND MANAGING VIABILITY 185

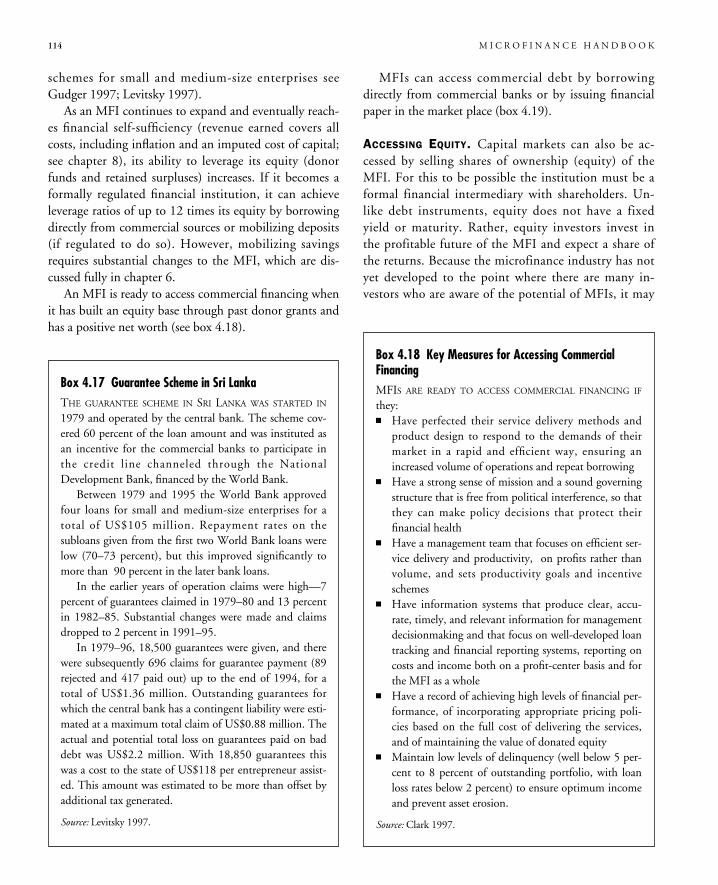

Chapter 8 Adjusting Financial Statements 187Accounting Adjustments 188Accounting for Loan Losses 188Accounting for Depreciation of Fixed Assets 192Accounting for Accrued Interest and Accrued Interest Expense 193

Adjusting for Subsidies and Inflation 194Accounting for Subsidies 195Accounting for Inflation 197

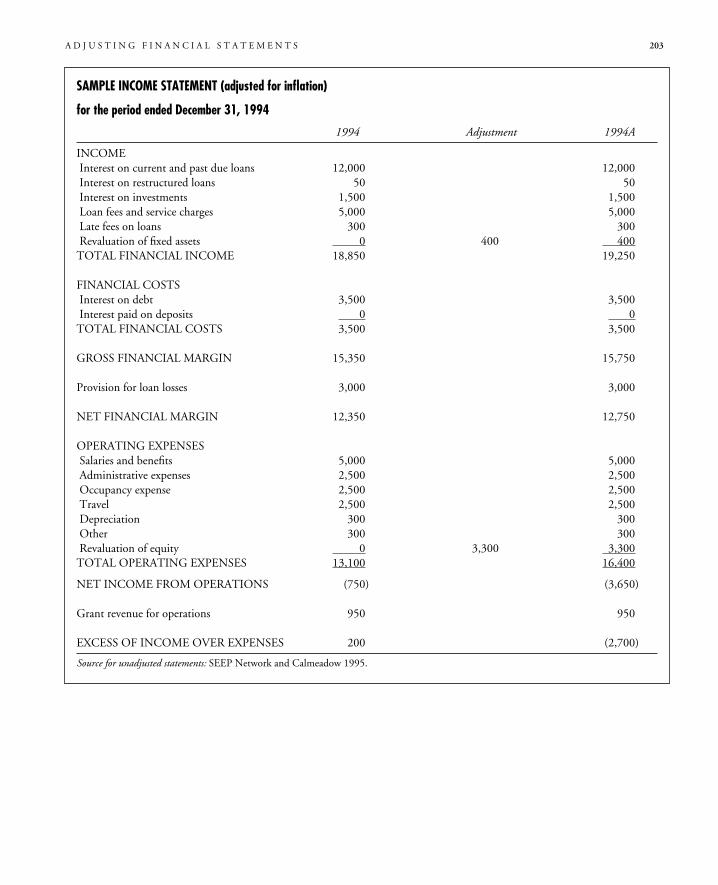

Restating Financial Statements in Constant Currency Terms 199Appendix 1. Sample Financial Statements Adjusted for Subsidies 200Appendix 2. Sample Financial Statements Adjusted for Inflation 202Sources and Further Reading 204

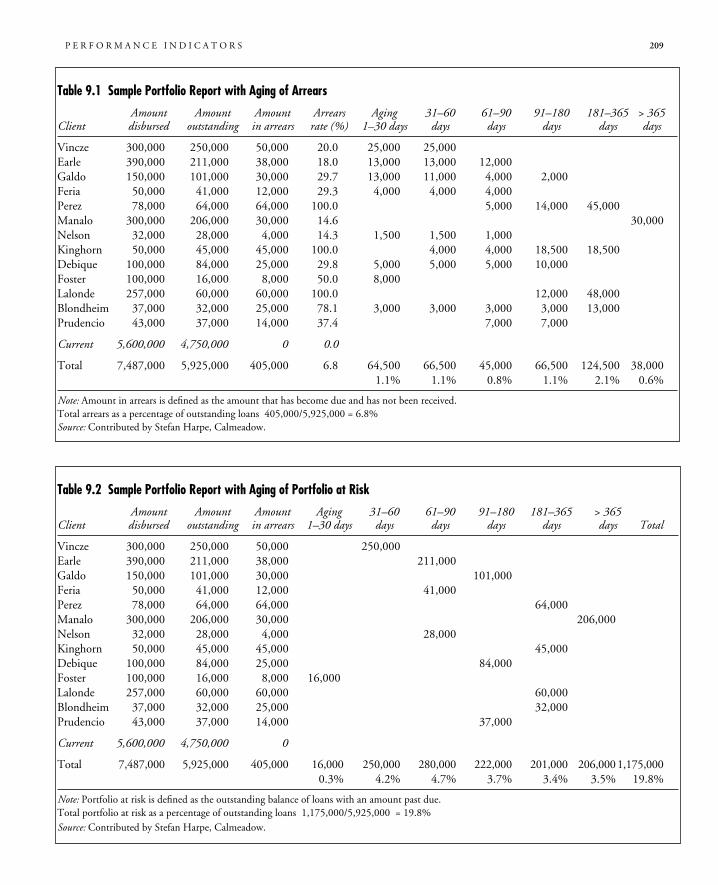

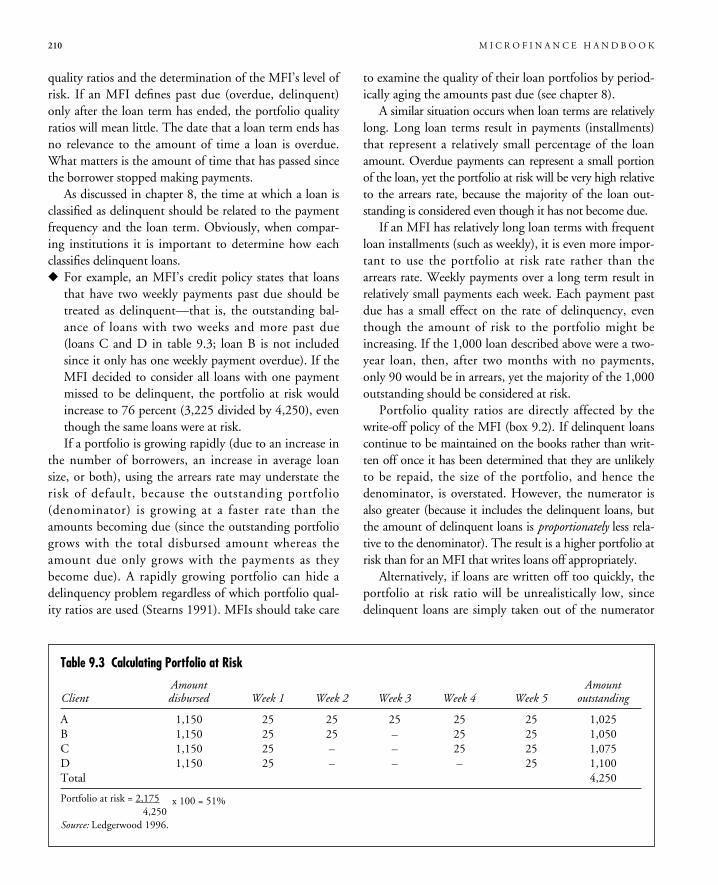

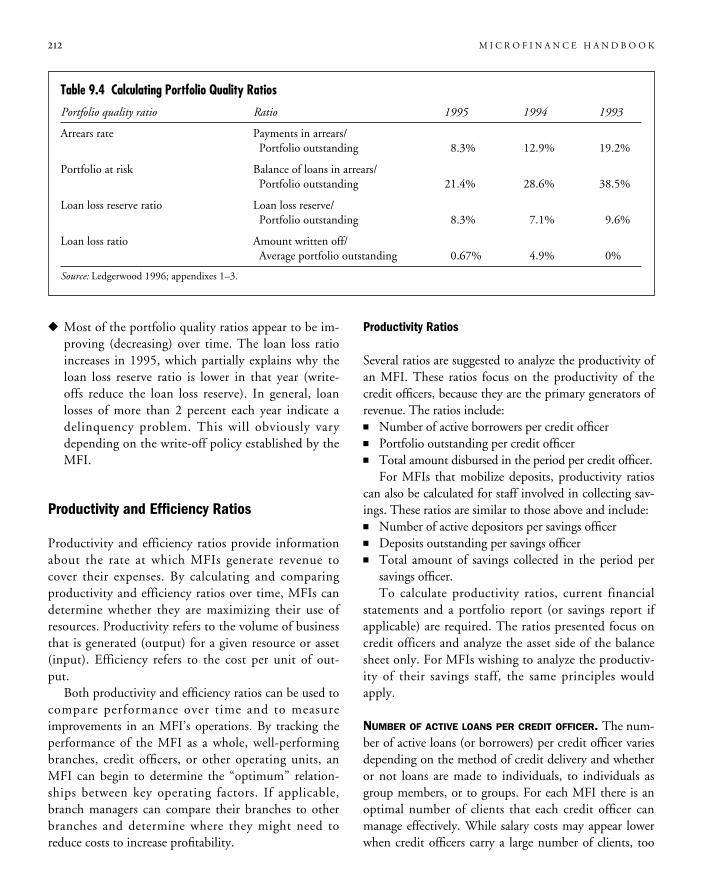

Chapter 9 Performance Indicators 205Portfolio Quality 206Repayment Rates 206Portfolio Quality Ratios 207Loan Loss Ratios 211

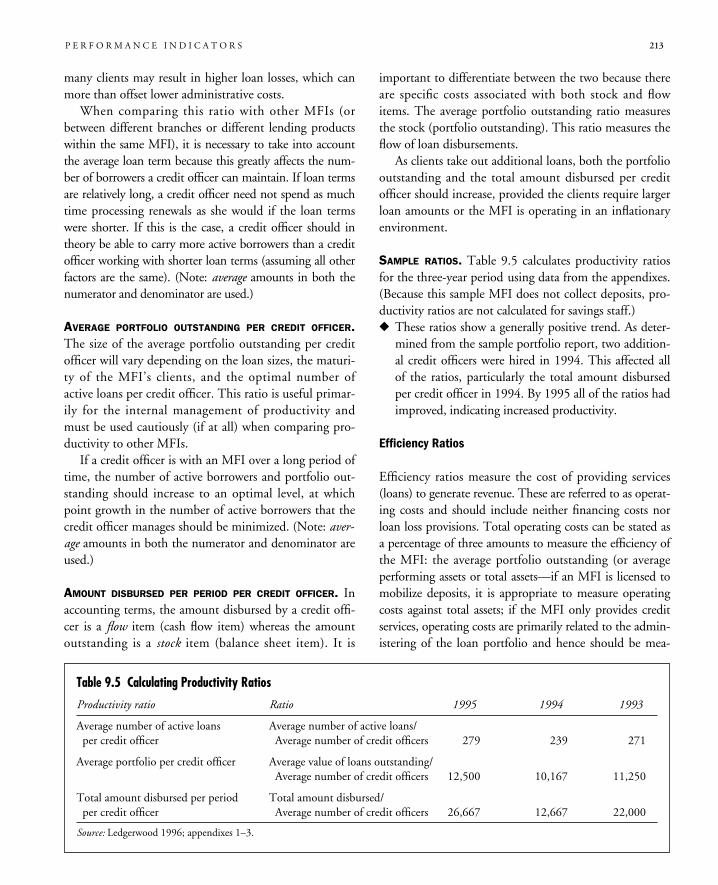

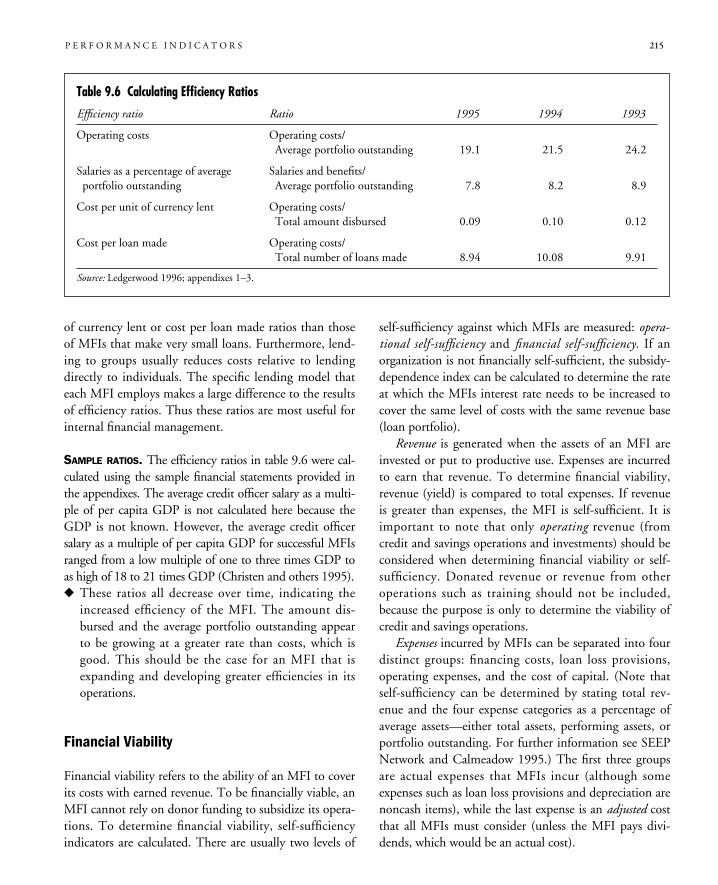

Productivity and Efficiency Ratios 212Productivity Ratios 212Efficiency Ratios 213

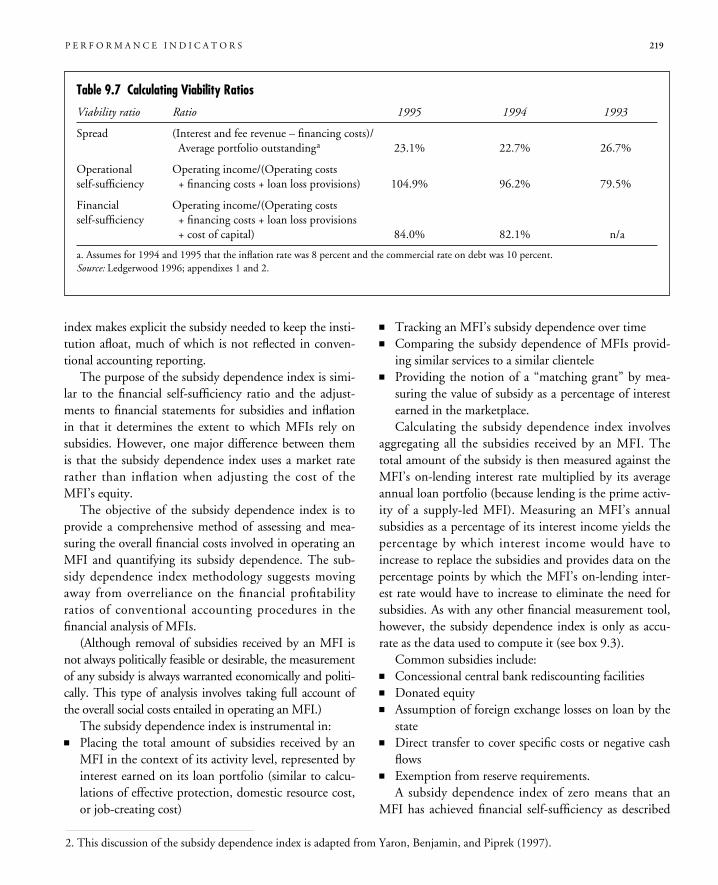

Financial Viability 215Financial Spread 216Two Levels of Self-Sufficiency 216Subsidy Dependence Index 218

Profitability Ratios 220Return on Assets Ratio 221Return on Business Ratio 222Return on Equity Ratio 223

Leverage and Capital Adequacy 223Leverage 224Capital Adequacy Standards 224

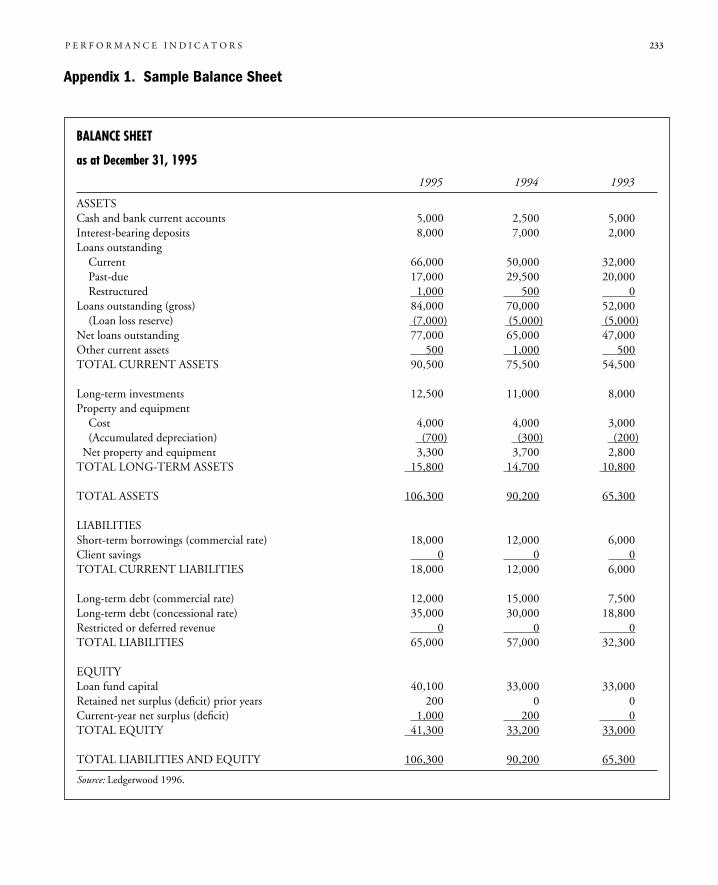

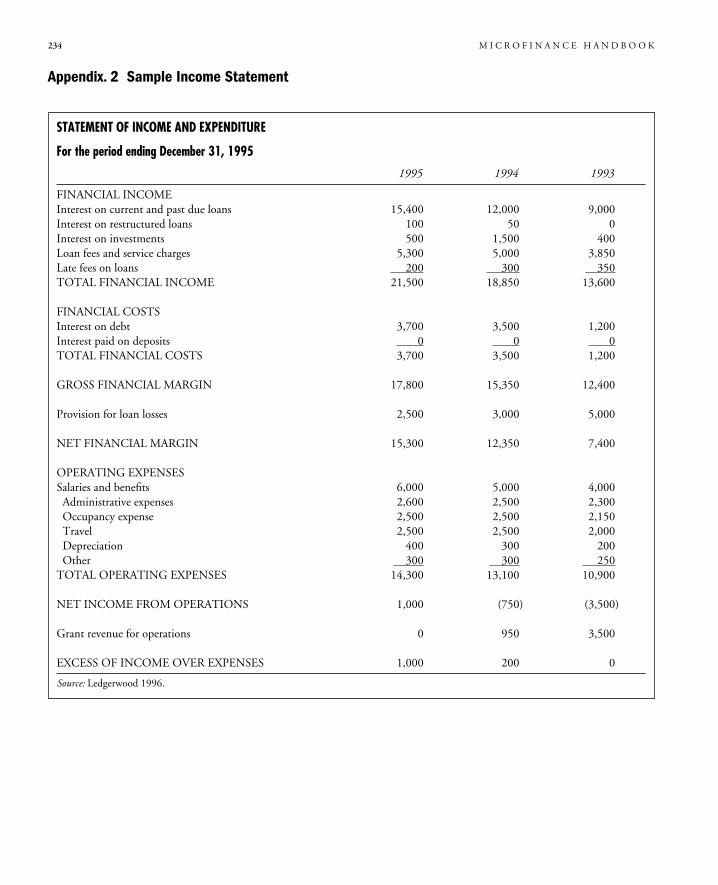

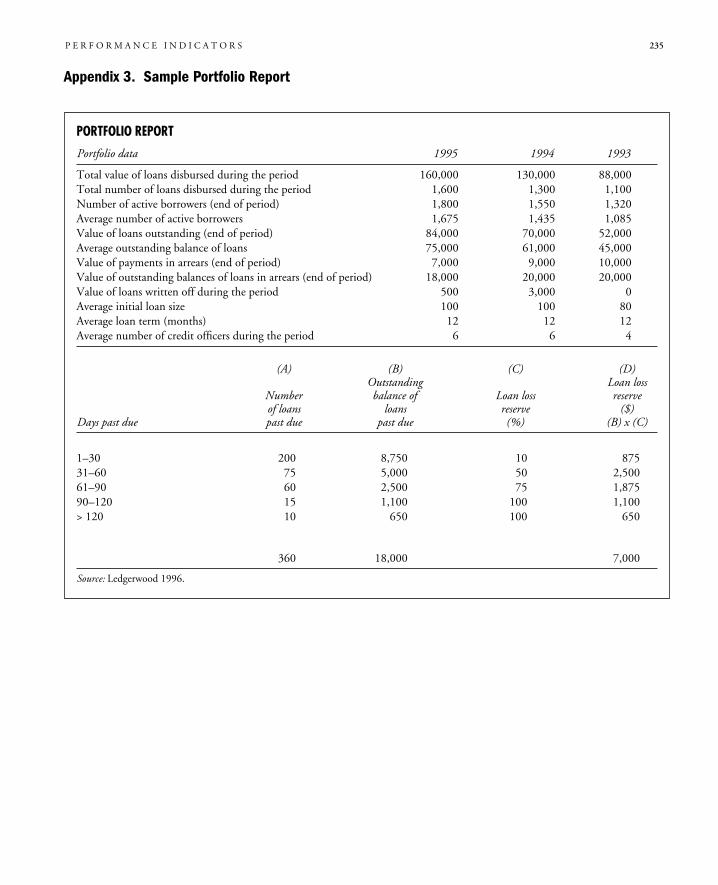

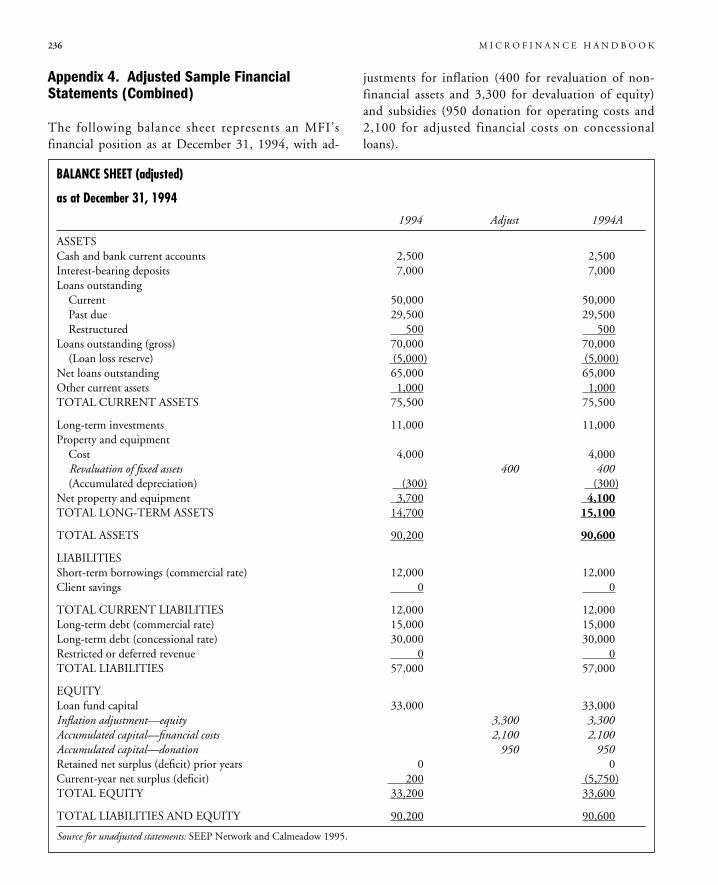

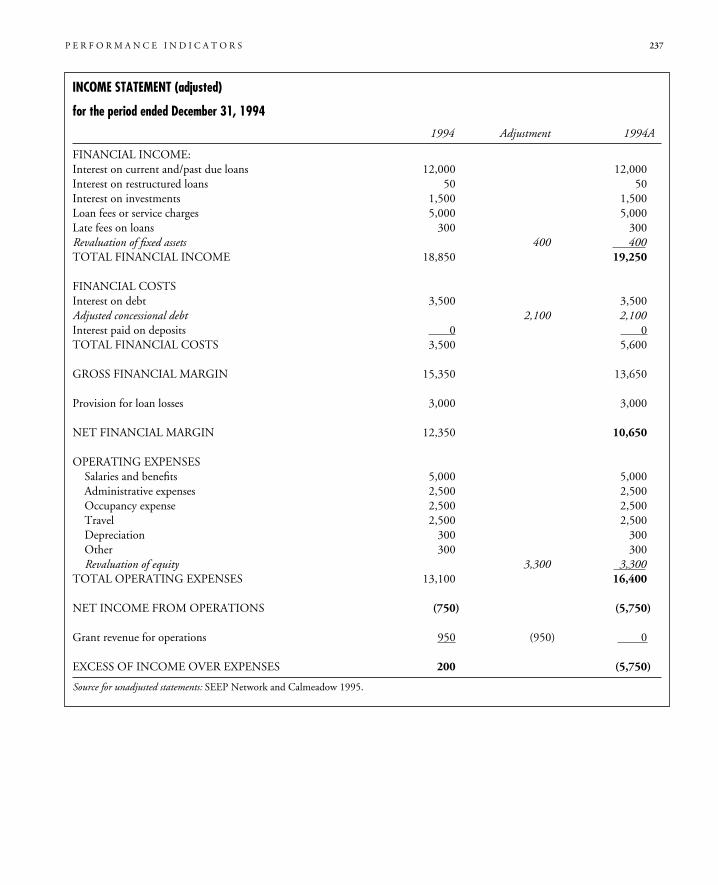

Scale and Depth of Outreach Indicators 225Performance Standards and Variations 227Appendix 1. Sample Balance Sheet 233Appendix 2. Sample Income Statement 234Appendix 3. Sample Portfolio Report 235Appendix 4. Adjusted Sample Financial Statements (Combined) 236Appendix 5. Analyzing an MFI’s Return on Assets 238Sources and Further Reading 241

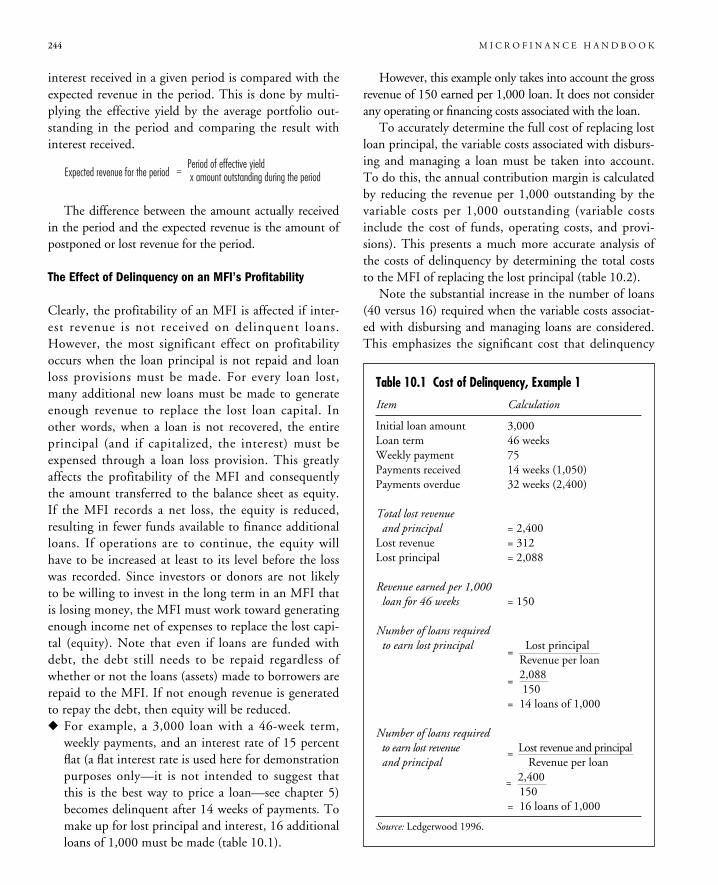

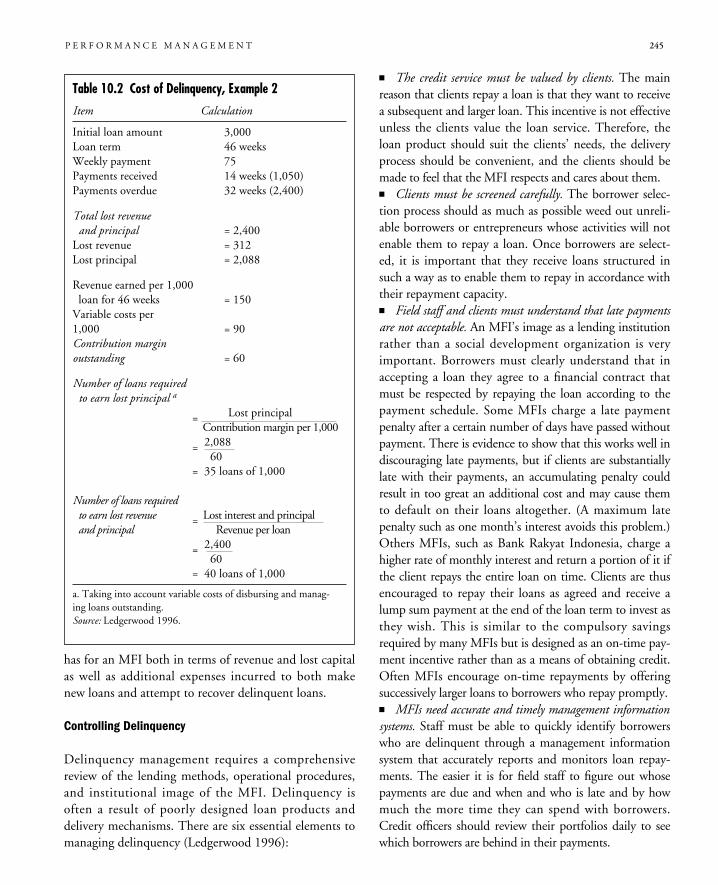

Chapter 10 Performance Management 243Delinquency Management 243The Effect of Delinquency on an MFI’s Profitability 244Controlling Delinquency 245Rescheduling or Refinancing Loans 246

Productivity and Efficiency Management 248Improving Staff Productivity 248Managing Costs 251

Risk Management 254Asset and Liability Management 254Operating Risk Management 258

Appendix 1. Gap Analysis 260Sources and Further Reading 261

GLOSSARY 263

INDEX 271

C O N T E N T S ix

Boxes1.1 Formal Sector Suppliers in Rural Mexico 141.2 Do Microfinance Clients Need Subsidized Interest Rates? 151.3 Credit Institutions as a Political Tool: Debt Foregiveness in India 151.4 Microfinance in Indonesia 161.5 Multilateral Development Banks’ Strategies for Microfinance 181.6 The Consultative Group to Assist the Poorest 191.7 Usury Laws in West Africa 191.8 Alexandria Business Association: Legal Sanctions 201.9 Regulating MFIs: The Case of Finansol 221.10 Enhancing the Effectiveness of Oversight 231.11 Private Financial Funds in Bolivia 251.12 Nonbank Financial Institutions in Ghana 261.13 Microfinance in Areas of Political Unrest 271.14 The Albanian Development Fund 281.15 Tax Laws in Argentina 292.1 Targeted Credit Activities 342.2 U.S. Agency for International Development Findings on Female Borrowers 382.3 The Kenya Rural Enterprise Programme 402.4 The Influence of Ethnicity and Language in Microfinance 412.5 Islamic Banking 422.6 The Association for the Development of Microenterprises’ Work with Existing Microenterprises 432.7 Foundation for Enterprise Finance and Development’s Approach to Sector Development 462.8 The Impact of Finance on the Rural Economy of India 472.9 PRODEM’s Impact and Market Analysis Project 503.1 Principles of Financially Viable Lending to Poor Entrepreneurs 673.2 Individual Loans at Fédération des Caisses d’Epargne et de Crédit Agricole Mutuel, Benin 693.3 The Association for the Development of Microenterprises 693.4 Rotating Savings and Credit Associations 703.5 Repayment Instability in Burkina Faso 713.6 The Role of Groups in Financial Intermediation 723.7 Caisses Villageoises, Pays Dogon, Mali 733.8 Self-Employed Women’s Association Insurance 753.9 The Association for the Development of Microenterprises’ MasterCard 753.10 Swazi Business Growth Trust Smart Cards 763.11 Demand for Payment Services at the Fédération des Caisses d’Epargne

et de Crédit Agricole Mutuel, Benin 763.12 Village Banks: An Example of a Parallel System 773.13 Social Intermediation in a Social Fund in Benin 783.14 Business Skills Training 793.15 Direct and Indirect Business Advisory Services 793.16 Cattle Dealers in Mali 793.17 Who Offers Social Services? 813.18 Freedom From Hunger—Providing Nutrition Training with Microfinance 81A3.1.1 Training for Replicators in West Africa 83A3.2.1 Policy Dialogue in El Salvador 90

x C O N T E N T S

4.1 Freedom From Hunger: Partnering with Local Institutions 964.2 Types of Financial Institutions 974.3 Development Banks 984.4 Tulay sa Pag-Unlad’s Transformation into a Private Development Bank 994.5 The Savings Bank of Madagascar 994.6 Caja Social: A Colombian Commercial Bank Reaching the Poor 1004.7 Caja de Ahorro y Prestamo Los Andes 1014.8 Accion Comunitaria del Peru 1014.9 The Rehabilitation of a Credit Union in Benin 1024.10 CARE Guatemala: The Women’s Village Banking Program 1044.11 The Use of Self-Help Groups in Nepal 1054.12 Using the Nongovernmental Organization as a Strategic Step in Expansion 1074.13 Catholic Relief Services: Using the Apex Model for Expansion 1084.14 Transformation from a Nongovernmental Organization to Financiera Calpía 1104.15 Catholic Relief Services’ Guatemala Development Bank 1104.16 BancoADEMI Ownership Structure 1124.17 Guarantee Scheme in Sri Lanka 1144.18 Key Measures for Accessing Commercial Financing 1144.19 Accessing Capital Markets by Issuing Financial Paper 1154.20 ProFund—an Equity Investment Fund for Latin America 1154.21 The Calvert Group—a Screened Mutual Fund 1164.22 DEVCAP—a Shared-Return Fund 1164.23 Credit Unions Retooled 118A4.2.1 Suggested Business Plan Format 125A4.2.2 Estimating the Market: An Example from Ecuador 1265.1 The Association for the Development of Microenterprises’ Collateral Requirements 1395.2 Cross-Subsidization of Loans 1436.1 Deposit Collectors in India 1566.2 Savings Mobilization at Bank Rakyat Indonesia 1586.3 Deposit Insurance in India 1596.4 Security of Deposits in the Bank for Agriculture and Agricultural Cooperatives, Thailand 1596.5 Ownership and Governance at the Bank for Agriculture and Agricultural Cooperatives, Thailand 1616.6 Using Local Human Resources in Caisses Villageoises d’Epargne et de Crédit Autogérées, Mali 1626.7 The Sequencing of Voluntary Savings Mobilization 1646.8 Bank Rakyat Indonesia Savings Instruments 1656.9 The Choice of Savings Products in Pays Dogon, Mali 1666.10 Administrative Costs for Banco Caja Social, Colombia 1677.1 Determining the Information Needs of an MFI 1707.2 Microfinance Institutions with Developed “In-House” Systems 1747.3 Improving Reporting Formats: Experience of the Workers Bank of Jamaica 1767.4 Management Information Systems at the Association for the Development

of Microenterprises, Dominican Republic 1777.5 Framework for a Management Information System at Freedom From Hunger 1787.6 Running Parallel Operations in the Fédération des Caisses d’Epargne et de Crédit Agricole Mutuel, Benin 1808.1 The Impact of Failure to Write Off Bad Debt 1918.2 Cash and Accrual Accounting for Microfinance Institutions 194

C O N T E N T S xi

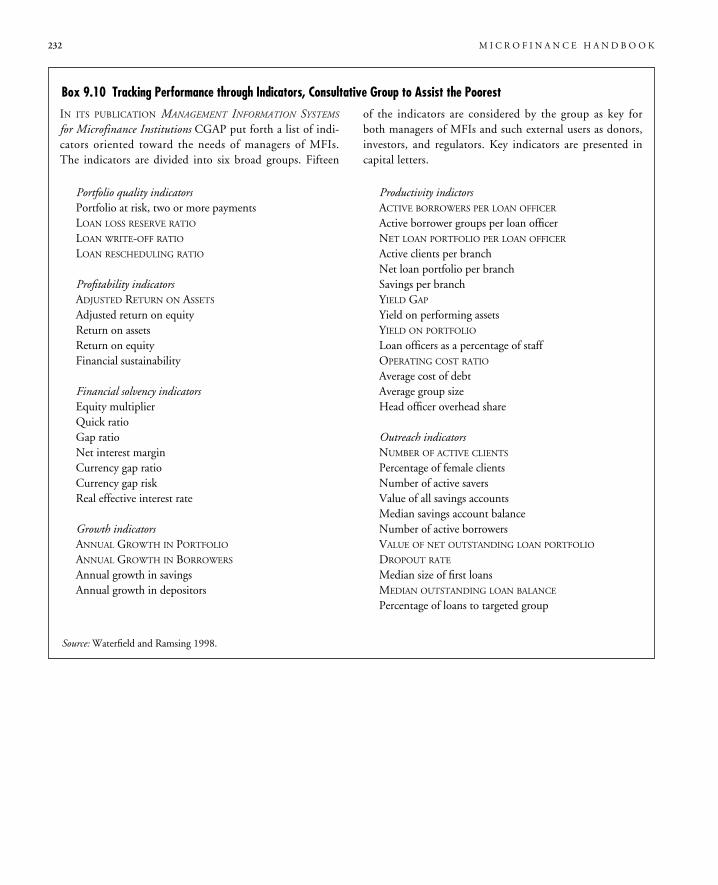

9.1 Repayment Rates Compared with Portfolio Quality Ratios 2089.2 The Effect of Write-off Policies 2119.3 Computation of the Subsidy Dependence Index 2209.4 CARE Guatemala’s Subsidy Dependence Index 2219.5 Outreach Indicators 2269.6 Depth of Outreach Diamonds 2289.7 CAMEL System, ACCION 2299.8 Financial Ratio Analysis for Microfinance Institutions, Small Enterprise and Promotion Network 2309.9 PEARLS System, World Council of Credit Unions 2319.10 Tracking Performance through Indicators, Consultative Group to Assist the Poorest 232A9.5.1 Analyzing a Financial Institution’s Return on Assets 23810.1 Fifteen Steps to Take in a Delinquency Crisis 24610.2 Unusual Gains in Efficiency at Women’s World Banking, Cali, Colombia 24810.3 Performance Incentives at the Association for the Development of Microenterprises, Dominican Republic 25010.4 Performance Incentive Schemes at Tulay Sa Pag-Unlad Inc., the Philippines 25110.5 Credit Officer Reports at the Association for the Development of Microenterprises 25210.6 Transfer Pricing at Bank Rakyat Indonesia and Grameen Bank in Bangladesh 25310.7 Standardization at Grameen Bank 25410.8 Institution Vulnerability to Fraud 25910.9 Fraud Control at Mennonite Economic Development Association 260

Figures1 Relationship between Level of Analysis and Technical Complexity in this Book 51.1 Understanding the Country Context 112.1 Client Characteristics 382.2 Types of Microenterprises 423.1 Minimalist and Integrated Approaches to Microfinance 653.2 Group Social Intermediation 78A3.2.1 The Entrepreneur’s Context 86

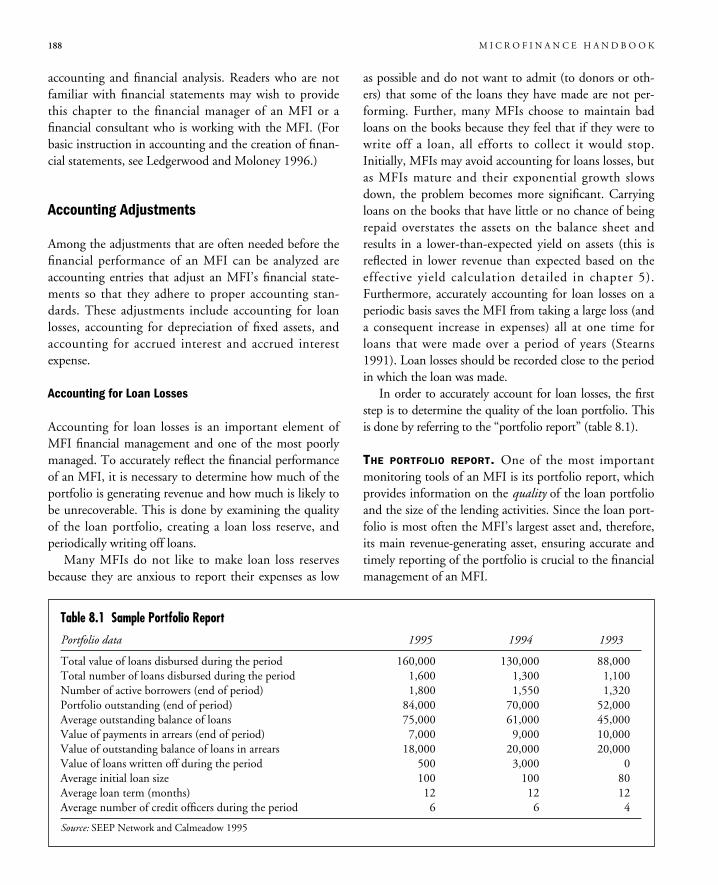

Tables1.1 Providers of Financial Intermediation Services 131.2 Private Institutions in Microenterprise Development 172.1 Enterprise Sector Credit Characteristics 454.1 Key Characteristics of a Strong Microfinance Institution 954.2 What Is at Stake for Microfinance Owners? 112A4.2.1 Financial Cost as a Weighted Average 1285.1 Examples of Loan Uses 1375.2 Declining Balance Method 1405.3 Flat Method 1415.4 Effective Rate Estimate, Declining Balance 1455.5 Effective Rate Estimate, Flat Method 1455.6 Change in Loan Fee and Loan Term Effect 1465.7 Variables Summary 147A5.3.1 Internal Rate of Return with Varying Cash Flows (Grace Period) 152A5.3.2 Internal Rate of Return with Varying Cash Flows (Lump Sum) 1528.1 Sample Portfolio Report 188

xii C O N T E N T S

8.2 Sample Loan Loss Reserve Calculation, December 31, 1995 1909.1 Sample Portfolio Report with Aging of Arrears 2099.2 Sample Portfolio Report with Aging of Portfolio at Risk 2099.3 Calculating Portfolio at Risk 2109.4 Calculating Portfolio Quality Ratios 2129.5 Calculating Productivity Ratios 2139.6 Calculating Efficiency Ratios 2159.7 Calculating Viability Ratios 2199.8 Effect of Leverage on Return on Equity 224A9.5.1 Breakdown of a Microfinance Institution’s Profit Margin and Asset Utilization 239A9.5.2 Analysis of ADEMI’s Return on Assets 24010.1 Cost of Delinquency, Example 1 24410.2 Cost of Delinquency, Example 2 24510.3 On-Time and Late or No Payments 24710.4 Branch Cash Flow Forecasts 256

C O N T E N T S xiii

xv

Foreword

The Sustainable Banking with the Poor Project(SBP) began several years ago as a rather unusualjoint effort by a regional technical department,

Asia Technical, and a central department, Agriculture andNatural Resources. Through the years and the institution-al changes, the project has maintained the support of theAsia Region and the Rural Development Department inthe Environmentally and Socially SustainableDevelopment vice presidency and the endorsement of theFinance, Private Sector and Infrastructure Network.An applied research and dissemination project, SBP

aims at improving the ability of donors, governments,and practitioners to design and implement policies andprograms to build sustainable financial institutions thateffectively reach the poor. While its main audience hasbeen World Bank Group staff, the project has con-tributed significantly to the knowledge base in themicrofinance and rural finance fields at large.More than 20 case studies of microfinance institutions

have been published and disseminated worldwide, manyof them in two languages; a seminar series at the WorldBank has held more than 30 sessions on microfinance andrural finance good practice and new developments; threeregional conferences have disseminated SBP products inAsia and Africa, while fostering and benefiting from exten-

sive discussions with practitioners, policymakers, anddonors. SBP also co-produced with the ConsultativeGroup to Assist the Poorest the "Microfinance PracticalGuide," today a regular source of practical reference forWorld Bank Group task team leaders and staff workingon microfinance operations or project components thatinvolve the provision of financial services to the poor.This volume, Microfinance Handbook: An

Institutional and Financial Perspective, represents in away a culmination of SBP work in pursuit of its princi-pal aim. A comprehensive source for donors, policymak-ers, and practitioners, the handbook first covers thepolicy, legal, and regulatory issues relevant to micro-finance development and subsequently treats rigorouslyand in depth the key elements in the process of buildingsustainable financial institutions with effective outreachto the poor.The handbook focuses on the institutional and finan-

cial aspects of microfinance. Although impact analysis isreviewed briefly, a thorough discussion of poverty target-ing and of the poverty alleviation effects of microfinance isleft to other studies and publications.We are confident that this handbook will contribute

significantly to the improvement of policies and prac-tices in the microfinance field.

Ian JohnsonVice PresidentEnvironmentally and Socially Sustainable Development

Masood AhmedActing Vice PresidentFinance, Private Sector and Infrastructure

Jean-Michel SeverinoVice PresidentEast Asia and Pacific Region

Mieko NishimizuVice PresidentSouth Asia Region

Preface

The Microfinance Handbook, one of the majorproducts of the World Bank’s SustainableBanking with the Poor Project, gathers and pre-

sents up-to-date knowledge directly or indirectly con-tributed by leading experts in the field of microfinance.It is intended as a comprehensive source for donors, poli-cymakers, and practitioners, as it covers in depth matterspertaining to the regulatory and policy framework andthe essential components of institutional capacity build-ing—product design, performance measuring and moni-toring, and management of microfinance institutions.The handbook was developed with contributions

from other parts of the World Bank, including theConsultative Group to Assist the Poorest. It also benefit-ed from the experience of a wide range of practitionersand donors from such organizations as ACCIONInternational, Calmeadow, CARE, Women’s WorldBanking, the Small Enterprise Education and PromotionNetwork, the MicroFinance Network, the U.S. Agencyfor International Development, Deutsche Gesellschaftfür Technische Zusammenarbeit, Caisse Française deDéveloppement, and the Inter-American DevelopmentBank.Special thanks are due to the outside sponsors of the

Sustainable Banking with the Poor Project—the SwissAgency for Development and Cooperation, the RoyalMinistry of Foreign Affairs of Norway, and the FordFoundation—for their patience, encouragement, andsupport.I would like to thank the many individuals who con-

tributed substantially to this handbook. A first draft wasprepared by staff members at both the SustainableBanking with the Poor Project and the Consultative

Group to Assist the Poorest. I am grateful to MikeGoldberg and Gregory Chen for their initial contribu-tions. Thomas Dichter wrote the sections on impactanalysis and enterprise development services and provid-ed comments on other chapters. Tony Sheldon wrotethe chapter on management information systems andprovided comments on the first draft. ReinhardtSchmidt contributed substantially to the chapter oninstitutions.I wish to thank especially Cecile Fruman for her ini-

tial and ongoing contributions, comments, and support.I also appreciate the support and flexibility of Carlos E.Cuevas, which were vital in keeping the process going.Thanks are extended to Julia Paxton and StephanieCharitonenko Church for their contributions as well asto the many people who reviewed various chapters andprovided comments, including Jacob Yaron, LynnBennett, Mohini Malhotra, McDonald Benjamin,Jeffrey Poyo, Jennifer Harold, Bikki Randhawa, JoyitaMukherjee, Jennifer Isern, and Joakim Vincze.I would also like to thank Laura Gomez for her con-

tinued support in formatting the handbook and manag-ing its many iterations.The book was edited, designed, and typeset by Com-

munications Development Inc.

*****

The Sustainable Banking with the Poor Project team isled by Lynn Bennett and Jacob Yaron, task managers.Carlos E. Cuevas is the technical manager and CecileFruman is the associate manager. Laura Gomez is theadministrative assistant.

xvi

1

Introduction

Ithas been estimated that there are 500 million econom-ically active poor people in the world operatingmicroenterprises and small businesses (Women’s World

Banking 1995). Most of them do not have access to ade-quate financial services. To meet this substantial demand forfinancial services by low-income microentrepreneurs,microfinance practitioners and donors alike must adopt along-term perspective. The purpose of this handbook is tobring together in a single source guiding principles and toolsthat will promote sustainable microfinance and create viableinstitutions.The goal of this book is to provide a comprehensive

source for the design, implementation, evaluation, andmanagement of microfinance activities.1

The handbook takes a global perspective, drawing onlessons learned from the experiences of microfinancepractitioners, donors, and others throughout the world.It offers readers relevant information that will help themto make informed and effective decisions suited to theirspecific environment and objectives.

Microfinance Defined

Microfinance has evolved as an economic developmentapproach intended to benefit low-income women andmen. The term refers to the provision of financial servicesto low-income clients, including the self-employed.

Financial services generally include savings and credit;however, some microfinance organizations also provideinsurance and payment services. In addition to financialintermediation, many MFIs provide social intermediationservices such as group formation, development of self-confidence, and training in financial literacy and manage-ment capabilities among members of a group. Thus thedefinition of microfinance often includes both financialintermediation and social intermediation. Microfinance isnot simply banking, it is a development tool.Microfinance activities usually involve:

� Small loans, typically for working capital� Informal appraisal of borrowers and investments� Collateral substitutes, such as group guarantees orcompulsory savings

� Access to repeat and larger loans, based on repaymentperformance

� Streamlined loan disbursement and monitoring� Secure savings products.Although some MFIs provide enterprise development

services, such as skills training and marketing, and socialservices, such as literacy training and health care, theseare not generally included in the definition of microfi-nance. (However, enterprise development services andsocial services are discussed briefly in chapter 3, as someMFIs provide these services.)MFIs can be nongovernmental organizations

(NGOs), savings and loan cooperatives, credit unions,

1. The term “microfinance activity” is used throughout to describe the operations of a microfinance institution, a microfinance pro-ject, or a microfinance component of a project. When referring to an organization providing microfinance services, whether regulat-ed or unregulated, the term “microfinance institution” (MFI) is used.

2 M I C R O F I N A N C E H A N D B O O K

government banks, commercial banks, or nonbankfinancial institutions. Microfinance clients are typicallyself-employed, low-income entrepreneurs in both urbanand rural areas. Clients are often traders, street vendors,small farmers, service providers (hairdressers, rickshawdrivers), and artisans and small producers, such as black-smiths and seamstresses. Usually their activities providea stable source of income (often from more than oneactivity). Although they are poor, they are generally notconsidered to be the “poorest of the poor.”Moneylenders, pawnbrokers, and rotating savings and

credit associations are informal microfinance providersand important sources of financial intermediation butthey are not discussed in detail in this handbook. Rather,the focus is on more formal MFIs.

Background

Microfinance arose in the 1980s as a response todoubts and research findings about state delivery ofsubsidized credit to poor farmers. In the 1970s govern-ment agencies were the predominant method of pro-viding productive credit to those with no previousaccess to credit facilities—people who had been forcedto pay usurious interest rates or were subject to rent-seeking behavior. Governments and internationaldonors assumed that the poor required cheap creditand saw this as a way of promoting agricultural pro-duction by small landholders. In addition to providingsubsidized agricultural credit, donors set up creditunions inspired by the Raiffeisen model developed inGermany in 1864. The focus of these cooperativefinancial institutions was mostly on savings mobiliza-tion in rural areas in an attempt to “teach poor farmershow to save.”Beginning in the mid-1980s, the subsidized, targeted

credit model supported by many donors was the objectof steady criticism, because most programs accumulatedlarge loan losses and required frequent recapitalization tocontinue operating. It became more and more evidentthat market-based solutions were required. This led to anew approach that considered microfinance as an inte-gral part of the overall financial system. Emphasis shiftedfrom the rapid disbursement of subsidized loans to targetpopulations toward the building up of local, sustainableinstitutions to serve the poor.

At the same time, local NGOs began to look for amore long-term approach than the unsustainable income-generation approaches to community development. InAsia Dr. Mohammed Yunus of Bangladesh led the waywith a pilot group lending scheme for landless people.This later became the Grameen Bank, which now servesmore than 2.4 million clients (94 percent of themwomen) and is a model for many countries. In LatinAmerica ACCION International supported the develop-ment of solidarity group lending to urban vendors, andFundación Carvajal developed a successful credit andtraining system for individual microentrepreneurs.Changes were also occurring in the formal financial

sector. Bank Rakyat Indonesia, a state-owned, ruralbank, moved away from providing subsidized credit andtook an institutional approach that operated on marketprinciples. In particular, Bank Rakyat Indonesia devel-oped a transparent set of incentives for its borrowers(small farmers) and staff, rewarding on-time loan repay-ment and relying on voluntary savings mobilization as asource of funds.Since the 1980s the field of microfinance has grown

substantially. Donors actively support and encouragemicrofinance activities, focusing on MFIs that are com-mitted to achieving substantial outreach and financialsustainability. Today the focus is on providing financialservices only, whereas the 1970s and much of the 1980swere characterized by an integrated package of credit andtraining—which required subsidies. Most recently,microfinance NGOs (including PRODEM/BancoSol inBolivia, K-REP in Kenya, and ADEMI/BancoADEMIin the Dominican Republic) have begun transforminginto formal financial institutions that recognize the needto provide savings services to their clients and to accessmarket funding sources, rather than rely on donor funds.This recognition of the need to achieve financial sustain-ability has led to the current “financial systems”approach to microfinance. This approach is characterizedby the following beliefs:� Subsidized credit undermines development.� Poor people can pay interest rates high enough tocover transaction costs and the consequences of theimperfect information markets in which lendersoperate.

� The goal of sustainability (cost recovery and eventu-ally profit) is the key not only to institutional perma-

I N T R O D U C T I O N 3

nence in lending, but also to making the lendinginstitution more focused and efficient.

� Because loan sizes to poor people are small, MFIsmust achieve sufficient scale if they are to becomesustainable.

� Measurable enterprise growth, as well as impacts onpoverty, cannot be demonstrated easily or accurately;outreach and repayment rates can be proxies for impact.One of the main assumptions in the above view is

that many poor people actively want productive creditand that they can absorb and use it. But as the field ofmicrofinance has evolved, research has increasinglyfound that in many situations poor people want securesavings facilities and consumption loans just as much asproductive credit and in some cases instead of produc-tive credit. MFIs are beginning to respond to thesedemands by providing voluntary savings services andother types of loans.

Size of the Microfinance Industry

During 1995 and 1996 the Sustainable Banking withthe Poor Project compiled a worldwide inventory ofMFIs. The list included nearly 1,000 institutions thatprovided microfinance services, reached at least 1,000clients, and had operated for a minimum of three years.From this inventory, more than 200 institutionsresponded to a two-page questionnaire covering basicinstitutional characteristics.According to the survey results, by September 1995

about US$7 billion in outstanding loans had been pro-vided to more than 13 million individuals and groups.In addition, more than US$19 billion had been mobi-lized in 45 million active deposit accounts.The general conclusions of the inventory were:

� Commercial and savings banks were responsible forthe largest share of the outstanding loan balance anddeposit balance.

� Credit unions represented 11 percent of the totalnumber of loans in the sample and 13 percent of theoutstanding loan balance.

� NGOs made up more than half of the sample, butthey accounted for only 9 percent of the total num-ber of outstanding loans and 4 percent of the out-standing loan balance.

� Sources of funds to finance loan portfolios differed bytype of institution. NGOs relied heavily on donorfunding or concessional funds for the majority of theirlending. Banks, savings banks, and credit unions fund-ed their loan portfolios with client and memberdeposits and commercial loans.

� NGOs offered the smallest loan sizes and relativelymore social services than banks, savings banks, orcredit unions.

� Credit unions and banks are leaders in serving largenumbers of clients with small deposit accounts.The study also found that basic accounting capacities

and reporting varied widely among institutions, in manycases revealing an inability to report plausible cost andarrears data. This shortcoming, notably among NGOs,highlights the need to place greater emphasis on financialmonitoring and reporting using standardized practices (aprimary purpose of this handbook). Overall, the findingssuggest that favorable macroeconomic conditions, man-aged growth, deposit mobilization, and cost control, incombination, are among the key factors that contributeto the success and sustainability of many microfinanceinstitutions.

Why is Microfinance Growing?

Microfinance is growing for several reasons:1. The promise of reaching the poor. Microfinance activi-ties can support income generation for enterprisesoperated by low-income households.

2. The promise of financial sustainability. Microfinanceactivities can help to build financially self-sufficient,subsidy-free, often locally managed institutions.

3. The potential to build on traditional systems. Micro-finance activities sometimes mimic traditional systems(such as rotating savings and credit associations). Theyprovide the same services in similar ways, but withgreater flexibility, at a more affordable price tomicroenterprises and on a more sustainable basis. Thiscan make microfinance services very attractive to alarge number of low-income clients.

4. The contribution of microfinance to strengthening andexpanding existing formal financial systems. Micro-finance activities can strengthen existing formalfinancial institutions, such as savings and loan coop-

4 M I C R O F I N A N C E H A N D B O O K

eratives, credit union networks, commercial banks,and even state-run financial institutions, by expand-ing their markets for both savings and credit—and,potentially, their profitability.

5. The growing number of success stories. There is anincreasing number of well-documented, innovativesuccess stories in settings as diverse as ruralBangladesh, urban Bolivia, and rural Mali. This is instark contrast to the records of state-run specializedfinancial institutions, which have received largeamounts of funding over the past few decades buthave failed in terms of both financial sustainabilityand outreach to the poor.

6. The availability of better financial products as a resultof experimentation and innovation. The innovationsthat have shown the most promise are solving theproblem of lack of collateral by using group-basedand character-based approaches; solving problems ofrepayment discipline through high frequency ofrepayment collection, the use of social and peerpressure, and the promise of higher repeat loans;solving problems of transaction costs by movingsome of these costs down to the group level and byincreasing outreach; designing staff incentives toachieve greater outreach and high loan repayment;and providing savings services that meet the needs ofsmall savers.

What Are the Risks of Microfinance?

Sound microfinance activities based on best practices playa decisive role in providing the poor with access to finan-cial services through sustainable institutions. However,there have been many more failures than successes:� Some MFIs target a segment of the population thathas no access to business opportunities because of lackof markets, inputs, and demand. Productive credit isof no use to such people without other inputs.

� Many MFIs never reach either the minimal scale orthe efficiency necessary to cover costs.

� Many MFIs face nonsupportive policy frameworks anddaunting physical, social, and economic challenges.

� Some MFIs fail to manage their funds adequatelyenough to meet future cash needs and, as a result,they confront a liquidity problem.

� Others develop neither the financial management sys-tems nor the skills required to run a successful operation.

� Replication of successful models has at times proveddifficult, due to differences in social contexts and lackof local adaptation.Ultimately, most of the dilemmas and problems

encountered in microfinance have to do with how clear theorganization is about its principal goals. Does an MFI pro-vide microfinance to lighten the heavy burdens of poverty?Or to encourage economic growth? Or to help poorwomen develop confidence and become empowered with-in their families? And so on. In a sense, goals are a matterof choice; and in development, an organization can chooseone or many goals—provided its constituents, governancestructure, and funding are all in line with those goals.

About This Book

This handbook was written for microfinance practition-ers, donors, and the wider readership of academics, con-sultants, and others interested in microfinance design,implementation, evaluation, and management. It offers aone-stop guide that covers most topics in enough detailthat most readers will not need to refer to other sources.At first glance it might seem that practitioners and

donors have very different needs and objectives and thuscould not possibly benefit equally from one book.The objectives of many donors who support microfi-

nance activities are to reduce poverty and empower spe-cific segments of the population (for example, women,indigenous peoples). Their primary concerns traditional-ly have been the amount of funds they are able to dis-burse and the timely receipt of requested (and, it ishoped, successful) performance indicators. Donors arerarely concerned with understanding the details ofmicrofinance. Rather, it is often enough for them tobelieve that microfinance simply works.Practitioners need to know how actually to operate a

microfinance institution. Their objectives are to meetthe needs of their clients and to continue to operate inthe long term.Given the purpose of this handbook, it seems to be

directed more toward practitioners than toward donors.However, donors are beginning to realize that MFIcapacity is a more binding constraint than the availability

of funds, making it essential for donors and practitionersto operate from the same perspective if they are to meeteffectively the substantial need for financial services. Infact, if we look briefly at the evolution of microfinance, itis apparent that both donors and practitioners need tounderstand how microfinance institutions operate.When microfinance first emerged as a development tool,

both donors and practitioners focused on the cumulativeamount of loans disbursed, with no concern for how well theloans suited borrower needs and little concern about whetheror not loans were repaid. Donors were rewarded for disburs-ing funds, and practitioners were rewarded for on-lendingthose funds to as many people (preferably women) as possi-ble. Neither was particularly accountable for the long-termsustainability of the microfinance institution or for the long-term effect on borrowers or beneficiaries.Now that the field of microfinance is more mature, it is

becoming clear that effective, efficient, and sustainableinstitutions are needed to provide financial services wellsuited to the demands of low-income clients. Both donorsand practitioners are beginning to be held accountable forresults. The focus is no longer solely on quantity—on theamount disbursed—but on the quality of operations. Thisview is based on the notion that borrowers will buy micro-finance products if they value the service; that is, if theproduct is right for them. Borrowers are now being treatedas clients rather than beneficiaries. Thus if they are to beeffective and truly meet their development objectives,donors must support MFIs that are “doing it right.” Todo so, they need to understand how to both recognize andevaluate a good microfinance provider.As it turns out, both donors and practitioners are real-

ly on the same side—their joint goal is to make availableappropriate services to low-income clients. Therefore, itfalls to donors and practitioners themselves to define bestpractices and to advocate policies that will encouragegrowth, consistency, and accountability in the field. Theintent of this handbook is to provide a basis of commonunderstanding among all stakeholders.

Organization of the Book

The handbook has three parts. Part I, “Issues in Micro-finance Provision,” takes a macroeconomc perspectivetoward general microfinance issues and is primarily non-

technical. Part II, “Designing and Monitoring FinancialProducts and Services,” narrows its focus to the provi-sion of financial intermediation, taking a more technicalapproach and moving progressively toward more specific(or micro) issues. Part III, “Measuring Performance andManaging Viability,” is the most technical part of thehandbook, focusing primarily on assessing the financialviability of MFIs. (These relationships are shown in fig-ure 1.)Part I addresses the broader considerations of microfi-

nance activities, including the supply of and demand forfinancial services, the products and services that an MFImight offer, and the institutions and institutional issuesinvolved. Part I is the least technical part of the hand-book; it requires no formal background in microfinanceor financial theory. Its perspective is more macro thanthat of parts II and III, which provide more detailed“how-to” discussions and are specifically focused on theprovision of financial services only. Part I will be of mostinterest to donors and those considering providing micro-finance. Practitioners may also benefit from part I if theyare considering redefining their market, changing theirinstitutional structure, offering additional services, orimplementing different service delivery methods.Part II, which addresses more specific issues in the

design of financial services (both lending and savings

I N T R O D U C T I O N 5

Figure 1. Relationship between Level of Analysis andTechnical Complexity in this Book

Macro

Micro

Low High

Leve

lofa

nalys

is

Technical complexity

Part IIssues to Consider WhenProviding Microfinance

Part IIDesigning and MonitoringFinancial Products and Services

Part IIIMeasuring Performanceand Managing Viability

6 M I C R O F I N A N C E H A N D B O O K

products) and the development of management informa-tion systems, will be of most interest to practitioners whoare developing, modifying, or refining their financial prod-ucts or systems, and donors or consultants who are evalu-ating microfinance organizations and the appropriatenessof the products and services that they provide. Part IIincorporates some basic financial theory and, accordingly,readers should have a basic understanding of financialmanagement. Readers should also be familiar with using afinancial calculator, computer spreadsheet, or both.Part III provides tools for evaluating the financial health

of an MFI and a means of managing operational issues.The material focuses primarily on financial intermediation(that is, credit and savings services, based on the assump-tion that the main activity of an MFI is the provision offinancial services). Social intermediation and enterprisedevelopment services are not addressed directly. However,basic financial theory that is relevant to the financial man-agement of MFIs delivering these services is provided aswell. The material also underscores the importance of theinterrelationship between serving clients well and movingtowards institutional and financial self-sufficiency. Thesetwo goals serve each other; neither is sufficient on its own.As the most technical section of the handbook, part

III will be of particular interest to practitioners and con-sultants. Donors will also benefit from part III if theywant to understand how MFIs should be adjusting theirfinancial statements and calculating performance indica-tors. While the technical information is fairly basic,some understanding of financial statements and finan-cial analysis is required.The overall purpose of part III is to improve the

level of financial understanding and management inMFI operations. As donors come to understand boththe complexity of microfinance and that it can be deliv-ered in a financially sustainable manner, knowledge ofthe more technical aspects of microfinance will becomeincreasingly important to them in deciding whether tosupport institutions and programs.Each chapter is designed to be used alone or in con-

junction with other chapters, depending on the specificneeds of the reader. A list of sources and additionalreading material is provided at the end of each chapter.Many of the publications listed at the end of each

chapter can be accessed through the following organiza-tions, either by mail or through their Web sites:

ACCION Publications Department733 15th Street NW, Suite 700Washington D.C. 20005Phone: 1 202 393 5113, Fax 1 202 393 5115Web: www.accion.orgE-mail: [email protected]

Calmeadow Resource Center365 Bay Street, Suite 600Toronto, Canada M5H 2V1Phone: 1 416 362 9670, Fax: 1 416 362 0769Web: www.calmeadow.comE-mail: [email protected]

CGAP SecretariatRoom G4-115, The World Bank1818 H Street NWWashington D.C. 20433Phone: 1 202 473 9594, Fax: 1 202 522 3744Web: www.worldbank.org/html/cgap/cgap.htmlE-mail: [email protected]

Micro Finance Network733 15th Street NW, Suite 700Washington D.C. 20005Phone: 1 202 347 2953, Fax 1 202 347 2959Web: www.bellanet.org/partners/mfnE-mail: [email protected]

PACT Publications777 United Nations PlazaNew York, NY 10017Phone: 1 212 697 6222, Fax: 1 212 692 9748Web: www.pactpub.comE-mail: [email protected]

Part I—Issues in Microfinance Provision

Chapter 1–The Country Context provides a frameworkfor analyzing contextual factors. It focuses on issues thataffect the supply of microfinance, including the finan-cial sector, financial sector policies and legal enforce-ment, financial sector regulation and supervision, andeconomic and social policies.

Chapter 2–The Target Market and Impact Analysislooks at the demand for financial services among low-

I N T R O D U C T I O N 7

income populations and presents ways of identifying atarget market based on client characteristics and thetypes of enterprises they operate. It also discusses impactanalysis and how the desired impact affects an MFI’schoice of target market.

Chapter 3–Products and Services considers the variousservices that low-income entrepreneurs might demand,including financial and social intermediation, enterprisedevelopment, and social services. An overview of well-known microfinance approaches is presented in theappendix.

Chapter 4–The Institution discusses the various typesof institutions that can effectively provide and managethe provision of microfinance activities. It addressesissues such as legal structures, governance, and institu-tional capacity, and also provides information on access-ing capital markets for funding.

Part II—Designing and Monitoring Financial Productsand Services

Chapter 5–Designing Lending Products provides informa-tion on how to design or modify lending products formicroentrepreneurs both to meet their needs and toensure financial sustainability of the MFI.

Chapter 6–Designing Savings Products provides infor-mation on the legal requirements to provide savings,types of savings products, and operational considerationsfor providing savings, including pricing. This chapterfocuses on the provision of voluntary savings; it does notaddress forced or compulsory savings often associatedwith lending products.

Chapter 7–Management Information Systems (MIS)presents an overview of effective MIS, includingaccounting systems, loan-tracking systems, and client-impact tracking systems. It also provides a brief discus-sion on the process of installing an MIS and a summaryevaluation of existing software packages.

Part III—Measuring Performance and Managing Viability

Chapter 8–Adjusting Financial Statements presents theadjustments to financial statements that are required toaccount for loan losses, depreciation, accrued interest,inflation, and subsidies. Adjustments are presented intwo groups: standard entries that should be included inthe financial statements and adjustments that restate

financial results to reflect more accurately the financialposition of an MFI.

Chapter 9–Performance Indicators details how to mea-sure and evaluate the financial performance of the MFI,focusing on ratio analysis to determine how successful isthe institution’s performance and which areas could beimproved. In addition, it provides various outreach indi-cators that can be monitored.

Chapter 10–Performance Management presents waysin which to improve the financial and resource manage-ment of microfinance institutions. It discusses delin-quency management, staff productivity and incentives,and risk management, including asset and liability man-agement.

A Necessary Caveat

Microfinance has recently become the favorite interven-tion for development institutions, due to its uniquepotential for poverty reduction and financial sustainabil-ity. However, contrary to what some may claim, micro-finance is not a panacea for poverty alleviation. In fact, apoorly designed microfinance activity can make thingsworse by disrupting informal markets that have reliablyprovided financial services to poor households over thepast couple of centuries, albeit at a high cost.There are many situations in which microfinance is

neither the most important nor the most feasible activi-ty for a donor or other agency to support. Infra-structure, health, education, and other social services arecritical to balanced economic development; and each inits own way contributes to a better environment formicrofinance activities in the future. Care should betaken to ensure that the provision of microfinance istruly demand driven, rather than simply a means to sat-isfy donors’ agendas.

Sources and Further Reading

Gonzalez-Vega, Claudio, and Douglas H. Graham. 1995.“State-Owned Agricultural Development Banks: Lessonsand Opportunities for Microfinance.” Occasional Paper2245. Ohio State University, Department of AgriculturalEconomics, Columbus, Ohio.

Mutua, Kimanthi, Pittayapol Nataradol, and Maria Otero.1996. “The View from the Field: Perspectives fromManagers of Microfinance Institutions.” In Lynn Bennettand Carlos Cuevas, eds., Journal of InternationalDevelopment 8 (2): 195–210.

Paxton, Julia. 1996. “A Worldwide Inventory of Microfinance

Institutions.” Sustainable Banking with the Poor, WorldBank, Washington, D.C.

Women’s World Banking Global Policy Forum. 1995.“The Missing Links: Financial Systems That Work forthe Majority.” Women’s World Banking (April). NewYork.

8 M I C R O F I N A N C E H A N D B O O K

Part I–Issues to Consider WhenProviding Microfinance

11

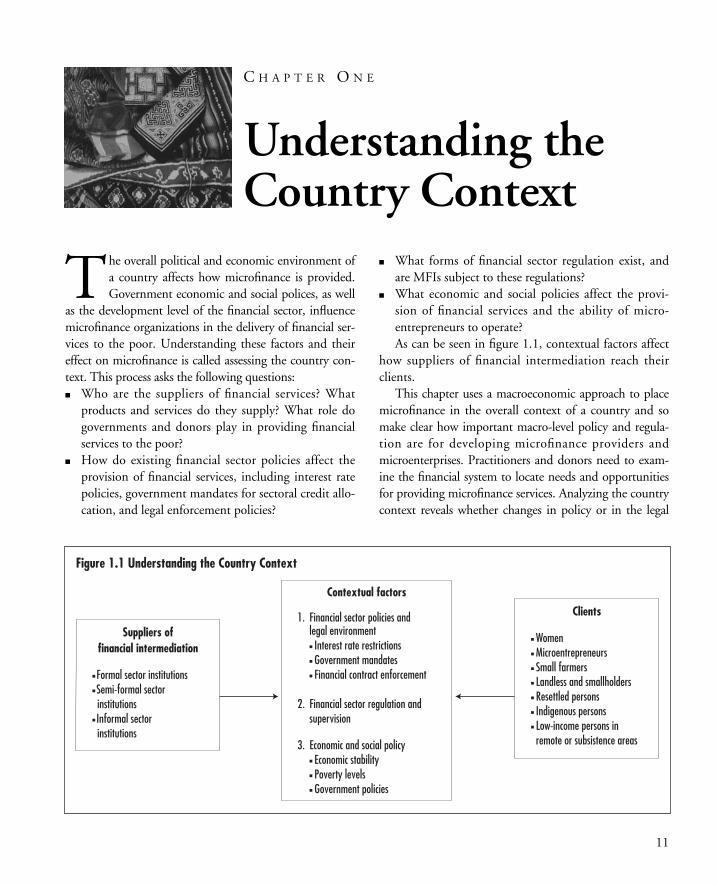

Understanding theCountry Context

C H A P T E R O N E

The overall political and economic environment ofa country affects how microfinance is provided.Government economic and social polices, as well

as the development level of the financial sector, influencemicrofinance organizations in the delivery of financial ser-vices to the poor. Understanding these factors and theireffect on microfinance is called assessing the country con-text. This process asks the following questions:� Who are the suppliers of financial services? Whatproducts and services do they supply? What role dogovernments and donors play in providing financialservices to the poor?

� How do existing financial sector policies affect theprovision of financial services, including interest ratepolicies, government mandates for sectoral credit allo-cation, and legal enforcement policies?

� What forms of financial sector regulation exist, andare MFIs subject to these regulations?

� What economic and social policies affect the provi-sion of financial services and the ability of micro-entrepreneurs to operate?As can be seen in figure 1.1, contextual factors affect

how suppliers of financial intermediation reach theirclients.This chapter uses a macroeconomic approach to place

microfinance in the overall context of a country and somake clear how important macro-level policy and regula-tion are for developing microfinance providers andmicroenterprises. Practitioners and donors need to exam-ine the financial system to locate needs and opportunitiesfor providing microfinance services. Analyzing the countrycontext reveals whether changes in policy or in the legal

Figure 1.1 Understanding the Country Context

Contextual factors

1. Financial sector policies andlegal environmentn Interest rate restrictionsn Government mandatesn Financial contract enforcement

2. Financial sector regulation andsupervision

3. Economic and social policyn Economic stabilityn Poverty levelsn Government policies

Clients

n Womenn Microentrepreneursn Small farmersn Landless and smallholdersn Resettled personsn Indigenous personsn Low-income persons inremote or subsistence areas

Suppliers offinancial intermediation

n Formal sector institutionsn Semi-formal sectorinstitutions

n Informal sectorinstitutions

12 M I C R O F I N A N C E H A N D B O O K

framework are needed to allow more efficient markets toemerge.

Suppliers of Financial Intermediation Services

The first step in understanding the context in which amicrofinance provider operates is to determine whomakes up the financial system.“The financial system (or financial sector, or finan-cial infrastructure) includes all savings and financ-ing opportunities and the financial institutions thatprovide savings and financing opportunities, as wellas the valid norms and modes of behavior related tothese institutions and their operations. Financialmarkets are the markets—supply, demand, and thecoordination thereof—for the services provided bythe financial institutions to the nonfinancial sectorsof the economy.” (Krahnen and Schmidt 1994, 3)To analyze a country’s financial system, it is necessary

to look at both the demand for and the supply of finan-cial services. This section focuses on the supply of finan-cial services; demand will be examined in chapter 2.Understanding a country’s financial system allows

microfinance providers to identify areas in which servicesor products for certain client groups are inadequate ornonexistent. It can also identify institutional gaps and thepotential for partnerships between different types ofinstitutions to reach the poor cost effectively.Intermediaries that provide financial services range

from highly formal institutions to informal moneylen-ders. Understanding the size, growth, number, gover-nance, and supervision of these institutions is animportant part of assessing how the financial systemworks. Financial intermediation varies with the servicesand products provided and depends to some extent onthe type of institution providing the services. Not allmarkets have access to the same services and products.Determining which financial services are currently beingprovided to the differing markets is important in identi-fying unserved or underserved clients.Financial systems can generally be divided into the

formal, semiformal, and informal sectors. The distinctionbetween formal and informal is based primarily onwhether there is a legal infrastructure that providesrecourse to lenders and protection to depositors. Table1.1 outlines the wide range of public and private

providers that can be found in each group. The dividinglines are not absolute, and regulatory structures vary. Forexample, credit unions may fall in the formal sector inone country and in the semiformal sector in another.

Formal financial institutions are chartered by the gov-ernment and are subject to banking regulations andsupervision. They include public and private banks,insurance firms, and finance companies. When theseinstitutions serve smaller businesses or farmers (as is oftenthe case with public sector financial institutions), there ispotential for them to move into the microfinance sector.Within the formal sector, private institutions generally

focus on urban areas, whereas many public institutionsprovide services in both urban and rural areas. Loansfrom private sector institutions are often large individualamounts and are usually allocated to large, established,private, and government-owned enterprises in modernindustrial sectors. Private formal sector institutions typi-cally mobilize the greatest amount of deposits from thegeneral public. Public sector rural institutions often pro-vide agricultural loans as a means of developing the ruralsector. Funding sources include government-distributedand foreign capital, with savings and deposits as sec-ondary sources. Processing of transactions entailsdetailed paperwork and bureaucratic procedures thatresult in high transaction costs, reinforcing the biastoward relatively large loans. Box 1.1 describes the oper-ations and problems of rural financial institutions inMexico.

Semiformal institutions are not regulated by bankingauthorities but are usually licensed and supervised byother government agencies. Examples are credit unionsand cooperative banks, which are often supervised by abureau in charge of cooperatives. (NGOs are sometimesconsidered part of the semiformal sector, because theyare often legally registered entities that are subject tosome form of supervision or reporting requirements.)These financial institutions, which vary greatly in size,typically serve midrange clients associated by a profes-sion or geographic location and emphasize depositmobilization.Semiformal institutions provide products and services

that fall somewhere between those offered by formal sec-tor and informal sector institutions. The design of theirloan and savings products often borrows characteristicsfrom both sectors. In many countries semiformal insti-tutions often receive donor or government support

through technical assistance or subsidies for theiroperations.

Informal financial intermediaries operate outsidethe structure of government regulation and supervi-sion. They include local moneylenders, pawnbrokers,self-help groups, and NGOs, as well as the savings offamily members who contribute to the microenter-prise. Often they do not comply with common book-keeping standards and are not reflected in officialstatistics on the depth and breadth of the nationalfinancial sector. Knowing where and how these finan-cial sources operate helps determine what services arein demand.These institutions concentrate on the informal

sector—on loans and deposits for small firms and house-holds. Often loans are granted without formal collateralon the basis of familiarity with the borrower. Social

sanctions within a family, a village, or a religious com-munity substitute for legal enforcement. Credit termsare typically adapted to the client’s situation. The totalamount lent, as well as the number and the frequency ofinstallments, is fitted to the borrower’s expected cashflow. Little if any paperwork is involved in applying fora loan (Krahnen and Schmidt 1994, 32).Depending on historical factors and the country’s

level of economic development, various combinations ofthese suppliers are present in the financial sectors ofdeveloping countries. Research increasingly shows thatthe financial sector is complex and that there are sub-stantial flows of funds between subsectors. Identifyingthe suppliers of financial services in a given country orregion leads to a greater understanding of the financialsystem and also reveals gaps for a microfinance providerto address.

U N D E R S T A N D I N G T H E C O U N T R Y C O N T E X T 13

Table 1.1 Providers of Financial Intermediation Services

Formal sector Semiformal sector Informal sector

Central bank Savings and credit cooperatives Savings associations

Banks Multipurpose cooperatives Combined savings and creditCommercial banks associations—rotating savings andMerchant banks Credit unions credit associations andSavings banks variantsRural banks Banques populairesPostal savings banks Informal financial firmsLabor banks Cooperative quasi-banks Indigenous bankersCooperative banks Finance companies

Employee savings funds Investment companiesDevelopment banksState-owned Village banks Nonregistered self-help groupsPrivate

Development projects Individual moneylendersOther nonbank institutions CommercialFinance companies Registered self-help groups and savings clubs NoncommercialTerm-lending institutions (friends, neighbors, relatives)

Nongovernmental organizations (NGOs)Building societies and credit unions Traders and shopkeepers

Contractual savings institutions NGOsPension fundsInsurance companies

MarketsStocksBonds

Source: Food and Agriculture Organization 1995, 5.

Existing Microfinance Providers

Microfinance providers are found in both the publicand the private sectors. To identify market gaps whenproviding or considering providing financial services tomicroentrepreneurs, it is important to determine whothe existing providers are and how well the needs ofthe market are being met. Donors can determine whois active in microfinance and who might require sup-port or funding. In areas where there is no microfi-nance activity, practitioners can determine who theircompetitors are and the effects they have on the mar-ketplace (such as developing awareness, increasing

demand, oversupplying, saturating or distorting themarket).

THE EFFECT OF GOVERNMENT PROGRAMS ON PRIVATE PRO-VIDERS. Depending on their approach, government-runmicrofinance programs can either contribute to or be detri-mental to successful microfinance activities. Governmentsthat operate subsidized, inefficient microfinance programsthrough health, social services, or other nonfinancial state-run ministries or departments (or through a state-run bank-ing system) negatively influence the provision of sustainablemicrofinance services (see box 1.2). Governments oftenhave little or no experience with implementing microfi-

14 M I C R O F I N A N C E H A N D B O O K

IN 1994 AND 1995 A WORLD BANK TEAM CONDUCTED AN

economic and sector study in Mexico to examine the effi-ciency and fairness of rural financial markets. The team con-ducted case studies of 96 nonbank lenders, plus a householdsurvey of 800 rural entrepreneurs and a review of the regula-tory framework for the uniones de crédito (credit unions) andthe sociedades de ahorro y préstamo (savings and loan compa-nies). All forms of formal and informal savings and loan ser-vices were analyzed.The study provided strong evidence about the poor per-

formance of rural financial markets in Mexico. These mar-kets proved to be shallow (only 45 percent of ruralentrepreneurs received a credit transaction during 1992-94),segmented, noncompetitive, inefficient, and inequitable(showing strong biases against disadvantaged individuals).The consequence was a weak supply of credit. The main rea-sons for this situation were underdeveloped institutionalinfrastructure (two-thirds of the municipalities have no bankoffices), inappropriate banking technologies for small mar-kets, and attenuated property rights. Past government inter-vention characterized by debt forgiveness and subsidizedinterest rates had contributed to the bad image of ruralfinance. Few bankers from the private sector truly believedthere was a business opportunity in this field. On thedemand side, 75 percent of the households interviewed hadnever requested a loan from the formal financial sector.Rural entrepreneurs felt this would be too risky, given theexcessive amount of collateral required and the noninstitu-tional techniques used to enforce contracts. Many entrepre-neurs admitted that they were afraid of formal institutionsand that they were unwilling to pay high transaction costs.

As a consequence of the inefficiency of rural financial mar-kets, the funds did not flow to the best uses, hindering ruraldevelopment in Mexico.The study convinced the government of Mexico to ask

the World Bank team to propose measures that would helpdevelop rural financial markets. The first measure proposedwas to expand the distribution network, introduce adequatefinancial products and technologies, and carry out organiza-tional reforms, including the introduction of incentives andinternal controls. The second was to improve environmentalconditions by developing better policies and regulations on abroad range of issues, such as secured transactions and theregulation of intermediaries (mostly nonbanks) and of relat-ed markets such as insurance.A pilot operation was designed to set up a network of

bank branches in localities of fewer than 20,000 inhabitantsin which no formal financial intermediary was present. Thefirst step was to convince commercial banks that there is abusiness opportunity in rural financial markets. The messagewas that profitability is possible if five conditions are met.First, banks must have a good understanding of their marketand offer simple financial products, such as deposits withshort maturities and small minimum balances, as well asshort-term credit lines. Second, they must keep their fixedcosts low, with minimum investments and two to fouremployees. Third, they must lend on the basis of a client’scharacter and reputation. Fourth, they must develop con-ducive incentive schemes, encouraging profit sharing andefficiency wages. Finally, their internal control mechanismsmust be credible, and there must be a credible threat of dis-missal for nonperforming staff.

Box 1.1 Formal Sector Suppliers in Rural Mexico

Source: Chaves and Sanchez 1997.

nance programs and no incentive to maintain long-termsustainability. Also, government microfinance programs areoften perceived as social welfare, as opposed to economicdevelopment efforts. Some government programs grow toolarge, without the necessary institutional base, and fail tocoordinate efforts with local NGOs or self-help groups.Governments that forgive existing debts of the poor

to state banks can have a tremendous effect on privatesector MFIs, whose borrowers may mistakenly under-stand that their loans need not be repaid either. In gen-eral, both donors and practitioners should determine theconsequences of existing or past credit subsidies or debtforgiveness (see box 1.3).Much discussion surrounds the involvement of gov-

ernment in the provision of microfinance. Some peopleargue that the government’s role is to create an enablingenvironment for the success of both microenterprises and

private sector microfinance organizations and that govern-ments should not lend funds directly to the poor. Othersargue that the government should provide financial ser-vices to microentrepreneurs but must do so on a commer-cial basis to provide continued access to microfinance andto avoid distorting the financial markets. Some advan-tages of government involvement include the capacity todisseminate the program widely and obtain political sup-port, the ability to address broader policy and regulatoryconcerns, and the capacity to obtain a significant amountof funds (Stearns and Otero 1990). A good example of asuccessfully run government operation is the Bank RakyatIndonesia, a profitable state bank in Indonesia that serveslow-income clients (box 1.4).

U N D E R S T A N D I N G T H E C O U N T R Y C O N T E X T 15

Box 1.2 Do Microfinance Clients Need SubsidizedInterest Rates?

MICROFINANCE CLIENTS TEND TO BORROW THE SAME

amount even if the interest rate increases, indicating that,within a certain range, they are not interest rate sensitive.In fact, people are often willing to pay higher rates forbetter service. Continued and reliable access to credit andsavings services is what is most needed.Subsidized lending programs provide a limited volume

of cheap loans. When these are scarce and desirable, theloans tend to be allocated predominantly to a local elitewith the influence to obtain them, bypassing those whoneed smaller loans (which can usually be obtained com-mercially only from informal lenders at far higher interestrates). In addition, there is substantial evidence fromdeveloping countries worldwide that subsidized ruralcredit programs result in high arrears, generate losses bothfor the financial institutions administering the programsand for the government or donor agencies, and depressinstitutional savings and, consequently, the developmentof profitable, viable rural financial institutions.Microfinance institutions that receive subsidized fund-

ing are less likely to effectively manage their financial per-formance, since they have little or no incentive to becomesustainable. Subsidized interest rates create excess demandthat may result in a form of rationing through privatetransactions between clients and credit officers.

Source: Robinson 1994.

Box 1.3 Credit Institutions as a Political Tool:Debt Forgiveness in India

RURAL FINANCIAL INSTITUTIONS THAT ARE ASSOCIATED WITHgovernments often become the target of politicians. Theinfluential clientele of these institutions makes them particu-larly attractive political targets. India’s government-appointedAgricultural Credit Review Committee reported in 1989:During the election years, and even at other times,there is considerable propaganda from politicalplatforms for postponement of loan recovery orpressure on the credit institutions to grant exten-sions to avoid or delay the enforcement process ofrecovery. In the course of our field visits, it wasoften reported that political factors were responsiblefor widespread defaults on the ostensible plea ofcrop failures in various regions.The “willful” defaulters are, in general, socially

and politically important people whose example oth-ers are likely to follow; and in the present democraticset-up, the credit agencies’ bureaucracy is reluctant totouch the influential rural elite who wield much for-mal and informal influence and considerable power.Farmers’ agitation in many parts of the country cantake a virulent form, and banners are put up in manyvillages declaring that no bank officer should enterthe village for loan recovery purposes. This dampensthe enthusiasm of even the conscientious members ofthe bank staff working in rural areas in recoveryefforts. The general climate, therefore, is becomingincreasingly hostile to recoveries.

Source: Yaron, Benjamin, and Piprek 1997, 102.

THE EFFECT OF PRIVATE MICROFINANCE PROVIDERS ON

OTHER SUPPLIERS. Private sector MFIs are often indige-nous groups or NGOs operated by local leaders in theircommunities. They are frequently supported by interna-tional donors and international NGOs that providetechnical assistance or funding, particularly in the start-up phase. Some private MFIs still subsidize interest ratesor deliver subsidized services; others create self-sufficientoperations and rely less and less on external donorfunds. A few are beginning to access funding throughcommercial banks and international money markets. Inaddition to NGOs, both banks and nonbank financialintermediaries may provide financial services to themicrosector.Private sector MFIs that have operated in or are cur-

rently operating in the country or region influence thesuccess of new providers by establishing client (or bene-ficiary) expectations. For example, in Bangladesh theGrameen Bank is so well known within the village pop-ulation that other microfinance providers routinelyadopt the Grameen lending model, and when GrameenBank changes its interest rate or adds a new product,clients of other MFIs demand the same. Microfinanceorganizations should be aware of the services offered byother MFIs and the effects they may have on the effec-tive delivery of financial services (see table 1.2).

What Role Do Donors Play in Microfinance?

Donors’ interest in microfinance has increased substan-tially over the past few years. Virtually all donors,including local, bilateral, and multilateral governmentdonors and local and international NGOs, supportmicrofinance activities in some way, providing one ormore of the following services:� Grants for institutional capacity building� Grants to cover operating shortfalls� Grants for loan capital or equity� Concessional loans to fund on-lending� Lines of credit� Guarantees for commercial funds� Technical assistance.Because donors are the primary funders of microfi-

nance activities (since most MFIs do not collect savingsand are not yet financially viable enough to access com-mercial funding), the approach they take to microfi-nance and the requirements they set for MFIs to accessfunding can greatly affect the development of the fieldof microfinance. Most donors have moved away fromsubsidized lending and are focusing more on capacitybuilding and the provision of loan capital. However,there is a variety of microfinance providers and a varietyof approaches taken by donors. In fact, most MFIs work

16 M I C R O F I N A N C E H A N D B O O K

THE BANK RAKYAT INDONESIA, A STATE-OWNED BANK, RANa program of directed subsidized credit for rice farmers until1983. The unit desa system was established in 1984 as aseparate profit center within the bank.The unit desa system is a nationwide network of small

village banks. The founding objectives were to replacedirected agricultural credit with broad-based credit for anytype of rural economic activity, to replace subsidized creditwith positive on-lending rates with spreads sufficient tocover all financial and operational intermediation costs, andto provide a full range of financial services (savings as well ascredit) to the rural population. All these objectives were metwithin just a few years. The system’s phenomenal success insavings mobilization is its distinguishing achievement.Although the unit desa system forms an integral part of

the Bank Rakyat Indonesia, it operates as a separate profit

center, and its management has a free hand in determiningits interest rates and other operating policies. In the 1980sthe Indonesian government implemented financial sectorreforms that deregulated certain interest rates and abolishedinterest rate ceilings. As the unit desa system struggled tobecome financially self-sustainable, market forces drove itsdecisionmaking and it became increasingly subject to com-petition from other financial institutions.Management has a high degree of autonomy and full

accountability for the performance of the unit desa system.This accountability is pushed down the line; every unit isresponsible for its own lending decisions and profits.Monetary staff incentives and the prospects of promotionreinforce individual accountability. Reforms to furtherenhance the unit desa system’s autonomy are currently beingstudied.

Box 1.4 Microfinance in Indonesia

Source: Yaron, Benjamin, and Piprek 1997.

with more than one donor, often developing separateproducts to meet each donor’s requirements.While it is true that donors should avoid duplicating

and (especially) contradicting each other’s efforts, it is dif-ficult to ensure that donors coordinate their efforts andcreate perfectly consistent strategies based on market seg-mentation and comparative advantages. Particularlybecause microfinance is perceived by some as a panaceafor poverty alleviation, donors may want to take on thesame kinds of activities, especially lending to the poorestof the poor. Meanwhile, areas in which donors may havereal advantages, such as capacity building and policy dia-logue, are greatly in need of resources. Indeed, a danger ofwidespread donor interest in microfinance is an oversup-ply of funds for on-lending in the face of limited institu-tional capacity to take on these funds.Some donors, such as the multilateral organizations,