presentation by roberto boer

TRANSCRIPT

Business Opportunity Tasman (H)REE Mine Sweden or what other (policy) option remains?

Roberto Boer Advisor Business Development

!

Economic Security and Raw Materials in Europe 30-01-2015

2

!”Advisor”!!- Over 20 years 200 Business development projects. Fair share as executive officer, always with a Procurement approach.!- Agriculture, Petrochemical Industry, Internet & E- Commerce and Raw materials;- What have all in common?: Each of those projects ment finding parties that were willing to communicate and collaborate.!So basically I am building bridges between parties (analyses & communication)!!The following ingredients brings me before you today:!Oct 2007: Financial system is broken. (which is another topic) but concluded; Crisis for at least 10 to 20 years meaning on average each ones wealth will decrease during each of those years.!!Made me refocus as a hobby project to raw materials, simply looking and scarcity. Where Supply and Demand were most out of balance. Which brought me to REE sector.!!Followed the most promising companies on a daily basis as off 2009. !!Living in Industrialized Rotterdam Area (Europoort - Botlek) I witnessed and took part of disappearing labour. From West to East.!!Long story short: I as a person (not as CEO of Petrochem) was and still am very concerned about our way of life and prosperity and our children's future. And was dismayed by initial reactions from former colleague CPO’s and others. Therefor I contacted/advised organizations like VNO-NCW, HCSS, FME, VNMI as well as Ministry of Foreign Affairs, Ministry of Economical Affairs. Due to the outcome of my personal analyses I also do advise Tasman Metals Ltd.!!!

One of our Challenges at hand

Will the EU act as well and secure its ‘own’ 40 years supply of the 11 most critical metals or be dependent of China dominance? ERECON: „Encourage the development of new mines and refineries in Europe, in particular for heavy rare earth elements” Price tag: One Boeing A380 Facts show there that Tasman deposit is the only logical location; ranked first as to:

1. Geological, 2. Geographical, 3. Mineable, 4. Financial.

China just continues its proven policy of total world dominance on these metals.

Chinese policy after 2013

source Roberto Boer

• WTO Ruling! To bad: has been circumvented swiftly by introducing „strict export license” requirements…

• Participations in several REE locations, NOT because they are economical viable, but ”just” taken off the market.

• A non-binding MOU Kvanjefeld. • Chinese Mining Co & China Investment Group contact Tasman.p.s. no China bashing: What if we had over 1.3 Billion people to feed?

-source Roberto Boer

source Roberto Boer

EU demand 2020-2030

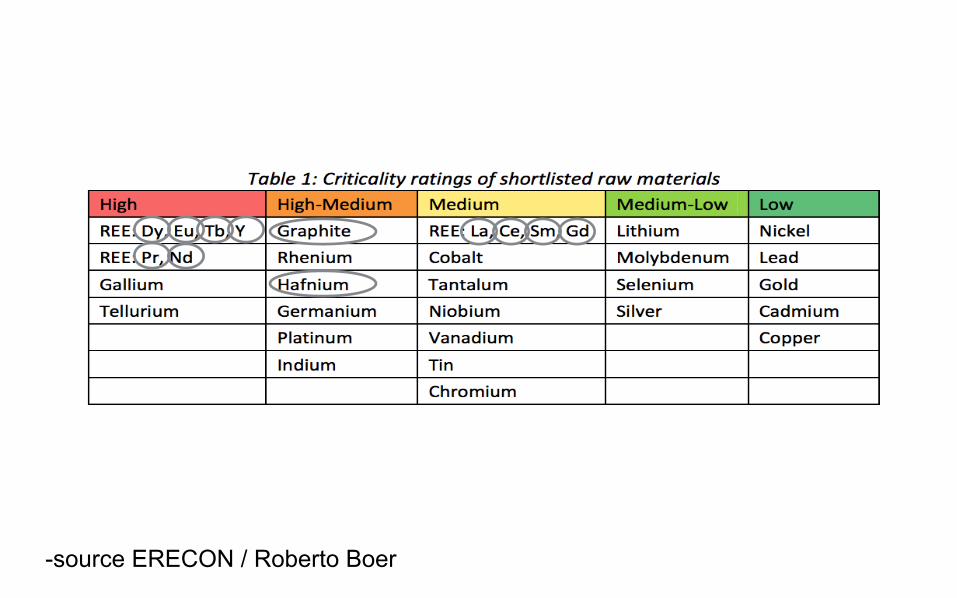

-source ERECON / Roberto Boer

-source ERECON / Roberto Boer

10

11

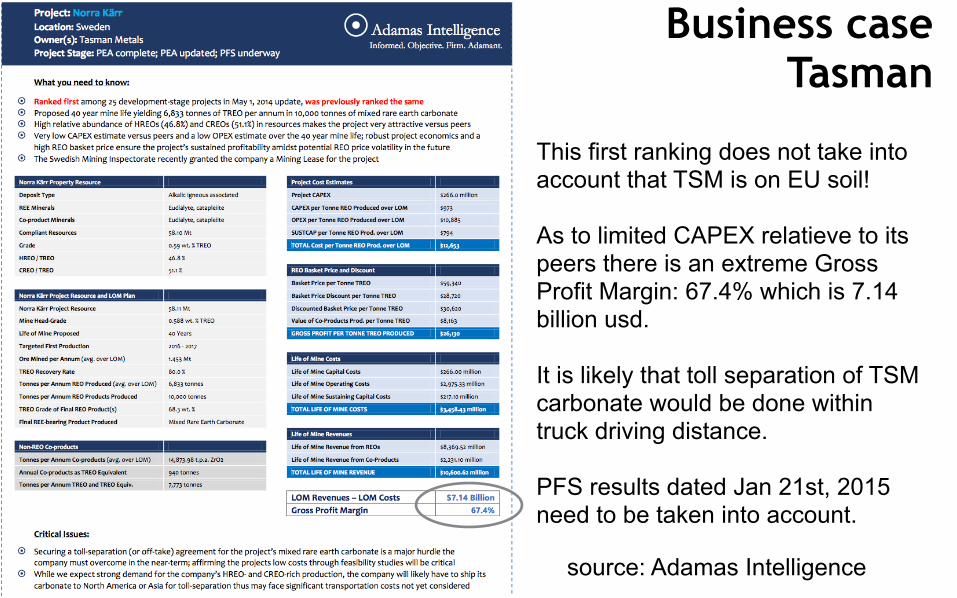

Business case Tasman

This first ranking does not take into account that TSM is on EU soil!As to limited CAPEX relatieve to its peers there is an extreme Gross Profit Margin: 67.4% which is 7.14 billion usd. It is likely that toll separation of TSM carbonate would be done within truck driving distance. !PFS results dated Jan 21st, 2015 need to be taken into account.

source: Adamas Intelligence

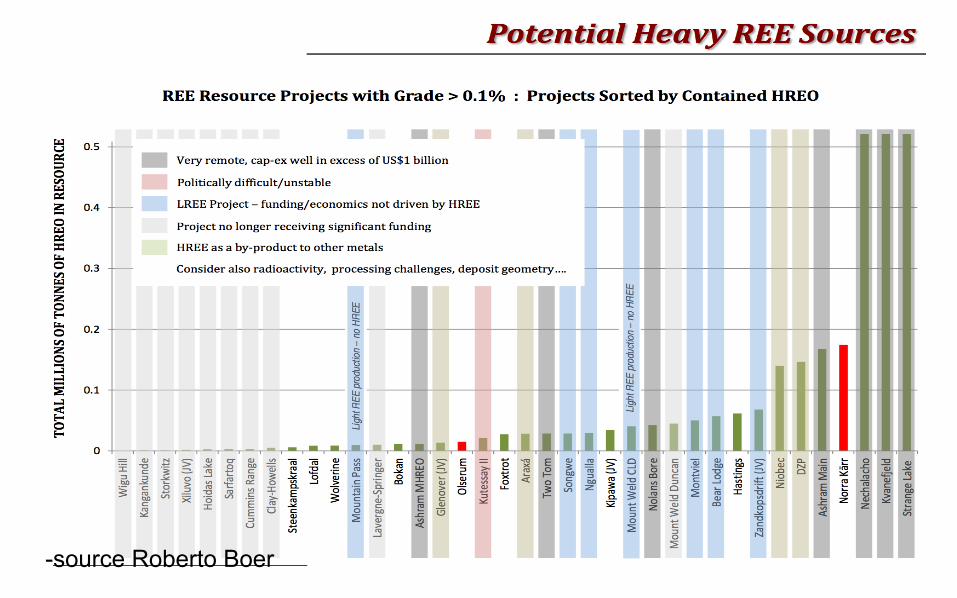

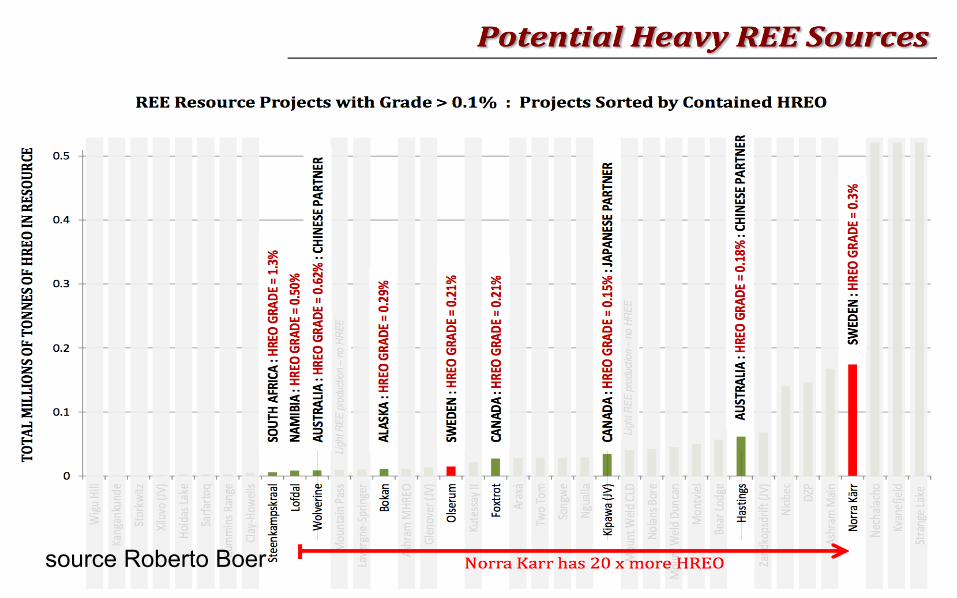

Comparison show that the only resource within Europe is also globally ranked in first position

* source Roberto Boer

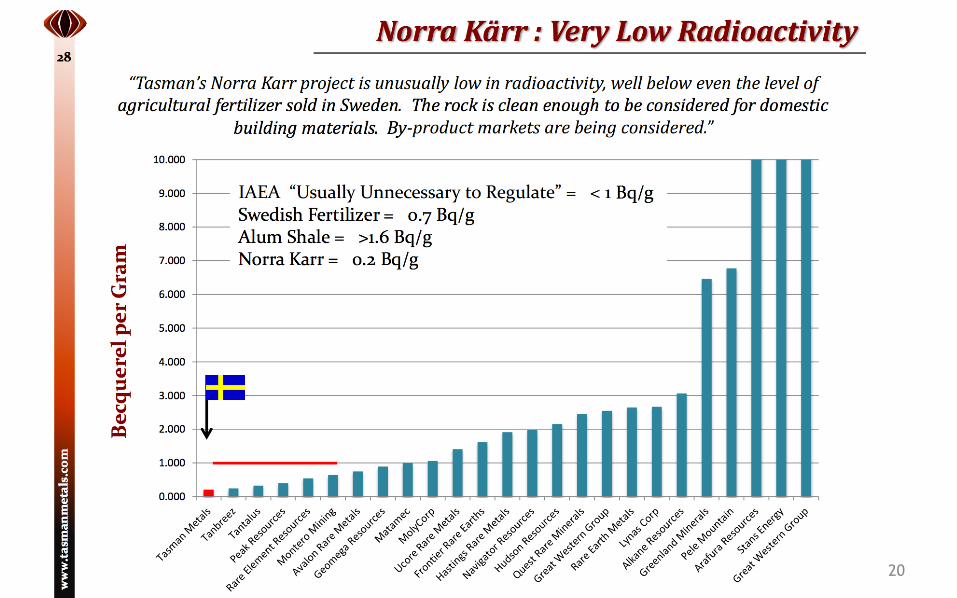

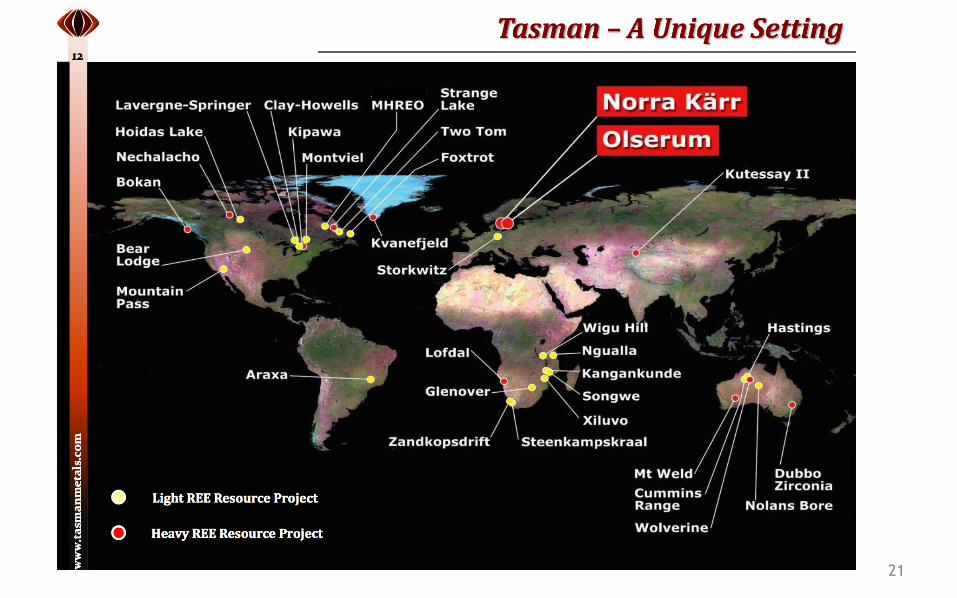

- Capex not a billion USD but 378 million USD (PFS) - the highest percentage of Heavy’s REE (0.61%),- Norra Karr is 10x the grade of Chinese source - the least radioactive material, (no requirements needed) - simple open pit mining (300x800mtrs),- only 500 meters next to existing highway, - within the mining friendly and stable country of Sweden, - with skilled local workforce, - Transport of the ores by Truck to the only Western separation company (Solvay) or to alternatives. - EU is best positioned to have a Western Supply Chain

Why no action taken yet?

-source Roberto Boer

• Exploration and Mining are a lost EU expertise!=> e.g. Procurement is well organized: Multi sourced & Just In Time

• Focus is primary on Price and secondary on TCO (=Availability)=> Risking closure - Transfer from West to East

• These metals are found ”glued together” => Not one company needs all. (Alexander Pulkert: Siemens does)

• Extreme Prices differences from 5 usd to 900 usd per kilo!! => Who needs what in which quantity and against which willingness to invest in the lost expertise of Exploration/Mining?

Result?

-source Roberto Boer

Mr. Shaun Bunn, Managing Director of Greenland Minerals and Energy Ltd, stated during ERECON final conference: “For a long period of 6 years we (Greenland Minerals and Energy/Kvanjefeld) invested in meeting and talking to all relevant Western/European Companies and Governments, including the EC. We tried to find interest in our project and its resources and we could not find any. We have spoken to GE, to Siemens, etc, etc, etc. None of them made concrete steps. The only people that are and were willing to come to us - and we didn’t even wanted them - are the Chinese. So our project is now under Chinese control. I know that you all are not happy, but I am happy.”

Final conclusion:

-source Roberto Boer

1) If we keep on analyzing there is no EU option left to choose. 2) Any single multinational can secure the Norra Karr site => but who is first? So far: None.3) EU Politics: ”not picking between winners and losers” => Disagree. One option means: We either take EU’s option or leave it for someone else.4) Who still believes in free markets? Not hoping, but truly Believing and at real stakes. 5) TSM needs is pocket money is some parts of the World. Expect that it will be provided. EU or Non EU. !Summary: EU corporations compete against Governmental bodies with Strategy and Investments! At stake is not a 4 billion (H)REO market but labour for several hundred thousand people*. Let’s keep them in the West. (* source: e.g. CREEN and Canadian Parliament)Government (e.g. Dutch - German - Sweden) need to step in. Hopefully joined by a handful multinationals. Initial investment is limited but should be aimed at building a mine / production!

Substitution & Recycling are certainly important but not enough. !We all get the future we deserve.

Contact information

Roberto A. Boer CEO Petrochem Group today spoken to you as private person aka Advisor !Happy to discuss to any one off you. Do your own due diligence to check my analysis and if you do, do it quickly.

+31 6 51 06 43 69 [email protected] !Visiting and Postal Address: Kerkweg 1, 3181 AK RozenburgP.O. Box 1156, 3180 AD Rozenburg The Netherlands

18

19

20

21

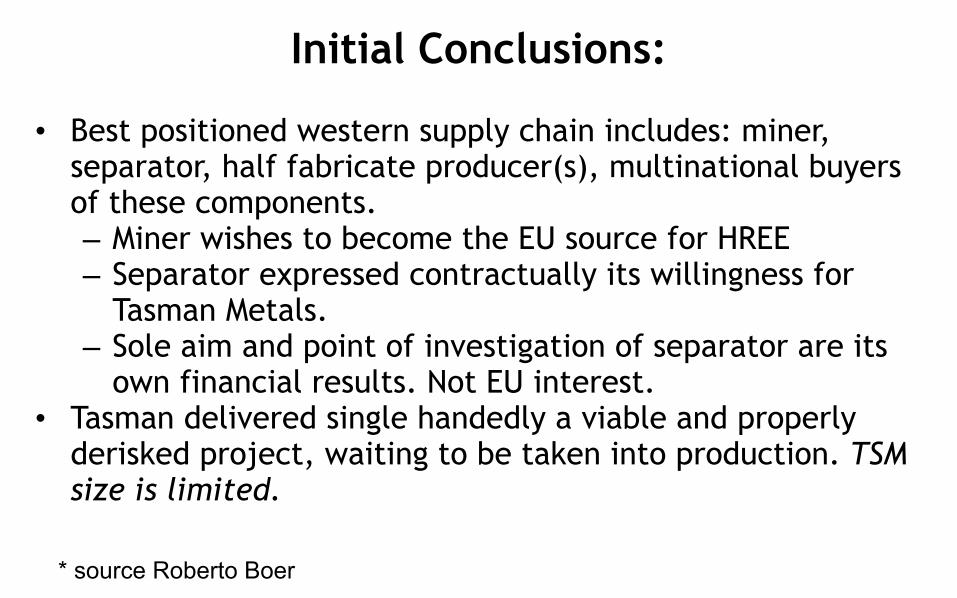

Initial Conclusions:

* source Roberto Boer

• Best positioned western supply chain includes: miner, separator, half fabricate producer(s), multinational buyers of these components. – Miner wishes to become the EU source for HREE – Separator expressed contractually its willingness for

Tasman Metals. – Sole aim and point of investigation of separator are its

own financial results. Not EU interest. • Tasman delivered single handedly a viable and properly

derisked project, waiting to be taken into production. TSM size is limited.