productivity and profitability analysis of banking sector ...3)-jul2015/ijems vol6(3)-4.pdf ·...

TRANSCRIPT

I.J.E.M.S., VOL.6 (3) 2015: 124 - 148 ISSN 2229-600X

124

PRODUCTIVITY AND PROFITABILITY ANALYSIS OF BANKING SECTORIN INDIA: IN THE POST RE-FORM PERIOD

Jena Rupak KumarDepartment of Accounting and Finance, Ministry of Education Ethiopia, Mettu University

Corresponding Authors Email: [email protected]

ABSTRACTThe present study is an attempt to examine the total productivity and profitability growth in Indian banking sector during 1991-1992 to 2010-2011. The data of four bank groups (SBI group, nationalized bank group, private sector bank group and foreignbank group) for twenty years has been collected from the official website of reserve bank of India, financial analysis of banks,performance high lights of different category of banks, IBA etc.. The productivity index data analyses are being used to measurethe productivity and profitability in four sectors banks over the years.

The empirical result show that the profitability analysis of the four sample bank groups have been undertaken by dividingthe twenty year period under study into two distinct phases; the first phase covering ten years and second phase comprising thelatter ten years. The analysis has been done through an analytical framework so as to find out the factors affecting profitability.This framework splits the income and expenditure statement to find out the relation between different components of incomeand expenditure and its impact on profitability. Basically, spread, difference between interests earned and interest paid andburden play major role in determining the profitability of a commercial bank. Both spread and burden are treated as primary onfirst associate factor. Factors which determine this primary factor are treated as secondary factor. Factors which determine theirsecondary factors are known as tertiary factor. The factors which influence this tertiary factor are termed as fourth associatefactors. The framework adopted for the purpose of analysis have spread, burden and its components are to be related to acommon denominator, volume of business (V) and to convert these into ratio. Establishment ratio is derived by dividing payoutper employee (M1) by volume of business per employee (M2).

Analysis of total sample (average of all four sample groups) during second phase reveals that fall in establishment expenses,fall in other expenses and rise in other income ratio are the major determinant and main contributors to profitability. However,fall in spread ratio had a negative impact on profitability. So, increase in volume of business, control over other expenses andincrease in fee-based business of banking sector have a positive impact on the profitability of the banking sector during the postreform era. Sample group wise, S.B.I. bank group has improved profitability ratio due to fall in establishment ratio, fall in otherexpenses ratio. In this case, spread and other income have made negative contribution to the profitability ratio. Here the key toprofitability is volume of business, check on other expenses and increase in commission based income. Analysis of nationalizedbank group indicates that both establishment ratio and other expenses ratio declined in the second phase. Over the same periodother income ratio also increased. Contrary to expectations, spread influenced negatively to the profitability ratio. Profitabilityof nationalized bank group improved in the second phase only due to positive contribution by burden ratio. So, increased volumeof business, check on other expenses and increase non-fund based business are the main contributors to the profitability ratio ofnationalized bank group.

Analysis undertaken for sample private sector bank group depicts that decrease in establishment ratio and increase in otherincome ratio made it possible to improve profitability for this group in the second phase despite negative support by spread andother expenses ratio. So, volume of business and fee-based income are main determinants of profitability in case of sampleprivate sector banks. Perusal of framework for analysis of foreign bank group indicates that spread and establishment expensescontributed negatively to the profitability in the second phase. But decrease in other expenses and increase in other income ratioare the main factors which improved profitability ratio of foreign bank group in the second phase of our study. Despite negativecontribution by establishment expenses ratio, burden ratio decreased in the second phase due to support of other expenses andincome ratio and profitability improved in a situation where spread, the interest income, went down to create negativecontribution on profitability. So, key to profitability in case of foreign bank group is proper handling of burden ratio.

Comparative study of all four groups reveals that in- spite of fall in spread ratio in the entire sample four bank groups in thesecond decade of the study period, profitability had improved in the second phase. None of the four sample bank groupsdeepened on spread ratio which is widely considered as the main determinant of profitability ratio of a bank. All the samplebank groups, alternatively stressed on the proper management of burden to increase profitability. Thus it is revealed that whencompulsive reasons does not allow enhancement of the spread volume by the banks, profitability can be improved with proper

Productivity and profitability analysis of banking sector in India

125

handling and managing of burden. So under Indian financial environment burden management seems to be an important strategyfor enhancing profitability along with successful discharge of social responsibility.

Keywords: Productivity and Profitability, Private and Public Sector Bank.

INTRODUCTIONA sound financial infrastructure is a pre-requisite for economicdevelopment. Commercial banks are the most importantsegment of the financial system. Financial sector plays a verycrucial role in the economic growth of a country. Theimportance of this sector’s contribution is more in a developingeconomy like India. Indian banking sector is like fuel providerto the Indian economy and is contributing so much towardsoverall growth of the economy. This sector has envisagedtremendous growth overtimes and gets a completely differentand advanced look in present times. International access,increased no. of banks, improved technology like e-banking,m-banking and t-banking itself tells the changing story ofIndian banking sector. At present, different kind of banks likepublic sector banks, private sector banks and foreign banks areoperating efficiently in the country. The era of globalizationhas also altered the structure and functioning of banking sectorin India. Soundness of the banking sector is synonymous withefficiency, productivity, profitability, stability and a shock freeenvironment of economy. According to RBI, Banks lubricatethe wheels of the real economy, are the conduits of monetarypolicy transmission and constitute the economy’s payment andsettlement system.

After Independence, the banking sector in India was not ina very good position. There was need to revive the wholeeconomy and it was not possible without a strong andcompetent banking sector. The banking sector has passedthrough different phases in India. 1969 was the era ofNationalization when major banks of India were nationalized.The Government also faced the balance of payment crisisin 1991 – 92 following which a stabilisation programmewas initiated with the help of International Monetary Fund(IMF) which specially included reform of the IndianFinancial System (IFS). After that, Government of Indiaset up a Committee under the Chairmanship of M.Narashimham popularly known as Narashimham Committeewho submitted its report in 1992. The report primarily aimedat enhancing the productivity, efficiency and profitabilityof the banking system in the country. Hence the committeerecommended far-reaching reforms in both structural andfunctional approach of the Indian banking system in orderto enhance their efficiency, productivity and profitability.The Narashimham Committee recommendations ware aimedat ensuring a degree of operational flexibility, internalautonomy for the public sector banks in their decision makingprocess and greater degree of professionalism in bankingoperations. Accordingly, the overall functioning of the bankingindustry, administrative, asset management, investment humanresources and so on has been undergoing in metamorphosis inrecent years. In the emerging financial scenario, competition,productivity, profits are no longer a taboo for the commercialbanks in India.

Further, the second phase of reform introduced in 1998was based on the recommendation of the Committee on theBanking Sector Reform and, Shri M. Narasimham was the

Chairman of this Committee. This phase of reform focusedmainly on structural measure and improvement of disclosurestandard and level of transparency so as to align Indianstandards with the internationally recognized best practices.All the above changes have added significantly to theperformance of Indian banking sector. Both the committeereports have been accepted and are being implement in aphased manner, the main thrust being strengthening the Indianbanking sector and make it globally competitive.. Presentlynew and improved techniques and research are used and thesame has entirely changed the functioning of Indian BankingSector.

PRODUCTIVITY IN BANKING SECTORProductivity is one of the very important indicators to assessthe economic performance of an economy. In simple termsproductivity is the ratio of output to input which means outputper unit produced for every unit of input used. Productivity isthe relationship between physical outputs of one or morephysical inputs used in production (Kopleman).

Productivity = total output / total input

When productivity is studied related to one factor is termed asfactor productivity. Like labour productivity or capitalproductivity. When all the factors are together studied it istermed as total factor productivity. Inputs and Outputs aredifferent in banking sector as compared to other sectorsbecause banks are mainly service providers. The products inthe banking sector are different than other sectors and includedeposits, borrowings, Interest etc. So study of productivity inbanking sector is different as it is studied in other sectors of theeconomy.

REVIEW OF LITERATUREThe present research is an attempt to analyse the comparativeefficiency and competitiveness of Indian commercial banks.As a matter a matter of fact, the efficiency of the banking sectoris one of the important economic agenda for governments allover the world. The main impulsion for this study has been therecommendation and implementation of the NarashimhamCommittee reports of 1991 and 1998 by the Government ofIndia in the banking sector reforms so as to strengthen theIndian banking system and make it globally competitive. Thisclearly requires that the relative efficiency of the bankingsector in India is examined. The present study thereforeexamines that efficiency of the banking sector by using thepopular productivity and profitability analysis of commercialbanks on India covering the post-reform period of twenty yearsspanning over 1991-92 to 2010-11. This study aims to examinethe relative efficiency of various commercial bank groups likeState Bank of India Group, (SBI Group) Nationalised BankGroup, Private Sector Bank Group (PB Group) and ForeignBank Group (FB Group) which are operating in India. Thereason that the period 1991-92 to 2010-11 is chosen for this

I.J.E.M.S., VOL.6 (3) 2015: 124 - 148 ISSN 2229-600X

126

study is that the current banking sector reforms were initiatedin 1991 and being continuously pursued in a phased manner.Thus the sample period of twenty years which is furtherdivided in to two phases of ten years each is good enough toprovide sufficient insight regarding the impact of reforms onIndian banking sector. In this study, the productivity andprofitability parameters for the two phases; namely first phasecovering 1991-92 to 2000-01 and second phase spanning 2001-2002 to 2010-11 have been calculated, analysed, compared andcontrasted in evaluating the relative efficiency of commercialbanks in India; both in aggregate and in groups.

RESEARCH METHODOLOGYA) Research objectives

i) To assess the overall profitability and productivity ofthe banking sector in the post reform period.

ii) To examine the relative profitability performanceof each bank group – State Bank of India group,Nationalized Bank group, Private Sector Bank groupand Foreign Bank group.

iii) To evaluate the relative productivity performance ofeach bank group during the study period.

iv) To study the influence of different factors contributingto the productivity and profitability trends of thebanking sector.

v) To indicate the extent to which reforms in thefinancial sector have contributed to improve theproductivity and profitability of the banking sector.

B) Research HypothesisI. The operational productivity of Indian banking sector

has increased during the post reform period.

II. Bank productivity is the cornerstone of profitability.

III. Ownership and management of commercial banks is amajor determinant of productivity.

IV. ‘Spread’ continues to be the major determinant ofcommercial bank productivity.

V. ‘Burden’ being an ‘outgo’ is a negative determinant ofbank profitability.

VI. In the changing financial environment, diversificationof bank business is the key to bank profitability.

VII. Volume of business is the contributing factor to the bankprofitability.

C) Selection of input and outputProductivity and profitability of different banks group aremeasured by relevant parameters such as deposit,advances, income, expenditure , profit to working fund, etc.

D) Research MethodologyThe commercial banking sector in India which includesthe State Bank of India and its associated banks, nationalisedbanks, major private sector banks and foreign banksoperating in India. Thus, the Indian banking sector havebeen broadly divided into four groups for the analysis ofprofitability and productivity during the post – reformperiod. More specifically the period of 20 years beginningfrom the year 1991- 92 to 2010 – 11 has been coveredunder this study. The study period has been divided intotwo distinct phases. The reform process started with theimplementation of Narashimham Committee reported in 1991.Thus the first phase covered the initial ten years covering 1991-92 to 2000-2001. Further intensification of reforms took placeafter the implementation of second report of NarashimhamCommittee in 1998. Thus, the second phase of the study coversthe second decade of the reform period i.e. 2001-02 to 2010-11. Thus, the study encompasses the whole of the reformperiod. Performance of banks can be measured by a number ofindicators. Productivity and profitability are the mostimportant and reliable indicator of the banking performance.For the purpose of the present study, both the performanceparameters have been used.

Banking profitability has been examined through thefollowing indicators:i) Interest earned as percentage of working fundii) Interest paid as percentage of working fundiii) Ratio of total income to working fundiv) Ratio of spread to working fundv) Ratio of non – interest expenditure to working fundvi) Other income as percentage of working fundvii) Ratio of burden to working fund

Banking productivity has been examined through thefollowing indicators:i) Cost of depositii) Business per employeeiii) Interest income to working fundiv) Non-interest income to working fundv) Spread as percentage of working fund

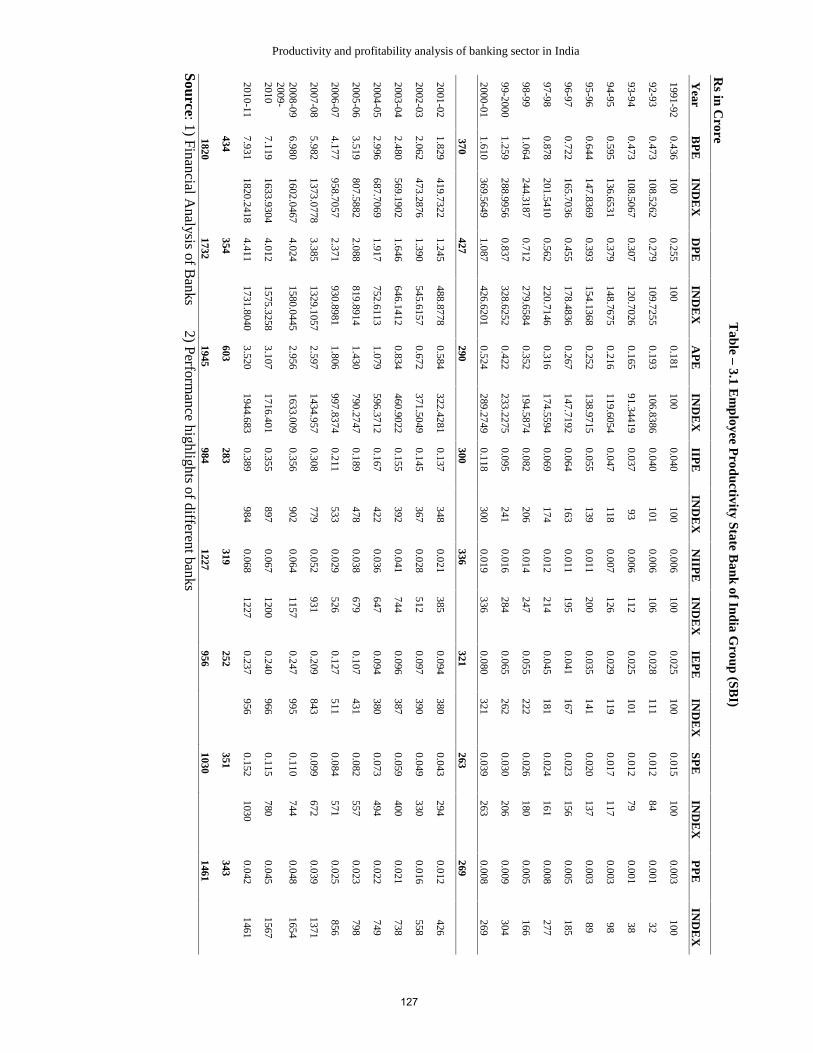

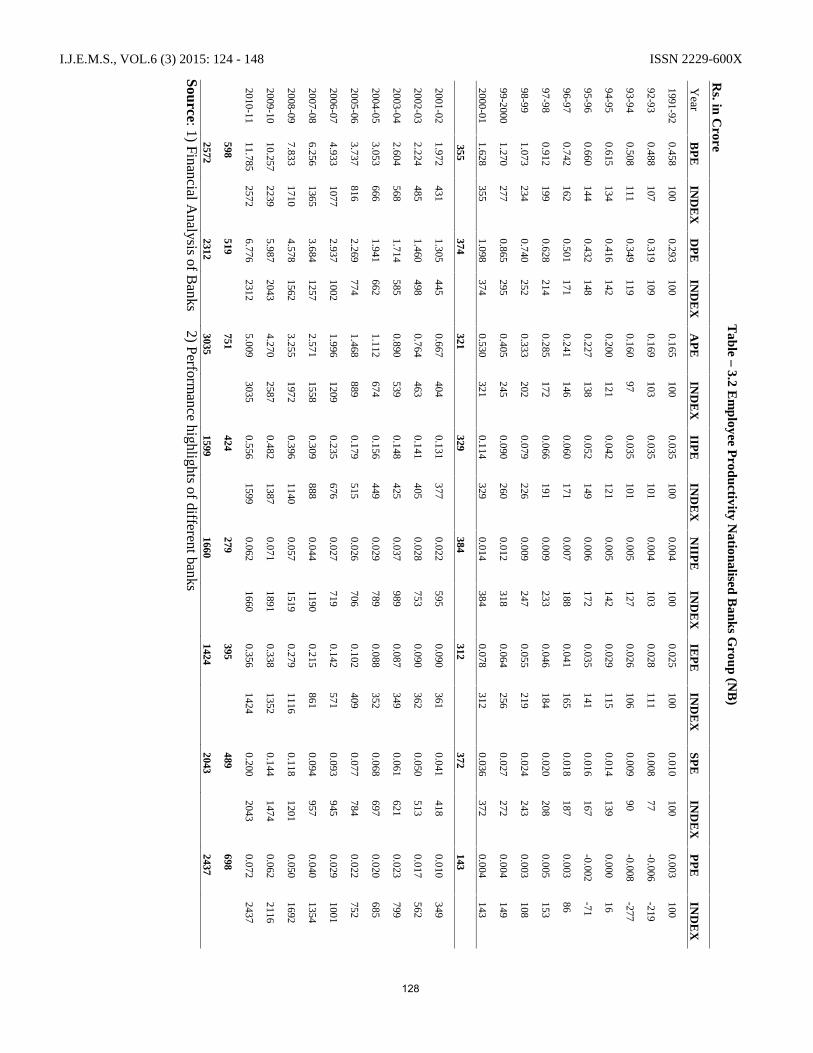

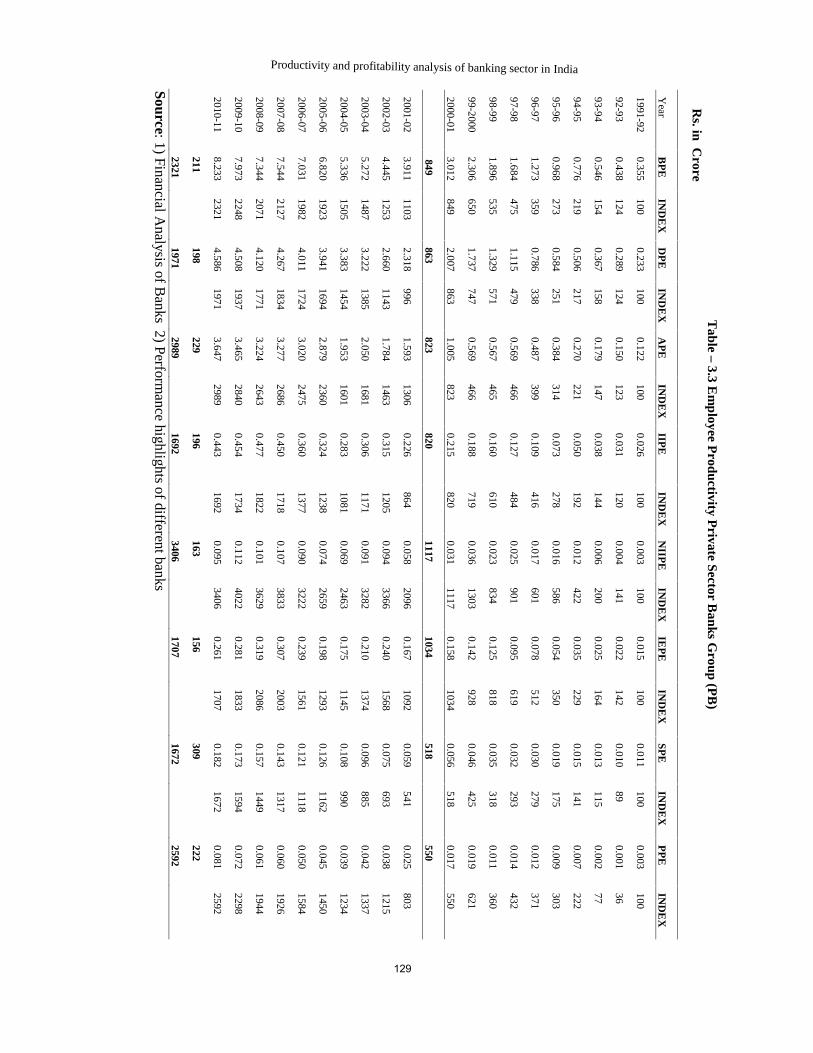

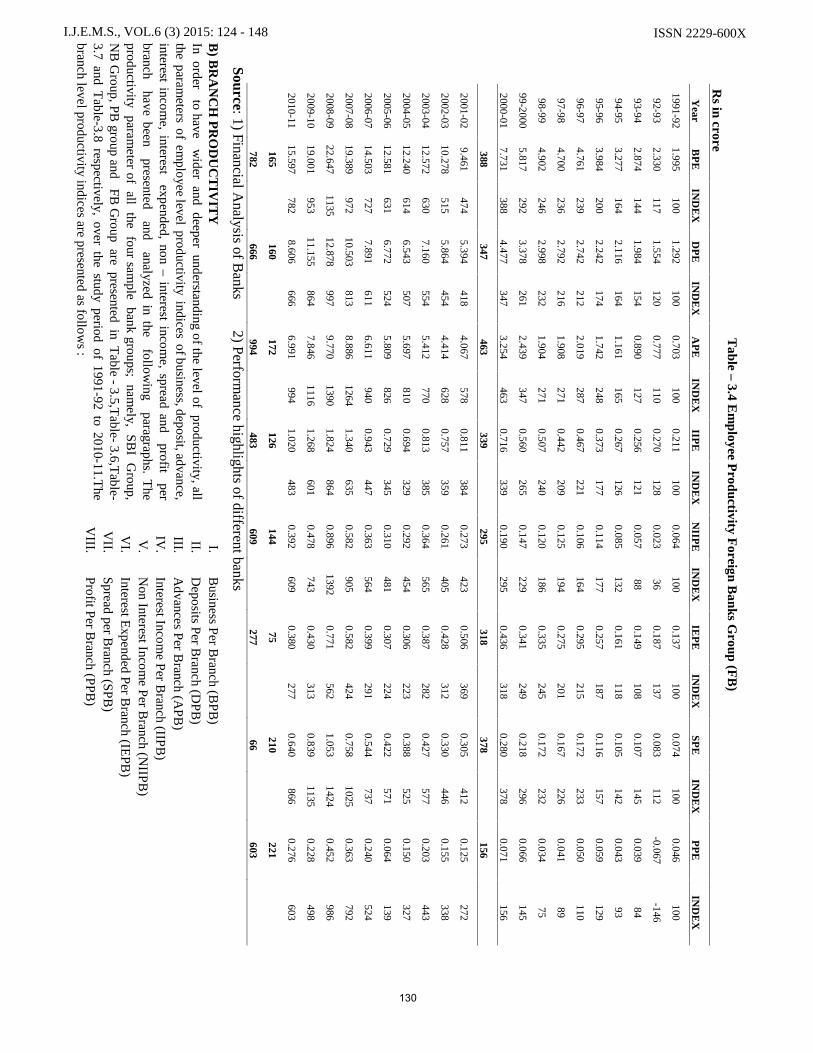

EMPIRICAL ANALYSIS (productivity)A) EMPLOYEE PRODUCTIVITYTable-3.1, Table-3.2, Table-3.3, and Table-3.4 present theemployee productivity indices (year wise) of SBI group,nationalised bank group, private sector bank group and foreignbank group respectively for the study period, covering 1991-92 to 2010-11. The employee productivity parameters arerepresented by eight indices which are as follows.I. Business Per Employee (BPE)II. Deposit Per Employee (DPE)III. Advance Per Employee (APE)IV. Interest Income Per Employee (IIPE)V. Non Interest Income Per Employee (NIIPE)VI. Interest Expended Per Employee (IEPE)VII. Spread Per Employee (SPE)VIII. Profit Per Employee (PPE)

Productivity and profitability analysis of banking sector in India

Table

–3.1

Em

ployee Productivity

State Bank of India G

roup (SBI)

Rs in C

rore

Year

BP

EIN

DE

XD

PE

IND

EX

AP

EIN

DE

XIIP

EIN

DE

XN

IIPE

IND

EX

IEP

EIN

DE

XSP

EIN

DE

XP

PE

IND

EX

1991-920.436

1000.255

1000.181

1000.040

1000.006

1000.025

1000.015

1000.003

100

92-930.473

108.52620.279

109.72550.193

106.83860.040

1010.006

1060.028

1110.012

840.001

32

93-940.473

108.50670.307

120.70260.165

91.344190.037

930.006

1120.025

1010.012

790.001

38

94-950.595

136.65310.379

148.76750.216

119.60540.047

1180.007

1260.029

1190.017

1170.003

98

95-960.644

147.83690.393

154.13680.252

138.97150.055

1390.011

2000.035

1410.020

1370.003

89

96-970.722

165.70360.455

178.48360.267

147.71920.064

1630.011

1950.041

1670.023

1560.005

185

97-980.878

201.54100.562

220.71460.316

174.55940.069

1740.012

2140.045

1810.024

1610.008

277

98-991.064

244.31870.712

279.65840.352

194.58740.082

2060.014

2470.055

2220.026

1800.005

166

99-20001.259

288.99560.837

328.62520.422

233.22750.095

2410.016

2840.065

2620.030

2060.009

304

2000-011.610

369.56491.087

426.62010.524

289.27490.118

3000.019

3360.080

3210.039

2630.008

269

370427

290300

336321

263269

2001-021.829

419.73221.245

488.87780.584

322.42810.137

3480.021

3850.094

3800.043

2940.012

426

2002-032.062

473.28761.390

545.61570.672

371.50490.145

3670.028

5120.097

3900.049

3300.016

558

2003-042.480

569.19021.646

646.14120.834

460.90220.155

3920.041

7440.096

3870.059

4000.021

738

2004-052.996

687.70691.917

752.61131.079

596.37120.167

4220.036

6470.094

3800.073

4940.022

749

2005-063.519

807.58822.088

819.89141.430

790.27470.189

4780.038

6790.107

4310.082

5570.023

798

2006-074.177

958.70572.371

930.89811.806

997.83740.211

5330.029

5260.127

5110.084

5710.025

856

2007-085.982

1373.07783.385

1329.10572.597

1434.9570.308

7790.052

9310.209

8430.099

6720.039

1371

2008-096.980

1602.04674.024

1580.04452.956

1633.0090.356

9020.064

11570.247

9950.110

7440.048

16542009-2010

7.1191633.9304

4.0121575.3258

3.1071716.401

0.355897

0.0671200

0.240966

0.115780

0.0451567

2010-117.931

1820.24184.411

1731.80403.520

1944.6830.389

9840.068

12270.237

9560.152

10300.042

1461

434354

603283

319252

351343

18201732

1945984

1227956

10301461

Source: 1) Financial Analysis of B

anks2) Perform

ance highlights of different banks

127

I.J.E.M.S., VOL.6 (3) 2015: 124 - 148 ISSN 2229-600X

Table

–3.2

Em

ployee Productivity N

ationalised Banks G

roup (NB

)R

s. in Crore

Year

BP

EIN

DE

XD

PE

IND

EX

AP

EIN

DE

XIIP

EIN

DE

XN

IIPE

IND

EX

IEP

EIN

DE

XSP

EIN

DE

XP

PE

IND

EX

1991-920.458

1000.293

1000.165

1000.035

1000.004

1000.025

1000.010

1000.003

100

92-930.488

1070.319

1090.169

1030.035

1010.004

1030.028

1110.008

77-0.006

-219

93-940.508

1110.349

1190.160

970.035

1010.005

1270.026

1060.009

90-0.008

-277

94-950.615

1340.416

1420.200

1210.042

1210.005

1420.029

1150.014

1390.000

16

95-960.660

1440.432

1480.227

1380.052

1490.006

1720.035

1410.016

167-0.002

-71

96-970.742

1620.501

1710.241

1460.060

1710.007

1880.041

1650.018

1870.003

86

97-980.912

1990.628

2140.285

1720.066

1910.009

2330.046

1840.020

2080.005

153

98-991.073

2340.740

2520.333

2020.079

2260.009

2470.055

2190.024

2430.003

108

99-20001.270

2770.865

2950.405

2450.090

2600.012

3180.064

2560.027

2720.004

149

2000-011.628

3551.098

3740.530

3210.114

3290.014

3840.078

3120.036

3720.004

143

355374

321329

384312

372143

2001-021.972

4311.305

4450.667

4040.131

3770.022

5950.090

3610.041

4180.010

349

2002-032.224

4851.460

4980.764

4630.141

4050.028

7530.090

3620.050

5130.017

562

2003-042.604

5681.714

5850.890

5390.148

4250.037

9890.087

3490.061

6210.023

799

2004-053.053

6661.941

6621.112

6740.156

4490.029

7890.088

3520.068

6970.020

685

2005-063.737

8162.269

7741.468

8890.179

5150.026

7060.102

4090.077

7840.022

752

2006-074.933

10772.937

10021.996

12090.235

6760.027

7190.142

5710.093

9450.029

1001

2007-086.256

13653.684

12572.571

15580.309

8880.044

11900.215

8610.094

9570.040

1354

2008-097.833

17104.578

15623.255

19720.396

11400.057

15190.279

11160.118

12010.050

1692

2009-1010.257

22395.987

20434.270

25870.482

13870.071

18910.338

13520.144

14740.062

2116

2010-1111.785

25726.776

23125.009

30350.556

15990.062

16600.356

14240.200

20430.072

2437

598519

751424

279395

489698

25722312

30351599

16601424

20432437

Source: 1) Financial Analysis of B

anks2) Perform

ance highlights of different banks

128

Productivity and profitability analysis of banking sector in India

Table

–3.3

Em

ployee Productivity P

rivate Sector Banks G

roup (PB

)R

s. inC

rore

Year

BP

EIN

DE

XD

PE

IND

EX

AP

EIN

DE

XIIP

EIN

DE

XN

IIPE

IND

EX

IEP

EIN

DE

XSP

EIN

DE

XP

PE

IND

EX

1991-920.355

1000.233

1000.122

1000.026

1000.003

1000.015

1000.011

1000.003

100

92-930.438

1240.289

1240.150

1230.031

1200.004

1410.022

1420.010

890.001

36

93-940.546

1540.367

1580.179

1470.038

1440.006

2000.025

1640.013

1150.002

77

94-950.776

2190.506

2170.270

2210.050

1920.012

4220.035

2290.015

1410.007

222

95-960.968

2730.584

2510.384

3140.073

2780.016

5860.054

3500.019

1750.009

303

96-971.273

3590.786

3380.487

3990.109

4160.017

6010.078

5120.030

2790.012

371

97-981.684

4751.115

4790.569

4660.127

4840.025

9010.095

6190.032

2930.014

432

98-991.896

5351.329

5710.567

4650.160

6100.023

8340.125

8180.035

3180.011

360

99-20002.306

6501.737

7470.569

4660.188

7190.036

13030.142

9280.046

4250.019

621

2000-013.012

8492.007

8631.005

8230.215

8200.031

11170.158

10340.056

5180.017

550

849863

823820

11171034

518550

2001-023.911

11032.318

9961.593

13060.226

8640.058

20960.167

10920.059

5410.025

803

2002-034.445

12532.660

11431.784

14630.315

12050.094

33660.240

15680.075

6930.038

1215

2003-045.272

14873.222

13852.050

16810.306

11710.091

32820.210

13740.096

8850.042

1337

2004-055.336

15053.383

14541.953

16010.283

10810.069

24630.175

11450.108

9900.039

1234

2005-066.820

19233.941

16942.879

23600.324

12380.074

26590.198

12930.126

11620.045

1450

2006-077.031

19824.011

17243.020

24750.360

13770.090

32220.239

15610.121

11180.050

1584

2007-087.544

21274.267

18343.277

26860.450

17180.107

38330.307

20030.143

13170.060

1926

2008-097.344

20714.120

17713.224

26430.477

18220.101

36290.319

20860.157

14490.061

1944

2009-107.973

22484.508

19373.465

28400.454

17340.112

40220.281

18330.173

15940.072

2298

2010-118.233

23214.586

19713.647

29890.443

16920.095

34060.261

17070.182

16720.081

2592

211198

229196

163156

309222

23211971

29891692

34061707

16722592

Source: 1) Financial Analysis of B

anks2) Perform

ance highlights of different banks

129

I.J.E.M.S., VOL.6 (3) 2015: 124 - 148 ISSN 2229-600X

Table

–3.4

Em

ployee Productivity F

oreign Banks G

roup (FB

)R

s in crore

Year

BP

EIN

DE

XD

PE

IND

EX

AP

EIN

DE

XIIP

EIN

DE

XN

IIPE

IND

EX

IEP

EIN

DE

XSP

EIN

DE

XP

PE

IND

EX

1991-921.995

1001.292

1000.703

1000.211

1000.064

1000.137

1000.074

1000.046

100

92-932.330

1171.554

1200.777

1100.270

1280.023

360.187

1370.083

112-0.067

-146

93-942.874

1441.984

1540.890

1270.256

1210.057

880.149

1080.107

1450.039

84

94-953.277

1642.116

1641.161

1650.267

1260.085

1320.161

1180.105

1420.043

93

95-963.984

2002.242

1741.742

2480.373

1770.114

1770.257

1870.116

1570.059

129

96-974.761

2392.742

2122.019

2870.467

2210.106

1640.295

2150.172

2330.050

110

97-984.700

2362.792

2161.908

2710.442

2090.125

1940.275

2010.167

2260.041

89

98-994.902

2462.998

2321.904

2710.507

2400.120

1860.335

2450.172

2320.034

75

99-20005.817

2923.378

2612.439

3470.560

2650.147

2290.341

2490.218

2960.066

145

2000-017.731

3884.477

3473.254

4630.716

3390.190

2950.436

3180.280

3780.071

156

388347

463339

295318

378156

2001-029.461

4745.394

4184.067

5780.811

3840.273

4230.506

3690.305

4120.125

272

2002-0310.278

5155.864

4544.414

6280.757

3590.261

4050.428

3120.330

4460.155

338

2003-0412.572

6307.160

5545.412

7700.813

3850.364

5650.387

2820.427

5770.203

443

2004-0512.240

6146.543

5075.697

8100.694

3290.292

4540.306

2230.388

5250.150

327

2005-0612.581

6316.772

5245.809

8260.729

3450.310

4810.307

2240.422

5710.064

139

2006-0714.503

7277.891

6116.611

9400.943

4470.363

5640.399

2910.544

7370.240

524

2007-0819.389

97210.503

8138.886

12641.340

6350.582

9050.582

4240.758

10250.363

792

2008-0922.647

113512.878

9979.770

13901.824

8640.896

13920.771

5621.053

14240.452

986

2009-1019.001

95311.155

8647.846

11161.268

6010.478

7430.430

3130.839

11350.228

498

2010-1115.597

7828.606

6666.991

9941.020

4830.392

6090.380

2770.640

8660.276

603

165160

172126

14475

210221

782666

994483

609277

66603

Source: 1) Financial Analysis of B

anks2) Perform

ance highlights of different banks

B)

BR

AN

CH

PR

OD

UC

TIV

ITY

In order to have wider and deeper understanding of the level of productivity, all

the parameters of em

ployee level productivity indices of business, deposit, advance,interest incom

e, interest expended, non–

interest income, spread and profit per

branch have been presented and analyzed in the following paragraphs. T

heproductivity param

eter of all the four sample bank groups; nam

ely, SBI G

roup,N

B G

roup, PB group and FB

Group are presented in T

able-

3.5,Table-

3.6,Table-

3.7 and Table-3.8 respectively, over the study period of 1991-92 to 2010-11.T

hebranch level productivity indices are presented as follow

s :

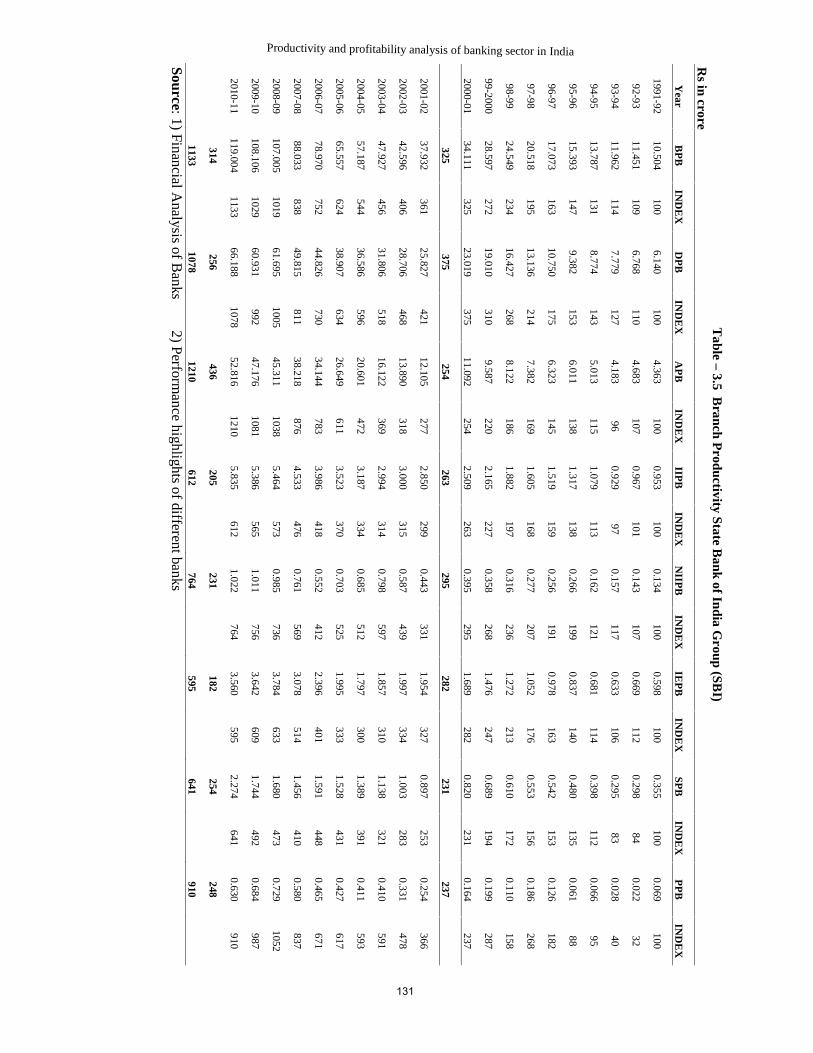

I.B

usiness Per B

ranch (BP

B)

II.D

eposits Per B

ranch (DP

B)

III.A

dvances Per B

ranch (AP

B)

IV.

Interest Income P

er Branch (IIP

B)

V.

Non Interest Incom

e Per B

ranch (NIIP

B)

VI.

Interest Expended P

er Branch (IE

PB)

VII.

Spread per Branch (SP

B)

VIII.

Profit P

er Branch (P

PB)

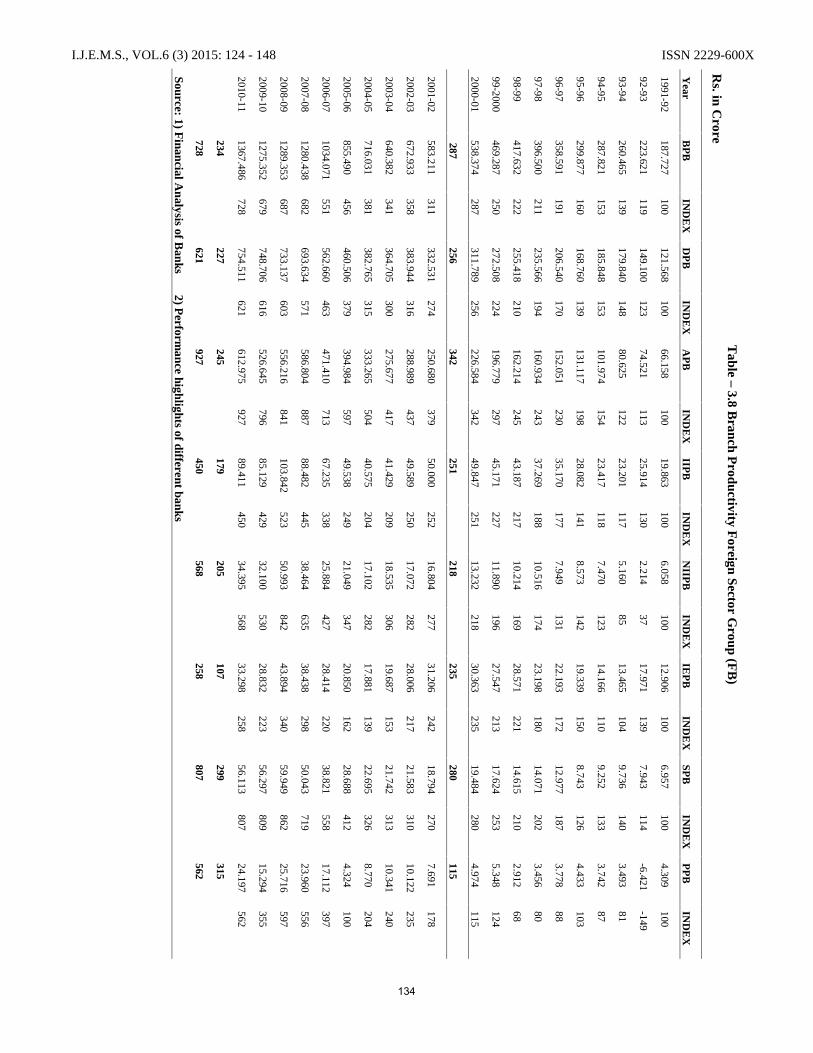

130

Productivity and profitability analysis of banking sector in India

Table

–3.5

Branch P

roductivity State Bank of India G

roup (SBI)

Rs in crore

Year

BP

BIN

DE

XD

PB

IND

EX

AP

BIN

DE

XIIP

BIN

DE

XN

IIPB

IND

EX

IEP

BIN

DE

XSP

BIN

DE

XP

PB

IND

EX

1991-9210.504

1006.140

1004.363

1000.953

1000.134

1000.598

1000.355

1000.069

100

92-9311.451

1096.768

1104.683

1070.967

1010.143

1070.669

1120.298

840.022

32

93-9411.962

1147.779

1274.183

960.929

970.157

1170.633

1060.295

830.028

40

94-9513.787

1318.774

1435.013

1151.079

1130.162

1210.681

1140.398

1120.066

95

95-9615.393

1479.382

1536.011

1381.317

1380.266

1990.837

1400.480

1350.061

88

96-9717.073

16310.750

1756.323

1451.519

1590.256

1910.978

1630.542

1530.126

182

97-9820.518

19513.136

2147.382

1691.605

1680.277

2071.052

1760.553

1560.186

268

98-9924.549

23416.427

2688.122

1861.882

1970.316

2361.272

2130.610

1720.110

158

99-200028.597

27219.010

3109.587

2202.165

2270.358

2681.476

2470.689

1940.199

287

2000-0134.111

32523.019

37511.092

2542.509

2630.395

2951.689

2820.820

2310.164

237

325375

254263

295282

231237

2001-0237.932

36125.827

42112.105

2772.850

2990.443

3311.954

3270.897

2530.254

366

2002-0342.596

40628.706

46813.890

3183.000

3150.587

4391.997

3341.003

2830.331

478

2003-0447.927

45631.806

51816.122

3692.994

3140.798

5971.857

3101.138

3210.410

591

2004-0557.187

54436.586

59620.601

4723.187

3340.685

5121.797

3001.389

3910.411

593

2005-0665.557

62438.907

63426.649

6113.523

3700.703

5251.995

3331.528

4310.427

617

2006-0778.970

75244.826

73034.144

7833.986

4180.552

4122.396

4011.591

4480.465

671

2007-0888.033

83849.815

81138.218

8764.533

4760.761

5693.078

5141.456

4100.580

837

2008-09107.005

101961.695

100545.311

10385.464

5730.985

7363.784

6331.680

4730.729

1052

2009-10108.106

102960.931

99247.176

10815.386

5651.011

7563.642

6091.744

4920.684

987

2010-11119.004

113366.188

107852.816

12105.835

6121.022

7643.560

5952.274

6410.630

910

314256

436205

231182

254248

11331078

1210612

764595

641910

Source: 1) Financial Analysis of B

anks2) Perform

ance highlights of different banks

131

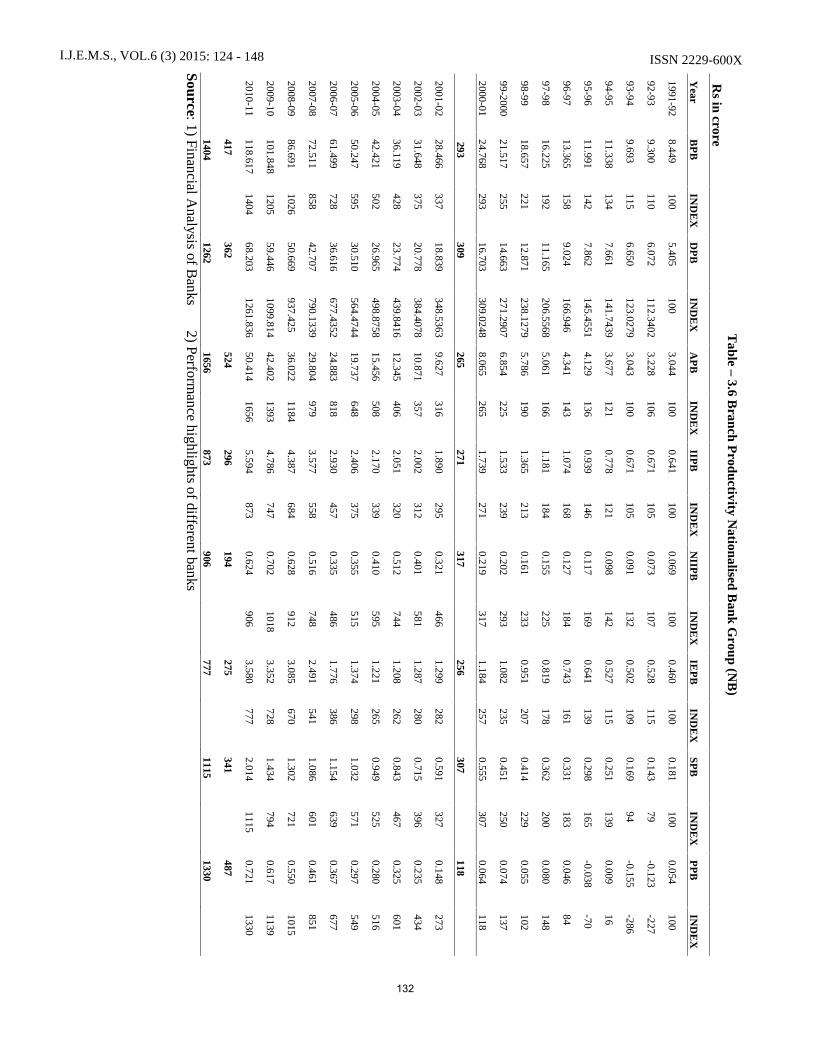

I.J.E.M.S., VOL.6 (3) 2015: 124 - 148 ISSN 2229-600X

Table

–3.6

Branch

Productivity N

ationalised Bank G

roup (NB

)R

s in crore

Year

BP

BIN

DE

XD

PB

IND

EX

AP

BIN

DE

XIIP

BIN

DE

XN

IIPB

IND

EX

IEP

BIN

DE

XSP

BIN

DE

XP

PB

IND

EX

1991-928.449

1005.405

1003.044

1000.641

1000.069

1000.460

1000.181

1000.054

100

92-939.300

1106.072

112.34023.228

1060.671

1050.073

1070.528

1150.143

79-0.123

-227

93-949.693

1156.650

123.02793.043

1000.671

1050.091

1320.502

1090.169

94-0.155

-286

94-9511.338

1347.661

141.74393.677

1210.778

1210.098

1420.527

1150.251

1390.009

16

95-9611.991

1427.862

145.45514.129

1360.939

1460.117

1690.641

1390.298

165-0.038

-70

96-9713.365

1589.024

166.9464.341

1431.074

1680.127

1840.743

1610.331

1830.046

84

97-9816.225

19211.165

206.55685.061

1661.181

1840.155

2250.819

1780.362

2000.080

148

98-9918.657

22112.871

238.12795.786

1901.365

2130.161

2330.951

2070.414

2290.055

102

99-200021.517

25514.663

271.29076.854

2251.533

2390.202

2931.082

2350.451

2500.074

137

2000-0124.768

29316.703

309.02488.065

2651.739

2710.219

3171.184

2570.555

3070.064

118

293309

265271

317256

307118

2001-0228.466

33718.839

348.53639.627

3161.890

2950.321

4661.299

2820.591

3270.148

273

2002-0331.648

37520.778

384.407810.871

3572.002

3120.401

5811.287

2800.715

3960.235

434

2003-0436.119

42823.774

439.841612.345

4062.051

3200.512

7441.208

2620.843

4670.325

601

2004-0542.421

50226.965

498.875815.456

5082.170

3390.410

5951.221

2650.949

5250.280

516

2005-0650.247

59530.510

564.474419.737

6482.406

3750.355

5151.374

2981.032

5710.297

549

2006-0761.499

72836.616

677.435224.883

8182.930

4570.335

4861.776

3861.154

6390.367

677

2007-0872.511

85842.707

790.133929.804

9793.577

5580.516

7482.491

5411.086

6010.461

851

2008-0986.691

102650.669

937.42536.022

11844.387

6840.628

9123.085

6701.302

7210.550

1015

2009-10101.848

120559.446

1099.81442.402

13934.786

7470.702

10183.352

7281.434

7940.617

1139

2010-11118.617

140468.203

1261.83650.414

16565.594

8730.624

9063.580

7772.014

11150.721

1330

417362

524296

194275

341487

14041262

1656873

906777

11151330

Source: 1) Financial Analysis of B

anks2) Perform

ance highlights of different banks

132

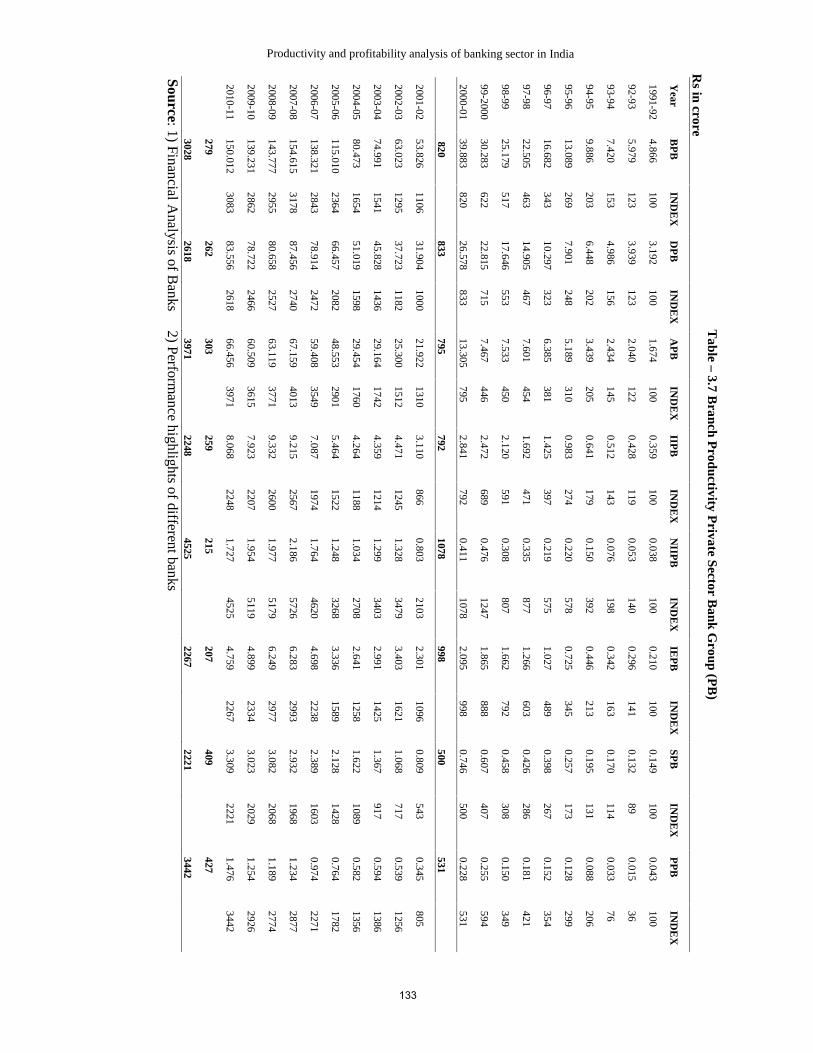

Productivity and profitability analysis of banking sector in India

Table

–3.7

Branch

Productivity P

rivate Sector Bank G

roup (PB

)R

s in crore

Year

BP

BIN

DE

XD

PB

IND

EX

AP

BIN

DE

XIIP

BIN

DE

XN

IIPB

IND

EX

IEP

BIN

DE

XSP

BIN

DE

XP

PB

IND

EX

1991-924.866

1003.192

1001.674

1000.359

1000.038

1000.210

1000.149

1000.043

100

92-935.979

1233.939

1232.040

1220.428

1190.053

1400.296

1410.132

890.015

36

93-947.420

1534.986

1562.434

1450.512

1430.076

1980.342

1630.170

1140.033

76

94-959.886

2036.448

2023.439

2050.641

1790.150

3920.446

2130.195

1310.088

206

95-9613.089

2697.901

2485.189

3100.983

2740.220

5780.725

3450.257

1730.128

299

96-9716.682

34310.297

3236.385

3811.425

3970.219

5751.027

4890.398

2670.152

354

97-9822.505

46314.905

4677.601

4541.692

4710.335

8771.266

6030.426

2860.181

421

98-9925.179

51717.646

5537.533

4502.120

5910.308

8071.662

7920.458

3080.150

349

99-200030.283

62222.815

7157.467

4462.472

6890.476

12471.865

8880.607

4070.255

594

2000-0139.883

82026.578

83313.305

7952.841

7920.411

10782.095

9980.746

5000.228

531

820833

795792

1078998

500531

2001-0253.826

110631.904

100021.922

13103.110

8660.803

21032.301

10960.809

5430.345

805

2002-0363.023

129537.723

118225.300

15124.471

12451.328

34793.403

16211.068

7170.539

1256

2003-0474.991

154145.828

143629.164

17424.359

12141.299

34032.991

14251.367

9170.594

1386

2004-0580.473

165451.019

159829.454

17604.264

11881.034

27082.641

12581.622

10890.582

1356

2005-06115.010

236466.457

208248.553

29015.464

15221.248

32683.336

15892.128

14280.764

1782

2006-07138.321

284378.914

247259.408

35497.087

19741.764

46204.698

22382.389

16030.974

2271

2007-08154.615

317887.456

274067.159

40139.215

25672.186

57266.283

29932.932

19681.234

2877

2008-09143.777

295580.658

252763.119

37719.332

26001.977

51796.249

29773.082

20681.189

2774

2009-10139.231

286278.722

246660.509

36157.923

22071.954

51194.899

23343.023

20291.254

2926

2010-11150.012

308383.556

261866.456

39718.068

22481.727

45254.759

22673.309

22211.476

3442

279262

303259

215207

409427

30282618

39712248

45252267

22213442

Source: 1) Financial Analysis of B

anks2) Perform

ance highlights of different banks

133

I.J.E.M.S., VOL.6 (3) 2015: 124 - 148 ISSN 2229-600X

Table

–3.8

Branch P

roductivity Foreign Sector G

roup (FB

)R

s. in Crore

Year

BP

BIN

DE

XD

PB

IND

EX

AP

BIN

DE

XIIP

BIN

DE

XN

IIPB

IND

EX

IEP

BIN

DE

XSP

BIN

DE

XP

PB

IND

EX

1991-92187.727

100121.568

10066.158

10019.863

1006.058

10012.906

1006.957

1004.309

100

92-93223.621

119149.100

12374.521

11325.914

1302.214

3717.971

1397.943

114-6.421

-149

93-94260.465

139179.840

14880.625

12223.201

1175.160

8513.465

1049.736

1403.493

81

94-95287.821

153185.848

153101.974

15423.417

1187.470

12314.166

1109.252

1333.742

87

95-96299.877

160168.760

139131.117

19828.082

1418.573

14219.339

1508.743

1264.433

103

96-97358.591

191206.540

170152.051

23035.170

1777.949

13122.193

17212.977

1873.778

88

97-98396.500

211235.566

194160.934

24337.269

18810.516

17423.198

18014.071

2023.456

80

98-99417.632

222255.418

210162.214

24543.187

21710.214

16928.571

22114.615

2102.912

68

99-2000469.287

250272.508

224196.779

29745.171

22711.890

19627.547

21317.624

2535.348

124

2000-01538.374

287311.789

256226.584

34249.847

25113.232

21830.363

23519.484

2804.974

115

287256

342251

218235

280115

2001-02583.211

311332.531

274250.680

37950.000

25216.804

27731.206

24218.794

2707.691

178

2002-03672.933

358383.944

316288.989

43749.589

25017.072

28228.006

21721.583

31010.122

235

2003-04640.382

341364.705

300275.677

41741.429

20918.535

30619.687

15321.742

31310.341

240

2004-05716.031

381382.765

315333.265

50440.575

20417.102

28217.881

13922.695

3268.770

204

2005-06855.490

456460.506

379394.984

59749.538

24921.049

34720.850

16228.688

4124.324

100

2006-071034.071

551562.660

463471.410

71367.235

33825.884

42728.414

22038.821

55817.112

397

2007-081280.438

682693.634

571586.804

88788.482

44538.464

63538.438

29850.043

71923.960

556

2008-091289.353

687733.137

603556.216

841103.842

52350.993

84243.894

34059.949

86225.716

597

2009-101275.352

679748.706

616526.645

79685.129

42932.100

53028.832

22356.297

80915.294

355

2010-111367.486

728754.511

621612.975

92789.411

45034.395

56833.298

25856.113

80724.197

562

234227

245179

205107

299315

728621

927450

568258

807562

Source: 1) Financial A

nalysis of Banks 2) P

erformance

highlights ofdifferent banks

134

Productivity and profitability analysis of banking sector in India

135

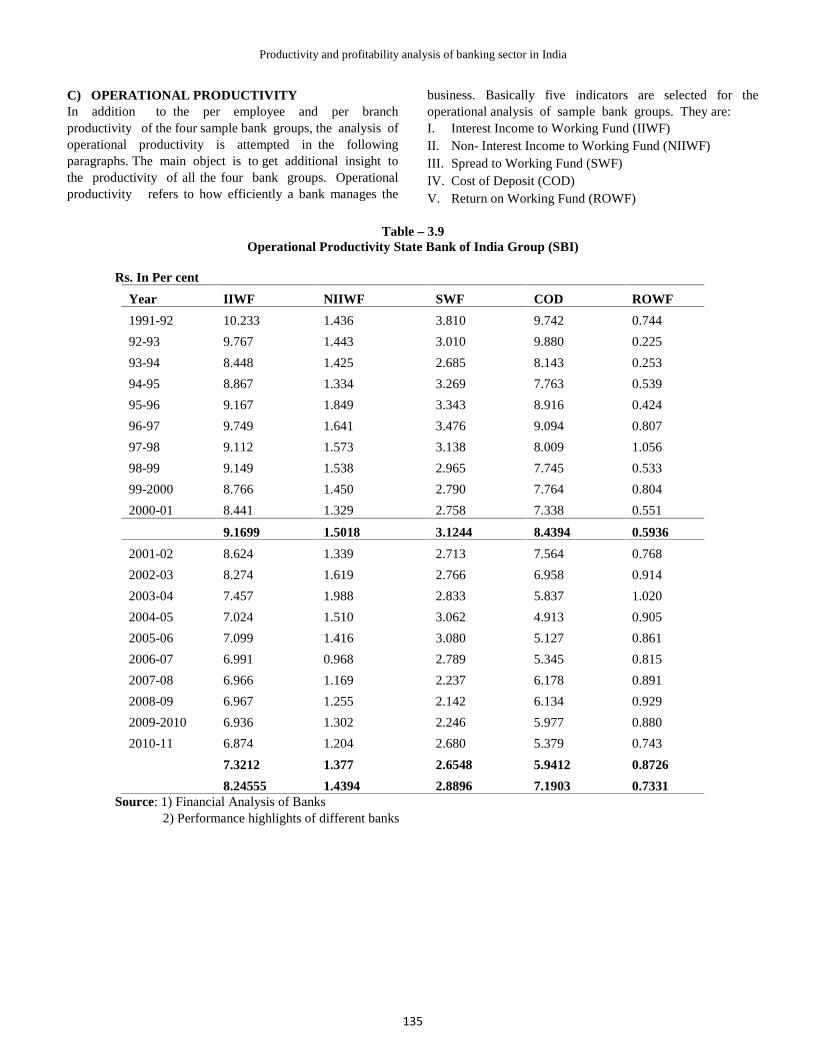

C) OPERATIONAL PRODUCTIVITYIn addition to the per employee and per branchproductivity of the four sample bank groups, the analysis ofoperational productivity is attempted in the followingparagraphs. The main object is to get additional insight tothe productivity of all the four bank groups. Operationalproductivity refers to how efficiently a bank manages the

business. Basically five indicators are selected for theoperational analysis of sample bank groups. They are:I. Interest Income to Working Fund (IIWF)II. Non- Interest Income to Working Fund (NIIWF)III. Spread to Working Fund (SWF)IV. Cost of Deposit (COD)V. Return on Working Fund (ROWF)

Table – 3.9Operational Productivity State Bank of India Group (SBI)

Rs. In Per cent

Year IIWF NIIWF SWF COD ROWF

1991-92 10.233 1.436 3.810 9.742 0.744

92-93 9.767 1.443 3.010 9.880 0.225

93-94 8.448 1.425 2.685 8.143 0.253

94-95 8.867 1.334 3.269 7.763 0.539

95-96 9.167 1.849 3.343 8.916 0.424

96-97 9.749 1.641 3.476 9.094 0.807

97-98 9.112 1.573 3.138 8.009 1.056

98-99 9.149 1.538 2.965 7.745 0.533

99-2000 8.766 1.450 2.790 7.764 0.804

2000-01 8.441 1.329 2.758 7.338 0.551

9.1699 1.5018 3.1244 8.4394 0.5936

2001-02 8.624 1.339 2.713 7.564 0.768

2002-03 8.274 1.619 2.766 6.958 0.914

2003-04 7.457 1.988 2.833 5.837 1.020

2004-05 7.024 1.510 3.062 4.913 0.905

2005-06 7.099 1.416 3.080 5.127 0.861

2006-07 6.991 0.968 2.789 5.345 0.815

2007-08 6.966 1.169 2.237 6.178 0.891

2008-09 6.967 1.255 2.142 6.134 0.929

2009-2010 6.936 1.302 2.246 5.977 0.880

2010-11 6.874 1.204 2.680 5.379 0.743

7.3212 1.377 2.6548 5.9412 0.8726

8.24555 1.4394 2.8896 7.1903 0.7331Source: 1) Financial Analysis of Banks

2) Performance highlights of different banks

I.J.E.M.S., VOL.6 (3) 2015: 124 - 148 ISSN 2229-600X

136

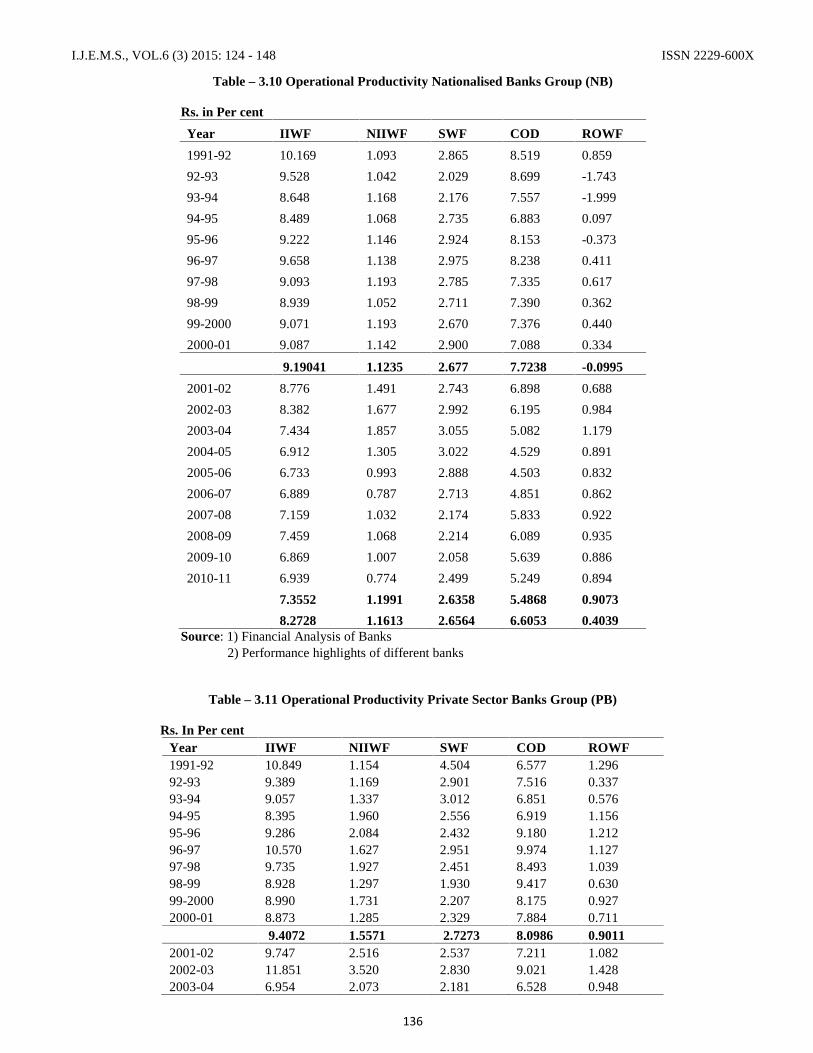

Table – 3.10 Operational Productivity Nationalised Banks Group (NB)

Rs. in Per cent

Year IIWF NIIWF SWF COD ROWF

1991-92 10.169 1.093 2.865 8.519 0.859

92-93 9.528 1.042 2.029 8.699 -1.743

93-94 8.648 1.168 2.176 7.557 -1.999

94-95 8.489 1.068 2.735 6.883 0.097

95-96 9.222 1.146 2.924 8.153 -0.373

96-97 9.658 1.138 2.975 8.238 0.411

97-98 9.093 1.193 2.785 7.335 0.617

98-99 8.939 1.052 2.711 7.390 0.362

99-2000 9.071 1.193 2.670 7.376 0.440

2000-01 9.087 1.142 2.900 7.088 0.334

9.19041 1.1235 2.677 7.7238 -0.0995

2001-02 8.776 1.491 2.743 6.898 0.688

2002-03 8.382 1.677 2.992 6.195 0.984

2003-04 7.434 1.857 3.055 5.082 1.179

2004-05 6.912 1.305 3.022 4.529 0.891

2005-06 6.733 0.993 2.888 4.503 0.832

2006-07 6.889 0.787 2.713 4.851 0.862

2007-08 7.159 1.032 2.174 5.833 0.922

2008-09 7.459 1.068 2.214 6.089 0.935

2009-10 6.869 1.007 2.058 5.639 0.886

2010-11 6.939 0.774 2.499 5.249 0.894

7.3552 1.1991 2.6358 5.4868 0.9073

8.2728 1.1613 2.6564 6.6053 0.4039Source: 1) Financial Analysis of Banks

2) Performance highlights of different banks

Table – 3.11 Operational Productivity Private Sector Banks Group (PB)

Rs. In Per centYear IIWF NIIWF SWF COD ROWF1991-92 10.849 1.154 4.504 6.577 1.29692-93 9.389 1.169 2.901 7.516 0.33793-94 9.057 1.337 3.012 6.851 0.57694-95 8.395 1.960 2.556 6.919 1.15695-96 9.286 2.084 2.432 9.180 1.21296-97 10.570 1.627 2.951 9.974 1.12797-98 9.735 1.927 2.451 8.493 1.03998-99 8.928 1.297 1.930 9.417 0.63099-2000 8.990 1.731 2.207 8.175 0.9272000-01 8.873 1.285 2.329 7.884 0.711

9.4072 1.5571 2.7273 8.0986 0.90112001-02 9.747 2.516 2.537 7.211 1.0822002-03 11.851 3.520 2.830 9.021 1.4282003-04 6.954 2.073 2.181 6.528 0.948

Productivity and profitability analysis of banking sector in India

137

2004-05 6.136 1.488 2.335 5.177 0.8372005-06 6.162 1.407 2.400 5.020 0.8622006-07 6.654 1.656 2.243 5.954 0.9142007-08 7.566 1.794 2.407 7.184 1.0132008-09 8.272 1.752 2.732 7.748 1.0542009-10 7.196 1.775 2.746 6.223 1.1392010-11 6.925 1.482 2.840 5.696 1.267

7.7463 1.9463 2.5251 6.5762 1.05448.57675 1.7517 2.6262 7.3374 0.97775

Source: 1) Financial Analysis of Banks2) Performance highlights of different banks

Table – 3.12 Operational Productivity Foreign Sector Banks Group (FB)Rs. In Per cent

Year IIWF NIIWF SWF COD ROWF

1991-92 11.202 3.416 3.923 10.617 2.430

92-93 11.617 0.993 3.561 12.053 -2.879

93-94 9.997 2.223 4.195 7.487 1.505

94-95 9.372 2.990 3.703 7.622 1.498

95-96 10.124 3.091 3.152 11.460 1.598

96-97 11.078 2.504 4.088 10.745 1.190

97-98 10.389 2.932 3.923 9.848 0.963

98-99 10.266 2.428 3.474 11.186 0.692

99-2000 9.873 2.599 3.852 10.109 1.169

2000-01 9.312 2.472 3.640 9.738 0.929

10.323 2.564 3.7511 10.0865 0.9095

2001-02 8.653 2.908 3.253 9.384 1.331

2002-03 7.674 2.642 3.340 7.294 1.566

2003-04 6.723 3.008 3.528 5.398 1.678

2004-05 6.837 2.882 3.824 4.671 1.478

2005-06 6.296 2.675 3.646 4.528 0.550

2006-07 6.481 2.495 3.742 5.050 1.650

2007-08 6.686 2.906 3.781 5.542 1.811

2008-09 6.781 3.330 3.915 5.987 1.679

2009-10 6.062 2.286 4.009 3.851 1.089

2010-11 5.803 2.232 3.642 4.413 1.570

6.799 2.736 3.668 5.6118 1.4402

8.561 2.647 3.709 7.3491 1.17485Source: 1) Financial Analysis of Banks

2) Performance highlights of different banks

The above analysis of bank productivity indicated that,business per employee productivity improved during the studyperiod of all four sample bank groups. However, business perbranch has decreased in three bank groups except nationalizedbank group. This indicates that SBI, PB and FB groups mustconcentrate on both deposits and advance pattern to increasethe interest income. It is observed that deposit per employee of

SBI, PB, and EB except NB declined which coincide withdeposit per branch productivity in which only NB has beenable to increase the deposit rate in the second phase and allother three groups have recorded a declining trend of depositper branch. On the other hand advance per employee (APE) ofthree bank groups; SBI, NB and PB witnessed an upwardmovement in the second phase except FB. Similarly APB

I.J.E.M.S., VOL.6 (3) 2015: 124 - 148 ISSN 2229-600X

138

(Advance per Branch) increased for SBI and NB groups but PBand FB groups experienced a negative productivity. SBI, PBbank groups have concentrated more on advance and loans andless on deposits resulting in a decrease in business per branchproductivity. These banks should emphasise more on thedeposit to increase their business per branch productivity.Further, FB group has given stress on deposits and lessattention on advance. In order to increase business productivityFB must focus on advances in order to increase businessproductivity and to earn more interest income.

It is seen from the analysis that interest income peremployee has increased for SBI, NB, PB groups. But FB grouphas experienced low productivity in IIPE the net result of lowproductivity both in APE and APB components. FB canrecover by giving more emphasis on advance and investments.Interest income per branch has declined for all except NBgroup since all the other three bank groups have opened eithermore branches than required or have some unviable brancheswhich need to be addressed by the management. Merger ofbranches can resolve the matter to a great extent.

The productivity analysis of NIIPE and NIIPB revealedthat both have moved different direction for all the four samplebank groups. NIIPE of the entire sample bank group have agrowth in productivity but NIIPB has a negative productivityfor all bank groups. This indicates that banks have earned morefrom diversified business. But NIIPB decreased because of theproblem of more branches or unviable branches. So it shouldeither close some unviable branches or take steps for merger ofbranches.

Interest expanded per employee (IEPE) and branch (IEPB)indices of productivity points out that SBI, PB and FB groupshave positive growth of productivity. But NB group hasnegative productivity indicating a high cost of fund.

The productivity analysis of spread to per employee andper branch showed a positive trend for SBI, NB and FB groups.PB has not able to improve it because it mostly comes underpressure due to differential pricing policy to meet thecompetition. PB should be more vigilant on mobilisingdeposits, borrowing and on expanding advances andinvestments. If PB continue with this trend of productivity itmay find difficult in enhancing profitability. The ratio ofinterest income / working fund for all of the four sample bankgroups had a negative growth almost for the entire studyperiod. Low productivity of interest income always affectsspread. Because severe competition in the banking industry itbecomes difficult for the entire bank group to increase interestincome. However, banks should concentrate in this mainbusiness of the bank to improve the growth rate interestincome.

Interest income/working fund of the entire four bank grouphave not increased. NB, PB, and FB groups have increased thisratio but SBI groups failed to improve the productivity in thesecond phase. It is to be considered that in the present bankingenvironment it is necessary to improve non interestproductivity as spread sparingly contribute to profitability. Soall the bank groups in general and SBI is particular mustconcentrate on increasing productivity.

The spread/ working fund were negative for the entirefour banks group and a decaling trend in the second phase. Thespread of the sample bank groups is coming under pressure dueto competition among banks. The cost of fund becoming highand at the same time priority sector lending factoring a low rateof interest income. In spite of these difficulties in order to bein the industry the bank should try to increase the spreadproductivity by reducing dependence on term deposit in orderto reduce the cost of fund and at the same time concentrate onreducing reverse requirement to allocate their resources inefficient manner. The cost of deposit of the entire four bankgroup should a positive sign. As all bank group have been ableto lowering the cost of deposit in the second phase indicatingtheir effort to improve productivity as well as productivity. Thebank should keep up this effort to improve speed.

Empirical analysis (profitability)

ANALYTICAL FRAME-WORKThe framework adopted for the purpose of analysis is chieflybased on the income and expenditure results in profit. There isdefinite relationship between income and expenditure whichneed to be carefully splitted and analysed, to derive theirrelative impact on profitability. At this juncture, it is importantto mention the various assumptions of the analyticalframework. The interest earned and interest paid are purely theprices of the funds lent and funds borrowed by banks.Manpower and all other expenses of a bank are incurred inorder to provide services to different customers including theborrowers and depositors. In other words, conceptually, aborrower pays interest only as the price for the funds put at hisdisposal. Lending by bank involves many other activities, i.e.processing of proposal, day to day operations in the accounts,or follow up of the accounts, all involving costs to the bank.Conceptually, these are services, and, it is a different matterwhether the bank charges for them separately or it provides thesame free of cost.

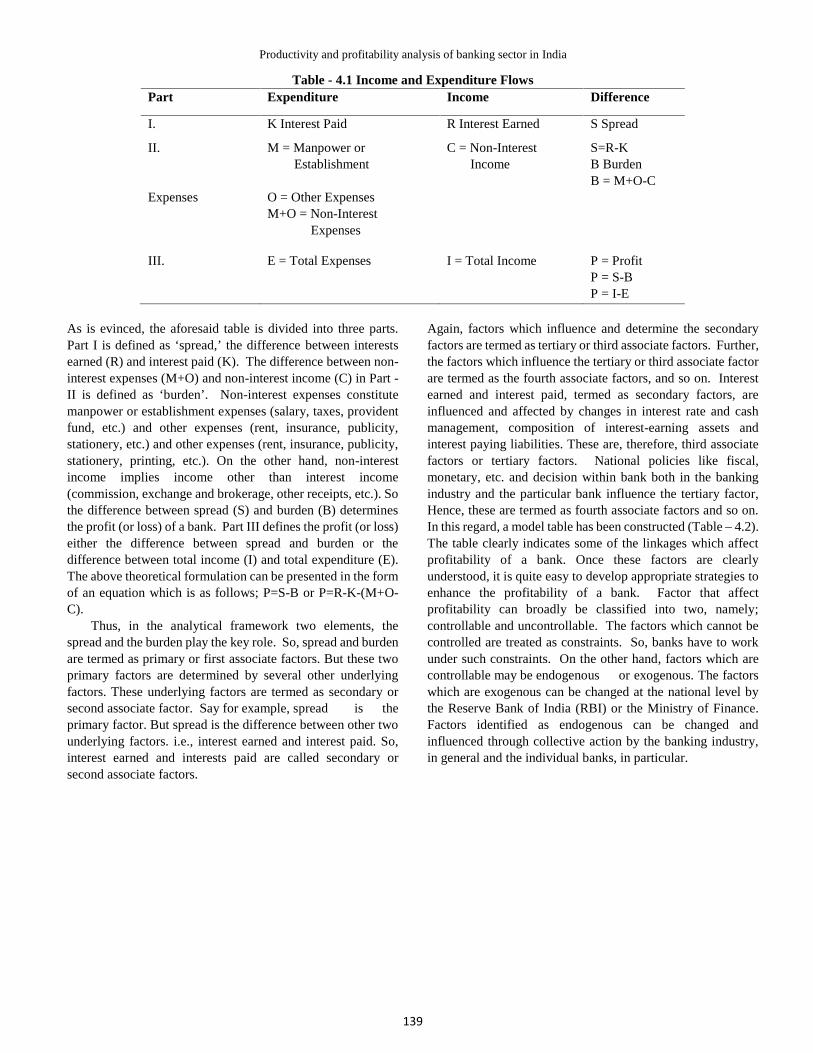

The key entities in income and expenditure statement of abank and their relationship are presented in Table-4.1 whichpresents the income and expenditure flows.

Productivity and profitability analysis of banking sector in India

139

Table - 4.1 Income and Expenditure FlowsPart Expenditure Income Difference

I. K Interest Paid R Interest Earned S Spread

II. M = Manpower orEstablishment

C = Non-InterestIncome

S=R-KB BurdenB = M+O-C

Expenses O = Other ExpensesM+O = Non-Interest

Expenses

III. E = Total Expenses I = Total Income P = ProfitP = S-BP = I-E

As is evinced, the aforesaid table is divided into three parts.Part I is defined as ‘spread,’ the difference between interestsearned (R) and interest paid (K). The difference between non-interest expenses (M+O) and non-interest income (C) in Part -II is defined as ‘burden’. Non-interest expenses constitutemanpower or establishment expenses (salary, taxes, providentfund, etc.) and other expenses (rent, insurance, publicity,stationery, etc.) and other expenses (rent, insurance, publicity,stationery, printing, etc.). On the other hand, non-interestincome implies income other than interest income(commission, exchange and brokerage, other receipts, etc.). Sothe difference between spread (S) and burden (B) determinesthe profit (or loss) of a bank. Part III defines the profit (or loss)either the difference between spread and burden or thedifference between total income (I) and total expenditure (E).The above theoretical formulation can be presented in the formof an equation which is as follows; P=S-B or P=R-K-(M+O-C).

Thus, in the analytical framework two elements, thespread and the burden play the key role. So, spread and burdenare termed as primary or first associate factors. But these twoprimary factors are determined by several other underlyingfactors. These underlying factors are termed as secondary orsecond associate factor. Say for example, spread is theprimary factor. But spread is the difference between other twounderlying factors. i.e., interest earned and interest paid. So,interest earned and interests paid are called secondary orsecond associate factors.

Again, factors which influence and determine the secondaryfactors are termed as tertiary or third associate factors. Further,the factors which influence the tertiary or third associate factorare termed as the fourth associate factors, and so on. Interestearned and interest paid, termed as secondary factors, areinfluenced and affected by changes in interest rate and cashmanagement, composition of interest-earning assets andinterest paying liabilities. These are, therefore, third associatefactors or tertiary factors. National policies like fiscal,monetary, etc. and decision within bank both in the bankingindustry and the particular bank influence the tertiary factor,Hence, these are termed as fourth associate factors and so on.In this regard, a model table has been constructed (Table – 4.2).The table clearly indicates some of the linkages which affectprofitability of a bank. Once these factors are clearlyunderstood, it is quite easy to develop appropriate strategies toenhance the profitability of a bank. Factor that affectprofitability can broadly be classified into two, namely;controllable and uncontrollable. The factors which cannot becontrolled are treated as constraints. So, banks have to workunder such constraints. On the other hand, factors which arecontrollable may be endogenous or exogenous. The factorswhich are exogenous can be changed at the national level bythe Reserve Bank of India (RBI) or the Ministry of Finance.Factors identified as endogenous can be changed andinfluenced through collective action by the banking industry,in general and the individual banks, in particular.

I.J.E.M.S., VOL.6 (3) 2015: 124 - 148 ISSN 2229-600X

140

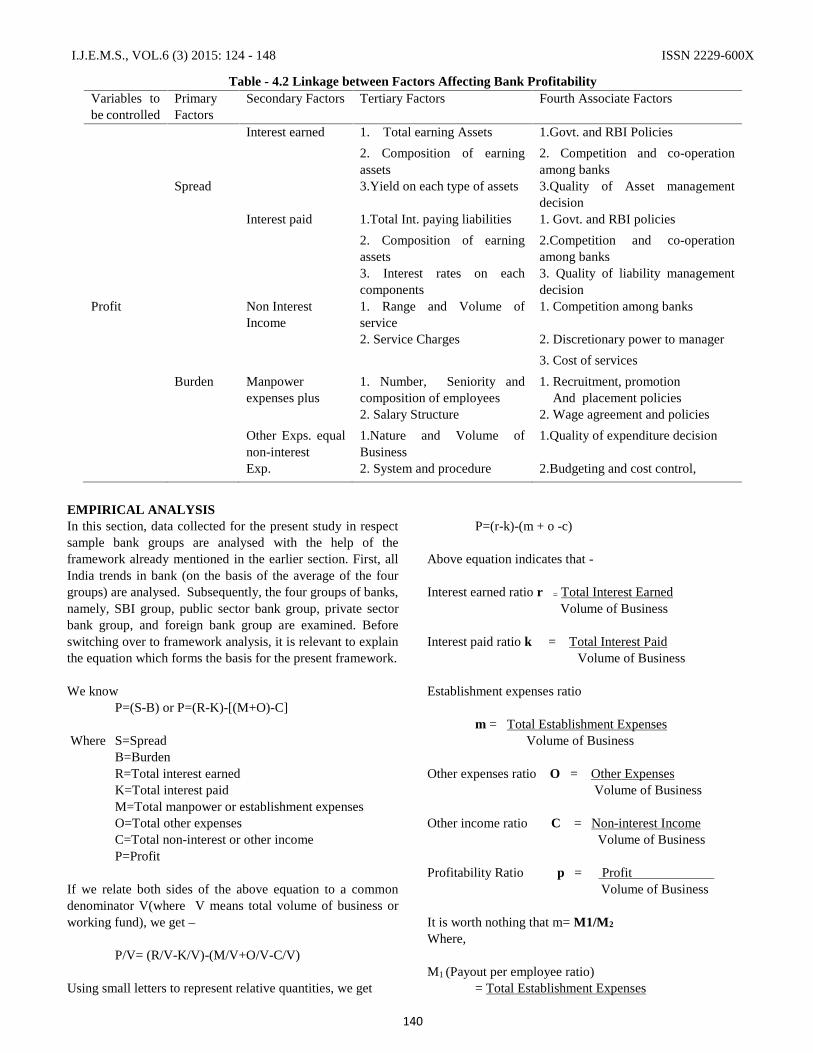

Table - 4.2 Linkage between Factors Affecting Bank ProfitabilityVariables tobe controlled

PrimaryFactors

Secondary Factors Tertiary Factors Fourth Associate Factors

Interest earned 1. Total earning Assets 1.Govt. and RBI Policies

2. Composition of earningassets

2. Competition and co-operationamong banks

Spread 3.Yield on each type of assets 3.Quality of Asset managementdecision

Interest paid 1.Total Int. paying liabilities 1. Govt. and RBI policies

2. Composition of earningassets

2.Competition and co-operationamong banks

3. Interest rates on eachcomponents

3. Quality of liability managementdecision

Profit Non InterestIncome

1. Range and Volume ofservice

1. Competition among banks

2. Service Charges 2. Discretionary power to manager

3. Cost of services

Burden Manpowerexpenses plus

1. Number, Seniority andcomposition of employees

1. Recruitment, promotionAnd placement policies

2. Salary Structure 2. Wage agreement and policies

Other Exps. equalnon-interest

1.Nature and Volume ofBusiness

1.Quality of expenditure decision

Exp. 2. System and procedure 2.Budgeting and cost control,

EMPIRICAL ANALYSISIn this section, data collected for the present study in respectsample bank groups are analysed with the help of theframework already mentioned in the earlier section. First, allIndia trends in bank (on the basis of the average of the fourgroups) are analysed. Subsequently, the four groups of banks,namely, SBI group, public sector bank group, private sectorbank group, and foreign bank group are examined. Beforeswitching over to framework analysis, it is relevant to explainthe equation which forms the basis for the present framework.

We knowP=(S-B) or P=(R-K)-[(M+O)-C]

Where S=SpreadB=BurdenR=Total interest earnedK=Total interest paidM=Total manpower or establishment expensesO=Total other expensesC=Total non-interest or other incomeP=Profit

If we relate both sides of the above equation to a commondenominator V(where V means total volume of business orworking fund), we get –

P/V= (R/V-K/V)-(M/V+O/V-C/V)

Using small letters to represent relative quantities, we get

P=(r-k)-(m + o -c)

Above equation indicates that -

Interest earned ratio r = Total Interest EarnedVolume of Business

Interest paid ratio k = Total Interest PaidVolume of Business

Establishment expenses ratio

m = Total Establishment ExpensesVolume of Business

Other expenses ratio O = Other ExpensesVolume of Business

Other income ratio C = Non-interest IncomeVolume of Business

Profitability Ratio p = ProfitVolume of Business

It is worth nothing that m= M1/M2

Where,

M1 (Payout per employee ratio)= Total Establishment Expenses

Productivity and profitability analysis of banking sector in India

141

Total Number of EmployeesM2 (Volume of business per employee ratio)

= Volume of BusinessTotal Number of Employees

Thus, the profit equation can be rewritten as follows;

P=(r-k)-(M1/M2+o-c)

It is apparent from the aforesaid equation that for increasingprofitability, a bank has to aim at widening the gap betweeninterest earned ratio and interest paid ratio so as to increasespread ratio and lowering the burden ratio. Increasing themagnitude of spread ratio can be achieved by increasing theinterest earned ratio (r) higher than the interest paid ratio (k).Lowering the burden ratio can be achieved by reducingmanpower or establishment expenses (m), other expenses (o),and increasing other income ratio (c). Again, lowering (m)ratio can be possible by increasing volume of business peremployee ratio (M2) faster than payout per employee ratio(M1). So, with the help of these indicators, analysis ofprofitability have been done for the all the sample bank groupsin the following sections.

EMPIRICAL ANALYSIS RESULT –TOTAL SAMPLE

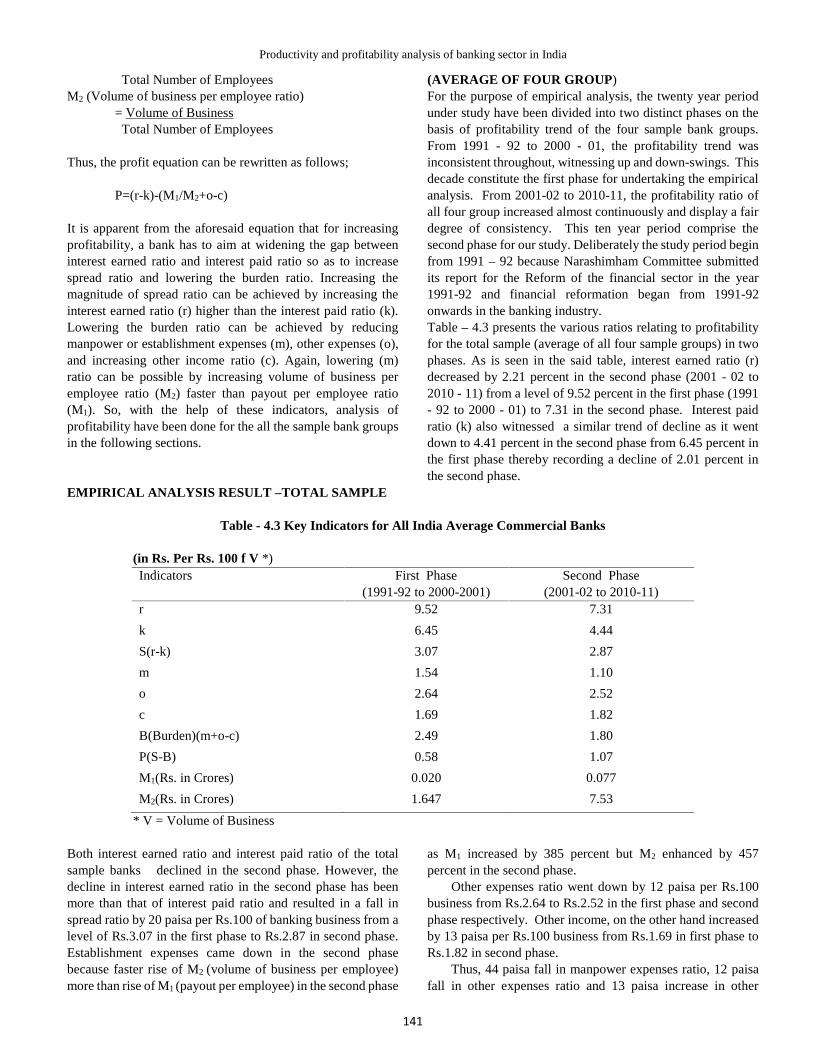

(AVERAGE OF FOUR GROUP)For the purpose of empirical analysis, the twenty year periodunder study have been divided into two distinct phases on thebasis of profitability trend of the four sample bank groups.From 1991 - 92 to 2000 - 01, the profitability trend wasinconsistent throughout, witnessing up and down-swings. Thisdecade constitute the first phase for undertaking the empiricalanalysis. From 2001-02 to 2010-11, the profitability ratio ofall four group increased almost continuously and display a fairdegree of consistency. This ten year period comprise thesecond phase for our study. Deliberately the study period beginfrom 1991 – 92 because Narashimham Committee submittedits report for the Reform of the financial sector in the year1991-92 and financial reformation began from 1991-92onwards in the banking industry.Table – 4.3 presents the various ratios relating to profitabilityfor the total sample (average of all four sample groups) in twophases. As is seen in the said table, interest earned ratio (r)decreased by 2.21 percent in the second phase (2001 - 02 to2010 - 11) from a level of 9.52 percent in the first phase (1991- 92 to 2000 - 01) to 7.31 in the second phase. Interest paidratio (k) also witnessed a similar trend of decline as it wentdown to 4.41 percent in the second phase from 6.45 percent inthe first phase thereby recording a decline of 2.01 percent inthe second phase.

Table - 4.3 Key Indicators for All India Average Commercial Banks

(in Rs. Per Rs. 100 f V *)Indicators First Phase

(1991-92 to 2000-2001)Second Phase

(2001-02 to 2010-11)r 9.52 7.31

k 6.45 4.44

S(r-k) 3.07 2.87

m 1.54 1.10

o 2.64 2.52

c 1.69 1.82

B(Burden)(m+o-c) 2.49 1.80

P(S-B) 0.58 1.07

M1(Rs. in Crores) 0.020 0.077

M2(Rs. in Crores) 1.647 7.53

* V = Volume of Business

Both interest earned ratio and interest paid ratio of the totalsample banks declined in the second phase. However, thedecline in interest earned ratio in the second phase has beenmore than that of interest paid ratio and resulted in a fall inspread ratio by 20 paisa per Rs.100 of banking business from alevel of Rs.3.07 in the first phase to Rs.2.87 in second phase.Establishment expenses came down in the second phasebecause faster rise of M2 (volume of business per employee)more than rise of M1 (payout per employee) in the second phase

as M1 increased by 385 percent but M2 enhanced by 457percent in the second phase.

Other expenses ratio went down by 12 paisa per Rs.100business from Rs.2.64 to Rs.2.52 in the first phase and secondphase respectively. Other income, on the other hand increasedby 13 paisa per Rs.100 business from Rs.1.69 in first phase toRs.1.82 in second phase.

Thus, 44 paisa fall in manpower expenses ratio, 12 paisafall in other expenses ratio and 13 paisa increase in other

I.J.E.M.S., VOL.6 (3) 2015: 124 - 148 ISSN 2229-600X

142

income ratio in the second phase of the study contributed anaggregate fall of 69 paisa (44+12+13) per Rs.100 of businessin burden ratio. Profitability ratio increased by 49 paisa perRs.100 business in the second phase from (58 paisa in the firstphase to Rs. 1.07 in the second phase). The growth of profit iscalculated as 84.48 percent in the second phase for theaggregate sample banks over the first phase of the study period.

It is inferred from Table- 4.3 that rise in the profitabilityratio of the sample banks in the second phase was only due tofall in burden ratio i.e. fall in both establishment ratio and otherexpenses ratio and rise in other income ratio. It is observed thatspread ratio which is regarded as the main contributor to theprofitability ratio, made a negative impact on profitability ratiodue to fall of 20 paisa per Rs.100 business. Despite thenegative contribution by sprea, sample commercial bankscould earn more profit due to good management of burdenwhich was responsible for rise in profit. The burden ratio(m+o-c) made positive impact on profit because decline inestablishment ratio which became possible due to faster rise involume of business (M2) than payment per employee (M1)ratio. Other expenses ratio, another constituent of burden ratioalso could make a positive impact on profitability ofcommercial banks because of fall of other expenses ratio.

Other income ratio of all the commercial banks alsoincreased in the second phase and made favorable impact onprofit. The other income based on non-fund based business

like commission based business such as guarantees, foreignexchange business, remittance of fund and other servicerendered to the customer have positive impact on profitabilityratio. So combine establishment ratio, other expenses ratio andother fee-based business otherwise known as other incomeratio can play a key role in improving the profitability ratioeven if there is a decline in spreads, as witnessed from theabove table. Hence we can conclude that increase in volumeof business, increase in non-fund business and control overnon-interest expenses (combine regarded as good managementof burden) can have positive impact on profitability ofcommercial banks. This can even negate the negative impactby spread.

EMPIRICAL ANALYSIS RESULTS: GROUP-WISEThe foregone analysis broadly explains the profitability of totalsample banks and the factor influencing for the twenty yearperiod under study. In this section profitability throughempirical analysis has been undertaken for the four samplebank groups i.e. S.B.I. group, nationalised bank group, privatesector bank group and foreign bank group operating in IndiaSuch an analysis would help to reach at a tentative conclusionabout the various factors that influences the profitability ofsample bank groups. Besides, it would also indicate whetherall the four bank groups under analysis have been influencedidentically or otherwise by the various factors of profitability.

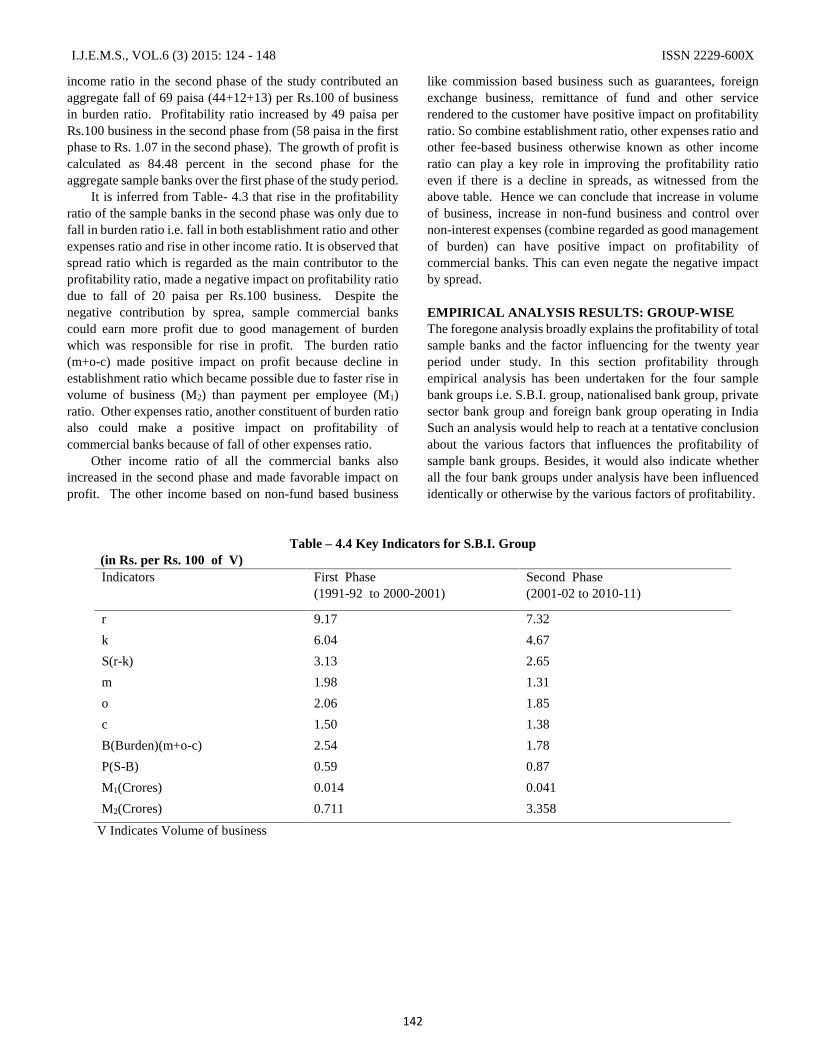

Table – 4.4 Key Indicators for S.B.I. Group(in Rs. per Rs. 100 of V)Indicators First Phase

(1991-92 to 2000-2001)Second Phase(2001-02 to 2010-11)

r 9.17 7.32

k 6.04 4.67

S(r-k) 3.13 2.65

m 1.98 1.31

o 2.06 1.85

c 1.50 1.38

B(Burden)(m+o-c) 2.54 1.78

P(S-B) 0.59 0.87

M1(Crores) 0.014 0.041

M2(Crores) 0.711 3.358

V Indicates Volume of business

Productivity and profitability analysis of banking sector in India

143

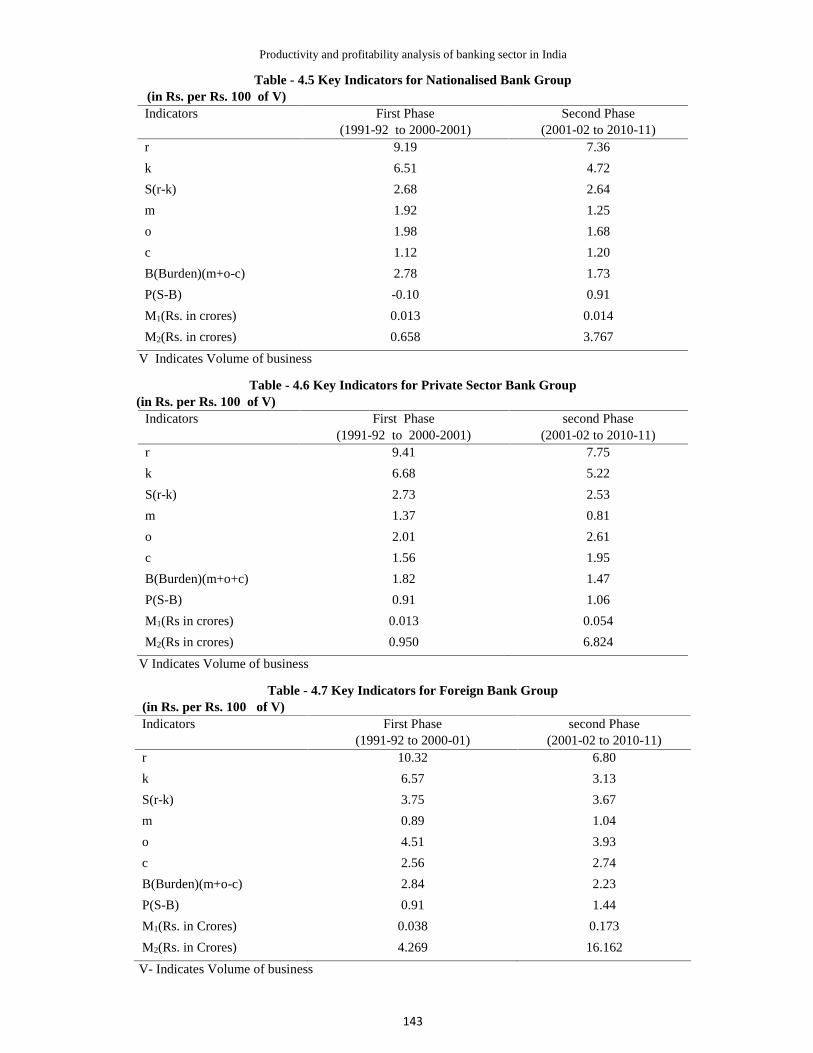

Table - 4.5 Key Indicators for Nationalised Bank Group(in Rs. per Rs. 100 of V)Indicators First Phase

(1991-92 to 2000-2001)Second Phase

(2001-02 to 2010-11)r 9.19 7.36

k 6.51 4.72

S(r-k) 2.68 2.64

m 1.92 1.25

o 1.98 1.68

c 1.12 1.20

B(Burden)(m+o-c) 2.78 1.73

P(S-B) -0.10 0.91

M1(Rs. in crores) 0.013 0.014

M2(Rs. in crores) 0.658 3.767

V Indicates Volume of business

Table - 4.6 Key Indicators for Private Sector Bank Group(in Rs. per Rs. 100 of V)

Indicators First Phase(1991-92 to 2000-2001)

second Phase(2001-02 to 2010-11)

r 9.41 7.75

k 6.68 5.22

S(r-k) 2.73 2.53

m 1.37 0.81

o 2.01 2.61

c 1.56 1.95

B(Burden)(m+o+c) 1.82 1.47

P(S-B) 0.91 1.06

M1(Rs in crores) 0.013 0.054

M2(Rs in crores) 0.950 6.824

V Indicates Volume of business

Table - 4.7 Key Indicators for Foreign Bank Group(in Rs. per Rs. 100 of V)Indicators First Phase

(1991-92 to 2000-01)second Phase

(2001-02 to 2010-11)r 10.32 6.80

k 6.57 3.13

S(r-k) 3.75 3.67

m 0.89 1.04

o 4.51 3.93

c 2.56 2.74

B(Burden)(m+o-c) 2.84 2.23

P(S-B) 0.91 1.44

M1(Rs. in Crores) 0.038 0.173

M2(Rs. in Crores) 4.269 16.162

V- Indicates Volume of business

I.J.E.M.S., VOL.6 (3) 2015: 124 - 148 ISSN 2229-600X

144

The above tables profitability analysis of the four sample bankgroups have been undertaken by dividing the twenty yearperiod under study into two distinct phases; the first phasecovering ten years and second phase comprising the latter tenyears. The analysis has been done through an analyticalframework so as to find out the factors affecting profitability.This framework splits the income and expenditure statement tofind out the relation between different components of incomeand expenditure and its impact on profitability. Basically,spread, difference between interests earned and interest paidand burden play major role in determining the profitability ofa commercial bank. Both spread and burden are treated asprimary on first associate factor. Factors which determine thisprimary factor are treated as secondary factor. Factors whichdetermine their secondary factors are known as tertiary factor.The factors which influence this tertiary factor are termed asfourth associate factors. The framework adopted for thepurpose of analysis have spread, burden and its components areto be related to a common denominator, volume of business(V) and to convert these into ratio. Establishment ratio isderived by dividing payout per employee (M1) by volume ofbusiness per employee (M2).

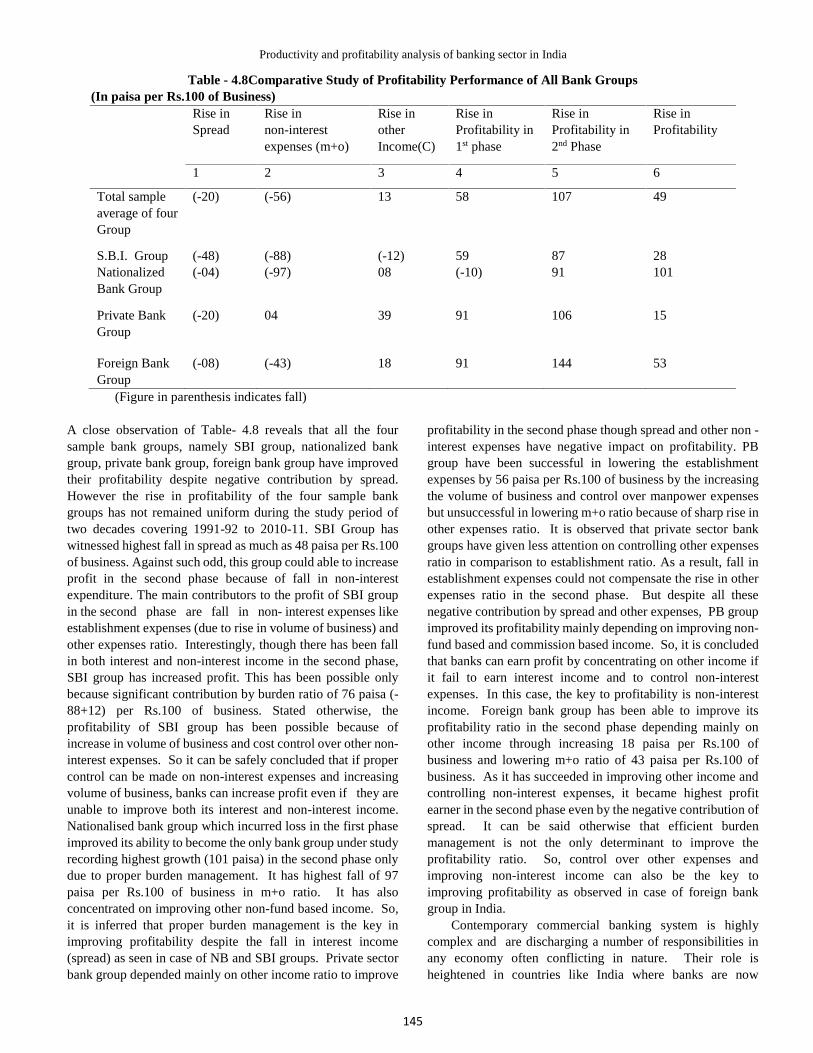

Analysis of total sample (average of all four samplegroups) during second phase reveals that fall in establishmentexpenses, fall in other expenses and rise in other income ratioare the major determinant and main contributors toprofitability. However, fall in spread ratio had a negativeimpact on profitability. So, increase in volume of business,control over other expenses and increase in fee-based businessof banking sector have a positive impact on the profitability ofthe banking sector during the post reform era.

Sample group wise, S.B.I. bank group has improvedprofitability ratio due to fall in establishment ratio, fall in otherexpenses ratio. In this case, spread and other income havemade negative contribution to the profitability ratio. Here thekey to profitability is volume of business, check on otherexpenses and increase in commission based income.

Analysis of nationalized bank group indicates that bothestablishment ratio and other expenses ratio declined in thesecond phase. Over the same period other income ratio alsoincreased. Contrary to expectations, spread influencednegatively to the profitability ratio. Profitability ofnationalized bank group improved in the second phase onlydue to positive contribution by burden ratio. So, increasedvolume of business, check on other expenses and increase non-

fund based business are the main contributors to theprofitability ratio of nationalized bank group.

Analysis undertaken for sample private sector bank groupdepicts that decrease in establishment ratio and increase inother income ratio made it possible to improve profitability forthis group in the second phase despite negative support byspread and other expenses ratio. So, volume of business andfee-based income are main determinants of profitability in caseof sample private sector banks.

Perusal of framework for analysis of foreign bank groupindicates that spread and establishment expenses contributednegatively to the profitability in the second phase. Butdecrease in other expenses and increase in other income ratioare the main factors which improved profitability ratio offoreign bank group in the second phase of our study. Despitenegative contribution by establishment expenses ratio, burdenratio decreased in the second phase due to support of otherexpenses and income ratio and profitability improved in asituation where spread, the interest income, went down tocreate negative contribution on profitability. So, key toprofitability in case of foreign bank group is proper handlingof burden ratio.

Comparative study of all four groups reveals that in- spiteof fall in spread ratio in the entire sample four bank groups inthe second decade of the study period, profitability hadimproved in the second phase. None of the four sample bankgroups deepened on spread ratio which is widely considered asthe main determinant of profitability ratio of a bank. All thesample bank groups, alternatively stressed on the propermanagement of burden to increase profitability. Thus it isrevealed that when compulsive reasons does not allowenhancement of the spread volume by the banks, profitabilitycan be improved with proper handling and managing ofburden. So under Indian financial environment burdenmanagement seems to be an important strategy for enhancingprofitability along with successful discharge of socialresponsibility.

COMPARATIVE ANALYSIS OF THE FOUR SAMPLEBANK GROUPSTable - 4.8 summaries study of the four sample bank groups aswell as of the total sample (average of four groups) with themagnitude of rise in spread ratio rise non-interest expenses(establishment plus other expenses) and rise in other incomeratio.

Productivity and profitability analysis of banking sector in India

145