preliminary results 2003 - cobham plc · preliminary results 2003 18 march 2004. ... avionics £83m...

TRANSCRIPT

Preliminary Results 2003

18 March 2004

Summary Profit and Loss Account

Orders

UnauditedYear to

31/12/03£m

Year to31/12/02

£mGrowth

Gross Profit

Margin

Operating profit

925.0672.7 37.5%

248.1211.7 17.2%

29.8%28.8% 1.0 pts

149.3125.5 19.0%

Turnover 832.6734.6 13.3%

Margin 17.9%17.1% 0.8 pts

Profit before taxation 137.8115.3 19.5%

All excluding integration costs, goodwill amortisation and exceptional loss on Westwind disposal

SSAP 24 Basis

Turnover and Profit by DivisionSSAP 24 Basis

2002 2003 % Growth 2002 2003 % Growth

Aerospace Systems 292.8 319.7 9.2% 55.8 67.8 21.5%

Avionics 251.5 316.1 25.7% 51.9 60.8 17.1%

Flight Operations and Services 174.8 179.7 2.8% 19.3 21.9 13.5%

Core Businesses 719.1 815.5 13.4% 127.0 150.5 18.5%

Westwind (now sold) 15.5 17.1 (1.5) (1.2)

Cobham Group 734.6 832.6 13.3% 125.5 149.3 19.0%

Underlying Operating Profit excludes integration costs, amortisation and exceptional loss on Westwind disposal

Aerospace Systems includes group headquarters

Turnover Underlying Operating Profit

Shareholders’ Returns

Earnings per Share

UnauditedYear to

31/12/03Year to

31/12/02

- underlying 95.2p

- basic

- fully diluted

86.2p

70.4p

Tax rate*

Dividend per Share 25.60p

18.9p

28.16p

18.8p69.9p

26.6%24.1%

Growth

(73)%

(73)%

10.4%

10.0%

* Based on PBT before integration costs, goodwill amortisation and exceptional loss on Westwind disposal

SSAP 24 Basis

Cashflow

Depreciation and other movements

UnauditedYear to

31/12/03£m

Year to31/12/02

£m

(29.0)

75.4%88.6%

(8.6)

Underlying operating profit (ex. JV)

Dividends

50.5

(11.0)

(20.3)

(27.6)

(23.6)

Net cashflow from op. activities

CapexOperating cashflowOperating cashflow % of op. profit

Interest

Tax

Net cashflow from business

Acquisitions and Disposals

Other (2003 – Placing £104.6m)

Dec./(inc.) in net borrowings

144.1

3.7

(39.2)

147.8

49.7

(127.2)

111.9

120.6

15.3

135.9

108.6

(38.8)

7.2

106.9

(24.2)

18.9 34.4

Growth

1.6%

SSAP 24 basis

Net debt ratios

Net debt (£m)

UnauditedYear to

31/12/03Year to

31/12/02

Gearing

Net debt/ebitda* (12m trailing)

154.4188.8

29.4%52.6%

0.9 times1.24 times

Shareholders’ Funds (£m) 525.8359.2

* Excluding integration costs and exceptional loss on Westwind disposal

Growth

(18.2)%

46.4%

SSAP 24 Basis

Acquisition DetailCompany Activity Location

GPS Tracking North America

North AmericaPositioning Systems

Complex Composites

Audio Equipment

6

1

4

2

Xybion Sensor Positioning Sys (Mar)

Orion Electronics (Mar)

dB Systems (May)

Atlas Composites (May)

Acquisition cost (£m)

Avionics

Avionics

Avionics

Avionics

Division

North AmericaSpecialist Radio Beacons 1Novatech Designs (June) Avionics

GermanyOxygen components 20Dräger Aerospace (June) Aerospace SystemsAviation Oxygen

Systems 47Litton Life Support (August) Aerospace Systems

5Racal Antennas (August) Avionics UKAntennas

22SeaTel (Sept) Avionics Antennas

40ERA Technology (Sept) Avionics UKTechnology Services

167Avionics £83m Aerospace Systems £73m Flight Ops £11m

North America

UK

North America

North America

TAA (Oct)

Nauticast (Nov)

Stanley Harrison (Dec)

Flight Ops Freight Outsourcing Australia 11

Avionics Identification Systems Austria 2

Aerospace Systems Fluid Connectors USA 6

US$ Exposure and Hedging

2004 Major US $ Flows in UK and European Subsidiaries

CheltonChelton (Europe)ASGDräger 2004 Group Total $160m

Major Hedging Instruments

2004 $145m20052006 2004 Hedges = c. 90%2007 £ average = c. $1.592008 Euro average = c. $1.232009Each of 2010-12

$m 0 50 100 150

if dollar below c. $1.80

Summary

Strong growth in business, profit and margins

Excellent Q4

Cashflow increasing towards target 80%

Investment in acquisitions, new equipment and R&D

Confidence in the outlook

Overview

Progress made on implementation of strategic planSustained earnings growthOrganic and acquisitive growthOperationally effectiveBalanced portfolioCreate a positive working environment

Major successes in 2003 have included:Strong financial performance across groupRe-organisation aligned to customers and marketsIncreased footprint in USASuccessful placement in JulyAirTanker in negotiations with DPA on FSTA

Performance Profitable Growth Innovation

SalesOrders *Underlying Operating Profit

Results for 2003 (SSAP 24 basis)

2002 2003

925+37%+37%

2002 2003

125

2002 2003

£m

833

149

+19%+19%

+13%+13%673 735

* Before goodwill amortisation

Performance Profitable Growth Innovation

Turnover by Destination2002 - £734.6m

Other EU 17%

RoW 28%

UK 24%

USA 31%Other EU 19%

RoW 23%

UK 22%

USA 36%

2003 - £832.6m

Performance Profitable Growth Innovation

Full Year Turnover Analysis

2002 - £734.6m

Commercial17%

Military 49%Other

34%

2003 - £832.6m

Commercial16%

Military 50%Other

34%

Performance Profitable Growth Innovation

COBHAM PLC

Aerospace Systems38%

Avionics38%

Flight Operations22%

Business Structure

Fluid and airdistribution

Countermeasures

Refuelling and Auxiliary mission equipment

Life Support

Antennas and EM Technologies

Composites

Avionics

Microwave

Flight Operations

Outsourced Aviation

Aviation Support

Aerospace SystemsReorganised in August 2003 to support customers and marketsLife Support has grown from £50m to £120m in two yearsContinued success, worldwide, on core AR programmesStrong and growing order book – particularly in USAExcellent position in niche marketsWon SDB sub-contract from Boeing - $13m; potential $160mWon £23m contract for IR Countermeasures for BAE SYSTEMSFirst order from USN for IR Countermeasures in TennesseeReceived orders from Boeing, BA, AF and JAL for B747 replacement pumpsKey business drivers are:

US Defence spendBranding in key marketsExploitation of core technologies

Commercial aerospace market growthCost base

Growth 9%Aerospace

Systems2003 Sales - £320m

Growth 7% Growth 41% Growth 6% Growth 35%

2003 Sales - £14m 2003 Sales - £102m 2003 Sales - £97m

Fluid and airdistribution Countermeasures Life Support

Refuelling andauxiliary mission

equipment

Aerospace Systems

2003 Sales - £129m

Excludes intergroup eliminations

AvionicsExcellent financial results in 2003Strong order intake, boosted by acquisitionsGrowing footprint in USARotary wing programmes offer best growth prospectsIncreased involvement in homeland securityImplementation of acquisition strategyBusiness drivers are:

Strength of US defence budgetAbility to address market opportunities in USProgramme and technology captureFurther consolidation opportunitiesAfter marketRotary wing market

Avionics(Chelton)

Antenna andEM Technologies Composites MicrowaveAvionics

Avionics

Growth 51% Growth 9% Growth 23% Growth 6%

2003 Sales - £36m 2003 Sales - £112m 2003 Sales - £104m2003 Sales - £103m

Excludes intergroup eliminations

Growth 26%

2003 Sales - £316m

Flight OperationsUnderlying operating profit improved by 12%Order book strengthened with some major programme winsAustralian Air Express (AaE) A$100m contract extension to 2010First two Proline IV upgrades completed for UK020 contractBusiness drivers are:

Long term contract opportunitiesExtending existing contractsNo.1 position on UK EW military trainingStrategic partnerships with key OEMsResource growth in AustraliaFurther opportunities for training and PFI outsourcingFSTA

Flight Operationsand Services

(FR Aviation)

Flight Operations Outsourced AviationServices Aviation Support

Flight Operations

Growth (5%) Growth 5% Growth (2%)

2003 Sales - £115m 2003 Sales - £17m2003 Sales - £63m

Excludes intergroup eliminations

Growth 3%

2003 Sales - £180m

FSTA

Monday, 26 January, AirTanker was judged by the MoD to offer the “best prospect of securing a value for money PFI service”Cobham has a 25% share in the AirTanker consortiumWe are currently working with the DPA to satisfy outstanding questions surrounding the bidNegotiations will continue until we agree on a contract with the DPA. This could take a further 15 months.The Cobham companies which would benefit from the AirTanker selection are:

Aerospace Systems Group – ARChelton Avionics – AntennasFR Aviation – Conversion and support

Areas for future growth

Increased footprint in USANetwork Enabled CapabilityUAV/UCAV platformsHomeland securityFurther consolidation of supply chainStrength in market nichesFurther outsourcing contracts

SummaryAnother set of outstanding resultsNew orders, including acquisitions, increased by 37% over 2002Successful acquisition of 13 companiesLong term strategy continues to prove successfulEstablished as the potential preferred bidder on FSTAOrganic growth has been 8% in 2003Balanced portfolio of products/technologiesConfidence in the outlook

Appendix

Aerospace Systems

Fluid and airdistribution

FR-HiTEMP

Stanley Aviation

Stanley Harrison

Cobham Fluid Systems

Countermeasures

Wallop Defence

FR Countermeasures

Life Support

Carleton

Carleton Life Support

Dräger

Conax

Refuelling andauxiliary mission

equipment

Flight Refuelling

Sargent Fletcher

Aerospace Systems

Fluid and airdistribution Countermeasures Life Support

Refuelling andAuxiliary mission

equipment

AircraftFuel systemsFuel pumpsGround equipmentActuation

Tube assembliesDuctingFiltration and liquid separation

Air to air refuellingWCRDASAircraft external fuel tanksRPVs - surveillance

AirborneIR CountermeasuresExpendable decoys

LV spectral flaresPyrotechnicsASM/ASW Countermeasures

Aircraft systemsOxygenCoolingEscape

Pressure vesselsProtection systemsSpace sub-systems

Commercial aerospaceCostAfter marketIndustry consolidationUS Defence spendNew product development

US Defence spendPlatforms and programmesUK Defence spendAfter marketMarket position

US footprintPreferred supplier baseUK Defence spendTechnologyCommercial market

US Defence spendMarket positionCommercial aerospaceAfter marketSpace

Pro

duct

s &

Ser

vice

sB

usin

ess

Driv

ers

Chelton

European Antennas

Culham

Chelton Defence Comms

Micromill

Chelton Antennas

Racal Antennas

Precision Antennas

ERA Technology

Omnipless

Avionics(Chelton)

Antenna and EM Technologies Composites

Cobham Composites

Chelton Radomes

Atlas Composites

Chelton Applied Composites

Slingsby

Nauticast

Microwave

Atlantic Microwave

Kevlin

Nurad Technologies

Continental

Atlantic Positioning

Air Precision

Label

Sivers

Hyper Technologies

Credowan

Salies

Avionics

Chelton Aviation

Comant

NAT

Orion

Sea Tel Inc

Artex

Wulfsberg

ACR

Siemac

Chelton Flight Systems

TEAM

Satori

Chelton Avionics

Avionics(Chelton)

Antenna and EM Technologies Composites MicrowaveAvionics

AntennasAirborneWirelessSatcom/Navcom

Static dischargersHomeland securityEM testingTechnology services

RadomesAdvanced compositesFirefly trainers

GPS antennasAudio systemsAvionics

Flight DeckSpecial Mission

Tracking/radio locatorsEFISSAR SYSTEMS

Microwave systemsRotary couplersWaveguide systemsSlip ring assemblies

US Defence spendPlatforms and programmesR&D expenditureUS-Europe interoperabilityAfter marketNetwork enabling capabilityUK Defence spend

European defence spendTransportationConsolidation

US Defence spendGeneral AviationTechnologyPlatformsAdjacent marketsEuropean Defence spend

US Defence spendPlatforms and programmesTechnologyAfter marketNetwork enabling capabilitySpaceEuropean Defence spend

Pro

duct

s &

Ser

vice

sB

usin

ess

Driv

ers

Military Training

FB Heliservices

Survey and Surveillance

Flight Inspection

National Air Support

Engineering Support

Military AviationSupport

Flight Operationsand Services(FR Aviation)

Flight Operations Aviation SupportOutsourced Aviation Services

National Jet Services

TAA

EW trainingAir defence trainingMilitary helicopter trainingSurvey and surveillanceAerial surveillanceEEZ monitoringSearch and rescueFlight inspection

Design servicesAircraft maintenanceRole conversionsFuel tank repairsEngine overhaul

Flight Operationsand Services(FR Aviation)

Flight Operations Aviation SupportOutsourced Aviation Services

Pro

duct

s &

Ser

vice

sB

usin

ess

Driv

ers

QantasAaEResource services

UK outsourcingAfter marketFurther consolidationEuropean outsourcingAustralian defence/government spendPFIFSTA

Commercial aerospaceMROAfter sales

Commercial aerospaceAustralian marketResource industry growthFurther consolidationLow cost airlines

Future Major ProgrammesProgramme/Platform Group

Eurofighter Typhoon Av+AeSYS

Airbus single aisle Av+AeSYS

Airbus A330/A340 Av+AeSYS

A380 Av+AeSYS

Boeing 7E7 AeSYS

A400M Av+AeSYS

Naval EH101 Av

NH90 Helicopters Av

F22 Av

F35 Av+AeSYS

Grippen Av+AeSYS

2004 2005 20152010 2020 Ship setValue

£800k

£40k

£350k

£620k

TBA

TBA

£500k

£50K

£150k

£120K

£280K

AFSOC AeSYS

900 series AR AeSYS

JTRS Av

N/A

N/A

TBA

Hawk Av+AeSYS £250K

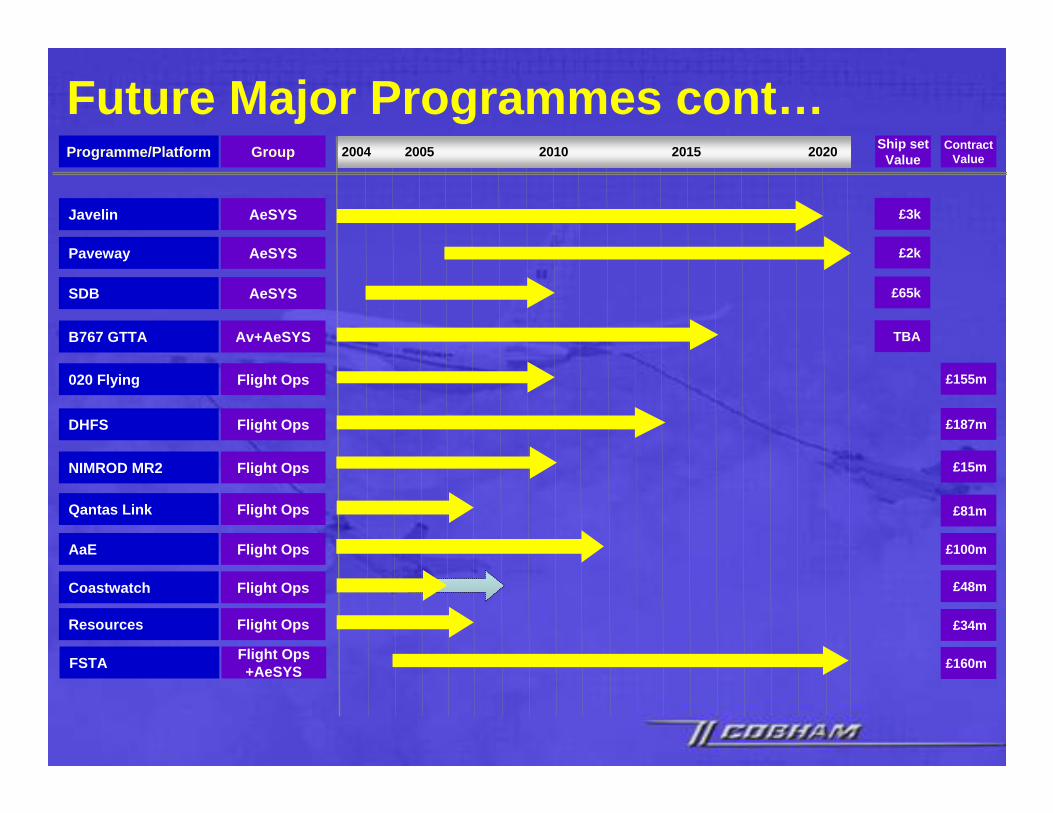

Future Major Programmes cont…Programme/Platform Group Contract

Value

Javelin AeSYS

Paveway AeSYS

SDB AeSYS

B767 GTTA Av+AeSYS

020 Flying Flight Ops

DHFS Flight Ops £187m

NIMROD MR2 Flight Ops £15m

Qantas Link Flight Ops £81m

AaE Flight Ops £100m

Coastwatch Flight Ops £48m

Resources Flight Ops £34m

2004 2005 20152010 2020 Ship setValue

£3k

£2k

£65k

TBA

£155m

FSTA Flight Ops+AeSYS £160m

Airbus booked 284 new orders in 2003 compared with 240 at Boeing. Deliveries totalled 305 versus 281 at Boeing. Airbus have launched “Route 06” aimed at reducing cost base by 15% commencing in 2006. A380 on track for entry into service in second quarter 2006. Current order book is 129.

AIRBUS

Discussions between two major suppliers – EADS and BAE SYSTEMS – and four nations continue for Tranche 2. Expected conclusion of these negotiations could be mid year 2004. This is over 6 months/9 months behind schedule and reflects the complexity of the programme. All four nations have re-iterated their commitment to the quantity of 236 for Tranche 2. Production rate for Tranche 1 has been slowed down in comparison to the original schedule. Still opportunities for export orders – Singapore have down selected the Typhoon – but the only firm commitment is for Austria (16 off).

TYPHOON

LHM is currently operating under an SDD contract for F-35 to supply 22 aircraft in 3 configurations CTOL, STOVL and CV. There will be 14 flying aircraft and 8 test aircraft. First delivery is scheduled for 2008. Quantity is 3,002 and the programmes is expected to cover 40 years. Cobham companies have approximately £120k per shipset including fuel systems and communications. Stanley Aviation in Denver is currently bidding into Eaton for the Fuel System Simulator (FSS). Decision expected in the second quarter 2004.

F35

FRL completed testing on the MK32B-900 AR system for C-130J at the end of 2003. Deliveries have commenced to Sweden and we are actively promoting MK32B with LHM on a global basis. Sargent Fletcher Inc in California is supporting LHM in delivery of AR equipment for the C-130J Marine Corps programme. These will also be supplied to Italy.

C130J

Programme Updates

Further growth projected despite cancellation of the $39bn US Army Comanche programme. Increased requirement forecast for both Apache and Blackhawk. Agusta Westland currently bidding on US101 in the USA.

HELICOPTERS

This is an NAS contract with the Australian Government. The current contract stretches out to the end of 2005. We have been asked to negotiate a contract extension – probably to 2007 - and then a new contract will carry through to 2012.

COASTWATCH

See separate slides and information presented at the meeting.FSTA

Precision guided bomb developed and produced by Raytheon and LHM. Raytheon won 70% of 2003/04 and LHM won 100% of supplemental buy. Carleton have supplied in excess of 27,000 systems for a value of £40m. On contract for a further 21,000 systems. After 2006 demand will stabilise to around 6,000 per year. In November 2003, DOD awarded LHM a $56m contract for the USAF and $53m for USN. This was in addition to the $107m contract placed in February 2003 for USM and USAF.

PAVEWAY

Launched at the end of 2003 by Boeing. The initial version will have a seating capacity 250 with a range up to 8,500 miles. Advanced technology reduces fuel burn by 20% and offers airlines higher revenues at a lower operating cost. Entry into service will be 2008 and work share contributors are Japan (35%) and Vought/Alenia (26%). Cobham companies are bidding on fuel, oxygen and communication systems either directly through Boeing or teamed with other suppliers. Potential value could be up to $500m.

BOEING 7E7

Outlook for Hawk improved considerably during 2003. The RAF selected the Hawk 128 for the AJT requirement of MFTS. Entry into service will be 2008. The total quantity could be up to 44. In September the Indian Government selected the Hawk 115Y AJT. The numbers involved could be as high as 66. Contract negotiations should be complete in 2004.

HAWK

In August 2003, the USAF awarded Boeing a contract for a small (250lb class) winged, long range ordinance carried on a single, four place Carriage System Assembly (CSA). Boeing contracted with SFI to develop and produce 2000 CSA over the life of the programme. Boeing have awarded SFI a $13m SDD contract and we have delivered on time, the first 3 to Boeing. The first production run is scheduled for 2006. Total contract value is up to $160m.

SDB

Replacement pumps now fully certified by FAA. Received orders from BA, JAL, Air France and Boeing. Deliveries have already started to all customers. Interest received from Virgin and KLM. Business proposal still being evaluated by Boeing for B737 replacement.

BOEING 747/737

Programme Updates cont…

In addition to the USA requirement ($130m in 2004) export orders have been achieved in Norway, Ireland, New Zealand, Australia and Israel. Orders are also expected from Oman, Kuwait, UAE, Saudi Arabia and Canada. There is a high probability that the UK will order a further 1,300 in September 2004

JAVELIN

Aerospace Systems Group, under leadership of SFI, is leading the USA in development of aerial refuelling equipment for small aircraft like munitions. We are working with Air Force Research Lab and Boeing Phantom works. Flight demonstrations could occur within 3 years. In two years, in-flight hardware will have been tested in wind tunnels and flight demonstrations.

UAV/UCAV

Military Market – 50%

Polarised between USA and RoW

USADOD budget $402bn in 2005 + 7%Forecast to increase to $490bn in 2009 +30%Procurement $75bn increasing to $114bn in 2009RDT&E $69bn in 2005 increasing to $71bn in 2009F-35 SDD phase increased from $33bn to $40bnIncreased C17 build from $3.7bn to $4.1bn

EUROPEDefence spending $125bn in 2004(E) – flatProcurement less than half of USADefence spending as a percentage of GDP < 2.2%, USA 3.7%RDT&E less than $10bn in 2003, 20% of USA!Interoperability now a critical issueSpecialisation within NATO on key strategic areas

Military Market cont… – priorities

Rapid deployment of assetsGlobal reachInteroperability between services and alliesPrecision strikeInformation securityNetwork enabled capability

Commercial Aerospace – 16%

Commercial aircraft demand is driven by:Revenue passenger kilometres (RPK)Airline profitabilityDevelopment of airline fleetsOperational developmentsGeographical developments

Global air travel fell by 3.9% in 2001, 0.4% in 2002, flat in 2003Projections indicate that demand will return and grow at a rate above GDP growthAirbus vs Boeing

Total fleet 15,660 – Boeing 75%; Airbus 25%Airline fleet will grow to > 19,000 by 2020

Commercial Aerospace – cont…

Airbus Predictions

ExistingRecycledReplacedGrowth

Source: Airbus – Market Forecast 2002

20,000

15,000

10,000

5,000

25,000

2000

10,900

1,530

8,832

6,349

2020

+3% pa

19,732

3,021

Additional markets – 34%General Aviation

Pattern of stability is returningProduction trough in 2004Increased demand in 2005 is forecast

OutsourcingStrong growth in Australia via Qantas and NASSeveral long term contracts –government and OEMsOpportunities for future growth in other geographical markets

Homeland SecurityUS budget is $36bn in 2004Focusing on four specific initiatives

Border and transportation securityEmergency ServicesCountermeasuresInformation analysis

Search and RescueSupported by companies in Europe, USA and CanadaGrowth expected to be > 10% annuallySome degree of synergy between Avionics and ASGDevelopment of GPS technology has enhanced our productsInternational sales growing in South America, Australia and NZ, and EuropeAcquisition of Seimac and Orion in Canada enhances portfolio

SpaceGlobal market worth $58bn – US accounts for $34bnAnnual growth of EU market is 6% to $8.1bn in 2013Limited growth opportunities but stable

The FSTA ProgrammeReplacement of current fleet of VC10 and TriStar aircraft

Introduction to Service 2008

27-year Private Finance Initiative (PFI) contract

Industry owns the aircraft and provides a service

MoD estimates £13bn expenditure

Contractor responsible for provision and certification of product and provides long-term service

RAF retains operational control

Programme plan

2004 2005 2006 2007 2008 2009 2010 2011

Key milestonesContractAward

IntroductionTo Service

ARIn-Service

Date

ATIn-Service

Date

FullService

Date1 Jan 12

Aircraft Design and Production

1st aircraft conversion

Aircraft Deliveries

Build New FacilitiesBuild and Fit Facilities

Design Review ClosuresPreliminary Critical

Design & Certification Process

Military Aircraft Release

Matching timescales2003 2013 2023 2033 2043

EF2000 deliveries

JSF deliveries On-going service

FSTA baseline for service delivery

AirTanker service can be extended

AirTanker will last the lifetime of EF2000 and JSF and A400M

?Receiverlives

FSTA

A400M - significant synergy opportunities

On-going service

AirTanker Structure and Shareholders

AirTanker Ltd

AirTanker Services LtdAircraft Supply

Shareholders

Shareholders

Contracts with the Authority

Dedicated accountable service delivery company responsible for delivery of the

FSTA service to the RAFProvides the certified tanker

UK equipment and conversion

Thales provides:• Mission console and systems• Instrumentation• Crew intercoms• Defensive Aids Suite for low

risk integration with existing digital flight deck systems

Thales provides:• Mission console and systems• Instrumentation• Crew intercoms• Defensive Aids Suite for low

risk integration with existing digital flight deck systems

Conversion undertaken by Cobham (FRA) at HurnCertification by QinetiQ at Boscombe Down

Conversion undertaken by Cobham (FRA) at HurnCertification by QinetiQ at Boscombe Down

Cobham (FRL) provides:• Refuelling pods• Fuselage refuelling units Proven technology already in RAF use

Cobham (FRL) provides:• Refuelling pods• Fuselage refuelling units Proven technology already in RAF use

High quality, high value UK content

17,000 man years of direct employment50,000 man years including indirect benefits

UK supply base

AirTanker has selected further world class suppliers from the UKQinetiQ - aircraft certificationGECAT - type trainingIBM - management systemsVT Aerospace - supplementary service management expertise

All the conversion and through life support activities are in the

UK: direct employment will peak at 3,000 and we will create

600 new jobs

All the conversion and through life support activities are in the

UK: direct employment will peak at 3,000 and we will create

600 new jobs

Glasgow

Engine assemblyand overhaulRolls-Royce

Engine assemblyand overhaulRolls-Royce

Cobham (FRA)

FSTA major workcentres and numbers of Airbus UK suppliers

FSTA major workcentres and numbers of Airbus UK suppliers

IT systemsIBMIT systemsIBM

Simulator manufactureThales

Simulator manufactureThales

WingmanufactureAirbus UK

WingmanufactureAirbus UK

ARequipmentCobham (FRL)

ARequipmentCobham (FRL) Aircraft

conversionCobham (FRA)

AircraftconversionCobham (FRA)

AirTankeroperationsAirTankeroperations

Bournemouth

London

Merseyside

Export Potential

Deployment capability and force projection are ever more vital for many nationsMarket of at least 500 aircraft

KC-X dominatesSignificant other opportunities: Australia, France, NATO etc

A330 attractive due to competitive advantages

CapableFlexibleModern

A330 Benefits:

Provides competition in the global market

High inherent UK content for all export sales

Provides only export potential for UK:

Refuelling systems

Engines

Mission equipment

A330 Benefits:

Provides competition in the global market

High inherent UK content for all export sales

Provides only export potential for UK:

Refuelling systems

Engines

Mission equipment

A330 provides high value, high quality UK export potential

Impact of Moving from SSAP 24 to FRS 17Unaudited

Year to 31/12/02

£m

Unaudited Year to

31/12/03 £m

(61.8) (70.0)

0.5 (2.5)

0.3p (1.7)p

Shareholders’ Funds

PBT

eps (p)

Increase/(decrease)

Summary Profit and Loss Account

Orders Received

UnauditedYear to

31/12/03£m

Year to31/12/02

£mGrowth

Gross Profit

Margin

Operating profit

925.0672.7 37.5%

248.1211.7 17.2%

29.8%28.8% 1.0 pts

147.7123.4 19.7%

Turnover 832.6734.6 13.3%

Margin 17.7%16.8% 0.9 pts

Profit before taxation 135.3115.8 16.8%

All excluding integration costs, goodwill amortisation and loss on disposal

FRS 17 Basis

Shareholders’ Returns

Earnings per Share

UnauditedYear to

31/12/03Year to

31/12/02

- underlying 93.5p

- basic

- fully diluted

86.4p

70.7p

Tax rate*

Dividend per Share 25.60p

17.2p

28.16p

17.1p70.2p

26.6%24.3%

Growth

(75.7)%

(75.6)%

8.2%

10.0%

* Based on PBT before goodwill amortisation, integration costs and loss on disposal

FRS 17 Basis

Net debt ratios

Net debt (£m)

UnauditedYear to

31/12/03Year to

31/12/02

Gearing

Net debt/ebitda* (12m trailing)

154.4188.8

33.9%63.5%

0.9 times1.30 times

Shareholders’ Funds (£m) 455.8297.4

* Excluding integration costs and loss on disposal

Growth

(18.2)%

53.3%

FRS 17 Basis