pertemuan 6 conceptual framework. g&np accounting and financial reporting based on distinctive...

TRANSCRIPT

PERTEMUAN 6PERTEMUAN 6

CONCEPTUAL FRAMEWORKCONCEPTUAL FRAMEWORK

G&NP ACCOUNTING ANDG&NP ACCOUNTING ANDFINANCIAL REPORTINGFINANCIAL REPORTING

Based on distinctive Based on distinctive ConceptsConceptsStandardsStandardsProceduresProcedures

not found in private business not found in private business organizationsorganizations

Designed to accommodate information Designed to accommodate information needs of the users of financial reportsneeds of the users of financial reports

G&NP ACCOUNTING ANDG&NP ACCOUNTING ANDFINANCIAL REPORTINGFINANCIAL REPORTING

Applicable to –Applicable to –– Local governmentsLocal governments– Central governmentCentral government– Nonprofit and governmentalNonprofit and governmental

UniversitiesUniversitiesHospitalsHospitalsVoluntary health and welfare organizationsVoluntary health and welfare organizationsOther not-for-profit organizationsOther not-for-profit organizations

UNIQUE CHARACTERISTICSUNIQUE CHARACTERISTICS

Absence of profit motive; most tax exemptAbsence of profit motive; most tax exempt

Constituency (citizen / taxpayer) ownership Constituency (citizen / taxpayer) ownership versus stockholder ownershipversus stockholder ownership

No direct relationship between resources No direct relationship between resources received and services providedreceived and services provided

Consensus policy-setting by elected or Consensus policy-setting by elected or appointed oversight bodyappointed oversight body

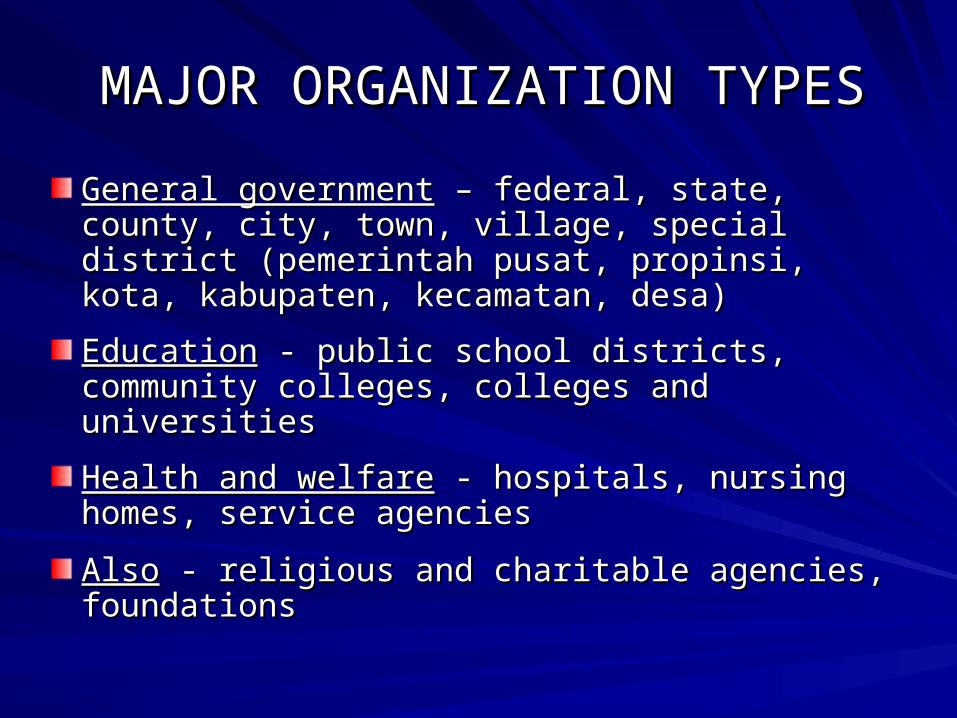

MAJOR ORGANIZATION TYPESMAJOR ORGANIZATION TYPES

General governmentGeneral government – federal, state, county, city, – federal, state, county, city, town, village, special district (pemerintah pusat, town, village, special district (pemerintah pusat, propinsi, kota, kabupaten, kecamatan, desa)propinsi, kota, kabupaten, kecamatan, desa)

EducationEducation - public school districts, community - public school districts, community colleges, colleges and universitiescolleges, colleges and universities

Health and welfareHealth and welfare - hospitals, nursing homes, - hospitals, nursing homes, service agenciesservice agencies

AlsoAlso - religious and charitable agencies, - religious and charitable agencies, foundationsfoundations

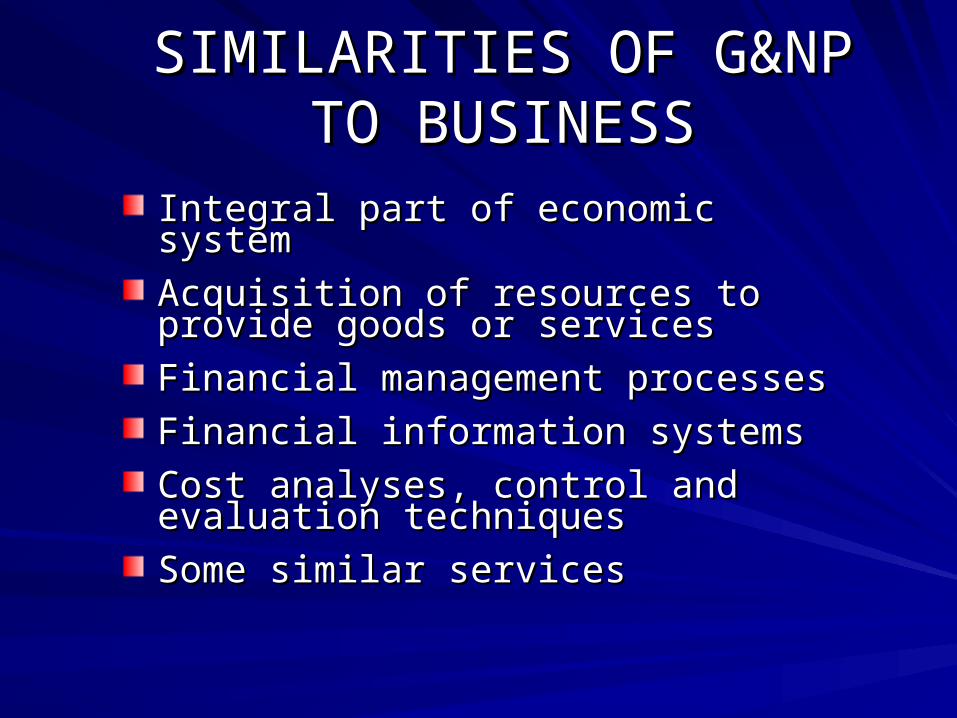

SIMILARITIES OF G&NPSIMILARITIES OF G&NPTO BUSINESSTO BUSINESS

Integral part of economic systemIntegral part of economic system

Acquisition of resources to provide goods Acquisition of resources to provide goods or servicesor services

Financial management processesFinancial management processes

Financial information systemsFinancial information systems

Cost analyses, control and evaluation Cost analyses, control and evaluation techniquestechniques

Some similar servicesSome similar services

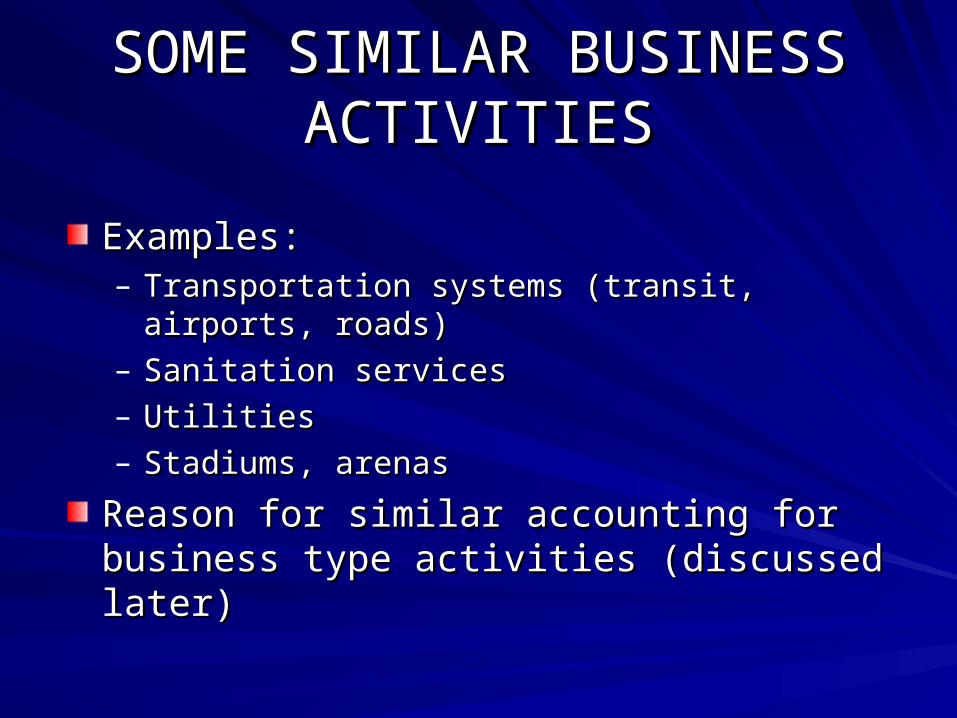

SOME SIMILAR BUSINESS SOME SIMILAR BUSINESS ACTIVITIESACTIVITIES

Examples:Examples:– Transportation systems (transit, airports, roads)Transportation systems (transit, airports, roads)– Sanitation servicesSanitation services– UtilitiesUtilities– Stadiums, arenasStadiums, arenas

Reason for similar accounting for business type Reason for similar accounting for business type activities (discussed later)activities (discussed later)

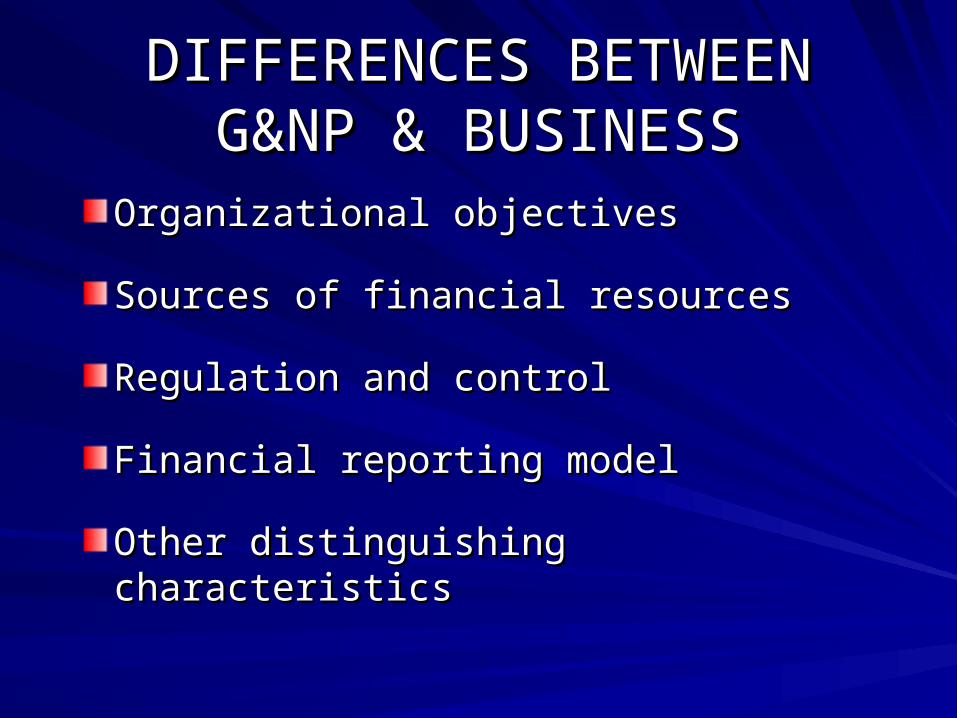

DIFFERENCES BETWEENDIFFERENCES BETWEENG&NP & BUSINESSG&NP & BUSINESS

Organizational objectivesOrganizational objectives

Sources of financial resourcesSources of financial resources

Regulation and controlRegulation and control

Financial reporting modelFinancial reporting model

Other distinguishing characteristicsOther distinguishing characteristics

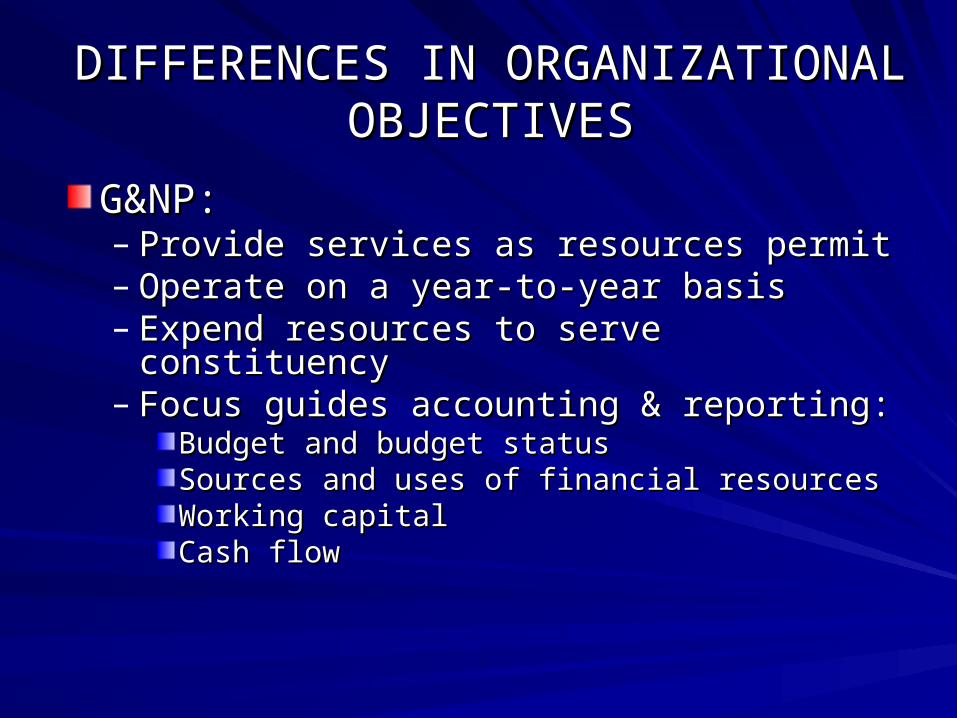

DIFFERENCES IN ORGANIZATIONAL DIFFERENCES IN ORGANIZATIONAL OBJECTIVESOBJECTIVES

G&NP:G&NP:– Provide services as resources permitProvide services as resources permit– Operate on a year-to-year basisOperate on a year-to-year basis– Expend resources to serve constituencyExpend resources to serve constituency– Focus guides accounting & reporting:Focus guides accounting & reporting:

Budget and budget statusBudget and budget statusSources and uses of financial resourcesSources and uses of financial resourcesWorking capitalWorking capitalCash flowCash flow

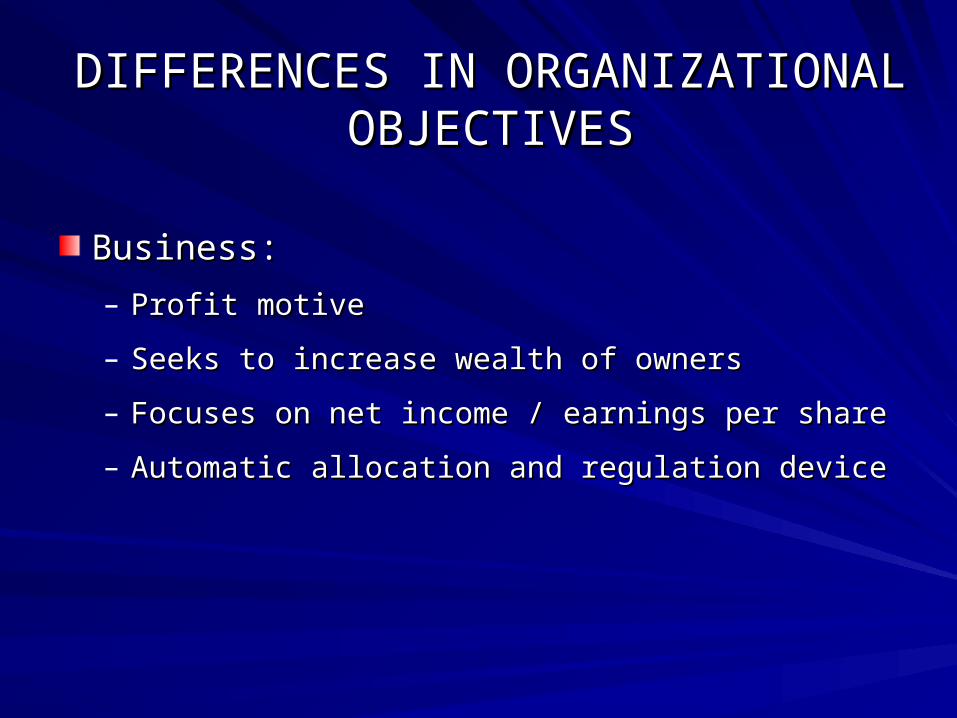

DIFFERENCES IN ORGANIZATIONAL DIFFERENCES IN ORGANIZATIONAL OBJECTIVESOBJECTIVES

Business:Business:

– Profit motiveProfit motive

– Seeks to increase wealth of ownersSeeks to increase wealth of owners

– Focuses on net income / earnings per shareFocuses on net income / earnings per share

– Automatic allocation and regulation deviceAutomatic allocation and regulation device

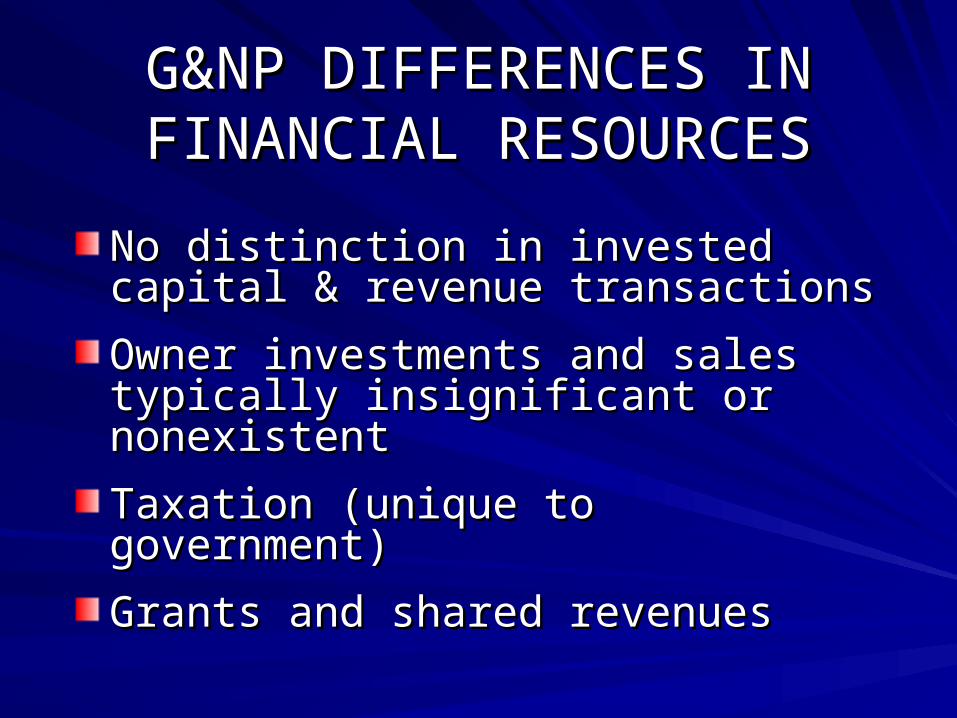

G&NP DIFFERENCES IN G&NP DIFFERENCES IN FINANCIAL RESOURCESFINANCIAL RESOURCES

No distinction in invested capital & No distinction in invested capital & revenue transactionsrevenue transactions

Owner investments and sales typically Owner investments and sales typically insignificant or nonexistentinsignificant or nonexistent

Taxation (unique to government)Taxation (unique to government)

Grants and shared revenuesGrants and shared revenues

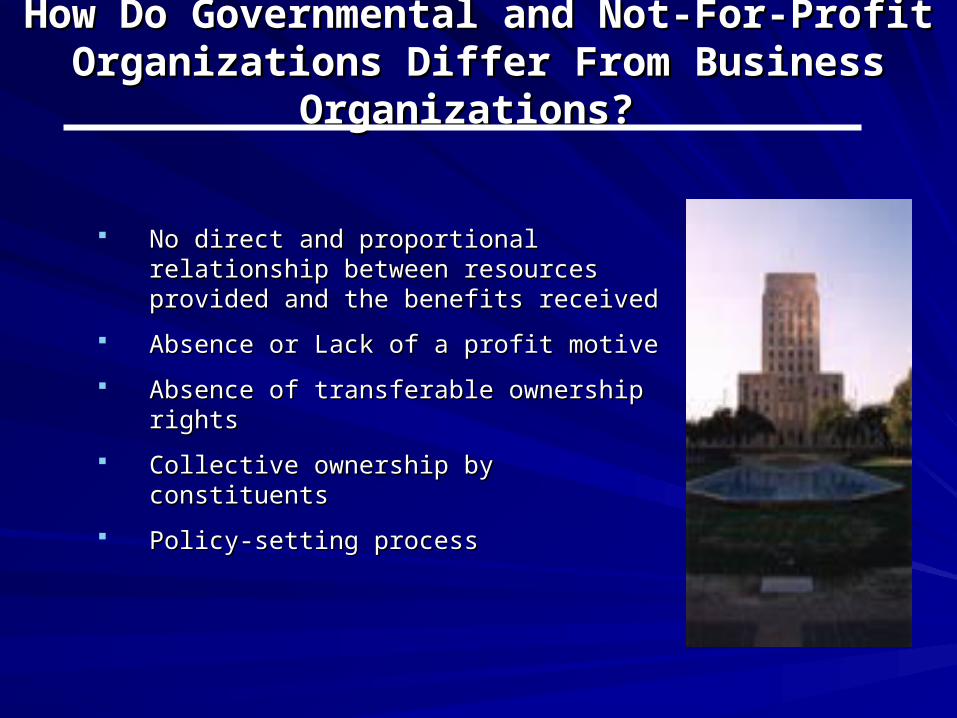

How Do Governmental and Not-For-Profit How Do Governmental and Not-For-Profit Organizations Differ From Business Organizations? Organizations Differ From Business Organizations?

No direct and proportional relationship No direct and proportional relationship between resources provided and the between resources provided and the benefits receivedbenefits received

Absence or Lack of a profit motiveAbsence or Lack of a profit motive

Absence of transferable ownership Absence of transferable ownership rightsrights

Collective ownership by constituentsCollective ownership by constituents

Policy-setting processPolicy-setting process

How Do Governmental and Not-For-Profit How Do Governmental and Not-For-Profit Organizations Differ From Business Organizations?Organizations Differ From Business Organizations?

For businesses, annual report is the most significant For businesses, annual report is the most significant financial document. For governments and non-profits, financial document. For governments and non-profits, budget is very important. budget is very important. Budget is the culmination of the political process. Budget is the culmination of the political process.

Need to ensure inter-period equity for most governments Need to ensure inter-period equity for most governments and non-profits.and non-profits.

Revenues may not be linked to constituent demand or Revenues may not be linked to constituent demand or satisfaction. satisfaction.

No direct link between revenues and expenses.No direct link between revenues and expenses. Many of the assets of government and non-profits are Many of the assets of government and non-profits are

restricted to particular activities and purposes. restricted to particular activities and purposes. No distinguished ownership interests.No distinguished ownership interests. Less distinction between internal and external accounting Less distinction between internal and external accounting

and reporting.and reporting.

Power ultimately rests in the hands of the Power ultimately rests in the hands of the people people

People vote and delegate that power to public People vote and delegate that power to public officialsofficials

Created by and accountable to a higher level Created by and accountable to a higher level government – ex. State Governments are government – ex. State Governments are accountable to Federal Governments while accountable to Federal Governments while City Governments are accountable to State City Governments are accountable to State Governments, etc.Governments, etc.

Power to tax citizens for revenuePower to tax citizens for revenue

How Do Governmental and Not-For-Profit Organizations Differ From Business Organizations?

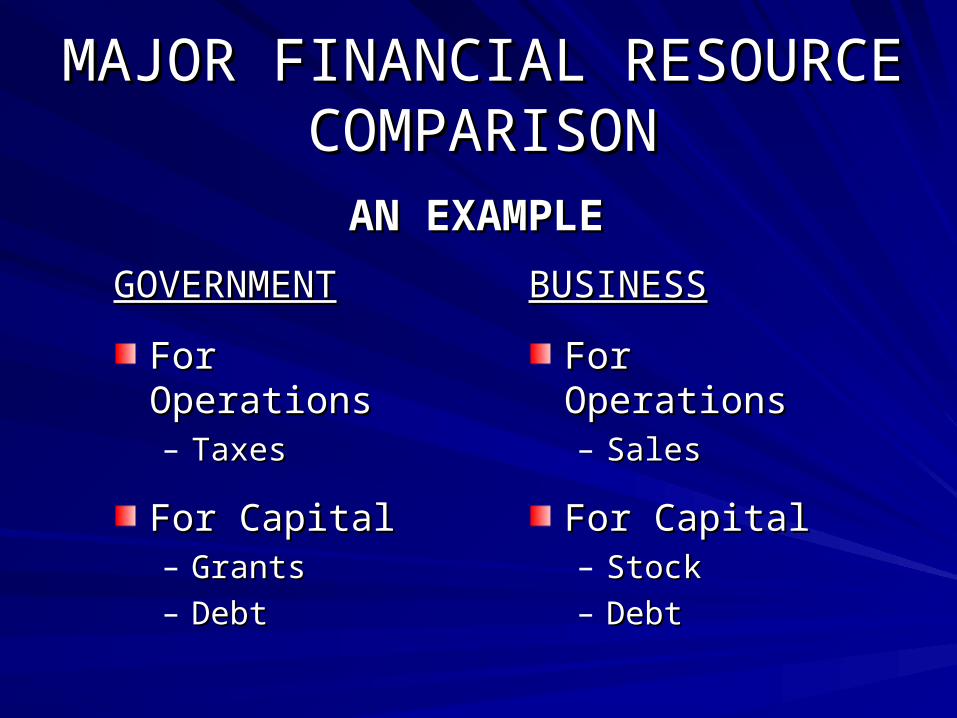

MAJOR FINANCIAL RESOURCE MAJOR FINANCIAL RESOURCE COMPARISONCOMPARISON

GOVERNMENTGOVERNMENT

For OperationsFor Operations– TaxesTaxes

For CapitalFor Capital– GrantsGrants– DebtDebt

BUSINESSBUSINESS

For OperationsFor Operations– SalesSales

For CapitalFor Capital– StockStock– DebtDebt

AN EXAMPLEAN EXAMPLE

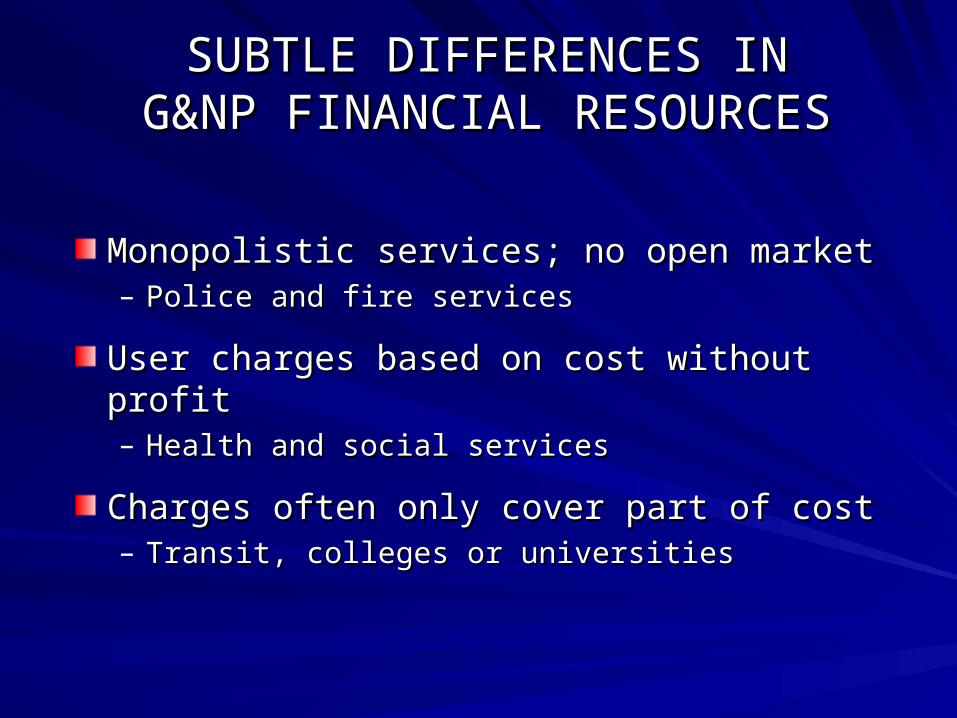

SUBTLE DIFFERENCES INSUBTLE DIFFERENCES ING&NP FINANCIAL RESOURCESG&NP FINANCIAL RESOURCES

Monopolistic services; no open marketMonopolistic services; no open market– Police and fire servicesPolice and fire services

User charges based on cost without profitUser charges based on cost without profit– Health and social servicesHealth and social services

Charges often only cover part of costCharges often only cover part of cost– Transit, colleges or universitiesTransit, colleges or universities

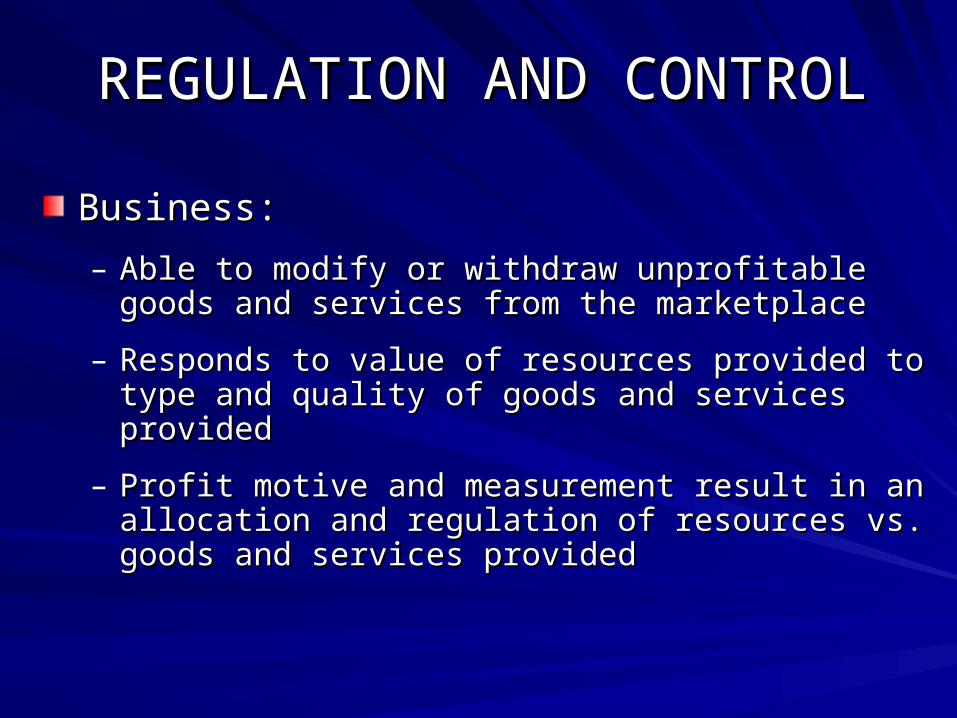

REGULATION AND CONTROLREGULATION AND CONTROL

Business:Business:

– Able to modify or withdraw unprofitable goods and Able to modify or withdraw unprofitable goods and services from the marketplaceservices from the marketplace

– Responds to value of resources provided to type and Responds to value of resources provided to type and quality of goods and services providedquality of goods and services provided

– Profit motive and measurement result in an allocation Profit motive and measurement result in an allocation and regulation of resources vs. goods and services and regulation of resources vs. goods and services providedprovided

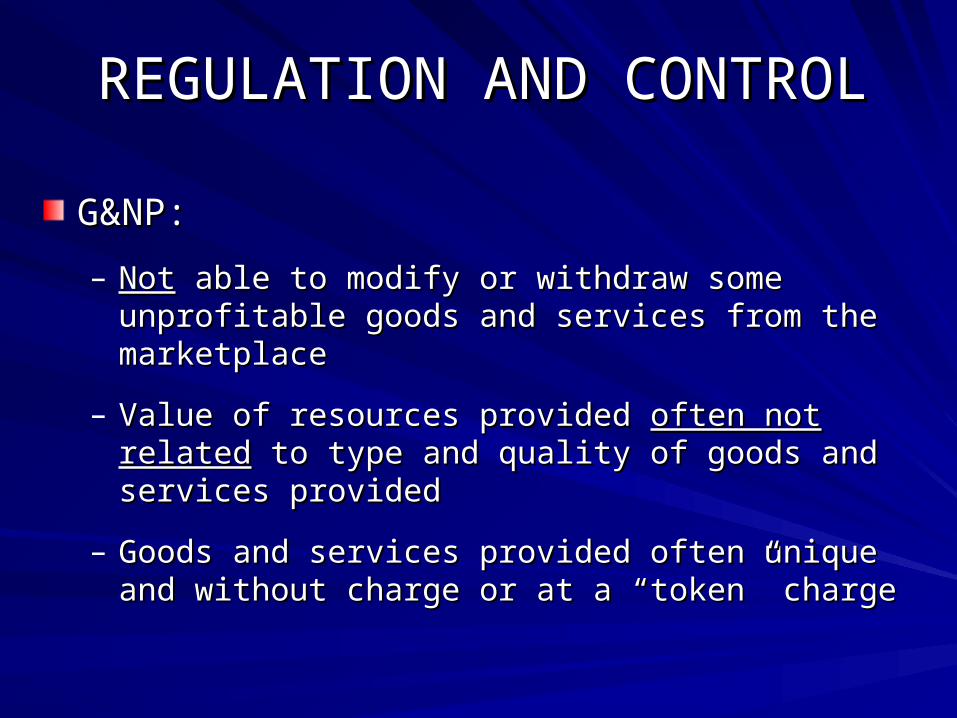

REGULATION AND CONTROLREGULATION AND CONTROL

G&NP:G&NP:

– NotNot able to modify or withdraw some unprofitable goods able to modify or withdraw some unprofitable goods and services from the marketplaceand services from the marketplace

– Value of resources provided Value of resources provided often not relatedoften not related to type and to type and quality of goods and services providedquality of goods and services provided

– Goods and services provided often unique and without Goods and services provided often unique and without charge or at a “token” chargecharge or at a “token” charge

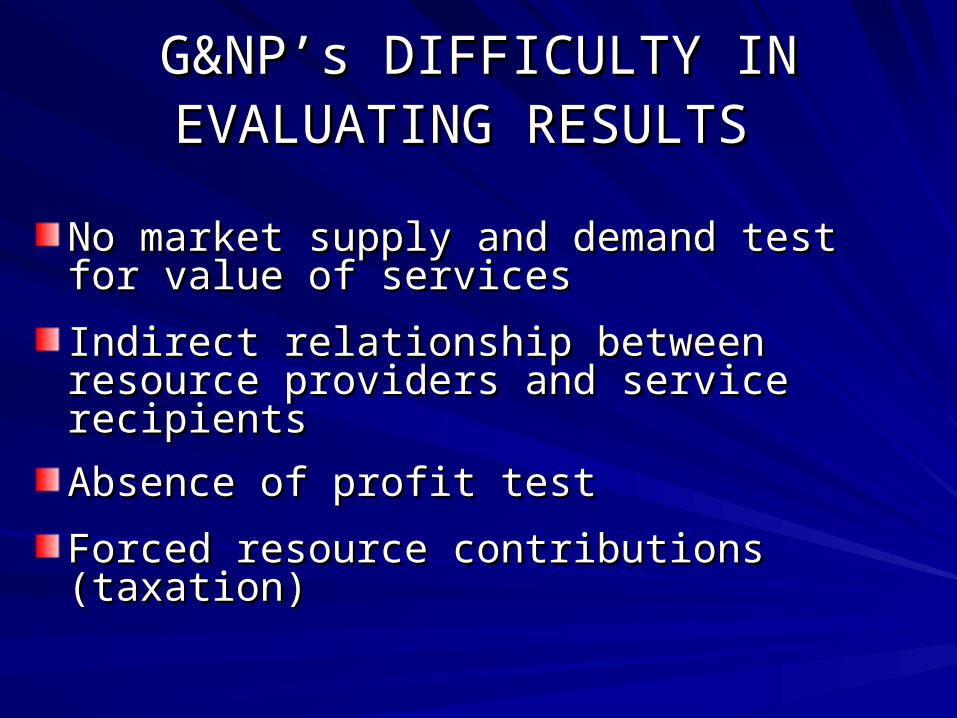

G&NP’s DIFFICULTY IN G&NP’s DIFFICULTY IN EVALUATING RESULTSEVALUATING RESULTS

No market supply and demand test for value No market supply and demand test for value of servicesof services

Indirect relationship between resource Indirect relationship between resource providers and service recipientsproviders and service recipients

Absence of profit testAbsence of profit test

Forced resource contributions (taxation)Forced resource contributions (taxation)

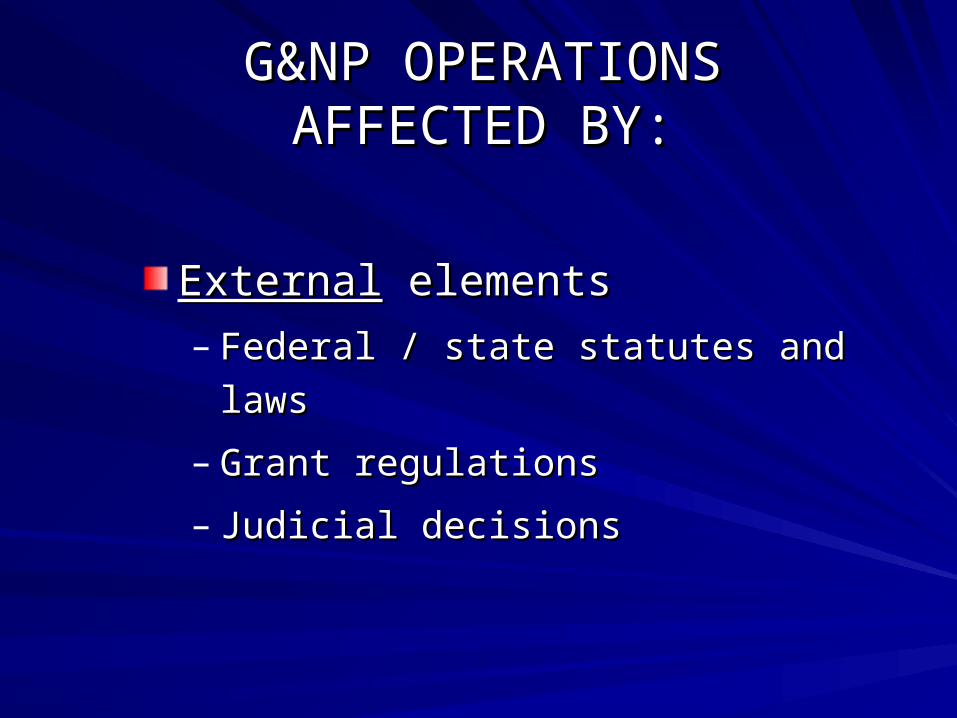

G&NP OPERATIONSG&NP OPERATIONSAFFECTED BY:AFFECTED BY:

ExternalExternal elements elements

– Federal / state statutes and lawsFederal / state statutes and laws

– Grant regulationsGrant regulations

– Judicial decisionsJudicial decisions

G&NP OPERATIONSG&NP OPERATIONSAFFECTED BY:AFFECTED BY:

InternalInternal elements elements

– Charter, by-laws, ordinancesCharter, by-laws, ordinances

– Contractual obligationsContractual obligations

– Trust / donor agreementsTrust / donor agreements

G&NP OPERATIONS REGULATED & G&NP OPERATIONS REGULATED & CONTROLLED BY:CONTROLLED BY:

Organization structureOrganization structure– Governance elected, line of authorityGovernance elected, line of authority

Personnel policies and proceduresPersonnel policies and procedures– Who hires / fires, compensationWho hires / fires, compensation

Source of financial resourcesSource of financial resources– Taxes, debt and rate limits Taxes, debt and rate limits

(Continued)(Continued)

G&NP OPERATIONS REGULATED & G&NP OPERATIONS REGULATED & CONTROLLED BY:CONTROLLED BY:

Use of financial resourcesUse of financial resources

– Restricted, budgeting, purchasingRestricted, budgeting, purchasing

Accounting and financial reportingAccounting and financial reporting

– Structure, reporting types, recipientsStructure, reporting types, recipients

AuditingAuditing– Who, frequency, scope, grantsWho, frequency, scope, grants

ACCOUNTING & FINANCIAL ACCOUNTING & FINANCIAL REPORTING OBJECTIVESREPORTING OBJECTIVES

Making resource allocation decisionsMaking resource allocation decisions

Setting goals and objectivesSetting goals and objectives

Directing and controlling resourcesDirecting and controlling resources

Reporting on resource custodianshipReporting on resource custodianship

Contributing to efficiency and effectivenessContributing to efficiency and effectivenessAmerican Accounting AssociationAmerican Accounting Association

ACCOUNTING & FINANCIAL ACCOUNTING & FINANCIAL REPORTING OBJECTIVESREPORTING OBJECTIVES

Objectives address needs of Objectives address needs of externalexternal users of financial informationusers of financial information

Managers and other Managers and other internalinternal users have users have specialized needs for financial informationspecialized needs for financial information

FASB - Statement of Financial Accounting Concepts No. 4FASB - Statement of Financial Accounting Concepts No. 4

ACCOUNTING & FINANCIAL ACCOUNTING & FINANCIAL REPORTING OBJECTIVESREPORTING OBJECTIVES

For general purpose For general purpose externalexternal financial reporting: financial reporting:

Making resource allocation decisionsMaking resource allocation decisions

Assessing services and ability to continueAssessing services and ability to continue

Assessing management stewardship responsibilities Assessing management stewardship responsibilities and performanceand performance

FASB - Statement of Financial Accounting Concepts No. 4FASB - Statement of Financial Accounting Concepts No. 4

FINANCIAL REPORTING FINANCIAL REPORTING INFORMATION NEEDSINFORMATION NEEDS

Economic resources, obligations, net resourcesEconomic resources, obligations, net resources

Effects of transactions / events on resourcesEffects of transactions / events on resources

Performance measurement of resource changesPerformance measurement of resource changes

Service efforts and accomplishmentsService efforts and accomplishments

Sources of cash flows and liquiditySources of cash flows and liquidityFASB - Statement of Financial Accounting Concepts No. 4FASB - Statement of Financial Accounting Concepts No. 4

ACCOUNTING & FINANCIAL ACCOUNTING & FINANCIAL REPORTING CHARACTERISTICSREPORTING CHARACTERISTICS

Remember –Remember –

AccountingAccounting– is a service function andis a service function and– must meet user information needs in a must meet user information needs in a

given environmentgiven environment

Accounting control provisions in Accounting control provisions in

G&NP environmentG&NP environment

ACCOUNTING & FINANCIAL ACCOUNTING & FINANCIAL REPORTING CHARACTERISTICSREPORTING CHARACTERISTICS

Accounting control provisions inAccounting control provisions in

G&NP environmentG&NP environment

– Use of “funds”Use of “funds”– Budgetary controlsBudgetary controls

ACCOUNTING & FINANCIAL ACCOUNTING & FINANCIAL REPORTING CHARACTERISTICSREPORTING CHARACTERISTICS

Therefore, the two most important legal and Therefore, the two most important legal and administrative controls affecting administrative controls affecting governmental and nonprofit accounting and governmental and nonprofit accounting and financial reportingfinancial reporting

1.1. Funds and fund accountingFunds and fund accounting

2.2. BudgetsBudgets and appropriations and appropriations

ACCOUNTING & FINANCIAL ACCOUNTING & FINANCIAL REPORTING CHARACTERISTICSREPORTING CHARACTERISTICS

What are What are key differenceskey differences of government and nonprofit from of government and nonprofit from business accounting & financial reporting?business accounting & financial reporting?

Use of fund accountingUse of fund accounting

Use of special accounting for restricted activitiesUse of special accounting for restricted activities

Presentation of budgetary comparisons in Presentation of budgetary comparisons in connection with regular financial reportingconnection with regular financial reporting

Financial reports are used primarily to:Financial reports are used primarily to: Compare actual financial results with legally adopted Compare actual financial results with legally adopted

budgetbudget Assess financial condition and results of operations Assess financial condition and results of operations Assist in determining compliance with finance-related Assist in determining compliance with finance-related

laws, rules, and regulations of the governmentlaws, rules, and regulations of the government Assist in evaluating efficiency and effectiveness of Assist in evaluating efficiency and effectiveness of

management, its resources and programsmanagement, its resources and programs

DISCUSSION: A large majority of citizens never have DISCUSSION: A large majority of citizens never have the time to evaluate the financial reports of SLGs, but the time to evaluate the financial reports of SLGs, but candidates seeking an elected position (those running candidates seeking an elected position (those running for election) in government, use these reports to attack for election) in government, use these reports to attack the incumbent.the incumbent.

Objectives of Financial Reporting—State and Local Governments (SLG)

Objectives of Financial ReportingObjectives of Financial Reporting

““ACCOUNTABILITYACCOUNTABILITY is the cornerstone of all is the cornerstone of all financial reporting in government,” (GASB financial reporting in government,” (GASB Concepts Statement No. 1Concepts Statement No. 1, par. 56). , par. 56).

Please see the summary of concepts Statement 1.Please see the summary of concepts Statement 1.

What do we mean by accountability?What do we mean by accountability? How does “interperiod equity” relateHow does “interperiod equity” relate

to accountability? to accountability?

These questions are very important!These questions are very important!

Q: What do we mean by accountability?Q: What do we mean by accountability?

A: Accountability arises from the citizens’ A: Accountability arises from the citizens’ “right to know.” It imposes a duty on “right to know.” It imposes a duty on public officials to be accountable to public officials to be accountable to citizens for raising public monies and citizens for raising public monies and how they are spent.how they are spent.

Objectives of Financial Reporting(cont’d)

Q: How does “interperiod equity” relate to Q: How does “interperiod equity” relate to accountability?accountability?

A:A: Interperiod equity is a government’s obligation to Interperiod equity is a government’s obligation to disclose whether current-year revenues were disclose whether current-year revenues were sufficient to pay for current-year benefits—or did sufficient to pay for current-year benefits—or did current citizens defer payments to future taxpayers? current citizens defer payments to future taxpayers?

(In other words, the expenses have been (In other words, the expenses have been incurred now and will be paid later from taxes incurred now and will be paid later from taxes collected in future years.)collected in future years.)

It is important to understand this concept of It is important to understand this concept of “interperiod equity”!“interperiod equity”!

Objectives of Financial Reporting: (cont’d)

Objectives of Financial Reporting—Objectives of Financial Reporting—Federal GovernmentFederal Government

Accountability is also the foundation of Accountability is also the foundation of federalfederal government financial reporting government financial reporting

Federal Accounting Standards Advisory Federal Accounting Standards Advisory Board (FASAB)’s standards are targeted at Board (FASAB)’s standards are targeted at both:both:

internal users (management), and internal users (management), and external usersexternal users

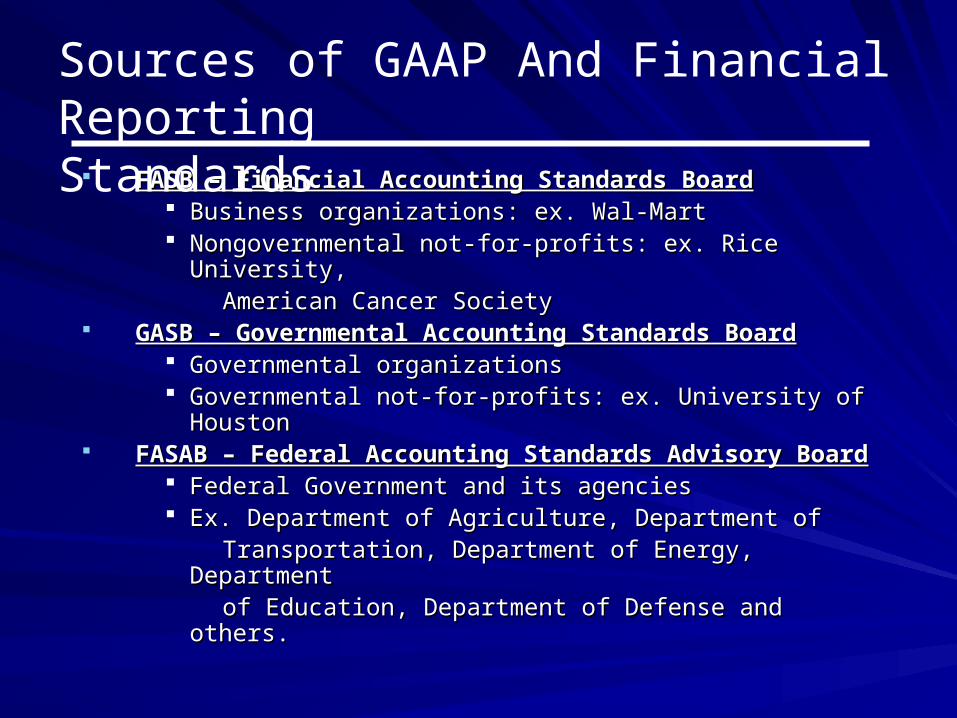

FASB – Financial Accounting Standards BoardFASB – Financial Accounting Standards Board Business organizations: ex. Wal-MartBusiness organizations: ex. Wal-Mart Nongovernmental not-for-profits: ex. Rice University, Nongovernmental not-for-profits: ex. Rice University, American Cancer SocietyAmerican Cancer Society

GASB – Governmental Accounting Standards BoardGASB – Governmental Accounting Standards Board Governmental organizationsGovernmental organizations Governmental not-for-profits: ex. University of HoustonGovernmental not-for-profits: ex. University of Houston

FASAB – Federal Accounting Standards Advisory BoardFASAB – Federal Accounting Standards Advisory Board Federal Government and its agenciesFederal Government and its agencies Ex. Department of Agriculture, Department of Ex. Department of Agriculture, Department of Transportation, Department of Energy, Department Transportation, Department of Energy, Department of Education, Department of Defense and others.of Education, Department of Defense and others.

Sources of GAAP And Financial Reporting Standards

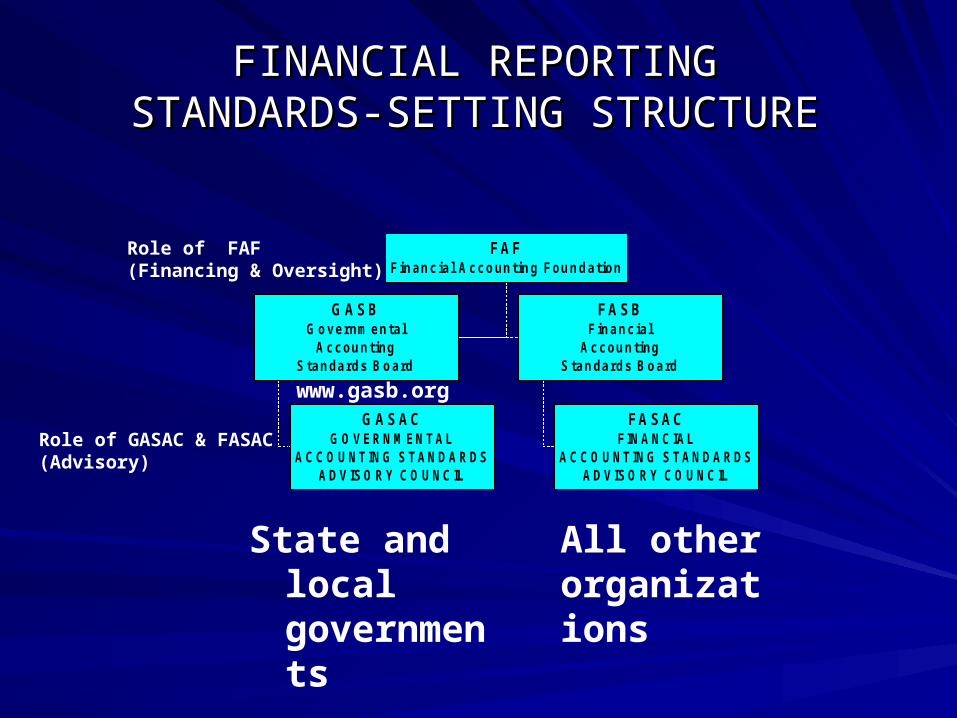

FINANCIAL REPORTINGFINANCIAL REPORTINGSTANDARDS-SETTING STRUCTURESTANDARDS-SETTING STRUCTURE

G A S ACG O VERNM ENT AL

ACCO UNT ING ST ANDARDSADVISO RY CO UNCIL

G A S BG overnm ental

AccountingStandards Board

F A S ACFINANCIAL

ACCO UNT ING ST ANDARDSADVISO RY CO UNCIL

F A S BFinancial

AccountingStandards Board

F AFFinancial Accounting Foundation

State and local governments

All other organizations

www.gasb.org

Role of FAF(Financing & Oversight)

Role of GASAC & FASAC(Advisory)

GASB and FASBGASB and FASB

The objectives of both GASB and FASB:The objectives of both GASB and FASB: Endorse the notion that financial reporting Endorse the notion that financial reporting

encompasses information on service efforts encompasses information on service efforts and accomplishments.and accomplishments.

Emphasize that the ability to measure Emphasize that the ability to measure accomplishments is still undeveloped. accomplishments is still undeveloped.

View this aspect of performance reporting as View this aspect of performance reporting as a long-term goal rather than an immediate a long-term goal rather than an immediate imperative.imperative.

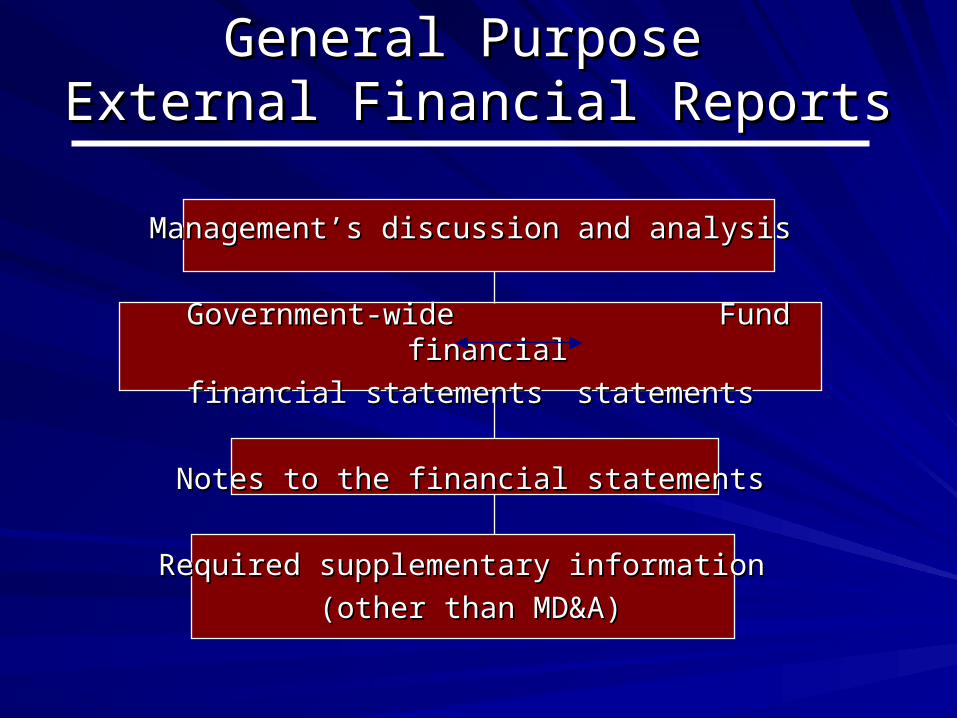

General Purpose General Purpose External Financial ReportsExternal Financial Reports

Management’s discussion and analysisManagement’s discussion and analysis

Government-wideGovernment-wide Fund financial Fund financial

financial statementsfinancial statements statementsstatements

Notes to the financial statementsNotes to the financial statements

Required supplementary information Required supplementary information

(other than MD&A)(other than MD&A)

Comprehensive Annual Financial Report Comprehensive Annual Financial Report (CAFR) -- recommended, but not (CAFR) -- recommended, but not

mandatory --mandatory -- Introductory sectionIntroductory section

Financial section Financial section

Statistical sectionStatistical section

NOTE: A hard copy of the NOTE: A hard copy of the City of Houston’s CAFR is City of Houston’s CAFR is available in Dr. available in Dr. Khumawala’s office for you Khumawala’s office for you to review if you are to review if you are interested.interested.

CAFR - Introductory SectionCAFR - Introductory Section Title page Title page

Contents page Contents page

Letter of transmittalLetter of transmittal

Other (as desired by management)Other (as desired by management)

You can view online at the City of Houston’s Annual You can view online at the City of Houston’s Annual Reports for the years 2004, 2003, and 2002 at the Reports for the years 2004, 2003, and 2002 at the following link: following link: http://www.ci.houston.tx.uh/mayoroffice/annualreport.html..

Auditor’s report Auditor’s report

MD&AMD&A

Basic Financial StatementsBasic Financial Statements

Required Supplementary InformationRequired Supplementary InformationRSI (Other than MD&A)RSI (Other than MD&A)

Combining the individual fundCombining the individual fundstatements and schedulesstatements and schedules

Remember GASB Statement No. 34 is the Remember GASB Statement No. 34 is the NEWNEW reporting reporting model that SLGs model that SLGs have to followhave to follow..

This is the NEW GAAP!!!This is the NEW GAAP!!!

CAFR—Financial Section CAFR—Financial Section (GASB Statement No. 34)(GASB Statement No. 34)

Management’s Discussion and Analysis (MD&A)

Brief objective narrative providing management’s analysis of the government’s financial performance

This is basically “Tell It Like It is.”

Basic Financial StatementsBasic Financial Statements

Government-wide Financial StatementsGovernment-wide Financial Statements

Statement of Net Assets Statement of Net Assets

Statement of Activities Statement of Activities

Fund Financial Statements (see next Fund Financial Statements (see next slide)slide)

Notes to the Financial StatementsNotes to the Financial Statements

The Government-wide Financial The Government-wide Financial Statements are required under GASB Statements are required under GASB 34.34.

Fund Financial StatementsFund Financial Statements

Balance Sheet - Governmental Funds Balance Sheet - Governmental Funds

Statement of Revenues, Expenditures, and Changes Statement of Revenues, Expenditures, and Changes in Fund Balances - Governmental Funds with in Fund Balances - Governmental Funds with reconciliationreconciliation

Statement of Net Assets - Proprietary Funds Statement of Net Assets - Proprietary Funds

Statement of Revenues, Expenses, and Changes in Statement of Revenues, Expenses, and Changes in Fund Net Assets - Proprietary Funds Fund Net Assets - Proprietary Funds

Statement of Cash Flows - Proprietary Funds Statement of Cash Flows - Proprietary Funds

Statement of Fiduciary Net Assets Statement of Fiduciary Net Assets

Statement of Changes in Fiduciary Net Assets Statement of Changes in Fiduciary Net Assets

Fund accounting reports financial information Fund accounting reports financial information for separate self-balancing sets of accounts, for separate self-balancing sets of accounts, segregated for separate purposes or to account segregated for separate purposes or to account for resources restricted as to use by donors or for resources restricted as to use by donors or grantors grantors

Funds are separate accounting and fiscal Funds are separate accounting and fiscal entitiesentities

Fund Accounting

FUNDS & FUND ACCOUNTINGFUNDS & FUND ACCOUNTING

Purpose –Purpose –

To control and segregate resources that are To control and segregate resources that are – externally restrictedexternally restricted and and – internally (managerially) designatedinternally (managerially) designated

To ensure and demonstrate compliance with To ensure and demonstrate compliance with legallegal and and administrativeadministrative requirements requirements

FUNDS & FUND ACCOUNTINGFUNDS & FUND ACCOUNTING

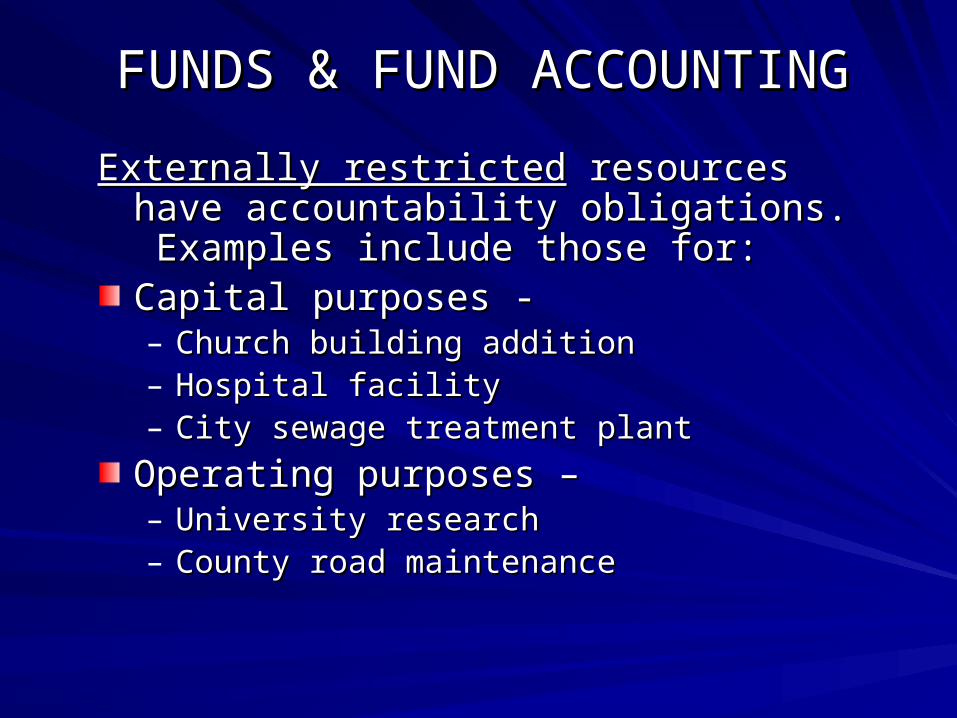

Externally restrictedExternally restricted resources have resources have accountability obligations. Examples accountability obligations. Examples include those for:include those for:Capital purposes - Capital purposes - – Church building additionChurch building addition– Hospital facilityHospital facility– City sewage treatment plantCity sewage treatment plant

Operating purposes –Operating purposes –– University researchUniversity research– County road maintenanceCounty road maintenance

FUNDS & FUND ACCOUNTINGFUNDS & FUND ACCOUNTING

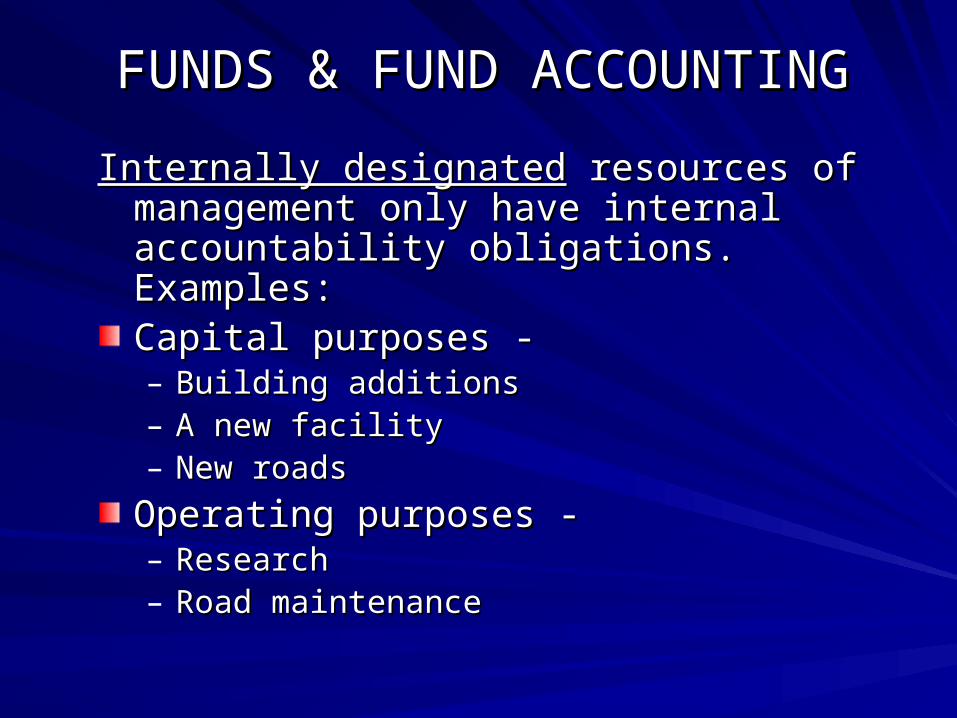

Internally designatedInternally designated resources of resources of management only have internal management only have internal accountability obligations. Examples:accountability obligations. Examples:Capital purposes -Capital purposes -– Building additionsBuilding additions– A new facilityA new facility– New roadsNew roads

Operating purposes -Operating purposes -– ResearchResearch– Road maintenanceRoad maintenance

FUNDS & FUND ACCOUNTINGFUNDS & FUND ACCOUNTING

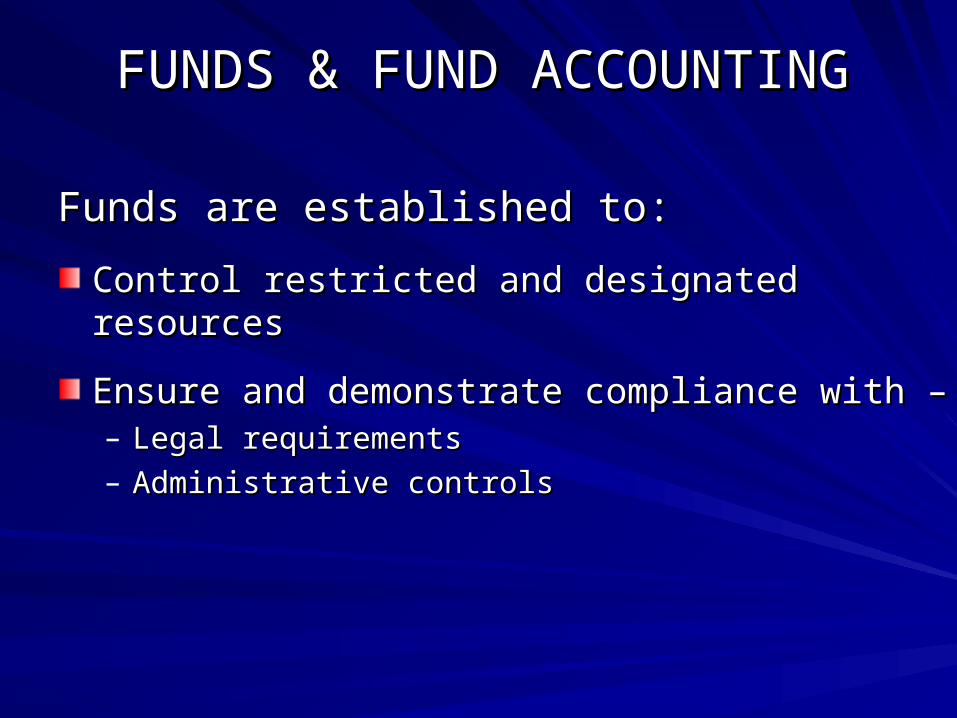

Funds are established to:Funds are established to:

Control restricted and designated resourcesControl restricted and designated resources

Ensure and demonstrate compliance with –Ensure and demonstrate compliance with –– Legal requirementsLegal requirements– Administrative controlsAdministrative controls

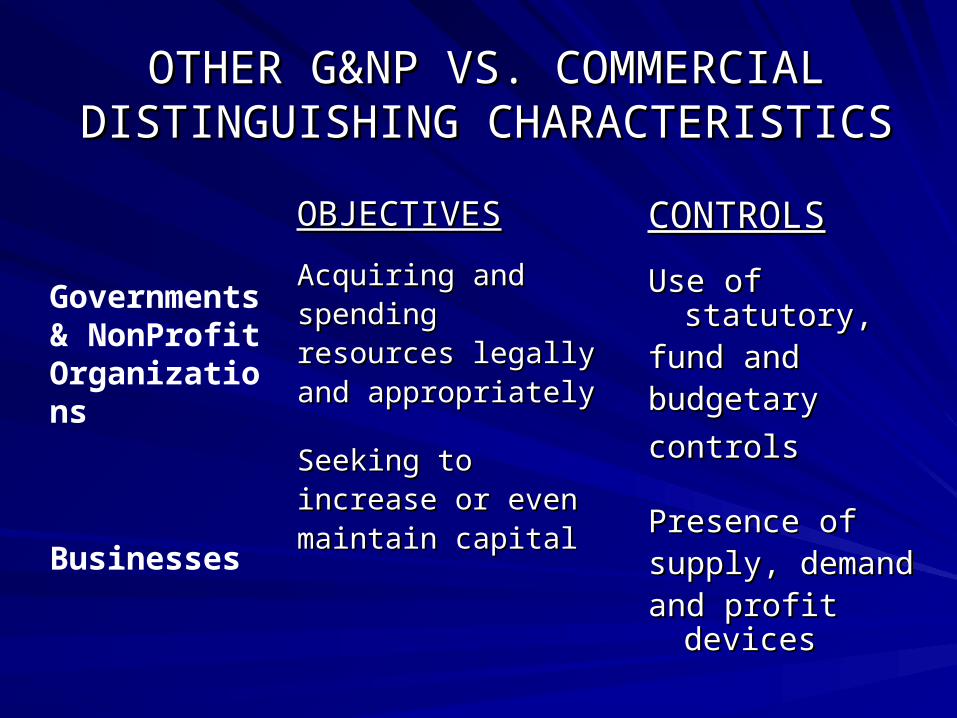

OTHER G&NP VS. COMMERCIAL OTHER G&NP VS. COMMERCIAL DISTINGUISHING CHARACTERISTICSDISTINGUISHING CHARACTERISTICS

OBJECTIVESOBJECTIVES

Acquiring andAcquiring andspendingspendingresources legallyresources legallyand appropriatelyand appropriately

Seeking toSeeking toincrease or evenincrease or evenmaintain capitalmaintain capital

CONTROLSCONTROLS

Use of statutory,Use of statutory,fund andfund andbudgetarybudgetary

controlscontrols

Presence ofPresence ofsupply, demandsupply, demandand profit devicesand profit devices

Governments & NonProfitOrganizations

Businesses

G&NP / COMMERCIAL G&NP / COMMERCIAL ACCOUNTING DIFFERENCESACCOUNTING DIFFERENCES

Compliance control and accountability in Compliance control and accountability in government and nonprofit organizations government and nonprofit organizations result in different concepts and terms in-result in different concepts and terms in-

AccountingAccounting

Financial reportingFinancial reporting

AuditingAuditing

G&NP / COMMERCIAL G&NP / COMMERCIAL ACCOUNTING DIFFERENCESACCOUNTING DIFFERENCES

Different meaning of terminology –Different meaning of terminology –

– Accounting entity = fundAccounting entity = fund– Reporting entity = entire organizationReporting entity = entire organization– Periodicity = flow of annual financial resourcesPeriodicity = flow of annual financial resources– Matching = use in business-type activities onlyMatching = use in business-type activities only– Going concern = business-type activitiesGoing concern = business-type activities