predictive underwriting: an update - mud group underwriting.pdf · predictive underwriting: an...

TRANSCRIPT

M.U.D. CONFERENCE | Jan. 30 2012 | New York

Predictive Underwriting: an update Improved customer experience and its impact Paul Hately, Global Head Accelerated Underwriting, Swiss Re

M.U.D. CONFERENCE | Jan. 30 2012 | New York

Session Overview

Predictive Underwriting: definition and context

Correlations between lifestyle and mortality: examples

Building a predictive model

What is sold through predictive underwriting?

Learnings & consumer reaction

The US mid-market

Q&A

2

M.U.D. CONFERENCE | Jan. 30 2012 | New York

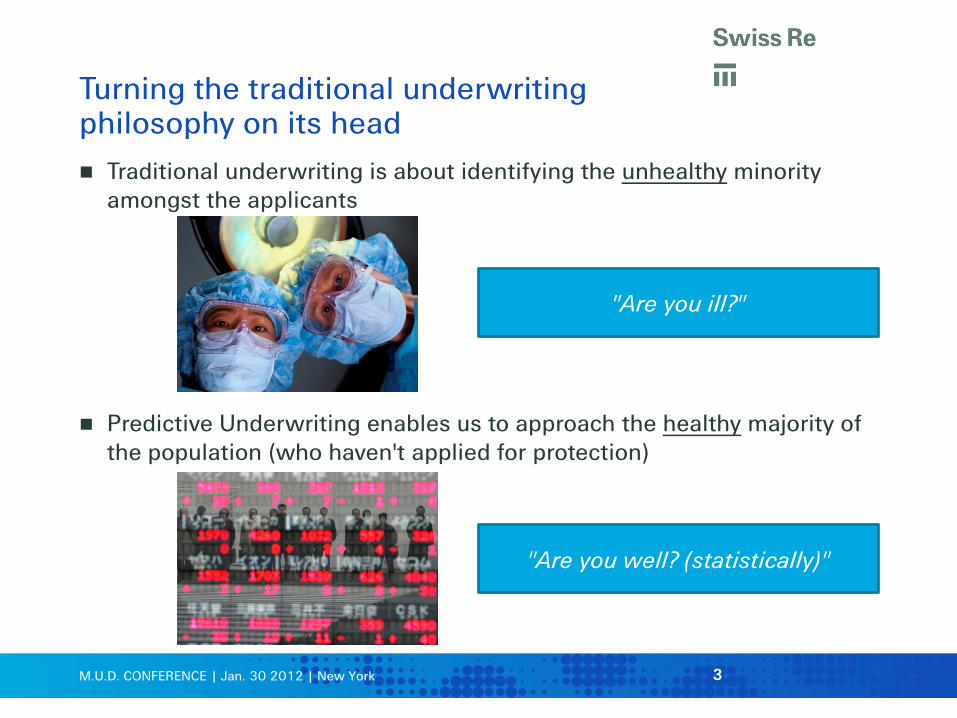

Turning the traditional underwriting philosophy on its head

Traditional underwriting is about identifying the unhealthy minority amongst the applicants

Predictive Underwriting enables us to approach the healthy majority of the population (who haven't applied for protection)

3

"Are you ill?"

"Are you well? (statistically)"

M.U.D. CONFERENCE | Jan. 30 2012 | New York

What do we mean by Predictive Underwriting?

The intelligent use of data held on consumers to reach a view as to their health status

Developments in the UK have focused on reducing the amount of traditional underwriting needed (where there is an existing data-rich relationship in place)

In the US, life industry focus is more on using predictive techniques to triage the underwriting process and avoid expensive medical tests for healthy people

Both approaches are valid and applicable in either markets

4

"You haven't applied for protection, but based on what we know about you, we will pre-approve you and make you an offer"

"Now you are applying for protection, let's run some data on you to remove certain tests, and speed up the process"

M.U.D. CONFERENCE | Jan. 30 2012 | New York

Scene-setter: the mid-market

If…

– consumers are massively under-insured

– they perceive that Protection costs more than it does

– medical underwriting is a barrier to sales

… then the key to success is having access to the consumer to engage with them, and:

– drawing their attention to their need for Protection

– demonstrating the relative cost and value of Protection

– making Protection easy-to-buy (hassle-free)

5

Source: Swiss Re Mortality Protection Gap 2011

M.U.D. CONFERENCE | Jan. 30 2012 | New York

Making use of available data

Intelligent data use is all around us

– Amazon: "Customers Who Bought This Also Bought…"

– YouTube / iTunes: recommended song you may like based on your download history and people like you

– Facebook: ads personalised to your interests, hobbies, searches

– Match.com: uses an algorithm to suggest possible partners based on your preferences and your behaviour on the site

– Google: ads in your Gmail account personalised to you

– Supermarkets online or using loyalty card: shopping basket advice and intelligent voucher/offers

Life insurance is woefully under-developed in this area

– General insurance moving faster than Life & Health (e.g. motor insurers using credit scores )

– What if we could predict mortality based on everyday information?

6

M.U.D. CONFERENCE | Jan. 30 2012 | New York

The premise:

7

There are correlations between lifestyle factors and mortality – you just need to unearth them

The following were found in depersonalised datasets

M.U.D. CONFERENCE | Jan. 30 2012 | New York 8

0

10

20

30

40

50

60

70

80

90

100

0

5

10

15

20

25

30

35

0 up to £2000 £2000 to £5000 £5000 +

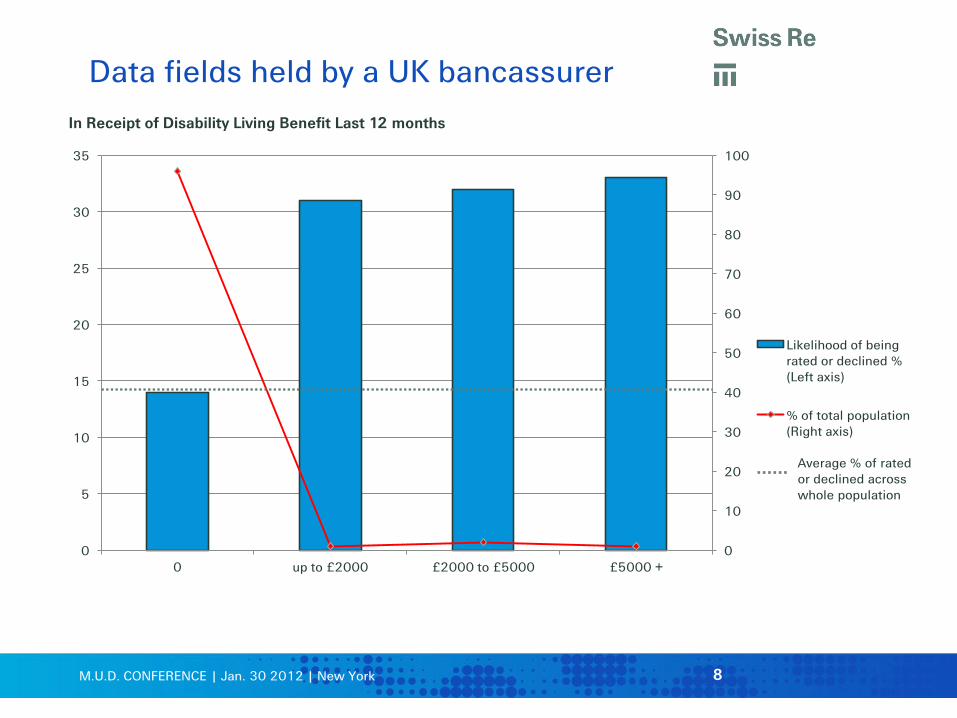

In Receipt of Disability Living Benefit Last 12 months

Likelihood of being rated or declined % (Left axis)

% of total population (Right axis)

Data fields held by a UK bancassurer

Average % of rated or declined across whole population

M.U.D. CONFERENCE | Jan. 30 2012 | New York 9

0

10

20

30

40

50

60

70

80

90

100

0

5

10

15

20

25

30

35

40

45

50

0 up to £2000 £2000 to £5000 £5000 +

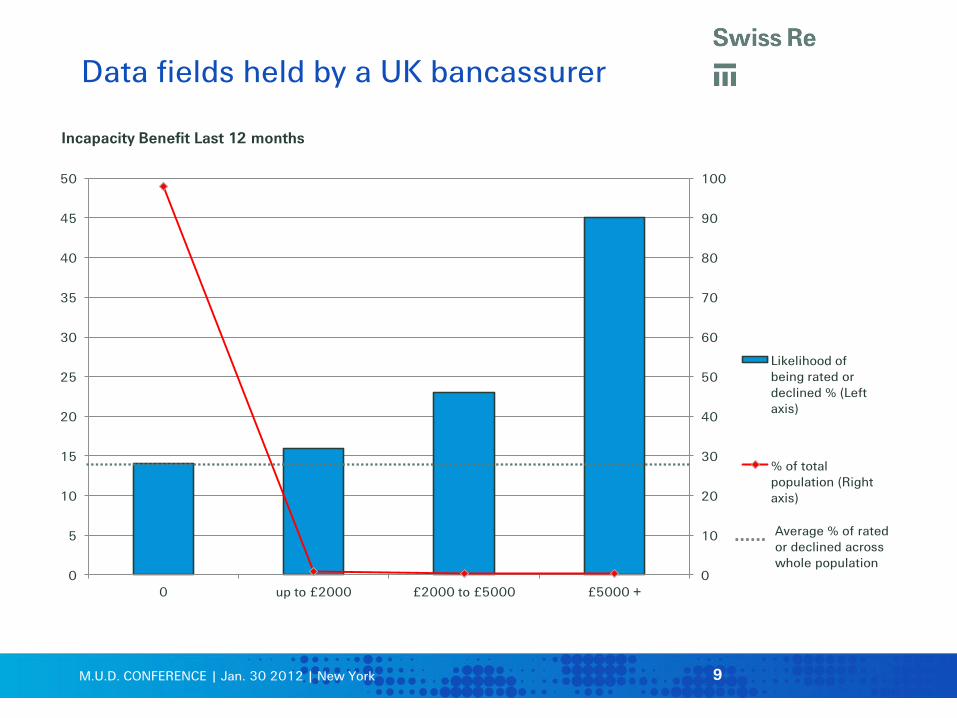

Incapacity Benefit Last 12 months

Likelihood of being rated or declined % (Left axis)

% of total population (Right axis)

Data fields held by a UK bancassurer

Average % of rated or declined across whole population

M.U.D. CONFERENCE | Jan. 30 2012 | New York

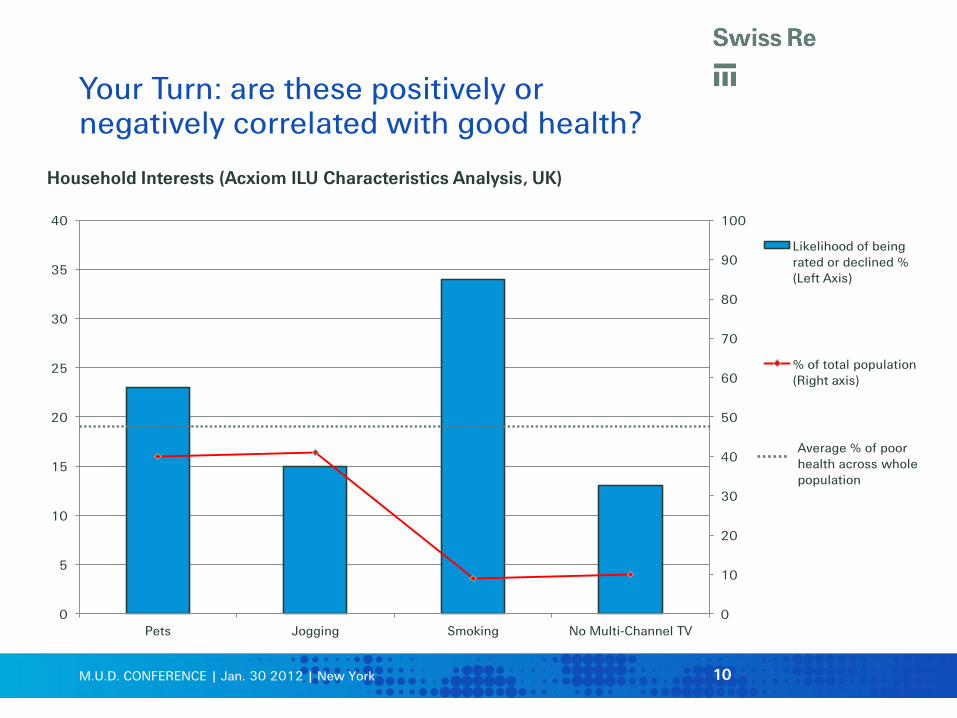

Your Turn: are these positively or negatively correlated with good health?

10

0

10

20

30

40

50

60

70

80

90

100

0

5

10

15

20

25

30

35

40

Pets Jogging Smoking No Multi-Channel TV

Household Interests (Acxiom ILU Characteristics Analysis, UK)

Likelihood of being rated or declined % (Left Axis)

% of total population (Right axis)

Average % of poor health across whole population

M.U.D. CONFERENCE | Jan. 30 2012 | New York

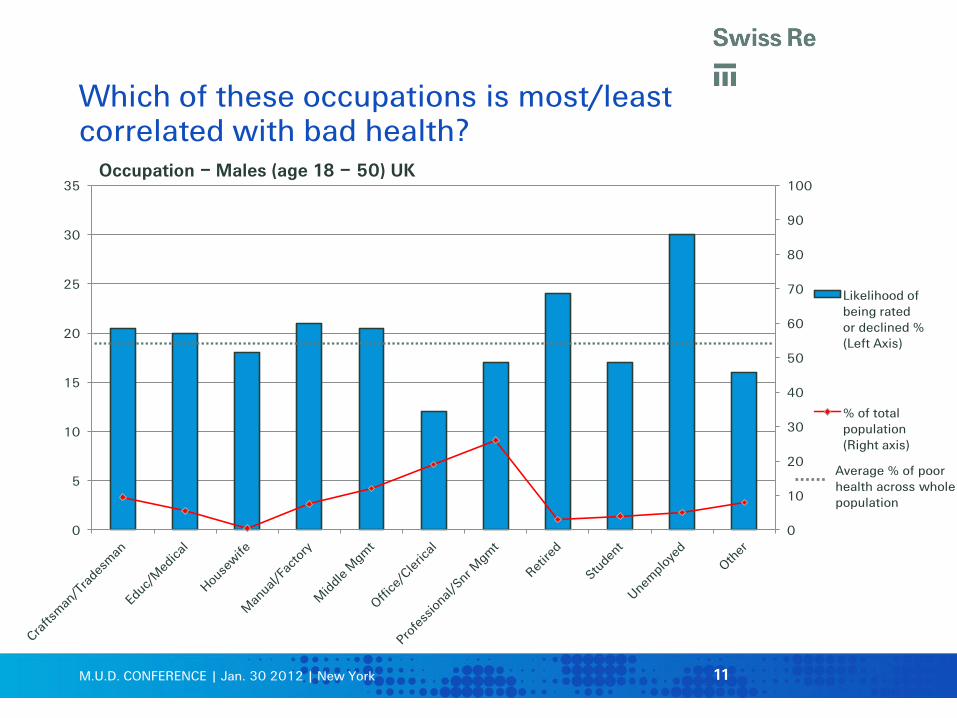

Which of these occupations is most/least correlated with bad health?

11

0

10

20

30

40

50

60

70

80

90

100

0

5

10

15

20

25

30

35 Occupation – Males (age 18 – 50) UK

Likelihood of being rated or declined % (Left Axis)

% of total population (Right axis)

Average % of poor health across whole population

M.U.D. CONFERENCE | Jan. 30 2012 | New York

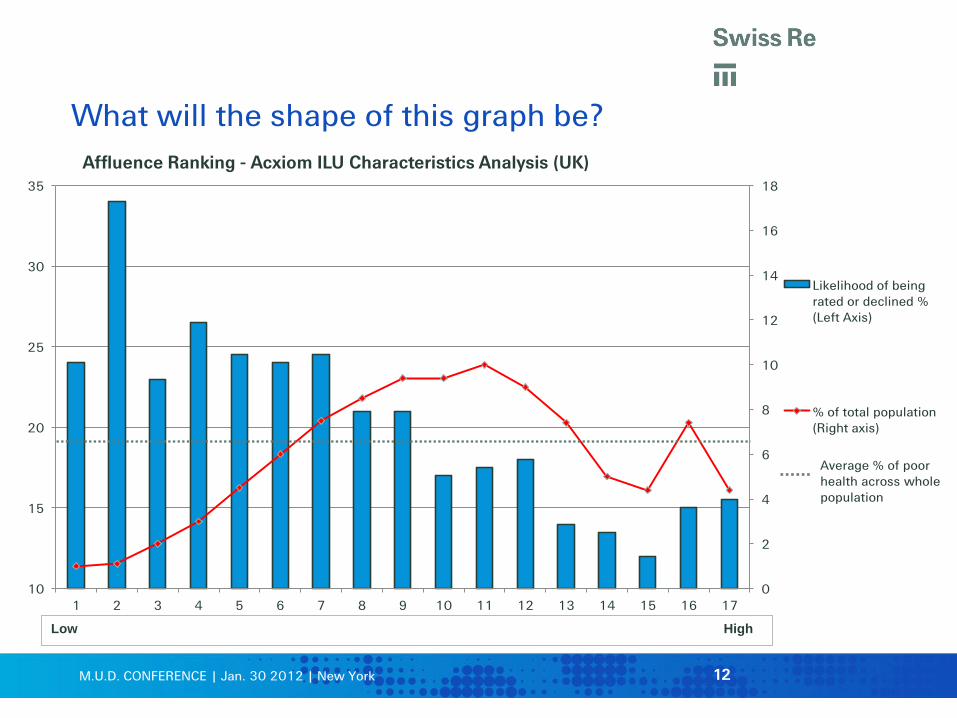

What will the shape of this graph be?

12

0

2

4

6

8

10

12

14

16

18

10

15

20

25

30

35

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17

Affluence Ranking - Acxiom ILU Characteristics Analysis (UK)

Likelihood of being rated or declined % (Left Axis)

% of total population (Right axis)

Low High

Average % of poor health across whole population

M.U.D. CONFERENCE | Jan. 30 2012 | New York

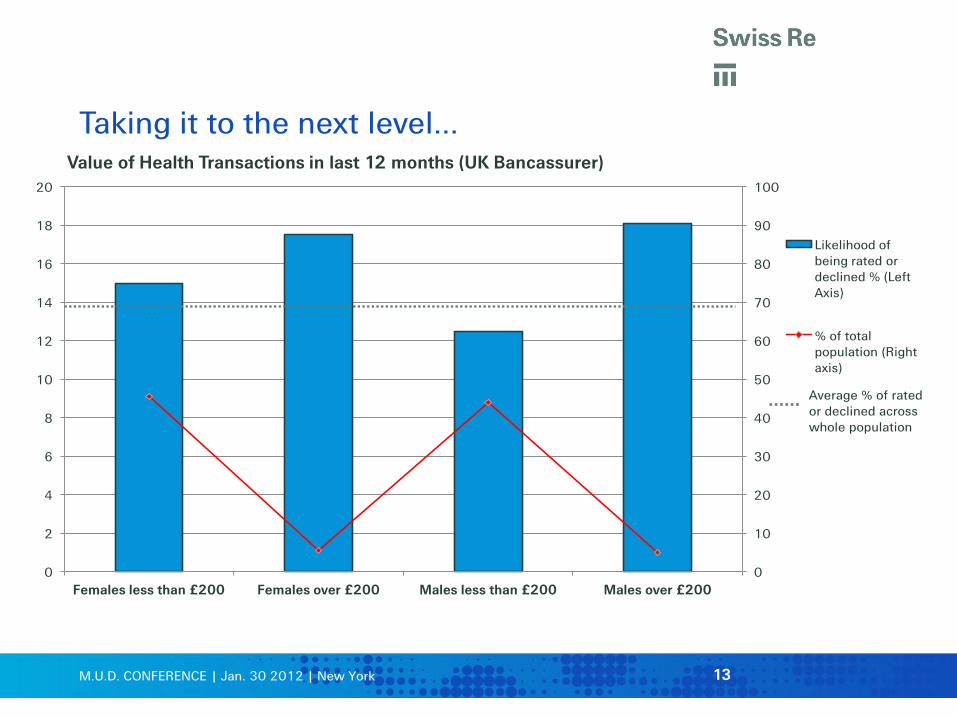

Taking it to the next level…

13

0

10

20

30

40

50

60

70

80

90

100

0

2

4

6

8

10

12

14

16

18

20

Females less than £200 Females over £200 Males less than £200 Males over £200

Value of Health Transactions in last 12 months (UK Bancassurer)

Likelihood of being rated or declined % (Left Axis)

% of total population (Right axis)

Average % of rated or declined across whole population

M.U.D. CONFERENCE | Jan. 30 2012 | New York

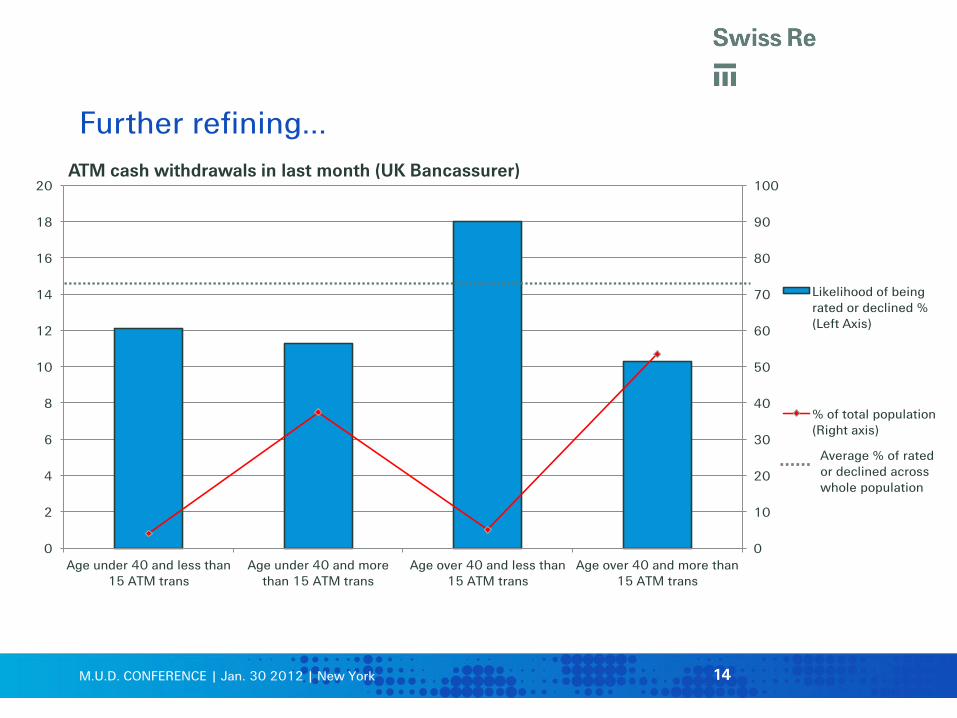

Further refining…

14

0

10

20

30

40

50

60

70

80

90

100

0

2

4

6

8

10

12

14

16

18

20

Age under 40 and less than 15 ATM trans

Age under 40 and more than 15 ATM trans

Age over 40 and less than 15 ATM trans

Age over 40 and more than 15 ATM trans

ATM cash withdrawals in last month (UK Bancassurer)

Likelihood of being rated or declined % (Left Axis)

% of total population (Right axis)

Average % of rated or declined across whole population

M.U.D. CONFERENCE | Jan. 30 2012 | New York 15

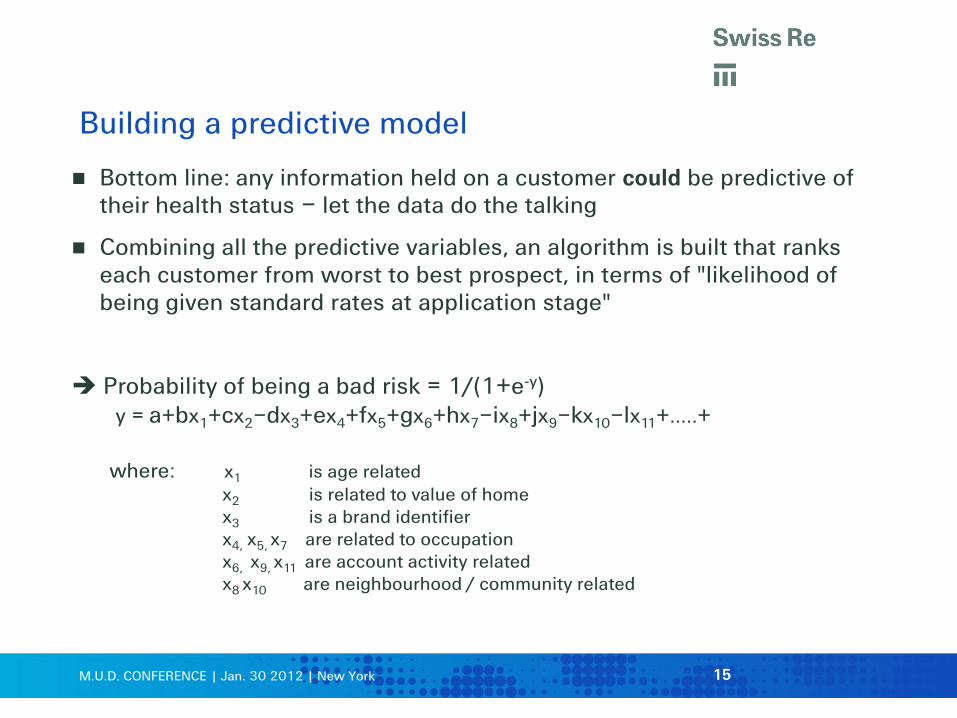

Building a predictive model

Bottom line: any information held on a customer could be predictive of their health status – let the data do the talking

Combining all the predictive variables, an algorithm is built that ranks each customer from worst to best prospect, in terms of "likelihood of being given standard rates at application stage"

Probability of being a bad risk = 1/(1+e-y) y = a+bx1+cx2–dx3+ex4+fx5+gx6+hx7–ix8+jx9–kx10–lx11+…..+

where: x1 is age related

x2 is related to value of home

x3 is a brand identifier

x4, x5, x7 are related to occupation x6, x9, x11 are account activity related x8 x10 are neighbourhood / community related

M.U.D. CONFERENCE | Jan. 30 2012 | New York

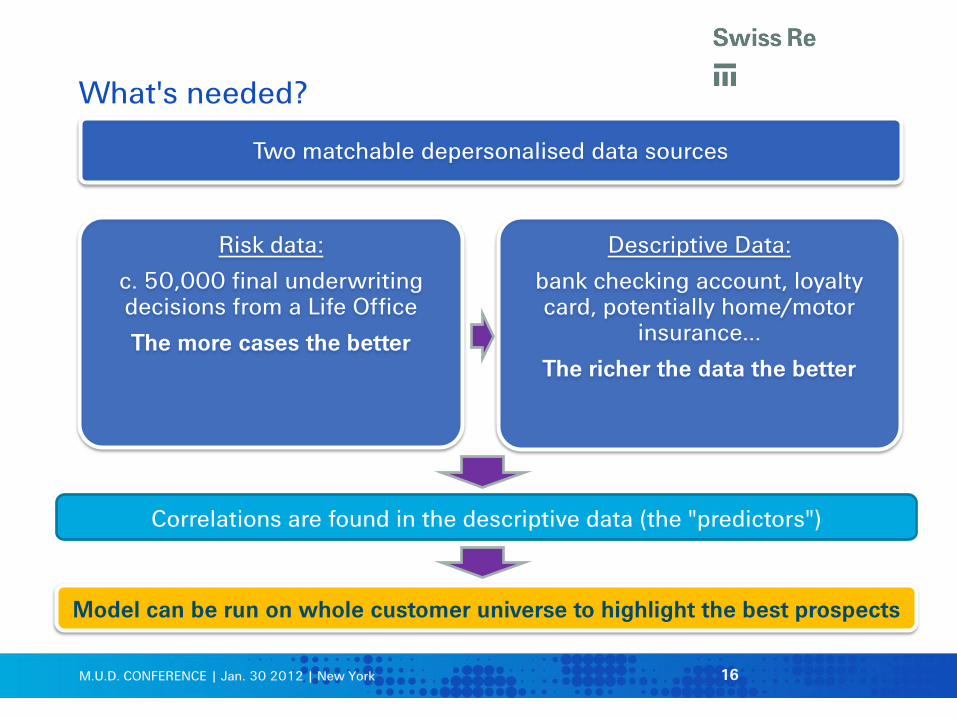

What's needed?

16

Two matchable depersonalised data sources

Risk data:

c. 50,000 final underwriting decisions from a Life Office

The more cases the better

Descriptive Data:

bank checking account, loyalty card, potentially home/motor

insurance…

The richer the data the better

Correlations are found in the descriptive data (the "predictors")

Model can be run on whole customer universe to highlight the best prospects

M.U.D. CONFERENCE | Jan. 30 2012 | New York

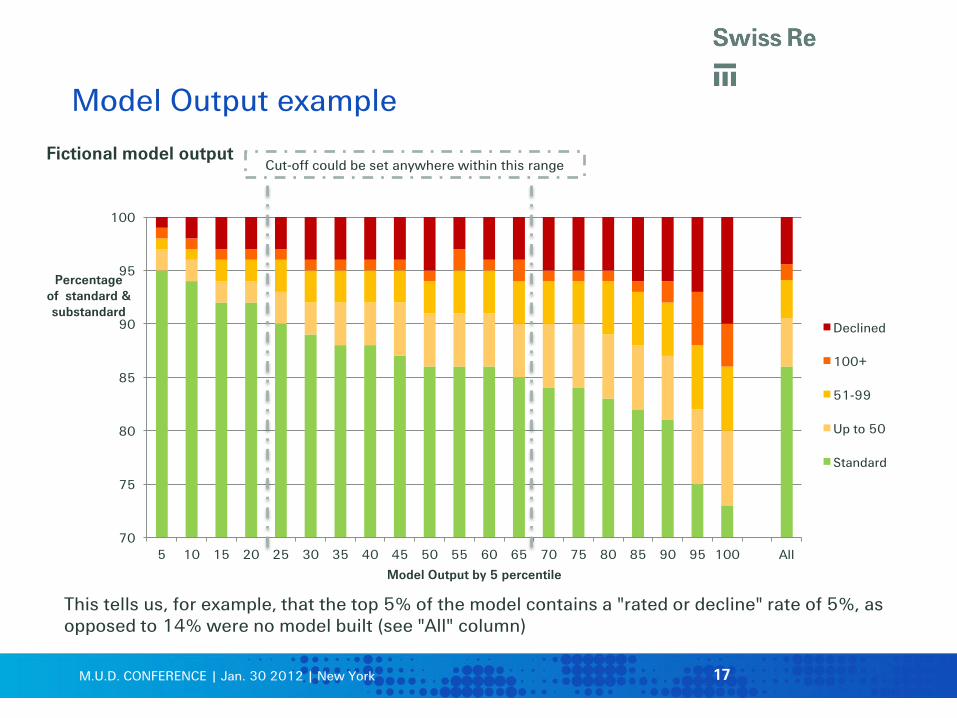

Model Output example

17

70

75

80

85

90

95

100

5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95 100 All

Percentage of standard & substandard

Model Output by 5 percentile

Fictional model output

Declined

100+

51-99

Up to 50

Standard

Cut-off could be set anywhere within this range

This tells us, for example, that the top 5% of the model contains a "rated or decline" rate of 5%, as opposed to 14% were no model built (see "All" column)

M.U.D. CONFERENCE | Jan. 30 2012 | New York

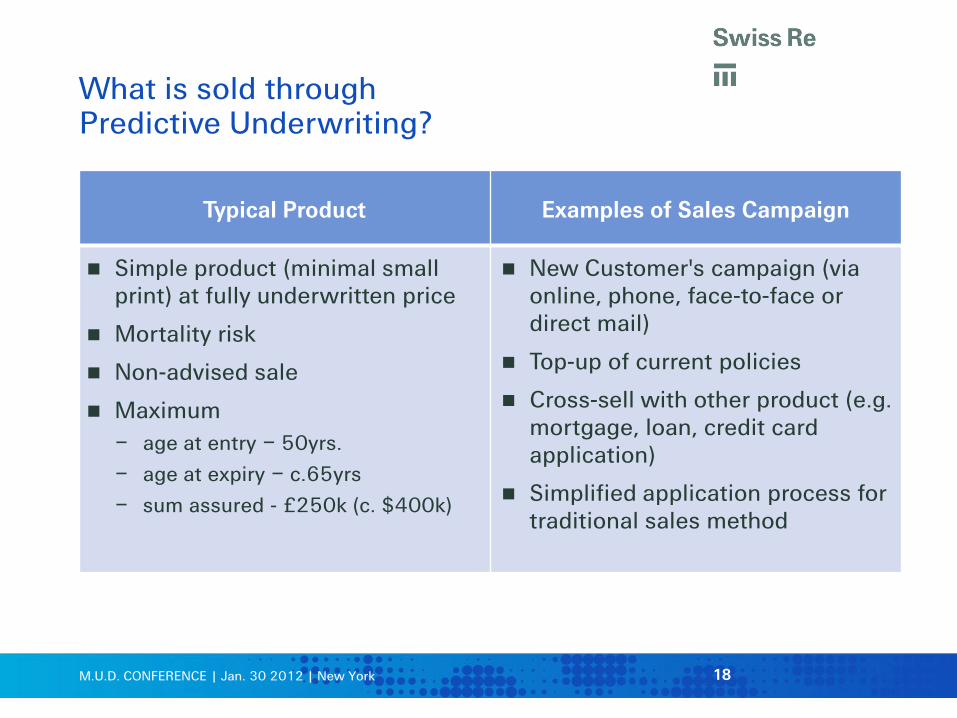

What is sold through Predictive Underwriting?

Typical Product Examples of Sales Campaign

18

Simple product (minimal small print) at fully underwritten price

Mortality risk

Non-advised sale

Maximum

– age at entry – 50yrs.

– age at expiry – c.65yrs

– sum assured - £250k (c. $400k)

New Customer's campaign (via online, phone, face-to-face or direct mail)

Top-up of current policies

Cross-sell with other product (e.g. mortgage, loan, credit card application)

Simplified application process for traditional sales method

M.U.D. CONFERENCE | Jan. 30 2012 | New York 19

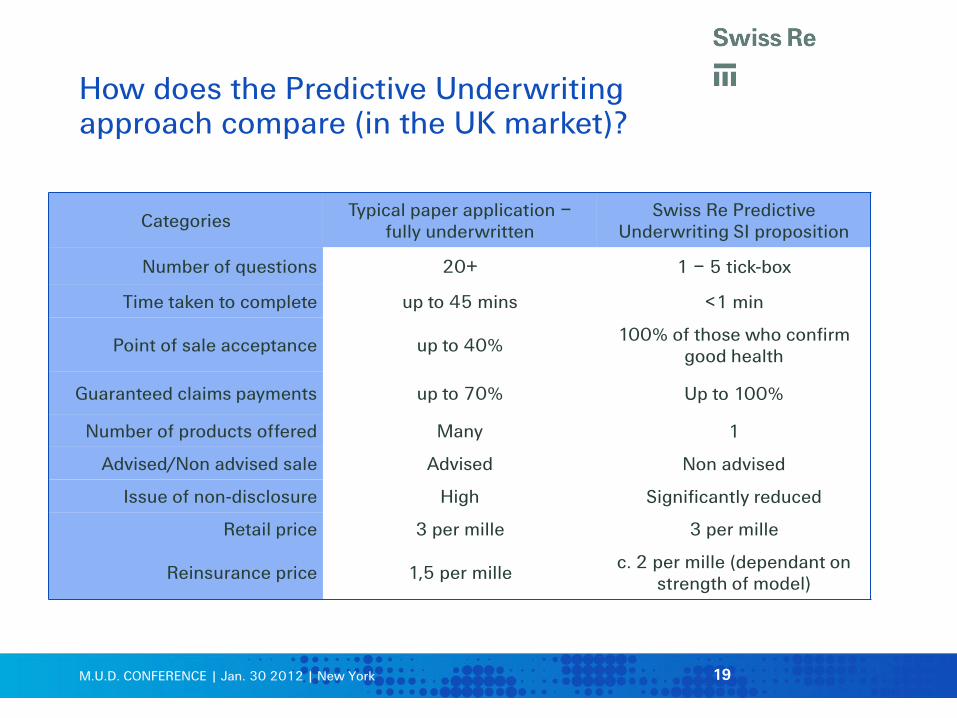

How does the Predictive Underwriting approach compare (in the UK market)?

Categories Typical paper application –

fully underwritten Swiss Re Predictive

Underwriting SI proposition

Number of questions 20+ 1 – 5 tick-box

Time taken to complete up to 45 mins <1 min

Point of sale acceptance up to 40% 100% of those who confirm

good health

Guaranteed claims payments up to 70% Up to 100%

Number of products offered Many 1

Advised/Non advised sale Advised Non advised

Issue of non-disclosure High Significantly reduced

Retail price 3 per mille 3 per mille

Reinsurance price 1,5 per mille c. 2 per mille (dependant on

strength of model)

M.U.D. CONFERENCE | Jan. 30 2012 | New York 20

Experience

Two bancassurers are currently selling a predictive product in the UK with Swiss Re

– both top-five UK bancassurers

– in both cases, strong buy-in from both parts of bancassurer

– strong models were built due to rich banking data available

– so far, distribution methods are: direct mailing, outbound telephony and internet pop-ups

– for both: Predictive Underwriting product a key part of the 2012 protection plan

– one partner now extending this to a global proposition in partnership with Swiss Re

– Client quote: "We see Predictive Underwriting as the future of life protection"

Significant interest around the globe on how to apply these techniques to other markets

M.U.D. CONFERENCE | Jan. 30 2012 | New York

Learnings

This is a new way to contact customers to make them an offer and does not need to be in conflict with the advice sale model, can work as a complement to it

Personal "prompt" increases likelihood to buy.

– "I had a follow up phone call and they convinced me”

Opportunity to significantly reduce cost of acquisition (e.g. telephone sales dropped from 45m to 7m due to the reduced underwriting)

Response rates are highest when combined with effective "Propensity to buy" modelling

The consumer places value on the existing "financial" relationship

– “It was a reasonable offer and I’m not under any other policy. Plus I am an customer [of the bank] so it made sense”

Increased response rates witnessed around key life events – a real opportunity to engage with the customer

– “I've had a child recently. It seemed like a good deal”

21

M.U.D. CONFERENCE | Jan. 30 2012 | New York

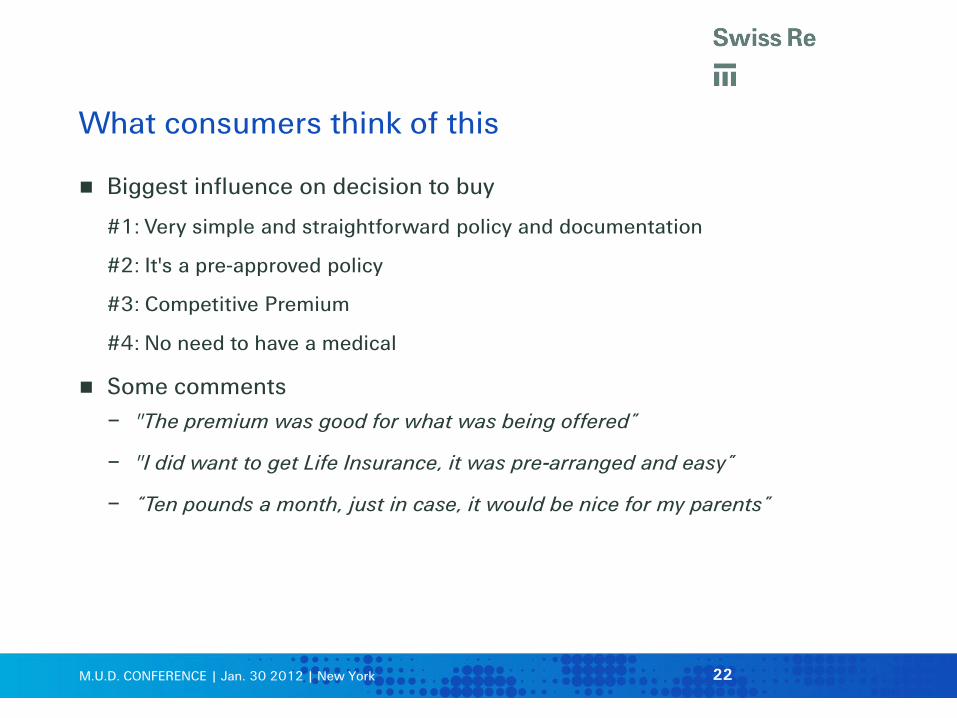

What consumers think of this

Biggest influence on decision to buy

#1: Very simple and straightforward policy and documentation

#2: It's a pre-approved policy

#3: Competitive Premium

#4: No need to have a medical

Some comments

– "The premium was good for what was being offered”

– "I did want to get Life Insurance, it was pre-arranged and easy”

– “Ten pounds a month, just in case, it would be nice for my parents”

22

M.U.D. CONFERENCE | Jan. 30 2012 | New York

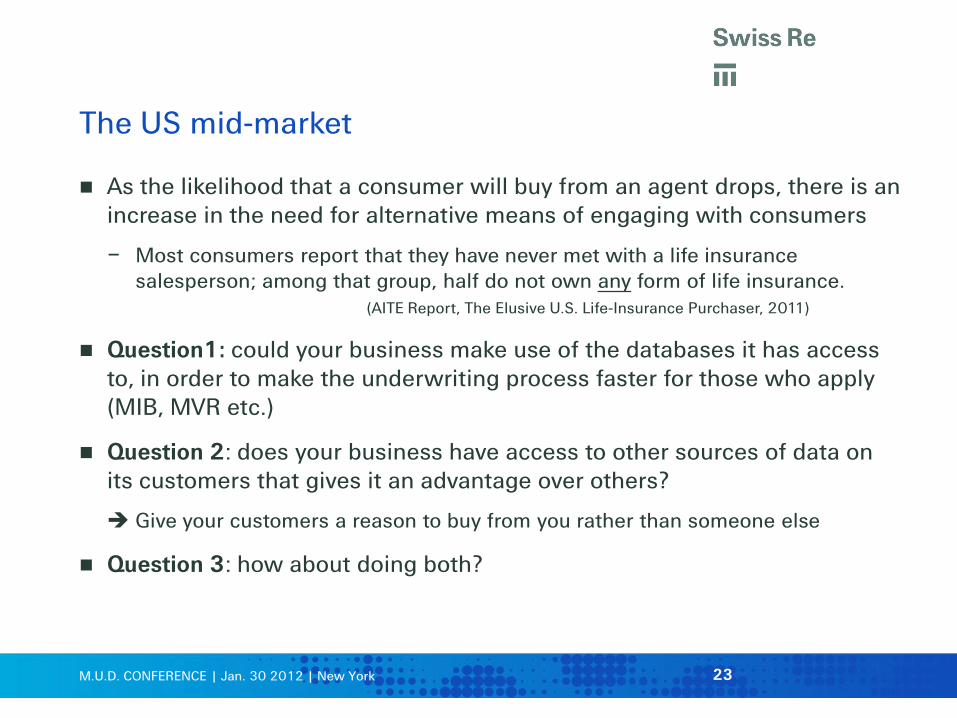

The US mid-market

As the likelihood that a consumer will buy from an agent drops, there is an increase in the need for alternative means of engaging with consumers

– Most consumers report that they have never met with a life insurance salesperson; among that group, half do not own any form of life insurance. (AITE Report, The Elusive U.S. Life-Insurance Purchaser, 2011)

Question1: could your business make use of the databases it has access to, in order to make the underwriting process faster for those who apply (MIB, MVR etc.)

Question 2: does your business have access to other sources of data on its customers that gives it an advantage over others?

Give your customers a reason to buy from you rather than someone else

Question 3: how about doing both?

23

Q&A "It is exceedingly difficult to make predictions – particularly about the future" Niels Bohr, Danish Physicist

Thank you

M.U.D. CONFERENCE | Jan. 30 2012 | New York

Legal notice

©2011 Swiss Re. All rights reserved. You are not permitted to create any modifications or derivatives of this presentation or to use it for commercial or other public purposes without the prior written permission of Swiss Re.

Although all the information used was taken from reliable sources, Swiss Re does not accept any responsibility for the accuracy or comprehensiveness of the details given. All liability for the accuracy and completeness thereof or for any damage resulting from the use of the information contained in this presentation is expressly excluded. Under no circumstances shall Swiss Re or its Group companies be liable for any financial and/or consequential loss relating to this presentation.

26