pathfinder fnd nov2010

TRANSCRIPT

THE INSTITUTE OF CHARTERED ACCOUNTANTS

OF NIGERIA

NOVEMBER 2010 FOUNDATION EXAMINATION

Question Papers

Suggested Solutions

Plus

Examiners’ Reports

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

1

FOREWORD

This issue of the PATHFINDER is published principally, in response to a growing

demand for an aid to:

(i) Candidates preparing to write future examinations of the Institute of

Chartered Accountants of Nigeria (ICAN);

(ii) Unsuccessful candidates in the identification of those areas in which they

lost marks and need to improve their knowledge and presentation;

(iii) Lecturers and students interested in acquisition of knowledge in the relevant

subjects contained herein; and

(iv) The profession; in improving pre-examinations and screening processes, and

thus the professional performance of candidates.

The answers provided in this publication do not exhaust all possible alternative

approaches to solving these questions. Efforts had been made to use the methods,

which will save much of the scarce examination time. Also, in order to facilitate

teaching, questions may be altered slightly so that some principles or application of

them may be more clearly demonstrated.

It is hoped that the suggested answers will prove to be of tremendous assistance to

students and those who assist them in their preparations for the Institute’s

Examinations.

NOTES

Although these suggested solutions have been published

under the Institute’s name, they do not represent the views of

the Council of the Institute. The suggested solutions are

entirely the responsibility of their authors and the Institute

will not enter into any correspondence on them.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

2

TABLE OF CONTENTS

SUBJECT PAGES

FUNDAMENTALS OF FINANCIAL ACCOUNTING 3 – 32

ECONOMICS AND BUSINESS ENVIRONMENT 33 – 55

CORPORATE AND BUSINESS LAW 56 – 78

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

3

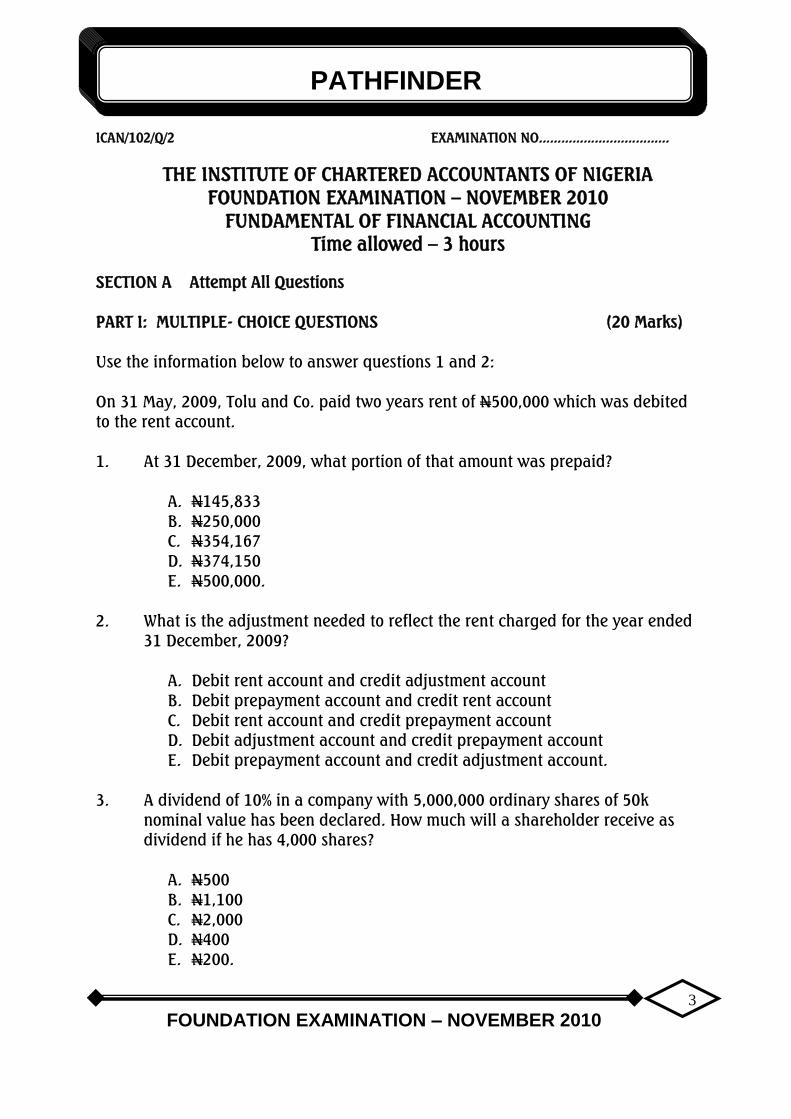

ICAN/102/Q/2 EXAMINATION NO...................................

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF NIGERIA

FOUNDATION EXAMINATION – NOVEMBER 2010

FUNDAMENTAL OF FINANCIAL ACCOUNTING

Time allowed – 3 hours

SECTION A Attempt All Questions

PART I: MULTIPLE- CHOICE QUESTIONS (20 Marks)

Use the information below to answer questions 1 and 2:

On 31 May, 2009, Tolu and Co. paid two years rent of N500,000 which was debited

to the rent account.

1. At 31 December, 2009, what portion of that amount was prepaid?

A. N145,833

B. N250,000

C. N354,167

D. N374,150

E. N500,000.

2. What is the adjustment needed to reflect the rent charged for the year ended

31 December, 2009?

A. Debit rent account and credit adjustment account

B. Debit prepayment account and credit rent account

C. Debit rent account and credit prepayment account

D. Debit adjustment account and credit prepayment account

E. Debit prepayment account and credit adjustment account.

3. A dividend of 10% in a company with 5,000,000 ordinary shares of 50k

nominal value has been declared. How much will a shareholder receive as

dividend if he has 4,000 shares?

A. N500

B. N1,100

C. N2,000

D. N400

E. N200.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

4

4. An advantage of the use of the voucher system is that it

A. reduces the number of cheques that will be written during any given period.

B. provides a highly flexible system for handling unusual transactions.

C. provides comprehensive record of business done with particular

supplier

D. ensures that every expenditure is reviewed and verified before

payment is made.

E. reduces the procedure of processing transactions.

5. In which of the following will the provision for bad and doubtful debts be

treated?

A. Trading Account

B. Profit and Loss Account

C. Fund Flow Statement

D. Cash Flow Statement

E. Value Added Statement.

6. When did the Act establishing the Institute of Chartered Accountants of

Nigeria (ICAN) come into being?

A. September 1, 1960

B. September 1, 1963

C. September 1, 1964

D. September 1, 1965

E September 1, 1966.

7. What is the accounting error which occurs as a result of a mistake made in

identifying a customer’s account?

A. Error of principle

B. Error of Commission

C. Error of Identity

D. Error of Complete Reversal of Entries

E. Error of Original Entry.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

5

8. In preparing a bank reconciliation statement, what action is required when a

bank statement does not show a credit balance?

A. Unpresented cheques are added to the balance as per bank statement

B. Uncredited lodgements are added to the balance as per bank

statement

C. Unpresented cheques are deducted from the balance as per bank

statement

D. Uncredited lodgements are deducted from the balance as per bank

statement

E. Unpresented cheques and uncredited lodgements are added to the

balance as per bank statement.

9. What is the name of the fore-runner of The Institute of Chartered Accountants

of Nigeria (ICAN)?

A. The Association of Professional Accountants of Nigeria

B. The Association of Professional Accountants in Nigeria

C. The Association of Accountants in Nigeria

D. The Association of Registered Accountants in Nigeria

E. The Association of Body of Accountants in Nigeria.

10. X and Y are in partnership without any agreement. If Z is admitted as a new

partner to take one-fifth as his share of profit, what should be the new

profits and losses sharing ratio of the partners?

A. X =1/3, Y =1/3 , Z = 1/5

B. X =1/5 , Y=1/5 , Z =1/5

C. X =2/5, Y= 2/5, Z = 1/5

D. X = 2/5, Y =1/5, Z =1/5

E. X = 2/5, Y= 3/5, Z = 1/5.

11. Which of the following is the purpose of maintaining a Branch Stock Account

at selling price in the head office books?

A. To check the excess of the head office members of staff

B. To check the excess of the management staff at the head of office

C. To check the excess of the customers

D. To check the excess of the members of staff at the branch

E. To check the excess of the transporter of the goods to the branch.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

6

12. What differentiates a private company from a public company?

A. It does not restrict the right to transfer its shares

B. It cannot invite members of the public to subscribe for its shares

C. Majority of its shares may be owned by one person

D. It can only offer its shares to members of the public for subscription

E. It does not require a certificate of incorporation.

13. What is the prime book of entry for motor vehicle bought on credit?

A. Purchases Day Book

B. Motor Vehicles Book

C. Creditors Book

D. Journal Proper

E. Motor Vehicle Register.

14. A cheque payment posted to the credit side of the cash book, but not in the

debit column of the bank statement, is

A. uncredited cheque

B. dishonoured cheque

C. standing order

D. unpresented cheque

E. undebited cheque.

15. Assigning revenue to the accounting period in which goods are sold or

services rendered and expenses incurred is known as

A. apportionment concept

B. consistency concept

C. accrual concept

D. revenue recognition concept

E. matching concept.

16. Which of the following describes an accounting year?

A. Time span during which taxes are paid to the Inland Revenue

B. Time span during which budget is prepared

C. Time span, usually one year, as disclosed by financial statements

D. Time span, usually one year, during which the economic viability of a

business enterprise is determined

E. Time span, usually one year, during which all financial transactions must

be concluded.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

7

17. Which of the following is NOT correct?

Assets Liabilities Capital

N N N

A. 390,000 120,000 270,000

B. 820,000 280,000 540,000

C. 392,500 62,500 330,000

D. 327,000 56,000 271,000

E. 477,750 57,500 410,000

18. What is the effect of overstated closing stock?

A. Understated gross profit

B. Overstated purchases

C. Understated sales

D. Overstated gross profit

E. Understated net profit.

19. What accounting entries are necessary for recording profit loading on goods

sent to the branch?

A. Credit Branch Stock Account and credit Branch Stock Adjustment

Account

B. Debit Branch Stock Account and credit Branch Stock Adjustment

Account

C. Debit Branch Stock Adjustment Account and credit Branch Stock

Account

D. Credit Branch Account and debit Goods Sent to Branch Account

E. Debit Goods Sent to Branch Account and credit Branch Stock Account.

20. What is a partner who has full powers of participating in the conduct of a

partnership business called?

A. Limited Partner

B. Sleeping Partner

C. General Partner

D. Nominal Partner

E. Special Partner.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

8

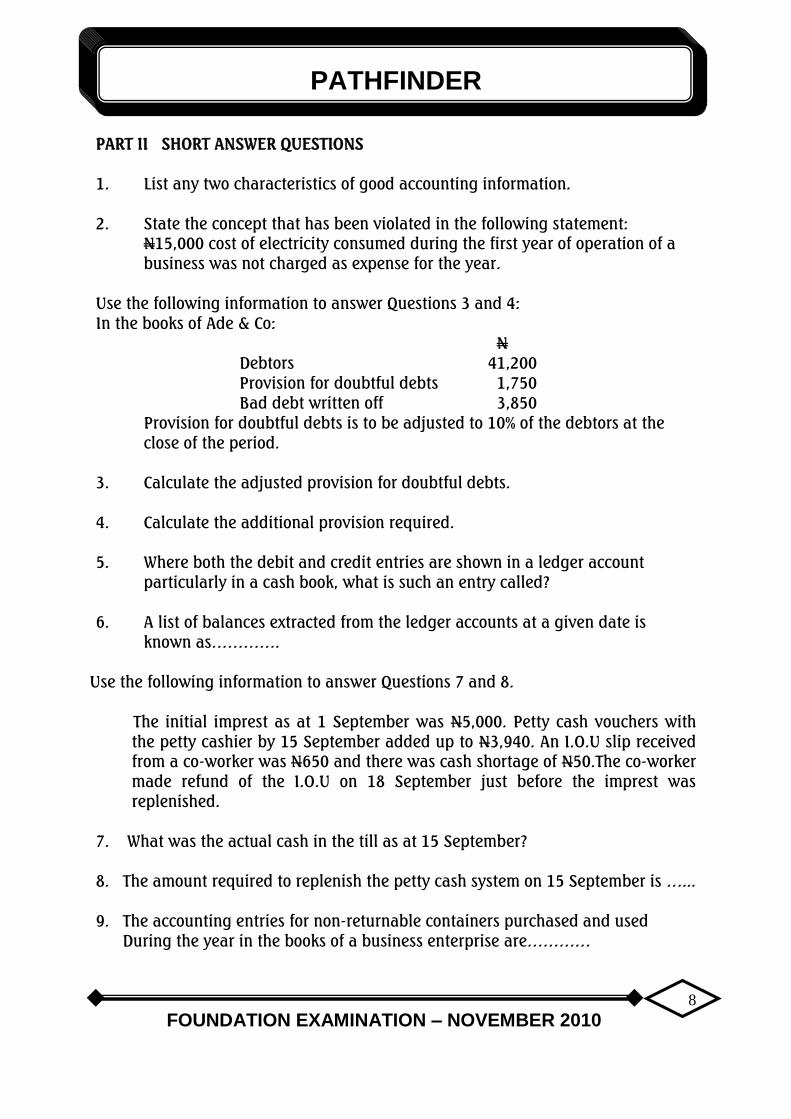

PART II SHORT ANSWER QUESTIONS

1. List any two characteristics of good accounting information.

2. State the concept that has been violated in the following statement:

N15,000 cost of electricity consumed during the first year of operation of a

business was not charged as expense for the year.

Use the following information to answer Questions 3 and 4:

In the books of Ade & Co:

N

Debtors 41,200

Provision for doubtful debts 1,750

Bad debt written off 3,850

Provision for doubtful debts is to be adjusted to 10% of the debtors at the

close of the period.

3. Calculate the adjusted provision for doubtful debts.

4. Calculate the additional provision required.

5. Where both the debit and credit entries are shown in a ledger account

particularly in a cash book, what is such an entry called?

6. A list of balances extracted from the ledger accounts at a given date is

known as………….

Use the following information to answer Questions 7 and 8.

The initial imprest as at 1 September was N5,000. Petty cash vouchers with

the petty cashier by 15 September added up to N3,940. An I.O.U slip received

from a co-worker was N650 and there was cash shortage of N50.The co-worker

made refund of the I.O.U on 18 September just before the imprest was

replenished.

7. What was the actual cash in the till as at 15 September?

8. The amount required to replenish the petty cash system on 15 September is …...

9. The accounting entries for non-returnable containers purchased and used

During the year in the books of a business enterprise are…………

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

9

10. A non-permanent or ad-hoc relationship which subsists between persons or

organizations carrying on a business in common with a view to making and

sharing profits therefrom in an agreed proportion is called……………….

11. State the type of rights that deals with special freedom granted by an owner

of intellectual property for others to produce and sell certain quantities of

the work at an agreed fee for a specific period.

12. The total of the discount column in the credit side of the cash book is posted

to the……………..

13. James returned part of the goods bought on credit worth N5,000 to XY

Enterprises due to defects. What document should James receive from XY

Enterprises?

14. ZY Enterprises Ltd bought AB Enterprises by issuing 3,000,000 ordinary

shares of 50k each at a discount of 5%.The assets of the vendor were Stock

N900,000 and Debtors N550,000.What is the purchase consideration?

15. Excess of purchase consideration over the fair value of the vendor’s assets is

called …………..

16. Prepaid rent of N650 had been recorded as N560.This is an error of………….

Use the following information to answer questions 17 and 18:

ZAX Ltd issued 2,000,000 ordinary shares at N1 each from its authorized

share capital of 3,000,000 ordinary shares of N1 each. At the end of the

first call, all shareholders paid in full, except for one subscriber who owes

N100,000.

17. What is the company’s paid up capital?

18. What is the uncalled- up- capital of the company?

19. Verification of the outcome of a joint venture is carried out in the ………..

20. The accounting entries for proceeds of scrapped containers using Containers

Trading Account Method are…………….

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

10

SECTION B ATTEMPT ANY FOUR QUESTIONS

QUESTION 1

Dawadu is the petty cashier of Royal Palms Ltd. She gets her reimbursement from

Ajayi, the main cashier. Expenses below N1,000 are usually paid by Dawadu out of

her weekly imprest of N20,000. Midway into the second week, she had gone to

Ajayi for reimbursement the second time. The main cashier is surprised at the rate

Dawadu is disbursing the petty cash float and has therefore, demanded to see her

petty cash book together with the accompanying receipts/invoices before granting

the reimbursement. Dawadu has called for your assistance in writing her books

from the following transactions that were incurred for the first eight days, duly

backed up by receipts/ invoices. The book has the columns for Postages and

Telephone, Travelling expenses, Office expenses, and Electricity.

Date Description of transactions.

Feb. 2009.

1. Received petty cash float from the main cashier. Bought postage stamps of

N450 for office use. Paid N575 for the carriage of palm kernels to the

warehouse.

2. Paid three petty cash vouchers for staff on official travels to Port Harcourt,

amounting to N9,090.

3. Bought petty cash register for N1,200; office stationery for N3,685; and tea

cups of N750 for office use and office electricity bill of N2,250 was paid.

4. Paid telephone bills of N1,750 and paid N120 for courier services.

5. Bought brooms for cleaners’ use in the office for N90.

6. Paid N3,750 for the repairs of office machines.

7. Bought postage stamps of N600, paid telephone bills of N1,200 and

travelling expenses of N300.

8. Bought copier papers of N4,500 for office use. She was instructed to pay in

respect of three ceiling fans bought for N9,600.

You are required to:

(a) Prepare the Petty Cash Book for the period. (11 Marks)

(b) State how these transactions will be treated in the ledgers. (4 Marks)

(Total 15 Marks)

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

11

QUESTION 2

The following transactions took place between Lexus Enterprises of 15, Kumapayi

Street, Lagos and its customer, Vitamix Ventures of 7, Inalende Lane, Ibadan in

April,2009:

April 1 Amount outstanding N291,000.

2 Invoiced N73,600 goods on invoice number 036.

3 Invoiced N25,000 goods on invoice number 039.

3 Carriage outwards N3,000, charged to the customer.

7 Received cheque of N276,440 from Vitamix Ventures.

7 Discount Allowed N1,456, to Vitamix Ventures.

8 Invoiced N91,000 goods on invoice number 053.

11 Invoiced N298,000 goods on invoice number 075.

12 Credit Note number 215 for N1,680.

12 Received cheque of N620,000 from Vitamix Ventures.

17 Forwarded N130,000 goods on invoice number 100.

29 Carriage outwards N2,800 charged to the customer.

29 Forwarded N161,000 goods on invoice number 153.

30 Interest on outstanding balance N962.

You are required to prepare:

a) A Vitamix Ventures Account in the books of Lexus Enterprises. (10 Marks)

b) Customer’s Statement of Account for the month of April 2009. (5 Marks)

(Total 15 Marks)

QUESTION 3

Jato is a trader and does not keep a complete set of accounting records. A summary

of his bank and cash transactions for the year ended 31 March 2009 is as follows:

Receipts Cash Bank

N N

Balance in hand - 1 April 2008 4,200 -

Balance at bank - 1 April 2008 - 588,840

Cash Sales - 921,200

Credit Sales - 828,800

Part of business premises sublet 14,560 -

Proceeds of sale of old furniture 2,800 -

Dividend from private investment - 49,000

Cash from bank 341,040

362,600 2,387,840

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

12

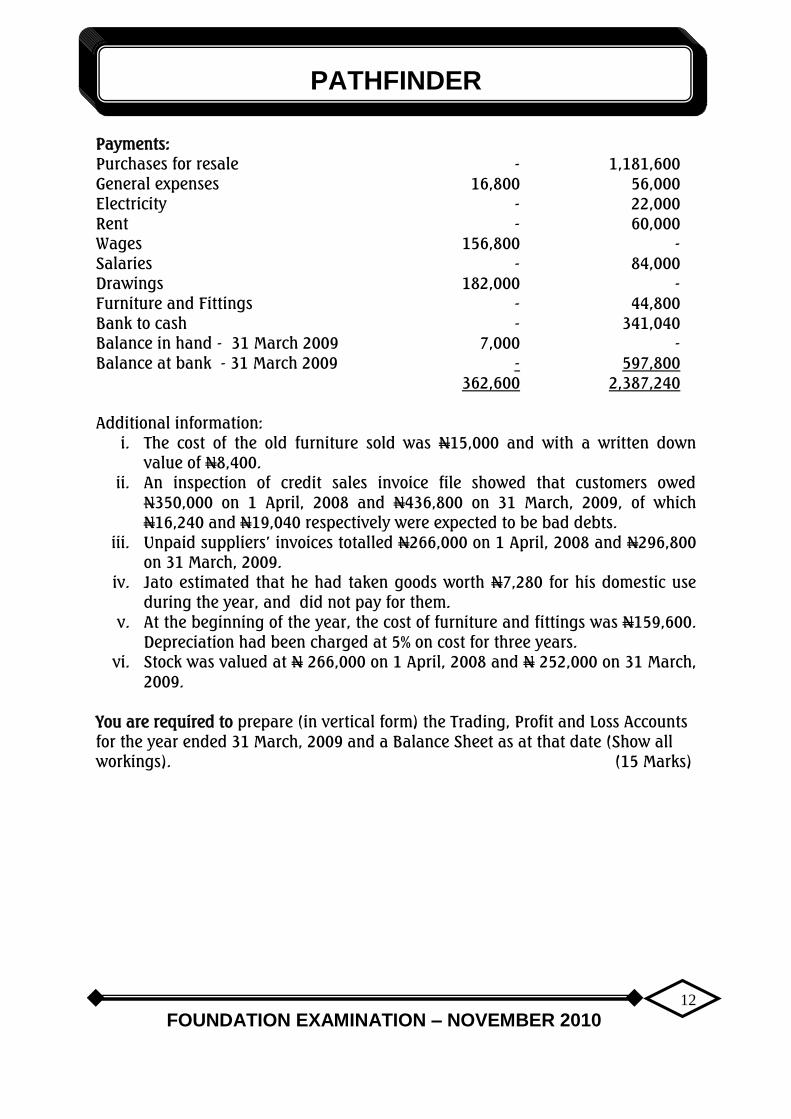

Payments:

Purchases for resale - 1,181,600

General expenses 16,800 56,000

Electricity - 22,000

Rent - 60,000

Wages 156,800 -

Salaries - 84,000

Drawings 182,000 -

Furniture and Fittings - 44,800

Bank to cash - 341,040

Balance in hand - 31 March 2009 7,000 -

Balance at bank - 31 March 2009 - 597,800

362,600 2,387,240

Additional information:

i. The cost of the old furniture sold was N15,000 and with a written down

value of N8,400.

ii. An inspection of credit sales invoice file showed that customers owed

N350,000 on 1 April, 2008 and N436,800 on 31 March, 2009, of which

N16,240 and N19,040 respectively were expected to be bad debts.

iii. Unpaid suppliers’ invoices totalled N266,000 on 1 April, 2008 and N296,800

on 31 March, 2009.

iv. Jato estimated that he had taken goods worth N7,280 for his domestic use

during the year, and did not pay for them.

v. At the beginning of the year, the cost of furniture and fittings was N159,600.

Depreciation had been charged at 5% on cost for three years.

vi. Stock was valued at N 266,000 on 1 April, 2008 and N 252,000 on 31 March,

2009.

You are required to prepare (in vertical form) the Trading, Profit and Loss Accounts

for the year ended 31 March, 2009 and a Balance Sheet as at that date (Show all

workings). (15 Marks)

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

13

QUESTION 4

Rosa and Frank were partners sharing profits/losses in the ratio Rosa two-thirds;

Frank one-third.

Balance Sheet as at 31 December, 2009

N N

Capital Accounts: Motor Vehicles 2,000,000

Rosa 1,973,500 Office Equipment 375,000

Frank 1,630,000 Furniture & Fittings 127,500

3,603,500 Debtors 585,000

Stock 960,000

Creditors 583,500 Cash at Bank 139,500

4,187,000 4,187,000

On 1 January, 2010 Rosa and Frank agreed to admit Danladi into the partnership

giving him one-fifth share of profits. Danladi is to bring in capital to the extent of

one-quarter of the combined capitals of Rosa and Frank, after adjusting for the

value of goodwill at N1,000,000. The assets were revalued as follows:

Office Equipment N1,275,000; Furniture & Fittings N90,000; Motor Vehicles

N1,800,000; Stock N1,014,000; Debtors N561,000. The old partners’ proportion of

profits and losses in the new firm of Rosa, Frank and Danladi are to be in the same

ratio between themselves as before, assuming Danladi will bring in the required

cash as capital.

You are required to:

a) Show the entries in the Assets Accounts, the Revaluation Account, and the

Partners’ Capital Accounts. (10 Marks)

b) Prepare a revised Balance Sheet (after the admission of Danladi).

(3 Marks)

c) State the proportion in which profits and losses will be shared among the

partners in future. (2 Marks)

(Total 15 Marks)

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

14

QUESTION 5

Presented below is the extract of the financial statements of Syllabus Limited as at

31 August, 2009.

Balance Sheet as at 31 August, 2009.

Share Capital Fixed Assets Cost Acc. Dep. NBV

N’000 N’000 N’000 N’000

5,000,000 Ordinary

shares of 50k each 2,500 Land and Buildings 5,250 2,250 3,000

Capital Reserve 500 Plant and Machinery 1,600 400 1,200

Profit & Loss 2,250 Motor Vehicles 1,350 600 750

5,250 Furniture and Fittings 900 300 600

9,100 3,550 5,550

Current Liabilities Current Assets

Creditors 1,200 Stock 850

Taxation 500 Net Debtors 900

Bank Overdraft 550 Cash in hand 200

1,950

7,500 7,500

However, the following information became known before the approval of the

financial statements by the Board of Directors, and it was agreed that they should

be incorporated in order to obtain accurate financial information:

(i) Depreciation of Plant & Machinery and Motor Vehicles which were computed

using straight-line method, was considered insufficient and the rates were to

be increased from 1 September 2009 as follows:-

Plant & Machinery from 10% to 15% and Motor Vehicles from 20% to 25%.

(ii) Stock included in the Balance Sheet at N150,000 which was considered

obsolete had the scrap value of N 25,000.

(iii) Provision for doubtful debts should be increased by N40,000.

(iv) The directors proposed a final dividend of 25% on Ordinary Shares.

(v) The provision for income tax on the profit of the year was estimated to be

N900,000.

(vi) There is contingent liability of N500,000 in respect of a pending court case.

(vii) The company has guaranteed car loan taken from a local bank by the

employees of N 1,100,000, on Balance Sheet date.

(viii) An invoice for raw materials in the sum of N125,000 has been found in a

filing tray. It is evident that this bill has not been passed through the books,

although the materials were included on the stock sheets.

(ix) Salaries and wages bill for the sum of N 500,000 was omitted from the

books.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

15

You are required to prepare:

a) The necessary journal entries to reflect the new developments. (10 Marks)

b) The revised Balance Sheet [in vertical format]of Syllabus Ltd

as at 31 August, 2009. (5 Marks)

(Total 15 Marks)

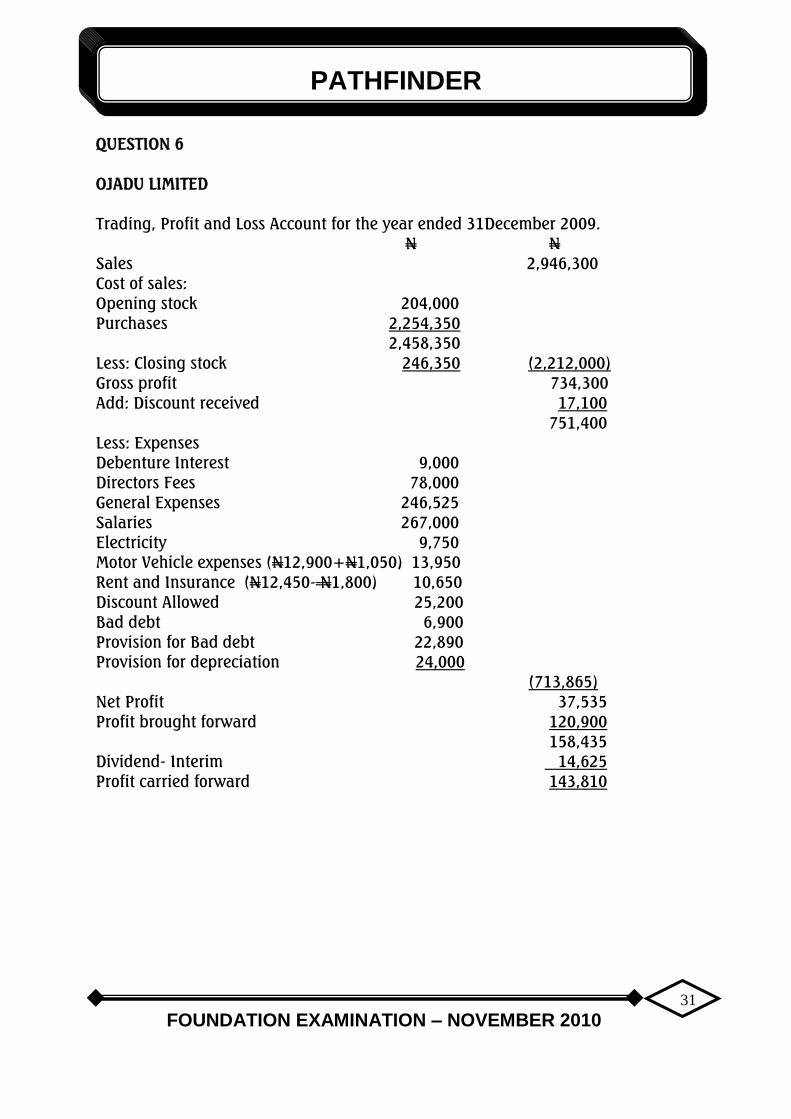

QUESTION 6

The following trial balance was extracted from the books of Ojadu Limited as at 31

December, 2009;

DR CR

N N

Paid Up Capital:

300,000 Ordinary Shares of N1 each 300,000

Share Premium 75,000

Freehold and Buildings(Cost) 316,500

6% Debentures, secured on Land and Building 150,000

Debenture Interest to 30 June 2009 4,500

Motor Vehicle (Cost N120,000) 48,000

Directors’ fees 78,000

Purchases/Sales 2,253,000 2,946,300

Stock 1 January 2009 204,000

General expenses 246,525

Salaries 267,000

Electricity 9,750

Balance at bank 80,850

Interim dividend paid 14,625

Motor Vehicle Expenses 12,900

Rent and Insurance 12,450

Discounts allowed and received 25,200 17,100

Bad debts 6,900

Provision for bad debts 4,800

Debtors and Creditors 276,900 243,000

Profit and Loss Account 1 January 2009 120,900

3,857,100 3,857,100

The following additional information were also available:

(i) The Authorized Share Capital of the company is N600,000 divided into

400,000 Ordinary Shares of N1 each and 200,000 Preference Shares of

N1 each.

(ii) The provision for debenture interest accrued should be made.

(iii) The provision for doubtful debts is to be adjusted to 10% of debtors as at 31

December, 2009.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

16

(iv) Rent and insurance prepaid in 2009 was N1,800.

(v) The provision for depreciation of Motor Vehicles is at the rate of 20% on cost.

(vi) Motor vehicle expenses outstanding at 31 December, 2009 amounted to

N1,050.

(vii) Provision is to be made for final dividend of 7% on the Paid Up Capital.

(viii) Entry is yet to be made in the books for goods purchased from Mama Royal

on credit on 31 December, 2009 amounting to N1,350.These goods were in

transit on 31 December , 2009 and adjustments must be made in the records

to reflect their inclusion.

(ix) At the end of the stock taking on 31 December 2009 the physical stock in the

premises was valued at N245,000.

You are required to prepare a Trading, Profit and Loss Accounts for the year ended

31 December, 2009 and a Balance Sheet as at that date. (15 Marks)

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

17

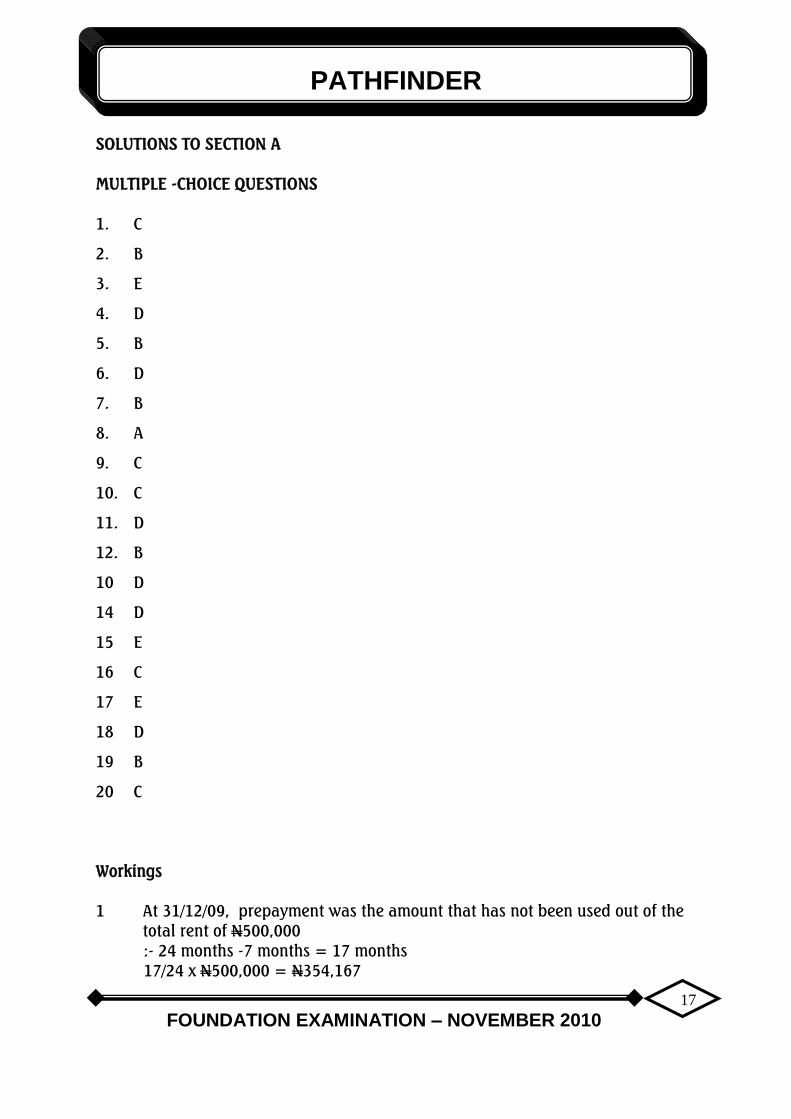

SOLUTIONS TO SECTION A

MULTIPLE -CHOICE QUESTIONS

1. C

2. B

3. E

4. D

5. B

6. D

7. B

8. A

9. C

10. C

11. D

12. B

10 D

14 D

15 E

16 C

17 E

18 D

19 B

20 C

Workings

1 At 31/12/09, prepayment was the amount that has not been used out of the

total rent of N500,000

:- 24 months -7 months = 17 months

17/24 x N500,000 = N354,167

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

18

3. Dividend on 4000 shares =10% x 4,000 x N0.50 = N200

EXAMINERS’ REPORT

The questions test candidates’ knowledge of various sections of the Syllabus. They

were attempted by all candidates and the performance was quite good.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

19

PART II SHORT-ANSWER QUESTIONS

1. Relevance, Timeliness, Accuracy, Sufficiency, Completeness, Adequacy

2. Matching concept /Accrual

3. N3,735

4. N1,985

5. Contra entry

6. Trial balance

7. N360

8 N3,940

9. Dr. Manufacturing Account and Cr. Cash Book

10. Joint Venture

11. Copyright

12. Discount Received Account

13. Credit Note

14. N1,425,000

15. Goodwill

16. Transposition

17. N1,900,000

18. N1,000,000

19. Joint Venture Memorandum Account

20. Dr. Cash Account and Cr. Containers Trading Account

Workings

3. 10% (N41,200- N3,850)= N3,735

4. Additional provision = N(3,735-1,750)= N1,985

This is an expense in the P& L account

7. N(5,000 -3,940 – 650 -50) = N360

10 240,000 + (240,000 divided by 6 x 1) = 280,000 Ordinary shares

14 50k – (5% x 50k) x 3,000,000 Ordinary shares = N1,425,000

17 N2,000,000 – N100,000 = N1,900,000

EXAMINERS’ REPORT

The questions test candidates’ knowledge of various sections of the Syllabus. They

were attempted by all candidates and the performance was quite good.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

20

SOLUTIONS TO SECTION B

QUESTION 1(a)

ROYAL PALMS LTD.

PETTY CASH BOOK

Receipts c/bk

fol.

Date 2009 Particulars Pcv no

folio

Total

payment

Postage

&Teleco

municati

on

Travelli

ng

Office Electricity Furnitu

re

N Balance b/d N N N N N N

20,000 1/2 Postage

stamps

450 450

- - - -

,, Carriage

inwards

575 - 575 - - -

2/2 Traveling exps. 9,090 - 9,090 - - -

4.2 Petty cash

register

1,200 - - 1,200 - -

,, Office

stationary

3,685 - - 3,685 - -

,, Office

expenses

750 - - 750 - -

,, Electricity bills 2,250 - - - 2,250 -

6/2 Telephone bills 1,750 1,750 - - - -

,, Courier 120 120 - - - -

7/2 Office

expenses

90 - - 90 - -

,, 19,960 12,320 9,665 5,725 2,250 -

7/2 Balance C/F 40

N 20,000 20,000

40 8/2 Balance B/F - - - - - -

19,960 ,, Reimbursemen

t

- - - - - -

10/2 Repairs of

machines

3,750 - - 3,750 - -

11/2 Postage

stamps

600 600 - - - -

,, Telephone bills 1,200 1,200 - - - -

,, Traveling exps. 300 - 300 - - -

12/2 photocopypap

ers

4,500 - - 4,500 - -

,, Ceiling fans

fittings

9,600 - - - - 9600

19,950 1,800 300 8,250 - 9600

12/2 Balance c/f 50

20,000 20,000 4,120 9,965 13,975 2,250 960

50 13/2 Balance b/f GL GL GL GL GL

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

21

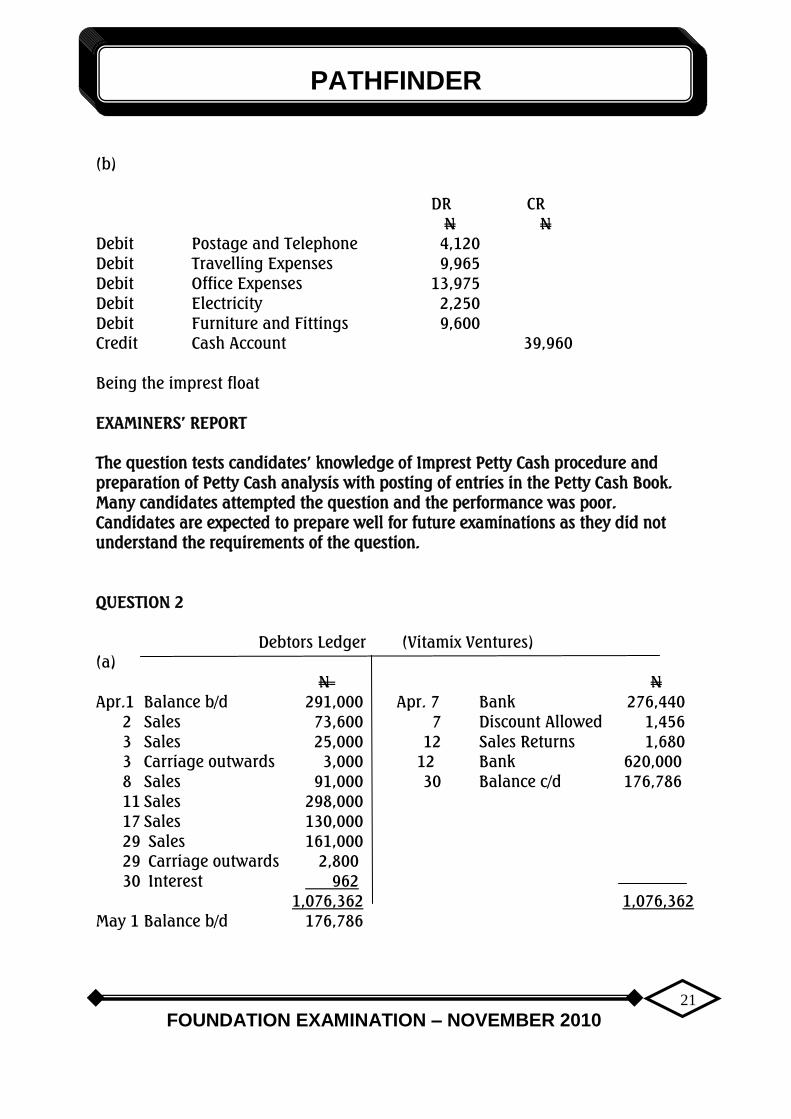

(b)

DR CR

N N

Debit Postage and Telephone 4,120

Debit Travelling Expenses 9,965

Debit Office Expenses 13,975

Debit Electricity 2,250

Debit Furniture and Fittings 9,600

Credit Cash Account 39,960

Being the imprest float

EXAMINERS’ REPORT

The question tests candidates’ knowledge of Imprest Petty Cash procedure and

preparation of Petty Cash analysis with posting of entries in the Petty Cash Book.

Many candidates attempted the question and the performance was poor.

Candidates are expected to prepare well for future examinations as they did not

understand the requirements of the question.

QUESTION 2

Debtors Ledger (Vitamix Ventures)

(a)

N N

Apr.1 Balance b/d 291,000 Apr. 7 Bank 276,440

2 Sales 73,600 7 Discount Allowed 1,456

3 Sales 25,000 12 Sales Returns 1,680

3 Carriage outwards 3,000 12 Bank 620,000

8 Sales 91,000 30 Balance c/d 176,786

11 Sales 298,000

17 Sales 130,000

29 Sales 161,000

29 Carriage outwards 2,800

30 Interest 962

1,076,362 1,076,362

May 1 Balance b/d 176,786

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

22

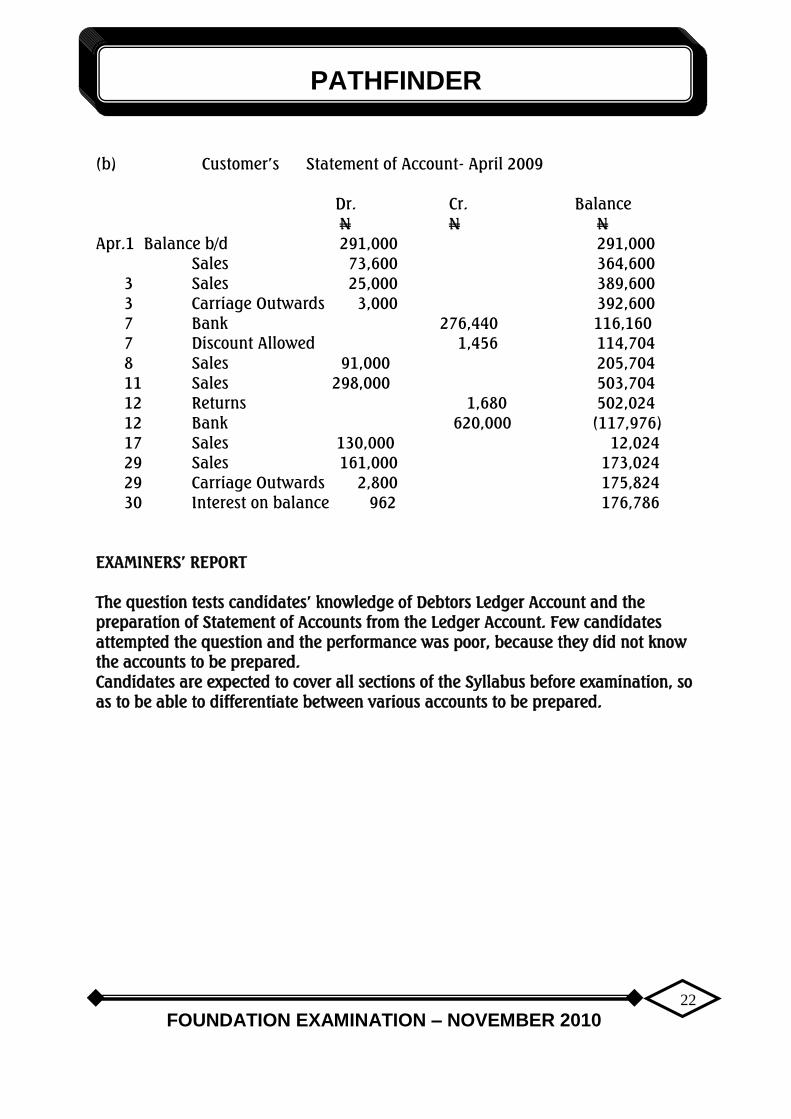

(b) Customer’s Statement of Account- April 2009

Dr. Cr. Balance

N N N

Apr.1 Balance b/d 291,000 291,000

Sales 73,600 364,600

3 Sales 25,000 389,600

3 Carriage Outwards 3,000 392,600

7 Bank 276,440 116,160

7 Discount Allowed 1,456 114,704

8 Sales 91,000 205,704

11 Sales 298,000 503,704

12 Returns 1,680 502,024

12 Bank 620,000 (117,976)

17 Sales 130,000 12,024

29 Sales 161,000 173,024

29 Carriage Outwards 2,800 175,824

30 Interest on balance 962 176,786

EXAMINERS’ REPORT

The question tests candidates’ knowledge of Debtors Ledger Account and the

preparation of Statement of Accounts from the Ledger Account. Few candidates

attempted the question and the performance was poor, because they did not know

the accounts to be prepared.

Candidates are expected to cover all sections of the Syllabus before examination, so

as to be able to differentiate between various accounts to be prepared.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

23

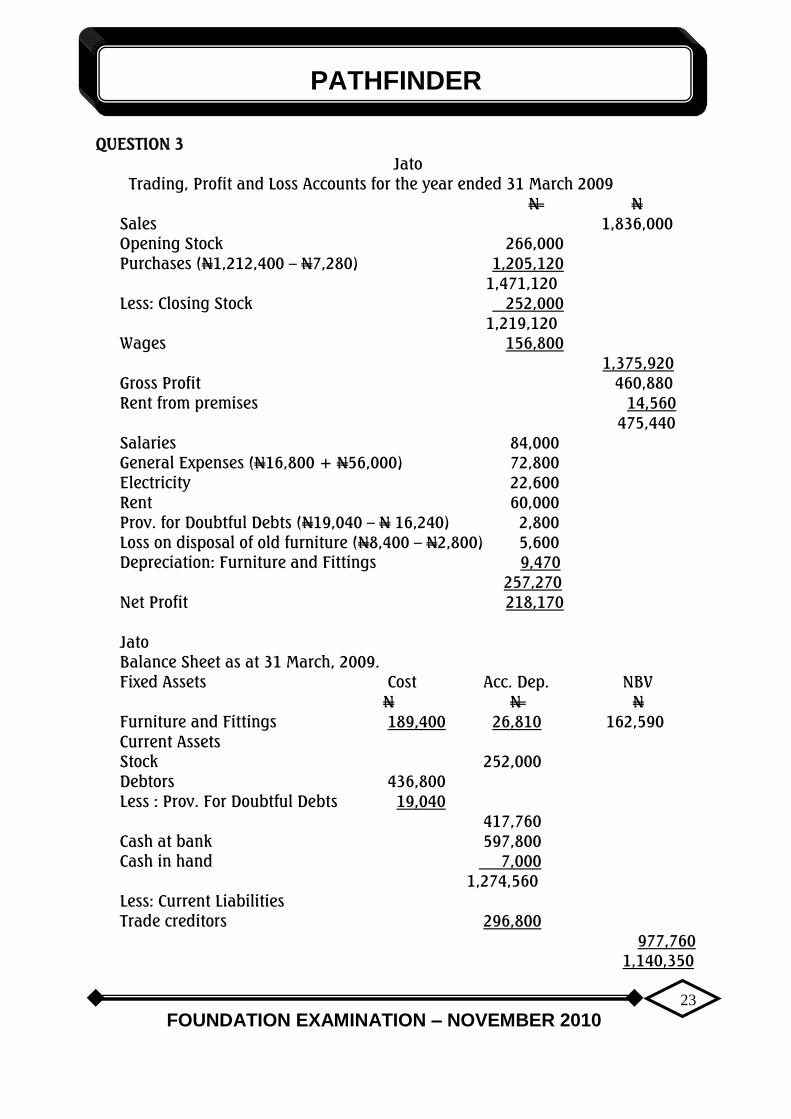

QUESTION 3

Jato

Trading, Profit and Loss Accounts for the year ended 31 March 2009

N N

Sales 1,836,000

Opening Stock 266,000

Purchases (N1,212,400 – N7,280) 1,205,120

1,471,120

Less: Closing Stock 252,000

1,219,120

Wages 156,800

1,375,920

Gross Profit 460,880

Rent from premises 14,560

475,440

Salaries 84,000

General Expenses (N16,800 + N56,000) 72,800

Electricity 22,600

Rent 60,000

Prov. for Doubtful Debts (N19,040 – N 16,240) 2,800

Loss on disposal of old furniture (N8,400 – N2,800) 5,600

Depreciation: Furniture and Fittings 9,470

257,270

Net Profit 218,170

Jato

Balance Sheet as at 31 March, 2009.

Fixed Assets Cost Acc. Dep. NBV

N N N

Furniture and Fittings 189,400 26,810 162,590

Current Assets

Stock 252,000

Debtors 436,800

Less : Prov. For Doubtful Debts 19,040

417,760

Cash at bank 597,800

Cash in hand 7,000

1,274,560

Less: Current Liabilities

Trade creditors 296,800

977,760

1,140,350

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

24

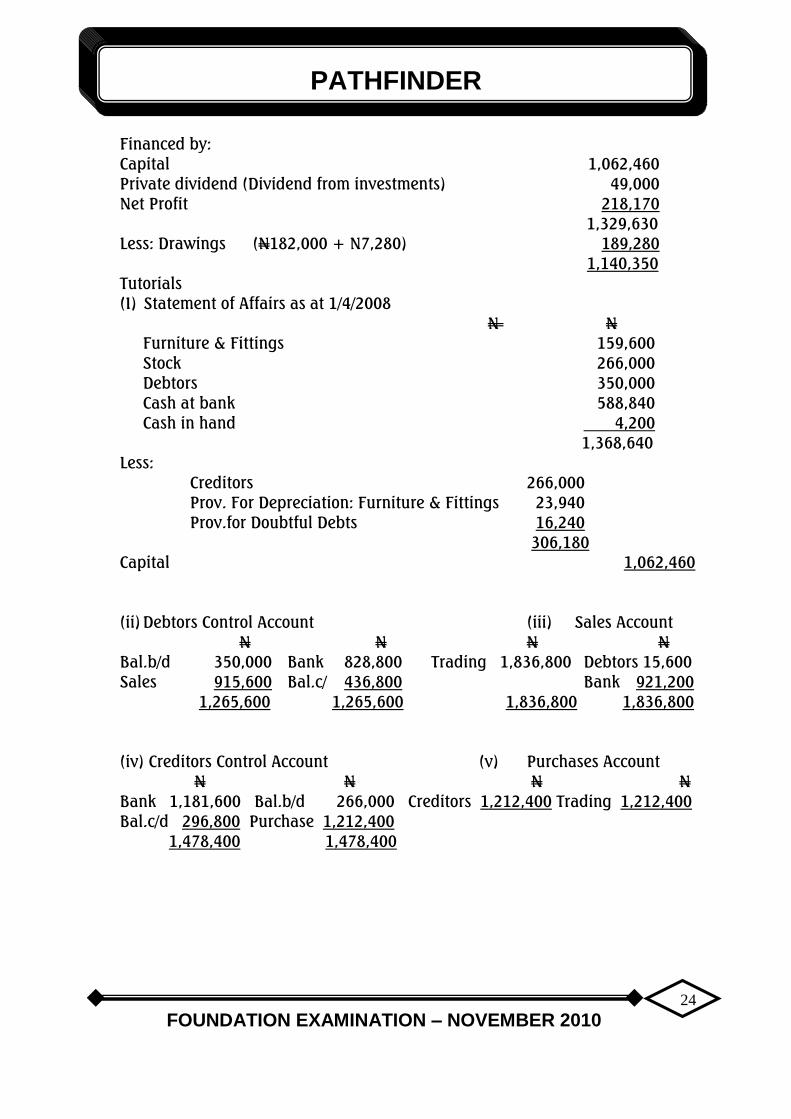

Financed by:

Capital 1,062,460

Private dividend (Dividend from investments) 49,000

Net Profit 218,170

1,329,630

Less: Drawings (N182,000 + N7,280) 189,280

1,140,350

Tutorials

(I) Statement of Affairs as at 1/4/2008

N N

Furniture & Fittings 159,600

Stock 266,000

Debtors 350,000

Cash at bank 588,840

Cash in hand 4,200

1,368,640

Less:

Creditors 266,000

Prov. For Depreciation: Furniture & Fittings 23,940

Prov.for Doubtful Debts 16,240

306,180

Capital 1,062,460

(ii) Debtors Control Account (iii) Sales Account

N N N N

Bal.b/d 350,000 Bank 828,800 Trading 1,836,800 Debtors 15,600

Sales 915,600 Bal.c/ 436,800 Bank 921,200

1,265,600 1,265,600 1,836,800 1,836,800

(iv) Creditors Control Account (v) Purchases Account

N N N N

Bank 1,181,600 Bal.b/d 266,000 Creditors 1,212,400 Trading 1,212,400

Bal.c/d 296,800 Purchase 1,212,400

1,478,400 1,478,400

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

25

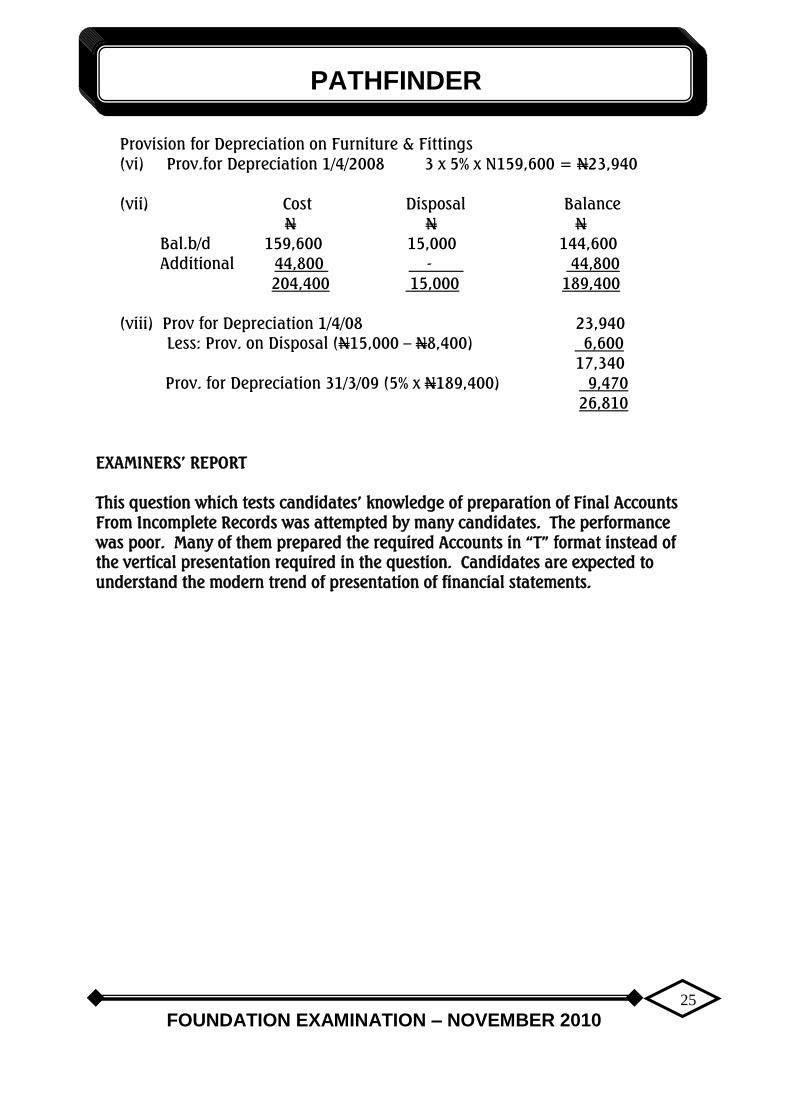

Provision for Depreciation on Furniture & Fittings

(vi) Prov.for Depreciation 1/4/2008 3 x 5% x N159,600 = N23,940

(vii) Cost Disposal Balance

N N N

Bal.b/d 159,600 15,000 144,600

Additional 44,800 - 44,800

204,400 15,000 189,400

(viii) Prov for Depreciation 1/4/08 23,940

Less: Prov. on Disposal (N15,000 – N8,400) 6,600

17,340

Prov. for Depreciation 31/3/09 (5% x N189,400) 9,470

26,810

EXAMINERS’ REPORT

This question which tests candidates’ knowledge of preparation of Final Accounts

From Incomplete Records was attempted by many candidates. The performance

was poor. Many of them prepared the required Accounts in “T” format instead of

the vertical presentation required in the question. Candidates are expected to

understand the modern trend of presentation of financial statements.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

26

QUESTION 4

a. Office Equipment Account Furniture & Fittings Account

N N N N

Balance b/d 375,000 Bal. c/d 1,275,000 Bal. b/d 127,500 Rev. 37,500

Revaluation 900,000 Bal.c/d 90,000

1,275,000 1,275,000 127,500 127,500

Balance b/d 1,275,000 Bal. b/d 90,000

Motor Vehicles Account Stock Account

N N N N

Bal. b/d 2,000,000 Rev. 200,000 Bal. b/d 960,000 Bal 1,014,000

Bal. c/d 1,800,000 Rev. 54,000

2,000,000 2,000,000 1,014,000 1,014,000

Bal. b/d 1,800,000 Bal. b/d 1,014,000

Debtors Account Creditors Account

N N N

Bal. b/d 585,000 Rev. 24,000 Bal. b/d 583,500

Bal. c/d 561,000

585,000 585,000

Bal. b/d 561,000

Capital account

Rosa Frank Danladi Rosa Frank Danladi

N N N N N N

Bal c/d 3,101,830 2,194,170 1,324,000 Bal b/d 1,973,500 1,630,000

Revaluation 1,128,330 564,170 -

Bank 1,324,000

3,101,830 2,194,170 1,324,000 3,101,830 2,194,170 1,324,000

Bal b/d 3,101,830 2,194,170 1,324,000

RevaluationAccount .

N N

Furniture and Fittings 37,500 Office Equipment 900,000

Motor Vehicles 200,000 Stock 54,000

Debtors 24,000 Goodwill 1,000,000

Balance c/d 1,692,500

1,954,000

1,954,000

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

27

Rosa [2/3X N1,692,500] 1,128,330 Balance b/d 1,692,500

Frank [1/3

X N169,250] 564,170 1,692,500 1,692,500

Goodwill Account

Revaluation 1,000,000

Cash Book [Bank]

N N

Balance b/d 139,500 Balance c/d 1,463,500

Capital: Danladi 1, 3 2 4 , 0 0 0

1,463,500 1,463,500

Balance b/d 1 , 4 6 3 , 5 0 0

(b) Revised Balance Sheet: Rosa, Frank and Danladi

N N

Capital Accounts Motor Vehicles 1,800,000

Rosa 3,101,830 Office Equipment 1,275,000

Frank 2,194,170 Furniture & Fitting 90,000

Danladi 1,324,000 Goodwill 1,000,000

6,620,000 Stock 1,014,000

Creditors 583,500 Debtors 561,000

________ Bank Balance 1,463,500

7,203,500 7,203,500

(c )Profits will be shared in future thus: As Danladi is to receive One-fifth of the

profits, the remaining four fifths [1-1/5] must be divided thus:

Rosa 2/3 X 4/5]= 8/15 ; Frank 1/3 X 4/5 = 4/15 while Danladi is to have 1/5 [3/15]

Note: Cash to be brought in by Danladi; 1/4 x [N3,101,830 + N2,194,170] =

N1,324,000

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

28

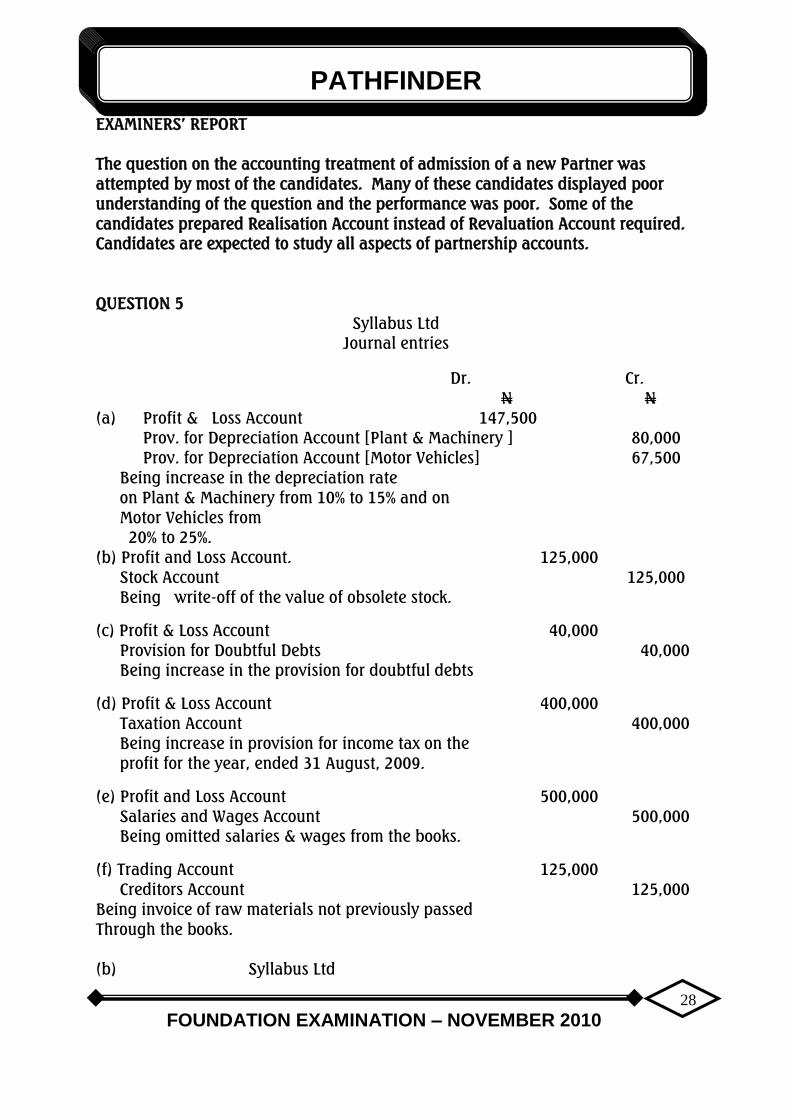

EXAMINERS’ REPORT

The question on the accounting treatment of admission of a new Partner was

attempted by most of the candidates. Many of these candidates displayed poor

understanding of the question and the performance was poor. Some of the

candidates prepared Realisation Account instead of Revaluation Account required.

Candidates are expected to study all aspects of partnership accounts.

QUESTION 5

Syllabus Ltd

Journal entries

Dr. Cr.

N N

(a) Profit & Loss Account 147,500

Prov. for Depreciation Account [Plant & Machinery ] 80,000

Prov. for Depreciation Account [Motor Vehicles] 67,500

Being increase in the depreciation rate

on Plant & Machinery from 10% to 15% and on

Motor Vehicles from

20% to 25%.

(b) Profit and Loss Account. 125,000

Stock Account 125,000

Being write-off of the value of obsolete stock.

(c) Profit & Loss Account 40,000

Provision for Doubtful Debts 40,000

Being increase in the provision for doubtful debts

(d) Profit & Loss Account 400,000

Taxation Account 400,000

Being increase in provision for income tax on the

profit for the year, ended 31 August, 2009.

(e) Profit and Loss Account 500,000

Salaries and Wages Account 500,000

Being omitted salaries & wages from the books.

(f) Trading Account 125,000

Creditors Account 125,000

Being invoice of raw materials not previously passed

Through the books.

(b) Syllabus Ltd

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

29

Revised Balance Sheet as at 31 August 2009

Fixed Assets Cost Acc. Dep. NBV

N’000 N’000 N’000

Land & Buildings 5,250 2,250 3,000

Plant & Machinery 1,600 480 1,120

Motor Vehicles 1,350 667.5 682.5

Furniture & Fittings 900 300 600

9,100 3,697.5 5,402.5

Current Assets

Stock (N850 - N125) 725

Net Debtors (N900 – N 40) 860

Cash at Bank 200

1,785

Less: Current Liabilities

Creditors (N1,200 + N125) 1,325

Taxation (N500 + N400) 900

Accruals 500

Bank Overdraft 550

3,275

(1,490)

3,912.5

Financed by:

5,000,000 Ordinary Shares of 50k each 2,500

Capital Reserve 500

Profit & Loss 912.5

3,912.5

Notes to the Accounts

(i) There is a contingent liability made up as follows:

N

Pending court case 500,000

Employees car loan agreement guaranteed by the company 1,100,000

1,600,000

(ii) The Directors proposed a final dividend of 25% on Ordinary Shares.

Tutorials

(i) Provision for Depreciation on Plant and Machinery N

Already provided for in the Accounts (10% x N1,600,00) = 160,000

Provision at the new rate of depreciation (15% x N1,600,00) = 240,000

Additional Provision 80,000

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

30

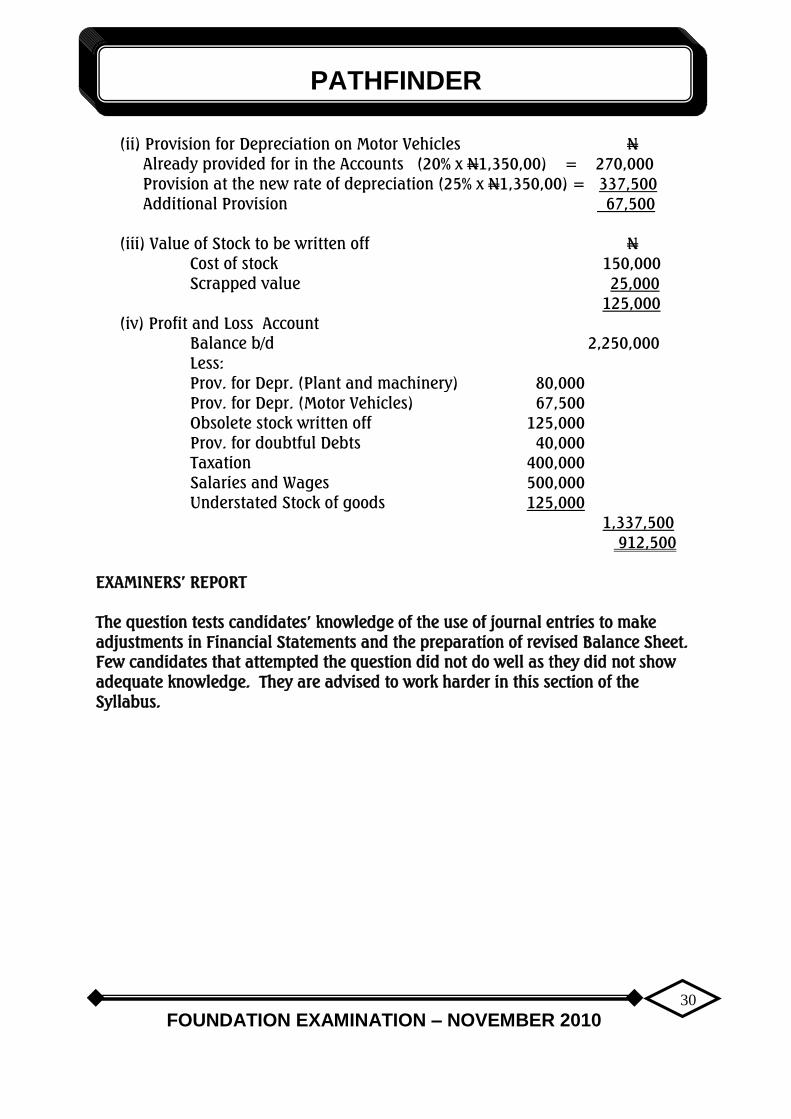

(ii) Provision for Depreciation on Motor Vehicles N

Already provided for in the Accounts (20% x N1,350,00) = 270,000

Provision at the new rate of depreciation (25% x N1,350,00) = 337,500

Additional Provision 67,500

(iii) Value of Stock to be written off N

Cost of stock 150,000

Scrapped value 25,000

125,000

(iv) Profit and Loss Account

Balance b/d 2,250,000

Less:

Prov. for Depr. (Plant and machinery) 80,000

Prov. for Depr. (Motor Vehicles) 67,500

Obsolete stock written off 125,000

Prov. for doubtful Debts 40,000

Taxation 400,000

Salaries and Wages 500,000

Understated Stock of goods 125,000

1,337,500

912,500

EXAMINERS’ REPORT

The question tests candidates’ knowledge of the use of journal entries to make

adjustments in Financial Statements and the preparation of revised Balance Sheet.

Few candidates that attempted the question did not do well as they did not show

adequate knowledge. They are advised to work harder in this section of the

Syllabus.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

31

QUESTION 6

OJADU LIMITED

Trading, Profit and Loss Account for the year ended 31December 2009.

N N

Sales 2,946,300

Cost of sales:

Opening stock 204,000

Purchases 2,254,350

2,458,350

Less: Closing stock 246,350 (2,212,000)

Gross profit 734,300

Add: Discount received 17,100

751,400

Less: Expenses

Debenture Interest 9,000

Directors Fees 78,000

General Expenses 246,525

Salaries 267,000

Electricity 9,750

Motor Vehicle expenses (N12,900+N1,050) 13,950

Rent and Insurance (N12,450- N1,800) 10,650

Discount Allowed 25,200

Bad debt 6,900

Provision for Bad debt 22,890

Provision for depreciation 24,000

(713,865)

Net Profit 37,535

Profit brought forward 120,900

158,435

Dividend- Interim 14,625

Profit carried forward 143,810

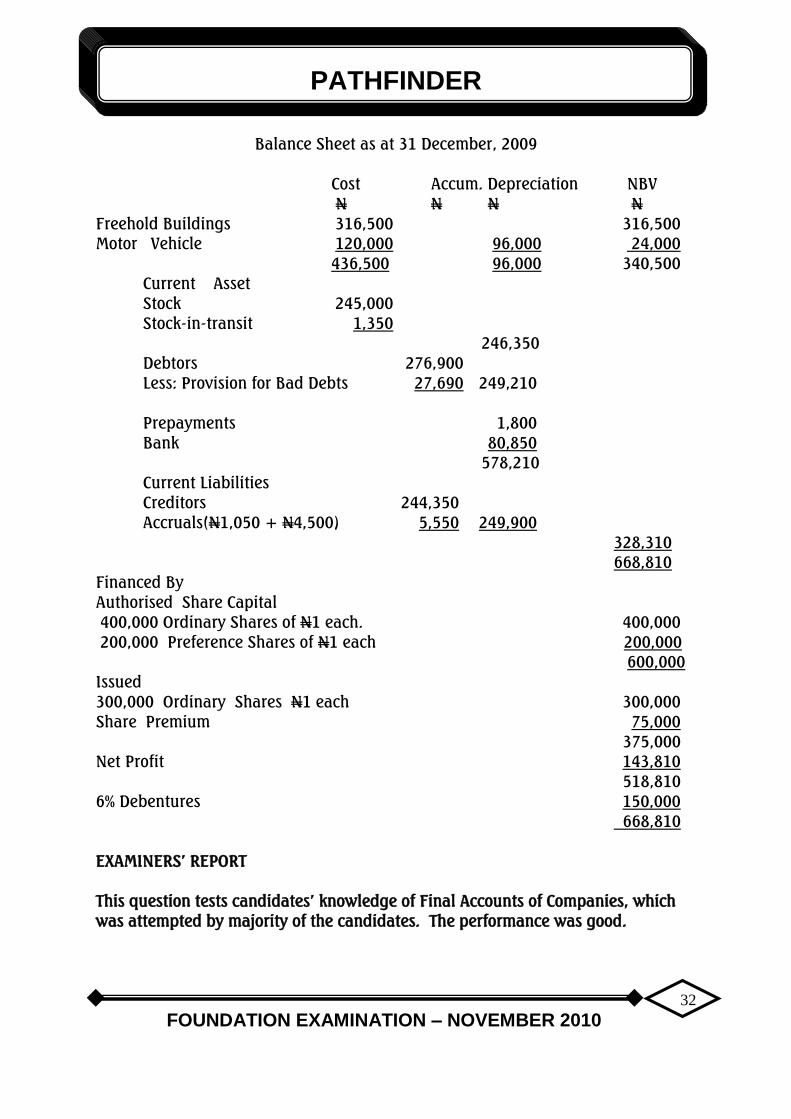

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

32

Balance Sheet as at 31 December, 2009

Cost Accum. Depreciation NBV

N N N N

Freehold Buildings 316,500 316,500

Motor Vehicle 120,000 96,000 24,000

436,500 96,000 340,500

Current Asset

Stock 245,000

Stock-in-transit 1,350

246,350

Debtors 276,900

Less: Provision for Bad Debts 27,690 249,210

Prepayments 1,800

Bank 80,850

578,210

Current Liabilities

Creditors 244,350

Accruals(N1,050 + N4,500) 5,550 249,900

328,310

668,810

Financed By

Authorised Share Capital

400,000 Ordinary Shares of N1 each. 400,000

200,000 Preference Shares of N1 each 200,000

600,000

Issued

300,000 Ordinary Shares N1 each 300,000

Share Premium 75,000

375,000

Net Profit 143,810

518,810

6% Debentures 150,000

668,810

EXAMINERS’ REPORT

This question tests candidates’ knowledge of Final Accounts of Companies, which

was attempted by majority of the candidates. The performance was good.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

33

ICAN/102/F/3 EXAMINATION NO.............................

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF NIGERIA

FOUNDATION EXAMINATION – NOVEMBER 2010

ECONOMICS AND BUSINESS ENVIRONMENT

Time allowed – 3 hours

SECTION A Attempt All Questions

PART I MULTIPLE-CHOICE QUESTIONS (20 Marks)

1. Which one of the following is NOT a component of balance of payments?

A. Current account

B. Capital account

C. Official reserve account

D. Official cash account

E. Trade balance

2. The demand for factors of production is

A. derived demand.

B. composite demand.

C. competitive demand.

D. complementary demand.

E. join t demand.

3. In the labour market, households ...........

A. are buyers and firms are sellers.

B. and firms are both buyers and sellers.

C. are sellers and firms are buyers.

D. and firms are both sellers.

E. and firms are neither buyers nor sellers.

4. The transfer of assets or economic activities from the public sector to the

private sector is termed ...................................

A. indigenization.

B. privatization.

C. commercialization.

D. liberalization.

E. deregulation.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

34

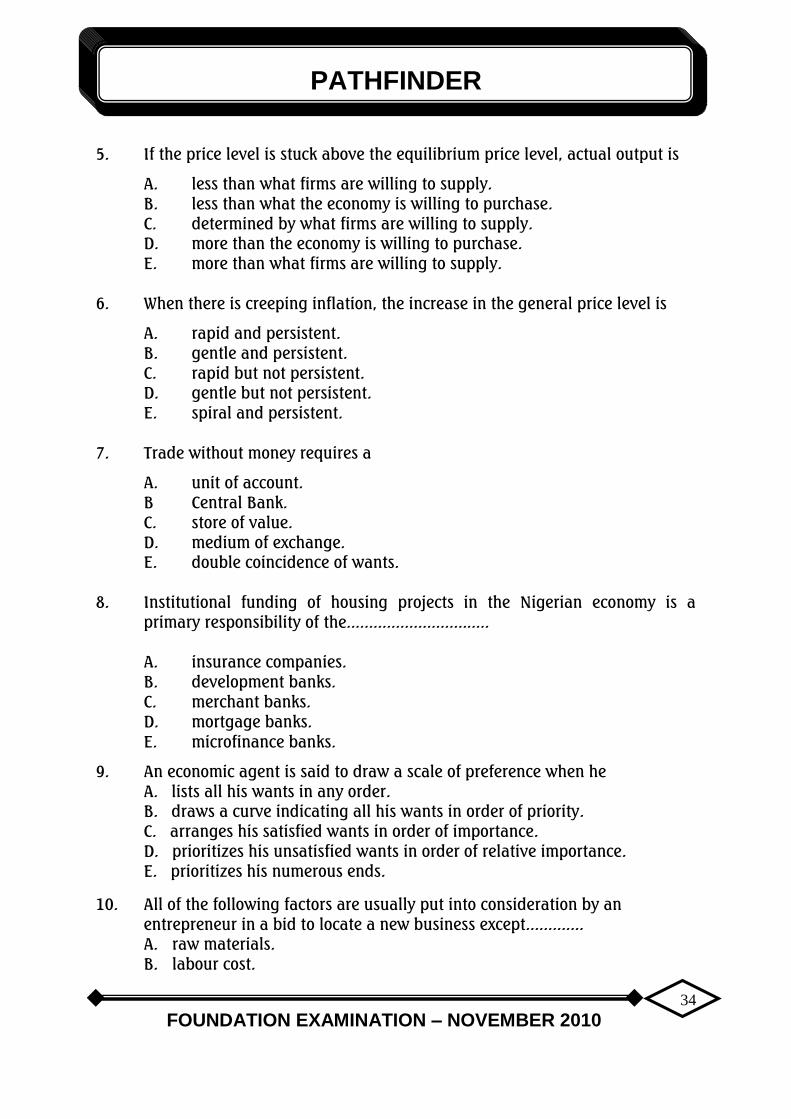

5. If the price level is stuck above the equilibrium price level, actual output is

A. less than what firms are willing to supply.

B. less than what the economy is willing to purchase.

C. determined by what firms are willing to supply.

D. more than the economy is willing to purchase.

E. more than what firms are willing to supply.

6. When there is creeping inflation, the increase in the general price level is

A. rapid and persistent.

B. gentle and persistent.

C. rapid but not persistent.

D. gentle but not persistent.

E. spiral and persistent.

7. Trade without money requires a

A. unit of account.

B Central Bank.

C. store of value.

D. medium of exchange.

E. double coincidence of wants.

8. Institutional funding of housing projects in the Nigerian economy is a

primary responsibility of the................................

A. insurance companies.

B. development banks.

C. merchant banks.

D. mortgage banks.

E. microfinance banks.

9. An economic agent is said to draw a scale of preference when he

A. lists all his wants in any order.

B. draws a curve indicating all his wants in order of priority.

C. arranges his satisfied wants in order of importance.

D. prioritizes his unsatisfied wants in order of relative importance.

E. prioritizes his numerous ends.

10. All of the following factors are usually put into consideration by an

entrepreneur in a bid to locate a new business except.............

A. raw materials.

B. labour cost.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

35

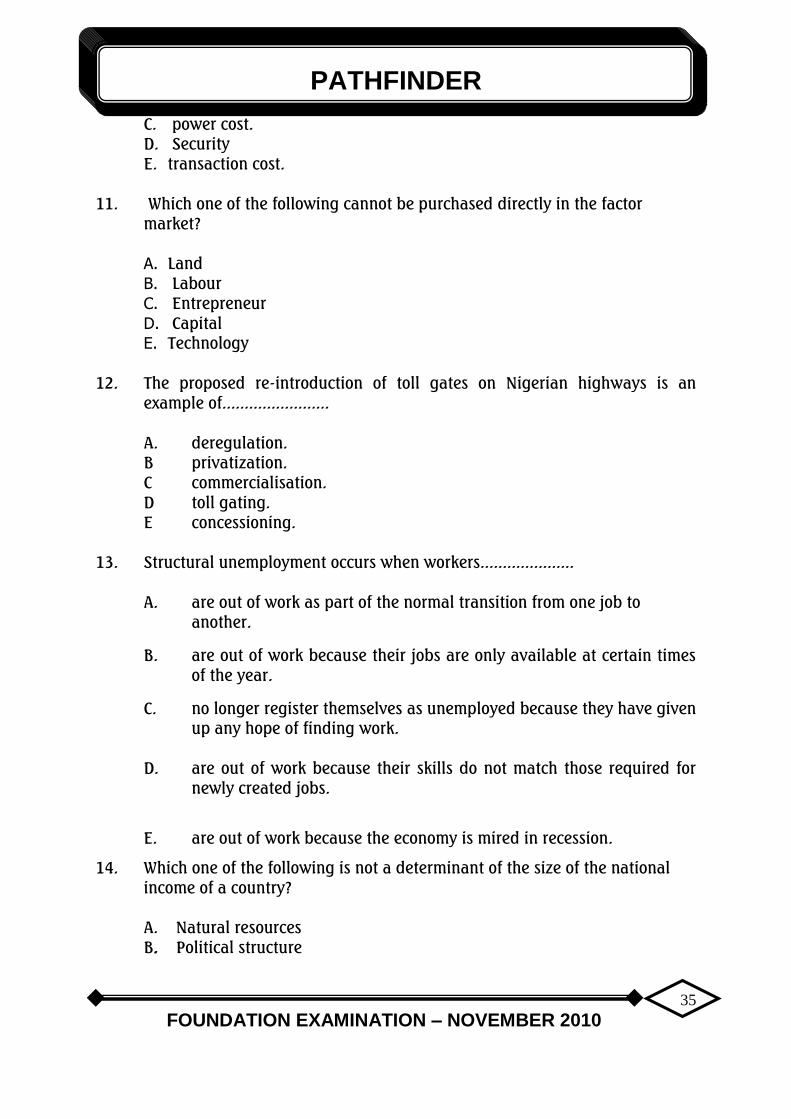

C. power cost.

D. Security

E. transaction cost.

11. Which one of the following cannot be purchased directly in the factor

market?

A. Land

B. Labour

C. Entrepreneur

D. Capital

E. Technology

12. The proposed re-introduction of toll gates on Nigerian highways is an

example of........................

A. deregulation.

B privatization.

C commercialisation.

D toll gating.

E concessioning.

13. Structural unemployment occurs when workers.....................

A. are out of work as part of the normal transition from one job to

another.

B. are out of work because their jobs are only available at certain times

of the year.

C. no longer register themselves as unemployed because they have given

up any hope of finding work.

D. are out of work because their skills do not match those required for

newly created jobs.

E. are out of work because the economy is mired in recession.

14. Which one of the following is not a determinant of the size of the national

income of a country?

A. Natural resources

B. Political structure

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

36

C. Technology

D. Human capital

E. Foreign investment

15. The statement in a newspaper that “consumer prices rose last month by 1

percent and if this trend continues, the annual rate of inflation will be 10

percent for the year” is an example of .............................

A. a normative economic statement.

B. unbiased but loaded terminology.

C. a positive economic statement.

D. a historical statement.

E. a philosophical statement.

16. If a price ceiling below equilibrium price is imposed in a market, then

A. rationing will be unnecessary.

B. surplus of the commodity will develop.

C. quantity demanded of the commodity will be greater than quantity supplied.

D. quantity supplied of the commodity will be greater than quantity demanded.

E. quantity supplied of the commodity will be equal to quantity demanded.

17. Which one of the following is true of a firm in the short run?

A. It cannot vary its output

B. It can vary all factors of production

C. It can change its fixed input

D. It can change output by using different levels of variable inputs

E. It cannot pull out of the industry

18. When economists describe “a market” they mean....................

A. a place where goods are traded.

B. information networks that allow individuals to keep in touch with each

other.

C. a hypothetical place where the production of goods and services take

place.

D. an arrangement which brings consumers and producers together for the

purpose of business transaction.

E. a place where services are traded.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

37

19. The output of Indians resident in Nigeria will form part of Nigeria’s

A. GDP

B. GNP

C. NNP

D. GNI

E. NNI

20. Suppose the model for the economy yielded the following data: C = N200m

+ 0.5Yd; Yd = Y- T; I = N60m; G = N86m; X = N40m; M = N45m; T = N30m.

The equilibrium national income is....................

A. N662m

B. N652m

C. N562m

D. N656m

E. N610m

PART II SHORT ANSWER QUESTIONS

1. The various combinations of two commodities that can be produced given a

certain amount of resources is depicted by ................................

2. The concept that measures how consumption of a good changes in response

to a change in income is known as....................

3. The explanation for the u-shaped nature of the average cost curve is

embedded in the law of ………………………….

4. The profit-maximising output level for a monopolistically competitive firm is

achieved at the point where …………

5. The total money value of all final goods and services produced within an

economy in a year is known as the……………………………….

6. If the commodity prices in 2006 (the base year) and 2010 (the current year)

were N200 and N500 respectively, the price index is ………………

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

38

7. If an economy is suffering from demand deficient unemployment, the Central

Bank could pursue ...............……….monetary policy.

8. When a bank is experiencing liquidity problem, it is said to be in....................

9. The process of reasoning from a part to the whole, from particular to general

or from the individual to the universal is called.......................

10. A business unit formed by a number of people who agree to contribute

towards its initial capital under the conditions stipulated by the Companies

and Allied Matters (CAMA) Act is known as .....................

11. The movement of workers from one job or one geographical location to

another is termed.....................................

12. The primary motivating factor for every decision taken by a firm is

....................

13. The slope of the aggregate consumption function is.....................

14. The expenditure incurred when new capital equipment is built and installed

is called ............................

15. An economic system where productive resources are controlled by private

individuals is termed...........................

16. A fall in the price of GSM handsets may likely cause the demand curve for SIM card

to shift to the .......................

17. The economic concept which describes how output responds to proportionate

variation in all inputs in a production process is called ............................

18. When firms in oligopolistic market collude, they form a ..........................

19. The unemployment rate which occurs when the labour market is in equilibrum is

called ...................

20. An economy that engages in unrestricted trade is described as ......................

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

39

SECTION B ATTEMPT ANY FOUR QUESTIONS (60 Marks)

QUESTION 1

(a) What is an Isoquant? (3 marks)

(b) Explain any THREE features of an Isoquant (12 marks)

(Total 15 Marks)

QUESTION 2

(a) What do you understand by demand for money? (3 marks)

(b) List and explain any THREE motives for holding money (12 marks)

(Total 15 Marks)

QUESTION 3

(a) What is economic corruption? (3 marks)

(b) Explain any FOUR adverse effects of economic corruption

on economic development in Nigeria. (12 marks)

(Total 15 Marks)

QUESTION 4

(a) What do you understand by balance of payments equilibrium? (3 marks)

(b) Explain any FOUR adverse effects of balance of payments disequilibrium in

your country. (12 marks)

(Total 15 Marks)

QUESTION 5

Describe any FIVE benefits that management can derive from budget preparation.

(15 Marks)

Question 6

Explain briefly the following production systems that may be found in

organisations:

(a) Job shop production (5 Marks)

(b) Batch Production (5 Marks)

(c) Flow Production (5 Marks)

(Total 15 Marks)

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

40

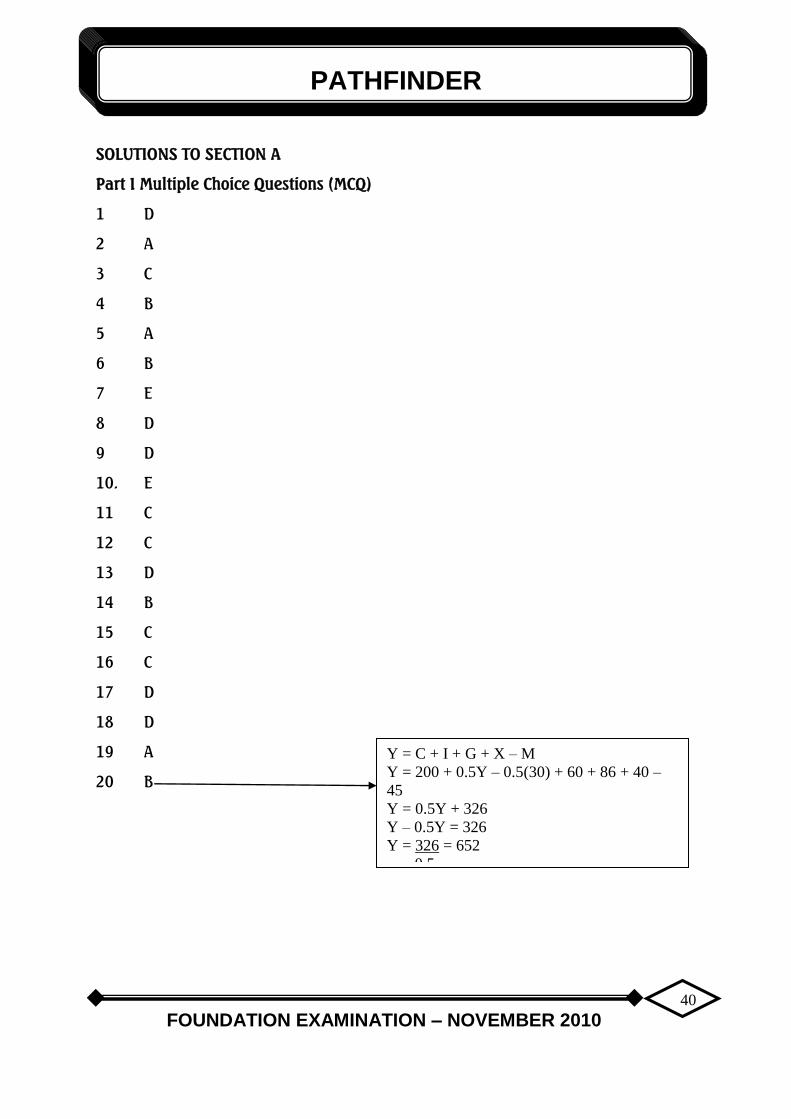

SOLUTIONS TO SECTION A

Part I Multiple Choice Questions (MCQ)

1 D

2 A

3 C

4 B

5 A

6 B

7 E

8 D

9 D

10. E

11 C

12 C

13 D

14 B

15 C

16 C

17 D

18 D

19 A

20 B

Y = C + I + G + X – M

Y = 200 + 0.5Y – 0.5(30) + 60 + 86 + 40 –

45

Y = 0.5Y + 326

Y – 0.5Y = 326

Y = 326 = 652

0.5

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

41

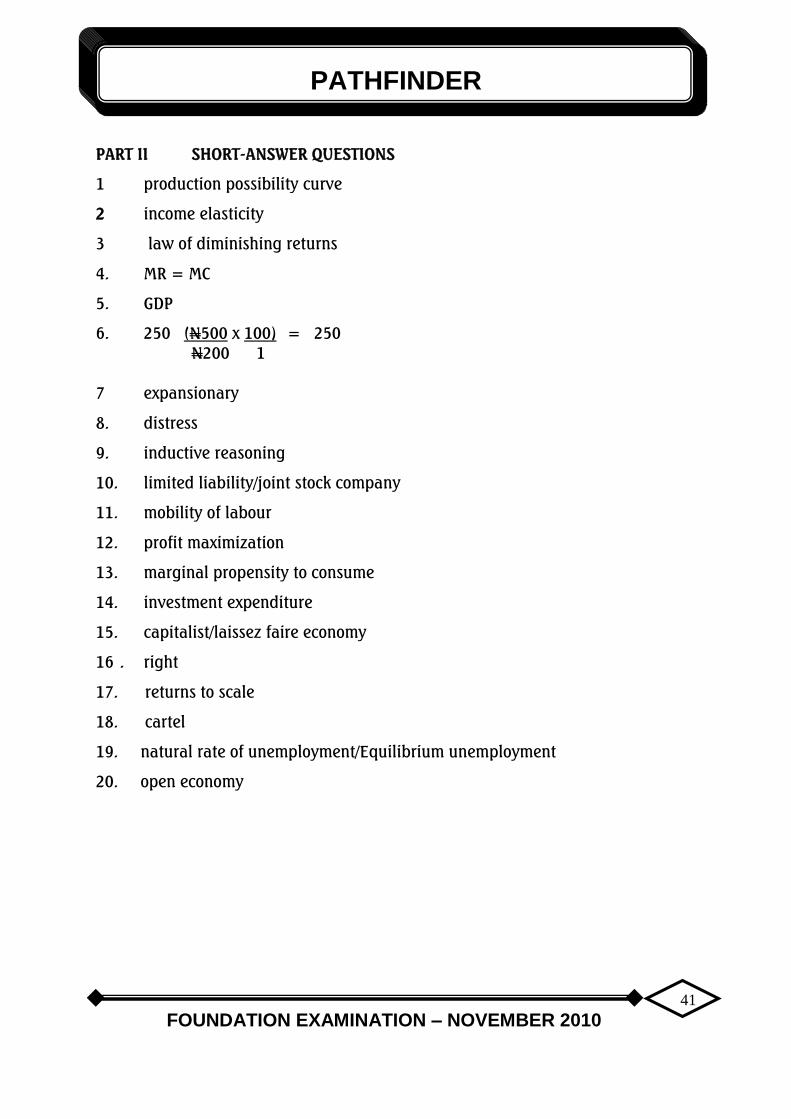

PART II SHORT-ANSWER QUESTIONS

1 production possibility curve

2 income elasticity

3 law of diminishing returns

4. MR = MC

5. GDP

6. 250 (N500 x 100) = 250

N200 1

7 expansionary

8. distress

9. inductive reasoning

10. limited liability/joint stock company

11. mobility of labour

12. profit maximization

13. marginal propensity to consume

14. investment expenditure

15. capitalist/laissez faire economy

16 . right

17. returns to scale

18. cartel

19. natural rate of unemployment/Equilibrium unemployment

20. open economy

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

42

SOLUTIONS TO SECTION B

QUESTION 1

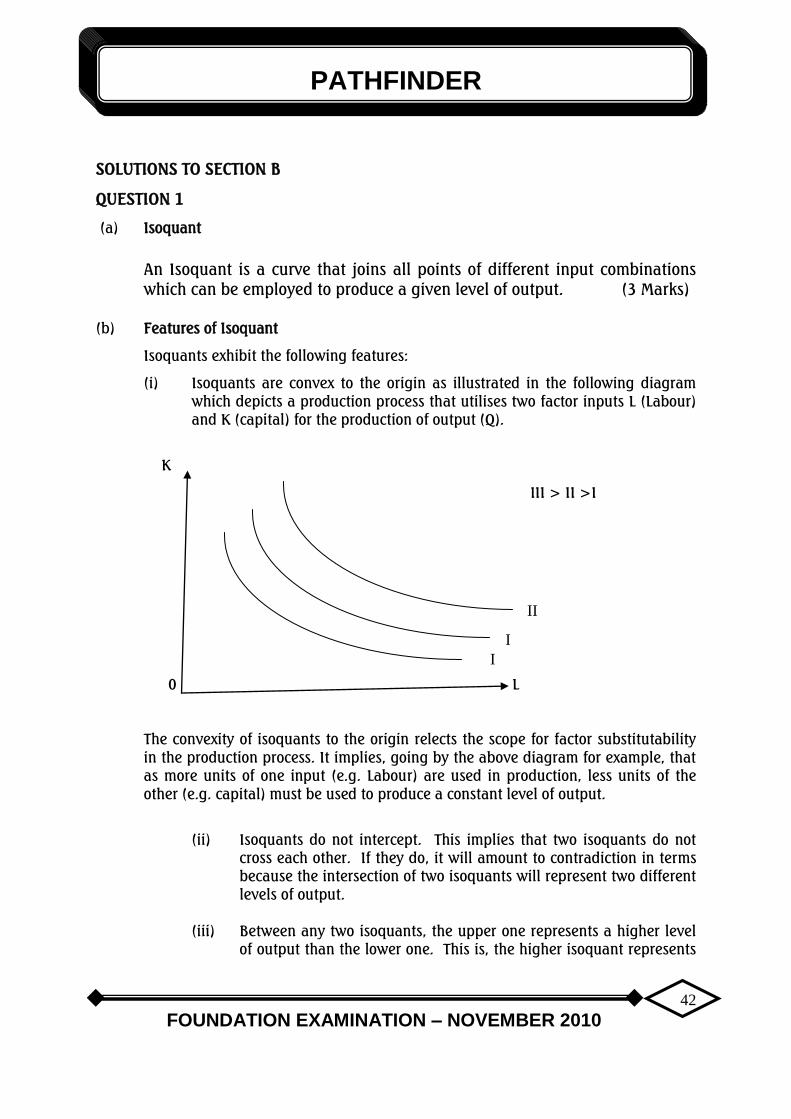

(a) Isoquant

An Isoquant is a curve that joins all points of different input combinations

which can be employed to produce a given level of output. (3 Marks)

(b) Features of Isoquant

Isoquants exhibit the following features:

(i) Isoquants are convex to the origin as illustrated in the following diagram

which depicts a production process that utilises two factor inputs L (Labour)

and K (capital) for the production of output (Q).

K

III > II >I

0 L

The convexity of isoquants to the origin relects the scope for factor substitutability

in the production process. It implies, going by the above diagram for example, that

as more units of one input (e.g. Labour) are used in production, less units of the

other (e.g. capital) must be used to produce a constant level of output.

(ii) Isoquants do not intercept. This implies that two isoquants do not

cross each other. If they do, it will amount to contradiction in terms

because the intersection of two isoquants will represent two different

levels of output.

(iii) Between any two isoquants, the upper one represents a higher level

of output than the lower one. This is, the higher isoquant represents

II

I I

I I

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

43

a higher level of output as shown in the above diagram where III >

II >I

(iv) A family of isoquants represents an isoquant map. An isoquant map

can be used to indicate decreasing, constant or increasing returns to

scale features of a production process, based on the distances

between successive pairs of isoquants. If the distance between those

isoquants increases as output increases, the firm’s production

function is exhibiting decreasing returns to scale; if the distance

between the isoquants decreases as output increases, the firm is

experiencing increasing returns to scale.

4 marks each for any 3 points = 12 marks

EXAMINERS’ REPORT

The question tested students’ understanding of the concept of isoquant from the

theory of production area of the syllabus. In essence, the question required the

students to define isoquant (part a) and to explain its features (part b) as done in

the suggested solutions above.

Part (a) of the question was satisfactorily answered by about 80 percent of the

candidates who attempted the question. A few candidates handled the question

carelessly on account of their misinterpretation of isoquant for indifference curve,

and unintelligently on account of their inappropriate definition of the concept.

Candidates lost marks in part (b) of the question because they merely outlined the

features of isoquants and failed to explain those features. Some candidates did not

have any clue as to what those features are. Additionally, a high proportion of the

candidates demonstrated poor communication skills. These pitfalls culminated into

very poor performance of the candidates who attempted the question.

QUESTION 2

(a) Demand for Money

Demand for money refers to the amount of money that individuals, firms or

governments are willing to hold during a given period of time. In other

words, it is the desire of economic agents to hold on to cash rather than

other assets.

(3 Marks)

(b) Motives for Holding Money

(i) The Transaction Motive:

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

44

Since money serves as a medium of exchange, it is demanded to meet

day-to-day business transaction. For example, households demand for

money to pay for goods and services they buy on daily basis.

(i) The Precautionary Motive:

This is the demand for money to meet unforeseen expenses arising

from unexpected emergencies, such as, sudden illness, accidents,

fire/flood disasters, vehicle breakdown etc.

(iii) The Speculative Motive

The speculative motive for demanding money arises in situations

where holding money is perceived to be less risky than the alternative

of lending the money or investing it in some other asset. For example,

if a stock market speculator feels or gets information that stock prices

will fall on the stock exchange market in the nearest future, he would

likely sell his current stock holdings today and use the proceeds to

buy more stocks when the stock prices must have fallen.

4 Marks each; 1 Mark for mentioning and 3 Marks for discussion.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

45

EXAMINERS’ REPORT

Candidates were expected to explain the concept of the demand for money (Par a)

and to explain any three motives for holding money (Part b). The candidates

showed a fair understanding of part of the question, though quite a number of

them mixed up the “demand for a commodity” with the “demand for money”.

More than 70 percent of the candidates were able to list the 3 motives for holding

money but not many of them could clearly explain the motives. In particular, a

substantial proportion of the candidates was unable to explain the speculative

motive for holding money.

Even some of those who appeared to have an idea explained it in the context of the

effect of speculation in the goods market rather than in the bond market. They

gave the panic buying of petroleum products by consumers/motorists in Nigeria as

an example of speculative motive for holding money. It is hoped that the solutions

given to the question above would clear the misunderstanding of candidates with

respect to the requirements of the question.

This question was very popular among the candidates as it was attempted by 98

percent of the candidates who sat for the examination. Candidates’ performance

was above average.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

46

QUESTION 3

(a) Economic Corruption

Economic corruption is an unethical act perpetuated by individual economic

agents when they misappropriate common economic resources for private

use or selfish purpose.

(3 Marks)

(i) Reduction in the Growth Rate of Aggregate Output: It is believed that

the level of economic growth will be adversely affected when there is

corruption in an economy. This is because the higher the level of

corruption, the lower the resources available for productive activities

to further wealth creation and the lower the growth in aggregate

output. It means that economic corruption can stifle economic

growth which can result in economic development failure.

(ii) Reduction in Employment: The Level of employment in an economy is

positively related to the level of economic activities or output

production. The higher the level of corruption, the lower the level of

output production and the lower the number of people that would be

engaged in production.

(iii) Reduction in Foreign Direct Investment: Economic corruption in an

economy will discourage foreign direct investment as there will be no

objectivity in business valuation and analysis. In effect, the higher

the level of corruption, the lower the resources available for

investment and the lower the actual investment in the country.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

47

(iv) Increase the Level of Poverty: The prevalence of corruption affects the

distribution of income. The most privileged people in the society

especially those that are corrupt amass wealth by taking more than

their share of the common resources, thereby impoverishing the

larger population and increasing the inequality gap. The higher the

inequality gap, the higher in most cases, the level of poverty since

most of the resources that are meant to provide for the needs of the

poor are already amassed by the rich.

(v) Increase in Cost of Doing Business: Corruption leads to increase in cost

of business transaction and inflation of contract values. At each stage

of business transaction, the agent always adds its own inducement to

the cost of the business transaction, the longer the chains of middle

men the higher the increase in the cost of such transaction. In effect,

a corrupt environment is conducive to increasing the cost of doing

business.

(vi) Promotion of Economic Crime: Corruption promotes economic crimes

by making it easier for criminals to bribe their way out of justice.

(vii) Distortion in the Working of the Price Mechanism. Corruption makes

the price system to fail in allocating resources efficiently. When there

is prevalence of corruption, an economic agent that has vested

interest in a particular business transaction may use his/her economic

power, acquired through corrupt practices, to subvert the transaction

and make price system ineffective in such business transaction.

3 marks each for any 4 points = 12 marks

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

48

EXAMINERS’ REPORT

The question tested candidates’ understanding of the concept of economic

corruption (part a), and its adverse effects on economic development in Nigeria

(part b). Many candidates had challenges defining economic corruption. They

interpreted corruption only in the context of public service, neglecting the possible

corruption in economic transactions in the private sector. In some instances,

candidates were unable to relate their discussions to developmental challenges in

Nigeria. But there were candidates who showed a good understanding of all the

requirements of the question. They were able to explain the concept of economic

corruption and the possible adverse effects of economic corruption on economic

development in Nigeria. This shows that some of the candidates are current and

follow trends in economic events and development in Nigeria. Overall, about 87

percent of the candidates attempted this question. Performance was fair.

QUESTION 4

(a) Balance of Payments Equilibrium

Balance of payment is a record of payment showing a country’s international

payments (for visible and invisible imports) and receipts (for visible and

invisible exports) with the rest of the world for a particular period usually a

year. It is the summary of a country’s financial transactions with the rest of

the world. It is in equilibrium if total receipts equals total payments.

(3 marks)

(b) Possible Adverse Effects of Balance of Payments Disequilibrium in Nigeria

(i) If balance of payments disequilibrium persists in Nigeria, it will make

the country to lose its reserve of foreign exchange and increase the country’s

international indebtedness.

(ii) The reduction in foreign reserves as a result of balance of payments

disequilibrium can retard the access of the people and government to

credit facilities available in the international financial market. Lack of

inflow of capital and other financial assistance will retard economic

growth.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

49

(iii) The use of foreign reserve to service external debt and correct balance

of payments disequilibrium will further create scarcity of foreign

exchange in the domestic economy. This will result into the inability of

local industries to get sufficient allocation of foreign exchange for the

procurement of essential raw materials and capital goods needed

from abroad thus reducing industrial capacity.

(iv) The government may be forced to resort to contracting debt

obligations in order to finance the balance of payments

disequilibrium.

(v) Reduction in foreign investment: Majority of foreign investors are

afraid of investing in an economy with persistent balance of payments

disequilibrium. Balance of payment disequilibrium gives negative

signals which creates fears for foreign investors about the friendliness

of the countries with such business environments.

3 marks each for any 4 points = 12 marks.

EXAMINERS’ REPORT

The question is clear and unambiguous and candidates’ understanding of it was, to

a large extent, not in doubt. Most of the candidates were aware of the concept of

balance of payments (BOP) equilibrium and the adverse consequence of BOP

disequilibrium.

The major pitfall in some candidates’ answers has to do with the definition of

balance of payment equilibrium where some candidates only touched the visible

items of the BOP and neglected the invisible aspect. This was a popular question

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

50

as it was attempted by about 80% of the candidates. Overall, candidates’

performance in the question was quite fair.

QUESTION 5

Five benefits that management can derive from budget preparation are:

(i) Coordination: One of the major means of coordinating the activities of the

organisation is the budget. The interaction between managers and

subordinates during the budget development process helps to define and

integrate the activities of the organisation. Budget preparation helps in

coordinating all the activities of an organisation and their respective

expenditures.

(ii) Clarification of Authority and Responsibility: Budget helps in clarifying the

various centres and those who exercise authority over them, and the

expected responsibilities to be carried out by the various position holders.

(iii) Communication: Prepared budget communicates the plan of the enterprise

over a period of time to insiders and outsiders with a view to aiding the

organisation to achieve their set objectives. It conveys information on the

allocation of the resources of the organisation and the timing of expected

results.

(iv) Establishes Standard of Performance: Budget establishes clear and

unambiguous standard of performance for a set time period, usually a year.

(v) Motivation and Goal Congruence: Budget preparation motivates

organisation members to contribute meaningfully to the attainment of group

goals. Budget preparation also ensures that there is goal congruence or

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

51

agreement between the basic philosophy and goals of the company and its

employees.

(vi) Performance Evaluation: Budget enables the organisation to evaluate their

performance as to whether the organisation is on course or not in terms of

the set objectives.

(vii) Control: At stated intervals, actual performance will be compared directly

with the budget. Deviation can be detected quickly and action taken to

effect corrective measures.

EXAMINERS’ REPORT

The question tested the benefits derivable from budgeting. Many of the candidates

attempted the question. Candidates had a shallow knowledge of the question and

their performance was below average. The candidates could not proffer correct

solution to the question because of various interpretations they had of the question.

They are advised to prepare adequately for future examinations by consulting

standard textbooks.

3 Marks for any 5 points = 15 Marks

QUESTION 6

(a) Job shop production: The essential feature of this method of production is

that it produces single articles or one –off items. These products may be

small or large single item for a particular customer.

The key characteristics of job shop production are as follows:

(i) There are a wide variety of different non-standardised operations to

be performed.

(ii) The sequences of operation vary from product to product.

(iii) The machinery and equipments utilised are general purpose types.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

52

(iv) The work layout varies on the basis of operation or process.

(v) Unpredictable demand on stores for inputs.

(vi) Supervisors and workers possess a wide range of skills.

(vii) The entire manufacturing process tends to be relatively expensive

compared with other forms of production. (5 marks)

(b) Batch Production: This is the production of standardised units or parts in

small or large lots. The unique feature of batch production is that it is

standardised in nature.

The key characteristics of batch production are as follows:

(i) A standardised set of operations is carried out intermittently as each

batch move from one operation to the next.

(ii) The machinery and plant utilised are general purpose types.

(iii) Large volume of raw materials are stored.

(iv) The skills required are limited.

(v) There is emphasis on production planning and progress monitoring,

(vi) Production runs are relatively short and intermittent. (5 marks)

(c) Flow Production: This is the system in which items are produced by flowing

uninterruptedly from one operation or process to the next until completion. It

requires high investment in plant and machinery as well as a high degree of

production planning. The characteristics of flow production are:

(i) Strict product specification.

(ii) Specialised machines and equipments arranged in a line formation.

(iii) Tools, materials and methods are standardised.

(iv) Production runs for each individual product is long.

(v) For each operation in the production line, the range of skills required

by workers is narrow. (5 marks)

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

53

EXAMINERS’ REPORT

About 56% of the candidates attempted this question which tested their

understanding of the various types of production. They were expected to discuss

features of job shop production, batch production and flow production.

Performance was below average. The candidates could not proffer more than one

characteristic feature of each of the production systems. Candidates are advised to

study harder and ensure effective coverage of the syllabus to enable them to

perform better in the future.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

54

ICAN/ EXAMINATION NO...................................

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF NIGERIA

INTERMEDIATE EXAMINATION-NOVEMBER 2010

CORPORATE AND BUSINESS LAW

Time allowed – 3 hours

SECTION A Attempt All Questions

PART I MULTIPLE-CHOICE QUESTIONS (20 Marks)

1. Mutual mistake in contract means ...................

A. both parties are mistaken about the same thing.

B. both parties are mistaken about matters outside the contract.

C. both parties are mistaken about one thing.

D. both parties are mistaken about different things.

E. both parties are mistaken about identical things.

2. When an agent’s appointment is done either orally or in writing by the

principal, agency by ............... is created

A. express appointment

B. ratification

C. estoppel

D. necessity

E. law

3. Which one of the following is NOT an important term of a contract of sale of

goods?

A. The parties.

B. The price.

C. The goods.

D. The time.

E. The quality.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

55

4. The principal duty of the insured during the period covered by the insurance

is.........

A. protection of the insured`s interest

B. maintenance of the property insured

C. payment of premium

D. publicity of the insurance

E. preparation of annual report

5. The membership of a partnership is from two to .............. persons.

A. ten

B. twenty

C. fifty

D. twenty-five

E. thirty

6. One major difference between a private and a public company is that

A. membership of private company is limited to fifty while that of public

company is unlimited.

B. only professionals can run a public company.

C. a public company’s business is not limited by the memorandum and

articles of association.

D. only a private company pays tax.

E. a public company is owned by government.

7. Sale in market overt requires all of the following EXCEPT

A. private and discreet sale

B. sale according to usual market practice

C. sale between sunrise and sunset

D. sale at the existing market price

E. goods displayed openly for sale

8. The hirer must take one of the following actions in order to become the

owner of the hired goods

A. Payment of all the agreed instalments

B. Exercise of his option to purchase

C. Exercise of his right to indemnity from the owner

D. Conversion of his right of possession to ownership

E. Notification to the owner.

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

56

9. Which of the following terms is NOT void in a hire purchase agreement?

A. A term which allows the owner to enter into the hirer’s premises to

recover the goods

B. A term which allows the hirer to terminate the agreement

C. A term which requires the hirer to use a particular insurer as the

agent of the hirer

D. A term which regards any person acting for the owner as the agent of

the hirer

E. A term which relieves the owner of liability for the acts or defects of

any person acting on his behalf

10. Identify which of the following, assignments is effected when the policy of

insurance is merely deposited with the other party?

A. Mutual assignment.

B. Legal assignment.

C. Equitable assignment.

D. Unilateral assignment.

E. Irregular assignment

11. One of the following is the principle of insurance law which states that once

the insurer has settled the claim of the insured, he becomes entitled to

anything which the insured may obtain from another person in respect of the

same loss

A. Indemnity

B. Re-instatement

C. Restoration

D. Subrogation

E. Contribution

12. Which of the following minimum number of persons can form a private and

public company respectively under the Companies and Allied Matters Act,

(Cap C.20) Laws of the Federation of Nigeria 2004?

A. One and two

B. Two and two

C. Two and seven

D. Two and twenty

E. Two and infinity

PATHFINDER

FOUNDATION EXAMINATION – NOVEMBER 2010

57

13. A company which has been allowed to issue its shares at a discount must do