paradise valley unified school district - azauditor.gov · paradise valley unified school district...

TRANSCRIPT

Performance Audit

Paradise ValleyUnified School District

Division of School Audits

Debra K. DavenportAuditor General

October • 2013Report No. 13-11

A REPORTTO THE

ARIZONA LEGISLATURE

The Auditor General is appointed by the Joint Legislative Audit Committee, a bipartisan committee composed of five senators and five representatives. Her mission is to provide independent and impartial information and specific recommendations to improve the operations of state and local government entities. To this end, she provides financial audits and accounting services to the State and political subdivisions, investigates possible misuse of public monies, and conducts performance audits of school districts, state agencies, and the programs they administer.

The Joint Legislative Audit Committee

Audit Staff

Ross Ehrick, Director Mike Quinlan, Manager and Contact Person

Briton Baxter, Team Leader Jenny Walker

Copies of the Auditor General’s reports are free.You may request them by contacting us at:

Office of the Auditor General2910 N. 44th Street, Suite 410 • Phoenix, AZ 85018 • (602) 553-0333

Additionally, many of our reports can be found in electronic format at:

www.azauditor.gov

Representative John Allen, Vice Chair

Representative Paul BoyerRepresentative Andrea DalessandroRepresentative Martin QuezadaRepresentative Kelly TownsendRepresentative Andy Tobin (ex officio)

Senator Chester Crandell, Chair

Senator Judy BurgesSenator David FarnsworthSenator Steve GallardoSenator Katie HobbsSenator Andy Biggs (ex officio)

2910 NORTH 44th STREET • SUITE 410 • PHOENIX, ARIZONA 85018 • (602) 553-0333 • FAX (602) 553-0051

MELANIE M. CHESNEY

DEPUTY AUDITOR GENERAL

DEBRA K. DAVENPORT, CPA

AUDITOR GENERAL

STATE OF ARIZONA

OFFICE OF THE

AUDITOR GENERAL

October 29, 2013

Members of the Arizona Legislature

The Honorable Janice K. Brewer, Governor

Governing Board Paradise Valley Unified School District

Dr. James Lee, Superintendent Paradise Valley Unified School District

Transmitted herewith is a report of the Auditor General, A Performance Audit of the Paradise Valley Unified School District, conducted pursuant to A.R.S. §41-1279.03. I am also transmitting within this report a copy of the Report Highlights for this audit to provide a quick summary for your convenience.

As outlined in its response, the District agrees with all of the findings and recommendations.

My staff and I will be pleased to discuss or clarify items in the report.

Sincerely,

Debbie Davenport Auditor General

2013October • Report No. 13-11

Our Conclusion

REPORT HIGHLIGHTSPERFORMANCE AUDIT

Similar student achievement and efficient operations overallStudent achievement similar to peer districts’—In fiscal year 2011, Paradise Valley USD’s student AIMS scores were similar to peer districts’. Additionally, under the Arizona Department of Education’s A-F Letter Grade Accountability System, the District received an overall letter grade of B, and the District’s 89 percent high school graduation rate was similar to the peer districts’ 90 percent average and higher than the State’s 78 percent average.

District operated efficiently overall—In fiscal year 2011, Paradise Valley USD operated efficiently overall with similar or lower costs in all operational areas. The District’s per pupil administrative costs were lower than peer districts’, its food service and transportation programs operated efficiently, and its per pupil plant operations costs were similar to peer districts’.

Paradise ValleyUnified School District

District’s solar power system contracts unlikely to meet cost-saving expectations, but District has taken action

Between March 2010 and February 2011, the District entered into contracts for 26 solar power systems in an effort to help lower its electricity costs. However, the contracts are unlikely to meet expectations for saving energy costs because of high initial contract rates for the solar power and because several systems were sized too large resulting in excess electricity that the District sells at a loss. To its credit, the District negotiated with its vendor to recover $1.34 million of estimated financial losses and reduce the size of some of its solar power systems.

High initial rates and oversized systems reduce the likelihood of cost savings—The District pays between 10.5 and 12.9 cents per kilowatt hour for solar power at 22 of the 26 sites. These rates are higher than the 9.4 cents per kilowatt hour that the District was paying its utility for electricity, on average, at these sites. Further, because several of the solar power systems were designed too large, they will generate more power than the District uses. This excess solar power is sold to the electric utility at a price far below what it costs the District to produce the electricity, resulting in a financial loss for the District.

0%10%20%30%40%50%60%70%80%90%

100%

Math Reading Writing

Paradise Valley USD Peer group State-wide

Percentage of students who met or exceeded state standards (AIMS)Fiscal year 2011

Comparison of per pupil expenditures by operational areaFiscal year 2011

Per pupil

Paradise Valley USD

Peer group

average Administration $559 $613 Plant operations 837 855 Food service 229 317 Transportation 275 330

In fiscal year 2011, Paradise Valley Unified School District’s student achievement was similar to peer districts’ and it operated efficiently overall. The District’s per pupil administrative costs were lower than peer districts’, and its food service and transportation programs operated efficiently. The District’s plant operations cost per square foot was lower than peer districts’. However, the District did not gain the full benefit of potential savings from this lower cost per square foot because it maintained a large amount of excess building space. The District should continue to review options to address its excess building capacity. Additionally, the District’s solar power system contracts are unlikely to meet expectations for cost savings, and although the District has taken action to recover estimated financial losses, it should continue to monitor its solar power production and electricity usage. The District also needs to strengthen controls over its computer systems.

Paradise ValleyUnified School District

REPORT HIGHLIGHTSPERFORMANCE AUDIT

October 2013 • Report No. 13-11

A copy of the full report is available at:

www.azauditor.gov

Contact person:

Mike Quinlan (602) 553-0333

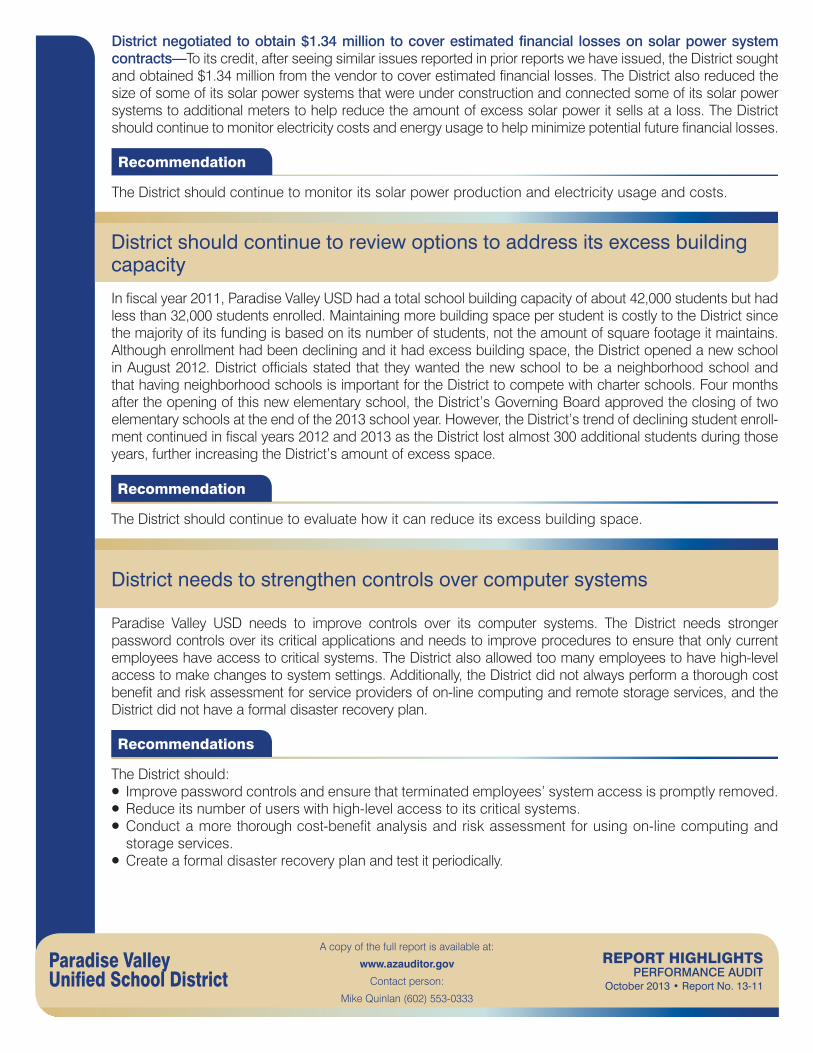

District negotiated to obtain $1.34 million to cover estimated financial losses on solar power system contracts—To its credit, after seeing similar issues reported in prior reports we have issued, the District sought and obtained $1.34 million from the vendor to cover estimated financial losses. The District also reduced the size of some of its solar power systems that were under construction and connected some of its solar power systems to additional meters to help reduce the amount of excess solar power it sells at a loss. The District should continue to monitor electricity costs and energy usage to help minimize potential future financial losses.

The District should continue to monitor its solar power production and electricity usage and costs.

Recommendation

District should continue to review options to address its excess building capacity

In fiscal year 2011, Paradise Valley USD had a total school building capacity of about 42,000 students but had less than 32,000 students enrolled. Maintaining more building space per student is costly to the District since the majority of its funding is based on its number of students, not the amount of square footage it maintains. Although enrollment had been declining and it had excess building space, the District opened a new school in August 2012. District officials stated that they wanted the new school to be a neighborhood school and that having neighborhood schools is important for the District to compete with charter schools. Four months after the opening of this new elementary school, the District’s Governing Board approved the closing of two elementary schools at the end of the 2013 school year. However, the District’s trend of declining student enroll-ment continued in fiscal years 2012 and 2013 as the District lost almost 300 additional students during those years, further increasing the District’s amount of excess space.

The District should continue to evaluate how it can reduce its excess building space.

Recommendation

District needs to strengthen controls over computer systems

Paradise Valley USD needs to improve controls over its computer systems. The District needs stronger password controls over its critical applications and needs to improve procedures to ensure that only current employees have access to critical systems. The District also allowed too many employees to have high-level access to make changes to system settings. Additionally, the District did not always perform a thorough cost benefit and risk assessment for service providers of on-line computing and remote storage services, and the District did not have a formal disaster recovery plan.

The District should: • Improve password controls and ensure that terminated employees’ system access is promptly removed. • Reduce its number of users with high-level access to its critical systems. • Conduct a more thorough cost-benefit analysis and risk assessment for using on-line computing and storage services. • Create a formal disaster recovery plan and test it periodically.

Recommendations

TABLE OF CONTENTS

continued

page i

Office of the Auditor General

District Overview 1

Student achievement similar to peer districts’ and slightly higher than state averages 1District operated efficiently with most costs lower than peer districts’ 2

Finding 1: District’s solar power system contracts unlikely to meet cost-saving expectations, but District has acted to recover estimated financial losses 3

District entered into 26 long-term solar power system contracts 3High initial rates and oversized systems reduce the likelihood of cost savings 4District negotiated to obtain $1.34 million to cover estimated financial losses, but should continue to monitor costs 5Recommendations 6

Finding 2: District should continue to review options to addressexcess building capacity 7

Many schools operated far below designed capacity 7District built new school despite having excess space and still has excess spacesince subsequently closing two schools 8Recommendation 8

Finding 3: District needs to strengthen controls over computersystems 9

Recommendations 11

TABLE OF CONTENTS

concluded

page iiState of Arizona

Finding 4: Some Classroom Site Fund monies spent inappropriately or without adequate support 13

District used some performance pay monies for purposes not listed in its plan, andpay records were not maintained 13Small amount of Classroom Site Fund monies paid to ineligible employees 14Recommendations 14

Other FindingsStudent transportation mileage misreported 15

Recommendation 15

AppendixObjectives, Scope, and Methodology a-1

District Response

Tables1 Comparison of per pupil expenditures by operational area

Fiscal year 2011 (Unaudited) 2

2 Number of students, capacity, and percentage of capacity used for schools thatoperated at less than 60 percent of capacity Fiscal year 2011(Unaudited) 7

Figure1 Percentage of students who met or exceeded state standards (AIMS)

Fiscal year 2011 (Unaudited) 1

DISTRICT OVERVIEW

page 1

Office of the Auditor General

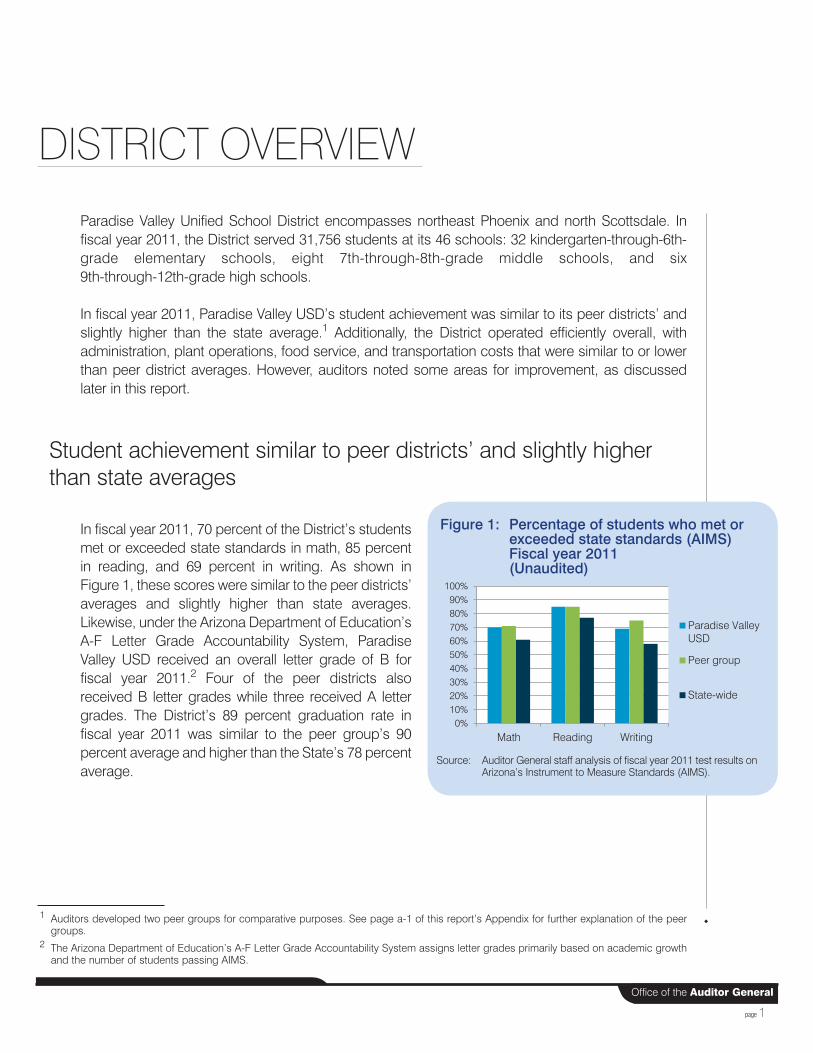

Paradise Valley Unified School District encompasses northeast Phoenix and north Scottsdale. In fiscal year 2011, the District served 31,756 students at its 46 schools: 32 kindergarten-through-6th-grade elementary schools, eight 7th-through-8th-grade middle schools, and six 9th-through-12th-grade high schools.

In fiscal year 2011, Paradise Valley USD’s student achievement was similar to its peer districts’ and slightly higher than the state average.1 Additionally, the District operated efficiently overall, with administration, plant operations, food service, and transportation costs that were similar to or lower than peer district averages. However, auditors noted some areas for improvement, as discussed later in this report.

Student achievement similar to peer districts’ and slightly higher than state averages

In fiscal year 2011, 70 percent of the District’s students met or exceeded state standards in math, 85 percent in reading, and 69 percent in writing. As shown in Figure 1, these scores were similar to the peer districts’ averages and slightly higher than state averages. Likewise, under the Arizona Department of Education’s A-F Letter Grade Accountability System, Paradise Valley USD received an overall letter grade of B for fiscal year 2011.2 Four of the peer districts also received B letter grades while three received A letter grades. The District’s 89 percent graduation rate in fiscal year 2011 was similar to the peer group’s 90 percent average and higher than the State’s 78 percent average.

1 Auditors developed two peer groups for comparative purposes. See page a-1 of this report’s Appendix for further explanation of the peer groups.

2 The Arizona Department of Education’s A-F Letter Grade Accountability System assigns letter grades primarily based on academic growth and the number of students passing AIMS.

0%10%20%30%40%50%60%70%80%90%

100%

Math Reading Writing

Paradise ValleyUSD

Peer group

State-wide

Figure 1: Percentage of students who met or exceeded state standards (AIMS)Fiscal year 2011(Unaudited)

Source: Auditor General staff analysis of fiscal year 2011 test results on Arizona’s Instrument to Measure Standards (AIMS).

page 2State of Arizona

District operated efficiently with most costs lower than peer districts’

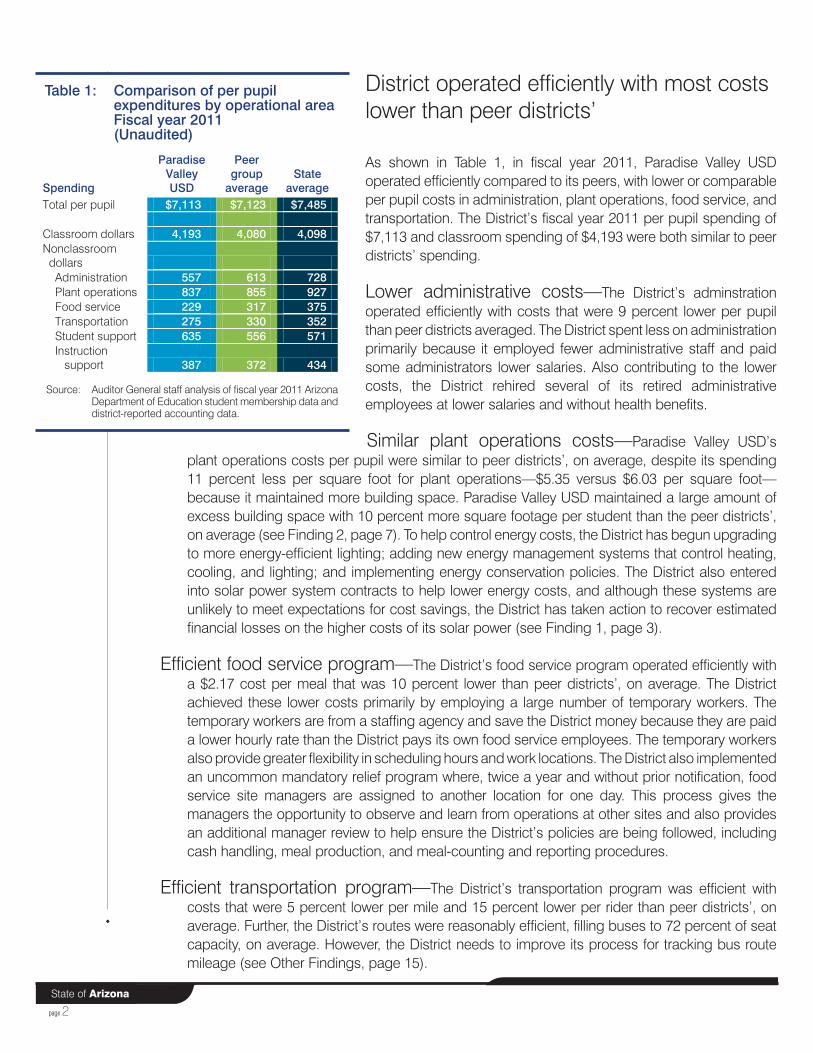

As shown in Table 1, in fiscal year 2011, Paradise Valley USD operated efficiently compared to its peers, with lower or comparable per pupil costs in administration, plant operations, food service, and transportation. The District’s fiscal year 2011 per pupil spending of $7,113 and classroom spending of $4,193 were both similar to peer districts’ spending.

Lower administrative costs—The District’s adminstration operated efficiently with costs that were 9 percent lower per pupil than peer districts averaged. The District spent less on administration primarily because it employed fewer administrative staff and paid some administrators lower salaries. Also contributing to the lower costs, the District rehired several of its retired administrative employees at lower salaries and without health benefits.

Similar plant operations costs—Paradise Valley USD’s plant operations costs per pupil were similar to peer districts’, on average, despite its spending 11 percent less per square foot for plant operations—$5.35 versus $6.03 per square foot—because it maintained more building space. Paradise Valley USD maintained a large amount of excess building space with 10 percent more square footage per student than the peer districts’, on average (see Finding 2, page 7). To help control energy costs, the District has begun upgrading to more energy-efficient lighting; adding new energy management systems that control heating, cooling, and lighting; and implementing energy conservation policies. The District also entered into solar power system contracts to help lower energy costs, and although these systems are unlikely to meet expectations for cost savings, the District has taken action to recover estimated financial losses on the higher costs of its solar power (see Finding 1, page 3).

Efficient food service program—The District’s food service program operated efficiently with a $2.17 cost per meal that was 10 percent lower than peer districts’, on average. The District achieved these lower costs primarily by employing a large number of temporary workers. The temporary workers are from a staffing agency and save the District money because they are paid a lower hourly rate than the District pays its own food service employees. The temporary workers also provide greater flexibility in scheduling hours and work locations. The District also implemented an uncommon mandatory relief program where, twice a year and without prior notification, food service site managers are assigned to another location for one day. This process gives the managers the opportunity to observe and learn from operations at other sites and also provides an additional manager review to help ensure the District’s policies are being followed, including cash handling, meal production, and meal-counting and reporting procedures.

Efficient transportation program—The District’s transportation program was efficient with costs that were 5 percent lower per mile and 15 percent lower per rider than peer districts’, on average. Further, the District’s routes were reasonably efficient, filling buses to 72 percent of seat capacity, on average. However, the District needs to improve its process for tracking bus route mileage (see Other Findings, page 15).

Spending

Paradise Valley USD

Peer group

average State

average Total per pupil $7,113 $7,123 $7,485

Classroom dollars 4,193 4,080 4,098 Nonclassroom dollars Administration 557 613 728 Plant operations 837 855 927 Food service 229 317 375 Transportation 275 330 352 Student support 635 556 571 Instruction support 387 372 434

Table 1: Comparison of per pupil expenditures by operational areaFiscal year 2011(Unaudited)

Source: Auditor General staff analysis of fiscal year 2011 Arizona Department of Education student membership data and district-reported accounting data.

page 3

Office of the Auditor General

FINDING 1

District’s solar power system contracts unlikely to meet cost-saving expectations, but District has acted to recover estimated financial losses

Between March 2010 and February 2011, Paradise Valley USD entered into contracts for 26 solar power systems in an effort to help lower its electricity costs. However, the contracts are unlikely to meet expectations for saving energy costs because the initial rates for most of the systems were higher than what the District was previously paying its utility for electricity. In addition, several of the solar power systems were sized too large, resulting in excess electricity that the District sells at a loss. To its credit, after seeing similar issues reported in prior Office of the Auditor General reports, the District sought and obtained $1.34 million from the vendor to cover estimated financial losses. The District also reduced the size of some of its solar power systems that were under construction and connected some of its solar power systems to additional meters to help reduce the amount of excess electricity it sells at a loss. The District should continue to monitor electricity costs and energy usage to help minimize potential future losses.

District entered into 26 long-term solar power system contracts

Between March 2010 and February 2011, to help lower its electricity costs, Paradise Valley USD entered into contracts for 26 solar power systems to be installed at 5 administration buildings and 21 of its schools, including 4 high schools. The contracts are for a period of 20 to 25 years and required no up-front payment for the systems’ capital costs. The contracts also establish rates that the District must pay for each kilowatt hour of electricity produced and provide the District the option to purchase the systems for their fair market value at varying times throughout each contract term. The 5 systems installed on the administration buildings began producing energy in December 2010 and January 2011, and the 4 high school systems began producing energy in March 2011. The remaining 17 systems were completed between December 2011 and December 2012.

For analysis purposes, the District’s solar power system contracts can be split into two basic groups based on initial cost per kilowatt hour and system size. The first group is the solar power systems installed at the 4 high schools, and their contracts include price escalators but start at a much lower cost per kilowatt hour and appear to provide more appropriately sized solar power systems. The second group is the 22 solar power systems installed at the administration buildings and the other schools, and their contracts have no price escalators but started at much higher costs per kilowatt

page 4State of Arizona

hour and include many systems that were sized too large. As a result of these differences, auditors determined that the 22 systems were of greater concern and therefore are the focus of the information that follows.

High initial rates and oversized systems reduce the likelihood of cost savings

The District’s solar power system contracts are unlikely to meet expectations for saving energy costs for two reasons. First, the initial kilowatt hour rates for the systems are higher than what the District was previously paying its utility for electricity. Second, several of the solar power systems were oversized and produce excess electricity that the District must sell at less than half the rate it is paying to produce the energy.

High initial solar power rates—The District’s initial contracted rates for solar power on the 22 systems were higher than what it was paying for traditional electricity, resulting in a financial loss for the District. More specifically, the District was paying its utility an average of 9.4 cents per kilowatt hour for electricity at these 22 sites prior to the solar power systems being installed. In contrast, the District paid 10.5 to 12.9 cents per kilowatt hour for its solar power at these sites. Although it varies by system, the District estimated that it will incur financial losses overall for the first 6 years of the contracts because the solar power rates are higher than what it was paying its utility. However, it is possible that the losses could extend for additional years. The District’s estimate was based on a 3 percent annual price escalation in energy costs from the District’s electric utility. Based on information provided by the utility, its commercial rates between 2005 and 2009 increased annually by 6.6 percent, on average; however, its average annual increase across the 20-year period, 1990 through 2009, was a much lower 1.2 percent.

Oversized solar power systems—Several of the District’s solar power systems were designed too large, generating more power than the District uses. This excess power is sold to the electric utility at a price far below what it costs the District to produce, resulting in a financial loss for the District. This further calls into question the District’s ability to save money on its total electricity costs under the solar power system contracts. More specifically, at different times of the day, the District’s solar power systems produce more kilowatt hours than the District needs. Depending on the electric utility’s rate plan in use for the specific power meter, the District can use the excess kilowatt hours to offset usage during the remainder of the month or the remainder of the calendar year when the District uses more power than it generates. However, excess credits remaining at the time of netting production and usage are sold to the District’s electric utility at only about 4 cents per kilowatt hour, less than half the 10.5 to 12.9 cents per kilowatt hour the District is paying for the solar power.

As an example of the oversized systems, auditors reviewed the District’s electricity bills and solar production for the five administration buildings with solar power and found the systems were producing more kilowatt hours of electricity than the sites were able to use. From

page 5

Office of the Auditor General

December 2010 through June 2011, these systems produced over 723,000 kilowatt hours on meters that used only 395,000 kilowatt hours during the same time period. These meters were on rate plans that sold excess power back to the electric utility at the end of each month, and therefore the District sold back 45 percent of the kilowatt hours of solar power that it produced. Because the District sells the power back at a much lower rate than it costs to produce, the District lost an average of $9,000 per month on the excess solar power generated by these five systems. Further, the District’s own analysis in the spring of 2012 found that many of the other 17 solar power systems were designed too large and would likely produce more electricity than the sites would be able to use, resulting in additional projected financial losses.

District negotiated to obtain $1.34 million to cover estimated financial losses, but should continue to monitor costs

To its credit, after seeing similar issues reported in prior Office of the Auditor General reports, the District took action to recover estimated financial losses on the solar power systems. In the spring of 2012, when the solar systems at the 5 administration buildings were operating and the other 17 systems were in various phases of completion, the District halted the construction that was in process and performed an in-depth review of the systems. This review focused on two primary concerns of the District—the financial loss in the early years of the contracts due to the solar power rates being higher than what the District would have paid for traditional electricity and the expected financial losses from selling excess power the solar systems generated. The vendor agreed to reduce the size of some of the systems that were in process, and the District also connected some of its solar power systems to additional meters to help reduce the amount of excess electricity it sells at a loss. Further, in October 2012, the vendor established escrow accounts totaling $1.34 million to cover the estimated losses, after which the District allowed the construction of the remaining sites to resume. The District will withdraw monies from the accounts annually to recover losses each year. However, the projected financial losses were based on many estimates, and the District should continue to monitor its actual electricity usage and costs to minimize future losses and determine if the amounts in the escrow accounts are sufficient to cover actual losses on the solar power systems.

The District should also review and continue to evaluate the rate plan options available from its electric utility. For example, the District’s administration buildings and a few of its school sites using solar power are on electric utility rate plans under which the District sells its excess generated solar power at the end of each month, thereby eliminating the ability of the District to use such excess solar power to offset utility electricity usage in future months. A separate utility rate plan would allow the District to sell its excess generated solar power at the end of the calendar year. Allowing credits from excess generated solar power to accumulate and be used for a full year would likely decrease the District’s need to sell excess solar power to the utility at a loss.

page 6State of Arizona

Recommendations

1. The District should continue to monitor its solar power production and electricity usage and costs to help ensure any financial losses are minimized and that the amounts in the escrow accounts are adequate to cover actual losses.

2. The District should regularly review its electric utility’s rate plan options, especially for the District’s sites with solar power systems, to determine if the District is on the best rate plan available for each site’s specific conditions.

page 7

Office of the Auditor General

FINDING 2

District should continue to review options to address excess building capacity

In fiscal year 2011, Paradise Valley USD’s plant operations cost per square foot of $5.35 was 11 percent lower than the peer districts’ average of $6.03. However, the District did not gain the full benefit of potential savings from this lower cost per square foot because it maintained a large amount of excess building space with 10 percent more square footage per student than the peer districts’, on average. Despite using only 75 percent of its buildings’ designed capacities on average, the District opened a new school in August 2012. Although the District closed two schools at the end of the 2013 school year, it still has a large amount of excess building capacity and should consider additional options to address its excess capacity.

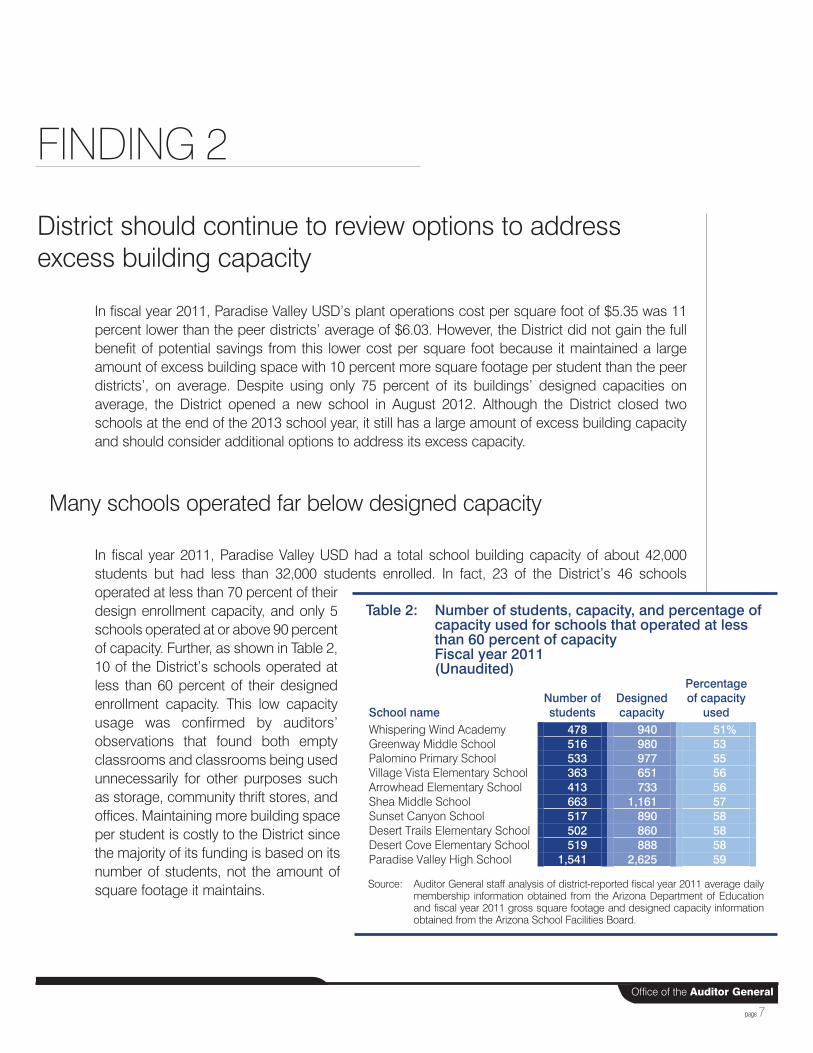

Many schools operated far below designed capacity

In fiscal year 2011, Paradise Valley USD had a total school building capacity of about 42,000 students but had less than 32,000 students enrolled. In fact, 23 of the District’s 46 schools operated at less than 70 percent of their design enrollment capacity, and only 5 schools operated at or above 90 percent of capacity. Further, as shown in Table 2, 10 of the District’s schools operated at less than 60 percent of their designed enrollment capacity. This low capacity usage was confirmed by auditors’ observations that found both empty classrooms and classrooms being used unnecessarily for other purposes such as storage, community thrift stores, and offices. Maintaining more building space per student is costly to the District since the majority of its funding is based on its number of students, not the amount of square footage it maintains.

Table 2: Number of students, capacity, and percentage of capacity used for schools that operated at less than 60 percent of capacityFiscal year 2011(Unaudited)

Source: Auditor General staff analysis of district-reported fiscal year 2011 average daily membership information obtained from the Arizona Department of Education and fiscal year 2011 gross square footage and designed capacity information obtained from the Arizona School Facilities Board.

School name Number of students

Designed capacity

Percentage of capacity

used Whispering Wind Academy 478 940 51% Greenway Middle School 516 980 53 Palomino Primary School 533 977 55 Village Vista Elementary School 363 651 56 Arrowhead Elementary School 413 733 56 Shea Middle School 663 1,161 57 Sunset Canyon School 517 890 58 Desert Trails Elementary School 502 860 58 Desert Cove Elementary School 519 888 58 Paradise Valley High School 1,541 2,625 59

page 8State of Arizona

District built new school despite having excess space and still has excess space since subsequently closing two schools

Although the District’s student enrollment declined steadily between 2005 and 2011, and it had substantial excess building space during this time, the District constructed a new elementary school, Fireside Elementary, which opened in August 2012. According to district officials, the new school was built to address expected future overcrowding at Wildfire Elementary school. However, auditors noted that the District already had three other elementary schools within approximately 4 miles of Wildfire Elementary school that were operating between 58 and 78 percent of capacity and could have easily accommodated anticipated growth in the area. District officials also stated that they wanted Fireside Elementary to be a neighborhood school and that having neighborhood schools is important for the District to compete with charter schools.

Four months after the opening of Fireside Elementary school, the District’s Governing Board approved closing two elementary schools at the end of the 2013 school year. However, the District’s trend of declining student enrollment continued in fiscal years 2012 and 2013 as the District lost almost 300 additional students during those years, further increasing the District’s amount of excess space.

Recommendation

In light of the District’s continued decline in student enrollment and excess building capacity even after closing two schools, the District should continue to evaluate how it can reduce its excess building space.

page 9

Office of the Auditor General

FINDING 3

District needs to strengthen controls over computer systems

Paradise Valley USD needs to improve controls over its computer systems. Although no improper transactions were detected by auditors, improving controls can reduce the risk of unauthorized access to critical systems and sensitive information. Additionally, the District’s lack of a disaster recovery plan could result in interrupted operations or loss of data. Specifically:

• Weak password requirements—The District needs stronger password controls over its critical applications, including the student information system, accounting system, and six other systems reviewed by auditors. The District’s Information Technology department developed, assigned, and stored user passwords, and users could not change their passwords to confidential ones. The District’s poor password process was primarily the result of using an outdated active directory service on its servers, and the District was in the process of evaluating alternatives to address this issue. Passwords should be user defined, based on specific composition requirements, known only to the user, and changed periodically. Common practice requires passwords to be confidential, be at least eight characters, contain a combination of alphabetic and numeric characters, and be changed every 90 days. This practice would decrease the risk of unauthorized persons’ gaining access to the systems.

• Inadequate procedures for removing access to critical systems—The District did not have sufficient procedures in place to ensure that only current employees had access to critical systems, including the accounting and student information systems. Auditors reviewed the system access of 392 former district employees and found that 30 of them still had active user accounts 1 to 11 months after they left the District. Although the District had procedures to disable employee accounts upon termination, these accounts were not always disabled. Active accounts linked to terminated employees increase the District’s risk of unauthorized use of sensitive information.

• Too many employees with high-level access—High-level access to systems such as the student information or accounting systems allows a user to control system settings such as the ability to add new users and modify the level of access users have in the system and to access sensitive information. Typically, only one or two information technology employees have this type of access. However, in reviewing five critical systems, auditors found several employees had high-level access to some of the systems. For example, the District’s student information system

page 10State of Arizona

had two employees who were system administrators with access to all system settings and information, three more employees who could add or delete users, and five additional employees who had access to user names and passwords. The District should review and restrict employee access to only what is necessary for their job duties.

• Cost benefit and risk assessment lacking for service providers—The District relied heavily on on-line computing and remote storage for many of its computerized systems, using several third-party vendors. This included the storage of electronic documents, and the processing and storage of e-mails, student information, and the accounting system. The vendors can potentially provide these services at lower costs than it would take to build and manage these systems in-house, and the information is more readily available from remote locations. However, the District did not always perform a thorough cost-benefit analysis supporting that the contracted services were lower cost than providing these services in-house. Further, there are risks in using these services that the District has not addressed. The most significant of these risks is that the District’s information is stored on the vendors’ servers and the District has little to no control over how this data is managed or who has access to the data. According to the contracts, the vendors are able to transfer, store, and process this data at any facilities they or their agents own, which in at least one case means the District’s information may be stored in unspecified countries around the world. This brings up potential data security, privacy, and liability issues concerning access to the data and liability for breach or loss of data, which is not sufficiently addressed in the contracts with these vendors.

• Lack of disaster recovery plan could result in interrupted operations or loss of data—The District did not have a formal, up-to-date, and tested disaster recovery plan. A written and properly designed disaster recovery plan would help ensure continued operations in the case of a system or equipment failure or interruption. Although Paradise Valley USD relies heavily on on-line computing for many of its systems, and some of these vendors manage disaster recovery independently, the District does not have a comprehensive plan to tie all of these systems together and address how to recover business operations as a whole. Further, the District had not tested its ability to restore electronic data files from its backup media for those systems that are backed up, which could result in the loss of sensitive and critical data due to the inability to restore this data successfully. Disaster recovery plans should be written, formalized, and tested periodically, and modifications should be made to correct any problems and ensure their effectiveness.

page 11

Office of the Auditor General

Recommendations

1. The District should improve password controls and require users to immediately change assigned passwords and then again periodically.

2. The District should enforce its policies to ensure that terminated employees have their IT system access promptly removed.

3. The District should reduce its number of users with high-level access to its critical systems.

4. The District should conduct a more thorough cost-benefit analysis and risk assessment for using on-line computing and storage services for sensitive information to evaluate the costs and risks of using these services.

5. The District should create a formal disaster recovery plan and test it periodically to identify and remedy deficiencies.

page 12State of Arizona

page 13

Office of the Auditor General

Some Classroom Site Fund monies spent inappropriately or without adequate support

In fiscal year 2011, Paradise Valley USD spent some Classroom Site Fund (CSF) monies inappropriately or without adequate support.1 The District spent a portion of its CSF performance pay monies for purposes other than those included in the District’s Governing Board-approved plan. In addition, the District did not maintain documentation showing whether some performance pay goals were met. Further, the District paid CSF monies to 128 individuals for a training they likely did not attend and paid CSF monies to a few employees who worked in positions that did not qualify for CSF performance pay.

District used some performance pay monies for purposes not listed in its plan, and pay records were not maintained

In fiscal year 2011, the District paid 1,636 employees 1 percent of their salaries from CSF monies to attend two training days designed to increase student achievement. However, payments for attending these trainings were not included in the Governing Board-approved performance pay plan. Further, the District did not take attendance or maintain rosters to ensure that employees who received the CSF monies to attend these trainings actually attended them. In fact, auditors identified 128 employees who received these monies despite not being employed by the District until after these trainings were held.

Additionally, the District did not always maintain documentation showing that performance pay goals were met. The District’s plan included both a site-level group goal and an individual goal, each worth $552 upon completion. Auditors reviewed the site-level goal at two of the District’s schools and found that no documentation was retained to show that the site goals were met. Additionally, auditors reviewed the individual performance pay goal payments made to 14 employees and found supporting documentation for only 3 of the 14 payments. As a result, the District could not show that its employees had met the required performance measures for performance pay they received in fiscal year 2011. School districts are required to retain this type of documentation for 4 years as required by state records retention schedules.2

1 In November 2000, voters passed Proposition 301, which increased the state-wide sales tax to provide additional resources for education programs. Under statute, these monies, also known as Classroom Site Fund monies, may be spent only for specific purposes, primarily increasing teacher pay.

2 Arizona State Library, Archives, and Public Records. General Records Retention Schedule for All Public Bodies, Finance Records. Schedule Number 000-11-76.

FINDING 4

page 14State of Arizona

Small amount of Classroom Site Fund monies paid to ineligible employees

Only individuals employed to provide instruction related to the District’s educational mission may receive CSF monies intended for teacher compensation increases. However, in fiscal year 2011, Paradise Valley USD paid about $9,000 in CSF salary increases and performance pay to three employees who were not directly involved in providing instruction. These employees performed administrative and attendance duties.

Recommendations

1. The District should ensure that it properly documents all requirements for eligible employees to receive CSF monies in its Governing Board-approved performance pay plan.

2. The District should ensure that it pays CSF monies in accordance with its Governing Board-approved performance pay plan.

3. The District should ensure that it retains adequate documentation for the required time period to demonstrate that performance pay goals were met.

4. The District should ensure that only eligible employees receive CSF monies.

page 15

Office of the Auditor General

OTHER FINDINGS

In addition to the four main findings presented in this report, auditors identified one other less significant area of concern that requires district action.

Student transportation mileage misreported

In fiscal year 2011, Paradise Valley USD incorrectly reported to the Arizona Department of Education (ADE) the number of route miles the District traveled. The District reported estimated miles rather than actual miles as required by ADE. This resulted in an overstatement of about 79,000 miles, or 3 percent of its total miles. This error did not impact the District’s transportation funding because its reported route miles for fiscal year 2011, although overstated by 79,000 miles, were still less than its reported route miles in fiscal year 2010. Since the State’s transportation funding formula contains a provision that increases funding for year-to-year increases in mileage but does not decrease funding for year-to-year decreases in mileage, the District’s error did not result in additional funding to the District. Still, the District should take steps to ensure it submits accurate route mileage to ADE for funding purposes.

Recommendation

The District should accurately calculate and report miles driven for state funding purposes.

page 16State of Arizona

APPENDIX

page a-1

Office of the Auditor General

Objectives, Scope, and Methodology

The Office of the Auditor General has conducted a performance audit of the Paradise Valley Unified School District pursuant to A.R.S. §41-1279.03(A)(9). Based in part on their effect on classroom dollars, as previously reported in the Auditor General’s annual report, Arizona School District Spending (Classroom Dollars report), this audit focused on the District’s efficiency and effectiveness in four operational areas: administration, plant operations and maintenance, food service, and student transportation. To evaluate costs in each of these areas, only current expenditures, primarily for fiscal year 2011, were considered.1 Further, because of the underlying law initiating these performance audits, auditors also reviewed the District’s use of Proposition 301 sales tax monies and how it accounted for dollars spent in the classroom.

In conducting this audit, auditors used a variety of methods, including examining various records, such as available fiscal year 2011 summary accounting data for all districts and Paradise Valley USD’s fiscal year 2011 detailed accounting data, contracts, and other district documents; reviewing district policies, procedures, and related internal controls; reviewing applicable statutes; and interviewing district administrators and staff.

To compare districts’ academic indicators, auditors developed a separate student achievement peer group using poverty as the primary factor because poverty has been shown to be associated with student achievement. Auditors also used secondary factors such as district type and location to further refine these groups. Paradise Valley USD’s student achievement peer group includes Paradise Valley USD and the seven other unified districts that also served student populations with poverty rates between 11 and 16 percent in cities and suburbs. Auditors compared Paradise Valley USD’s student AIMS scores to those of its peer group averages. Generally, auditors considered Paradise Valley USD’s student AIMS scores to be similar if they were within 5 percentage points of peer averages, slightly higher/lower if they were within 6 to 10 percentage points of peer averages, higher/lower if they were within 11 to 15 percentage points of peer averages, and much higher/lower if they were more than 15 percentage points higher/lower than peer averages. In determining the District’s overall student achievement level, auditors considered the differences in AIMS scores between Paradise Valley USD and its peers, as well as the District’s graduation rate and ADE-assigned letter grade.

To analyze Paradise Valley USD’s operational efficiency, auditors selected a group of peer districts based on their similarities in district size, type, and location. This operational peer group includes Paradise Valley USD and the nine other high school and unified districts that also served more than

1 Operational spending includes costs incurred for the District’s day-to-day operations. It excludes costs associated with repaying debt, capital outlay (such as purchasing land, buildings, and equipment), and programs such as adult education and community service that are outside the scope of preschool through grade-12 education.

page a-2State of Arizona

20,000 students and were located in cities and suburbs. Auditors compared Paradise Valley USD’s costs to its peer group averages. Generally, auditors considered Paradise Valley USD’s costs to be similar if they were within 5 percent of peer averages, slightly higher/lower if they were within 6 to 10 percent of peer averages, higher/lower if they were within 11 to 15 percent of peer averages, and much higher/lower if they were more than 15 percent higher/lower than peer averages. However, in determining the overall efficiency of Paradise Valley USD’s nonclassroom operational areas, auditors also considered other factors that affect costs and operational efficiency such as staffing levels, square footage per student, meal participation rates, and bus capacity utilization, as well as auditor observations and any unique or unusual challenges the District had. Additionally:

• To assess whether the District’s plant operations and maintenance function was managed appropriately and functioned efficiently, auditors reviewed and evaluated fiscal year 2011 plant operations and maintenance costs and district building space, and compared these costs and capacities to peer districts’. To analyze the District’s solar power system contracts and its effect on electricity costs, auditors reviewed solar power bills; interviewed district staff; obtained information related to the District’s electric utility usage, costs, and rate plans; and reviewed 19 solar contracts from other Arizona school districts.

• To assess the District’s computer information systems and network, auditors evaluated certain controls over its logical and physical security, including user access to sensitive data and critical systems, and the security of servers that house the data and systems. Auditors also evaluated certain district policies over the system such as data sensitivity, backup, and recovery; and reviewed the District’s written agreements with IT service providers that process and/or store district data.

• To assess whether the District was in compliance with Proposition 301’s Classroom Site Fund requirements, auditors reviewed fiscal year 2011 expenditures to determine whether they were appropriate and if the District properly accounted for them. Auditors also reviewed the District’s performance pay plan and whether the individuals who received Classroom Site Fund monies were eligible based on their job descriptions. Auditors also analyzed how performance pay was being distributed.

• To assess whether the District’s transportation program was managed appropriately and functioned efficiently, auditors reviewed and evaluated required transportation reports, driver files, bus maintenance and safety records, bus routing, and bus capacity usage. Auditors also reviewed fiscal year 2011 transportation costs and compared them to peer districts’.

• To assess the District’s financial accounting data, auditors evaluated the District’s internal controls related to expenditure processing and scanned all payroll and accounts payable transactions for proper account classification and reasonableness. Additionally, auditors reviewed detailed payroll and personnel records for 30 of the 4,888 individuals who received payments through the District’s payroll system and reviewed supporting documentation for 30 of the 59,629 accounts payable transactions in fiscal year 2011. Auditors also evaluated other internal controls that were considered significant to the audit objectives and reviewed fiscal year 2011 spending across operational areas.

page a-3

Office of the Auditor General

• To assess whether the District’s administration effectively and efficiently managed district operations, auditors evaluated administrative procedures and controls at the district and school level, including reviewing personnel files and other pertinent documents, reviewing contracted employee agreements and invoices, and interviewing district and school administrators about their duties. Auditors also reviewed and evaluated fiscal year 2011 administration costs and compared these to peer districts’.

• To assess whether the District’s food service program was managed appropriately and functioned efficiently, auditors reviewed fiscal year 2011 food service revenues and expenditures, including labor and food costs, compared costs and staffing levels to peer districts’, reviewed the Arizona Department of Education’s food service monitoring reports, and observed food service operations.

We conducted this performance audit in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

The Auditor General and her staff express their appreciation to the Paradise Valley Unified School District’s board members, superintendent, and staff for their cooperation and assistance throughout the audit.

page a-4State of Arizona

DIS

TRIC

T RE

SP

ON

SE

DISTRICT RESPONSE

October 22, 2013

Ms. Debra K. Davenport, Auditor General Division of School Audits 2910 North 44th Street, Suite 410 Phoenix, Arizona 85018 Dear Ms. Davenport: The Paradise Valley Unified School District respectfully submits its response to the Performance Audit for the 2011 Fiscal Year conducted by the Office of the Auditor General, Division of School Audits. The District would like to thank the Auditor General staff and the leadership of Mike Quinlan, manager, and Brit Baxter, audit senior, for their professionalism, direction and education with regard to this audit, and agree with the audit findings and recommendations. The Paradise Valley Unified School District is proud of the academic success highlighted in the Performance Audit report. In fiscal year 2011, 85 percent of district students met or exceeded state standards in reading, 70 percent in math, and 69 percent in writing. These scores were higher than state averages. The District is equally proud of its cost-efficient programs noted in the Performance Audit. The report overview indicates that the district operated efficiently overall, with most costs lower than peer districts. The District is grateful that the report highlighted the fact that the District spent less per pupil overall than its peer district or state average, but spent more in the classroom than its peer districts and state average. District administrative costs were nine percent lower than its peer districts averaged, and 22 percent lower than the state average for administrative costs. District food service and transportation programs were both determined to be operated efficiently. The Paradise Valley Unified School District remains committed to increasing student achievement while maintaining fiscal responsibility, transparency, and effective stewardship of taxpayer funds. We value the input and collaboration from the Auditor General staff in this process. Please contact us if there are any questions regarding our response. Sincerely, James P. Lee, Ed.D. Superintendent

Office of the Superintendent District Administrative Center 15002 North 32nd Street Phoenix AZ 85032

Finding 1: District’s solar power system contracts unlikely to meet cost‐saving expectations, but District has acted to recover estimated financial losses The District agrees with the finding. The District has implemented the recommendations. Recommendation 1 The District should continue to monitor its solar power production and electricity usage and costs to help ensure any financial losses are minimized and that the amounts in the escrow accounts are adequate to cover actual losses. The District agrees with the recommendation and has procedures in place to monitor power production,

electricity use and costs and will continue the monitoring through the duration of the contract.

Recommendation 2 The District should regularly review its electric utility’s rate plan options, especially for the District’s sites with solar power systems, to determine if the District is on the best rate plan available for each site’s specific conditions. The District has begun reviewing the utility rate plans when there is a change in order to determine if a

change in the District’s rate plan(s) is warranted. The District has recently made changes in rate plans at

several sites to take advantage of changes in Arizona Public Service rate structures.

Finding 2: District should continue to review options to address excess building capacity The District agrees with the finding and has implemented the recommendation. Recommendation In light of the District’s continued decline in student enrollment and excess building capacity even after closing two schools, the District should continue to evaluate how it can reduce its excess building space.

The District continually monitors enrollment trends, housing construction, occupancy rates and other

factors and is diligent in its facility planning. There are many factors beyond the District’s control,

including open enrollment and state‐sponsored charter schools, that have contributed to schools in the

southern portion of the district being operated at less than capacity. It is important to note that there

are factors other than square feet per student that are considered when making building capacity

decisions. The District takes into consideration the needs and desires of its students, parents and

communities as well as geographic realities such as State Route 101, which divides the northern third of

the district, as well as projected growth rates north of the 101, when determining use of its space.

These factors and needs notwithstanding, the District will continue to include reduction of excess

building space in its facility planning.

Finding 3: District needs to strengthen controls over computer systems

The District agrees with the finding and will implement the recommendations.

Recommendation 1 The District should improve password controls and require users to immediately change assigned passwords and then again periodically.

The District has implemented a new password control process via a preferred method of security by

layers. Unique passwords for each employee/critical system are used, as required. All employees are

required to complete annual training on the password control/recovery process and best practices of

confidentiality and security of information technology. The District is developing a protocol requiring

the periodic changing of passwords.

Recommendation 2 The District should enforce its policies to ensure that terminated employees have their IT system access promptly removed.

The District is enforcing its policies via an automated system that disables access to HR/Financial,

student information and communication systems upon employee termination. Automation occurs

nightly or can be triggered immediately with HR administration notification to IT administration.

Recommendation 3 The District should reduce its number of users with high-level access to its critical systems.

The District has reduced its number of users with high‐level access in certain areas and continues to

review who should have what levels of access to confidential systems. The review includes determining

which employees need to have access based on job duties, federal and state requirements, and

necessity of redundancy for workflow and emergency response purposes.

Recommendation 4 The District should conduct a more thorough cost-benefit analysis and risk assessment for using on-line computing and storage services for sensitive information to evaluate the costs and risks of using these services.

In the future the District will conduct more thorough cost‐benefit and risk assessments for its on‐line

computing and storage services for sensitive information. The District will continue to conduct periodic

risk assessments of its on‐line computing and storage services and will better document its efforts in

these areas.

Recommendation 5 The District should create a formal disaster recovery plan and test it periodically to identify and remedy deficiencies.

The District agrees with the recommendation and will document the process as it creates and tests the

plan based upon guidance from the Auditor General staff.

Finding 4: Some Classroom Site Fund monies spent inappropriately or without adequate support The District agrees with the finding has implemented the recommendations. Recommendation 1 The District should ensure that it properly documents all requirements for eligible employees to receive CSF monies in its Governing Board-approved performance pay plan. The District will ensure that all pay for performance components are included in the plan annually approved by the Governing Board. Recommendation 2 The District should ensure that it pays CSF monies in accordance with its Governing Board-approved performance pay plan. The District will ensure that it pays all CSF pay for performance salaries in accordance with its pay for performance plan. Recommendation 3 The District should ensure that it retains adequate documentation for the required time period to demonstrate that performance pay goals were met. The District has reviewed and revised its records retention practices to ensure that adequate documentation is maintained for the required time period. Recommendation 4 The District should ensure that only eligible employees receive CSF monies. The District strives to properly classify its employee eligibility for CSF funding. The District has reviewed and revised its coding procedures to prevent such errors in the future. Other Finding: Student transportation mileage misreported The District agrees with the finding and has implemented the recommendation. Recommendation The District should accurately calculate and report miles driven for state funding purposes The District has implemented the route mile calculation methodology recommended by the Auditor General staff.