procter & gamble - ubs · procter & gamble confidently, leading the industry forward...

TRANSCRIPT

www.ubs.com/investmentresearch

This report has been prepared by UBS Securities LLC. ANALYST CERTIFICATION AND REQUIRED DISCLOSURES BEGIN ON PAGE 12. UBS does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

Global Research 17 April 2020

Procter & Gamble Confidently, Leading the Industry Forward

Procter issues insightful state of the industry commentary Procter's CFO and COO fielded its F3Q earnings call with a refreshingly candid account of portfolio performance and end-market insights. PG was keen to note that a global demand surge in March for at-home use products pulled-forward +2pp in sales from its (Apr-Jun) qtr, resulting in an implied FQ4 sales and EPS range below Sell-side ests. In our view, this is not a negative. Fundamentally, PG is gaining customer wallet share and is leveraging global supply chain dependability to gain mindshare w/key retailers. Though Procter is bracing for global recession, Procter is confident in its ability to grow org sales, volume, cash flow and dividend in this setting. We anticipate Street FQ4 ests to come-in, given increased FX pressure & pantry deload effects. For FY21 we anticipate global org sales to grow 2-3% as PG mentioned end-markets could slow 1pp.

Insights on PG’s portfolio performance and end-market growth By region in FQ3, the US org sales grew +10%, European Enterprise markets +15%, Lat Am +11% (price/mix +7%, w/ Mexico +6%, Brazil +3%) and India declined -8% from a halt in shopping trips (but is expected to normalize as consumers generally don’t hold much inventory and shops are expected to reopen in coming weeks). By channel, Ecommerce grew +40% in FQ3, driven by the US and China. Usage occasions in dishwashing and laundry have increased, with some categories growing 50+%, reducing volume sold on promotion -5%. Beauty in mainland China market is expected to improve sequentially in FQ4, though travel retail sales remain a partial headwind.

Assessing PG’s recession durability and long term implications In bracing for a global recession, PG’s current portfolio is now more indexed to daily use products, with value and superior function relative to its competition in the last recession. Consumer behavioral changes (more time spent at home, cleanliness standards) are long term growth drivers to PG’s end categories. With retailers now contemplating longer term SKU count reductions, Procter could benefit from lower costs from the simplification and challenger brands more at bay given shelf streamlines.

Valuation: Maintain $126 PT based on 25x P/E and 17x EV/EBITDA multiples We lower our Q4 organic sales to 0.4% (from +1.5%) and our adj EPS to $0.94 from $1.01. Our FY20 organic sales est of +4.5% and adj EPS of $4.90 are unchanged.

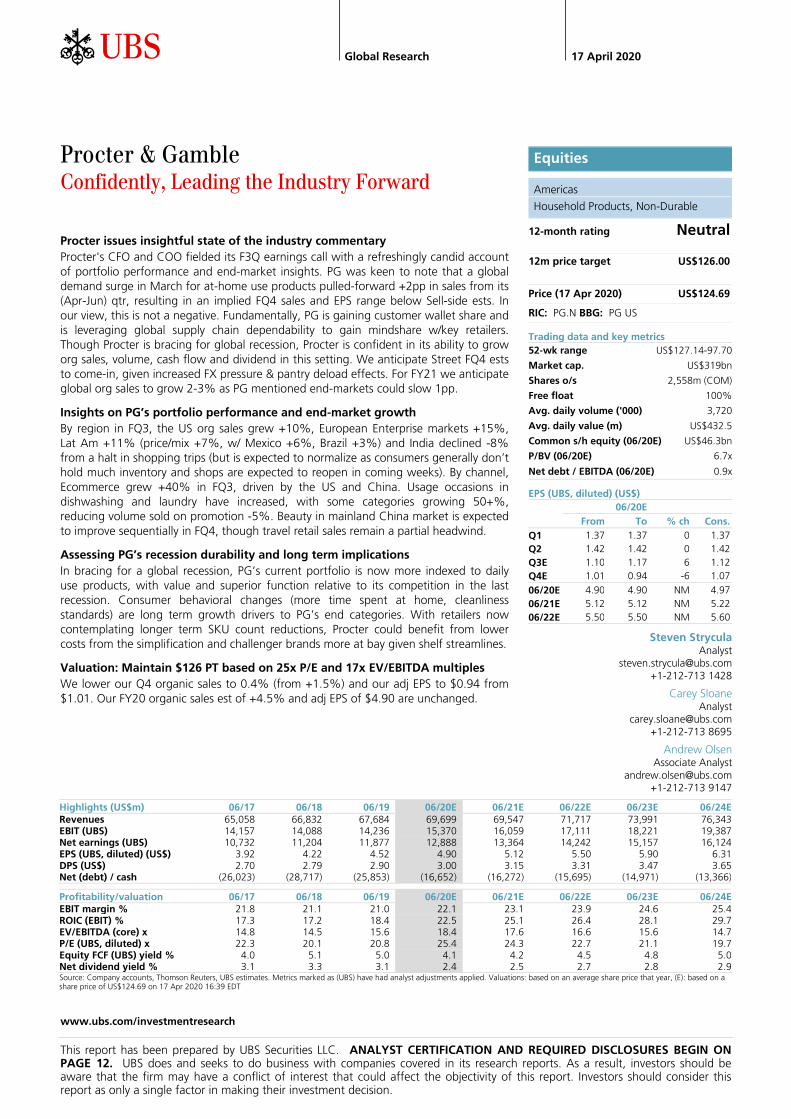

Equities

Americas

Household Products, Non-Durable

12-month rating Neutral

12m price target US$126.00

Price (17 Apr 2020) US$124.69

RIC: PG.N BBG: PG US

Trading data and key metrics 52-wk range US$127.14-97.70

Market cap. US$319bn

Shares o/s 2,558m (COM)

Free float 100%

Avg. daily volume ('000) 3,720

Avg. daily value (m) US$432.5

Common s/h equity (06/20E) US$46.3bn

P/BV (06/20E) 6.7x

Net debt / EBITDA (06/20E) 0.9x

EPS (UBS, diluted) (US$) 06/20E From To % ch Cons.

Q1 1.37 1.37 0 1.37 Q2 1.42 1.42 0 1.42 Q3E 1.10 1.17 6 1.12 Q4E 1.01 0.94 -6 1.07

06/20E 4.90 4.90 NM 4.97 06/21E 5.12 5.12 NM 5.22 06/22E 5.50 5.50 NM 5.60

Steven Strycula Analyst

[email protected] +1-212-713 1428

Carey Sloane Analyst

[email protected] +1-212-713 8695

Andrew Olsen Associate Analyst

[email protected] +1-212-713 9147

Highlights (US$m) 06/17 06/18 06/19 06/20E 06/21E 06/22E 06/23E 06/24E Revenues 65,058 66,832 67,684 69,699 69,547 71,717 73,991 76,343 EBIT (UBS) 14,157 14,088 14,236 15,370 16,059 17,111 18,221 19,387 Net earnings (UBS) 10,732 11,204 11,877 12,888 13,364 14,242 15,157 16,124 EPS (UBS, diluted) (US$) 3.92 4.22 4.52 4.90 5.12 5.50 5.90 6.31 DPS (US$) 2.70 2.79 2.90 3.00 3.15 3.31 3.47 3.65 Net (debt) / cash (26,023) (28,717) (25,853) (16,652) (16,272) (15,695) (14,971) (13,366)

Profitability/valuation 06/17 06/18 06/19 06/20E 06/21E 06/22E 06/23E 06/24E EBIT margin % 21.8 21.1 21.0 22.1 23.1 23.9 24.6 25.4 ROIC (EBIT) % 17.3 17.2 18.4 22.5 25.1 26.4 28.1 29.7 EV/EBITDA (core) x 14.8 14.5 15.6 18.4 17.6 16.6 15.6 14.7 P/E (UBS, diluted) x 22.3 20.1 20.8 25.4 24.3 22.7 21.1 19.7 Equity FCF (UBS) yield % 4.0 5.1 5.0 4.1 4.2 4.5 4.8 5.0 Net dividend yield % 3.1 3.3 3.1 2.4 2.5 2.7 2.8 2.9 Source: Company accounts, Thomson Reuters, UBS estimates. Metrics marked as (UBS) have had analyst adjustments applied. Valuations: based on an average share price that year, (E): based on a share price of US$124.69 on 17 Apr 2020 16:39 EDT

Steven Strycula, Analyst, [email protected], +1-212-713 1428

Procter & Gamble 17 April 2020

2

Procter & Gamble Neutral (Price target US$126.00)

UBS Research THESIS MAP a guide to our thinking and what's where in this report

PIVOTAL QUESTIONS Q: Can Procter grow modestly ahead of underlying market growth of +3-3.5% long term? Yes, we forecast P&G to grow sales at least in-line with category end-markets of 3%, if not more. We model a 3-year organic sales CAGR of +3%. Our analysis credits P&G for its scale advantage which has resulted in #1 share positioning across ~88% of its top 16 U.S. categories.

"The Procter Effect” 1 year later: Measuring How HPC Peers Stack-up Against P&G " 10/10/2019

Q: Can P&G’s cost plan generate upside to Street FY21 EBIT margin? Possibly. We forecast FY21 EBIT margin expansion of +110 bps. A key source of upside will be if PG is able to deliver on its $10 billion cost plan. Three years into Procter’s second $10 billion productivity program, PG has realized $5.3 billion of the $10 billion in savings, signifying a greater cadence of cost savings coming in FY20 and FY21.

UBS VIEW

Procter's $10 billion reinvestment cycle and scale across a diverse set of CPG categories will engage profit pool battles and is likely to limit EPS upside for its most direct competitors. After undergoing organizational changes and portfolio divestitures, P&G has #1 share positioning across 88% of its top categories and has positive share changes across 69% in its top categories. We view Kimberly-Clark and Edgewell as the most exposed to PG and the largest share donors to PG as well. Given PG’s scale across the CPG space, we expect PG to maintain its leading market position and deliver growth in-line or above its category growth rates of +3-3.5%.

EVIDENCE

We leverage Nielsen data to identify category/company combinations with the most overlap to P&G, categories where PG is outperforming its peers and the category growth rate, and then identify the dollar impact to the most and least exposed companies. We then analyze portfolio divestitures and organizational changes PG has made since 2014 to assess the drivers behind its share gains and sales acceleleration.

WHAT'S PRICED IN? Consensus forecast P&G to grow +4.5% in FY20 and +2.1% in FY21. We see modest upside to these estimates. But ~25x EPS, P&G trades ~1x higher than its peers and at a 7% premium to its historical averages. And at ~17x EV/EBITDA, an 11% premium to its 5-year average, it appears the market already is crediting PG for its sales turn and continued strong top line growth.

UPSIDE / DOWNSIDE SPECTRUM

Value drivers

3-year organic sales CAGR

FY2020 gross margins

FY2020 EBIT margins

FY2020 adj EPS

$146 upside 3.3% 50.9% 22.7% $4.94 $126 base 2.3% 50.6% 22.1% $4.90 $104 downside 1.3% 50.4% 21.4% $4.79 Source: UBS

more

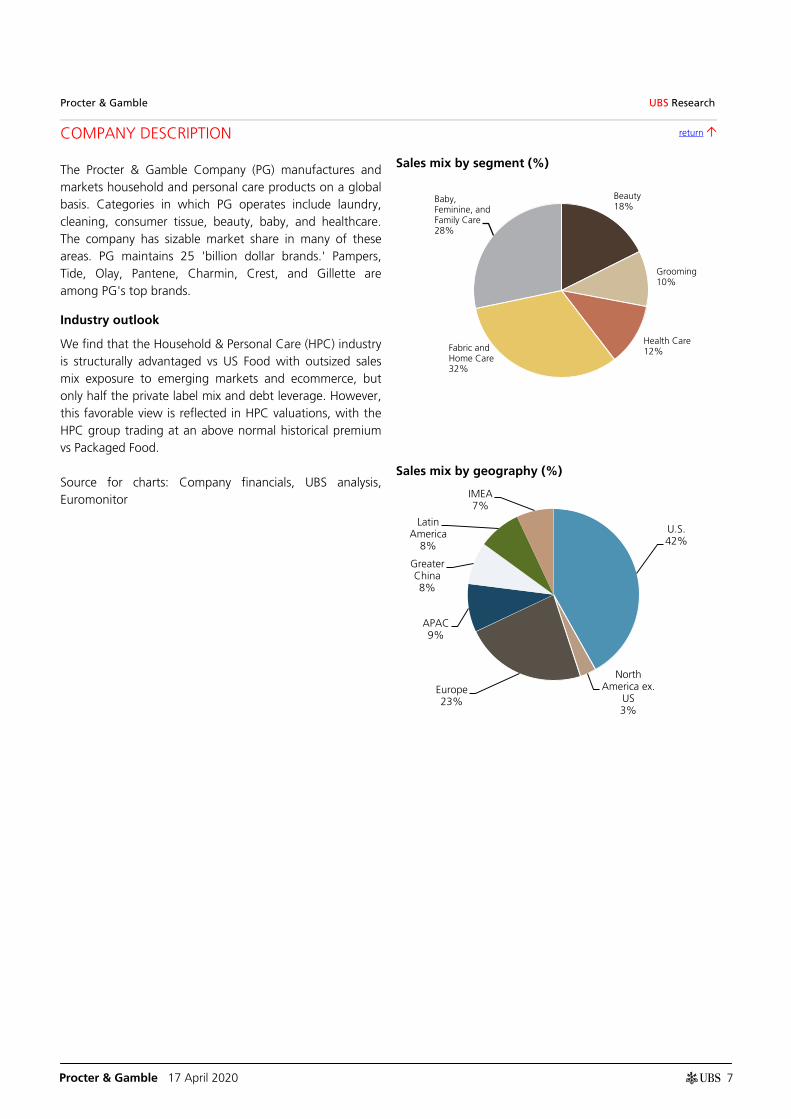

COMPANY DESCRIPTION The Procter & Gamble Company (PG) manufactures and markets household and personal care products on a global basis. Categories in which PG operates include laundry, cleaning,...

more

+17%

+1%

-17%

7080

90

100

110

120

130

140

150

160

2018 2019 2020

Upside:

Base:

Downside:

146.00 =

126.00 =

104.00 =

29.6x

25.7x

21.7x

4.94 x

4.90 x

4.79 x

US$124.69PG.N Price

17 Apr +12 mo.

P/E (UBS) Implied

EPS (UBS) 06/20E

Upside to Downside

1 to 1

Source: UBS Research

Procter & Gamble 17 April 2020

3

Procter & Gamble UBS Research

return

Notes from PG’s 3Q earnings call and follow-up call

Sales Trends

Organic Sales shift: PG expects 2% of organic sales growth from shift from Q4 into Q3 from pantry loading. Guidance implies F4Q sales of 0% to 4% which is equivalent to -2% to +2% post the 2% shift from F3Q.

Organic Sales: 9 of 10 categories growing organic sales with broad based share gains. Org sales by region: +10% US; 14% Canada; 6% European Focus markets; 15% in Euro Enterprise markets; 11% Lat Am.

Recession: PG believes they have built a better portfolio if they were to see a more drastic recessionary environment through its shift to daily use categories and messaging on value proposition of the premium products. In the ’08-’09 recession category growth rates contracted about 1%.

Baby and Family: Recent share decline in baby and family is due to out of stocks in high demand brands. Expect share softness to continue as pantry loading is extreme.

Near term trends: April in the US = +DD from an order stand point, expect to level off with retailer restocking and consumer demand. PG is seeing increased consumption levels, not just buying and stocking up.

Longer term trends: Could be more time spent at home, cleaning at home, demand for established brands, less experimental, ecommerce growth. In terms of assortment there may be potential for cutting long tailed, inefficient SKUs.

Ecommerce: Online salse grew +40% in the quarter and is now near ~10% of total mix. US and China are largest contributors. Longer term trend could result in a more permanent shift of sales mix moving online.

Private Label: Procter is seeing modest increases in PL share in North America; Europe PL share declines are more consistent.

Innovation: The window to roll out new innovation is typically in the January to April timeframe so PG was able to distribute a lot of innovation market ahead of the COVID-19 demand surge. For example Microban 24, Tide power pods and Dawn Power wash were already out and marketed.

Regional Trends

China: At CAGNY (end of Feb), PG expected China to be down possibly 20% but given the changing dynamics in just a few weeks, Greater China was down -8% ex travel-retail in Q3.

Travel Retail: This ~$700-800m business is down significantly YoY. The +1% growth in Beauty was inclusive of a greater than -20% reduction in SKII sales, showing the resiliency of other areas of PG’s Beauty portfolio.

Procter & Gamble 17 April 2020

4

India: Sales in FQ3 were -8% as March sales slowed from store foot traffic declines and store closures. PG's biggest categories in India are Baby Care, Fem care and Personal Care (Vics). In a recessionary environment absolute sales might slightly decline, but PG would try to grow share and outgrow its categories.

Emerging Markets: No change to PG’s strategy in EMs and they expect to see continued growth in this region. As an example, Lat AM grew +11% in the quarter so EM will be an important growth driver going forward.

Margins

Promotion Spend: For the full quarter, the amount of volume on promo is down 5% due to the surge in demand. Mgmt anticipates potential for less promo in coming quarters as overall consumption remains elevated.

Margins: Saw positive margin development in FQ3, guidance implies positive margins for the year. Commodities are a tailwind more long term (FY21) with continued efforts on the productivity program.

Financial

Guidance: PG believes current top and bottom ranges of FY guidance are still relevant. The company reaffirmed organic sales of +4 to +5% but lowered net sales to +3 to +4% (from +4 to +5%) from stronger headwinds from FX (expected to be 2pp headwinds).

Liquidity: Liquidity remains strong and PG is focused on maintaining investment grade credit rating. Issued a $5 billion bond, issued three weeks ago, that brings total cash on hand to $15 billion (and are generating more each day). PG can cover upcoming maturities with this cash on hand and doesn’t expect the need to draw on its untapped $8 billion bank credit lines.

Currency: Watching the FX markets carefully over the next 12-18 months. Uncertain how the current deflationary environment will last and if they persist for a longer duration, PG will adjust hedging strategy as necessary. In the fourth quarter, FX is currently forecast to be a 7 point hit to core EPS growth.

Procter & Gamble 17 April 2020

5

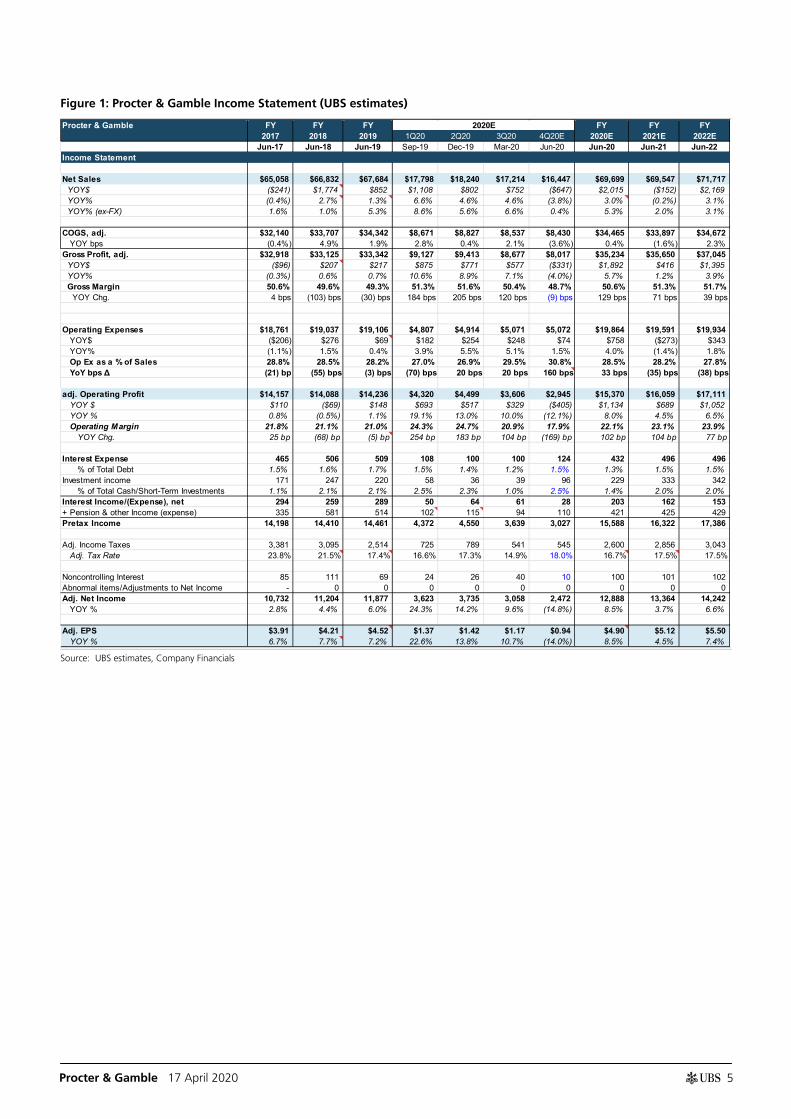

Figure 1: Procter & Gamble Income Statement (UBS estimates)

Source: UBS estimates, Company Financials

Procter & Gamble FY FY FY 2020E FY FY FYIncome Statement 2017 2018 2019 1Q20 2Q20 3Q20 4Q20E 2020E 2021E 2022E

Jun-17 Jun-18 Jun-19 Sep-19 Dec-19 Mar-20 Jun-20 Jun-20 Jun-21 Jun-22Income Statement

Net Sales $65,058 $66,832 $67,684 $17,798 $18,240 $17,214 $16,447 $69,699 $69,547 $71,717 YOY$ ($241) $1,774 $852 $1,108 $802 $752 ($647) $2,015 ($152) $2,169 YOY% (0.4%) 2.7% 1.3% 6.6% 4.6% 4.6% (3.8%) 3.0% (0.2%) 3.1% YOY% (ex-FX) 1.6% 1.0% 5.3% 8.6% 5.6% 6.6% 0.4% 5.3% 2.0% 3.1%

COGS, adj. $32,140 $33,707 $34,342 $8,671 $8,827 $8,537 $8,430 $34,465 $33,897 $34,672 YOY bps (0.4%) 4.9% 1.9% 2.8% 0.4% 2.1% (3.6%) 0.4% (1.6%) 2.3%Gross Profit, adj. $32,918 $33,125 $33,342 $9,127 $9,413 $8,677 $8,017 $35,234 $35,650 $37,045 YOY$ ($96) $207 $217 $875 $771 $577 ($331) $1,892 $416 $1,395 YOY% (0.3%) 0.6% 0.7% 10.6% 8.9% 7.1% (4.0%) 5.7% 1.2% 3.9% Gross Margin 50.6% 49.6% 49.3% 51.3% 51.6% 50.4% 48.7% 50.6% 51.3% 51.7% YOY Chg. 4 bps (103) bps (30) bps 184 bps 205 bps 120 bps (9) bps 129 bps 71 bps 39 bps

Operating Expenses $18,761 $19,037 $19,106 $4,807 $4,914 $5,071 $5,072 $19,864 $19,591 $19,934 YOY$ ($206) $276 $69 $182 $254 $248 $74 $758 ($273) $343 YOY% (1.1%) 1.5% 0.4% 3.9% 5.5% 5.1% 1.5% 4.0% (1.4%) 1.8% Op Ex as a % of Sales 28.8% 28.5% 28.2% 27.0% 26.9% 29.5% 30.8% 28.5% 28.2% 27.8% YoY bps Δ (21) bp (55) bps (3) bps (70) bps 20 bps 20 bps 160 bps 33 bps (35) bps (38) bps

adj. Operating Profit $14,157 $14,088 $14,236 $4,320 $4,499 $3,606 $2,945 $15,370 $16,059 $17,111 YOY $ $110 ($69) $148 $693 $517 $329 ($405) $1,134 $689 $1,052 YOY % 0.8% (0.5%) 1.1% 19.1% 13.0% 10.0% (12.1%) 8.0% 4.5% 6.5% Operating Margin 21.8% 21.1% 21.0% 24.3% 24.7% 20.9% 17.9% 22.1% 23.1% 23.9% YOY Chg. 25 bp (68) bp (5) bp 254 bp 183 bp 104 bp (169) bp 102 bp 104 bp 77 bp

Interest Expense 465 506 509 108 100 100 124 432 496 496 % of Total Debt 1.5% 1.6% 1.7% 1.5% 1.4% 1.2% 1.5% 1.3% 1.5% 1.5%Investment income 171 247 220 58 36 39 96 229 333 342 % of Total Cash/Short-Term Investments 1.1% 2.1% 2.1% 2.5% 2.3% 1.0% 2.5% 1.4% 2.0% 2.0%Interest Income/(Expense), net 294 259 289 50 64 61 28 203 162 153+ Pension & other Income (expense) 335 581 514 102 115 94 110 421 425 429Pretax Income 14,198 14,410 14,461 4,372 4,550 3,639 3,027 15,588 16,322 17,386

Adj. Income Taxes 3,381 3,095 2,514 725 789 541 545 2,600 2,856 3,043 Adj. Tax Rate 23.8% 21.5% 17.4% 16.6% 17.3% 14.9% 18.0% 16.7% 17.5% 17.5%

Noncontrolling Interest 85 111 69 24 26 40 10 100 101 102Abnormal items/Adjustments to Net Income - 0 0 0 0 0 0 0 0 0Adj. Net Income 10,732 11,204 11,877 3,623 3,735 3,058 2,472 12,888 13,364 14,242 YOY % 2.8% 4.4% 6.0% 24.3% 14.2% 9.6% (14.8%) 8.5% 3.7% 6.6%

Adj. EPS $3.91 $4.21 $4.52 $1.37 $1.42 $1.17 $0.94 $4.90 $5.12 $5.50 YOY % 6.7% 7.7% 7.2% 22.6% 13.8% 10.7% (14.0%) 8.5% 4.5% 7.4%

Procter & Gamble 17 April 2020

6

Procter & Gamble UBS Research

UPSIDE / DOWNSIDE SPECTRUM return

Value drivers

3-year organic sales CAGR

FY2020 gross margins

FY2020 EBIT margins

FY2020 adj EPS

$146 upside 3.3% 50.9% 22.7% $4.94 $126 base 2.3% 50.6% 22.1% $4.90 $104 downside 1.3% 50.4% 21.4% $4.79 Source: UBS

PG is trading at US$124.69 (as of April 17th, 2020).

Risk to the current share price is balanced at 1 to 1

PG is trading at US$124.69 (as of April 17th, 2020).

Upside (US$146): Our upside case models a +3.3% 3yr organic sales CAGR. Additionally, we expect 50.9% 2020E gross margins, 22.7% 2020E EBIT margins, and 2020 EPS of $4.94.

Base (US$126): Our base case models a +2.3% 3yr organic sales CAGR. Additionally, we expect 50.6% 2020E gross margins, 22.1% 2020E EBIT margins, and 2020 EPS of $4.90.

Downside (US$104): Our downside case models a +1.3% 3yr organic sales CAGR. Additionally, we expect 50.4% 2020E gross margins, 21.4% 2020E EBIT margins, and 2020 EPS of $4.79.

+17%

+1%

-17%

7080

90

100

110

120

130

140

150

160

2018 2019 2020

Upside:

Base:

Downside:

146.00 =

126.00 =

104.00 =

29.6x

25.7x

21.7x

4.94 x

4.90 x

4.79 x

US$124.69PG.N Price

17 Apr +12 mo.

P/E (UBS) Implied

EPS (UBS) 06/20E

Upside to Downside

1 to 1

Source: UBS Research

Procter & Gamble 17 April 2020

7

Procter & Gamble UBS Research

COMPANY DESCRIPTION return

The Procter & Gamble Company (PG) manufactures and markets household and personal care products on a global basis. Categories in which PG operates include laundry, cleaning, consumer tissue, beauty, baby, and healthcare. The company has sizable market share in many of these areas. PG maintains 25 'billion dollar brands.' Pampers, Tide, Olay, Pantene, Charmin, Crest, and Gillette are among PG's top brands.

Industry outlook

We find that the Household & Personal Care (HPC) industry is structurally advantaged vs US Food with outsized sales mix exposure to emerging markets and ecommerce, but only half the private label mix and debt leverage. However, this favorable view is reflected in HPC valuations, with the HPC group trading at an above normal historical premium vs Packaged Food. Source for charts: Company financials, UBS analysis, Euromonitor

Sales mix by segment (%)

Sales mix by geography (%)

Beauty 18%

Grooming 10%

Health Care 12% Fabric and

Home Care 32%

Baby, Feminine, and Family Care 28%

U.S. 42%

North America ex.

US 3%

Europe 23%

APAC 9%

Greater China 8%

Latin America

8%

IMEA 7%

Procter & Gamble 17 April 2020

8

Procter & Gamble (PG.N)

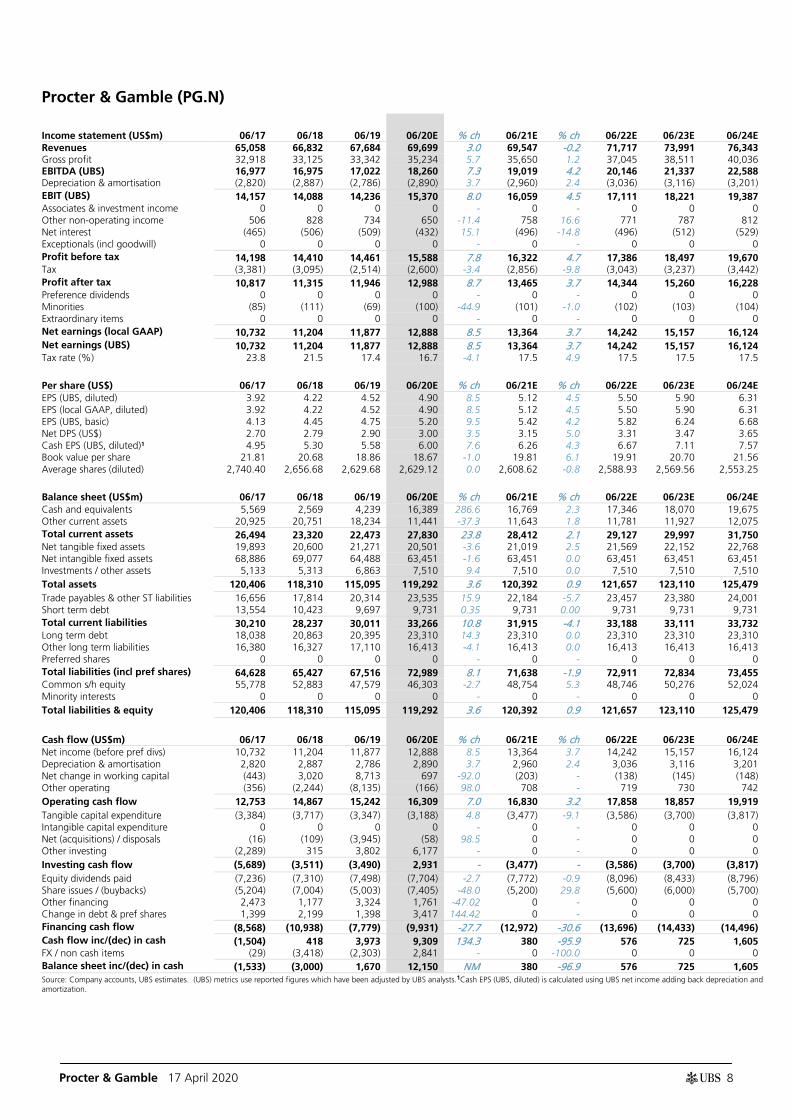

Income statement (US$m) 06/17 06/18 06/19 06/20E % ch 06/21E % ch 06/22E 06/23E 06/24E Revenues 65,058 66,832 67,684 69,699 3.0 69,547 -0.2 71,717 73,991 76,343 Gross profit 32,918 33,125 33,342 35,234 5.7 35,650 1.2 37,045 38,511 40,036 EBITDA (UBS) 16,977 16,975 17,022 18,260 7.3 19,019 4.2 20,146 21,337 22,588 Depreciation & amortisation (2,820) (2,887) (2,786) (2,890) 3.7 (2,960) 2.4 (3,036) (3,116) (3,201) EBIT (UBS) 14,157 14,088 14,236 15,370 8.0 16,059 4.5 17,111 18,221 19,387 Associates & investment income 0 0 0 0 - 0 - 0 0 0 Other non-operating income 506 828 734 650 -11.4 758 16.6 771 787 812 Net interest (465) (506) (509) (432) 15.1 (496) -14.8 (496) (512) (529) Exceptionals (incl goodwill) 0 0 0 0 - 0 - 0 0 0 Profit before tax 14,198 14,410 14,461 15,588 7.8 16,322 4.7 17,386 18,497 19,670 Tax (3,381) (3,095) (2,514) (2,600) -3.4 (2,856) -9.8 (3,043) (3,237) (3,442) Profit after tax 10,817 11,315 11,946 12,988 8.7 13,465 3.7 14,344 15,260 16,228 Preference dividends 0 0 0 0 - 0 - 0 0 0 Minorities (85) (111) (69) (100) -44.9 (101) -1.0 (102) (103) (104) Extraordinary items 0 0 0 0 - 0 - 0 0 0 Net earnings (local GAAP) 10,732 11,204 11,877 12,888 8.5 13,364 3.7 14,242 15,157 16,124 Net earnings (UBS) 10,732 11,204 11,877 12,888 8.5 13,364 3.7 14,242 15,157 16,124 Tax rate (%) 23.8 21.5 17.4 16.7 -4.1 17.5 4.9 17.5 17.5 17.5

Per share (US$) 06/17 06/18 06/19 06/20E % ch 06/21E % ch 06/22E 06/23E 06/24E EPS (UBS, diluted) 3.92 4.22 4.52 4.90 8.5 5.12 4.5 5.50 5.90 6.31 EPS (local GAAP, diluted) 3.92 4.22 4.52 4.90 8.5 5.12 4.5 5.50 5.90 6.31 EPS (UBS, basic) 4.13 4.45 4.75 5.20 9.5 5.42 4.2 5.82 6.24 6.68 Net DPS (US$) 2.70 2.79 2.90 3.00 3.5 3.15 5.0 3.31 3.47 3.65 Cash EPS (UBS, diluted)1 4.95 5.30 5.58 6.00 7.6 6.26 4.3 6.67 7.11 7.57 Book value per share 21.81 20.68 18.86 18.67 -1.0 19.81 6.1 19.91 20.70 21.56 Average shares (diluted) 2,740.40 2,656.68 2,629.68 2,629.12 0.0 2,608.62 -0.8 2,588.93 2,569.56 2,553.25

Balance sheet (US$m) 06/17 06/18 06/19 06/20E % ch 06/21E % ch 06/22E 06/23E 06/24E Cash and equivalents 5,569 2,569 4,239 16,389 286.6 16,769 2.3 17,346 18,070 19,675 Other current assets 20,925 20,751 18,234 11,441 -37.3 11,643 1.8 11,781 11,927 12,075 Total current assets 26,494 23,320 22,473 27,830 23.8 28,412 2.1 29,127 29,997 31,750 Net tangible fixed assets 19,893 20,600 21,271 20,501 -3.6 21,019 2.5 21,569 22,152 22,768 Net intangible fixed assets 68,886 69,077 64,488 63,451 -1.6 63,451 0.0 63,451 63,451 63,451 Investments / other assets 5,133 5,313 6,863 7,510 9.4 7,510 0.0 7,510 7,510 7,510 Total assets 120,406 118,310 115,095 119,292 3.6 120,392 0.9 121,657 123,110 125,479 Trade payables & other ST liabilities 16,656 17,814 20,314 23,535 15.9 22,184 -5.7 23,457 23,380 24,001 Short term debt 13,554 10,423 9,697 9,731 0.35 9,731 0.00 9,731 9,731 9,731 Total current liabilities 30,210 28,237 30,011 33,266 10.8 31,915 -4.1 33,188 33,111 33,732 Long term debt 18,038 20,863 20,395 23,310 14.3 23,310 0.0 23,310 23,310 23,310 Other long term liabilities 16,380 16,327 17,110 16,413 -4.1 16,413 0.0 16,413 16,413 16,413 Preferred shares 0 0 0 0 - 0 - 0 0 0 Total liabilities (incl pref shares) 64,628 65,427 67,516 72,989 8.1 71,638 -1.9 72,911 72,834 73,455 Common s/h equity 55,778 52,883 47,579 46,303 -2.7 48,754 5.3 48,746 50,276 52,024 Minority interests 0 0 0 0 - 0 - 0 0 0 Total liabilities & equity 120,406 118,310 115,095 119,292 3.6 120,392 0.9 121,657 123,110 125,479

Cash flow (US$m) 06/17 06/18 06/19 06/20E % ch 06/21E % ch 06/22E 06/23E 06/24E Net income (before pref divs) 10,732 11,204 11,877 12,888 8.5 13,364 3.7 14,242 15,157 16,124 Depreciation & amortisation 2,820 2,887 2,786 2,890 3.7 2,960 2.4 3,036 3,116 3,201 Net change in working capital (443) 3,020 8,713 697 -92.0 (203) - (138) (145) (148) Other operating (356) (2,244) (8,135) (166) 98.0 708 - 719 730 742 Operating cash flow 12,753 14,867 15,242 16,309 7.0 16,830 3.2 17,858 18,857 19,919 Tangible capital expenditure (3,384) (3,717) (3,347) (3,188) 4.8 (3,477) -9.1 (3,586) (3,700) (3,817) Intangible capital expenditure 0 0 0 0 - 0 - 0 0 0 Net (acquisitions) / disposals (16) (109) (3,945) (58) 98.5 0 - 0 0 0 Other investing (2,289) 315 3,802 6,177 - 0 - 0 0 0 Investing cash flow (5,689) (3,511) (3,490) 2,931 - (3,477) - (3,586) (3,700) (3,817) Equity dividends paid (7,236) (7,310) (7,498) (7,704) -2.7 (7,772) -0.9 (8,096) (8,433) (8,796) Share issues / (buybacks) (5,204) (7,004) (5,003) (7,405) -48.0 (5,200) 29.8 (5,600) (6,000) (5,700) Other financing 2,473 1,177 3,324 1,761 -47.02 0 - 0 0 0 Change in debt & pref shares 1,399 2,199 1,398 3,417 144.42 0 - 0 0 0 Financing cash flow (8,568) (10,938) (7,779) (9,931) -27.7 (12,972) -30.6 (13,696) (14,433) (14,496) Cash flow inc/(dec) in cash (1,504) 418 3,973 9,309 134.3 380 -95.9 576 725 1,605 FX / non cash items (29) (3,418) (2,303) 2,841 - 0 -100.0 0 0 0 Balance sheet inc/(dec) in cash (1,533) (3,000) 1,670 12,150 NM 380 -96.9 576 725 1,605 Source: Company accounts, UBS estimates. (UBS) metrics use reported figures which have been adjusted by UBS analysts.1Cash EPS (UBS, diluted) is calculated using UBS net income adding back depreciation and amortization.

Procter & Gamble 17 April 2020

9

Procter & Gamble (PG.N)

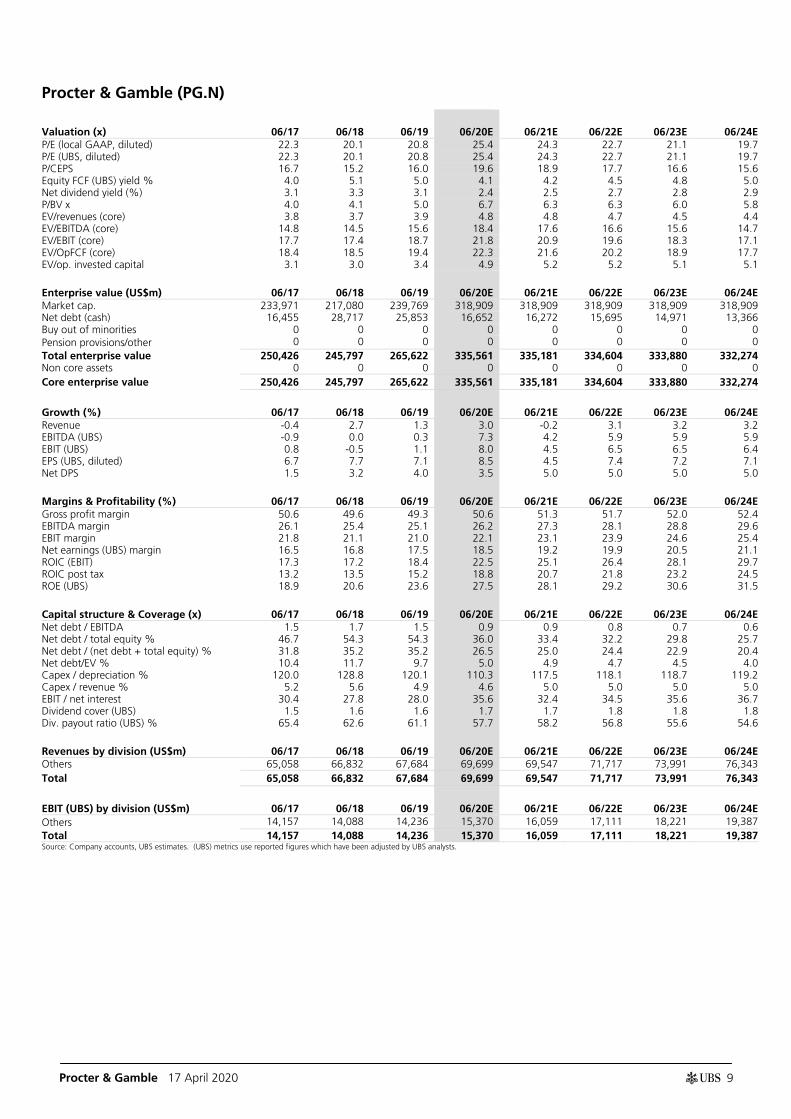

Valuation (x) 06/17 06/18 06/19 06/20E 06/21E 06/22E 06/23E 06/24E P/E (local GAAP, diluted) 22.3 20.1 20.8 25.4 24.3 22.7 21.1 19.7 P/E (UBS, diluted) 22.3 20.1 20.8 25.4 24.3 22.7 21.1 19.7 P/CEPS 16.7 15.2 16.0 19.6 18.9 17.7 16.6 15.6 Equity FCF (UBS) yield % 4.0 5.1 5.0 4.1 4.2 4.5 4.8 5.0 Net dividend yield (%) 3.1 3.3 3.1 2.4 2.5 2.7 2.8 2.9 P/BV x 4.0 4.1 5.0 6.7 6.3 6.3 6.0 5.8 EV/revenues (core) 3.8 3.7 3.9 4.8 4.8 4.7 4.5 4.4 EV/EBITDA (core) 14.8 14.5 15.6 18.4 17.6 16.6 15.6 14.7 EV/EBIT (core) 17.7 17.4 18.7 21.8 20.9 19.6 18.3 17.1 EV/OpFCF (core) 18.4 18.5 19.4 22.3 21.6 20.2 18.9 17.7 EV/op. invested capital 3.1 3.0 3.4 4.9 5.2 5.2 5.1 5.1

Enterprise value (US$m) 06/17 06/18 06/19 06/20E 06/21E 06/22E 06/23E 06/24E Market cap. 233,971 217,080 239,769 318,909 318,909 318,909 318,909 318,909 Net debt (cash) 16,455 28,717 25,853 16,652 16,272 15,695 14,971 13,366 Buy out of minorities 0 0 0 0 0 0 0 0 Pension provisions/other 0 0 0 0 0 0 0 0 Total enterprise value 250,426 245,797 265,622 335,561 335,181 334,604 333,880 332,274 Non core assets 0 0 0 0 0 0 0 0 Core enterprise value 250,426 245,797 265,622 335,561 335,181 334,604 333,880 332,274

Growth (%) 06/17 06/18 06/19 06/20E 06/21E 06/22E 06/23E 06/24E Revenue -0.4 2.7 1.3 3.0 -0.2 3.1 3.2 3.2 EBITDA (UBS) -0.9 0.0 0.3 7.3 4.2 5.9 5.9 5.9 EBIT (UBS) 0.8 -0.5 1.1 8.0 4.5 6.5 6.5 6.4 EPS (UBS, diluted) 6.7 7.7 7.1 8.5 4.5 7.4 7.2 7.1 Net DPS 1.5 3.2 4.0 3.5 5.0 5.0 5.0 5.0

Margins & Profitability (%) 06/17 06/18 06/19 06/20E 06/21E 06/22E 06/23E 06/24E Gross profit margin 50.6 49.6 49.3 50.6 51.3 51.7 52.0 52.4 EBITDA margin 26.1 25.4 25.1 26.2 27.3 28.1 28.8 29.6 EBIT margin 21.8 21.1 21.0 22.1 23.1 23.9 24.6 25.4 Net earnings (UBS) margin 16.5 16.8 17.5 18.5 19.2 19.9 20.5 21.1 ROIC (EBIT) 17.3 17.2 18.4 22.5 25.1 26.4 28.1 29.7 ROIC post tax 13.2 13.5 15.2 18.8 20.7 21.8 23.2 24.5 ROE (UBS) 18.9 20.6 23.6 27.5 28.1 29.2 30.6 31.5

Capital structure & Coverage (x) 06/17 06/18 06/19 06/20E 06/21E 06/22E 06/23E 06/24E Net debt / EBITDA 1.5 1.7 1.5 0.9 0.9 0.8 0.7 0.6 Net debt / total equity % 46.7 54.3 54.3 36.0 33.4 32.2 29.8 25.7 Net debt / (net debt + total equity) % 31.8 35.2 35.2 26.5 25.0 24.4 22.9 20.4 Net debt/EV % 10.4 11.7 9.7 5.0 4.9 4.7 4.5 4.0 Capex / depreciation % 120.0 128.8 120.1 110.3 117.5 118.1 118.7 119.2 Capex / revenue % 5.2 5.6 4.9 4.6 5.0 5.0 5.0 5.0 EBIT / net interest 30.4 27.8 28.0 35.6 32.4 34.5 35.6 36.7 Dividend cover (UBS) 1.5 1.6 1.6 1.7 1.7 1.8 1.8 1.8 Div. payout ratio (UBS) % 65.4 62.6 61.1 57.7 58.2 56.8 55.6 54.6

Revenues by division (US$m) 06/17 06/18 06/19 06/20E 06/21E 06/22E 06/23E 06/24E Others 65,058 66,832 67,684 69,699 69,547 71,717 73,991 76,343 Total 65,058 66,832 67,684 69,699 69,547 71,717 73,991 76,343

EBIT (UBS) by division (US$m) 06/17 06/18 06/19 06/20E 06/21E 06/22E 06/23E 06/24E Others 14,157 14,088 14,236 15,370 16,059 17,111 18,221 19,387 Total 14,157 14,088 14,236 15,370 16,059 17,111 18,221 19,387 Source: Company accounts, UBS estimates. (UBS) metrics use reported figures which have been adjusted by UBS analysts.

Procter & Gamble 17 April 2020

10

Procter & Gamble 17 April 2020

11

Forecast returns

Forecast price appreciation +1.1%

Forecast dividend yield 2.5%

Forecast stock return +3.6%

Market return assumption 5.2%

Forecast excess return -1.6%

Valuation Method and Risk Statement

Risks to PG include any material changes in: (a) General consumer preferences and/or government regulation pertaining to the consumption of HPC products (including taxation, restrictions on sales, the introduction or subsidization of substitute products, etc.); (b) Government regulation with respect to commerce and/or taxation in general; (c) Macroeconomic trends, interest rate, and/or credit environments within any of our companies' key markets; (d) Competitive intensity between HPC companies within any of our companies' key markets; (e) Customer or supplier relationships; (f) Commodity cost and/or foreign exchange fluctuations; (g) Weather, as related to certain HPC categories (e.g., women's wet shave etc.); (h) Our companies' own ability to execute, whether with respect to R&D, sales and marketing, and/or ongoing productivity efforts; (i) Our companies' stance towards M&A (whether related to acquisitions, JVs, divestments, or otherwise), or the prioritization of cash in general (whether related to organic business investment, dividends, share repurchases, etc.). Our PT for PG is based on P/E and EV/EBITDA multiples.

Procter & Gamble 17 April 2020

12

Required Disclosures

This report has been prepared by UBS Securities LLC, an affiliate of UBS AG. UBS AG, its subsidiaries, branches and affiliates are referred to herein as UBS.

For information on the ways in which UBS manages conflicts and maintains independence of its research product; historical performance information; and certain additional disclosures concerning UBS research recommendations, please visit www.ubs.com/disclosures. The figures contained in performance charts refer to the past; past performance is not a reliable indicator of future results. Additional information will be made available upon request. UBS Securities Co. Limited is licensed to conduct securities investment consultancy businesses by the China Securities Regulatory Commission. UBS acts or may act as principal in the debt securities (or in related derivatives) that may be the subject of this report. This recommendation was finalized on: 17 April 2020 09:53 PM GMT. UBS has designated certain Research department members as Derivatives Research Analysts where those department members publish research principally on the analysis of the price or market for a derivative, and provide information reasonably sufficient upon which to base a decision to enter into a derivatives transaction. Where Derivatives Research Analysts co-author research reports with Equity Research Analysts or Economists, the Derivatives Research Analyst is responsible for the derivatives investment views, forecasts, and/or recommendations.

Analyst Certification:Each research analyst primarily responsible for the content of this research report, in whole or in part, certifies that with respect to each security or issuer that the analyst covered in this report: (1) all of the views expressed accurately reflect his or her personal views about those securities or issuers and were prepared in an independent manner, including with respect to UBS, and (2) no part of his or her compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed by that research analyst in the research report.

UBS Investment Research: Global Equity Rating Definitions

12-Month Rating Definition Coverage1 IB Services2

Buy FSR is > 6% above the MRA. 48% 32%

Neutral FSR is between -6% and 6% of the MRA. 40% 28%

Sell FSR is > 6% below the MRA. 13% 20%

Short-Term Rating Definition Coverage3 IB Services4

Buy Stock price expected to rise within three months from the time the rating was assigned because of a specific catalyst or event. <1% <1%

Sell Stock price expected to fall within three months from the time the rating was assigned because of a specific catalyst or event. <1% <1%

Source: UBS. Rating allocations are as of 31 March 2020. 1:Percentage of companies under coverage globally within the 12-month rating category. 2:Percentage of companies within the 12-month rating category for which investment banking (IB) services were provided within the past 12 months. 3:Percentage of companies under coverage globally within the Short-Term rating category. 4:Percentage of companies within the Short-Term rating category for which investment banking (IB) services were provided within the past 12 months.

KEY DEFINITIONS:Forecast Stock Return (FSR) is defined as expected percentage price appreciation plus gross dividend yield over the next 12 months. In some cases, this yield may be based on accrued dividends. Market Return Assumption (MRA) is defined as the one-year local market interest rate plus 5% (a proxy for, and not a forecast of, the equity risk premium). Under Review (UR) Stocks may be flagged as UR by the analyst, indicating that the stock's price target and/or rating are subject to possible change in the near term, usually in response to an event that may affect the investment case or valuation. Short-Term Ratings reflect the expected near-term (up to three months) performance of the stock and do not reflect any change in the fundamental view or investment case. Equity Price Targets have an investment horizon of 12 months.

Procter & Gamble 17 April 2020

13

EXCEPTIONS AND SPECIAL CASES:UK and European Investment Fund ratings and definitions are: Buy: Positive on factors such as structure, management, performance record, discount; Neutral: Neutral on factors such as structure, management, performance record, discount; Sell: Negative on factors such as structure, management, performance record, discount. Core Banding Exceptions (CBE): Exceptions to the standard +/-6% bands may be granted by the Investment Review Committee (IRC). Factors considered by the IRC include the stock's volatility and the credit spread of the respective company's debt. As a result, stocks deemed to be very high or low risk may be subject to higher or lower bands as they relate to the rating. When such exceptions apply, they will be identified in the Company Disclosures table in the relevant research piece.

Research analysts contributing to this report who are employed by any non-US affiliate of UBS Securities LLC are not registered/qualified as research analysts with FINRA. Such analysts may not be associated persons of UBS Securities LLC and therefore are not subject to the FINRA restrictions on communications with a subject company, public appearances, and trading securities held by a research analyst account. The name of each affiliate and analyst employed by that affiliate contributing to this report, if any, follows.

UBS Securities LLC: Steven Strycula; Carey Sloane; Andrew Olsen.

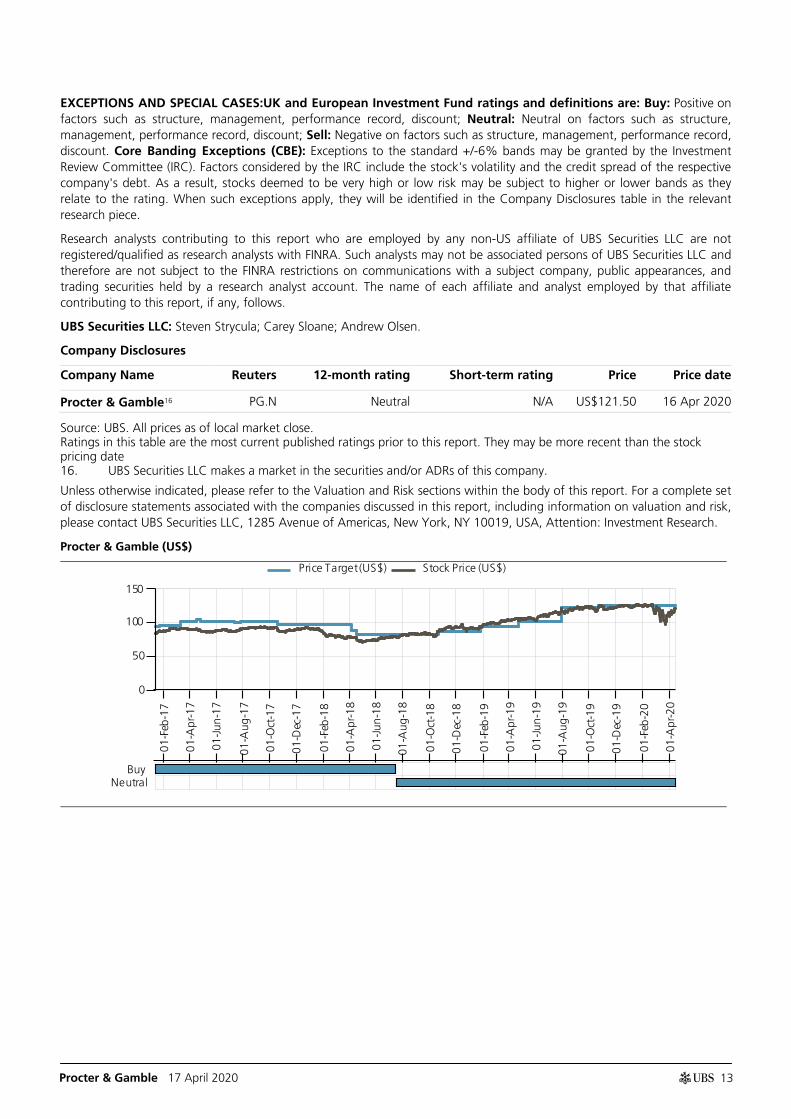

Company Disclosures

Company Name Reuters 12-month rating Short-term rating Price Price date

Procter & Gamble16 PG.N Neutral N/A US$121.50 16 Apr 2020

Source: UBS. All prices as of local market close. Ratings in this table are the most current published ratings prior to this report. They may be more recent than the stock pricing date 16. UBS Securities LLC makes a market in the securities and/or ADRs of this company.

Unless otherwise indicated, please refer to the Valuation and Risk sections within the body of this report. For a complete set of disclosure statements associated with the companies discussed in this report, including information on valuation and risk, please contact UBS Securities LLC, 1285 Avenue of Americas, New York, NY 10019, USA, Attention: Investment Research.

Procter & Gamble (US$)

01-F

eb-1

7

01-A

pr-1

7

01-Ju

n-17

01-A

ug-1

7

01-O

ct-1

7

01-D

ec-1

7

01-F

eb-1

8

01-A

pr-1

8

01-Ju

n-18

01-A

ug-1

8

01-O

ct-1

8

01-D

ec-1

8

01-F

eb-1

9

01-A

pr-1

9

01-Ju

n-19

01-A

ug-1

9

01-O

ct-1

9

01- D

e c-1

9

01-F

eb-2

0

01-A

pr-2

0

0

50

100

150

Price Target (US$) Stock Price (US$)

BuyNeutral

Procter & Gamble 17 April 2020

14

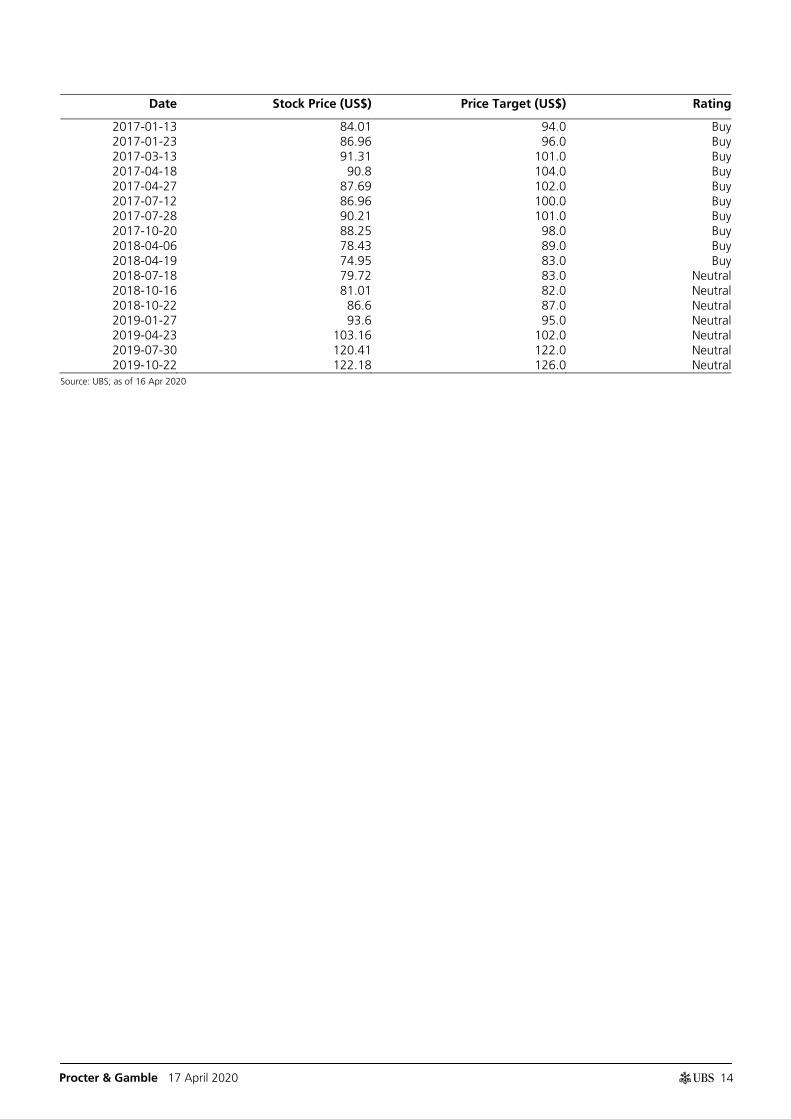

Date Stock Price (US$) Price Target (US$) Rating

2017-01-13 84.01 94.0 Buy 2017-01-23 86.96 96.0 Buy 2017-03-13 91.31 101.0 Buy 2017-04-18 90.8 104.0 Buy 2017-04-27 87.69 102.0 Buy 2017-07-12 86.96 100.0 Buy 2017-07-28 90.21 101.0 Buy 2017-10-20 88.25 98.0 Buy 2018-04-06 78.43 89.0 Buy 2018-04-19 74.95 83.0 Buy 2018-07-18 79.72 83.0 Neutral 2018-10-16 81.01 82.0 Neutral 2018-10-22 86.6 87.0 Neutral 2019-01-27 93.6 95.0 Neutral 2019-04-23 103.16 102.0 Neutral 2019-07-30 120.41 122.0 Neutral 2019-10-22 122.18 126.0 Neutral

Source: UBS; as of 16 Apr 2020

Procter & Gamble 17 April 2020

15

The Disclaimer relevant to Global Wealth Management clients follows the Global Disclaimer.

Global Disclaimer This document has been prepared by UBS Securities LLC, an affiliate of UBS AG. UBS AG, its subsidiaries, branches and affiliates are referred to herein as UBS.

This Document is provided solely to recipients who are expressly authorized by UBS to receive it. If you are not so authorized you must immediately destroy the Document.

Global Research is provided to our clients through UBS Neo, and in certain instances, UBS.com and any other system or distribution method specifically identified in one or more communications distributed through UBS Neo or UBS.com (each a system) as an approved means for distributing Global Research. It may also be made available through third party vendors and distributed by UBS and/or third parties via e-mail or alternative electronic means. The level and types of services provided by Global Research to a client may vary depending upon various factors such as a client's individual preferences as to the frequency and manner of receiving communications, a client's risk profile and investment focus and perspective (e.g., market wide, sector specific, long-term, short-term, etc.), the size and scope of the overall client relationship with UBS and legal and regulatory constraints.

All Global Research is available on UBS Neo. Please contact your UBS sales representative if you wish to discuss your access to UBS Neo.

When you receive Global Research through a System, your access and/or use of such Global Research is subject to this Global Research Disclaimer and to the UBS Neo Platform Use Agreement (the "Neo Terms") together with any other relevant terms of use governing the applicable System.

When you receive Global Research via a third party vendor, e-mail or other electronic means, you agree that use shall be subject to this Global Research Disclaimer, the Neo Terms and where applicable the UBS Investment Bank terms of business (https://www.ubs.com/global/en/investment-bank/regulatory.html) and to UBS's Terms of Use/Disclaimer (http://www.ubs.com/global/en/legalinfo2/disclaimer.html). In addition, you consent to UBS processing your personal data and using cookies in accordance with our Privacy Statement (http://www.ubs.com/global/en/legalinfo2/privacy.html) and cookie notice (http://www.ubs.com/global/en/homepage/cookies/cookie-management.html).

If you receive Global Research, whether through a System or by any other means, you agree that you shall not copy, revise, amend, create a derivative work, provide to any third party, or in any way commercially exploit any UBS research provided via Global Research or otherwise, and that you shall not extract data from any research or estimates provided to you via Global Research or otherwise, without the prior written consent of UBS.

This document is for distribution only as may be permitted by law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject UBS to any registration or licensing requirement within such jurisdiction.

This document is a general communication and is educational in nature; it is not an advertisement nor is it a solicitation or an offer to buy or sell any financial instruments or to participate in any particular trading strategy. Nothing in this document constitutes a representation that any investment strategy or recommendation is suitable or appropriate to an investor’s individual circumstances or otherwise constitutes a personal recommendation. By providing this document, none of UBS or its representatives has any responsibility or authority to provide or have provided investment advice in a fiduciary capacity or otherwise. Investments involve risks, and investors should exercise prudence and their own judgment in making their investment decisions. None of UBS or its representatives is suggesting that the recipient or any other person take a specific course of action or any action at all. By receiving this document, the recipient acknowledges and agrees with the intended purpose described above and further disclaims any expectation or belief that the information constitutes investment advice to the recipient or otherwise purports to meet the investment objectives of the recipient. The financial instruments described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors.

Options, structured derivative products and futures (including OTC derivatives) are not suitable for all investors. Trading in these instruments is considered risky and may be appropriate only for sophisticated investors. Prior to buying or selling an option, and for the complete risks relating to options, you must receive a copy of "The Characteristics and Risks of Standardized Options." You may read the document at http://www.theocc.com/publications/risks/riskchap1.jsp or ask your salesperson for a copy. Various theoretical explanations of the risks associated with these instruments have been published. Supporting documentation for any claims, comparisons, recommendations, statistics or other technical data will be supplied upon request. Past performance is not necessarily indicative of future results. Transaction costs may be significant in option strategies calling for multiple purchases and sales of options, such as spreads and straddles. Because of the importance of tax considerations to many options transactions, the investor considering options should consult with his/her tax advisor as to how taxes affect the outcome of contemplated options transactions.

Mortgage and asset-backed securities may involve a high degree of risk and may be highly volatile in response to fluctuations in interest rates or other market conditions. Foreign currency rates of exchange may adversely affect the value, price or income of any security or related instrument referred to in the document. For investment advice, trade execution or other enquiries, clients should contact their local sales representative.

The value of any investment or income may go down as well as up, and investors may not get back the full (or any) amount invested. Past performance is not necessarily a guide to future performance. Neither UBS nor any of its directors, employees or agents accepts any liability for any loss (including investment loss) or damage arising out of the use of all or any of the Information.

Prior to making any investment or financial decisions, any recipient of this document or the information should take steps to understand the risk and return of the investment and seek individualized advice from his or her personal financial, legal, tax and other professional advisors that takes into account all the particular facts and circumstances of his or her investment objectives.

Any prices stated in this document are for information purposes only and do not represent valuations for individual securities or other financial instruments. There is no representation that any transaction can or could have been effected at those prices, and any prices do not necessarily reflect UBS's internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by UBS or any other source may yield substantially different results.

No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in any materials to which this document relates (the "Information"), except with respect to Information concerning UBS. The Information is not intended to be a complete statement or summary of the securities, markets or developments referred to in the document. UBS does not undertake to update or keep current the Information. Any opinions expressed in this document may change without notice and may differ or be contrary to opinions expressed by other business areas or groups, personnel or other representative of UBS. Any statements contained in this report attributed to a third party represent UBS's interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party. In no circumstances may this document or any of the Information (including any forecast, value, index or other calculated amount ("Values")) be used for any of the following purposes:

(i) valuation or accounting purposes;

(ii) to determine the amounts due or payable, the price or the value of any financial instrument or financial contract; or

(iii) to measure the performance of any financial instrument including, without limitation, for the purpose of tracking the return or performance of any Value or of defining the asset allocation of portfolio or of computing performance fees.

By receiving this document and the Information you will be deemed to represent and warrant to UBS that you will not use this document or any of the Information for any of the above purposes or otherwise rely upon this document or any of the Information.

UBS has policies and procedures, which include, without limitation, independence policies and permanent information barriers, that are intended, and upon which UBS relies, to manage potential conflicts of interest and control the flow of information within divisions of UBS and among its subsidiaries, branches and affiliates. For further information on the ways in which UBS manages conflicts and maintains independence of its research products, historical performance information and certain additional disclosures concerning UBS research recommendations, please visit www.ubs.com/disclosures.

Procter & Gamble 17 April 2020

16

Research will initiate, update and cease coverage solely at the discretion of UBS Research Management, which will also have sole discretion on the timing and frequency of any published research product. The analysis contained in this document is based on numerous assumptions. All material information in relation to published research reports, such as valuation methodology, risk statements, underlying assumptions (including sensitivity analysis of those assumptions), ratings history etc. as required by the Market Abuse Regulation, can be found on UBS Neo. Different assumptions could result in materially different results.

The analyst(s) responsible for the preparation of this document may interact with trading desk personnel, sales personnel and other parties for the purpose of gathering, applying and interpreting market information. UBS relies on information barriers to control the flow of information contained in one or more areas within UBS into other areas, units, groups or affiliates of UBS. The compensation of the analyst who prepared this document is determined exclusively by research management and senior management (not including investment banking). Analyst compensation is not based on investment banking revenues; however, compensation may relate to the revenues of UBS and/or its divisions as a whole, of which investment banking, sales and trading are a part, and UBS's subsidiaries, branches and affiliates as a whole.

For financial instruments admitted to trading on an EU regulated market: UBS AG, its affiliates or subsidiaries (excluding UBS Securities LLC) acts as a market maker or liquidity provider (in accordance with the interpretation of these terms under English law or, if not carried out by UBS in the UK the law of the relevant jurisdiction in which UBS determines it carries out the activity) in the financial instruments of the issuer save that where the activity of liquidity provider is carried out in accordance with the definition given to it by the laws and regulations of any other EU jurisdictions, such information is separately disclosed in this document. For financial instruments admitted to trading on a non-EU regulated market: UBS may act as a market maker save that where this activity is carried out in the US in accordance with the definition given to it by the relevant laws and regulations, such activity will be specifically disclosed in this document. UBS may have issued a warrant the value of which is based on one or more of the financial instruments referred to in the document. UBS and its affiliates and employees may have long or short positions, trade as principal and buy and sell in instruments or derivatives identified herein; such transactions or positions may be inconsistent with the opinions expressed in this document.

Within the past 12 months UBS AG, its affiliates or subsidiaries may have received or provided investment services and activities or ancillary services as per MiFID II which may have given rise to a payment or promise of a payment in relation to these services from or to this company.

Where Global Research refers to "UBS Evidence Lab Inside" or has made use of data provided by UBS Evidence Lab you understand that UBS Evidence Lab is a separate department to Global Research and that UBS Evidence Lab does not provide research, investment recommendations or advice.

United Kingdom: This material is distributed by UBS AG, London Branch to persons who are eligible counterparties or professional clients. UBS AG, London Branch is authorised by the Prudential Regulation Authority and subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. Europe: Except as otherwise specified herein, these materials are distributed by UBS Europe SE, a subsidiary of UBS AG, to persons who are eligible counterparties or professional clients (as detailed in the Bundesanstalt fur Finanzdienstleistungsaufsicht (BaFin)Rules and according to MIFID) and are only available to such persons. The information does not apply to, and should not be relied upon by, retail clients. UBS Europe SE is authorised by the [European Central Bank (ECB)] and regulated by the BaFin and the ECB. France: Prepared by UBS Europe SE and distributed by UBS Europe SE and UBS Securities France S.A. UBS Securities France S.A. is regulated by the ACPR (Autorité de Contrôle Prudentiel et de Résolution) and the Autorité des Marchés Financiers (AMF). Where an analyst of UBS Securities France S.A. has contributed to this document, the document is also deemed to have been prepared by UBS Securities France S.A. Germany, Luxembourg, the Netherlands, Belgium and Ireland: Prepared by UBS AG, London Branch and distributed by UBS AG, London Branch and UBS Europe SE. Spain: Prepared by UBS Europe SE and distributed by UBS Europe SE and UBS Securities España SV, SA. UBS Securities España SV, SA is regulated by the Comisión Nacional del Mercado de Valores (CNMV). Turkey: Distributed by UBS AG, London Branch. No information in this document is provided for the purpose of offering, marketing and sale by any means of any capital market instruments and services in the Republic of Turkey. Therefore, this document may not be considered as an offer made or to be made to residents of the Republic of Turkey. UBS AG, London Branch is not licensed by the Turkish Capital Market Board under the provisions of the Capital Market Law (Law No. 6362). Accordingly, neither this document nor any other offering material related to the instruments/services may be utilized in connection with providing any capital market services to persons within the Republic of Turkey without the prior approval of the Capital Market Board. However, according to article 15 (d) (ii) of the Decree No. 32, there is no restriction on the purchase or sale of the securities abroad by residents of the Republic of Turkey. Poland: Distributed by UBS Europe SE (spolka z ograniczona odpowiedzialnoscia) Oddzial w Polsce regulated by the Polish Financial Supervision Authority. Where an analyst of UBS Europe SE (spolka z ograniczona odpowiedzialnoscia) Oddzial w Polsce has contributed to this document, the document is also deemed to have been prepared by UBS Europe SE (spolka z ograniczona odpowiedzialnoscia) Oddzial w Polsce. Russia: Prepared and distributed by UBS Bank (OOO). Switzerland: Distributed by UBS AG to persons who are institutional investors only. UBS AG is regulated by the Swiss Financial Market Supervisory Authority (FINMA). Italy: Prepared by UBS Europe SE and distributed by UBS Europe SE and UBS Europe SE, Italy Branch. Where an analyst of UBS Europe SE, Italy Branch has contributed to this document, the document is also deemed to have been prepared by UBS Europe SE, Italy Branch.South Africa: Distributed by UBS South Africa (Pty) Limited (Registration No. 1995/011140/07), an authorised user of the JSE and an authorised Financial Services Provider (FSP 7328). Israel: This material is distributed by UBS AG, London Branch. UBS Securities Israel Ltd is a licensed Investment Marketer that is supervised by the Israel Securities Authority (ISA). UBS AG, London Branch and its affiliates incorporated outside Israel are not licensed under the Israeli Advisory Law. UBS AG, London Branch is not covered by insurance as required from a licensee under the Israeli Advisory Law. UBS may engage among others in issuance of Financial Assets or in distribution of Financial Assets of other issuers for fees or other benefits. UBS AG, London Branch and its affiliates may prefer various Financial Assets to which they have or may have Affiliation (as such term is defined under the Israeli Advisory Law). Nothing in this Material should be considered as investment advice under the Israeli Advisory Law. This Material is being issued only to and/or is directed only at persons who are Eligible Clients within the meaning of the Israeli Advisory Law, and this material must not be relied on or acted upon by any other persons. Saudi Arabia: This document has been issued by UBS AG (and/or any of its subsidiaries, branches or affiliates), a public company limited by shares, incorporated in Switzerland with its registered offices at Aeschenvorstadt 1, CH-4051 Basel and Bahnhofstrasse 45, CH-8001 Zurich. This publication has been approved by UBS Saudi Arabia (a subsidiary of UBS AG), a Saudi closed joint stock company incorporated in the Kingdom of Saudi Arabia under commercial register number 1010257812 having its registered office at Tatweer Towers, P.O. Box 75724, Riyadh 11588, Kingdom of Saudi Arabia. UBS Saudi Arabia is authorized and regulated by the Capital Market Authority to conduct securities business under license number 08113-37. UAE / Dubai: The information distributed by UBS AG Dubai Branch is only intended for Professional Clients and/or Market Counterparties, as classified under the DFSA rulebook. No other person should act upon this material/communication. The information is not for further distribution within the United Arab Emirates. UBS AG Dubai Branch is regulated by the DFSA in the DIFC. UBS is not licensed to provide banking services in the UAE by the Central Bank of the UAE, nor is it licensed by the UAE Securities and Commodities Authority. United States: Distributed to US persons by either UBS Securities LLC or by UBS Financial Services Inc., subsidiaries of UBS AG; or by a group, subsidiary or affiliate of UBS AG that is not registered as a US broker-dealer (a ‘non-US affiliate’) to major US institutional investors only. UBS Securities LLC or UBS Financial Services Inc. accepts responsibility for the content of a document prepared by another non-US affiliate when distributed to US persons by UBS Securities LLC or UBS Financial Services Inc. All transactions by a US person in the securities mentioned in this document must be effected through UBS Securities LLC or UBS Financial Services Inc., and not through a non-US affiliate. UBS Securities LLC is not acting as a municipal advisor to any municipal entity or obligated person within the meaning of Section 15B of the Securities Exchange Act (the "Municipal Advisor Rule"), and the opinions or views contained herein are not intended to be, and do not constitute, advice within the meaning of the Municipal Advisor Rule. Canada: Distributed by UBS Securities Canada Inc., a registered investment dealer in Canada and a Member-Canadian Investor Protection Fund, or by another affiliate of UBS AG that is registered to conduct business in Canada or is otherwise exempt from registration. Mexico: This report has been distributed and prepared by UBS Casa de Bolsa, S.A. de C.V., UBS Grupo Financiero, an entity that is part of UBS Grupo Financiero, S.A. de C.V. and is a subsidiary of UBS AG. This document is intended for distribution to institutional or sophisticated investors only. Research reports only reflect the views of the analysts responsible for the reports. Analysts do not receive any compensation from persons or entities different from UBS Casa de Bolsa, S.A. de C.V., UBS Grupo Financiero, or different from entities belonging to the same financial group or business group of such. For Spanish translations of applicable disclosures, please go to www.ubs.com/disclosures. Brazil: Except as otherwise specified herein, this material is prepared by UBS Brasil CCTVM S.A. to persons who are eligible investors residing in Brazil, which are considered to be Investidores Profissionais, as designated by the applicable regulation, mainly the CVM Instruction No. 539 from the 13th of November 2013 (determines the duty to verify the suitability of products, services and transactions with regards to the client´s profile). Hong Kong: Distributed by UBS Securities Asia Limited and/or UBS AG, Hong Kong Branch, which is incorporated in Switzerland with limited liability. Please contact local licensed/registered representatives of UBS Securities Asia Limited and/or UBS AG, Hong Kong Branch in respect of any matters arising from, or in connection with, the analysis or document. Singapore: Distributed by UBS Securities Pte. Ltd. [MCI (P) 009/09/2018 and Co. Reg. No.: 198500648C] or UBS AG, Singapore Branch. Please contact UBS Securities Pte. Ltd., an exempt financial adviser under the Singapore Financial Advisers Act (Cap. 110); or UBS AG, Singapore Branch, an exempt financial adviser under the Singapore Financial Advisers Act (Cap. 110) and a wholesale bank licensed under the Singapore Banking Act (Cap. 19) regulated by the Monetary Authority of Singapore, in respect of any matters arising from, or in connection with, the analysis or document. The recipients of this document represent and warrant that they are accredited and institutional investors as defined in the Securities and Futures Act (Cap. 289). Japan: Distributed by UBS Securities Japan Co., Ltd. to professional investors (except as otherwise permitted). Where this document has been prepared by UBS Securities Japan Co., Ltd., UBS Securities Japan Co., Ltd. is the author, publisher and distributor of the document. Distributed by UBS AG, Tokyo Branch to Professional Investors (except as otherwise permitted) in relation to foreign exchange and other banking businesses when relevant. Australia: Clients of UBS AG: Distributed by UBS AG (ABN 47 088 129 613 and holder of Australian Financial Services License No. 231087). Clients of UBS Securities Australia Ltd: Distributed by UBS Securities Australia Ltd (ABN 62 008 586 481 and holder of Australian Financial Services License No. 231098). This Document contains general information and/or general advice only and does not constitute personal financial product advice. As such, the Information in this document has been prepared without taking into account any investor’s objectives, financial situation or needs, and investors should, before acting

Procter & Gamble 17 April 2020

17

on the Information, consider the appropriateness of the Information, having regard to their objectives, financial situation and needs. If the Information contained in this document relates to the acquisition, or potential acquisition of a particular financial product by a ‘Retail’ client as defined by section 761G of the Corporations Act 2001 where a Product Disclosure Statement would be required, the retail client should obtain and consider the Product Disclosure Statement relating to the product before making any decision about whether to acquire the product. The UBS Securities Australia Limited Financial Services Guide is available at: www.ubs.com/ecs-research-fsg. New Zealand: Distributed by UBS New Zealand Ltd. UBS New Zealand Ltd is not a registered bank in New Zealand. You are being provided with this UBS publication or material because you have indicated to UBS that you are a “wholesale client” within the meaning of section 5C of the Financial Advisers Act 2008 of New Zealand (Permitted Client). This publication or material is not intended for clients who are not Permitted Clients (non-permitted Clients). If you are a non-permitted Client you must not rely on this publication or material. If despite this warning you nevertheless rely on this publication or material, you hereby (i) acknowledge that you may not rely on the content of this publication or material and that any recommendations or opinions in such this publication or material are not made or provided to you, and (ii) to the maximum extent permitted by law (a) indemnify UBS and its associates or related entities (and their respective Directors, officers, agents and Advisors) (each a ‘Relevant Person’) for any loss, damage, liability or claim any of them may incur or suffer as a result of, or in connection with, your unauthorised reliance on this publication or material and (b) waive any rights or remedies you may have against any Relevant Person for (or in respect of) any loss, damage, liability or claim you may incur or suffer as a result of, or in connection with, your unauthorised reliance on this publication or material. Korea: Distributed in Korea by UBS Securities Pte. Ltd., Seoul Branch. This document may have been edited or contributed to from time to time by affiliates of UBS Securities Pte. Ltd., Seoul Branch. This material is intended for professional/institutional clients only and not for distribution to any retail clients. Malaysia: This material is authorized to be distributed in Malaysia by UBS Securities Malaysia Sdn. Bhd (Capital Markets Services License No.: CMSL/A0063/2007). This material is intended for professional/institutional clients only and not for distribution to any retail clients. India: Distributed by UBS Securities India Private Ltd. (Corporate Identity Number U67120MH1996PTC097299) 2/F, 2 North Avenue, Maker Maxity, Bandra Kurla Complex, Bandra (East), Mumbai (India) 400051. Phone: +912261556000. It provides brokerage services bearing SEBI Registration Number: INZ000259830; merchant banking services bearing SEBI Registration Number: INM000010809 and Research Analyst services bearing SEBI Registration Number: INH000001204. UBS AG, its affiliates or subsidiaries may have debt holdings or positions in the subject Indian company/companies. Within the past 12 months, UBS AG, its affiliates or subsidiaries may have received compensation for non-investment banking securities-related services and/or non-securities services from the subject Indian company/companies. The subject company/companies may have been a client/clients of UBS AG, its affiliates or subsidiaries during the 12 months preceding the date of distribution of the research report with respect to investment banking and/or non-investment banking securities-related services and/or non-securities services. With regard to information on associates, please refer to the Annual Report at: http://www.ubs.com/global/en/about_ubs/investor_relations/annualreporting.htmlTaiwan: Distributed by UBS Securities Pte. Ltd., Taipei Branch which is regulated by the Taiwan Securities and Futures Bureau. This documents contains general information and/or general advice only and does NOT constitute any "Recommendation" to clients for the covered companies or any companies mentioned in this document. Indonesia: This report is being distributed by PT UBS Sekuritas Indonesia and is delivered by its licensed employee(s), including marketing/sales person, to its client. PT UBS Sekuritas Indonesia, having its registered office at Wisma GKBI, 22nd floor, JL. Jend. Sudirman, kav.28, Jakarta 10210, Indonesia, is a subsidiary company of UBS AG and licensed under Capital Market Law no. 8 year 1995, a holder of broker-dealer and underwriter licenses issued by the Capital Market and Financial Institution Supervisory Agency (now Otoritas Jasa Keuangan/OJK). PT UBS Sekuritas Indonesia is also a member of Indonesia Stock Exchange and supervised by Otoritas Jasa Keuangan (OJK). Neither this report nor any copy hereof may be distributed in Indonesia or to any Indonesian citizens except in compliance with applicable Indonesian capital market laws and regulations. This report is not an offer of securities in Indonesia and may not be distributed within the territory of the Republic of Indonesia or to Indonesian citizens in circumstance which constitutes an offering within the meaning of Indonesian capital market laws and regulations.

The disclosures contained in research documents produced by UBS AG, London Branch or UBS Europe SE shall be governed by and construed in accordance with English law.

UBS specifically prohibits the redistribution of this document in whole or in part without the written permission of UBS and in any event UBS accepts no liability whatsoever for any redistribution of this document or its contents or the actions of third parties in this respect. Images may depict objects or elements that are protected by third party copyright, trademarks and other intellectual property rights. © UBS 2020. The key symbol and UBS are among the registered and unregistered trademarks of UBS. All rights reserved.

Global Wealth Management Disclaimer You receive this document in your capacity as a client of UBS Global Wealth Management. This publication has been distributed to you by UBS Switzerland AG (regulated by FINMA in Switzerland) or its affiliates ("UBS") with whom you have a banking relationship with. The full name of the distributing affiliate and its competent authority can be found in the country-specific disclaimer at the end of this document.

The date and time of the first dissemination of this publication is the same as the date and time of its publication.

Risk information:

You agree that you shall not copy, revise, amend, create a derivative work, provide to any third party, or in any way commercially exploit any UBS research, and that you shall not extract data from any research or estimates, without the prior written consent of UBS.

This document is for distribution only as may be permitted by law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject UBS to any registration or licensing requirement within such jurisdiction.

This document is a general communication and is educational in nature; it is not an advertisement nor is it a solicitation or an offer to buy or sell any financial instruments or to participate in any particular trading strategy. Nothing in this document constitutes a representation that any investment strategy or recommendation is suitable or appropriate to an investor’s individual circumstances or otherwise constitutes a personal recommendation. By providing this document, none of UBS or its representatives has any responsibility or authority to provide or have provided investment advice in a fiduciary capacity or otherwise. Investments involve risks, and investors should exercise prudence and their own judgment in making their investment decisions. None of UBS or its representatives is suggesting that the recipient or any other person take a specific course of action or any action at all. By receiving this document, the recipient acknowledges and agrees with the intended purpose described above and further disclaims any expectation or belief that the information constitutes investment advice to the recipient or otherwise purports to meet the investment objectives of the recipient. The financial instruments described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors.

Options, derivative products and futures are not suitable for all investors, and trading in these instruments is considered risky. Mortgage and asset-backed securities may involve a high degree of risk and may be highly volatile in response to fluctuations in interest rates or other market conditions. Foreign currency rates of exchange may adversely affect the value, price or income of any security or related instrument referred to in the document. For investment advice, trade execution or other enquiries, clients should contact their local sales representative.

The value of any investment or income may go down as well as up, and investors may not get back the full (or any) amount invested. Past performance is not necessarily a guide to future performance. Neither UBS nor any of its directors, employees or agents accepts any liability for any loss (including investment loss) or damage arising out of the use of all or any of the information (as defined below).

Prior to making any investment or financial decisions, any recipient of this document or the information should take steps to understand the risk and return of the investment and seek individualized advice from his or her personal financial, legal, tax and other professional advisors that takes into account all the particular facts and circumstances of his or her investment objectives.

Any prices stated in this document are for information purposes only and do not represent valuations for individual securities or other financial instruments. There is no representation that any transaction can or could have been effected at those prices, and any prices do not necessarily reflect UBS's internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by UBS or any other source may yield substantially different results.

No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in any materials to which this document relates (the "Information"), except with respect to Information concerning UBS. The Information is not intended to be a complete statement or summary of the securities, markets or developments referred to in the document. UBS does not undertake to update or keep current the Information. Any opinions expressed in this document may change without notice and may differ or be contrary to opinions expressed by other business areas or groups, personnel or other representative of UBS. Any statements contained in this report attributed to a third party represent UBS's interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party. In no circumstances may this document or any of the Information (including any forecast, value, index or other calculated amount ("Values")) be used for any of the following purposes:

Procter & Gamble 17 April 2020

18

(i) valuation or accounting purposes;

(ii) to determine the amounts due or payable, the price or the value of any financial instrument or financial contract; or

(iii) to measure the performance of any financial instrument including, without limitation, for the purpose of tracking the return or performance of any Value or of defining the asset allocation of portfolio or of computing performance fees.

By receiving this document and the Information you will be deemed to represent and warrant to UBS that you will not use this document or any of the Information for any of the above purposes or otherwise rely upon this document or any of the Information.

UBS has policies and procedures, which include, without limitation, independence policies and permanent information barriers, that are intended, and upon which UBS relies, to manage potential conflicts of interest and control the flow of information within divisions of UBS (including between Global Wealth Management and Research) and among its subsidiaries, branches and affiliates. For further information on the ways in which UBS manages conflicts and maintains independence of its research products, historical performance information and certain additional disclosures concerning UBS research recommendations, please visit www.ubs.com/disclosures.

Research will initiate, update and cease coverage solely at the discretion of research management, which will also have sole discretion on the timing and frequency of any published research product. The analysis contained in this document is based on numerous assumptions. Different assumptions could result in materially different results.

The analyst(s) responsible for the preparation of this document may interact with trading desk personnel, sales personnel and other parties for the purpose of gathering, applying and interpreting market information. UBS relies on information barriers to control the flow of information contained in one or more areas within UBS into other areas, units, groups or affiliates of UBS. The compensation of the analyst who prepared this document is determined exclusively by research management and senior management (not including investment banking). Analyst compensation is not based on investment banking revenues; however, compensation may relate to the revenues of UBS and/or its divisions as a whole, of which investment banking, sales and trading are a part, and UBS's subsidiaries, branches and affiliates as a whole.

For financial instruments admitted to trading on an EU regulated market: UBS AG, its affiliates or subsidiaries (excluding UBS Securities LLC) acts as a market maker or liquidity provider (in accordance with the interpretation of these terms in the UK) in the financial instruments of the issuer save that where the activity of liquidity provider is carried out in accordance with the definition given to it by the laws and regulations of any other EU jurisdictions, such information is separately disclosed in this document. For financial instruments admitted to trading on a non-EU regulated market: UBS may act as a market maker save that where this activity is carried out in the US in accordance with the definition given to it by the relevant laws and regulations, such activity will be specifically disclosed in this document. UBS may have issued a warrant the value of which is based on one or more of the financial instruments referred to in the document. UBS and its affiliates and employees may have long or short positions, trade as principal and buy and sell in instruments or derivatives identified herein; such transactions or positions may be inconsistent with the opinions expressed in this document.

Within the past 12 months UBS Switzerland AG, its affiliates or subsidiaries may have received or provided investment services and activities or ancillary services as per MiFID II which may have given rise to a payment or promise of a payment in relation to these services from or to this company.

If you require detailed information on disclosures of interest or conflict of interest as required by Market Abuse Regulation please contact the mailbox [email protected]. Please note that e-mail communication is unsecured.

External Asset Managers / External Financial Consultants: In case this research or publication is provided to an External Asset Manager or an External Financial Consultant, UBS expressly prohibits that it is redistributed by the External Asset Manager or the External Financial Consultant and is made available to their clients and/or third parties.

Distributed to US persons by UBS Financial Services Inc. or UBS Securities LLC, subsidiaries of UBS AG. UBS Switzerland AG, UBS Europe SE, UBS Bank, S.A., UBS Brasil Administradora de Valores Mobiliarios Ltda, UBS Asesores Mexico, S.A. de C.V., UBS Securities Japan Co., Ltd, UBS Wealth Management Israel Ltd and UBS Menkul Degerler AS are affiliates of UBS AG. UBS Financial Services Incorporated of Puerto Rico is a subsidiary of UBS Financial Services Inc. UBS Financial Services Inc. accepts responsibility for the content of a report prepared by a non-US affiliate when it distributes reports to US persons. All transactions by a US person in the securities mentioned in this report should be effected through a US-registered broker dealer affiliated with UBS, and not through a non-US affiliate. The contents of this report have not been and will not be approved by any securities or investment authority in the United States or elsewhere. UBS Financial Services Inc. is not acting as a municipal advisor to any municipal entity or obligated person within the meaning of Section 15B of the Securities Exchange Act (the "Municipal Advisor Rule") and the opinions or views contained herein are not intended to be, and do not constitute, advice within the meaning of the Municipal Advisor Rule.