pakistan fy17 budget review june 2016 - arx.cfa budget fy17-focusing on... · pakistan fy17 budget...

TRANSCRIPT

Best Local Brokerage House

Brokers Poll 2011, 2012, 2013 & 2014

PAKISTAN

FY17 BUDGET REVIEW

June 2016

Topline Securities, PakistanREP-057

www.jamapunji.pk

Executive Summary

� After achieving macroeconomic stabilization during the last three years, PakistanGovt. has now shifted its focus towards growth as it unveiled pro growth FY17budget.

� The focus of the budget remained on revival of Agriculture sector that contributes21% of GDP and Textile sector that is the main driver of country’s exports.

� The budget was largely neutral for the local Equity Market as taxes on dividend andcapital gains were unchanged, other than for non-tax filers, which we believe willhave minimal impact as most investors are tax filers.

� We expect Pakistan market to gradually improve post budget due to 1) incentivesfor Fertilizer and Textile sectors and 2) Incentives for industrial sector and new

2

for Fertilizer and Textile sectors and 2) Incentives for industrial sector and newlistings.

� Though budgetary measures are negative for insurance and neutral to negative forbanks and consumers, we believe that pro-growth policies of the current Govt. andpositive macroeconomic outlook will gradually filter across the board and help keepmarket sentiments in positive territory.

Stock Market – Expected Measures & Impact

Capital Gains Tax (CGT)

� The Govt. has not made any changes in capital gain tax for tax filers, which ispositive for market as most investors, we believe, are filers. Currently, 15% CGT islevied on sale of shares within 12 months, 12.5% on sale between 12-24 monthsand 7.5% tax if sold between 2-4 years for filers.

� For non-filers, capital gains tax will be 18% (compared to 15% for filers) if holdingperiod is less than 12 months. If holding period is between 12 to 24 months, thenthe rate will be 16% (compared to 12.5% for filers). If holding period is 24 to 48months then the rate will be 11% (compared to 7.5% for filers).

3

Stock Market: CGT over the years

Tax Year

Rate of tax where holding period is

<6m> 6m but <

12m<12m

12m or more but <24m

24m or more but < 48m

2012 10.0% 8.0% - - -

2013 10.0% 8.0% - - -

2014 10.0% 8.0% - - -

2015 12.5% 12.5% 12.5% 10.0% -

2016 15.0% 15.0% 15.0% 12.5% 7.5%

2017 - Filer 15.0% 15.0% 15.0% 12.5% 7.5%

2017 - Non Filer 18.0% 18.0% 18.0% 16.0% 11.0%

Source: Budget 2016-17 Document, Topline Research

Tax on Dividend Income

� The Govt., similar to CGT, has not changed the tax regime on tax filers for dividendincome, which stands at 12.5%. However, for non-filers, tax on dividend incomehas been increased from 17.5% to 20.0%.

Alternative Corporate Tax

� In Federal Budget FY16, the Govt. imposed Alternate Corporate Tax (ACT) of 17%of accounting income as companies were required to pay higher of the corporatetax or ACT. The Govt. in this budget has proposed to collect advance tax on ACT,which is expected to raise additional taxes of Rs16bn from companies.

Tax on Bonus Shares

� Ever since imposition of 5% tax on bonus shares, there has been a major decline in

Stock Market (contd.)

4

� Ever since imposition of 5% tax on bonus shares, there has been a major decline inannouncement of bonus shares by listed firms. The Govt. in this budget has notchanged the tax regime for bonus shares.

Corporate Tax & Super Tax

� Corporate tax rate has been proposed to be reduced to 31% in FY17 from current32% in line with the Govt. policy to reduce corporate tax rate gradually. This 1%reduction will increase profits of non-banks by 1.5% and is already incorporated inour forecasts.

� Super tax that was levied in Tax Year 2015 to meet revenue needs is beingextended to Tax Year 2016. As per income tax ordinance, companies who areearning more than Rs500mn in pre-tax profits will be subject to 3% tax (4% forbanks). This will have negative earnings impact of ~3% on our sample companies.

Incentives for new listings

� Currently, there is a 20% tax credit for new listings on Pakistan stock exchange for1 year. In order to encourage enlistment of companies on PSX, tax credit is beingextended to 2 years.

� At present, 100% tax credit on tax payable is allowed if 100% fresh equity is raisedthrough issuance of new shares. This tax credit is allowable for five years fromcommercial production. It is proposed to reduce condition of 100% fresh equity to70% equity and tax credit would be allowed proportionately on owned new equity.This is expected to further promote new listings on PSX.

Taxation for not distributing dividends

� In last year’s budget, the Govt. imposed tax on reserves if listed companies (other

Stock Market (contd.)

5

� In last year’s budget, the Govt. imposed tax on reserves if listed companies (otherthan bank/modaraba) did not distribute dividends. This led to overall higherdividend payouts and improved investor sentiments. This measure remainsenforced and is positive for market sentiments.

Increased tax on brokers

� The Govt. has now revised rate of advance tax from 0.01% of purchase/sale valueto 0.02% of purchase/sale value. This may have an impact on broker margins.

Minimum tax on companies

� The Govt. has proposed to implement minimum tax of 1% on turnover oncompanies declaring gross losses. Currently companies declaring gross loss areexempt from payment of minimum tax. This will help reduce tax avoidance ascurrently individuals and Association of Persons (AOPs) are subject to this tax.

Stock Market (contd.)Conclusion: Neutral for the market

� Overall, we think Budget FY17 is ‘Neutral’ for the market. Pakistan’s entry intoMSCI emerging market remains a key trigger for the market.

� We are ‘Over-weight’ on Cement, Autos, OMCs, and Consumer sectors.

Top Picks: Key Numbers

PE (x) Dividend Yield PBV (x)

2016E 2017F 2018F 2016E 2017F 2018F 2016E 2017F 2018F

Market 9.8 8.6 7.7 5% 6% 7% 1.6 1.4 1.3

Market (ex-Oil) 9.5 8.4 7.7 6% 7% 7% 1.6 1.5 1.4

OGDC 10.4 9.4 7.9 3% 4% 5% 1.2 1.1 1.1

MCB 10.9 10.1 9.4 6% 7% 8% 1.7 1.6 1.6

6

MCB 10.9 10.1 9.4 6% 7% 8% 1.7 1.6 1.6

UBL 7.8 7.2 6.5 7% 7% 8% 1.3 1.2 1.2

KEL 6.5 5.1 4.9 0% 0% 0% 2.0 1.5 1.5

LUCK 11.9 9.8 8.4 2% 2% 3% 2.3 2.0 2.0

ENGRO 10.8 9.3 8.2 7% 8% 9% 3.0 2.8 2.8

HUBC 11.8 10.2 9.5 8% 9% 10% 4.0 4.0 4.0

PSO 11.4 6.0 5.0 2% 5% 6% 1.1 1.1 1.1

DGKC 8.5 6.9 5.8 3% 4% 5% 1.1 1.0 1.0

INDU 7.4 6.8 6.3 12% 13% 14% 3.2 3.0 3.0

MLCF 10.0 7.9 5.9 0% 5% 7% 2.5 2.1 2.1

NML 5.5 4.7 4.7 4% 4% 4% 0.5 0.5 0.5

KOHC 8.2 6.8 5.5 6% 6% 8% 3.0 2.4 2.4

PAEL 8.1 7.1 6.3 4% 5% 5% 1.8 1.5 1.5

IGIIL 13.8 12.6 10.9 3% 3% 4% 1.7 1.5 1.5

AICL 6.3 5.4 4.6 9% 9% 9% 1.2 1.1 1.1

Source: Topline Research

� As expected the Govt. has focused on the agriculture sector in this year’s budgetand in this spirit has announced reduction in Urea prices. This has been done intwo steps. Firstly, the Govt. has reduced GST on Urea from 17% to 5%, whichresults in Rs185/bag at current price of Rs1,800 per bag. Further, Federal andProvincial Govts. will be giving subsidy of Rs215/bag to reduce price of Urea toRs1,400/bag. Total burden of this subsidy is expected at Rs36bn.

� The Govt. has also announced subsidy on DAP to reduce its price to Rs2,500/bagfrom Rs2,800/bag, which is expected to cost the Govt. Rs10bn. These areextremely positive measures and will improve Urea off take that had come off lateand had resulted in piling up of inventories. We expect significant reduction in ureainventory levels, which bodes well for local urea producers.

�

PositiveFertilizer

Sector Impact Analysis

7

� There is no change in GIDC on either Feed of Fuel tariff. There were expectationthat this might be reduced.

� Improved farmer liquidity due to elimination of 7% GST on pesticides should helpsupport sales of fertilizer.

� The Govt. has announced the following relief for the agriculture sector, whichshould further improve farmer liquidity and benefit local fertilizer sales:

1. Increased Agriculture Credit target to Rs700bn from Rs600bn last year.

2. The Govt. has reduced electricity tariff for tube wells from Rs8.85/unit toRs5.35/unit, which is expected to cost Rs27bn in subsidy.

3. SBP has developed a framework to reduce mark-up rates of ZTBL, NBP, Bank ofPunjab and Punjab Co-operative by 2.0% to Agriculture.

Sector Impact Analysis (contd.)

� The Govt., as expected, has given zero-rated status to Textile Sector, which shouldhelp improve liquidity of the sector. The sector is now subject to no tax and norefund policy under GST and will not have any funds stuck up as receivables fromthe Govt. that affects their business.

� The Govt. to further provide liquidity to the sector has committed to refund stuck upsales tax by Aug 2016. These measures should help improve profitability to someextent given lower working capital requirements and financial charges.

� The Govt. has reduced export refinance rate from 3.5% to 3.0%, which shouldfurther help reduce borrowing costs for the sector.

� Relief measures announced in previous year’s budget including duty drawbackrates on various textile products and duty free textile machinery imports have been

PositiveTextile

8

� From Pakistan State Oil (PSO), the Govt. expects to receive dividend income ofRs660mn (Rs2.2/share). While it expects to receive dividend income of Rs500mn(Rs0.8/share) and Rs1,500mn (Rs1.7/share) from Sui Northern Gas (SNGP) andSui Southern Gas (SSGC), respectively. However we expect dividend per share ofRs15 from PSO thanks to improving cash flows while SNGP is estimated to declareRs1.3 in FY17 while we do not expected any dividend from SSGC.

� Minimum turnover tax has been maintained at 0.5% on OMCs.

� The Govt. has set target of Rs150bn collection under petroleum development levy(PDL) in FY17, which is up 11%. This will have no impact on the sector.

NeutralOMCs

rates on various textile products and duty free textile machinery imports have beenannounced in this year’s budget as well.

� Concessionary duties on man made fibers not produced locally are proposed to becontinued in this year’s budget, which should be positive for local textile industry.

Sector Impact Analysis (contd.)� The Govt. has proposed to change the Federal Excise Duty (FED) mechanism from

variable 5% of Marginal Retail Price (MRP) to a fixed Rs1/kg (Rs50 per bag). Thischange will not only increase existing FED (around Rs22 on 50kg bag ofRs515), but also increase sales tax in absolute terms as sales tax is beingcalculated on top of FED. Consequently, cost will be increased by Rs33 per bag(Rs660 per ton).

� On the other hand, the Govt. has reduced import duty on coal from 6% to5%, which will have a positive impact of Rs1/bag. We believe that the net impact ofRs32/bag will be neutral for the industry in the long run as contraction in supply-demand gap and robust demand will enable cement manufacturers to graduallypass on the impact to final consumers.

� The Govt. is expected to set consolidated PSDP (Public Sector Development)

Cements Neutral

9

� The Govt. is expected to set consolidated PSDP (Public Sector Development)target of Rs1.67tn (up 11%) for FY17. With no IMF restrictions and decent fiscalspace, this higher Govt. spending bodes well for the sector as this will result inincreased construction activities. Further, the Govt. has allocated Rs188bn forconstruction of roads, highways and bridges, which is an increase of about 18% ascompared to last year.

� In order to promote housing, the Govt. has increased maximum deductableallowance from Rs1mn to Rs2mn on payment of profit on debt for construction of anew house or acquisition of house. This would help increase housing demand andwould result in improved cement sales.

� The Govt. has imposed final tax on builders/land developers on basis of per unitarea, which is expected to generate Rs25bn in new taxes. This proposal hasalready been vetted by local association of builders and we do not expect this tohave any meaningful impact on booming construction activities in the country.

Sector Impact Analysis (contd.)

� The Govt. plans on adding 10,000MW by Mar 2018, which will help alleviate poweroutages in the country.

� Due to lower oil prices, piling up of circular debt has reduced, which bodes well forthe country’s energy sector chain and particularly the power sector.

Power Neutral

� The Govt. has increased rate of sales tax on mobile phones, which will result inhigher prices of mobiles, which we believe will be neutral for the telecom sector.

� In order to promote information technology (IT) sector, income tax exemption for

Telecom Neutral

� The Govt. has also increased customs duty on import of clinker from 2% to11%, which will be positive for local industry and will discourage clinker imports.

Cements (cont.)

10

� In order to promote information technology (IT) sector, income tax exemption forexporters of IT services is proposed to be extended for the next 3 years.

� The Govt. expects to receive dividend of Rs35bn (Rs8/share) from Oil and GasDevelopment Company (OGDC). This is higher than our expectations of Rs5/sh.Further, the Govt. expects dividend from Pakistan Petroleum Limited (PPL) ofRs7bn (Rs3.4/share). This is lower than our expectation of Rs6/share.

E&Ps Neutral

Sector Impact Analysis (contd.)

� The Govt. has endorsed recently announced Auto Policy in this year’s budget.Previously, there were expectations that import duty on used cars may be reduced.

� Advance tax of 3% has been imposed on financing/leasing on vehicles to becollected by financial institutions. We do not expect this to have meaningful impacton car financing as this is an adjustable tax expense.

� Positive policies for agriculture sector should help boost farm incomes and is likelyto result in improved auto demand from rural areas of the country.

� Regulatory duty of 10% on import of bead wire has been removed, which should beslightly positive for local tire manufacturers.

Auto Neutral

� In continuation of policy announced in FY16 budget, the Govt. has extended theBanks Neutral to

11

� In continuation of policy announced in FY16 budget, the Govt. has extended thelevy of super tax of 4% on bank’s income for tax year 2016. It will have an earningsimpact of around 6% in 2016 as banks will likely book additional tax burden in2Q2016 just like in 2015.

� Govt. has clarified that WHT on cash withdrawal of over Rs50,000 shall beaggregates from all banks in a single day rather than separate transaction ofRs50,000 from each bank account. This rule will also apply on WHT of 0.6% forbanking transactions of over Rs50,000 for non- tax filers. This could discouragecash withdrawals and deposit mobilization in the banking system. Overall impact isnot significant on banking deposits.

� The proposal to increase WHT from 0.4% on cash withdrawals for tax filers and0.6% on non-filers has not been accepted and there is no change in the ruling.

� Govt. has set a target of Rs700bn (up 17%) for Agriculture credit in FY17, which isto be financed by commercial banks. If this happen it bodes well for local banks.

Banks Neutral to

Negative

Sector Impact Analysis (contd.)

� Zero-rated status on milk products has been withdrawn and these have beenplaced in tax exempt category. Local milk producers will therefore not be able toclaim refund on sales tax paid on inputs, which will have an impact of aroundRs6/ltr. To recall both Nestle and Engro Foods have raised their packaged milkprices by Rs5/ltr in last few weeks. Going forward another price increase to pass onthis cost to consumers cannot be ruled out. This rising prices will increase thepricing differential between packaged and loose milk. This may slightly affect salesgrowth of packaged milk producers, we believe.

Consumer Neutral to

Negative

� Govt. targets to raise Rs452bn in FY17 from total bank borrowing vs. Rs199bn inFY16. With IMF program completing in Sep 2016, Govt. may reduce itsdependence on commercial bank borrowing in favor of borrowing from centralbank. That may force banks to lend aggressively to private sector.

Banks (cont.)

12

growth of packaged milk producers, we believe.

� The Govt. has proposed to increase regulatory duty on powdered milk from 25% to45%, which will primarily impact tea whiteners (Tarang by EFOOD and Everyday byNESTLE) by Rs2-4/ltr. However, given strong competition in this segment, theimpact of this will partially be passed on to consumers and will affect margins in theshort run.

� The Govt. has continued with its tradition of increasing duties on cigarettes. In thisyear’s budget, the FED on cigarettes has been raised by 7.5%. Phillip Morris hasalready increased price of cigarettes by 3% few days back and we think they willpass on the impact to the consumers.

� The Govt. has also continued with its tradition of raising duties on aerated water asthese have been increased to 11.5% from 10.5%.

Sector Impact Analysis (contd.)

� It is proposed that all sources of income for insurance companies includingdividend income and capital gains are taxed at the level of corporate tax rate whichis 31% for FY17. Before this dividend and capital gain was taxed at lower rate. Thiswill have a negative earnings impact of 5%-10% for insurance companies that relyon returns from stock market.

� It is proposed to impose WHT of 4% on premium of non-life insurance on non-taxfilers and WHT of 1% on life insurance if the premium amount exceeds Rs0.2mn fornon-tax filers. This could slightly affect growth in insurance premium.

� At present, tax credit is available on the payment of life insurance premium up toRs1.5mn. A new tax credit @ 5% of tax payable or Rs100,000 whichever is less isproposed to be allowed on payment of premium of health insurance. Govt. has also

Insurance Negative

13

proposed to be allowed on payment of premium of health insurance. Govt. has alsoannounced health insurance scheme which targets to distribute insurance policy tothe tune of Rs9bn by FY18.

� At present, Commission paid to life insurance agents is taxed at the rate of 12% forfilers. The rate of tax is being reduced to 8% for tax filers on commission receivedup to Rs500,000.

� After achieving macroeconomic stabilization during last three years, Govt. has nowshifted its focus towards growth as it unveiled pro Growth FY17 budget. The focusof the budget remained on revival of Agriculture sector that contributes around 21%of GDP and Textile sector that is the main driver of country’s exports.

� Budget proposal prepared by the Govt. is based on principles including, 1) Gradualwithdrawal of tax concessions, 2) penalizing non-filers to encourage tax filing, 3)broadening tax base & documentation of economy and 4) increasing the share ofdirect taxation.

� The total outlay for budget FY17 is Rs 4.9tn (14.8% of GDP), which is 10% higherthan previous budget estimate of Rs4.4tn.

FY17 Budget Highlights

14

� The Govt. has total tax revenue target of Rs3.9tn (12.9% of GDP), 16% higher thanthe estimate for FY16. Non-tax revenues are estimated at Rs959bn (2.9% of GDP),5% higher than the estimated amount for FY16.

� These additional tax revenues will be collected from new tax measures to the tuneof Rs250bn and the remaining Rs286mn will likely be collected from normal GDPgrowth.

� Current Expenditures for FY17 is expected to clock in at Rs3.4tn (14.9% of GDP),which is 4% higher than the estimate of Rs3.2tn for FY16.

� Defense budget is estimated to increase by 11% at Rs860bn (2.6% of GDP),whereas debt servicing is likely to go up by 3% to Rs1.3tn (4.1% of GDP).

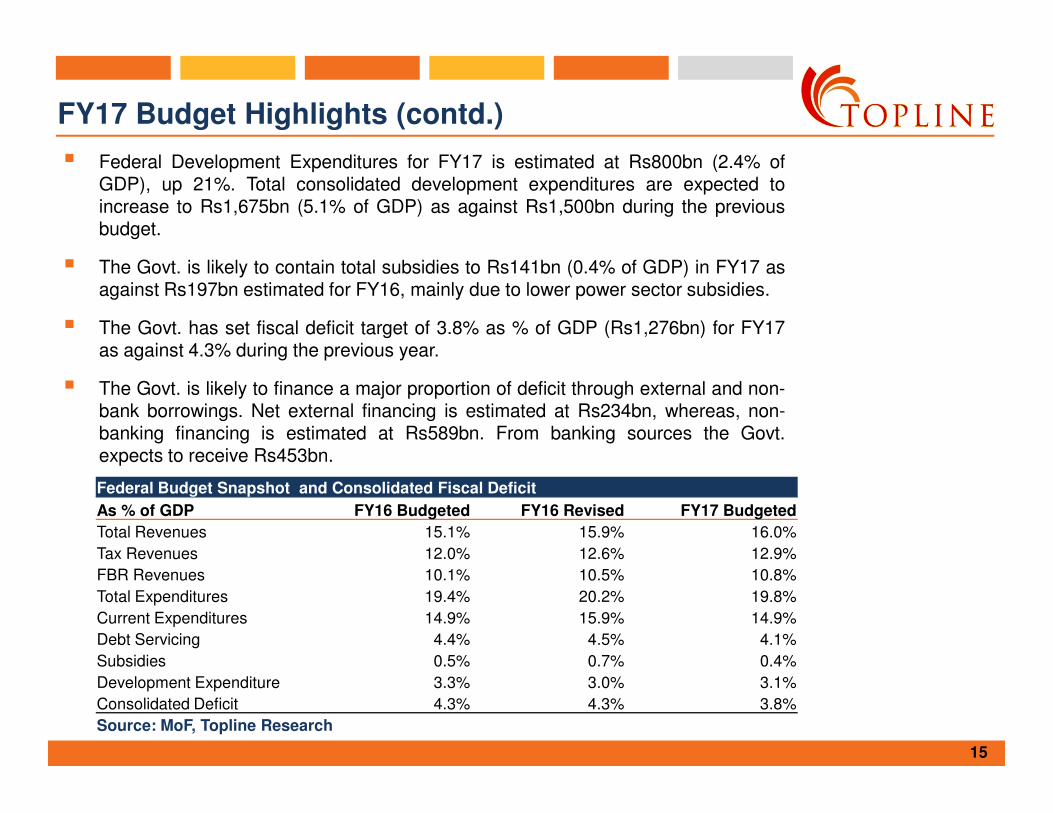

� Federal Development Expenditures for FY17 is estimated at Rs800bn (2.4% ofGDP), up 21%. Total consolidated development expenditures are expected toincrease to Rs1,675bn (5.1% of GDP) as against Rs1,500bn during the previousbudget.

� The Govt. is likely to contain total subsidies to Rs141bn (0.4% of GDP) in FY17 asagainst Rs197bn estimated for FY16, mainly due to lower power sector subsidies.

� The Govt. has set fiscal deficit target of 3.8% as % of GDP (Rs1,276bn) for FY17as against 4.3% during the previous year.

� The Govt. is likely to finance a major proportion of deficit through external and non-bank borrowings. Net external financing is estimated at Rs234bn, whereas, non-

FY17 Budget Highlights (contd.)

15

bank borrowings. Net external financing is estimated at Rs234bn, whereas, non-banking financing is estimated at Rs589bn. From banking sources the Govt.expects to receive Rs453bn.

Federal Budget Snapshot and Consolidated Fiscal Deficit

As % of GDP FY16 Budgeted FY16 Revised FY17 Budgeted

Total Revenues 15.1% 15.9% 16.0%

Tax Revenues 12.0% 12.6% 12.9%

FBR Revenues 10.1% 10.5% 10.8%

Total Expenditures 19.4% 20.2% 19.8%

Current Expenditures 14.9% 15.9% 14.9%

Debt Servicing 4.4% 4.5% 4.1%

Subsidies 0.5% 0.7% 0.4%

Development Expenditure 3.3% 3.0% 3.1%

Consolidated Deficit 4.3% 4.3% 3.8%

Source: MoF, Topline Research

FY17 Budget Highlights (contd.)

New Fiscal Year Economic Targets

� The Govt. has set GDP target of 5.7% in FY17 and plans to increase it to 7.0% byFY19.

� Fiscal deficit will be reduced to 3.8% of GDP (Rs1,276bn) in FY17 as against 4.3%in FY16. In the medium term, the Govt. will target to further contain fiscal deficit to3.5% by FY19.

� CPI inflation is expected to be lower than 3% in FY16 and the Govt. plans to keep itin single digit during the next three years.

� The Govt. targets to increase investment-to-GDP ratio to 21% from the existing15% by 2019. In FY16, it is expected to clock in at 15.2% vs. 15.5% last year.

16

Key Economic Indicators

FY12A FY13A FY14A FY15A FY16E FY17F

Real GDP growth (%) 3.8% 3.7% 4.1% 4.0% 4.7% 5.7%Inflation (%) 11.0% 7.4% 8.6% 4.6% 2.7% 6.0%Fiscal Deficit (%) 6.8% 8.2% 5.5% 5.3% 4.3% 3.8%Investment to GDP ratio (%) 15.0% 14.6% 14.9% 15.5% 15.2% 17.0%Current Account as % of GDP -2.1% -1.0% -1.3% -1.0% -0.6% 1.5%FX reserves (US$bn) 15.3 11.0 14.0 18.2 21.6 23.6

Remittances (US$bn) 13.2 13.9 15.8 17.9 19.4 21.3 Source: MoF, PBS, SBP

FY17 Budget Highlights (contd.)

Federal Budget Snapshot and Consolidated Fiscal Deficit

Rsbn FY16 Budgeted FY16 Revised FY17 Budgeted

Tax Revenues 3,418 3,420 3,956

FBR Revenues 3,104 3,104 3,621

Other Taxes 315 316 335

Non Tax Revenues 895 913 959

Gross Revenue Receipts 4,313 4,333 4,916

Net Revenue Receipts 2,463 2,481 2,780

Current Expenditure 3,166 3,282 3,400

17

Debt Servicing 1,280 1,315 1,360

Defense 781 776 860

Subsidies 138 197 141

Development Expenditures 969 879 1,051

PSDP-Federal 700 661 800

PSDP-Total 1,514 1,394 1,675

Other Development Expenditure 164 128 157

Total Expenditure 4,451 4,479 4,895

Fiscal Deficit 1,328 1,255 1,276

Source: MoF, Topline Research

2%

3%

4%

5%

6%

0

300

600

900

1200

1500

1800F

Y06A

FY

07A

FY

08A

FY

09A

FY

10A

FY

11A

FY

12A

FY

13A

FY

14A

FY

15A

FY

16E

FY

17F

Rsbn PSDP Allocation (bn) PSDP allocation percent of GDP

PSDP Budget Allocation & Actual Spending

18

2%

3%

4%

5%

6%

0

300

600

900

1200

1500

FY

06A

FY

07A

FY

08A

FY

09A

FY

10A

FY

11A

FY

12A

FY

13A

FY

14A

FY

15A

FY

16E

FY

17F

Rsbn Total PSDP spending Spending as % of GDP

Source: Source: Source: Source: MoFMoFMoFMoF, Topline Research, Topline Research, Topline Research, Topline Research

FY17 Budget – Other Measures

Tax Measures:

� It is proposed to extend holding period for taxation of capital gain on sale ofimmovable property from 2 years to 5 years to be charged at uniform 10% rate.

� At present, minimum tax on turnover is paid by individuals and AOPs havingturnover exceeding Rs50mn. A large number of Individuals and AOPs havingturnover below Rs50mn are filing returns yet they are not paying any tax. It isproposed that minimum tax @ 1% of turnover may be made payable by Individualsand AOPs having turnover exceeding Rs10mn.

� In order to expand the tax base, it is proposed that a withholding tax at the rate of5% of the value of minerals be collected from non-filers.

� The rate of withholding tax for providing or rendering services by print and

19

� The rate of withholding tax for providing or rendering services by print andelectronic media is 1%, whereas for others it ranges from 8-10% and for low marginsectors it is up to 2%. It is proposed that the withholding tax for providing orrendering services by print and electronic media to be enhanced from 1% to 1.5%.

� Rate of withholding tax for commercial bills of trading sector up to Rs20,000 permonth is fixed with various slabs. Rate of withholding tax for commercial bills aboveRs20,000 is 10%. This rate is proposed to be increased to 12%. There will be nochange for industrial consumers.

� It is also proposed that any person making payment for a foreign producedadvertisement shall collect withholding tax at the rate of 20% of the payment.

� Concessionary rates of Customs Duty and sales tax on major poultry feedingredients like soybean meal and vitamin premixes shall remain intact.However, other ingredients that are subject to sales tax at the rate of 5% areproposed to be subjected to sales tax at 10%.

FY17 Budget – Other Measures (contd.)

Relief Measures

� In order to promote industrial growth and employment generation tax credit @ 1%of the tax payable for a period of ten years that is allowed for every 50 employeesin an industrial undertaking to be set up by Jun 2018, is proposed to be increasedto 2%. This concession will be made available for 10 years to the industrialundertakings set up by Jun 2019.

� At present, tax credit on BMR (Balancing Modernization and replacement) isallowable at the rate of 10% of investment against tax payable for two years. Incase of investment through 100% new equity, tax credit on BMR is allowable at therate of 20% of investment against tax payable for five years. The period isproposed to be extended to 30th Jun 2019.

20

proposed to be extended to 30th Jun 2019.

� At present a manufacturer registered under sales tax that is making over 90% salesto registered sales tax persons is entitled to a tax credit of 2.5% of tax payable. Thetax credit is proposed to be enhanced from 2.5% to 3% of tax payable.

� Import of solar panels and related components were exempted from customs dutyregardless of local manufacturing of their substitutes till 30th June 2016. It isproposed that this relaxation be extended till 30th June, 2017.

� Sales tax on import of dumper trucks for Thar Coal is proposed to be abolished.

� In order to provide relief on education expenses which are unbearable for lowincome groups, it is proposed that individuals having taxable income less thanRs1mn should be given tax relief equal to 5% of school fee of up to Rs60,000/childper annum.

� At present a tax credit is available for contribution in an approved Pension Fundwith a maximum of 20% taxable income. An additional contribution of 2% forpersons above 41 years of age to a maximum of 50% of taxable income isavailable up to Jun 6, 2016. It is proposed that the period may be extended up toJun 6, 2019 with condition that the maximum tax credit be restricted to 30% oftaxable income of the preceding year.

� Large Trading Houses were exempted from payment of minimum tax at the rate of1% during the first 10 years of commencement of business operations. Thisexemption shall expire in Jun 2016. In order to incentivize this organized section ofthe retail sector and to attract foreign investment, this exemption is proposed to begradually withdrawn and minimum tax is proposed to be reduced to 0.5% of the

FY17 Budget – Other Measures (contd.)

21

gradually withdrawn and minimum tax is proposed to be reduced to 0.5% of theentire turnover up to Tax Year 2019.

Contact usMr. Mohammed Sohail CEO Dir: +92 (21) 35303333-4 [email protected]

Cell: +92 300 8232726

Research Team:

Mr. Saad HashemyChief Economist &

+92 (21) 35303346 [email protected] Research

Mr. Muhammad Tahir Saeed Deputy Head of Research +92 (21) 35303330 [email protected]

Mr. Umair Naseer Senior Research Analyst +92 (21) 35303330 [email protected]

Mr. Nabeel Khursheed Senior Research Analyst +92 (21) 35303330 [email protected]

Mr. Hamza Raza Research Analyst +92 (21) 35303330 [email protected]

Mr. Fahad Qasim Manager Research +92 (21) 35303330 [email protected]. Fahad Qasim Manager Research +92 (21) 35303330 [email protected]

Mr. Uzair Ahmed Research Officer +92 (21) 35303330 [email protected]

Mr. Asif Habib Assistant Database +92 (21) 35303330 [email protected]

Equity Sales Team:

Mr. Muhammad Rizwan Head of Sales Dir: +92 (21) 35303337 [email protected]

Ms. Samar Iqbal VP Equity Sales Dir: +92 (21) 35370799 [email protected]

Mr. Hammad Aman Manager Equity Sales +92-21 35303029 [email protected]

Corporate Office:

508, Continental Trade Center,

Block-8, Clifton, Karachi, Pakistan

Tel: +9221-35303330-2

Fax: +9221-35303349