private equity funding

TRANSCRIPT

Different Forms Of

Private Equity Funding

Contents

• Why do companies need funds?

• When is equity financing preferred?

• Forms of Private Equity Funding

• Recent Trends

• General Process

• Valuations

• Structures and Instruments

• Exit Options

• Advantages and Disadvantages

• Important factors for consideration

• PE at crossroads…

2

Why does a company need funds?

• Plant & Machinery

• Land & BuildingCapital Expenditure

• Fund Based

• Non Fund BasedWorking Capital

• Term Loan RepaymentRetiring Debt

• Vertical – New Product Lines / New Segment

• Geographical – Operations in International MarketsExpansion

• Leverage Buy-out

• Management Buy-outAcquisition Finance

3

When is equity financing preferred?

Equity Financing

Over leveraged

Inconsistent cash flows

Difficult to meet interest commitments

Ideal for start ups

4

Forms of Private Equity Funding

Ideas

Micro

Business

SME’s

Mid - Large

Business

Mature

Business

Incubation

Funds by

Promoters

Family &

Friends,

“Angel” Investors &

Venture Capitalist

Venture Capital,

Private Equity

& Mezzanine

Capital Markets /

Private Equity

& Mezzanine

Buy Out Funds/ Capital

Markets

Stages of Business

Types of Private Equity Funds

5

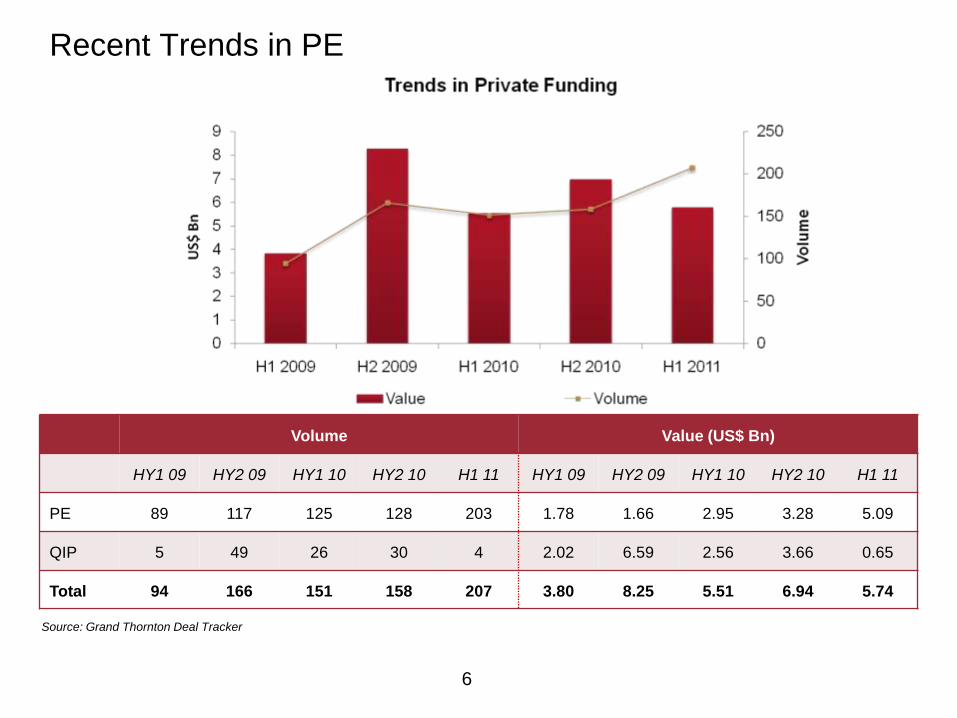

Recent Trends in PE

Volume Value (US$ Bn)

HY1 09 HY2 09 HY1 10 HY2 10 H1 11 HY1 09 HY2 09 HY1 10 HY2 10 H1 11

PE 89 117 125 128 203 1.78 1.66 2.95 3.28 5.09

QIP 5 49 26 30 4 2.02 6.59 2.56 3.66 0.65

Total 94 166 151 158 207 3.80 8.25 5.51 6.94 5.74

Source: Grand Thornton Deal Tracker

6

Source: Grand Thornton Deal Tracker

7

Recent Trends in PE - Sectorial Breakup

For H1 2011

Recent Trends in PE - Performance of various funds

8

• Expansion / growth capital accounts for 46% of total deals of 2011

• Big trends for 2011 was surge in start-up/early stage deals from 18% of total in 2010 to 33% of total in

2011

Source: Economic Times on 6th January, 2011

Angel Investor

• Provides „seed funding‟

• Usually affluent individual providing capital for business start-ups

• Different from venture capitalists

• Limitation on amount of money that can be raised

• Bear high risk

• Require very high return

• Investment holding period of <5 years

9

Transactions (Illustrative)

10

Venture Capital

• Typically occurs after seed funding stage

• Subset of private equity

• Venture capital consists of investing in equity, quasi equity and/or conditional loan in order to

promote unlisted, high risk or high tech firms driven by technically or professionally qualified

entrepreneurs.

• Finance companies that have demonstrated extraordinary business potential

• The risk anticipated is very high

• Follow the concept of “high risk, high return”

• Year 2011 is record year for early-stage Venture Capital investing

– Deal values & volumes at all time high

– Euphoria around e-commerce, across mobile, internet and related verticals

– Evident from recent deals of InMobi, Fashionandyou, Snapdeal

– Exit in MakeMyTrip touted as poster deal for domestic venture industry

– JustDial , One97 Communications and others lining up for exit over coming months

11

Venture Capital

Sector

Early Stage

Key Driver -

Innovation

Investment

& Exit

Success

Majorly in

emerging sectors

Funds start up

& early expansion

Highly skilled

professionals,

scientist &

innovators with

innovative

business idea,

new product &

new technology

Upto $10 mn, exit

through strategic

sale or IPO

High mortality rate

& few great

success

12

Transactions (Illustrative)

13

Private Equity

• Equity investments in relatively mature, primarily unlisted companies requiring growth capital

• An asset class that involves value enhancement and high returns generation by sharing business

expertise of the Investor complementing the Entrepreneur

• Typical value additions from the PE Fund House could include Strategy Formulation Financial

Formulation, Expertise and Global/Domestic Networks (including other investee companies)

• Offer greater opportunity to exercise control over investments as compared with other passive asset

classes like equities, mutual fund, real estate, commodities, fixed income

– Active involvement and influence on the company, including board seat

• Each investment is backed by an investment thesis which plays out over a period of 3 to 5 years

• Private Investment in Public Entities (PIPES)

14

Growth Stage – Private Equity

Sector

All growth sectors

Growth

Stage

Investor funds at

growth stage of

the company

Key Driver -

Innovation

Capacity expansion,

new products, new

geography etc.

Investment

& Exit

From $5 mn to

$500 mn, exit

through IPO

Success

Few failures &

great success

15

Transactions (Illustrative)

16

Buyout Funds

• Globally most important strategy of PE; though not a very prevalent strategy in India

• Generally buyout‟s done at matured stage of business

• Mature companies with leading market position, active management team, strong cash‐flow

• Taking a controlling stake in the company through leveraged buyout (LBO) or through management

team alongside the PE fund (MBO)

• PE funds provide capital for expansion, promoters‟ / corporate divestures, succession issues…

• Development of a business plan over 4 to 6 years in order to add value

• Revenue growth + Margins improvement + deleveraging = added value

17

Transactions (Illustrative)

18

Company Financial Investor Value (US$ Mn) Type

Flextronics Software Systems Kohlberg Kravis Roberts & Co. 900 LBO

GE Capital International Services (GECIS)General Atlantic Partners, Oak

Hills600 LBO

Phoenix Lamps Actis Capital 29 MBO

Nilgiris Dairy Farm Actis Capital 65 MBO

WNS Global Services Warburg Pincus 40 MBO

Infomedia India ICICI Venture 25 LBO

Nirula‟s Navis Capital Partners 20 MBO

Gokaldas Export Blackstone 165 MBO

Paras PharmaceuticalsActis Capital

Sequoia CapitalN.A. MBO

Mezzanine Debt / Structured Product

• Mezzanine financing is provided by mezzanine funds and sometimes hedge funds

• Finance as Debt instrument / structured product like partly or optionally convertible instruments etc.,

immediately subordinated to equity

• Mezzanine financing might include, besides coupon bearing debt, an equity sweetener as well

• Considered as debt instrument with very high yield which at times in substitution of equity

• Returns generated by the fund are

– Interest ‐ fixed rate or fluctuate along an index (e.g. LIBOR) OR a pre agreed IRR

– Upside potential through Equity

• Illustrations:

19

Sector focused funds

• Real estate funds

– Focus on investments in real estate and real estate intensive businesses

• Infrastructure funds

– Roadways

– Port projects

– Railway projects

– Power projects

– Telecom

– Logistics

20

Key Differentiators

Particulars Stage Level of risk Assessment Focus Investment Size

Angel Investors Very Early Very High Mostly Technology < $ 1 Mn

Venture Capital Early High Mostly technology < $ 10 Mn

Private Equity Growth Moderate Diversified > $ 10 Mn

Buyout‟s Mature Moderate Diversified > $ 50 Mn

Mezzanine All stages Moderate Diversified > $ 5 Mn

21

» Identify target

Investors

» Share

Information

» Follow-ups

» Promoter

Meetings

» Plant visits

» Negotiate

valuations and

other terms of

the

transaction

» Due Diligence

» Definitive

Agreements

Stage

Process

PreparationInvestor

IdentificationTerm Sheet

Final negotiations

and Closing

Timing

4-6 weeks4-6 weeks3-5 weeks3-4 weeks Total Time

14 – 21 weeks

Sign NDAs Sign Term Sheet Sign Definitive Agreements

» Understanding

and evaluating

historical

performance

» Recast of

Historical

numbers; if

needed

» Preparation of

IM and

Projections

» Industry

Overview

» Pre & Post

Closure

formalities

General Process

22

Valuations

Peer/transaction Multiples

NAV

Revenue

EBIDTA

PAT

DCF

Willing Buyer – Willing Seller

23

Structures and Instruments

Primary Investment

• Involves fresh infusion of capital in the company against issue of fresh shares to augment future

growth

• Ideal for growth companies

Secondary Investment

• Involves payment to existing shareholders of the company

• Could be either on account of buying out or providing some liquidity to existing shareholders

• Ideal when promoters wants to cash out (fully or partially) or buyouts

24

Structures and Instruments

Private Equity Investment

Primary Investment

Direct EquityConvertible

Preference Shares / Debentures

Warrants / Options

Secondary Investment

Equity Purchase / Earnouts

25

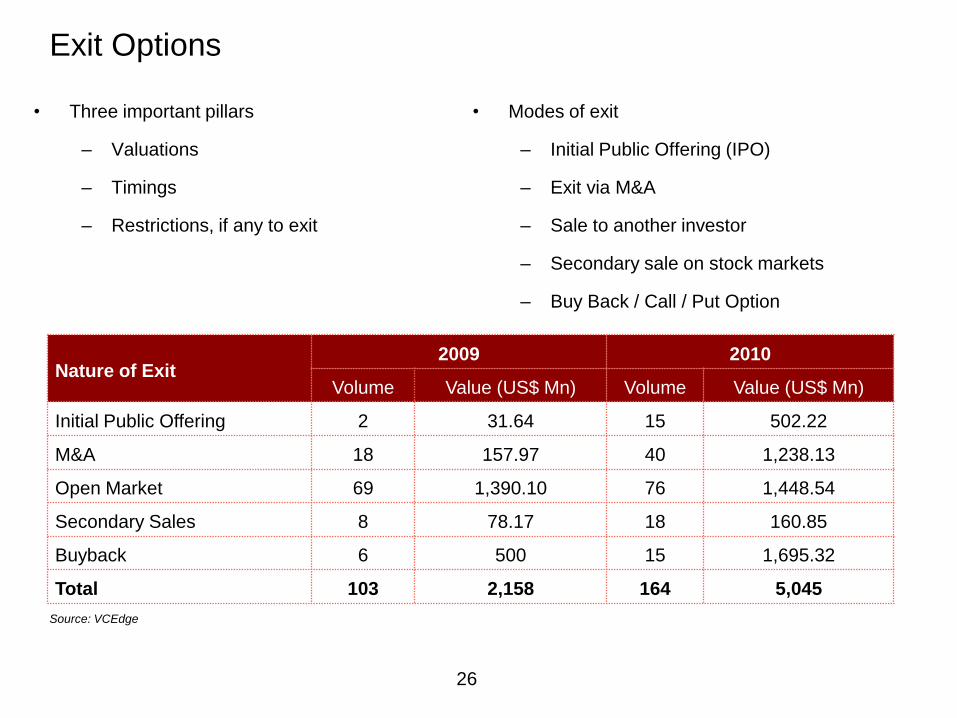

Exit Options

• Modes of exit

– Initial Public Offering (IPO)

– Exit via M&A

– Sale to another investor

– Secondary sale on stock markets

– Buy Back / Call / Put Option

• Three important pillars

– Valuations

– Timings

– Restrictions, if any to exit

Nature of Exit2009 2010

Volume Value (US$ Mn) Volume Value (US$ Mn)

Initial Public Offering 2 31.64 15 502.22

M&A 18 157.97 40 1,238.13

Open Market 69 1,390.10 76 1,448.54

Secondary Sales 8 78.17 18 160.85

Buyback 6 500 15 1,695.32

Total 103 2,158 164 5,045

Source: VCEdge

26

Advantages

• Fills funding gaps for long term capital

• No interest cost. Seeks return through capital appreciation rather than immediate and regular interest

payments

• Adds value because, apart from funding, PE contribution includes:

– Financing expertise and strategic management support

– Networking and Global Integration

– Confidential as compared to IPO or even debt funding

– Independence of the capital markets volatility

• Positive signaling effects to the market:

– Debt, IPO

– M&A

– Employees, Suppliers and Customers

– Increases Industry Visibility

• Corporate Governance

• Relatively less expensive fund raising exercise in comparison to IPO

27

Disadvantages

• Raising Private Equity finance is demanding, time consuming; at times the business may suffer if

promoter devotes more time for the transaction

• Depending on the investor, promoters may lose a certain amount of power to make management

decisions

• Will have to invest management time to provide regular information for the investor to monitor

• Might create conflict or differing opinion in long‐term strategy due to pressures of EXIT from the

investor

• The cost of complying with regulations could be relatively higher

• Non‐alignment of Interest of fund manager on the board and entrepreneur could hamper the growth

of company

28

Important factors for consideration

Growth Potential

Market Positioning

Management Bandwidth

Historical Performance

Competitive Scenario

Industry Trends

Project Period

Stage / Sector / Structure

Returns

Exit

29

• PE operating in a challenging environment today

• Difficult fund raising environment

• A large number of India focused funds were raised during 2004-06. Many of these are due to raise their

next fund

• Funds with dry powder putting monies to work in environment beset with intense competition

• Tremendous competition amongst funds to win deals resulting in bid war

• Expensive entry valuation continues to frustrate

• Investments by real estate funds have reduced - slowdown in sales & high borrowing cost continue to

plague the sector

30

17,828Announced

2011

2,024Raised

16,853Announced

2010

4,111Raised

Value of funds raised and announced ($ Mn)

Particulars 2010 2011

Funds Announced 52 51

Funds Raised 10 25

Number of funds raised and announced

PE at Crossroads…

Source: Economic Times on 6th January, 2011

31

• Deep inventory of future exits in the PE pipeline

– PE exits will take a lot of PE manager‟s time, energy and

bandwidth

– Approximately 68% of PE deals made through boom years of

2006-08 remain in PE funds‟ portfolios

– Now reaching the upper end of their investment holding periods,

many of these holdings should soon be coming up for sale

– PE exits account for only 20% of PE activity in 2011, indicating

strong potential for M&A transactions in the coming years. Also

reflected in increased preference towards exit through M&A route.

More than 100% rise in instances of exit through this option in

2010 over 2009

• Funds will look to learn from past and spend greater time on deal evaluation and make investment

decisions based on merits rather than sentiments

• PE firms also expected to spend considerable time on their portfolio management as holding periods have

been stretched

Source: Economic Times on 6th January, 2011

PE at Crossroads… (contd.)

• Motivation for PE players to provide high yield debt finance continues to grow. Such endeavors

undertaken to cater to all investment needs of promoter, debt & equity

• Increased activity in PIPES deals

– Volatile capital markets in 2011

– Conventional fund raising options for listed companies not available

– New Takeover code provides a boost for PE funds

– Greater number of listed companies expected to source growth capital needs from PE

• Early stage investing is in the limelight & will continue to gain momentum

• Deals in cloud computing, clean technology, online commerce and technology enabled services such as

mobile & online advertising, analytics and data management business will continue to attract Venture

Capital funding

• Strong growth potential for Venture Capital, Buyout funds and Pre-IPO / late stage placements

32

PE at Crossroads… (contd.)