presented by: dr. nanny dewi, se.,m.comm, ca head of undergraduate accounting program faculty of...

TRANSCRIPT

Indonesia Accounting Curriculum

Presented by:

Dr. Nanny Dewi, SE.,M.comm, CAHead of Undergraduate Accounting Program

Faculty of Economics and Business (FEB) – Padjadjaran University

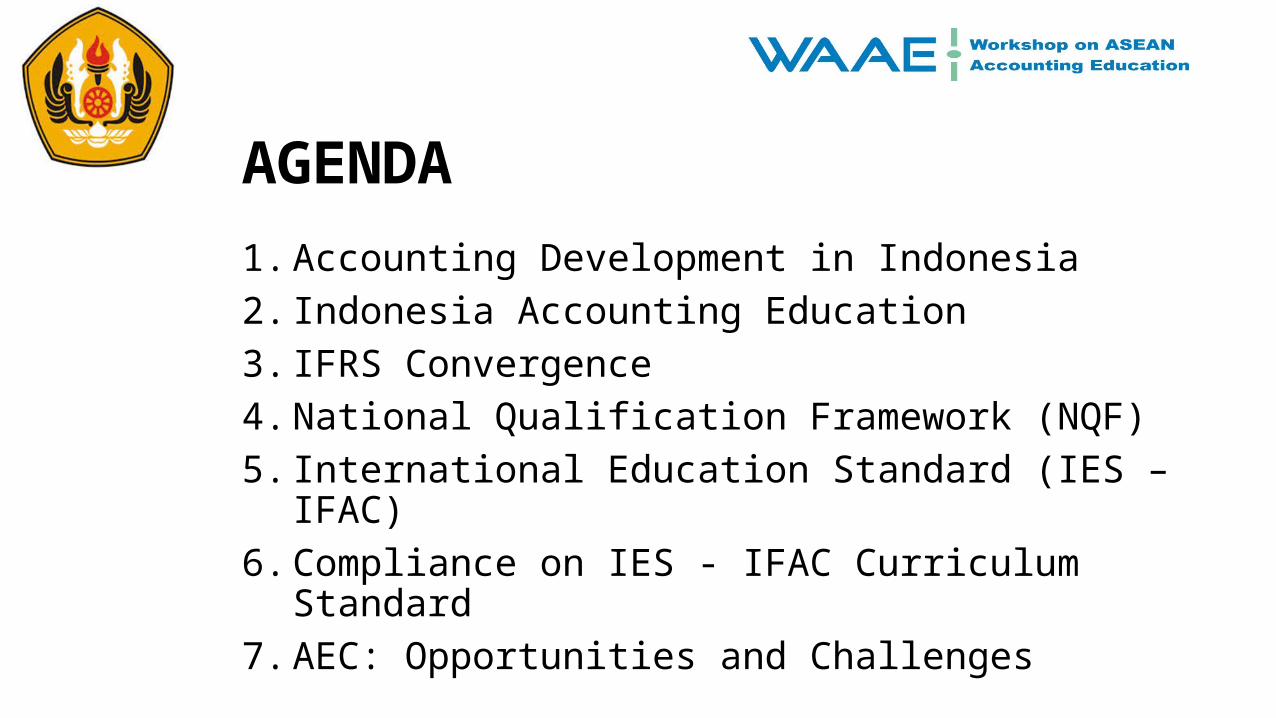

AGENDA

1. Accounting Development in Indonesia2. Indonesia Accounting Education3. IFRS Convergence4. National Qualification Framework (NQF)5. International Education Standard (IES – IFAC)6. Compliance on IES - IFAC Curriculum Standard7. AEC: Opportunities and Challenges

Accounting Development in Indonesia

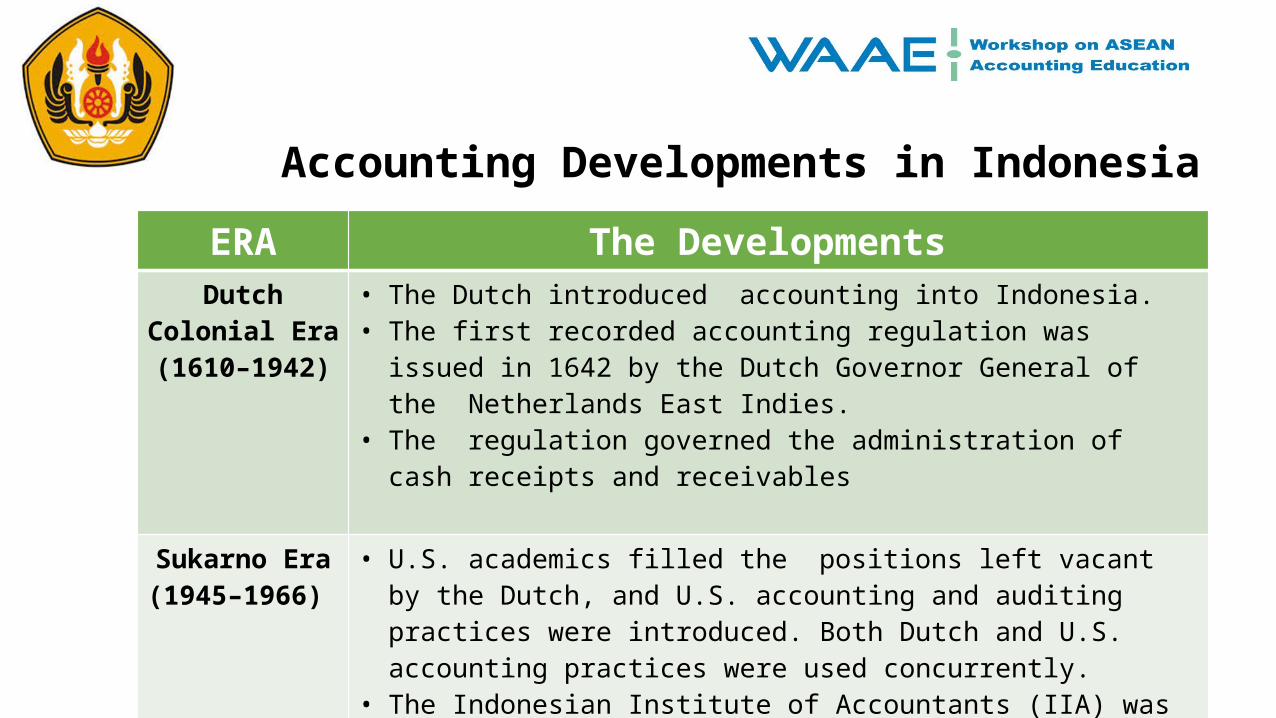

Accounting Developments in Indonesia

ERA The Developments Dutch Colonial

Era (1610–1942)• The Dutch introduced accounting into Indonesia. • The first recorded accounting regulation was issued in 1642 by the Dutch

Governor General of the Netherlands East Indies.• The regulation governed the administration of cash receipts and

receivables

Sukarno Era (1945–1966)

• U.S. academics filled the positions left vacant by the Dutch, and U.S. accounting and auditing practices were introduced. Both Dutch and U.S. accounting practices were used concurrently.

• The Indonesian Institute of Accountants (IIA) was established in 1957 to guide and coordinate the activities of accountants.

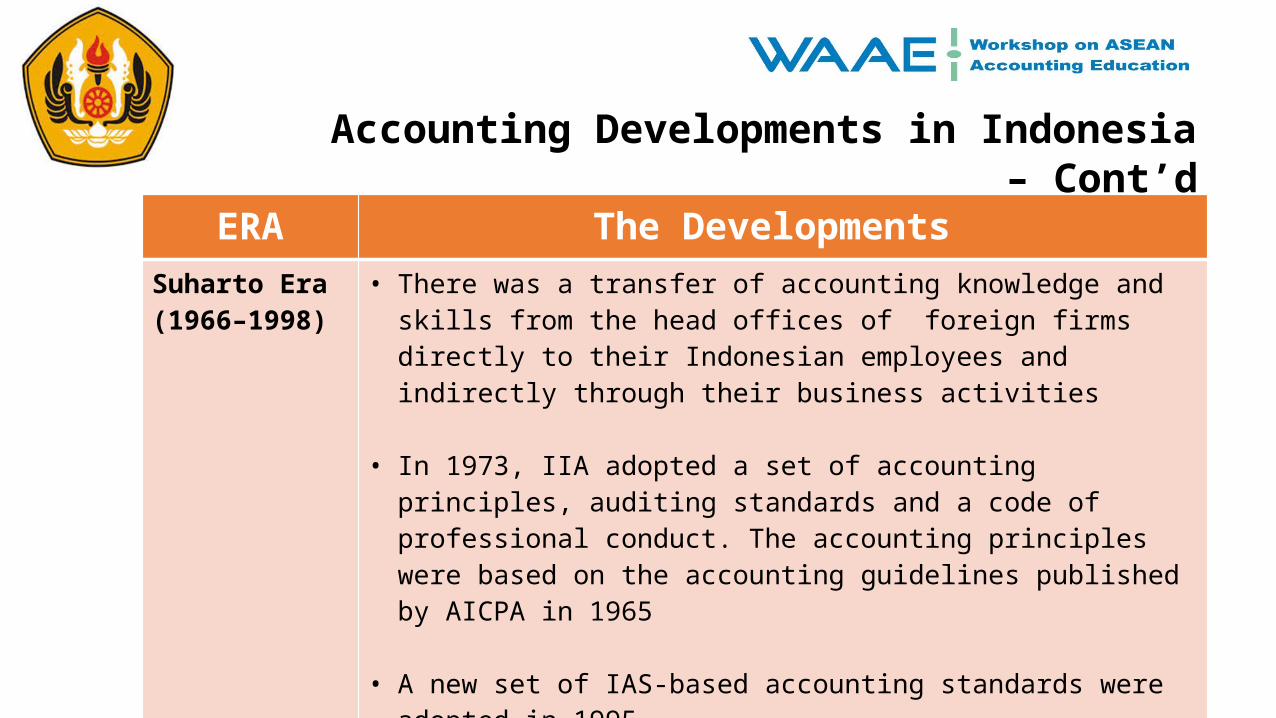

Accounting Developments in Indonesia – Cont’d

ERA The Developments

Suharto Era (1966–1998)

• There was a transfer of accounting knowledge and skills from the head offices of foreign firms directly to their Indonesian employees and indirectly through their business activities

• In 1973, IIA adopted a set of accounting principles, auditing standards and a code of professional conduct. The accounting principles were based on the accounting guidelines published by AICPA in 1965

• A new set of IAS-based accounting standards were adopted in 1995Post-Suharto Era (post 1998)

• Regulations are tightened to improve financial disclosure

Millenium Era • IFRS Convergency

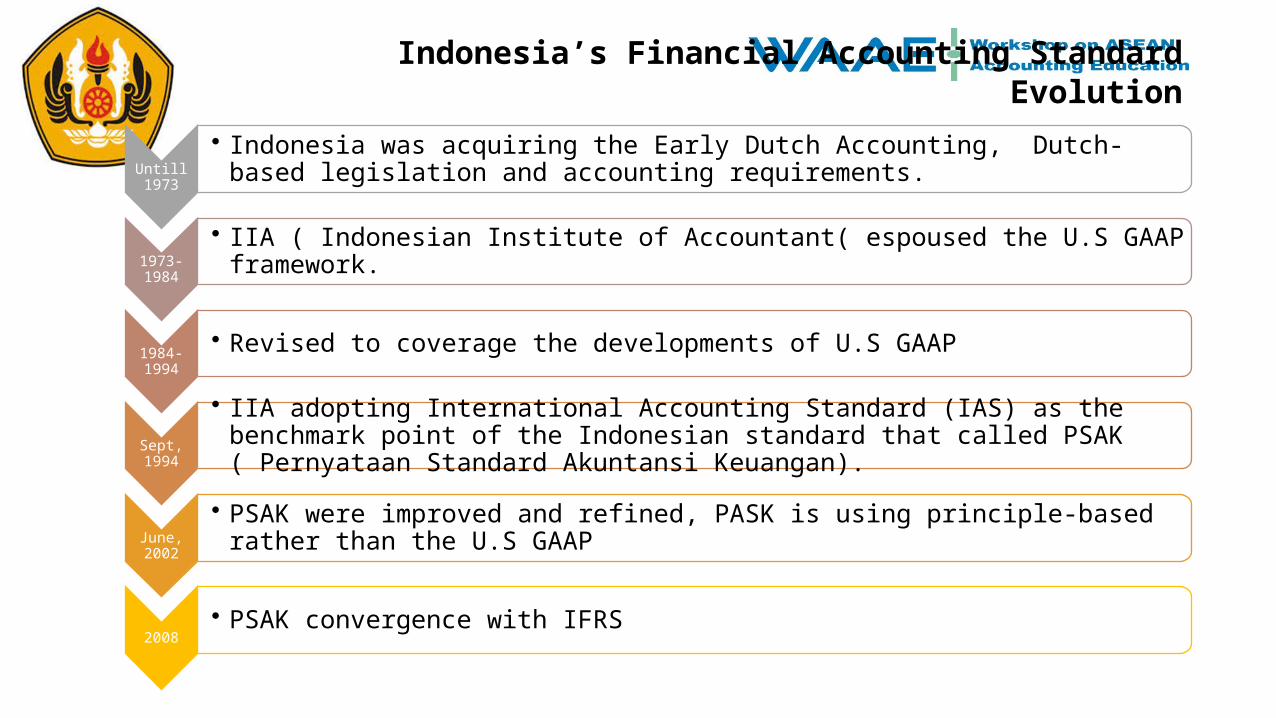

Indonesia’s Financial Accounting Standard Evolution

Untill

1973

• Indonesia was acquiring the Early Dutch Accounting, Dutch-based legislation and accounting requirements.

1973-

1984

• IIA ( Indonesian Institute of Accountant( espoused the U.S GAAP framework.

1984-

1994

• Revised to coverage the developments of U.S GAAP

Sept,

1994

• IIA adopting International Accounting Standard (IAS) as the benchmark point of the Indonesian standard that called PSAK ( Pernyataan Standard Akuntansi Keuangan).

June,

2002

• PSAK were improved and refined, PASK is using principle-based rather than the U.S GAAP

2008

• PSAK convergence with IFRS

IFRS Convergence

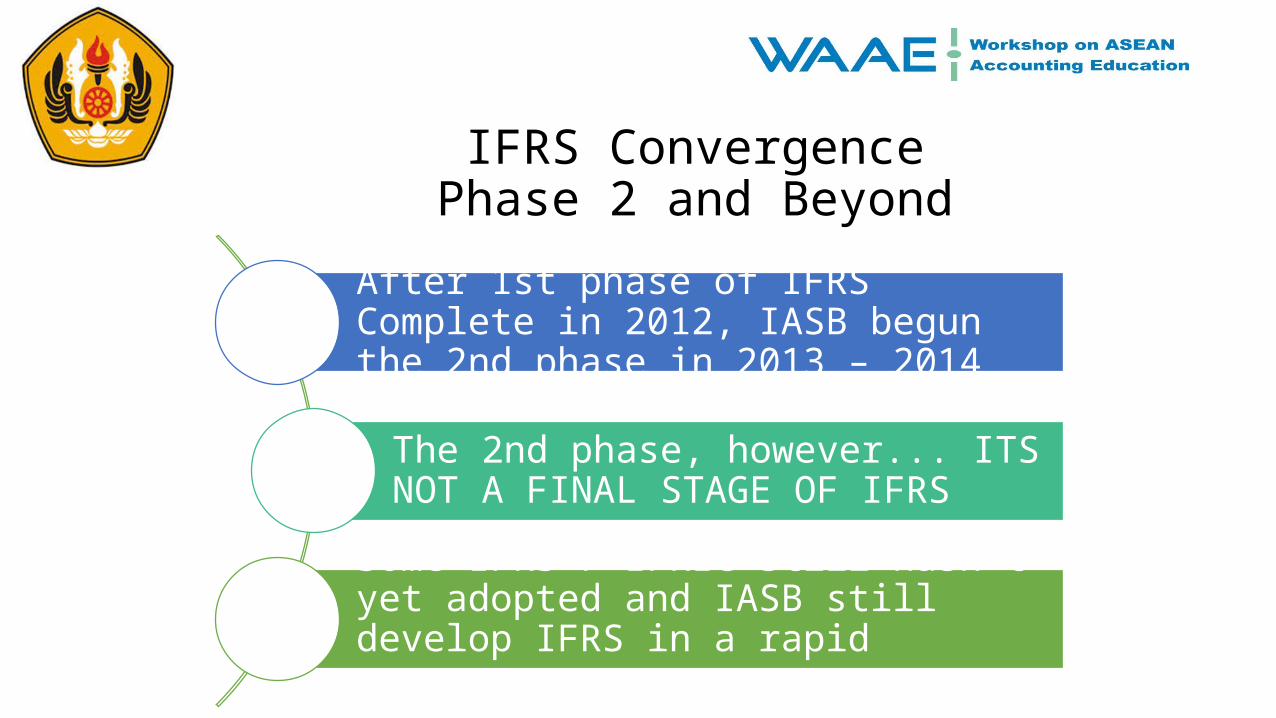

IFRS ConvergencePhase 2 and Beyond

After 1st phase of IFRS Complete in 2012, IASB begun the 2nd phase in 2013 – 2014

The 2nd phase, however... ITS NOT A FINAL STAGE OF IFRS

Some IFRS / IFRIC still hasn’t yet adopted and IASB still develop IFRS in a rapid sequence

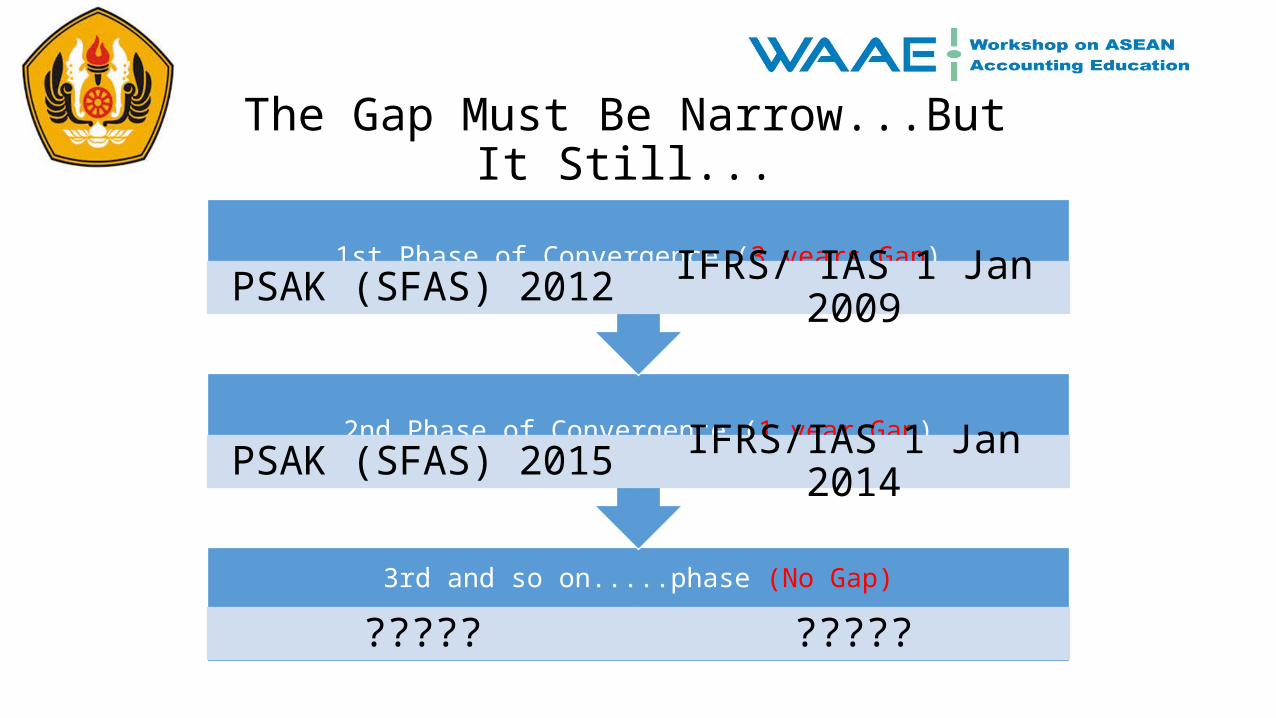

The Gap Must Be Narrow...But It Still...

3rd and so on.....phase (No Gap)

????? ?????

2nd Phase of Convergence (1 year Gap)PSAK (SFAS) 2015 IFRS/IAS 1 Jan 2014

1st Phase of Convergence (3 years Gap)PSAK (SFAS) 2012 IFRS/ IAS 1 Jan 2009

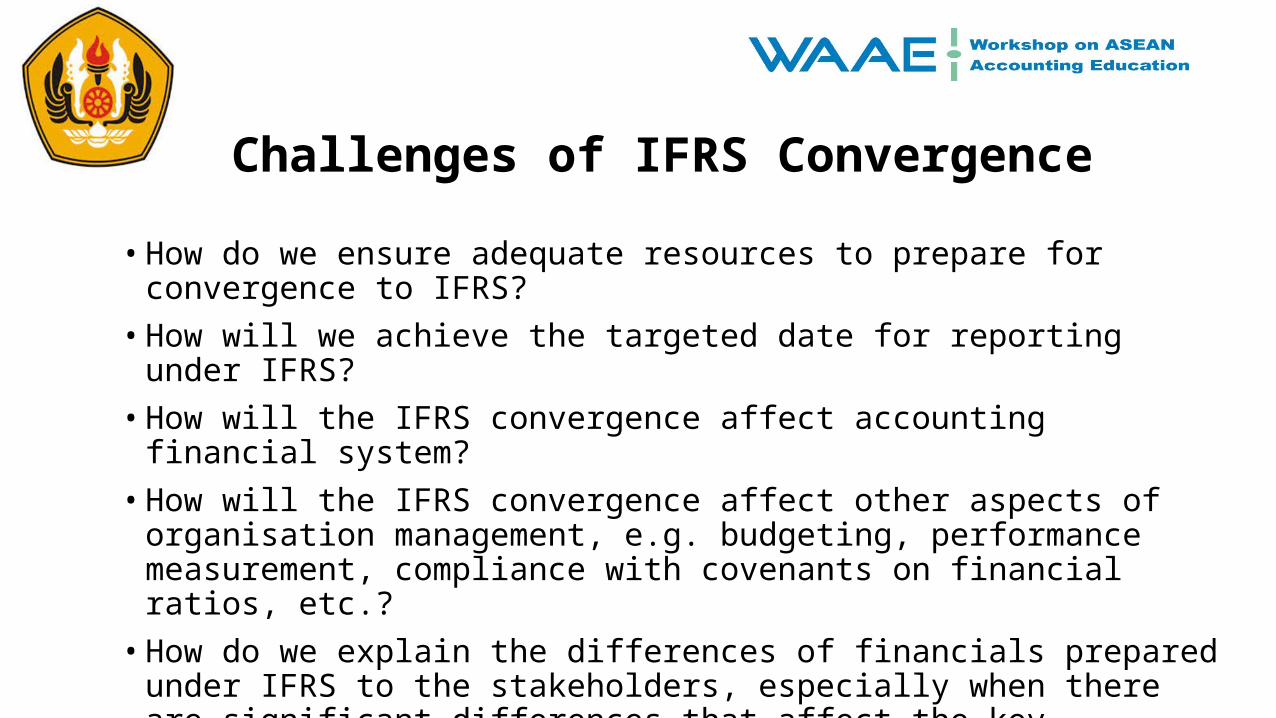

Challenges of IFRS Convergence

• How do we ensure adequate resources to prepare for convergence to IFRS? • How will we achieve the targeted date for reporting under IFRS?• How will the IFRS convergence affect accounting financial system?• How will the IFRS convergence affect other aspects of organisation management,

e.g. budgeting, performance measurement, compliance with covenants on financial ratios, etc.?

• How do we explain the differences of financials prepared under IFRS to the stakeholders, especially when there are significant differences that affect the key performance items, such as revenues, earnings, financial ratios, etc.?

Indonesia’s Commitment Towards Converging Into IFRS

• The general approach taken by Indonesia with regard to the IFRS convergence process is to gradually converge the local standards with IFRSs, starting with minimizing the significant differences between the two

• Indonesia intends to analyze the readiness of industry and other constituents in implementing the first wave of standards resulting from the convergence process before developing the next wave of new standards.

• Indonesia aims to provide a sufficient transitional period of 3 to 4 years for new standards while minimizing any gaps between the effective dates of new IFRSs and new Indonesian standards

Indonesia Accounting Education and Curriculum

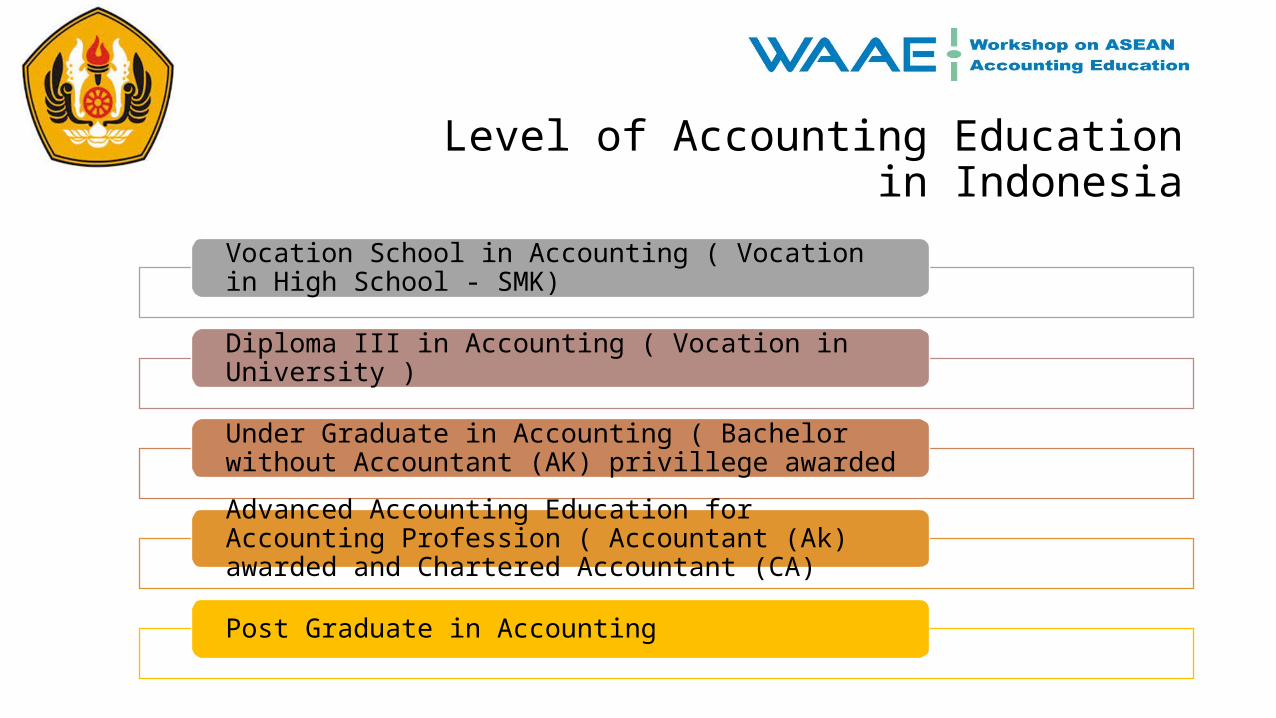

Level of Accounting Education in Indonesia

Vocation School in Accounting ( Vocation in High School - SMK)

Diploma III in Accounting ( Vocation in University )

Under Graduate in Accounting ( Bachelor without Accountant (AK) privillege awarded

Advanced Accounting Education for Accounting Profession ( Accountant (Ak) awarded and Chartered Accountant (CA)

Post Graduate in Accounting

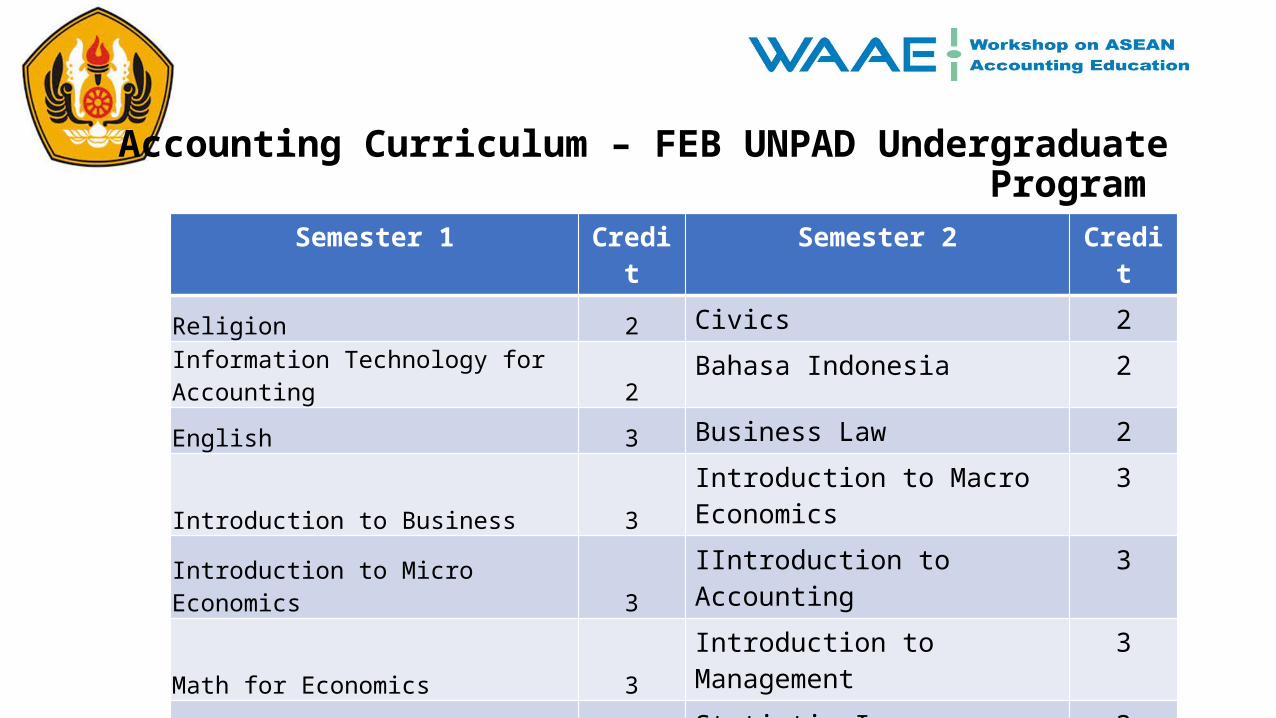

Accounting Curriculum – FEB UNPAD Undergraduate Program

Semester 1 Credit Semester 2 Credit

Religion 2 Civics 2

Information Technology for Accounting 2 Bahasa Indonesia 2

English 3 Business Law 2

Introduction to Business 3 Introduction to Macro Economics 3

Introduction to Micro Economics 3 IIntroduction to Accounting 3

Math for Economics 3 Introduction to Management 3Statistic I 3Basic Pshycology 2Elective Cource 3

Total 16 Total 23

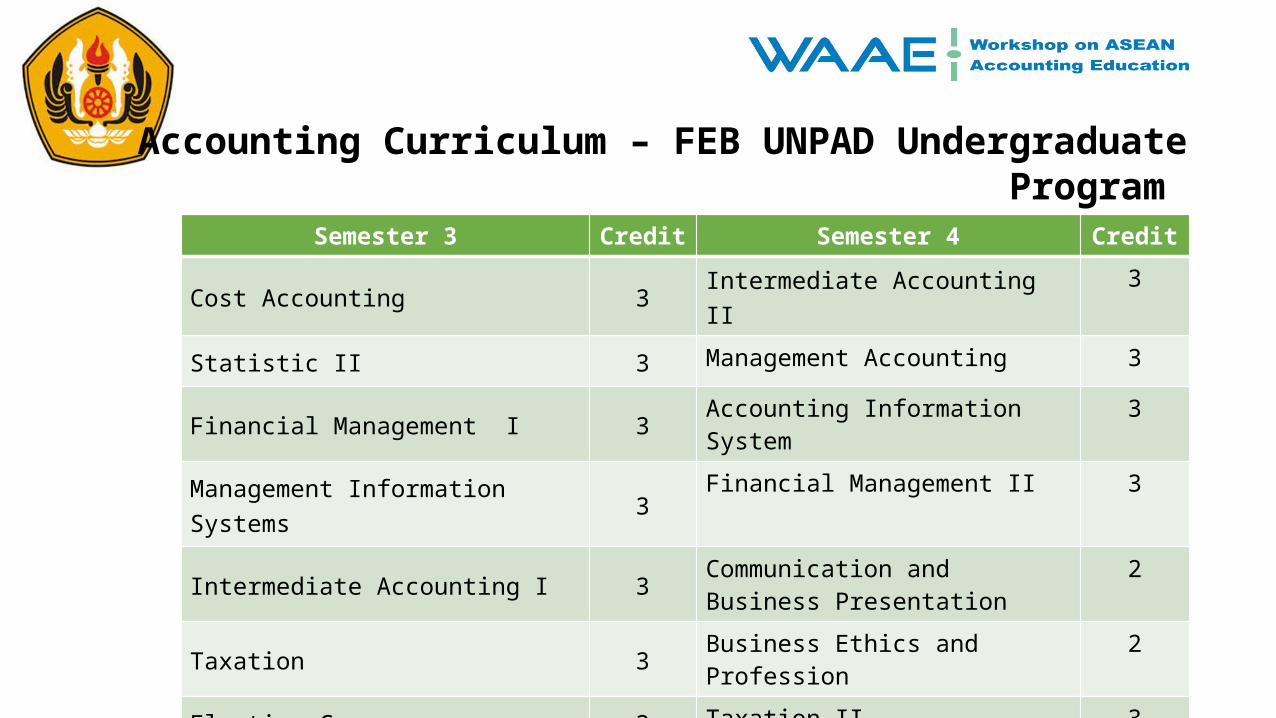

Accounting Curriculum – FEB UNPAD Undergraduate Program

Semester 3 Credit Semester 4 Credit

Cost Accounting 3 Intermediate Accounting II 3

Statistic II 3 Management Accounting 3

Financial Management I 3 Accounting Information System 3

Management Information Systems 3 Financial Management II 3

Intermediate Accounting I 3 Communication and Business Presentation

2

Taxation 3 Business Ethics and Profession 2

Elective Cources 3 Taxation II 3

Elective Course 3

Total 21 Total 22

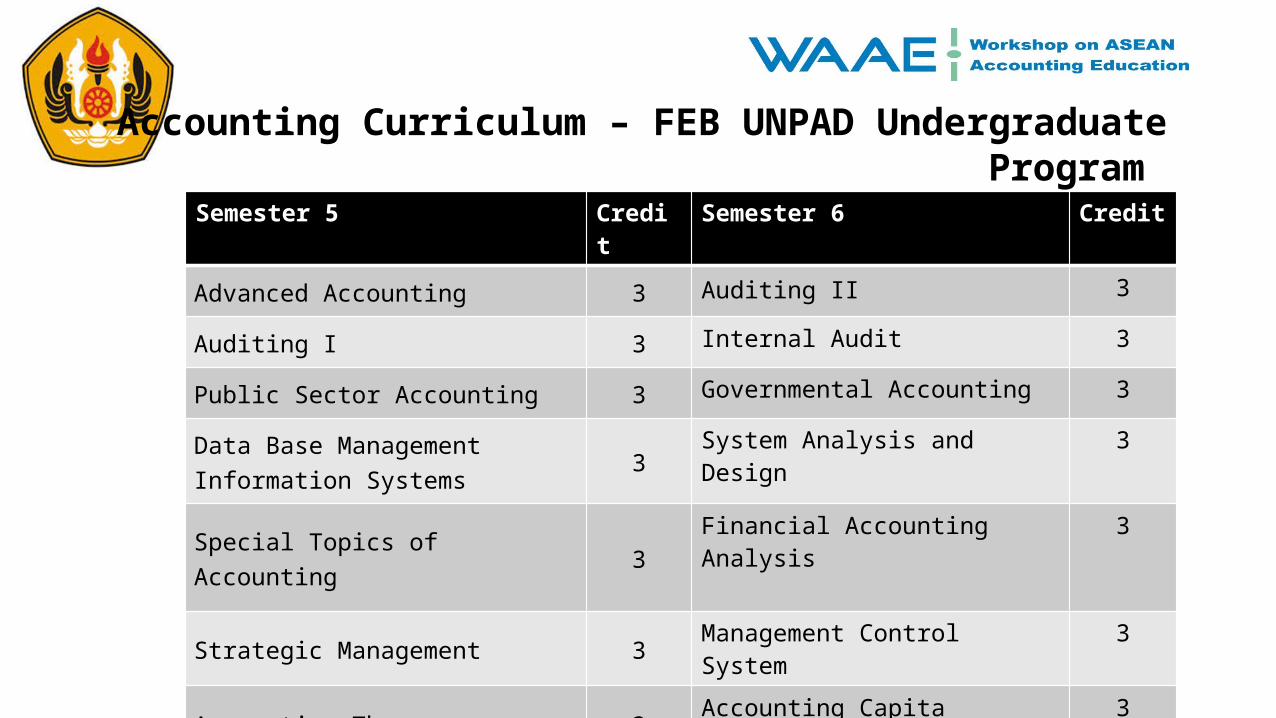

Accounting Curriculum – FEB UNPAD Undergraduate Program

Semester 5 Credit Semester 6 Credit

Advanced Accounting 3 Auditing II 3

Auditing I 3 Internal Audit 3

Public Sector Accounting 3 Governmental Accounting 3

Data Base Management Information Systems 3

System Analysis and Design 3

Special Topics of Accounting 3 Financial Accounting Analysis 3

Strategic Management 3 Management Control System 3

Accounting Theory 3 Accounting Capita Selecta 3

Elective Cources 3 Elective Course

Total 24 Total 24

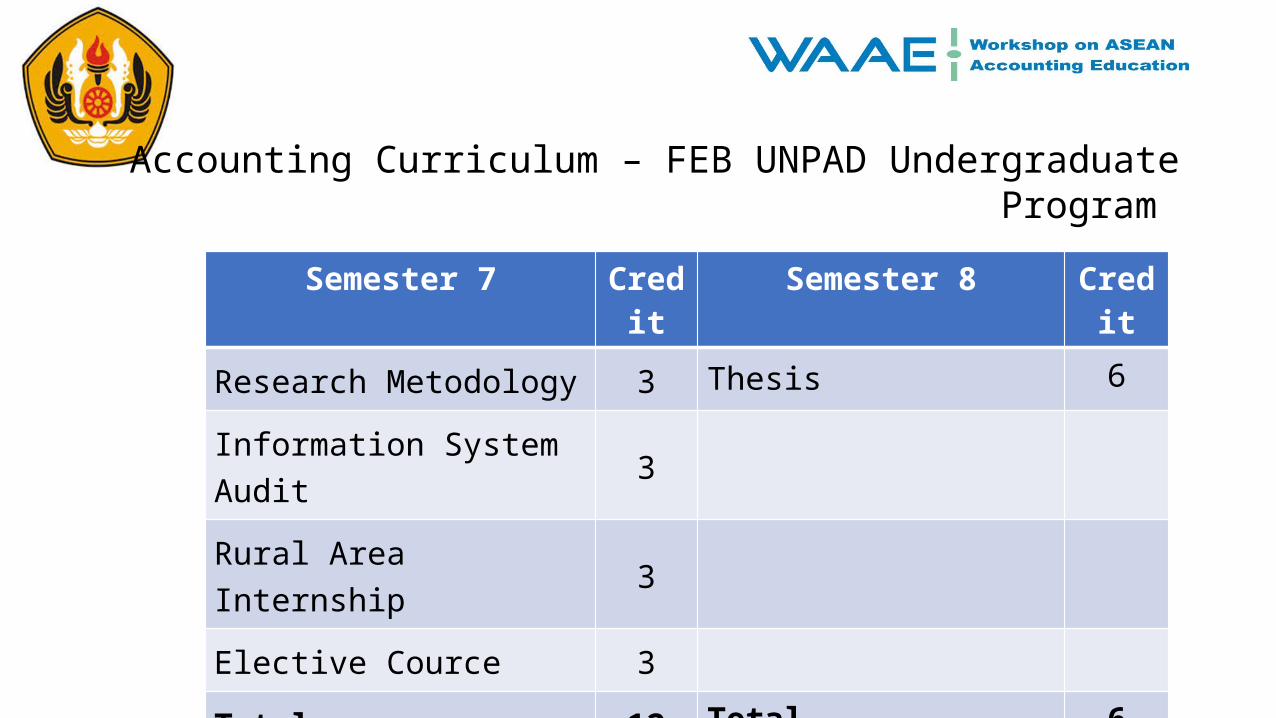

Accounting Curriculum – FEB UNPAD Undergraduate Program

Semester 7 Credit Semester 8 CreditResearch Metodology 3 Thesis 6

Information System Audit 3

Rural Area Internship 3

Elective Cource 3

Total 12 Total 6

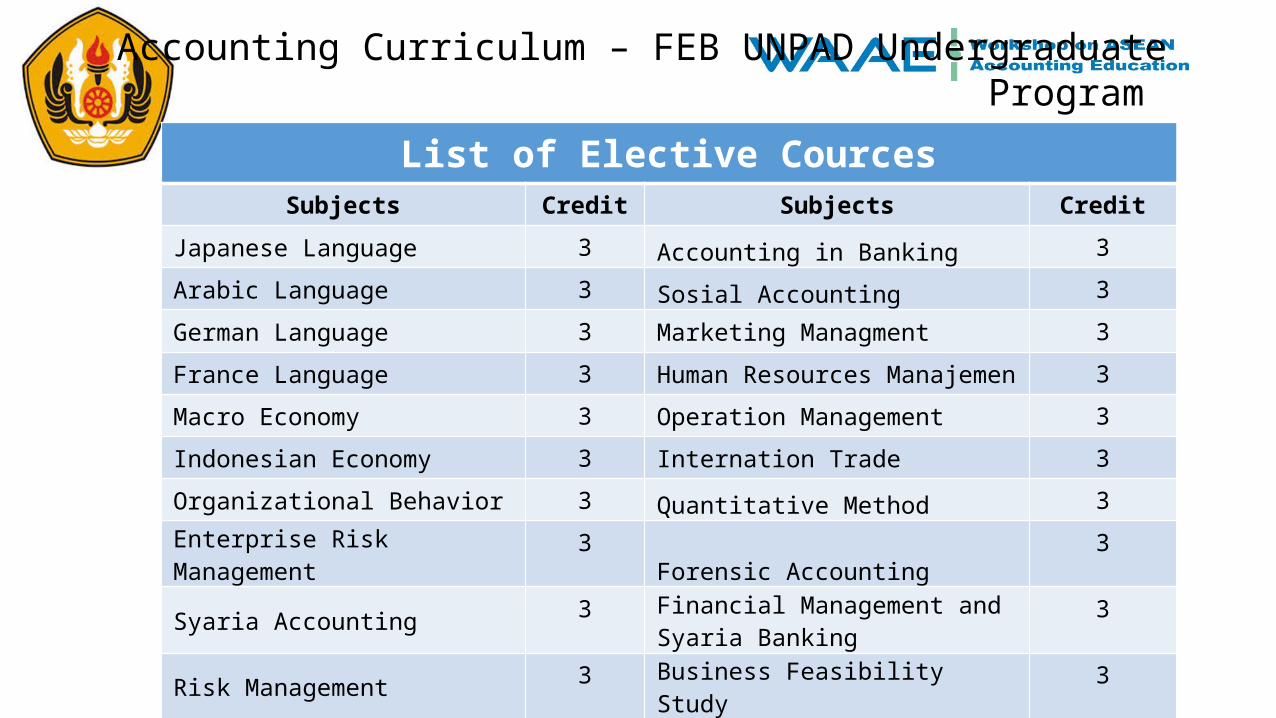

Accounting Curriculum – FEB UNPAD Undergraduate Program

List of Elective CourcesSubjects Credit Subjects Credit

Japanese Language 3 Accounting in Banking 3

Arabic Language 3 Sosial Accounting 3

German Language 3 Marketing Managment 3

France Language 3 Human Resources Manajemen 3

Macro Economy 3 Operation Management 3

Indonesian Economy 3 Internation Trade 3

Organizational Behavior 3 Quantitative Method 3

Enterprise Risk Management 3 Forensic Accounting 3

Syaria Accounting 3 Financial Management and Syaria Banking

3

Risk Management 3 Business Feasibility Study 3

Oil and Gas Accounting 3 Capita Selecta in Taxation 3

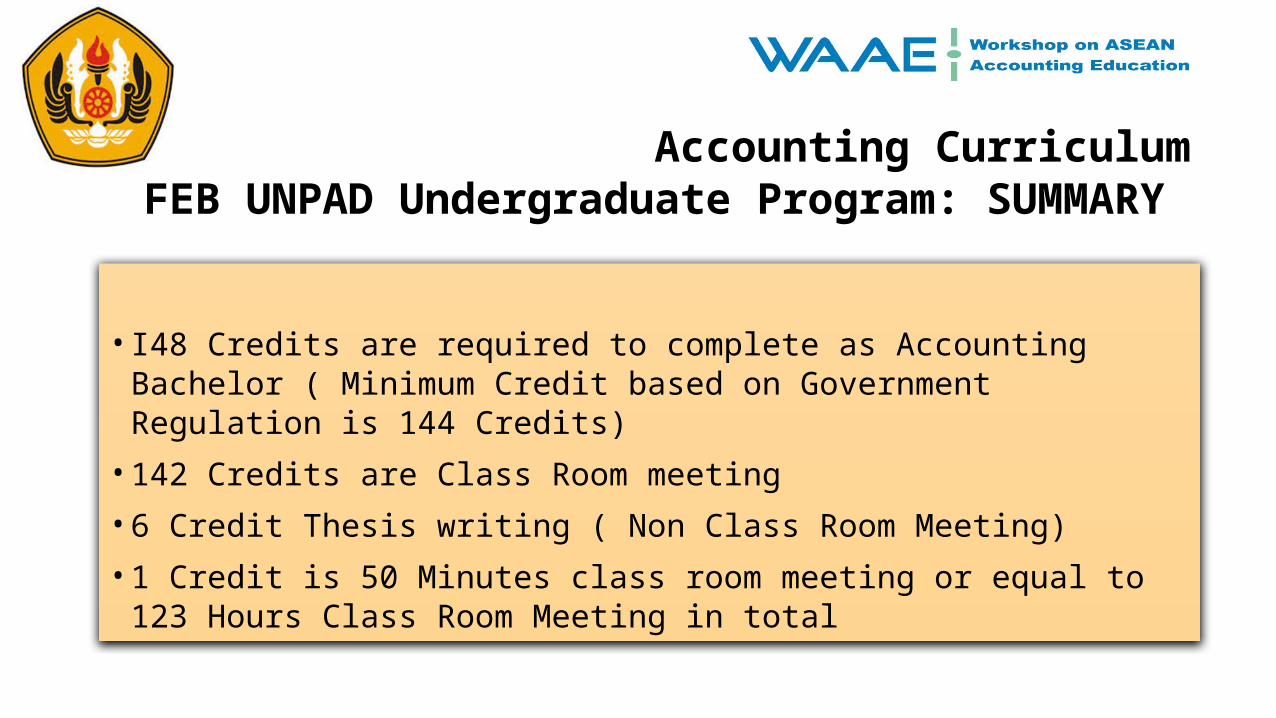

Accounting CurriculumFEB UNPAD Undergraduate Program:

SUMMARY

• I48 Credits are required to complete as Accounting Bachelor ( Minimum Credit based on Government Regulation is 144 Credits)

• 142 Credits are Class Room meeting• 6 Credit Thesis writing ( Non Class Room Meeting)• 1 Credit is 50 Minutes class room meeting or equal to 123 Hours Class

Room Meeting in total

Accountant Profession in Indonesia

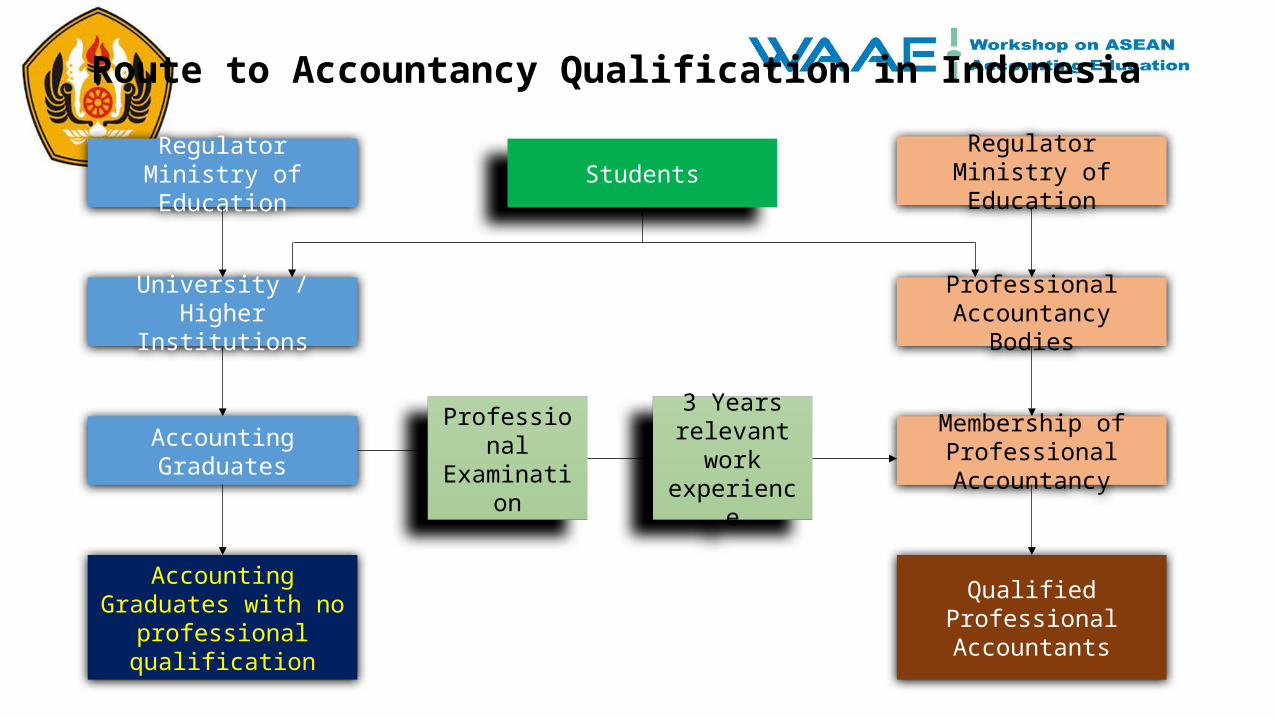

Route to Accountancy Qualification in Indonesia

RegulatorMinistry of Education

University / Higher Institutions

Accounting Graduates

Accounting Graduates with no professional

qualification

Students

Professional Accountancy Bodies

Membership of Professional Accountancy

Qualified ProfessionalAccountants

RegulatorMinistry of Education

Professional Examination

3 Years relevant work

experience

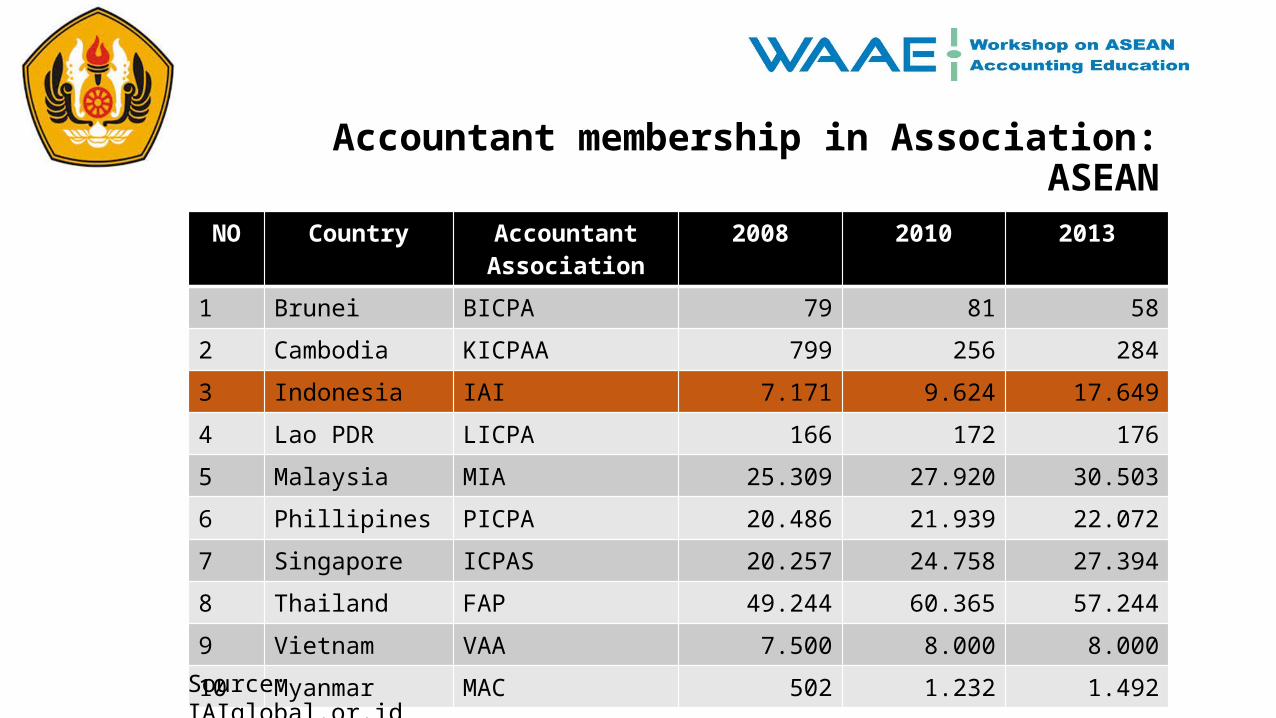

Accountant membership in Association: ASEAN

NO Country Accountant Association

2008 2010 2013

1 Brunei BICPA 79 81 58

2 Cambodia KICPAA 799 256 284

3 Indonesia IAI 7.171 9.624 17.649

4 Lao PDR LICPA 166 172 176

5 Malaysia MIA 25.309 27.920 30.503

6 Phillipines PICPA 20.486 21.939 22.072

7 Singapore ICPAS 20.257 24.758 27.394

8 Thailand FAP 49.244 60.365 57.244

9 Vietnam VAA 7.500 8.000 8.000

10 Myanmar MAC 502 1.232 1.492

Source: IAIglobal.or.id

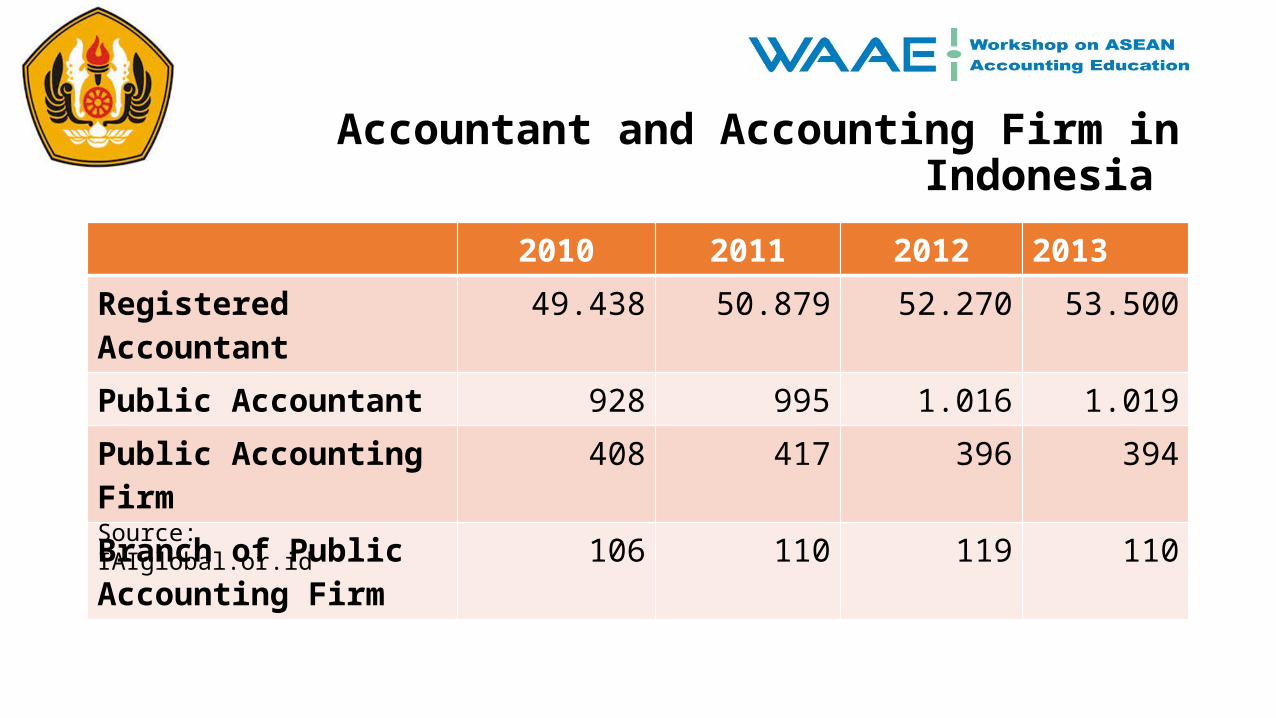

Accountant and Accounting Firm in Indonesia

2010 2011 2012 2013Registered Accountant 49.438 50.879 52.270 53.500Public Accountant 928 995 1.016 1.019Public Accounting Firm 408 417 396 394Branch of Public Accounting Firm

106 110 119 110

Source: IAIglobal.or.id

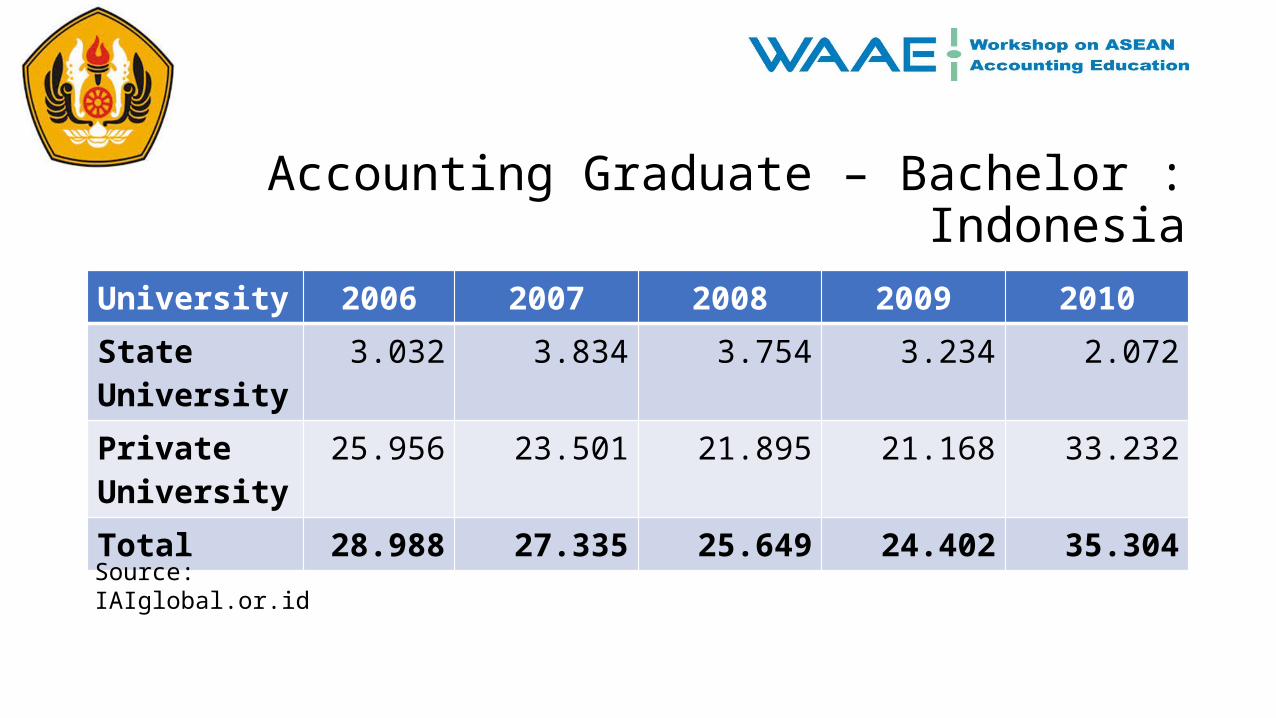

Accounting Graduate – Bachelor : Indonesia

University 2006 2007 2008 2009 2010State University

3.032 3.834 3.754 3.234 2.072

Private University

25.956 23.501 21.895 21.168 33.232

Total 28.988 27.335 25.649 24.402 35.304

Source: IAIglobal.or.id

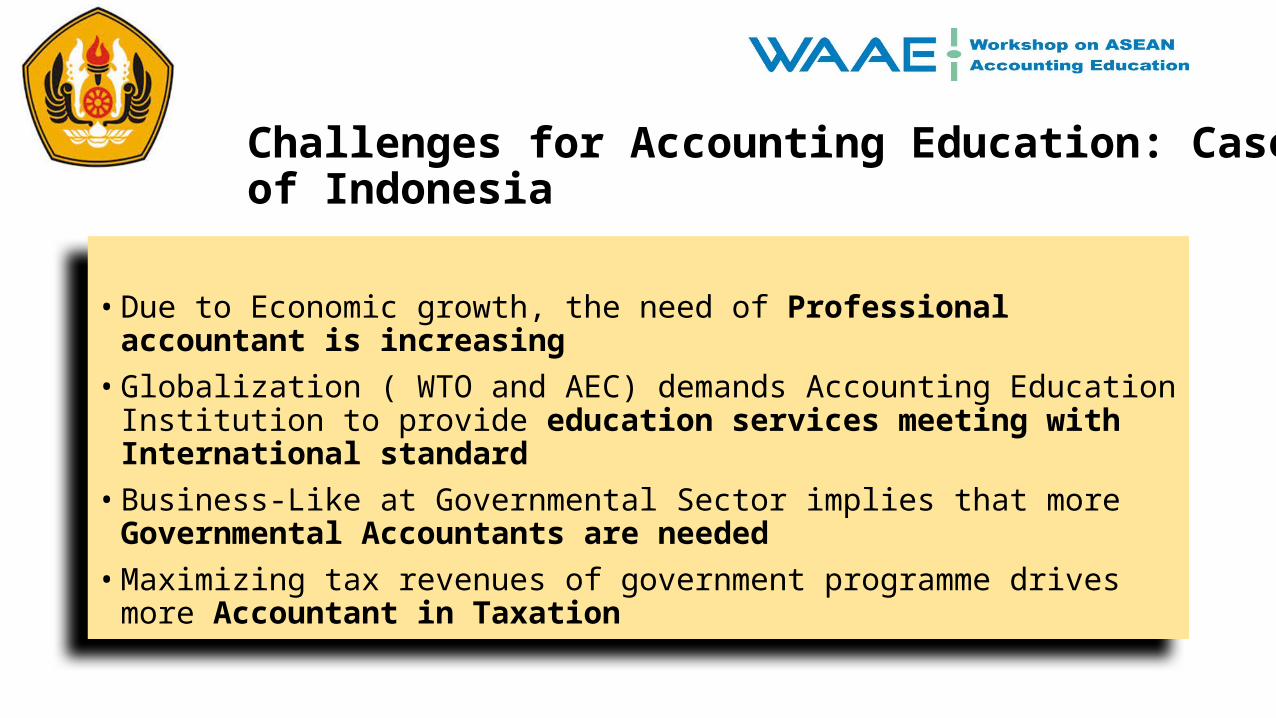

Challenges for Accounting Education: Case of Indonesia

• Due to Economic growth, the need of Professional accountant is increasing• Globalization ( WTO and AEC) demands Accounting Education Institution to

provide education services meeting with International standard• Business-Like at Governmental Sector implies that more Governmental

Accountants are needed• Maximizing tax revenues of government programme drives more Accountant in

Taxation

National Quality Framework (NQF)

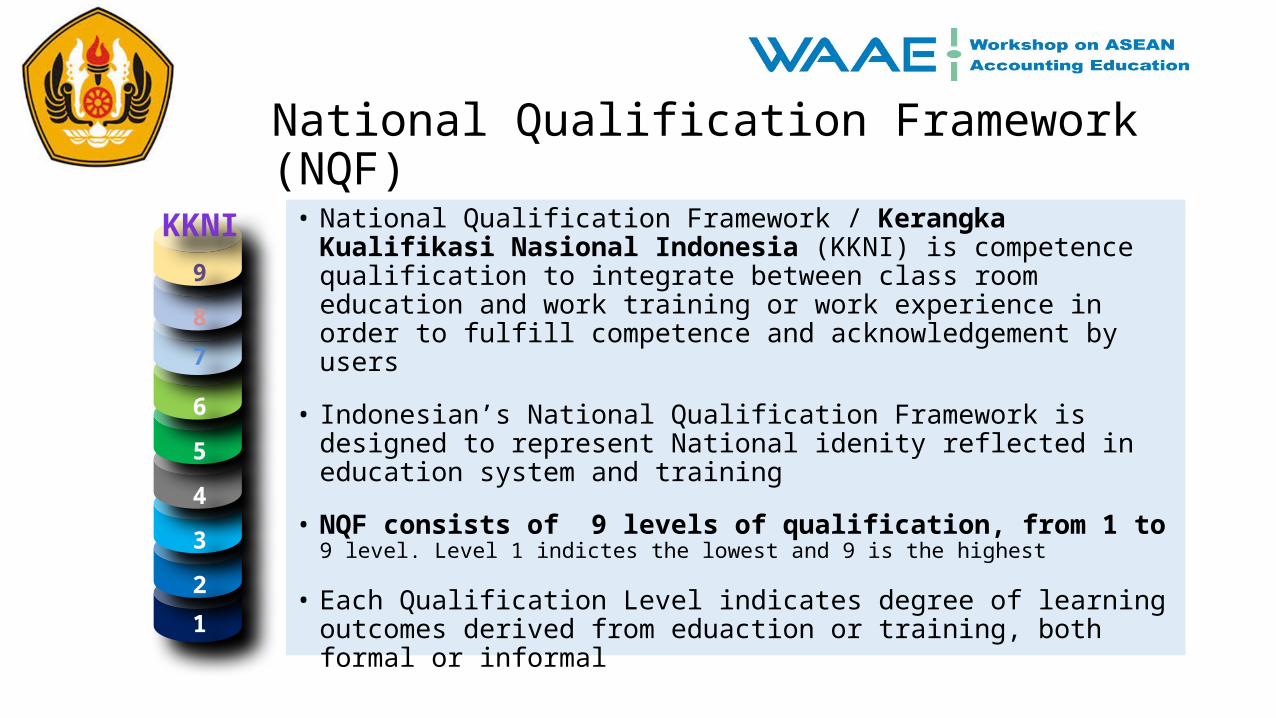

National Qualification Framework (NQF)

• National Qualification Framework / Kerangka Kualifikasi Nasional Indonesia (KKNI) is competence qualification to integrate between class room education and work training or work experience in order to fulfill competence and acknowledgement by users

• Indonesian’s National Qualification Framework is designed to represent National idenity reflected in education system and training

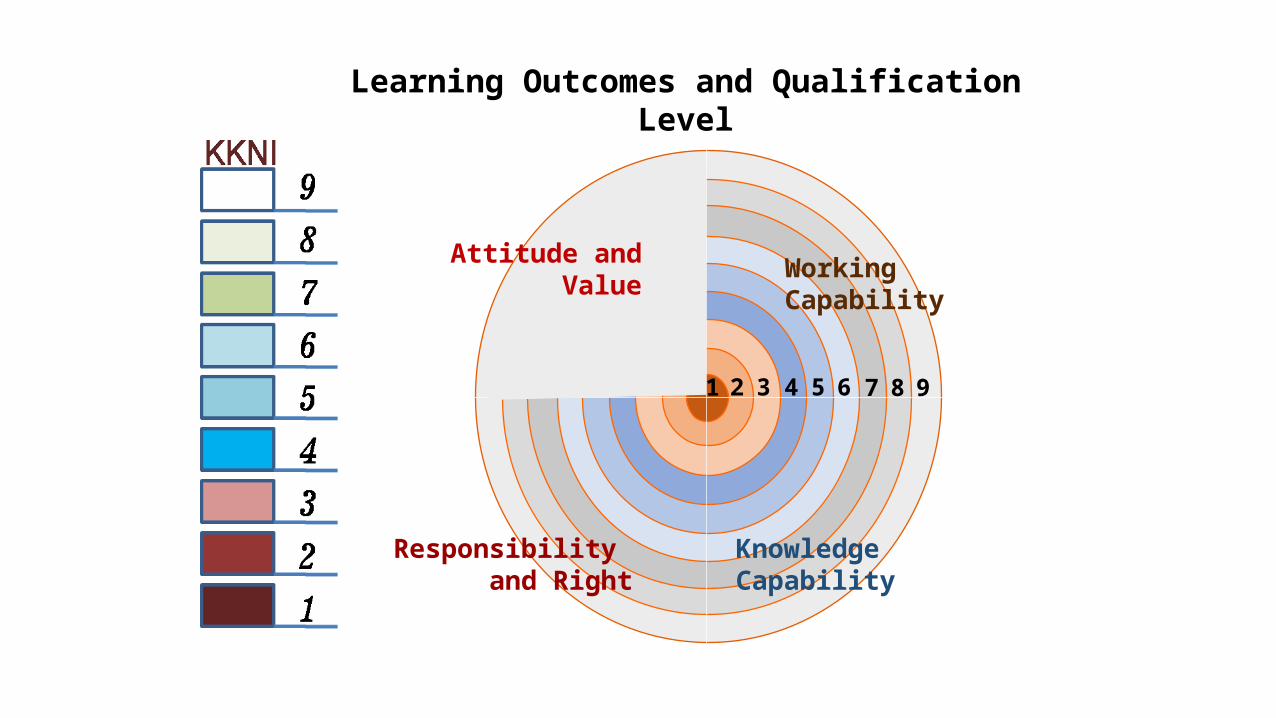

• NQF consists of 9 levels of qualification, from 1 to 9 level. Level 1 indictes the lowest and 9 is the highest

• Each Qualification Level indicates degree of learning outcomes derived from eduaction or training, both formal or informal

1

2

3

4

5

7

8

9

6

KKNI

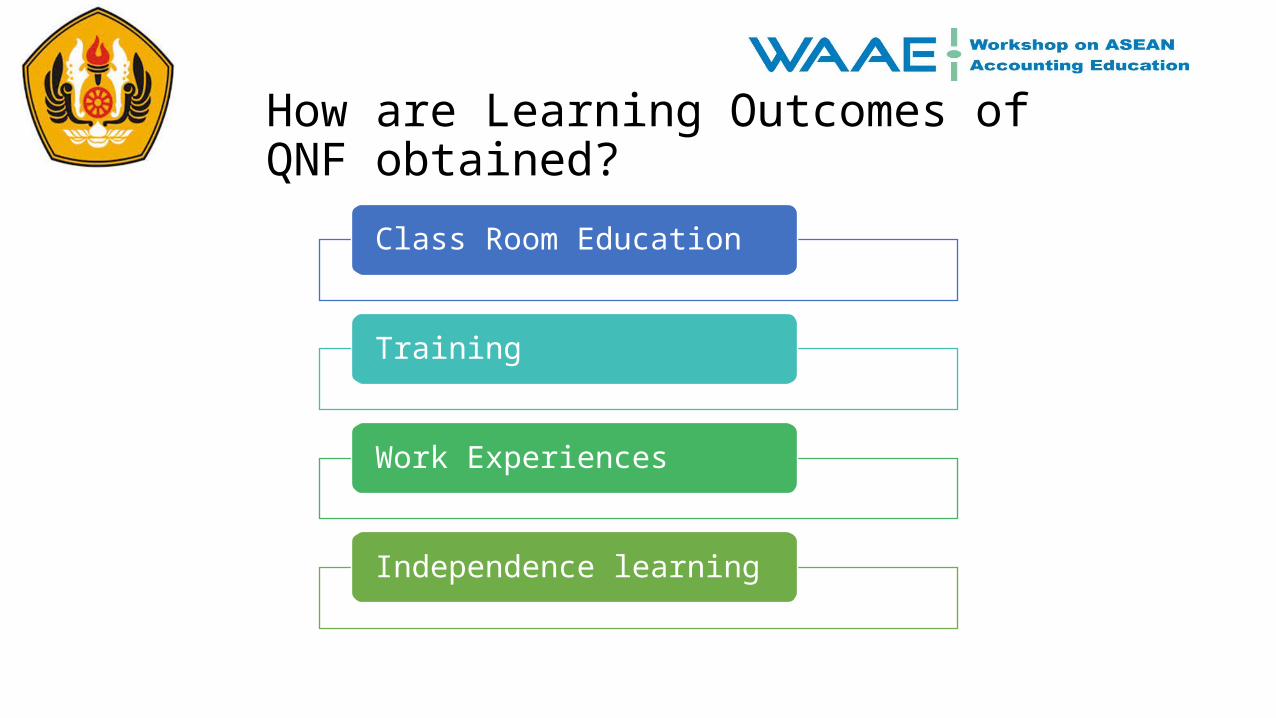

How are Learning Outcomes of QNF obtained?

Class Room Education

Training

Work Experiences

Independence learning

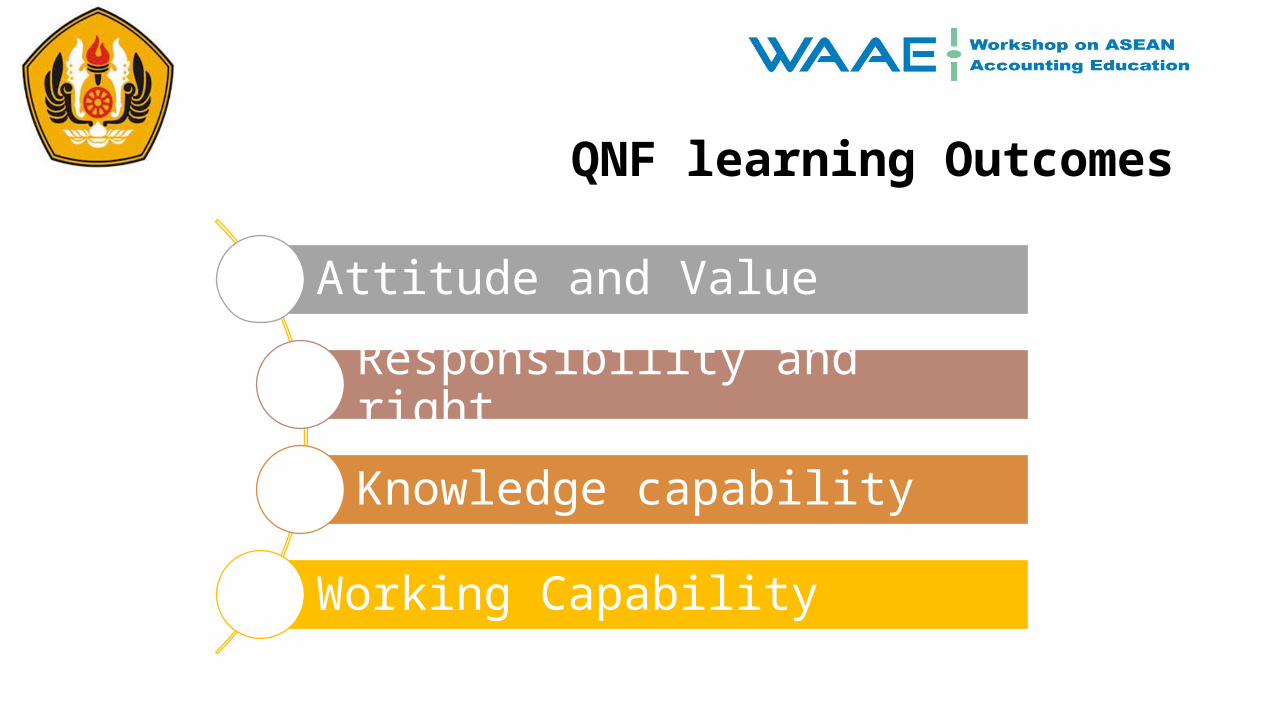

QNF learning Outcomes

Attitude and Value

Responsibility and right

Knowledge capability

Working Capability

Learning Outcomes and Qualification Level

1 2 3 4 5 6 7 8 9

Working Capability

Knowledge CapabilityResponsibility and Right

Attitude and Value

Profession :Certification

IndustryJob Position

Formal Education Academic Degree

Autodidact :Experience and Special Skill

Learning Outcomes Achievement: Various Path

SMP

SMA D1 D2 D3 S1 PR

O S2 S3

9

U 8

M D 7

M 6

5

4

3

2

1

OPERATOR ANALIS AHLI

International Education Standards

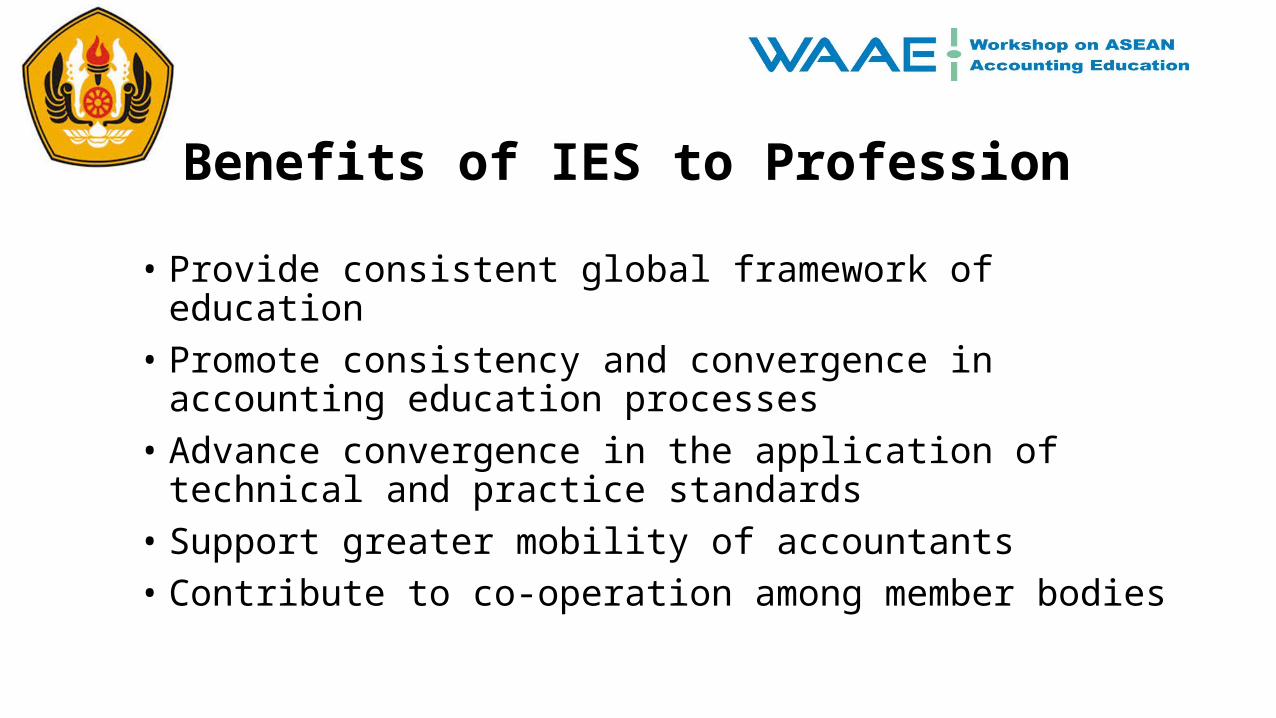

Benefits of IES to Profession

• Provide consistent global framework of education• Promote consistency and convergence in accounting education

processes• Advance convergence in the application of technical and practice

standards• Support greater mobility of accountants• Contribute to co-operation among member bodies

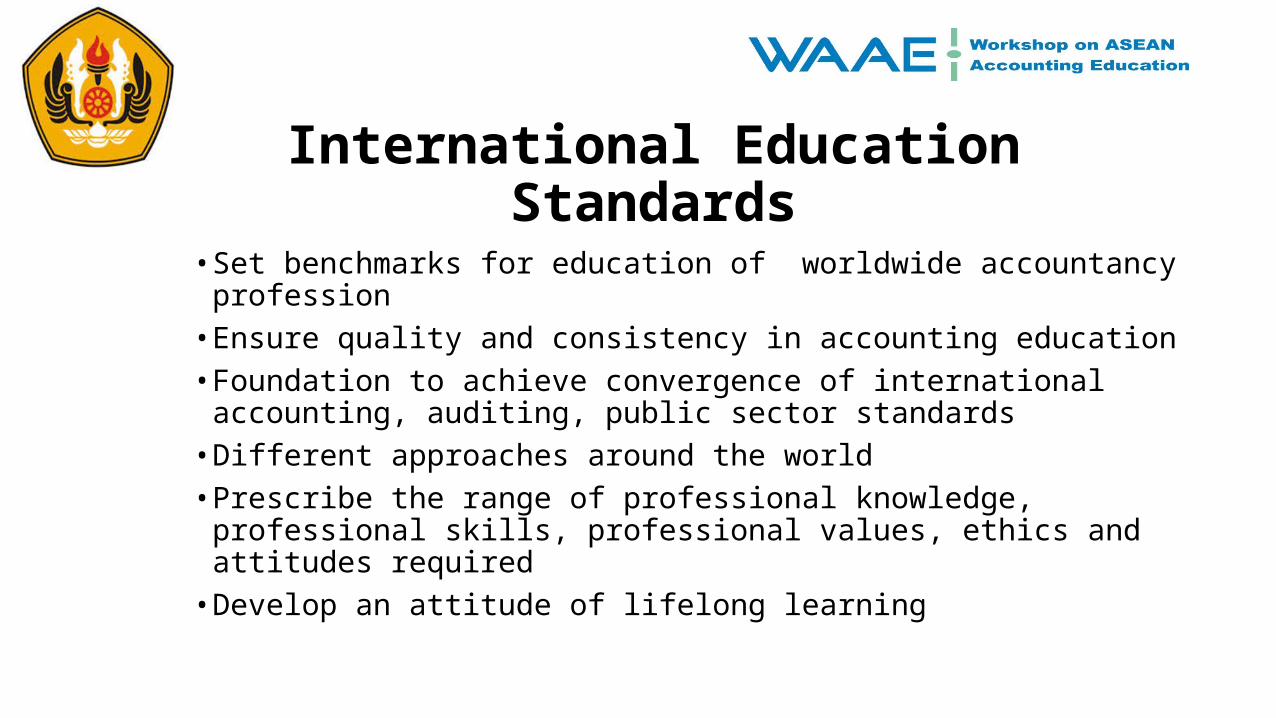

International Education Standards

• Set benchmarks for education of worldwide accountancy profession

• Ensure quality and consistency in accounting education• Foundation to achieve convergence of international accounting,

auditing, public sector standards• Different approaches around the world• Prescribe the range of professional knowledge, professional skills,

professional values, ethics and attitudes required• Develop an attitude of lifelong learning

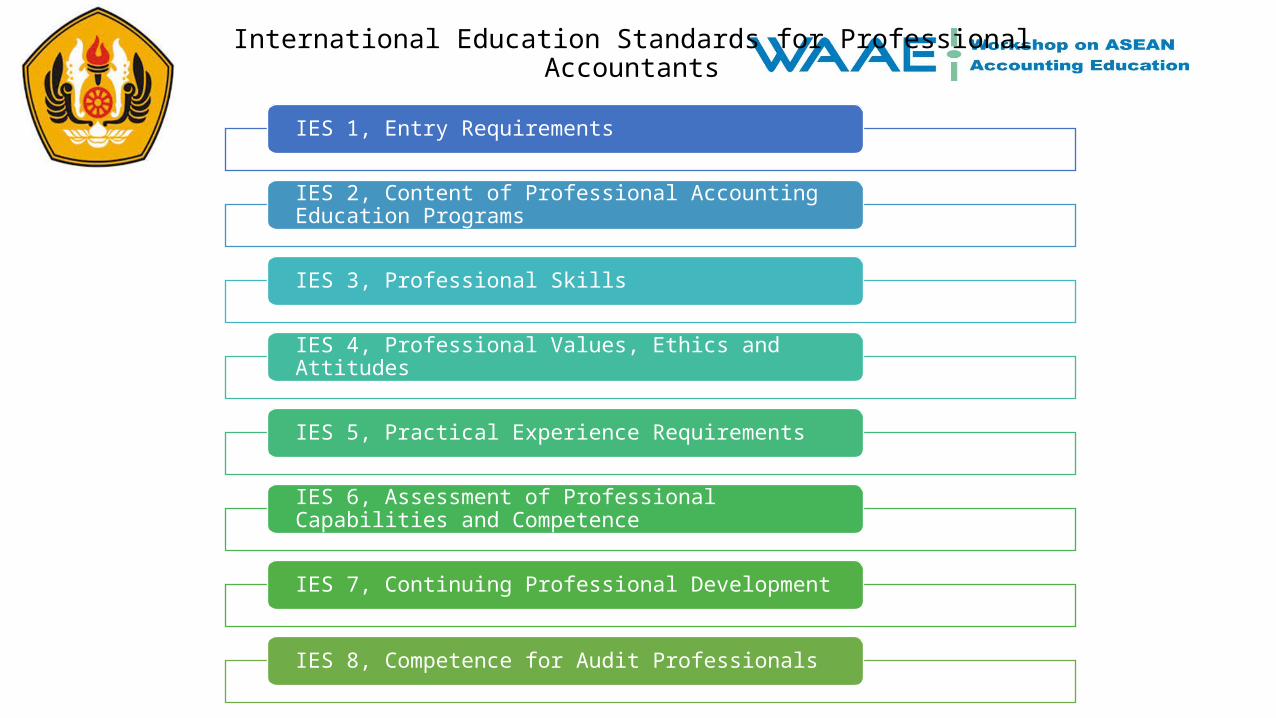

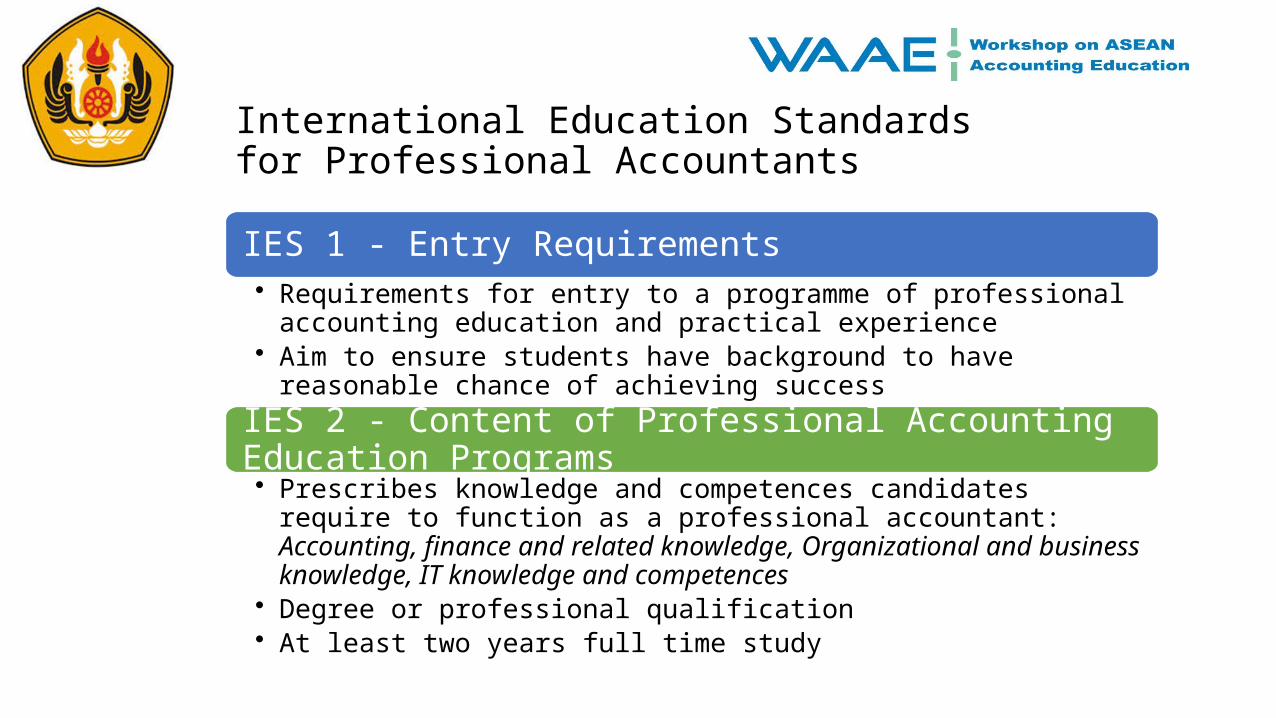

International Education Standards for Professional Accountants

IES 1, Entry Requirements

IES 2, Content of Professional Accounting Education Programs

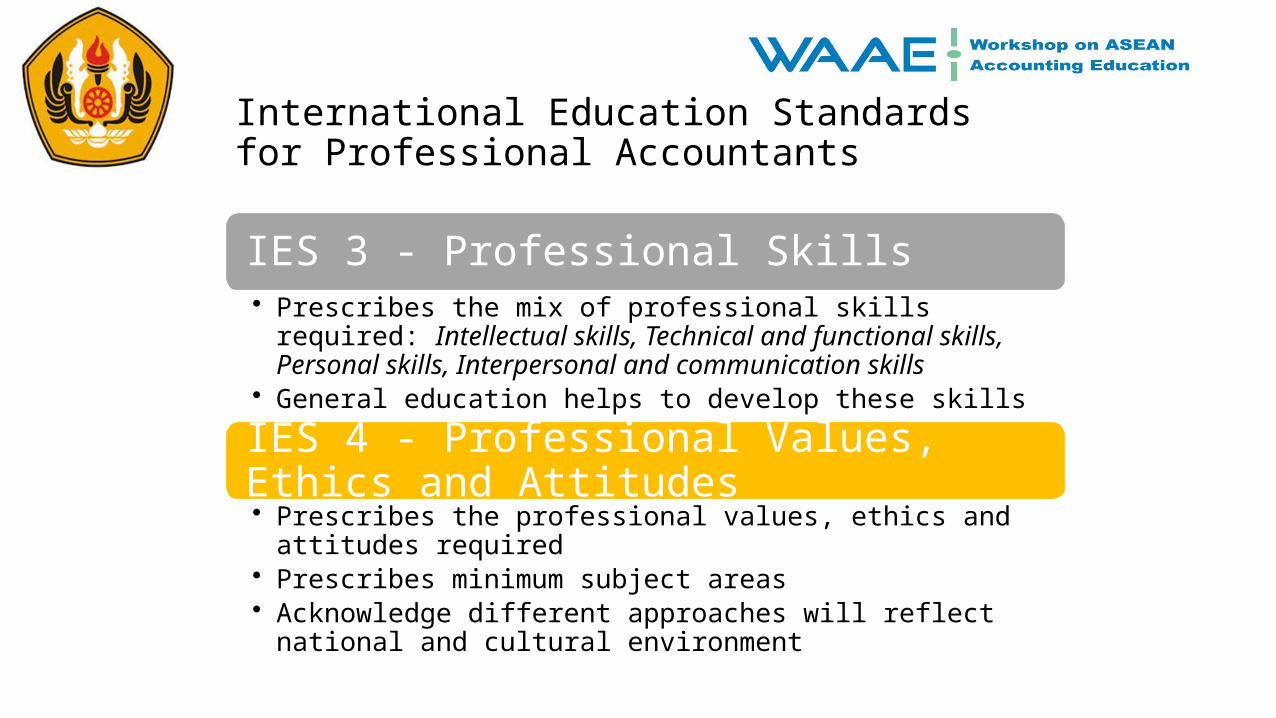

IES 3, Professional Skills

IES 4, Professional Values, Ethics and Attitudes

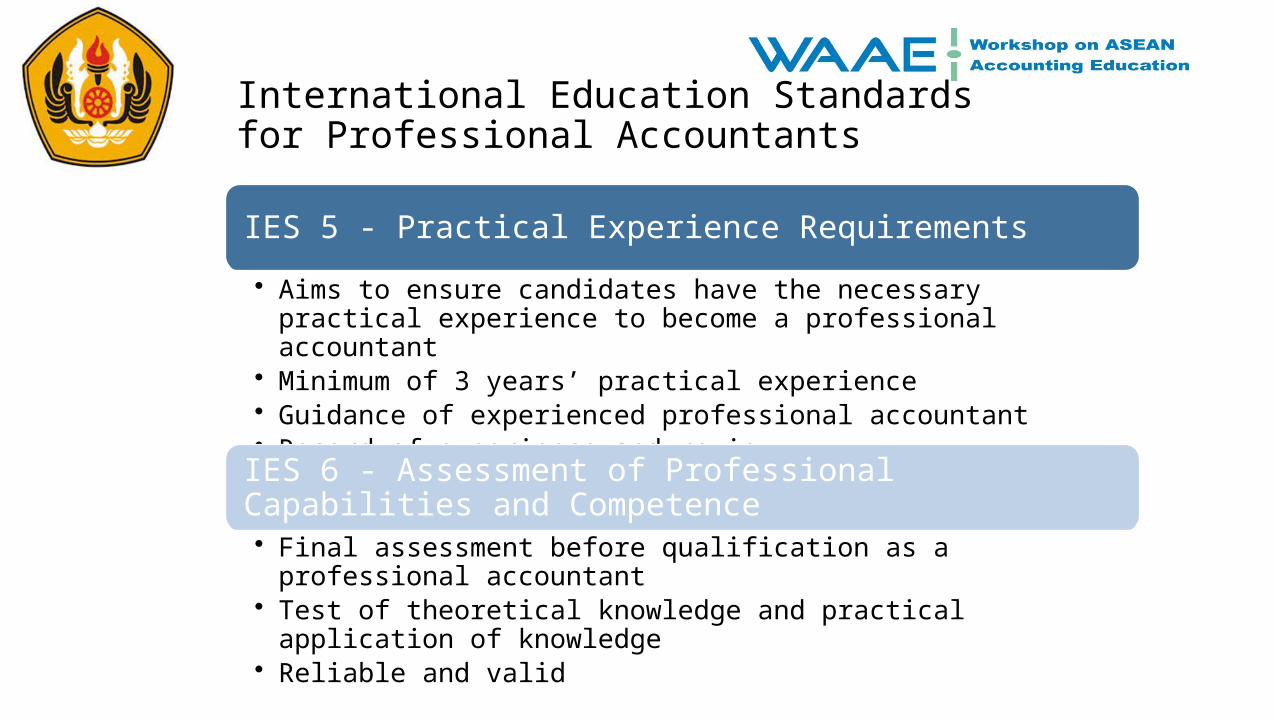

IES 5, Practical Experience Requirements

IES 6, Assessment of Professional Capabilities and Competence

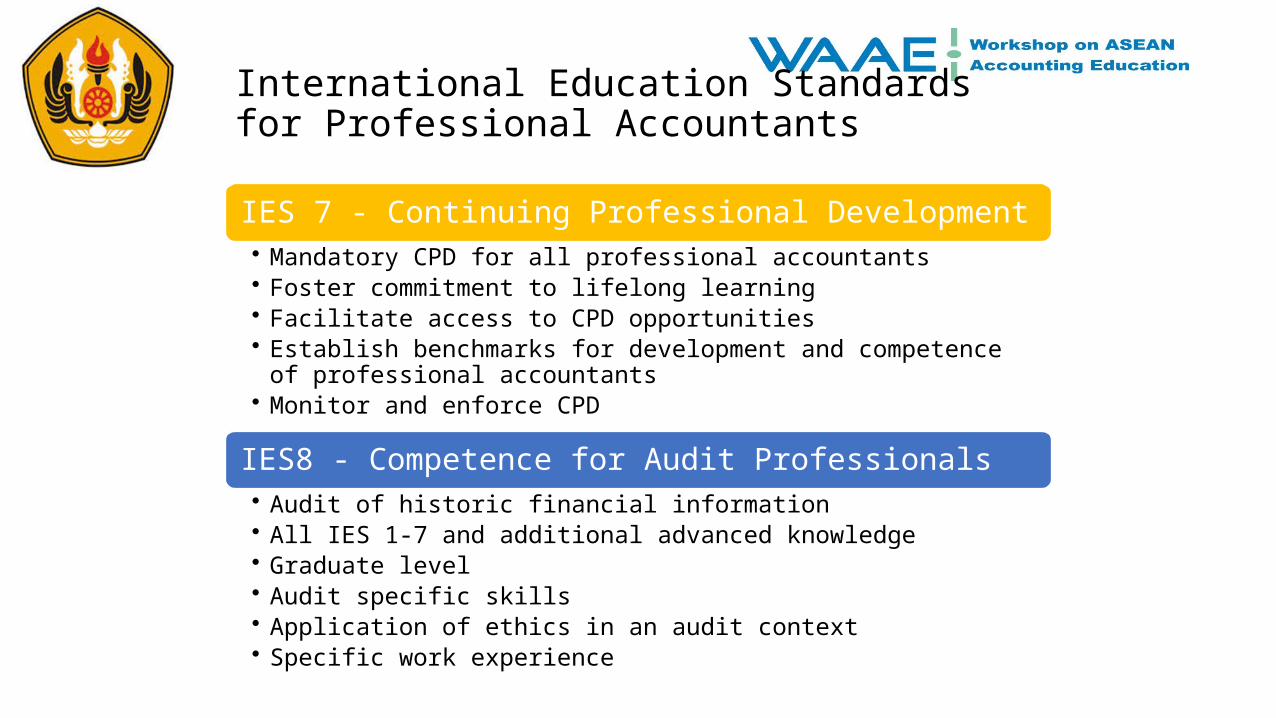

IES 7, Continuing Professional Development

IES 8, Competence for Audit Professionals

International Education Standards for Professional Accountants

IES 1 - Entry Requirements• Requirements for entry to a programme of professional accounting education

and practical experience• Aim to ensure students have background to have reasonable chance of

achieving success

IES 2 - Content of Professional Accounting Education Programs• Prescribes knowledge and competences candidates require to function as a

professional accountant: Accounting, finance and related knowledge, Organizational and business knowledge, IT knowledge and competences

• Degree or professional qualification • At least two years full time study

International Education Standards for Professional Accountants

IES 3 - Professional Skills• Prescribes the mix of professional skills required: Intellectual skills,

Technical and functional skills, Personal skills, Interpersonal and communication skills

• General education helps to develop these skills

IES 4 - Professional Values, Ethics and Attitudes• Prescribes the professional values, ethics and attitudes required• Prescribes minimum subject areas• Acknowledge different approaches will reflect national and cultural

environment

International Education Standards for Professional Accountants

IES 5 - Practical Experience Requirements

• Aims to ensure candidates have the necessary practical experience to become a professional accountant

• Minimum of 3 years’ practical experience• Guidance of experienced professional accountant• Record of experience and review

IES 6 - Assessment of Professional Capabilities and Competence

• Final assessment before qualification as a professional accountant• Test of theoretical knowledge and practical application of knowledge• Reliable and valid

International Education Standards for Professional Accountants

IES 7 - Continuing Professional Development• Mandatory CPD for all professional accountants• Foster commitment to lifelong learning• Facilitate access to CPD opportunities • Establish benchmarks for development and competence of professional

accountants• Monitor and enforce CPD

IES8 - Competence for Audit Professionals• Audit of historic financial information• All IES 1-7 and additional advanced knowledge• Graduate level• Audit specific skills• Application of ethics in an audit context• Specific work experience

Compliance on IES - IFAC Curriculum Standard

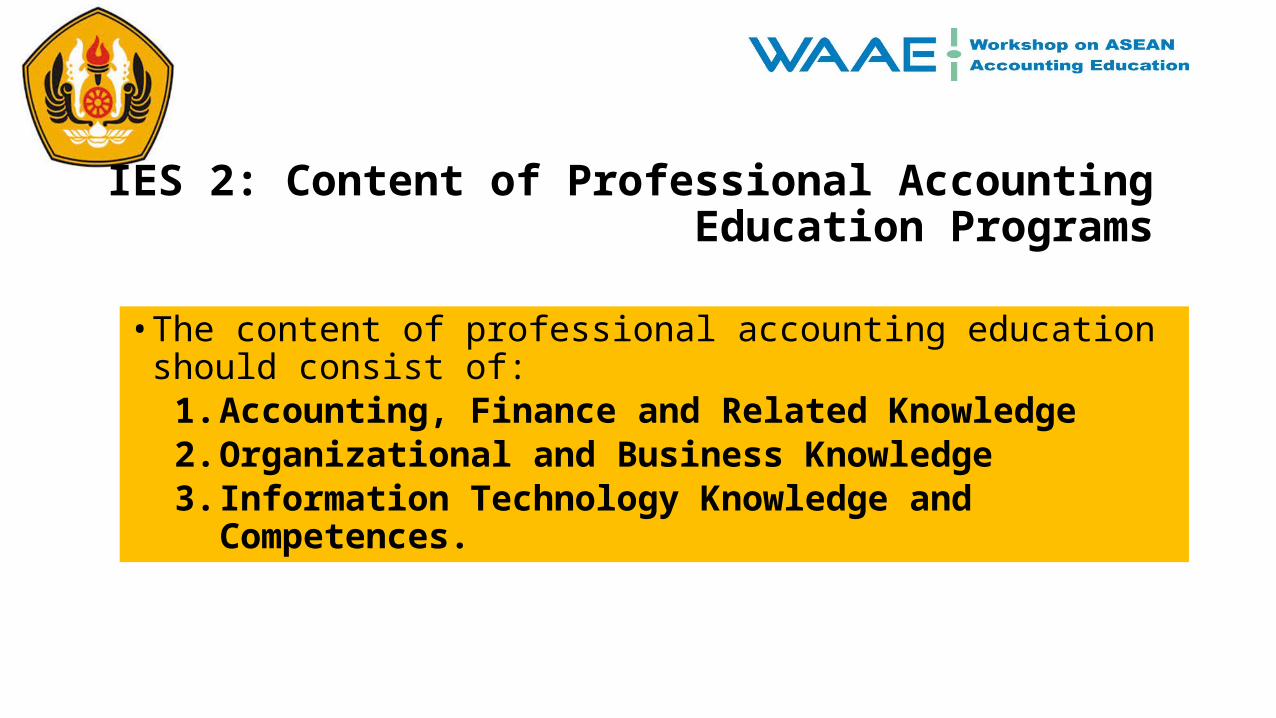

IES 2: Content of Professional Accounting Education Programs

• The content of professional accounting education should consist of:1. Accounting, Finance and Related Knowledge2. Organizational and Business Knowledge 3. Information Technology Knowledge and Competences.

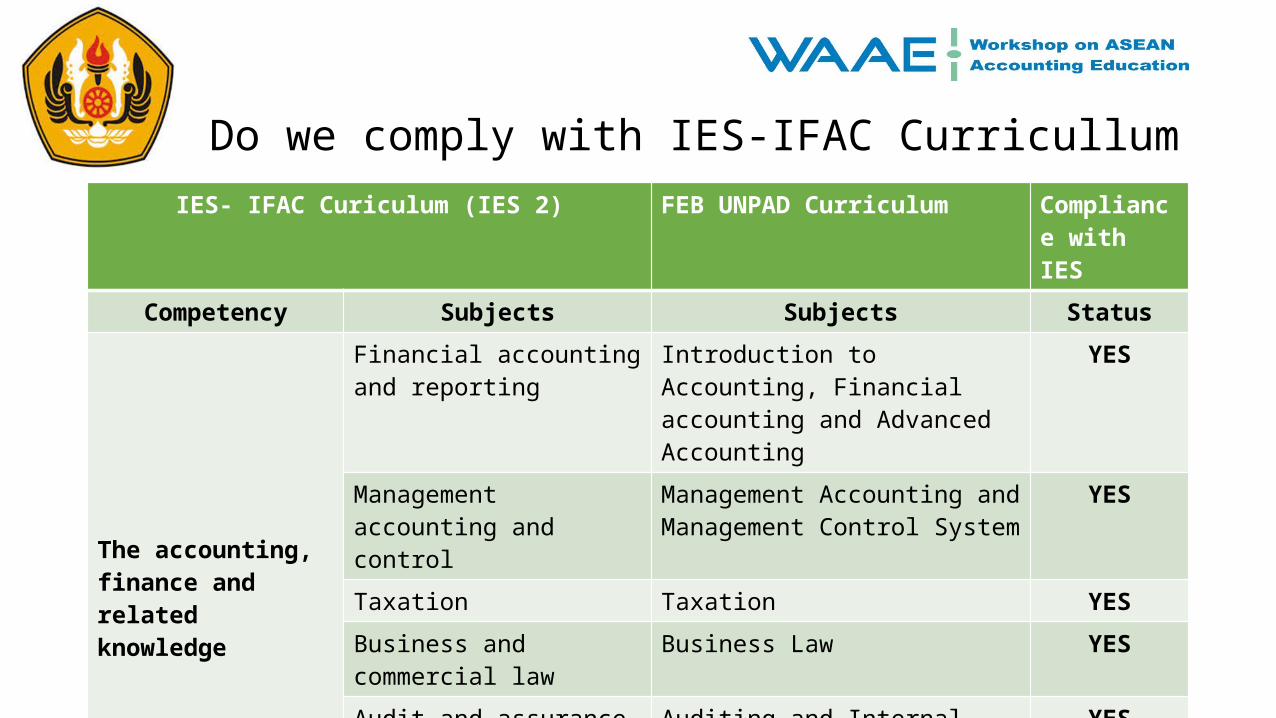

Do we comply with IES-IFAC CurricullumIES- IFAC Curiculum (IES 2) FEB UNPAD Curriculum Compliance

with IESCompetency Subjects Subjects Status

The accounting, finance and related knowledge

Financial accounting and reporting

Introduction to Accounting, Financial accounting and Advanced Accounting

YES

Management accounting and control

Management Accounting and Management Control System

YES

Taxation Taxation YES

Business and commercial law Business Law YES

Audit and assurance Auditing and Internal Audit YES

Finance and financial management

Financial Management and Advanced Financial Management

YES

Professional values and ethics

Business Ethic and Profession YES

How do we comply with IES-IFAC CurricullumIES- IFAC Curicullum (IES 2) FEB UNPAD Curicullum Compliance with

IESCompetency Subjects Subjects Status

The organizational and business knowledge

Economics Introduction to Micro and Introduction Macro Economics

YES

Business environment Introduction to Business YES

Corporate governance N/A NOT YET

Business ethics Business Ethics and Profession YES

Financial markets Financial Management YES

Quantitative methods Quantitative Method YES

Organizational behavior Organizational behavior ( Elective) YES

Management and strategic decision making

Introduction to Management and Strategic Management

YES

Marketing Marketing (Elective) YES

International business and globalization

International Trade (elective) YES

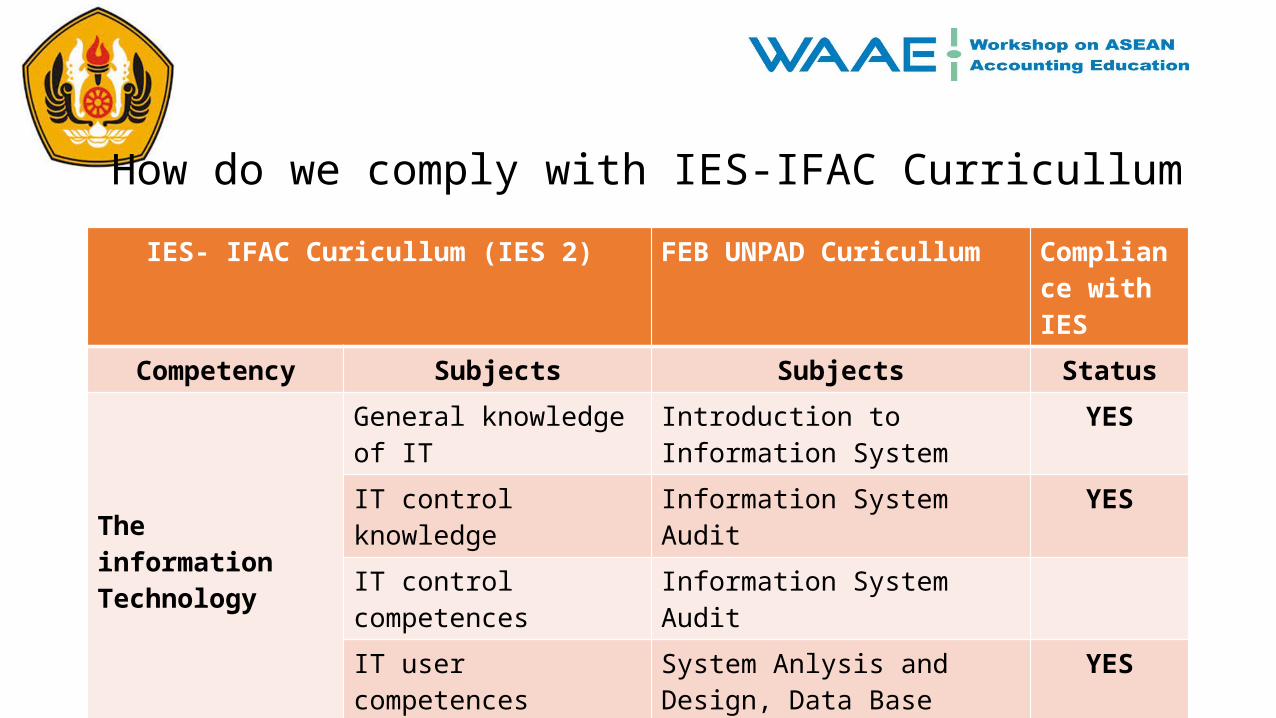

How do we comply with IES-IFAC Curricullum

IES- IFAC Curicullum (IES 2) FEB UNPAD Curicullum Compliance with IES

Competency Subjects Subjects Status

The information Technology

General knowledge of IT Introduction to Information System

YES

IT control knowledge Information System Audit YESIT control competences Information System AuditIT user competences System Anlysis and Design, Data

Base Management Syestem, Management Information System

YES

The ASEAN Economic Community (AEC):

Opportunities and Challenges

About AEC

• The ASEAN Economic Community (AEC), a regional initiative designed to transform Southeast Asia into a more unified and competitive market zone

• Determined to achieve higher levels of economic dynamism, sustained prosperity, inclusive growth and integrated development of ASEAN

• The AEC includes the 10 ASEAN countries: Singapore, Philippines, Malaysia, Thailand, Indonesia, Vietnam, Laos, Cambodia, Brunei, and Myanmar

AEC 4 Pillars

1. Creation of a single production and market zone.• All Southeast Asian states retain national sovereignty but eliminate virtually all

tariffs and open their borders to a much freer flow of trade, capital, investment and labor.

2. Enhancing the economic competitiveness of the region• various measures designed to promote ease of doing business, including

infrastructure development projects, better consumer rights and IP laws, and policies designed to foster competition.

3. Promoting equal economic development • policies that are designed to bridge the development gap between the countries

richest and poorest members.

4. Enhancing integration into the world economy• free trade agreements with external powers.

AEC: Opportunities

• Foreign Direct Investment (FDI)• ASEAN offers a huge market• Labour forces markets• Development of production networks• Allowing ASEAN to become central to global supply chains. • Transaction costs reduction, due to simplification, harmoniziation,

and standardization trade and customs processes and procedures

AEC : Challenges• Competitive advantages of business entities ( Productivity,

Efficiency, Quality)• International standard of human capital qualifications• fears relating to immigration and cultural impacts.• free trade in goods and services• Mobility of skilled labor

Thank You for your Attention

Question and Answer Session