project financial appraisal skills- finance for non financial managers course

TRANSCRIPT

www.businessservicessupport.com

PROJECT FINANCIAL APPRAISAL

TECHNIQUES- PART OF OUR ADVANCED

FINANCE FOR NON FINANCIAL MANAGERS

COURSE PROGRAMME

COPYRIGHT© TO BUSINESS SERVICES SUPPORT LIMITED 2011

KEY OBJECTIVES

What is financial evaluation

Why project financial evaluation techniques

Project financial risks assessment

Practice illustration of financial plan

2

COPYRIGHT© TO BUSINESS SERVICES SUPPORT LIMITED 2011

DEFINITION OF FINANCIAL EVALUATION

Concern with the assessment of financial viability of projects

Assessment of risk profile and financial efficiency

3

COPYRIGHT© TO BUSINESS SERVICES SUPPORT LIMITED 2011

WHY PROJECT FINANCIAL EVALUATION

Does the project create financial wealth

How quickly can we recover project investment

How risky is the project vis a viv it returns potentials

How much capital do we need to invest

4

COPYRIGHT© TO BUSINESS SERVICES SUPPORT LIMITED 2011

Demand Risk

Competition Risk

Financial Risk

Operational Risk

Interest Rate Risk

FINANCIAL RISKS FACING PROJECTS

5

COPYRIGHT© TO BUSINESS SERVICES SUPPORT LIMITED 2011

FINANCIAL EVALUATION TECHNIQUES FOR

EFFECTIVE PROJECT MANAGEMENT

6

Payback PeriodReturn On Investment

Profit Based Measures

Net Present Value Method

COPYRIGHT© TO BUSINESS SERVICES SUPPORT LIMITED 2011

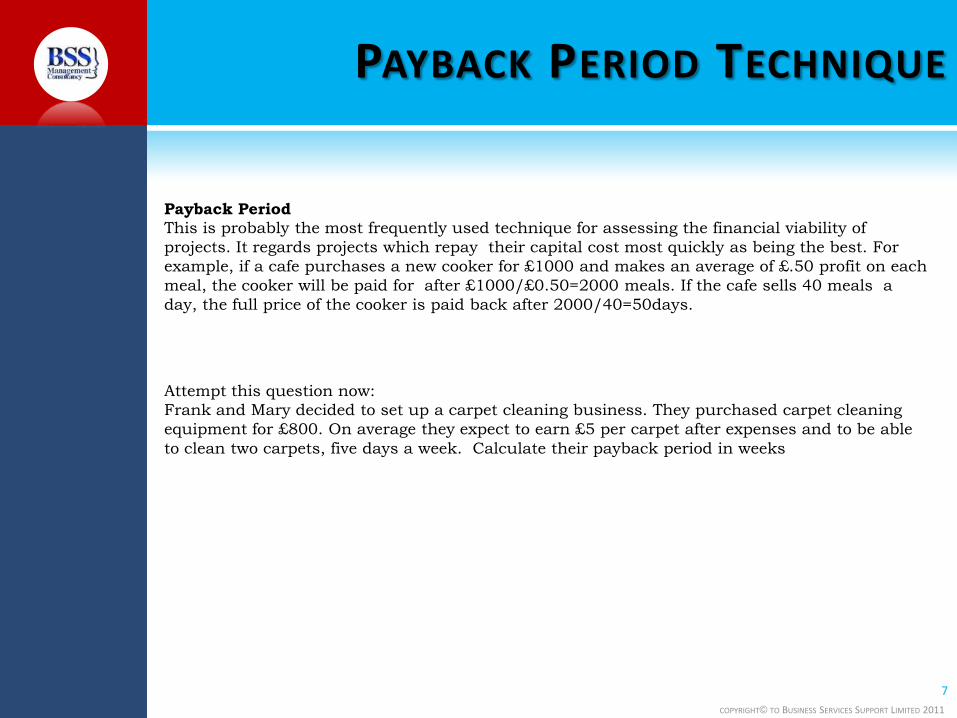

PAYBACK PERIOD TECHNIQUE

7

Payback Period

This is probably the most frequently used technique for assessing the financial viability of

projects. It regards projects which repay their capital cost most quickly as being the best. For

example, if a cafe purchases a new cooker for £1000 and makes an average of £.50 profit on each

meal, the cooker will be paid for after £1000/£0.50=2000 meals. If the cafe sells 40 meals a

day, the full price of the cooker is paid back after 2000/40=50days.

Attempt this question now:

Frank and Mary decided to set up a carpet cleaning business. They purchased carpet cleaning

equipment for £800. On average they expect to earn £5 per carpet after expenses and to be able

to clean two carpets, five days a week. Calculate their payback period in weeks

COPYRIGHT© TO BUSINESS SERVICES SUPPORT LIMITED 2011

PAYBACK PERIOD TECHNIQUE

8

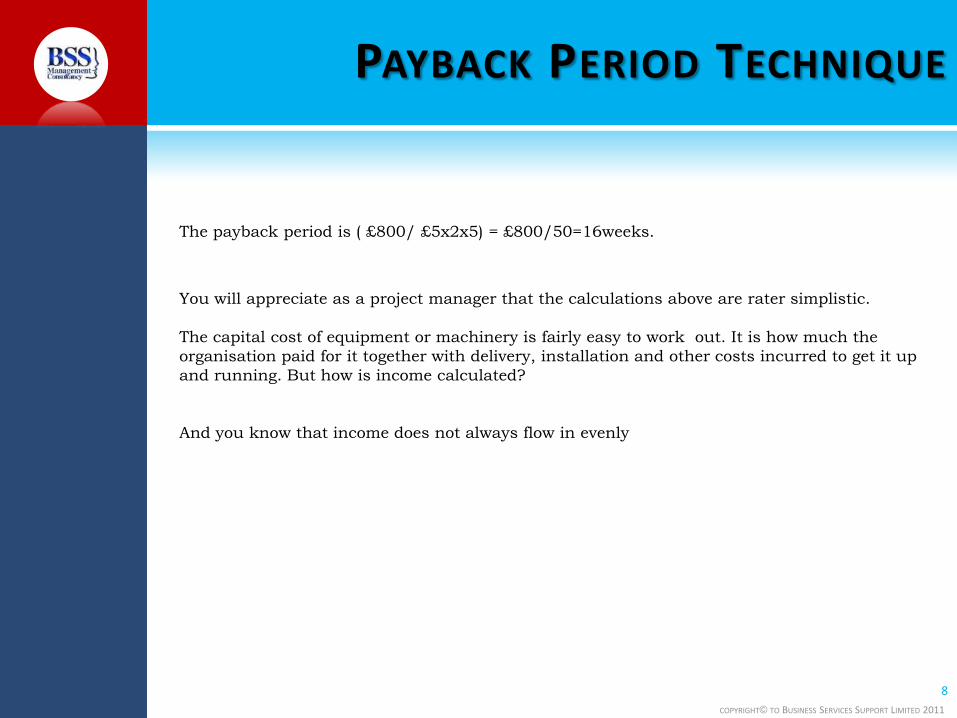

The payback period is ( £800/ £5x2x5) = £800/50=16weeks.

You will appreciate as a project manager that the calculations above are rater simplistic.

The capital cost of equipment or machinery is fairly easy to work out. It is how much the

organisation paid for it together with delivery, installation and other costs incurred to get it up

and running. But how is income calculated?

And you know that income does not always flow in evenly

COPYRIGHT© TO BUSINESS SERVICES SUPPORT LIMITED 2011

PROJECT MANAGEMENT – REVENUE

& COST PROJECTIONS

9

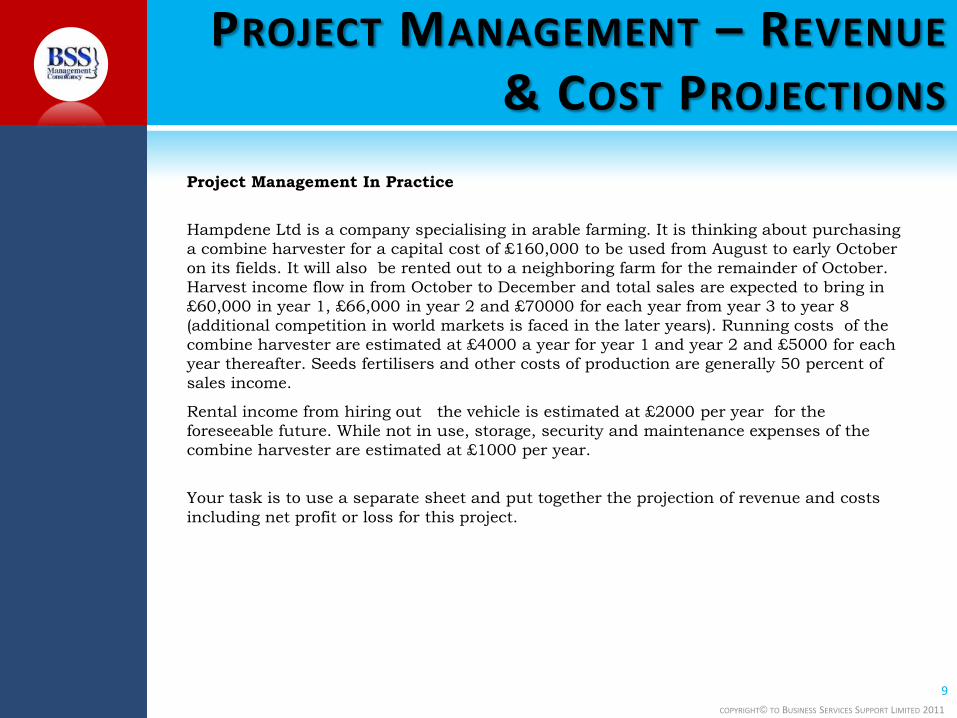

Project Management In Practice

Hampdene Ltd is a company specialising in arable farming. It is thinking about purchasing

a combine harvester for a capital cost of £160,000 to be used from August to early October

on its fields. It will also be rented out to a neighboring farm for the remainder of October.

Harvest income flow in from October to December and total sales are expected to bring in

£60,000 in year 1, £66,000 in year 2 and £70000 for each year from year 3 to year 8

(additional competition in world markets is faced in the later years). Running costs of the

combine harvester are estimated at £4000 a year for year 1 and year 2 and £5000 for each

year thereafter. Seeds fertilisers and other costs of production are generally 50 percent of

sales income.

Rental income from hiring out the vehicle is estimated at £2000 per year for the

foreseeable future. While not in use, storage, security and maintenance expenses of the

combine harvester are estimated at £1000 per year.

Your task is to use a separate sheet and put together the projection of revenue and costs

including net profit or loss for this project.

COPYRIGHT© TO BUSINESS SERVICES SUPPORT LIMITED 2011

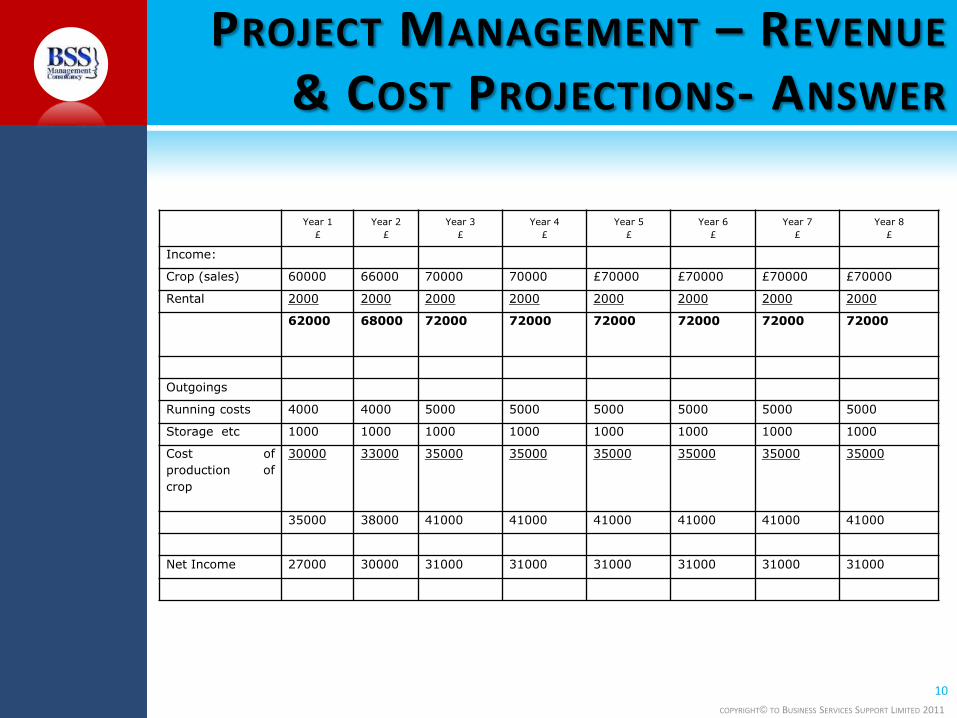

PROJECT MANAGEMENT – REVENUE

& COST PROJECTIONS- ANSWER

10

Year 1

£

Year 2

£

Year 3

£

Year 4

£

Year 5

£

Year 6

£

Year 7

£

Year 8

£

Income:

Crop (sales) 60000 66000 70000 70000 £70000 £70000 £70000 £70000

Rental 2000 2000 2000 2000 2000 2000 2000 2000

62000 68000 72000 72000 72000 72000 72000 72000

Outgoings

Running costs 4000 4000 5000 5000 5000 5000 5000 5000

Storage etc 1000 1000 1000 1000 1000 1000 1000 1000

Cost of

production of

crop

30000 33000 35000 35000 35000 35000 35000 35000

35000 38000 41000 41000 41000 41000 41000 41000

Net Income 27000 30000 31000 31000 31000 31000 31000 31000

COPYRIGHT© TO BUSINESS SERVICES SUPPORT LIMITED 2011

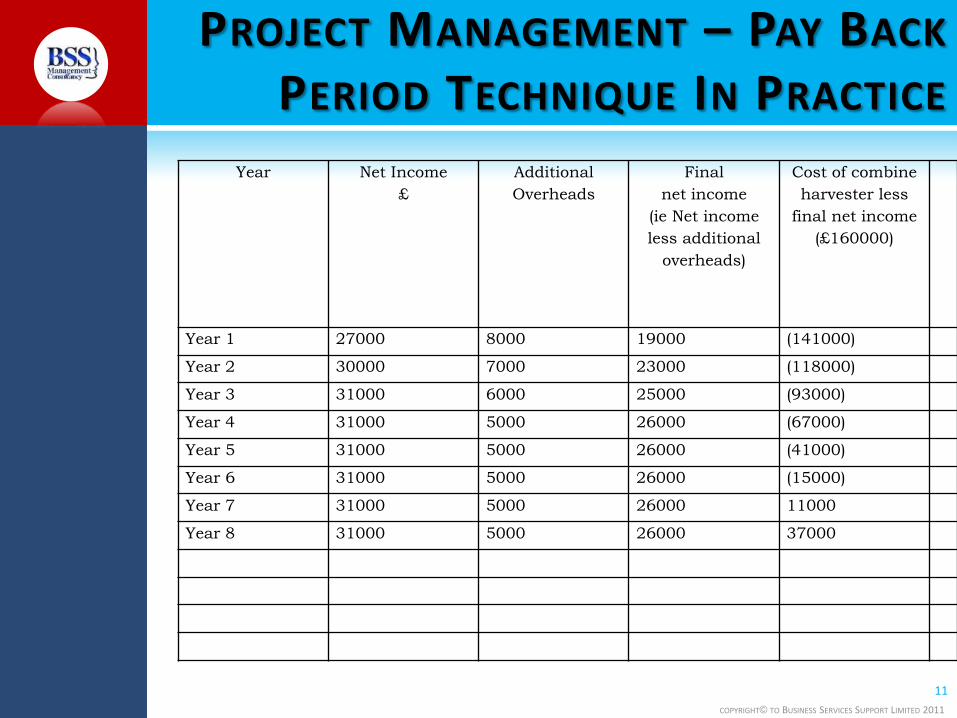

PROJECT MANAGEMENT – PAY BACK

PERIOD TECHNIQUE IN PRACTICE

11

Year Net Income

£

Additional

Overheads

Final

net income

(ie Net income

less additional

overheads)

Cost of combine

harvester less

final net income

(£160000)

Year 1 27000 8000 19000 (141000)

Year 2 30000 7000 23000 (118000)

Year 3 31000 6000 25000 (93000)

Year 4 31000 5000 26000 (67000)

Year 5 31000 5000 26000 (41000)

Year 6 31000 5000 26000 (15000)

Year 7 31000 5000 26000 11000

Year 8 31000 5000 26000 37000

COPYRIGHT© TO BUSINESS SERVICES SUPPORT LIMITED 2011

PROJECT MANAGEMENT –NET

PRESENT VALUE TECHNIQUE V TIME

12

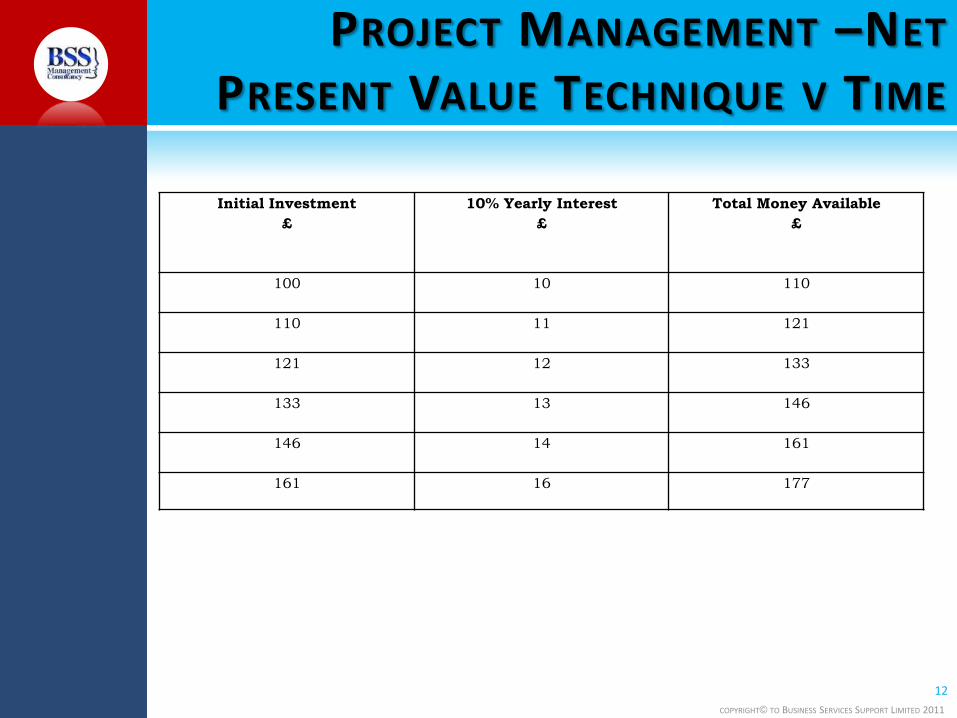

Initial Investment

£

10% Yearly Interest

£

Total Money Available

£

100 10 110

110 11 121

121 12 133

133 13 146

146 14 161

161 16 177

COPYRIGHT© TO BUSINESS SERVICES SUPPORT LIMITED 2011

PROJECT MANAGEMENT –NET

PRESENT VALUE TECHNIQUE V TIME

13

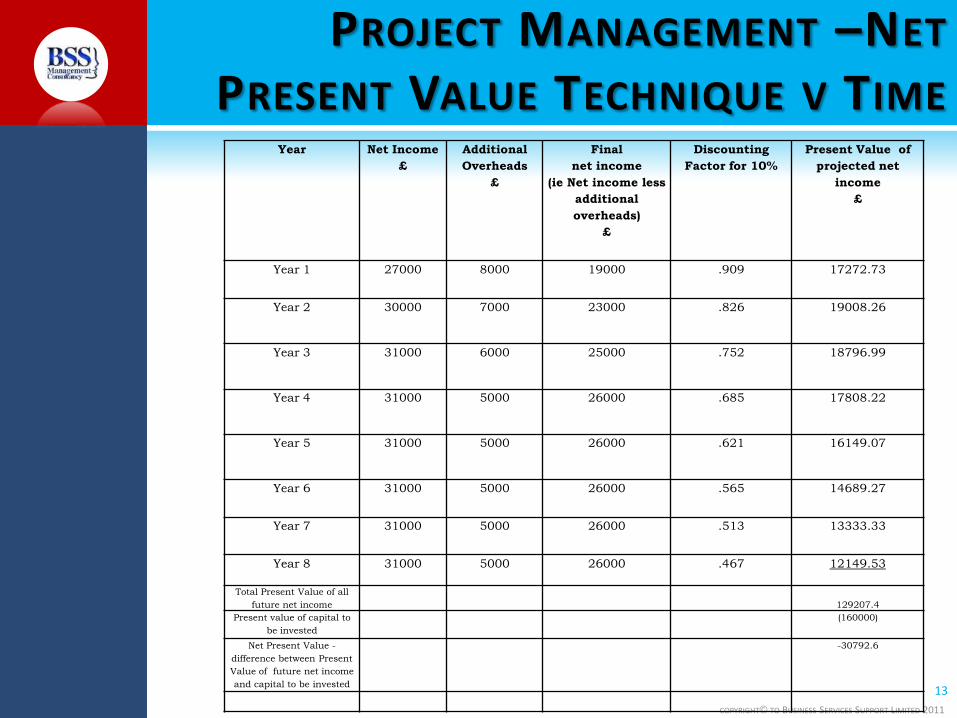

Year Net Income

£

Additional

Overheads

£

Final

net income

(ie Net income less

additional

overheads)

£

Discounting

Factor for 10%

Present Value of

projected net

income

£

Year 1 27000 8000 19000 .909 17272.73

Year 2 30000 7000 23000 .826 19008.26

Year 3 31000 6000 25000 .752 18796.99

Year 4 31000 5000 26000 .685 17808.22

Year 5 31000 5000 26000 .621 16149.07

Year 6 31000 5000 26000 .565 14689.27

Year 7 31000 5000 26000 .513 13333.33

Year 8 31000 5000 26000 .467 12149.53

Total Present Value of all

future net income 129207.4

Present value of capital to

be invested

(160000)

Net Present Value -

difference between Present

Value of future net income

and capital to be invested

-30792.6

COPYRIGHT© TO BUSINESS SERVICES SUPPORT LIMITED 2011

CONCLUSION – THE END

For more information about our courses visit:

http://www.businessservicessupport.com

14