private equity - actuaries institute · • venture capital fund managers bring capital, contacts,...

TRANSCRIPT

Private Equity

Chris Condon

Chief Investment Officer, MLC

2

Private Equity – Agenda

• Characteristics

• A private equity bubble?

• What’s important

3

Private equity is “managed entrepreneurship”

• Venture capital fund managers bring capital, contacts, and skills in a potent cocktail to help drive growth in their investments

• Buyout fund managers take majority stakes in companies to enact significant strategic and operational change

Buy Widgets Inc. Purchase price

of business = $150 m

Sell Widgets Inc. Sale price

of business = $300 m

Inject capex/hire

staff to

commercialise

new products Outsource

component

manufacturing

Change

product mix to

emphasise

high margin

products

Close/divest

loss making

businesses

Pro

fit = $20 m

Return Multiple = 2 x Cost

IRR = 20% p.a. over 4 yrs

Pro

fit = $10 m

Growth in company profit

of Widgets Inc.

Return comes from activist value creation not just passive capital investment

4

Definitions: Closed End Funds

Commitment: Investors commit to investing a fixed amount during the life of the fund.

Drawdown: When the fund acquires a business, committed capital is drawndown

Fund term: Funds have a fixed term, usually 10-12 years and is wound up after that

period.

Vintage Year: The year the fund was formed. Due to the cyclicality of the asset class,

the best comparisons are with other funds of the same vintage year.

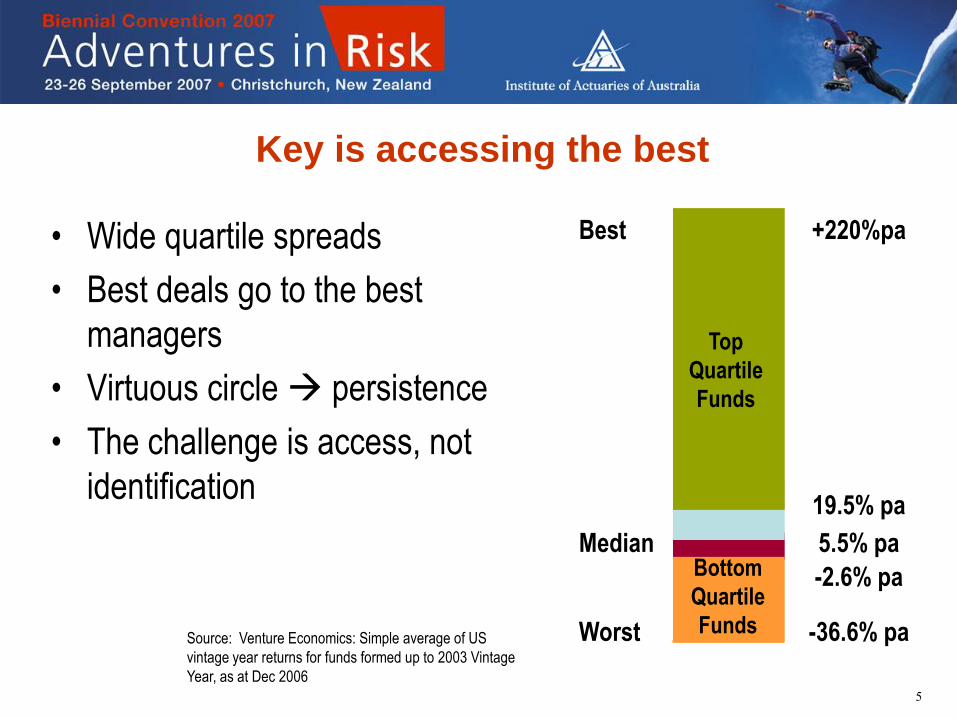

Difficult to forecast the timing of drawdowns and distributions

5

Source: Venture Economics: Simple average of US

vintage year returns for funds formed up to 2003 Vintage

Year, as at Dec 2006

Median 5.5% pa

-2.6% pa Bottom

Quartile

Funds

19.5% pa

Top

Quartile

Funds

Best +220%pa

Worst -36.6% pa

Key is accessing the best

• Wide quartile spreads

• Best deals go to the best

managers

• Virtuous circle persistence

• The challenge is access, not

identification

6

A private equity bubble?

Global LBO Activity by Region

Total Enterprise Value of LBO Transactions, USD Billions

0

100

200

300

400

500

600

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007*

Australian LBO

Asian LBO

Euro LBO

US LBO

*2007 is annualised year to date at 1 May 2007

Source: S&P, JPMorgan, Dealogic

7

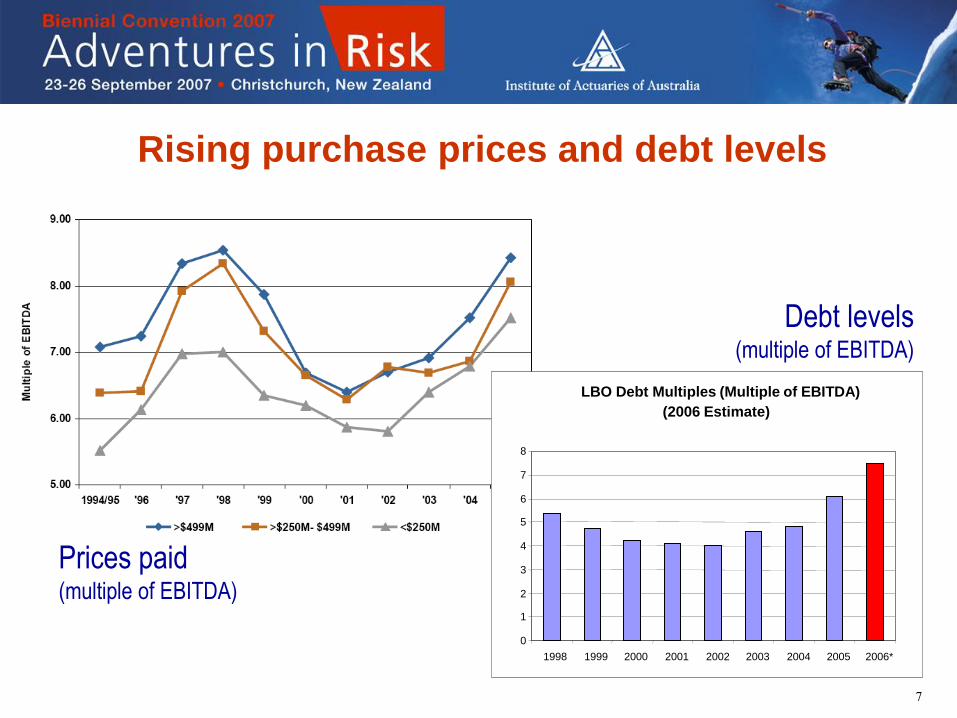

Rising purchase prices and debt levels

LBO Debt Multiples (Multiple of EBITDA)

(2006 Estimate)

0

1

2

3

4

5

6

7

8

1998 1999 2000 2001 2002 2003 2004 2005 2006*

Debt levels (multiple of EBITDA)

Prices paid (multiple of EBITDA)

8

Quadrupling of private equity’s share of M&A

PE as a Percentage of Total M&A Activity, Global

0

5

10

15

20

25

1999 2000 2001 2002 2003 2004 2005 2006

PE as a % of M&A

Source: Citigroup Global Markets

9

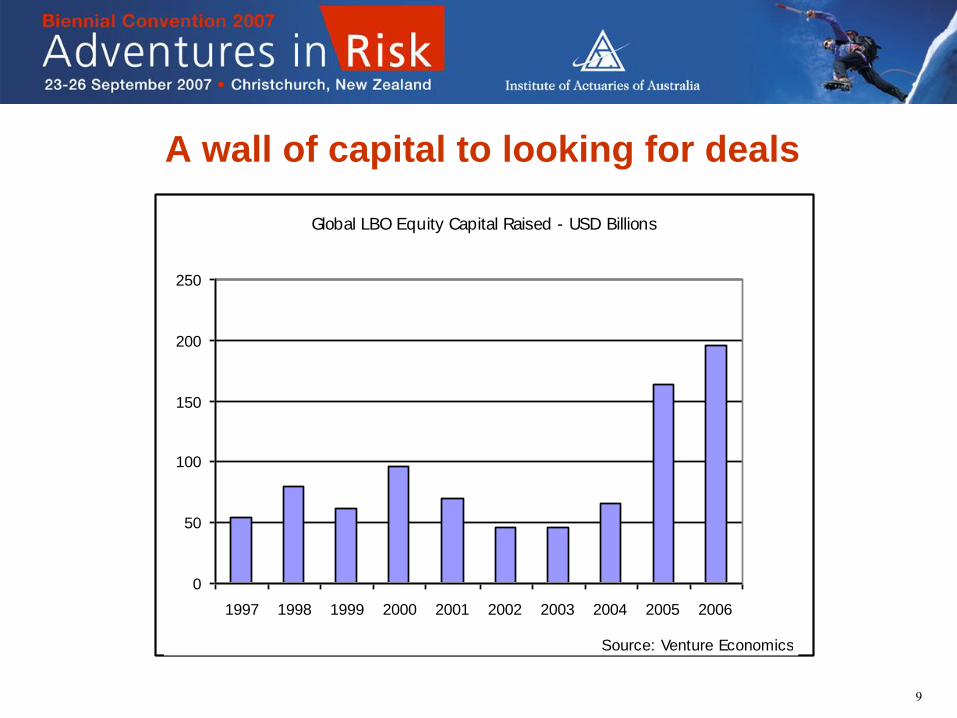

A wall of capital to looking for deals

Global LBO Equity Capital Raised - USD Billions

0

50

100

150

200

250

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Source: Venture Economics

10

Higher prices funded by leverage

Acquisition Multiples for Large Cap Deals showing Equity and Leverage-

Average Multiple of EBITDA for Winning Bids

4 .74 .2 4 .1 4

4 .6 4 .95.4 5.5 5.7

8 .3

7.0 6 .7 7.0 7.3

7.9

8 .8 8 .8 9 .1

0

1

2

3

4

5

6

7

8

9

10

19 9 9 2 0 0 0 2 0 0 1 2 0 0 2 2 0 0 3 2 0 0 4 2 0 0 5 2 0 0 6 2 0 0 7*

Equity

Debt

Source: S&P, LCD

11

Margins ain’t what they used to be

LEV ERA G ED LO A N INTERES T RA TE & LB O PURC HA S E YIELD S

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Ma

r-9

8

Se

p-9

8

Ma

r-9

9

Se

p-9

9

Ma

r-0

0

Se

p-0

0

Ma

r-0

1

Se

p-0

1

Ma

r-0

2

Se

p-0

2

Ma

r-0

3

Se

p-0

3

Ma

r-0

4

Se

p-0

4

Ma

r-0

5

Se

p-0

5

Ma

r-0

6

Se

p-0

6

Ma

r-0

7

Se

p-0

7

%

A V E R A G E L O A N R A T E *

P U R C H A S E Y I E L D * *

* O N LEVERAGED LO AN S

* * O N EBITD A, FO R LBO TRAN S AC TIO N S

S O U RC E: S TAN D ARD & PO O R'S

Source: Morgan Stanley

12

20 is today’s 30

Comparitive US Investment Returns - IRR%

0

5

10

15

20

25

30

35

40

1 Year 3 Year 5 Year 7 Year 15 Year

US Buy-out Top Quartile

All US Buyout

S&P 500

Source: Thomson, Venture Economics

13

The bubble has now been pricked!

Source: Bridgewater® Daily Observations 21 August 2007

14

Venture Capital – ugly sister or opportunity?

VC Investments by Region, USD Billions

$41

$22 $20$23 $23

$15

$6

$4

$5 $3

$5

$3

$3

$3 $7

$0

$10

$20

$30

$40

$50

$60

$70

2001 2002 2003 2004 2005

Asia

Europe

US

Source: HRJ, PwC, Venture Source, IVC Online

US Venture Capital IRRs by Vintage Year

-20%

0%

20%

40%

60%

80%

100%

120%

140%

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

Note that the "J-Curve" effect is apparent from 2005 onward.

Source: Venture Economics

VC investments

halved since 2001

And returns

evaporated

15

What’s important…

• Access to top tier managers is key – Sophistication, discipline, consistency, quick decisions

• Vintage year diversification – Today’s commitments invested over 1-3 years

– You can’t time the cycle

• But be prepared to say no

• Today? – don’t confuse leveraged luck for skill

– look for fundamental value creation